MultiLife Discount Program

|

|

|

- Edith Porter

- 10 years ago

- Views:

Transcription

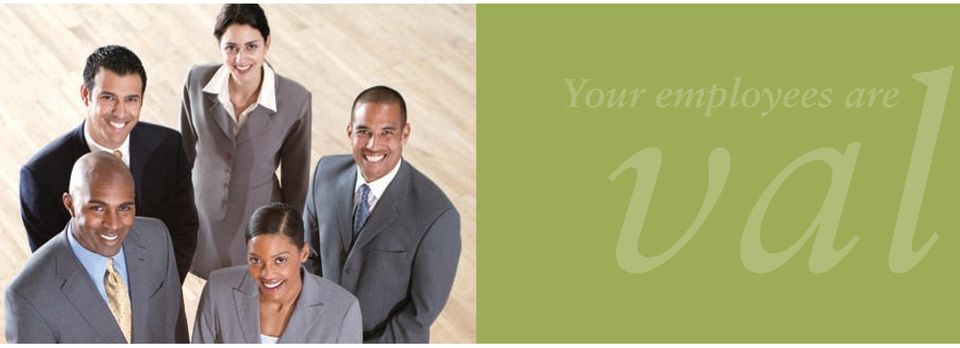

1 MultiLife Discount Program Sponsored Long-Term Care Insurance E m p l oy e r s G u i d e LTC (0507)

2 Your valu employees are

3 able Protect your key resource. Contents Your Employees are Your Business 1 Employee Benefits Solutions 1 2 Potential Impact of Long-term Care 3 MultiLife Discount Program 4 Why Offer Long-term Care Insurance? 4 Tax Advantages 5 A Name You Can Trust 6 Industry Evolution 7 Effective Communications 7

4 Your company depends on its Your Employees are Your Business In order to protect your business, you need to take care of your employees. Most companies couldn t succeed without their employees. Like many businesses that compete for employees as well as customers, you want to protect your most valuable resources. Employee Benefit Solutions One effective way to attract, retain and protect employees is with a comprehensive employee benefit package. What benefits are you currently offering to attract and retain quality employees? Health insurance Life insurance Disability income insurance retirement and savings plans How does your benefits package address your challenges? Long-term soundness and stability rewards and incentives for employees at all levels Value for recruiting and retention Did you know? According to the U.S. Department of Labor, the labor force in the next 10 years will be affected by the aging of the babyboomers (those born between 1946 and 1964). The labor force will experience an annual growth rate of the 55-and-older group that will be 4 times the rate of growth of the overall labor force. By contrast, the growth rate for 25-to-54 year age group will be 0.3%. 1 1 U.S. Department of Labor, Bureau of Labor Statistics, Labor force projections to 2014: retiring boomers (November 2005, Vol. 128, No. 11) 1

5 people, and your people depend on you. What if you, your employees, or family members should be affected by a need for long-term care services? Long-term care encompasses services provided to individuals suffering from a chronic illness, disabling condition or cognitive impairment. Services may be provided in the home, in your community, in an alternate living facility or in a nursing home. Is your company already dealing with these situations today? Potential Impact of Long-Term Care Long-term care can be a family concern. It presents physical and emotional challenges for your employees, and their families, that can affect their attendance and productivity at work. That means it s an issue that can affect your business. Nearly six in ten caregivers (59%) are employed either full-time or part-time. 2 About 10 million Americans need long-term care, and out-of-pocket payments cost recipients and their families $37 billion in % of family caregivers have had to make some adjustments to their work life, from reporting late to work to giving up work entirely. 2 23% of caregivers report having left his or her job either temporarily or permanently, and 10% of employed family caregivers go from full-time to part-time jobs because of their caregiving responsibilities. 2 Accidents and disabling diseases such as Multiple Sclerosis or strokes may require a young person to receive long-term care services. 2 National Alliance for Caregiving and AARP. Caregiving in the U.S. Washington, DC: Author, Georgetown University Long-term Care Financing Project National Spending for Long-Term Care Washington, DC: Georgetown University Press, February

6 Are your employees and their How might this impact your business? Northwestern Long Term Care Insurance Company (Northwestern LTC) has an opportunity to help you and your business. With the MultiLife Discount Program, your company can offer employees long-term care insurance that will help to: recognize, reward and protect your valued employees and their families Protect you, and your family members Help attract and retain quality employees Differentiate your employee benefits program from competitors Offer potential tax advantages to your business Provide a cutting edge benefit, while enabling caregivers to continue working Did you know? By 2050, the number of individuals using paid long-term care services in any setting (e.g., at home, residential care such as assisted living, or skilled nursing facilities) will likely double from the 15 million using services in 2000, to 27 million people. This estimate is influenced by growth in the population of older people in need of care. 4 4 U.S. Department of Health and Human Services, and U.S. Department of Labor. The future supply of long-term care workers in relation to the aging baby boom generation: Report to Congress. Washington, DC: Office of the Assistant Secretary for Planning and Evaluation, (2003). (20 Jan 2005) 3

will likely double from the 15 million using services in 2000, to 27 million people.")

