The Reformed New World of Health Insurance Exchanges. Arthur Lerner Barbara Ryland

|

|

|

- Muriel Welch

- 8 years ago

- Views:

Transcription

1 The Reformed New World of Health Insurance Exchanges Arthur Lerner Barbara Ryland

2 Introduction State Insurance Exchanges are a key component of the health reform legislation What are the Exchanges? What is the objective? How are they going to work? Who gets to play? How big is your briefcase?

3 Exchanges Each State must establish by 1/1/2014 an American Health Benefit Exchange that will make insurers qualified health plans ( QHPs ) available to individuals and small groups. Outside the Exchange: Individuals and employers may purchase non-exchange health plans, and employers may self-insure. A State can have one Exchange for individual coverage and another for a Small Business Health Options Program ( SHOP Exchange ) or may merge them. An Exchange can be a government agency or a nonprofit entity established by the State. Multi-state Exchanges are permitted. Exchanges can charge insurers user fees.

4 Exchange Functions Certify QHPs for participation Determine insurer products to include in Exchange offerings Provide ratings of plan premiums and quality Internet portal for consumers Can contract for administrative support, but not with a health insurer or any entity related to an insurer

5 Navigators Navigators act essentially as consumer ombudsmen, educating the public, distributing information about QHPs, availability of premium tax credits and cost-sharing reductions, facilitating enrollment, providing referrals related to grievances or complaints or questions about health plans or coverage or claim determinations. Navigators can be trade or professional associations, consumer groups, unions, chambers of commerce, insurance agents and brokers, and resource partners of the Small Business Administration, chosen by the Exchange. Navigators must meet standards and may not be health insurance issuers.

6 Eligible Individuals Any person qualifies for individual Exchange QHP coverage if he or she lives in the State, is not incarcerated (except for those awaiting disposition of charges) and is a citizen or an alien anticipated to be lawfully in the country for the enrollment period.

7 Small Groups A small employer with an ERISA group health plan can participate in the Exchange if all full-time employees are eligible for coverage. Small group means an employer that in the previous year averaged 1 or more employees but not more than 100. Until 2016, a State can substitute 50 for 100. A small employer in the Exchange will continue to be treated as small until it leaves the Exchange, even if it becomes larger.

8 Large Groups Large groups may not participate in state Exchanges until Starting in 2017, a State may permit insurers to provide coverage for large employers through the Exchange. The law clearly provides that States can permit issuers to include large employers in Exchange products in Other language suggests that if the State does so, an employer electing to buy through the Exchange cannot be denied participation by an insurer.

9 Exchange Standards The Secretary will set minimum standards that Exchanges must use in certifying QHPs for participation. Required standards will be set for: marketing; network adequacy; inclusion of essential community providers willing to accept the generally applicable payment rates of the plan; accreditation; quality improvement; uniform enrollment forms; and standardized benefit presentation format permitting consumer comparisons.

10 Essential Health Benefits Each QHP must offer a core set of essential health benefits set by HHS. The scope of essential health benefits must equal the scope of benefits provided under a typical employer plan. Financial incentives will discourage States from requiring Exchange plans to offer additional benefits. If a State mandates additional benefits, it must provide payment to the enrollee, or to the plan on the individual s behalf, for the incremental premium cost attributable to the extra mandated benefit. No impact on state benefit mandates outside Exchange.

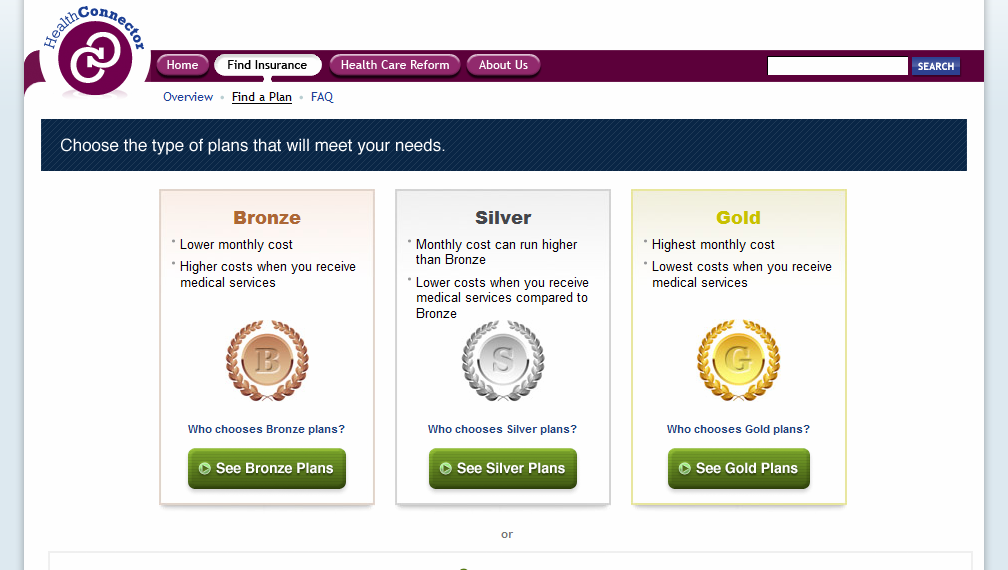

11 Levels of Coverage Plans will be offered at bronze, silver, gold and platinum levels, representing 60, 70, 80 and 90% actuarial value of the full covered benefits (i.e., as if there were no cost sharing provisions). Employer contributions to HSAs to count in determining actuarial value of a plan. If a QHP is offered through the Exchange at any of the four levels, the issuer must also offer it as a separate QHP for individuals under the age of 21. Catastrophic plan may also be a QHP, but only for those under age 30 or those who satisfy hardship or prior uninsured status requirements. Employer can choose the level of coverage (e.g., bronze, silver, gold or platinum) to support via contribution.

12 Deductibles Employer small group plans in Exchange may not have deductibles >$2,000 for individual coverage and >$4,000 for family coverage. These may be increased by employer contributions under flexible spending plans. The cap rises by a percentage formula for years after 2014 and is then rounded up to the nearest $50 increment

13 Massachusetts Exchange Visiting the Connector

14

15

16

17

18 Premium and Rating Rules Exchange coverage insurers must agree to charge the same premium for each QHP it issues, whether it is offered through an Exchange, directly from the issuer or through an agent. The Act does not provide further detail on this requirement of uniform pricing both within and outside the Exchange. Same community rating type rules apply in Exchange and out. Insurers can vary rates within state by rating area. There are specific risk pooling requirements for QHP issuers. All individual enrollees (except in grandfathered plans), including those who do not enroll through the Exchange, are members of a single risk pool. All small group enrollees in a State are also to be considered a single risk pool (excluding grandfathered plan enrollment). A State may require these individual and small group pools to be combined.

, including those who do not enroll through the Exchange, are members of a single risk pool.")

19 Grandfathered Plans Grandfathered plans are those in which an individual was enrolled on March 23, The Act s requirements for medical loss ratios and uniform coverage documents apply to grandfathered plans. Family members of an individual in a grandfathered plan are permitted to enroll in the plan or coverage if enrollment was permitted under the terms of the plan in effect as of March 23, A group health plan already providing coverage on the date of enactment may also cover new employees and their families Health insurance coverage provided pursuant to one or more collective bargaining agreements is grandfathered until the last of the collective bargaining agreements terminates.

