Chap 3 CAPM, Arbitrage, and Linear Factor Models

|

|

|

- Kerry Terry

- 10 years ago

- Views:

Transcription

1 Chap 3 CAPM, Arbitrage, and Linear Factor Models 1

2 Asset Pricing Model a logical extension of portfolio selection theory is to consider the equilibrium asset pricing consequences of investors individually rational actions. The portfolio choices of individual investors represent their particular demands for assets. By aggregating these investor demands and equating them to asset supplies, equilibrium asset prices can be determined. 2

3 CAPM Capital Asset Pricing Model (CAPM), was derived at about the same time by four individuals: Jack Treynor William Sharpe John Lintner Jan Mossin. CAPM predicts that assets risk premia result from a single risk factor, the returns on the market portfolio of all risky assets which, in equilibrium, is a mean variance efficient portfolio. 3

4 William Forsyth Sharpe (born June 16, 1934) is William Sharpe the STANCO 25 Professor of Finance, Emeritus at Stanford University's Graduate School of Business and the winner of the 1990 Nobel Memorial Prize in Economic Sciences. He was one of the originators of the Capital Asset Pricing Model, created the Sharpe ratio for risk adjusted investment performance analysis, contributed to the development of the binomial method for the valuation of options, the gradient method for asset allocation optimization, and returns based style analysis for evaluating the style and performance of investment funds. 4

5 Arbitrage Pricing Model it is not hard to imagine that a weakening of CAPM s restrictive assumptions could generate risk premia deriving from multiple factors. We derive this relationship not based on a model of investor preferences as was done in deriving CAPM but based on the concept that competitive and efficient securities markets should not permit arbitrage. 5

6 Arbitrage Pricing Model Arbitrage pricing is the primary technique for valuing one asset in terms of another. (Relative Pricing) It is the basis of so called relative pricing models, contingent claims models, or derivative pricing models. study the multifactor Arbitrage Pricing Theory (APT) developed by Stephen Ross (Ross 1976). 6

7 Stephen A. Ross Stephen A. Ross is the Franco Modigliani Professor of Financial Economics and a Professor of Finance at the MIT Sloan School of Management. Ross is best known for the development of the arbitrage pricing theory (mid 1970s) as well as for his role in developing the binomial options pricing model (1979; also known as the Cox Ross Rubinstein model). He was an initiator of the fundamental financial concept of risk neutral pricing. 7

as well as for his role in")

8 CAPM It does assume that investors have identical beliefs regarding the probability distribution of asset returns all risky assets can be traded there are no indivisibilities in asset holdings there are no limits on borrowing or lending at the riskfree rate. does not assume a representative investor in the sense of requiring all investors to have identical utility functions or beginning of period wealth. 8

9 CAPM 9

10 10

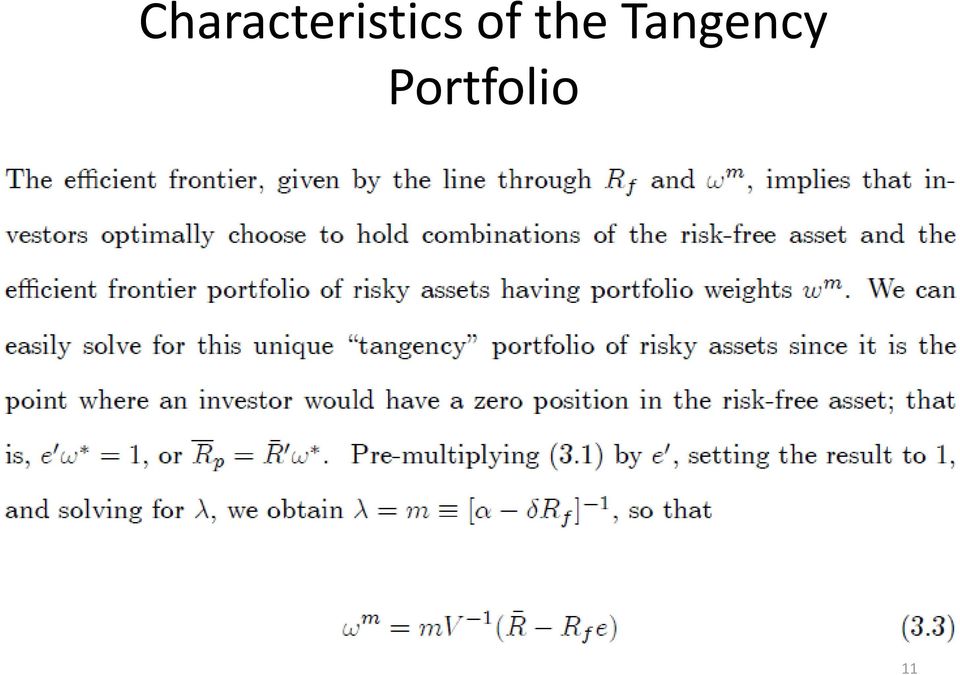

11 Characteristics of the Tangency Portfolio 11

12 covariance between the tangency portfolio and the individual risky assets. 12

13 a simple relationship links the excess expected to the excess expected returns on the individual risky assets 13

14 Asset Demand suppose that individual investors, each taking the set of individual assets expected returns and covariances as fixed (exogenous), all choose mean variance efficient portfolios. Thus, each investor decides to allocate his or her wealth between the risk free asset and the unique tangency portfolio. Because individual investors demand the risky assets in the same relative proportions, we know that the aggregate demands for the risky assets will have the same relative proportions, namely, those of the tangency portfolio. 14

15 Assets Supply Fixed Supply One way to model asset supplies is to assume they are fixed. For example, the economy could be characterized by a fixed quantity of physical assets that produce random output at the end of the period. Such an economy is often referred to as an endowment economy, and we detail a model of this type in Chapter 6. In this case, equilibrium occurs by adjustment of the date 0 assets prices so that investors demands conform to the inelastic assets supplies. 15

16 Assets Supply Variable Supply to assume that the economy s asset return distributions are fixed but allow the quantities of these assets to be elastically supplied. This type of economy is known as a production economy, and a model of it is presented in Chapter

17 Assets Supply Variable Supply Such a model assumes that there are n risky, constant returns to scale technologies. These technologies require date 0 investments of physical capital and produce end of period physical investment returns having a distribution with mean and covariance matrix of V at the end of the period. there could be a risk free technology that generates a one period return on physical capital of. In this case of a fixed return distribution, supplies of the assets adjust to the demands for the tangency portfolio and the risk free asset determined by the technological return distribution. As it turns out, how one models asset supplies does not affect the results that we now derive regarding the equilibrium relationship between asset returns. 17

18 In Equilibrium Demand= Supply 18

19 Market Portfolio Weight in Equilibrium In equilibrium, the tangency portfolio chosen by all investors must be the market portfolio of all risky assets. the tangency portfolio having weights must be the equilibrium portfolio of risky assets supplied in the market. (3.6) is an equilibrium relationship between the excess expected return on any asset and the excess expected return on the market portfolio. 19

20 The only case for which investors have a long position in the tangency portfolio is Rf < Rmv. for asset markets to clear, that is, for the outstanding stocks of assets to be owned by investors, the situation depicted in Figure 3.1 can be the only equilibrium efficient frontier 20

21 21

22 Market Portfolio Weight in Equilibrium Can market portfolio weight in equilibrium negative? No since assets must have nonnegative supplies, equilibrium market clearing implies that assets prices or individuals choice of technologies must adjust (effectively changing R and/or V ) to make the portfolio demands for individual assets nonnegative. 22

23 implications of CAPM we consider realized, rather than expected, asset returns. 23

24 24

25 OLS estimation 25

26 Capital Market Line 26

27 27

28 28

29 The Expression and Implication of CAPM The essence of CAPM is that the expected return on any asset is a positive linear function of its beta and that beta is the only measure of risk needed to explain the crosssectionofexpectedreturns. The spirit of CAPM is. No, no CAPM.

