Form W-8BEN Completion & Submission Guidelines for Corbis Corporation Contributors

|

|

|

- Gervais Fitzgerald

- 8 years ago

- Views:

Transcription

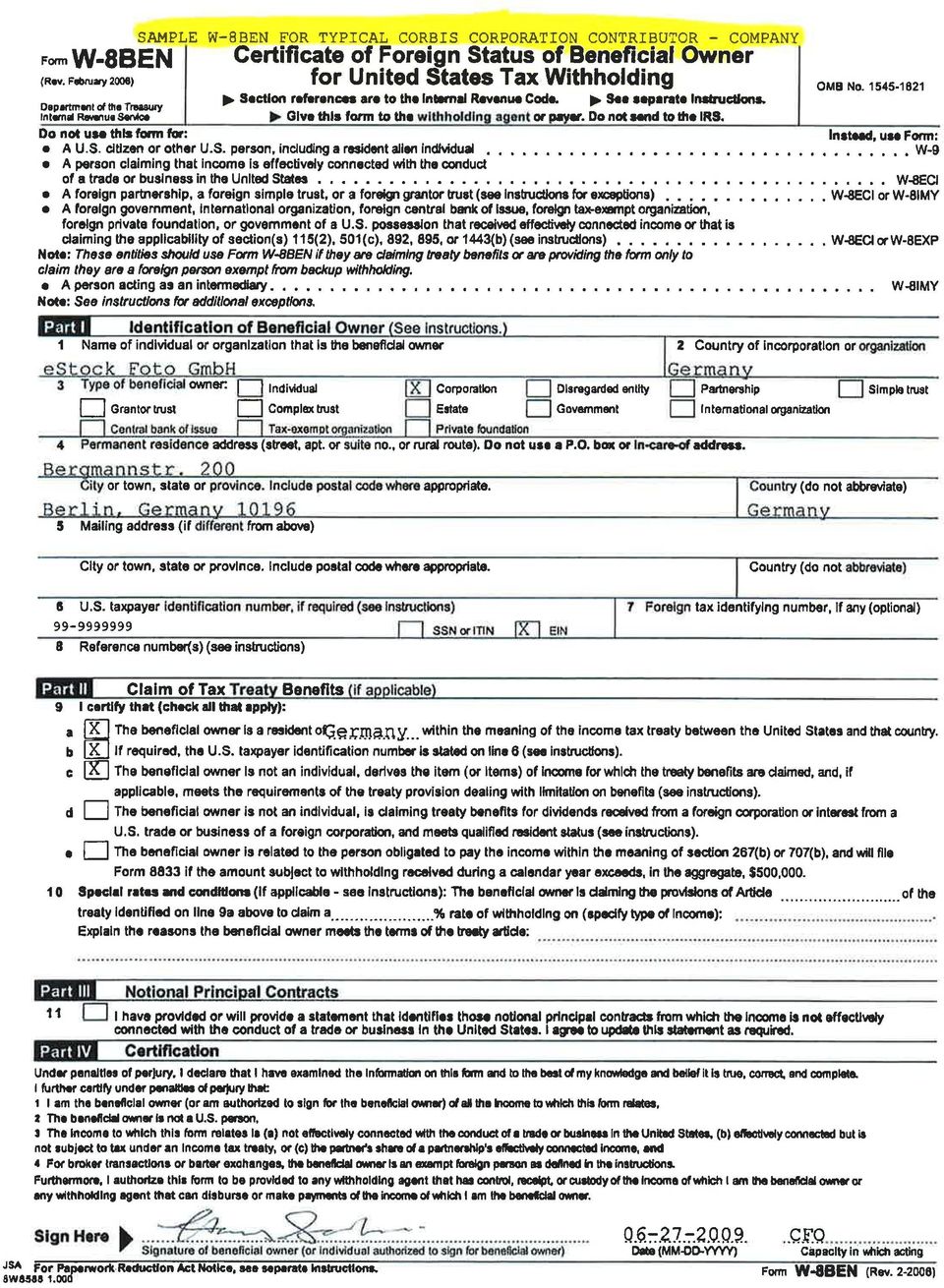

1 Form W-8BEN Completion & Submission Guidelines for Corbis Corporation Contributors Overview - Corbis Corporation, a US corporation, is required to deduct 30% withholding tax from royalties paid to individuals and companies who are not US citizens or US tax residents. This 30% withholding tax rate may be reduced or eliminated if you are resident of a country that has entered into a tax treaty with the United States and you provide Corbis with a properly completed treaty claim. To facilitate the administration of these laws, the US Internal Revenue Service (IRS) requires us to obtain a W-8BEN from each non-us contributor. The Form W-8BEN has been specifically designed for the purposes of: Certifying that you or your company is not a US citizen or US tax resident, and / or Claiming an exemption from, or reduction in, US withholding tax under an applicable income tax treaty. The information contained in this package is intended to assist individuals and entities who are not US citizens or US tax residents on the completion of Form W-8BEN. For your reference, we have included as listing of US tax treaty rates that apply to various royalty types in this package. The W-8BEN needs to be completed by the Beneficial Owner of your Corbis royalties. If you contract with Corbis as an individual (including through a sole proprietorship), you will be considered the Beneficial Owner of your royalties, and you should complete the W-8BEN. If you contract with Corbis through a company or trust, you will need to determine which party(ies) is considered the Beneficial Owner of Corbis royalties: the entity or its owners/beneficiaries. If the company or trust is considered the Beneficial Owner, it should complete the W-8BEN. If the owner(s) of the company or beneficiaries of the trust are considered the Beneficial Owner of the Corbis royalties, then the company or trust will need to complete a W-8IMY and each Beneficial Owner will need to complete a W-8BEN. If needed, please contact Royalty Accounting at RoyaltyAccounting@corbis.com, and we will send you a W-8IMY package. Guidelines on the determination of the Beneficial Owner are located on page 3.

requires us to obtain a W-8BEN from each non-us contributor.")

