Flood Risk Assessment, Insurance and Damage mitigation. Jeroen Aerts, VU University Amsterdam

|

|

|

- Pearl Johns

- 8 years ago

- Views:

Transcription

1 Flood Risk Assessment, Insurance and Damage mitigation Jeroen Aerts, VU University Amsterdam

2 Contents Catastrophe / risk assessment models Using multiple scenarios Future Insurance premiums Lower risk; damage mitigation measures Relation insurance & damage mitigation Willingness to purchase Insurance Other issues 2

3 Contents Catastrophe / risk assessment models Using multiple scenarios Future Insurance premiums Lower risk; damage mitigation measures Relation insurance & damage mitigation Willingness to purchase Insurance Other issues 3

4 Catastrophe flood risk modeling Exposure Flood risk /yr Hazard 4

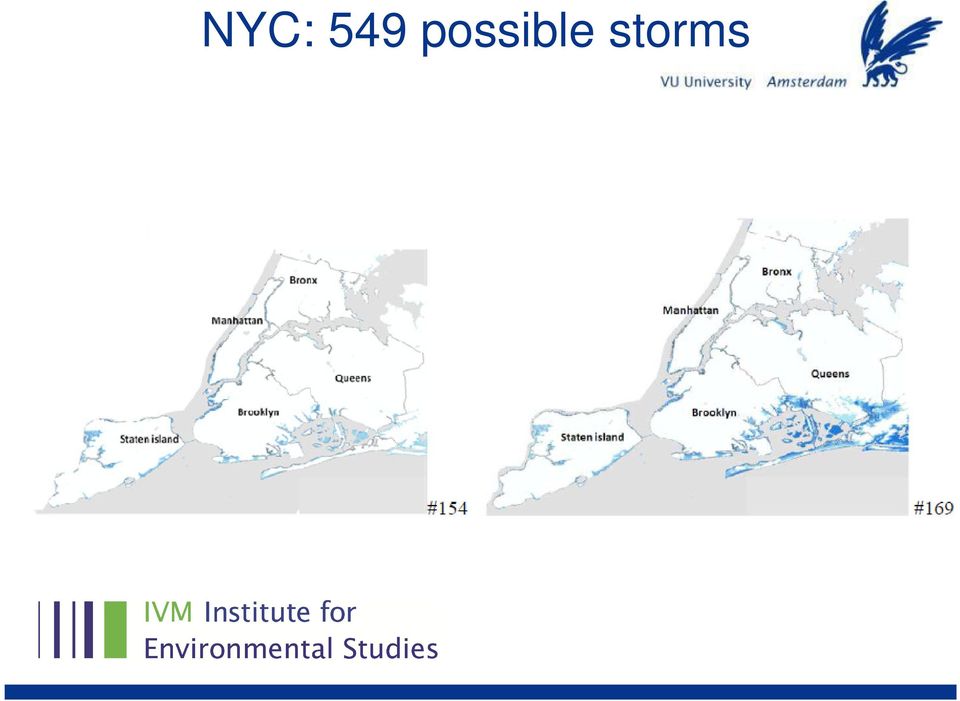

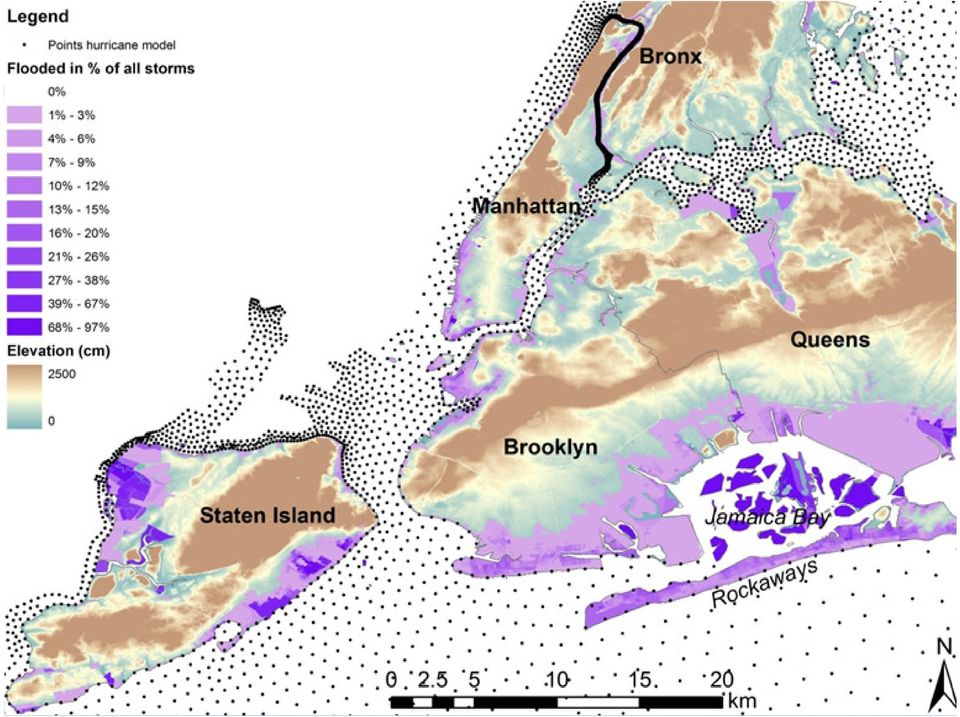

5 549 possible storms (MIT) Exposure Flood risk /yr Hazard 5 1/10 1/100 1/500 1/500 Insurance premium

6 NYC: 549 possible storms

7 7

8 Flood damage NYC for 549 storms New York City 1/100 1/75 Aerts et al., 2013, Risk Analysis 8

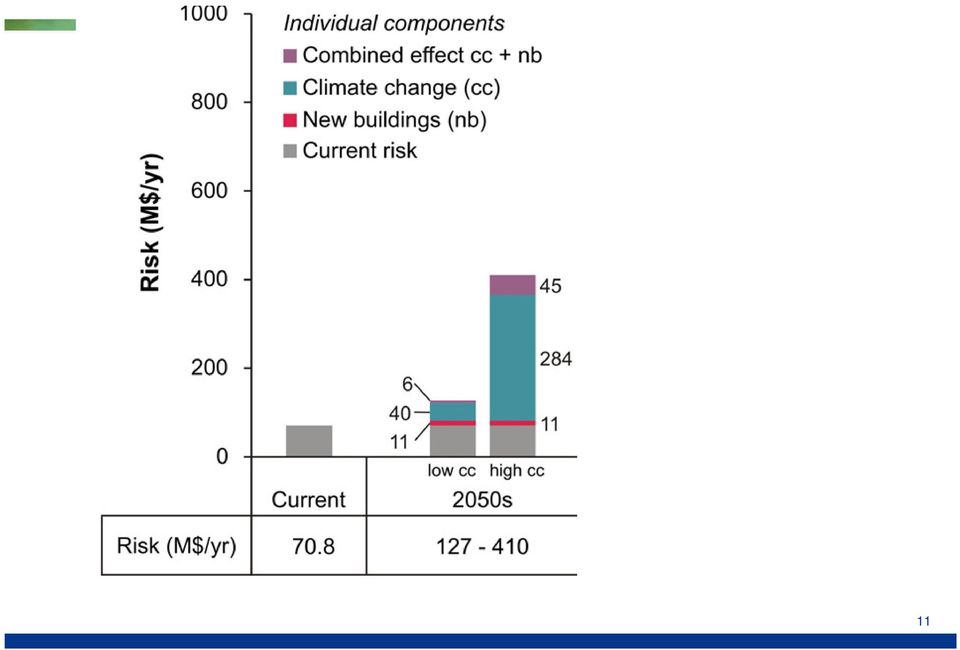

9 Future Flood risk Exposure Hazard /10 1/100 1/500 1/500 Flood risk 2010 /2050 /yr Insurance premiums

10 10

11 11

12 12

13 Contents Catastrophe / risk assessment models Using multiple scenarios Future Insurance premiums Lower risk; damage mitigation measures Relation insurance & damage mitigation Willingness to purchase Insurance Other issues 13