20 Medical Home Plans QHPs can provide coverage through a qualified direct primary care medical home plan that meets regulatory criteria if the medical home plan services are coordinated with the entity offering the QHP. Medical home model of care is coordinated and integrated care that includes: personal physicians for individual enrollee; evidence-informed medicine; use of health information technology; continuous quality improvements; expanded access to care; and payment that recognizes added value from additional components of patient-centered care.

21 CO-OPs Up to $6 billion in loan and grant money by 7/1/2013 to seed new non-profit Consumer Operated and Oriented Plans ( CO OPs ) to offer QHPs to individuals and small groups. HHS to ensure that there is enough funding to establish at least one new CO-OP in each State. HHS to give priority to funding CO-OPs that will offer QHPs on a state-wide basis, will utilize integrated care models, and have significant private support. CO-OP cannot be an entity that is already an insurer or that is affiliated with an entity already an insurer as of July CO-OP must be governed by its members, and governing documents must protect against insurance industry involvement and interference. CO-OPs may form a private purchasing council to do collective purchasing, such as for claims administration, administrative services, and health information technology.

22 Basic Health Programs States can establish a basic health program outside the Exchange, that offers a standard health plan with essential health benefits for individuals who qualify based on income. Basic health program can provide benefits directly or through contract with the following: Licensed HMOs or insurance issuers; Network[s] of health care providers established to offer services under the program can contract with the state to provide the standard health plan

23 Cross-State Choice Compacts States may create health care choice compacts. QHP could be offered in the individual market in each of the States, but will largely be subject to the laws only of the State in which the plan was written or issued (i.e., not where it was delivered). Each participating State s laws would continue to apply in the areas of market conduct, unfair trade practices, network adequacy and consumer protection standards. Issuers would either have to be licensed in each participating State or submit to the jurisdiction of each State for permitted regulation.

24 Federal Multi-State Plan Contracts Office of Personnel Management ( OPM ) to contract with health insurance issuers to offer two multi-state QHPs to be available through each Exchange. Issuer may be group of issuers affiliated by common control or common use of national licensed service mark. At least one of the contracts must be with a non-profit entity. Federal government will negotiate premiums, profit margin and medical loss ratio. Contracting process modeled after FEHBP practice for experience rated carriers Approved multi-state QHPs are deemed certified for Exchange participation. By its fourth year, multi-state QHP must cover whole country.

25 Subsidy for Individual Plan Risk Adjustment Reinsurance By January 1, 2014, each State should establish or contract with reinsurance entities for a program under which health insurers, and TPAs on behalf of group health plans, must make payments, except for plans that have a grandfather exception. Collected premiums paid out as risk adjustments to participating health insurance issuers that cover high risk individuals in the individual market. Contributions will proportionally reflect issuer s fully insured commercial book of business for major medical products and the total value of fees charged by the issuer and the costs of coverage administered by the issuer as a TPA. Additional amounts may be assessed to fund the reinsurance entity s administrative expenses.

26 TPA Interface with Customer Plans to Fund Risk Adjustment Reinsurance Payment TPA is responsible for paying reinsurance contributions on behalf of self-insured group health plans, but the law does not establish a mechanism for collecting or recouping funds by TPA from self-insured plans. For protection, TPAs will need to secure funding for payments in advance or in real time via contracts with plans.

27 Risk Corridors for Exchange Plans HHS will set up risk corridors for for QHPs in the individual or small group market based on ratio of allowable costs to the plan s aggregate premium. If costs are more than 103%, but not more than 108%, of a target amount : HHS will pay the plan 50% of the excess in costs over 103% of the target. If costs are more than 108% of the target: HHS will pay the plan 2.5% of the target, plus 80% of the costs exceeding 108% of the target. If costs are less than 97%, but not less than 92%, of target: plan will pay HHS 50% of the excess of 97% of the target over the costs. If costs are less than 92% of the target: plan will pay HHS 2.5% of the target amount, plus 80% of the excess of 92% of the target over the costs.

28 Actuarial Risk Adjustment Program Each State will assess a charge on low actuarial risk plans group health plans and health insurance issuers where the actuarial risk of their enrollees is less than the average actuarial risk for all enrollees in plans or coverage in the State that are not self-insured group health plans. The State will make a corresponding payment to high actuarial risk plans whose enrollments actuarial risk is higher than the average. Risk adjustment program applies to health plans and issuers providing coverage in the individual or small group market in a state. The risk adjustment provisions do not apply to grandfathered health plans or the issuers of such plans.

29 Level Playing Field Coverage by private health insurance issuers is exempt from a broad range of federal and state laws if a QHP under the CO- OP or a new Exchange multi-state QHP is not subject to the same law, including: licensure; rating, solvency and other financial requirements; guaranteed renewal, non-discrimination and preexisting conditions; quality improvement and reporting; fraud and abuse; market conduct; prompt payment; appeals and grievances; privacy and confidentiality; and benefit plan materials or information.

Patient Protection and Affordable Care Act of 2009: Health Insurance Exchanges

Patient Protection and Affordable Care Act of 2009: Health Insurance Exchanges Provision Notes Standards SUBTITLE D AVAILABLE COVERAGE CHOICES FOR ALL AMERICANS PART I Establishment of Qualified Health

Patient Protection and Affordable Care Act of 2009: Health Insurance Exchanges Provision Notes Standards SUBTITLE D AVAILABLE COVERAGE CHOICES FOR ALL AMERICANS PART I Establishment of Qualified Health

Focus on Reform: Private Health Insurance Provisions of PPACA

Focus on Reform: Private Health Insurance Provisions of PPACA Bernadette Fernandez May 14, 2010 Agenda Private Health Insurance: Market Reforms and Coverage Programs Pre-PPACA Private health insurance

Focus on Reform: Private Health Insurance Provisions of PPACA Bernadette Fernandez May 14, 2010 Agenda Private Health Insurance: Market Reforms and Coverage Programs Pre-PPACA Private health insurance

EXPLAINING HEALTH CARE REFORM: Risk Adjustment, Reinsurance, and Risk Corridors

EXPLAINING HEALTH CARE REFORM: Risk Adjustment, Reinsurance, and Risk Corridors As of January 1, 2014, insurers are no longer able to deny coverage or charge higher premiums based on preexisting conditions

EXPLAINING HEALTH CARE REFORM: Risk Adjustment, Reinsurance, and Risk Corridors As of January 1, 2014, insurers are no longer able to deny coverage or charge higher premiums based on preexisting conditions

Kansas Insurance Department

Kansas Insurance Department The Affordable Care Act What Happens Now? Kansas Society of CPAs June 5, 2013 Linda J. Sheppard, Special Counsel & Director of Health Care Policy and Analysis 2010 Affordable

Kansas Insurance Department The Affordable Care Act What Happens Now? Kansas Society of CPAs June 5, 2013 Linda J. Sheppard, Special Counsel & Director of Health Care Policy and Analysis 2010 Affordable

