If you do not have all of the above forms, please call Junn De Guzman at (732)

|

|

|

- Arron Roberts

- 8 years ago

- Views:

Transcription

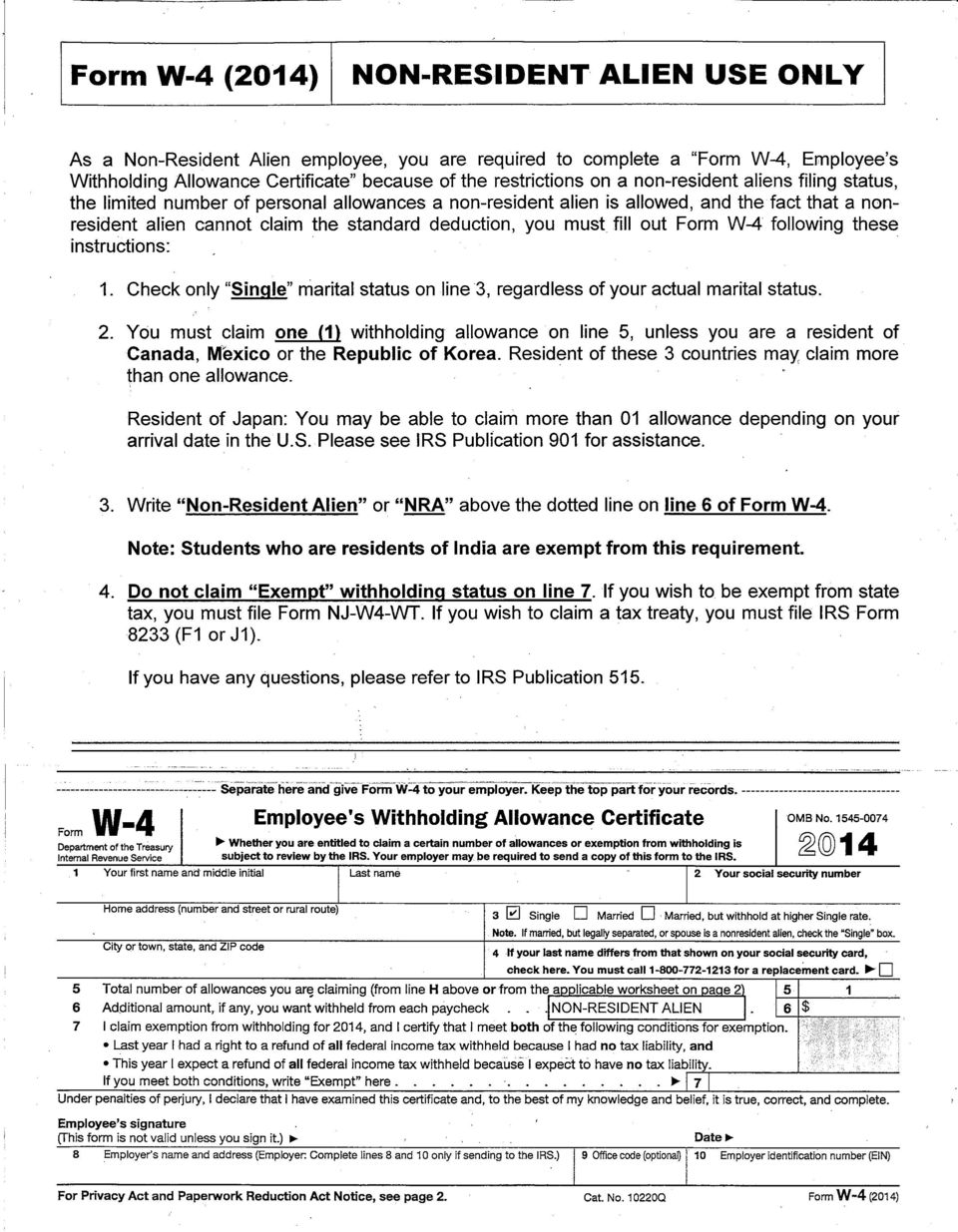

1 To: Non-Resident Aliens Requesting Special Tax Treatment From: Junn De Guzman, Sr. Accountant Payroll Services Date: January 9, 2014 Re: Requirements for Tax Benefits for Calendar Year 2014 Enclosed please find your 2014 Request for Tax Benefits Package. These forms are only for calendar year 2014 and must be submitted and approved by the Payroll Services in order for your tax exemption benefits to be processed and take effect. The University is required by the Internal Revenue Service (IRS) to obtain new tax benefit documentation yearly. Your package should contain the following forms: Form 8233 with Instructions (please include your foreign residence address on Form 8233, Line 4) Personal Statement Letter Substantial Presence Test Form W-4 for 2014 If you do not have all of the above forms, please call Junn De Guzman at (732) INSTRUCTIONS FOR COMPLETING THE ABOVE FORMS: Form 8233: 1. Fill in all of Part I, Part II 11(a)(b), 12(a)(b)(c) and sign and date on Part III. 2. The IRS will reject all incomplete forms, which will require the University to withhold Federal Income Taxes without any income tax treaty benefit to which you may have been entitled. The University will not issue tax refunds. You will be required to submit a 2013 Form 1040NR to the IRS to claim any refund. Personal Statement Letter: 1. Please fill in the blank lines with the applicable information. 2. Sign and date the form. 1

to obtain new tax benefit documentation yearly.")

2 3. All incomplete or unsigned forms will be returned for correction and resubmission. Substantial Presence Test: This test determines your status as a non-resident or resident alien for taxation purposes only. You must accurately complete and sign this form per the instructions to the form. 1. Please fill in blank lines with applicable information. 2. Sign and date the form. 3. Attach copies of your valid VISA with I-94 attached and your DS-2019 (J1) or I-20-ID (F1). Note: Those who are determined to be substantially present are resident aliens and are required to pay Social Security and Medicare taxes. Those who are determined to be not substantially present are non-resident aliens and are entitled to receive tax-exempt status for Social Security and Medicare taxes. This exemption is only valid as long as you retain your non-resident alien status. Form W-4 for 2014: 1. Marital Status must be completed as Single on line One (1) withholding allowance may be claimed on line Write Non-Resident Alien or NRA on line Sign and date the form. An EXEMPT withholding status may NOT be claimed. Do not fill in "Exempt" on line 7. Please complete the enclosed package immediately and return it to the following address: Rutgers, The State University of New Jersey Junn De Guzman, Payroll Services Liberty Plaza, 4 th Floor 335 George Street New Brunswick, NJ Or Inter-Office Mail: Junn De Guzman Dept: Payroll Bldg/Rm#: LP/4300 Campus: NB If you have any questions, please call Junn De Guzman at (732) or me at deguzmjt@ca.rutgers.edu. Thank you. 2

or I-20-ID (F1).")

3 Payroll Services Foreign National Checklist Form 8233 Personal Statement Letter Substantial Presence Test Form W-4 for 2014 Copy of VISA (with I-94 attached) Copy of Passport Copy of Certificate of Eligibility for Nonimmigrant (F1) Student (I-20) or Copy of Certificate of Eligibility for Exchange Visitor Status (J1 - DS-2019) or Copy of Petition for Nonimmigrant (H1B - I-797B) Form I-9 Senders Name : Department : Phone Number : Address :

or Copy of Petition for Nonimmigrant (H1B - I-797B) Form I-9 Senders Name : Department : Phone Number")

