Business Valuation and Buy-Sell Review

|

|

|

- Paulina Norris

- 10 years ago

- Views:

Transcription

1 Generating SALES with a Business Valuation and Buy-Sell Review Will Heidbreder, JD, MBA, CPA, CLU National Advanced Solutions Consultant *JD is an educational degree and the holder does not provide legal services behalf of Principal Financial Group.

2 The Challenge for Small Business Unstable Economic conditions Business Values have changed Business Needs have changed Financial Gaps may have appeared Tax and Regulatory changes Family and Personnel change Bottom Line: the owner s buy-sell plan may be out-of-date

3 The Opportunity For YOU Business Owners have the need Many have the ability to pay The Principal Financial Group can help and it s free to you, your reps and their clients!

4 Why Business Owner and Executive Solutions? Solid Close Rate. Average is 25 to 30% close rate. Some experienced advisors have 100% close rate. More Life Policies per Case. Average 2 to 3 policies per buy-sell case. Larger Life Premiums per Case. Buy-Sell - $11,800 Key Person - $12,000 Executive Bonus - $17,000 Select Rewards - $14,300

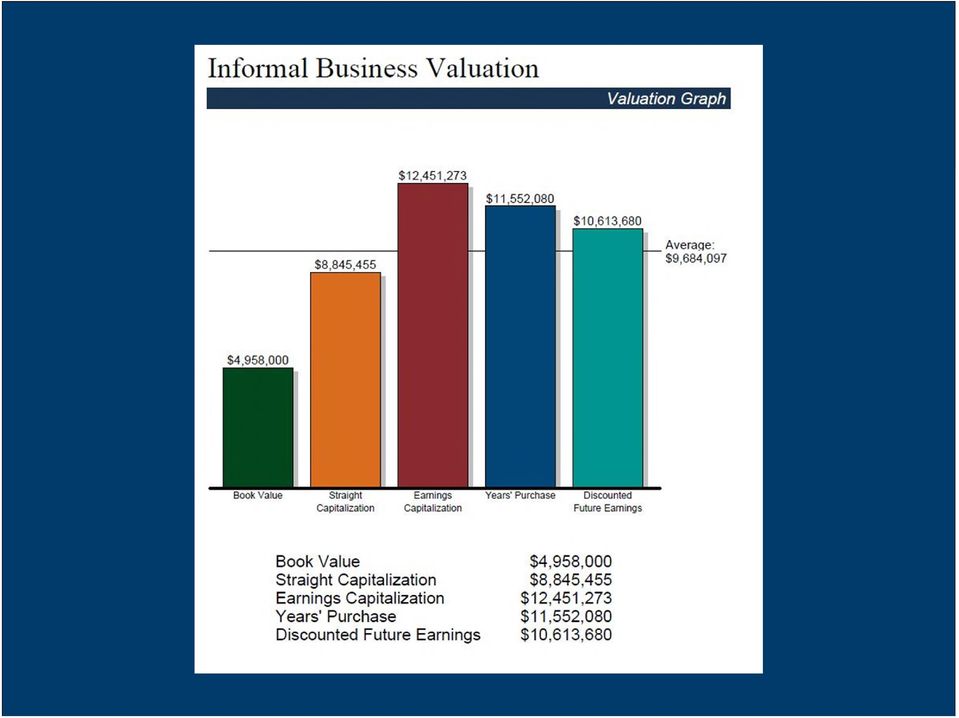

5 What Is an Informal Business Valuation? The Principal creates customized reports based on a review of the documents you provide. We provide a complimentary informal business valuation using five commonly used valuation methods. A Starting Point for discussions with tax and legal advisors To identify issues or Confirm the agreement meets current objectives

6 What Is a Buy-Sell Review? The Principal creates customized reports based on a review of the documents you provide. Report includes: Highlights of your existing buy-sell agreement. Gives our recommendations based on your business needs. Review also includes a summary of your current funding and options to help meet your business needs. We believe that adequate funding of the buy-sell agreement is the key to its success.

7 Sales Opportunities Buy-Sell Existing Buy-Sell Plans New Buy-Sell Plans Single Owner Businesses Business Protection Key Person Loan Protection Exit Planning Selling the Business Additional Family Protection

8 Sales Opportunities Retirement Bonus Plans Investment of Sales Proceeds IRAs Qualified Plans Estate Planning Estate Equalization ILITs

9 Case Study #1 Facts Construction Company in Maine (3 related entities) 2 Owners Broker requested an informal valuation and a buy sell review Discovered buy sell was at book value with deductions and not all entities had an executed buy sell agreement. Each owner had $1,000,000 of term that they owned on themselves.

