Financial Transmission Rights in the Nordic Electricity Market

|

|

|

- Simon Barton

- 10 years ago

- Views:

Transcription

1 Financial Transmission Rights in the Nordic Electricity Market

2 2 What is the purpose of issuing FTRs FTRs allow market parties to hedge the area price spread risk => This makes it potentially easier for market participants to compete in the longer-term market

3 3 (Physical and Financial ) products to hedge the area price risk Physical Transmission Rights (PTRs) - Physical transmission right to the trader (market participant) entitling her to use a physical capacity (MW) - ISO/TSO issues Financial Transmission Right (FTR) Purely Financial product for area price difference Different versions of the FTR product (Obligations vs. Options) TSO typically issues The Nordic TSOs have long ago decided not to issue physical transmission rights explicitly; instead all physical transmission capacity is made available to the market implicitly Contracts for Differences (CfDs) - CfD products hedge price difference between system and area price - Market participants issue the product - Payoff profile is that of an obligation

- CfD products hedge price difference between system and area price - Market participants issue the product - Payoff profile is that of an")

4 4 Current premise for planning - Zonal market model -100% of physical capacity between bidding areas allocated implicitly D-1 - TSOs obtain 100% of congestion revenue Long-term FTR gives the holder a right for the congestion rent, TSO gets the auction price of FTR as a compensation - FTR price and congestion rent may be equal or different - If FTR underpriced at auction, FTR holder will win and TSO lose, and vice versa - Compared to current Nordic regime, FTR would shift risks from trader to TSOs Can systematic undervaluation at auction occur? FTR / Pekka Sulamaa

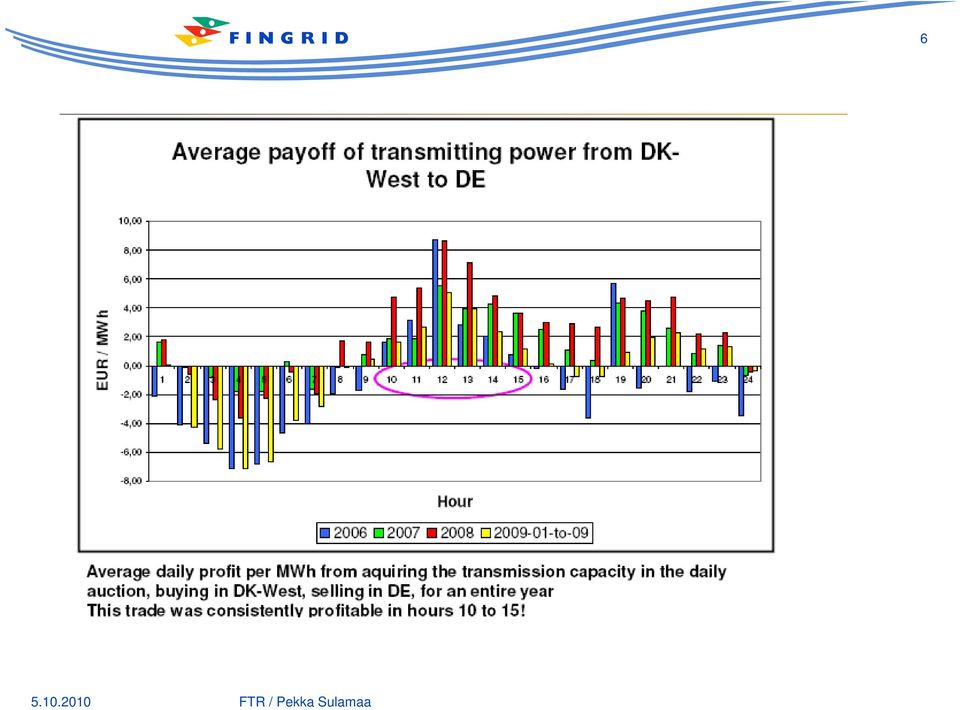

5 5 Auctioning transmission rights may not be sufficient to avoid mispricing

6 6

7 7 Key concern of TSOs: Safeguard appropriate valuation of capacity Benchmark: without FTRs, TSOs obtain 100% of congestion revenue on behalf of society; if they issue FTRs, then the revenue from auctioning FTRs may be less than the congestion revenue (undervaluation) ex post reductions in capacity may lead to very sizeable financial risk because TSOs would still have to pay out the price difference without being hedged by the congestion revenue

8 8 Trader/producer view The Financial Transmission Rights should be auctioned on time horizons supporting longterm forward contracts. The capacity to be auctioned should be based on the underlying liquidity structure on the specific forward market TSOs shall auction the maximum of available capacity over appropriate time frames. Auctioning at least one year ahead two thirds of the available capacity (and most of the remainder monthly or quarterly) would be in line with common term-sales arrangements, and would thus help develop liquidity in a traded secondary capacity market. FTRs would increase competition in the CfD market and make it possible to get a balance between fundamental buyers and sellers in each price area Transmission rights must be firm Secondary market for FTRs

9 9 Summary on FTRs Long-term FTRs allow market parties to hedge the area price risks If TSOs issue FTRs then use obligations instead of options (attachement example) The potential FTR risks need to be managed Maximum payment to FTR holders should not exceed the realised congestion revenue Congestion revenues will be used to FTR payments, not to the infrastructure investments or other activities There are no reasons why private parties could not issue equivalent hedging products

10 10 FTRs in Nordic market? Forthcoming EU legislation will allow CfDs as alternative for FTRs, Nordic TSOs are under no obligation to issue FTRs However Nordic/Continental border may need to provide PTRs/FTRs Whether to introduce internal Nordic FTRs. Would the market be better off? Interactions with existing CfD market at Nordpool Liquidity, better for FTRs than CfDs? Mitigation of market power? Better hedge for trader? Or same as 2 x CfD? New risks for TSOs, to be socialised in grid tariffs possible shift of liquidity from system price to area price?

11 11 Appendix 1: Finnpower sells Swedload at 25/MWh Finnpower (connected to Finnish network) can sell into NPS in Finland and put in an unlimited bid to procure power in the Swedish bidding area Payoff without hedging (cost assumed to be zero for simplicity) (25 - NPS_SE + NPS_FI) / MWh Finnpower worried about high price in Sweden and/or low price in Finland If Finnpower could buy a security that pays exactly [NPS_SE] - [NPS_FI)] against a cost of C (resp. K) its payoff per MWh would be: 25 - NPS_SE + NPS_FI + [NPS_SE] - [NPS_FI)] - C = (25 - C) This security is the equivalent of an FTR obligation

![worried about high price in Sweden and/or low price in Finland If Finnpower could buy a security that pays exactly [NPS_SE] - [NPS_FI)] against a cost](/docs-images/45/11529010/images/page_11.jpg "of C (resp.")

