CHAPTER 6 CREDITS AND SPECIAL TAXES

|

|

|

- Peregrine Pierce

- 8 years ago

- Views:

Transcription

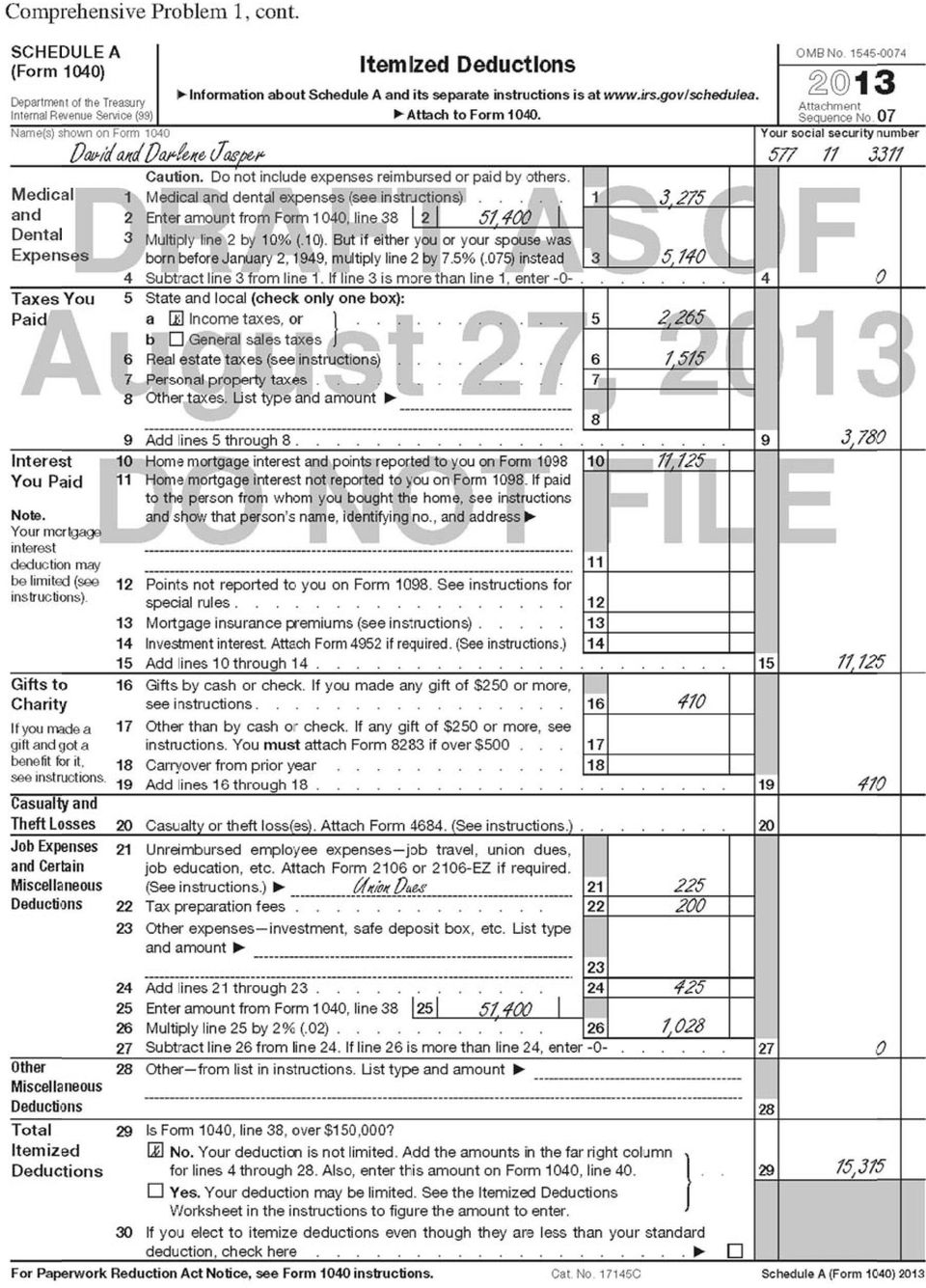

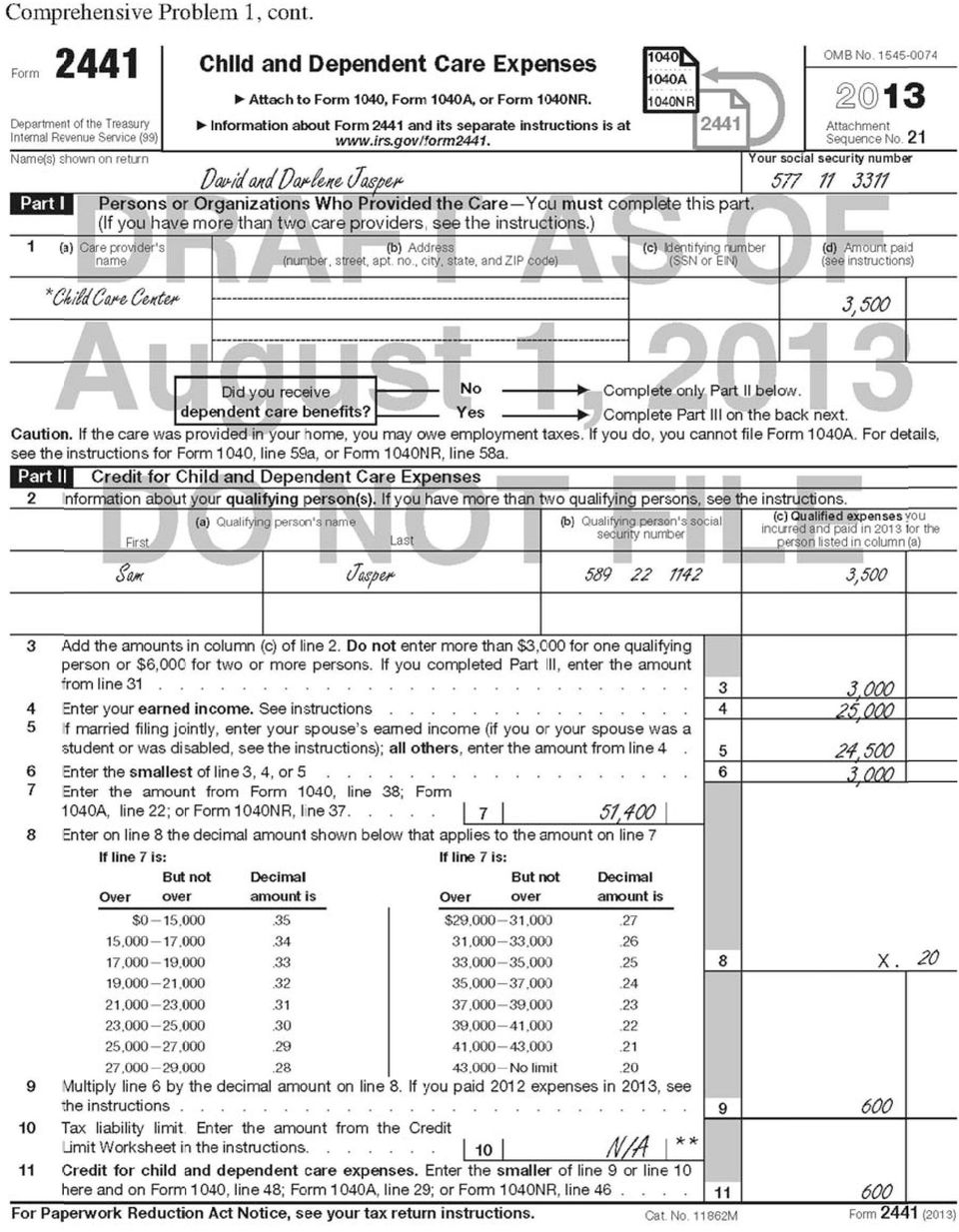

1 119 Group 1 - Multiple Choice Questions CHAPTER 6 CREDITS AND SPECIAL TAXES 1. D (LO 6.1) 11. C (LO 6.4) 2. C (LO 6.1) 12. C Limited to ($100,000 / 300, C (LO 6.2) x $90,000) (LO 6.5) 4. D (LO 6.3) 13. B (LO 6.6) 5. C (LO 6.4) 14. A (LO 6.6) 6. B (LO 6.4) 15. C (LO 6.6) 7. E $440 (LO 6.4) 16. D (LO 6.6) 8. A (LO 6.4) 17. E (LO 6.8) 9. C (LO 6.4) 18. E $35,000 each (LO 6.10) 10. D (LO 6.4) 19. B (LO 6.10) Group 2 - Problems 1. a. $750. $79,600 $75,000 = $4,600 $1,000 = 4.6, which is rounded up to 5; 5 x $50 = $250 of $1,000 child credit is phased out due to AGI limits. b. $2,000. The income is less than the phase-out range for married taxpayers, so two child credits are allowed at $1,000 each. c. $1,450. $120,400 $110,000 = $10,400 $1,000 = 10.4, which is rounded up to 11; 11 x $50 = $550 of the $2,000 child credit is phased out due to AGI limits. $2,000 $550 = $1,450 (LO 6.1) 2. The earned income credit is designed to provide financial relief to low-income taxpayers. Taxpayers may receive a refund for the credit even though the credit exceeds their tax liability. (LO 6.2) 3. Earned income credit: Amount from Earned Income Credit Table for earned income of $17,100 = $5,372 Amount from Earned Income Credit Table for AGI of $17,800 = 5,310 Lesser of two amounts $5,310 Diane must compute the credit using both earned income and AGI because her AGI exceeds the threshhold amount of $17,530. (LO 6.2) 4. Earned income credit: $5,372 See Schedule EIC on page 125. (LO 6.2) 5. A taxpayer may have a maximum of $3,300 of investment income in 2013 and still claim the earned income credit. The likely reason for the investment income limit is that the government intends the earned income credit to give a helping hand to the working poor. If a low-income worker has investment income over $3,300 they have savings that indicate to the government that the taxpayer may not need a helping hand as badly as other taxpayers. (LO 6.2) 6. a. $653 = $2,250 (student income limitation $250 x 9 months) x 29%. b. $1,260 = $6,000 (qualified expense limitation) x 21%. c. $1,800 = $6,000 x 30%. (LO 6.3) 7. Qualified expenses $3,000 For two dependents, lesser of $6,000 maximum or actual $3,000 Credit percentage from table 33% Credit allowed $ 990 (LO 6.3)

2 8. See the answer to Problem 7. The purpose of this problem is to familiarize the students with the interactive documents available on the IRS website. As of the date of this book, the forms do not do calculations, so students should be told to have a calculator handy. (LO 6.3) 9. None. The credit is intended to help taxpayers who work at income-earning jobs. Therefore, since John does not earn income (though many would argue that he has a very difficult job caring for two young children and deserves a respite), no credit is allowed. (LO 6.3) 10. $ % of $3,000 (LO 6.3) 11. $900. Jean gets credit for $500 a month of earned income while she attends school for 9 months, or $4,500 of earned income for the year. Therefore, the maximum qualifying expenses for their dependents are limited to $4,500. The credit is calculated as $4,500 (which is less than the $6,000 maximum costs allowed for two children, and less than the $10,000 actually paid) x 20% = $900. (LO 6.3) 12. The American Opportunity credit and lifetime learning credit are in the tax law to give assistance to low and middle-income students and/or their parents in paying for education. As discussed in Chapter 1, the tax law is used to encourage certain activities, and a well-educated, skilled and competitive workforce is obviously the goal of these education tax credits. Congress hopes to encourage students in pursuing college and ongoing lifetime education. (LO 6.4) 13. The American Opportunity credit covers only the first 4 years of post-secondary education with at least a half-time course load, so it encourages students to continue their education after high school. The