10

11

12 Case Study #1 Recommendations/Results Advanced Solutions case notes to Broker: Confirm all agreements are executed and in force. Inadequate amount of life insurance. $1M vs. $3.250M. No DI. Business sold at book value minus offsets Consider FMV sales price. Owner should consider an S-Corp Bonus to compliment current 401k. Because of company value, consider Estate Tax Analysis. Results: Meeting with both partners, not all agreements executed. Attorney fixing. Did not know book value sales price. Never wanted that. Attorney fixing. Currently underwriting for more life insurance and new disability insurance based on informal valuation. Owner interested in S-Corp Bonus currently proposing. Broker taking over $4M 401k that wasn t even discussed in first meeting.

13 Case Study #2 Facts Petroleum Distribution Company in TX 1 owner Broker requested Informal Valuation to assist owner in planning. Very successful and quickly growing company. Recently secured a long term distribution agreement with a large refinery.

14

15 Case Study #2 Recommendations/Results Advanced Solutions case notes to Broker: Closely held company. Discuss intended succession plan with owner. Consider unilateral buy-sell using Select Buy-Out Plan. High value for a closely held company. Discuss Estate planning and offer Estate Tax Analysis. Owner should consider an Executive Bonus for key employees to compliment current safe harbor 401k. Results: Meeting with owner. Interested in Estate Tax Analysis. Gathering information. Interested in Select Reward for two key employees to take over business. Interested in Executive Bonus for key employees currently proposing.

16 Case Study #3 Facts Logistics Company in CT 4 owners (G2 s wife and 3 kids) Broker requested an informal business valuation. G2 recently passed away and wife interested in value of business. All 3 siblings involved in business. Some more than others. Parents want to keep the 3 rd Generation business in the family.

17

18

19 Case Study #3 Recommendations/Results Advanced Solutions case notes to Broker: Consider an Estate Tax Analysis on G2 s wife. Asset growing inside estate. Analyze/illustrate insurance and gifting to assist with efficient estate transfer. Consider a Business Continuation Proposal among the siblings to assure company remains in the family. Illustrating $5M of UL on each. Results: Meeting with G2 s son (CEO) Interested in buy-sell between siblings. Gathering additional information for detailed proposal. Meeting with family attorney to discuss estate planning for G2 s wife. Concerned about the growing asset in G2 s estate. Discussions of life insurance.

Interested in buy-sell between siblings. Gathering additional information for detailed proposal.")

20 Buy-Sell Review: The Process Collect Documents Review the Customized Report Discuss and Review Highlights and Recommendations with: The Business Owner Tax and Legal Advisors COLLECT AND PROVIDE: AGREEMENTS ENTITY TYPE OWNERS FINANCIALS INSURANCE OTHER MATERIALS

21 Marketing Guide

22 Request for Proposal

23 Reports and Proposals

24 Q&A?

25 While this communication may be used to promote or market a transaction or an idea that is discussed in the publication, it is intended to provide general information about the subject matter covered and is provided with the understanding that The Principal is not rendering legal, accounting, or tax advice. It is not a marketed opinion and may not be used to avoid penalties under the Internal Revenue Code. You should consult with appropriate counsel or other advisors on all matters pertaining to legal, tax, or accounting obligations and requirements. Insurance products from the Principal Financial Group (The Principal ) are issued by Principal National Life Insurance Company (except in New York) and Principal Life Insurance Company. Principal National and Principal Life are members of the Principal Financial Group, Des Moines, IA No part of this presentation may be reproduced or used in any form or by any means, electronic or mechanical, including photocopying or recording, or by any information storage and retrieval system, without prior written permission from the Principal Financial Group. Copyright 2009 Principal Financial Services, Inc. #

LPL INSURANCE ASSOCIATES. Taking Care of Business. Insurance Strategies to Help You Protect Your Business

LPL INSURANCE ASSOCIATES Taking Care of Business Insurance Strategies to Help You Protect Your Business Opportunities, Rewards and Responsibilities Not many business owners want to think about the time

LPL INSURANCE ASSOCIATES Taking Care of Business Insurance Strategies to Help You Protect Your Business Opportunities, Rewards and Responsibilities Not many business owners want to think about the time

FG Guarantee-Platinum. A Single Premium, Fixed Deferred Annuity with tax-deferred earnings featuring a choice of a 3, 5 or 7-year rate guarantee

A Single Premium, Fixed Deferred Annuity with tax-deferred earnings featuring a choice of a 3, 5 or 7-year rate guarantee ADV 1010 (01-2011) Fidelity & Guaranty Life Insurance Company Rev. 07-2014 12-716

A Single Premium, Fixed Deferred Annuity with tax-deferred earnings featuring a choice of a 3, 5 or 7-year rate guarantee ADV 1010 (01-2011) Fidelity & Guaranty Life Insurance Company Rev. 07-2014 12-716

FG Guarantee-Platinum 5 Year Product

5 Year Product Applications for the FG Guarantee-Platinum 5 year product must be submitted electronically. Please log on to Saleslink for additional details at https://www.fglife.com. Fidelity & Guaranty

5 Year Product Applications for the FG Guarantee-Platinum 5 year product must be submitted electronically. Please log on to Saleslink for additional details at https://www.fglife.com. Fidelity & Guaranty

Get Financially Fit. Define short-and long-term goals. Have your goals changed from 2-3 years ago? When goals change, adjust your plan.