12 12 If the FTR were defined as an option, the payoff would be X - NPS_SE + NPS_FI + max {0, NPS_SE - NPS_FI} - K = IF (NPS_SE - NPS_FI) 0 : X-K IF (NPS_SE - NPS_FI) < 0 : (X-K) - NPS_SE + NPS_FI > (X-K) Option seemingly leads to a higher payoff because it leaves some upside However, all else equal a risk-averse market party would always prefer the obligation The "upside" is worth less to a risk-averse market party than its expected value It can be shown that even where capacities are not symmetric, the TSO(s) can break even issuing obligations.

can break even issuing obligations.")

13 13 Payoff Finnpower's Payoff from covering physical obligation in the spot market [NPS_FI - NPS_SE] Price spread [NPS_SE - NPS_FI] Price agreed with Swedload for delivery in Sweden (X=25)

14 14 Payoff Payoff of FTR option (FI_to_SE) Price spread [NPS_SE - NPS_FI] Price agreed with Swedload for delivery in Sweden (X=25) Payoff from physically covering position in the spot market [NPS_FI - NPS_SE] Payoff of FTR option (FI_to_SE)

![[NPS_SE - NPS_FI] Price agreed with Swedload for delivery in Sweden (X=25) Payoff from](/docs-images/45/11529010/images/page_14.jpg "physically covering position in the spot market [NPS_FI - NPS_SE] Payoff of FTR option")

15 15 Payoff Payoff of FTR obligation (FI_to_SE) Price spread [NPS_SE - NPS_FI] Price agreed with Swedload for delivery in Sweden (X=25) Payoff from physically covering position in the spot market [NPS_FI - NPS_SE] Payoff of FTR obligation (FI_to_SE)

![[NPS_SE - NPS_FI] Price agreed with Swedload for delivery in Sweden (X=25) Payoff from](/docs-images/45/11529010/images/page_15.jpg "physically covering position in the spot market [NPS_FI - NPS_SE] Payoff of FTR")

16 16 Payoff Total payoff from selling at X=25 + covering physical obligation in the spot market + FTR obligation Price spread [NPS_SE - NPS_FI] Price agreed with Swedload for delivery in Sweden (X=25) Total payoff from selling at X=25 + physically covering position in the spot market + FTR obligation

![100-20 -40-60 -80-100 Price spread [NPS_SE - NPS_FI] Price agreed with Swedload for delivery in](/docs-images/45/11529010/images/page_16.jpg "Sweden (X=25) Total payoff from selling at X=25 + physically covering position in the spot market +")

17 17 Payoff Total payoff from selling at X=25 + covering physical obligation in the spot market + FTR option Price spread [NPS_SE - NPS_FI] Price agreed with Swedload for delivery in Sweden (X=25) Total payoff from selling at X=25 + physically covering position in the spot market + FTR option

![100-20 -40-60 -80-100 Price spread [NPS_SE - NPS_FI] Price agreed with Swedload for delivery in](/docs-images/45/11529010/images/page_17.jpg "Sweden (X=25) Total payoff from selling at X=25 + physically covering position in the spot market +")

Forward Risk-Hedging Products PC_2012_E_13

Answer to public consultation Petteri Haveri 26.10.2012 1(5) Agency for the cooperation of energy regulators [email protected] Forward Risk-Hedging Products PC_2012_E_13 The Finnish Energy

Answer to public consultation Petteri Haveri 26.10.2012 1(5) Agency for the cooperation of energy regulators [email protected] Forward Risk-Hedging Products PC_2012_E_13 The Finnish Energy

How To Create A Power Market In European Power Markets

THEMA Report 2011-15 ISBN no. 978-82-93150-07-7 Market design and the use of FTRs and CfDs A report prepared for Energy Norway September 2011 CONTENT 1 SUMMARY AND CONCLUSIONS...3 2 INTRODUCTION...4 3

THEMA Report 2011-15 ISBN no. 978-82-93150-07-7 Market design and the use of FTRs and CfDs A report prepared for Energy Norway September 2011 CONTENT 1 SUMMARY AND CONCLUSIONS...3 2 INTRODUCTION...4 3

Hedging with FTRs and CCfDs Introduction

Hedging with FTRs and CCfDs Introduction This document discusses hedging with Financial Transmission Rights (FTRs) and Cross-border Contracts for Difference (CCfDs) Further, the presentation discusses

Hedging with FTRs and CCfDs Introduction This document discusses hedging with Financial Transmission Rights (FTRs) and Cross-border Contracts for Difference (CCfDs) Further, the presentation discusses

FI/RU electricity exchange area setup

FI/RU electricity exchange area setup Daily routines at Nord Pool Spot Time (CET) Action 9:30 Transmission capacities published on NPS web Daily at 9:30 CET the relevant TSOs submit the available transmission

FI/RU electricity exchange area setup Daily routines at Nord Pool Spot Time (CET) Action 9:30 Transmission capacities published on NPS web Daily at 9:30 CET the relevant TSOs submit the available transmission

The Nordic Electricity Exchange and The Nordic Model for a Liberalized Electricity Market

The Nordic Electricity Exchange and The Nordic Model for a Liberalized Electricity Market 1 The market When the electricity market is liberalized, electricity becomes a commodity like, for instance, grain

The Nordic Electricity Exchange and The Nordic Model for a Liberalized Electricity Market 1 The market When the electricity market is liberalized, electricity becomes a commodity like, for instance, grain

Feedback from Nordenergi on PCG target model and roadmap propositions

Our ref. CHS PCG/ERGEG Regional Initiatives Group, [email protected] ERI Northern region [email protected] Copenhagen, 30 October 2009 Feedback from Nordenergi on PCG target model and roadmap propositions Dear Madam/Sir,

Our ref. CHS PCG/ERGEG Regional Initiatives Group, [email protected] ERI Northern region [email protected] Copenhagen, 30 October 2009 Feedback from Nordenergi on PCG target model and roadmap propositions Dear Madam/Sir,

The Liberalized Electricity Market

1. The market When the electricity market is liberalized, electricity becomes a commodity like, for instance, grain or oil. At the outset, there is as in all other markets a wholesale market and a retail