2 W-8BEN Completion Guidelines The information that each Beneficial Owner is required to provide on From W-8BEN, and the amount of tax that Corbis is required to withhold, depends on whether you are tax resident of a country that has entered into an income treaty with the US. If so, and you wish to claim treaty benefits, you must do the following: If needed to claim treaty benefits, apply for a US Taxpayer Identification Number (US TIN). See below for a discussion of US TIN requirements. Complete Parts I, II and IV of the W-8BEN. (Be sure to list your US TIN in Part I, Line 6, if claiming treaty benefits.) Sign and date the W-8BEN and note that capacity in which you are acting. If you are not claiming treaty benefits, you only need to complete Parts I and IV of the W-8BEN and do not need to obtain a US TIN. Once completed, send the W-8BEN containing an original signature, along with the related W-8IMY (if applicable), to the address provided on the W-8BEN completion check list. Applying for a US taxpayer identification number In those cases where you (or your company) does not own the copyrights to all images licensed to Corbis, but instead will pay a royalty to a third party for their use, each Beneficial Owner will need a US TIN in order for their treaty claim to be respected. If you do not already have a US TIN, you will need to apply for one. You can request the requisite US TIN application form by sending an to Royalty Accounting at RoyaltyAccounting@corbis.com. The application form that you will need is: Individuals Form W-7 Application for US Individual Taxpayer Identification Number (US ITIN) Entities Form SS-4 Application for Employer Identification Number (EIN) Note - The process to apply for a US TIN can be quite time-consuming and, as such, we urge you to act quickly. Foreign country treatment of withholding tax - To negate the effects of double taxation, you will likely be able to claim a tax benefit in your local country related to any US withholding tax deducted from your royalty. We recommend that you consult with your local country tax advisor on this matter. We strongly recommend that you consult a qualified tax advisor if you have questions regarding any of the information contained within this information package. 2

3 Determination of Beneficial Owner - In general, the Beneficial Owner of Corbis royalties will be the party to whom the income is attributable, as determined under US tax principals. This determination is modified, somewhat, if your company is resident of a country that has an income tax treaty with the US. In treaty countries, the Beneficial Owner of income is generally the party who pays tax on the income, as determined under local law, and providing that entity type qualifies for tax relief under the terms of the treaty. If your company or trust is not considered the Beneficial Owner of Corbis royalties, then the owners of the company or beneficiary of the trust will likely be treated as the Beneficial Owners. Some high level guidelines on which party will be considered the Beneficial Owner of Corbis royalties, which may be helpful but are not necessarily determinative, are: The Beneficial Owner of Corbis royalties will generally be: Your Company if: The Owners of your Company if: Companies resident of a country that has an income tax treaty with the US. The company is required to pay income tax on Corbis royalties. The company does not pay local country income tax on its earnings, but instead the owners of the company pay tax on their respective share of income. Companies resident of a country that does not have an income tax treaty with the US. The company provides all owners a degree of liability protection. (i.e. a corporation or limited liability company). The owners of the company if one or more are fully liable for the debts of the company. Further information on the determination of which party is the Beneficial Owner is contained in the instructions to the W-8BEN. If you have any questions on whether you company is considered a Beneficial Owner, we recommend that you consult with your tax advisor. If you require another Form W-8BEN or any other form in the W-8 series, please visit the IRS website at 3

4 W-8BEN COMPLETION CHECKLIST To be completed by the Beneficial Owner W-8BEN COMPLETION: ALL CONTRIBUTORS Part I Box 1 Enter your complete legal name. Box 2 Enter the country of incorporation or organization. Box 3 Check the entity type box that applies to you. Box 4 Enter your permanent address. Please note that this is not your mailing address. Do not use a P.O. Box, unless you live in a country that does not have street addresses. Box 5 - Your mailing address, if different from your permanent address entered in Box 4. CONTRIBUTORS CLAIMING TREATY BENEFITS Part I Box 6 If required for claiming treaty benefits, enter your US taxpayer identification number if you already have one. Formatting is 9 numeric characters, as follows: SSN or US ITIN: XXX-XX-XXXX EIN: XX-XXXXXXX If you do not have a US taxpayer identification number you will need to apply for one. Please see the section titled Applying for a US Taxpayer Identification Number above. Check the box indicating whether your US TIN is a SSN or ITIN or EIN. Part II Box 9a Check this box and enter the country where you claim to be a resident for income tax treaty purposes on the space provided. Box 9b Check this box if you are required to enter a US taxpayer identification number. Box 9c (Companies only) Check this box to certify that the beneficial owner is not an individual and, if applicable, it meets the requirements of any Limitation of Benefits clause contained in the treaty. Note - The Limitation of Benefits clause contained in most US tax treaties basically provides that, to claim treaty benefits, your company must be owned by persons who are resident of the country where the company if formed and/or it must conduct an active trade or business in such country. We recommend that you consult your tax advisor with any questions that you may have on this matter. ALL CONTRIBUTORS Part IV Sign, Date the form and note the capacity in which acting (i.e. self, company officer, etc.) SUBMITTAL: Mail the documents [Form W-8IMY, if applicable, and all related W-8BENs], containing original signatures, to the following address: Corbis Corporation Royalty Accounting 710 Second Avenue, Suite 200 Seattle, WA USA