4 Form 8233 (Rev. March 2009) Department of the Treasury Internal Revenue Service Exemption From Withholding on Compensation for Independent (and Certain Dependent) Personal Services of a Nonresident Alien Individual See separate instructions. OMB No Who Should Use This Form? Note: For definitions of terms used in this section and detailed instructions on required withholding forms for each type of income, see Definitions on pages 1 and 2 of the instructions. DO NOT Use This Form... IF you are a nonresident alien individual who is receiving... Compensation for independent personal services performed in the United States Compensation for dependent personal services performed in the United States Noncompensatory scholarship or fellowship income and personal services income from the same withholding agent IF you are a beneficial owner who is... Receiving compensation for dependent personal services performed in the United States and you are not claiming a tax treaty withholding exemption for that compensation Receiving noncompensatory scholarship or fellowship income and you are not receiving any personal services income from the same withholding agent Claiming only foreign status or treaty benefits with respect to income that is not compensation for personal services THEN, if you are the beneficial owner of that income, use this form to claim... A tax treaty withholding exemption (Independent personal services, Business profits) for part or all of that compensation and/or to claim the daily personal exemption amount. A tax treaty withholding exemption for part or all of that compensation. Note: Do not use Form 8233 to claim the daily personal exemption amount. A tax treaty withholding exemption for part or all of both types of income. INSTEAD, use... Form W-4 (See page 2 of the Instructions for Form 8233 for how to complete Form W-4.) Form W-8BEN or, if elected by the withholding agent, Form W-4 for the noncompensatory scholarship or fellowship income Form W-8BEN This exemption is applicable for compensation for calendar year and ending., or other tax year beginning Part I Identification of Beneficial Owner (See instructions.) 1 Name of individual who is the beneficial owner 2 U.S. taxpayer identifying number 3 Foreign tax identifying number, if any (optional) 4 Permanent residence address (street, apt. or suite no., or rural route). Do not use a P.O. box. City or town, state or province. Include postal code where appropriate. Country (do not abbreviate) 5 Address in the United States (street, apt. or suite no., or rural route). Do not use a P.O. box. City or town, state, and ZIP code 6 Note: Citizens of Canada or Mexico are not required to complete lines 7a and 7b. U.S. visa type 7a Country issuing passport 7b Passport number 8 Date of entry into the United States 9a Current nonimmigrant status 9b Date your current nonimmigrant status expires 10 If you are a foreign student, trainee, professor/teacher, or researcher, check this box Caution: See the line 10 instructions for the required additional statement you must attach. For Privacy Act and Paperwork Reduction Act Notice, see separate instructions. Cat. No K Form 8233 (Rev )

5 Form 8233 (Rev ) Part II Claim for Tax Treaty Withholding Exemption and/or Personal Exemption Amount 11 Compensation for independent (and certain dependent) personal services: a Description of personal services you are providing Page 2 b Total compensation you expect to be paid for these services in this calendar or tax year $ 12 If compensation is exempt from withholding based on a tax treaty benefit, provide: a Tax treaty and treaty article on which you are basing exemption from withholding b Total compensation listed on line 11b above that is exempt from tax under this treaty $ c Country of permanent residence Note: Do not complete lines 13a through 13c unless you also received compensation for personal services from the same withholding agent. 13 Noncompensatory scholarship or fellowship income: a Amount $ b Tax treaty and treaty article on which you are basing exemption from withholding c Total income listed on line 13a above that is exempt from tax under this treaty $ 14 Sufficient facts to justify the exemption from withholding claimed on line 12 and/or line 13 (see instructions) Note: Lines 15 through 18 are to be completed only for certain independent personal services (see instructions). 15 Number of personal exemptions 16 How many days will you perform services in claimed the United States during this tax year? 17 Daily personal exemption amount claimed (see instructions) 18 Total personal exemption amount claimed. Multiply line 16 by line 17 Part III Certification Under penalties of perjury, I declare that I have examined the information on this form and to the best of my knowledge and belief it is true, correct, and complete. I further certify under penalties of perjury that: I am the beneficial owner (or am authorized to sign for the beneficial owner) of all the income to which this form relates. The beneficial owner is not a U.S. person. The beneficial owner is a resident of the treaty country listed on line 12a and/or 13b above within the meaning of the income tax treaty between the United States and that country. Furthermore, I authorize this form to be provided to any withholding agent that has control, receipt, or custody of the income of which I am the beneficial owner or any withholding agent that can disburse or make payments of the income of which I am the beneficial owner. Sign Here Signature of beneficial owner (or individual authorized to sign for beneficial owner) Date Part IV Name Withholding Agent Acceptance and Certification Employer identification number Address (number and street) (Include apt. or suite no. or P.O. box, if applicable.) City, state, and ZIP code Telephone number Under penalties of perjury, I certify that I have examined this form and any accompanying statements, that I am satisfied that an exemption from withholding is warranted, and that I do not know or have reason to know that the nonresident alien individual is not entitled to the exemption or that the nonresident alien s eligibility for the exemption cannot be readily determined. Signature of withholding agent Date Form 8233 (Rev )

6 To Whom It May Concern: Personal Statement Letter Effective: January 1, 2014 through December 31, 2014 I am a resident of. I arrived in the United States on (Your Country). I am not a citizen. I have not been lawfully accorded the (Date) privilege of permanently residing in the United States as an immigrant. I have accepted an invitation by the Rutgers, The State University of New Jersey as a and I will be performing I expect to receive $ (Date) (Your Country) (Description of your position at RUTGERS) (Your annual salary in 2014) (Job Title). My start date at the University was and my anticipated return to my country is. (Date) has a tax treaty with the United States under tax treaty Article Number. This treaty exemption is good for years. (per treaty article citation) (Number) Any training I perform will be undertaken in the public interest and not for the private benefit of any specific person or persons. I have attached a copy of my current VISA and a copy of my DS 2019 (J1 VISA) or I-20-ID (Student Copy) (F1 VISA). Print Name Date, 2014 Signature University ID # or SSN

(Job Title). My start date at the University was and my anticipated return to my country is.")

7 SUBSTANTIAL PRESENCE TEST 2014 For Determination of Resident or Non-Resident Alien Tax Status Effective: January 1, 2014 through December 31, 2014 Name: (Last name, First name, Middle Initial) University ID# or SSN: 1. Are you a lawful, permanent resident of the United States? Please check one box Yes No (e.g. If you are a green card holder check Yes.) If you checked Yes, skip sections 2 through 4 and sign and date the bottom of the form. 2. Current VISA status information: Current VISA Status: (e.g. J1, F1, etc.) Issuing Country: Initial Date of U.S. Entry: Note: Your initial date of entry for this VISA type may have occurred in a prior year if this is not your first visit. Expiration Date: 3. Counting Exempt years : Is this your first visit to the U.S.? Please check one box Yes No If Yes, skip to section 4. If NO, complete the following: List all previous years in U.S. under F-1 or J-1 student VISA status. List all previous years in U.S. under J-1 non-student VISA status (e.g. teacher, professor, trainee, alien physicians, researcher, short-term scholar) 4. Substantial Presence Test: Number of days present in the U.S. for the current and two previous years-do not count exempt years. ( Exempt years are defined as the first 5 years in the U.S. for F-1 or J-1 student VISA holders, or 2 of the last 6 years for J-1 non-student VISA holders). Project the last date you expect to be in the U.S. for current year (2013) and enter it here: Current Year 2014 Number of days in U.S. x 1.00 = 1 st previous year 2013 Number of days in U.S. x 0.34 = 2 nd previous year 2012 Number of days in U.S. x 0.17 = Total days counted for U.S. tax residency (sum the values from the 3 rows above) = * *If Total days counted are at least 183, you pass the Substantial Presence Test and will be treated as a resident alien for tax purposes. CERTIFICATION: I certify that the information provided above is true and that I am subject to penalties for perjury if false. In addition, I agree to notify the UMDNJ Payroll Department immediately if any of the information I provided on this form changes. If I fail to do so, the Payroll Department is authorized to begin withholding taxes in accordance with IRS regulations. Signature Date 2014

Issuing Country: Initial Date of U.S. Entry: Note: Your initial date of entry for this VISA type may have occurred in a prior year if this is not your first visit. Expiration Date: 3.")

8 Statement of Income Tax Treaty Benefits Back-to-Back Clause I confirm that I have been notified that the income tax treaty between the U.S. and my country of tax residence,, contains a back-to-back clause. I understand this exemption is available to me only if I have not previously claimed an exemption as a student or trainee in a previous period. I confirm I have not previously claimed such an exemption. Employee Name: SSN/ID: Signature: Date:, 2014 Note : Non-Resident Aliens with J1 Visa from these countries should complete this form : Belgium Czech Republic Egypt Germany Iceland Israel Japan Netherland Norway Philippines Poland Portugal Romania Slovak Republic U.S.S.R.