1. The market When the electricity market is liberalized, electricity becomes a commodity like, for instance, grain or oil. At the outset, there is as in all other markets a wholesale market and a retail

Reliability Options in Ireland and Northern Ireland Obligations and Penalties

Reliability Options in Ireland and Northern Ireland Obligations and Penalties European Commission Technical Working Group on Energy: Subgroup on generation adequacy 14 April, Brussels Background Single

Reliability Options in Ireland and Northern Ireland Obligations and Penalties European Commission Technical Working Group on Energy: Subgroup on generation adequacy 14 April, Brussels Background Single

ACER consultation on Forward Risk-Hedging Products and Harmonisation of Long-Term Capacity Allocation Rules EFET RESPONSE

Amstelveenseweg 998 1081 JS Amsterdam Phone: + 31 20 520 7970 Fax: + 31 346 283 258 Email: [email protected] Website: www.efet.org ACER consultation on Forward Risk-Hedging Products and Harmonisation

Amstelveenseweg 998 1081 JS Amsterdam Phone: + 31 20 520 7970 Fax: + 31 346 283 258 Email: [email protected] Website: www.efet.org ACER consultation on Forward Risk-Hedging Products and Harmonisation

Role of Power Traders in enhancing market dynamics

Role of Power Traders in enhancing market dynamics Date: 08 th March 2011 Sunil Agrawal (Head GMR Energy Trading) & Tanmay Pramanik (Assoc. Mgr GMR Energy Trading) Evolution of Power Trading business Internationally

Role of Power Traders in enhancing market dynamics Date: 08 th March 2011 Sunil Agrawal (Head GMR Energy Trading) & Tanmay Pramanik (Assoc. Mgr GMR Energy Trading) Evolution of Power Trading business Internationally

THE STRUCTURE OF AN ELECTRICITY MARKET

THE STRUCTURE OF AN ELECTRICITY MARKET Lectures 1-2 in EG2200 Power Generation Operation and Planning Mikael Amelin 1 COURSE OBJECTIVE To pass the course, the students should show that they are able to

THE STRUCTURE OF AN ELECTRICITY MARKET Lectures 1-2 in EG2200 Power Generation Operation and Planning Mikael Amelin 1 COURSE OBJECTIVE To pass the course, the students should show that they are able to

Final Draft Framework Guidelines on Capacity Allocation and Congestion Management for Electricity Ref: E10-ENM-20-03 3 February 2011

Final Draft Framework Guidelines on Capacity Allocation and Congestion Management for Electricity Ref: E10-ENM-20-03 3 February 2011 European Regulators Group for Electricity and Gas Contact: Council of

Final Draft Framework Guidelines on Capacity Allocation and Congestion Management for Electricity Ref: E10-ENM-20-03 3 February 2011 European Regulators Group for Electricity and Gas Contact: Council of

7: The electricity market

7: The electricity market 94 : Facts 2008 : Energy and Water Resources in Norway The power sector in Norway is regulated by the Energy Act. Market-based power trading is one of the principles incorporated

7: The electricity market 94 : Facts 2008 : Energy and Water Resources in Norway The power sector in Norway is regulated by the Energy Act. Market-based power trading is one of the principles incorporated

Options for coordinating different capacity mechanisms

Options for coordinating different capacity mechanisms Håkan Feuk, Chair of EURELECTRIC Working Group on Wholesale Market Design Brussels, 12 December 2013 Generation adequacy measures have clear cross-border

Options for coordinating different capacity mechanisms Håkan Feuk, Chair of EURELECTRIC Working Group on Wholesale Market Design Brussels, 12 December 2013 Generation adequacy measures have clear cross-border

XIV. Additional risk information on forward transactions in CFDs

XIV. Additional risk information on forward transactions in CFDs The following information is given in addition to the general risks associated with forward transactions. Please read the following information

XIV. Additional risk information on forward transactions in CFDs The following information is given in addition to the general risks associated with forward transactions. Please read the following information

A stock is a share in the ownership of a company. Stock represents a claim on the company s assets and earnings.

Stock Market Basics What are stocks? A stock is a share in the ownership of a company. Stock represents a claim on the company s assets and earnings. As an owner (shareholder), you are entitled to your

Stock Market Basics What are stocks? A stock is a share in the ownership of a company. Stock represents a claim on the company s assets and earnings. As an owner (shareholder), you are entitled to your

Mark Pearce National Grid Interconnectors Business National Grid House Warwick Technology Park Gallows Hill Warwick CV34 6DA 23 June 2006

Mark Pearce National Grid Interconnectors Business National Grid House Warwick Technology Park Gallows Hill Warwick CV34 6DA 23 June 2006 Dear Mark, Re: Proposal for the implementation of revised use it

Mark Pearce National Grid Interconnectors Business National Grid House Warwick Technology Park Gallows Hill Warwick CV34 6DA 23 June 2006 Dear Mark, Re: Proposal for the implementation of revised use it

Secondary and short term natural gas markets International experiences

Secondary and short term natural gas markets International experiences Bogotá, 13 th May 2011 Presented by: Dan Harris Principal The Brattle Group Copyright 2011 The Brattle Group, Inc. www.brattle.com

Secondary and short term natural gas markets International experiences Bogotá, 13 th May 2011 Presented by: Dan Harris Principal The Brattle Group Copyright 2011 The Brattle Group, Inc. www.brattle.com

ELECTRICITY MARKET REFORM (EMR) & THE ENERGY BILL INENCO OVERVIEW

& THE ENERGY BILL INENCO OVERVIEW") ELECTRICITY MARKET REFORM (EMR) & THE ENERGY BILL INENCO OVERVIEW February 2014 ELECTRICITY MARKET REFORM (EMR) & THE ENERGY BILL The Energy Bill is the government s flagship energy policy. There have

ELECTRICITY MARKET REFORM (EMR) & THE ENERGY BILL INENCO OVERVIEW February 2014 ELECTRICITY MARKET REFORM (EMR) & THE ENERGY BILL The Energy Bill is the government s flagship energy policy. There have

CONTRACTS FOR DIFFERENCE

CONTRACTS FOR DIFFERENCE Contracts for Difference (CFD s) were originally developed in the early 1990s in London by UBS WARBURG. Based on equity swaps, they had the benefit of being traded on margin. They

CONTRACTS FOR DIFFERENCE Contracts for Difference (CFD s) were originally developed in the early 1990s in London by UBS WARBURG. Based on equity swaps, they had the benefit of being traded on margin. They

