Strategies for Paying Off Debt

|

|

|

- Reynold Fletcher

- 8 years ago

- Views:

Transcription

1 Strategies for Paying Off Debt This program is made possible by a grant from the FINRA Investor Education Foundation through Smart Investing@your library, a partnership with the American Library Association.

2 What will we discuss? Debt repayment methods. How do the repayment strategies affect your credit. Helpful tools or apps to use to track your progress and repay your debts.

3 Debt and Emotion

4 Strategies to Repay Your Debt

5 Pay the Debts on Your Own 1.Stop using your credit cards. Cut them up! Freeze them! Lock them up! 2. Find out who you owe. Create a list. Pull your credit report. 3. Use cash to make purchases. 4. Create a spending plan. Budget! Where is your money going? 5. Do you need to increase your income?

6 Pay the Debts on Your Own 6. Sell things that you aren t using. Local Classifieds, Online Classifieds 7. Look for a part-time job. 8. Save something. Even quarters add up. 9. Don t add more debt. 10. Start paying your debt back. 11. Borrow finance books from the library.

7 Pay the Debt on Your Own Snowball Method Focus on paying off the debt with the smallest balance first. When the smallest balance is paid off, roll that payment onto the debt with the next smallest balance. Rewarding to see the results. Look for extra cash to put towards debts.

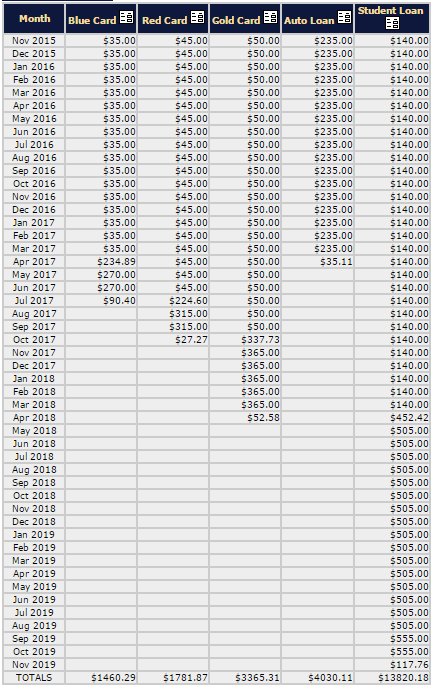

8 Snowball Method Order your debts with the smallest balance first. Creditor Balance Minimum Payment Interest Rate Blue Card $1,200 $ % Red Card $1,500 $ % Gold Card $2,500 $ % Auto Loan $3,933 $ % Student Loan $11,500 $ % Power Pay:

9 Power Pay

10 Power Pay-Snowball

11 Pay the Debt on Your Own Avalanche Focus on paying the debt with the highest interest rate. Mathematically this usually saves the most moneydepending on balances and interest rates. Use the plan that motivates you.

12 Avalanche Method Order your debts with the highest interest rate first. Creditor Balance Minimum Payment Interest Rate Gold Card $2,500 $ % Blue Card $1,200 $ % Red Card $1,500 $ % Student Loan $11,500 $ % Auto Loan $3,933 $ %

13 Avalanche Method

14 Avalanche

15 Avalanche Method Saves $22.94 Snowball Method

16 Potential Set-Backs to Paying on Your Own Unexpected expenses New debt Decrease in income from job loss Changes in living arrangements Lack of discipline Failure to change spending habits

17 Help from Third Parties: Do Your Homework Save and Invest: Consumer Financial Protecting Bureau Google Search: Reviews and complaints for company. Rip off Report: Better Business Bureau State Bar Association Website: Contact your Attorney General s office: Federal Trade Commission: Search debt relief or credit counseling

18 Debt Management Plans Work with a certified credit counseling agency who contacts your creditors to lower your interest rates and set up a payment plan to pay off your accounts in 3-5 years. You make one monthly payment to the credit counseling agency and they divide the payment up and send it to your creditors. It is NOT a settlement or consolidation. Requires credit counseling Legitimate credit counseling agencies are affiliated with AICCA, NFCC, ACCPros Accounts must be closed on the program. Individual States regulate the allowable fees.

19 Questions to ask about DMPs Do all creditors work with DMPs? Can anyone use a DMP? How will I know if this is a good choice for me? How much does a DMP cost? What monthly fees do I have to pay? Can I still use my credit cards on a DMP? Will a DMP hurt my credit score? How long will it take to pay off the debt?

20 Potential Downside of a DMP Cost of setting up the plan. Lowering your average account age on your credit report when the accounts have to be closed. New debt that needs to be added to the plan. Time length 3-5 years. Failure to change habits.

21 Consolidation or Balance Transfer Combine all debts into one payment. May be easier to handle just one payment. Lower monthly payments and possibly interest. Could extend repayment period. Avoid making unsecured debts secured. Risky to add another loan. Watch for loan origination fees. Paying debt with debt.

22 Types of Consolidation Loans Peer to Peer (P2P) Loans or Lending Circles Low interest or 0% credit cards Home Equity Loan or Line of Credit Unsecured Personal Bank Loans Student Loan Consolidation Family Members or Friends

23 What Can Go Wrong with Consolidation? 70% of those who use a consolidation loan end up back in consumer debt. Risk losing assets you used as collateral. May be a lengthy time frame to pay off the debts. Failure to change spending habits could result in new debt not being added into the plan.

24 Bankruptcy Helps consumers eliminate their debts or repay them under the protection of bankruptcy court. With Chapter 7 the debts are eliminated or discharged. Usually known as straight bankruptcy. You must liquidate all your assets except for automobiles, workrelated tools, and basic furnishings. Some property may be sold by a court official or turned over to a creditor. Chapter 7 bankruptcy stays on your credit report 10 years.

25 Bankruptcy Chapter 13 Ch. 13 is used if there is a steady income. Set up a payment plan with the court to pay back debts. Can keep a mortgaged house or car, that may be lost with a Chapter 7. Payment plan is for 3-5 years rather than surrendering property. After the payment plan is completed you receive a discharge on your debts. Chapter 13 stays on your credit report 7 years.

26 The Bankruptcy Process 1. Find an attorney you trust. 2. Prepare the documentation. (Petition and Schedules) 3. Take the required credit counseling class. 4. File for bankruptcy. 5. Go to your bankruptcy hearing. 6. Take the second part of the counseling. 7. Wait for the discharge of your debts.

27 Should I Pursue Bankruptcy? Are you unsure how much you actually owe? Is your debt too high for a debt management plan? Do you use credit cards to pay for necessities. Do you avoid dealing with your creditors and loans? Are you behind on payments? Do creditors call you? Are you only making the minimum payments? What other options do you have?

28 Things to Consider 16% of bankruptcy filers are repeat filers. CHANGE YOUR HABITS! It can be difficult to get life insurance, a home, and a job. Not all debts are forgiven. Child support, alimony, fines, taxes, and some student loan obligations. SPEAK WITH A CREDIT COUNSELOR for FREE!!!!

29 Debt Settlement Company negotiates with your creditors to settle or pay a portion of your debts. Usually for profit companies. Settlement companies tell you to stop making your payments. You deposit money for 36 months before your debts are settled. Creditors DO NOT have to agree to the terms. Interest and fees continue to accrue. Negative impact on credit when you stop making payments. Subject to legal action from creditor.