Get Financially Fit Reduce debt. Save for today. Save for tomorrow. Define short-and long-term goals. Have your goals changed from 2-3 years ago? When goals change, adjust your plan. 1 What Do Your Financial

Get Financially Fit Reduce debt. Save for today. Save for tomorrow. Define short-and long-term goals. Have your goals changed from 2-3 years ago? When goals change, adjust your plan. 1 What Do Your Financial

White Paper: Using Cash Value Life Insurance for Retirement Savings

White Paper: Using Cash Value Life Insurance for Retirement Savings www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member

White Paper: Using Cash Value Life Insurance for Retirement Savings www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member

What Makes IDI Great

Principal Life Insurance Company What Makes IDI Great What s New with Individual DI Supplemental Health Benefit Rider* Select Professional Program Business Owner Market Enhancements * Available 9/22; May

Principal Life Insurance Company What Makes IDI Great What s New with Individual DI Supplemental Health Benefit Rider* Select Professional Program Business Owner Market Enhancements * Available 9/22; May

Insurance-Related Best Practices Guide for Buy-Sell Agreements

Insurance-Related Best Practices Guide for Buy-Sell Agreements The buy-sell agreement review and feedback process at the Principal Financial Group has allowed us to observe many different drafting approaches

Insurance-Related Best Practices Guide for Buy-Sell Agreements The buy-sell agreement review and feedback process at the Principal Financial Group has allowed us to observe many different drafting approaches

FG Guarantee-Platinum. A Single Premium, Fixed Deferred Annuity with tax-deferred earnings featuring a choice of a 3, 5 or 7-year rate guarantee

A Single Premium, Fixed Deferred Annuity with tax-deferred earnings featuring a choice of a 3, 5 or 7-year rate guarantee ADV 1010 (01-2011) Fidelity & Guaranty Life Insurance Company Rev. 07-2014 12-716

A Single Premium, Fixed Deferred Annuity with tax-deferred earnings featuring a choice of a 3, 5 or 7-year rate guarantee ADV 1010 (01-2011) Fidelity & Guaranty Life Insurance Company Rev. 07-2014 12-716

Estate Tax Concepts. for Edward and Tina Collins

Estate Tax Concepts for Edward and Tina Collins Joseph Davis, CLU, ChFC 215 Broad Street Charlotte, North Carolina 26292 Phone: 704-927-5555 Mobile Phone: 704-549-5555 Fax: 704-549-6666 Email: [email protected]

Estate Tax Concepts for Edward and Tina Collins Joseph Davis, CLU, ChFC 215 Broad Street Charlotte, North Carolina 26292 Phone: 704-927-5555 Mobile Phone: 704-549-5555 Fax: 704-549-6666 Email: [email protected]

ESOP Repurchase Obligation Funding

FOR BUSINESS OWNERS Employee Stock Ownership Plans ESOP Repurchase Obligation Funding What is your obligation? Repurchase obligation is the liability a company incurs when vested terminated participants

FOR BUSINESS OWNERS Employee Stock Ownership Plans ESOP Repurchase Obligation Funding What is your obligation? Repurchase obligation is the liability a company incurs when vested terminated participants

Succession and Exit Planning Using Life Insurance. June 2011 1 Hour CE MKTG-OC-841A For Insurance Professional Use Only. Not for Use with the Public.

Succession and Exit Planning Using Life Insurance June 2011 1 Hour CE MKTG-OC-841A Agenda Role of business succession planning in overall business strategy Impact life insurance has on a business Case

Succession and Exit Planning Using Life Insurance June 2011 1 Hour CE MKTG-OC-841A Agenda Role of business succession planning in overall business strategy Impact life insurance has on a business Case

Life Insurance Technical Manual

Life Insurance Technical Manual Technical issues surrounding one of the biggest assets owned by successful clients life insurance. Presented by: Daniel Tasciotti, CLU, ChFC, CFP, AEP, MBA There are worse

Life Insurance Technical Manual Technical issues surrounding one of the biggest assets owned by successful clients life insurance. Presented by: Daniel Tasciotti, CLU, ChFC, CFP, AEP, MBA There are worse

Buy-Sell Review SAMPLE. Summary and Analysis. Prepared for Hawkeye Medical Group, P.C. Sample City, IL

Buy-Sell Review Summary and Analysis SAMPLE Prepared for Hawkeye Medical Group, P.C. Sample City, IL Thank you for requesting a Principal Buy-Sell Review. We have received the following documents: Hawkeye

Buy-Sell Review Summary and Analysis SAMPLE Prepared for Hawkeye Medical Group, P.C. Sample City, IL Thank you for requesting a Principal Buy-Sell Review. We have received the following documents: Hawkeye

White Paper Life Insurance Coverage on a Key Employee

White Paper Life Insurance Coverage on a Key Employee www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC,

White Paper Life Insurance Coverage on a Key Employee www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC,

Control & Restricted Stock: More Flexible Than Ever?