9 Statement of Retroactive Income Tax Treaty Benefits I confirm that I have been notified that the income tax treaty between the U.S. and my country of tax residence,, contains certain retroactive benefits. I understand my possible tax treaty exemption period is (Original Date of Entry) (Less 1 Day of 2 Years from the (Original Date of Entry); if I remain in the U.S. until or after 2 years, I may be subject to taxation in the U.S. for the entire period of my visit. At this time, I do not expect to remain in the U.S. for a period longer that the allowed tax treaty time limit (Two Years from the Original Date of Entry to the U.S.). I confirm that I believe I qualify for an exemption from tax based on the U.S. treaty and it is my choice to claim the tax treaty exemption. If my expected stay in the U.S. changes, I will notify the Sr. Accountant in Payroll Services at as soon as possible to end the tax treaty exemption. Employee Name: SSN/ID: Signature: Date: Note : Non-Resident Aliens with J1 Visa from these countries should complete this form : India Luxembourg Netherlands Philippines U.K.

. I confirm that I believe I qualify for an exemption from tax based on the U.S. treaty and it is my choice to claim the tax treaty exemption. If my expected stay in the U.S. changes, I will notify the Sr.")

10

Instructions for Form 8233 (Rev. June 2011)

") Instructions for Form 8233 (Rev. June 2011) Department of the Treasury Internal Revenue Service (Use with the March 2009 revision of Form 8233.) Exemption From Withholding on Compensation for Independent

Instructions for Form 8233 (Rev. June 2011) Department of the Treasury Internal Revenue Service (Use with the March 2009 revision of Form 8233.) Exemption From Withholding on Compensation for Independent

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

U.S. Taxation of J-1 Exchange Visitors

U.S. Taxation of J-1 Exchange Visitors By Paula N. Singer, Esq. 1 ONESOURCE TAX INFORMATION REPORTING The J-1 Exchange Visitor Program has long been used by institutions of higher education, teaching hospitals

U.S. Taxation of J-1 Exchange Visitors By Paula N. Singer, Esq. 1 ONESOURCE TAX INFORMATION REPORTING The J-1 Exchange Visitor Program has long been used by institutions of higher education, teaching hospitals

Davy Select Telephone Trading Account (Execution-Only)

") www.davyselect.ie Davy Select Telephone Trading Account (Execution-Only) Application Form Thank you for choosing Davy Select Please read the accompanying Execution-Only Service Terms (and related documentation)

www.davyselect.ie Davy Select Telephone Trading Account (Execution-Only) Application Form Thank you for choosing Davy Select Please read the accompanying Execution-Only Service Terms (and related documentation)

MIT U.S. Income Tax Presentation Non US Resident Students

MIT U.S. Income Tax Presentation Non US Resident Students PwC Boston Nabih Daaboul Carol McNeil Rich Wagman 1 Basic U.S. Tax Overview for International Students A foreign national is a person born outside

MIT U.S. Income Tax Presentation Non US Resident Students PwC Boston Nabih Daaboul Carol McNeil Rich Wagman 1 Basic U.S. Tax Overview for International Students A foreign national is a person born outside

Tax Treaty Benefits for Workers, Trainees, Students, and Researchers

Tax Treaty Benefits for Workers, Trainees, Students, and Researchers By Paula N. Singer, Esq. 1 ONESOURCE NONRESIDENT ALIEN TAXATION As organizations, both large and small, become increasingly more global,

Tax Treaty Benefits for Workers, Trainees, Students, and Researchers By Paula N. Singer, Esq. 1 ONESOURCE NONRESIDENT ALIEN TAXATION As organizations, both large and small, become increasingly more global,

Davy Select Trading Account (Execution-Only)

") www.davyselect.ie Davy Select Trading Account (Execution-Only) Application Form Thank you for choosing Davy Select The Davy Select Trading Account (Execution- Only) is designed for those who are comfortable

www.davyselect.ie Davy Select Trading Account (Execution-Only) Application Form Thank you for choosing Davy Select The Davy Select Trading Account (Execution- Only) is designed for those who are comfortable

Personal Deposit Account Application

Personal Deposit Account Application Banking Made Easier This Quick Start Form Makes It Easy To Open Your New Accounts. Go ahead. Tell us how you want to bank. 1. Start Right Here. This application makes

Personal Deposit Account Application Banking Made Easier This Quick Start Form Makes It Easy To Open Your New Accounts. Go ahead. Tell us how you want to bank. 1. Start Right Here. This application makes

Guide for filing a United States Non-Resident Income Tax Return

Guide for filing a United States Non-Resident Income Tax Return Tax Year 2012 Prepared for Re:Sound By Deloitte LLP, Global Employer Services, Toronto September 6, 2013 Deloitte LLP and affiliated entities.

Guide for filing a United States Non-Resident Income Tax Return Tax Year 2012 Prepared for Re:Sound By Deloitte LLP, Global Employer Services, Toronto September 6, 2013 Deloitte LLP and affiliated entities.

Policy and Procedure Manual

RENSSELAER POLYTECHNIC INSTITUTE Payments Made to Nonresident Aliens Policy and Procedure Manual Payments Made to Nonresident Aliens Policy & Procedure Manual Page 1 of 36 Updated February 2010 TABLE OF

RENSSELAER POLYTECHNIC INSTITUTE Payments Made to Nonresident Aliens Policy and Procedure Manual Payments Made to Nonresident Aliens Policy & Procedure Manual Page 1 of 36 Updated February 2010 TABLE OF

INTERNATIONAL TAX LAW FREQUENTLY ASKED QUESTIONS

INTERNATIONAL TAX LAW FREQUENTLY ASKED QUESTIONS 1 Table of Contents Page(s) Basic Rules of U.S. Taxation 3 Canadian Questions 4 Capital Gain Income (Nonresidents) 5 Currency Issues 6 Determination of

INTERNATIONAL TAX LAW FREQUENTLY ASKED QUESTIONS 1 Table of Contents Page(s) Basic Rules of U.S. Taxation 3 Canadian Questions 4 Capital Gain Income (Nonresidents) 5 Currency Issues 6 Determination of

Nonresident Alien Tax Issues and the GLACIER System. A Primer

Nonresident Alien Tax Issues and the System A Primer April 4, 2014 Objectives Review Nonresident Alien tax issues Glacier: Who, What, Where, When & Why? Online Demonstration Pay Period Implications to

Nonresident Alien Tax Issues and the System A Primer April 4, 2014 Objectives Review Nonresident Alien tax issues Glacier: Who, What, Where, When & Why? Online Demonstration Pay Period Implications to

Nonresident Alien Reference Guide

Nonresident Alien Reference Guide - 1 - Definition Nonresident Alien (NRA) is defined as any employee who is NOT a United States Citizen or a Permanent Resident (Resident Alien or Green Card holder). Responsibilities

Nonresident Alien Reference Guide - 1 - Definition Nonresident Alien (NRA) is defined as any employee who is NOT a United States Citizen or a Permanent Resident (Resident Alien or Green Card holder). Responsibilities

Frequently Asked Questions for Non Resident Alien Taxation

Frequently Asked Questions for Non Resident Alien Taxation A. Income 1. Compensation I worked abroad for the summer. Do I have to include this income on my tax return? 2. Scholarships and Fellowships I

Frequently Asked Questions for Non Resident Alien Taxation A. Income 1. Compensation I worked abroad for the summer. Do I have to include this income on my tax return? 2. Scholarships and Fellowships I

U.S. Immigration System. Processing Payments

U.S. Immigration System Typical Temporary Visas Used by Institutions of Higher Education Residency Status for IRS Tax Purposes Processing Payments 2 Basic Types of Immigration into the U.S. PERMANENT

U.S. Immigration System Typical Temporary Visas Used by Institutions of Higher Education Residency Status for IRS Tax Purposes Processing Payments 2 Basic Types of Immigration into the U.S. PERMANENT