30 Beware of these Settlement Claims and Practices. Guarantee that they can make the debt go away. Guarantee that the unsecured debt is paid for pennies on the dollar. Charging fees and upfront costs before the debts are cleared. Telling you to stop paying your bills and they don t speak to your creditors. Telling you they can stop debt collections and law suits.

31 Things to Consider about Settlement It is very expensive. Fees to start, increased interest rates and late fees with your creditors. Damages your credit. Possible legal action from creditors. May still have debt that remains after settlement. Tax Implications

32 Helpful Tools to Repay your Debts Websites FINRA Tools PowerPay CNN Money Bankrate Apps PowerPay in the App store There are many free apps. Just remember to do your research and read reviews. Be careful who you trust with your full account numbers.

33 Find Inspiration Personal Finance Videos on YouTube Blogs Find a Goal Friend Financial Counselor Create a Vision Board

34 Sample Vision Boards Where are you now? Where do you want to be? What is your plan for getting there? Focus on how you want to feel

35 You Can Do It! Review your options. Do your homework. Review your goals. Be Patient.

36 Helpful Websites Federal Trade Commission: coping-debt FINRA s Save and Invest Website: Consumer Financial Protection Bureau: Call and ask for a list of free financial counselors in your area.

37 Thank you! This program is made possible by a grant from the FINRA Investor Education Foundation through Smart investing@your library, a partnership with the American Library Association.

Coping with debt. Self-help. Dealing with debt collectors. Managing your auto and home loans. Developing a budget. Contacting your creditors

Coping with debt Having trouble paying your bills? Getting collection notices from creditors? Are your accounts being turned over to debt collectors? Are you worried about losing your home or your car?

Coping with debt Having trouble paying your bills? Getting collection notices from creditors? Are your accounts being turned over to debt collectors? Are you worried about losing your home or your car?

FTC Facts. For Consumers Federal Trade Commission. Having trouble paying your bills? Getting dunning. Knee Deep in Debt. Self-Help

FTC Facts For Consumers Federal Trade Commission For The Consumer November 2003 Knee Deep in Debt www.ftc.gov 1-877-ftc-help Having trouble paying your bills? Getting dunning notices from creditors? Are

FTC Facts For Consumers Federal Trade Commission For The Consumer November 2003 Knee Deep in Debt www.ftc.gov 1-877-ftc-help Having trouble paying your bills? Getting dunning notices from creditors? Are

FTC Facts. For Consumers Federal Trade Commission. Having trouble paying your bills? Getting dunning. Knee Deep in Debt. Self-Help

FTC Facts For Consumers Federal Trade Commission For The Consumer December 2005 Knee Deep in Debt www.ftc.gov 1-877-ftc-help Having trouble paying your bills? Getting dunning notices from creditors? Are

FTC Facts For Consumers Federal Trade Commission For The Consumer December 2005 Knee Deep in Debt www.ftc.gov 1-877-ftc-help Having trouble paying your bills? Getting dunning notices from creditors? Are

Coping With Debt. Federal Trade Commission ftc.gov

Coping With Debt Federal Trade Commission ftc.gov Having trouble paying your bills? Getting dunning notices from creditors? Are your accounts being turned over to debt collectors? Are you worried about

Coping With Debt Federal Trade Commission ftc.gov Having trouble paying your bills? Getting dunning notices from creditors? Are your accounts being turned over to debt collectors? Are you worried about

Knee Deep in Debt. A WorkLife4You Guide

A WorkLife4You Guide Knee Deep in Debt Having trouble paying your bills? Getting dunning notices from creditors? Are your accounts being turned over to debt collectors? Are you worried about losing your

A WorkLife4You Guide Knee Deep in Debt Having trouble paying your bills? Getting dunning notices from creditors? Are your accounts being turned over to debt collectors? Are you worried about losing your

Debt Management Options

Get and Stay on Track Debt Management Options Where should you start? The first step to determine which debt management tool is best for you is to review your financial situation and your financial goals.

Get and Stay on Track Debt Management Options Where should you start? The first step to determine which debt management tool is best for you is to review your financial situation and your financial goals.

Knee Deep in Debt. Self-help

Knee Deep in Debt Having trouble paying your bills? Getting dunning notices from creditors? Are your accounts being turned over to debt collectors? Are you worried about losing your home or your car? You're

Knee Deep in Debt Having trouble paying your bills? Getting dunning notices from creditors? Are your accounts being turned over to debt collectors? Are you worried about losing your home or your car? You're

Credit Reports and Credit Scores

Credit Reports and Credit Scores This program is made possible by a grant from the FINRA Investor Education Foundation through Smart Investing@Your Library, a partnership with the American Library Association.

Credit Reports and Credit Scores This program is made possible by a grant from the FINRA Investor Education Foundation through Smart Investing@Your Library, a partnership with the American Library Association.

TYPES OF BANKRUPTCY There are three main types of bankruptcy cases. These are referred to by their chapter number in the Bankruptcy Code.

SOME INFORMATION ABOUT BANKRUPTCY People who are having trouble paying their debts sometimes consider bankruptcy as a remedy for this situation. An individual, called a debtor, usually files bankruptcy

SOME INFORMATION ABOUT BANKRUPTCY People who are having trouble paying their debts sometimes consider bankruptcy as a remedy for this situation. An individual, called a debtor, usually files bankruptcy

K.2 Answers to Common Bankruptcy Questions

Adapted from Consumer Bankruptcy Law and Practice, 10 th Edition, National Consumer Law Center, copyright 2012. Used by permission. K.2 Answers to Common Bankruptcy Questions A decision to file for bankruptcy

Adapted from Consumer Bankruptcy Law and Practice, 10 th Edition, National Consumer Law Center, copyright 2012. Used by permission. K.2 Answers to Common Bankruptcy Questions A decision to file for bankruptcy

The Goodman Law Firm, P.A. 1 Dana Street, 4th Floor P.O. Box 7523 Portland, ME 04101

The Goodman Law Firm, P.A. 1 Dana Street, 4th Floor P.O. Box 7523 Portland, ME 04101 Fax: (207) 772-2778 www.goodmanlawfirm.com Tel: (207) 775-4335 joseph@goodmanlawfirm.com What Is Bankruptcy? ANSWERS

The Goodman Law Firm, P.A. 1 Dana Street, 4th Floor P.O. Box 7523 Portland, ME 04101 Fax: (207) 772-2778 www.goodmanlawfirm.com Tel: (207) 775-4335 joseph@goodmanlawfirm.com What Is Bankruptcy? ANSWERS

TABLE OF CONTENTS. Introduction...3 What is Debt Consolidation?...5. Debt Consolidation Program Processes...19

TABLE OF CONTENTS Introduction...3 What is Debt Consolidation?...5 A) CHAPTER 13 B) WHAT DEBTS ARE ADDRESSED? Debt Consolidation Program Processes...19 A) DEBT MANAGEMENT PROGRAM B) DEBT SETTLEMENT PROGRAM

TABLE OF CONTENTS Introduction...3 What is Debt Consolidation?...5 A) CHAPTER 13 B) WHAT DEBTS ARE ADDRESSED? Debt Consolidation Program Processes...19 A) DEBT MANAGEMENT PROGRAM B) DEBT SETTLEMENT PROGRAM

What Does Bankruptcy Mean to Me?