lifetime learning credit may be claimed for any year of college or graduate school, and may also be claimed for educational courses taken during any stage of life, so it encourages lifelong ongoing education. The education is not required to be at the more than half-time level so it includes students who take a class occasionally. (LO 6.4) 14. a. $1,250. Janie s American Opportunity credit before any phase-out, will be 100% of the first $2,000 plus 25% of the next $2,000, or $2,500. Because her parents have AGI over $160,000 the credit is phased out partially: the credit is reduced by the following amount $2,500 x ($170,000 $160,000) / $20,000 = $1,250. Therefore, the credit is $2,500 $1,250 = $1,250. b. $2,500. Janie s parents have AGI below the phase-out range so they qualify for the full American Opportunity credit. (LO 6.4) 15. a. $0. Jasper s income is too high to qualify for the lifetime learning credit. The ceiling for claiming any part of the credit for single taxpayers is $63,000. If Jasper were married and supporting a nonworking wife, however, he would qualify for the full credit since the credit begins to phase-out for married taxpayers at $107,000. If he were married, his credit would be $400, or 20% of $2,000. b. Jasper qualifies for the full credit of $400, or 20% of $2,000. (LO 6.4) 16. Martha and Lew should claim the credit. If they deduct the taxes, they will have a $100 tax benefit ($400 deduction at a 25% tax rate). If they claim the $400 credit, they will have a full $400 tax benefit. (LO 6.5)

, no credit is allowed. (LO 6.3) 10. $600.")

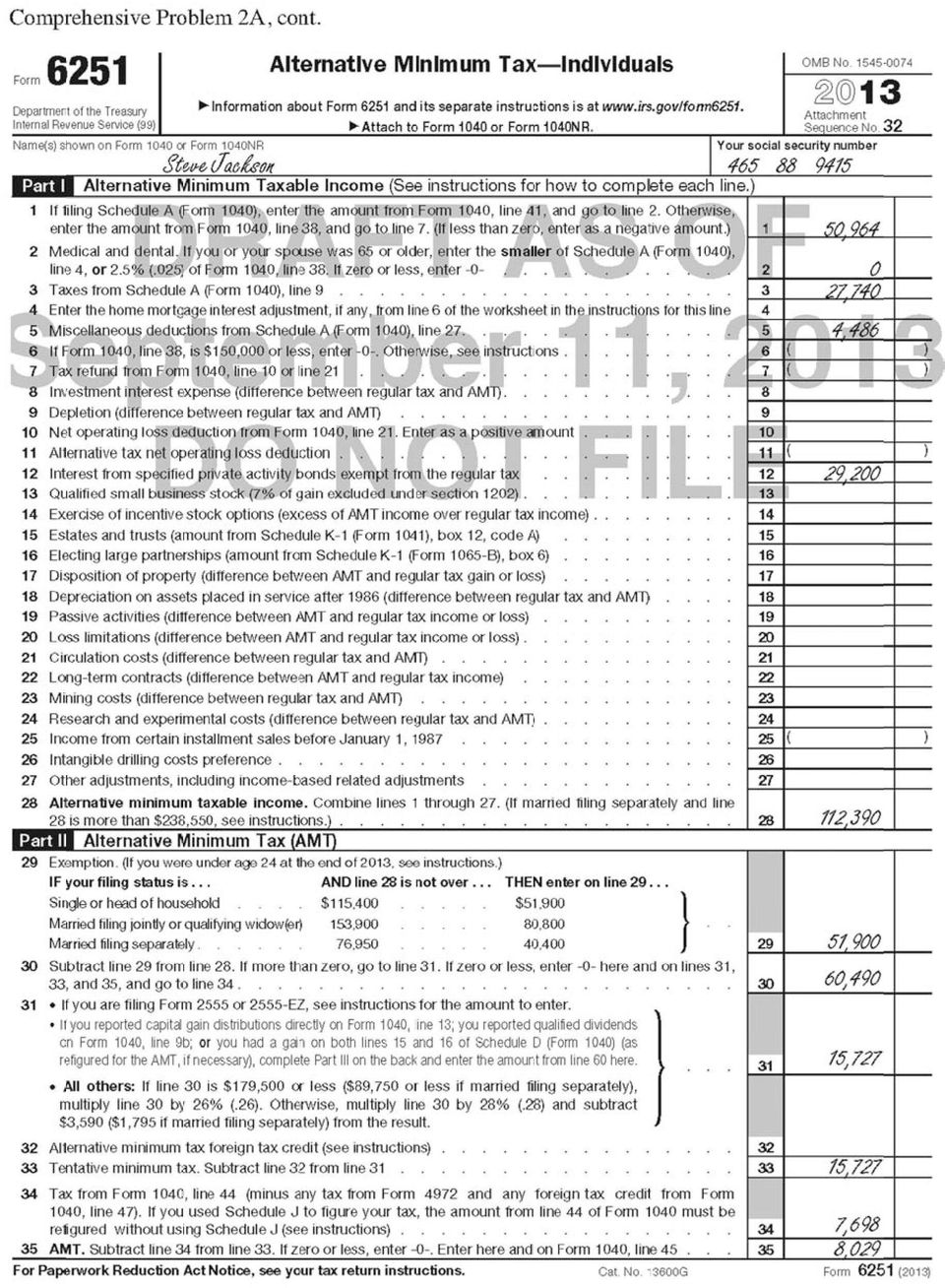

3 17. a. $12,970. They may claim the maximum credit of $12,970 in 2013 since that is the year the adoption was finalized and their qualified adoption expenses exceed the amount of the credit. b. $0. If the adoption is never finalized, no credit is allowed, since it is a foreign adoption. c. $11,050. Carl and Jenny have income in the phase-out range for the adoption credit. The phase-out is calculated as follows: ($200,500 $194,580) / $40,000 x $12,970 = $1,920. Only $11,050 of the credit is allowed ($12,970 $1,920). (LO 6.6) 18. Mike s credit would be $0. No credit is allowed if the property is used to heat a swimming pool or spa. (LO 6.7) 19. Jeff s credit is $1,800. ($6,000 x 30%) (LO 6.7) 20. AMTI = $115,300. ($80,300 $25,000 $7,500 + $67,500) (LO 6.8) 21. Some of the most common deductions allowed for regular tax and not for AMT are: The standard deduction Personal and dependency exemptions State income taxes, property taxes, and all other taxes deducted on Schedule A Miscellaneous itemized deductions taken on Schedule A The interest deduction for up to $100,000 of home equity debt which is not used to purchase or improve part of a principal residence (LO 6.8) 22. In computing the AMT, deductions for personal and dependency exemptions are not allowed, and state income taxes and real estate property taxes are also not allowed. The elimination of these two kinds of deductions when calculating AMT may be enough to cause a taxpayer to pay AMT instead of the regular income tax. (LO 6.8) 23. Because of the reduction in regular tax rates in recent years that has not been matched by a reduction in AMT tax rates, many more taxpayers are now paying AMT than in the past. Most of these taxpayers are not the people the AMT originally targeted, as they do not have complex tax shelters designed to reduce their taxable income. Instead, normal deductions such as personal and dependency exemptions, state income and property taxes and miscellaneous deductions are causing taxpayers to pay AMT. (LO 6.8) % and 28% (LO 6.8) 25. Regular taxable income (before exemptions and standard deductions) + Plus or minus AMT tax preferences and adjustments = Equals alternative minimum taxable income (AMTI) Less AMT exemption (phased out to zero as AMTI increases) = Equals amount subject to AMT x Multiplied by the AMT tax rate(s) = Equals tentative minimum tax Less regular tax = Equals amount of AMT due with tax return, if it is a positive amount (LO 6.8)