5 Corbis Corporation US Withholding Tax on License Fees / Royalties paid to Non US Taxpayers Artistic Payments to Residents of Tax Treaty Countries: IRS Country Code Copyrights (Music & Photography) Treaty Article Motion Pictures Treaty Article Other Royalties Treaty Article Australia 2 AS 5.00% Art. 12(2) 5.00% Art. 12(2) 5.00% Art. 12(2),(4)(b) Austria AU 0.00% Art. 12(1) 10.00% Art. 12(2) 0.00% Art. 12(1) Bangladesh BG 10.00% Art. 12(2) 10.00% Art. 12(2) 10.00% Art. 12(2) Barbados BB 5.00% Art. 12(2) 5.00% Art. 12(2) 5.00% Art. 12(2) Belgium BE 0.00% Art. 12(1) 0.00% Art.12(1) 0.00% Arts. 12(1), 7 Bulgaria BU 5.00% Art. 12(2) 5.00% Art. 12(2) 5.00% Art. 12(2) Canada CA 0.00% Art. 12(3) 10.00% Arts. 12(2),12(3) 10.00% Arts. 12(2),12(3) China, People's Republic of 5 CH 10.00% Art. 11(2) 10.00% Art. 11(2) 10.00% Art. 11(2) Commonwealth of Ind. States 1 Varies 0.00% Art. 3(a) 0.00% Art. 3(a) 0.00% Art. 3(a) Cyprus CY 0.00% Art. 14(1) 0.00% Art. 14(1) 0.00% Art. 14(1) Czech Republic EZ 0.00% Art. 12(2) 0.00% Art. 12(2) 0.00% Art. 12(2) Denmark DA 0.00% Art. 12(1) 0.00% Art. 12(1) 0.00% Art. 12(1) Egypt EG 15.00% Art. 13(1) 0.00% Art. 13(2) 15.00% Arts. 13(1), 8 Estonia EN 10.00% Art. 12(2)(b) 10.00% Art. 12(2)(b) 10.00% Art. 12(2)(b) Finland FI 0.00% Art. 12(1) 0.00% Art. 12(1) 0.00% Art. 12(1) France 3 FR 0.00% Art. 12(3) 0.00% Art. 12(3) 0.00% Art. 12(3) Germany GM 0.00% Art. 12(1) 0.00% Art % Arts. 12(1) Greece GR 0.00% Art. VII 30.00% Not covered 0.00% Art. VII Hungary HU 0.00% Art. 11(1) 0.00% Art. 11(1) 0.00% Art. 11(1) Iceland IC 0.00% Art. 12(1) 5.00% Art. 12(2)(b) % Arts. 12(2), 7 India IN 15.00% Art % Art % Art. 12(2) Indonesia ID 10.00% Art. 13(2) 10.00% Art. 13(2) 10.00% Art. 13(2) Ireland EI 0.00% Art. 12(1) 0.00% Art. 12(1) 0.00% Art. 12(1) Israel IS 10.00% Art. 14(1)(b) 10.00% Art. 14(1)(b) 10.00% Art. 14(1)(b) Italy IT 0.00% Art. 12(2)(b) 8.00% Art. 12(2)(b) 8.00% Arts. 12(2)(b) Jamaica JM 10.00% Art. 12(2) 10.00% Art. 12(2) 10.00% Art. 12(2) Japan JA 0.00% Art. 12(1) 0.00% Art. 12(1) 0.00% Art. 12(1) Kazakhstan KZ 10.00% Art. 12(2) 10.00% Art. 12(2) 10.00% Art. 12(2) Korea, Rep. Of KS 10.00% Art. 14(2) 10.00% Art. 14(2) 10.00% Art. 14(2) Latvia LG 10.00% Art. 12(2)(b) 10.00% Art. 12(2)(b) 10.00% Art. 12(2)(b) Lithuania LH 10.00% Art. 12(2)(b) 10.00% Art. 12(2)(b) 10.00% Art. 12(2)(b) Luxembourg LU 0.00% Art. 13(1) 0.00% Art. 13(1) 0.00% Art. 13(1) Mexico MX 10.00% Art. 12(2) 10.00% Art. 12(2) 10.00% Art. 12(2) Morocco MO 10.00% Art. 12(2) 10.00% Art. 12(2) 10.00% Art. 12(2) Netherlands NL 0.00% Art. 13(1) 0.00% Art % Arts. 13(1),7(1) New Zealand NZ 10.00% Art. 12(2) 10.00% Art. 12(2) 10.00% Art. 12(2) Norway NO 0.00% Art. 10(1) 0.00% Art % Arts. 10(1), 5 Pakistan PK 0.00% Art. 8(1) 30.00% Not covered 0.00% Art. 8(1) Philippines RP 15.00% Art. 13(2)(a) 15.00% Art. 13(2)(a) 15.00% Art. 13(2) Poland PL 10.00% Art. 13(2) 10.00% Art. 13(2) 10.00% Art. 13(2) Portugal PO 10.00% Art. 13(2) 10.00% Art. 13(2) 10.00% Art. 13(2) Romania RO 10.00% Art. 12(2) 10.00% Art. 12(2) 10.00% Art. 12(2) Russia RS 0.00% Art. 12(1) 0.00% Art. 12(1) 0.00% Art. 12(1) Slovak Republic LO 0.00% Art. 12(2) 0.00% Art. 12(2) 0.00% Art. 12(2) Slovenia SI 5.00% Art. 12(2) 5.00% Art. 12(2) 5.00% Art. 12(2) South Africa SF 0.00% Art. 12(1) 0.00% Art. 12(1) 0.00% Art. 12(1) Spain SP 5.00% Art. 12(2)(a) 8.00% Art. 12(2)(b) 10.00% Art. 12(2)(c) Sri Lanka CE 10.00% Art. 12(2) 10.00% Art. 12(2) 10.00% Art. 12(2) Sweden SW 0.00% Art. 12(1) 0.00% Art. 12(1) 0.00% Art. 12(1) Switzerland SZ 0.00% Art. 12(1) 0.00% Art % Arts. 12(1), 7 Thailand TH 5.00% Art. 12(2)(a) 5.00% Art. 12(2)(a) 5.00% Art. 12(2)(a) Trinidad & Tobago TD 0.00% Art. 12(2) 30.00% Not covered 0.00% Art. 12(2) Tunisia TS 15.00% Art. 12(2) 15.00% Art. 12(2) 15.00% Art. 12(2) Turkey TU 10.00% Art. 12(2) 10.00% Art. 12(2) 10.00% Art. 12(2) Ukraine UP 10.00% Art. 12(2) 10.00% Art. 12(2) 10.00% Art. 12(2) United Kingdom 4 UK 0.00% Art. 12(2) 0.00% Art. 12(2) 0.00% Art. 12(2) Venezuela VE 10.00% Art. 12(2)(b) 10.00% Art. 12(2)(b) 10.00% Art. 12(2)(b) Payments to residents of non-treaty countries: 30.00% 30.00% 30.00% Notes: 1. Includes the countries of Armenia (AM), Azerbaijan (AJ), Belarus (BO), Georgia (GG), Kyrgyzstan (KG), Moldova (MD), Tajikistan (TI), Turkmenistan (TX) & Uzbekistan (UZ) 2. Includes the countries of Norfolk Island (NF), Christmas Island (KT), Cocos (Keeling) Islands (CK), Ashmore & Cartier Islands (AT), Coral Sea Islands Territory (CR) 3. Includes the countries of French Guiana (FG), Guadeloupe (GP), Martinique (MB) & Reunion (RE). 4. Includes the countries of Great Britain (United Kingdom) (UK) and Northern Ireland (UK). 5. Does not include payments received from Hong Kong. 6. Motion Contributors: Under these tax treaties, payments for the use of a motion picture (footage) are specifically excluded from the definition of "royalties". Any such payments to residents of these countries should be treated as industrial or commercial (business) profits. Business profits are subject to US income tax, at the graduated rates, if they are attributable to a US Permanent Establishment. or "PE". Payments for the use of motion picture that are not attributed to a PE are exempt from US income tax, including withholding tax, under the referenced treaty article. 7. Motion Contributors: Motion picture film or work on film or videotape or other means of reproduction for use in connection with television is 5%, other motion royalties are 0%