Q. Do you own control stock? That depends on who you are. Q. Are you aware of your company's trading policies? Q. How can you sell, borrow against and otherwise monetize your shares? Q. How can you use

Q. Do you own control stock? That depends on who you are. Q. Are you aware of your company's trading policies? Q. How can you sell, borrow against and otherwise monetize your shares? Q. How can you use

13930Z-42 REV 05-11 GUARANTEED MINIMUM DEATH BENEFIT RIDER 14923Z PRT 06-11

13930Z-42 REV 05-11 GUARANTEED MINIMUM DEATH BENEFIT RIDER 14923Z PRT 06-11 ENHANCE YOUR DEATH BENEFIT WITH AN OPTIONAL RIDER ADDED TO YOUR FIXED INDEX ANNUITY In addition to your retirement planning goals,

13930Z-42 REV 05-11 GUARANTEED MINIMUM DEATH BENEFIT RIDER 14923Z PRT 06-11 ENHANCE YOUR DEATH BENEFIT WITH AN OPTIONAL RIDER ADDED TO YOUR FIXED INDEX ANNUITY In addition to your retirement planning goals,

concept Marketing Strategies

Turn Ideas into results. Individual Life Insurance concept Marketing Strategies Find Inside XXConcept-Product Matrix XXKey Sales Concepts XXService & Support Generate more opportunities with solutions

Turn Ideas into results. Individual Life Insurance concept Marketing Strategies Find Inside XXConcept-Product Matrix XXKey Sales Concepts XXService & Support Generate more opportunities with solutions

Randall A. Lenz CORPORATION/S-CORPORATION TAX ORGANIZER (1120, 1120S) COMPREHENSIVE

COMPREHENSIVE") Randall A. Lenz Attorney-at-Law Certified Public Accountant 199 14 th Street, NE Suite 1907 Atlanta, Georgia 30309-3688 (404) 815-1731, Cell (404) 323-1731, FAX (404) 815-0717 [email protected]

Randall A. Lenz Attorney-at-Law Certified Public Accountant 199 14 th Street, NE Suite 1907 Atlanta, Georgia 30309-3688 (404) 815-1731, Cell (404) 323-1731, FAX (404) 815-0717 [email protected]

Fact Finder for Small Business

Fact Finder for Small Business A. Company Background Company Name: How did you get started in your business? When did you establish your business? What makes your business unique? How is your business

Fact Finder for Small Business A. Company Background Company Name: How did you get started in your business? When did you establish your business? What makes your business unique? How is your business

EMPLOYEE BENEFITS IN MERGERS & ACQUISITIONS

EMPLOYEE BENEFITS IN MERGERS & ACQUISITIONS PRESENTED BY: Bret A. McKitrick, JD Vice President HR Consultant Associated Financial Group Employee Benefits. Insurance. HR Solutions. LEARNING OBJECTIVES By

EMPLOYEE BENEFITS IN MERGERS & ACQUISITIONS PRESENTED BY: Bret A. McKitrick, JD Vice President HR Consultant Associated Financial Group Employee Benefits. Insurance. HR Solutions. LEARNING OBJECTIVES By

Protect your business, your family, and your legacy.

An Educational Guide for Business Owners Protect your business, your family, and your legacy. Take a closer look at buy-sell agreements. Needs-based Strategies Your business is probably your single largest

An Educational Guide for Business Owners Protect your business, your family, and your legacy. Take a closer look at buy-sell agreements. Needs-based Strategies Your business is probably your single largest

Effective Planning with Life Insurance

Effective Planning with Life Insurance The Tax Considerations... Ken Knox, CLU, ChFC Regional Director The Penn Mutual Life Insurance Company 1304529TM_Sept17 Retirement Planning Case Scenario #1... Client

Effective Planning with Life Insurance The Tax Considerations... Ken Knox, CLU, ChFC Regional Director The Penn Mutual Life Insurance Company 1304529TM_Sept17 Retirement Planning Case Scenario #1... Client

OWNERSHIP TRANSITION

OWNERSHIP TRANSITION PLANNING AHEAD Peter W. Bennett, Esquire Winer and Bennett, LLP 111 Concord Street, P.O. Box 488 Nashua, NH 03061-0488 (603) 882-5157 [email protected] DEFINING THE PROBLEM

OWNERSHIP TRANSITION PLANNING AHEAD Peter W. Bennett, Esquire Winer and Bennett, LLP 111 Concord Street, P.O. Box 488 Nashua, NH 03061-0488 (603) 882-5157 [email protected] DEFINING THE PROBLEM

Estate planning strategies using life insurance in a trust Options for handling distributions, rollovers and conversions

Estate planning strategies using life insurance in a trust Options for handling distributions, rollovers and conversions Life s better when we re connected Table of contents Find your questions review

