Don t Make Main Street Insurance Consumers Subsidize Wall Street

|

|

|

- Joan Pierce

- 8 years ago

- Views:

Transcription

1 Don t Make Main Street Insurance Consumers Subsidize Wall Street To address the economic turmoil caused by the collapse of several major Wall Street firms, Congress now faces the difficult charge of crafting reform legislation that will address gaps in our current financial services regulatory systems. In so doing, it is imperative that Congress fix what is broken without undermining those portions of the regulatory system that have successfully protected the interest of consumers. Property Casualty Insurance is Not Systemically Risky One sector of the financial services industry where regulation has worked exceptionally well is the state solvency oversight of home, auto and business insurance ( propertycasualty insurance ). The property-casualty insurance industry is stable and healthy and, as an industry, overwhelmingly rejected federal bailout money. The Administration s 2009 white paper on financial regulatory reform explicitly recognized that the current crisis did not stem from widespread problems in the insurance industry. Propertycasualty insurers did not fail during the economic crisis because they are fundamentally different from riskier firms in other parts of the financial services sector. It would be an enormous mistake for Congress to rush towards a one-size-fits-all solution that causes the well-regulated and non-systemically risky insurers on Main Street to subsidize Wall Street firms. Property-Casualty Insurers Have Low Leverage. The financial firms that failed in the recent crisis were highly leveraged. Propertycasualty insurers, which thrived through the crisis, were not highly leveraged their inherent liquidity needs and strict state solvency regulatory oversight do not permit it. In a MSCI Barra Research study of financial leverage in 35 industry sectors during the years , the insurance industry was ranked 28 th while the banking industry was ranked 7 th. The 2009 Economic Report of the President indicated that [b]efore the financial crisis, the major investment banks were leveraged roughly 25 to 1. PCI has calculated that the insurance industry was leveraged at roughly 3 to 1 prior to the financial crisis. Property-casualty insurance is fundamentally about mitigating risk as a service for consumers, not leveraging it for a fee to obtain an investment return for consumers as in other industries. Chart #1 underscores how different property-casualty is from other major financial sectors. Property-Casualty Insurers are Not Interconnected with Other Financial Firms. Banks and securities firms make money in part by taking a risk and then off-loading it elsewhere in transactions with others. Thus, failures within those sectors can have negative impacts on counterparties and can therefore create a domino effect throughout the banking and securities sectors. In contrast, property-casualty insurers own the risks they insure they cannot off-load them. Although they can buy reinsurance to protect their liabilities, reinsurance does not extinguish their liabilities. The risks remain on the primary insurer s books, and there is therefore little counterparty exposure to an insurer failure.

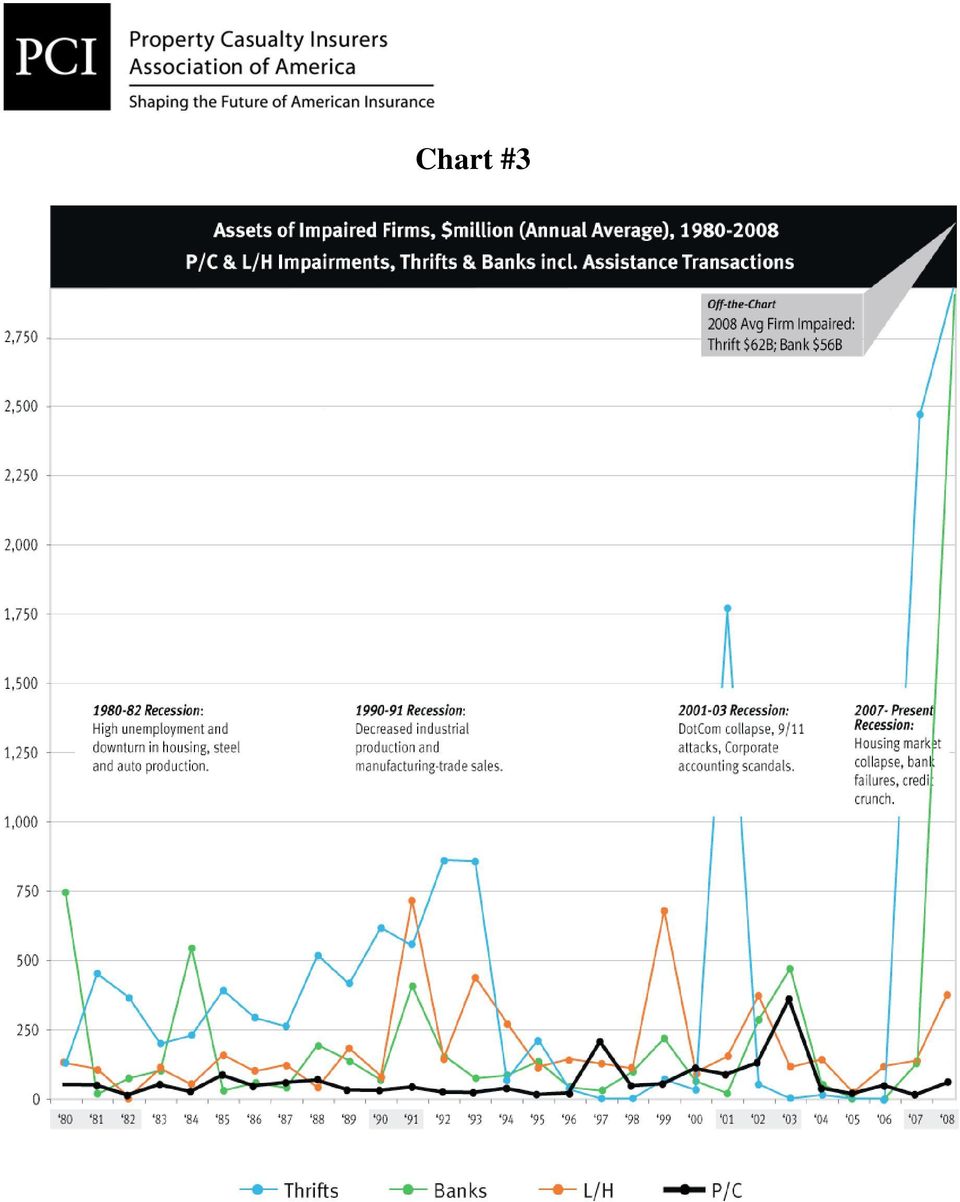

2 No Run on the Bank Threat in the Insurance Industry. Demand and capital supply in the property-casualty industry is also fundamentally distinct from other financial sectors. Consumer and investor fears can trigger a sudden run on a bank or securities firm, leading to loss of highly leveraged capital, a freezing of credit and capital markets, causing cascading interconnectedness failures stemming from the interconnectedness of those firms. There are no runs on property-casualty insurers. Most consumers must have auto insurance to drive, homeowners insurance to protect their investments in their homes, and workers compensation and liability insurance to run a business. There is no extra leveraged cash value or discretionary or investment component to withdraw, no potential for insurer failures to freeze markets, and no interconnectedness that creates a likelihood of cascading failures from one institution to others. Insurers are Highly Competitive with Low Market Concentration. Home, auto, and business insurance markets are extremely competitive, with well over 2,000 companies and very low market concentration among the top firms. Chart #2 lists the concentration indexes for insurers, which are all far below even the level considered to be moderately concentrated by the Department of Justice. In the rare instance that a property-casualty insurer becomes impaired, there are many competitors waiting and able to pick up that business. Moreover, unlike any other industry sector, there are well-run residual markets (i.e., insurers of last resort ) in almost every state to ensure that every property-casualty insurance consumer has access to the market. Property-Casualty Insurers Have Low Failure Rates. Unlike other financial sectors, auto, home, and business insurers have a consistently low and counter-cyclical failure rate. One reason is that property-casualty losses stem from events such as natural disasters that are independent of market cycles. Another reason is that property-casualty insurers are required to hold surplus funds to protect their ability to pay claims to consumers, which means that their investments must be extremely conservative and liquid. Unlike in other financial services industries, economic downturns do not cause insurer failures and insurer failures do not cause economic downturns. Chart #3 shows the low impairment rate of property-casualty insurers as compared to other financial firms and the lack of correlation between insurer impairments and economic downturns. Insurers Already Have Their Own Effective Resolution Authority. Finally, and also unlike some other financial services sectors, most home, auto, and business insurance consumers are fully protected by guaranty funds in every state. If a derivatives firm fails, its investors lose everything. If a property-casualty insurer fails, most policyholders lose nothing. In the last 40 years, the property-casualty insurance guaranty system has paid out roughly $21 billion in policyholder claims on behalf of insolvent insurers. The existing system of state guaranty funds has served the industry and its consumers well and any new federal regulation of the financial services industry should recognize and preserve that system s strong protections. In part because of the state guaranty fund system, even the failure of one of the largest property-casualty holding companies would be unlikely to create systemic risk or require additional government intervention.