7 families dealing with long-term issues today? MultiLife Discount Program 5% premium discount 5 Three W-2 employees to qualify Discount then applies to: employees and their spouses employee s parents, parents-in-law Retirees, and the retiree s spouse applies regardless of whether the employer is paying all, part or none of the premium 5 a 15 percent spousal discount may be leveraged with the 5% MultiLife discount 6 Note: Employees who already own Northwestern LTC insurance policies may help the employer meet the three-participant minimum. Advantages/Benefits of Long-Term Care Insurance Companies can choose to pay part, or all, of the premium for employees who meet a certain criteria. The is one of the few health-care-related benefit programs that can be offered on a discretionary basis. 7 all policies are underwritten individually and are issued as individual policies to employees. Employees may take their coverage with them if they retire or leave the company. Participants who leave the employer and keep their policy in force will retain eligibility for the MultiLife premium discount. any necessary changes made to issued policies are handled directly by Northwestern LTC s Administration Office. northwestern LTC helps minimize the possibility of your employees becoming distracted, encountering frequent personal interruptions or increased stress due to LTC concerns about themselves or their families, which may lead to a decrease in productivity. 5 Policies issued in New Jersey, New York and Pennsylvania with the MultiLife Discount have the form number RS.LTC.ML(1101). In New Jersey, the MultiLife discount is available for ages 40 and above only. In New York employer may not pay more than 50% of the premium. When spouses apply together and both policies are approved. 6 In Montana, discounts based on marital status are not available. A caregiver discount is available in Montana only. Please see your network representative for more information. Discount may be applied when both spouses apply for and are issued policies. 7 Employers should consult with their legal and tax advisors for specific advice. 4

8 Tax Advantages Many people don t realize that for the individual who is insured, tax-qualified policy benefits that are paid on a long-term care claim are generally received tax free. (a) A company that pays for some or all of its employees premiums may deduct a portion of the premiums paid for these tax-qualified policies, depending on how the business is structured. S-Corp, LLC, partnership or sole proprietor C-Corp Owners 8 Employees where the company pays the premium Eligible, age-based premium may be withdrawn tax-free from a Health Savings Account (HSA). (b) Premiums paid using non-hsa funds must be included in income and then deducted according to age-based limitations. (c) The employer can deduct the premium. The employee does not have to include the premium as part of income. Premiums are deductible for spouses who are not employees. The company can deduct the premium. (d) The owner, if participating in the plan as an employee, does not have to include the premium as part of income. (e) The company can deduct the premium. (d) The employee does not have to include the premium as part of income. (e) Premiums are deductible for spouses who are not employees. (d) Maximum Eligible Premium in 2007 indexed for inflation annually Self-employed deductibility guidelines (f) Age Amount 40 or less $ $ $1, $2, and older $3,680 Tax Codes: (a) IRC 7702B(a), 104(a)(3), 105(b) (b) IRC 223(d)(2), 223(f)1) (c) IRC 213(d)(10), 162(l) (d) IRC 162(a) (e) IRC 106(a) (f) IRC 213(d)(10) 5 8 Two percent or more shareholder. Employers should consult with their legal and tax advisors for specific advice. The Employee Retirement Income Security Act of 1974 (ERISA) establishes employer responsibilities for some employer-supported insurance plans. Employees of companies that do not pay LTC insurance premiaums: Individuals paying their own premiums on tax-qualified long-term care insurance may deduct such premiums (subject to the above age-based limitations on amount) to the extent that those premiums and other unreimbursed medical expenses exceed 7.5 percent of their adjusted gross income for the year. A tax advisor should be consulted for definitive advice with respect to individual situations.

Premiums paid using non-hsa funds must be included in income and then deducted according to age-based limitations. (c) The employer can deduct the premium.")

9 Trust Why Northwestern LTC? Northwestern LTC is a wholly owned subsidiary of The Northwestern Mutual Life Insurance Company (Northwestern Mutual), the only company in Fortune s prestigious list of the world s most admired companies to rank first in its industry every year since Northwestern LTC shares a commitment to the same values and guiding principles. Our Commitment Values of mutuality We make decisions based on the best long-term interest of policyowners guided by the principle of equitable treatment for all, and building long-term relationships to meet their needs. Financial strength We have the best possible insurance financial strength ratings from all four major industry ratings services. Flexibility in plan design We offer the ability to customize the plan design and individual insurance policies to meet your specific needs. Claims handling It is Northwestern LTC s philosophy to pay claims promptly, fairly and accurately, compatible with Northwestern s principle of fairness to all customers. Policy participation We offer a participating long-term care insurance policy, and announced a [$3.9 million dividend for 2007.] Recognized Financial Strength 9 Financial strength is and has been integral to Northwestern LTC s vision for policyowners, who own the company. Northwestern LTC maintains the best possible insurance financial strength ratings from all four major rating services. These ratings provide a professional assessment of Northwestern LTC s financial strength and security and represent our A++ AAA AAA Aaa A.M. Best Superior Standard & Poor s Extremely Strong Fitch Ratings Extremely Strong Moody s Exceptional Highest Highest Highest Best Possible Rating Rating Rating Rating promise to pay our claims and meet our obligations. Additionally, benefits of Northwestern LTC policies have been 100 percent guaranteed by Northwestern Mutual. Neither the existence nor the amount of a dividend is guaranteed in any given year. Decisions with respect to the determination and allocation of divisible surplus are left to the discretion and sound business judgment of the Board of Directors. There is no guaranteed specific method or formula for the determination and allocation of divisible surplus. Northwestern Long Term Care Insurance Company s approach is subject to change. Any dividends paid will be used to reduce future premiums. 9 The four agencies listed base ratings on the financial strength of the insurance company. These ratings are not recommendations of specific policy provisions, rates or practices of the insurance company. Since its entrance into the long-term care insurance market in 1998, all four agencies have given Northwestern Long Term Care Insurance Company the best possible insurance financial strength ratings. At the time of this publication, our most current ratings are for the following dates: A.M. Best (May 2006), Fitch Ratings (May 2005), Moody s (March 2006), and Standard & Poor s (May 2006). 6