CAPACITY MECHANISMS IN EU POWER MARKETS

CAPACITY MECHANISMS IN EU POWER MARKETS Can we progress to bilateral energy options? Simon Bradbury Ultimately, European renewable targets mean that prices and dispatch patterns will be dictated by wind

CAPACITY MECHANISMS IN EU POWER MARKETS Can we progress to bilateral energy options? Simon Bradbury Ultimately, European renewable targets mean that prices and dispatch patterns will be dictated by wind

INTRODUCTION TO OPTIONS MARKETS QUESTIONS

INTRODUCTION TO OPTIONS MARKETS QUESTIONS 1. What is the difference between a put option and a call option? 2. What is the difference between an American option and a European option? 3. Why does an option

INTRODUCTION TO OPTIONS MARKETS QUESTIONS 1. What is the difference between a put option and a call option? 2. What is the difference between an American option and a European option? 3. Why does an option

Market Coupling: a method with implicit advantages. B. Den Ouden CEO, Amsterdam Power Exchange Spotmarket BV (APX)

") Market Coupling: a method with implicit advantages B. Den Ouden CEO, Amsterdam Power Exchange Spotmarket BV (APX) Daily spot market Prijs Vraag Aanbod Conditional bids marktprijs 24x + blocks: Daily program

Market Coupling: a method with implicit advantages B. Den Ouden CEO, Amsterdam Power Exchange Spotmarket BV (APX) Daily spot market Prijs Vraag Aanbod Conditional bids marktprijs 24x + blocks: Daily program

Convergence Bidding Tutorial & Panel Discussion

Convergence Bidding Tutorial & Panel Discussion CAISO June 13, 2006 Joe Bowring PJM Market Monitor www.pjm.com Convergence Basics Day-Ahead Market basics Day-Ahead and Real-Time Market interactions Increment

Convergence Bidding Tutorial & Panel Discussion CAISO June 13, 2006 Joe Bowring PJM Market Monitor www.pjm.com Convergence Basics Day-Ahead Market basics Day-Ahead and Real-Time Market interactions Increment

The financial market. An introduction to Nord Pool s financial market and its products. Bernd Botzet

The financial market An introduction to Nord Pool s financial market and its products Bernd Botzet Introduction to Nord Pool s financial market Financial products Case: Forwards Contracts for difference

The financial market An introduction to Nord Pool s financial market and its products Bernd Botzet Introduction to Nord Pool s financial market Financial products Case: Forwards Contracts for difference

PUREDMA TRADING MANUAL

PUREDMA TRADING MANUAL Contents 1. An Introduction to DMA trading 02 - What is DMA? 02 - Benefits of DMA 02 2. Getting Started 02 - Activating DMA 02 - Permissions & Data Feeds 03 3. Your DMA Deal Ticket

PUREDMA TRADING MANUAL Contents 1. An Introduction to DMA trading 02 - What is DMA? 02 - Benefits of DMA 02 2. Getting Started 02 - Activating DMA 02 - Permissions & Data Feeds 03 3. Your DMA Deal Ticket

TRADING PLATFORM CLEARING AND SETTLEMENT MEMBERSHIP

TRADING PLATFORM CLEARING AND SETTLEMENT MEMBERSHIP TRADING PLATFORM Wilhelm Söderström, Nord Pool Spot Ante Mikulić, CROPEX European day ahead market A fair and transparent calculation of dayahead power

TRADING PLATFORM CLEARING AND SETTLEMENT MEMBERSHIP TRADING PLATFORM Wilhelm Söderström, Nord Pool Spot Ante Mikulić, CROPEX European day ahead market A fair and transparent calculation of dayahead power

Electricity Trading In Competitive Power Market: An Overview And Key Issues

Electricity Trading In Competitive Power Market: An Overview And Key Issues Prabodh Bajpai and S. N. Singh Abstract- A robust trading system is very important for free and fair competitive electricity

Electricity Trading In Competitive Power Market: An Overview And Key Issues Prabodh Bajpai and S. N. Singh Abstract- A robust trading system is very important for free and fair competitive electricity

PI.'s"'1-SlttlllIl. bstili

PI.'s"'1-SlttlllIl. bstili Market Implementation linda J. Clarke Strategist PJM Market Design y Supports many options for energy traders. balanced bilateral transactions (Le. scheduling coordinator) with

PI.'s"'1-SlttlllIl. bstili Market Implementation linda J. Clarke Strategist PJM Market Design y Supports many options for energy traders. balanced bilateral transactions (Le. scheduling coordinator) with

TRADING APPENDIX 1. Trading Appendix 1. Definitions. Nord Pool Spot Market. Issued by Nord Pool Spot AS COPYRIGHT NORD POOL SPOT AS 1(11)

") Trading Appendix 1 Definitions Nord Pool Spot Market Issued by Nord Pool Spot AS COPYRIGHT NORD POOL SPOT AS 1(11) Version 1 Effective from: NWE/PCR go-live 2014 DEFINITIONS This document sets out the

Trading Appendix 1 Definitions Nord Pool Spot Market Issued by Nord Pool Spot AS COPYRIGHT NORD POOL SPOT AS 1(11) Version 1 Effective from: NWE/PCR go-live 2014 DEFINITIONS This document sets out the

EURELECTRIC presentation. EURELECTRIC contribution to a reference model for European capacity markets. DG COMP workshop 30 June 2015

EURELECTRIC presentation EURELECTRIC contribution to a reference model for European capacity markets DG COMP workshop 30 June 2015 EURELECTRIC believes that energy, flexibility and capacity are all needed

EURELECTRIC presentation EURELECTRIC contribution to a reference model for European capacity markets DG COMP workshop 30 June 2015 EURELECTRIC believes that energy, flexibility and capacity are all needed

Pricing Transmission

1 / 37 Pricing Transmission Quantitative Energy Economics Anthony Papavasiliou 2 / 37 Pricing Transmission 1 Equilibrium Model of Power Flow Locational Marginal Pricing Congestion Rent and Congestion Cost

1 / 37 Pricing Transmission Quantitative Energy Economics Anthony Papavasiliou 2 / 37 Pricing Transmission 1 Equilibrium Model of Power Flow Locational Marginal Pricing Congestion Rent and Congestion Cost

CONGESTION MANAGEMENT POLICY

1 (8) CONGESTION MANAGEMENT POLICY Contents 1 General... 2 2 Principles of congestion management... 2 3 Congestion management in the Finnish transmission grid... 3 3.1 Normal situation... 3 3.2 Planned