3 Fix What is Broken Not What Isn t Some diversified financial firms that conduct insurance activities within their groups did receive federal assistance most notably, AIG. It is critical to recognize, however, that the problems at AIG stemmed not from its property-casualty insurance operations but primarily from risky derivatives trading in one of its non-insurer subsidiaries. No federal assistance has been provided to any company as a result of a failure in its home, auto, or business insurance operations and PCI opposed such subsidies for insurers. It is appropriate for any reform legislation to address risky, non-insurance activities taking place in diversified firms that include insurers. It is not appropriate, however, for those reforms to disturb the strong, non-risky, and well-regulated insurance activities of those firms. Financial services regulatory reform must not overreach into the insurance industry and overturn years of successful state insurance solvency regulation dating back to the 19 th century. Don t break what doesn t need fixing. Home, auto and business insurance are not systemically risky. Protect their consumers and exclude property-casualty insurance from the Financial Stability Improvement Act of HOME AUTO /BUSINESS /INSURANCE Not systemically risky Very low leveraging Low executive compensation and R.O. E. Consistently low failure rate No cyclicality No interconnectedness No run on the bank Very high liquidity Low interconnectedness Low market concentration Low volatility Consumers protected by guaranty fund Residual markets fill any gaps PCI is composed of more than 1,000 member companies, representing the broadest cross-section of insurers of any national trade association. PCI members write over $180 billion in annual premium, 37.4 percent of the nation s property casualty insurance. Member companies write 44 percent of the U.S. automobile insurance market, 30.7 percent of the homeowners market, 35.1 percent of the commercial property and liability market, and 41.7 percent of the private workers compensation market.

4 Chart #1 Financial Industry Sector Distinctions Profitability, Leverage and Executive Compensation Profitability (ROE) P/C Insurers $5.6M Exec Comp Commercial Banks $18.0M Exec Comp L/H Insurers $11.8M Exec Comp Investment Banks $22.1M Exec Comp Leverage Circle size reflects executive compensation Source Information: 1. Profitability is based on industry average annual rate of return; Insurance Information Institute, and Securities Industry and Financial Markets Association. 2. Leverage reflects 2007 Property/Casualty, Life/Health, commercial bank and investment bank results; 2009 Economic Report of the President (banks) and PCI calculations of total liabilities as a proportion of net admitted assets using A.M. Best data (insurers). Chart depicts investment banks levered 25 to 1; commercial banks 12 to 1; L/H insurers 20 to 1; and P/C insurers 3 to Executive compensation is based on annual average CEO compensation from the top three firms in 2008 where data are publicly available; Morningstar.com and for State Farm, P/C Annual Statements and Pantagraph.com newspaper article. Please note the L/H figure is based on the 1 st, 4 th and 7 th largest L/H insurers as executive compensation figures are not publicly available for all of the top three; similarly, the commercial banks figure is based on the 2 nd, 3 rd and 5 th largest firms; and the investment banks figure is based on the 2 nd - 4 th largest firms. In the chart above, the size of each industry s circle represents executive compensation: P/C insurers $5.6 million; L/H insurers $11.8 million; commercial banks $18.0 million; investment banks $22.1 million.

and PCI calculations of total liabilities as a")

5 P/C Market Concentration Analysis Chart #2 Herfindahl-Hirschman Index (HHI) based on 2007 U.S. Total (all states and DC) HHI HHI Number of Line Indiv. Cos. Groups Indiv. Cos. Groups Homeowners Personal Auto Commercial Auto Commercial Multi-Peril Workers Compensation Other Liability Medical Malpractice Product Liability Notes: 1. The HHI takes into account the relative size and distribution of the firms in a market and approaches zero when a market consists of a large number of firms of relatively equal size. The HHI increases both as the number of firms in the market decreases and as the disparity in size between those firms increases. 2. Markets in which the HHI is between 1000 and 1800 points are considered to be moderately concentrated, and those in which the HHI is in excess of 1800 points are considered to be concentrated. Source: NAIC Annual Statement Database via National Underwriter Insurance Data Services/Highline Data The Herfindahl-Hirschman Index (HHI) is a commonly accepted measure of market concentration and indicator of the level of competition amongst firms within an industry. It is an economic concept but widely applied in competition law and antitrust, and utilized by the U.S. Department of Justice and the Federal Trade Commission. The HHI shown above is calculated on an individual company and company group basis for comparison.

6 Chart #3

PROPERTY/CASUALTY INSURANCE AND SYSTEMIC RISK

PROPERTY/CASUALTY INSURANCE AND SYSTEMIC RISK Steven N. Weisbart, Ph.D., CLU Chief Economist President April 2011 INTRODUCTION To prevent another financial meltdown like the one that affected the world

PROPERTY/CASUALTY INSURANCE AND SYSTEMIC RISK Steven N. Weisbart, Ph.D., CLU Chief Economist President April 2011 INTRODUCTION To prevent another financial meltdown like the one that affected the world

Maryland Insurance Administration. 2009 Report on the Effect of Competitive Rating on the Insurance Markets in Maryland

Maryland Insurance Administration 2009 Report on the Effect of Competitive Rating on the Insurance Markets in Maryland January, 2010 Maryland Insurance Administration 2009 Report on the Effect of Competitive

Maryland Insurance Administration 2009 Report on the Effect of Competitive Rating on the Insurance Markets in Maryland January, 2010 Maryland Insurance Administration 2009 Report on the Effect of Competitive

Who s Watching Your Back? An Assessment of Life Insurance Policyholder Protections Following the Passage of the Budget Control Act of 2011

Who s Watching Your Back? An Assessment of Life Insurance Policyholder Protections Following the Passage of the Budget Control Act of 2011 Nease, Lagana, Eden & Culley, Inc. 2100 RiverEdge Parkway, Suite

Who s Watching Your Back? An Assessment of Life Insurance Policyholder Protections Following the Passage of the Budget Control Act of 2011 Nease, Lagana, Eden & Culley, Inc. 2100 RiverEdge Parkway, Suite

How Property/Casualty Insurance Companies Invest Premium Dollars

How Property/Casualty Insurance Companies Invest Premium Dollars OVERVIEW Every day, property/casualty insurers enable our economy to function by helping individuals and businesses address the various

How Property/Casualty Insurance Companies Invest Premium Dollars OVERVIEW Every day, property/casualty insurers enable our economy to function by helping individuals and businesses address the various

Surplus Lines and Residual Markets: Maintaining the Public s Right to Freedom of Choice

Surplus Lines and Residual Markets: Maintaining the Public s Right to Freedom of Choice A position paper published by the National Association of Professional Surplus Lines Offices, Ltd. 1 2 SURPLUS LINES

Surplus Lines and Residual Markets: Maintaining the Public s Right to Freedom of Choice A position paper published by the National Association of Professional Surplus Lines Offices, Ltd. 1 2 SURPLUS LINES