, 7 Bulgaria BU 5.00% Art. 12(2) 5.00% Art. 12(2) 5.00% Art. 12(2) Canada CA 0.00% Art. 12(3) 10.00% Arts. 12(2),12(3) 10.00% Arts. 12(2),12(3) China, People's Republic of 5 CH 10.00% Art. 11(2) 10.")

6 Form W-8BEN Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding (Rev. February 2006) OMB No Department of the Treasury Section references are to the Internal Revenue Code. See separate instructions. Internal Revenue Service Give this form to the withholding agent or payer. Do not send to the IRS. Do not use this form for: Instead, use Form: A U.S. citizen or other U.S. person, including a resident alien individual W-9 A person claiming that income is effectively connected with the conduct of a trade or business in the United States W-8ECI A foreign partnership, a foreign simple trust, or a foreign grantor trust (see instructions for exceptions) W-8ECI or W-8IMY A foreign government, international organization, foreign central bank of issue, foreign tax-exempt organization, foreign private foundation, or government of a U.S. possession that received effectively connected income or that is claiming the applicability of section(s) 115(2), 501(c), 892, 895, or 1443(b) (see instructions) W-8ECI or W-8EXP Note: These entities should use Form W-8BEN if they are claiming treaty benefits or are providing the form only to claim they are a foreign person exempt from backup withholding. A person acting as an intermediary W-8IMY Note: See instructions for additional exceptions. Part I Identification of Beneficial Owner (See instructions.) 1 Name of individual or organization that is the beneficial owner 2 Country of incorporation or organization 3 4 Type of beneficial owner: Individual Corporation Disregarded entity Partnership Simple trust Grantor trust Complex trust Estate Government International organization Central bank of issue Tax-exempt organization Private foundation Permanent residence address (street, apt. or suite no., or rural route). Do not use a P.O. box or in-care-of address. City or town, state or province. Include postal code where appropriate. Country (do not abbreviate) 5 Mailing address (if different from above) City or town, state or province. Include postal code where appropriate. Country (do not abbreviate) 6 U.S. taxpayer identification number, if required (see instructions) 7 SSN or ITIN EIN 8 Reference number(s) (see instructions) Foreign tax identifying number, if any (optional) Part II 9 10 a b c d e Claim of Tax Treaty Benefits (if applicable) I certify that (check all that apply): The beneficial owner is a resident of within the meaning of the income tax treaty between the United States and that country. If required, the U.S. taxpayer identification number is stated on line 6 (see instructions). The beneficial owner is not an individual, derives the item (or items) of income for which the treaty benefits are claimed, and, if applicable, meets the requirements of the treaty provision dealing with limitation on benefits (see instructions). The beneficial owner is not an individual, is claiming treaty benefits for dividends received from a foreign corporation or interest from a U.S. trade or business of a foreign corporation, and meets qualified resident status (see instructions). The beneficial owner is related to the person obligated to pay the income within the meaning of section 267(b) or 707(b), and will file Form 8833 if the amount subject to withholding received during a calendar year exceeds, in the aggregate, $500,000. Special rates and conditions (if applicable see instructions): The beneficial owner is claiming the provisions of Article of the treaty identified on line 9a above to claim a % rate of withholding on (specify type of income):. Explain the reasons the beneficial owner meets the terms of the treaty article: Part III Notional Principal Contracts 11 I have provided or will provide a statement that identifies those notional principal contracts from which the income is not effectively connected with the conduct of a trade or business in the United States. I agree to update this statement as required. Part IV Certification Under penalties of perjury, I declare that I have examined the information on this form and to the best of my knowledge and belief it is true, correct, and complete. I further certify under penalties of perjury that: 1 I am the beneficial owner (or am authorized to sign for the beneficial owner) of all the income to which this form relates, 2 The beneficial owner is not a U.S. person, 3 The income to which this form relates is (a) not effectively connected with the conduct of a trade or business in the United States, (b) effectively connected but is not subject to tax under an income tax treaty, or (c) the partner s share of a partnership s effectively connected income, and 4 For broker transactions or barter exchanges, the beneficial owner is an exempt foreign person as defined in the instructions. Furthermore, I authorize this form to be provided to any withholding agent that has control, receipt, or custody of the income of which I am the beneficial owner or any withholding agent that can disburse or make payments of the income of which I am the beneficial owner. Sign Here Signature of beneficial owner (or individual authorized to sign for beneficial owner) Date (MM-DD-YYYY) Capacity in which acting For Paperwork Reduction Act Notice, see separate instructions. Cat. No Z Form W-8BEN (Rev ) Printed on Recycled Paper