1 (8) CONGESTION MANAGEMENT POLICY Contents 1 General... 2 2 Principles of congestion management... 2 3 Congestion management in the Finnish transmission grid... 3 3.1 Normal situation... 3 3.2 Planned

Single Electricity Market (SEM) and interaction with EMIR. Central Bank of Ireland

and interaction with EMIR. Central Bank of Ireland") Single Electricity Market (SEM) and interaction with EMIR Central Bank of Ireland 11 th July 2014 About EAI Overview of SEM and its Participants The market is a gross mandatory pool and consists of generators

Single Electricity Market (SEM) and interaction with EMIR Central Bank of Ireland 11 th July 2014 About EAI Overview of SEM and its Participants The market is a gross mandatory pool and consists of generators

Regulatory Briefing. Capital Markets Day. 17 October 2013

Regulatory Briefing Capital Markets Day 17 October 2013 Agenda Andrew Koss Director of Strategy Damien Speight Head Trader Renewables Obligation Contracts for Difference Levy Control Framework Capacity

Regulatory Briefing Capital Markets Day 17 October 2013 Agenda Andrew Koss Director of Strategy Damien Speight Head Trader Renewables Obligation Contracts for Difference Levy Control Framework Capacity

Investing in the Infrastructure for Energy Markets

Investing in the Infrastructure for Energy Markets Executive Summary: The European Commission, energy ministers and energy regulatory authorities have recognised that, if the European electricity and gas

Investing in the Infrastructure for Energy Markets Executive Summary: The European Commission, energy ministers and energy regulatory authorities have recognised that, if the European electricity and gas

Online Appendix: Payoff Diagrams for Futures and Options

Online Appendix: Diagrams for Futures and Options As we have seen, derivatives provide a set of future payoffs based on the price of the underlying asset. We discussed how derivatives can be mixed and

Online Appendix: Diagrams for Futures and Options As we have seen, derivatives provide a set of future payoffs based on the price of the underlying asset. We discussed how derivatives can be mixed and

Energy Trading. Jonas Abrahamsson Senior Vice President Trading. E.ON Capital Market Day Nordic Stockholm, July 3, 2006

Energy Trading Jonas Abrahamsson Senior Vice President Trading E.ON Capital Market Day Nordic Stockholm, July 3, 2006 Agenda The Nordic Power Market The Role of Energy Trading within E.ON Nordic Page 2

Energy Trading Jonas Abrahamsson Senior Vice President Trading E.ON Capital Market Day Nordic Stockholm, July 3, 2006 Agenda The Nordic Power Market The Role of Energy Trading within E.ON Nordic Page 2

Regulation of the Energy Market in Finland, Nordic Countries and EU. Veli-Pekka Saajo Head of Economic Regulation Energy Market Authority

Regulation of the Energy Market in Finland, Nordic Countries and EU Veli-Pekka Saajo Head of Economic Regulation Energy Market Authority PROACTIVE MARKET SUPERVISION Energy Market Authority (EMV) supervises

Regulation of the Energy Market in Finland, Nordic Countries and EU Veli-Pekka Saajo Head of Economic Regulation Energy Market Authority PROACTIVE MARKET SUPERVISION Energy Market Authority (EMV) supervises

International Experience in Pipeline Capacity Trading

International Experience in Pipeline Capacity Trading Presented to: AEMO Presented by: Dan Harris Copyright 2013 The Brattle Group, Inc. 7 August 2013 www.brattle.com Antitrust/Competition Commercial Damages

International Experience in Pipeline Capacity Trading Presented to: AEMO Presented by: Dan Harris Copyright 2013 The Brattle Group, Inc. 7 August 2013 www.brattle.com Antitrust/Competition Commercial Damages

The UK Electricity Market Reform and the Capacity Market

The UK Electricity Market Reform and the Capacity Market Neil Bush, Head Energy Economist University Paris-Dauphine Tuesday 16 th April, 2013 Overview 1 Rationale for Electricity Market Reform 2 Why have

The UK Electricity Market Reform and the Capacity Market Neil Bush, Head Energy Economist University Paris-Dauphine Tuesday 16 th April, 2013 Overview 1 Rationale for Electricity Market Reform 2 Why have

VALUING FLEXIBILITY 20 May 2014 Florence Forum Stephen Woodhouse, Director, Pöyry Management Consulting

VALUING FLEXIBILITY 20 May 2014 Florence Forum Stephen Woodhouse, Director, Pöyry Management Consulting THE NEED FOR FLEXIBILITY IS GROWING With new forms of generation. prices and dispatch patterns will

VALUING FLEXIBILITY 20 May 2014 Florence Forum Stephen Woodhouse, Director, Pöyry Management Consulting THE NEED FOR FLEXIBILITY IS GROWING With new forms of generation. prices and dispatch patterns will

Introduction to Options

Introduction to Options By: Peter Findley and Sreesha Vaman Investment Analysis Group What Is An Option? One contract is the right to buy or sell 100 shares The price of the option depends on the price

Introduction to Options By: Peter Findley and Sreesha Vaman Investment Analysis Group What Is An Option? One contract is the right to buy or sell 100 shares The price of the option depends on the price

Electricity Exchanges in South Asia The Indian Energy Exchange Model

Electricity Exchanges in South Asia The Indian Energy Exchange Model 18 Mar 14 Rajesh K Mediratta Director (BD) [email protected] www.iexindia.com In this presentation Overview - Indian Market

Electricity Exchanges in South Asia The Indian Energy Exchange Model 18 Mar 14 Rajesh K Mediratta Director (BD) [email protected] www.iexindia.com In this presentation Overview - Indian Market

A market design to support climate policy

A market design to support climate policy Karsten Neuhoff, [email protected] David Newbery, Christian von Hirschhausen, Benjamin Hobbs, Christoph Weber, Janusz Bialek, Frieder Borggrefe, Julian

A market design to support climate policy Karsten Neuhoff, [email protected] David Newbery, Christian von Hirschhausen, Benjamin Hobbs, Christoph Weber, Janusz Bialek, Frieder Borggrefe, Julian

THE EQUITY OPTIONS STRATEGY GUIDE

THE EQUITY OPTIONS STRATEGY GUIDE APRIL 2003 Table of Contents Introduction 2 Option Terms and Concepts 4 What is an Option? 4 Long 4 Short 4 Open 4 Close 5 Leverage and Risk 5 In-the-money, At-the-money,