Joseph C. Kohmann Chief Financial Officer and Treasurer Westfield Group May 20, 2014

Testimony of the Property Casualty Insurers Association of America (PCI) Before the Committee on Financial Services, Subcommittee on Housing and Insurance United States House of Representatives Joseph

Testimony of the Property Casualty Insurers Association of America (PCI) Before the Committee on Financial Services, Subcommittee on Housing and Insurance United States House of Representatives Joseph

Massachusetts Insurance Federation Two Center Plaza 8 th Floor Boston, MA 02108

Massachusetts Insurance Federation Two Center Plaza 8 th Floor Boston, MA 02108 (617) 557-5538 STATEMENT OF THE MASSACHUSETTS INSURANCE FEDERATION TO THE DIVISION OF INSURANCE IN CONNECTION WITH ITS INFORMATIONAL

Massachusetts Insurance Federation Two Center Plaza 8 th Floor Boston, MA 02108 (617) 557-5538 STATEMENT OF THE MASSACHUSETTS INSURANCE FEDERATION TO THE DIVISION OF INSURANCE IN CONNECTION WITH ITS INFORMATIONAL

Systemic Risk and the Insurance Industry

Systemic Risk and the Insurance Industry J. David Cummins, Temple University The Brookings Institution Conference on Regulating Non-Bank SIFIs May 9, 2013 Copyright J. David Cummins, 2013, all rights reserved.

Systemic Risk and the Insurance Industry J. David Cummins, Temple University The Brookings Institution Conference on Regulating Non-Bank SIFIs May 9, 2013 Copyright J. David Cummins, 2013, all rights reserved.

Is My Life Insurance Policy Protected?

The life insurance industry has in place a safety net of conservatism, regulation and oversight that, in these challenging economic times, may not be readily apparent. This document explains the many different

The life insurance industry has in place a safety net of conservatism, regulation and oversight that, in these challenging economic times, may not be readily apparent. This document explains the many different

Chapter 27 Government Regulation of Private Insurers in the United States

Chapter 27 Government Regulation of Private Insurers in the United States Overview You ve probably heard of The Food and Drug Administration (FDA), The Security and Exchange Commission (SEC), and the Environmental

Chapter 27 Government Regulation of Private Insurers in the United States Overview You ve probably heard of The Food and Drug Administration (FDA), The Security and Exchange Commission (SEC), and the Environmental

STATE INSURANCE REGULATION

STATE INSURANCE REGULATION This article provides an overview of state insurance regulation, including a brief history, discussion of state regulatory roles and institutions involved. A Brief History Benjamin

STATE INSURANCE REGULATION This article provides an overview of state insurance regulation, including a brief history, discussion of state regulatory roles and institutions involved. A Brief History Benjamin

VIA ELECTRONIC TRANSMISSION. www.regulations.gov. June 12, 2013.

Nationwide. Mark R. Thresher. Executive Vice President. Chief Financial Officer. Nationwide Insurance. VIA ELECTRONIC TRANSMISSION. www.regulations.gov June 12, 2013. Robert dev. Frierson, Secretary. Board

Nationwide. Mark R. Thresher. Executive Vice President. Chief Financial Officer. Nationwide Insurance. VIA ELECTRONIC TRANSMISSION. www.regulations.gov June 12, 2013. Robert dev. Frierson, Secretary. Board

How To Write An Insurance Profile Summary

EXHIBIT H INSURER PROFILE SUMMARY TEMPLATE Introductory Guidance An Insurer Profile Summary should be developed by the domestic state for each domestic insurer. The Insurer Profile Summary should be updated

EXHIBIT H INSURER PROFILE SUMMARY TEMPLATE Introductory Guidance An Insurer Profile Summary should be developed by the domestic state for each domestic insurer. The Insurer Profile Summary should be updated

Audit Report. Risk Management Agency Financial Management Controls Over Reinsured Companies. U.S. Department of Agriculture

U.S. Department of Agriculture Office of Inspector General Great Plains Region Audit Report Risk Management Agency Financial Management Controls Over Reinsured Companies Report No. 05801-3-KC April 2006

U.S. Department of Agriculture Office of Inspector General Great Plains Region Audit Report Risk Management Agency Financial Management Controls Over Reinsured Companies Report No. 05801-3-KC April 2006

Insurance is an essential element in the operation of sophisticated national economies throughout the world today.

THE ROLE OF INSURANCE INTERMEDIARIES Introduction The importance of insurance in modern economies is unquestioned and has been recognized for centuries. Insurance is practically a necessity to business

THE ROLE OF INSURANCE INTERMEDIARIES Introduction The importance of insurance in modern economies is unquestioned and has been recognized for centuries. Insurance is practically a necessity to business

Understanding Two Different Industries

The Business of and Banking Understanding Two Different Industries Banks bipartisanpolicy.org @BPC_Bipartisan facebook.com/bipartisanpolicycenter @BPC_Bipartisan Introduction Immediately after the enactment

The Business of and Banking Understanding Two Different Industries Banks bipartisanpolicy.org @BPC_Bipartisan facebook.com/bipartisanpolicycenter @BPC_Bipartisan Introduction Immediately after the enactment

An Overview of the Property and Casualty Insurance Guaranty Fund System

While American insurance consumers may not know it, they are protected by a nationwide system of insurance guaranty associations (sometimes also called guaranty funds ). State lawmakers and insurance regulators

While American insurance consumers may not know it, they are protected by a nationwide system of insurance guaranty associations (sometimes also called guaranty funds ). State lawmakers and insurance regulators

Financial-Institutions Management. Solutions 5. Chapter 18: Liability and Liquidity Management Reserve Requirements

Solutions 5 Chapter 18: Liability and Liquidity Management Reserve Requirements 8. City Bank has estimated that its average daily demand deposit balance over the recent 14- day reserve computation period

Solutions 5 Chapter 18: Liability and Liquidity Management Reserve Requirements 8. City Bank has estimated that its average daily demand deposit balance over the recent 14- day reserve computation period

Insolvency Trends 2010 Mid Year Report A Publication of the National Conference of Insurance Guaranty Funds

Insolvency Trends 2010 Mid Year Report A Publication of the National Conference of Insurance Guaranty Funds Welcome to the 2010 mid-year issue of the NCIGF s Insolvency Trends. Authored by the legal and

Insolvency Trends 2010 Mid Year Report A Publication of the National Conference of Insurance Guaranty Funds Welcome to the 2010 mid-year issue of the NCIGF s Insolvency Trends. Authored by the legal and

Recent and Expected Regulatory Reforms

1 1 Chris Longeway, Allstate Insurance Company Kimberly Shaul, Deputy Commissioner of Insurance, State of Wisconsin Kevin Fitzgerald, Partner, Foley & Lardner LLP Randy Wichinski, Managing Director, Insurance

1 1 Chris Longeway, Allstate Insurance Company Kimberly Shaul, Deputy Commissioner of Insurance, State of Wisconsin Kevin Fitzgerald, Partner, Foley & Lardner LLP Randy Wichinski, Managing Director, Insurance

Who s Watching Your Back? An Assessment of Life Insurance Policyholder Protections in the Wake of the Financial Downturn

Who s Watching Your Back? An Assessment of Life Insurance Policyholder Protections in the Wake of the Financial Downturn MBL Advisors Inc. 100 N Tryon St., Suite 5410 Charlotte, NC 28202 704.333.8461 704.342.0782

Who s Watching Your Back? An Assessment of Life Insurance Policyholder Protections in the Wake of the Financial Downturn MBL Advisors Inc. 100 N Tryon St., Suite 5410 Charlotte, NC 28202 704.333.8461 704.342.0782

2101 L Street.NW Suite 400 Washington,DC 20037 202-828-7100 Fax 202-293-1219 www.aiadc.org. April 30, 2013 BY ELECTRONIC MAIL