7

8

9 Instructions for Form W-8BEN (Rev. February 2006) Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding Department of the Treasury Internal Revenue Service If applicable, claim a reduced rate of, or exemption General Instructions from, withholding as a resident of a foreign country with Section references are to the Internal Revenue Code which the United States has an income tax treaty. unless otherwise noted. You may also be required to submit Form W-8BEN to For definitions of terms used throughout these claim an exception from domestic information reporting instructions, see Definitions on pages 3 and 4. and backup withholding for certain types of income that are not subject to foreign-person withholding. Such Purpose of form. Foreign persons are subject to U.S. income includes: tax at a 30% rate on income they receive from U.S. Broker proceeds. sources that consists of: Short-term (183 days or less) original issue discount Interest (including certain original issue discount (OID). (OID)); Bank deposit interest. Dividends; Foreign source interest, dividends, rents, or royalties. Rents; Proceeds from a wager placed by a nonresident alien Royalties; individual in the games of blackjack, baccarat, craps, Premiums; roulette, or big-6 wheel. Annuities; You may also use Form W-8BEN to certify that income Compensation for, or in expectation of, services from a notional principal contract is not effectively performed; connected with the conduct of a trade or business in the Substitute payments in a securities lending transaction; United States. or A withholding agent or payer of the income may rely Other fixed or determinable annual or periodical gains, on a properly completed Form W-8BEN to treat a profits, or income. payment associated with the Form W-8BEN as a This tax is imposed on the gross amount paid and is payment to a foreign person who beneficially owns the generally collected by withholding under section 1441 or amounts paid. If applicable, the withholding agent may 1442 on that amount. A payment is considered to have rely on the Form W-8BEN to apply a reduced rate of been made whether it is made directly to the beneficial withholding at source. owner or to another person, such as an intermediary, Provide Form W-8BEN to the withholding agent or agent, or partnership, for the benefit of the beneficial payer before income is paid or credited to you. Failure to owner. provide a Form W-8BEN when requested may lead to In addition, section 1446 requires a partnership withholding at a 30% rate (foreign-person withholding) or conducting a trade or business in the United States to the backup withholding rate. withhold tax on a foreign partner s distributive share of Additional information. For additional information and the partnership s effectively connected taxable income. instructions for the withholding agent, see the Instructions Generally, a foreign person that is a partner in a for the Requester of Forms W-8BEN, W-8ECI, W-8EXP, partnership that submits a Form W-8 for purposes of and W-8IMY. section 1441 or 1442 will satisfy the documentation Who must file. You must give Form W-8BEN to the requirements under section 1446 as well. However, in withholding agent or payer if you are a foreign person some cases the documentation requirements of sections and you are the beneficial owner of an amount subject to 1441 and 1442 do not match the documentation withholding. Submit Form W-8BEN when requested by requirements of section See Regulations sections the withholding agent or payer whether or not you are through Further, the owner of a claiming a reduced rate of, or exemption from, disregarded entity, rather than the disregarded entity withholding. itself, shall submit the appropriate Form W-8 for purposes of section Do not use Form W-8BEN if: You are a U.S. citizen (even if you reside outside the If you receive certain types of income, you must United States) or other U.S. person (including a resident provide Form W-8BEN to: alien individual). Instead, use Form W-9, Request for Establish that you are not a U.S. person; Taxpayer Identification Number and Certification. Claim that you are the beneficial owner of the income You are a disregarded entity with a single owner that is for which Form W-8BEN is being provided or a partner in a U.S. person and you are not a hybrid entity claiming a partnership subject to section 1446; and treaty benefits. Instead, provide Form W-9. Cat. No H