Professional Services Agreement. Frequently Asked Questions

Professional Services Agreements Frequently Asked Questions Acronyms used throughout the Frequently Asked Questions Nonresident Alien Social Security Administration Social Security Number Individual Tax

Professional Services Agreements Frequently Asked Questions Acronyms used throughout the Frequently Asked Questions Nonresident Alien Social Security Administration Social Security Number Individual Tax

Payments Made to Nonresident Aliens

Payments Made to Nonresident Aliens Procedure Manual This Procedures for Payments Made to Nonresident Aliens guide was prepared by Arctic International LLC in connection with Loyola Marymount University

Payments Made to Nonresident Aliens Procedure Manual This Procedures for Payments Made to Nonresident Aliens guide was prepared by Arctic International LLC in connection with Loyola Marymount University

2. Since I already had taxes withheld from my paycheck, do I need to file an income tax return?

GENERAL FILING REQUIREMENTS 1. Who needs to file an income tax return? If you are visiting the U.S. from another country on an F, J, M or Q visa and are classified as a nonresident for U.S. tax purposes,

GENERAL FILING REQUIREMENTS 1. Who needs to file an income tax return? If you are visiting the U.S. from another country on an F, J, M or Q visa and are classified as a nonresident for U.S. tax purposes,

2015 Publication 4011

01 Publication 4011 Foreign Student and Scholar Volunteer Resource Guide For Use in Preparing Tax Year 01 Returns»» Volunteer Income Tax Assistance (VITA)»» Tax Counseling for the Elderly (TCE) For the

01 Publication 4011 Foreign Student and Scholar Volunteer Resource Guide For Use in Preparing Tax Year 01 Returns»» Volunteer Income Tax Assistance (VITA)»» Tax Counseling for the Elderly (TCE) For the

1. All supplier invoices must be emailed as individual attachments to LyndenAPinvoices@Lynden.com. PDF format is preferred.

ATTN: Accounts Receivable/Billing Department/Credit Department As a valued supplier of the Lynden family of companies, please follow the guidelines below to ensure your invoices are processed completely

ATTN: Accounts Receivable/Billing Department/Credit Department As a valued supplier of the Lynden family of companies, please follow the guidelines below to ensure your invoices are processed completely

DISCLAIMER. The information contained in this presentation is current as of the date it was presented. It should not be considered official guidance.

DISCLAIMER The information contained in this presentation is current as of the date it was presented. It should not be considered official guidance. 1 INTRODUCTION This webinar is intended to provide basic

DISCLAIMER The information contained in this presentation is current as of the date it was presented. It should not be considered official guidance. 1 INTRODUCTION This webinar is intended to provide basic

Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services

University of Washington Student Fiscal Services") Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services Agenda Important Information for 2012 Returns U. S. Source of Income Scholarships Fellowships Tuition Waivers Prizes Stipends

Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services Agenda Important Information for 2012 Returns U. S. Source of Income Scholarships Fellowships Tuition Waivers Prizes Stipends

Immigration and Tax Compliance on Payments to Foreign National (FN) Independent Contractors and Guest Speakers

Independent Contractors and Guest Speakers") Immigration and Tax Compliance on Payments to Foreign National (FN) Independent Contractors and Guest Speakers WHY? Federal Law System Changes Who does this policy apply to? How many foreign national independent

Immigration and Tax Compliance on Payments to Foreign National (FN) Independent Contractors and Guest Speakers WHY? Federal Law System Changes Who does this policy apply to? How many foreign national independent

Tax Information for Foreign National Students/Scholars/Researchers

Tax Information for Foreign National Students/Scholars/Researchers Disclaimer: This is general information designed to assist nonresident aliens with questions about their tax status, tax return filing

Tax Information for Foreign National Students/Scholars/Researchers Disclaimer: This is general information designed to assist nonresident aliens with questions about their tax status, tax return filing

Welcome to Tax Orientation for International Students & Scholars for the 2014 Filing Season. Marea Clarke Paul Cullen

Welcome to Tax Orientation for International Students & Scholars for the 2014 Filing Season Marea Clarke Paul Cullen Agenda Overview of US Tax System International Student Tax Clinics Clinic Process &

Welcome to Tax Orientation for International Students & Scholars for the 2014 Filing Season Marea Clarke Paul Cullen Agenda Overview of US Tax System International Student Tax Clinics Clinic Process &

Welcome to Tax Orientation for International Students & Scholars for the 2013 Filing Season" Marea Clarke" Paul Cullen

Welcome to Tax Orientation for International Students & Scholars for the 2013 Filing Season" Marea Clarke" Paul Cullen Overview of the U.S. Income Tax System" Your employer withholds from your earnings

Welcome to Tax Orientation for International Students & Scholars for the 2013 Filing Season" Marea Clarke" Paul Cullen Overview of the U.S. Income Tax System" Your employer withholds from your earnings

Frequently Asked Tax Questions 2014 Tax Filing Season

Frequently Asked Tax Questions 2014 Tax Filing Season Q. How do I determine if I am a resident alien for tax purposes? A. F-1, J-1, M or Q students are considered non-residents for tax purposes for their

Frequently Asked Tax Questions 2014 Tax Filing Season Q. How do I determine if I am a resident alien for tax purposes? A. F-1, J-1, M or Q students are considered non-residents for tax purposes for their

7/22/2013. Failure to follow taxation regulations applicable to Foreign Nationals only affects the employee? Training Objectives

FOREIGN NATIONALS TAX COMPLIANCE TRAINING How To Optimize Your Processing of Foreign Nationals and Current Issues Update July 25, 2013 Presenters Jennifer Pacheco, Foreign Nationals Tax Compliance Program

FOREIGN NATIONALS TAX COMPLIANCE TRAINING How To Optimize Your Processing of Foreign Nationals and Current Issues Update July 25, 2013 Presenters Jennifer Pacheco, Foreign Nationals Tax Compliance Program

U.S. Tax Guide for Aliens

Publication 519 Contents U.S. Tax Guide for Aliens Introduction.................. 1 Cat. No. 15023T Department of the Treasury Internal Revenue Service For use in preparing 2015 Returns What's New... 2

Publication 519 Contents U.S. Tax Guide for Aliens Introduction.................. 1 Cat. No. 15023T Department of the Treasury Internal Revenue Service For use in preparing 2015 Returns What's New... 2

FNIS Set Up and Data Entry For State Agencies

S T A T E W I D E F O R E I G N N A T I O N A L T A X C O M P L I A N C E P R O G R A M FNIS Set Up and Data Entry For State Agencies O f f i c e o f t h e S t a t e C o n t r o l l e r S t a t e o f N

S T A T E W I D E F O R E I G N N A T I O N A L T A X C O M P L I A N C E P R O G R A M FNIS Set Up and Data Entry For State Agencies O f f i c e o f t h e S t a t e C o n t r o l l e r S t a t e o f N

International Student Taxes. Information compiled by International Student Services

International Student Taxes Information compiled by International Student Services International Student Taxes The Basics Specific Tax Scenarios What You Can Do Now Resolving Tax Issues Top Ten Tax Myths

International Student Taxes Information compiled by International Student Services International Student Taxes The Basics Specific Tax Scenarios What You Can Do Now Resolving Tax Issues Top Ten Tax Myths

Instructions for Form 1040NR-EZ U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents

2009 Instructions for Form 1040NR-EZ U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Department of the Treasury Internal Revenue Service Section references are to the Internal

2009 Instructions for Form 1040NR-EZ U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Department of the Treasury Internal Revenue Service Section references are to the Internal

United States Taxation for International Students. Introduction to U.S. Taxation Rules, Tax Withholding and Tax Treaties

United States Taxation for International Students Introduction to U.S. Taxation Rules, Tax Withholding and Tax Treaties 1 Disclaimer Please keep in mind that University of Arizona employees, while in their

United States Taxation for International Students Introduction to U.S. Taxation Rules, Tax Withholding and Tax Treaties 1 Disclaimer Please keep in mind that University of Arizona employees, while in their

TAX GUIDE FOR FOREIGN VISITORS

TAX GUIDE FOR FOREIGN VISITORS FOR USE BY: All Employees and Students Anne E. Davenport, CPA October 2012 Table of Contents Introduction...1 Section 1: Definition of Terms...2 1.1 Candidate for a Degree......