30 Fama MacBeth Approach The basic idea of the approach is the use of a time series (first pass) regression to estimate betas and the use of a cross sectional (second pass) regression to test the hypothesis derived from the CAPM.

31 Fama MacBeth Approach Step1(First Pass Regression): For each of the N securities included in the sample, we first run the following regression over time to estimate beta: R it i R i mt i (1) Step2(Second Pass Regression) We run the following cross section regression over the sample period over the N securities: R it 2 ˆ ˆ ˆ ˆ 3 0 t 1t i 2 t i t ei it S (2)

32 Fama MacBeth Approach ˆ3 should not be significantly different from zero, or residual risk does not affect return. ˆ2 should not be significantly different from zero, or the expected return on any asset is a positive linear function of its beta. ˆ1 must be more than zero: there is a positive price of risk in the capital markets, namely, a positive relationship exists between systematic risk and expected return.

33 Zero Beta CAPM If a riskless asset does not exist so that all assets are risky, Fischer Black (Black 1972) showed that a similar asset pricing relationship exists. But with respect to the expected return on the portfolio that has zero covariance with the market portfolio Zero beta portfolio Derivation: see the textbook 33

34 Fischer Black Fischer Sheffey Black (January 11, 1938 August 30, 1995) was an American economist, best known as one of the authors of the famous Black Scholes equation. 34

35 Zero Beta CAPM 35

36 Arbitrage It involves the possibility of getting something for nothing while having no possibility of loss. A more mathematical interpretation will be given in Shreve Chap 5 36

37 Arbitrage Specifically, consider constructing a portfolio involving both long and short positions in assets such that no initial wealth is required to form the portfolio. Proceeds from short sales (or borrowing) are used to purchase (take long positions in) other assets. If this zero net investment portfolio can sometimes produce a positive return but can never produce a negative return, then it represents an arbitrage: starting from zero wealth, a profit can sometimes be made but a loss can never occur. 37

38 Arbitrage A special case of arbitrage is when this zeronet investment portfolio produces a riskless return. If this certain return is positive (negative), an arbitrage is to buy (sell ) the portfolio and reap a riskless profit, or free lunch. Only if the return is zero would there be no arbitrage. 38

39 Arbitrage Opportunity If a portfolio that requires a nonzero initial net investment is created such that it earns a certain rate of return, then this rate of return must equal the current (competitive market) risk free interest rate. Otherwise, there would also be an arbitrage opportunity. 39

40 Arbitrage Opportunity For example, if the portfolio required a positive initial investment but earned less than the risk free rate an arbitrage would be to (short ) sell the portfolio and invest the proceeds at the riskfree rate, thereby earning a riskless profit equal to the difference between the risk free rate and the portfolio s certain (lower) rate of return. 40

41 Arbitrage Opportunity In efficient, competitive, asset markets where arbitrage trades are feasible, it is reasonable to think that arbitrage opportunities are rare and fleeting. Should arbitrage temporarily exist, then trading by investors to earn this profit will tend to move asset prices in a direction that eliminates the arbitrage opportunity. it may be reasonable to assume that equilibrium asset prices reflect an absence of arbitrage opportunities. 41

42 No Arbitrage and Law of One Price No arbitrage assumption leads to a law of one price If different assets produce exactly the same future payoffs, then the current prices of these assets must be the same. This simple result has powerful asset pricing implications. 42

43 limited arbitrage For some markets, it may be impossible to execute pure arbitrage trades due to significant transactions costs and/or restrictions on short selling or borrowing. Andrei Shleifer and Robert Vishny (Shleifer and Vishny 1997) discuss why the conditions needed to apply arbitrage pricing are not present in many asset markets. 43

44 The link bet. CAPM and APT To motivate how arbitrage pricing might apply to a very simple version of the CAPM, suppose that there is a risk free asset that returns Rf and multiple risky assets. 44

45 The link bet. CAPM and APT 45

46 The link bet. CAPM and APT 46

47 The link bet. CAPM and APT This condition states that the expected return in excess of the risk free rate, per unit of risk, must be equal for all assets, and we define this ratio as λ. Thus, this no arbitrage condition is really a law of one price in that the price of risk, λ, which 47 is the risk premium divided by the quantity of risk, must be the same for all assets.

48 The link bet. CAPM and APT 48

49 CAPM is not reasonable The CAPM assumption that all assets can be held by all individual investors is clearly an oversimplification. Transactions costs and other trading "frictions that arise from distortions such as capital controls and taxes might prevent individuals from holding a global portfolio of marketable assets. many assets simply are nonmarketable and cannot be traded. the CAPM s prediction that risk from a market portfolio is the only source of priced risk has not received strong empirical support. 49

50 CAPM is not reasonable Roll s Critique Richard Roll (Roll 1977) has argued that CAPM is not a reasonable theory, because A true "market" portfolio consisting of all risky assets cannot be observed or owned by investors. Moreover, empirical tests of CAPM are infeasible because proxies for the market portfolio (such as the S&P500 stock index) may not be mean variance efficient, even if the true market portfolio is. Conversely, a proxy for the market portfolio could be mean variance efficient even though the true market portfolio is not. 50

51 motivation for the Multifactor APT model. APT assumes that an individual asset s return is driven by multiple risk factors and by an idiosyncratic component. APT is a relative pricing model in the sense that it determines the risk premia on all assets relative to the risk premium for each of the factors and each asset s sensitivity to each factor. No assumptions regarding investor preferences but uses arbitrage pricing to restrict an asset s risk premium. The main assumptions of the model are that the returns on all assets are linearly related to a finite number of risk factors and the number of assets in the economy is large relative to the number of factors. 51

52 52

53 53

54 How to hedge away asset s idiosyncratic risk we will argue that if the number of assets is large, a portfolio can be constructed that has "close" to a riskless return, because the idiosyncratic components of assets returns are diversifiable. we can use the notion of asymptotic arbitrage to argue that assets expected returns will be "close" to the relationship that would result if they had no idiosyncratic risk. 54

55 Asymptotic Arbitrage an asymptotic arbitrage exists if the following conditions hold The portfolio requires zero net investment The portfolio return becomes certain as n gets large The portfolio s expected return is always bounded above zero 55

56 56

57 APT 57

58 APT 58

59 APT Proof: See the textbook 59

60 APT We see that APT, given by the relation can be interpreted as a multi beta generalization of CAPM. CAPM says that its single beta should be the sensitivity of an asset s return to that of the market portfolio 60

61 APT and ICAPM Robert Merton s Intertemporal Capital Asset Pricing Model (ICAPM) (Merton 1973a) A multi beta asset pricing model the ICAPM is sometimes used to justify the APT the static (single period) APT framework may not be compatible with some of the predictions of the more dynamic (multiperiod) ICAPM. 61

62 Robert C. Merton Robert C. Merton (born 31 July 1944) is an American economist, Nobel laureate in Economics, and professor at the MIT Sloan School of Management, known for his pioneering contributions to continuous time finance, especially the first continuous time option pricing model, the Black Scholes Merton formula. 62

63 APT and ICAPM In general, the ICAPM allows for changing riskfree rates and predicts that assets expected returns should be a function of such changing investment opportunities. The ICAPM model also predicts that an asset s multiple betas are unlikely to remain constant through time, which can complicate deriving estimates of betas from historical data. 63