10 Stability Industry Evolution Many of our competitors have either abandoned the long-term care insurance marketplace or have merged their product line with another company. Of the top ten companies selling long-term care insurance in 1996, many are no longer selling long-term care insurance today and few are of the same ownership*. Northwestern Long Term Care Insurance Company began issuing long-term care insurance in 1998 only after closely examining the long-term care insurance marketplace, and we have quickly moved into the top ten companies for newly issued business while pricing to promote long-term stability. Effective Communication Effective communication to your employees regarding the value of a long-term care insurance program is essential to its success. Northwestern LTC can provide various resources to help you market long-term care insurance to your employees: Workplace marketing and promotion Letters, brochures, payroll stuffers, table tents Intranet and newsletter articles employee education presentations templates 7 *As reported by LIMRA International in 2007.

11

12 Your state s insurance department may have additional information, including a buyer s guide, explaining longterm care insurance. This insurance policy contains exclusions and limitations. For costs and complete details, please contact your Financial Representative. Northwestern Long Term Care Insurance Company A Subsidiary of The Northwestern Mutual Life Insurance Company Milwaukee, WI The purpose of this material is for the marketing and solicitation of insurance. Policy forms: RS.LTC.(1101) & RS.LTC.ML.(1101). RS.LTC.ML.(1101) is only available in New Jersey, New York and Pennsylvania LTC (0507)

& RS.LTC.ML.")

Tax advantages of long-term care insurance

Tax advantages of long-term care insurance For you and your business LTC-4920 6/08 Long-Term Care Insurance REV. 1/14 Proactive LTC planning for your business and your future A comfortable and secure future

Tax advantages of long-term care insurance For you and your business LTC-4920 6/08 Long-Term Care Insurance REV. 1/14 Proactive LTC planning for your business and your future A comfortable and secure future

Long Term Care Insurance

LifeSecure Insurance Company Long Term Care Insurance Solutions for the Worksite California LS-13001-LTC CA 12/13 Help your employees protect what they ve worked so hard to build. Long Term Care Insurance

LifeSecure Insurance Company Long Term Care Insurance Solutions for the Worksite California LS-13001-LTC CA 12/13 Help your employees protect what they ve worked so hard to build. Long Term Care Insurance

Guaranteed Lifetime Income Annuities

THE NORTHWESTERN MUTUAL LIFE INSURANCE COMPANY (NORTHWESTERN MUTUAL) Guaranteed Lifetime Income Annuities Guaranteed Income Today Select Immediate Income Annuity Select Portfolio Immediate Income Annuity

THE NORTHWESTERN MUTUAL LIFE INSURANCE COMPANY (NORTHWESTERN MUTUAL) Guaranteed Lifetime Income Annuities Guaranteed Income Today Select Immediate Income Annuity Select Portfolio Immediate Income Annuity

Metropolitan Life Insurance Company ( MetLife ) ExecutiveCare SM

ExecutiveCare SM") Metropolitan Life Insurance Company ( MetLife ) ExecutiveCare SM MetLife s Long-Term Care Insurance Executive Benefit Program ADF# 1665.06 MetLife Investors L06079UZ9(exp0707)MLIC-LD PEANUTS United Feature

Metropolitan Life Insurance Company ( MetLife ) ExecutiveCare SM MetLife s Long-Term Care Insurance Executive Benefit Program ADF# 1665.06 MetLife Investors L06079UZ9(exp0707)MLIC-LD PEANUTS United Feature

WHAT EVERY EMPLOYER SHOULD KNOW ABOUT Long Term Care Insurance

WHAT EVERY EMPLOYER SHOULD KNOW ABOUT Long Term Care Insurance Unum Life Insurance Company of America 2211 Congress Street, Portland, Maine 04122 A-36015 (7-00) (8-01) UNDERSTANDING LONG TERM CARE Today

WHAT EVERY EMPLOYER SHOULD KNOW ABOUT Long Term Care Insurance Unum Life Insurance Company of America 2211 Congress Street, Portland, Maine 04122 A-36015 (7-00) (8-01) UNDERSTANDING LONG TERM CARE Today

Prudential s Long Term Care Insurance Tax Guide

Prudential s Long Term Care Insurance Tax Guide Table of Contents Contributory arrangement 3 Corporation (C-corporation or entity with a 501 trust providing coverage to its employees) 5 Individual who

Prudential s Long Term Care Insurance Tax Guide Table of Contents Contributory arrangement 3 Corporation (C-corporation or entity with a 501 trust providing coverage to its employees) 5 Individual who

2015 Guide. Tax Breaks & Incentives. for Long Term Care Insurance. Federal AND State

2015 Guide Tax Breaks & Incentives for Long Term Care Insurance Federal AND State Table of Contents Introduction...3 Disclaimer...3 Premiums Paid by an Individual...3 Premiums Paid by an Employer...3 Taxation