14 Premium Development over Time Spatial distribution of flood risk premiums in per year for 2015 and 2040 under a low economic growth scenario and sea level rise of 24 cm, assuming no adaptation 14

15 Insurance model The Netherlands Insurers / Re- insurers Damage coverage: max 20bn Euro Households Deductibles 15

16 Long term insurance Million Euro Capital Reserve, only Dike Ring areas RC low growth GE high growth

17 Million Euro Capital Reserve, Scenario 1 RC low growth GE high growth billion Euro damage 12 billion Euro damage 17

18 Insurance model The Netherlands Government Damage coverage: > $ 5Bn Insurers / Re- insurers Damage coverage: Max. $5Bn Households Deductible: $1Bn 18

19 Capital Reserve, Scenario 1 Million Euro RC low growth GE high growth billion Euro damage 12 billion Euro damage 19

20 Contents Catastrophe / risk assessment models Using multiple scenarios Future Insurance premiums Lower risk; damage mitigation measures Relation insurance & damage mitigation Willingness to purchase Insurance Other issues 20

21 Dry / Wet Floodproofing ODPM, Scotland,

22 Insurance & Building codes NFIP: National Flood Insurance Program $250,000 building coverage only (no contents coverage), for a single-family, one-story structure without a basement 22

23 23

24 24

25 Contents Catastrophe / risk assessment models Using multiple scenarios Future Insurance premiums Lower risk; damage mitigation measures Relation insurance & damage mitigation Willingness to purchase Insurance Other issues 25

26 Relation Flood event & implementation of pre cautionary measures (River Rhine, Germany) 26

27 Insured households more often implement mitigation measures Kreibich et al., 2005; Nat Hazards and Earth Sys Sc

28 What motivates households to implement flood proofing measures? Knowing measure works & idea of implementing measure themselves 28

29 What motivates households to implement flood proofing measures? Knowing the hazard Probability & impact 29

30 What motivates households to implement flood proofing measures? Own experience & Activity neighbors 30

31 Communicating Small Probabilities with Risk Ladders 31 31

32 Effectiveness of damage mitigation The Netherlands (Max damage in = 11 billion euros) 32

33 Contents Catastrophe / risk assessment models Using multiple scenarios Future Insurance premiums Lower risk; damage mitigation measures Relation insurance & damage mitigation Willingness to purchase Insurance Other issues 33

34 Choice Experiment

35 Demand for insurance under different scenarios (premiums adjusted to risk) Market penetration would be 50% for current conditions (49% in the USA) Will be 60% without government compensation Market for insurance is low for high probabilities > 1/

36 Contents Catastrophe / risk assessment models Using multiple scenarios Future Insurance premiums Lower risk; damage mitigation measures Relation insurance & damage mitigation Willingness to purchase Insurance Other issues 36

37 Damage to critical infrasrcuture Improve flood risk assessments, special focus on: Industrial/port areas Indirect effects: business interruption and supply-chain disruption Criticial infrastructure (e.g. energy/water supply) De Kort, 2012 Thailand,

38 Murphy Oil Spill, 2005 New Orleans 38

39 Economic losses: case Rotterdam Largest harbour in Europe Infrastructural hub: Gateway to Europe Soruce: Port authority of Rotterdam webiste 39 39

40 Economic losses Port of Rotterdam 40

41 Results economic losses model Flood damage in billions Euro Return period Direct damage Indirecte losses Total losses 1/ / /1, /2, /4, /10,

42 Thanks for your attention! 42 42

Regional economic effects of flooding

Regional economic effects of flooding Olaf Koops, Olga Ivanova and Wouter Jonkhoff Contents Dutch water management Flood damage: short and long term Case Rotterdam Conclusions 2 Dutch water management

Regional economic effects of flooding Olaf Koops, Olga Ivanova and Wouter Jonkhoff Contents Dutch water management Flood damage: short and long term Case Rotterdam Conclusions 2 Dutch water management

The Dutch Delta Approach

Sweden Mission from Skane The Dutch Delta Approach Future proof flood risk management in the Netherlands Martien Beek Special advisor to Delta Program Commissioner 18 September 2013 1 The Netherlands exposure

Sweden Mission from Skane The Dutch Delta Approach Future proof flood risk management in the Netherlands Martien Beek Special advisor to Delta Program Commissioner 18 September 2013 1 The Netherlands exposure

2014 Delaware Ordinance Workshops and assistance. Higher Standards identified by Delaware Senate Bill 64

INCREASING FLOOD RESILIENCY THROUGHT IMPROVED FLOOD CODES Michael S. Powell, Hazard Mitigation Program Manager, DNREC New Coastal Study and Floodplain Maps 2014 Delaware Ordinance Workshops and assistance

INCREASING FLOOD RESILIENCY THROUGHT IMPROVED FLOOD CODES Michael S. Powell, Hazard Mitigation Program Manager, DNREC New Coastal Study and Floodplain Maps 2014 Delaware Ordinance Workshops and assistance

URBAN FLOOD AWARENESS ACT. Brian Eber, CFM IDNR Office of Water Resources

URBAN FLOOD AWARENESS ACT Brian Eber, CFM IDNR Office of Water Resources Report Overview Report sections: 1. Analyze Past, Current, and Future flooding 2. Effectiveness of Programs and Policies 3. Strategies

URBAN FLOOD AWARENESS ACT Brian Eber, CFM IDNR Office of Water Resources Report Overview Report sections: 1. Analyze Past, Current, and Future flooding 2. Effectiveness of Programs and Policies 3. Strategies

Contents. Regional economic effects of flooding. Dutch water management. Flood damage: short and long term. Case Rotterdam.

Regional economic effects of flooding Olaf Koops, Olga Ivanova and Wouter Jonkhoff Wouter Jonkhoff Contents Dutch water management Flood damage: short and long term Case Rotterdam Conclusions 2 1 Dutch

Regional economic effects of flooding Olaf Koops, Olga Ivanova and Wouter Jonkhoff Wouter Jonkhoff Contents Dutch water management Flood damage: short and long term Case Rotterdam Conclusions 2 1 Dutch

Changing Flood Maps: A Guide for Homeowners and Consumers

Changing Flood Maps: A Guide for Homeowners and Consumers The flood maps in your community are being changed. What does this mean to you? Flood maps, also known as Flood Insurance Rate Maps or FIRMs, are

Changing Flood Maps: A Guide for Homeowners and Consumers The flood maps in your community are being changed. What does this mean to you? Flood maps, also known as Flood Insurance Rate Maps or FIRMs, are

Flood Risk Management Plans

Flood Risk Management Plans Main topics of interest and the workshop programme Jos van Alphen 26-01-2010 Content 1. Floods in Europe and related measures 2. The Floods Directive and Flood Risk Management

Flood Risk Management Plans Main topics of interest and the workshop programme Jos van Alphen 26-01-2010 Content 1. Floods in Europe and related measures 2. The Floods Directive and Flood Risk Management

Flood Insurance Coverage/Rates Summary Excerpted From Unit 9 of Managing Floodplain Development Through the National Flood Insurance Program

Flood Insurance Coverage/Rates Summary Excerpted From Unit 9 of Managing Floodplain Development Through the National Flood Insurance Program Amount of coverage Insurance rates for all buildings are based

Flood Insurance Coverage/Rates Summary Excerpted From Unit 9 of Managing Floodplain Development Through the National Flood Insurance Program Amount of coverage Insurance rates for all buildings are based

Martine Jak 1 and Matthijs Kok 2

A DATABASE OF HISTORICAL FLOOD EVENTS IN THE NETHERLANDS Martine Jak 1 and Matthijs Kok 2 1 Department of Transport, Public works and Water Management Road and Hydraulic Engineering Division P.O. Box 5044

A DATABASE OF HISTORICAL FLOOD EVENTS IN THE NETHERLANDS Martine Jak 1 and Matthijs Kok 2 1 Department of Transport, Public works and Water Management Road and Hydraulic Engineering Division P.O. Box 5044

The National Flood Insurance Program (NFIP)

") The National Flood Insurance Program (NFIP) Insurance Information Institute 110 William Street New York, NY 10038 (212) 346-5500 www.iii.org October 2005 Robert P. Hartwig, Ph.D., CPCU Senior Vice President

The National Flood Insurance Program (NFIP) Insurance Information Institute 110 William Street New York, NY 10038 (212) 346-5500 www.iii.org October 2005 Robert P. Hartwig, Ph.D., CPCU Senior Vice President

Climate change and increased risk for the insurance sector: a global perspective and an assessment for the Netherlands

Nat Hazards (2010) 52:577 598 DOI 10.1007/s11069-009-9404-1 ORIGINAL PAPER Climate change and increased risk for the insurance sector: a global perspective and an assessment for the Netherlands W. J. W.