THE EQUITY OPTIONS STRATEGY GUIDE APRIL 2003 Table of Contents Introduction 2 Option Terms and Concepts 4 What is an Option? 4 Long 4 Short 4 Open 4 Close 5 Leverage and Risk 5 In-the-money, At-the-money,

Contents. 01 An Introduction to DMA trading within What is DMA? Benefits of DMA

DMA Trading Manual DMA Trading Manual Contents Contents 01 An Introduction to DMA trading within What is DMA? Benefits of DMA 02 Getting Started Activating DMA Permissions & Data Feeds Your DMA Deal Ticket

DMA Trading Manual DMA Trading Manual Contents Contents 01 An Introduction to DMA trading within What is DMA? Benefits of DMA 02 Getting Started Activating DMA Permissions & Data Feeds Your DMA Deal Ticket

Nordic Balance Settlement

Nordic Balance Settlement Handbook for Market Participants (DRAFT) 17.12.2013 Business process: Nordic Balance settlement Version: 0 Status: For review and comments Date: December 17st, 2013 Nordic Balance

Nordic Balance Settlement Handbook for Market Participants (DRAFT) 17.12.2013 Business process: Nordic Balance settlement Version: 0 Status: For review and comments Date: December 17st, 2013 Nordic Balance

Two-State Options. John Norstad. [email protected] http://www.norstad.org. January 12, 1999 Updated: November 3, 2011.

Two-State Options John Norstad [email protected] http://www.norstad.org January 12, 1999 Updated: November 3, 2011 Abstract How options are priced when the underlying asset has only two possible

Two-State Options John Norstad [email protected] http://www.norstad.org January 12, 1999 Updated: November 3, 2011 Abstract How options are priced when the underlying asset has only two possible

Fund Management Charges, Investment Costs and Performance

Investment Management Association Fund Management Charges, Investment Costs and Performance IMA Statistics Series Paper: 3 Chris Bryant and Graham Taylor May 2012 2 Fund management charges, investment

Investment Management Association Fund Management Charges, Investment Costs and Performance IMA Statistics Series Paper: 3 Chris Bryant and Graham Taylor May 2012 2 Fund management charges, investment

Nordic Balance Settlement (NBS)

") Nordic Balance Settlement (NBS) Common Balance & Reconciliation Settlement Design December 22 nd, 2011 Content Terminology...4 Executive Summary...6 1 Introduction... 8 1.1 Scope of the Nordic Balance

Nordic Balance Settlement (NBS) Common Balance & Reconciliation Settlement Design December 22 nd, 2011 Content Terminology...4 Executive Summary...6 1 Introduction... 8 1.1 Scope of the Nordic Balance

GLOSSARY. Issued by Nord Pool Spot

GLOSSARY Issued by Nord Pool Spot Date: September 29, 2011 Glossary Nord Pool Spot Area Price Balancing market Bidding area Bilateral contract Block bid Whenever there are grid congestions, the Elspot

GLOSSARY Issued by Nord Pool Spot Date: September 29, 2011 Glossary Nord Pool Spot Area Price Balancing market Bidding area Bilateral contract Block bid Whenever there are grid congestions, the Elspot

Trading CFDs with Trader Dealer ABN 17 090 611 680 (AFSL NO 333297)

") Trading CFDs with Trader Dealer ABN 17 090 611 680 (AFSL NO 333297) Pages 1. Overview 3 2. What is a CFD? 3 3. Why Trade CFDs? 3 4. How Do CFDs Work? 4 4.1 Margin 4 4.2 Commission 5 4.3 Financing 6 4.4

Trading CFDs with Trader Dealer ABN 17 090 611 680 (AFSL NO 333297) Pages 1. Overview 3 2. What is a CFD? 3 3. Why Trade CFDs? 3 4. How Do CFDs Work? 4 4.1 Margin 4 4.2 Commission 5 4.3 Financing 6 4.4

Chapter 2 An Introduction to Forwards and Options

Chapter 2 An Introduction to Forwards and Options Question 2.1. The payoff diagram of the stock is just a graph of the stock price as a function of the stock price: In order to obtain the profit diagram

Chapter 2 An Introduction to Forwards and Options Question 2.1. The payoff diagram of the stock is just a graph of the stock price as a function of the stock price: In order to obtain the profit diagram

Evolution Strategy. Evolution Highlights. Chryson Evolution Strategy & Performance 2012-2013

Evolution Strategy Chryson Evolution Strategy & Performance 20-20 Evolution Highlights Trading with defined strategy Trade CFDs only in FTSE 100 companies Utilising short and long positions Due to the

Evolution Strategy Chryson Evolution Strategy & Performance 20-20 Evolution Highlights Trading with defined strategy Trade CFDs only in FTSE 100 companies Utilising short and long positions Due to the

Your Assets: Financing and Refinancing Properties

The Business Library Resource Report #35 Your Assets: Financing and Refinancing Properties Personal, Investment, and Business Properties! Basic Analysis of How and When! Fixed vs. Variable Interest Rate!

The Business Library Resource Report #35 Your Assets: Financing and Refinancing Properties Personal, Investment, and Business Properties! Basic Analysis of How and When! Fixed vs. Variable Interest Rate!

11 Option. Payoffs and Option Strategies. Answers to Questions and Problems

11 Option Payoffs and Option Strategies Answers to Questions and Problems 1. Consider a call option with an exercise price of $80 and a cost of $5. Graph the profits and losses at expiration for various

11 Option Payoffs and Option Strategies Answers to Questions and Problems 1. Consider a call option with an exercise price of $80 and a cost of $5. Graph the profits and losses at expiration for various

ABOUT ELECTRICITY MARKETS. Power Markets and Trade in South Asia: Opportunities for Nepal

ABOUT ELECTRICITY MARKETS Power Markets and Trade in South Asia: Opportunities for Nepal February 14-15, 2011 Models can be classified based on different structural characteristics. Model 1 Model 2 Model

ABOUT ELECTRICITY MARKETS Power Markets and Trade in South Asia: Opportunities for Nepal February 14-15, 2011 Models can be classified based on different structural characteristics. Model 1 Model 2 Model

CommSeC CFDS: IntroDuCtIon to FX

CommSec CFDs: Introduction to FX Important Information This brochure has been prepared without taking account of the objectives, financial and taxation situation or needs of any particular individual.