64 APT APT gives no guidance as to what are the economy s multiple underlying risk factors. An empirical application of APT by Nai Fu Chen, Richard Roll, and Stephen Ross (Chen, Roll, and Ross 1986) assumed that The risk factors were macroeconomic in nature, as proxied by industrial production, expected and unexpected inflation, the spread between long and short maturity interest rates, and the spread between high and low credit quality bonds. 64

65 Other models Other researchers have tended to select risk factors based on those that provide the best fit to historical asset returns. The well known Eugene Fama and Kenneth French (Fama and French 1993) model is an example of this. 65

66 Fama and French (1993) Its risk factors are returns on three different portfolios: a market portfolio of stocks (like CAPM), a portfolio that is long the stocks of small firms and short the stocks of large firms, and a portfolio that is long the stocks having high book tomarket ratios (value stocks) and short stocks having low book tomarket ratios (growth stocks). The Fama French model predicts that a given stock s expected return is determined by its three betas for these three portfolios. lacking a theoretical foundation for its risk factors. 66

67 Fama and French Eugene Francis "Gene" Fama (born February 14, 1939) is an American economist, known for his work on portfolio theory and asset pricing, both theoretical and empirical. He is currently Robert R. McCormick Distinguished Service Professor of Finance at the University of Chicago Booth School of Business. Kenneth Ronald "Ken" French (born March 10, 1954) is the Carl E. and Catherine M. Heidt Professor of Finance at the Tuck School of Business, Dartmouth College. He has previously been a faculty member at MIT, the Yale School of Management, and the University of Chicago Booth School of Business. He is most famous for his work on asset pricing with Eugene Fama. 67

68 Theoretical Foundation The theoretical foundation for factor models is still a on going research 68

CAPM, Arbitrage, and Linear Factor Models

CAPM, Arbitrage, and Linear Factor Models CAPM, Arbitrage, Linear Factor Models 1/ 41 Introduction We now assume all investors actually choose mean-variance e cient portfolios. By equating these investors

CAPM, Arbitrage, and Linear Factor Models CAPM, Arbitrage, Linear Factor Models 1/ 41 Introduction We now assume all investors actually choose mean-variance e cient portfolios. By equating these investors

Black Scholes Merton Approach To Modelling Financial Derivatives Prices Tomas Sinkariovas 0802869. Words: 3441

Black Scholes Merton Approach To Modelling Financial Derivatives Prices Tomas Sinkariovas 0802869 Words: 3441 1 1. Introduction In this paper I present Black, Scholes (1973) and Merton (1973) (BSM) general

Black Scholes Merton Approach To Modelling Financial Derivatives Prices Tomas Sinkariovas 0802869 Words: 3441 1 1. Introduction In this paper I present Black, Scholes (1973) and Merton (1973) (BSM) general

Lecture 6: Arbitrage Pricing Theory

Lecture 6: Arbitrage Pricing Theory Investments FIN460-Papanikolaou APT 1/ 48 Overview 1. Introduction 2. Multi-Factor Models 3. The Arbitrage Pricing Theory FIN460-Papanikolaou APT 2/ 48 Introduction

Lecture 6: Arbitrage Pricing Theory Investments FIN460-Papanikolaou APT 1/ 48 Overview 1. Introduction 2. Multi-Factor Models 3. The Arbitrage Pricing Theory FIN460-Papanikolaou APT 2/ 48 Introduction

Black-Scholes-Merton approach merits and shortcomings

Black-Scholes-Merton approach merits and shortcomings Emilia Matei 1005056 EC372 Term Paper. Topic 3 1. Introduction The Black-Scholes and Merton method of modelling derivatives prices was first introduced

Black-Scholes-Merton approach merits and shortcomings Emilia Matei 1005056 EC372 Term Paper. Topic 3 1. Introduction The Black-Scholes and Merton method of modelling derivatives prices was first introduced

Models of Risk and Return

Models of Risk and Return Aswath Damodaran Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

Models of Risk and Return Aswath Damodaran Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

Portfolio Performance Measures

Portfolio Performance Measures Objective: Evaluation of active portfolio management. A performance measure is useful, for example, in ranking the performance of mutual funds. Active portfolio managers

Portfolio Performance Measures Objective: Evaluation of active portfolio management. A performance measure is useful, for example, in ranking the performance of mutual funds. Active portfolio managers

FINANCIAL ECONOMICS OPTION PRICING

OPTION PRICING Options are contingency contracts that specify payoffs if stock prices reach specified levels. A call option is the right to buy a stock at a specified price, X, called the strike price.

OPTION PRICING Options are contingency contracts that specify payoffs if stock prices reach specified levels. A call option is the right to buy a stock at a specified price, X, called the strike price.

Review for Exam 2. Instructions: Please read carefully

Review for Exam 2 Instructions: Please read carefully The exam will have 25 multiple choice questions and 5 work problems You are not responsible for any topics that are not covered in the lecture note

Review for Exam 2 Instructions: Please read carefully The exam will have 25 multiple choice questions and 5 work problems You are not responsible for any topics that are not covered in the lecture note

The Binomial Option Pricing Model André Farber

1 Solvay Business School Université Libre de Bruxelles The Binomial Option Pricing Model André Farber January 2002 Consider a non-dividend paying stock whose price is initially S 0. Divide time into small

1 Solvay Business School Université Libre de Bruxelles The Binomial Option Pricing Model André Farber January 2002 Consider a non-dividend paying stock whose price is initially S 0. Divide time into small

How Many Days Equal A Year? Non-trivial on the Mean-Variance Model

How Many Days Equal A Year? Non-trivial on the Mean-Variance Model George L. Ye, Dr. Sobey School of Business Saint Mary s University Halifax, Nova Scotia, Canada Christine Panasian, Dr. Sobey School of

How Many Days Equal A Year? Non-trivial on the Mean-Variance Model George L. Ye, Dr. Sobey School of Business Saint Mary s University Halifax, Nova Scotia, Canada Christine Panasian, Dr. Sobey School of

SAMPLE MID-TERM QUESTIONS

SAMPLE MID-TERM QUESTIONS William L. Silber HOW TO PREPARE FOR THE MID- TERM: 1. Study in a group 2. Review the concept questions in the Before and After book 3. When you review the questions listed below,

SAMPLE MID-TERM QUESTIONS William L. Silber HOW TO PREPARE FOR THE MID- TERM: 1. Study in a group 2. Review the concept questions in the Before and After book 3. When you review the questions listed below,

15.401 Finance Theory

Finance Theory MIT Sloan MBA Program Andrew W. Lo Harris & Harris Group Professor, MIT Sloan School Lectures 10 11 11: : Options Critical Concepts Motivation Payoff Diagrams Payoff Tables Option Strategies

Finance Theory MIT Sloan MBA Program Andrew W. Lo Harris & Harris Group Professor, MIT Sloan School Lectures 10 11 11: : Options Critical Concepts Motivation Payoff Diagrams Payoff Tables Option Strategies

Tilted Portfolios, Hedge Funds, and Portable Alpha

MAY 2006 Tilted Portfolios, Hedge Funds, and Portable Alpha EUGENE F. FAMA AND KENNETH R. FRENCH Many of Dimensional Fund Advisors clients tilt their portfolios toward small and value stocks. Relative

MAY 2006 Tilted Portfolios, Hedge Funds, and Portable Alpha EUGENE F. FAMA AND KENNETH R. FRENCH Many of Dimensional Fund Advisors clients tilt their portfolios toward small and value stocks. Relative

The capital asset pricing model (CAPM) of William Sharpe (1964) and John

of William Sharpe (1964) and John") Journal of Economic Perspectives Volume 18, Number 3 Summer 2004 Pages 25 46 The Capital Asset Pricing Model: Theory and Evidence Eugene F. Fama and Kenneth R. French The capital asset pricing model (CAPM)