Estate planning strategies using life insurance in a trust Options for handling distributions, rollovers and conversions Life s better when we re connected Table of contents Find your questions review

Business life insurance overview

Allianz Life Insurance Company of North America Business life insurance overview Business planning with life insurance M-5115 Page 1 of 6 There are over 5.6 million businesses in the U.S. with fewer than

Allianz Life Insurance Company of North America Business life insurance overview Business planning with life insurance M-5115 Page 1 of 6 There are over 5.6 million businesses in the U.S. with fewer than

Chattahoochee Technical College

An Educational Course for Adults Ages 50 to 70 Retirement Planning Today Now being conducted at Chattahoochee Technical College Location Dates & Times Chattahoochee Technical College Thursdays North Metro

An Educational Course for Adults Ages 50 to 70 Retirement Planning Today Now being conducted at Chattahoochee Technical College Location Dates & Times Chattahoochee Technical College Thursdays North Metro

Getting the Most from Your Insurance

SMART STRATEGIES Getting the Most from Your Insurance This information is written in connection with the promotion or marketing of the matters addressed in this material. The information cannot be used

SMART STRATEGIES Getting the Most from Your Insurance This information is written in connection with the promotion or marketing of the matters addressed in this material. The information cannot be used

Annuity Owner Mistakes Tips and Ideas That Could Save You Thousands

Annuity Owner Mistakes Tips and Ideas That Could Save You Thousands Provided to you by: Milton D. Flanagan ChFC, CLU, CASL, MBA Annuity Owner Mistakes Written by Financial Educators Provided to you by

Annuity Owner Mistakes Tips and Ideas That Could Save You Thousands Provided to you by: Milton D. Flanagan ChFC, CLU, CASL, MBA Annuity Owner Mistakes Written by Financial Educators Provided to you by

Business Uses of Life Insurance

Select Portfolio Management, Inc. David M. Jones, MBA Wealth Advisor 120 Vantis, Suite 430 Aliso Viejo, CA 92656 949-975-7900 [email protected] www.selectportfolio.com Business Uses of Life

Select Portfolio Management, Inc. David M. Jones, MBA Wealth Advisor 120 Vantis, Suite 430 Aliso Viejo, CA 92656 949-975-7900 [email protected] www.selectportfolio.com Business Uses of Life

Estate Planning. Farm Credit East, ACA Stephen Makarevich

Estate Planning Farm Credit East, ACA Stephen Makarevich Farm Business Consultant 9 County Road 618 Lebanon, NJ 08833 1.800.787.3276 [email protected] 1 What is Estate Planning? 2 Estate

Estate Planning Farm Credit East, ACA Stephen Makarevich Farm Business Consultant 9 County Road 618 Lebanon, NJ 08833 1.800.787.3276 [email protected] 1 What is Estate Planning? 2 Estate

2015 Savvy Year-End Tax Planning Thoughts & Ideas

2015 Savvy Year-End Tax Planning Thoughts & Ideas JONATHAN GASSMAN CFP, CPA/PFS November 11, 2015 2015 Tax Rates Ordinary Income Qualified Dividends & Long-Term Capital Gains 10% 15% 25% 28% 2015 Rates

2015 Savvy Year-End Tax Planning Thoughts & Ideas JONATHAN GASSMAN CFP, CPA/PFS November 11, 2015 2015 Tax Rates Ordinary Income Qualified Dividends & Long-Term Capital Gains 10% 15% 25% 28% 2015 Rates

A Sole Proprietor Insured Buy-Sell Plan

A Sole Proprietor Insured Buy-Sell Plan At a sole proprietor s death, the business is dissolved and all business assets and liabilities become part of the sole proprietor's personal estate. Have you evaluated

A Sole Proprietor Insured Buy-Sell Plan At a sole proprietor s death, the business is dissolved and all business assets and liabilities become part of the sole proprietor's personal estate. Have you evaluated

Section 79 Permanent Life Insurance

Section 79 Permanent Life Insurance Your business success depends on the expertise of a few key employees How can you provide life insurance as a benefit to business owners and their employees in a tax

Section 79 Permanent Life Insurance Your business success depends on the expertise of a few key employees How can you provide life insurance as a benefit to business owners and their employees in a tax

Business, Legal, And Tax Planning for the Dental Practice

Quarterly Supplement To Business, Legal, And Tax Planning for the Dental Practice Second Edition The purpose of the Quarterly Supplement is to continually update the material contained in Business, Legal,

Quarterly Supplement To Business, Legal, And Tax Planning for the Dental Practice Second Edition The purpose of the Quarterly Supplement is to continually update the material contained in Business, Legal,

Understanding Indexed Universal Life Insurance A General Educational Overview

Understanding Indexed Universal Life Insurance The Power To Help You Succeed Steve Guerra Field Vice President Greater Texas RLO Pacific Life Insurance Company 24 Waterway Avenue, Suite 825 The Woodlands,