What Can Bankruptcy Do for Me? Bankruptcy may make it possible for you to: Eliminate the legal obligation to pay most or all of your debts. This is called a discharge of debts. It is designed to give you

What Can Bankruptcy Do for Me? Bankruptcy may make it possible for you to: Eliminate the legal obligation to pay most or all of your debts. This is called a discharge of debts. It is designed to give you

IMPORTANCE OF CREDIT HISTORY AND SUCCESSFUL SAVING

IMPORTANCE OF CREDIT HISTORY AND SUCCESSFUL SAVING From America Saves and Experian WHAT IS A CREDIT REPORT AND SCORE? A credit score is a three digit number that measures how likely you are to repay a

IMPORTANCE OF CREDIT HISTORY AND SUCCESSFUL SAVING From America Saves and Experian WHAT IS A CREDIT REPORT AND SCORE? A credit score is a three digit number that measures how likely you are to repay a

Consumer Bankruptcy in Florida

Consumer Bankruptcy in Florida SOME INFORMATION ABOUT BANKRUPTCY People who are having trouble paying their debts sometimes consider bankruptcy as a strategy for resolving this situation. An individual,

Consumer Bankruptcy in Florida SOME INFORMATION ABOUT BANKRUPTCY People who are having trouble paying their debts sometimes consider bankruptcy as a strategy for resolving this situation. An individual,

SOME IDEAS THAT MAY HELP WITH. Credit Problems and How to Get Help

66308 1083 9/9/04 3:03 PM Page Cov1 SOME IDEAS THAT MAY HELP WITH Credit Problems and How to Get Help 66308 1083 9/9/04 3:03 PM Page Cov2 Table of Contents Do you have a credit problem? 1 Minor credit

66308 1083 9/9/04 3:03 PM Page Cov1 SOME IDEAS THAT MAY HELP WITH Credit Problems and How to Get Help 66308 1083 9/9/04 3:03 PM Page Cov2 Table of Contents Do you have a credit problem? 1 Minor credit

Deciding Which Bills to Pay First

Deciding Which Bills to Pay First When you do not have enough money to cover your family s basic living expenses and pay all your creditors, you face some difficult financial decisions. When family income

Deciding Which Bills to Pay First When you do not have enough money to cover your family s basic living expenses and pay all your creditors, you face some difficult financial decisions. When family income

Answers to Common Bankruptcy Questions 1

Answers to Common Bankruptcy Questions 1 A decision to file for bankruptcy should be made only after determining that bankruptcy is the best way to deal with your financial problems. This handbook can

Answers to Common Bankruptcy Questions 1 A decision to file for bankruptcy should be made only after determining that bankruptcy is the best way to deal with your financial problems. This handbook can

Bankruptcy in Florida

Bankruptcy in Florida SOME INFORMATION ABOUT BANKRUPTCY People who are having trouble paying their debts sometimes consider bankruptcy as a remedy for this situation. An individual, called a debtor, usually

Bankruptcy in Florida SOME INFORMATION ABOUT BANKRUPTCY People who are having trouble paying their debts sometimes consider bankruptcy as a remedy for this situation. An individual, called a debtor, usually

Why File Bankruptcy?

Why File Bankruptcy? You are trying to keep debts current, but are borrowing from one card to pay the other. You are trying to keep debts current by using your savings. You are trying to keep debts current

Why File Bankruptcy? You are trying to keep debts current, but are borrowing from one card to pay the other. You are trying to keep debts current by using your savings. You are trying to keep debts current

NYC Bankruptcy Assistance Project

NYC Bankruptcy Assistance Project A Project of Legal Services for New York City Answers to Common Bankruptcy Questions A decision to file for bankruptcy should be made only after determining that bankruptcy

NYC Bankruptcy Assistance Project A Project of Legal Services for New York City Answers to Common Bankruptcy Questions A decision to file for bankruptcy should be made only after determining that bankruptcy

ANSWERS TO COMMON BANKRUPTCY QUESTIONS

Wayne Howell, PLLC ANSWERS TO COMMON BANKRUPTCY QUESTIONS A decision to file for bankruptcy should be made only after determining that bankruptcy is the best way to deal with your financial problems. This

Wayne Howell, PLLC ANSWERS TO COMMON BANKRUPTCY QUESTIONS A decision to file for bankruptcy should be made only after determining that bankruptcy is the best way to deal with your financial problems. This

Bankruptcy may make it possible for you to:

A decision to file for bankruptcy should be made only after determining that bankruptcy is the best way to deal with your financial problems. This brochure cannot explain every aspect of the bankruptcy

A decision to file for bankruptcy should be made only after determining that bankruptcy is the best way to deal with your financial problems. This brochure cannot explain every aspect of the bankruptcy

In Home Sales Training Manual. Debt Settlement Program

In Home Sales Training Manual Debt Settlement Program Introduction to the industry The debt relief business is booming because of the rise in unemployment rates, the poor economy, and those who have found

In Home Sales Training Manual Debt Settlement Program Introduction to the industry The debt relief business is booming because of the rise in unemployment rates, the poor economy, and those who have found

THE 14 MUST-ANSWER QUESTIONS FOR ANY DEBT SETTLEMENT COMPANY

THE 14 MUST-ANSWER QUESTIONS FOR ANY DEBT SETTLEMENT COMPANY 1. Do you charge fees before settlement? No debt settlement company should charge you any fees at all unless or until your debt is settled.

THE 14 MUST-ANSWER QUESTIONS FOR ANY DEBT SETTLEMENT COMPANY 1. Do you charge fees before settlement? No debt settlement company should charge you any fees at all unless or until your debt is settled.

What You Should Know About Bankruptcy What Is Bankruptcy?

FACTS FOR National Consumer Law Center What You Should Know About Bankruptcy What Is Bankruptcy? Bankruptcy is a process under federal law designed to help people and businesses get protection from their

FACTS FOR National Consumer Law Center What You Should Know About Bankruptcy What Is Bankruptcy? Bankruptcy is a process under federal law designed to help people and businesses get protection from their

WHAT BANKRUPTCY CAN T DO

A decision to file for bankruptcy should only be made after determining that bankruptcy is the best way to deal with your financial problems. This brochure cannot explain every aspect of the bankruptcy

A decision to file for bankruptcy should only be made after determining that bankruptcy is the best way to deal with your financial problems. This brochure cannot explain every aspect of the bankruptcy

Coping with Debt Having trouble paying your bills? Getting notices from creditors? Are your accounts being turned over to debt collectors? Are you worried about losing your home or your car? You re not

Coping with Debt Having trouble paying your bills? Getting notices from creditors? Are your accounts being turned over to debt collectors? Are you worried about losing your home or your car? You re not

COMMON QUESTIONS ABOUT BANKRUPTCY

SCUDDER G. STEVENS, P.A. ATTORNEYS AT LAW A PROFESSIONAL ASSOCIATION 120 North Union Street P.O. Box 1156 Kennett Square, PA 19348 (610) 444-9840 (800) 294-4242 FAX (610) 444-9841 COMMON QUESTIONS ABOUT

SCUDDER G. STEVENS, P.A. ATTORNEYS AT LAW A PROFESSIONAL ASSOCIATION 120 North Union Street P.O. Box 1156 Kennett Square, PA 19348 (610) 444-9840 (800) 294-4242 FAX (610) 444-9841 COMMON QUESTIONS ABOUT

Chapter 12 is a reorganization for family farmers and fishing families, which is similar to Chapter 13.