American Insurance Association April 30, 2013 2101 L Street.NW Suite 400 Washington,DC 20037 202-828-7100 Fax 202-293-1219 www.aiadc.org BY ELECTRONIC MAIL Board of Governors of the Federal Reserve System

American Insurance Association April 30, 2013 2101 L Street.NW Suite 400 Washington,DC 20037 202-828-7100 Fax 202-293-1219 www.aiadc.org BY ELECTRONIC MAIL Board of Governors of the Federal Reserve System

USAA. April 30, 2012. 9800 Fredericksburg Road San Antonio, Texas 78288

USAA 9800 Fredericksburg Road San Antonio, Texas 78288 April 30, 2012 Ms. Jennifer J. Johnson, Secretary Board of Governors of the Federal Reserve System 20th Street and Constitution Avenue, NW Washington,

USAA 9800 Fredericksburg Road San Antonio, Texas 78288 April 30, 2012 Ms. Jennifer J. Johnson, Secretary Board of Governors of the Federal Reserve System 20th Street and Constitution Avenue, NW Washington,

Subcommittee on Courts and Competition Policy United States House of Representatives

Subcommittee on Courts and Competition Policy United States House of Representatives Hearing on H.R. 3596, the Health Insurance Industry Antitrust Enforcement Act of 2009 Statement of James D. Hurley,

Subcommittee on Courts and Competition Policy United States House of Representatives Hearing on H.R. 3596, the Health Insurance Industry Antitrust Enforcement Act of 2009 Statement of James D. Hurley,

FROM JANUARY 21, 2007

FROM JANUARY 21, 2007 Negotiations between the Senate and House on the issue of property insurance reform began on Friday, January 19th and continued throughout the weekend. All of the almost 87 provisions

FROM JANUARY 21, 2007 Negotiations between the Senate and House on the issue of property insurance reform began on Friday, January 19th and continued throughout the weekend. All of the almost 87 provisions

OREGON S WORKERS COMPENSATION INSURANCE MARKET

LEGISLATIVE REVENUE OFFICE State Capitol Building 900 Court Street NE, H-197 Salem, Oregon 97301 (503) 986-1266 http://www.leg.state.or.us/comm/lro/home.htm Research Report Number 10-00 September 7, 2000

LEGISLATIVE REVENUE OFFICE State Capitol Building 900 Court Street NE, H-197 Salem, Oregon 97301 (503) 986-1266 http://www.leg.state.or.us/comm/lro/home.htm Research Report Number 10-00 September 7, 2000

A.M. Best - Congressional Testimony Committee on Financial Services America s Insurance Industry: Keeping the Promise

A.M. Best - Congressional Testimony Committee on Financial Services America s Insurance Industry: Keeping the Promise The horrible events of September 11 th caused shocks throughout the world s financial

A.M. Best - Congressional Testimony Committee on Financial Services America s Insurance Industry: Keeping the Promise The horrible events of September 11 th caused shocks throughout the world s financial

INSURANCE MARKETS. Impacts of and Regulatory Response to the 2007-2009 Financial Crisis. Report to Congressional Requesters

United States Government Accountability Office Report to Congressional Requesters June 2013 INSURANCE MARKETS Impacts of and Regulatory Response to the 2007-2009 Financial Crisis GAO-13-583 June 2013 INSURANCE

United States Government Accountability Office Report to Congressional Requesters June 2013 INSURANCE MARKETS Impacts of and Regulatory Response to the 2007-2009 Financial Crisis GAO-13-583 June 2013 INSURANCE

Re: Advance Notice of Proposed Rulemaking Regarding Authority to Require Supervision and Regulation of Certain Nonbank Financial Companies

JAMES D. MACPHEE Chairman SALVATORE MARRANCA Chairman-Elect JEFFREY L. GERHART Vice Chairman JACK A. HARTINGS Treasurer WAYNE A. COTTLE Secretary R. MICHAEL MENZIES SR. Immediate Past Chairman November

JAMES D. MACPHEE Chairman SALVATORE MARRANCA Chairman-Elect JEFFREY L. GERHART Vice Chairman JACK A. HARTINGS Treasurer WAYNE A. COTTLE Secretary R. MICHAEL MENZIES SR. Immediate Past Chairman November

How to Choose a Life Insurance Company *YP½PPMRK 4VSQMWIW A 2014 GUIDE THROUGH RELEVANT INDUSTRY INFORMATION

How to Choose a Life Insurance Company *YP½PPMRK 4VSQMWIW A 2014 GUIDE THROUGH RELEVANT INDUSTRY INFORMATION Because the most important people in your life will car, or computer, most people are completely

How to Choose a Life Insurance Company *YP½PPMRK 4VSQMWIW A 2014 GUIDE THROUGH RELEVANT INDUSTRY INFORMATION Because the most important people in your life will car, or computer, most people are completely

BEFORE THE U.S. HOUSE OF REPRESENTATIVES FINANCIAL SERVICES COMMITTEE CAPITAL MARKETS, INSURANCE AND GOVERNMENT SPONSORED ENTERPRISES SUBCOMMITTEE

TESTIMONY OF VERMONT STATE REPRESENTATIVE MARK YOUNG, NATIONAL CONFERENCE OF INSURANCE LEGISLATORS (NCOIL) VICE CHAIR OF THE STATE-FEDERAL RELATIONS COMMITTEE BEFORE THE U.S. HOUSE OF REPRESENTATIVES FINANCIAL

TESTIMONY OF VERMONT STATE REPRESENTATIVE MARK YOUNG, NATIONAL CONFERENCE OF INSURANCE LEGISLATORS (NCOIL) VICE CHAIR OF THE STATE-FEDERAL RELATIONS COMMITTEE BEFORE THE U.S. HOUSE OF REPRESENTATIVES FINANCIAL

April 10, 2003 10:00 a.m. Ernst N. Csiszar Director of Insurance State of South Carolina

Outline of Testimony Before the Congress of the United States of America House of Representatives Committee on Financial Services Subcommittee on Capital Markets, Insurance, and Government Sponsored Enterprises

Outline of Testimony Before the Congress of the United States of America House of Representatives Committee on Financial Services Subcommittee on Capital Markets, Insurance, and Government Sponsored Enterprises

Regulatory Solvency Assessment of Property/Casualty Insurance Companies in the United States

Regulatory Solvency Assessment of Property/Casualty Insurance Companies in the United States A presentation by Robert F. Conger Past-President, Casualty Actuarial Society September 2013 Regulatory Solvency

Regulatory Solvency Assessment of Property/Casualty Insurance Companies in the United States A presentation by Robert F. Conger Past-President, Casualty Actuarial Society September 2013 Regulatory Solvency

Information Canada s Financial Services Sector

Property and Casualty Insurance in Canada Overview Information Canada s Financial Services Sector The property and casualty (P&C) insurance industry in Canada provides coverage for all risks other than

Property and Casualty Insurance in Canada Overview Information Canada s Financial Services Sector The property and casualty (P&C) insurance industry in Canada provides coverage for all risks other than

Coastal Property Insurance: The Carolinas. Steven J. Schallau Senior Appalachian State University Dr. Dave Wood, CPCU, CRM

Coastal Property Insurance: The Carolinas Steven J. Schallau Senior Appalachian State University Dr. Dave Wood, CPCU, CRM 2 Coastal Property Insurance: The Carolinas The Carolinas are home to almost 500

Coastal Property Insurance: The Carolinas Steven J. Schallau Senior Appalachian State University Dr. Dave Wood, CPCU, CRM 2 Coastal Property Insurance: The Carolinas The Carolinas are home to almost 500

Many Banks and Thrifts Overly Reliant on Hot Money Deposits:

Many Banks and Thrifts Overly Reliant on Hot Money Deposits: Why an FDIC Coverage Increase to $250,000 May Not Stop Bank Runs and Could Cause Other Collateral Damage Submitted by Martin D. Weiss, Ph.D.