Understanding Indexed Universal Life Insurance The Power To Help You Succeed Steve Guerra Field Vice President Greater Texas RLO Pacific Life Insurance Company 24 Waterway Avenue, Suite 825 The Woodlands,

Life Insurance Review

Life Insurance Review A Sales Tool for All Clients Agenda Why a Life Insurance Review Typical Client Situations MetLife Support 1 Why a Life Insurance Review Role of Life Insurance Central in Completion

Life Insurance Review A Sales Tool for All Clients Agenda Why a Life Insurance Review Typical Client Situations MetLife Support 1 Why a Life Insurance Review Role of Life Insurance Central in Completion

PARTIES TO AN ANNUITY CONTRACT By: Edward J. Barrett

PARTIES TO AN ANNUITY CONTRACT By: Edward J. Barrett Overview An annuity is a contract between an annuity owner and an insurance company. However, while most other types of contracts involve only two parties,

PARTIES TO AN ANNUITY CONTRACT By: Edward J. Barrett Overview An annuity is a contract between an annuity owner and an insurance company. However, while most other types of contracts involve only two parties,

FG Immediate-Income. Single Premium Immediate Annuity. ADV 1011 (01-2011) Fidelity & Guaranty Life Insurance Company Rev.

Fidelity & Guaranty Life Insurance Company Rev.") Single Premium Immediate Annuity ADV 1011 (01-2011) Fidelity & Guaranty Life Insurance Company Rev. 07-2014 12-715 Single Premium Immediate Annuity Americans are living longer than ever before. Source:

Single Premium Immediate Annuity ADV 1011 (01-2011) Fidelity & Guaranty Life Insurance Company Rev. 07-2014 12-715 Single Premium Immediate Annuity Americans are living longer than ever before. Source:

ING Fixed Annuities Product Guide

ING Fixed Annuities Product Guide ANNUITIES For agent use only. Not for public distribution. Your future. Made easier. ING Secure Series Features ING Secure Index Opportunities Plus Annuity ING Secure

ING Fixed Annuities Product Guide ANNUITIES For agent use only. Not for public distribution. Your future. Made easier. ING Secure Series Features ING Secure Index Opportunities Plus Annuity ING Secure

The Power of Choice. A Transamerica Company

The Power of Choice A Transamerica Company A diverse portfolio allows you to prepare for your future. A Wealth of Resources World Financial Group, Inc. (WFG) and its associates are committed to offering

The Power of Choice A Transamerica Company A diverse portfolio allows you to prepare for your future. A Wealth of Resources World Financial Group, Inc. (WFG) and its associates are committed to offering

Buy-Sell Planning. Succession Planning for Business Owners. Guiding you through life. SALES STRATEGY BUSINESS. Advanced Markets. Situation.

Guiding you through life. SALES STRATEGY BUSINESS Buy-Sell Planning Succession Planning for Owners Situation owners should plan to protect their business in case of the sudden death, retirement, or disability

Guiding you through life. SALES STRATEGY BUSINESS Buy-Sell Planning Succession Planning for Owners Situation owners should plan to protect their business in case of the sudden death, retirement, or disability

BUSINESS STRATEGIES. Stock Redemption Arrangement for Closely Held Corporations. A successful business has a business succession strategy.

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA BUSINESS STRATEGIES Stock Redemption Arrangement for Closely Held Corporations BUSINESS CONTINUATION A successful business has a business succession strategy.

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA BUSINESS STRATEGIES Stock Redemption Arrangement for Closely Held Corporations BUSINESS CONTINUATION A successful business has a business succession strategy.

Annuities. Fixed Annuity: An annuity which the amount paid out is fixed sum and is usually guaranteed.

Annuities Fixed Annuity: An annuity which the amount paid out is fixed sum and is usually guaranteed. Loads: The fees or charges paid when you purchase an annuity. Includes sales commissions. Author: Douglas

Annuities Fixed Annuity: An annuity which the amount paid out is fixed sum and is usually guaranteed. Loads: The fees or charges paid when you purchase an annuity. Includes sales commissions. Author: Douglas

Traditional Life Insurance Premium Financing

Traditional Life Insurance Premium Financing Cascade Wealth Preservation is the advanced planning destination. For years, high net worth individuals have faced the challenge of weighing the need to purchase

Traditional Life Insurance Premium Financing Cascade Wealth Preservation is the advanced planning destination. For years, high net worth individuals have faced the challenge of weighing the need to purchase

Executive Summary of the Defined Benefit Plan Engineering Financial and Economic Security for Multiple Generations

Executive Summary of the Defined Benefit Plan Engineering Financial and Economic Security for Multiple Generations Benefit Focused vs. Lump Sum Focused Overview: What distinguishes a retirement plan which

Executive Summary of the Defined Benefit Plan Engineering Financial and Economic Security for Multiple Generations Benefit Focused vs. Lump Sum Focused Overview: What distinguishes a retirement plan which

Survivorship Builder. An indexed survivorship life policy AS2000 (04-15)

") Survivorship Builder An indexed survivorship life policy AS2000 (04-15) Accordia Life believes in the essence of family. Your family may be a traditional one. It may be a group of people who care for

Survivorship Builder An indexed survivorship life policy AS2000 (04-15) Accordia Life believes in the essence of family. Your family may be a traditional one. It may be a group of people who care for

Questions to Ask WHEN CHOOSING A FINANCIAL PLANNER CERTIFIED FINANCIAL PLANNER BOARD OF STANDARDS, INC.