Journal of Economic Perspectives Volume 18, Number 3 Summer 2004 Pages 25 46 The Capital Asset Pricing Model: Theory and Evidence Eugene F. Fama and Kenneth R. French The capital asset pricing model (CAPM)

The Capital Asset Pricing Model (CAPM)

") Prof. Alex Shapiro Lecture Notes 9 The Capital Asset Pricing Model (CAPM) I. Readings and Suggested Practice Problems II. III. IV. Introduction: from Assumptions to Implications The Market Portfolio Assumptions

Prof. Alex Shapiro Lecture Notes 9 The Capital Asset Pricing Model (CAPM) I. Readings and Suggested Practice Problems II. III. IV. Introduction: from Assumptions to Implications The Market Portfolio Assumptions

AFM 472. Midterm Examination. Monday Oct. 24, 2011. A. Huang

AFM 472 Midterm Examination Monday Oct. 24, 2011 A. Huang Name: Answer Key Student Number: Section (circle one): 10:00am 1:00pm 2:30pm Instructions: 1. Answer all questions in the space provided. If space

AFM 472 Midterm Examination Monday Oct. 24, 2011 A. Huang Name: Answer Key Student Number: Section (circle one): 10:00am 1:00pm 2:30pm Instructions: 1. Answer all questions in the space provided. If space

The Risk-Free Rate s Impact on Stock Returns with Representative Fund Managers

School of Economics and Management Department of Business Administration FEKN90 Business Administration- Degree Project Master of Science in Business and Economics Spring term of 2013 The Risk-Free Rate

School of Economics and Management Department of Business Administration FEKN90 Business Administration- Degree Project Master of Science in Business and Economics Spring term of 2013 The Risk-Free Rate

CFA Examination PORTFOLIO MANAGEMENT Page 1 of 6

PORTFOLIO MANAGEMENT A. INTRODUCTION RETURN AS A RANDOM VARIABLE E(R) = the return around which the probability distribution is centered: the expected value or mean of the probability distribution of possible

PORTFOLIO MANAGEMENT A. INTRODUCTION RETURN AS A RANDOM VARIABLE E(R) = the return around which the probability distribution is centered: the expected value or mean of the probability distribution of possible

Models of Asset Pricing The implications for asset allocation

Models of Asset Pricing The implications for asset allocation 2004 Finance & Investment Conference 28 June 2004 Tim Giles CHARLES RIVER ASSOCIATES Vice President CRA London CRA 2004 Agenda New orthodoxy

Models of Asset Pricing The implications for asset allocation 2004 Finance & Investment Conference 28 June 2004 Tim Giles CHARLES RIVER ASSOCIATES Vice President CRA London CRA 2004 Agenda New orthodoxy

M.I.T. Spring 1999 Sloan School of Management 15.415. First Half Summary

M.I.T. Spring 1999 Sloan School of Management 15.415 First Half Summary Present Values Basic Idea: We should discount future cash flows. The appropriate discount rate is the opportunity cost of capital.

M.I.T. Spring 1999 Sloan School of Management 15.415 First Half Summary Present Values Basic Idea: We should discount future cash flows. The appropriate discount rate is the opportunity cost of capital.

The Evolution of Investing

Bringing the Best of Academic Research to Real-World Investment Strategies The Science of Investing from the Halls of Academia An enormous Industry has developed over the years that s very familiar to

Bringing the Best of Academic Research to Real-World Investment Strategies The Science of Investing from the Halls of Academia An enormous Industry has developed over the years that s very familiar to

BINOMIAL OPTION PRICING

Darden Graduate School of Business Administration University of Virginia BINOMIAL OPTION PRICING Binomial option pricing is a simple but powerful technique that can be used to solve many complex option-pricing

Darden Graduate School of Business Administration University of Virginia BINOMIAL OPTION PRICING Binomial option pricing is a simple but powerful technique that can be used to solve many complex option-pricing

Option pricing. Vinod Kothari

Option pricing Vinod Kothari Notation we use this Chapter will be as follows: S o : Price of the share at time 0 S T : Price of the share at time T T : time to maturity of the option r : risk free rate

Option pricing Vinod Kothari Notation we use this Chapter will be as follows: S o : Price of the share at time 0 S T : Price of the share at time T T : time to maturity of the option r : risk free rate

1 Portfolio mean and variance

Copyright c 2005 by Karl Sigman Portfolio mean and variance Here we study the performance of a one-period investment X 0 > 0 (dollars) shared among several different assets. Our criterion for measuring

Copyright c 2005 by Karl Sigman Portfolio mean and variance Here we study the performance of a one-period investment X 0 > 0 (dollars) shared among several different assets. Our criterion for measuring

1 Capital Asset Pricing Model (CAPM)

") Copyright c 2005 by Karl Sigman 1 Capital Asset Pricing Model (CAPM) We now assume an idealized framework for an open market place, where all the risky assets refer to (say) all the tradeable stocks available

Copyright c 2005 by Karl Sigman 1 Capital Asset Pricing Model (CAPM) We now assume an idealized framework for an open market place, where all the risky assets refer to (say) all the tradeable stocks available

Lecture 1: Asset Allocation

Lecture 1: Asset Allocation Investments FIN460-Papanikolaou Asset Allocation I 1/ 62 Overview 1. Introduction 2. Investor s Risk Tolerance 3. Allocating Capital Between a Risky and riskless asset 4. Allocating

Lecture 1: Asset Allocation Investments FIN460-Papanikolaou Asset Allocation I 1/ 62 Overview 1. Introduction 2. Investor s Risk Tolerance 3. Allocating Capital Between a Risky and riskless asset 4. Allocating

CHAPTER 10 RISK AND RETURN: THE CAPITAL ASSET PRICING MODEL (CAPM)

") CHAPTER 10 RISK AND RETURN: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concepts Review and Critical Thinking Questions 1. Some of the risk in holding any asset is unique to the asset in question.

CHAPTER 10 RISK AND RETURN: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concepts Review and Critical Thinking Questions 1. Some of the risk in holding any asset is unique to the asset in question.

Lecture 15: Final Topics on CAPM

Lecture 15: Final Topics on CAPM Final topics on estimating and using beta: the market risk premium putting it all together Final topics on CAPM: Examples of firm and market risk Shorting Stocks and other

Lecture 15: Final Topics on CAPM Final topics on estimating and using beta: the market risk premium putting it all together Final topics on CAPM: Examples of firm and market risk Shorting Stocks and other

15.401 Finance Theory

Finance Theory MIT Sloan MBA Program Andrew W. Lo Harris & Harris Group Professor, MIT Sloan School Lecture 13 14 14: : Risk Analytics and Critical Concepts Motivation Measuring Risk and Reward Mean-Variance

Finance Theory MIT Sloan MBA Program Andrew W. Lo Harris & Harris Group Professor, MIT Sloan School Lecture 13 14 14: : Risk Analytics and Critical Concepts Motivation Measuring Risk and Reward Mean-Variance

TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II + III

SOLUTIONS RE-EXAMS 2014 II + III") TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II III Instructions 1. Only one problem should be treated on each sheet of paper and only one side of the sheet should be used. 2. The solutions folder

TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II III Instructions 1. Only one problem should be treated on each sheet of paper and only one side of the sheet should be used. 2. The solutions folder

OPTIONS and FUTURES Lecture 2: Binomial Option Pricing and Call Options

OPTIONS and FUTURES Lecture 2: Binomial Option Pricing and Call Options Philip H. Dybvig Washington University in Saint Louis binomial model replicating portfolio single period artificial (risk-neutral)