Many Banks and Thrifts Overly Reliant on Hot Money Deposits: Why an FDIC Coverage Increase to $250,000 May Not Stop Bank Runs and Could Cause Other Collateral Damage Submitted by Martin D. Weiss, Ph.D.

THE CONSUMERS SAFETY NET

INSURANCE GUARANTY ASSOCIATIONS IN CONNECTICUT THE CONSUMERS SAFETY NET Note: It is a prohibited unfair trade practice and a violation of state law for any person to make use in any manner of the existence,

INSURANCE GUARANTY ASSOCIATIONS IN CONNECTICUT THE CONSUMERS SAFETY NET Note: It is a prohibited unfair trade practice and a violation of state law for any person to make use in any manner of the existence,

UNITED STATES SENATE COMMITTEE ON BANKING, HOUSING AND URBAN AFFAIRS

UNITED STATES SENATE COMMITTEE ON BANKING, HOUSING AND URBAN AFFAIRS "AN EXAMINATION OF THE AVAILABILITY AND AFFORDABILITY OF PROPERTY AND CASUALTY INSURANCE IN THE GULF COAST AND OTHER COASTAL REGIONS"

UNITED STATES SENATE COMMITTEE ON BANKING, HOUSING AND URBAN AFFAIRS "AN EXAMINATION OF THE AVAILABILITY AND AFFORDABILITY OF PROPERTY AND CASUALTY INSURANCE IN THE GULF COAST AND OTHER COASTAL REGIONS"

Overview of assets, liabilities and capital of financial intermediaries and regulatory supervision of them

Mathematics 483, Fall 2014 Overview of assets, liabilities and capital of financial intermediaries and regulatory supervision of them Real assets in the economy are assets that are used for production

Mathematics 483, Fall 2014 Overview of assets, liabilities and capital of financial intermediaries and regulatory supervision of them Real assets in the economy are assets that are used for production

REINSURANCE RISK MANAGEMENT GUIDELINE

REINSURANCE RISK MANAGEMENT GUIDELINE Initial publication: April 2010 Update: July 2013 Table of Contents Preamble... 2 Introduction... 3 Scope... 5 Coming into effect and updating... 6 1. Reinsurance

REINSURANCE RISK MANAGEMENT GUIDELINE Initial publication: April 2010 Update: July 2013 Table of Contents Preamble... 2 Introduction... 3 Scope... 5 Coming into effect and updating... 6 1. Reinsurance

MUNICH RE AMERICA CORPORATION

MUNICH RE AMERICA CORPORATION Annual Report For The Fiscal Year Ended December 31, 2014 (Pursuant to Section 4.04 of the Indenture between the Company and the holders of the Company s 7.45% Senior Notes*)

MUNICH RE AMERICA CORPORATION Annual Report For The Fiscal Year Ended December 31, 2014 (Pursuant to Section 4.04 of the Indenture between the Company and the holders of the Company s 7.45% Senior Notes*)

How to Choose a Life Insurance Company

How to Choose a Life Insurance Company A Guide through Financial Data and Industry Information The Guardian Life Insurance Company of America New York, NY 10004-4025 Table of Contents Page 1. Mutuality...

How to Choose a Life Insurance Company A Guide through Financial Data and Industry Information The Guardian Life Insurance Company of America New York, NY 10004-4025 Table of Contents Page 1. Mutuality...

Liberty Mutual Insurance Reports Second Quarter 2013 Results

Liberty Mutual Insurance Reports Second Quarter 2013 Results BOSTON, Mass., August 6, 2013 Liberty Mutual Holding Company Inc. and its subsidiaries (collectively LMHC or the Company ) today reported net

Liberty Mutual Insurance Reports Second Quarter 2013 Results BOSTON, Mass., August 6, 2013 Liberty Mutual Holding Company Inc. and its subsidiaries (collectively LMHC or the Company ) today reported net

Property/Casualty Insurance Results 2014

Property/Casualty Insurance Results 2014 By Robert Gordon, Senior Vice President, Policy Development and Research, PCI, and Beth Fitzgerald, President, ISO Insurance Programs and Analytic Services Private

Property/Casualty Insurance Results 2014 By Robert Gordon, Senior Vice President, Policy Development and Research, PCI, and Beth Fitzgerald, President, ISO Insurance Programs and Analytic Services Private

April 24, 2008. Honorable George Miller Chairman Committee on Education and Labor U.S. House of Representatives Washington, DC 20515

CONGRESSIONAL BUDGET OFFICE U.S. Congress Washington, DC 20515 Peter R. Orszag, Director April 24, 2008 Honorable George Miller Chairman Committee on Education and Labor U.S. House of Representatives Washington,

CONGRESSIONAL BUDGET OFFICE U.S. Congress Washington, DC 20515 Peter R. Orszag, Director April 24, 2008 Honorable George Miller Chairman Committee on Education and Labor U.S. House of Representatives Washington,

A.M. Best Company. White Paper. The Quality Difference: Adding Value to Insurance Data and Information

A.M. Best Company White Paper The Quality Difference: Adding Value to Insurance Data and Information Insurance industry financial data is used to analyze companies, develop business strategies, compare

A.M. Best Company White Paper The Quality Difference: Adding Value to Insurance Data and Information Insurance industry financial data is used to analyze companies, develop business strategies, compare

TERRA BRASIS RESSEGUROS. Sao Paulo, SP 04543-000, Brazil B++

TERRA BRASIS RESSEGUROS Sao Paulo, SP 04543-000, Brazil Operating Company Composite TERRA BRASIS RESSEGUROS Av. Juscelino Kubitcheck, 1700, 12 Andar, Itaim Bibi, Sao Paulo, SP 04543-000, Brazil Web: www.terrabrasis.com.br

TERRA BRASIS RESSEGUROS Sao Paulo, SP 04543-000, Brazil Operating Company Composite TERRA BRASIS RESSEGUROS Av. Juscelino Kubitcheck, 1700, 12 Andar, Itaim Bibi, Sao Paulo, SP 04543-000, Brazil Web: www.terrabrasis.com.br

INSURANCE RATING METHODOLOGY

INSURANCE RATING METHODOLOGY The primary function of PACRA is to evaluate the capacity and willingness of an entity / issuer to honor its financial obligations. Our ratings reflect an independent, professional

INSURANCE RATING METHODOLOGY The primary function of PACRA is to evaluate the capacity and willingness of an entity / issuer to honor its financial obligations. Our ratings reflect an independent, professional

Commercial Insurance >

Commercial Insurance AIG Commercial Insurance combines one of the world s farthest reaching property casualty networks with our diversified, multichannel distribution network to offer our customers a broad

Commercial Insurance AIG Commercial Insurance combines one of the world s farthest reaching property casualty networks with our diversified, multichannel distribution network to offer our customers a broad

Operational Risk Management in a Property/Casualty Insurance Company

Operational Risk Management in a Property/Casualty Insurance Company Mark Verheyen, FCAS, MAAA Enterprise Risk Management Symposium May 2005 A Carvill service Operational Risk Management in a Property/Casualty

Operational Risk Management in a Property/Casualty Insurance Company Mark Verheyen, FCAS, MAAA Enterprise Risk Management Symposium May 2005 A Carvill service Operational Risk Management in a Property/Casualty

MUNICH RE AMERICA CORPORATION

MUNICH RE AMERICA CORPORATION Annual Report For The Fiscal Year Ended December 31, 2013 (Pursuant to Section 4.04 of the Indenture between the Company and the holders of the Company s 7.45% Senior Notes*)

MUNICH RE AMERICA CORPORATION Annual Report For The Fiscal Year Ended December 31, 2013 (Pursuant to Section 4.04 of the Indenture between the Company and the holders of the Company s 7.45% Senior Notes*)