TAX GUIDE FOR FOREIGN VISITORS FOR USE BY: All Employees and Students Anne E. Davenport, CPA October 2012 Table of Contents Introduction...1 Section 1: Definition of Terms...2 1.1 Candidate for a Degree......

Nonresident Tax Information Session. Thursday, March 6, 2014 5 to 6 PM McConomy Auditorium, University Center

Nonresident Tax Information Session Thursday, March 6, 2014 5 to 6 PM McConomy Auditorium, University Center What we will cover. 1. Federal tax issues 2. Forms you receive and fill out 3. Determination

Nonresident Tax Information Session Thursday, March 6, 2014 5 to 6 PM McConomy Auditorium, University Center What we will cover. 1. Federal tax issues 2. Forms you receive and fill out 3. Determination

Prepared by the Disbursing Office This replaces Administrative Procedure No. A8.868 dated December 1993 A8.868 July 1996

Prepared by the Disbursing Office This replaces Administrative Procedure No. A8.868 dated December 1993 A8.868 July 1996 A8.868 Disbursing/Accounts Payable and Payroll p 1 of 53 A8.868 Reporting and Withholding

Prepared by the Disbursing Office This replaces Administrative Procedure No. A8.868 dated December 1993 A8.868 July 1996 A8.868 Disbursing/Accounts Payable and Payroll p 1 of 53 A8.868 Reporting and Withholding

Federal Income Tax Brochure

P R O F E S S I O N A L N E T W O R K S International Student and Scholar Advising Federal Income Tax Brochure James Tenney, Judy Todd, Robin Catmur February, 2011 The information contained in this resource

P R O F E S S I O N A L N E T W O R K S International Student and Scholar Advising Federal Income Tax Brochure James Tenney, Judy Todd, Robin Catmur February, 2011 The information contained in this resource

BASIC TAX WORKSHOP FOR INT L STUDENTS. Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2016

BASIC TAX WORKSHOP FOR INT L STUDENTS Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2016 MIT International Students Office & Office of the Vice President

BASIC TAX WORKSHOP FOR INT L STUDENTS Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2016 MIT International Students Office & Office of the Vice President

WEST USA REALTY, PROPERTY MANAGEMENT 16150 N ARROWHEAD FOUNTAIN CENTER DR # 100 PEORIA, ARIZONA 85382 602-942-1410 BROKER S OBLIGATIONS

WEST USA REALTY, PROPERTY MANAGEMENT 16150 N ARROWHEAD FOUNTAIN CENTER DR # 100 PEORIA, ARIZONA 85382 602-942-1410 AGENT NAME: DATE: This agreement by and between WEST USA REALTY, hereafter know as BROKER,

WEST USA REALTY, PROPERTY MANAGEMENT 16150 N ARROWHEAD FOUNTAIN CENTER DR # 100 PEORIA, ARIZONA 85382 602-942-1410 AGENT NAME: DATE: This agreement by and between WEST USA REALTY, hereafter know as BROKER,

Substitute W-4P Tax Withholding Certificate for Pension or Annuity Payments Wis. Stat. 40.08 (1)

") Substitute W-4P Tax Withholding Certificate for Pension or Annuity Payments Wis. Stat. 40.08 (1) Wisconsin Department of Employee Trust Funds 801 W Badger Road PO Box 7931 Madison WI 53707-7931 1-877-533-5020

Substitute W-4P Tax Withholding Certificate for Pension or Annuity Payments Wis. Stat. 40.08 (1) Wisconsin Department of Employee Trust Funds 801 W Badger Road PO Box 7931 Madison WI 53707-7931 1-877-533-5020

Federal Agency Seminar 2011. Withholding and Reporting of Tax on Wage Payments to Foreign Persons

Federal Agency Seminar 2011 Withholding and Reporting of Tax on Wage Payments to Foreign Persons 1 Objectives Know why tax residency is important Which income non-resident alien are subject to FIT withholding

Federal Agency Seminar 2011 Withholding and Reporting of Tax on Wage Payments to Foreign Persons 1 Objectives Know why tax residency is important Which income non-resident alien are subject to FIT withholding

Internal Revenue Service Wage and Investment

Internal Revenue Service Wage and Investment Stakeholder Partnerships, Education and Communication Winter/Spring 2015 Income Tax Workshop for Nonresident Aliens Please Note This workshop is for students

Internal Revenue Service Wage and Investment Stakeholder Partnerships, Education and Communication Winter/Spring 2015 Income Tax Workshop for Nonresident Aliens Please Note This workshop is for students

Instructions for Form 1040NR-EZ

2012 Instructions for Form 1040NR-EZ Department of the Treasury Internal Revenue Service U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Section references are to the Internal

2012 Instructions for Form 1040NR-EZ Department of the Treasury Internal Revenue Service U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Section references are to the Internal

Employee Name: Employee # Department (if applicable): Position Description:

: Position Description:") ADMIN: Rec d Dt Via Processed by Date Add/change done E-Verify done File Cabinet Employee Action Form ***See New Employee Checklist Below Employer Name: Employer Location (if applicable): Action (mark

ADMIN: Rec d Dt Via Processed by Date Add/change done E-Verify done File Cabinet Employee Action Form ***See New Employee Checklist Below Employer Name: Employer Location (if applicable): Action (mark

Prepared by Mark Brockman, CPA 6435 Lindyann Lane, Houston, TX 77008-3233 (832) 408-3963 (evenings/weekends) e-mail: BrockmanPC@sbcglobal.

408-3963 (evenings/weekends) e-mail: BrockmanPC@sbcglobal.") International Students and Scholars Taxation Workshop The University of Texas M.D. Anderson Cancer Center Academic and Visa Administration February 18, 2015 Prepared by Mark Brockman, CPA 6435 Lindyann

International Students and Scholars Taxation Workshop The University of Texas M.D. Anderson Cancer Center Academic and Visa Administration February 18, 2015 Prepared by Mark Brockman, CPA 6435 Lindyann

PREVENTIVE LAW SERIES. Legal Assistance Program APPLYING FOR AN INDIVIDUAL TAXPAYER IDENTIFICATION NUMBER

PREVENTIVE LAW SERIES Legal Assistance Program TOPIC: APPLYING FOR AN INDIVIDUAL TAXPAYER IDENTIFICATION NUMBER October 2014 If you have questions concerning the topic of this pamphlet, please contact

PREVENTIVE LAW SERIES Legal Assistance Program TOPIC: APPLYING FOR AN INDIVIDUAL TAXPAYER IDENTIFICATION NUMBER October 2014 If you have questions concerning the topic of this pamphlet, please contact

International Student Employment FAQs

International Student Employment FAQs Introduction May I work while at Northeastern University? How do I look for a job? What do I have to do once I am hired? Do I need a Social Security Number to Work?

International Student Employment FAQs Introduction May I work while at Northeastern University? How do I look for a job? What do I have to do once I am hired? Do I need a Social Security Number to Work?