Nat Hazards (2010) 52:577 598 DOI 10.1007/s11069-009-9404-1 ORIGINAL PAPER Climate change and increased risk for the insurance sector: a global perspective and an assessment for the Netherlands W. J. W.

35 YEARS FLOOD INSURANCE CLAIMS

40 RESOURCES NO. 191 WINTER 2016 A Look at 35 YEARS FLOOD INSURANCE CLAIMS of An analysis of more than one million flood claims under the National Flood Insurance Program reveals insights to help homeowners

40 RESOURCES NO. 191 WINTER 2016 A Look at 35 YEARS FLOOD INSURANCE CLAIMS of An analysis of more than one million flood claims under the National Flood Insurance Program reveals insights to help homeowners

Geohazards: Minimizing Risk, Maximizing Awareness The Role of the Insurance Industry

Geohazards: Minimizing Risk, Maximizing Awareness The Role of the Insurance Industry Prof. Dr. Peter Hoeppe Head of Geo Risks Research Munich Re International Year of Planet Earth, Paris, 13 February 2008

Geohazards: Minimizing Risk, Maximizing Awareness The Role of the Insurance Industry Prof. Dr. Peter Hoeppe Head of Geo Risks Research Munich Re International Year of Planet Earth, Paris, 13 February 2008

Willingness of Homeowners to Mitigate Climate Risk through Insurance

Willingness of Homeowners to Mitigate Climate Risk through Insurance W.J.W. Botzen Institute for Environmental Studies Vrije Universiteit, Amsterdam wouter.botzen@ivm.vu.nl and J.C.J.H. Aerts Institute

Willingness of Homeowners to Mitigate Climate Risk through Insurance W.J.W. Botzen Institute for Environmental Studies Vrije Universiteit, Amsterdam wouter.botzen@ivm.vu.nl and J.C.J.H. Aerts Institute

FLOOD MITIGATION Hampton Roads. MICHAEL VERNON Director of Business Development

FLOOD MITIGATION Hampton Roads MICHAEL VERNON Director of Business Development Changing weather patterns Bigger, stronger storms Rising sea levels Long term erosion Poor building decisions FLOODMAP Elevation

FLOOD MITIGATION Hampton Roads MICHAEL VERNON Director of Business Development Changing weather patterns Bigger, stronger storms Rising sea levels Long term erosion Poor building decisions FLOODMAP Elevation

Hurricane Preparation and Response Insurance & Risk Management AAPA

Hurricane Preparation and Response Insurance & Risk Management December 6-7, 2012 AAPA Miami, Florida Risk Management Pre Loss Planning What to do before a loss: Identification of insurance policies that

Hurricane Preparation and Response Insurance & Risk Management December 6-7, 2012 AAPA Miami, Florida Risk Management Pre Loss Planning What to do before a loss: Identification of insurance policies that

Willis 2012 Latin American Energy Conference

Willis 2012 Latin American Energy Conference Contingent Business Interruption aggregates, Supply Chain Management, all under control? Olivier Perraut, CUO Energy and Natural Resources - SCOR Global P&C

Willis 2012 Latin American Energy Conference Contingent Business Interruption aggregates, Supply Chain Management, all under control? Olivier Perraut, CUO Energy and Natural Resources - SCOR Global P&C

IBC s New Flood Maps - Leveraging data to effectively assess and manage flood risk

IBC s New Flood Maps - Leveraging data to effectively assess and manage flood risk Speakers: Lapo Calamai - Director, Catastrophe Risk and Economic Analysis, IBC Simon de la Hoyde - Head of Sales, Insurance,

IBC s New Flood Maps - Leveraging data to effectively assess and manage flood risk Speakers: Lapo Calamai - Director, Catastrophe Risk and Economic Analysis, IBC Simon de la Hoyde - Head of Sales, Insurance,

Finances. Table 1: Insured Policies. 2005, Center on Federal Financial Institutions 3

The Center on Federal Financial Institutions (COFFI) is a nonprofit, nonpartisan, nonideological policy institute focused on federal insurance and lending activities. original issue date: August 10, 2005,

The Center on Federal Financial Institutions (COFFI) is a nonprofit, nonpartisan, nonideological policy institute focused on federal insurance and lending activities. original issue date: August 10, 2005,

5-Day Training Workshop On Flood Mitigation. On: February 17, 2010. Islamabad. Sequence of Lecture

5-Day Training Workshop On Flood Mitigation Title: Flood Proofing On: February 17, 2010 At: Organized By: Islamabad NDMA-UNDP Sequence of Lecture Definition; Objectives; Types of flood proofing; Structural

5-Day Training Workshop On Flood Mitigation Title: Flood Proofing On: February 17, 2010 At: Organized By: Islamabad NDMA-UNDP Sequence of Lecture Definition; Objectives; Types of flood proofing; Structural

Insurance against damage by natural forces

Insurance against damage by natural forces I. Summary Insurance against damage by natural forces covers chattels and buildings arising from high water, floods, storm, hail, avalanche, snow pressure, rockslide,

Insurance against damage by natural forces I. Summary Insurance against damage by natural forces covers chattels and buildings arising from high water, floods, storm, hail, avalanche, snow pressure, rockslide,

Supply Chain Risk Offering

Supply Chain Risk Offering 2010 & 2011 Catastrophes Emphasize Supply Chain Vulnerability Iceland Volcano ~ $200 million USD per Day >$5 billion USD total economic loss Japan Earthquake and Tsunami ~ $300

Supply Chain Risk Offering 2010 & 2011 Catastrophes Emphasize Supply Chain Vulnerability Iceland Volcano ~ $200 million USD per Day >$5 billion USD total economic loss Japan Earthquake and Tsunami ~ $300

Adding more detail to Potential Flood Damage Assessment An object based approach

Adding more detail to Potential Flood Damage Assessment An object based approach Student: R.J. Joling Studentnumber: 1871668 Thesis BSc Aarde & Economie Attendant: E. Koomen Vrije Universiteit Amsterdam

Adding more detail to Potential Flood Damage Assessment An object based approach Student: R.J. Joling Studentnumber: 1871668 Thesis BSc Aarde & Economie Attendant: E. Koomen Vrije Universiteit Amsterdam

Catastrophic Risks and Insurance

Catastrophic Risks and Insurance Problems and Perspectives Prof. Alberto Monti Bocconi University, Milan (Italy) Email: alberto.monti@unibocconi.it VI Conference on Insurance Regulation and Supervision

Catastrophic Risks and Insurance Problems and Perspectives Prof. Alberto Monti Bocconi University, Milan (Italy) Email: alberto.monti@unibocconi.it VI Conference on Insurance Regulation and Supervision

Key Issues in Loss Mitigation - Catastrophic Events / Commercial Property Insurance