19. Jeff s credit is $1,800. ($6,000 x 30%) (LO 6.7) 20. AMTI = $115,300.")

4 26. The provision is designed to prevent taxpayers from transferring income-earning assets to a minor child in order to take advantage of the child s lower tax rate. Assuming the child has a relatively small amount of taxable income, the child s tax rate will be lower due to the progressive tax rate structure. (LO 6.9) 27. a. $2,500 = $4,500 $1,000 (greater of standard deduction of $1,000 or investment expenses of $250) $1,000. b. $375 = $7,286 (tax on the sum of $52,000 + $2,500) $6,911 (tax on $52,000 only) c. $475 = $375 + $100 (tax at an assumed rate of 10 percent on regular taxable income of $1,000). Regular taxable income is $1,000 ($4,500 $1,000 (standard deduction) $2,500 (net unearned income)). (LO 6.9) 28. a. $1,440 = $6,000 / $10,000 x $2,400. b. $960 = $4,000 / $10,000 x $2,400. (LO 6.9) 29. The kiddie tax may be computed on Form 8615, which shows the income of the parents and provides a calculation of the child s tax at the parents tax rates. This form is attached to the child s separate tax return. Alternatively, parents may elect to include the child s income with their own return. To make this election, the child s unearned income must be more than $1,000 and less than $10,000 and consist only of interest and dividends. In this case, the parents must attach Form 8814 to their tax return showing the child s income that is taxed in their tax return. (The basic answer is that either the child or the parent may report the unearned income and pay the tax.) (LO 6.9) 30. No, the kiddie tax does not apply to wages earned by minors. The purpose of the tax is only to prevent investment income shifting from the generally higher tax rates of parents to the lower rates of the child. Wages earned by minors are taxed at the child s separate low income tax rates. (LO 6.9) 31. Publication 555, Community Property, is the source the student should find. (LO 6.10) 32. a. Paul Cindy Paul s salary (50% each) $22,500 $22,500 Dividends on Paul s stock 4,000 0 Cindy s salary (50% each) 13,500 13,500 Interest income (50% each) Total income $40,750 $36,750 b. Paul Cindy Paul s salary (50% each) $22,500 $22,500 Dividends on Paul s stock (50% each) 2,000 2,000 Cindy s salary (50% each) 13,500 13,500 Interest income (50% each) Total income $38,750 $38,750 (LO 6.10) Group 3 - Writing Assignment Research Solution: Whittenburg, Gill, and Altus-Buller, CPAs San Diego, CA March 22, 20xx

$2,500 (net unearned income)). (LO 6.9) 28. a. $1,440 = $6,000 / $10,000 x $2,400. b. $960 = $4,000 / $10,000 x $2,400. (LO 6.9) 29.")

5 Relevant Facts Scott and Heather Moore are married and file a joint return. The Moores have one daughter, Elizabeth, age 8. Scott is a wildlife biologist, earning $36,000, and Heather is a full-time student at Online University. Online University offers courses only through the Internet. Scott and Heather pay $3,000 for child care expenses during the year. Specific Issues How much of the child care expenses paid can be claimed as a child and dependent care credit? Conclusions Mr. and Mrs. Moore are not allowed to claim a child and dependent care credit for the child care expenses paid. Support A child and dependent care credit is allowed for married taxpayers who file a joint return. The qualifying dependent care expenses are limited to the lesser of either spouse s earned income. In the case of taxpayers who are students, earned income of $250 per month (for one dependent) is deemed to be income of the taxpayer, provided the taxpayer is a full-time student enrolled at school. This would generally apply to Heather, however, IRS Publication 503, Child and Dependent Care Expenses, specifically states that a school which only offers courses through the Internet does not qualify. Since Heather does not meet the qualifications of a full-time student, she is treated as having no earned income. The Moore s dependent care expenses would be limited to the lesser of $3,000 or $0. Actions to Be Taken Review results with client. Preparer: Trevor Malcolm Reviewer: Martha Altus-Buller Group 4 - Comprehensive Problems 1. See Forms on pages 127 through A. See Forms on pages 133 through B. See Forms on pages 138 through 142.

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

Unit12. Special Tax Computation Methods, Tax Credits, and Payment of Tax [Pak Ch. 14]

![Unit12. Special Tax Computation Methods, Tax Credits, and Payment of Tax [Pak Ch. 14]](/thumbs/26/9340123.jpg "Unit12. Special Tax Computation Methods, Tax Credits, and Payment of Tax [Pak Ch. 14]") 1 Unit12. Special Tax Computation Methods, Tax Credits, and Payment of Tax [Pak Ch. 14] This chapter covers several topics: the Alternative Minimum Tax, Tax Credits, and Tax Payments. Outline 2 1. Alternative

1 Unit12. Special Tax Computation Methods, Tax Credits, and Payment of Tax [Pak Ch. 14] This chapter covers several topics: the Alternative Minimum Tax, Tax Credits, and Tax Payments. Outline 2 1. Alternative

Education Tax Benefits Presented by: Michael S. McDonough, CPA, MST February 7, 2014

Education Tax Benefits Presented by: Michael S. McDonough, CPA, MST February 7, 2014 2013. American Student Assistance. All rights reserved. Disclaimer This presentation is for educational and informational

Education Tax Benefits Presented by: Michael S. McDonough, CPA, MST February 7, 2014 2013. American Student Assistance. All rights reserved. Disclaimer This presentation is for educational and informational

2011 Tax And Financial Planning Tables

2011 Tax and Financial PLanning Tables Investment Planning 2011 Tax And Financial Planning Tables Tax planning is an important component for your overall financial plan. 2011 Tax and Financial PLanning

2011 Tax and Financial PLanning Tables Investment Planning 2011 Tax And Financial Planning Tables Tax planning is an important component for your overall financial plan. 2011 Tax and Financial PLanning

2015 vs. 2016 Key Facts and Figures Note: We highlighted the information that changed between 2015 and 2016 with a box.

2015 vs. 2016 Key Facts and Figures Note: We highlighted the information that changed between 2015 and 2016 with a box. 2016 Keir Educational Resources Key Facts-1 800-795-5347 Personal Exemption 2015

2015 vs. 2016 Key Facts and Figures Note: We highlighted the information that changed between 2015 and 2016 with a box. 2016 Keir Educational Resources Key Facts-1 800-795-5347 Personal Exemption 2015

2014 TAX AND FINANCIAL PLANNING TABLES. An overview of important changes, rates, rules and deadlines to assist your 2014 tax planning.

2014 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2014 tax planning. 2014 2014 TAX TAX AND AND FINANCIAL FINANCIAL PLANNING PLANNING TABLES

2014 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2014 tax planning. 2014 2014 TAX TAX AND AND FINANCIAL FINANCIAL PLANNING PLANNING TABLES

News Release Date: 1/8/13

News Release Date: 1/8/13 American Taxpayer Relief Act of 2012 Cross References H.R. 8, the American Taxpayer Relief Act of 2012 TheTaxBook, 2012 Tax Year, 1040 Edition/Deluxe Edition, pages 1-6 and 1-7.

News Release Date: 1/8/13 American Taxpayer Relief Act of 2012 Cross References H.R. 8, the American Taxpayer Relief Act of 2012 TheTaxBook, 2012 Tax Year, 1040 Edition/Deluxe Edition, pages 1-6 and 1-7.