TENNESSEE CONSOLIDATED RETIREMENT SYSTEM 502 Deaderick Street Nashville, Tennessee 37243-0201 1-800-770-8277 http://tcrs.tn.gov

Retirement Application for Service or Early Retirement Benefits TENNESSEE CONSOLIDATED RETIREMENT SYSTEM 502 Deaderick Street Nashville, Tennessee 37243-0201 1-800-770-8277 http://tcrs.tn.gov Refer to

Retirement Application for Service or Early Retirement Benefits TENNESSEE CONSOLIDATED RETIREMENT SYSTEM 502 Deaderick Street Nashville, Tennessee 37243-0201 1-800-770-8277 http://tcrs.tn.gov Refer to

University of Northern Iowa

University of Northern Iowa Direct Deposit of Payroll Authorization Form Name (Please Print) (Last, First, MI) UNI ID# I hereby authorize the University of Northern Iowa to initiate direct deposit credit

University of Northern Iowa Direct Deposit of Payroll Authorization Form Name (Please Print) (Last, First, MI) UNI ID# I hereby authorize the University of Northern Iowa to initiate direct deposit credit

Tax Information for International Students and Scholars. Contents

MARCH 2011 Tax Information for International Students and Scholars Contents 1. Tax Information for International Students and Scholars 2. Tax Preparation Software: CINTAX and other programs 3. Tax Filing

MARCH 2011 Tax Information for International Students and Scholars Contents 1. Tax Information for International Students and Scholars 2. Tax Preparation Software: CINTAX and other programs 3. Tax Filing

Frequently Asked Questions

Frequently Asked Questions Questions and answers are divided into the following topics BEFORE USING GLACIER Tax Prep ENTERING DATA INTO GLACIER Tax Prep RESULTS FROM GLACIER Tax Prep WHAT TO DO WHEN FINISHED

Frequently Asked Questions Questions and answers are divided into the following topics BEFORE USING GLACIER Tax Prep ENTERING DATA INTO GLACIER Tax Prep RESULTS FROM GLACIER Tax Prep WHAT TO DO WHEN FINISHED

Student Employee Onboarding Checklist

Student Employee Onboarding Checklist US Ci zen The final component of the University of Pi sburgh s student hiring process is for you to complete this onboarding checklist along with the required documents.

Student Employee Onboarding Checklist US Ci zen The final component of the University of Pi sburgh s student hiring process is for you to complete this onboarding checklist along with the required documents.

TAX INFORMATION SESSION FOR INTERNATIONAL STUDENTS AND SCHOLARS

TAX INFORMATION SESSION FOR INTERNATIONAL STUDENTS AND SCHOLARS Presented by: Lisa Kosiewicz Doran International Student Specialist Office of International Programs Sarah Hintz, CPA Tax and Compliance

TAX INFORMATION SESSION FOR INTERNATIONAL STUDENTS AND SCHOLARS Presented by: Lisa Kosiewicz Doran International Student Specialist Office of International Programs Sarah Hintz, CPA Tax and Compliance

Application for Extension of Time To File an Exempt Organization Return

Form 8868 (Rev. January 2014) Department of the Treasury Internal Revenue Service for Extension of Time To File an Exempt Organization File a separate application for each return. Information about Form

Form 8868 (Rev. January 2014) Department of the Treasury Internal Revenue Service for Extension of Time To File an Exempt Organization File a separate application for each return. Information about Form

Request to Transfer Ownership and/or Change Beneficiaries

Allianz Life Insurance Company of North America PO Box 59060 Minneapolis, MN 55459-0060 Phone: 800.950.1962 Fax: 763.582.6006 allianzlife.com Request to Transfer Ownership and/or Change Beneficiaries The

Allianz Life Insurance Company of North America PO Box 59060 Minneapolis, MN 55459-0060 Phone: 800.950.1962 Fax: 763.582.6006 allianzlife.com Request to Transfer Ownership and/or Change Beneficiaries The

Note: Form 2553 begins on the next page.

Note: Form 2553 begins on the next page. Cincinnati Fax Number for Filing Form 2553 Has Changed The fax number for filing Form 2553 with the IRS center in Cincinnati has changed. The new number is 855-270-4081.

Note: Form 2553 begins on the next page. Cincinnati Fax Number for Filing Form 2553 Has Changed The fax number for filing Form 2553 with the IRS center in Cincinnati has changed. The new number is 855-270-4081.

Instructions for Form 1040NR-EZ

2010 Instructions for Form 1040NR-EZ U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Department of the Treasury Internal Revenue Service Section references are to the Internal

2010 Instructions for Form 1040NR-EZ U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Department of the Treasury Internal Revenue Service Section references are to the Internal

Withholding of Tax on Nonresident Aliens and Foreign Entities

Department of the Treasury Internal Revenue Service Publication 515 Cat. No. 15019L Withholding of Tax on Nonresident Aliens and Foreign Entities For use in 2013 Contents What's New... 1 Reminders... 2

Department of the Treasury Internal Revenue Service Publication 515 Cat. No. 15019L Withholding of Tax on Nonresident Aliens and Foreign Entities For use in 2013 Contents What's New... 1 Reminders... 2

Scholarships awarded to Nonresident Alien Students

Scholarships awarded to Nonresident Alien Students IRS Compliance Issues Doug Podoll Georgia State University dougpodoll@gsu.edu, 404-413-2070 General Rule Section 1441 of the Internal Revenue Code states

Scholarships awarded to Nonresident Alien Students IRS Compliance Issues Doug Podoll Georgia State University dougpodoll@gsu.edu, 404-413-2070 General Rule Section 1441 of the Internal Revenue Code states

J-1 Exchange Visitors

THE UNIVERSITY OF TEXAS AT EL PASO J-1 Exchange Visitors INSTRUCTIONS & APPLICATION INFORMATION / UTEP DEPARTMENTS 2014-2015 WHAT IS A J-1 EXCHANGE VISITOR? The J-1 visa is used for foreign national exchange

THE UNIVERSITY OF TEXAS AT EL PASO J-1 Exchange Visitors INSTRUCTIONS & APPLICATION INFORMATION / UTEP DEPARTMENTS 2014-2015 WHAT IS A J-1 EXCHANGE VISITOR? The J-1 visa is used for foreign national exchange

US Federal Income Tax for F-1 Student Visa Holders

1 US Federal Income Tax for F-1 Student Visa Holders 2 Please do not mistake the following information for tax advice; the following slides are intended for use as a frame of reference for the US Federal

1 US Federal Income Tax for F-1 Student Visa Holders 2 Please do not mistake the following information for tax advice; the following slides are intended for use as a frame of reference for the US Federal

Organizations with Foreign Employees Face Compliance Challenges

Organizations with Foreign Employees Face Compliance Challenges By Paula N. Singer, Esq. ONESOURCE NONRESIDENT ALIEN TAXATION In this global economy, U.S. employers both large and small routinely employ

Organizations with Foreign Employees Face Compliance Challenges By Paula N. Singer, Esq. ONESOURCE NONRESIDENT ALIEN TAXATION In this global economy, U.S. employers both large and small routinely employ

IRS FORM 1099 REPORTING REQUIREMENTS

IRS FORM 1099 REPORTING REQUIREMENTS The Internal Revenue Service (IRS) requires businesses (including not-for-profit organizations) to issue a Form 1099 to any individual or unincorporated business paid

IRS FORM 1099 REPORTING REQUIREMENTS The Internal Revenue Service (IRS) requires businesses (including not-for-profit organizations) to issue a Form 1099 to any individual or unincorporated business paid

Opening Your International Charles Schwab Stock Plan Account

Opening Your International Charles Schwab Stock Plan Account Online Process Approximately 15 20 Minutes Through Charles Schwab, you can open and manage your account online by following the detailed instructions

Opening Your International Charles Schwab Stock Plan Account Online Process Approximately 15 20 Minutes Through Charles Schwab, you can open and manage your account online by following the detailed instructions

Guide to completing W-8BEN-E entity US tax forms

Guide to completing W-8BEN-E entity US tax forms Applicable to Companies, Trusts, Self-Managed Superannuation Funds and Deceased Estates Macquarie Wrap 1 macquarie.com Contents 1 General information 01

Guide to completing W-8BEN-E entity US tax forms Applicable to Companies, Trusts, Self-Managed Superannuation Funds and Deceased Estates Macquarie Wrap 1 macquarie.com Contents 1 General information 01

Foreign Buyer s Guide

Foreign Buyer s Guide PINNACLE PEAK ARROWHEAD SURPRISE KIERLAND PARADISE VALLEY CAMELBACK PALM VALLEY SUNLAND LAKESHORE AHWATUKEE Ahwatukee 15215 S. 48th St. Building 5 Suite 154 Phoenix, AZ 85044 (480)

Foreign Buyer s Guide PINNACLE PEAK ARROWHEAD SURPRISE KIERLAND PARADISE VALLEY CAMELBACK PALM VALLEY SUNLAND LAKESHORE AHWATUKEE Ahwatukee 15215 S. 48th St. Building 5 Suite 154 Phoenix, AZ 85044 (480)