Key Issues in Loss Mitigation - Catastrophic Events / Commercial Property Insurance Area Business Disaster Recovery Symposium Myrtle Beach Convention Center January 31, 2014 James W. Errico 1 Brief Bio

Key Issues in Loss Mitigation - Catastrophic Events / Commercial Property Insurance Area Business Disaster Recovery Symposium Myrtle Beach Convention Center January 31, 2014 James W. Errico 1 Brief Bio

**READ YOUR INSURANCE POLICY FOR COMPLETE POLICY TERMS AND CONDITIONS**

HOMEOWNERS HO P 002 06 11 IMPORTANT INFORMATION REQUIRED BY THE LOUISIANA DEPARTMENT OF INSURANCE Homeowners Insurance Policy Coverage Disclosure Summary This form is promulgated pursuant to LSA-R.S. 22:1332

HOMEOWNERS HO P 002 06 11 IMPORTANT INFORMATION REQUIRED BY THE LOUISIANA DEPARTMENT OF INSURANCE Homeowners Insurance Policy Coverage Disclosure Summary This form is promulgated pursuant to LSA-R.S. 22:1332

NAR Section by Section Highlights Biggert-Waters Flood Insurance Reform Act of 2012 1

NAR Section by Section Highlights Biggert-Waters Flood Insurance Reform Act of 2012 1 On July 6, 2012, the President signed into law a 5-year reauthorization of the National Flood Insurance Program (NFIP)

NAR Section by Section Highlights Biggert-Waters Flood Insurance Reform Act of 2012 1 On July 6, 2012, the President signed into law a 5-year reauthorization of the National Flood Insurance Program (NFIP)

National Flood Insurance Program (NFIP) Overview A Local Government How to Guide

Overview A Local Government How to Guide") National Flood Insurance Program (NFIP) Overview A Local Government How to Guide William R. Whitson, IMCA-CM Managing Director Local Government Visions, LLC wwwhitson@aol.com Danny Hinson, CFM, FPEM Florida

National Flood Insurance Program (NFIP) Overview A Local Government How to Guide William R. Whitson, IMCA-CM Managing Director Local Government Visions, LLC wwwhitson@aol.com Danny Hinson, CFM, FPEM Florida

Estimating Flood Impacts: A Status Report

: A Status Report Mark P. Berkman 1 and Toby Brown 2 1 The Brattle Group, San Francisco, California, United States; mark.berkman@brattle.com 2 The Brattle Group, San Francisco, California, United States;

: A Status Report Mark P. Berkman 1 and Toby Brown 2 1 The Brattle Group, San Francisco, California, United States; mark.berkman@brattle.com 2 The Brattle Group, San Francisco, California, United States;

Catastrophe Bond Risk Modelling

Catastrophe Bond Risk Modelling Dr. Paul Rockett Manager, Risk Markets 6 th December 2007 Bringing Science to the Art of Underwriting Agenda Natural Catastrophe Modelling Index Linked Securities Parametric

Catastrophe Bond Risk Modelling Dr. Paul Rockett Manager, Risk Markets 6 th December 2007 Bringing Science to the Art of Underwriting Agenda Natural Catastrophe Modelling Index Linked Securities Parametric

32 Contingencies MAR/APR.06

32 Contingencies MAR/APR.06 New Catastrophe Models for Hard Times B Y P A T R I C I A G R O S S I A N D H O W A R D K U N R E U T H E R Driven by the increasing frequency and severity of natural disasters

32 Contingencies MAR/APR.06 New Catastrophe Models for Hard Times B Y P A T R I C I A G R O S S I A N D H O W A R D K U N R E U T H E R Driven by the increasing frequency and severity of natural disasters

GOOD MORNING MR. CHAIRMAN AND MEMBERS OF THE COMMITTEE. I AM BOB HUNTER, DIRCETOR OF INSURANCE FOR CONSUMER FEDERATION OF AMERICA.

GOOD MORNING MR. CHAIRMAN AND MEMBERS OF THE COMMITTEE. I AM BOB HUNTER, DIRCETOR OF INSURANCE FOR CONSUMER FEDERATION OF AMERICA. THE COMMITTEE ASKED FOR COMMENTS ON HOW TO MAKE POST-DISASTER CLAIMS MORE

GOOD MORNING MR. CHAIRMAN AND MEMBERS OF THE COMMITTEE. I AM BOB HUNTER, DIRCETOR OF INSURANCE FOR CONSUMER FEDERATION OF AMERICA. THE COMMITTEE ASKED FOR COMMENTS ON HOW TO MAKE POST-DISASTER CLAIMS MORE

Flood Risk Considerations

CHECKLIST FOR MITIGATING OR AVOIDING FLOOD DAMAGE It may not seem the case, but individuals are not powerless in influencing their potential exposure to catastrophes, such as floods. Property owners have

CHECKLIST FOR MITIGATING OR AVOIDING FLOOD DAMAGE It may not seem the case, but individuals are not powerless in influencing their potential exposure to catastrophes, such as floods. Property owners have

Flooding Fast Facts. flooding), seismic events (tsunami) or large landslides (sometime also called tsunami).

, seismic events (tsunami) or large landslides (sometime also called tsunami).") Flooding Fast Facts What is a flood? Flooding is the unusual presence of water on land to a depth which affects normal activities. Flooding can arise from: Overflowing rivers (river flooding), Heavy rainfall

Flooding Fast Facts What is a flood? Flooding is the unusual presence of water on land to a depth which affects normal activities. Flooding can arise from: Overflowing rivers (river flooding), Heavy rainfall

Town of Hingham. Changes to Flood Insurance Rate Maps and Flood Insurance Costs Frequently Asked Questions

Town of Hingham 1. What is a floodplain? Changes to Flood Insurance Rate Maps and Flood Insurance Costs Frequently Asked Questions A floodplain is an area of land where water collects, pools and flows

Town of Hingham 1. What is a floodplain? Changes to Flood Insurance Rate Maps and Flood Insurance Costs Frequently Asked Questions A floodplain is an area of land where water collects, pools and flows

Preparing for Climate Change: Insurance and Small Business

The Geneva Papers, 2008, 33, (110 116) r 2008 The International Association for the Study of Insurance Economics 1018-5895/08 $30.00 www.palgrave-journals.com/gpp Preparing for Climate Change: Insurance

The Geneva Papers, 2008, 33, (110 116) r 2008 The International Association for the Study of Insurance Economics 1018-5895/08 $30.00 www.palgrave-journals.com/gpp Preparing for Climate Change: Insurance

The Insurance Perspective: Setting the Stage

The Insurance Perspective: Setting the Stage Charles Nyce, PhD Exploring Impediments to a Real Estate Recovery: A Policy Discussion Federal Reserve Bank of Atlanta Center for Real Estate Analytics Property

The Insurance Perspective: Setting the Stage Charles Nyce, PhD Exploring Impediments to a Real Estate Recovery: A Policy Discussion Federal Reserve Bank of Atlanta Center for Real Estate Analytics Property

Affordability of the National Flood Insurance Program: Application to Charleston County, South Carolina

Affordability of the National Flood Insurance Program: Application to Charleston County, South Carolina Wendy Zhao The Wharton School University of Pennsylvania Howard Kunreuther The Wharton School University

Affordability of the National Flood Insurance Program: Application to Charleston County, South Carolina Wendy Zhao The Wharton School University of Pennsylvania Howard Kunreuther The Wharton School University

PART 1: ADUSTING RESIDENTIAL FLOOD CLAIMS UNDER THE NFIP DWELLING POLICY

National Online Flood Adjuster Training Program: The 4-Corners of Flood Insurance Table of Contents Table of Contents Introduction i vi PART 1: ADUSTING RESIDENTIAL FLOOD CLAIMS UNDER THE NFIP DWELLING

