Defined Contribution Registered Pension Plan for Unionized Associates. together at CCR

|

|

|

- Elfrieda Powell

- 10 years ago

- Views:

Transcription

1 to Manulife Financial Defined Contribution Registered Pension Plan for Unionized Associates together at CCR

2 A message from Coca-Cola Refreshments Canada The Coca-Cola Refreshment Canada (CCRC) Defined Contribution Registered Pension Plan has been established with Manulife Financial to assist you in preparing for retirement. When you join the plan, CCRC helps you save even more for your retirement. Take advantage of this opportunity by joining the plan today. About this Enrolment Guide This Guide provides information you will need to enroll in the CCRC Defined Contribution Registered Pension Plan. This process will take a bit of your time, but it will be time well invested. A step-by-step process will help you navigate through this Guide. Each step includes a To Do box showing what you must complete to enroll. The boxes separate what you must do from what you should keep in mind. 2

3 Here s what you need to do... Step one: Step two: Step three: Step four: Learn about your program Decide how to enroll Decide how to invest Check to see you ve completed each step Let s Get Started... 3

4 Step one Learn about your program To do! Learn about the advantages of your program. Review the details of your program. Advantages of the CCRC Defined Contribution Registered Pension Plan To help ensure you are prepared for life after work, CCRC has taken the first step toward helping you save for your retirement by offering you a retirement program. Now, it s up to you to take the next step and join your program. Your plan provides these benefits that may not be available to you through an individual savings or investment account: Tax-deferred growth Your registered savings grow in a tax-sheltered environment until you withdraw from the plan to purchase your retirement income. Lower investment management fees Take advantage of the competitive investment management fees (IMFs) offered by your group plan. Lower IMFs leave more of your savings in your account and growing for you. Leading fund managers Through your group plan, you have access to some of the world s leading fund managers and their funds. Many of these funds aren t available to individual investors. Secure website and telephone account access Manage your account and investments using the service option you prefer. Access your account via the secure member website and/or the Customer Service Centre. Easy-to-read statements Manulife s member statements provide updates on your savings and include tips and reminders to help you build an effective retirement savings plan. 4

5 Step one Details of your program The details of your program shown below are subject to change by CCRC. The terms of your specific Collective Bargaining Agreement may also override the details as shown. Defined Contribution Registered Pension Plan (RPP) Policy number Who is eligible to join this plan? Do I have to join? When can I join? How much can I contribute? All full-time permanent employees over the age of 18 hired on or after January 1, Yes, participation is mandatory. You must join once you have completed one year of full-time permanent employment. Participation will commence on the first business day of the month after becoming eligible to join. You do not contribute to this plan. How much does the Company contribute? Who decides how contributions will be invested? Can I transfer money into the plan? Can I make additional one-time contributions? Can I take money out of the plan while I am employed? What happens if I leave or retire from the Company? What happens if I die while employed with the Company? CCRC will contribute 4% of eligible earnings. You decide how the contributions made by CCRC will be invested. No. No. No. The full value of your account belongs to you. Your spouse will be entitled to the full value of your account. If you do not have a spouse, your appointed beneficiary(s) will be entitled to the portion of your account that you have specified. If you do not have a spouse and you have not appointed a beneficiary, the full value of your account will be paid to your estate. Note: All contributions to the RPP are subject to the annual contribution limits of Canada Revenue Agency (CRA). 5

6 Step two Decide how to enroll To do! Decide how you want to enroll either online or with paper forms. Follow the instructions for your preferred enrolment option. To enroll online Go to Enter the policy number and access code CCR44. Follow all of the steps to complete your online enrolment. Tips for enrolling online: Review the section titled Your Investment Choices starting on page 19 to view the investments available through your program and their investment management fees (IMFs). Print your Beneficiary confirmation when you finish enrolling in each plan. Complete and sign the form(s), then return them to Manulife in the envelope provided. Print your Enrolment confirmation when you finish enrolling in each plan so you have a copy for your records. You will need the Customer Number shown on your confirmation to identify yourself to the Customer Service Centre and to access online services. Choose your Personal Identification Number (PIN) to access the secure website at the end of the enrolment process. Remember to keep this number in a safe place. 6

, then return them to Manulife in the envelope provided.")

7 Step two To enroll using paper forms Detach the Application form for the plan below. All forms you need to complete are located in this Guide. Application form for the Registered Pension Plan Page 23 Complete the following sections on each Application form: Tell us about your plan Your personal information Name your beneficiary (or beneficiaries) Once you have completed these sections on each Application form, go to the next step in this Guide. 7

Once you have")

8 Step three Decide how to invest To do! Follow the instructions on the next page to determine your investor style and select your investments. Note - If you consult a Financial Planner for advice regarding funds for your savings, provide him or her with this Guide. If you do not generally seek the advice of a financial planner before making investment decisions, please continue reading. You decide how all contributions will be invested. If you do not provide instructions on where to invest contributions to your plans, contributions will be deposited to the plan default investment MLI BlackRock LifePath Index fund closest to the year you turn 65. If Manulife does not have your date of birth on file, contributions will be deposited to MLI Canadian Money Market Fund (MAM). You are strongly encouraged to take an active role in how your retirement savings are invested and ensure you are invested in fund(s) that suit you. Your plan s default investment is intended as a temporary destination for your contributions and may not be appropriate for your long-term retirement planning. Want to learn more about investments? View the online learning module at 8

9 Step three Determine what type of investor you are To do! Answer the questions below to determine whether you should build your own portfolio or select a single, ready-made fund. How interested are you in selecting investments for your retirement savings? A I have some interest. B I am very interested. How likely are you to monitor and rebalance your investments on an annual basis? I review my investments annually. I check my investments on a regular basis (at least quarterly). How would you rate your investment knowledge? I understand the basics of investing. I am confident in my investment knowledge. If you chose two or more responses from... The best investment strategy for you is... Turn to page... Column A...to select a Retirement Date Fund. A Retirement Date Fund offers a well-balanced investment portfolio inside a single fund. Each fund is identified by its year of maturity, and as the maturity date approaches the fund gradually rebalances to become more conservative. 10 Column B...to build your own portfolio. Choose from the individual funds available through your program to build your own portfolio. 11 9