Understanding your Forms W-2 and 1042-S

Understanding your Forms W-2 and 1042-S Each year, employees will receive a Form W-2 that provides details of prior year earnings, taxes withheld and other miscellaneous data (such as cost of employer

Understanding your Forms W-2 and 1042-S Each year, employees will receive a Form W-2 that provides details of prior year earnings, taxes withheld and other miscellaneous data (such as cost of employer

Application for Part-Time Employment LSU Athletics Gameday Event Staff

Application for Part-Time Employment LSU Athletics Gameday Event Staff Please follow the directions below, take your time and print neatly. Be sure to review all pages for accuracy. Incomplete packets

Application for Part-Time Employment LSU Athletics Gameday Event Staff Please follow the directions below, take your time and print neatly. Be sure to review all pages for accuracy. Incomplete packets

Tax Issues Associated with Reporting Fellowships

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Marcia Johnson Senior Tax Analyst Benjamin Tsai Senior Tax Analyst

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Marcia Johnson Senior Tax Analyst Benjamin Tsai Senior Tax Analyst

Form W-8BEN Completion & Submission Guidelines for Corbis Corporation Contributors

Form W-8BEN Completion & Submission Guidelines for Corbis Corporation Contributors Overview - Corbis Corporation, a US corporation, is required to deduct 30% withholding tax from royalties paid to individuals

Form W-8BEN Completion & Submission Guidelines for Corbis Corporation Contributors Overview - Corbis Corporation, a US corporation, is required to deduct 30% withholding tax from royalties paid to individuals

Instructions for Form 1040NR-EZ

2011 Instructions for Form 1040NR-EZ U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Department of the Treasury Internal Revenue Service Section references are to the Internal

2011 Instructions for Form 1040NR-EZ U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Department of the Treasury Internal Revenue Service Section references are to the Internal

Foreign Investment in Real Property Tax Act 1980 Buyer AND Seller Beware. By R. Scott Jones, Esq.

Foreign Investment in Real Property Tax Act 1980 Buyer AND Seller Beware By R. Scott Jones, Esq. This article summarizes the tax withholding rules imposed on a buyer and his/her agent when purchasing U.S.

Foreign Investment in Real Property Tax Act 1980 Buyer AND Seller Beware By R. Scott Jones, Esq. This article summarizes the tax withholding rules imposed on a buyer and his/her agent when purchasing U.S.

8/19/2010 FOREIGN NATIONAL TAX COMPLIANCE TRAINING. Best Practices and Policies and Procedures Update for State Agencies. Panelist

FOREIGN NATIONAL TAX COMPLIANCE TRAINING Best Practices and Policies and Procedures Update for State Agencies August 18, 2010 Panelist Michelle Anderson, Foreign National Tax Specialist NC State University

FOREIGN NATIONAL TAX COMPLIANCE TRAINING Best Practices and Policies and Procedures Update for State Agencies August 18, 2010 Panelist Michelle Anderson, Foreign National Tax Specialist NC State University

Book Outline TABLE OF CONTENTS PREFACE PART I. INTERNATIONAL ASPECTS OF INDIVIDUAL U.S. TAX RETURNS. Background Information

US Tax Compliance For Immigrants And Book Outline TABLE OF CONTENTS PREFACE PART I. INTERNATIONAL ASPECTS OF INDIVIDUAL U.S. TAX RETURNS Background Information Chapter 1. Introduction 1.1 Immigration Basics

US Tax Compliance For Immigrants And Book Outline TABLE OF CONTENTS PREFACE PART I. INTERNATIONAL ASPECTS OF INDIVIDUAL U.S. TAX RETURNS Background Information Chapter 1. Introduction 1.1 Immigration Basics

PAYROLL CLIENT EMPLOYEE SETUP FORM

EMPLOYEE INFORMATION EMPLOYEE DEMOGRAPHIC INFORMATION Employee ID EIN/SSN # First Name Middle Initial Last Name TAXING (HOME) ADDRESS: Address PAYROLL CLIENT EMPLOYEE SETUP FORM EMPLOYMENT/PERSONAL INFORMATION

EMPLOYEE INFORMATION EMPLOYEE DEMOGRAPHIC INFORMATION Employee ID EIN/SSN # First Name Middle Initial Last Name TAXING (HOME) ADDRESS: Address PAYROLL CLIENT EMPLOYEE SETUP FORM EMPLOYMENT/PERSONAL INFORMATION

Verifying Lawful Presence

Verifying Lawful Presence An applicant for a driver license (DL) or identification card (ID) must present proof of lawful presence in the US. The table on the following pages describes the acceptable documents

Verifying Lawful Presence An applicant for a driver license (DL) or identification card (ID) must present proof of lawful presence in the US. The table on the following pages describes the acceptable documents

New Hire Submission and Return Receipt PLEASE SUBMIT FORMS TO: SERVICE@ADVANCEDPEO.COM OR FAX 1-866-611-9598

1933 E EDGEWOOD DR SUITE 102 LAKELAND, FL 33803 1-877-518-2881 WWW.ADVANCEDPEO.COM New Hire Submission and Return Receipt PLEASE SUBMIT FORMS TO: SERVICE@ADVANCEDPEO.COM OR FAX 1-866-611-9598 Notice to

1933 E EDGEWOOD DR SUITE 102 LAKELAND, FL 33803 1-877-518-2881 WWW.ADVANCEDPEO.COM New Hire Submission and Return Receipt PLEASE SUBMIT FORMS TO: SERVICE@ADVANCEDPEO.COM OR FAX 1-866-611-9598 Notice to

Overseas Resident Trading Account Application Pack

Overseas Resident Trading Account Application Pack Thank you for choosing to open a Computershare Trading Account. Should you have any queries about completing your account application, please contact

Overseas Resident Trading Account Application Pack Thank you for choosing to open a Computershare Trading Account. Should you have any queries about completing your account application, please contact

Limited Liability Company (LLC) Questionnaire

Questionnaire") Limited Liability Company (LLC) Questionnaire (See page 3 for instructions.) CLIENT INFORMATION 1. Client 2. Contact Info: Phone Email 3. Client Washington 732 Broadway, Suite 201 Tacoma, WA 98402 Fax:

Limited Liability Company (LLC) Questionnaire (See page 3 for instructions.) CLIENT INFORMATION 1. Client 2. Contact Info: Phone Email 3. Client Washington 732 Broadway, Suite 201 Tacoma, WA 98402 Fax:

CALIFORNIA PRODUCER APPOINTMENT PACKAGE

CALIFORNIA PRODUCER APPOINTMENT PACKAGE Please complete the attached application in its entirety and submit it Multi-State Insurance Services, Inc. via one of the options listed below: Mail: E-Mail: Multi-State

CALIFORNIA PRODUCER APPOINTMENT PACKAGE Please complete the attached application in its entirety and submit it Multi-State Insurance Services, Inc. via one of the options listed below: Mail: E-Mail: Multi-State

Overview: Inviting and Paying Foreign Visitors

Overview: Inviting and Paying Foreign Visitors This article is intended to be a brief reference for departments that are planning to pay foreign visitors who are considered nonresident aliens for services

Overview: Inviting and Paying Foreign Visitors This article is intended to be a brief reference for departments that are planning to pay foreign visitors who are considered nonresident aliens for services

CONTRACTOR APPLICATION HOUSING REHABILITATION PROGRAM

CITY OF GALVESTON GRANTS & HOUSING DEPARTMENT P.O. Box 779 Galveston, Texas 77553 Office (409) 797 3820 Fax (409) 797 3888 CONTRACTOR APPLICATION HOUSING REHABILITATION PROGRAM CONTRACTOR APPLICATION HOUSING

CITY OF GALVESTON GRANTS & HOUSING DEPARTMENT P.O. Box 779 Galveston, Texas 77553 Office (409) 797 3820 Fax (409) 797 3888 CONTRACTOR APPLICATION HOUSING REHABILITATION PROGRAM CONTRACTOR APPLICATION HOUSING

Withdrawal Request - In Service 401 Corporate ERISA

Withdrawal Request - In Service 401 Corporate ERISA ING Life Insurance and Annuity Company 151 Farmington Avenue Hartford, CT 06156-1268 Telephone: 1-800-262-3862 ING Life Insurance and Annuity Company

Withdrawal Request - In Service 401 Corporate ERISA ING Life Insurance and Annuity Company 151 Farmington Avenue Hartford, CT 06156-1268 Telephone: 1-800-262-3862 ING Life Insurance and Annuity Company

North Dakota University System

North Dakota University System Payroll Manual PEOPLESOFT VERSION 9.1 Payroll Page 1 Table of Contents EMPLOYEE TAX DISTRIBUTION... 6 Overview... 6 Update Tax Distribution Data... 6 Tax Distribution...