10 You are a nonresident alien individual who claims W-8IMY and accompanying documentation. See exemption from withholding on compensation for Regulations sections through independent or dependent personal services performed Giving Form W-8BEN to the withholding agent. Do in the United States. Instead, provide Form 8233, not send Form W-8BEN to the IRS. Instead, give it to the Exemption from Withholding on Compensation for person who is requesting it from you. Generally, this will Independent (and Certain Dependent) Personal Services be the person from whom you receive the payment, who of a Nonresident Alien Individual, or Form W-4, credits your account, or a partnership that allocates Employee s Withholding Allowance Certificate. income to you. Give Form W-8BEN to the person You are receiving income that is effectively connected requesting it before the payment is made to you, credited with the conduct of a trade or business in the United to your account or allocated. If you do not provide this States, unless it is allocable to you through a partnership. form, the withholding agent may have to withhold at the Instead, provide Form W-8ECI, Certificate of Foreign 30% rate, backup withholding rate, or the rate applicable Person s Claim That Income Is Effectively Connected under section If you receive more than one type of With the Conduct of a Trade or Business in the United income from a single withholding agent for which you States. If any of the income for which you have provided claim different benefits, the withholding agent may, at its a Form W-8BEN becomes effectively connected, this is a option, require you to submit a Form W-8BEN for each change in circumstances and Form W-8BEN is no longer different type of income. Generally, a separate Form valid. You must file Form W-8ECI. See Change in W-8BEN must be given to each withholding agent. circumstances on this page. Note. If you own the income or account jointly with You are filing for a foreign government, international one or more other persons, the income or account will be organization, foreign central bank of issue, foreign treated by the withholding agent as owned by a foreign tax-exempt organization, foreign private foundation, or person if Forms W-8BEN are provided by all of the government of a U.S. possession claiming the owners. If the withholding agent receives a Form W-9 applicability of section 115(2), 501(c), 892, 895, or from any of the joint owners, the payment must be 1443(b). Instead, provide Form W-8EXP, Certificate of treated as made to a U.S. person. Foreign Government or Other Foreign Organization for Change in circumstances. If a change in United States Tax Withholding. However, you should use circumstances makes any information on the Form Form W-8BEN if you are claiming treaty benefits or are W-8BEN you have submitted incorrect, you must notify providing the form only to claim you are a foreign person the withholding agent or payer within 30 days of the exempt from backup withholding. You should use Form change in circumstances and you must file a new Form W-8ECI if you received effectively connected income (for W-8BEN or other appropriate form. example, income from commercial activities). If you use Form W-8BEN to certify that you are a You are a foreign flow-through entity, other than a foreign person, a change of address to an address in the hybrid entity, claiming treaty benefits. Instead, provide United States is a change in circumstances. Generally, a Form W-8IMY, Certificate of Foreign Intermediary, change of address within the same foreign country or to Foreign Flow-Through Entity, or Certain U.S. Branches another foreign country is not a change in circumstances. for United States Tax Withholding. However, if you are a However, if you use Form W-8BEN to claim treaty partner, beneficiary, or owner of a flow-through entity and benefits, a move to the United States or outside the you are not yourself a flow-through entity, you may be country where you have been claiming treaty benefits is a required to furnish a Form W-8BEN to the flow-through change in circumstances. In that case, you must notify entity. the withholding agent or payer within 30 days of the You are a disregarded entity for purposes of section move Instead, the owner of the entity must submit the If you become a U.S. citizen or resident alien after you form. submit Form W-8BEN, you are no longer subject to the You are a reverse hybrid entity transmitting beneficial 30% withholding rate or the withholding tax on a foreign owner documentation provided by your interest holders to partner s share of effectively connected income. You claim treaty benefits on their behalf. Instead, provide must notify the withholding agent or payer within 30 days Form W-8IMY. of becoming a U.S. citizen or resident alien. You may be You are a withholding foreign partnership or a required to provide a Form W-9. For more information, withholding foreign trust within the meaning of sections see Form W-9 and instructions and 1442 and the accompanying regulations. A Expiration of Form W-8BEN. Generally, a Form withholding foreign partnership or a withholding foreign W-8BEN provided without a U.S. taxpayer identification trust is a foreign partnership or trust that has entered into number (TIN) will remain in effect for a period starting on a withholding agreement with the IRS under which it the date the form is signed and ending on the last day of agrees to assume primary withholding responsibility for the third succeeding calendar year, unless a change in each partner s, beneficiary s, or owner s distributive share circumstances makes any information on the form of income subject to withholding that is paid to the incorrect. For example, a Form W-8BEN signed on partnership or trust. Instead, provide Form W-8IMY. September 30, 2005, remains valid through December You are acting as an intermediary (that is, acting not 31, A Form W-8BEN furnished with a U.S. TIN will for your own account, but for the account of others as an remain in effect until a change in circumstances makes agent, nominee, or custodian). Instead, provide Form any information on the form incorrect, provided that the W-8IMY. withholding agent reports on Form 1042-S at least one You are a foreign partnership or foreign grantor trust payment annually to the beneficial owner who provided for purposes of section Instead, provide Form the Form W-8BEN. See the instructions for line 6-2-

Personal Services be the person from whom you receive the payment, who of a Nonresident Alien Individual, or Form W-4, credits your account,")