2015 Guide Tax Breaks & Incentives for Long Term Care Insurance Federal AND State Table of Contents Introduction...3 Disclaimer...3 Premiums Paid by an Individual...3 Premiums Paid by an Employer...3 Taxation

Program Overview. The Federal Long Term Care Insurance Program. Make long term care insurance part of your plan

The Federal Long Term Care Insurance Program Make long term care insurance part of your plan Program Overview See inside for: Long term care and long term care insurance facts Program benefits Eligibility

The Federal Long Term Care Insurance Program Make long term care insurance part of your plan Program Overview See inside for: Long term care and long term care insurance facts Program benefits Eligibility

MassMutual CareChoice SM One

An Overview Guide MassMutual CareChoice SM One Prepare for the possibilities MassMutual CareChoice One (CareChoice One) is a single premium whole life insurance policy with a qualified long term care insurance

An Overview Guide MassMutual CareChoice SM One Prepare for the possibilities MassMutual CareChoice One (CareChoice One) is a single premium whole life insurance policy with a qualified long term care insurance

Long Term Care Insurance - Analysis

Long Term Care Insurance at the Worksite: An Overview Provided Courtesy of: About LTC Financial Partners Long term care planning is a very complex issue. Fortunately, each LTC Financial Partner is a neighbor,

Long Term Care Insurance at the Worksite: An Overview Provided Courtesy of: About LTC Financial Partners Long term care planning is a very complex issue. Fortunately, each LTC Financial Partner is a neighbor,

Financial Information Understanding Long Term Care Insurance

Financial Information Understanding Long Term Care Insurance Many Americans do not plan ahead financially for their long term care needs. Others wrongly assume that Medicare, Medicare supplemental policies

Financial Information Understanding Long Term Care Insurance Many Americans do not plan ahead financially for their long term care needs. Others wrongly assume that Medicare, Medicare supplemental policies

Transamerica Financial Life Insurance Company. Facts for Agents and Producers 2014 Edition

Transamerica Life Insurance Company Transamerica Financial Life Insurance Company Frequently Asked Tax uestions for Long Term Care Insurance Facts for Agents and Producers 2014 Edition ICC13 TLC3 A TG

Transamerica Life Insurance Company Transamerica Financial Life Insurance Company Frequently Asked Tax uestions for Long Term Care Insurance Facts for Agents and Producers 2014 Edition ICC13 TLC3 A TG

PROTECTION LONG-TERM CARE RIDER. An Accelerated Death Benefit Rider Protection when you need it most PRODUCER GUIDE

PRODUCER GUIDE PROTECTION An Accelerated Death Benefit Rider Protection when you need it most THIS MATERIAL IS FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC. Strength.

PRODUCER GUIDE PROTECTION An Accelerated Death Benefit Rider Protection when you need it most THIS MATERIAL IS FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC. Strength.

The cost of employee benefits keeps rising.

The cost of employee benefits keeps rising. Here s how we can help. Your employees mean a lot to your business. You probably pay for numerous benefits that make their lives better, and make your workplace

The cost of employee benefits keeps rising. Here s how we can help. Your employees mean a lot to your business. You probably pay for numerous benefits that make their lives better, and make your workplace

A CONSUMER S GUIDE TO LONG-TERM CARE INSURANCE PROTECTION. A WOMAN S GUIDE TO Long-TermCare. Insurance. Practical Planning Information For Women

A CONSUMER S GUIDE TO LONG-TERM CARE INSURANCE PROTECTION A WOMAN S GUIDE TO Long-TermCare Insurance Protection Practical Planning Information For Women Women with Spouses or Partners or Women Living Alone

A CONSUMER S GUIDE TO LONG-TERM CARE INSURANCE PROTECTION A WOMAN S GUIDE TO Long-TermCare Insurance Protection Practical Planning Information For Women Women with Spouses or Partners or Women Living Alone

Planning for Long-Term Care

long-term care insurance october 2013 2 What is Long-Term Care? 4 Why Should You Consider Long-Term Care Coverage? 6 Protecting Your Assets, As Well As Your Health Planning for Long-Term Care summary the

long-term care insurance october 2013 2 What is Long-Term Care? 4 Why Should You Consider Long-Term Care Coverage? 6 Protecting Your Assets, As Well As Your Health Planning for Long-Term Care summary the

EMPLOYEE BENEFITS PROGRAM

EMPLOYEE BENEFITS PROGRAM YOUR HEALTH. YOUR LIFE. YOUR FUTURE. 2014 CRC s benefit plans and programs are designed to provide you and your family with the protection you need today and the opportunity to

EMPLOYEE BENEFITS PROGRAM YOUR HEALTH. YOUR LIFE. YOUR FUTURE. 2014 CRC s benefit plans and programs are designed to provide you and your family with the protection you need today and the opportunity to

American National Insurance Company. Business Owner Retirement Plans

American National Insurance Company Business Owner Retirement Plans What is Your Ultimate Financial Goal? If you are a business owner seeking a retirement funding opportunity, or evaluating your existing

American National Insurance Company Business Owner Retirement Plans What is Your Ultimate Financial Goal? If you are a business owner seeking a retirement funding opportunity, or evaluating your existing

The Long-Term Care Rider

Producer Guide An Accelerated Death Benefit Rider FOR BROKER/DEALER USE ONLY. NOT FOR USE WITH THE PUBLIC. The Long-Term Care Rider The Long-Term Care Rider The Long-Term Care (LTC) rider 1 is designed

Producer Guide An Accelerated Death Benefit Rider FOR BROKER/DEALER USE ONLY. NOT FOR USE WITH THE PUBLIC. The Long-Term Care Rider The Long-Term Care Rider The Long-Term Care (LTC) rider 1 is designed

LONG-TERM CARE RIDER. An Accelerated Death Benefit Rider Protection when you need it most PRODUCER GUIDE

PRODUCER GUIDE PROTECTION An Accelerated Death Benefit Rider Protection when you need it most THIS MATERIAL IS FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC. Strength.