North Dakota University System Payroll Manual PEOPLESOFT VERSION 9.1 Payroll Page 1 Table of Contents EMPLOYEE TAX DISTRIBUTION... 6 Overview... 6 Update Tax Distribution Data... 6 Tax Distribution...

Number, street, and room or suite no. If a P.O. box, see the instructions. City or town, state or province, country, and ZIP or foreign postal code

Form 1065 Department of the Treasury Internal Revenue Service A Principal business activity U.S. Return of Partnership Income For calendar year 2015, or tax year beginning, 2015, ending, 20. Information

Form 1065 Department of the Treasury Internal Revenue Service A Principal business activity U.S. Return of Partnership Income For calendar year 2015, or tax year beginning, 2015, ending, 20. Information

Missouri Lottery Winner Claim Form Official Missouri Lottery Claim Form

[ STAPLE TICKET HERE ] Missouri Lottery Winner Claim Form Official Missouri Lottery Claim Form A B C PLEASE PRINT your name, address and phone number on the back of your ticket - YOU MUST SIGN YOUR TICKET.

[ STAPLE TICKET HERE ] Missouri Lottery Winner Claim Form Official Missouri Lottery Claim Form A B C PLEASE PRINT your name, address and phone number on the back of your ticket - YOU MUST SIGN YOUR TICKET.

1. Nonresident Alien or Resident Alien?

U..S.. Tax Guiide for Non-Resiidents Table of Contents A. U.S. INCOME TAXES ON NON-RESIDENTS 1. Nonresident Alien or Resident Alien? o Nonresident Aliens o Resident Aliens Green Card Test Substantial Presence

U..S.. Tax Guiide for Non-Resiidents Table of Contents A. U.S. INCOME TAXES ON NON-RESIDENTS 1. Nonresident Alien or Resident Alien? o Nonresident Aliens o Resident Aliens Green Card Test Substantial Presence

DS-2019 Application for J-1 Exchange Visitors

International Affairs MTSU-Box120 Murfreesboro, TN 37132 Email:international@mtsu.edu www.mtsu.edu/international DS-2019 Application for J-1 Exchange Visitors Plans to invite an individual in J-1 status

International Affairs MTSU-Box120 Murfreesboro, TN 37132 Email:international@mtsu.edu www.mtsu.edu/international DS-2019 Application for J-1 Exchange Visitors Plans to invite an individual in J-1 status

$ 2 Amounts billed for 2016 qualified tuition and related expenses. reporting method for 2016. 4 Adjustments made for a prior year.

Attention: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of Copy A of this IRS form is scannable,

Attention: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of Copy A of this IRS form is scannable,

U.S. Income Tax Return for an S Corporation

Form 1120S U.S. Income Tax Return for an S Corporation Do not file this form unless the corporation has filed or is attaching Form 2553 to elect to be an S corporation. Information about Form 1120S and

Form 1120S U.S. Income Tax Return for an S Corporation Do not file this form unless the corporation has filed or is attaching Form 2553 to elect to be an S corporation. Information about Form 1120S and

U.S. TAX ISSUES FOR CANADIANS

March 2015 CONTENTS Snowbirds Canadians owning U.S. rental properties Summary U.S. TAX ISSUES FOR CANADIANS If you own rental property in the United States or spend extended periods of time there, you

March 2015 CONTENTS Snowbirds Canadians owning U.S. rental properties Summary U.S. TAX ISSUES FOR CANADIANS If you own rental property in the United States or spend extended periods of time there, you

SOCIAL SECURITY ADMINISTRATION Application for a Social Security Card

SOCIAL SECURITY ADMINISTRATION Application for a Social Security Card USE THIS APPLICATION TO: Applying for a Social Security Card is free! Apply for an original Social Security card Apply for a replacement

SOCIAL SECURITY ADMINISTRATION Application for a Social Security Card USE THIS APPLICATION TO: Applying for a Social Security Card is free! Apply for an original Social Security card Apply for a replacement

Tax Information for International Postdocs

Tax Information for International Postdocs Sharon L. Shaff, CPA, MST March 7, 2012 Measured by Your Success For Over 100 Years 1 Circular 230 Disclosure Any tax advice contained in the body of this presentation

Tax Information for International Postdocs Sharon L. Shaff, CPA, MST March 7, 2012 Measured by Your Success For Over 100 Years 1 Circular 230 Disclosure Any tax advice contained in the body of this presentation

Tax Highlights for U.S. Citizens and Residents Going Abroad. Publication 593 (Rev. Nov. 94) Cat. No. 46595Q

Cat. No. 46595Q") Department of the Treasury Internal Revenue Service Publication 593 (Rev. Nov. 94) Cat. No. 46595Q Tax Highlights for U.S. Citizens and Residents Going Abroad Important Reminders Form 2555 EZ. You may

Department of the Treasury Internal Revenue Service Publication 593 (Rev. Nov. 94) Cat. No. 46595Q Tax Highlights for U.S. Citizens and Residents Going Abroad Important Reminders Form 2555 EZ. You may

Disability Benefits Application Instructions (Includes Service Retirement During Evaluation of a Disability Application)

") Disability Benefits Application Instructions (Includes Service Retirement During Evaluation of a Disability Application) This application is for Defined Benefit members who are applying for a disability

Disability Benefits Application Instructions (Includes Service Retirement During Evaluation of a Disability Application) This application is for Defined Benefit members who are applying for a disability

International Student and Scholar Services Middle Tennessee State University. J-1 Visitor s Handbook

International Student and Scholar Services Middle Tennessee State University J-1 Visitor s Handbook Table of Contents Important Documents and Acronyms...1 Your Activities as a J-1 Visitor...3 Time Limits...4

International Student and Scholar Services Middle Tennessee State University J-1 Visitor s Handbook Table of Contents Important Documents and Acronyms...1 Your Activities as a J-1 Visitor...3 Time Limits...4

Attention: See IRS Publications 1141, 1167, 1179 and other IRS resources for information about printing these tax forms.

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

Students: undergraduate and graduate students who are currently enrolled in universities

DUO-Korea: 1. General Description CAUTION: If any application falls under the following 3 cases, the application is disqualified and will not be considered for selection. If such case is found after the

DUO-Korea: 1. General Description CAUTION: If any application falls under the following 3 cases, the application is disqualified and will not be considered for selection. If such case is found after the

Payments for Professional Services

Payments for Professional Services 512-471-8802 askus@austin.utexas.edu www.utexas.edu/business/accounting Contents INTRODUCTION 3 Authorization of Professional (Individual) Services Procedures 3 Purchasing

Payments for Professional Services 512-471-8802 askus@austin.utexas.edu www.utexas.edu/business/accounting Contents INTRODUCTION 3 Authorization of Professional (Individual) Services Procedures 3 Purchasing

Alaska Supplemental Annuity Plan Benefit Payment Election

Alaska Supplemental Annuity Plan Benefit Payment Election FOR OFFICE USE ONLY S T A T E O F A L A S K A Toll-Free: 1-800-821-2251 www.state.ak.us/drb Division of Retirement and Benefits PO Box 110203 Juneau,

Alaska Supplemental Annuity Plan Benefit Payment Election FOR OFFICE USE ONLY S T A T E O F A L A S K A Toll-Free: 1-800-821-2251 www.state.ak.us/drb Division of Retirement and Benefits PO Box 110203 Juneau,