GENERAL INFORMATION ABOUT THE BANKRUPTCY SYSTEM INCLUDING THE RIGHTS AND DUTIES OF CHAPTER 13 DEBTORS (and other information necessary to assist a debtor in completion of the chapter 13 plan) WHAT IS BANKRUPTCY?

GENERAL INFORMATION ABOUT THE BANKRUPTCY SYSTEM INCLUDING THE RIGHTS AND DUTIES OF CHAPTER 13 DEBTORS (and other information necessary to assist a debtor in completion of the chapter 13 plan) WHAT IS BANKRUPTCY?

JUDGE LAW FIRM 2123 E. GRANT ROAD TUCSON, ARIZONA 85712 (520) 388-5665

388-5665") JUDGE LAW FIRM 2123 E. GRANT ROAD TUCSON, ARIZONA 85712 (520) 388-5665 ARIZONA BANKRUPTCY REPORT A decision to file for bankruptcy should be made only after careful consideration of your financial situation

JUDGE LAW FIRM 2123 E. GRANT ROAD TUCSON, ARIZONA 85712 (520) 388-5665 ARIZONA BANKRUPTCY REPORT A decision to file for bankruptcy should be made only after careful consideration of your financial situation

BANKRUPTCY SOME FREQUENTLY ASKED QUESTIONS AND ANSWERS

BANKRUPTCY SOME FREQUENTLY ASKED QUESTIONS AND ANSWERS 1 You should file for bankruptcy only after carefully deciding that bankruptcy is the best way to deal with your financial problems. This pamphlet

BANKRUPTCY SOME FREQUENTLY ASKED QUESTIONS AND ANSWERS 1 You should file for bankruptcy only after carefully deciding that bankruptcy is the best way to deal with your financial problems. This pamphlet

lesson thirteen in trouble overheads

lesson thirteen in trouble overheads why consumers don t pay loss of income (48%) Unemployment (24%) Illness (16%) Other (divorce, death) (8%) overextension (25%) Poor money management Emergencies Materialism

lesson thirteen in trouble overheads why consumers don t pay loss of income (48%) Unemployment (24%) Illness (16%) Other (divorce, death) (8%) overextension (25%) Poor money management Emergencies Materialism

A decision to file for bankruptcy should be made only after determining that bankruptcy is the best way to deal with your financial problems.

A decision to file for bankruptcy should be made only after determining that bankruptcy is the best way to deal with your financial problems. This booklet cannot explain every aspect of the bankruptcy

A decision to file for bankruptcy should be made only after determining that bankruptcy is the best way to deal with your financial problems. This booklet cannot explain every aspect of the bankruptcy

BANKRUPTCY. What is the difference between a Chapter 7 and a Chapter 13 bankruptcy?

BANKRUPTCY Bankruptcy means you ask the court to excuse you from your duty to repay your creditors. A person or business you owe money to is called a creditor. Bankruptcy allows you to discharge (get rid

BANKRUPTCY Bankruptcy means you ask the court to excuse you from your duty to repay your creditors. A person or business you owe money to is called a creditor. Bankruptcy allows you to discharge (get rid

Consumer Credit Counseling. Knowing Your Options A Briefing for Individuals Contemplating Bankruptcy

Consumer Credit Counseling Knowing Your Options A Briefing for Individuals Contemplating Bankruptcy Part 1 Overview You are contemplating bankruptcy and probably have a number of questions. Is bankruptcy

Consumer Credit Counseling Knowing Your Options A Briefing for Individuals Contemplating Bankruptcy Part 1 Overview You are contemplating bankruptcy and probably have a number of questions. Is bankruptcy

FTC Facts. For Consumers Federal Trade Commission. Living paycheck to paycheck? Worried about debt. Fiscal Fitness: Choosing a Credit Counselor

FTC Facts For Consumers Federal Trade Commission For The Consumer December 2005 Fiscal Fitness: Choosing a Credit Counselor Living paycheck to paycheck? Worried about debt collectors? Can t seem to develop

FTC Facts For Consumers Federal Trade Commission For The Consumer December 2005 Fiscal Fitness: Choosing a Credit Counselor Living paycheck to paycheck? Worried about debt collectors? Can t seem to develop

What is the cause of bankruptcy? Debt!

Bankruptcy What is the cause of bankruptcy? Debt! Reasons for high bankruptcy rates: Sustained high levels of household debt. They are overextended and can t get out from under their debt. Major life-changing

Bankruptcy What is the cause of bankruptcy? Debt! Reasons for high bankruptcy rates: Sustained high levels of household debt. They are overextended and can t get out from under their debt. Major life-changing

2. The Four Chapters of the Bankruptcy Code Available to Individual Consumer Debtors

UNITED STATES BANKRUPTCY COURT EASTERN DISTRICT OF MICHIGAN NOTICE TO CONSUMER DEBTOR(S) UNDER 342(b) OF THE BANKRUPTCY CODE In accordance with 342(b) of the Bankruptcy Code, this notice to individuals

UNITED STATES BANKRUPTCY COURT EASTERN DISTRICT OF MICHIGAN NOTICE TO CONSUMER DEBTOR(S) UNDER 342(b) OF THE BANKRUPTCY CODE In accordance with 342(b) of the Bankruptcy Code, this notice to individuals

Credit Counseling. Credit Repair. Debt Management Plans. Debt Settlement and Negotiation. United Way of the Coastal Bend

K C A B G N I Y A P Credit Counseling Credit Repair Debt Management Plans Debt Settlement and Negotiation United Way of the Coastal Bend INTRODUCTION United Way of the Coastal Bend (UWCB) is a nonprofit

K C A B G N I Y A P Credit Counseling Credit Repair Debt Management Plans Debt Settlement and Negotiation United Way of the Coastal Bend INTRODUCTION United Way of the Coastal Bend (UWCB) is a nonprofit

Debt Management. Dealing with Personal Debt

Debt Management Dealing with Personal Debt Apprisen. All rights reserved. 8/24/2015 1 Setting Financial Goals Building a Strong Foundation Conduct a realistic self-assessment-think about what you want

Debt Management Dealing with Personal Debt Apprisen. All rights reserved. 8/24/2015 1 Setting Financial Goals Building a Strong Foundation Conduct a realistic self-assessment-think about what you want

BANKRUPTCY WHAT IS BANKRUPTCY?

BANKRUPTCY Most military personnel and their families handle their financial affairs in a responsible and timely manner. Those who have problems usually seek timely assistance from financial counselors.

BANKRUPTCY Most military personnel and their families handle their financial affairs in a responsible and timely manner. Those who have problems usually seek timely assistance from financial counselors.

Bankruptcy Guide for Beginners

Bankruptcy Guide for Beginners Answers to 20 common bankruptcy questions We hope you find this guide useful and informative. We look forward to helping you eliminate debt and get a fresh financial start.