Small Business Health Care Tax Credit: Frequently Asked Questions

Small Business Health Care Tax Credit: Frequently Asked Questions The new health reform law gives a tax credit to certain small employers that provide health care coverage to their employees, effective

Small Business Health Care Tax Credit: Frequently Asked Questions The new health reform law gives a tax credit to certain small employers that provide health care coverage to their employees, effective

2014 tax planning tables

2014 tax planning tables 2014 important deadlines Last day to January 15 Pay fourth-quarter 2013 federal individual estimated income tax January 27 Buy in to close a short-against-the-box position (regular-way

2014 tax planning tables 2014 important deadlines Last day to January 15 Pay fourth-quarter 2013 federal individual estimated income tax January 27 Buy in to close a short-against-the-box position (regular-way

What s New for the 2009 Income Tax Return and the 2010 Tax Year

LAW OFFICES OF BLOOM, BLOOM & ASSOCIATES, P.C. 31275 NORTHWESTERN HIGHWAY SUITE 145 FARMINGTON HILLS, MI 48334-2531 (248) 932-5200 WWW.BLOOMLAWFIRM.COM E-MAIL INFO@BLOOMLAWFIRM.COM KENNETH J. BLOOM*+ FACSIMILE

LAW OFFICES OF BLOOM, BLOOM & ASSOCIATES, P.C. 31275 NORTHWESTERN HIGHWAY SUITE 145 FARMINGTON HILLS, MI 48334-2531 (248) 932-5200 WWW.BLOOMLAWFIRM.COM E-MAIL INFO@BLOOMLAWFIRM.COM KENNETH J. BLOOM*+ FACSIMILE

2013 TAX PLANNING TIPS FOR INDIVIDUALS

2013 TAX PLANNING TIPS FOR INDIVIDUALS The 2012 American Taxpayer Relief Act, which was enacted in early January 2013, was a sweeping tax package that included permanent extension of the Bush-era tax cuts

2013 TAX PLANNING TIPS FOR INDIVIDUALS The 2012 American Taxpayer Relief Act, which was enacted in early January 2013, was a sweeping tax package that included permanent extension of the Bush-era tax cuts

Income, Gift, and Estate Tax Update

Income, Gift, and Estate Tax Update Individual Income Tax Rates p. 1 Phil Harris Department of Agricultural and Applied Economics University of Wisconsin-Madison Marriage Penalty Relief p. 1 Capital Gains

Income, Gift, and Estate Tax Update Individual Income Tax Rates p. 1 Phil Harris Department of Agricultural and Applied Economics University of Wisconsin-Madison Marriage Penalty Relief p. 1 Capital Gains

2016 Tax Planning & Reference Guide

2016 Tax Planning & Reference Guide The 2016 Tax Planning & Reference Guide is designed as a reference and is not intended to function as tax advice. Please consult your professional accounting advisor

2016 Tax Planning & Reference Guide The 2016 Tax Planning & Reference Guide is designed as a reference and is not intended to function as tax advice. Please consult your professional accounting advisor

2015 -- S 0163 S T A T E O F R H O D E I S L A N D

======== LC000 ======== 01 -- S 01 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 A N A C T RELATING TO TAXATION - PERSONAL INCOME TAX Introduced By: Senators Goldin,

======== LC000 ======== 01 -- S 01 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 A N A C T RELATING TO TAXATION - PERSONAL INCOME TAX Introduced By: Senators Goldin,

HIGHLIGHTS OF 2007 TAX LAW CHANGES SMALL BUSINESS AND WORK OPPORTUNITY TAX ACT OF 2007

American Tax Abroad Chemin du Canal 5 1260 Nyon Switzerland Phone: +41 22 363 91 48 Fax: +41 22 363 91 49 Mobile: +41 79 599 60 11 info@americantaxabroad.com www.americantaxabroad.com HIGHLIGHTS OF 2007

American Tax Abroad Chemin du Canal 5 1260 Nyon Switzerland Phone: +41 22 363 91 48 Fax: +41 22 363 91 49 Mobile: +41 79 599 60 11 info@americantaxabroad.com www.americantaxabroad.com HIGHLIGHTS OF 2007

Completing and Filing Schedule O

Department of the Treasury Instructions for Schedule O Internal Revenue Service (Form 1120) (Rev. December 2012) Consent Plan and Apportionment Schedule for a Controlled Group Section references are to

Department of the Treasury Instructions for Schedule O Internal Revenue Service (Form 1120) (Rev. December 2012) Consent Plan and Apportionment Schedule for a Controlled Group Section references are to

How To Calculate Tax In The United States

TAXATION OF U.S. EXPATRIATES gtn.com C O N T E N T S 1. Introduction 1 2. Case Study Facts 2 3. U.S. Income Taxation Overview 4 Federal Income Tax Calculation 5 Foreign Earned Income and Housing Exclusions

TAXATION OF U.S. EXPATRIATES gtn.com C O N T E N T S 1. Introduction 1 2. Case Study Facts 2 3. U.S. Income Taxation Overview 4 Federal Income Tax Calculation 5 Foreign Earned Income and Housing Exclusions

How To Get A Health Insurance Tax Credit

Small Business Health Care Tax Credit: Frequently Asked Questions The new health reform law gives a tax credit to certain small employers that provide health care coverage to their employees, effective

Small Business Health Care Tax Credit: Frequently Asked Questions The new health reform law gives a tax credit to certain small employers that provide health care coverage to their employees, effective

Small Employer Health Care Tax Credit: Questions & Answers (Q&A)

") Brought to you by Seubert & Associates Small Employer Health Care Tax Credit: Questions & Answers (Q&A) The Patient Protection and Affordable Care Act (ACA) provides a tax credit to certain small employers

Brought to you by Seubert & Associates Small Employer Health Care Tax Credit: Questions & Answers (Q&A) The Patient Protection and Affordable Care Act (ACA) provides a tax credit to certain small employers

2014 Individual Income Tax Changes. Individual Income Tax Law changes effective for tax years beginning on or after January 1, 2014

2014 Individual Income Tax Changes Individual Income Tax Law changes effective for tax years beginning on or after January 1, 2014 Revised 10/15/2014 The NC Department of Revenue provides this information

2014 Individual Income Tax Changes Individual Income Tax Law changes effective for tax years beginning on or after January 1, 2014 Revised 10/15/2014 The NC Department of Revenue provides this information

Crunch or Crucible? Upcoming Changes in the Federal Tax Law A Special Edition Tax Guide for Friends and Alumni of Pomona College

Upcoming Changes in the Federal Tax Law A Special Edition Tax Guide for Friends and Alumni of Pomona College Pomona College, Office of Trusts & Estates, 550 N. College Ave., Claremont, CA 91711 www.pomona.planyourlegacy.org

Upcoming Changes in the Federal Tax Law A Special Edition Tax Guide for Friends and Alumni of Pomona College Pomona College, Office of Trusts & Estates, 550 N. College Ave., Claremont, CA 91711 www.pomona.planyourlegacy.org

The Need for Life Insurance

Page 1 of 5 From Jared Adams Condie & Adams, PLLC 603 4th Avenue, Suite 200 Kirkland, WA 98033 4254501040 Volume 2, Issue 2 Planning for the New "Zero Percent" Tax Bracket The Need for Life Insurance Condie

Page 1 of 5 From Jared Adams Condie & Adams, PLLC 603 4th Avenue, Suite 200 Kirkland, WA 98033 4254501040 Volume 2, Issue 2 Planning for the New "Zero Percent" Tax Bracket The Need for Life Insurance Condie

TAX LETTER for May 2004 INCOME ATTRIBUTION RULES SPLIT INCOME OF MINOR CHILDREN FEDERAL BUDGET HIGHLIGHTS AROUND THE COURTS

BLAIN M. ARCHER, B.Sc., CA* PAUL M. FOURNIER, B.Sc., CA* RUSS J. WILSON, B.Sc., CA* KATRIN BRAUN, B.B.A., CA* KELLY A. RIEHL, B. Comm., CA* TAX LETTER for May 2004 INCOME ATTRIBUTION RULES SPLIT INCOME

BLAIN M. ARCHER, B.Sc., CA* PAUL M. FOURNIER, B.Sc., CA* RUSS J. WILSON, B.Sc., CA* KATRIN BRAUN, B.B.A., CA* KELLY A. RIEHL, B. Comm., CA* TAX LETTER for May 2004 INCOME ATTRIBUTION RULES SPLIT INCOME

SPECIAL REPORT: PROJECTED 2016 INFLATION-ADJUSTED TAX BRACKETS AND OTHER KEY FIGURES

SPECIAL REPORT: PROJECTED 2016 INFLATION-ADJUSTED TAX BRACKETS AND OTHER KEY FIGURES TABLE OF CONTENTS Tax rate schedules 3 Standard deductions 5 Kiddie tax 5 Personal exemption 5 Phase-out of personal

SPECIAL REPORT: PROJECTED 2016 INFLATION-ADJUSTED TAX BRACKETS AND OTHER KEY FIGURES TABLE OF CONTENTS Tax rate schedules 3 Standard deductions 5 Kiddie tax 5 Personal exemption 5 Phase-out of personal

Tax Facts Quick Reference 2012

Wealth Management Services Tax Facts Quick Reference 2012 Income Investment Estate Retirement Social Security FOR USE BY FINANCIAL ADVISORS AND CLIENTS IN CONSULTATION WITH THEIR FINANCIAL ADVISOR FOR