ADVERSE SELECTION ISSUES AND HEALTH INSURANCE EXCHANGES UNDER THE AFFORDABLE CARE ACT

Draft: 6/22/11 Reflects revisions to the June 17 draft as discussed during the Health Insurance and Managed Care (B) Committee conference call June 22, 2011 Background ADVERSE SELECTION ISSUES AND HEALTH

Draft: 6/22/11 Reflects revisions to the June 17 draft as discussed during the Health Insurance and Managed Care (B) Committee conference call June 22, 2011 Background ADVERSE SELECTION ISSUES AND HEALTH

Health Care Reform. Overview of Federal Health Insurance Reform Requirements and TDI Implementation Planning

Health Care Reform Overview of Federal Health Insurance Reform Requirements and TDI Implementation Planning Presentation to House Select Committee on Federal Legislation April 22, 2010 Mike Geeslin, Commissioner

Health Care Reform Overview of Federal Health Insurance Reform Requirements and TDI Implementation Planning Presentation to House Select Committee on Federal Legislation April 22, 2010 Mike Geeslin, Commissioner

REGULATORY UPDATE Vol. 1 No. 18

REGULATORY UPDATE Vol. 1 No. 18 FAQs on Exchanges August 7, 2013 IN THIS ISSUE FAQs on Exchanges Employer Mandate Delay Transitional Guidance Issued Individual Mandate Final Rules Issued Possible Exchange

REGULATORY UPDATE Vol. 1 No. 18 FAQs on Exchanges August 7, 2013 IN THIS ISSUE FAQs on Exchanges Employer Mandate Delay Transitional Guidance Issued Individual Mandate Final Rules Issued Possible Exchange

How To Get Health Care Reform For The United States

Federal Health Care Reform: Implications for New York Division of Coverage and Enrollment Office of Health Insurance Programs Health Bureau Insurance Department June 2010 Federal Health Care Reform: Where

Federal Health Care Reform: Implications for New York Division of Coverage and Enrollment Office of Health Insurance Programs Health Bureau Insurance Department June 2010 Federal Health Care Reform: Where

The Healthcare Law April 19, 2010

The Healthcare Law April 19, 2010 This healthcare bill, recently made law, is a comprehensive overhaul that increases coverage to 94% of Americans and makes sweeping changes to our current healthcare system.

The Healthcare Law April 19, 2010 This healthcare bill, recently made law, is a comprehensive overhaul that increases coverage to 94% of Americans and makes sweeping changes to our current healthcare system.

The Role of Insurance Agents and Brokers Under Health Care Reform

T HE J AECKLE A LERT HEALTH CARE PRACTICE GROUP ATTORNEY ADVERTISING The Role of Insurance Agents and Brokers Under Health Care Reform The New York Health Benefit Exchange, the health insurance exchange

T HE J AECKLE A LERT HEALTH CARE PRACTICE GROUP ATTORNEY ADVERTISING The Role of Insurance Agents and Brokers Under Health Care Reform The New York Health Benefit Exchange, the health insurance exchange

HEALTH INSURANCE REFORM in ILLINOIS

HEALTH INSURANCE REFORM in ILLINOIS Overview of Federal Health Insurance Reform Requirements Illinois Department of Insurance Implementation Planning PAT QUINN Governor MICHAEL T. McRAITH Director May

HEALTH INSURANCE REFORM in ILLINOIS Overview of Federal Health Insurance Reform Requirements Illinois Department of Insurance Implementation Planning PAT QUINN Governor MICHAEL T. McRAITH Director May

Health Insurance Exchange Overview

Health Insurance Exchange Overview House Health and Human Services Finance February 15, 2011 April Todd-Malmlov Health Insurance Exchange Director - State Health Economist Minnesota Departments of Commerce

Health Insurance Exchange Overview House Health and Human Services Finance February 15, 2011 April Todd-Malmlov Health Insurance Exchange Director - State Health Economist Minnesota Departments of Commerce

Coinsurance A percentage of a health care provider's charge for which the patient is financially responsible under the terms of the policy.

Glossary of Health Insurance Terms On March 23, 2010, President Obama signed the Patient Protection and Affordable Care Act (PPACA) into law. When making decisions about health coverage, consumers should

Glossary of Health Insurance Terms On March 23, 2010, President Obama signed the Patient Protection and Affordable Care Act (PPACA) into law. When making decisions about health coverage, consumers should

Update: Health Insurance Reforms and Rate Review. Health Insurance Reform Requirements for the Group and Individual Insurance Markets

By Katherine Jett Hayes and Taylor Burke Background Update: Health Insurance Reforms and Rate Review The Patient Protection and Affordable Care Act (ACA) included health insurance market reforms designed

By Katherine Jett Hayes and Taylor Burke Background Update: Health Insurance Reforms and Rate Review The Patient Protection and Affordable Care Act (ACA) included health insurance market reforms designed

HEALTH REFORM AND MULTIEMPLOYER PLAN COVERAGE 2014 AND BEYOND

WWW.BKLAWYERS.COM HEALTH REFORM AND MULTIEMPLOYER PLAN COVERAGE 2014 AND BEYOND ABA SECTION OF LABOR AND EMPLOYMENT LAW EMPLOYEE BENEFITS COMMITTEE MID- WINTER MEETING 201 BLITMAN & KING LLP Franklin Center,

WWW.BKLAWYERS.COM HEALTH REFORM AND MULTIEMPLOYER PLAN COVERAGE 2014 AND BEYOND ABA SECTION OF LABOR AND EMPLOYMENT LAW EMPLOYEE BENEFITS COMMITTEE MID- WINTER MEETING 201 BLITMAN & KING LLP Franklin Center,

Final Regulations on Health Insurance Exchanges

Health Care Reform Legislative Brief Final Regulations on Health Insurance Exchanges Beginning in 2014, individuals and small businesses will be able to purchase private health insurance through state-based

Health Care Reform Legislative Brief Final Regulations on Health Insurance Exchanges Beginning in 2014, individuals and small businesses will be able to purchase private health insurance through state-based

Nebraska Health Insurance Exchange Update

Nebraska Health Insurance Exchange Update State of Nebraska s Health Insurance Exchange A Presentation to the Public September, 2012 TODAY'S AGENDA Section 1: Overview of Health Insurance Exchanges Section

Nebraska Health Insurance Exchange Update State of Nebraska s Health Insurance Exchange A Presentation to the Public September, 2012 TODAY'S AGENDA Section 1: Overview of Health Insurance Exchanges Section

Health Insurance Exchange Overview

Health Insurance Exchange Overview Minnesota Health Insurance Exchange Advisory Task Force November 8, 2011 Overview Existing Market Challenges What is an Exchange? Exchange Opportunities Exchange Components

Health Insurance Exchange Overview Minnesota Health Insurance Exchange Advisory Task Force November 8, 2011 Overview Existing Market Challenges What is an Exchange? Exchange Opportunities Exchange Components

Health Insurance Marketplace. vhealth insurance exchanges. What to expect in 2014. What to expect in 2014

vhealth insurance exchanges Health Insurance Marketplace What to expect in 2014 What to expect in 2014 The basics of exchanges As part of the Affordable Care Act (ACA or health care reform law), starting

vhealth insurance exchanges Health Insurance Marketplace What to expect in 2014 What to expect in 2014 The basics of exchanges As part of the Affordable Care Act (ACA or health care reform law), starting