National Online Flood Adjuster Training Program: The 4-Corners of Flood Insurance Table of Contents Table of Contents Introduction i vi PART 1: ADUSTING RESIDENTIAL FLOOD CLAIMS UNDER THE NFIP DWELLING

Flood Insurance Essentials

(Examples adapted from materials developed for FEMA/NFIP training for insurance agents.) Flood Insurance Essentials Agent Training for the National Flood Insurance Program The Least You Need to Know Every

(Examples adapted from materials developed for FEMA/NFIP training for insurance agents.) Flood Insurance Essentials Agent Training for the National Flood Insurance Program The Least You Need to Know Every

Elevator Installation for Buildings Located in Special Flood Hazard Areas in accordance with the National Flood Insurance Program

Elevator Installation for Buildings Located in Special Flood Hazard Areas in accordance with the National Flood Insurance Program FEDERAL EMERGENCY MANAGEMENT AGENCY FEDERAL INSURANCE ADMINISTRATION FIA-TB-4

Elevator Installation for Buildings Located in Special Flood Hazard Areas in accordance with the National Flood Insurance Program FEDERAL EMERGENCY MANAGEMENT AGENCY FEDERAL INSURANCE ADMINISTRATION FIA-TB-4

Climate Change,City Change. Climate Change,City Change

Rotterdam Watercity 2035 Climate Change,City Change Climate Change,City Change The Flood: threat of chance? Nico Tillie Hamburg conference Storyline introduction 1.Adaptation Rotterdam Watercity 2035 2.Mitigation

Rotterdam Watercity 2035 Climate Change,City Change Climate Change,City Change The Flood: threat of chance? Nico Tillie Hamburg conference Storyline introduction 1.Adaptation Rotterdam Watercity 2035 2.Mitigation

Using Insurance Catastrophe Models to Investigate the Economics of Climate Change Impacts and Adaptation

Using Insurance Catastrophe Models to Investigate the Economics of Climate Change Impacts and Adaptation Dr Nicola Patmore Senior Research Analyst Risk Management Solutions (RMS) Bringing Science to the

Using Insurance Catastrophe Models to Investigate the Economics of Climate Change Impacts and Adaptation Dr Nicola Patmore Senior Research Analyst Risk Management Solutions (RMS) Bringing Science to the

qeb=^ppl`f^qflk=lc=_ofqfpe=fkprobop= ^ka= qeb=p`lqqfpe=dlsbokjbkq= ^=glfkq=pq^qbjbkq= lk= qeb=molsfpflk=lc=cilla=fkpro^k`b= = = ab`bj_bo=ommu

qeb=^ppl`f^qflk=lc=_ofqfpe=fkprobop= ^ka= qeb=p`lqqfpe=dlsbokjbkq= ^=glfkq=pq^qbjbkq= lk= qeb=molsfpflk=lc=cilla=fkpro^k`b= = = ab`bj_bo=ommu ^_fl=dlsbokjbkq=pq^qbjbkq= = lk=cillafkd=^ka=fkpro^k`b=clo=p`lqi^ka=

qeb=^ppl`f^qflk=lc=_ofqfpe=fkprobop= ^ka= qeb=p`lqqfpe=dlsbokjbkq= ^=glfkq=pq^qbjbkq= lk= qeb=molsfpflk=lc=cilla=fkpro^k`b= = = ab`bj_bo=ommu ^_fl=dlsbokjbkq=pq^qbjbkq= = lk=cillafkd=^ka=fkpro^k`b=clo=p`lqi^ka=

Global Marine Insurance Report. Astrid Seltmann Fact and Figures Committee: Analyst/Actuary, Cefor - The Nordic Association of Marine Insurers, Oslo

Global Marine Insurance Report Astrid Seltmann Fact and Figures Committee: Analyst/Actuary, Cefor - The Nordic Association of Marine Insurers, Oslo Warming up Find a suitable Shakespeare quote! IUMI and

Global Marine Insurance Report Astrid Seltmann Fact and Figures Committee: Analyst/Actuary, Cefor - The Nordic Association of Marine Insurers, Oslo Warming up Find a suitable Shakespeare quote! IUMI and

Changes to the National Flood Insurance Program What to Expect

Changes to the National Flood Insurance Program What to Expect Impact of changes to the NFIP under Homeowner Flood Insurance Affordability Act of 2014 October 2014 Key Priorities FEMA continues to analyze

Changes to the National Flood Insurance Program What to Expect Impact of changes to the NFIP under Homeowner Flood Insurance Affordability Act of 2014 October 2014 Key Priorities FEMA continues to analyze

IPR Workshop 5-24-10 Response to Follow Up Questions Property Insurance

IPR Workshop 5-24-10 Response to Follow Up Questions Property Insurance 1. Provide legal statement on BPA s ability to purchase property insurance. Early in the property insurance evaluation process BPA

IPR Workshop 5-24-10 Response to Follow Up Questions Property Insurance 1. Provide legal statement on BPA s ability to purchase property insurance. Early in the property insurance evaluation process BPA

Reducing Natural Hazard Risks in New Residential Developments

Reducing Natural Hazard Risks in New Residential Developments Dan Sandink, MA, MScPl Manager, Resilient Communities & Research Institute for Catastrophic Loss Reduction CHBA Urban Council Ottawa Oct. 24,

Reducing Natural Hazard Risks in New Residential Developments Dan Sandink, MA, MScPl Manager, Resilient Communities & Research Institute for Catastrophic Loss Reduction CHBA Urban Council Ottawa Oct. 24,

Two messages... Council of Europe. Flood Research

Bonn, 12 May 2003 Insurance and Maladaptation Professor David Crichton University College London Middlesex University, London University of Dundee, Scotland Fellow of the Chartered Insurance Institute

Bonn, 12 May 2003 Insurance and Maladaptation Professor David Crichton University College London Middlesex University, London University of Dundee, Scotland Fellow of the Chartered Insurance Institute

4.14 Netherlands. Interactive flood risk map of a part of the province of Gelderland in the Netherlands. Atlas of Flood Maps

4.14 Netherlands The Netherlands is flood prone for about 60% of its surface. 95 so-called dike-rings protect the polders from being flooded from the North Sea, rivers or lakes. The protection level has

4.14 Netherlands The Netherlands is flood prone for about 60% of its surface. 95 so-called dike-rings protect the polders from being flooded from the North Sea, rivers or lakes. The protection level has

Water Management in the Netherlands

Water Management in the Netherlands Eric Boessenkool Senior Advisor to the Management Board of RIjkswaterstaat Ministry of Infrastructure and the Environment New ministry since end of 2010 Merger of Ministry

Water Management in the Netherlands Eric Boessenkool Senior Advisor to the Management Board of RIjkswaterstaat Ministry of Infrastructure and the Environment New ministry since end of 2010 Merger of Ministry

October 15, 2013. Mayor and Council City of New Westminster 511 Royal Avenue New Westminster, BC V3L 1H9

October 15, 2013 Mayor and Council City of New Westminster 511 Royal Avenue New Westminster, BC V3L 1H9 RE: Business Plan Advancing a Collaborative, Regional Approach to Flood Management in BC s Lower

October 15, 2013 Mayor and Council City of New Westminster 511 Royal Avenue New Westminster, BC V3L 1H9 RE: Business Plan Advancing a Collaborative, Regional Approach to Flood Management in BC s Lower

Benefits and Opportunities of Europa Re Programme for the Insurance Industry

Europa Re 2nd Regional Insurance Conference "New Generation of Insurance Solutions" Benefits and Opportunities of Europa Re Programme for the Insurance Industry KLIME POPOSKI BELGRADE, O CTOBER 2 014 Natural

Europa Re 2nd Regional Insurance Conference "New Generation of Insurance Solutions" Benefits and Opportunities of Europa Re Programme for the Insurance Industry KLIME POPOSKI BELGRADE, O CTOBER 2 014 Natural

Flood Risk Assessment in the Netherlands: A Case Study for Dike Ring South Holland