OPTIONS and FUTURES Lecture 2: Binomial Option Pricing and Call Options Philip H. Dybvig Washington University in Saint Louis binomial model replicating portfolio single period artificial (risk-neutral)

FIN 3710. Final (Practice) Exam 05/23/06

Exam 05/23/06") FIN 3710 Investment Analysis Spring 2006 Zicklin School of Business Baruch College Professor Rui Yao FIN 3710 Final (Practice) Exam 05/23/06 NAME: (Please print your name here) PLEDGE: (Sign your name

FIN 3710 Investment Analysis Spring 2006 Zicklin School of Business Baruch College Professor Rui Yao FIN 3710 Final (Practice) Exam 05/23/06 NAME: (Please print your name here) PLEDGE: (Sign your name

t = 1 2 3 1. Calculate the implied interest rates and graph the term structure of interest rates. t = 1 2 3 X t = 100 100 100 t = 1 2 3

MØA 155 PROBLEM SET: Summarizing Exercise 1. Present Value [3] You are given the following prices P t today for receiving risk free payments t periods from now. t = 1 2 3 P t = 0.95 0.9 0.85 1. Calculate

MØA 155 PROBLEM SET: Summarizing Exercise 1. Present Value [3] You are given the following prices P t today for receiving risk free payments t periods from now. t = 1 2 3 P t = 0.95 0.9 0.85 1. Calculate

Mid-Term Spring 2003

Mid-Term Spring 2003 1. (1 point) You want to purchase XYZ stock at $60 from your broker using as little of your own money as possible. If initial margin is 50% and you have $3000 to invest, how many shares

Mid-Term Spring 2003 1. (1 point) You want to purchase XYZ stock at $60 from your broker using as little of your own money as possible. If initial margin is 50% and you have $3000 to invest, how many shares

A Mean-Variance Framework for Tests of Asset Pricing Models

A Mean-Variance Framework for Tests of Asset Pricing Models Shmuel Kandel University of Chicago Tel-Aviv, University Robert F. Stambaugh University of Pennsylvania This article presents a mean-variance

A Mean-Variance Framework for Tests of Asset Pricing Models Shmuel Kandel University of Chicago Tel-Aviv, University Robert F. Stambaugh University of Pennsylvania This article presents a mean-variance

Rate of Return. Reading: Veronesi, Chapter 7. Investment over a Holding Period

Rate of Return Reading: Veronesi, Chapter 7 Investment over a Holding Period Consider an investment in any asset over a holding period from time 0 to time T. Suppose the amount invested at time 0 is P

Rate of Return Reading: Veronesi, Chapter 7 Investment over a Holding Period Consider an investment in any asset over a holding period from time 0 to time T. Suppose the amount invested at time 0 is P

The Tangent or Efficient Portfolio

The Tangent or Efficient Portfolio 1 2 Identifying the Tangent Portfolio Sharpe Ratio: Measures the ratio of reward-to-volatility provided by a portfolio Sharpe Ratio Portfolio Excess Return E[ RP ] r

The Tangent or Efficient Portfolio 1 2 Identifying the Tangent Portfolio Sharpe Ratio: Measures the ratio of reward-to-volatility provided by a portfolio Sharpe Ratio Portfolio Excess Return E[ RP ] r

Fundamentals of Futures and Options (a summary)

") Fundamentals of Futures and Options (a summary) Roger G. Clarke, Harindra de Silva, CFA, and Steven Thorley, CFA Published 2013 by the Research Foundation of CFA Institute Summary prepared by Roger G.

Fundamentals of Futures and Options (a summary) Roger G. Clarke, Harindra de Silva, CFA, and Steven Thorley, CFA Published 2013 by the Research Foundation of CFA Institute Summary prepared by Roger G.

Chapter 2 Portfolio Management and the Capital Asset Pricing Model

Chapter 2 Portfolio Management and the Capital Asset Pricing Model In this chapter, we explore the issue of risk management in a portfolio of assets. The main issue is how to balance a portfolio, that

Chapter 2 Portfolio Management and the Capital Asset Pricing Model In this chapter, we explore the issue of risk management in a portfolio of assets. The main issue is how to balance a portfolio, that

Review for Exam 2. Instructions: Please read carefully

Review for Exam Instructions: Please read carefully The exam will have 1 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation questions.

Review for Exam Instructions: Please read carefully The exam will have 1 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation questions.

How To Understand The Theory Of Finance

University of Pennsylvania The Wharton School FNCE 911: Foundations for Financial Economics Prof. Jessica A. Wachter Fall 2010 Office: SH-DH 2322 Classes: Mon./Wed. 1:30-3:00 Email: [email protected]

University of Pennsylvania The Wharton School FNCE 911: Foundations for Financial Economics Prof. Jessica A. Wachter Fall 2010 Office: SH-DH 2322 Classes: Mon./Wed. 1:30-3:00 Email: [email protected]

Introduction to Options. Derivatives

Introduction to Options Econ 422: Investment, Capital & Finance University of Washington Summer 2010 August 18, 2010 Derivatives A derivative is a security whose payoff or value depends on (is derived

Introduction to Options Econ 422: Investment, Capital & Finance University of Washington Summer 2010 August 18, 2010 Derivatives A derivative is a security whose payoff or value depends on (is derived

Four Derivations of the Black Scholes PDE by Fabrice Douglas Rouah www.frouah.com www.volopta.com

Four Derivations of the Black Scholes PDE by Fabrice Douglas Rouah www.frouah.com www.volopta.com In this Note we derive the Black Scholes PDE for an option V, given by @t + 1 + rs @S2 @S We derive the

Four Derivations of the Black Scholes PDE by Fabrice Douglas Rouah www.frouah.com www.volopta.com In this Note we derive the Black Scholes PDE for an option V, given by @t + 1 + rs @S2 @S We derive the

On Black-Scholes Equation, Black- Scholes Formula and Binary Option Price

On Black-Scholes Equation, Black- Scholes Formula and Binary Option Price Abstract: Chi Gao 12/15/2013 I. Black-Scholes Equation is derived using two methods: (1) risk-neutral measure; (2) - hedge. II.

On Black-Scholes Equation, Black- Scholes Formula and Binary Option Price Abstract: Chi Gao 12/15/2013 I. Black-Scholes Equation is derived using two methods: (1) risk-neutral measure; (2) - hedge. II.

Journal of Exclusive Management Science May 2015 -Vol 4 Issue 5 - ISSN 2277 5684

Journal of Exclusive Management Science May 2015 Vol 4 Issue 5 ISSN 2277 5684 A Study on the Emprical Testing Of Capital Asset Pricing Model on Selected Energy Sector Companies Listed In NSE Abstract *S.A.

Journal of Exclusive Management Science May 2015 Vol 4 Issue 5 ISSN 2277 5684 A Study on the Emprical Testing Of Capital Asset Pricing Model on Selected Energy Sector Companies Listed In NSE Abstract *S.A.

ON THE RISK ADJUSTED DISCOUNT RATE FOR DETERMINING LIFE OFFICE APPRAISAL VALUES BY M. SHERRIS B.A., M.B.A., F.I.A., F.I.A.A. 1.