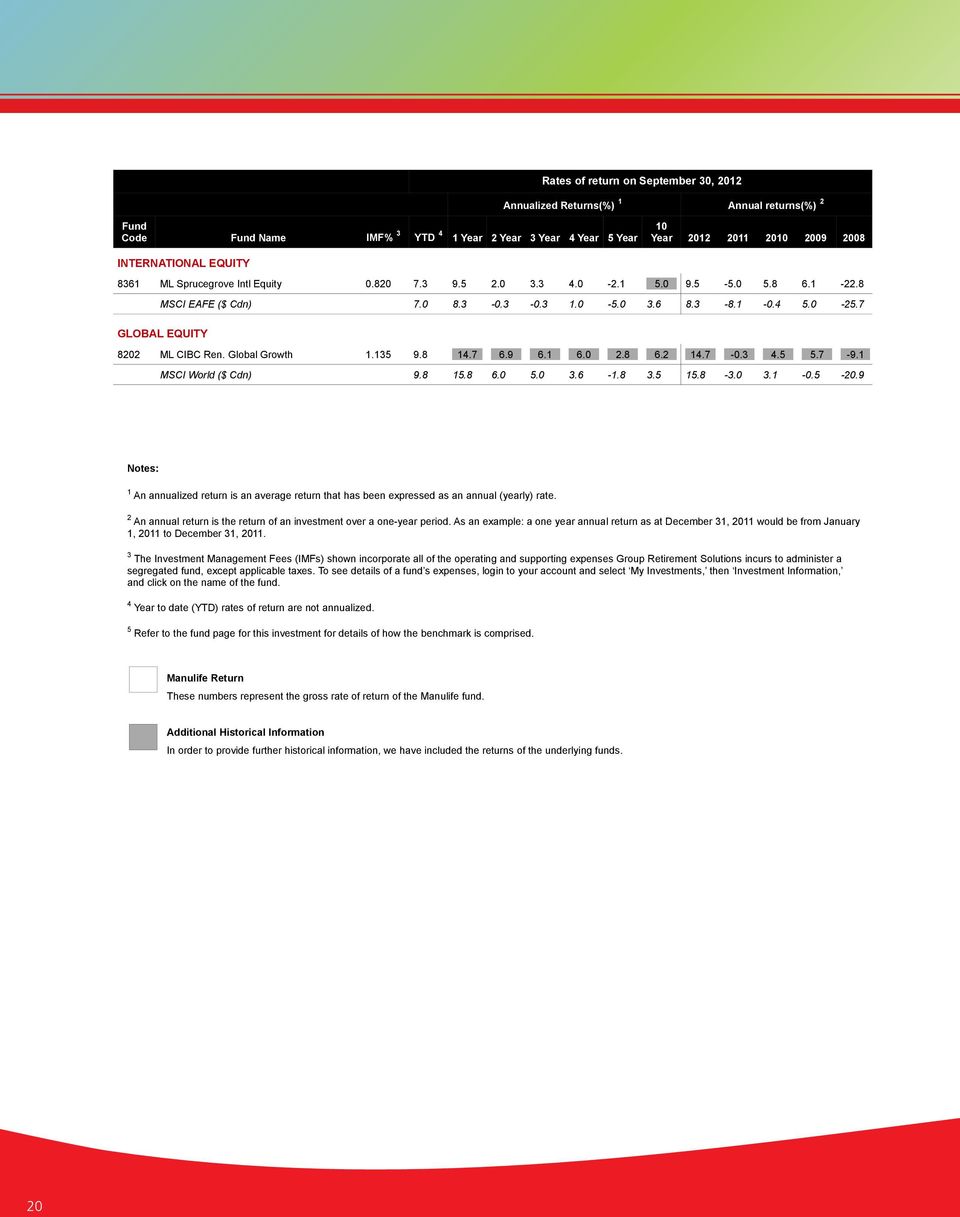

10 Step three How to choose a Retirement Date Fund To do! Decide what age you plan to retire: Calculate what year you plan to retire: Use the table below to select the Retirement Date Fund that is best suited to you. For example: If you plan to retire in 2033, the fund best suited to you is the MLI BlackRock LifePath Index 2035 fund. Specify the 4-digit fund code for the Retirement Date Fund you select in Your investment instructions section on each Application form. If you plan to retire during the period The Retirement Date fund for you is Fund code Before 2016 MLI BlackRock LifePath Index MLI BlackRock LifePath Index MLI BlackRock LifePath Index MLI BlackRock LifePath Index MLI BlackRock LifePath Index MLI BlackRock LifePath Index or later MLI BlackRock LifePath Index If you are close to retirement, there is an income fund MLI BlackRock Retirement Income that might interest you. To see the investment management fees and historical rates of returns for these funds, turn to page 19. Please refer to the Retirement Program Investment Funds information found on the employee portal to obtain a detailed description of each Retirement Date Fund. You have now finished the fund selection process. Please proceed to Step four of this Guide to complete your enrolment. 10

11 Step three How to build your own portfolio To do! Determine your investor style by circling one answer for each question. Write your score shown in brackets at the end of each answer in the box to the right of each question. Tally the scores you record for each question to get your total. Your age, the numbers of years remaining until you retire, and how you feel about risk will determine your investor style. Once you know your investor style, you can choose funds for your retirement savings. Your score 1. What is your investment horizon when will you need this money? a. Within 3 years (0) b. 3-5 years (3) c years (5) d years (8) e years (10) 2. What is your most important investment goal? a. To preserve your money (0) b. To see modest growth in your account (4) c. To see more significant growth in your account (7) d. To earn the highest return possible (10) 3. Please indicate which statement reflects your overall view of managing risk: a. I don t like risk and I am not prepared to expose my investments to any market fluctuations in order to earn higher long-term returns. (0) b. I am prepared to experience modest short-term market fluctuations in order to generate growth of capital. (2) c. I am prepared to experience average short-term market fluctuations in order to achieve a higher long-term return. (4) d. I want to maximize my long-term returns and am comfortable with significant short-term market fluctuations. (6) 11

b.")

12 Step three 4. If you owned an investment that declined by 20% over a short period, what would you do? a. Sell all of the remaining investment (0) b. Sell a portion of the remaining investment (2) c. Hold the investment and sell nothing (4) d. Buy more of the investment (6) 5. If you could increase your chances of improving your investment returns by taking more risk, would you: a. Be unlikely to take more risk (0) b. Be willing to take a little more risk with some of your portfolio (2) c. Be willing to take a lot more risk with some of your portfolio (4) d. Be willing to take a lot more risk with your entire portfolio (6) 6. The following picture shows three model portfolios and the highest and lowest returns each is likely to earn in any given year. Which portfolio would you be most likely to hold? Return (%) a. Portfolio A (0) b. Portfolio B (3) c. Portfolio C (6) Portfolio A Portfolio B -12 Portfolio C 7. After several years of following your retirement plan, you review your progress and determine you are behind schedule and will need to modify your strategy in order to retire at your preferred age. What would you do? a. Keep the same investments you currently hold, but increase your contributions as much as possible. (0) b. Slightly increase your exposure to riskier investments and slightly increase your contributions. (3) c. Move your entire portfolio to riskier investments, hoping to achieve the highest long-term return. (6) 12

6. The following picture shows three model portfolios and the highest and lowest returns each is likely to earn in any given year.")

13 Step three 8. Which statement best applies to your approach regarding achieving your retirement income goals on time? a. I must achieve my financial goal by my target retirement date. (0) b. I would like to come close to achieving my financial goal by my target retirement date. (2) c. If I have not reached my financial goal by my target retirement date, I have the flexibility to delay my target retirement date. (4) d. I re-evaluate my financial goals and target retirement date regularly and have the flexibility to adjust them to align with the performance of my investments. (6) Your total score: Match your score to an investor style below. If your score is between Your investor style is About your investor style 0 7 Conservative Protecting your money is your chief concern. You may be approaching retirement, or simply prefer to take a cautious approach to investing and preserve your money Moderate You want your money to grow, but are more concerned about protecting it. Retirement may be in your near future or you may prefer to be cautious with your investments and preserve your money Balanced You want a balance between growth and security although you will accept some risk to have the potential for higher returns over time Growth You want to increase your money and are somewhat comfortable riding the ups and downs of the market in exchange for the possibility of higher returns over the long term. You may have time on your side until you retire Aggressive You want to maximize the long-term growth of your retirement savings. You understand the ups and downs of the markets and are comfortable taking a lot of risk to maximize potential returns. You have plenty of time to wait out market cycles until you retire. My investor style is: 13

14 Step three To do! Your investor style (from page 13): Find the sample portfolio that matches your investor style. You can use the sample portfolios as a guideline to help you choose individual funds. To ensure you create a well-diversified portfolio, select at least one fund from each asset class. Specify the percentage of contributions you want to invest in each fund in Your investment instructions section on each Application form. Each asset class in the sample portfolio is represented by a different colour. For example, all Fixed Income funds are blue, and all U.S. Equity fund descriptions are orange. Keep this in mind when researching and choosing funds to invest in. You should also consider how your savings outside of this plan are invested. Your other investments may already fulfill some parts of the sample portfolios. The guidelines provided are only suggestions. If your investor style is... Conservative A recommended asset mix for you is... International Equity and Global Equity 5% U.S. Equity 5% Canadian Money Market and GIAs 12% Canadian Large Cap Equity 10% Fixed Income 68% Moderate International Equity and Global Equity 8% Canadian Money Market and GIAs 7% U.S. Equity 7% Canadian Small Cap Equity 5% Canadian Large Cap Equity 20% Fixed Income 53% 14

15 International Equity and Global Equity 8% Step three If your investor style is... A recommended asset mix for you is... Balanced International Equity and Global Equity 13% Canadian Money Market and GIAs 5% U.S. Equity 11% Canadian Small Cap Equity 6% Canadian Large Cap Equity 30% Canadian Money Market and GIAs 5% Fixed Income 35% International Equity and Global Equity 17% International Equity Growth and Global Equity 17% Fixed Income 20% U.S. Equity 15% U.S. Equity 15% Canadian Small Cap Equity 9% Canadian Large Cap Equity 39% Aggressive International Equity and Global Equity 21% U.S. Equity 19% Canadian Large Cap Equity 44% Canadian Small Cap Equity 16% Actions américaines 5 % Actions canadiennes à forte capitalisation 10 % Actions internationales et mondiales 5 % Marché monétaire et comptes à intérêt garanti 12 % Actions américaines 7 % Actions canadiennes à faible et moyenne capitalisation 5 % Actions internationa et mondiales 8 % 15

16 Step three Asset class Fund name Fund code Money Market MLI Canadian Money Market (MAM) 3132 Fixed Income MLI PH&N Bond 4271 Canadian Equity MLI McLean Budden Canadian Equity 7164 U.S. Equity MLI ING U.S. Large Cap Growth 8771 International Equity MLI Sprucegrove International Equity 8361 Global Equity MLI CIBC Renaissance Global Growth 8202 You can find descriptions of all available funds on the employee portal under Retirement Program Investment Funds. To see the investment management fees and historical rates of returns for these funds, turn to page 19. You have now finished the fund selection process. Please proceed to Step four of this Guide to complete your enrolment. 16

17 Step four Check to see you ve completed each step To do! Make sure you ve fully completed your enrolment. Have you... Completed Your personal information? Named your beneficiary (or beneficiaries)? Provided instructions on how to invest contributions? Signed and dated each form? 17

?")