Wealth Management Services Tax Facts Quick Reference 2012 Income Investment Estate Retirement Social Security FOR USE BY FINANCIAL ADVISORS AND CLIENTS IN CONSULTATION WITH THEIR FINANCIAL ADVISOR FOR

Tax Planning Circa 2011. The Rules We Live By

Tax Planning Circa 2011 FPA Houston December 6, 2011 The Rules We Live By 2010 Tax Relief Act (December 17, 2010) Patient Protection and Affordable Care Act (PPACA) Hiring Incentives to Restore Employment

Tax Planning Circa 2011 FPA Houston December 6, 2011 The Rules We Live By 2010 Tax Relief Act (December 17, 2010) Patient Protection and Affordable Care Act (PPACA) Hiring Incentives to Restore Employment

BACKGROUND AND PRESENT LAW RELATED TO TAX BENEFITS FOR EDUCATION

BACKGROUND AND PRESENT LAW RELATED TO TAX BENEFITS FOR EDUCATION Scheduled for a Public Hearing Before the SENATE COMMITTEE ON FINANCE on June 24, 2014 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION

BACKGROUND AND PRESENT LAW RELATED TO TAX BENEFITS FOR EDUCATION Scheduled for a Public Hearing Before the SENATE COMMITTEE ON FINANCE on June 24, 2014 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION

APPENDIX G: PROVIDED TAX TABLES

APPENDIX G: PROVIDED TAX TABLES The tax tables and limits below are provided to individuals taking the July 2016 CFP Certification Examination. Exam Window Tax Rates, Tables, & Law Tested July 2016 2016

APPENDIX G: PROVIDED TAX TABLES The tax tables and limits below are provided to individuals taking the July 2016 CFP Certification Examination. Exam Window Tax Rates, Tables, & Law Tested July 2016 2016

VETERANS' EDUCATION BENEFITS

GAO United States General Accounting Office Report to the Ranking Minority Member, Committee on Veterans Affairs, U.S. Senate February 2002 VETERANS' EDUCATION BENEFITS Comparison of Federal Assistance

GAO United States General Accounting Office Report to the Ranking Minority Member, Committee on Veterans Affairs, U.S. Senate February 2002 VETERANS' EDUCATION BENEFITS Comparison of Federal Assistance

Tax Planning for Form 1040

Steven I. Yeh Invest Financial Corp Anthony S. Scalise Financial Advisor SY Associates 1408 Sweet Home Road, Suite 6 Amherst, NY 14228 716-348-3425 steven.yeh@investfinancial.com Tax Planning for Form

Steven I. Yeh Invest Financial Corp Anthony S. Scalise Financial Advisor SY Associates 1408 Sweet Home Road, Suite 6 Amherst, NY 14228 716-348-3425 steven.yeh@investfinancial.com Tax Planning for Form

16. Individual Retirement Accounts

16. Individual Retirement Accounts Introduction Through enactment of the Employee Retirement Income Security Act of 1974 (ERISA), Congress established individual retirement accounts (IRAs) to provide workers

16. Individual Retirement Accounts Introduction Through enactment of the Employee Retirement Income Security Act of 1974 (ERISA), Congress established individual retirement accounts (IRAs) to provide workers

2013 YEAR-END INDIVIDUAL TAX PLANNING LETTER

Bollenback & Forret, P.A. Michael D. Bollenback, CPA Richard G. Buschart, CPA, ABV, CVA Suzanne E. Patrick, CPA Janet K. Rosenquist, CPA Roderick B. Stuart, CPA J. Patrick Callan, CPA Peter B. Forret,

Bollenback & Forret, P.A. Michael D. Bollenback, CPA Richard G. Buschart, CPA, ABV, CVA Suzanne E. Patrick, CPA Janet K. Rosenquist, CPA Roderick B. Stuart, CPA J. Patrick Callan, CPA Peter B. Forret,

PREPARE FOR AFFORDABLE CARE ACT NOW & AVOID PENALTIES!

PREPARE FOR AFFORDABLE CARE ACT NOW & AVOID PENALTIES! Ken Laks, Tax Specialist Eric Dielmann, Employee Benefit Specialist PRESENTED BY WHY WORRY? Employer Mandate has Been Postponed until 2015! Guaranteed

PREPARE FOR AFFORDABLE CARE ACT NOW & AVOID PENALTIES! Ken Laks, Tax Specialist Eric Dielmann, Employee Benefit Specialist PRESENTED BY WHY WORRY? Employer Mandate has Been Postponed until 2015! Guaranteed

Annual contributions: Conversion of a traditional IRA account: Rollovers from a qualified plan:

The Roth IRA differs from the traditional IRA in that contributions are never deductible and, if certain requirements are met, account distributions are free of federal income tax. 1 Annual contributions:

The Roth IRA differs from the traditional IRA in that contributions are never deductible and, if certain requirements are met, account distributions are free of federal income tax. 1 Annual contributions:

TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University. 2015 - Tax Planning

TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2015 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2015 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

529 Plan Distributions and Federal Tax Credits

529 Plan Distributions and Federal Tax Credits by Gregory Geisler, PhD, CPA Rebecca Bischoff, MAcc ABSTRACT A common misperception among some financial service professionals is that an individual with

529 Plan Distributions and Federal Tax Credits by Gregory Geisler, PhD, CPA Rebecca Bischoff, MAcc ABSTRACT A common misperception among some financial service professionals is that an individual with

MICHIGAN EARNED INCOME TAX CREDIT Tax Year 2013

MICHIGAN EARNED INCOME TAX CREDIT Office of Revenue and Tax Analysis Michigan Department of Treasury February 2015 MICHIGAN EARNED INCOME TAX CREDIT Office of Revenue and Tax Analysis Michigan Department

MICHIGAN EARNED INCOME TAX CREDIT Office of Revenue and Tax Analysis Michigan Department of Treasury February 2015 MICHIGAN EARNED INCOME TAX CREDIT Office of Revenue and Tax Analysis Michigan Department

Economic Stimulus Act of 2008

Economic Stimulus Act of 2008 H.R. 5140. Passed by both the House and Senate on February 7, 2008, the Economic Stimulus Act of 2008 provides rebates for individuals and incentives for business investment.

Economic Stimulus Act of 2008 H.R. 5140. Passed by both the House and Senate on February 7, 2008, the Economic Stimulus Act of 2008 provides rebates for individuals and incentives for business investment.

The American Tax Relief Act of 2012 (HR 8, the Act )

") NATIONAL CAPITAL GIFT PLANNING COUNCIL The Fiscal Cliff, Taxes and Planned Giving: Where Are We Now? Robert E. Madden Susan Leahy BLANK ROME LLP JANUARY 9, 2013 The American Tax Relief Act of 2012 (HR

NATIONAL CAPITAL GIFT PLANNING COUNCIL The Fiscal Cliff, Taxes and Planned Giving: Where Are We Now? Robert E. Madden Susan Leahy BLANK ROME LLP JANUARY 9, 2013 The American Tax Relief Act of 2012 (HR

Small Business Health Care Tax Credit

Small Business Health Care Tax Credit Small Business Health Tax Credit Began in 2010 Helps small businesses and tax-exempt organizations afford the cost of covering their employees Specifically targeted

Small Business Health Care Tax Credit Small Business Health Tax Credit Began in 2010 Helps small businesses and tax-exempt organizations afford the cost of covering their employees Specifically targeted

How To Get A Small Business Tax Credit

2010 FOCUS ON BUSINESS December 1, 2010 FEDERAL TAX UPDATE 2010 SMALL BUSINESS JOBS ACT & MISCELLANEOUS TAX PROVISIONS PRESENTED BY: DAVID P. VENISKEY, CPA TAX PARTNER EFP ROTENBERG, LLP TAX RATES Income

2010 FOCUS ON BUSINESS December 1, 2010 FEDERAL TAX UPDATE 2010 SMALL BUSINESS JOBS ACT & MISCELLANEOUS TAX PROVISIONS PRESENTED BY: DAVID P. VENISKEY, CPA TAX PARTNER EFP ROTENBERG, LLP TAX RATES Income

Present Law. The various provisions contain numerous and differing eligibility rules summarized in the accompanying table. Background and Analysis

American Institute of Certified Public Accountants Written Testimony for the Record Senate Finance Committee Hearing on Education Tax Incentives and Tax Reform July 25, 2012 The American Institute of Certified

American Institute of Certified Public Accountants Written Testimony for the Record Senate Finance Committee Hearing on Education Tax Incentives and Tax Reform July 25, 2012 The American Institute of Certified

An Overview of The Tax Relief Act on 2010

An Overview of The Tax Relief Act on 2010 On December 17, 2010, the President signed a multi-billion dollar tax cut package, the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act

An Overview of The Tax Relief Act on 2010 On December 17, 2010, the President signed a multi-billion dollar tax cut package, the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act

CALIFORNIA WITHHOLDING SCHEDULES FOR 2015

California provides two methods for determining the amount of wages and salaries to be withheld for state personal income tax: METHOD A - WAGE BRACKET TABLE METHOD (Limited to wages/salaries less than