Health Reform. Senate Leadership Bill Patient Protection and Affordable Care Act (H.R. 3590)

") on Health Reform Comprehensive health reform legislation is currently being debated in Congress. On November 7, 2009, the U.S. House of Representatives passed the Affordable Health Care for America Act

on Health Reform Comprehensive health reform legislation is currently being debated in Congress. On November 7, 2009, the U.S. House of Representatives passed the Affordable Health Care for America Act

Federally-facilitated Marketplace Agent and Broker Training Outline and Summary

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard Baltimore, Maryland 21244-1850 Center for Consumer Information & Insurance Oversight Federally-facilitated

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard Baltimore, Maryland 21244-1850 Center for Consumer Information & Insurance Oversight Federally-facilitated

OVERVIEW OF PRIVATE INSURANCE MARKET REFORMS IN THE PATIENT PROTECTION AND AFFORDABLE CARE ACT AND RESOURCES FOR FREQUENTLY ASKED QUESTIONS

OVERVIEW OF PRIVATE INSURANCE MARKET REFORMS IN THE PATIENT PROTECTION AND AFFORDABLE CARE ACT AND RESOURCES FOR FREQUENTLY ASKED QUESTIONS Brief Prepared by MATTHEW COKE Senior Research Attorney LEGISLATIVE

OVERVIEW OF PRIVATE INSURANCE MARKET REFORMS IN THE PATIENT PROTECTION AND AFFORDABLE CARE ACT AND RESOURCES FOR FREQUENTLY ASKED QUESTIONS Brief Prepared by MATTHEW COKE Senior Research Attorney LEGISLATIVE

Exchange 101. August 2013

Exchange 101 August 2013 455430 27517 Penalties for individuals 2017 and beyond: Annual adjustments 2016: Greater of $695 or 2.5% of taxable income 2015: Greater of $325 or 2% of taxable income 2014: Greater

Exchange 101 August 2013 455430 27517 Penalties for individuals 2017 and beyond: Annual adjustments 2016: Greater of $695 or 2.5% of taxable income 2015: Greater of $325 or 2% of taxable income 2014: Greater

Health insurance Marketplace. What to expect in 2014

Health insurance Marketplace What to expect in 2014 Overview The Affordable Care Act (ACA) includes several provisions geared to extend greater access to health insurance benefits to more people. Beginning

Health insurance Marketplace What to expect in 2014 Overview The Affordable Care Act (ACA) includes several provisions geared to extend greater access to health insurance benefits to more people. Beginning

Health Care Reform: Ready or Not, Here it Comes! Presented by:

Broader Perspective. Business Solutions. Health Care Reform: Ready or Not, Here it Comes! Presented by: Ryan Fridborg, MAOD, SPHR Executive Vice President, Employee Benefits rfridborg@boltonco.com Marilyn

Broader Perspective. Business Solutions. Health Care Reform: Ready or Not, Here it Comes! Presented by: Ryan Fridborg, MAOD, SPHR Executive Vice President, Employee Benefits rfridborg@boltonco.com Marilyn

DRAFT FOR PUBLIC COMMENT February 8, 2016

State of Vermont Department of Vermont Health Access [Phone] 802-879-5900 280 State Drive, NOB 1 South Waterbury, VT 05671-1010 http://dvha.vermont.gov Agency of Human Services Vermont s Proposal to Waive

State of Vermont Department of Vermont Health Access [Phone] 802-879-5900 280 State Drive, NOB 1 South Waterbury, VT 05671-1010 http://dvha.vermont.gov Agency of Human Services Vermont s Proposal to Waive

The Health Benefit Exchange and the Commercial Insurance Market

The Health Benefit Exchange and the Commercial Insurance Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges, that

The Health Benefit Exchange and the Commercial Insurance Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges, that

Patient Protection and Affordable Care Act of 2009: Immediate Health Insurance Market Reforms

Patient Protection and Affordable Care Act of 2009: Immediate Health Insurance Market Reforms Provision Notes Standards Development Applicability Effective Date PPACA Statutory Annual and Lifetime Limits

Patient Protection and Affordable Care Act of 2009: Immediate Health Insurance Market Reforms Provision Notes Standards Development Applicability Effective Date PPACA Statutory Annual and Lifetime Limits

SMALL BUSINESS HEALTH OPTIONS PROGRAM

SMALL BUSINESS HEALTH OPTIONS PROGRAM This summary provides an overview of what is currently known about the Small Business Health Options Program (commonly referred to as "SHOP"), an aspect of the American

SMALL BUSINESS HEALTH OPTIONS PROGRAM This summary provides an overview of what is currently known about the Small Business Health Options Program (commonly referred to as "SHOP"), an aspect of the American

Private Health Insurance Provisions in the Patient Protection and Affordable Care Act (PPACA)

") Private Health Insurance Provisions in the Patient Protection and Affordable Care Act (PPACA) Hinda Chaikind Specialist in Health Care Financing Bernadette Fernandez Analyst in Health Care Financing Mark

Private Health Insurance Provisions in the Patient Protection and Affordable Care Act (PPACA) Hinda Chaikind Specialist in Health Care Financing Bernadette Fernandez Analyst in Health Care Financing Mark

Summary of the Major Provisions in the Patient Protection and Affordable Health Care Act

Summary of the Major Provisions in the Patient Protection and Affordable Care Act Updated 10/22/10 On March 23, 2010, President Barack Obama signed into law comprehensive health care reform legislation,

Summary of the Major Provisions in the Patient Protection and Affordable Care Act Updated 10/22/10 On March 23, 2010, President Barack Obama signed into law comprehensive health care reform legislation,

How To Get Rid Of The Health Insurance Mandate In The United States

on Health Reform Comprehensive health reform legislation is currently being debated in Congress. On November 7, 2009, the U.S. House of Representatives passed the Affordable Health Care for America Act

on Health Reform Comprehensive health reform legislation is currently being debated in Congress. On November 7, 2009, the U.S. House of Representatives passed the Affordable Health Care for America Act

Senate HELP Committee Affordable Health Choices Act (S. 1679) June 9, 2009 (passed by Committee July 15, 2009)

June 9, 2009 (passed by Committee July 15, 2009)") on Health Reform This side-by-side compares the leading comprehensive reform proposals across a number of key characteristics and plan components. Included in this side-byside are proposals for moving

on Health Reform This side-by-side compares the leading comprehensive reform proposals across a number of key characteristics and plan components. Included in this side-byside are proposals for moving

FAQ New Health Insurance Law

FAQ New Health Insurance Law (Enacted on March 21, signed into law on March 23, and amended on March 25) On March 23, 2010 President Barack Obama signed the Patient Protection & Affordable Care Act (H.R.

FAQ New Health Insurance Law (Enacted on March 21, signed into law on March 23, and amended on March 25) On March 23, 2010 President Barack Obama signed the Patient Protection & Affordable Care Act (H.R.