18 Step four You ve successfully enrolled What s next? If you enrolled online You received your Customer Number and chose your Personal Identification Number (PIN) at the end of the enrolment process. You can use this information to access your account online anytime. Instructions for accessing your account online appear below. If you enrolled using paper forms You ll receive a letter from Manulife welcoming you to your group program. This letter will provide your Customer Number and explain how to get your Personal Identification Number (PIN). With your Customer Number and PIN, you can access the online tools Manulife offers to help you track and manage your savings. How can I track the progress of my account? Member statements You ll receive easy-to-understand member statements updating you about your account activity and growth. Internet You can access your account information 24 hours a day, 7 days a week at Phone You can contact Customer Service at to speak with a Manulife customer service representative, Monday to Friday from 8 a.m. to 8 p.m. ET. 18

.")

19 Your Investment Choices Market-based funds The investments available through your plans appear here. The rates of return in this chart reflect performance before investment management fees (IMFs) are deducted. Benchmark returns are also provided to help you compare fund performance. These returns, marked in italics, are for comparison purposes only and are not available for investment. 19

20 20

21 Forms Here is a list of forms found in your Enrolment Guide: An Application form for the Registered Pension Plan 21

22 The personal information statement Your consent to use your personal information By signing this Application form, you give your consent for us to obtain, verify, and share your personal information, as set out below, in administering your account, now and in the future, with the plan sponsor, the plan administrator, the plan advisor and its employees and other parties in the performance of their duties for us. You authorize us to use your Social Insurance Number (SIN) if applicable, to uniquely identify you during the administration of your account. How we will maintain and use your personal information You agree that we may use the personal information that we collect to: comply with legal and regulatory requirements, confirm your identity and the accuracy of the information you ve provided, conduct searches to locate you and update your member information, administer this plan while you actively work for your employer, and after you no longer work with your employer, administer any other products and service that we provide to you, and determine your eligibility for, and provide you with details of, other select financial products or services that may be of interest to you that are offered by us, our affiliates or other select financial product providers. Who may access your personal information The following individuals may have access to your personal information: our employees and representatives who require this information to do their jobs, the plan advisor, including its employees, appointed by your Plan Sponsor to provide ongoing benefit counselling or plan administrative services, people to whom you have granted access, people who are legally authorized to view your personal information, and service providers who require this information to do their jobs. This may include data processing, programming, printing, mailing, distribution, research and marketing or administration and investigation services. Asking us not to use your personal information You may withdraw your consent for us to use your SIN for non-tax administration purposes. You may also withdraw your consent for us to use your personal information to provide you with other product or service offerings, except those that are mailed with your statements. If you wish to withdraw your consent for us to collect, use, retain or share your personal information, you may contact us by phoning our customer service centre at or by writing to the Privacy Officer at the address below. How long we can keep your personal information You authorize us to keep your personal information for the longer of: the time period required by law and by guidelines set for the financial services industry, and the time period required to administer the products and services we provide. The information we collect with your consent will be protected and maintained in your Manulife plan member file. The personal information that we must have You may not withdraw your consent for us to collect, use, retain or share personal information that we need to issue or administer your account unless federal or provincial laws give you this right. If you do so, we may no longer be able to properly administer your account and this is what could happen: benefits will not be payable as provided under the plan, we may treat your withdrawal of consent as a request to terminate your contract, and your rights, and the rights of your beneficiary or estate under the plan may be limited. Recording your customer service calls to us We may record your customer service calls to us for the following reasons: quality service controls, information verification, and training. If you do not wish to have your calls recorded, you must communicate with us in writing to Group Retirement Solutions, 25 Water Street South, Kitchener, ON N2G 4Y5, and request that any response by us also be in writing. Questions, updates and requests for additional information If you have a request, a concern, or wish to receive more information about our privacy policies, or if you wish to review your personal information in our files or correct any inaccuracies, you may contact us by sending a written request to: Privacy Officer, Group Retirement Solutions, 25 Water Street South, Kitchener ON N2G 4Y5. 22 The Manufacturers Life Insurance Company Retain a copy for your files. GP0760E Wat (04/2011)

23 Please print clearly in the blank boxes. Application Form Registered Pension Plan (RP P) If you aren t sure how to complete any of these boxes, your Plan Administrator can help you or you can call Customer Service at Tell us about the plan Plan Sponsor/Employer Policy number Coca-Cola Refreshments Member number Date you started with your employer (mmm/dd/yyyy) Date you are joining the plan (mmm/dd/yyyy) Division Member class Province of Employment Union (Post January 1, 2012) Your personal information Gender First name Middle initial Last name Mailing address (number, street and apartment number) City Province Country Postal Code Your preferred language Date of birth (mmm/dd/yyyy) Social Insurance Number (SIN) Marital status Home telephone number Spouse s name (optional) Spouse s date of birth (mmm/dd/yyyy) (optional) Work telephone number Ext. Personal address A revocable beneficiary can be changed at anytime. An irrevocable beneficiary can only be changed with written consent from that beneficiary. You will also need your beneficiary s consent to withdraw or transfer money from your account A parent or guardian cannot provide consent on behalf of a minor who has been named as irrevocable beneficiary. If you want to name more than three beneficiaries, attach a separate page with the names and the percentage of proceeds for each beneficiary. If you have locked-in money in your RPP and you have a spouse on the date of your death, the law may require any death benefit be paid to your spouse, regardless of other beneficiaries you ve named. If you die while your beneficiary is still a minor, the trustee you name on this form will act on the child s behalf. Name your beneficiary (or beneficiaries) If you do not name a beneficiary and you do not have a spouse at the date of your death, proceeds will be paid to your estate. Check here if you have attached a separate page listing your beneficiaries. Please sign and date. Name Relationship Percentage of proceeds The above beneficiary designations are considered revocable unless you write irrevocable in the chart above. For Quebec only: The designation of a spouse as beneficiary is deemed to be irrevocable unless specified here: Trustee for a minor beneficiary named above (not applicable in Quebec) Any payment to a beneficiary who is a minor will be paid in trust to the trustee named below. In Quebec, the proceeds will be paid in trust to the minor child's tutor. Trustee name Relationship Revocable The Manufacturers Life Insurance Company Retain a copy for your files. GP0761E CCRC Union Post (01/2012) 23

24 Your investment instructions If you do not complete this section, or the total does not add up to 100%, your contributions will be invested in the plan default fund. You can go online at anytime to change the funds you have chosen. The minimum amount you can invest in a fund is 5%. Percentages must be whole numbers. Note: the investment performance of a market-based fund is not guaranteed. Follow the instructions on page 3 of your Fund Selection Guide to see what type of investor you are. Then fill in one of the sections below according to your type. Complete if Retirement Date Fund is your investment strategy 1. Follow the instructions starting on page 4 of your Fund Selection Guide to choose your Retirement Date Fund. 2. Write in the 4-digit fund code for your Retirement Date Fund below. Fund code Fund name Percentage of your contribution MLI BlackRock LifePath Index Fund 100% Complete if Build your own portfolio is your investment strategy 1. Follow the instructions starting on page 5 of your Fund Selection Guide to determine your investor style and choose your funds. 2. Specify the percentage of contributions you want to invest in each fund. Your percentages must add to 100%. Fund code Fund name % 3132 MLI Canadian Money Market Fund MLI PH&N Bond Fund MLI McLean Budden Canadian Equity Fund MLI CIBC Renaissance Global Growth Equity Fund MLI Sprucegrove International Equity Fund MLI ING US Large Cap Growth Equity Fund Your percentages must add up to 100%. 100% Send your completed form to: Manulife Financial Attn: GRS Client Services, KC-6 PO BOX 396 STN WATERLOO WATERLOO, ON N2J 4A9 Please sign here I confirm that I have read, understood and agreed to the information in this form, including the Enrolment and Registration Authorization section below, and the Personal Information Statement. I also confirm that information in this form is correct to the best of my knowledge. Enrolment and Registration Authorization I request that Manulife enrol me as a Member in this plan. If applicable, I authorize the Plan Sponsor/Employer to deduct my contributions to the plan from my earnings. If I have selected Group IncomePlus, I acknowledge that I have read and understood The Bold Print and by signing below, I agree to the terms, conditions and fees applicable to that option. Your signature Date signed (mmm/dd/yyyy) Plan administrator s signature Date signed (mmm/dd/yyyy) For Manulife use Manulife customer number Date (mmm/dd/yyyy) 24 The Manufacturers Life Insurance Company Retain a copy for your files. GP0761E CCRC Union Post (01/2012)