Bankruptcy Guide for Beginners Answers to 20 common bankruptcy questions We hope you find this guide useful and informative. We look forward to helping you eliminate debt and get a fresh financial start.

NOTICE NO. 1. Notice Mandated By Section 342(b)(1) and 527(a)(1) of the Bankruptcy Code PURPOSES, BENEFITS AND COSTS OF BANKRUPTCY

(1) and 527(a)(1) of the Bankruptcy Code PURPOSES, BENEFITS AND COSTS OF BANKRUPTCY") NOTICE NO. 1 Notice Mandated By Section 342(b)(1) and 527(a)(1) of the Bankruptcy Code PURPOSES, BENEFITS AND COSTS OF BANKRUPTCY The United States Constitution provides a method whereby individuals, burdened

NOTICE NO. 1 Notice Mandated By Section 342(b)(1) and 527(a)(1) of the Bankruptcy Code PURPOSES, BENEFITS AND COSTS OF BANKRUPTCY The United States Constitution provides a method whereby individuals, burdened

A GUIDE TO FILING FOR BANKRUPTCY PROTECTION UNDER CHAPTER 7 OF THE BANKRUPTCY CODE

A GUIDE TO FILING FOR BANKRUPTCY PROTECTION UNDER CHAPTER 7 OF THE BANKRUPTCY CODE Michael R. Totaro Totaro & Shanahan P.O. Box 789 Pacific Palisades, CA 90272 310 573 0276 (v) 310 496 1260 (f) Mtotaro@aol.com

A GUIDE TO FILING FOR BANKRUPTCY PROTECTION UNDER CHAPTER 7 OF THE BANKRUPTCY CODE Michael R. Totaro Totaro & Shanahan P.O. Box 789 Pacific Palisades, CA 90272 310 573 0276 (v) 310 496 1260 (f) Mtotaro@aol.com

In Debt? Dealing with your creditors Call: 0800 157 7330 or 01257 251319 www.debtproblemsuk.com

Debtfocus Business Recovery & Insolvency Ltd In Debt? Dealing with your creditors Call: 0800 157 7330 or 01257 251319 www.debtproblemsuk.com Content highlights Before you read this guide in detail, you

Debtfocus Business Recovery & Insolvency Ltd In Debt? Dealing with your creditors Call: 0800 157 7330 or 01257 251319 www.debtproblemsuk.com Content highlights Before you read this guide in detail, you

CONSUMER CONFUSION WHO DO I WORK WITH TO PAY DOWN DEBT?

CONSUMER CONFUSION WHO DO I WORK WITH TO PAY DOWN DEBT? Presented by Kathy Virgallito Consumer Credit Counseling Service, now known as What We ll Cover Today Options for paying down debt Scams to watch

CONSUMER CONFUSION WHO DO I WORK WITH TO PAY DOWN DEBT? Presented by Kathy Virgallito Consumer Credit Counseling Service, now known as What We ll Cover Today Options for paying down debt Scams to watch

Surviving a Layoff. A straight forward guide to making the right decisions while coping with a job loss.

Surviving a Layoff A straight forward guide to making the right decisions while coping with a job loss. It s not easy, but Apprisen has a great guide to help you get through your layoff Listen to the news

Surviving a Layoff A straight forward guide to making the right decisions while coping with a job loss. It s not easy, but Apprisen has a great guide to help you get through your layoff Listen to the news

CONSUMER BANKRUPTCY. Q: What is bankruptcy? Q: How does someone know whether to file a Chapter 7 or 13? Q: How is an action filed in bankruptcy court?

CONSUMER BANKRUPTCY R. Michael Drose * Thomas M. Fryar * Ann U. Bell * Certified Bankruptcy Specialist Q: What is bankruptcy? A: Bankruptcy laws are federal laws and are the same in every state, although

CONSUMER BANKRUPTCY R. Michael Drose * Thomas M. Fryar * Ann U. Bell * Certified Bankruptcy Specialist Q: What is bankruptcy? A: Bankruptcy laws are federal laws and are the same in every state, although

WHAT IS THE DIFFERENCE BETWEEN CHAPTER 7 AND CHAPTER 13?

NEW JERSEY BANKRUPTCY WHAT IS THE DIFFERENCE BETWEEN CHAPTER 7 AND CHAPTER 13? Because the Difference Between Chapter 7 and Chapter 13 Can Have Serious Consequences for a Client Who Files the Wrong Case,

NEW JERSEY BANKRUPTCY WHAT IS THE DIFFERENCE BETWEEN CHAPTER 7 AND CHAPTER 13? Because the Difference Between Chapter 7 and Chapter 13 Can Have Serious Consequences for a Client Who Files the Wrong Case,

The Truth About Debt Consolidation

The Truth About Debt Consolidation What Your Options Are and What Debt Consolidation Companies Don t Tell You K a i n & S c o t t, P. A. 1 3 7 t h A v e. S S t. C l o u d, M N ( 3 2 0 ) 2 5 8. 7 2 8 7

The Truth About Debt Consolidation What Your Options Are and What Debt Consolidation Companies Don t Tell You K a i n & S c o t t, P. A. 1 3 7 t h A v e. S S t. C l o u d, M N ( 3 2 0 ) 2 5 8. 7 2 8 7

GETTING OUT AND STAYING OUT! Your No-Nonsense Guide to Surviving Debt

GETTING OUT AND STAYING OUT! Your No-Nonsense Guide to Surviving Debt TABLE OF CONTENTS Introduction: You re Not Alone! Debt Relief Options Minimum Payments Snowball vs. Avalanche Debt Resolution Credit

GETTING OUT AND STAYING OUT! Your No-Nonsense Guide to Surviving Debt TABLE OF CONTENTS Introduction: You re Not Alone! Debt Relief Options Minimum Payments Snowball vs. Avalanche Debt Resolution Credit

Wealth Strategies. www.rfawealth.com. Debt Management: Getting Started The Basics. www.rfawealth.com

www.rfawealth.com Wealth Strategies Debt Management: Getting Started The Basics Part 4 of 12 Debt Management: The Basics WEALTH STRATEGIES Page 1 What is Debt Management? As a consumer in today s world,

www.rfawealth.com Wealth Strategies Debt Management: Getting Started The Basics Part 4 of 12 Debt Management: The Basics WEALTH STRATEGIES Page 1 What is Debt Management? As a consumer in today s world,

How to Use Credit. Latino Community Credit Union & Latino Community Development Center

How to Use Credit Latino Community Credit Union & Latino Community Development Center How to Use Credit Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright

How to Use Credit Latino Community Credit Union & Latino Community Development Center How to Use Credit Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright

After Bankruptcy: What You Need to Know

After Bankruptcy: What You Need to Know The Path to Creditworthiness Bankruptcy offers some resolution to your financial worries. However, it also carries negative consequences and major responsibilities

After Bankruptcy: What You Need to Know The Path to Creditworthiness Bankruptcy offers some resolution to your financial worries. However, it also carries negative consequences and major responsibilities

How do I get good credit?