CommSec CFDs: Introduction to FX Important Information This brochure has been prepared without taking account of the objectives, financial and taxation situation or needs of any particular individual.

Derivative Users Traders of derivatives can be categorized as hedgers, speculators, or arbitrageurs.

OPTIONS THEORY Introduction The Financial Manager must be knowledgeable about derivatives in order to manage the price risk inherent in financial transactions. Price risk refers to the possibility of loss

OPTIONS THEORY Introduction The Financial Manager must be knowledgeable about derivatives in order to manage the price risk inherent in financial transactions. Price risk refers to the possibility of loss

Option Theory Basics

Option Basics What is an Option? Option Theory Basics An option is a traded security that is a derivative product. By derivative product we mean that it is a product whose value is based upon, or derived

Option Basics What is an Option? Option Theory Basics An option is a traded security that is a derivative product. By derivative product we mean that it is a product whose value is based upon, or derived

Specific amendments to the Capacity Allocation and Congestion Management Network Code

Annex: Specific amendments to the Capacity Allocation and Congestion Management Network Code I. Amendments with respect to entry into force and application The Network Code defines deadlines for several

Annex: Specific amendments to the Capacity Allocation and Congestion Management Network Code I. Amendments with respect to entry into force and application The Network Code defines deadlines for several

TMX TRADING SIMULATOR QUICK GUIDE. Reshaping Canada s Equities Trading Landscape

TMX TRADING SIMULATOR QUICK GUIDE Reshaping Canada s Equities Trading Landscape OCTOBER 2014 Markets Hours All market data in the simulator is delayed by 15 minutes (except in special situations as the

TMX TRADING SIMULATOR QUICK GUIDE Reshaping Canada s Equities Trading Landscape OCTOBER 2014 Markets Hours All market data in the simulator is delayed by 15 minutes (except in special situations as the

Geoff Considine, Ph.D.

Google Employee Stock Options: A Case Study Geoff Considine, Ph.D. Copyright Quantext, Inc. 2007 1 Employee stock option grants are available to roughly 15% of white collar worker in companies with 100

Google Employee Stock Options: A Case Study Geoff Considine, Ph.D. Copyright Quantext, Inc. 2007 1 Employee stock option grants are available to roughly 15% of white collar worker in companies with 100

An Overview of the Midwest ISO Market Design. Michael Robinson 31 March 2009

An Overview of the Midwest ISO Market Design Michael Robinson 31 March 2009 The Role of RTOs Monitor flow of power over the grid Schedule transmission service Perform transmission security analysis for

An Overview of the Midwest ISO Market Design Michael Robinson 31 March 2009 The Role of RTOs Monitor flow of power over the grid Schedule transmission service Perform transmission security analysis for

CHAPTER 3: ANSWERS OF HOW SECURITIES ARE TRADED

CHAPTER 3: ANSWERS OF HOW SECURITIES ARE TRADED PROBLEM SETS 1. Answers to this problem will vary. 2. The dealer sets the bid and asked price. Spreads should be higher on inactively traded stocks and lower

CHAPTER 3: ANSWERS OF HOW SECURITIES ARE TRADED PROBLEM SETS 1. Answers to this problem will vary. 2. The dealer sets the bid and asked price. Spreads should be higher on inactively traded stocks and lower

Market Coupling in Gas?

Market Coupling in Gas? European Gas Target Model 3 rd Workshop London, 11 April 2011 Authors: Jens Büchner Robert Gersdorf Tobias Paulun Nicole Täumel Agenda 1 Scope and Objectives of the Presentation

Market Coupling in Gas? European Gas Target Model 3 rd Workshop London, 11 April 2011 Authors: Jens Büchner Robert Gersdorf Tobias Paulun Nicole Täumel Agenda 1 Scope and Objectives of the Presentation

6. Foreign Currency Options

6. Foreign Currency Options So far, we have studied contracts whose payoffs are contingent on the spot rate (foreign currency forward and foreign currency futures). he payoffs from these instruments are

6. Foreign Currency Options So far, we have studied contracts whose payoffs are contingent on the spot rate (foreign currency forward and foreign currency futures). he payoffs from these instruments are

Centrally Cleared CFDs (cccfd) Frequently Asked Questions LCH.Clearnet/Chi-X CFD clearing service

Frequently Asked Questions LCH.Clearnet/Chi-X CFD clearing service") Centrally Cleared CFDs (cccfd) Frequently Asked Questions LCH.Clearnet/Chi-X CFD clearing service Scope & Background SB1. What is the go-live date? The target go-live is third quarter 2010. SB2. Which

Centrally Cleared CFDs (cccfd) Frequently Asked Questions LCH.Clearnet/Chi-X CFD clearing service Scope & Background SB1. What is the go-live date? The target go-live is third quarter 2010. SB2. Which

Transmission Pricing. Donald Hertzmark July 2008

Transmission Pricing Donald Hertzmark July 2008 Topics 1. Key Issues in Transmission Pricing 2. Experiences in Other Systems 3. Pricing Alternatives 4. Electricity Market Structure and Transmission Services

Transmission Pricing Donald Hertzmark July 2008 Topics 1. Key Issues in Transmission Pricing 2. Experiences in Other Systems 3. Pricing Alternatives 4. Electricity Market Structure and Transmission Services

PJM Overview and Wholesale Power Markets. John Gdowik PJM Member Relations

PJM Overview and Wholesale Power Markets John Gdowik PJM Member Relations PJM s Role Ensures the reliability of the high-voltage electric power system Coordinates and directs the operation of the region

PJM Overview and Wholesale Power Markets John Gdowik PJM Member Relations PJM s Role Ensures the reliability of the high-voltage electric power system Coordinates and directs the operation of the region

Before we discuss a Call Option in detail we give some Option Terminology:

Call and Put Options As you possibly have learned, the holder of a forward contract is obliged to trade at maturity. Unless the position is closed before maturity the holder must take possession of the

Call and Put Options As you possibly have learned, the holder of a forward contract is obliged to trade at maturity. Unless the position is closed before maturity the holder must take possession of the

Vision Paper LT UIOLI

Vision Paper LT UIOLI 1 / 10 1 Introduction The CMP Guidelines 1 introduced new and more detailed obligations on transmission system operators (TSOs) and National Regulatory Authorities (NRAs) regarding

Vision Paper LT UIOLI 1 / 10 1 Introduction The CMP Guidelines 1 introduced new and more detailed obligations on transmission system operators (TSOs) and National Regulatory Authorities (NRAs) regarding

