DESCRIPTION OF H.R. 636, THE AMERICA S SMALL BUSINESS TAX RELIEF ACT OF 2015

|

|

|

- Beatrice McCoy

- 8 years ago

- Views:

Transcription

1 DESCRIPTION OF H.R. 636, THE AMERICA S SMALL BUSINESS TAX RELIEF ACT OF 2015 Scheduled for Markup by the HOUSE COMMITTEE ON WAYS AND MEANS on February 4, 2015 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION February 3, 2015 JCX-12-15

2 CONTENTS INTRODUCTION... 1 Page A. Expensing Certain Depreciable Business Assets for Small Business (sec. 179 of the Code)... 2 B. Estimated Revenue Effects... 5 i

... 2 B.")

3 INTRODUCTION The House Committee on Ways and Means has scheduled a committee markup of H.R. 636, the America s Small Business Tax Relief Act of 2015, on February 4, This document, 1 prepared by the staff of the Joint Committee on Taxation, provides a description of the bill. 1 This document may be cited as follows: Joint Committee on Taxation, Description of H.R. 636, the America s Small Business Tax Relief Act of 2015 (JCX-12-15), February 3, This document can also be found on the Joint Committee on Taxation website at 1

, February 3, 2015.")

4 A. Expensing Certain Depreciable Business Assets for Small Business (sec. 179 of the Code) Present Law A taxpayer may elect under section 179 to deduct (or expense ) the cost of qualifying property, rather than to recover such costs through depreciation deductions, subject to limitation. For taxable years beginning in 2014, the maximum amount a taxpayer may expense is $500,000 of the cost of qualifying property placed in service for the taxable year. 2 The $500,000 amount is reduced (but not below zero) by the amount by which the cost of qualifying property placed in service during the taxable year exceeds $2,000, The $500,000 and $2,000,000 amounts are not indexed for inflation. In general, qualifying property is defined as depreciable tangible personal property that is purchased for use in the active conduct of a trade or business. 4 Qualifying property excludes investments in air conditioning and heating units. 5 For taxable years beginning before 2015, qualifying property also includes off-the-shelf computer software and qualified real property (i.e., qualified leasehold improvement property, qualified restaurant property, and qualified retail improvement property). 6 Of the $500,000 expense amount available under section 179, the maximum amount available with respect to qualified real property is $250,000 for each taxable year. 7 For taxable years beginning in 2015 and thereafter, a taxpayer may elect to deduct up to $25,000 of the cost of qualifying property placed in service for the taxable year, subject to limitation. The $25,000 amount is reduced (but not below zero) by the amount by which the cost of qualifying property placed in service during the taxable year exceeds $200,000. The $25,000 and $200,000 amounts are not indexed for inflation. In general, qualifying property is defined as depreciable tangible personal property (not including off-the-shelf computer software, qualified real property, or air conditioning and heating units) that is purchased for use in the active conduct of a trade or business. 2 For the years 2003 through 2006, the relevant dollar amount is $100,000 (indexed for inflation); in 2007, the dollar limitation is $125,000; for the 2008 and 2009 years, the relevant dollar amount is $250,000; and for the years 2010 through 2013, the relevant dollar limitation is $500,000. Sec. 179(b)(1). 3 For the years 2003 through 2006, the relevant dollar amount is $400,000 (indexed for inflation); in 2007, the dollar limitation is $500,000; for the 2008 and 2009 years, the relevant dollar amount is $800,000; and for the years 2010 through 2013, the relevant dollar limitation is $2,000,000. Sec. 179(b)(2). 4 Passenger automobiles subject to the section 280F limitation are eligible for section 179 expensing only to the extent of the dollar limitations in section 280F. For sport utility vehicles above the 6,000 pound weight rating, which are not subject to the limitation under section 280F, the maximum cost that may be expensed for any taxable year under section 179 is $25,000. Sec. 179(b)(5). 5 Sec. 179(d)(1) flush language. 6 Sec. 179(d)(1)(A)(ii) and (f). 7 Sec. 179(f)(3). 2

by the amount by which the cost of qualifying property placed in service during the taxable year exceeds $2,000,000.")

5 The amount eligible to be expensed for a taxable year may not exceed the taxable income for such taxable year that is derived from the active conduct of a trade or business (determined without regard to this provision). 8 Any amount that is not allowed as a deduction because of the taxable income limitation may be carried forward to succeeding taxable years (subject to limitations). However, amounts attributable to qualified real property that are disallowed under the trade or business income limitation may only be carried over to taxable years in which the definition of eligible section 179 property includes qualified real property. 9 Thus, if a taxpayer s section 179 deduction for 2013 with respect to qualified real property is limited by the taxpayer s active trade or business income, such disallowed amount may be carried over to Any such carryover amounts that are not used in 2014 are treated as property placed in service in 2014 for purposes of computing depreciation. That is, the unused carryover amount from 2013 is considered placed in service on the first day of the 2014 taxable year. 10 No general business credit under section 38 is allowed with respect to any amount for which a deduction is allowed under section If a corporation makes an election under section 179 to deduct expenditures, the full amount of the deduction does not reduce earnings and profits. Rather, the expenditures that are deducted reduce corporate earnings and profits ratably over a five-year period. 12 An expensing election is made under rules prescribed by the Secretary. 13 In general, any election or specification made with respect to any property may not be revoked except with the consent of the Commissioner. However, an election or specification under section 179 may be revoked by the taxpayer without consent of the Commissioner for taxable years beginning after 2002 and before Sec. 179(b)(3). 9 Section 179(f)(4) details the special rules that apply to disallowed amounts with respect to qualified real property. 10 For example, assume that during 2013, a company s only asset purchases are section 179-eligible equipment costing $100,000 and qualifying leasehold improvements costing $200,000. Assume the company has no other asset purchases during 2013, and has a taxable income limitation of $150,000. The maximum section 179 deduction the company can claim for 2013 is $150,000, which is allocated pro rata between the properties, such that the carryover to 2014 is allocated $100,000 to the qualified leasehold improvements and $50,000 to the equipment. Assume further that in 2014, the company had no asset purchases and had no taxable income. The $100,000 carryover from 2013 attributable to qualified leasehold improvements is treated as placed in service as of the first day of the company s 2014 taxable year under section 179(f)(4)(C). The $50,000 carryover allocated to equipment is carried over to 2014 under section 179(b)(3)(B). 11 Sec. 179(d)(9). 12 Sec. 312(k)(3)(B). 13 Sec. 179(c)(1). 14 Sec. 179(c)(2). 3

6 Description of Proposal The proposal provides that the maximum amount a taxpayer may expense, for taxable years beginning after 2014, is $500,000 of the cost of qualifying property placed in service for the taxable year. The $500,000 amount is reduced (but not below zero) by the amount by which the cost of qualifying property placed in service during the taxable year exceeds $2,000,000. The $500,000 and $2,000,000 amounts are indexed for inflation for taxable years beginning after In addition, the proposal makes permanent the treatment of off-the-shelf computer software as qualifying property. The proposal also makes permanent the treatment of qualified real property as eligible section 179 property and removes the limitation related to the amount of section 179 property that may be attributable to qualified real property for taxable years beginning after Further, the proposal strikes the flush language in section 179(d)(1) that excludes air conditioning and heating units from the definition of qualifying property. The proposal also makes permanent the permission granted to a taxpayer to revoke without the consent of the Commissioner any election, and any specification contained therein, made under section 179. The proposal exempts any budgetary effects from the PAYGO scorecards under the Statutory Pay-As-You-Go Act of Effective Date The proposal applies to taxable years beginning after December 31,