Risk Analysis, Vol. 28, No. 5, 2008 DOI: 10.1111/j.1539-6924.2008.01103.x Flood Risk Assessment in the Netherlands: A Case Study for Dike Ring South Holland Sebastiaan N. Jonkman, 1,2 Matthijs Kok, 1,3

Risk Analysis, Vol. 28, No. 5, 2008 DOI: 10.1111/j.1539-6924.2008.01103.x Flood Risk Assessment in the Netherlands: A Case Study for Dike Ring South Holland Sebastiaan N. Jonkman, 1,2 Matthijs Kok, 1,3

INSURANCE CHECKLIST #2

INSURANCE CHECKLIST #2 Flood Insurance Proof of Loss and Statute of Limitations Homeowner (Non- Flood) Insurance Proof of Loss and Statute of Limitations Additional Tips This is the second checklist that

INSURANCE CHECKLIST #2 Flood Insurance Proof of Loss and Statute of Limitations Homeowner (Non- Flood) Insurance Proof of Loss and Statute of Limitations Additional Tips This is the second checklist that

Submission on Northern Australia Insurance Premiums Taskforce INTERIM REPORT 2015

16 September 2015 Northern Australia Insurance Premiums Taskforce The Treasury Langton Crescent PARKES ACT 2600 Email: NorthernAustraliaInsurancePremiumsTaskforce@treasury.gov.au Submission on Northern

16 September 2015 Northern Australia Insurance Premiums Taskforce The Treasury Langton Crescent PARKES ACT 2600 Email: NorthernAustraliaInsurancePremiumsTaskforce@treasury.gov.au Submission on Northern

Darja Tretjakova MANAGING FLOOD RISK IN INTERNATIONAL HARBOURS

Darja Tretjakova MANAGING FLOOD RISK IN INTERNATIONAL HARBOURS Outline Origins and reasons Methodology Results Conclusions 2 Why this research? Increasing flood risk: CC, socio-economic development Port

Darja Tretjakova MANAGING FLOOD RISK IN INTERNATIONAL HARBOURS Outline Origins and reasons Methodology Results Conclusions 2 Why this research? Increasing flood risk: CC, socio-economic development Port

STATEMENT BEFORE THE COMMITTEE ON SMALL BUSINESS AND ENTREPRENEURSHIP U.S. SENATE NEW ORLEANS, LA

STATEMENT OF BRAD KIESERMAN DEPUTY ASSOCIATE ADMINISTRATOR FOR INSURANCE FEDERAL INSURANCE AND MITIGATION ADMINISTRATION FEDERAL EMERGENCY MANAGEMENT AGENCY U.S. DEPARTMENT OF HOMELAND SECURITY ROY WRIGHT

STATEMENT OF BRAD KIESERMAN DEPUTY ASSOCIATE ADMINISTRATOR FOR INSURANCE FEDERAL INSURANCE AND MITIGATION ADMINISTRATION FEDERAL EMERGENCY MANAGEMENT AGENCY U.S. DEPARTMENT OF HOMELAND SECURITY ROY WRIGHT

More Changes Coming to the National Flood Insurance Program What to Expect

More Changes Coming to the National Flood Insurance Program What to Expect Impact of changes to the NFIP under Homeowner Flood Insurance Affordability Act of 2014 More Changes are Coming to the NFIP On

More Changes Coming to the National Flood Insurance Program What to Expect Impact of changes to the NFIP under Homeowner Flood Insurance Affordability Act of 2014 More Changes are Coming to the NFIP On

Community Engagement and Cost Benefit Analysis for Sea Level Rise and Storm Surge Adaptation

Community Engagement and Cost Benefit Analysis for Sea Level Rise and Storm Surge Adaptation Methods, Case Studies, and Wetland-specific Opportunities Samuel B. Merrill, Ph.D. December 10, 2012 Muskie

Community Engagement and Cost Benefit Analysis for Sea Level Rise and Storm Surge Adaptation Methods, Case Studies, and Wetland-specific Opportunities Samuel B. Merrill, Ph.D. December 10, 2012 Muskie

Risk Selection and Moral Hazard in Natural Disaster Insurance Markets: Empirical evidence from Germany and the United States

Risk Selection and Moral Hazard in Natural Disaster Insurance Markets: Empirical evidence from Germany and the United States Paul Hudson Department of Environmental Economics, Institute for Environmental

Risk Selection and Moral Hazard in Natural Disaster Insurance Markets: Empirical evidence from Germany and the United States Paul Hudson Department of Environmental Economics, Institute for Environmental

Making flood insurable for Canadian homeowners. by Glenn McGillivray Managing Director, Institute for Catastrophic Loss Reduction

Making flood insurable for Canadian homeowners by Glenn McGillivray Managing Director, Institute for Catastrophic Loss Reduction Insurance Institute of Ontario, Conestoga Chapter Annual Speakers Luncheon

Making flood insurable for Canadian homeowners by Glenn McGillivray Managing Director, Institute for Catastrophic Loss Reduction Insurance Institute of Ontario, Conestoga Chapter Annual Speakers Luncheon

Louisiana: Bulletin No. 06-06 Commercial and Homeowners Insurance Disclosure Forms. Bulletin No. 06-06 and disclosure forms attached there-in

market bulletin From Director, Worldwide Markets (extn 6863) Date 26 January 2007 Reference Subject Subject areas Attachments Action points Y3963 Louisiana: Bulletin No. 06-06 Commercial and Homeowners

market bulletin From Director, Worldwide Markets (extn 6863) Date 26 January 2007 Reference Subject Subject areas Attachments Action points Y3963 Louisiana: Bulletin No. 06-06 Commercial and Homeowners

Natural Perils Insurance without Equal. 18 october 2011

Natural Perils Insurance without Equal 18 october 2011 2 Imprint Recipients: Interested parties within and outside the insurance industry Published by: Swiss Insurance Association SIA Conrad-Ferdinand-Meyer-Strasse

Natural Perils Insurance without Equal 18 october 2011 2 Imprint Recipients: Interested parties within and outside the insurance industry Published by: Swiss Insurance Association SIA Conrad-Ferdinand-Meyer-Strasse

The Role of the Insurance Industry

The Role of the Insurance Industry Prof. Dr. Peter Hoeppe Geo Risks Research Munich Reinsurance Company ECF Annual Conference, Berlin, 27 March 2007 The Insurance Industry as an Early Alerter to Global

The Role of the Insurance Industry Prof. Dr. Peter Hoeppe Geo Risks Research Munich Reinsurance Company ECF Annual Conference, Berlin, 27 March 2007 The Insurance Industry as an Early Alerter to Global

HOMEOWNER FLOOD INSURANCE AFFORDABILITY ACT KEY PROVISIONS OF SENATE AND HOUSE MEASURES

Pre-FIRM Properties 1 actuarial costs Pushes pre-firm subsidized primary residences to full risk rates upon sale or lapse of policy years annual premium insurance rate increases associated with the sale

Pre-FIRM Properties 1 actuarial costs Pushes pre-firm subsidized primary residences to full risk rates upon sale or lapse of policy years annual premium insurance rate increases associated with the sale

GUIDANCE FOR SEVERE REPETITIVE LOSS PROPERTIES

Previous Section Main Menu Table of Contents Next Section GUIDANCE FOR SEVERE REPETITIVE LOSS PROPERTIES I. GENERAL DESCRIPTION The primary objective of the Severe Repetitive Loss (SRL) properties strategy

Previous Section Main Menu Table of Contents Next Section GUIDANCE FOR SEVERE REPETITIVE LOSS PROPERTIES I. GENERAL DESCRIPTION The primary objective of the Severe Repetitive Loss (SRL) properties strategy

Floodplain Information

Floodplain Information A large percentage of the Ellis community is located in the floodplain of Big Creek. The term floodplain means the low-lying areas on both sides of Big Creek that will be covered