25 Notes 25

26 26 Notes

27 27

28 Questions? Contact Manulife Visit us at Log in to access your account. Through the secure website, you can: Check your account balance and view a summary of contributions Transfer money between investments Get current unit values Change the amount you contribute to the plan through payroll deduction Activate the RRSP Contribution Limit Monitoring service on your account View your personal rates of return for each individual investment and for your overall plan Get detailed investment information, such as fund profiles, retirement planning tools and much more Call the Customer Service Centre toll-free at Bilingual Customer Service Representatives will answer account inquiries Monday to Friday from 8 a.m. to 8 p.m. ET. Financial Education Specialists offer assistance by answering questions about investments and retirement planning Monday to Friday from 9 a.m. to 5 p.m. Via at [email protected]. Group Retirement Solutions' group retirement products and services are offered through Manulife Financial (The Manufacturers Life Insurance Company). Manulife, Manulife Financial, Manulife Financial For Your Future logo and the block design are service marks and trademarks of The Manufacturers Life Insurance Company and are used by it and its affiliates under license. Coca-Cola Union DC RPP EG/FSG (11/2012) 03892d

Determine what type of investor you are

Determine what type of investor you are Answer the questions below to determine whether you should build your own portfolio or select a single, ready-made fund. A How interested are you in selecting investments

Determine what type of investor you are Answer the questions below to determine whether you should build your own portfolio or select a single, ready-made fund. A How interested are you in selecting investments

Schneider Electric Canada Defined Contribution Pension Plan

Schneider Electric Canada Defined Contribution Pension Plan Agenda About Manulife Financial Defined Contribution (DC) Pension Plan Investment Selection Manulife Tools, Resources and Support Services Next

Schneider Electric Canada Defined Contribution Pension Plan Agenda About Manulife Financial Defined Contribution (DC) Pension Plan Investment Selection Manulife Tools, Resources and Support Services Next

EMPIRE LIFE GUARANTEED INVESTMENT FUNDS 75/100 APPLICATION FOR A NOMINEE/INTERMEDIARY ACCOUNT

VERSION DATE: NOVEMBER 2014 EMPIRE LIFE GUARANTEED INVESTMENT FUNDS 75/100 APPLICATION FOR A NOMINEE/INTERMEDIARY ACCOUNT Upon receiving confirmation of your contract purchase please record your contract

VERSION DATE: NOVEMBER 2014 EMPIRE LIFE GUARANTEED INVESTMENT FUNDS 75/100 APPLICATION FOR A NOMINEE/INTERMEDIARY ACCOUNT Upon receiving confirmation of your contract purchase please record your contract

so sodexo Welcome to Your Sodexo Retirement Program Your future P L A N O V E R V I E W A valuable benefit that lets you share in Sodexo s success

P L A N O V E R V I E W Your future so sodexo Welcome to Your Sodexo Retirement Program A valuable benefit that lets you share in Sodexo s success SOD_Enroll_Guide Mar_09 09IAS-03-003 2009 ING Institutional

P L A N O V E R V I E W Your future so sodexo Welcome to Your Sodexo Retirement Program A valuable benefit that lets you share in Sodexo s success SOD_Enroll_Guide Mar_09 09IAS-03-003 2009 ING Institutional

Group Retirement Savings Plan. Registered Retirement Savings Plan and Deferred Profit Sharing Plan

Group Retirement Savings Plan Registered Retirement Savings Plan and Deferred Profit Sharing Plan FutureStep is an innovative group retirement savings plan designed to help businesses like yours be competitive

Group Retirement Savings Plan Registered Retirement Savings Plan and Deferred Profit Sharing Plan FutureStep is an innovative group retirement savings plan designed to help businesses like yours be competitive

Plan at a glance: University of Saskatchewan Group Retirement Fund Prescribed Retirement Income Fund PRIF Registered Retirement Income Fund RRIF

Plan at a glance: Group Retirement Prescribed Retirement Income PRIF Registered Retirement Income RRIF Your plan at a glance We know how hard you have saved for your future. Now it s time for you to make

Plan at a glance: Group Retirement Prescribed Retirement Income PRIF Registered Retirement Income RRIF Your plan at a glance We know how hard you have saved for your future. Now it s time for you to make

Group Retirement Savings Plan for Ryerson University CUPE 3904 PT&S

Group Retirement Savings Plan for Ryerson University CUPE 3904 PT&S Prepared June 2009 Policy/Plan Number 42745 Ryerson Group Retirement Pension Plan Table of Contents An Introduction to your Group Plan,

Group Retirement Savings Plan for Ryerson University CUPE 3904 PT&S Prepared June 2009 Policy/Plan Number 42745 Ryerson Group Retirement Pension Plan Table of Contents An Introduction to your Group Plan,

my plan Simplified Pension Plan for Employees of Bishop s University Member Booklet

my plan Simplified Pension Plan for Employees of Bishop s University Member Booklet Client ID 2RT-01 May 2015 Table of Contents Introduction... 1 What type of plan do I have?... 1 What are my responsibilities?...

my plan Simplified Pension Plan for Employees of Bishop s University Member Booklet Client ID 2RT-01 May 2015 Table of Contents Introduction... 1 What type of plan do I have?... 1 What are my responsibilities?...

YOUR GOVERNMENT OF NEWFOUNDLAND AND LABRADOR MONEY PURCHASE PENSION PLAN (GMPP)

") Government of NL Money Purchase Pension Plan for Substitute Teachers YOUR GOVERNMENT OF NEWFOUNDLAND AND LABRADOR MONEY PURCHASE PENSION PLAN (GMPP) General Type of Plan Eligibility You will receive a

Government of NL Money Purchase Pension Plan for Substitute Teachers YOUR GOVERNMENT OF NEWFOUNDLAND AND LABRADOR MONEY PURCHASE PENSION PLAN (GMPP) General Type of Plan Eligibility You will receive a

The Quebec Voluntary Retirement Savings Plan (VRSP) An overview of the newly announced workplace retirement savings plan

An overview of the newly announced workplace retirement savings plan") The Quebec Voluntary Retirement Savings Plan (VRSP) An overview of the newly announced workplace retirement savings plan Use this summary of Quebec s recently-introduced Voluntary Retirement Savings Plan

The Quebec Voluntary Retirement Savings Plan (VRSP) An overview of the newly announced workplace retirement savings plan Use this summary of Quebec s recently-introduced Voluntary Retirement Savings Plan

my plan Husky Oil Operations Limited Retirement Program Defined Contribution Pension Plan Group Registered Retirement Savings Plan Member Booklet

my plan Husky Oil Operations Limited Retirement Program Defined Contribution Pension Plan Group Registered Retirement Savings Plan Member Booklet For Manitoba permanent employees Client ID 16R-01 Prepared

my plan Husky Oil Operations Limited Retirement Program Defined Contribution Pension Plan Group Registered Retirement Savings Plan Member Booklet For Manitoba permanent employees Client ID 16R-01 Prepared

How To Maximize Your Retirement Savings From The Western Retirement Plan

Retirement Plan Summary july 2013 » Table of Contents Welcome to Your Retirement Journey...3 Important Note...4 Your Plan at a Glance...5 Your Responsibilities...6 Joining the Plan...7 Regular Full-time

Retirement Plan Summary july 2013 » Table of Contents Welcome to Your Retirement Journey...3 Important Note...4 Your Plan at a Glance...5 Your Responsibilities...6 Joining the Plan...7 Regular Full-time

The Road to Retirement: Beginning your journey

The Road to Retirement: Beginning your journey CSS Pension Plan Welcome! This Road to Retirement series has been designed to help you understand your pension plan, and save for retirement. [When you see

The Road to Retirement: Beginning your journey CSS Pension Plan Welcome! This Road to Retirement series has been designed to help you understand your pension plan, and save for retirement. [When you see