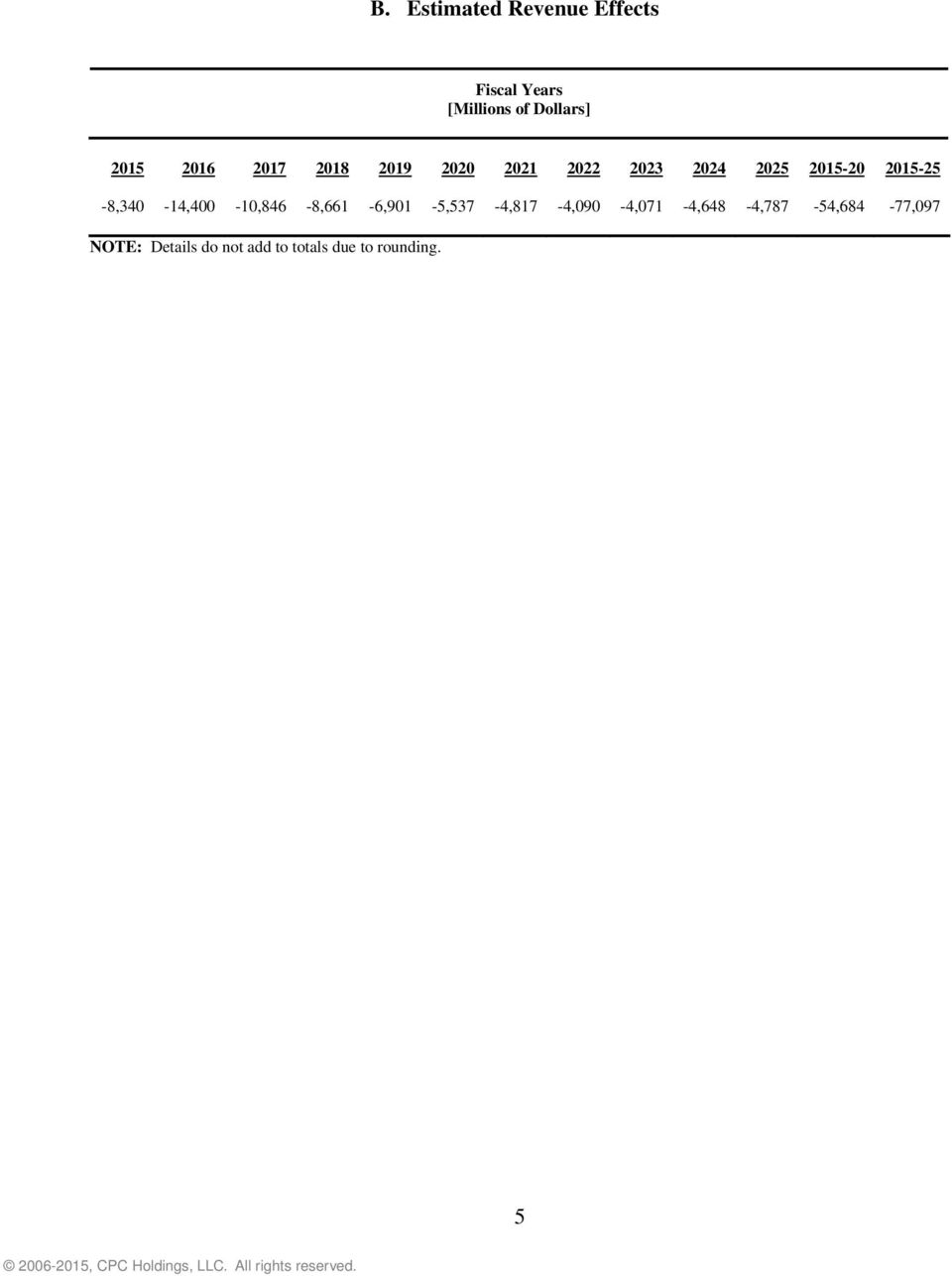

7 B. Estimated Revenue Effects Fiscal Years [Millions of Dollars] ,340-14,400-10,846-8,661-6,901-5,537-4,817-4,090-4,071-4,648-4,787-54,684-77,097 NOTE: Details do not add to totals due to rounding. 5

TECHNICAL EXPLANATION OF THE TAX PROVISIONS IN SENATE AMENDMENT 4594 TO H.R

TECHNICAL EXPLANATION OF THE TAX PROVISIONS IN SENATE AMENDMENT 4594 TO H.R. 5297, THE SMALL BUSINESS JOBS ACT OF 2010, SCHEDULED FOR CONSIDERATION BY THE SENATE ON SEPTEMBER 16, 2010 Prepared by the Staff

TECHNICAL EXPLANATION OF THE TAX PROVISIONS IN SENATE AMENDMENT 4594 TO H.R. 5297, THE SMALL BUSINESS JOBS ACT OF 2010, SCHEDULED FOR CONSIDERATION BY THE SENATE ON SEPTEMBER 16, 2010 Prepared by the Staff

DESCRIPTION OF THE CHAIRMAN S MARK RELATING TO MODIFICATIONS TO ALTERNATIVE TAX FOR CERTAIN SMALL INSURANCE COMPANIES

DESCRIPTION OF THE CHAIRMAN S MARK RELATING TO MODIFICATIONS TO ALTERNATIVE TAX FOR CERTAIN SMALL INSURANCE COMPANIES Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on February 11, 2015 Prepared

DESCRIPTION OF THE CHAIRMAN S MARK RELATING TO MODIFICATIONS TO ALTERNATIVE TAX FOR CERTAIN SMALL INSURANCE COMPANIES Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on February 11, 2015 Prepared

Scheduled for Markup by the HOUSE COMMITTEE ON WAYS AND MEANS on May 29, 2014. Prepared by the Staff of the JOINT COMMITTEE ON TAXATION

DESCRIPTION OF H.R. 4619, A BILL TO MAKE PERMANENT THE RULE ALLOWING CERTAIN TAX-FREE DISTRIBUTIONS FROM INDIVIDUAL RETIREMENT ACCOUNTS FOR CHARITABLE PURPOSES Scheduled for Markup by the HOUSE COMMITTEE

DESCRIPTION OF H.R. 4619, A BILL TO MAKE PERMANENT THE RULE ALLOWING CERTAIN TAX-FREE DISTRIBUTIONS FROM INDIVIDUAL RETIREMENT ACCOUNTS FOR CHARITABLE PURPOSES Scheduled for Markup by the HOUSE COMMITTEE

JOBS AND GROWTH TAX RELIEF RECONCILIATION ACT OF 2003

PUBLIC LAW 108 27 MAY 28, 2003 JOBS AND GROWTH TAX RELIEF RECONCILIATION ACT OF 2003 VerDate 11-MAY-2000 08:56 Jun 03, 2003 Jkt 019139 PO 00027 Frm 00001 Fmt 6579 Sfmt 6579 E:\PUBLAW\PUBL027.108 APPS06

PUBLIC LAW 108 27 MAY 28, 2003 JOBS AND GROWTH TAX RELIEF RECONCILIATION ACT OF 2003 VerDate 11-MAY-2000 08:56 Jun 03, 2003 Jkt 019139 PO 00027 Frm 00001 Fmt 6579 Sfmt 6579 E:\PUBLAW\PUBL027.108 APPS06

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL TO CREATE A MILITARY SPOUSE JOB CONTINUITY CREDIT

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL TO CREATE A MILITARY SPOUSE JOB CONTINUITY CREDIT Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on February 11, 2015 Prepared by the Staff of

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL TO CREATE A MILITARY SPOUSE JOB CONTINUITY CREDIT Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on February 11, 2015 Prepared by the Staff of

RIA Special Study: Depreciation and Expensing Provisions Retroactively Extended by the Tax Increase Prevention Act of 2014

RIA Special Study: Depreciation and Expensing Provisions Retroactively Extended by the Tax Increase Prevention Act of 2014 On Dec. 16, 2014, Congress passed the "Tax Increase Prevention Act of 2014" (TIPA,

RIA Special Study: Depreciation and Expensing Provisions Retroactively Extended by the Tax Increase Prevention Act of 2014 On Dec. 16, 2014, Congress passed the "Tax Increase Prevention Act of 2014" (TIPA,

Instructions for Form 4562

2010 Instructions for Form 4562 Depreciation and Amortization (Including Information on Listed Property) Who Must File Department of the Treasury Internal Revenue Service Section references are to the

2010 Instructions for Form 4562 Depreciation and Amortization (Including Information on Listed Property) Who Must File Department of the Treasury Internal Revenue Service Section references are to the

PRESENT LAW AND LEGISLATIVE BACKGROUND RELATING TO DEPRECIATION AND SECTION 179 EXPENSING

PRESENT LAW AND LEGISLATIVE BACKGROUND RELATING TO DEPRECIATION AND SECTION 179 EXPENSING Scheduled for a Public Hearing Before the SUBCOMMITTEE ON LONG-TERM GROWTH AND DEBT REDUCTION of the SENATE COMMITTEE

PRESENT LAW AND LEGISLATIVE BACKGROUND RELATING TO DEPRECIATION AND SECTION 179 EXPENSING Scheduled for a Public Hearing Before the SUBCOMMITTEE ON LONG-TERM GROWTH AND DEBT REDUCTION of the SENATE COMMITTEE