PRODUCER GUIDE PROTECTION An Accelerated Death Benefit Rider Protection when you need it most THIS MATERIAL IS FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC. Strength.

IMPORTANT FACTS. about the tax treatment of disability insurance products

IMPORTANT FACTS about the tax treatment of disability insurance products Taxes Disability insurance premiums and benefits are subject to various tax laws, both on an individual and a business basis. This

IMPORTANT FACTS about the tax treatment of disability insurance products Taxes Disability insurance premiums and benefits are subject to various tax laws, both on an individual and a business basis. This

Zurich North America Total Rewards (U.S.) Summary information

Summary information") Zurich North America Total Rewards (U.S.) Summary information Zurich North America Total Rewards (U.S.) Summary Founded in Switzerland in 1872, Zurich is one of the world s most experienced insurers. Our

Zurich North America Total Rewards (U.S.) Summary information Zurich North America Total Rewards (U.S.) Summary Founded in Switzerland in 1872, Zurich is one of the world s most experienced insurers. Our

Building your coverage under a Group Long Term Care Insurance Policy underwritten by Aetna Life Insurance Company (Aetna)

") Building your coverage under a Group Long Term Care Insurance Policy underwritten by Aetna Life Insurance Company (Aetna) When you make the decision to purchase Long Term Care (LTC) insurance, you are

Building your coverage under a Group Long Term Care Insurance Policy underwritten by Aetna Life Insurance Company (Aetna) When you make the decision to purchase Long Term Care (LTC) insurance, you are

I don t have health insurance, can I get an HSA? Unfortunately, you cannot establish and contribute to an HSA unless you have coverage under a HDHP.

FREQUENTLY ASKED QUESTIONS (Information obtained from US Treasury HSA website) HSA Basics What is a Health Savings Account ( HSA )? A Health Savings Account is an alternative to traditional health insurance;

FREQUENTLY ASKED QUESTIONS (Information obtained from US Treasury HSA website) HSA Basics What is a Health Savings Account ( HSA )? A Health Savings Account is an alternative to traditional health insurance;

MassMutual Whole Life Insurance

A Technical Overview for Clients and their Advisors MassMutual Whole Life Insurance The product design and pricing process Contents 1 Foreword 2 A Brief History of Whole Life Insurance 3 Whole Life Basics

A Technical Overview for Clients and their Advisors MassMutual Whole Life Insurance The product design and pricing process Contents 1 Foreword 2 A Brief History of Whole Life Insurance 3 Whole Life Basics

Understanding Variations in Long-term Care and Chronic Illness Riders

Understanding Variations in Long-term Care and Chronic Illness Riders Shawn Britt, CLU Director, Advance Consulting Group America is aging. The Baby Boomer generation - once our nation s largest group

Understanding Variations in Long-term Care and Chronic Illness Riders Shawn Britt, CLU Director, Advance Consulting Group America is aging. The Baby Boomer generation - once our nation s largest group

Health Care Reform Frequently Asked Questions

Health Care Reform Frequently Asked Questions On March 23, 2010, President Obama signed federal health care reform into law, also known as the Patient Protection and Affordability Act. A second, or reconciliation

Health Care Reform Frequently Asked Questions On March 23, 2010, President Obama signed federal health care reform into law, also known as the Patient Protection and Affordability Act. A second, or reconciliation

Pacific PremierCare Advantage

Pacific Life Insurance Company Pacific PremierCare Advantage Universal Life Insurance with Long-Term Care Benefits 1 Client Guide 1 Pacific Life Insurance Company s Pacific PremierCare Advantage (Policy

Pacific Life Insurance Company Pacific PremierCare Advantage Universal Life Insurance with Long-Term Care Benefits 1 Client Guide 1 Pacific Life Insurance Company s Pacific PremierCare Advantage (Policy

Endorsement Split-Dollar

Endorsement Split-Dollar Allowing an Executive to Share in the Benefits of an Employer-Owned Life Insurance Policy AD-OC-859A Endorsement Split-Dollar Searching for Executive Benefit Solutions Retaining

Endorsement Split-Dollar Allowing an Executive to Share in the Benefits of an Employer-Owned Life Insurance Policy AD-OC-859A Endorsement Split-Dollar Searching for Executive Benefit Solutions Retaining

PruLife Index Advantage UL

PruLife Index Advantage UL Life insurance protection with a potential cash value growth advantage. Issued by Pruco Life Insurance Company or Pruco Life Insurance Company of New Jersey. 0214196 Ed. 01/2015