Floodplain Information A large percentage of the Ellis community is located in the floodplain of Big Creek. The term floodplain means the low-lying areas on both sides of Big Creek that will be covered

Flood Insurance. NFIP Flood Insurance

Flood Insurance 11 Flood insurance is essential in helping people repair, recover, rebuild, and even install some retrofitting measures. Flood insurance has many advantages, especially for people in areas

Flood Insurance 11 Flood insurance is essential in helping people repair, recover, rebuild, and even install some retrofitting measures. Flood insurance has many advantages, especially for people in areas

Business Continuity and Disaster Recovery Planning: A Collaborative Approach. Dr. Gillian Cambers, Disaster Risk Management Specialist, CDB

Business Continuity and Disaster Recovery Planning: A Collaborative Approach Dr. Gillian Cambers, Disaster Risk Management Specialist, CDB Regional Workshop for Health Planners and Policy Makers, September

Business Continuity and Disaster Recovery Planning: A Collaborative Approach Dr. Gillian Cambers, Disaster Risk Management Specialist, CDB Regional Workshop for Health Planners and Policy Makers, September

Indemnity based Nat Cat insurance covers for sovereign risks Example: FONDEN, Mexico

Indemnity based Nat Cat insurance covers for sovereign risks Example: FONDEN, Mexico Workshop World Bank / Munich Re Washington: 23 April 2013 Dott. Ing. Paolo Bussolera Head of Claims - Europe and Latin

Indemnity based Nat Cat insurance covers for sovereign risks Example: FONDEN, Mexico Workshop World Bank / Munich Re Washington: 23 April 2013 Dott. Ing. Paolo Bussolera Head of Claims - Europe and Latin

Flood Insurance Rating: Facts and Factors. Jana Green, CFM 2013 NJAFM Annual Conference October 17, 2013 Concurrent Session #3

Flood Insurance Rating: Facts and Factors Jana Green, CFM 2013 NJAFM Annual Conference October 17, 2013 Concurrent Session #3 Purpose of Presentation THIS PRESENTATION IS INTENDED TO PROVIDE: A clear and

Flood Insurance Rating: Facts and Factors Jana Green, CFM 2013 NJAFM Annual Conference October 17, 2013 Concurrent Session #3 Purpose of Presentation THIS PRESENTATION IS INTENDED TO PROVIDE: A clear and

Flooding in London A London Assembly Scrutiny Report Follow up review Submission by Association of British Insurers (revised April 2004)

") Flooding in London A London Assembly Scrutiny Report Follow up review Submission by Association of British Insurers (revised April 2004) 1. The Association of British Insurers (ABI) is the trade association

Flooding in London A London Assembly Scrutiny Report Follow up review Submission by Association of British Insurers (revised April 2004) 1. The Association of British Insurers (ABI) is the trade association

Flood insurance why have it? Where can I buy it?

Flood insurance why have it? Where can I buy it? NOAA/National Weather Service Des Moines, Iowa June 2010 Thank you for your interest in flood insurance. Below are frequently asked questions and answers

Flood insurance why have it? Where can I buy it? NOAA/National Weather Service Des Moines, Iowa June 2010 Thank you for your interest in flood insurance. Below are frequently asked questions and answers

National Flood Insurance Program Summary of Coverage

National Flood Insurance Program Summary of Coverage FEMA F-679 / November 2012 This document was prepared by the National Flood Insurance Program (NFIP) to help you understand your flood insurance policy.

National Flood Insurance Program Summary of Coverage FEMA F-679 / November 2012 This document was prepared by the National Flood Insurance Program (NFIP) to help you understand your flood insurance policy.

Avoiding Errors & Omissions In Flood Insurance

Avoiding Errors & Omissions In Flood Insurance Moderator: M. Rita Hollada, CPCU, CIC, CPIA Sally Combs, Technical Director, Professional Liability Claims, Fireman s Fund Ins. Co. Patrice Collingwood, Senior

Avoiding Errors & Omissions In Flood Insurance Moderator: M. Rita Hollada, CPCU, CIC, CPIA Sally Combs, Technical Director, Professional Liability Claims, Fireman s Fund Ins. Co. Patrice Collingwood, Senior

Flood Insurance Premium Increases And Increased Cost of Compliance Eligibility

Flood Insurance Premium Increases And Increased Cost of Compliance Eligibility January 11, 2015 (This document is updated frequently, so please consult the most recent edition) Margaret Becker Director

Flood Insurance Premium Increases And Increased Cost of Compliance Eligibility January 11, 2015 (This document is updated frequently, so please consult the most recent edition) Margaret Becker Director

Panel 4: Flood insurance and adaptation: What can the US and EU learn from each other? Flood Insurance: Comparison of the US and UK

Panel 4: Flood insurance and adaptation: What can the US and EU learn from each other? Flood Insurance: Comparison of the US and UK Michael McShane, Old Dominion University Diane Horn, Birkbeck College,

Panel 4: Flood insurance and adaptation: What can the US and EU learn from each other? Flood Insurance: Comparison of the US and UK Michael McShane, Old Dominion University Diane Horn, Birkbeck College,

FLOOD HAZARD MANAGEMENT SPECIFIC PLAN GUIDELINES

INFORMATION BULLETIN / PUBLIC - BUILDING CODE REFERENCE NO.: L.A. Ordinance 172081 Effective: 01-01-2014 DOCUMENT NO.: P/BC 2014-064 Revised: Previously Issued As: P/BC 2011-064 FLOOD HAZARD MANAGEMENT

INFORMATION BULLETIN / PUBLIC - BUILDING CODE REFERENCE NO.: L.A. Ordinance 172081 Effective: 01-01-2014 DOCUMENT NO.: P/BC 2014-064 Revised: Previously Issued As: P/BC 2011-064 FLOOD HAZARD MANAGEMENT

Please see Section IX. for Additional Information:

The Florida Senate BILL ANALYSIS AND FISCAL IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) BILL: CS/SB 1094 Prepared By: The

The Florida Senate BILL ANALYSIS AND FISCAL IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) BILL: CS/SB 1094 Prepared By: The

Climate change & the insurance industry. Cheuvreux Financials Conference, London, 1 & 2 December 2009

Climate change & the insurance industry Cheuvreux Financials Conference, London, 1 & 2 December 2009 Climate change A global threat to the insurance industry Weather conditions have become more extreme

Climate change & the insurance industry Cheuvreux Financials Conference, London, 1 & 2 December 2009 Climate change A global threat to the insurance industry Weather conditions have become more extreme

FLOODS ARE THE #1 NATURAL DISASTER IN THE UNITED STATES.

F-671 (10-12) Here is the National Flood Insurance Guide that you requested. This brochure will not only show you how to purchase flood insurance, it will also show you how to protect your home or business

F-671 (10-12) Here is the National Flood Insurance Guide that you requested. This brochure will not only show you how to purchase flood insurance, it will also show you how to protect your home or business

Climate Change and Infrastructure Planning Ahead

Climate Change and Infrastructure Planning Ahead Climate Change and Infrastructure Planning Ahead Infrastructure the physical facilities that support our society, such as buildings, roads, railways, ports

Climate Change and Infrastructure Planning Ahead Climate Change and Infrastructure Planning Ahead Infrastructure the physical facilities that support our society, such as buildings, roads, railways, ports

Climate Change and resilience building: a reinsurer's perspective. Southeast Florida Regional Climate Leadership Summit

Climate Change and resilience building: a reinsurer's perspective Southeast Florida Regional Climate Leadership Summit The cost of disasters is widening along with the gap between uninsured and insured

Climate Change and resilience building: a reinsurer's perspective Southeast Florida Regional Climate Leadership Summit The cost of disasters is widening along with the gap between uninsured and insured

Agent Guide to Flood Insurance. Have a flair for selling flood? This guide will make it even easier

Agent Guide to Flood Insurance Have a flair for selling flood? This guide will make it even easier Growth! That s what selling flood insurance can mean for your business. But selling and servicing flood