10 Questions to Ask WHEN CHOOSING A FINANCIAL PLANNER CERTIFIED FINANCIAL PLANNER BOARD OF STANDARDS, INC. You may be considering help from a financial planner for a number of reasons, whether it s deciding

10 Questions to Ask WHEN CHOOSING A FINANCIAL PLANNER CERTIFIED FINANCIAL PLANNER BOARD OF STANDARDS, INC. You may be considering help from a financial planner for a number of reasons, whether it s deciding

Loan Application. Please fax to 770.809.5060 or email to [email protected]. Full Legal Name: Date of Birth: Social Security Number:

Loan Application Please fax to 770.809.5060 or email to [email protected] Borrower Information: Full Legal Name: of Birth: Social Security Number: Home Address: Home Phone Number: Cell

Loan Application Please fax to 770.809.5060 or email to [email protected] Borrower Information: Full Legal Name: of Birth: Social Security Number: Home Address: Home Phone Number: Cell

C o n f i d e n t i a l. Business Fact Finder. Client Name PLC.2873 (04.09)

") C o n f i d e n t i a l Business Fact Finder Client Name PLC.2873 (04.09) Confidential Questionnaire G e n e r a l I n f o r m at i o n Business Name: Address: City: State: Zip: Phone: Fax: Cell: E-Mail:

C o n f i d e n t i a l Business Fact Finder Client Name PLC.2873 (04.09) Confidential Questionnaire G e n e r a l I n f o r m at i o n Business Name: Address: City: State: Zip: Phone: Fax: Cell: E-Mail:

Lincoln universal and term life insurance portfolio at-a-glance

FOR LIFE Universal and Term Life Insurance Lincoln universal and term life insurance portfolio at-a-glance Product Menu The Lincoln National Life Insurance Company Lincoln Life & Annuity Company of New

FOR LIFE Universal and Term Life Insurance Lincoln universal and term life insurance portfolio at-a-glance Product Menu The Lincoln National Life Insurance Company Lincoln Life & Annuity Company of New

Business Continuation Planning with Life Insurance

Business Continuation Planning with Life Insurance Maintaining Business Continuity After the Death or Retirement of a Business Owner AD-OC-745C Business Continuation Planning Using Life Insurance FUTURES

Business Continuation Planning with Life Insurance Maintaining Business Continuity After the Death or Retirement of a Business Owner AD-OC-745C Business Continuation Planning Using Life Insurance FUTURES

Please contact us for more information and/or for additional white paper titles or copies.

Harris Private Bank has helped affluent families grow and preserve their wealth for more than 100 years. We work closely with your existing advisors to make sure all aspects of your wealth strategy fit

Harris Private Bank has helped affluent families grow and preserve their wealth for more than 100 years. We work closely with your existing advisors to make sure all aspects of your wealth strategy fit

CROSS-PURCHASE BUY-SELL AGREEMENT

Presented for: YOUR CLIENT"S NAME HERE Presented by: YOUR NAME HERE U.S. Treasury Circular 230 may require Pentera Group, Inc. to advise you that any tax information provided in this document is not intended

Presented for: YOUR CLIENT"S NAME HERE Presented by: YOUR NAME HERE U.S. Treasury Circular 230 may require Pentera Group, Inc. to advise you that any tax information provided in this document is not intended

PROTECTING BUSINESS OWNERS AND PRESERVING BUSINESSES FOR FUTURE GENERATIONS

BASICS OF BUY-SELL PLANNING A buy-sell arrangement (or business continuation agreement ) is an arrangement for the disposition of a business interest upon a specific triggering event such as a business

BASICS OF BUY-SELL PLANNING A buy-sell arrangement (or business continuation agreement ) is an arrangement for the disposition of a business interest upon a specific triggering event such as a business

Sample Corporate Cross Purchase Agreement

Sample Corporate Cross Purchase Agreement (Optional Disability Buy-Out) This sample agreement has been prepared as a guide to assist attorneys. Our publication, Buy-Sell Arrangements, A Guide for Professional

Sample Corporate Cross Purchase Agreement (Optional Disability Buy-Out) This sample agreement has been prepared as a guide to assist attorneys. Our publication, Buy-Sell Arrangements, A Guide for Professional