PruLife Index Advantage UL Life insurance protection with a potential cash value growth advantage. Issued by Pruco Life Insurance Company or Pruco Life Insurance Company of New Jersey. 0214196 Ed. 01/2015

LONG-TERM CARE RIDER An Accelerated Death Benefit Rider Protection when you need it most TECHNICAL GUIDE

TECHNICAL GUIDE LONG-TERM CARE RIDER An Accelerated Death Benefit Rider Protection when you need it most FOR AGENT USE ONLY. NOT FOR USE WITH THE PUBLIC. Table of Contents Product Overview... 2 Accelerating

TECHNICAL GUIDE LONG-TERM CARE RIDER An Accelerated Death Benefit Rider Protection when you need it most FOR AGENT USE ONLY. NOT FOR USE WITH THE PUBLIC. Table of Contents Product Overview... 2 Accelerating

Unum Life Insurance Company of America 2211 Congress Street Portland, Maine 04122 (207) 575-2211

575-2211") Unum Life Insurance Company of America 2211 Congress Street Portland, Maine 04122 (207) 575-2211 QUALIFIED LONG TERM CARE INSURANCE OUTLINE OF COVERAGE FOR THE EMPLOYEES OF CHEROKEE BOARD OF COMMISSIONERS

Unum Life Insurance Company of America 2211 Congress Street Portland, Maine 04122 (207) 575-2211 QUALIFIED LONG TERM CARE INSURANCE OUTLINE OF COVERAGE FOR THE EMPLOYEES OF CHEROKEE BOARD OF COMMISSIONERS

Long-term care insurance designed with you in mind

John Hancock Life Insurance Company (U.S.A.) Florida Long-term care insurance designed with you in mind Custom Care III featuring BENEFIT BUILDER LTC-8500FL 1/14 Long-Term Care Insurance Valuable coverage

John Hancock Life Insurance Company (U.S.A.) Florida Long-term care insurance designed with you in mind Custom Care III featuring BENEFIT BUILDER LTC-8500FL 1/14 Long-Term Care Insurance Valuable coverage

PORTFOLIO OVERVIEW. MutualCare Solutions Long-Term Care Insurance. Mutual of Omaha Insurance Company

MutualCare Solutions Long-Term Care Insurance Mutual of Omaha Insurance Company PORTFOLIO OVERVIEW M28381 For producer use only. Not for use with the general public. MutualCare Solutions It s a new approach

MutualCare Solutions Long-Term Care Insurance Mutual of Omaha Insurance Company PORTFOLIO OVERVIEW M28381 For producer use only. Not for use with the general public. MutualCare Solutions It s a new approach

Life Insurance with BenefitAccess Rider A CHRONIC AND TERMINAL ILLNESS RIDER THAT GIVES YOU FREEDOM, CHOICE, AND CONTROL

Life Insurance with BenefitAccess Rider A CHRONIC AND TERMINAL ILLNESS RIDER THAT GIVES YOU FREEDOM, CHOICE, AND CONTROL This brochure must be accompanied or preceded by a product brochure. Issued by Pruco

Life Insurance with BenefitAccess Rider A CHRONIC AND TERMINAL ILLNESS RIDER THAT GIVES YOU FREEDOM, CHOICE, AND CONTROL This brochure must be accompanied or preceded by a product brochure. Issued by Pruco

Planning for Long-Term Care

long-term care insuranceo october 2014 2 The Reality of Living Longer 4 Why Should You Consider Long-Term Care Coverage? 7 Protecting Your Assets, As Well As Your Health Planning for Long-Term Care Summary

long-term care insuranceo october 2014 2 The Reality of Living Longer 4 Why Should You Consider Long-Term Care Coverage? 7 Protecting Your Assets, As Well As Your Health Planning for Long-Term Care Summary

Comparing Your Long-Term Care Insurance Choices The table below compares the long-term care insurance programs available to you in several key areas.

Comparing Your Long-Term Care Insurance Choices The table below compares the long-term care insurance programs available to you in several key areas. ADMINISTRATION Who administers the program? ELIGIBILITY

Comparing Your Long-Term Care Insurance Choices The table below compares the long-term care insurance programs available to you in several key areas. ADMINISTRATION Who administers the program? ELIGIBILITY

Frequently Asked Questions

Frequently Asked Questions What is a Health Savings Account (HSA)? A Health Savings Account (HSA) is an alternative to traditional health insurance; it is a savings product that offers a different way

Frequently Asked Questions What is a Health Savings Account (HSA)? A Health Savings Account (HSA) is an alternative to traditional health insurance; it is a savings product that offers a different way

What You Should Know About Long Term Care. Answers to the most commonly asked questions from the Indiana Long Term Care Insurance Program

What You Should Know About Long Term Care Answers to the most commonly asked questions from the Indiana Long Term Care Insurance Program What You Should Know About Long Term Care The Indiana Long Term

What You Should Know About Long Term Care Answers to the most commonly asked questions from the Indiana Long Term Care Insurance Program What You Should Know About Long Term Care The Indiana Long Term

Health and Benefits Long Term Care Program. Frequently Asked Questions

The Maryland-National Capital Park and Planning Commission Health and Benefits Long Term Care Program Frequently Asked Questions Please read the enclosed information carefully Long Term Care (LTC) Frequently

The Maryland-National Capital Park and Planning Commission Health and Benefits Long Term Care Program Frequently Asked Questions Please read the enclosed information carefully Long Term Care (LTC) Frequently

Business Owner s Bonus Plan. Producer Guide. For agent/registered representative use only. Not for public distribution.