ON THE RISK ADJUSTED DISCOUNT RATE FOR DETERMINING LIFE OFFICE APPRAISAL VALUES BY M. SHERRIS B.A., M.B.A., F.I.A., F.I.A.A. 1. INTRODUCTION 1.1 A number of papers have been written in recent years that

ON THE RISK ADJUSTED DISCOUNT RATE FOR DETERMINING LIFE OFFICE APPRAISAL VALUES BY M. SHERRIS B.A., M.B.A., F.I.A., F.I.A.A. 1. INTRODUCTION 1.1 A number of papers have been written in recent years that

Futures Price d,f $ 0.65 = (1.05) (1.04)

(1.04)") 24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

Chapter 21 Valuing Options

Chapter 21 Valuing Options Multiple Choice Questions 1. Relative to the underlying stock, a call option always has: A) A higher beta and a higher standard deviation of return B) A lower beta and a higher

Chapter 21 Valuing Options Multiple Choice Questions 1. Relative to the underlying stock, a call option always has: A) A higher beta and a higher standard deviation of return B) A lower beta and a higher

Midterm Exam:Answer Sheet

Econ 497 Barry W. Ickes Spring 2007 Midterm Exam:Answer Sheet 1. (25%) Consider a portfolio, c, comprised of a risk-free and risky asset, with returns given by r f and E(r p ), respectively. Let y be the

Econ 497 Barry W. Ickes Spring 2007 Midterm Exam:Answer Sheet 1. (25%) Consider a portfolio, c, comprised of a risk-free and risky asset, with returns given by r f and E(r p ), respectively. Let y be the

1. CFI Holdings is a conglomerate listed on the Zimbabwe Stock Exchange (ZSE) and has three operating divisions as follows:

and has three operating divisions as follows:") NATIONAL UNIVERSITY OF SCIENCE AND TECHNOLOGY FACULTY OF COMMERCE DEPARTMENT OF FINANCE BACHELOR OF COMMERCE HONOURS DEGREE IN FINANCE PART II 2 ND SEMESTER FINAL EXAMINATION MAY 2005 CORPORATE FINANCE

NATIONAL UNIVERSITY OF SCIENCE AND TECHNOLOGY FACULTY OF COMMERCE DEPARTMENT OF FINANCE BACHELOR OF COMMERCE HONOURS DEGREE IN FINANCE PART II 2 ND SEMESTER FINAL EXAMINATION MAY 2005 CORPORATE FINANCE

Chapter 11. Topics Covered. Chapter 11 Objectives. Risk, Return, and Capital Budgeting

Chapter 11 Risk, Return, and Capital Budgeting Topics Covered Measuring Market Risk Portfolio Betas Risk and Return CAPM and Expected Return Security Market Line CAPM and Stock Valuation Chapter 11 Objectives

Chapter 11 Risk, Return, and Capital Budgeting Topics Covered Measuring Market Risk Portfolio Betas Risk and Return CAPM and Expected Return Security Market Line CAPM and Stock Valuation Chapter 11 Objectives

a. What is the portfolio of the stock and the bond that replicates the option?

Practice problems for Lecture 2. Answers. 1. A Simple Option Pricing Problem in One Period Riskless bond (interest rate is 5%): 1 15 Stock: 5 125 5 Derivative security (call option with a strike of 8):?

Practice problems for Lecture 2. Answers. 1. A Simple Option Pricing Problem in One Period Riskless bond (interest rate is 5%): 1 15 Stock: 5 125 5 Derivative security (call option with a strike of 8):?

CAPITAL ASSET PRICES WITH AND WITHOUT NEGATIVE HOLDINGS

CAPITAL ASSET PRICES WITH AND WITHOUT NEGATIVE HOLDINGS Nobel Lecture, December 7, 1990 by WILLIAM F. SHARPE Stanford University Graduate School of Business, Stanford, California, USA INTRODUCTION* Following

CAPITAL ASSET PRICES WITH AND WITHOUT NEGATIVE HOLDINGS Nobel Lecture, December 7, 1990 by WILLIAM F. SHARPE Stanford University Graduate School of Business, Stanford, California, USA INTRODUCTION* Following

CHARACTERISTICS OF INVESTMENT PORTFOLIOS PASSIVE MANAGEMENT STRATEGY ON THE CAPITAL MARKET

Mihaela Sudacevschi 931 CHARACTERISTICS OF INVESTMENT PORTFOLIOS PASSIVE MANAGEMENT STRATEGY ON THE CAPITAL MARKET MIHAELA SUDACEVSCHI * Abstract The strategies of investment portfolios management on the

Mihaela Sudacevschi 931 CHARACTERISTICS OF INVESTMENT PORTFOLIOS PASSIVE MANAGEMENT STRATEGY ON THE CAPITAL MARKET MIHAELA SUDACEVSCHI * Abstract The strategies of investment portfolios management on the

CHAPTER 11: ARBITRAGE PRICING THEORY

CHAPTER 11: ARBITRAGE PRICING THEORY 1. The revised estimate of the expected rate of return on the stock would be the old estimate plus the sum of the products of the unexpected change in each factor times

CHAPTER 11: ARBITRAGE PRICING THEORY 1. The revised estimate of the expected rate of return on the stock would be the old estimate plus the sum of the products of the unexpected change in each factor times

Lecture Notes: Basic Concepts in Option Pricing - The Black and Scholes Model

Brunel University Msc., EC5504, Financial Engineering Prof Menelaos Karanasos Lecture Notes: Basic Concepts in Option Pricing - The Black and Scholes Model Recall that the price of an option is equal to

Brunel University Msc., EC5504, Financial Engineering Prof Menelaos Karanasos Lecture Notes: Basic Concepts in Option Pricing - The Black and Scholes Model Recall that the price of an option is equal to

ANALYSIS AND MANAGEMENT

ANALYSIS AND MANAGEMENT T H 1RD CANADIAN EDITION W. SEAN CLEARY Queen's University CHARLES P. JONES North Carolina State University JOHN WILEY & SONS CANADA, LTD. CONTENTS PART ONE Background CHAPTER 1

ANALYSIS AND MANAGEMENT T H 1RD CANADIAN EDITION W. SEAN CLEARY Queen's University CHARLES P. JONES North Carolina State University JOHN WILEY & SONS CANADA, LTD. CONTENTS PART ONE Background CHAPTER 1

Forward Contracts and Forward Rates

Forward Contracts and Forward Rates Outline and Readings Outline Forward Contracts Forward Prices Forward Rates Information in Forward Rates Reading Veronesi, Chapters 5 and 7 Tuckman, Chapters 2 and 16

Forward Contracts and Forward Rates Outline and Readings Outline Forward Contracts Forward Prices Forward Rates Information in Forward Rates Reading Veronesi, Chapters 5 and 7 Tuckman, Chapters 2 and 16

Foundations of Asset Management Goal-based Investing the Next Trend

Foundations of Asset Management Goal-based Investing the Next Trend Robert C. Merton Distinguished Professor of Finance MIT Finance Forum May 16, 2014 #MITSloanFinance 1 Agenda Goal-based approach to investment

Foundations of Asset Management Goal-based Investing the Next Trend Robert C. Merton Distinguished Professor of Finance MIT Finance Forum May 16, 2014 #MITSloanFinance 1 Agenda Goal-based approach to investment

Applied Economics For Managers Recitation 5 Tuesday July 6th 2004

Applied Economics For Managers Recitation 5 Tuesday July 6th 2004 Outline 1 Uncertainty and asset prices 2 Informational efficiency - rational expectations, random walks 3 Asymmetric information - lemons,

Applied Economics For Managers Recitation 5 Tuesday July 6th 2004 Outline 1 Uncertainty and asset prices 2 Informational efficiency - rational expectations, random walks 3 Asymmetric information - lemons,

Mutual Fund Performance

Mutual Fund Performance When measured before expenses passive investors who simply hold the market portfolio must earn zero abnormal returns. This means that active investors as a group must also earn

Mutual Fund Performance When measured before expenses passive investors who simply hold the market portfolio must earn zero abnormal returns. This means that active investors as a group must also earn

Agenda. The IS LM Model, Part 2. The Demand for Money. The Demand for Money. The Demand for Money. Asset Market Equilibrium.