Slide 1 Credit The information provided in this e-course is intended for educational purposes only and does not constitute specific advice for you as an individual. When evaluating your particular needs,

Slide 1 Credit The information provided in this e-course is intended for educational purposes only and does not constitute specific advice for you as an individual. When evaluating your particular needs,

PLAN TO PAY CREDITORS AND PROTECT FAMILY WELFARE

February 2002 FL/FF-I-06 PLAN TO PAY CREDITORS AND PROTECT FAMILY WELFARE Barbara R. Rowe, Ph.D. Professor and Family Resource Management Specialist Utah State University 1 Many circumstances can lead

February 2002 FL/FF-I-06 PLAN TO PAY CREDITORS AND PROTECT FAMILY WELFARE Barbara R. Rowe, Ph.D. Professor and Family Resource Management Specialist Utah State University 1 Many circumstances can lead

This guide has been produced by the Insolvency Service with the help and support of the IVA Standing Committee. The Insolvency Service would like to

This guide has been produced by the Insolvency Service with the help and support of the IVA Standing Committee. The Insolvency Service would like to thank the members of the IVA Standing Committee for

This guide has been produced by the Insolvency Service with the help and support of the IVA Standing Committee. The Insolvency Service would like to thank the members of the IVA Standing Committee for

Using Credit to Your Advantage

Hands on Banking Using Credit to Your Advantage Credit Reports, Credit Scores and Dealing with Debt The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the

Hands on Banking Using Credit to Your Advantage Credit Reports, Credit Scores and Dealing with Debt The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the

How to Get Out of Debt & Build Wealth. Stephen T. Craig Bankruptcy Attorney Professional Debt Negotiator

How to Get Out of Debt & Build Wealth Stephen T. Craig Bankruptcy Attorney Professional Debt Negotiator Psychology of Spending Intention- who am I trying to impress? Ask will this improve the quality of

How to Get Out of Debt & Build Wealth Stephen T. Craig Bankruptcy Attorney Professional Debt Negotiator Psychology of Spending Intention- who am I trying to impress? Ask will this improve the quality of

Answers to Common Bankruptcy Questions

Mailing PO Box 9440 Naples, FL 34101 Naples 5470 Bryson Court, Suite 103 Naples, FL 34109 Telephone 239-642-1485 Facsimile 239-642-1487 Email info@patrickneale.com Marco Island 950 North Collier Blvd.

Mailing PO Box 9440 Naples, FL 34101 Naples 5470 Bryson Court, Suite 103 Naples, FL 34109 Telephone 239-642-1485 Facsimile 239-642-1487 Email info@patrickneale.com Marco Island 950 North Collier Blvd.

OPTIONS IN FORECLOSURE

Section II: KEEPING YOUR HOME OPTIONS IN FORECLOSURE Deciding whether or not to keep your home is something that only you, the homeowner, can determine. The best housing counselors will ask what you d

Section II: KEEPING YOUR HOME OPTIONS IN FORECLOSURE Deciding whether or not to keep your home is something that only you, the homeowner, can determine. The best housing counselors will ask what you d

SUCCESSFUL HOW TO BE IN YOUR CHAPTER 13 BANKRUPTCY. Table of Contents. Huon Le, Chapter 13 Trustee-Augusta

He looks the whole world in the face for he owes not any man. ~Henry Wadsworth Longfellow HOW TO BE SUCCESSFUL IN YOUR CHAPTER 13 BANKRUPTCY Huon Le, Chapter 13 Trustee-Augusta Table of Contents IMPORTANT

He looks the whole world in the face for he owes not any man. ~Henry Wadsworth Longfellow HOW TO BE SUCCESSFUL IN YOUR CHAPTER 13 BANKRUPTCY Huon Le, Chapter 13 Trustee-Augusta Table of Contents IMPORTANT

CONSULTATION AGREEEMENT and ACKNOWLEDGEMENT OF RECEIPT OF DICLOSURES AND INSTRUCTIONS

CONSULTATION AGREEEMENT and ACKNOWLEDGEMENT OF RECEIPT OF DICLOSURES AND INSTRUCTIONS This agreement is entered on this day between the undersigned (hereinafter referred to as "Client") and ADRIAN M. LAPAS,

CONSULTATION AGREEEMENT and ACKNOWLEDGEMENT OF RECEIPT OF DICLOSURES AND INSTRUCTIONS This agreement is entered on this day between the undersigned (hereinafter referred to as "Client") and ADRIAN M. LAPAS,

DEBT HOLE TRAPPED IN THE. Daddy, why are you coming home late again?

2015 TRAPPED IN THE DEBT HOLE Daddy, why are you coming home late again? Jonathan is a typical American consumer. He works hard to provide for his family and enjoy his time off, but he never seems to have

2015 TRAPPED IN THE DEBT HOLE Daddy, why are you coming home late again? Jonathan is a typical American consumer. He works hard to provide for his family and enjoy his time off, but he never seems to have

Understanding Your Credit Report

Understanding Your Credit Report What is credit? Credit is the use of someone else s money in exchange for a promise to pay it back on a given date. There are two major types of credit: Revolving and Installment.

Understanding Your Credit Report What is credit? Credit is the use of someone else s money in exchange for a promise to pay it back on a given date. There are two major types of credit: Revolving and Installment.

NOTICE NO. 1 Notice Mandated by Section 342(b)(1) and 527(a)(1) Of The Bankruptcy Code:

(1) and 527(a)(1) Of The Bankruptcy Code:") Mandatory Bankruptcy Disclosures The following mandatory disclosures are required under Section 527 and 342 of the Bankruptcy Abuse Prevention and Consumer Protection Act (BAPCPA) of 2005. NOTICE NO. 1

Mandatory Bankruptcy Disclosures The following mandatory disclosures are required under Section 527 and 342 of the Bankruptcy Abuse Prevention and Consumer Protection Act (BAPCPA) of 2005. NOTICE NO. 1

Understanding Bankruptcy

Understanding Bankruptcy What is Bankruptcy? Bankruptcy is a legal process where an individual or organizational debtor is able to seek some financial relief. A fundamental goal of the federal bankruptcy

Understanding Bankruptcy What is Bankruptcy? Bankruptcy is a legal process where an individual or organizational debtor is able to seek some financial relief. A fundamental goal of the federal bankruptcy

New bankruptcy law will still allow debtors to obtain a fresh start. The Bankruptcy Abuse Prevention and Consumer Prevention Act (BAPCA) that

that") New bankruptcy law will still allow debtors to obtain a fresh start The Bankruptcy Abuse Prevention and Consumer Prevention Act (BAPCA) that took effect October 17, 2005, has added a few new twists to

New bankruptcy law will still allow debtors to obtain a fresh start The Bankruptcy Abuse Prevention and Consumer Prevention Act (BAPCA) that took effect October 17, 2005, has added a few new twists to

Managing Your Finances During a Furlough

Managing Your Finances During a Furlough A straight forward guide to making the right decisions while coping with the reduction of income caused by a furlough. Managing Your Finances During a Furlough

Managing Your Finances During a Furlough A straight forward guide to making the right decisions while coping with the reduction of income caused by a furlough. Managing Your Finances During a Furlough

taking control of your debt Using Smart Money Management to Reduce Your Debt

taking control of your debt Using Smart Money Management to Reduce Your Debt F I N A N C I A L M E N T O R I N G P R O G R A M IN THIS MODULE YOU WILL LEARN HOW TO: Identify warning signs of debt problems.

taking control of your debt Using Smart Money Management to Reduce Your Debt F I N A N C I A L M E N T O R I N G P R O G R A M IN THIS MODULE YOU WILL LEARN HOW TO: Identify warning signs of debt problems.