California provides two methods for determining the amount of wages and salaries to be withheld for state personal income tax: METHOD A - WAGE BRACKET TABLE METHOD (Limited to wages/salaries less than

In the Know December 30, 2010

In the Know December 30, 2010 On December 17, 2010, President Obama signed the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 aka the 2010 Tax Relief Act. Below we break

In the Know December 30, 2010 On December 17, 2010, President Obama signed the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 aka the 2010 Tax Relief Act. Below we break

Tax-Savvy Planning for College Expenses

3/31/14 Tax-Savvy Planning for College Expenses The American Opportunity Tax Credit Remains Available through 2017 If you are a parent with hopes of future college diplomas for your children, you are likely

3/31/14 Tax-Savvy Planning for College Expenses The American Opportunity Tax Credit Remains Available through 2017 If you are a parent with hopes of future college diplomas for your children, you are likely

Small Business Health Care Tax Credit: Presented by Maureen O Gara-Adford, CPA & David Fox, Senior Accountant

Small Business Health Care Tax Credit: Presented by Maureen O Gara-Adford, CPA & David Fox, Senior Accountant Today s Speakers Maureen O Gara-Adford, CPA Practicing CPA since 1989 Managing partner since

Small Business Health Care Tax Credit: Presented by Maureen O Gara-Adford, CPA & David Fox, Senior Accountant Today s Speakers Maureen O Gara-Adford, CPA Practicing CPA since 1989 Managing partner since

DEDUCTING MBA EDUCATION COSTS

1 1. WHO MAY DEDUCT MBA EDUCATION COSTS? A typical MBA candidate can deduct education expenses if he or she currently operates a business, currently has a job with professional or managerial duties, or

1 1. WHO MAY DEDUCT MBA EDUCATION COSTS? A typical MBA candidate can deduct education expenses if he or she currently operates a business, currently has a job with professional or managerial duties, or

2015 Individual Tax Planning Letter

2015 Individual Tax Planning Letter Just as the daylight hours are getting shorter, so is the time for fine tuning any last-minute strategies to lower your 2015 tax bill. While year-end legislation extending

2015 Individual Tax Planning Letter Just as the daylight hours are getting shorter, so is the time for fine tuning any last-minute strategies to lower your 2015 tax bill. While year-end legislation extending

A PROFESSIONAL S GUIDE TO EDUCATION SAVINGS

CPAs Attorneys Enrolled Agents Tax Professionals A PROFESSIONAL S GUIDE TO EDUCATION SAVINGS www.edwardjones.com/teamwork Professional Education Network TM CONTENTS 1 Introduction 2 Saving versus Borrowing

CPAs Attorneys Enrolled Agents Tax Professionals A PROFESSIONAL S GUIDE TO EDUCATION SAVINGS www.edwardjones.com/teamwork Professional Education Network TM CONTENTS 1 Introduction 2 Saving versus Borrowing

2015 YEAR-END TAX PLANNING NEWSLETTER

2015 YEAR-END TAX PLANNING NEWSLETTER Dear Client: As the end of the year approaches, it is a good time to think of planning moves that will help lower your tax bill for this year and possibly the next.

2015 YEAR-END TAX PLANNING NEWSLETTER Dear Client: As the end of the year approaches, it is a good time to think of planning moves that will help lower your tax bill for this year and possibly the next.

BMO Funds State Street Bank and Trust Company Universal Individual Retirement Account Disclosure Statement. Part One: Description of Traditional IRAs

BMO Funds State Street Bank and Trust Company Universal Individual Retirement Account Disclosure Statement Part One: Description of Traditional IRAs Part One of the Disclosure Statement describes the rules

BMO Funds State Street Bank and Trust Company Universal Individual Retirement Account Disclosure Statement Part One: Description of Traditional IRAs Part One of the Disclosure Statement describes the rules

Roth IRAs. Funding a Roth IRA

The Roth IRA differs from the traditional IRA in that contributions are never deductible and, if certain requirements are met, account distributions are free of federal income tax. Funding a Roth IRA Annual

The Roth IRA differs from the traditional IRA in that contributions are never deductible and, if certain requirements are met, account distributions are free of federal income tax. Funding a Roth IRA Annual

H.R. 1836 CONGRESSIONAL BUDGET OFFICE PAY-AS-YOU-GO ESTIMATE. Economic Growth and Tax Relief Reconciliation Act of 2001.

CONGRESSIONAL BUDGET OFFICE PAY-AS-YOU-GO ESTIMATE June 4, 2001 H.R. 1836 Economic Growth and Tax Relief Reconciliation Act of 2001 As cleared by the Congress on May 26, 2001 SUMMARY The Economic Growth

CONGRESSIONAL BUDGET OFFICE PAY-AS-YOU-GO ESTIMATE June 4, 2001 H.R. 1836 Economic Growth and Tax Relief Reconciliation Act of 2001 As cleared by the Congress on May 26, 2001 SUMMARY The Economic Growth

Here is a quick summary of most-important tax changes starting with those that affect individuals. Payroll Tax Holiday Is Dead (So Far)

") Dear Clients: The American Taxpayer Relief Act of 2012 (better known as the fiscal cliff legislation) became law on 1/2/13. Due to the expiration of the so-called payroll tax holiday, all workers will

Dear Clients: The American Taxpayer Relief Act of 2012 (better known as the fiscal cliff legislation) became law on 1/2/13. Due to the expiration of the so-called payroll tax holiday, all workers will

United States General Accounting Office. Testimony Before the Committee on Finance, United States Senate

GAO United States General Accounting Office Testimony Before the Committee on Finance, United States Senate For Release on Delivery Expected at 10:00 a.m. EST on Thursday March 8, 2001 ALTERNATIVE MINIMUM

GAO United States General Accounting Office Testimony Before the Committee on Finance, United States Senate For Release on Delivery Expected at 10:00 a.m. EST on Thursday March 8, 2001 ALTERNATIVE MINIMUM

PATRICK J. RUBEY & COMPANY, LTD. CERTIFIED PUBLIC ACCOUNTANTS

PATRICK J. RUBEY & COMPANY, LTD. CERTIFIED PUBLIC ACCOUNTANTS American Taxpayer Relief Act January 1, 2013 Here are the act s main tax features: Individual tax rates All the individual marginal tax rates

PATRICK J. RUBEY & COMPANY, LTD. CERTIFIED PUBLIC ACCOUNTANTS American Taxpayer Relief Act January 1, 2013 Here are the act s main tax features: Individual tax rates All the individual marginal tax rates

Tax Credit for Small Employers

Employers Defined: Tax Credit Small employer definition for Tax Credit - number of full-time employees Fewer than 25 full-time employees with average wages of less than $50,000 Divide total hours for which

Employers Defined: Tax Credit Small employer definition for Tax Credit - number of full-time employees Fewer than 25 full-time employees with average wages of less than $50,000 Divide total hours for which

Instructions for Form 1045

2015 Instructions for Form 1045 Application for Tentative Refund Department of the Treasury Internal Revenue Service General Instructions Future developments. For the latest information about developments

2015 Instructions for Form 1045 Application for Tentative Refund Department of the Treasury Internal Revenue Service General Instructions Future developments. For the latest information about developments

Section 45R Tax Credit for Employee Health Insurance Expenses of Small Employers

Part III - Administrative, Procedural, and Miscellaneous Section 45R Tax Credit for Employee Health Insurance Expenses of Small Employers Notice 2010-44 I. PURPOSE AND BACKGROUND Section 45R of the Internal

Part III - Administrative, Procedural, and Miscellaneous Section 45R Tax Credit for Employee Health Insurance Expenses of Small Employers Notice 2010-44 I. PURPOSE AND BACKGROUND Section 45R of the Internal

Who Must Make Estimated Tax Payments

2014 Form Estimated Income Tax for Estates and Trusts Section references are to the Internal Revenue Code unless otherwise noted. Future Developments For the latest information about developments related

2014 Form Estimated Income Tax for Estates and Trusts Section references are to the Internal Revenue Code unless otherwise noted. Future Developments For the latest information about developments related

Instructions for Form 1045

2014 Instructions for Form 1045 Application for Tentative Refund Department of the Treasury Internal Revenue Service General Instructions Future developments. For the latest information about developments

2014 Instructions for Form 1045 Application for Tentative Refund Department of the Treasury Internal Revenue Service General Instructions Future developments. For the latest information about developments

Summary of Small Business Health Insurance Tax Credit Under PPACA (P.L. 111-148)

") Summary of Small Business Health Insurance Tax Credit Under PPACA (P.L. 111-148) Chris L. Peterson Hinda Chaikind April 20, 2010 Congressional Research Service CRS Report for Congress Prepared for Members

Summary of Small Business Health Insurance Tax Credit Under PPACA (P.L. 111-148) Chris L. Peterson Hinda Chaikind April 20, 2010 Congressional Research Service CRS Report for Congress Prepared for Members

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences

We will continue to expand on the provisions of the taxpayer relief act as more information becomes available. If you have any questions please feel free to contact us. Congress passes 2012 Taxpayer Relief

We will continue to expand on the provisions of the taxpayer relief act as more information becomes available. If you have any questions please feel free to contact us. Congress passes 2012 Taxpayer Relief