Everything about Exchanges you ve wanted to know... HHS Issues Proposed Rules

This article originally appeared in the July 2011 Quarterly Review. Everything about Exchanges you ve wanted to know... HHS Issues Proposed Rules New Proposed Rules set standards, certify health plans,

This article originally appeared in the July 2011 Quarterly Review. Everything about Exchanges you ve wanted to know... HHS Issues Proposed Rules New Proposed Rules set standards, certify health plans,

How To Pass The Health Care Reform Bill

The Patient Protection and Affordable Care Act as Passed Section by Section Analysis with Changes Made by Title X included within Titles I IX, where Appropriate Some parts of Title X made changes to provisions

The Patient Protection and Affordable Care Act as Passed Section by Section Analysis with Changes Made by Title X included within Titles I IX, where Appropriate Some parts of Title X made changes to provisions

The Affordable Care Act: The Health Insurance Marketplace -- What Does It Mean for Individuals, Families, and Employers?

The Patient Protection and Affordable Care Act (ACA) includes provisions that will have significant implications for individuals, families and employers in 2014. These provisions include: The creation

The Patient Protection and Affordable Care Act (ACA) includes provisions that will have significant implications for individuals, families and employers in 2014. These provisions include: The creation

Nebraska Health Insurance Exchange Update

Nebraska Health Insurance Exchange Update Affordable Care Act Implementation March 2013 IMPLEMENTATION TIMELINE 2010 2011 2012 2013 2014 2015 2016 2017 Temporary High Risk Pool Program Temporary Reinsurance

Nebraska Health Insurance Exchange Update Affordable Care Act Implementation March 2013 IMPLEMENTATION TIMELINE 2010 2011 2012 2013 2014 2015 2016 2017 Temporary High Risk Pool Program Temporary Reinsurance

Patient Protection and Affordable Care Act (ACA) ACA Guide for Group Employers Agent and Broker Information

ACA Guide for Group Employers Agent and Broker Information") Patient Protection and Affordable Care Act (ACA) ACA Guide for Group Employers Agent and Broker Information DISCLAIMER 2 This information is being provided in an effort to alert you to changes required

Patient Protection and Affordable Care Act (ACA) ACA Guide for Group Employers Agent and Broker Information DISCLAIMER 2 This information is being provided in an effort to alert you to changes required

Health Care Reform Update

Small Businesses No Financial Requirements for Small Businesses: The ACA imposes no financial requirements for small businesses to contribute to their employees health insurance. However, beginning in

Small Businesses No Financial Requirements for Small Businesses: The ACA imposes no financial requirements for small businesses to contribute to their employees health insurance. However, beginning in

Christy Tinnes, Brigen Winters and Christine Keller, Groom Law Group, Chartered

Preparing for Health Care Reform A Chronological Guide for Employers This Article provides an overview of the major provisions of health care reform legislation affecting employers and explains the requirements

Preparing for Health Care Reform A Chronological Guide for Employers This Article provides an overview of the major provisions of health care reform legislation affecting employers and explains the requirements

Health Insurance Exchange Proposed Rules

Health Insurance Exchange Proposed Rules Karen Fisher, J.D. 202-862-6140 kfisher@aamc.org Jane Eilbacher 202-828-0896 jeilbacher@aamc.org Will Dardani 202-828-0541 wdardani@aamc.org Exchange Rules Overview

Health Insurance Exchange Proposed Rules Karen Fisher, J.D. 202-862-6140 kfisher@aamc.org Jane Eilbacher 202-828-0896 jeilbacher@aamc.org Will Dardani 202-828-0541 wdardani@aamc.org Exchange Rules Overview

American Health Benefit Exchanges Fact Sheet A Provision of the Patient Protection and Affordable Care Act (PPACA)

") American Health Benefit Exchanges Fact Sheet A Provision of the Patient Protection and Affordable Care Act (PPACA) This Fact Sheet reflects the Final Ruling published by the Department of Health and Human

American Health Benefit Exchanges Fact Sheet A Provision of the Patient Protection and Affordable Care Act (PPACA) This Fact Sheet reflects the Final Ruling published by the Department of Health and Human

Simple answers to health reform s complex issues facing every employer, and what you can do now to protect your business and your future.

Simple answers to health reform s complex issues facing every employer, and what you can do now to protect your business and your future. If you have any questions, please contact: Health Reform: A Guide

Simple answers to health reform s complex issues facing every employer, and what you can do now to protect your business and your future. If you have any questions, please contact: Health Reform: A Guide

Patient Protection and Affordable Care Act (H.R. 3590)

") on Health Reform Passing comprehensive health care reform has been a priority of the President and Congress. The U.S. House of Representatives passed the Affordable Health Care for America Act on November

on Health Reform Passing comprehensive health care reform has been a priority of the President and Congress. The U.S. House of Representatives passed the Affordable Health Care for America Act on November

Overview of Health Insurance Exchanges in the USET Area. USET Impact Week February 4-7, 2013 Washington, DC

Overview of Health Insurance Exchanges in the USET Area USET Impact Week February 4-7, 2013 Washington, DC 1 Affordable Care Act (ACA) Insurance Reforms No lifetime limits, annual limits Pre-existing conditions

Overview of Health Insurance Exchanges in the USET Area USET Impact Week February 4-7, 2013 Washington, DC 1 Affordable Care Act (ACA) Insurance Reforms No lifetime limits, annual limits Pre-existing conditions

Health Policy Essentials: Private Health Insurance. Bernadette Fernandez, Annie Mach, & Namrata Uberoi February 13, 2015

Health Policy Essentials: Private Health Insurance Bernadette Fernandez, Annie Mach, & Namrata Uberoi February 13, 2015 Briefing Agenda What is the purpose of private health insurance (PHI)? How is PHI

Health Policy Essentials: Private Health Insurance Bernadette Fernandez, Annie Mach, & Namrata Uberoi February 13, 2015 Briefing Agenda What is the purpose of private health insurance (PHI)? How is PHI

Health Care Reform Frequently Asked Questions (FAQ) Consumers Employers

Consumers Employers") This page provides answers to frequently asked questions (FAQ) regarding The Patient Protection and Affordable Care Act (PPACA; P.L. 111-148) and the Health Care and Education Reconciliation Act of 2010

This page provides answers to frequently asked questions (FAQ) regarding The Patient Protection and Affordable Care Act (PPACA; P.L. 111-148) and the Health Care and Education Reconciliation Act of 2010

Adverse Selection Issues and Health Insurance Exchanges Under the Affordable Care Act. Not for Reprint

Adverse Selection Issues and Health Insurance Exchanges Under the Affordable Care Act Adverse Selection Issues and Health Insurance Exchanges Under the Affordable Care Act 2011 The NAIC is the authoritative

Adverse Selection Issues and Health Insurance Exchanges Under the Affordable Care Act Adverse Selection Issues and Health Insurance Exchanges Under the Affordable Care Act 2011 The NAIC is the authoritative

Overview of Private Health Insurance Provisions in the Patient Protection and Affordable Care Act (ACA)

") Overview of Private Health Insurance Provisions in the Patient Protection and Affordable Care Act (ACA) Annie L. Mach Analyst in Health Care Financing Namrata K. Uberoi Analyst in Health Care Financing