DESCRIPTION OF H.R. 5458, THE VETERANS TRICARE CHOICE ACT

DESCRIPTION OF H.R. 5458, THE VETERANS TRICARE CHOICE ACT Scheduled for Markup by the HOUSE COMMITTEE ON WAYS AND MEANS on June 15, 2016 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION June 14,

DESCRIPTION OF H.R. 5458, THE VETERANS TRICARE CHOICE ACT Scheduled for Markup by the HOUSE COMMITTEE ON WAYS AND MEANS on June 15, 2016 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION June 14,

Internal Revenue Code, Section 47

REHABILITATION CREDIT This Act became law on November 5, 1990 (Public Law 101-508; 26 U.S.C. 47). It is the current version of the certified rehabilitation section previously contained in Section 48(g)

REHABILITATION CREDIT This Act became law on November 5, 1990 (Public Law 101-508; 26 U.S.C. 47). It is the current version of the certified rehabilitation section previously contained in Section 48(g)

S Corporation Questions & Answers

S Corporation Questions & Answers Provisions in Chapter 173, P.L. 1993 provide that a corporation may elect to be treated as a New Jersey S corporation. The following is designed to address the most commonly

S Corporation Questions & Answers Provisions in Chapter 173, P.L. 1993 provide that a corporation may elect to be treated as a New Jersey S corporation. The following is designed to address the most commonly

LIST OF EXPIRING FEDERAL TAX PROVISIONS 2014-2025

LIST OF EXPIRING FEDERAL TAX PROVISIONS 2014-2025 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION January 9, 2015 JCX-1-15 CONTENTS Page INTRODUCTION...1 I. FEDERAL TAX PROVISIONS EXPIRING 2014-2025...2

LIST OF EXPIRING FEDERAL TAX PROVISIONS 2014-2025 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION January 9, 2015 JCX-1-15 CONTENTS Page INTRODUCTION...1 I. FEDERAL TAX PROVISIONS EXPIRING 2014-2025...2

Instructions for Form 4562

2014 Instructions for Form 4562 Depreciation and Amortization (Including Information on Listed Property) Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

2014 Instructions for Form 4562 Depreciation and Amortization (Including Information on Listed Property) Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL FOR A WASTE-HEAT-TO-POWER INVESTMENT TAX CREDIT

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL FOR A WASTE-HEAT-TO-POWER INVESTMENT TAX CREDIT Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on February 11, 2015 Prepared by the Staff of the

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL FOR A WASTE-HEAT-TO-POWER INVESTMENT TAX CREDIT Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on February 11, 2015 Prepared by the Staff of the

Tax Information Publication

TIP 11C01-01 Date Issued: July 18, 2011 Tax Information Publication Changes to Florida Corporate Income Tax and Emergency Excise Tax Please note the effective date of each change made to the corporate

TIP 11C01-01 Date Issued: July 18, 2011 Tax Information Publication Changes to Florida Corporate Income Tax and Emergency Excise Tax Please note the effective date of each change made to the corporate

Business Tax Breaks Retroactively Reinstated and Extended by the 2012 Taxpayer Relief Act

Page 1 of 14 Business Tax Breaks Retroactively Reinstated and Extended by the 2012 Taxpayer Relief Act On January 1, 2013, Congress passed the American Taxpayer Relief Act (2012 Taxpayer Relief Act), which

Page 1 of 14 Business Tax Breaks Retroactively Reinstated and Extended by the 2012 Taxpayer Relief Act On January 1, 2013, Congress passed the American Taxpayer Relief Act (2012 Taxpayer Relief Act), which

2011 IRS Tax Law Updates

2011 IRS Tax Law Updates IRS Texas New Mexico Regional Practitioner Meeting 2011 Stakeholder Liaison, Field May - July 2011 Small Business Health Care Tax Credit Eligibility Rules Providing health care

2011 IRS Tax Law Updates IRS Texas New Mexico Regional Practitioner Meeting 2011 Stakeholder Liaison, Field May - July 2011 Small Business Health Care Tax Credit Eligibility Rules Providing health care

PRESERVATION OF ACCESS TO CARE FOR MEDICARE BENEFICIARIES AND PENSION RELIEF ACT OF 2010

PRESERVATION OF ACCESS TO CARE FOR MEDICARE BENEFICIARIES AND PENSION RELIEF ACT OF 2010 VerDate Nov 24 2008 01:34 Jul 03, 2010 Jkt 089139 PO 00192 Frm 00001 Fmt 6579 Sfmt 6579 E:\PUBLAW\PUBL192.111 GPO1

PRESERVATION OF ACCESS TO CARE FOR MEDICARE BENEFICIARIES AND PENSION RELIEF ACT OF 2010 VerDate Nov 24 2008 01:34 Jul 03, 2010 Jkt 089139 PO 00192 Frm 00001 Fmt 6579 Sfmt 6579 E:\PUBLAW\PUBL192.111 GPO1

830 CMR 63.38R.1: Massachusetts Historic Rehabilitation Tax Credit Corporate Excise

830 CMR 63.38R.1: Massachusetts Historic Rehabilitation Tax Credit Corporate Excise 830 CMR: DEPARTMENT OF REVENUE 830 CMR 63.00: TAXATION OF CORPORATIONS 830 CMR 63.00 is amended by adding the following

830 CMR 63.38R.1: Massachusetts Historic Rehabilitation Tax Credit Corporate Excise 830 CMR: DEPARTMENT OF REVENUE 830 CMR 63.00: TAXATION OF CORPORATIONS 830 CMR 63.00 is amended by adding the following

Enhance and permanently extend the research tax credit, and increase the rate of the alternative simplified research credit (ASC) from 14% to 17%.

from 14% to 17%.") This update covers some of the provisions being suggested in the President s new budget for fiscal year 2015. I ve highlighted the items that are of greatest importance. 2015 Tax Proposals For Businesses

This update covers some of the provisions being suggested in the President s new budget for fiscal year 2015. I ve highlighted the items that are of greatest importance. 2015 Tax Proposals For Businesses

DESCRIPTION OF THE CHAIRMAN S MODIFICATION TO H.R. 1562, THE KATRINA HOUSING TAX RELIEF ACT OF 2007

DESCRIPTION OF THE CHAIRMAN S MODIFICATION TO H.R. 1562, THE KATRINA HOUSING TAX RELIEF ACT OF 2007 Scheduled for Markup by the HOUSE COMMITTEE ON WAYS AND MEANS on March 21, 2007 Prepared by the Staff

DESCRIPTION OF THE CHAIRMAN S MODIFICATION TO H.R. 1562, THE KATRINA HOUSING TAX RELIEF ACT OF 2007 Scheduled for Markup by the HOUSE COMMITTEE ON WAYS AND MEANS on March 21, 2007 Prepared by the Staff

COMPARISON OF REVENUE PROVISIONS IN H.R. 2990 AS PASSED BY THE HOUSE AND THE SENATE

COMPARISON OF REVENUE PROVISIONS IN H.R. 2990 AS PASSED BY THE HOUSE AND THE SENATE Prepared by the Staff of the JOINT COMMITTEE ON TAXATION November 2, 1999 JCX-77-99 CONTENTS INTRODUCTION AND LEGISLATIVE

COMPARISON OF REVENUE PROVISIONS IN H.R. 2990 AS PASSED BY THE HOUSE AND THE SENATE Prepared by the Staff of the JOINT COMMITTEE ON TAXATION November 2, 1999 JCX-77-99 CONTENTS INTRODUCTION AND LEGISLATIVE

Obama Tax Compromise APPROVED by Congress

December 17, 2010 Obama Tax Compromise APPROVED by Congress on Thursday, December 16, 2010 The $858 billion tax deal negotiated by President Obama and Republican leadership was overwhelmingly approved

December 17, 2010 Obama Tax Compromise APPROVED by Congress on Thursday, December 16, 2010 The $858 billion tax deal negotiated by President Obama and Republican leadership was overwhelmingly approved

Instructions for Completing Wisconsin Schedule I 2014

NOTE An individual who elects to claim a different amount of Internal Revenue Code sec. 179 expense deduction for Wisconsin than for federal tax purpose may use Schedule I to report that election. For

NOTE An individual who elects to claim a different amount of Internal Revenue Code sec. 179 expense deduction for Wisconsin than for federal tax purpose may use Schedule I to report that election. For

Highlights of the 2010 Tax Relief Act

On December 7, 200, President Barack Obama signed into law H.R. 4853, the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 200 (the 200 Tax Relief Act). This massive bill affects