5 Little Known Facts About Bankruptcy In Utah Other Attorneys May Not Tell You About.

Lewis Adams & Associates Utah Bankruptcy Attorneys Personal Reliable Professional (801) 396-0856 www.utah-bankruptcy.org 5 Little Known Facts About Bankruptcy In Utah Other Attorneys May Not Tell You About.

Lewis Adams & Associates Utah Bankruptcy Attorneys Personal Reliable Professional (801) 396-0856 www.utah-bankruptcy.org 5 Little Known Facts About Bankruptcy In Utah Other Attorneys May Not Tell You About.

Financial Empowerment Curriculum Moving Ahead Through Financial Management. Workshop Credit Overview

Financial Empowerment Curriculum Moving Ahead Through Financial Management Workshop Credit Overview 1 Workshop Objectives Explain why credit is important. Access and read a copy of your credit report.

Financial Empowerment Curriculum Moving Ahead Through Financial Management Workshop Credit Overview 1 Workshop Objectives Explain why credit is important. Access and read a copy of your credit report.

How To Pay Off Debt Through Bankruptcy

Bankruptcy 13 Bankruptcy Debts & Debt Collection What happens if I can't pay my bills? Persons to whom you owe money have several methods of recourse if you fail to pay a debt. The method used depends

Bankruptcy 13 Bankruptcy Debts & Debt Collection What happens if I can't pay my bills? Persons to whom you owe money have several methods of recourse if you fail to pay a debt. The method used depends

Getting out from under debt

NET GAIN Scoring points for your financial future AS SEEN IN USA TODAY APRIL 18, 2003 Getting out from under debt Consider your options before diving into bankruptcy By Christine Dugas USA TODAY Even if

NET GAIN Scoring points for your financial future AS SEEN IN USA TODAY APRIL 18, 2003 Getting out from under debt Consider your options before diving into bankruptcy By Christine Dugas USA TODAY Even if

Bankruptcy Basics. Answers to Common Questions about Bankruptcy. from the law office of William Waldner

Bankruptcy Basics Answers to Common Questions about Bankruptcy from the law office of William Waldner Contents 4 Introduction 5 What is Bankruptcy? 7 Should I File for Bankruptcy? 9 What Are the Types

Bankruptcy Basics Answers to Common Questions about Bankruptcy from the law office of William Waldner Contents 4 Introduction 5 What is Bankruptcy? 7 Should I File for Bankruptcy? 9 What Are the Types

Overcoming the Credit Barrier. Poor Credit Affects Your Ability to Plan

Overcoming the Credit Barrier: Clearing the Way to Your Financial Goals was written and designed for The National Foundation for Credit Counseling (NFCC ) and the Financial Planning Association (FPA )

Overcoming the Credit Barrier: Clearing the Way to Your Financial Goals was written and designed for The National Foundation for Credit Counseling (NFCC ) and the Financial Planning Association (FPA )

WHAT YOU SHOULD KNOW ABOUT YOUR CHAPTER 13 BANKRUPTCY. Your Trustee is: Locke D. Barkley 601-355-6661. www.barkley13.com. Your Case Number is:

WHAT YOU SHOULD KNOW ABOUT YOUR CHAPTER 13 BANKRUPTCY This booklet contains some basic, general information about your Chapter 13 bankruptcy. Read this pamphlet completely to understand your obligations

WHAT YOU SHOULD KNOW ABOUT YOUR CHAPTER 13 BANKRUPTCY This booklet contains some basic, general information about your Chapter 13 bankruptcy. Read this pamphlet completely to understand your obligations

Credit History CREDIT REPORTS CREDIT SCORES BUILDING A STRONG CREDIT REPORT

CREDIT What You Should Know About... Credit History CREDIT REPORTS CREDIT SCORES BUILDING A STRONG CREDIT REPORT YourMoneyCounts Understanding what your credit history is what s in it, what s not in it

CREDIT What You Should Know About... Credit History CREDIT REPORTS CREDIT SCORES BUILDING A STRONG CREDIT REPORT YourMoneyCounts Understanding what your credit history is what s in it, what s not in it

Teens. lesson thirteen. in trouble. presentation slides 04/09

Teens lesson thirteen in trouble presentation slides 04/09 why consumers don t pay loss of income (48%) Unemployment (24%) Illness (16%) Other (divorce, death) (8%) overextension (25%) Poor money management

Teens lesson thirteen in trouble presentation slides 04/09 why consumers don t pay loss of income (48%) Unemployment (24%) Illness (16%) Other (divorce, death) (8%) overextension (25%) Poor money management

Bankruptcy Questions. FAQ > Bankruptcy Questions WHAT IS CHAPTER 7 BANKRUPTCY?

FAQ > Bankruptcy Questions Bankruptcy Questions WHAT IS CHAPTER 7 BANKRUPTCY? Chapter 7 bankruptcy is sometimes called a straight bankruptcy or a liquidation proceeding. The number one goal in an individual

FAQ > Bankruptcy Questions Bankruptcy Questions WHAT IS CHAPTER 7 BANKRUPTCY? Chapter 7 bankruptcy is sometimes called a straight bankruptcy or a liquidation proceeding. The number one goal in an individual

Bankruptcy Q&A. When filing a bankruptcy there are several different chapters under which you can file:

Bankruptcy Q&A Chapter 7: What types of bankruptcy are available? When filing a bankruptcy there are several different chapters under which you can file: This is the most basic bankruptcy and is available

Bankruptcy Q&A Chapter 7: What types of bankruptcy are available? When filing a bankruptcy there are several different chapters under which you can file: This is the most basic bankruptcy and is available

For more in-depth information about Chapter 7 and how it can help you, please contact our

Introduction This Ebook gives you an overview of Chapter 7 bankruptcy and how it can help you eliminate debt. We hope that you find this Ebook useful and informative. For more in-depth information about

Introduction This Ebook gives you an overview of Chapter 7 bankruptcy and how it can help you eliminate debt. We hope that you find this Ebook useful and informative. For more in-depth information about

Improving a Credit Profile

Improving a Credit Profile Steps to improving a credit profile STEP 1. Order your credit Report STEP 2. Evaluate & develop a plan STEP 3. Is the personal information accurate? STEP 4. Are the tradelines

Improving a Credit Profile Steps to improving a credit profile STEP 1. Order your credit Report STEP 2. Evaluate & develop a plan STEP 3. Is the personal information accurate? STEP 4. Are the tradelines

How To Get Rid Of Debt

Leader Instructions Overall Strategies of Debt Reduction (15 minutes) Review the Debt-to-Income Ratio sheet and do board examples of the math and the case study of Mary. Discuss the Paying More than Minimums

Leader Instructions Overall Strategies of Debt Reduction (15 minutes) Review the Debt-to-Income Ratio sheet and do board examples of the math and the case study of Mary. Discuss the Paying More than Minimums