Overview of Private Health Insurance Provisions in the Patient Protection and Affordable Care Act (ACA) Annie L. Mach Analyst in Health Care Financing Namrata K. Uberoi Analyst in Health Care Financing

Connecticut Health Insurance Exchange. June 2012 [SHOP BRIEFING] An overview of the Small Business Health Options Program (SHOP) Exchange

![Connecticut Health Insurance Exchange. June 2012 [SHOP BRIEFING] An overview of the Small Business Health Options Program (SHOP) Exchange](/thumbs/32/15645614.jpg "Connecticut Health Insurance Exchange. June 2012 [SHOP BRIEFING] An overview of the Small Business Health Options Program (SHOP) Exchange") Connecticut Health Insurance Exchange June 2012 [SHOP BRIEFING] An overview of the Small Business Health Options Program (SHOP) Exchange Overview The federal health care reform law directs states to set

Connecticut Health Insurance Exchange June 2012 [SHOP BRIEFING] An overview of the Small Business Health Options Program (SHOP) Exchange Overview The federal health care reform law directs states to set

The Affordable Care Act: What Does it Mean for Individuals and Families?

The Affordable Care Act: What Does it Mean for Individuals and Families? FIRM Team Fact Sheet 13-04 Available at http://www.firm.msue.msu.edu David B. Schweikhardt Adam J. Kantrovich Brenda R. Long Michigan

The Affordable Care Act: What Does it Mean for Individuals and Families? FIRM Team Fact Sheet 13-04 Available at http://www.firm.msue.msu.edu David B. Schweikhardt Adam J. Kantrovich Brenda R. Long Michigan

Keeping up with the new health care reform law. Helping you better understand what to expect and when to expect it. anthem.com/ca 14376CAEENABC 8/10

Keeping up with the new health care reform law Helping you better understand what to expect and when to expect it. 14376CAEENABC 8/10 anthem.com/ca 1 Staying up to date Here s a timeline of what you can

Keeping up with the new health care reform law Helping you better understand what to expect and when to expect it. 14376CAEENABC 8/10 anthem.com/ca 1 Staying up to date Here s a timeline of what you can

Section by Section Analysis with Changes Made by Title X and Reconciliation

Section by Section Analysis with Changes Made by Title X and Reconciliation Some parts of Title X (the Managers Amendment) and the Health Care and Education Reconciliation Act (Reconciliation Act) made

Section by Section Analysis with Changes Made by Title X and Reconciliation Some parts of Title X (the Managers Amendment) and the Health Care and Education Reconciliation Act (Reconciliation Act) made

Self-insured Plans under Health Care Reform

Brought to you by Good Neighbor Insurance Self-insured Plans under Health Care Reform The Affordable Care Act (ACA) includes numerous reforms affecting the health coverage that employers provide to their

Brought to you by Good Neighbor Insurance Self-insured Plans under Health Care Reform The Affordable Care Act (ACA) includes numerous reforms affecting the health coverage that employers provide to their

What an employer should know about Health Care Reform

What an employer should know about Health Presented By David L. Fear, Sr. RHU NAHU Education Foundation Sponsored by PPACA - history Signed into law in March, 2010 2,700 page rough draft became the law

What an employer should know about Health Presented By David L. Fear, Sr. RHU NAHU Education Foundation Sponsored by PPACA - history Signed into law in March, 2010 2,700 page rough draft became the law

Patient Protection and Affordable Care Act (ACA) ACA Guide for Group Employers Employer Information

ACA Guide for Group Employers Employer Information") Patient Protection and Affordable Care Act (ACA) ACA Guide for Group Employers Employer Information DISCLAIMER 2 This information is being provided in an effort to alert you to changes required by the

Patient Protection and Affordable Care Act (ACA) ACA Guide for Group Employers Employer Information DISCLAIMER 2 This information is being provided in an effort to alert you to changes required by the

Selected Employer Provisions in the Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act of 2010

Selected Employer Provisions in the Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act of 2010 This chart outlines, in depth, selected provisions in the Patient

Selected Employer Provisions in the Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act of 2010 This chart outlines, in depth, selected provisions in the Patient

Update. Director of Policy and National Health Care Reform Coordinator. Roni Mansur Chief Operating Officer. Board of Directors Meeting March 8, 2012

National Health Care Reform Update Kaitlyn Kenney Director of Policy and National Health Care Reform Coordinator Roni Mansur Chief Operating Officer Board of Directors Meeting March 8, 2012 Agenda Update

National Health Care Reform Update Kaitlyn Kenney Director of Policy and National Health Care Reform Coordinator Roni Mansur Chief Operating Officer Board of Directors Meeting March 8, 2012 Agenda Update

Legislative Brief: COMPREHENSIVE HEALTH COVERAGE ESSENTIAL HEALTH BENEFITS PACKAGE

Laurus Strategies Legislative Brief: COMPREHENSIVE HEALTH COVERAGE ESSENTIAL HEALTH BENEFITS PACKAGE The Affordable Care Act (ACA) requires non grandfathered health insurance plans in the individual and

Laurus Strategies Legislative Brief: COMPREHENSIVE HEALTH COVERAGE ESSENTIAL HEALTH BENEFITS PACKAGE The Affordable Care Act (ACA) requires non grandfathered health insurance plans in the individual and

Health Care Reform. Employer Action Overview

Health Care Reform Page 1 of 6 Health Care Reform Immediatemmediate Employer Action Required Notes Employers must provide a reasonable break time for employees who are nursing mothers to express breast

Health Care Reform Page 1 of 6 Health Care Reform Immediatemmediate Employer Action Required Notes Employers must provide a reasonable break time for employees who are nursing mothers to express breast

Nebraska Health Insurance Exchange Update

Nebraska Health Insurance Exchange Update Overview of the Affordable Care Act and the Federally Facilitated marketplace. September 2014 AFFORDABLE CARE ACT» The Affordable Care Act: Establishes a Health

Nebraska Health Insurance Exchange Update Overview of the Affordable Care Act and the Federally Facilitated marketplace. September 2014 AFFORDABLE CARE ACT» The Affordable Care Act: Establishes a Health

to Health Care Reform

The Employer s Guide to Health Care Reform What you need to know now to: Consider your choices Decide what s best for you Follow the rules 2013-2014 Health care reform is the law of the land. Some don

The Employer s Guide to Health Care Reform What you need to know now to: Consider your choices Decide what s best for you Follow the rules 2013-2014 Health care reform is the law of the land. Some don

Small Business Tax Credit

Small Business Tax Credit Effective January 1, 2010 Up to 4 million small businesses are eligible for tax credits to help them provide insurance benefits to their workers. The first phase of this provision

Small Business Tax Credit Effective January 1, 2010 Up to 4 million small businesses are eligible for tax credits to help them provide insurance benefits to their workers. The first phase of this provision

Reporting Requirements for Employers and Health Plans

Brought to you by Cross Employee Benefits Reporting Requirements for Employers and Health Plans The Affordable Care Act (ACA) created a number of federal reporting requirements for employers and health