Solut!ons for financial planning

Understanding your options this RRSP season 16 Solut!ons for financial planning Consider mutual funds and segregated fund contracts You ve likely heard it before: you should regularly contribute to a Registered

Understanding your options this RRSP season 16 Solut!ons for financial planning Consider mutual funds and segregated fund contracts You ve likely heard it before: you should regularly contribute to a Registered

my money @ work my Investments Canada Post Corporation Defined Contribution and Group Retirement Savings Plans

my money @ work my Investments Canada Post Corporation Defined Contribution and Group Retirement Savings Plans my money. my tools. As a member of a company group retirement savings plan, you have access

my money @ work my Investments Canada Post Corporation Defined Contribution and Group Retirement Savings Plans my money. my tools. As a member of a company group retirement savings plan, you have access

universal life UNIVERSAL LIFE INVESTOR PROFILER QUESTIONNAIRE

universal life UNIVERSAL LIFE INVEST PROFILER QUESTIONNAIRE UNIVERSAL LIFE INVEST PROFILER QUESTIONNAIRE Universal life combines the benefits of cost-effective life insurance protection with tax-advantaged

universal life UNIVERSAL LIFE INVEST PROFILER QUESTIONNAIRE UNIVERSAL LIFE INVEST PROFILER QUESTIONNAIRE Universal life combines the benefits of cost-effective life insurance protection with tax-advantaged

Local 804 Pension Plan

Local 804 Pension Plan A guide to your pension plan benefits Union Benefit Plans Services Contact Contact us If you have any questions about the plan, please contact the plan administrator: Union Benefit

Local 804 Pension Plan A guide to your pension plan benefits Union Benefit Plans Services Contact Contact us If you have any questions about the plan, please contact the plan administrator: Union Benefit

Administration PIVOTAL SOLUTIONS/PIVOTAL SOLUTIONS DSC. Savings and Retirement. Retirement Income Fund Life Income Fund

Administration PIVOTAL SOLUTIONS/PIVOTAL SOLUTIONS DSC Savings and Retirement Retirement Income Fund Life Income Fund Name of Advisor (please print) Advisor Code OR FundSERV Sales Rep. ID (only one - whichever

Administration PIVOTAL SOLUTIONS/PIVOTAL SOLUTIONS DSC Savings and Retirement Retirement Income Fund Life Income Fund Name of Advisor (please print) Advisor Code OR FundSERV Sales Rep. ID (only one - whichever

Group Retirement Savings Plan for the Province of New Brunswick

All Members Group Retirement Savings Plan for the Province of New Brunswick Dear plan member, To help you* achieve financial security during your retirement years, the Province of New Brunswick has established

All Members Group Retirement Savings Plan for the Province of New Brunswick Dear plan member, To help you* achieve financial security during your retirement years, the Province of New Brunswick has established

Are you online? Sign up to mypensionplan and get your pension information online, anytime.

Member Handbook Are you online? Sign up to mypensionplan and get your pension information online, anytime. Go Green! Help the environment and eliminate paper waste by registering on mypensionplan. We ll

Member Handbook Are you online? Sign up to mypensionplan and get your pension information online, anytime. Go Green! Help the environment and eliminate paper waste by registering on mypensionplan. We ll

Application for a. Single Premium Immediate Annuity

Application for a Single Premium Immediate Annuity BMO Life Assurance Company 60 Yonge Street, Toronto, Ontario, Canada M5E 1H5 Tel 416-596-3900 Fax 416-596-4143 Toll Free 1-877-742-5244 348E (2010/11/18)

Application for a Single Premium Immediate Annuity BMO Life Assurance Company 60 Yonge Street, Toronto, Ontario, Canada M5E 1H5 Tel 416-596-3900 Fax 416-596-4143 Toll Free 1-877-742-5244 348E (2010/11/18)

Retires in. Bob plans to retire in 2039. He s somewhat concerned about fluctuating investment values, so you could call him a balanced investor.

Harmonized risk-adjusted target date funds Investing in your retirement has never been easier with Harmonized risk-adjusted target date funds. Think of risk-adjusted target date funds as a single-fund

Harmonized risk-adjusted target date funds Investing in your retirement has never been easier with Harmonized risk-adjusted target date funds. Think of risk-adjusted target date funds as a single-fund

EMPIRE CLASS SEGREGATED FUNDS INFORMATION FOLDER AND POLICY PROVISIONS THE EMPIRE LIFE INSURANCE COMPANY

THE EMPIRE LIFE INSURANCE COMPANY EMPIRE CLASS SEGREGATED FUNDS INFORMATION FOLDER AND POLICY PROVISIONS This document contains the information folder and the contract provisions for the Empire Class Segregated

THE EMPIRE LIFE INSURANCE COMPANY EMPIRE CLASS SEGREGATED FUNDS INFORMATION FOLDER AND POLICY PROVISIONS This document contains the information folder and the contract provisions for the Empire Class Segregated

Application/Instructions Form. TFSA Savings Annuity T087 (06-2015)

") Application/Instructions Form TFSA Savings Annuity T087 (06-2015) Application/Instructions Form TFSA Savings Annuity New client? Yes If so, complete the Contractholder s Identification section No If not,

Application/Instructions Form TFSA Savings Annuity T087 (06-2015) Application/Instructions Form TFSA Savings Annuity New client? Yes If so, complete the Contractholder s Identification section No If not,

ScotiaMcLeod Investment Planning Questionnaire

ScotiaMcLeod Investment Planning Questionnaire Your responses to this questionnaire are very important. They will provide the basis for us to evaluate your risk tolerance level that will be used to develop

ScotiaMcLeod Investment Planning Questionnaire Your responses to this questionnaire are very important. They will provide the basis for us to evaluate your risk tolerance level that will be used to develop

Planning Retirement. Information for BCGEU Pension Plan Members

Planning Retirement Information for BCGEU Pension Plan Members January 2012 PAGE ONE PAGE TWO PAGE THREE PAGE FOUR PAGE FIVE PAGE SIX PAGE SEVEN PAGE EIGHT PAGE NINE PAGE TWELVE TABLE OF CONTENTS Preparing

Planning Retirement Information for BCGEU Pension Plan Members January 2012 PAGE ONE PAGE TWO PAGE THREE PAGE FOUR PAGE FIVE PAGE SIX PAGE SEVEN PAGE EIGHT PAGE NINE PAGE TWELVE TABLE OF CONTENTS Preparing

Early Retirement Strategies

If you or a member of your family is facing a permanent lay-off, voluntary early retirement or forced early retirement, there are many important decisions to be made decisions that can have a significant

If you or a member of your family is facing a permanent lay-off, voluntary early retirement or forced early retirement, there are many important decisions to be made decisions that can have a significant

Making the Best Choice for Your Future Survivor Pension Options

Making the Best Choice for Your Future Survivor Pension Options How does the death of my pension partner affect my pension benefits? What options do I have? And what action must I take next in order to

Making the Best Choice for Your Future Survivor Pension Options How does the death of my pension partner affect my pension benefits? What options do I have? And what action must I take next in order to

Self Directed Investment Account Handbook. Managing Your Own Investments Through a Schwab Personal Choice Retirement Account

Self Directed Investment Account Handbook Managing Your Own Investments Through a Schwab Personal Choice Retirement Account INTRODUCTION SELF DIRECTED INVESTMENT ACCOUNT OFFERED THROUGH SCHWAB PERSONAL

Self Directed Investment Account Handbook Managing Your Own Investments Through a Schwab Personal Choice Retirement Account INTRODUCTION SELF DIRECTED INVESTMENT ACCOUNT OFFERED THROUGH SCHWAB PERSONAL

Notice to All Employees Eligible to Participate in the Halliburton Retirement and Savings Plan

Notice to All Employees Eligible to Participate in the Halliburton Retirement and Savings Plan Halliburton Company (the Company ) has made saving for retirement under the Halliburton Retirement and Savings

Notice to All Employees Eligible to Participate in the Halliburton Retirement and Savings Plan Halliburton Company (the Company ) has made saving for retirement under the Halliburton Retirement and Savings

MACHINISTS LODGE 692 HEALTH AND BENEFIT PLAN

MACHINISTS LODGE 692 HEALTH AND BENEFIT PLAN REVISED CARD CHECK HERE h APPLICATION FOR ENROLMENT AND BENEFICIARY DESIGNATION Please complete in ink and print clearly. This is a two-sided form please see

MACHINISTS LODGE 692 HEALTH AND BENEFIT PLAN REVISED CARD CHECK HERE h APPLICATION FOR ENROLMENT AND BENEFICIARY DESIGNATION Please complete in ink and print clearly. This is a two-sided form please see

Welcome to your new 401(k) home

home") Welcome to your new 401(k) home Introducing Vanguard... your new 401(k) partner We are excited to welcome Vanguard to the Anheuser-Busch 401(k) Savings and Retirement Plan as our new investment manager,

Welcome to your new 401(k) home Introducing Vanguard... your new 401(k) partner We are excited to welcome Vanguard to the Anheuser-Busch 401(k) Savings and Retirement Plan as our new investment manager,

We respect your privacy and will not disclose this information to any outside parties without your expressed written consent.