Appropriate Checklists for Year-End Tax Planning

LPL Financial Dennis R. Marvin, CFP Branch Manager 28025 Clemens Road Suite 2A Westlake, OH 44145 440-250-9990 Fax: 440-250-9986 dennis@marvinwealth.com www.marvinwealth.com Appropriate Checklists for

LPL Financial Dennis R. Marvin, CFP Branch Manager 28025 Clemens Road Suite 2A Westlake, OH 44145 440-250-9990 Fax: 440-250-9986 dennis@marvinwealth.com www.marvinwealth.com Appropriate Checklists for

ANALYSIS OF AMERICAN TAXPAYER RELIEF ACT OF 2012 (INCLUDING CALIFORNIA CONFORMITY)

") ANALYSIS OF AMERICAN TAXPAYER RELIEF ACT OF 2012 (INCLUDING CALIFORNIA CONFORMITY) AMERICAN TAXPAYER RELIEF ACT OF 2012 In the wee hours of New Year s morning, the Senate passed the American Taxpayer Relief

ANALYSIS OF AMERICAN TAXPAYER RELIEF ACT OF 2012 (INCLUDING CALIFORNIA CONFORMITY) AMERICAN TAXPAYER RELIEF ACT OF 2012 In the wee hours of New Year s morning, the Senate passed the American Taxpayer Relief

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2012

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2012 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION February 24, 2012 JCX-18-12 CONTENTS Page INTRODUCTION... 1 I. SUMMARY OF PRESENT-LAW FEDERAL

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2012 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION February 24, 2012 JCX-18-12 CONTENTS Page INTRODUCTION... 1 I. SUMMARY OF PRESENT-LAW FEDERAL

Tax Alpha. Robert S. Keebler, CPA, M.S.T., AEP. Keebler & Associates, LLP 420 South Washington Street Green Bay, WI 54301.

Tax Alpha Presented by Robert S. Keebler, CPA, M.S.T., AEP Keebler & Associates, LLP 420 South Washington Street Green Bay, WI 54301 Agenda 1. Five Dimensional Tax System Ordinary Income Rates Capital

Tax Alpha Presented by Robert S. Keebler, CPA, M.S.T., AEP Keebler & Associates, LLP 420 South Washington Street Green Bay, WI 54301 Agenda 1. Five Dimensional Tax System Ordinary Income Rates Capital

Instructions for Form 6251

2015 Instructions for Form 6251 Alternative Minimum Tax Individuals Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. General

2015 Instructions for Form 6251 Alternative Minimum Tax Individuals Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. General

Obama Tax Compromise APPROVED by Congress

December 17, 2010 Obama Tax Compromise APPROVED by Congress on Thursday, December 16, 2010 The $858 billion tax deal negotiated by President Obama and Republican leadership was overwhelmingly approved

December 17, 2010 Obama Tax Compromise APPROVED by Congress on Thursday, December 16, 2010 The $858 billion tax deal negotiated by President Obama and Republican leadership was overwhelmingly approved

State Street Bank and Trust Company Universal Individual Retirement Account Information Kit

State Street Bank and Trust Company Universal Individual Retirement Account Information Kit The Federated Funds State Street Bank and Trust Company Universal Individual Retirement Custodial Account Instructions

State Street Bank and Trust Company Universal Individual Retirement Account Information Kit The Federated Funds State Street Bank and Trust Company Universal Individual Retirement Custodial Account Instructions

Client Tax Letter. Reducing Uncertainty, Increasing. Complexity. What s Inside. April/May/June 2013

Client Tax Letter Tax Saving and Planning Strategies from your Trusted Business Advisor sm Reducing Uncertainty, Increasing Complexity Each April, most Americans file their income tax returns for the previous

Client Tax Letter Tax Saving and Planning Strategies from your Trusted Business Advisor sm Reducing Uncertainty, Increasing Complexity Each April, most Americans file their income tax returns for the previous

EXECUTIVE SUMMARY American Taxpayer Relief Act of 2012

TAX LEGISLATION January 2013 EXECUTIVE SUMMARY American Taxpayer Relief Act of 2012 Late in the night, on January 1, 2013, Congress completed work on the tax piece of the so-called fiscal cliff negotiations.

TAX LEGISLATION January 2013 EXECUTIVE SUMMARY American Taxpayer Relief Act of 2012 Late in the night, on January 1, 2013, Congress completed work on the tax piece of the so-called fiscal cliff negotiations.

CHAPTER VIII CONSUMPTION TAX. General

CHAPTER VIII CONSUMPTION TAX General Taxable Items General Transactions subject to Consumption Tax Criteria for Classification of Domestic and Overseas Transactions a. b. c. Non-taxable Transactions

CHAPTER VIII CONSUMPTION TAX General Taxable Items General Transactions subject to Consumption Tax Criteria for Classification of Domestic and Overseas Transactions a. b. c. Non-taxable Transactions

Summary of Small Business Health Insurance Tax Credit Under PPACA (P.L. 111-148)

") Summary of Small Business Health Insurance Tax Credit Under PPACA (P.L. 111-148) Chris L. Peterson Hinda Chaikind April 5, 2010 Congressional Research Service CRS Report for Congress Prepared for Members

Summary of Small Business Health Insurance Tax Credit Under PPACA (P.L. 111-148) Chris L. Peterson Hinda Chaikind April 5, 2010 Congressional Research Service CRS Report for Congress Prepared for Members

TAX. Fast. Facts. Special thanks to:

The online version of Tax will be updated for tax law changes. Check it out at www.calcpa.org/fasttaxfacts. As of Oct. 21, 2015 Welcome to our annual at-a-glance compilation of federal and state tax information.

The online version of Tax will be updated for tax law changes. Check it out at www.calcpa.org/fasttaxfacts. As of Oct. 21, 2015 Welcome to our annual at-a-glance compilation of federal and state tax information.

PRESENT LAW AND HISTORICAL OVERVIEW OF THE FEDERAL TAX SYSTEM

PRESENT LAW AND HISTORICAL OVERVIEW OF THE FEDERAL TAX SYSTEM Scheduled for a Public Hearing Before the COMMITTEE ON WAYS AND MEANS on January 20, 2011 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION

PRESENT LAW AND HISTORICAL OVERVIEW OF THE FEDERAL TAX SYSTEM Scheduled for a Public Hearing Before the COMMITTEE ON WAYS AND MEANS on January 20, 2011 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION

PRESENT LAW AND HISTORICAL OVERVIEW OF THE FEDERAL TAX SYSTEM

PRESENT LAW AND HISTORICAL OVERVIEW OF THE FEDERAL TAX SYSTEM Scheduled for a Public Hearing Before the SENATE COMMITTEE ON FINANCE on December 2, 2010 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION

PRESENT LAW AND HISTORICAL OVERVIEW OF THE FEDERAL TAX SYSTEM Scheduled for a Public Hearing Before the SENATE COMMITTEE ON FINANCE on December 2, 2010 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION

Tax Benefits for Education: Information Center. Credits

Tax Benefits for Education: Information Center There is a variety of tax credits, deductions and savings plans available to taxpayers to assist with the expense of higher education. A tax credit reduces

Tax Benefits for Education: Information Center There is a variety of tax credits, deductions and savings plans available to taxpayers to assist with the expense of higher education. A tax credit reduces

Table of contents. 2 Federal income tax rates. 12 Required minimum distributions. 4 Child credits. 13 Roths. 5 Taxes: estates, gifts, Social Security

2015 Tax Guide Table of contents 2 Federal income tax rates 4 Child credits 5 Taxes: estates, gifts, Social Security 6 Rules on retirement plans 8 Saver s credit 12 Required minimum distributions 13 Roths

2015 Tax Guide Table of contents 2 Federal income tax rates 4 Child credits 5 Taxes: estates, gifts, Social Security 6 Rules on retirement plans 8 Saver s credit 12 Required minimum distributions 13 Roths

Year-End Tax and Financial Planning Ideas

Private Wealth Management Products & Services Year-End Tax and Financial Planning Ideas A year without change provides a nice respite. Will it last? Whoever said Variety is the spice of life clearly wasn

Private Wealth Management Products & Services Year-End Tax and Financial Planning Ideas A year without change provides a nice respite. Will it last? Whoever said Variety is the spice of life clearly wasn

New 2012 & 2013 Global Mobility Tax & Payroll Issues

New 2012 & 2013 Global Mobility Tax & Payroll Issues Speaker: David S. Oltman oltman@relotax.com Title: Chief Compliance Officer Ineo/Co-Founder Relocation Taxes, LLC Location: Pittsburgh, PA Date: 9/14/12

New 2012 & 2013 Global Mobility Tax & Payroll Issues Speaker: David S. Oltman oltman@relotax.com Title: Chief Compliance Officer Ineo/Co-Founder Relocation Taxes, LLC Location: Pittsburgh, PA Date: 9/14/12

Can Deduction Be Taken Prior to Investing the Funds?