Brought to you by Cross Employee Benefits Reporting Requirements for Employers and Health Plans The Affordable Care Act (ACA) created a number of federal reporting requirements for employers and health

Attached is a revised version of our side-by-side comparison of key provisions of the House and Senate-passed bills in the following areas:

Both the House and Senate have now passed comprehensive health care reform bills. The House passed the "Affordable Health Care for America Act" (H.R. 3962) on November 7, 2009, while the Senate passed

Both the House and Senate have now passed comprehensive health care reform bills. The House passed the "Affordable Health Care for America Act" (H.R. 3962) on November 7, 2009, while the Senate passed

Presentation for Licensed Producers The Affordable Care Act

Presentation for Licensed Producers The Affordable Care Act Bruce Donaldson, CHC Producer & Stakeholder Specialist Arkansas Insurance Department Affordable Care Act The ACA was passed by Congress and signed

Presentation for Licensed Producers The Affordable Care Act Bruce Donaldson, CHC Producer & Stakeholder Specialist Arkansas Insurance Department Affordable Care Act The ACA was passed by Congress and signed

Issue Brief: The Health Benefit Exchange and the Small Employer Market

Issue Brief: The Health Benefit Exchange and the Small Employer Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges,

Issue Brief: The Health Benefit Exchange and the Small Employer Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges,

Health Reform: A Guide for Employers

Updated with information on the Supreme Court health reform decision July 2012 Health Reform: A Guide for Employers Simple answers to health reform s complex issues facing every employer and what you can

Updated with information on the Supreme Court health reform decision July 2012 Health Reform: A Guide for Employers Simple answers to health reform s complex issues facing every employer and what you can

Introduction. Affordable Care Act Overview of Changes

Introduction Affordable Care Act Overview of Changes Presented by: Tim Dillingham, CLU Benefit Resource Group, Inc. 201 E Broad Street, Suite 1 Linden, MI 48451 810-735-6500 810-735-6610 (fax) tim@benefitresourcegroup.net

Introduction Affordable Care Act Overview of Changes Presented by: Tim Dillingham, CLU Benefit Resource Group, Inc. 201 E Broad Street, Suite 1 Linden, MI 48451 810-735-6500 810-735-6610 (fax) tim@benefitresourcegroup.net

Important Effective Dates for Employers and Health Plans

Brought to you by Sullivan Benefits Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into law.

Brought to you by Sullivan Benefits Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into law.

What is a state health insurance exchange (i.e. "American Health Benefit Exchange")?

?") MEMORANDUM DATE: 11/07/2011 TO: Members of the House Appropriation Subcommittee for LARA FROM: Paul Holland, Fiscal Analyst RE: State Health Insurance Exchanges In response to the requirements pertaining

MEMORANDUM DATE: 11/07/2011 TO: Members of the House Appropriation Subcommittee for LARA FROM: Paul Holland, Fiscal Analyst RE: State Health Insurance Exchanges In response to the requirements pertaining

Federal Health Reform FAQs

Federal Health Reform FAQs Individuals 1. What is an exchange? An exchange, as created under the Affordable Care Act (ACA), is a place where consumers can purchase subsidized health insurance coverage.

Federal Health Reform FAQs Individuals 1. What is an exchange? An exchange, as created under the Affordable Care Act (ACA), is a place where consumers can purchase subsidized health insurance coverage.

Insurance Market Reforms in the Patient Protection & Affordable Care Act and the Health Care & Education Reconciliation Act

Insurance Market Reforms in the Patient Protection & Affordable Care Act and the Health Care & Education Reconciliation Act The new health care reform legislation will provide significant new options for

Insurance Market Reforms in the Patient Protection & Affordable Care Act and the Health Care & Education Reconciliation Act The new health care reform legislation will provide significant new options for

1. Establishment of SHOPs

Page 1 of 10 Checkpoint Contents Pension & Benefits Library Pension & Benefits Editorial Materials EBIA Benefits Compliance Library Health Care Reform for Employers and Advisors XXI. Exchanges, Qualified

Page 1 of 10 Checkpoint Contents Pension & Benefits Library Pension & Benefits Editorial Materials EBIA Benefits Compliance Library Health Care Reform for Employers and Advisors XXI. Exchanges, Qualified

The Patient Protection and Affordable Care Act. Implementation Timeline

The Patient Protection and Affordable Care Act Implementation Timeline 2009 Credit to Encourage Investment in New Therapies: A two year temporary credit subject to an overall cap of $1 billion to encourage

The Patient Protection and Affordable Care Act Implementation Timeline 2009 Credit to Encourage Investment in New Therapies: A two year temporary credit subject to an overall cap of $1 billion to encourage

6/26/2012. Data Requirements for Rate Filings SERFF Requirements Data Required by Federal Regulations. Rate Review in the Exchange

HEALTH INSURANCE RATE REVIEW AND REGULATORY ISSUES Jan Graeber, ASA, MAAA Director and Chief Actuary Rate and Form Review Office Texas Department of Insurance 1 Actuaries Club of the Southwest Spring 2012

HEALTH INSURANCE RATE REVIEW AND REGULATORY ISSUES Jan Graeber, ASA, MAAA Director and Chief Actuary Rate and Form Review Office Texas Department of Insurance 1 Actuaries Club of the Southwest Spring 2012

How To Prepare A Health Care Plan For A Job Interview

Health Care Reform 2013 & 2014 Planning Employers should review the fast-approaching 2013 and 2014 health care reform requirements. State Exchanges will be opening enrollment as soon as October 1, 2013

Health Care Reform 2013 & 2014 Planning Employers should review the fast-approaching 2013 and 2014 health care reform requirements. State Exchanges will be opening enrollment as soon as October 1, 2013

SHOP Exchange Technology Enablement Options. March 13, 2012

SHOP Exchange Technology Enablement Options March 13, 2012 Agenda 1. SHOP Overview 2. SHOP Principles 3. Design Options 4. Option Comparisons 5. Timeline and Recommendation - 1 - Overview: Small Business

SHOP Exchange Technology Enablement Options March 13, 2012 Agenda 1. SHOP Overview 2. SHOP Principles 3. Design Options 4. Option Comparisons 5. Timeline and Recommendation - 1 - Overview: Small Business

Q. My company already offers employee health coverage, how does the law impact me?

Frequently Asked Questions Q. Will my business be required to provide employee health insurance under the health care law? A. The law does not mandate employers provide employees health care coverage.

Frequently Asked Questions Q. Will my business be required to provide employee health insurance under the health care law? A. The law does not mandate employers provide employees health care coverage.