CLIENT INTAKE FORM Date: Complete this form prior to your appointment. Please print clearly. If you are unsure of any information, leave it blank. It is okay to approximate amounts and include attachments

CLIENT INTAKE FORM Date: Complete this form prior to your appointment. Please print clearly. If you are unsure of any information, leave it blank. It is okay to approximate amounts and include attachments

SUMMARY PLAN DESCRIPTION

SUMMARY PLAN DESCRIPTION January 2012 DEATH BENEFIT RETIREMENT BENEFIT DISABILITY BENEFIT WITHDRAWAL BENEFIT Introduction The IBEW District Ten NECA Individual Equity Retirement Plan (often referred to

SUMMARY PLAN DESCRIPTION January 2012 DEATH BENEFIT RETIREMENT BENEFIT DISABILITY BENEFIT WITHDRAWAL BENEFIT Introduction The IBEW District Ten NECA Individual Equity Retirement Plan (often referred to

A p p l i c a t i o n f o r a S i n g l e P r e m i u m Pa y o u t A n n u i t y Po l i cy

A p p l i c a t i o n f o r a S i n g l e P r e m i u m Pa y o u t A n n u i t y Po l i cy Registered and Non-Registered In this application, the terms you and your mean the owner of The Canada Life Payout

A p p l i c a t i o n f o r a S i n g l e P r e m i u m Pa y o u t A n n u i t y Po l i cy Registered and Non-Registered In this application, the terms you and your mean the owner of The Canada Life Payout

GROUP LIFE INCOME FUND (LIF) FOR MCGILL FACULTY & STAFF

FOR MCGILL FACULTY & STAFF") GROUP LIFE INCOME FUND (LIF) FOR MCGILL FACULTY & STAFF MY GROUP LIF/RIF PLAN... IN BRIEF At the earlier of your retirement date and attaining age 65, you will be eligible to start receiving a retirement

GROUP LIFE INCOME FUND (LIF) FOR MCGILL FACULTY & STAFF MY GROUP LIF/RIF PLAN... IN BRIEF At the earlier of your retirement date and attaining age 65, you will be eligible to start receiving a retirement

EMPIRE LIFE GUARANTEED INVESTMENT FUNDS 75/75 AND GUARANTEED INVESTMENT FUNDS 75/100 INFORMATION FOLDER AND CONTRACT PROVISIONS

THE EMPIRE LIFE INSURANCE COMPANY EMPIRE LIFE GUARANTEED INVESTMENT FUNDS 75/75 AND GUARANTEED INVESTMENT FUNDS 75/100 INFORMATION FOLDER AND CONTRACT PROVISIONS This document contains the information

THE EMPIRE LIFE INSURANCE COMPANY EMPIRE LIFE GUARANTEED INVESTMENT FUNDS 75/75 AND GUARANTEED INVESTMENT FUNDS 75/100 INFORMATION FOLDER AND CONTRACT PROVISIONS This document contains the information

smart Two Paths to Investing for Retirement Which one is right for you? Massachusetts Deferred Compensation SMART Plan INVEST

smart S A V E M O N E Y A N D R E T I R E T O M O R R O W INVEST Two Paths to Investing for Retirement Which one is right for you? Massachusetts Deferred Compensation SMART Plan Office of the State Treasurer

smart S A V E M O N E Y A N D R E T I R E T O M O R R O W INVEST Two Paths to Investing for Retirement Which one is right for you? Massachusetts Deferred Compensation SMART Plan Office of the State Treasurer

Human Resources A GUIDE TO THE SHELL CANADA PENSION PLAN INITIAL DC AND DB/DC DUO

Human Resources A GUIDE TO THE SHELL CANADA PENSION PLAN INITIAL DC AND DB/DC DUO October 2015 INTRODUCTION Each of us has a responsibility to plan and save for a financially secure retirement. The primary

Human Resources A GUIDE TO THE SHELL CANADA PENSION PLAN INITIAL DC AND DB/DC DUO October 2015 INTRODUCTION Each of us has a responsibility to plan and save for a financially secure retirement. The primary

Investor Guide. RRIF Investing. Managing your money in retirement

Investor Guide RRIF Investing Managing your money in retirement 1 What s inside It s almost time to roll over your RRSP...3 RRIFs...4 Frequently asked questions...5 Manage your RRIF...8 Your advisor...10

Investor Guide RRIF Investing Managing your money in retirement 1 What s inside It s almost time to roll over your RRSP...3 RRIFs...4 Frequently asked questions...5 Manage your RRIF...8 Your advisor...10

CANADIAN MERCHANT SERVICE GUILD

2006 CANADIAN MERCHANT SERVICE GUILD WESTERN BRANCH PENSION PLAN (Towboats) This statement has been prepared for: 2006 CANADIAN MERCHANT SERVICE GUILD WESTERN BRANCH PENSION PLAN (Towboats) Printed March

2006 CANADIAN MERCHANT SERVICE GUILD WESTERN BRANCH PENSION PLAN (Towboats) This statement has been prepared for: 2006 CANADIAN MERCHANT SERVICE GUILD WESTERN BRANCH PENSION PLAN (Towboats) Printed March

Information Booklet. I.A.T.S.E. Local 212

Information Booklet Group Plan 62724 I.A.T.S.E. Local 212 INTRODUCTION The I.A.T.S.E. Canadian Retirement Plan came into effect in 2005. As of September 1, 2008, all the District Councils of the Directors

Information Booklet Group Plan 62724 I.A.T.S.E. Local 212 INTRODUCTION The I.A.T.S.E. Canadian Retirement Plan came into effect in 2005. As of September 1, 2008, all the District Councils of the Directors

Fill in the necessary information corresponding to the account s owner.

IRA APPLICATION It s easy to establish your account. Simply fill out this application, completing all relevant sections, sign in ink and return to: Regular Mail FundX Upgrader Funds c/o US Bancorp Fund

IRA APPLICATION It s easy to establish your account. Simply fill out this application, completing all relevant sections, sign in ink and return to: Regular Mail FundX Upgrader Funds c/o US Bancorp Fund

Highlights of the. Boehringer Ingelheim. Retirement Savings Plan Retirement Plan. This brochure is intended for eligible employees of

Highlights of the Boehringer Ingelheim: Retirement Savings Plan Retirement Plan This brochure is intended for eligible employees of Boehringer Ingelheim hired after December 31, 2003. Table of Contents

Highlights of the Boehringer Ingelheim: Retirement Savings Plan Retirement Plan This brochure is intended for eligible employees of Boehringer Ingelheim hired after December 31, 2003. Table of Contents

Each applicant must provide approved ID or W8/W9*

Page 1 of 8 CIBC Investor s Edge Investment Account Application ORDER EECUTION ONLY ACCOUNT CIBC Investor Services Inc. Please review the Account Agreements and Disclosures Booklet before completing this

Page 1 of 8 CIBC Investor s Edge Investment Account Application ORDER EECUTION ONLY ACCOUNT CIBC Investor Services Inc. Please review the Account Agreements and Disclosures Booklet before completing this

I request a refund in accordance with paragraph 7(b); or

; or") CIBC RETIREMENT SAVINGS PLAN AGREEMENT 1. ESTABLISHMENT OF PLAN: Canadian Imperial Bank of Commerce ( CIBC ) agrees to hold on deposit in a CIBC Retirement Savings Plan (the Plan ) contributions received

CIBC RETIREMENT SAVINGS PLAN AGREEMENT 1. ESTABLISHMENT OF PLAN: Canadian Imperial Bank of Commerce ( CIBC ) agrees to hold on deposit in a CIBC Retirement Savings Plan (the Plan ) contributions received

Professionally Managed Portfolios of Exchange-Traded Funds

ETF Portfolio Partners C o n f i d e n t i a l I n v e s t m e n t Q u e s t i o n n a i r e Professionally Managed Portfolios of Exchange-Traded Funds P a r t I : I n v e s t o r P r o f i l e Account

ETF Portfolio Partners C o n f i d e n t i a l I n v e s t m e n t Q u e s t i o n n a i r e Professionally Managed Portfolios of Exchange-Traded Funds P a r t I : I n v e s t o r P r o f i l e Account

2015 Product Disclosure Statement

2015 Product Disclosure Statement Personal Division Issued 1 November 2015 Contents 1. About NSF Super 2. How super works 3. Benefits of investing with NSF Super 4. Risks of super 5. How we invest your

2015 Product Disclosure Statement Personal Division Issued 1 November 2015 Contents 1. About NSF Super 2. How super works 3. Benefits of investing with NSF Super 4. Risks of super 5. How we invest your

Direct Rollover IRA Form

Direct Rollover IRA Form PO Box 55932 Boston, MA 02205-5932 800-379-7603 Use this form to invest an eligible rollover distribution from an employer s retirement plan into a new or existing IRA at Janus.