On December 7, 200, President Barack Obama signed into law H.R. 4853, the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 200 (the 200 Tax Relief Act). This massive bill affects

In the Senate of the United States,

In the Senate of the United States, December 1, 010. Resolved, That the bill from the House of Representatives (H.R. 8) entitled An Act to amend the Internal Revenue Code of 198 to extend the funding and

In the Senate of the United States, December 1, 010. Resolved, That the bill from the House of Representatives (H.R. 8) entitled An Act to amend the Internal Revenue Code of 198 to extend the funding and

CONGRESSIONAL BUDGET OFFICE COST ESTIMATE. Tax Relief Extension Act of 2015

CONGRESSIONAL BUDGET OFFICE COST ESTIMATE August 4, 2015 Tax Relief Extension Act of 2015 As ordered reported by the Senate Committee on Finance on July 21, 2015 SUMMARY The Tax Relief Extension Act of

CONGRESSIONAL BUDGET OFFICE COST ESTIMATE August 4, 2015 Tax Relief Extension Act of 2015 As ordered reported by the Senate Committee on Finance on July 21, 2015 SUMMARY The Tax Relief Extension Act of

PRESENT LAW AND ANALYSIS RELATING TO TAX BENEFITS FOR HIGHER EDUCATION

PRESENT LAW AND ANALYSIS RELATING TO TAX BENEFITS FOR HIGHER EDUCATION Scheduled for a Public Hearing Before the SUBCOMMITTEE ON SELECT REVENUE MEASURES of the HOUSE COMMITTEE ON WAYS AND MEANS on May

PRESENT LAW AND ANALYSIS RELATING TO TAX BENEFITS FOR HIGHER EDUCATION Scheduled for a Public Hearing Before the SUBCOMMITTEE ON SELECT REVENUE MEASURES of the HOUSE COMMITTEE ON WAYS AND MEANS on May

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL TO CONVERT THE TAX ON LIQUEFIED NATURAL GAS AND LIQUEFIED PETROLEUM GAS TO AN ENERGY EQUIVALENT BASIS

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL TO CONVERT THE TAX ON LIQUEFIED NATURAL GAS AND LIQUEFIED PETROLEUM GAS TO AN ENERGY EQUIVALENT BASIS Scheduled for Markup by the SENATE COMMITTEE ON FINANCE

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL TO CONVERT THE TAX ON LIQUEFIED NATURAL GAS AND LIQUEFIED PETROLEUM GAS TO AN ENERGY EQUIVALENT BASIS Scheduled for Markup by the SENATE COMMITTEE ON FINANCE

ANALYSIS OF AMERICAN TAXPAYER RELIEF ACT OF 2012 (INCLUDING CALIFORNIA CONFORMITY)

") ANALYSIS OF AMERICAN TAXPAYER RELIEF ACT OF 2012 (INCLUDING CALIFORNIA CONFORMITY) AMERICAN TAXPAYER RELIEF ACT OF 2012 In the wee hours of New Year s morning, the Senate passed the American Taxpayer Relief

ANALYSIS OF AMERICAN TAXPAYER RELIEF ACT OF 2012 (INCLUDING CALIFORNIA CONFORMITY) AMERICAN TAXPAYER RELIEF ACT OF 2012 In the wee hours of New Year s morning, the Senate passed the American Taxpayer Relief

Briggs & Veselka Co. CPAs and Business Advisors. Small Business Jobs Act September 2010

More Depreciation Deductions (buying fixed assets for your business) Section 179 Expense is raised to $500,000 o Section 179 is the immediate write off of an asset s purchase price in the year the asset

More Depreciation Deductions (buying fixed assets for your business) Section 179 Expense is raised to $500,000 o Section 179 is the immediate write off of an asset s purchase price in the year the asset

HIRE Act Pending Tax Matters OtherActsof Congress 2010 Small Business Jobs Act of 2010 Uncertain Tax Positions

HIRE Act 2010 Legislative Update Pending Tax Matters OtherActsof Congress 2010 Small Business Jobs Act of 2010 Uncertain Tax Positions HIRE ACT Signed into law by President Obama on March 18, 2010 Two

HIRE Act 2010 Legislative Update Pending Tax Matters OtherActsof Congress 2010 Small Business Jobs Act of 2010 Uncertain Tax Positions HIRE ACT Signed into law by President Obama on March 18, 2010 Two

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL TO CLARIFY SPECIAL RULE FOR CERTAIN GOVERNMENTAL PLANS

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL TO CLARIFY SPECIAL RULE FOR CERTAIN GOVERNMENTAL PLANS Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on February 11, 2015 Prepared by the Staff

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL TO CLARIFY SPECIAL RULE FOR CERTAIN GOVERNMENTAL PLANS Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on February 11, 2015 Prepared by the Staff

Tax Increase Prevention Act of 2014 (Changes Effective in 2014)

") Individual s and Exclusions Cancellation of Debt (COD) Mortgage Debt Educator s Expenses Mortgage Insurance Premiums Charitable Distributions (QCDs) Conservation Small Business Stock (QSBS) Gain Exclusion

Individual s and Exclusions Cancellation of Debt (COD) Mortgage Debt Educator s Expenses Mortgage Insurance Premiums Charitable Distributions (QCDs) Conservation Small Business Stock (QSBS) Gain Exclusion

EXECUTIVE SUMMARY American Taxpayer Relief Act of 2012

TAX LEGISLATION January 2013 EXECUTIVE SUMMARY American Taxpayer Relief Act of 2012 Late in the night, on January 1, 2013, Congress completed work on the tax piece of the so-called fiscal cliff negotiations.

TAX LEGISLATION January 2013 EXECUTIVE SUMMARY American Taxpayer Relief Act of 2012 Late in the night, on January 1, 2013, Congress completed work on the tax piece of the so-called fiscal cliff negotiations.

TECHNICAL EXPLANATION OF THE TAX PROVISIONS OF H.R. 4541, THE COMMODITY FUTURES MODERNIZATION ACT OF 2000"

TECHNICAL EXPLANATION OF THE TAX PROVISIONS OF H.R. 4541, THE COMMODITY FUTURES MODERNIZATION ACT OF 2000" Prepared by the Staff of the JOINT COMMITTEE ON TAXATION October 19, 2000 JCX-108-00 CONTENTS

TECHNICAL EXPLANATION OF THE TAX PROVISIONS OF H.R. 4541, THE COMMODITY FUTURES MODERNIZATION ACT OF 2000" Prepared by the Staff of the JOINT COMMITTEE ON TAXATION October 19, 2000 JCX-108-00 CONTENTS

26 CFR 601.105: Examination of returns and claims for refund, credit or abatement; determination of correct tax liability. (Also Part I, 172, 6411)

") Part III Administrative, Procedural, and Miscellaneous 26 CFR 601.105: Examination of returns and claims for refund, credit or abatement; determination of correct tax liability. (Also Part I, 172, 6411)

Part III Administrative, Procedural, and Miscellaneous 26 CFR 601.105: Examination of returns and claims for refund, credit or abatement; determination of correct tax liability. (Also Part I, 172, 6411)

By: Michael Shelby, CPA, MST

By: Michael Shelby, CPA, MST Introduction Michael K. Shelby, CPA, MST Principal of Michael K. Shelby, CPA, LLC Main office in Lanham, Satellite office in Annapolis Currently staff of 5, need to add at

By: Michael Shelby, CPA, MST Introduction Michael K. Shelby, CPA, MST Principal of Michael K. Shelby, CPA, LLC Main office in Lanham, Satellite office in Annapolis Currently staff of 5, need to add at

OVERVIEW OF FEDERAL INCOME TAX PROVISIONS RELATING TO EMPLOYEE STOCK OPTIONS

OVERVIEW OF FEDERAL INCOME TAX PROVISIONS RELATING TO EMPLOYEE STOCK OPTIONS Scheduled for a Hearing Before the SUBCOMMITTEE ON OVERSIGHT of the HOUSE COMMITTEE ON WAYS AND MEANS on October 12, 2000 Prepared

OVERVIEW OF FEDERAL INCOME TAX PROVISIONS RELATING TO EMPLOYEE STOCK OPTIONS Scheduled for a Hearing Before the SUBCOMMITTEE ON OVERSIGHT of the HOUSE COMMITTEE ON WAYS AND MEANS on October 12, 2000 Prepared

SMALL BUSINESS LENDING BILL PROVISIONS September 20, 2010

SMALL BUSINESS LENDING BILL PROVISIONS September 20, 2010 Below is a summary of provisions of the Small Business Lending bill that was debated and passed in the Senate during the week of September 13,