11 beginning on page 4 for circumstances under which you must provide a U.S. TIN. Definitions Beneficial owner. For payments other than those for which a reduced rate of withholding is claimed under an income tax treaty, the beneficial owner of income is generally the person who is required under U.S. tax principles to include the income in gross income on a tax return. A person is not a beneficial owner of income, however, to the extent that person is receiving the income as a nominee, agent, or custodian, or to the extent the person is a conduit whose participation in a transaction is disregarded. In the case of amounts paid that do not constitute income, beneficial ownership is determined as if the payment were income. Foreign partnerships, foreign simple trusts, and foreign grantor trusts are not the beneficial owners of income paid to the partnership or trust. The beneficial owners of income paid to a foreign partnership are generally the partners in the partnership, provided that the partner is not itself a partnership, foreign simple or grantor trust, nominee or other agent. The beneficial owners of income paid to a foreign simple trust (that is, a foreign trust that is described in section 651(a)) are generally the beneficiaries of the trust, if the beneficiary is not a foreign partnership, foreign simple or grantor trust, nominee or other agent. The beneficial owners of a foreign grantor trust (that is, a foreign trust to the extent that all or a portion of the income of the trust is treated as owned by the grantor or another person under sections 671 through 679) are the persons treated as the owners of the trust. The beneficial owners of income paid to a foreign complex trust (that is, a foreign trust that is not a foreign simple trust or foreign grantor trust) is the trust itself. For purposes of section 1446, the same beneficial owner rules apply, except that under section 1446 a foreign simple trust rather than the beneficiary provides the form to the partnership. The beneficial owner of income paid to a foreign estate is the estate itself. Note. A payment to a U.S. partnership, U.S. trust, or U.S. estate is treated as a payment to a U.S. payee that is not subject to 30% withholding. A U.S. partnership, trust, or estate should provide the withholding agent with a Form W-9. For purposes of section 1446, a U.S. grantor trust or disregarded entity shall not provide the withholding agent a Form W-9 in its own right. Rather, the grantor or other owner shall provide the withholding agent the appropriate form. Foreign person. A foreign person includes a nonresident alien individual, a foreign corporation, a foreign partnership, a foreign trust, a foreign estate, and any other person that is not a U.S. person. It also includes a foreign branch or office of a U.S. financial institution or U.S. clearing organization if the foreign branch is a qualified intermediary. Generally, a payment to a U.S. branch of a foreign person is a payment to a foreign person. Nonresident alien individual. Any individual who is not a citizen or resident alien of the United States is a nonresident alien individual. An alien individual meeting either the green card test or the substantial presence test for the calendar year is a resident alien. Any person not meeting either test is a nonresident alien individual. Additionally, an alien individual who is a resident of a foreign country under the residence article of an income tax treaty, or an alien individual who is a bona fide resident of Puerto Rico, Guam, the Commonwealth of the Northern Mariana Islands, the U.S. Virgin Islands, or American Samoa is a nonresident alien individual. See Pub. 519, U.S. Tax Guide for Aliens, for more information on resident and nonresident alien status. Even though a nonresident alien individual! married to a U.S. citizen or resident alien may CAUTION choose to be treated as a resident alien for certain purposes (for example, filing a joint income tax return), such individual is still treated as a nonresident alien for withholding tax purposes on all income except wages. Flow-through entity. A flow-through entity is a foreign partnership (other than a withholding foreign partnership), a foreign simple or foreign grantor trust (other than a withholding foreign trust), or, for payments for which a reduced rate of withholding is claimed under an income tax treaty, any entity to the extent the entity is considered to be fiscally transparent (see below) with respect to the payment by an interest holder s jurisdiction. For purposes of section 1446, a foreign partnership or foreign grantor trust must submit Form W-8IMY to establish the partnership or grantor trust as a look through entity. The Form W-8IMY may be accompanied by this form or another version of Form W-8 or Form W-9 to establish the foreign or domestic status of a partner or grantor or other owner. See Regulations section Hybrid entity. A hybrid entity is any person (other than an individual) that is treated as fiscally transparent (see below) in the United States but is not treated as fiscally transparent by a country with which the United States has an income tax treaty. Hybrid entity status is relevant for claiming treaty benefits. See the instructions for line 9c on page 5. Reverse hybrid entity. A reverse hybrid entity is any person (other than an individual) that is not fiscally transparent under U.S. tax law principles but that is fiscally transparent under the laws of a jurisdiction with which the United States has an income tax treaty. See the instructions for line 9c on page 5. Fiscally transparent entity. An entity is treated as fiscally transparent with respect to an item of income for which treaty benefits are claimed to the extent that the interest holders in the entity must, on a current basis, take into account separately their shares of an item of income paid to the entity, whether or not distributed, and must determine the character of the items of income as if they were realized directly from the sources from which realized by the entity. For example, partnerships, common trust funds, and simple trusts or grantor trusts are generally considered to be fiscally transparent with respect to items of income received by them. Disregarded entity. A business entity that has a single owner and is not a corporation under Regulations section (b) is disregarded as an entity separate from its owner. -3-