Determining a reasonable range of loss reserves, required

C OVER S TORY By R USTY K UEHN Medical Malpractice Loss Reserves: Risk and Reasonability On March 1 of every calendar year, property/casualty insurance companies file a Statement of Actuarial Opinion (SAO),

C OVER S TORY By R USTY K UEHN Medical Malpractice Loss Reserves: Risk and Reasonability On March 1 of every calendar year, property/casualty insurance companies file a Statement of Actuarial Opinion (SAO),

August 20, 2012. Docket number: 2012-15685. Dear Director McRaith,

Director, Federal Insurance Office Department of the Treasury Federal Insurance Office 1500 Pennsylvania Avenue NW Washington, D.C. 20220 Re: Input to FIO s study on the breadth and scope of the global

Director, Federal Insurance Office Department of the Treasury Federal Insurance Office 1500 Pennsylvania Avenue NW Washington, D.C. 20220 Re: Input to FIO s study on the breadth and scope of the global

Securitizing Property Catastrophe Risk Sara Borden and Asani Sarkar

August 1996 Volume 2 Number 9 Securitizing Property Catastrophe Risk Sara Borden and Asani Sarkar The trading of property catastrophe risk using standard financial instruments such as options and bonds

August 1996 Volume 2 Number 9 Securitizing Property Catastrophe Risk Sara Borden and Asani Sarkar The trading of property catastrophe risk using standard financial instruments such as options and bonds

Guidance Note: Stress Testing Class 2 Credit Unions. November, 2013. Ce document est également disponible en français

Guidance Note: Stress Testing Class 2 Credit Unions November, 2013 Ce document est également disponible en français This Guidance Note is for use by all Class 2 credit unions with assets in excess of $1

Guidance Note: Stress Testing Class 2 Credit Unions November, 2013 Ce document est également disponible en français This Guidance Note is for use by all Class 2 credit unions with assets in excess of $1

Insurance Company Solvency Regulation

Insurance Company Solvency Regulation An Overview for the Financial Services Commission Presented by Insurance Commissioner Kevin M. McCarty January 13, 2009 1 Overview Evolution of the Florida property

Insurance Company Solvency Regulation An Overview for the Financial Services Commission Presented by Insurance Commissioner Kevin M. McCarty January 13, 2009 1 Overview Evolution of the Florida property

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective Paul Thornton International Actuarial Association Presentation to OECD Insurance and Pensions Committee June 2010

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective Paul Thornton International Actuarial Association Presentation to OECD Insurance and Pensions Committee June 2010

The Principal Financial Group. An Annuity Provider You Can Rely On

The Principal Financial Group An Annuity Provider You Can Rely On The U.S. Department of Labor (DOL) has issued guidelines to help fiduciaries select appropriate annuity providers (Interpretive Bulletin

The Principal Financial Group An Annuity Provider You Can Rely On The U.S. Department of Labor (DOL) has issued guidelines to help fiduciaries select appropriate annuity providers (Interpretive Bulletin

A Profile of the State Auto Insurance Companies

two thousand nine A Profile of the State Auto Insurance Companies Financial Statements About State Auto The State Automobile Mutual was founded in 1921 in Columbus, Ohio, with the promise of providing

two thousand nine A Profile of the State Auto Insurance Companies Financial Statements About State Auto The State Automobile Mutual was founded in 1921 in Columbus, Ohio, with the promise of providing

Risk Concentrations Principles

Risk Concentrations Principles THE JOINT FORUM BASEL COMMITTEE ON BANKING SUPERVISION INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS Basel December

Risk Concentrations Principles THE JOINT FORUM BASEL COMMITTEE ON BANKING SUPERVISION INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS Basel December

The promise and pitfalls of cyber insurance January 2016

www.pwc.com/us/insurance The promise and pitfalls of cyber insurance January 2016 2 top issues The promise and pitfalls of cyber insurance Cyber insurance is a potentially huge but still largely untapped

www.pwc.com/us/insurance The promise and pitfalls of cyber insurance January 2016 2 top issues The promise and pitfalls of cyber insurance Cyber insurance is a potentially huge but still largely untapped

A State Approach to Flood Insurance Reform in Florida. By Christian R. Cámara Florida Director The R Street Institute

P.O. Box 10577 Tallahassee FL 32302 Free Markets. Real Solutions. 305.608.4300 www.rstreet.org ccamara@rstreet.org A State Approach to Flood Insurance Reform in Florida By Christian R. Cámara Florida Director

P.O. Box 10577 Tallahassee FL 32302 Free Markets. Real Solutions. 305.608.4300 www.rstreet.org ccamara@rstreet.org A State Approach to Flood Insurance Reform in Florida By Christian R. Cámara Florida Director

Saxo Capital Markets CY Limited

Saxo Capital Markets CY Limited DISCLOSURES IN ACCORDANCE WITH THE REGULATION FOR THE CAPITAL REQUIREMENTS OF INVESTMENT FIRMS FOR THE YEAR ENDED 31 DECEMBER 2014 MAY 2015 CONTENTS 1. GENERAL INFORMATION

Saxo Capital Markets CY Limited DISCLOSURES IN ACCORDANCE WITH THE REGULATION FOR THE CAPITAL REQUIREMENTS OF INVESTMENT FIRMS FOR THE YEAR ENDED 31 DECEMBER 2014 MAY 2015 CONTENTS 1. GENERAL INFORMATION

Pension Funds Investing in Hedge Funds

Order Code RS22679 June 15, 2007 Pension Funds Investing in Hedge Funds Summary William Klunk Actuary Domestic Social Policy Division The proportion of U.S. corporate-defined benefit pension funds investing

Order Code RS22679 June 15, 2007 Pension Funds Investing in Hedge Funds Summary William Klunk Actuary Domestic Social Policy Division The proportion of U.S. corporate-defined benefit pension funds investing

Berkshire Hathaway and Loss Portfolio Transfers: Do They Make Sense?

Berkshire Hathaway the New Goliath: Strategies for the Boy David Berkshire Hathaway and Loss Portfolio Transfers: Do They Make Sense? Jonathan Terrell President, KCIC Washington, DC INTRODUCTION Through

Berkshire Hathaway the New Goliath: Strategies for the Boy David Berkshire Hathaway and Loss Portfolio Transfers: Do They Make Sense? Jonathan Terrell President, KCIC Washington, DC INTRODUCTION Through

Minnesota Department of Commerce Medical Malpractice Insurance in Minnesota Data as of 12/31/2012

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Minnesota Department

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Minnesota Department

World Bank Distance Learning

World Bank Distance Learning The Early Warning Test Ratios for General Insurers Washington, DC April 9, 2001 Lawrie Savage & Associates Inc. History of Early Warning Ratios Until early 1970's, everyone

World Bank Distance Learning The Early Warning Test Ratios for General Insurers Washington, DC April 9, 2001 Lawrie Savage & Associates Inc. History of Early Warning Ratios Until early 1970's, everyone

Effective downside risk management

Effective downside risk management Aymeric Forest, Fund Manager, Multi-Asset Investments November 2012 Since 2008, the desire to avoid significant portfolio losses has, more than ever, been at the front

Effective downside risk management Aymeric Forest, Fund Manager, Multi-Asset Investments November 2012 Since 2008, the desire to avoid significant portfolio losses has, more than ever, been at the front

Potential Indicators of Risk: Continuing Education, Business Practices, and Professional Licensure

Potential Indicators of Risk: Continuing Education, Business Practices, and Professional Licensure 2011 Victor O. Schinnerer & Company, Inc. The information presented herein is for professional liability

Potential Indicators of Risk: Continuing Education, Business Practices, and Professional Licensure 2011 Victor O. Schinnerer & Company, Inc. The information presented herein is for professional liability

Is Account Receivables Your Largest Asset? Unleash the Hidden Values A/R Insurance Can Deliver to Your Company. Presented by Glenn Robins