SMALL BUSINESS LENDING BILL PROVISIONS September 20, 2010 Below is a summary of provisions of the Small Business Lending bill that was debated and passed in the Senate during the week of September 13,

TAX PROVISIONS IN THE AMERICAN TAXPAYER RELIEF ACT OF 2012 (ATRA) James Nunns and Jeffrey Rohaly Urban-Brookings Tax Policy Center January 9, 2013

James Nunns and Jeffrey Rohaly Urban-Brookings Tax Policy Center January 9, 2013") TAX PROVISIONS IN THE AMERICAN TAXPAYER RELIEF ACT OF 2012 (ATRA) James Nunns and Jeffrey Rohaly Urban-Brookings Tax Policy Center January 9, 2013 ABSTRACT The fiscal cliff debate culminated in the passage

TAX PROVISIONS IN THE AMERICAN TAXPAYER RELIEF ACT OF 2012 (ATRA) James Nunns and Jeffrey Rohaly Urban-Brookings Tax Policy Center January 9, 2013 ABSTRACT The fiscal cliff debate culminated in the passage

LIST OF EXPIRING FEDERAL TAX PROVISIONS 2001-2010

LIST OF EXPIRING FEDERAL TAX PROVISIONS 2001-2010 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION June 25, 2001 JCX-56-01 CONTENTS Page INTRODUCTION... 1 EXPIRING FEDERAL TAX PROVISIONS 2001-2010...

LIST OF EXPIRING FEDERAL TAX PROVISIONS 2001-2010 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION June 25, 2001 JCX-56-01 CONTENTS Page INTRODUCTION... 1 EXPIRING FEDERAL TAX PROVISIONS 2001-2010...

2015 -- S 0163 S T A T E O F R H O D E I S L A N D

======== LC000 ======== 01 -- S 01 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 A N A C T RELATING TO TAXATION - PERSONAL INCOME TAX Introduced By: Senators Goldin,

======== LC000 ======== 01 -- S 01 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 A N A C T RELATING TO TAXATION - PERSONAL INCOME TAX Introduced By: Senators Goldin,

Date Filed with the Secretary of the State: September 29, 2004

State of California Franchise Tax Board-Legislative Services Bureau Telephone: (916) 845-4326 PO Box 1468 ATSS: 468-4326 Sacramento, CA 95812-1468 FAX: (916) 845-5472 Legislative Change No. 04-37 Bill

State of California Franchise Tax Board-Legislative Services Bureau Telephone: (916) 845-4326 PO Box 1468 ATSS: 468-4326 Sacramento, CA 95812-1468 FAX: (916) 845-5472 Legislative Change No. 04-37 Bill

Department of Legislative Services 2014 Session

Senate Bill 596 Budget and Taxation Department of Legislative Services 2014 Session FISCAL AND POLICY NOTE Revised (Senator Peters, et al.) SB 596 Ways and Means Income Tax Subtraction Modification - Mortgage

Senate Bill 596 Budget and Taxation Department of Legislative Services 2014 Session FISCAL AND POLICY NOTE Revised (Senator Peters, et al.) SB 596 Ways and Means Income Tax Subtraction Modification - Mortgage

New Qualified Plug In Electric Drive Motor Vehicle Credit

FEDERAL New Qualified Plug In Electric Drive Motor Vehicle Credit Short Description: An income tax credit of zero to $7,500 for the purchase of a new qualified plug in electric drive motor vehicle. Beneficiary:

FEDERAL New Qualified Plug In Electric Drive Motor Vehicle Credit Short Description: An income tax credit of zero to $7,500 for the purchase of a new qualified plug in electric drive motor vehicle. Beneficiary:

2013 Federal Income Tax Update with The American Taxpayer Relief Act of 2012

THE UNIVERSITY OF TENNESSEE 2013 SINGLETON B. WOLFE MEMORIAL TAX CONFERENCE OCTOBER 31, 2013 2013 Federal Income Tax Update with The American Taxpayer Relief Act of 2012 JOHN D. HOUSTON, CPA Certified

THE UNIVERSITY OF TENNESSEE 2013 SINGLETON B. WOLFE MEMORIAL TAX CONFERENCE OCTOBER 31, 2013 2013 Federal Income Tax Update with The American Taxpayer Relief Act of 2012 JOHN D. HOUSTON, CPA Certified

BE IT ENACTED BY THE GENERAL ASSEMBLY OF THE STATE OF IOWA:

House File 2453 AN ACT RELATING TO THE ADMINISTRATION OF THE HISTORIC PRESERVATION AND CULTURAL AND ENTERTAINMENT DISTRICT TAX CREDIT PROGRAM BY THE DEPARTMENT OF CULTURAL AFFAIRS, PROVIDING FOR FEES,

House File 2453 AN ACT RELATING TO THE ADMINISTRATION OF THE HISTORIC PRESERVATION AND CULTURAL AND ENTERTAINMENT DISTRICT TAX CREDIT PROGRAM BY THE DEPARTMENT OF CULTURAL AFFAIRS, PROVIDING FOR FEES,

Internal Revenue Code Section 168(k)(2)(D)(i)(II) Accelerated cost recovery system.

(2)(D)(i)(II) Accelerated cost recovery system.") Internal Revenue Code Section 168(k)(2)(D)(i)(II) Accelerated cost recovery system.... CLICK HERE to return to the home page (k) Special allowance for certain property acquired after December 31, 2007,

Internal Revenue Code Section 168(k)(2)(D)(i)(II) Accelerated cost recovery system.... CLICK HERE to return to the home page (k) Special allowance for certain property acquired after December 31, 2007,

Senate passes 2010 Tax Relief Act, featuring extension of Bush-era tax cuts & other tax breaks, plus stimulus measures

Senate passes 2010 Tax Relief Act, featuring extension of Bush-era tax cuts & other tax breaks, plus stimulus measures On December 15, the Senate passed, today by a vote of 81-19, the Tax Relief, Unemployment

Senate passes 2010 Tax Relief Act, featuring extension of Bush-era tax cuts & other tax breaks, plus stimulus measures On December 15, the Senate passed, today by a vote of 81-19, the Tax Relief, Unemployment

New Qualified Plug-In Electric Drive Motor Vehicles

FEDERAL New Qualified Plug-In Electric Drive Motor Vehicles Short Description: An income tax credit of zero to $7,500 for the purchase of a new qualified plug-in electric drive motor vehicle. Beneficiary:

FEDERAL New Qualified Plug-In Electric Drive Motor Vehicles Short Description: An income tax credit of zero to $7,500 for the purchase of a new qualified plug-in electric drive motor vehicle. Beneficiary:

Multistate Impact of the American Taxpayer Relief Act of 2012 March 5, 2013

Multistate Tax EXTERNAL ALERT Multistate Impact of the American Taxpayer Relief Act of 2012 March 5, 2013 Overview On January 2, 2013, President Barack Obama signed into law the American Taxpayer Relief

Multistate Tax EXTERNAL ALERT Multistate Impact of the American Taxpayer Relief Act of 2012 March 5, 2013 Overview On January 2, 2013, President Barack Obama signed into law the American Taxpayer Relief

2013 Year End Tax Planning Seminar

2013 Year End Tax Planning Seminar Walter H. Deyhle, CPA, CFP December 4, 2013 GRF s Tax Team 2 Disclosure This presentation and these materials are designed to provide accurate and authoritative information

2013 Year End Tax Planning Seminar Walter H. Deyhle, CPA, CFP December 4, 2013 GRF s Tax Team 2 Disclosure This presentation and these materials are designed to provide accurate and authoritative information

Small Business Tax Saving Strategies for the 2012 Filing Season

Small Business Tax Saving Strategies for the 2012 Filing Season Few business sectors embody today s entrepreneurial spirit, drive for innovation and unwavering perseverance more than the small business

Small Business Tax Saving Strategies for the 2012 Filing Season Few business sectors embody today s entrepreneurial spirit, drive for innovation and unwavering perseverance more than the small business

BACKGROUND AND PRESENT LAW RELATED TO TAX BENEFITS FOR EDUCATION

BACKGROUND AND PRESENT LAW RELATED TO TAX BENEFITS FOR EDUCATION Scheduled for a Public Hearing Before the SENATE COMMITTEE ON FINANCE on June 24, 2014 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION

BACKGROUND AND PRESENT LAW RELATED TO TAX BENEFITS FOR EDUCATION Scheduled for a Public Hearing Before the SENATE COMMITTEE ON FINANCE on June 24, 2014 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION

LIST OF EXPIRING FEDERAL TAX PROVISIONS 2013-2023

LIST OF EXPIRING FEDERAL TAX PROVISIONS 2013-2023 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION January 11, 2013 JCX-3-13 CONTENTS Page INTRODUCTION...1 I. FEDERAL TAX PROVISIONS EXPIRING 2013-2023...2

LIST OF EXPIRING FEDERAL TAX PROVISIONS 2013-2023 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION January 11, 2013 JCX-3-13 CONTENTS Page INTRODUCTION...1 I. FEDERAL TAX PROVISIONS EXPIRING 2013-2023...2

Tax Relief Act of 2010 extends Bush-era tax cuts and carries a host of other tax breaks

Tax Relief Act of 2010 extends Bush-era tax cuts and carries a host of other tax breaks Late on December 9, Senate Majority Leader Harry Reid (D-NV) introduced H.R. 4853, the Tax Relief, Unemployment Insurance

Tax Relief Act of 2010 extends Bush-era tax cuts and carries a host of other tax breaks Late on December 9, Senate Majority Leader Harry Reid (D-NV) introduced H.R. 4853, the Tax Relief, Unemployment Insurance

Business Tax Provisions of the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act of 2010

Business Tax Provisions of the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act of 2010 On December 17, 2010, the president signed into law the Tax Relief, Unemployment Insurance

Business Tax Provisions of the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act of 2010 On December 17, 2010, the president signed into law the Tax Relief, Unemployment Insurance

EDUCATION TAX CREDIT PROGRAMS: AN ANALYSIS OF PROVISIONS BY STATE

EDUCATION TAX CREDIT PROGRAMS: AN ANALYSIS OF PROVISIONS BY STATE OCTOBER 2013 The Foundation for Opportunity in Education TO THE POINT As of 2013, 13 states have laws in place to provide a tax credit

EDUCATION TAX CREDIT PROGRAMS: AN ANALYSIS OF PROVISIONS BY STATE OCTOBER 2013 The Foundation for Opportunity in Education TO THE POINT As of 2013, 13 states have laws in place to provide a tax credit

TAX RELIEF ACT UPDATED DECEMBER 29, 2010

2010 TAX RELIEF ACT UPDATED DECEMBER 29, 2010 TAX RELIEF, UNEMPLOYMENT INSURANCE RE-AUTHORIZATION, AND JOB CREATION ACT OF 2010 INTRODUCTION On December 17, 2010, President Obama signed the much-anticipated

2010 TAX RELIEF ACT UPDATED DECEMBER 29, 2010 TAX RELIEF, UNEMPLOYMENT INSURANCE RE-AUTHORIZATION, AND JOB CREATION ACT OF 2010 INTRODUCTION On December 17, 2010, President Obama signed the much-anticipated

Department, Board, Or Commission Author Bill Number. Research Expenses Credit/Reduce Excess Carryover Credit/R&D-Small Business Grant Program

BILL ANALYSIS Department, Board, Or Commission Author Bill Number Franchise Tax Board Atkins & Mullin AB 437 SUBJECT Research Expenses Credit/Reduce Excess Carryover Credit/R&D-Small Business Grant Program

BILL ANALYSIS Department, Board, Or Commission Author Bill Number Franchise Tax Board Atkins & Mullin AB 437 SUBJECT Research Expenses Credit/Reduce Excess Carryover Credit/R&D-Small Business Grant Program

H.R. 1836 CONGRESSIONAL BUDGET OFFICE PAY-AS-YOU-GO ESTIMATE. Economic Growth and Tax Relief Reconciliation Act of 2001.

CONGRESSIONAL BUDGET OFFICE PAY-AS-YOU-GO ESTIMATE June 4, 2001 H.R. 1836 Economic Growth and Tax Relief Reconciliation Act of 2001 As cleared by the Congress on May 26, 2001 SUMMARY The Economic Growth

CONGRESSIONAL BUDGET OFFICE PAY-AS-YOU-GO ESTIMATE June 4, 2001 H.R. 1836 Economic Growth and Tax Relief Reconciliation Act of 2001 As cleared by the Congress on May 26, 2001 SUMMARY The Economic Growth

Gleim CPA Review Updates to Regulation 2013 Edition, 1st Printing June 2013

Page 1 of 12 Gleim CPA Review Updates to Regulation 2013 Edition, 1st Printing June 2013 NOTE: Text that should be deleted is displayed with a line through the text. New text is shown with a blue background.

Page 1 of 12 Gleim CPA Review Updates to Regulation 2013 Edition, 1st Printing June 2013 NOTE: Text that should be deleted is displayed with a line through the text. New text is shown with a blue background.

An Overview of The Tax Relief Act on 2010

An Overview of The Tax Relief Act on 2010 On December 17, 2010, the President signed a multi-billion dollar tax cut package, the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act

An Overview of The Tax Relief Act on 2010 On December 17, 2010, the President signed a multi-billion dollar tax cut package, the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act

Higher Education Tax Benefits: Brief Overview and Budgetary Effects

Higher Education Tax Benefits: Brief Overview and Budgetary Effects Margot L. Crandall-Hollick Analyst in Public Finance Mark P. Keightley Analyst in Public Finance August 24, 2011 CRS Report for Congress

Higher Education Tax Benefits: Brief Overview and Budgetary Effects Margot L. Crandall-Hollick Analyst in Public Finance Mark P. Keightley Analyst in Public Finance August 24, 2011 CRS Report for Congress

2013-2014 Tax Update Lead Story Headline

December Daniel, Ratliff & Company 704-371-5000 2013-2014 Tax Updates 2013-2014 Tax Update Lead Story Headline Contents 50% Bonus Depreciation Scheduled to Expire After 2013 2 Expanded Section 179 Deduction

December Daniel, Ratliff & Company 704-371-5000 2013-2014 Tax Updates 2013-2014 Tax Update Lead Story Headline Contents 50% Bonus Depreciation Scheduled to Expire After 2013 2 Expanded Section 179 Deduction

PART C: GENERAL BUSINESS CREDIT

PART C: GENERAL BUSINESS CREDIT 15. CREDIT FOR INVESTING IN PROPERTY IN SOUTH CAROLINA South Carolina Code 12-14-60 allows a taxpayer a credit against income taxes for qualified manufacturing and productive

PART C: GENERAL BUSINESS CREDIT 15. CREDIT FOR INVESTING IN PROPERTY IN SOUTH CAROLINA South Carolina Code 12-14-60 allows a taxpayer a credit against income taxes for qualified manufacturing and productive

THE FEDERAL LOW-INCOME HOUSING TAX CREDIT AND HISTORIC REHABILITATION TAX CREDIT

THE FEDERAL LOW-INCOME HOUSING TAX CREDIT AND HISTORIC REHABILITATION TAX CREDIT This outline provides an overview of the federal low-income housing tax credit and historic rehabilitation tax credit. I.

THE FEDERAL LOW-INCOME HOUSING TAX CREDIT AND HISTORIC REHABILITATION TAX CREDIT This outline provides an overview of the federal low-income housing tax credit and historic rehabilitation tax credit. I.

Department of Legislative Services 2014 Session

Department of Legislative Services 2014 Session HB 264 House Bill 264 Ways and Means FISCAL AND POLICY NOTE (Delegate Luedtke) Budget and Taxation Income Tax - Subtraction Modification - Student Loan Debt

Department of Legislative Services 2014 Session HB 264 House Bill 264 Ways and Means FISCAL AND POLICY NOTE (Delegate Luedtke) Budget and Taxation Income Tax - Subtraction Modification - Student Loan Debt

Small Business Tax Credit for Employee Health Expenses

Small Business Tax Credit for Employee Health Expenses Summary: Provides a sliding scale tax credit to small employers with fewer than 25 employees and average annual wages of less than $40,000 that purchase

Small Business Tax Credit for Employee Health Expenses Summary: Provides a sliding scale tax credit to small employers with fewer than 25 employees and average annual wages of less than $40,000 that purchase

Caution: DRAFT NOT FOR FILING

Caution: DRAFT NOT FOR FILING This is an early release draft of an IRS tax form, instructions, or publication, which the IRS is providing for your information as a courtesy. Do not file draft forms. Also,

Caution: DRAFT NOT FOR FILING This is an early release draft of an IRS tax form, instructions, or publication, which the IRS is providing for your information as a courtesy. Do not file draft forms. Also,