Agenda The IS LM Model, Part 2 Asset Market Equilibrium The LM Curve 13-1 13-2 The demand for money is the quantity of money people want to hold in their portfolios. The demand for money depends on expected

Agenda The IS LM Model, Part 2 Asset Market Equilibrium The LM Curve 13-1 13-2 The demand for money is the quantity of money people want to hold in their portfolios. The demand for money depends on expected

The Capital Asset Pricing Model: Some Empirical Tests

The Capital Asset Pricing Model: Some Empirical Tests Fischer Black* Deceased Michael C. Jensen Harvard Business School [email protected] and Myron Scholes Stanford University - Graduate School of Business

The Capital Asset Pricing Model: Some Empirical Tests Fischer Black* Deceased Michael C. Jensen Harvard Business School [email protected] and Myron Scholes Stanford University - Graduate School of Business

The Valuation of Currency Options

The Valuation of Currency Options Nahum Biger and John Hull Both Nahum Biger and John Hull are Associate Professors of Finance in the Faculty of Administrative Studies, York University, Canada. Introduction

The Valuation of Currency Options Nahum Biger and John Hull Both Nahum Biger and John Hull are Associate Professors of Finance in the Faculty of Administrative Studies, York University, Canada. Introduction

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Options These notes consider the way put and call options and the underlying can be combined to create hedges, spreads and combinations. We will consider the

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Options These notes consider the way put and call options and the underlying can be combined to create hedges, spreads and combinations. We will consider the

Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.)

") Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.) The primary focus of the next two chapters will be to examine the debt/equity choice by firms. In particular,

Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.) The primary focus of the next two chapters will be to examine the debt/equity choice by firms. In particular,

Cost of Capital, Valuation and Strategic Financial Decision Making

Cost of Capital, Valuation and Strategic Financial Decision Making By Dr. Valerio Poti, - Examiner in Professional 2 Stage Strategic Corporate Finance The financial crisis that hit financial markets in

Cost of Capital, Valuation and Strategic Financial Decision Making By Dr. Valerio Poti, - Examiner in Professional 2 Stage Strategic Corporate Finance The financial crisis that hit financial markets in

Risk and Return Models: Equity and Debt. Aswath Damodaran 1

Risk and Return Models: Equity and Debt Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

Risk and Return Models: Equity and Debt Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for

Chapter 7 Risk, Return, and the Capital Asset Pricing Model

Chapter 7 Risk, Return, and the Capital Asset Pricing Model MULTIPLE CHOICE 1. Suppose Sarah can borrow and lend at the risk free-rate of 3%. Which of the following four risky portfolios should she hold

Chapter 7 Risk, Return, and the Capital Asset Pricing Model MULTIPLE CHOICE 1. Suppose Sarah can borrow and lend at the risk free-rate of 3%. Which of the following four risky portfolios should she hold

Discussion of Momentum and Autocorrelation in Stock Returns

Discussion of Momentum and Autocorrelation in Stock Returns Joseph Chen University of Southern California Harrison Hong Stanford University Jegadeesh and Titman (1993) document individual stock momentum:

Discussion of Momentum and Autocorrelation in Stock Returns Joseph Chen University of Southern California Harrison Hong Stanford University Jegadeesh and Titman (1993) document individual stock momentum:

NIKE Case Study Solutions

NIKE Case Study Solutions Professor Corwin This case study includes several problems related to the valuation of Nike. We will work through these problems throughout the course to demonstrate some of the

NIKE Case Study Solutions Professor Corwin This case study includes several problems related to the valuation of Nike. We will work through these problems throughout the course to demonstrate some of the

The Capital Asset Pricing Model

Journal of Economic Perspectives Volume 18, Number 3 Summer 2004 Pages 3 24 The Capital Asset Pricing Model André F. Perold A fundamental question in finance is how the risk of an investment should affect

Journal of Economic Perspectives Volume 18, Number 3 Summer 2004 Pages 3 24 The Capital Asset Pricing Model André F. Perold A fundamental question in finance is how the risk of an investment should affect

CHAPTER 15. Option Valuation

CHAPTER 15 Option Valuation Just what is an option worth? Actually, this is one of the more difficult questions in finance. Option valuation is an esoteric area of finance since it often involves complex

CHAPTER 15 Option Valuation Just what is an option worth? Actually, this is one of the more difficult questions in finance. Option valuation is an esoteric area of finance since it often involves complex

8.1 Summary and conclusions 8.2 Implications

Conclusion and Implication V{tÑàxÜ CONCLUSION AND IMPLICATION 8 Contents 8.1 Summary and conclusions 8.2 Implications Having done the selection of macroeconomic variables, forecasting the series and construction

Conclusion and Implication V{tÑàxÜ CONCLUSION AND IMPLICATION 8 Contents 8.1 Summary and conclusions 8.2 Implications Having done the selection of macroeconomic variables, forecasting the series and construction

Chapter 13 : The Arbitrage Pricing Theory

Chapter 13 : The Arbitrage Pricing Theory 13.1 Introduction We have made two first attempts (Chapters 10 to 12) at asset pricing from an arbitrage perspective, that is, without specifying a complete equilibrium

Chapter 13 : The Arbitrage Pricing Theory 13.1 Introduction We have made two first attempts (Chapters 10 to 12) at asset pricing from an arbitrage perspective, that is, without specifying a complete equilibrium

The CAPM (Capital Asset Pricing Model) NPV Dependent on Discount Rate Schedule

NPV Dependent on Discount Rate Schedule") The CAPM (Capital Asset Pricing Model) Massachusetts Institute of Technology CAPM Slide 1 of NPV Dependent on Discount Rate Schedule Discussed NPV and time value of money Choice of discount rate influences

The CAPM (Capital Asset Pricing Model) Massachusetts Institute of Technology CAPM Slide 1 of NPV Dependent on Discount Rate Schedule Discussed NPV and time value of money Choice of discount rate influences

Call Price as a Function of the Stock Price

Call Price as a Function of the Stock Price Intuitively, the call price should be an increasing function of the stock price. This relationship allows one to develop a theory of option pricing, derived

Call Price as a Function of the Stock Price Intuitively, the call price should be an increasing function of the stock price. This relationship allows one to develop a theory of option pricing, derived

KENNETH R. FRENCH. Roth Family Distinguished Professor of Finance 85 Trescott Road Tuck School of Business at Dartmouth

KENNETH R. FRENCH August 2015 Preferred Address: Roth Family Distinguished Professor of Finance 85 Trescott Road Tuck School of Business at Dartmouth Etna, NH 03750 100 Tuck Hall Hanover, NH 03755-9000

KENNETH R. FRENCH August 2015 Preferred Address: Roth Family Distinguished Professor of Finance 85 Trescott Road Tuck School of Business at Dartmouth Etna, NH 03750 100 Tuck Hall Hanover, NH 03755-9000

CHAPTER 7: OPTIMAL RISKY PORTFOLIOS

CHAPTER 7: OPTIMAL RIKY PORTFOLIO PROLEM ET 1. (a) and (e).. (a) and (c). After real estate is added to the portfolio, there are four asset classes in the portfolio: stocks, bonds, cash and real estate.

CHAPTER 7: OPTIMAL RIKY PORTFOLIO PROLEM ET 1. (a) and (e).. (a) and (c). After real estate is added to the portfolio, there are four asset classes in the portfolio: stocks, bonds, cash and real estate.