Agent Guide to Flood Insurance Have a flair for selling flood? This guide will make it even easier Growth! That s what selling flood insurance can mean for your business. But selling and servicing flood

Flood Insurance IV. Frequently Asked Questions

Flood Insurance IV. Frequently Asked Questions Frequently Asked Questions - Determination When is a bank required to get a new determination? Part 339 requires that each time a bank makes, increases, extends,

Flood Insurance IV. Frequently Asked Questions Frequently Asked Questions - Determination When is a bank required to get a new determination? Part 339 requires that each time a bank makes, increases, extends,

Please see Section IX. for Additional Information:

The Florida Senate BILL ANALYSIS AND FISCAL IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) BILL: CS/SB 1094 Prepared By: The

The Florida Senate BILL ANALYSIS AND FISCAL IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) BILL: CS/SB 1094 Prepared By: The

Cost benefit analysis and flood damage mitigation in the Netherlands

Cost benefit analysis and flood damage mitigation in the Netherlands M.Brinkhuis-Jak & S.R. Holterman Road and Hydraulic Engineering Institute; Ministry of Transport, Public Works and Water Management

Cost benefit analysis and flood damage mitigation in the Netherlands M.Brinkhuis-Jak & S.R. Holterman Road and Hydraulic Engineering Institute; Ministry of Transport, Public Works and Water Management

Reducing Flood Risk to Residential Buildings That Cannot Be Elevated

Reducing Flood Risk to Residential Buildings That Cannot Be Elevated FEMA P-1037 / September 2015 Elevated utility readable from standing height ~6.5' above grade Basement infill with gravel Approximate

Reducing Flood Risk to Residential Buildings That Cannot Be Elevated FEMA P-1037 / September 2015 Elevated utility readable from standing height ~6.5' above grade Basement infill with gravel Approximate

Flood Insurance Repetitive Loss Property

Flood Insurance Repetitive Loss Property When our system of canals, ditches and culverts was built over 20 years ago, it could handle all but the largest tropical storms and hurricanes; since then, urban

Flood Insurance Repetitive Loss Property When our system of canals, ditches and culverts was built over 20 years ago, it could handle all but the largest tropical storms and hurricanes; since then, urban

Flood Damage Mitigation And Insurance Costs

Flood Damage Mitigation And Insurance Costs Friday, September 25, 2015 at 7:00 PM Saturday, September 26, 2015 at 10:00 AM This presentation was prepared by the Town of South Bethany using Federal Funds

Flood Damage Mitigation And Insurance Costs Friday, September 25, 2015 at 7:00 PM Saturday, September 26, 2015 at 10:00 AM This presentation was prepared by the Town of South Bethany using Federal Funds

Discussion about the practicability of implementing flood risk. management and urban flood insurance in China. Longhua Gao, Xiaoqing Zhou

Discussion about the practicability of implementing flood risk management and urban flood insurance in China Longhua Gao, Xiaoqing Zhou Abstract: This paper explains the flood risk management at first,

Discussion about the practicability of implementing flood risk management and urban flood insurance in China Longhua Gao, Xiaoqing Zhou Abstract: This paper explains the flood risk management at first,

Changes to the National Flood Insurance Program What to Expect

Changes to the National Flood Insurance Program What to Expect Impact of changes to the NFIP under Homeowner Flood Insurance Affordability Act of 2014 More Changes are Coming to the NFIP On March 21, 2014,

Changes to the National Flood Insurance Program What to Expect Impact of changes to the NFIP under Homeowner Flood Insurance Affordability Act of 2014 More Changes are Coming to the NFIP On March 21, 2014,

limate Change, SIDS and Insurance ick Silver NFCC Expert Meeting on Adaptation for SIDS arotonga, Cook Islands 26-28 February 2007

limate Change, SIDS and Insurance ick Silver NFCC Expert Meeting on Adaptation for SIDS arotonga, Cook Islands 26-28 February 2007 Issues for further consideration (c) Is insurance the most suitable mechanism

limate Change, SIDS and Insurance ick Silver NFCC Expert Meeting on Adaptation for SIDS arotonga, Cook Islands 26-28 February 2007 Issues for further consideration (c) Is insurance the most suitable mechanism

UNFCCC expert meeting on loss and damage 9 11 November, 2012 Barbados pcrafi.sopac.org

Disaster Risk Assessment Tools and Applications UNFCCC expert meeting on loss and damage 9 11 November, 2012 Barbados pcrafi.sopac.org Main Outputs Pacific disaster risk assessment Probabilistic assessment

Disaster Risk Assessment Tools and Applications UNFCCC expert meeting on loss and damage 9 11 November, 2012 Barbados pcrafi.sopac.org Main Outputs Pacific disaster risk assessment Probabilistic assessment

Disaster Ready. By: Katie Tucker, Sales Representative, Rolyn Companies, Inc

By: Katie Tucker, Sales Representative, Rolyn Companies, Inc Are you and your facility disaster ready? As reported by the Red Cross, as many as 40 percent of small businesses do not reopen after a major

By: Katie Tucker, Sales Representative, Rolyn Companies, Inc Are you and your facility disaster ready? As reported by the Red Cross, as many as 40 percent of small businesses do not reopen after a major

SUBSIDIZING RISK: THE REGRESSIVE AND COUNTERPRODUCTIVE NATURE OF NATIONAL FLOOD INSURANCE RATE SETTING IN MASSACHUSETTS

PPC Working Paper Series- Working Paper No. ENV-2015-01 SUBSIDIZING RISK: THE REGRESSIVE AND COUNTERPRODUCTIVE NATURE OF NATIONAL FLOOD INSURANCE RATE SETTING IN MASSACHUSETTS June, 2015 Chad McGuire Associate

PPC Working Paper Series- Working Paper No. ENV-2015-01 SUBSIDIZING RISK: THE REGRESSIVE AND COUNTERPRODUCTIVE NATURE OF NATIONAL FLOOD INSURANCE RATE SETTING IN MASSACHUSETTS June, 2015 Chad McGuire Associate

Mortgage lending and flood insurance in Poland

Mortgage lending and flood insurance in Poland 2011 Agenda 1. General information on mortgage lending in Poland 2. Mortgage lendings and insurance 3. Polish flood exposure 4. Recent Polish major floods

Mortgage lending and flood insurance in Poland 2011 Agenda 1. General information on mortgage lending in Poland 2. Mortgage lendings and insurance 3. Polish flood exposure 4. Recent Polish major floods

TESTIMONY JACQUES E. DUBOIS CHAIRMAN AND CEO, SWISS RE AMERICA HOLDING ON BEHALF OF SWISS RE BEFORE

TESTIMONY OF JACQUES E. DUBOIS CHAIRMAN AND CEO, SWISS RE AMERICA HOLDING ON BEHALF OF SWISS RE BEFORE THE UNITED STATES SENATE COMMITTEE ON BANKING, HOUSING AND URBAN AFFAIRS OVERSIGHT OF THE TERRORISM

TESTIMONY OF JACQUES E. DUBOIS CHAIRMAN AND CEO, SWISS RE AMERICA HOLDING ON BEHALF OF SWISS RE BEFORE THE UNITED STATES SENATE COMMITTEE ON BANKING, HOUSING AND URBAN AFFAIRS OVERSIGHT OF THE TERRORISM

Intercona Re - Nestlé s Captive. The successful use of a captive as a loss prevention enabler

Intercona Re - Nestlé s Captive The successful use of a captive as a loss prevention enabler Andrew R. Bradley Head of Group Risk Services, Nestec Ltd and CEO of Intercona Re Our World 2 Our ambition Enhancing

Intercona Re - Nestlé s Captive The successful use of a captive as a loss prevention enabler Andrew R. Bradley Head of Group Risk Services, Nestec Ltd and CEO of Intercona Re Our World 2 Our ambition Enhancing