Business Owner s Bonus Plan Producer Guide For agent/registered representative use only. Not for public distribution. Business Owner s Bonus Plan Producer Guide The Business Owner s Bonus Plan is a personally

Business Owner s Bonus Plan Producer Guide For agent/registered representative use only. Not for public distribution. Business Owner s Bonus Plan Producer Guide The Business Owner s Bonus Plan is a personally

PruLife Custom Premier II

THE PROTECTION OF LIFE INSURANCE. THE POTENTIAL FOR LONG-TERM GROWTH. PruLife Custom Premier II NOT FOR USE IN CA Issued by Pruco Life Insurance Company In New York, it is issued by Pruco Life Insurance

THE PROTECTION OF LIFE INSURANCE. THE POTENTIAL FOR LONG-TERM GROWTH. PruLife Custom Premier II NOT FOR USE IN CA Issued by Pruco Life Insurance Company In New York, it is issued by Pruco Life Insurance

Mary, age 62, and Bob, age 65, have worked

Long-Term Care Insurance Could Montana s New Partnership Plan Have Helped the Smiths? by Jerry Furniss and Michael Harrington Editor s Note: On July 1, 2009, Montana joined 29 other states by having regulations

Long-Term Care Insurance Could Montana s New Partnership Plan Have Helped the Smiths? by Jerry Furniss and Michael Harrington Editor s Note: On July 1, 2009, Montana joined 29 other states by having regulations

2015 Tax Implications. of Long Term Care Insurance (LTCi) for Individuals and Businesses. Tax Solutions Guide for Individuals and Businesses

for Individuals and Businesses. Tax Solutions Guide for Individuals and Businesses") Tax Solutions Guide for Individuals and Businesses 2015 Tax Implications of Long Term Care Insurance (LTCi) for Individuals and Businesses Insurance Strategies LTC1419 What are the Tax Implications of

Tax Solutions Guide for Individuals and Businesses 2015 Tax Implications of Long Term Care Insurance (LTCi) for Individuals and Businesses Insurance Strategies LTC1419 What are the Tax Implications of

Pacific PremierCare Advantage Multi-Pay Fixed Premium Universal Life Insurance with Long-Term Care Benefits 1

Client Guide Pacific Life Insurance Company Pacific PremierCare Advantage Multi-Pay Fixed Premium Universal Life Insurance with Long-Term Care Benefits 1 LOCKABLE BENEFITS with 1 Pacific Life Insurance

Client Guide Pacific Life Insurance Company Pacific PremierCare Advantage Multi-Pay Fixed Premium Universal Life Insurance with Long-Term Care Benefits 1 LOCKABLE BENEFITS with 1 Pacific Life Insurance

The Pennsylvania Insurance Department s. Your Guide to Long-Term Care. Insurance

Your Guide to Long-Term Care Insurance When you re in the prime of life, it s hard to imagine being unable to do the basic activities of daily living because of age or disability. But the reality is that

Your Guide to Long-Term Care Insurance When you re in the prime of life, it s hard to imagine being unable to do the basic activities of daily living because of age or disability. But the reality is that

What You Should Know About Long Term Care. Answers to the most commonly asked questions from the Indiana Long Term Care Insurance Program

What You Should Know About Long Term Care Answers to the most commonly asked questions from the Indiana Long Term Care Insurance Program What You Should Know About Long Term Care The Indiana Long Term

What You Should Know About Long Term Care Answers to the most commonly asked questions from the Indiana Long Term Care Insurance Program What You Should Know About Long Term Care The Indiana Long Term

Pacific PremierCare Advantage* Flexible Premium Adjustable Life Insurance

Providing Life Insurance with LONG-TERM CARE BENEFITS Payable Through Reimbursements Pacific Life Insurance Company Pacific PremierCare Advantage* Flexible Premium Adjustable Life Insurance Prepared For:

Providing Life Insurance with LONG-TERM CARE BENEFITS Payable Through Reimbursements Pacific Life Insurance Company Pacific PremierCare Advantage* Flexible Premium Adjustable Life Insurance Prepared For:

Prudential Long Term Care

prudential s GROUP INSURANCE Prudential Long Term Care Solid Solutions SM 20 Questions concerning long-term care insurance The Prudential Insurance Company of America (Prudential) 0238884 Should you be

prudential s GROUP INSURANCE Prudential Long Term Care Solid Solutions SM 20 Questions concerning long-term care insurance The Prudential Insurance Company of America (Prudential) 0238884 Should you be

How To Get A Long Term Care Insurance Plan From Prudential

2010 Insurance Benefits Guide www.eip.sc.gov Employee Insurance Program 141 Insurance Benefits Guide 2010 Table of Contents Insurance...143 Important Information About the Plan...143 Plan Details...144

2010 Insurance Benefits Guide www.eip.sc.gov Employee Insurance Program 141 Insurance Benefits Guide 2010 Table of Contents Insurance...143 Important Information About the Plan...143 Plan Details...144

How To Get A Health Care Plan

Your financial well-being Everyone needs to plan ahead for Medicare Having a thorough understanding of how Medicare works and the choices you need to make about its coverage is an essential part of retirement

Your financial well-being Everyone needs to plan ahead for Medicare Having a thorough understanding of how Medicare works and the choices you need to make about its coverage is an essential part of retirement

A Guide to Planning for Retirement INVESTMENT BASICS SERIES

A Guide to Planning for Retirement INVESTMENT BASICS SERIES It s Never Too Early to Start What You Need to Know About Saving for Retirement Most of us don t realize how much time we may spend in retirement.