Norges Bank s Expert Group on Principles for Risk Adjustment of Performance Figures Final Report

Norges Bank s Expert Group on Principles for Risk Adjustment of Performance Figures Final Report November 16, 2015 Magnus Dahlquist Professor, Stockholm School of Economics Christopher Polk Professor,

Norges Bank s Expert Group on Principles for Risk Adjustment of Performance Figures Final Report November 16, 2015 Magnus Dahlquist Professor, Stockholm School of Economics Christopher Polk Professor,

The required return on equity for regulated gas and electricity network businesses

The required return on equity for regulated gas and electricity network businesses Report for Jemena Gas Networks, ActewAGL Distribution, Ergon, and Transend 27 May 2014 Level 1, South Bank House Cnr.

The required return on equity for regulated gas and electricity network businesses Report for Jemena Gas Networks, ActewAGL Distribution, Ergon, and Transend 27 May 2014 Level 1, South Bank House Cnr.

Tax-adjusted discount rates with investor taxes and risky debt

Tax-adjusted discount rates with investor taxes and risky debt Ian A Cooper and Kjell G Nyborg October 2004 Abstract This paper derives tax-adjusted discount rate formulas with Miles-Ezzell leverage policy,

Tax-adjusted discount rates with investor taxes and risky debt Ian A Cooper and Kjell G Nyborg October 2004 Abstract This paper derives tax-adjusted discount rate formulas with Miles-Ezzell leverage policy,

Solution: The optimal position for an investor with a coefficient of risk aversion A = 5 in the risky asset is y*:

Problem 1. Consider a risky asset. Suppose the expected rate of return on the risky asset is 15%, the standard deviation of the asset return is 22%, and the risk-free rate is 6%. What is your optimal position

Problem 1. Consider a risky asset. Suppose the expected rate of return on the risky asset is 15%, the standard deviation of the asset return is 22%, and the risk-free rate is 6%. What is your optimal position

Two-State Option Pricing

Rendleman and Bartter [1] present a simple two-state model of option pricing. The states of the world evolve like the branches of a tree. Given the current state, there are two possible states next period.

Rendleman and Bartter [1] present a simple two-state model of option pricing. The states of the world evolve like the branches of a tree. Given the current state, there are two possible states next period.

Excess Volatility and Closed-End Fund Discounts

Excess Volatility and Closed-End Fund Discounts Michael Bleaney School of Economics University of Nottingham Nottingham NG7 RD, U.K. Tel. (+44) 115 951 5464 Fax (+44) 115 951 4159 e-mail: [email protected]

Excess Volatility and Closed-End Fund Discounts Michael Bleaney School of Economics University of Nottingham Nottingham NG7 RD, U.K. Tel. (+44) 115 951 5464 Fax (+44) 115 951 4159 e-mail: [email protected]

10 Binomial Trees. 10.1 One-step model. 1. Model structure. ECG590I Asset Pricing. Lecture 10: Binomial Trees 1

ECG590I Asset Pricing. Lecture 10: Binomial Trees 1 10 Binomial Trees 10.1 One-step model 1. Model structure ECG590I Asset Pricing. Lecture 10: Binomial Trees 2 There is only one time interval (t 0, t

ECG590I Asset Pricing. Lecture 10: Binomial Trees 1 10 Binomial Trees 10.1 One-step model 1. Model structure ECG590I Asset Pricing. Lecture 10: Binomial Trees 2 There is only one time interval (t 0, t

ATHENS UNIVERSITY OF ECONOMICS AND BUSINESS

ATHENS UNIVERSITY OF ECONOMICS AND BUSINESS Masters in Business Administration (MBA) Offered by the Departments of: Business Administration & Marketing and Communication PORTFOLIO ANALYSIS AND MANAGEMENT

ATHENS UNIVERSITY OF ECONOMICS AND BUSINESS Masters in Business Administration (MBA) Offered by the Departments of: Business Administration & Marketing and Communication PORTFOLIO ANALYSIS AND MANAGEMENT

Investment Portfolio Philosophy

Investment Portfolio Philosophy The performance of your investment portfolio and the way it contributes to your lifestyle goals is always our prime concern. Our portfolio construction process for all of

Investment Portfolio Philosophy The performance of your investment portfolio and the way it contributes to your lifestyle goals is always our prime concern. Our portfolio construction process for all of

Caput Derivatives: October 30, 2003

Caput Derivatives: October 30, 2003 Exam + Answers Total time: 2 hours and 30 minutes. Note 1: You are allowed to use books, course notes, and a calculator. Question 1. [20 points] Consider an investor

Caput Derivatives: October 30, 2003 Exam + Answers Total time: 2 hours and 30 minutes. Note 1: You are allowed to use books, course notes, and a calculator. Question 1. [20 points] Consider an investor

Chapter 8 Financial Options and Applications in Corporate Finance ANSWERS TO END-OF-CHAPTER QUESTIONS

Chapter 8 Financial Options and Applications in Corporate Finance ANSWERS TO END-OF-CHAPTER QUESTIONS 8-1 a. An option is a contract which gives its holder the right to buy or sell an asset at some predetermined

Chapter 8 Financial Options and Applications in Corporate Finance ANSWERS TO END-OF-CHAPTER QUESTIONS 8-1 a. An option is a contract which gives its holder the right to buy or sell an asset at some predetermined

Discussions of Monte Carlo Simulation in Option Pricing TIANYI SHI, Y LAURENT LIU PROF. RENATO FERES MATH 350 RESEARCH PAPER

Discussions of Monte Carlo Simulation in Option Pricing TIANYI SHI, Y LAURENT LIU PROF. RENATO FERES MATH 350 RESEARCH PAPER INTRODUCTION Having been exposed to a variety of applications of Monte Carlo

Discussions of Monte Carlo Simulation in Option Pricing TIANYI SHI, Y LAURENT LIU PROF. RENATO FERES MATH 350 RESEARCH PAPER INTRODUCTION Having been exposed to a variety of applications of Monte Carlo

FIN 432 Investment Analysis and Management Review Notes for Midterm Exam

FIN 432 Investment Analysis and Management Review Notes for Midterm Exam Chapter 1 1. Investment vs. investments 2. Real assets vs. financial assets 3. Investment process Investment policy, asset allocation,

FIN 432 Investment Analysis and Management Review Notes for Midterm Exam Chapter 1 1. Investment vs. investments 2. Real assets vs. financial assets 3. Investment process Investment policy, asset allocation,

THE FUNDAMENTAL THEOREM OF ARBITRAGE PRICING

THE FUNDAMENTAL THEOREM OF ARBITRAGE PRICING 1. Introduction The Black-Scholes theory, which is the main subject of this course and its sequel, is based on the Efficient Market Hypothesis, that arbitrages

THE FUNDAMENTAL THEOREM OF ARBITRAGE PRICING 1. Introduction The Black-Scholes theory, which is the main subject of this course and its sequel, is based on the Efficient Market Hypothesis, that arbitrages

The Conversion of Cooperatives to Publicly Held Corporations: A Financial Analysis of Limited Evidence

The Conversion of Cooperatives to Publicly Held Corporations: A Financial Analysis of Limited Evidence Robert A. Collins Recent reorganizations of agricultural cooperatives have created concern that the

The Conversion of Cooperatives to Publicly Held Corporations: A Financial Analysis of Limited Evidence Robert A. Collins Recent reorganizations of agricultural cooperatives have created concern that the

Rethinking Fixed Income

Rethinking Fixed Income Challenging Conventional Wisdom May 2013 Risk. Reinsurance. Human Resources. Rethinking Fixed Income: Challenging Conventional Wisdom With US Treasury interest rates at, or near,

Rethinking Fixed Income Challenging Conventional Wisdom May 2013 Risk. Reinsurance. Human Resources. Rethinking Fixed Income: Challenging Conventional Wisdom With US Treasury interest rates at, or near,