Direct Rollover IRA Form PO Box 55932 Boston, MA 02205-5932 800-379-7603 Use this form to invest an eligible rollover distribution from an employer s retirement plan into a new or existing IRA at Janus.

Protect your plan savings for retirement. New York University 457(b) Deferred Compensation Plan

Deferred Compensation Plan") Protect your plan savings for retirement New York University 457(b) Deferred Compensation Plan Whether you have left the workforce or have simply changed employers, it is important to protect the money

Protect your plan savings for retirement New York University 457(b) Deferred Compensation Plan Whether you have left the workforce or have simply changed employers, it is important to protect the money

Vanguard Financial Education Series investing. How to invest your retirement savings

Vanguard Financial Education Series investing How to invest your retirement savings During your working life, you ve saved and invested for retirement. Now that you re finally reaching retirement, consider

Vanguard Financial Education Series investing How to invest your retirement savings During your working life, you ve saved and invested for retirement. Now that you re finally reaching retirement, consider

Mailing Address: Des Moines, IA 50392-0001

Mailing Address: Des Moines, IA 50392-0001 Principal Life Insurance Company Complete this form to withdraw part of the retirement account in cash while still employed. Participant/Spouse complete Sections

Mailing Address: Des Moines, IA 50392-0001 Principal Life Insurance Company Complete this form to withdraw part of the retirement account in cash while still employed. Participant/Spouse complete Sections

Workplace Education Series. Making the Most of Your New Workplace Savings Plan

Making the Most of Your New Workplace Savings Plan Making the Most of Your New Workplace Savings Plan Guiding you through exciting plan changes ahead Today s agenda: New plan features Steps to prioritizing

Making the Most of Your New Workplace Savings Plan Making the Most of Your New Workplace Savings Plan Guiding you through exciting plan changes ahead Today s agenda: New plan features Steps to prioritizing

www.mnsaves.org ENROLLMENT MATERIALS

ENROLLMENT MATERIALS www.mnsaves.org Why should you save for college? What you might need. Paying for a college education can be one of the most pressing family financial challenges. Although it may seem

ENROLLMENT MATERIALS www.mnsaves.org Why should you save for college? What you might need. Paying for a college education can be one of the most pressing family financial challenges. Although it may seem

Brock University Pension Plan

Brock University Pension Plan Contents Part 1: Your future is worth the investment 3 For more information 3 Part 2: Welcome to the pension plan 4 A hybrid plan 4 More than a retirement benefit 4 Who pays

Brock University Pension Plan Contents Part 1: Your future is worth the investment 3 For more information 3 Part 2: Welcome to the pension plan 4 A hybrid plan 4 More than a retirement benefit 4 Who pays

YOUR GUIDE TO GETTING STARTED

George Mason University Cash Match Plan (#72170) Invest in your retirement and yourself today, with help from The George Mason 401(a) Match Plan and Fidelity. YOUR GUIDE TO GETTING STARTED Invest some

George Mason University Cash Match Plan (#72170) Invest in your retirement and yourself today, with help from The George Mason 401(a) Match Plan and Fidelity. YOUR GUIDE TO GETTING STARTED Invest some

Your Guide to Retirement Income Planning

Your Guide to Retirement Income Planning Your Guide to Retirement Income Planning 3 Your retirement income plan How to create secure income in retirement Your retirement will be as unique as you are. Travel,

Your Guide to Retirement Income Planning Your Guide to Retirement Income Planning 3 Your retirement income plan How to create secure income in retirement Your retirement will be as unique as you are. Travel,

YOUR PENSION PLAN GUIDE

YOUR PENSION PLAN GUIDE YOUR PLAN Your rights and obligations 2 Understanding your annual pension 3 Plan management 4 How we serve you 5 THE BASICS Automatic membership 7 Contributing to your pension 7

YOUR PENSION PLAN GUIDE YOUR PLAN Your rights and obligations 2 Understanding your annual pension 3 Plan management 4 How we serve you 5 THE BASICS Automatic membership 7 Contributing to your pension 7

An Easy-to-Understand Introduction to the Retirement Plan and the Savings Plan. How the Plans Work. Contributions. Other Benefits

An Easy-to-Understand Introduction to the Retirement Plan and the Savings Plan Annuities How the Plans Work Contributions Eligibility Enrollment Other Benefits November 2015 WELCOME TO THE YMCA RETIREMENT

An Easy-to-Understand Introduction to the Retirement Plan and the Savings Plan Annuities How the Plans Work Contributions Eligibility Enrollment Other Benefits November 2015 WELCOME TO THE YMCA RETIREMENT

CBS & YOU PREPARE. DECIDE. ACT.

YOUR HR/BENEFITS PROGRAM PREPARE. DECIDE. ACT. YOUR HR PORTAL Dear YOUR CBS CBS Employee: 401(K) PLAN Congratulations, you re now eligible to participate in the CBS 401(k) Plan. As you ll see, your CBS

YOUR HR/BENEFITS PROGRAM PREPARE. DECIDE. ACT. YOUR HR PORTAL Dear YOUR CBS CBS Employee: 401(K) PLAN Congratulations, you re now eligible to participate in the CBS 401(k) Plan. As you ll see, your CBS

Investor Profile Questionnaire

Investor Profile Questionnaire Making the right investment choice about your universal life investment portfolio always starts with an understanding of your personal goals and objectives. Working with

Investor Profile Questionnaire Making the right investment choice about your universal life investment portfolio always starts with an understanding of your personal goals and objectives. Working with

McGill University Pension Plan

The presentation can be accessed in online at: www.mcgill.ca/hr/bp/pensions/infosessions. McGill University Pension Plan PENSION PLAN SETTLEMENT OPTIONS INFORMATION SESSION Human Resources This presentation

The presentation can be accessed in online at: www.mcgill.ca/hr/bp/pensions/infosessions. McGill University Pension Plan PENSION PLAN SETTLEMENT OPTIONS INFORMATION SESSION Human Resources This presentation

INVEST EASILY FOR YOUR DAY ONE OF RETIREMENT AND BEYOND SUCCEED. Prudential SmartSolution IRA Investment Guide

SUCCEED SUNRISE PHOTOS TAKEN BY REAL PEOPLE OF THEIR ACTUAL DAY ONES OF RETIREMENT. WHAT WILL YOURS LOOK LIKE? INVEST EASILY FOR YOUR DAY ONE OF RETIREMENT AND BEYOND Prudential SmartSolution IRA Investment

SUCCEED SUNRISE PHOTOS TAKEN BY REAL PEOPLE OF THEIR ACTUAL DAY ONES OF RETIREMENT. WHAT WILL YOURS LOOK LIKE? INVEST EASILY FOR YOUR DAY ONE OF RETIREMENT AND BEYOND Prudential SmartSolution IRA Investment

Retirement Planning Guide

County of Los Angeles 401(k) Savings Plan Retirement Planning Guide El Matador State Beach Inside this guide you will find information on the 401(k) Savings Plan and how it can help you prepare for the

County of Los Angeles 401(k) Savings Plan Retirement Planning Guide El Matador State Beach Inside this guide you will find information on the 401(k) Savings Plan and how it can help you prepare for the

How To Pay Taxes On A Pension From A Retirement Plan

Payout Guide A GUIDE TO OPTIONS FOR YOUR STATE OF MICHIGAN 401(K) AND 457 PLAN ACCOUNTS 1-800-748-6128 http://stateofmi.ingplans.com State of Michigan 401(k) and 457 Plan Participant: You ve worked hard

Payout Guide A GUIDE TO OPTIONS FOR YOUR STATE OF MICHIGAN 401(K) AND 457 PLAN ACCOUNTS 1-800-748-6128 http://stateofmi.ingplans.com State of Michigan 401(k) and 457 Plan Participant: You ve worked hard

Investment Guide Funds offered through the Washington State Investment Board

Investment Guide Funds offered through the Washington State Investment Board Investing Overview Asset allocation 2 Two investment approaches 2 Build and Monitor 3 One-Step 3 Diversification 4 Trading restrictions

Investment Guide Funds offered through the Washington State Investment Board Investing Overview Asset allocation 2 Two investment approaches 2 Build and Monitor 3 One-Step 3 Diversification 4 Trading restrictions

Are you online? Sign up to mypensionplan and get your pension information online, anytime.