1. HOW DOES FOREIGN EXCHANGE TRADING WORK?

XV. Important additional information on forex transactions / risks associated with foreign exchange transactions (also in the context of forward exchange transactions) The following information is given

XV. Important additional information on forex transactions / risks associated with foreign exchange transactions (also in the context of forward exchange transactions) The following information is given

Progress on market reform: EMR, the I-SEM and the TEM

Progress on market reform: EMR, the I-SEM and the TEM David Newbery Electricity Market Reform Belfast 28 th March 2014 http://www.eprg.group.cam.ac.uk 1 Disclaimer Although I am an independent member of

Progress on market reform: EMR, the I-SEM and the TEM David Newbery Electricity Market Reform Belfast 28 th March 2014 http://www.eprg.group.cam.ac.uk 1 Disclaimer Although I am an independent member of

What is Equity Linked Note

What is Equity Linked Note Equity Linked Note (ELN) is a yield enhancement instrument which relates to equities & provides investors with the opportunity to attain superior yield over money market instruments.

What is Equity Linked Note Equity Linked Note (ELN) is a yield enhancement instrument which relates to equities & provides investors with the opportunity to attain superior yield over money market instruments.

Response by NIE Energy (PPB)

") NIE Energy Limited Power Procurement Business (PPB) Review of K factors & Supply Margins and Tariff Structure Review Consultation Paper CER-09-093 Response by NIE Energy (PPB) 11 September 2009. Introduction

NIE Energy Limited Power Procurement Business (PPB) Review of K factors & Supply Margins and Tariff Structure Review Consultation Paper CER-09-093 Response by NIE Energy (PPB) 11 September 2009. Introduction

How To Trade Electricity Derivatives

CEEM Specialised Training Program EI Restructuring in Australia Derivative Markets and the NEM Iain MacGill and Hugh Outhred Centre for Energy and Environmental Markets School of Electrical Engineering

CEEM Specialised Training Program EI Restructuring in Australia Derivative Markets and the NEM Iain MacGill and Hugh Outhred Centre for Energy and Environmental Markets School of Electrical Engineering

Nordic Imbalance Settlement Model

Nordic Imbalance Settlement Model Contents Executive Summary Nordic Imbalance Settlement Model Settlement Structure Management Metering Settlement Data Reporting Imbalance Settlement Invoicing Communication

Nordic Imbalance Settlement Model Contents Executive Summary Nordic Imbalance Settlement Model Settlement Structure Management Metering Settlement Data Reporting Imbalance Settlement Invoicing Communication

Power market integration. Geir-Arne Mo Team Lead Nordic Spot Trading Bergen Energi AS

Power market integration Geir-Arne Mo Team Lead Nordic Spot Trading Bergen Energi AS 1 Geir-Arne Mo Some background information: Working for Bergen Energi since 2015 Team Lead Nordic Spot Trading I work

Power market integration Geir-Arne Mo Team Lead Nordic Spot Trading Bergen Energi AS 1 Geir-Arne Mo Some background information: Working for Bergen Energi since 2015 Team Lead Nordic Spot Trading I work

CHAPTER 22: FUTURES MARKETS

CHAPTER 22: FUTURES MARKETS 1. a. The closing price for the spot index was 1329.78. The dollar value of stocks is thus $250 1329.78 = $332,445. The closing futures price for the March contract was 1364.00,

CHAPTER 22: FUTURES MARKETS 1. a. The closing price for the spot index was 1329.78. The dollar value of stocks is thus $250 1329.78 = $332,445. The closing futures price for the March contract was 1364.00,

Credit Management and the ERCOT Nodal Market

Credit Management and the ERCOT Nodal Market Legal Disclaimers and Admonitions PROTOCOL DISCLAIMER This presentation provides a general overview of the Texas Nodal Market Implementation and is not intended

Credit Management and the ERCOT Nodal Market Legal Disclaimers and Admonitions PROTOCOL DISCLAIMER This presentation provides a general overview of the Texas Nodal Market Implementation and is not intended

ESB NATIONAL GRID RESPONSE TO CER/03/266 INTERCONNECTOR TRADING PRINCIPLES IN THE MAE

ESB NATIONAL GRID RESPONSE TO CER/03/266 INTERCONNECTOR TRADING PRINCIPLES IN THE MAE ESB NATIONAL GRID PAGE 1 EXECUTIVE SUMMARY There are a number of considerations to be made in relation to interconnector

ESB NATIONAL GRID RESPONSE TO CER/03/266 INTERCONNECTOR TRADING PRINCIPLES IN THE MAE ESB NATIONAL GRID PAGE 1 EXECUTIVE SUMMARY There are a number of considerations to be made in relation to interconnector

Module 1 Introduction Programme

Module 1 Introduction Programme CFDs: overview and trading online Introduction programme, October 2012, edition 18 1 In this module we look at the basics: what CFDs are and how they work. We look at some

Module 1 Introduction Programme CFDs: overview and trading online Introduction programme, October 2012, edition 18 1 In this module we look at the basics: what CFDs are and how they work. We look at some

How To Invest In Stocks And Bonds

Review for Exam 1 Instructions: Please read carefully The exam will have 21 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation

Review for Exam 1 Instructions: Please read carefully The exam will have 21 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation

SCHEDULING AND IMBALANCE SETTLEMENTS RECOMMENDATIONS FOR ELECTRICITY EXPORTS TO TURKEY

Hydropower Investment Promotion Project (HIPP) SCHEDULING AND IMBALANCE SETTLEMENTS RECOMMENDATIONS FOR ELECTRICITY EXPORTS TO TURKEY REPORT, JUNE 2012 This publication was produced for review by the United

Hydropower Investment Promotion Project (HIPP) SCHEDULING AND IMBALANCE SETTLEMENTS RECOMMENDATIONS FOR ELECTRICITY EXPORTS TO TURKEY REPORT, JUNE 2012 This publication was produced for review by the United

This seeks to define Contracts for Difference (CfDs) and their relevance to energy related development in Copeland.

and their relevance to energy related development in Copeland.") Contracts for Difference and Electricity Market Reform LEAD OFFICER: REPORT AUTHOR: John Groves Denice Gallen Summary and Recommendation: This seeks to define Contracts for Difference (CfDs) and their

Contracts for Difference and Electricity Market Reform LEAD OFFICER: REPORT AUTHOR: John Groves Denice Gallen Summary and Recommendation: This seeks to define Contracts for Difference (CfDs) and their