A Guide to Planning for Retirement INVESTMENT BASICS SERIES It s Never Too Early to Start What You Need to Know About Saving for Retirement Most of us don t realize how much time we may spend in retirement.

Life Insurance Protection for Your Working Years

Life Insurance Protection for Your Working Years Issued by Pruco Life Insurance Company or, in New York if available, by Pruco Life Insurance Company of New Jersey. 0194055 0194055-00001-00 WorkLife 65

Life Insurance Protection for Your Working Years Issued by Pruco Life Insurance Company or, in New York if available, by Pruco Life Insurance Company of New Jersey. 0194055 0194055-00001-00 WorkLife 65

CLIENT BROCHURE Nationwide YourLife Indexed UL. Find balance in life

CLIENT BROCHURE Nationwide YourLife Indexed UL Find balance in life Planning for the future may seem stressful these days especially with so much market uncertainty. But it doesn t have to be that way.

CLIENT BROCHURE Nationwide YourLife Indexed UL Find balance in life Planning for the future may seem stressful these days especially with so much market uncertainty. But it doesn t have to be that way.

Insurance. Survivorship Life. Insurance. The Company You Keep

Insurance Survivorship Life Insurance The Company You Keep Permanent Life Insurance Protection for Two People You ve built a legacy, but who will be the recipients your heirs or the IRS? 1 Now is the time

Insurance Survivorship Life Insurance The Company You Keep Permanent Life Insurance Protection for Two People You ve built a legacy, but who will be the recipients your heirs or the IRS? 1 Now is the time

Group Long Term Disability. Income Protection. For State IIA Association Members Effective July, 2001. with monthly benefits to $10,000

Group Long Term Disability Income Protection with monthly benefits to $10,000 Since 1964 KELSEY NATIONAL CORPORATION With Your State IIA Endorsed Group Long Term Disability Income Protection You Get These

Group Long Term Disability Income Protection with monthly benefits to $10,000 Since 1964 KELSEY NATIONAL CORPORATION With Your State IIA Endorsed Group Long Term Disability Income Protection You Get These

How to Choose a Disability Insurance Company

How to Choose a Disability Insurance Company Fulfilling Promises A 2014 GUIDE THROUGH RELEVANT INDUSTRY INFORMATION The Guardian Life Insurance Company of America (Guardian) is one of the largest mutual

How to Choose a Disability Insurance Company Fulfilling Promises A 2014 GUIDE THROUGH RELEVANT INDUSTRY INFORMATION The Guardian Life Insurance Company of America (Guardian) is one of the largest mutual

Asset-based LTC solutions

State Life Care Solutions Asset-based LTC solutions Product overview and training guide Products and financial services provided by The State Life Insurance Company a OneAmerica company For company use

State Life Care Solutions Asset-based LTC solutions Product overview and training guide Products and financial services provided by The State Life Insurance Company a OneAmerica company For company use

Blueprints for Business. Executive Bonus Arrangements Using Life Insurance Producer Guide. Your future. Made easier. SM LIFE

Blueprints for Business Executive Bonus Arrangements Using Life Insurance Producer Guide These materials are not intended to be used to avoid tax penalties and were prepared to support the promotion or

Blueprints for Business Executive Bonus Arrangements Using Life Insurance Producer Guide These materials are not intended to be used to avoid tax penalties and were prepared to support the promotion or

The Prudential Insurance Company of America. Long-Term Care Insurance. Questions. concerning long-term care insurance 0163472-00002-00

The Prudential Insurance Company of America Long-Term Care Insurance 20 Questions concerning long-term care insurance 0163472 0163472-00002-00 1WHAT IS LONG-TERM CARE? Long-term care covers a wide range

The Prudential Insurance Company of America Long-Term Care Insurance 20 Questions concerning long-term care insurance 0163472 0163472-00002-00 1WHAT IS LONG-TERM CARE? Long-term care covers a wide range

How To Buy The Long Term Care Services Sm Rider

life insurance AXA Equitable Life Insurance Company MONY Life Insurance Company of America one strategy can help address two needs Long-Term Care Services SM Rider (an accelerated death benefit rider)

life insurance AXA Equitable Life Insurance Company MONY Life Insurance Company of America one strategy can help address two needs Long-Term Care Services SM Rider (an accelerated death benefit rider)

Personal Long-Term Care Plan Long-Term Care Insurance. Plan Benefits First-Occurrence Nursing Home Assisted-Living Home Care

Personal Long-Term Care Plan Long-Term Care Insurance Plan Benefits First-Occurrence Nursing Home Assisted-Living Home Care Form A27075B1 IC(1/08) Personal Long-Term Care Plan Policy Series A-27000 When

Personal Long-Term Care Plan Long-Term Care Insurance Plan Benefits First-Occurrence Nursing Home Assisted-Living Home Care Form A27075B1 IC(1/08) Personal Long-Term Care Plan Policy Series A-27000 When