Member Handbook Are you online? Sign up to mypensionplan and get your pension information online, anytime. Go Green! Help the environment and eliminate paper waste by registering on mypensionplan. We ll

Member Handbook Are you online? Sign up to mypensionplan and get your pension information online, anytime. Go Green! Help the environment and eliminate paper waste by registering on mypensionplan. We ll

JUNE 2016. Great-West Life investment plans Information folder. Program MANAGED-MONEY. This document is not an insurance contract.

JUNE 2016 Great-West Life investment plans Information folder Program MANAGED-MONEY This document is not an insurance contract. This information folder is not an insurance contract. The information in

JUNE 2016 Great-West Life investment plans Information folder Program MANAGED-MONEY This document is not an insurance contract. This information folder is not an insurance contract. The information in

$17,500 balance in each account at the time of the transfer. Each subsequent transfer into your PCRA must be at least $500.

$17,500 balance in each account at the time of the transfer. Each subsequent transfer into your PCRA must be at least $500. HOW IS THE PCRA DIFFERENT FROM THE PLAN S CORE INVESTMENT OPTIONS? The difference

$17,500 balance in each account at the time of the transfer. Each subsequent transfer into your PCRA must be at least $500. HOW IS THE PCRA DIFFERENT FROM THE PLAN S CORE INVESTMENT OPTIONS? The difference

REVIEWING YOUR TIAA-CREF INCOME CHOICES A GUIDE TO YOUR PAYMENT OPTIONS

REVIEWING YOUR TIAA-CREF INCOME CHOICES A GUIDE TO YOUR PAYMENT OPTIONS FLEXIBILITY & CHOICE TIAA-CREF UNDERSTANDS YOUR FINANCIAL PRIORITIES can change over time, which is why we offer you a wide range

REVIEWING YOUR TIAA-CREF INCOME CHOICES A GUIDE TO YOUR PAYMENT OPTIONS FLEXIBILITY & CHOICE TIAA-CREF UNDERSTANDS YOUR FINANCIAL PRIORITIES can change over time, which is why we offer you a wide range

Salaried Investment and Savings Plan Summary Plan Description (SPD)

") Salaried Investment and Savings Plan Summary Plan Description (SPD) As of January 1, 2012 (Including updates through 7/31/2012) TABLE OF CONTENTS TABLE OF CONTENTS... 1 ABOUT THIS SPD... 3 ISP AT A GLANCE...

Salaried Investment and Savings Plan Summary Plan Description (SPD) As of January 1, 2012 (Including updates through 7/31/2012) TABLE OF CONTENTS TABLE OF CONTENTS... 1 ABOUT THIS SPD... 3 ISP AT A GLANCE...

Define your goals. Understand your objectives.

Define your goals. Understand your objectives. As an investor, you are unique. Your financial goals, current financial situation, investment experience and attitude towards risk all help determine the

Define your goals. Understand your objectives. As an investor, you are unique. Your financial goals, current financial situation, investment experience and attitude towards risk all help determine the

CHOOSING YOUR INVESTMENTS

CHOOSING YOUR INVESTMENTS FOR ASSISTANCE GO ONLINE For more information on your retirement plan, investment education, retirement planning tools and more, please go to www.tiaa-cref.org/carnegiemellon.

CHOOSING YOUR INVESTMENTS FOR ASSISTANCE GO ONLINE For more information on your retirement plan, investment education, retirement planning tools and more, please go to www.tiaa-cref.org/carnegiemellon.

APPLICATION INSTRUCTIONS

VANTAGEPOINT PAYROLL DEDUCTION IRA ACCOUNT APPLICATION INSTRUCTIONS Carefully read the instructions before completing the attached application. You may find it helpful to detach the application and refer

VANTAGEPOINT PAYROLL DEDUCTION IRA ACCOUNT APPLICATION INSTRUCTIONS Carefully read the instructions before completing the attached application. You may find it helpful to detach the application and refer

Customer Investment Profile

Customer Name: Account Number: Contact Number: The purpose of this investment profile form is for us to better understand your financial means, investment experience, investment objectives and general

Customer Name: Account Number: Contact Number: The purpose of this investment profile form is for us to better understand your financial means, investment experience, investment objectives and general

HALIFAX CASH ISA. Conditions and information

HALIFAX CASH ISA. Conditions and information Welcome to Halifax 3 Section 1 How these conditions work 5 Section 2 Special Conditions 7 ISA Saver Variable 12 ISA Saver Online 13 ISA Saver Fixed 14 Junior

HALIFAX CASH ISA. Conditions and information Welcome to Halifax 3 Section 1 How these conditions work 5 Section 2 Special Conditions 7 ISA Saver Variable 12 ISA Saver Online 13 ISA Saver Fixed 14 Junior

Frequently Asked Questions: Lump Sum Reminder

Frequently Asked Questions: Lump Sum Reminder IMPORTANT NOTE: In these Frequently Asked Questions (FAQs), the terms you, I, or my refer to someone who is a former employee of HP or one of its acquired

Frequently Asked Questions: Lump Sum Reminder IMPORTANT NOTE: In these Frequently Asked Questions (FAQs), the terms you, I, or my refer to someone who is a former employee of HP or one of its acquired

Building Your Retirement Portfolio

Building Your Retirement Portfolio With the Help of TIAA-CREF 111075_L01.indd 1 ABOUT TIAA-CREF: For more than 90 years, we at TIAA-CREF have dedicated ourselves to helping those who serve the greater

Building Your Retirement Portfolio With the Help of TIAA-CREF 111075_L01.indd 1 ABOUT TIAA-CREF: For more than 90 years, we at TIAA-CREF have dedicated ourselves to helping those who serve the greater

Base Plan Account Withdrawal

Base Plan Account Withdrawal Purpose of the Form Use this form to choose how you want PERSI to handle the withdrawal of your PERSI Base Plan contributions and interest when you terminate employment with

Base Plan Account Withdrawal Purpose of the Form Use this form to choose how you want PERSI to handle the withdrawal of your PERSI Base Plan contributions and interest when you terminate employment with

JOHNS HOPKINS UNIVERSITY. Retirement Choice Decision Guide. Changes begin January 1, 2016

JOHNS HOPKINS UNIVERSITY Retirement Choice Decision Guide Changes begin January 1, 2016 ACTION REQUIRED BEGINNING OCTOBER 14, 2015 You MUST take action during the Retirement Choice period Between October

JOHNS HOPKINS UNIVERSITY Retirement Choice Decision Guide Changes begin January 1, 2016 ACTION REQUIRED BEGINNING OCTOBER 14, 2015 You MUST take action during the Retirement Choice period Between October

Investment Policy Questionnaire

Investment Policy Questionnaire Name: Date: Ferguson Investment Services, PLLC Investment Policy Questionnaire Introduction: The information you provide on this questionnaire will remain confidential.

Investment Policy Questionnaire Name: Date: Ferguson Investment Services, PLLC Investment Policy Questionnaire Introduction: The information you provide on this questionnaire will remain confidential.

Information Folder and Annuity Policy Client Document Package M.V.P. - RIF. insured by Sun Life Assurance Company of Canada

Information Folder and Annuity Policy Client Document Package Sun Life Assurance Company of Canada M.V.P. - RIF managed by CI Investments Inc. insured by Sun Life Assurance Company of Canada Important

Information Folder and Annuity Policy Client Document Package Sun Life Assurance Company of Canada M.V.P. - RIF managed by CI Investments Inc. insured by Sun Life Assurance Company of Canada Important

Ohio Alternative Retirement Plan

Ohio Alternative Retirement Plan For the State of Ohio Public Higher Education System Your future. Made easier. What is the Ohio Alternative Retirement Plan? The Ohio Alternative Retirement Plan (ARP)

Ohio Alternative Retirement Plan For the State of Ohio Public Higher Education System Your future. Made easier. What is the Ohio Alternative Retirement Plan? The Ohio Alternative Retirement Plan (ARP)