White Paper Life Insurance Policy Provisions

White Paper www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

White Paper www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

AMG Financial Services. a division of. Presents. Life Settlements

AMG Financial Services a division of Presents Life Settlements Life Settlements Our Product is Simple. We provide a solid financial tool to people who want a safe, stable, easy to understand financial

AMG Financial Services a division of Presents Life Settlements Life Settlements Our Product is Simple. We provide a solid financial tool to people who want a safe, stable, easy to understand financial

ADVISING CLIENTS ABOUT LIFE INSURANCE: A PRIMER 1. By Andrew J. Willms, J.D. LL.M. John C. Zimdars, Jr., CLU ChFC. Introduction

ADVISING CLIENTS ABOUT LIFE INSURANCE: A PRIMER 1 By Andrew J. Willms, J.D. LL.M. John C. Zimdars, Jr., CLU ChFC Introduction Over the last several years, tax reform has made tax planning increasingly

ADVISING CLIENTS ABOUT LIFE INSURANCE: A PRIMER 1 By Andrew J. Willms, J.D. LL.M. John C. Zimdars, Jr., CLU ChFC Introduction Over the last several years, tax reform has made tax planning increasingly

64168 MK3373(0209) TC45365(0209) Premium Financing Alternative Funding to Help Meet Your Life Insurance Needs

TC45365(0209) Premium Financing Alternative Funding to Help Meet Your Life Insurance Needs") 64168 MK3373(0209) TC45365(0209) Premium Financing Alternative Funding to Help Meet Your Life Insurance Needs What is Premium Financing? Simply put, premium financing is a strategy for paying for life

64168 MK3373(0209) TC45365(0209) Premium Financing Alternative Funding to Help Meet Your Life Insurance Needs What is Premium Financing? Simply put, premium financing is a strategy for paying for life

EMPLOYEE STOCK OWNERSHIP PLANS (ESOPs): A BUSINESS SUCCESSION PLANNING TOOL WORTH CONSIDERING

: A BUSINESS SUCCESSION PLANNING TOOL WORTH CONSIDERING") EMPLOYEE STOCK OWNERSHIP PLANS (ESOPs): A BUSINESS SUCCESSION PLANNING TOOL WORTH CONSIDERING By: Chuck Coyne, ASA Empire Valuation Consultants, LLC Tabitha Croscut, Esq. Steiker, Greenapple & Crosut,

EMPLOYEE STOCK OWNERSHIP PLANS (ESOPs): A BUSINESS SUCCESSION PLANNING TOOL WORTH CONSIDERING By: Chuck Coyne, ASA Empire Valuation Consultants, LLC Tabitha Croscut, Esq. Steiker, Greenapple & Crosut,

Canadian Health Insurance

Case study Canadian Health Insurance tax Guide Critical illness insurance in a disability buy-sell agreement December 2013 Life s brighter under the sun Sun Life Assurance Company of Canada, 2013. Sun

Case study Canadian Health Insurance tax Guide Critical illness insurance in a disability buy-sell agreement December 2013 Life s brighter under the sun Sun Life Assurance Company of Canada, 2013. Sun

Planning Solutions. Executive Bonus Plan. Program Highlights & Fact Finder. Transamerica Occidental Life Insurance Company

Planning Solutions Executive Bonus Plan Program Highlights & Fact Finder Transamerica Occidental Life Insurance Company A Rewarding Way to Meet Financial Goals Providing for the family, putting the kids

Planning Solutions Executive Bonus Plan Program Highlights & Fact Finder Transamerica Occidental Life Insurance Company A Rewarding Way to Meet Financial Goals Providing for the family, putting the kids

Understanding Plan Fees and Expenses

Understanding Plan Fees and Expenses Susan M. Wright, CPA, APM Executive Director, Consulting Topics of Discussion Fiduciary Responsibilities Settlor vs. Non-settlor Expenses Revenue Holding Accounts Questions

Understanding Plan Fees and Expenses Susan M. Wright, CPA, APM Executive Director, Consulting Topics of Discussion Fiduciary Responsibilities Settlor vs. Non-settlor Expenses Revenue Holding Accounts Questions

The owner is usually the purchaser of the policy. However, the owner may also acquire the policy by gift, sale, exchange, or bequest.

Annuity Ownership Considerations What is an annuity owner? What are the owner's rights? Who should be the owner? What if the owner dies? Is the annuity includable in the owner's estate? What risks does

Annuity Ownership Considerations What is an annuity owner? What are the owner's rights? Who should be the owner? What if the owner dies? Is the annuity includable in the owner's estate? What risks does

Premium Finance Programs

Marketing Guide Life Insurance Premium Finance Programs Information and Guidelines FOR BROKER-DEALER OR AGENT USE ONLY LBL8190 Providing the life insurance coverage your customers need. Help your customers

Marketing Guide Life Insurance Premium Finance Programs Information and Guidelines FOR BROKER-DEALER OR AGENT USE ONLY LBL8190 Providing the life insurance coverage your customers need. Help your customers