Deadline to Establish and Fund an IRA An IRA can be established and funded at any time from January of the current year and up to and including the date an individual s income tax return is due (generally,

Deadline to Establish and Fund an IRA An IRA can be established and funded at any time from January of the current year and up to and including the date an individual s income tax return is due (generally,

INDIVIDUAL TAX STRATEGIES

BY SCOTT HENSLEY SHENSLEY@STANCILCPA.COM DECEMBER 4, 2014 STANCIL & COMPANY CERTIFIED PUBLIC ACCOUNTANTS 4909 WINDY HILL DRIVE RALEIGH, NC 27609 919-872-1260 TOPICS TO BE COVERED TODAY WHAT IS TAX PLANNING

BY SCOTT HENSLEY SHENSLEY@STANCILCPA.COM DECEMBER 4, 2014 STANCIL & COMPANY CERTIFIED PUBLIC ACCOUNTANTS 4909 WINDY HILL DRIVE RALEIGH, NC 27609 919-872-1260 TOPICS TO BE COVERED TODAY WHAT IS TAX PLANNING

Highlights of the 2010 Tax Relief Act

On December 7, 200, President Barack Obama signed into law H.R. 4853, the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 200 (the 200 Tax Relief Act). This massive bill affects

On December 7, 200, President Barack Obama signed into law H.R. 4853, the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 200 (the 200 Tax Relief Act). This massive bill affects

Individual Retirement Arrangements (IRAs)

") Department of the Treasury Internal Revenue Service Publication 590 Cat. No. 15160x Individual Retirement Arrangements (IRAs) (Including Roth IRAs and Education IRAs) For use in preparing 2000 Returns

Department of the Treasury Internal Revenue Service Publication 590 Cat. No. 15160x Individual Retirement Arrangements (IRAs) (Including Roth IRAs and Education IRAs) For use in preparing 2000 Returns

CLIFF A CASE FOR CHARITABLE GIVING AND DEFENSIVE POSITIONING

THE FISCAL CLIFF A CASE FOR CHARITABLE GIVING AND DEFENSIVE POSITIONING The CriTTenTon FoundaTion & LJPr, LLC Leon C. LaBreCque, JD, CPa, CFP, CFa ! Preface The Perfect Tax Storm: Prospective Expiration

THE FISCAL CLIFF A CASE FOR CHARITABLE GIVING AND DEFENSIVE POSITIONING The CriTTenTon FoundaTion & LJPr, LLC Leon C. LaBreCque, JD, CPa, CFP, CFa ! Preface The Perfect Tax Storm: Prospective Expiration

Gleim CPA Review Updates to Regulation 2013 Edition, 1st Printing September 2013

Page 1 of 11 Gleim CPA Review Updates to Regulation 2013 Edition, 1st Printing September 2013 NOTE: Text that should be deleted is displayed with a line through the text. New text is shown with a blue

Page 1 of 11 Gleim CPA Review Updates to Regulation 2013 Edition, 1st Printing September 2013 NOTE: Text that should be deleted is displayed with a line through the text. New text is shown with a blue

SAMPLE EXAMINATION I Answer Key

FCS 5530 Income Tax Planning (Dr. Jessie Fan) Student name Sample Exam UNID SAMPLE EXAMINATION I Answer Key I. Multiple Choice Questions (Please choose the Best answer for teach question. 10 points each,

FCS 5530 Income Tax Planning (Dr. Jessie Fan) Student name Sample Exam UNID SAMPLE EXAMINATION I Answer Key I. Multiple Choice Questions (Please choose the Best answer for teach question. 10 points each,

Individual Retirement Arrangements (IRAs)

") Department of the Treasury Internal Revenue Service Publication 590 Cat. No. 15160x Individual Retirement Arrangements (IRAs) (Including Roth IRAs and Education IRAs) For use in preparing 1999 Returns

Department of the Treasury Internal Revenue Service Publication 590 Cat. No. 15160x Individual Retirement Arrangements (IRAs) (Including Roth IRAs and Education IRAs) For use in preparing 1999 Returns

TAX RELIEF ACT UPDATED DECEMBER 29, 2010

2010 TAX RELIEF ACT UPDATED DECEMBER 29, 2010 TAX RELIEF, UNEMPLOYMENT INSURANCE RE-AUTHORIZATION, AND JOB CREATION ACT OF 2010 INTRODUCTION On December 17, 2010, President Obama signed the much-anticipated

2010 TAX RELIEF ACT UPDATED DECEMBER 29, 2010 TAX RELIEF, UNEMPLOYMENT INSURANCE RE-AUTHORIZATION, AND JOB CREATION ACT OF 2010 INTRODUCTION On December 17, 2010, President Obama signed the much-anticipated

- all the money you receive in a year - money from wages, tips, interest you earn, dividends, capital gains, etc.

4D Income Taxes there are 5 different categories Single You must be unmarried at the end of the year. Married filing jointly this is how most married people will file. Married filing separately occasionally,

4D Income Taxes there are 5 different categories Single You must be unmarried at the end of the year. Married filing jointly this is how most married people will file. Married filing separately occasionally,

TAX GUIDE 15. A Publication of RubinBrown LLP

TAX GUIDE 15 A Publication of RubinBrown LLP Welcome Today s tax environment is more dynamic than ever before. This year, we sought to find a way to keep our clients and friends as up-to-date as possible

TAX GUIDE 15 A Publication of RubinBrown LLP Welcome Today s tax environment is more dynamic than ever before. This year, we sought to find a way to keep our clients and friends as up-to-date as possible

LIFE INSURANCE DIVISION

TAX LAW SUMMARY American Taxpayer Relief Act MKTG-OC-1053A LIFE INSURANCE DIVISION TAX LAW SUMMARY American Taxpayer Relief Act INDIVIDUAL TAX PROVISIONS...3 Individual Tax Rates...3 Marriage Penalty Relief...4

TAX LAW SUMMARY American Taxpayer Relief Act MKTG-OC-1053A LIFE INSURANCE DIVISION TAX LAW SUMMARY American Taxpayer Relief Act INDIVIDUAL TAX PROVISIONS...3 Individual Tax Rates...3 Marriage Penalty Relief...4

Custodial accounts 3. Kiddie tax 4. Estimated tax payments 4. Retirement plans 6. 2015 individual income tax rates 10. Charitable contributions 12

a b 2015 tax planning guide The confidence to pursue all your life goals begins with a plan. Advice. Beyond investing. Your financial life encompasses much more than the current markets. It includes your

a b 2015 tax planning guide The confidence to pursue all your life goals begins with a plan. Advice. Beyond investing. Your financial life encompasses much more than the current markets. It includes your

Traditional IRA s Contribution rules-

A Traditional IRA is a retirement plan that allows you to save money for retirement. In the case of a traditional IRA, you may also be offered an immediate tax shelter for the contributions that you make

A Traditional IRA is a retirement plan that allows you to save money for retirement. In the case of a traditional IRA, you may also be offered an immediate tax shelter for the contributions that you make

! There are currently two types of IRAs.

An IRA can be established and funded at any time from January 1 of the current year and up to and including the date an individual s income tax return is due (generally, April 1 of the following year),

An IRA can be established and funded at any time from January 1 of the current year and up to and including the date an individual s income tax return is due (generally, April 1 of the following year),

Tax-Saving Opportunities for "Active" Business Owners

S CORPORATIONS Tax-Saving Opportunities for "Active" Business Owners S corporations now provide business owners with a unique opportunity to minimize earnings subject to both the recently imposed additional

S CORPORATIONS Tax-Saving Opportunities for "Active" Business Owners S corporations now provide business owners with a unique opportunity to minimize earnings subject to both the recently imposed additional

Calculating Foreign Tax Credit Relief on income

Helpsheet 263 Tax year 6 April 2013 to 5 April 2014 Calculating Foreign Tax Credit Relief on income A Contacts Please phone: the number printed on page TR 1 of your tax return the SA Helpline on 0300 200

Helpsheet 263 Tax year 6 April 2013 to 5 April 2014 Calculating Foreign Tax Credit Relief on income A Contacts Please phone: the number printed on page TR 1 of your tax return the SA Helpline on 0300 200

FAQ for the First-time Homebuyer Tax Credit

FAQ for the First-time Homebuyer Tax Credit The following 24 questions and answers provide basic information about the new home buyer tax credit. If you have more specific questions, we strongly encourage

FAQ for the First-time Homebuyer Tax Credit The following 24 questions and answers provide basic information about the new home buyer tax credit. If you have more specific questions, we strongly encourage

2013 Federal Income Tax Update with The American Taxpayer Relief Act of 2012

THE UNIVERSITY OF TENNESSEE 2013 SINGLETON B. WOLFE MEMORIAL TAX CONFERENCE OCTOBER 31, 2013 2013 Federal Income Tax Update with The American Taxpayer Relief Act of 2012 JOHN D. HOUSTON, CPA Certified

THE UNIVERSITY OF TENNESSEE 2013 SINGLETON B. WOLFE MEMORIAL TAX CONFERENCE OCTOBER 31, 2013 2013 Federal Income Tax Update with The American Taxpayer Relief Act of 2012 JOHN D. HOUSTON, CPA Certified