Understanding the Health Insurance Marketplace. August 2013

Understanding the Health Insurance Marketplace August 2013 Objectives This session will help you Explain the Health Insurance Marketplace Identify who will benefit Define who is eligible Explain the enrollment

Understanding the Health Insurance Marketplace August 2013 Objectives This session will help you Explain the Health Insurance Marketplace Identify who will benefit Define who is eligible Explain the enrollment

Important Effective Dates for Employers and Health Plans

Brought to you by Krempa Associates, Inc. Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into

Brought to you by Krempa Associates, Inc. Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into

The Future is Now Christine C. Rinn

Health Insurance Market Reforms Under PPACA: The Future is Now Christine C. Rinn Introduction PPACA created numerous market reforms affecting group health plans and health insurance issuers in the group

Health Insurance Market Reforms Under PPACA: The Future is Now Christine C. Rinn Introduction PPACA created numerous market reforms affecting group health plans and health insurance issuers in the group

Fact Sheet. AARP Public Policy Institute. Health Reform Changes Insurance Rules

Fact Sheet Health Reform Changes Insurance Rules The Affordable Care Act (ACA) will greatly increase the availability of health insurance and broadly impact the delivery of health care in America. This

Fact Sheet Health Reform Changes Insurance Rules The Affordable Care Act (ACA) will greatly increase the availability of health insurance and broadly impact the delivery of health care in America. This

PART 1: ENABLING AUTHORITY AND GOVERNANCE

Application for Approval of an American Health Benefit Exchange On March 23, 2010, the President signed into law the Patient Protection and Affordable Care Act (P.L. 111-148). On March 30, 2010, the Health

Application for Approval of an American Health Benefit Exchange On March 23, 2010, the President signed into law the Patient Protection and Affordable Care Act (P.L. 111-148). On March 30, 2010, the Health

American Health Benefit Exchange

American Health Benefit Exchange The Patient Protection and Affordable Care Act ( PPACA ) requires the creation of state-based health insurance exchanges for individuals and small businesses to purchase

American Health Benefit Exchange The Patient Protection and Affordable Care Act ( PPACA ) requires the creation of state-based health insurance exchanges for individuals and small businesses to purchase

National Health Insurance Reform

JANUARY2011 National Health Insurance Reform Impact Year by Year With the passage of National Health Insurance Reform it is crucial that employers and plan sponsors have clear information about the impact

JANUARY2011 National Health Insurance Reform Impact Year by Year With the passage of National Health Insurance Reform it is crucial that employers and plan sponsors have clear information about the impact

the Affordable Care Act: What Colorado Businesses Need to Know

22 About questions the Affordable Care Act: What Colorado Businesses Need to Know 1 What is the Affordable Care Act? Who is impacted (small, large businesses and self-insured)? The Patient Protection and

22 About questions the Affordable Care Act: What Colorado Businesses Need to Know 1 What is the Affordable Care Act? Who is impacted (small, large businesses and self-insured)? The Patient Protection and

Important Effective Dates for Employers and Health Plans

Brought to you by Hipskind Seyfarth Risk Solutions Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act

Brought to you by Hipskind Seyfarth Risk Solutions Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act

Douglas A. Conrad, PhD, Professor of Health Services University of Washington Member: Washington Health Benefits Exchange Board Presentation for:

Douglas A. Conrad, PhD, Professor of Health Services University of Washington Member: Washington Health Benefits Exchange Board Presentation for: Washington Policy Center Conference: July 10, 2012 1 This

Douglas A. Conrad, PhD, Professor of Health Services University of Washington Member: Washington Health Benefits Exchange Board Presentation for: Washington Policy Center Conference: July 10, 2012 1 This

Summary of 2010 Health Care Reform Legislation: AT A GLANCE

April 19, 2010 Summary of 2010 Health Care Reform Legislation: The Patient Protection and Affordable Care Act (H.R. 3590) and Health Care and Education Reconciliation Act (H.R. 4872) AT A GLANCE On March

April 19, 2010 Summary of 2010 Health Care Reform Legislation: The Patient Protection and Affordable Care Act (H.R. 3590) and Health Care and Education Reconciliation Act (H.R. 4872) AT A GLANCE On March

Consumer Operated and Oriented Plan (CO OP) Advisory Board

Advisory Board") Consumer Operated and Oriented Plan (CO OP) Advisory Board Summary: Requires the Secretary to award loans for start up costs and grants to meet solvency requirements, until July 1, 2013, to member run

Consumer Operated and Oriented Plan (CO OP) Advisory Board Summary: Requires the Secretary to award loans for start up costs and grants to meet solvency requirements, until July 1, 2013, to member run

The following capture key take-away points from the meeting:

July 2011 Changes in Health Care Financing & Organization issue brief Considerations Related to Pricing Individual and Small Group Health Insurance under Health Reform Changes in Health Care Financing

July 2011 Changes in Health Care Financing & Organization issue brief Considerations Related to Pricing Individual and Small Group Health Insurance under Health Reform Changes in Health Care Financing

A Comparative Analysis of Private Health Insurance Provisions of H.R. 3962 and Senate-Passed H.R. 3590

A Comparative Analysis of Private Health Insurance Provisions of H.R. 3962 and Senate-Passed H.R. 3590 Chris L. Peterson, Coordinator Specialist in Health Care Financing Hinda Chaikind Specialist in Health

A Comparative Analysis of Private Health Insurance Provisions of H.R. 3962 and Senate-Passed H.R. 3590 Chris L. Peterson, Coordinator Specialist in Health Care Financing Hinda Chaikind Specialist in Health

Health Care Reform Overview

Health Care Reform Overview By Marcia S. Wagner The Wagner Law Group 99 Summer Street, 13th Floor Boston, MA 02110 www.erisa-lawyers.com Introduction President Obama signed the Patient Protection and Affordable

Health Care Reform Overview By Marcia S. Wagner The Wagner Law Group 99 Summer Street, 13th Floor Boston, MA 02110 www.erisa-lawyers.com Introduction President Obama signed the Patient Protection and Affordable

Health Insurance Exchange

Health Insurance Exchange Lynn A. Blewett, Ph.D. Professor, Division of Health Policy and Management, University of Minnesota School of Public Health Director, State Health Access Data Assistance Center

Health Insurance Exchange Lynn A. Blewett, Ph.D. Professor, Division of Health Policy and Management, University of Minnesota School of Public Health Director, State Health Access Data Assistance Center

Summary of HBE activities to date A discussion of issues facing large employers as a result of the federal and state legislation

A Review of Washington s Health Insurance Exchange and Issues Facing Large Employers Employee Benefits Planning Association Education Program April 5, 2012 Presented by: Melanie K. Curtice Stoel Rives

A Review of Washington s Health Insurance Exchange and Issues Facing Large Employers Employee Benefits Planning Association Education Program April 5, 2012 Presented by: Melanie K. Curtice Stoel Rives

New York Health Benefit Exchange & Small Business Health Options Program (SHOP) Frequently Asked Questions for Agents and Brokers

Frequently Asked Questions for Agents and Brokers") New York Health Benefit Exchange & Small Business Health Options Program (SHOP) Frequently Asked Questions for Agents and Brokers May 9, 2013 Carrier Participation in the Exchange 1. Q: What carriers have

New York Health Benefit Exchange & Small Business Health Options Program (SHOP) Frequently Asked Questions for Agents and Brokers May 9, 2013 Carrier Participation in the Exchange 1. Q: What carriers have

Presented by South Dakota Community Action Partnership

Presented by South Dakota Community Action Partnership The project described was supported by Funding Opportunity Number CA-NAV-13-001 from the U.S Department of Health and Human Services, Centers for

Presented by South Dakota Community Action Partnership The project described was supported by Funding Opportunity Number CA-NAV-13-001 from the U.S Department of Health and Human Services, Centers for