Department of Legislative Services 2012 Session

House Bill 600 Ways and Means Department of Legislative Services 2012 Session FISCAL AND POLICY NOTE Revised (Delegate Zucker, et al.) HB 600 Budget and Taxation Income Tax - Subtraction Modification -

House Bill 600 Ways and Means Department of Legislative Services 2012 Session FISCAL AND POLICY NOTE Revised (Delegate Zucker, et al.) HB 600 Budget and Taxation Income Tax - Subtraction Modification -

DESCRIPTION OF THE CHAIRMAN S MARK OF THE EXPIRING PROVISIONS IMPROVEMENT REFORM AND EFFICIENCY (EXPIRE) ACT

ACT") DESCRIPTION OF THE CHAIRMAN S MARK OF THE EXPIRING PROVISIONS IMPROVEMENT REFORM AND EFFICIENCY (EXPIRE) ACT Scheduled for Markup Before the SENATE COMMITTEE ON FINANCE on April 3, 2014 Prepared by the

DESCRIPTION OF THE CHAIRMAN S MARK OF THE EXPIRING PROVISIONS IMPROVEMENT REFORM AND EFFICIENCY (EXPIRE) ACT Scheduled for Markup Before the SENATE COMMITTEE ON FINANCE on April 3, 2014 Prepared by the

LIFE INSURANCE DIVISION

TAX LAW SUMMARY American Taxpayer Relief Act MKTG-OC-1053A LIFE INSURANCE DIVISION TAX LAW SUMMARY American Taxpayer Relief Act INDIVIDUAL TAX PROVISIONS...3 Individual Tax Rates...3 Marriage Penalty Relief...4

TAX LAW SUMMARY American Taxpayer Relief Act MKTG-OC-1053A LIFE INSURANCE DIVISION TAX LAW SUMMARY American Taxpayer Relief Act INDIVIDUAL TAX PROVISIONS...3 Individual Tax Rates...3 Marriage Penalty Relief...4

How To Get A Pension Plan Startup Cost Credit

Page 1 of 5 425 $500 maximum credit for pension plan startup costs of small employers during each of the first three years of the plan--costs paid or incurred in tax years beginning after Dec. 31, 2001

Page 1 of 5 425 $500 maximum credit for pension plan startup costs of small employers during each of the first three years of the plan--costs paid or incurred in tax years beginning after Dec. 31, 2001

Sec. 831. Tax On Insurance Companies Other Than Life Insurance Companies

Sec. 831. Tax On Insurance Companies Other Than Life Insurance Companies 831(a) General Rule Taxes computed as provided in section 11 shall be imposed for each taxable year on the taxable income of every

Sec. 831. Tax On Insurance Companies Other Than Life Insurance Companies 831(a) General Rule Taxes computed as provided in section 11 shall be imposed for each taxable year on the taxable income of every

business owner issues and depreciation deductions

business owner issues and depreciation deductions Individuals who are owners of a business, whether as sole proprietors or through a partnership, limited liability company or S corporation, have specific

business owner issues and depreciation deductions Individuals who are owners of a business, whether as sole proprietors or through a partnership, limited liability company or S corporation, have specific

PATRICK J. RUBEY & COMPANY, LTD. CERTIFIED PUBLIC ACCOUNTANTS

PATRICK J. RUBEY & COMPANY, LTD. CERTIFIED PUBLIC ACCOUNTANTS American Taxpayer Relief Act January 1, 2013 Here are the act s main tax features: Individual tax rates All the individual marginal tax rates

PATRICK J. RUBEY & COMPANY, LTD. CERTIFIED PUBLIC ACCOUNTANTS American Taxpayer Relief Act January 1, 2013 Here are the act s main tax features: Individual tax rates All the individual marginal tax rates

The Jobs and Growth Tax Relief Reconciliation Act of 2003: What Businesses and Investors Need to Know

VENTAPS: Venable Tax Policy Summary JUNE/JULY 2003 The Jobs and Growth Tax Relief Reconciliation Act of 2003: What Businesses and Investors Need to Know On May 28, 2003, President Bush signed into law

VENTAPS: Venable Tax Policy Summary JUNE/JULY 2003 The Jobs and Growth Tax Relief Reconciliation Act of 2003: What Businesses and Investors Need to Know On May 28, 2003, President Bush signed into law

North Carolina s Reference to the Internal Revenue Code Updated - Impact on 2015 North Carolina Corporate and Individual income Tax Returns

June 3, 2016 North Carolina s Reference to the Internal Revenue Code Updated - Impact on 2015 North Carolina Corporate and Individual income Tax Returns Governor McCrory signed into law Session Law 2016-6

June 3, 2016 North Carolina s Reference to the Internal Revenue Code Updated - Impact on 2015 North Carolina Corporate and Individual income Tax Returns Governor McCrory signed into law Session Law 2016-6

June 2, 2003. Re: Jobs and Growth Tax Relief Reconciliation Act of 2003

June 2, 2003 Re: Jobs and Growth Tax Relief Reconciliation Act of 2003 On Wednesday, May 28, 2003, President Bush signed into law the third largest tax cut in U.S. history. The Jobs and Growth Tax Relief

June 2, 2003 Re: Jobs and Growth Tax Relief Reconciliation Act of 2003 On Wednesday, May 28, 2003, President Bush signed into law the third largest tax cut in U.S. history. The Jobs and Growth Tax Relief

ESTIMATED IMPACT ON STATE REVENUES OF CONFORMITY TO THE REVISIONS MADE TO THE INTERNAL REVENUE CODE DURING CALENDAR YEAR 2015

ESTIMATED IMPACT ON STATE REVENUES OF CONFORMITY TO THE REVISIONS MADE TO THE INTERNAL REVENUE CODE DURING CALENDAR YEAR 2015 Prepared by the Arizona Department of Revenue Office of Economic Research and

ESTIMATED IMPACT ON STATE REVENUES OF CONFORMITY TO THE REVISIONS MADE TO THE INTERNAL REVENUE CODE DURING CALENDAR YEAR 2015 Prepared by the Arizona Department of Revenue Office of Economic Research and

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences

We will continue to expand on the provisions of the taxpayer relief act as more information becomes available. If you have any questions please feel free to contact us. Congress passes 2012 Taxpayer Relief

We will continue to expand on the provisions of the taxpayer relief act as more information becomes available. If you have any questions please feel free to contact us. Congress passes 2012 Taxpayer Relief

Unit12. Special Tax Computation Methods, Tax Credits, and Payment of Tax [Pak Ch. 14]

![Unit12. Special Tax Computation Methods, Tax Credits, and Payment of Tax [Pak Ch. 14]](/thumbs/26/9340123.jpg "Unit12. Special Tax Computation Methods, Tax Credits, and Payment of Tax [Pak Ch. 14]") 1 Unit12. Special Tax Computation Methods, Tax Credits, and Payment of Tax [Pak Ch. 14] This chapter covers several topics: the Alternative Minimum Tax, Tax Credits, and Tax Payments. Outline 2 1. Alternative

1 Unit12. Special Tax Computation Methods, Tax Credits, and Payment of Tax [Pak Ch. 14] This chapter covers several topics: the Alternative Minimum Tax, Tax Credits, and Tax Payments. Outline 2 1. Alternative

How To File A Tax Return In Massachusetts

I E O EN S P E TI T E E M V T DEPARTMENT OF REVENUE MASSACHUSETTS P L A C I D A M S V B L IBERTATE Commonwealth of Massachusetts Department of Revenue 2009 Massachusetts Premium Excise Return for Life

I E O EN S P E TI T E E M V T DEPARTMENT OF REVENUE MASSACHUSETTS P L A C I D A M S V B L IBERTATE Commonwealth of Massachusetts Department of Revenue 2009 Massachusetts Premium Excise Return for Life

PROVISIONS ENACTED BY THE AMERICAN TAXPAYER RELIEF ACT OF 2012 THAT CREATE CONFORMITY ISSUES WITH A SIGNIFICANT IMPACT ON MAINE INCOME TAXES

PROVISIONS ENACTED BY THE AMERICAN TAXPAYER RELIEF ACT OF 2012 THAT CREATE CONFORMITY ISSUES WITH A SIGNIFICANT IMPACT ON MAINE INCOME TAXES INTRODUCTION Maine income and estate taxes are substantially

PROVISIONS ENACTED BY THE AMERICAN TAXPAYER RELIEF ACT OF 2012 THAT CREATE CONFORMITY ISSUES WITH A SIGNIFICANT IMPACT ON MAINE INCOME TAXES INTRODUCTION Maine income and estate taxes are substantially