Is Account Receivables Your Largest Asset? Unleash the Hidden Values A/R Insurance Can Deliver to Your Company Presented by Glenn Robins US Companies Profile On Insuring Assets Compare Balance Sheet Assets

Is Account Receivables Your Largest Asset? Unleash the Hidden Values A/R Insurance Can Deliver to Your Company Presented by Glenn Robins US Companies Profile On Insuring Assets Compare Balance Sheet Assets

GLOSSARY OF SELECTED INSURANCE AND RELATED FINANCIAL TERMS

In an effort to help our investors and other interested parties better understand our regular SEC reports and other disclosures, we are providing a Glossary of Selected Insurance Terms. Most of the definitions

In an effort to help our investors and other interested parties better understand our regular SEC reports and other disclosures, we are providing a Glossary of Selected Insurance Terms. Most of the definitions

RISK-BASED SUPERVISORY FRAMEWORK TEMPLATE FOR INSURANCE COMPANIES

RISK-BASED SUPERVISORY FRAMEWORK TEMPLATE FOR INSURANCE COMPANIES JUNE 26, 2006 This publication was produced for review by the United States Agency for International Development. It was prepared by Stephen

RISK-BASED SUPERVISORY FRAMEWORK TEMPLATE FOR INSURANCE COMPANIES JUNE 26, 2006 This publication was produced for review by the United States Agency for International Development. It was prepared by Stephen

Filing Smart Financial and Data Services Filings Guide

The Filing Smart web page is divided into nine sections http://www.tdi.texas.gov/financial/indexsmart.html Filing Smart General Information NAIC Checklists Company Licensing and Registration Holding Company

The Filing Smart web page is divided into nine sections http://www.tdi.texas.gov/financial/indexsmart.html Filing Smart General Information NAIC Checklists Company Licensing and Registration Holding Company

How should I invest my Pension/Investment money? Thank you to AXA Wealth for their contribution to this guide.

How should I invest my Pension/Investment money? Thank you to AXA Wealth for their contribution to this guide. www.increaseyourpension.co.uk Welcome to making investing simple Investing doesn t have to

How should I invest my Pension/Investment money? Thank you to AXA Wealth for their contribution to this guide. www.increaseyourpension.co.uk Welcome to making investing simple Investing doesn t have to

2012 US Insurance ERM & ORSA Survey Key results and findings

www.pwc.com 2012 US Insurance ERM & ORSA Survey Key results and findings June 2013 Henry Jupe Director, Insurance Risk and Capital Practice henry.m.x.jupe@us.pwc.com Antitrust notice The Casualty Actuarial

www.pwc.com 2012 US Insurance ERM & ORSA Survey Key results and findings June 2013 Henry Jupe Director, Insurance Risk and Capital Practice henry.m.x.jupe@us.pwc.com Antitrust notice The Casualty Actuarial

The Economics and Regulation of Captive Reinsurance in Life Insurance. Scott E. Harrington. Wharton School, University of Pennsylvania

The Economics and Regulation of Captive Reinsurance in Life Insurance Scott E. Harrington Wharton School, University of Pennsylvania January, 2015 Abstract The use of captive reinsurance arrangements in

The Economics and Regulation of Captive Reinsurance in Life Insurance Scott E. Harrington Wharton School, University of Pennsylvania January, 2015 Abstract The use of captive reinsurance arrangements in

Thinking About Insurance Capital. A Public Interest Perspective. Marcus Stanley Policy Director Americans for Financial Reform

Thinking About Insurance Capital A Public Interest Perspective Marcus Stanley Policy Director Americans for Financial Reform AIA Life Insurance, Singapore, 2008 Conventional Insurance Diversified risk

Thinking About Insurance Capital A Public Interest Perspective Marcus Stanley Policy Director Americans for Financial Reform AIA Life Insurance, Singapore, 2008 Conventional Insurance Diversified risk

Insurance Risk 101. Pat Teufel, FSA, MAAA Timothy J. Tongson, FSA, MAAA James E. Rech, MBA, ACAS, ASA, MAAA July 9, 2001 RHOB 2220

Insurance Risk 101 Pat Teufel, FSA, MAAA Timothy J. Tongson, FSA, MAAA James E. Rech, MBA, ACAS, ASA, MAAA July 9, 2001 RHOB 2220 Insurance Risk 101 1 Life Insurance Risk 101 Timothy J. Tongson, FSA, MAAA

Insurance Risk 101 Pat Teufel, FSA, MAAA Timothy J. Tongson, FSA, MAAA James E. Rech, MBA, ACAS, ASA, MAAA July 9, 2001 RHOB 2220 Insurance Risk 101 1 Life Insurance Risk 101 Timothy J. Tongson, FSA, MAAA

Specialty Insurance Where Are We Headed?

2013 PLUS D&O Symposium Specialty Insurance Where Are We Headed? David Cash Endurance Specialty New York - February 6-7, 2013 Keynote Outline 1. Who are the Specialty Companies? 2. Economic drivers for

2013 PLUS D&O Symposium Specialty Insurance Where Are We Headed? David Cash Endurance Specialty New York - February 6-7, 2013 Keynote Outline 1. Who are the Specialty Companies? 2. Economic drivers for

INSURANCE MARKETS AND RISK TRENDS IN 2014 JANUARY 2014

JANUARY 2014 UNITED STATES INSURANCE MARKET REPORT 2014 For a copy of Marsh s US Insurance Market Report 2014, please visit marsh.com or ask your Marsh representative. AVERAGE PROPERTY RATE CHANGES ALL

JANUARY 2014 UNITED STATES INSURANCE MARKET REPORT 2014 For a copy of Marsh s US Insurance Market Report 2014, please visit marsh.com or ask your Marsh representative. AVERAGE PROPERTY RATE CHANGES ALL

SEAC June 04. Triple X Phase IV. The Continuing Saga

SEAC June 04 Triple X Phase IV The Continuing Saga Developing a Solvency Reserve Basis from First Principles Assume Discretionary not prescribed Easy to apply formula Never less than zero Developing a

SEAC June 04 Triple X Phase IV The Continuing Saga Developing a Solvency Reserve Basis from First Principles Assume Discretionary not prescribed Easy to apply formula Never less than zero Developing a

H-232 U.S. Capitol 522 Hart Senate Office Building Washington, DC 20515 Washington, DC 20510

The Honorable Nancy Pelosi The Honorable Harry Reid Speaker, U.S. House of Representatives Majority Leader, U.S. Senate H-232 U.S. Capitol 522 Hart Senate Office Building Washington, DC 20515 Washington,

The Honorable Nancy Pelosi The Honorable Harry Reid Speaker, U.S. House of Representatives Majority Leader, U.S. Senate H-232 U.S. Capitol 522 Hart Senate Office Building Washington, DC 20515 Washington,

RE: Regulation YY - Proposed Rule Regarding Enhanced Prudential Standards and Early Remediation Requirements for Covered Companies (RIN 7100-AD-86),

,") April 30, 2012, Ms. Jennifer J. Johnson Secretary Board of Governors of the Federal Reserve System 20th Street and Constitution Avenue, NW, Washington, DC 20551, Submitted electronically via http://www.regulations.gov,

April 30, 2012, Ms. Jennifer J. Johnson Secretary Board of Governors of the Federal Reserve System 20th Street and Constitution Avenue, NW, Washington, DC 20551, Submitted electronically via http://www.regulations.gov,

Goldman Sachs U.S. Financial Services Conference 2012

Goldman Sachs U.S. Financial Services Conference 2012 Steven A. Kandarian Chairman, President & Chief Executive Officer December 4, 2012 Cautionary Statement on Forward Looking Statements and Non-GAAP

Goldman Sachs U.S. Financial Services Conference 2012 Steven A. Kandarian Chairman, President & Chief Executive Officer December 4, 2012 Cautionary Statement on Forward Looking Statements and Non-GAAP

Financial Market Infrastructure

CHAPTER 11 Financial Market Infrastructure Too Important to Fail Darrell Duffie 1 A major focus of this book is the development of failure resolution methods, including bankruptcy and administrative forms

CHAPTER 11 Financial Market Infrastructure Too Important to Fail Darrell Duffie 1 A major focus of this book is the development of failure resolution methods, including bankruptcy and administrative forms

Solutions to Past CAS Questions Associated with NAIC Property/Casualty Insurance Company Risk Based Capital Requirements Feldblum, S.