Growing Dollars and $ense: Personal Financial Planning Seminar

Growing Dollars and $ense: Personal Financial Planning Seminar The Coalition for Debtor Education Kimberly Allman www.debtoreducati0n.org Email: cde@law.fordham.edu This program is made possible by a grant

Growing Dollars and $ense: Personal Financial Planning Seminar The Coalition for Debtor Education Kimberly Allman www.debtoreducati0n.org Email: cde@law.fordham.edu This program is made possible by a grant

LAUREN ROSS Attorney at Law 2550 N. Hollywood Way Suite 404 Burbank, CA 91505-5046 Tel.(818) 847-0211 Facsimile (818) 847-0214

847-0211 Facsimile (818) 847-0214") LAUREN ROSS Attorney at Law 2550 N. Hollywood Way Suite 404 Burbank, CA 91505-5046 Tel.(818) 847-0211 Facsimile (818) 847-0214 INITIAL CONSULTATION AGREEMENT AND REQUIRED NOTICES Please Note: These documents

LAUREN ROSS Attorney at Law 2550 N. Hollywood Way Suite 404 Burbank, CA 91505-5046 Tel.(818) 847-0211 Facsimile (818) 847-0214 INITIAL CONSULTATION AGREEMENT AND REQUIRED NOTICES Please Note: These documents

Common Questions of Personal Bankruptcy

Common Questions of Personal Bankruptcy Here are a few common questions many have asked with the answers from our experienced bankruptcy attorneys. If you have any common questions, please call Amicus

Common Questions of Personal Bankruptcy Here are a few common questions many have asked with the answers from our experienced bankruptcy attorneys. If you have any common questions, please call Amicus

Webinar #3: Effective Credit and Debt Management

1 Webinar #3: Effective Credit and Debt Management Sponsored by: Massachusetts Financial Literacy Trust Fund The Office of Massachusetts State Treasurer & Receiver General Facilitator: Jacqueline Cooper

1 Webinar #3: Effective Credit and Debt Management Sponsored by: Massachusetts Financial Literacy Trust Fund The Office of Massachusetts State Treasurer & Receiver General Facilitator: Jacqueline Cooper

QUESTIONS CONCERNING BANKRUPTCY

QUESTIONS CONCERNING BANKRUPTCY The Law Office of Paul D. Post, P.A. is a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code. The assistance provided to clients may

QUESTIONS CONCERNING BANKRUPTCY The Law Office of Paul D. Post, P.A. is a debt relief agency. We help people file for bankruptcy relief under the Bankruptcy Code. The assistance provided to clients may

Always Ask Questions Before you Retain a Bankruptcy Attorney

Always Ask Questions Before you Retain a Bankruptcy Attorney Deciding to file bankruptcy is a stressful time. You're about to turn your life upside down in order to eliminate debt that you can't pay. Because

Always Ask Questions Before you Retain a Bankruptcy Attorney Deciding to file bankruptcy is a stressful time. You're about to turn your life upside down in order to eliminate debt that you can't pay. Because

Adviceguide Advice that makes a difference

Jargon Buster A Z of financial terms This fact sheet explains some of the financial terms that you might come across when you are dealing with financial matters. ACCOUNT:- this is provided by a bank or

Jargon Buster A Z of financial terms This fact sheet explains some of the financial terms that you might come across when you are dealing with financial matters. ACCOUNT:- this is provided by a bank or

Adviceguide Advice that makes a difference

Jargon Buster A Z of financial terms This fact sheet explains some of the financial terms that you might come across when you are dealing with financial matters. ACCOUNT:- this is provided by a bank or

Jargon Buster A Z of financial terms This fact sheet explains some of the financial terms that you might come across when you are dealing with financial matters. ACCOUNT:- this is provided by a bank or

Bankruptcy/Debt Collection

Bankruptcy/Debt Collection [ADVOCATE: Give caller advice per script. Check case acceptance list and refer to appropriate offfice for more services.] I. Explain Judgment Proof Judgment proof means you have

Bankruptcy/Debt Collection [ADVOCATE: Give caller advice per script. Check case acceptance list and refer to appropriate offfice for more services.] I. Explain Judgment Proof Judgment proof means you have

RIGHTS AND RESPONSIBILITIES OF CHAPTER 13 DEBTORS AND ATTORNEYS

Filer s Name, Address, Phone, Fax, Email: UNITED STATES BANKRUPTCY COURT DISTRICT OF HAWAII 1132 Bishop Street, Suite 250 Honolulu, Hawaii 96813 hib_2016-1g1 (12/09) Debtor: Case No.: Joint Debtor: (if

Filer s Name, Address, Phone, Fax, Email: UNITED STATES BANKRUPTCY COURT DISTRICT OF HAWAII 1132 Bishop Street, Suite 250 Honolulu, Hawaii 96813 hib_2016-1g1 (12/09) Debtor: Case No.: Joint Debtor: (if

FSA Credit Counseling Service. Debt Management Program. Client Handbook. Client Number:

FSA Credit Counseling Service Debt Management Program Client Handbook Client Number: Confidentiality All services provided by CCS are strictly confidential. You have been asked to sign a "Release of Information"

FSA Credit Counseling Service Debt Management Program Client Handbook Client Number: Confidentiality All services provided by CCS are strictly confidential. You have been asked to sign a "Release of Information"

FORECLOSURE. I don t think I can make my mortgage payments but I don t want to go through a foreclosure. What are some of my options?

FORECLOSURE When you borrow money to buy a house or land, the creditor usually takes a security interest in the property you buy. This means that if you don t pay, the creditor can foreclose upon (or take

FORECLOSURE When you borrow money to buy a house or land, the creditor usually takes a security interest in the property you buy. This means that if you don t pay, the creditor can foreclose upon (or take

Slaying the Dragon: Dealing with Credit Card, Student Loan & Medical Debt

Slaying the Dragon: Dealing with Credit Card, Student Loan & Medical Debt Don t be scorched By the Dragon of Debt! Credit Card Debt? Reasons for the Balances Struggle Neglecting the power of compound interest

Slaying the Dragon: Dealing with Credit Card, Student Loan & Medical Debt Don t be scorched By the Dragon of Debt! Credit Card Debt? Reasons for the Balances Struggle Neglecting the power of compound interest

Your Guide to Bankruptcy for Individuals

Consumer Legal Guide Your Guide to Bankruptcy for Individuals ILLINOIS STATE BAR ASSOCIATION ASK A LAWYER WHAT IS BANKRUPTCY? Bankruptcy is a court proceeding that is governed by the federal law known

Consumer Legal Guide Your Guide to Bankruptcy for Individuals ILLINOIS STATE BAR ASSOCIATION ASK A LAWYER WHAT IS BANKRUPTCY? Bankruptcy is a court proceeding that is governed by the federal law known

Debt Options Information guide

Debt Options Information guide Debt & Money Advice Support CIC (DMAS CIC) is authorised and regulated by the Financial Conduct Authority FRN: 631799. A company registered in England & Wales 9203918. 1

Debt Options Information guide Debt & Money Advice Support CIC (DMAS CIC) is authorised and regulated by the Financial Conduct Authority FRN: 631799. A company registered in England & Wales 9203918. 1