TECHNICAL EXPLANATION OF H.R. 7006, THE DISASTER TAX RELIEF ACT OF 2008

TECHNICAL EXPLANATION OF H.R. 7006, THE DISASTER TAX RELIEF ACT OF 2008 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION September 24, 2008 JCX-73-08 CONTENTS INTRODUCTION...1 Page A. Losses Attributable

TECHNICAL EXPLANATION OF H.R. 7006, THE DISASTER TAX RELIEF ACT OF 2008 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION September 24, 2008 JCX-73-08 CONTENTS INTRODUCTION...1 Page A. Losses Attributable

One Hundred Twelfth Congress of the United States of America

H. R. 8 One Hundred Twelfth Congress of the United States of America AT THE SECOND SESSION Begun and held at the City of Washington on Tuesday, the third day of January, two thousand and twelve An Act

H. R. 8 One Hundred Twelfth Congress of the United States of America AT THE SECOND SESSION Begun and held at the City of Washington on Tuesday, the third day of January, two thousand and twelve An Act

LIST OF EXPIRING FEDERAL TAX PROVISIONS 2013-2024

LIST OF EXPIRING FEDERAL TAX PROVISIONS 2013-2024 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION January 10, 2014 JCX-1-14 CONTENTS Page INTRODUCTION...1 I. FEDERAL TAX PROVISIONS EXPIRING 2013-2024...2

LIST OF EXPIRING FEDERAL TAX PROVISIONS 2013-2024 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION January 10, 2014 JCX-1-14 CONTENTS Page INTRODUCTION...1 I. FEDERAL TAX PROVISIONS EXPIRING 2013-2024...2

1. Property with useful life of less than 4 years $ 33 1/3% $ 2. Property with useful life of 4 years or more but less than 6 $ 66 2/3% $

SCHEDULE WV/SRDTC-1 STRATEGIC RESEARCH AND DEVELOPMENT TAX CREDIT THIS SCHEDULE IS FOR QUALIFIED INVESTMENT ITEMS PLACED INTO SERVICE BETWEEN JANUARY 1, 2003 AND DECEMBER 31, 2013 WV/SRDTC-1 Rev. 11/14

SCHEDULE WV/SRDTC-1 STRATEGIC RESEARCH AND DEVELOPMENT TAX CREDIT THIS SCHEDULE IS FOR QUALIFIED INVESTMENT ITEMS PLACED INTO SERVICE BETWEEN JANUARY 1, 2003 AND DECEMBER 31, 2013 WV/SRDTC-1 Rev. 11/14

In the Senate of the United States,

In the Senate of the United States, July, 01. Resolved, That the bill from the House of Representatives (H.R. 1) entitled An Act to amend the Higher Education Act of 1 to establish interest rates for new

In the Senate of the United States, July, 01. Resolved, That the bill from the House of Representatives (H.R. 1) entitled An Act to amend the Higher Education Act of 1 to establish interest rates for new

PRESENT LAW AND BACKGROUND RELATING TO SELECTED BUSINESS INCOME TAX PROVISIONS

PRESENT LAW AND BACKGROUND RELATING TO SELECTED BUSINESS INCOME TAX PROVISIONS Scheduled for a Public Hearing Before the COMMITTEE ON WAYS AND MEANS on June 2, 2011 Prepared by the Staff of the JOINT COMMITTEE

PRESENT LAW AND BACKGROUND RELATING TO SELECTED BUSINESS INCOME TAX PROVISIONS Scheduled for a Public Hearing Before the COMMITTEE ON WAYS AND MEANS on June 2, 2011 Prepared by the Staff of the JOINT COMMITTEE

Ch. 143 TAX PAYMENTS 61 143.1 CHAPTER 143. TAX PAYMENTS

Ch. 143 TAX PAYMENTS 61 143.1 CHAPTER 143. TAX PAYMENTS Sec. 143.1. Liability for payment. 143.2. Payment. 143.3. Receipt of payments. 143.4. Tax due date. 143.5. Employer withholding. 143.6. Estimated

Ch. 143 TAX PAYMENTS 61 143.1 CHAPTER 143. TAX PAYMENTS Sec. 143.1. Liability for payment. 143.2. Payment. 143.3. Receipt of payments. 143.4. Tax due date. 143.5. Employer withholding. 143.6. Estimated

S. 1693 IN THE SENATE OF THE UNITED STATES

II TH CONGRESS ST SESSION S. 9 To amend the Internal Revenue Code of 98 to prevent the avoidance of tax by insurance companies through reinsurance with non-taxed affiliates. IN THE SENATE OF THE UNITED

II TH CONGRESS ST SESSION S. 9 To amend the Internal Revenue Code of 98 to prevent the avoidance of tax by insurance companies through reinsurance with non-taxed affiliates. IN THE SENATE OF THE UNITED

The American Tax Relief Act of 2012 (HR 8, the Act )

") NATIONAL CAPITAL GIFT PLANNING COUNCIL The Fiscal Cliff, Taxes and Planned Giving: Where Are We Now? Robert E. Madden Susan Leahy BLANK ROME LLP JANUARY 9, 2013 The American Tax Relief Act of 2012 (HR

NATIONAL CAPITAL GIFT PLANNING COUNCIL The Fiscal Cliff, Taxes and Planned Giving: Where Are We Now? Robert E. Madden Susan Leahy BLANK ROME LLP JANUARY 9, 2013 The American Tax Relief Act of 2012 (HR

2011 Massachusetts S Corporation Excise Return Form 355S

I E O EN S P E TI T E E M V T MASSACHUSETTS DEPARTMENT OF REVENUE P L A C I D A M S V B L IBERTATE Commonwealth of Massachusetts Department of Revenue 2011 Massachusetts S Corporation Excise Return Form

I E O EN S P E TI T E E M V T MASSACHUSETTS DEPARTMENT OF REVENUE P L A C I D A M S V B L IBERTATE Commonwealth of Massachusetts Department of Revenue 2011 Massachusetts S Corporation Excise Return Form

BUSINESS INVESTMENT AND JOBS EXPANSION CREDIT AND CORPORATE HEADQUARTERS RELOCATION CREDIT (SUPER CREDITS)

") WV/BCS-1 Rev. March, 2004 BUSINESS INVESTMENT AND JOBS EXPANSION CREDIT AND CORPORATE HEADQUARTERS RELOCATION CREDIT (SUPER CREDITS) The following information, instructions, and forms are not a substitute

WV/BCS-1 Rev. March, 2004 BUSINESS INVESTMENT AND JOBS EXPANSION CREDIT AND CORPORATE HEADQUARTERS RELOCATION CREDIT (SUPER CREDITS) The following information, instructions, and forms are not a substitute

Tax Relief in 2001 through 2011

in 2001 through 2011 Department of the Treasury May 2008 in 2001 through 2011 The tax relief enacted during the President s term in office, principally in the Economic Growth and Relief Reconciliation

in 2001 through 2011 Department of the Treasury May 2008 in 2001 through 2011 The tax relief enacted during the President s term in office, principally in the Economic Growth and Relief Reconciliation

ECONOMIC GROWTH AND TAX RELIEF RECONCILIATION ACT OF 2001

PUBLIC LAW 107 16 JUNE 7, 2001 ECONOMIC GROWTH AND TAX RELIEF RECONCILIATION ACT OF 2001 VerDate 11-MAY-2000 03:04 Jun 12, 2001 Jkt 089139 PO 00016 Frm 00001 Fmt 6579 Sfmt 6579 E:\PUBLAW\PUBL016.107 APPS27

PUBLIC LAW 107 16 JUNE 7, 2001 ECONOMIC GROWTH AND TAX RELIEF RECONCILIATION ACT OF 2001 VerDate 11-MAY-2000 03:04 Jun 12, 2001 Jkt 089139 PO 00016 Frm 00001 Fmt 6579 Sfmt 6579 E:\PUBLAW\PUBL016.107 APPS27

Presentation of Income and Deductions

TAXATION OF S CORPORATIONS Accounting 551T - Lecture 8 Schlesinger: Chapters 6-8 Robert A. Scharlach Presentation of Income and Deductions Two Categories Separately stated items Non-separately stated items

TAXATION OF S CORPORATIONS Accounting 551T - Lecture 8 Schlesinger: Chapters 6-8 Robert A. Scharlach Presentation of Income and Deductions Two Categories Separately stated items Non-separately stated items