Solutions to Past CAS Questions Associated with Feldblum, S. Solutions to questions from the 1997 Exam: 18. Calculate the adjusted policyholder surplus for this company. Step 1: Write an equation for adjusted

Solutions to Past CAS Questions Associated with Feldblum, S. Solutions to questions from the 1997 Exam: 18. Calculate the adjusted policyholder surplus for this company. Step 1: Write an equation for adjusted

The Life Insurance Business Did Not Cause the Financial Crisis

Life Insurers as SIFIs: A Case of Mistaken Identity? Steven A. Kandarian Chairman, President and CEO MetLife, Inc. Capital Markets Summit U.S. Chamber of Commerce Washington, D.C. April 10, 2013 As Prepared

Life Insurers as SIFIs: A Case of Mistaken Identity? Steven A. Kandarian Chairman, President and CEO MetLife, Inc. Capital Markets Summit U.S. Chamber of Commerce Washington, D.C. April 10, 2013 As Prepared

Chart 1 - Expense Rates. 0.0 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 Year

Policies and Developments INVESTMENT PERFORMANCE OF LIFE INSURERS Introduction Life insurance has evolved over many decades from a pure risk insurance to whole life and endowment insurance and more recently

Policies and Developments INVESTMENT PERFORMANCE OF LIFE INSURERS Introduction Life insurance has evolved over many decades from a pure risk insurance to whole life and endowment insurance and more recently

Associated With: Cincinnati Financial Corporation THE CINCINNATI INSURANCE COMPANIES

THE CINCINNATI INSURANCE COMPANIES Cincinnati Insurance Company A+ Cincinnati Specialty Undrs Ins A+ Cincinnati Casualty Company A+ Cincinnati Indemnity Company A+ Associated With: Cincinnati Financial

THE CINCINNATI INSURANCE COMPANIES Cincinnati Insurance Company A+ Cincinnati Specialty Undrs Ins A+ Cincinnati Casualty Company A+ Cincinnati Indemnity Company A+ Associated With: Cincinnati Financial

Introduction to Mortgage Insurance. Mexico City November 2003

Introduction to Mortgage Insurance Mexico City November 2003 Agenda United Guaranty Mortgage guaranty insurance Industry history Product structure and risk factors Advantages of mortgage insurance Process

Introduction to Mortgage Insurance Mexico City November 2003 Agenda United Guaranty Mortgage guaranty insurance Industry history Product structure and risk factors Advantages of mortgage insurance Process

The Journey to ORSA Begins. Assessing the Results of the 2015 ORSA Survey from St. John s University and Protiviti

The Journey to ORSA Begins Assessing the Results of the 2015 ORSA Survey from St. John s University and Protiviti Executive Summary PUBLIC COMPANIES HAVE SOX. FINANCIAL SERVICES ORGANIZATIONS (AND OTHERS)

The Journey to ORSA Begins Assessing the Results of the 2015 ORSA Survey from St. John s University and Protiviti Executive Summary PUBLIC COMPANIES HAVE SOX. FINANCIAL SERVICES ORGANIZATIONS (AND OTHERS)

The Allstate Corporation. Bernstein 2015 Strategic Decisions Conference Thomas J. Wilson: Chairman and Chief Executive Officer May 28, 2015

The Allstate Corporation Bernstein 2015 Strategic Decisions Conference Thomas J. Wilson: Chairman and Chief Executive Officer May 28, 2015 Forward-Looking Statements and Non-GAAP Financial Information

The Allstate Corporation Bernstein 2015 Strategic Decisions Conference Thomas J. Wilson: Chairman and Chief Executive Officer May 28, 2015 Forward-Looking Statements and Non-GAAP Financial Information

Counterparty Risk Mitigation Strategies for Commodity Merchants

Counterparty Risk Mitigation Strategies for Commodity Merchants By Alice Birnbaum As many clients of the BBH Commodities & Logistics group are well aware, recent consolidation among commodity consumers

Counterparty Risk Mitigation Strategies for Commodity Merchants By Alice Birnbaum As many clients of the BBH Commodities & Logistics group are well aware, recent consolidation among commodity consumers

What Investors Should Know about Money Market Reforms

What Investors Should Know about Money Market Reforms What Investors Should Know about Money Market Reforms Executive Summary Ò New SEC regulations for the $2.7 trillion money market industry may present

What Investors Should Know about Money Market Reforms What Investors Should Know about Money Market Reforms Executive Summary Ò New SEC regulations for the $2.7 trillion money market industry may present

Pacific Life Insurance Company Indexed Universal Life Insurance: Frequently Asked Questions

Pacific Life Insurance Company Indexed Universal Life Insurance: Frequently Asked Questions THE GROWTH CAP, PARTICIPATION RATE, AND FLOOR RATEE 1. What accounts for the gap in indexed cap rates from one

Pacific Life Insurance Company Indexed Universal Life Insurance: Frequently Asked Questions THE GROWTH CAP, PARTICIPATION RATE, AND FLOOR RATEE 1. What accounts for the gap in indexed cap rates from one

Reinsurance: What? Who? Why? How?

Knowledge. Experience. Performance. THE POWER OF INSIGHT. sm Life Reinsurance Rejean Besner, FSA, MAAA, FCIA, FASSA Vice President & Chief Actuary, International Division Presented to the Conference on

Knowledge. Experience. Performance. THE POWER OF INSIGHT. sm Life Reinsurance Rejean Besner, FSA, MAAA, FCIA, FASSA Vice President & Chief Actuary, International Division Presented to the Conference on

Finance for growth, the role of the insurance industry

Finance for growth, the role of the insurance industry Dario Focarelli Director General ANIA Visiting Professor, Risk Management and Insurance, 'La Sapienza' Roma Adjunct Professor, 'Tanaka Business School',

Finance for growth, the role of the insurance industry Dario Focarelli Director General ANIA Visiting Professor, Risk Management and Insurance, 'La Sapienza' Roma Adjunct Professor, 'Tanaka Business School',

Cambridge, Ontario June 1, 2011 CHECK AGAINST DELIVERY. For additional information contact:

Remarks by Superintendent Julie Dickson Office of the Superintendent of Financial Institutions Canada (OSFI) to the 2011 Property and Casualty Insurance Industry Forum Cambridge, Ontario June 1, 2011 CHECK

Remarks by Superintendent Julie Dickson Office of the Superintendent of Financial Institutions Canada (OSFI) to the 2011 Property and Casualty Insurance Industry Forum Cambridge, Ontario June 1, 2011 CHECK

The Changing Winds in Florida

The Changing Winds in Florida Property Insurance Implications By Bob Betz, Judith Durdan, Lloyd Stofko and Brian O Neill Florida s experiences over the past six years provide a window into the impact of

The Changing Winds in Florida Property Insurance Implications By Bob Betz, Judith Durdan, Lloyd Stofko and Brian O Neill Florida s experiences over the past six years provide a window into the impact of

Basis of the Financial Stability Oversight Council s Final Determination Regarding General Electric Capital Corporation, Inc.

Introduction Basis of the Financial Stability Oversight Council s Final Determination Regarding General Electric Capital Corporation, Inc. Pursuant to section 113 of the Dodd-Frank Wall Street Reform and

Introduction Basis of the Financial Stability Oversight Council s Final Determination Regarding General Electric Capital Corporation, Inc. Pursuant to section 113 of the Dodd-Frank Wall Street Reform and