12 A disregarded entity shall not submit this form to a partnership for purposes of section Instead, the owner of such entity shall provide appropriate documentation. See Regulations section Amounts subject to withholding. Generally, an amount subject to withholding is an amount from sources within the United States that is fixed or determinable annual or periodical (FDAP) income. FDAP income is all income included in gross income, including interest (as well as OID), dividends, rents, royalties, and compensation. FDAP income does not include most gains from the sale of property (including market discount and option premiums). For purposes of section 1446, the amount subject to withholding is the foreign partner s share of the partnership s effectively connected taxable income. Withholding agent. Any person, U.S. or foreign, that has control, receipt, or custody of an amount subject to withholding or who can disburse or make payments of an amount subject to withholding is a withholding agent. The withholding agent may be an individual, corporation, partnership, trust, association, or any other entity, including (but not limited to) any foreign intermediary, foreign partnership, and U.S. branches of certain foreign banks and insurance companies. Generally, the person who pays (or causes to be paid) the amount subject to withholding to the foreign person (or to its agent) must withhold. For purposes of section 1446, the withholding agent is the partnership conducting the trade or business in the United States. For a publicly traded partnership, the withholding agent may be the partnership, a nominee holding an interest on behalf of a foreign person, or both. See Regulations sections through governed. If you are an individual, enter N/A (for not applicable ). Line 3. Check the one box that applies. By checking a box, you are representing that you qualify for this classification. You must check the box that represents your classification (for example, corporation, partnership, trust, estate, etc.) under U.S. tax principles. Do not check the box that describes your status under the law of the treaty country. If you are a partnership or disregarded entity receiving a payment for which treaty benefits are being claimed, you must check the Partnership or Disregarded entity box. If you are a sole proprietor, check the Individual box, not the Disregarded entity box. Only entities that are tax-exempt under section! 501 should check the Tax-exempt organization CAUTION box. Such organizations should use Form W-8BEN only if they are claiming a reduced rate of withholding under an income tax treaty or some code exception other than section 501. Use Form W-8EXP if you are claiming an exemption from withholding under section 501. Line 4. Your permanent residence address is the address in the country where you claim to be a resident for purposes of that country s income tax. If you are giving Form W-8BEN to claim a reduced rate of withholding under an income tax treaty, you must determine your residency in the manner required by the treaty. Do not show the address of a financial institution, a post office box, or an address used solely for mailing purposes. If you are an individual who does not have a tax residence in any country, your permanent residence is where you normally reside. If you are not an individual and you do not have a tax residence in any country, the permanent residence address is where you maintain your principal office. Line 5. Enter your mailing address only if it is different Specific Instructions from the address you show on line 4. Line 6. If you are an individual, you are generally A hybrid entity should give Form W-8BEN to a required to enter your social security number (SSN). To TIP withholding agent only for income for which it is apply for an SSN, get Form SS-5 from a Social Security claiming a reduced rate of withholding under an Administration (SSA) office or, if in the United States, you income tax treaty. A reverse hybrid entity should give may call the SSA at Fill in Form SS-5 Form W-8BEN to a withholding agent only for income for and return it to the SSA. which no treaty benefit is being claimed. If you do not have an SSN and are not eligible to get one, you must get an individual taxpayer identification Part I number (ITIN). To apply for an ITIN, file Form W-7 with Line 1. Enter your name. If you are a disregarded entity the IRS. It usually takes 4-6 weeks to get an ITIN. with a single owner who is a foreign person and you are An ITIN is for tax use only. It does not entitle you not claiming treaty benefits as a hybrid entity, this form to social security benefits or change your should be completed and signed by your foreign single! CAUTION employment or immigration status under U.S. law. owner. If the account to which a payment is made or credited is in the name of the disregarded entity, the If you are not an individual or you are an individual foreign single owner should inform the withholding agent who is an employer or you are engaged in a U.S. trade or of this fact. This may be done by including the name and business as a sole proprietor, you must enter an account number of the disregarded entity on line 8 employer identification number (EIN). If you do not have (reference number) of the form. However, if you are a an EIN, you should apply for one on Form SS-4, disregarded entity that is claiming treaty benefits as a Application for Employer Identification Number. If you are hybrid entity, this form should be completed and signed a disregarded entity claiming treaty benefits as a hybrid by you. entity, enter your EIN. Line 2. If you are a corporation, enter the country of A partner in a partnership conducting a trade or incorporation. If you are another type of entity, enter the business in the United States will likely be allocated country under whose laws you are created, organized, or effectively connected taxable income. The partner is -4-

.")

13 required to file a U.S. federal income tax return and must Meets the limitation on benefits provisions contained have a U.S. taxpayer identification number (TIN). in the treaty, if any. You must provide a U.S. TIN if you are: An item of income may be derived by either the entity Claiming an exemption from withholding under section receiving the item of income or by the interest holders in 871(f) for certain annuities received under qualified plans, the entity or, in certain circumstances, both. An item of A foreign grantor trust with 5 or fewer grantors, income paid to an entity is considered to be derived by Claiming benefits under an income tax treaty, or the entity only if the entity is not fiscally transparent under Submitting the form to a partnership that conducts a the laws of the entity s jurisdiction with respect to the item trade or business in the United States. of income. An item of income paid to an entity shall be However, a U.S. TIN is not required to be shown in considered to be derived by the interest holder in the order to claim treaty benefits on the following items of entity only if: income: The interest holder is not fiscally transparent in its Dividends and interest from stocks and debt jurisdiction with respect to the item of income, and obligations that are actively traded; The entity is considered to be fiscally transparent Dividends from any redeemable security issued by an under the laws of the interest holder s jurisdiction with investment company registered under the Investment respect to the item of income. An item of income paid Company Act of 1940 (mutual fund); directly to a type of entity specifically identified in a treaty Dividends, interest, or royalties from units of beneficial as a resident of a treaty jurisdiction is treated as derived interest in a unit investment trust that are (or were upon by a resident of that treaty jurisdiction. issuance) publicly offered and are registered with the If an entity is claiming treaty benefits on its own behalf, SEC under the Securities Act of 1933; and it should complete Form W-8BEN. If an interest holder in Income related to loans of any of the above securities. an entity that is considered fiscally transparent in the interest holder s jurisdiction is claiming a treaty benefit, You may want to obtain and provide a U.S. TIN the interest holder should complete Form W-8BEN on its TIP on Form W-8BEN even though it is not required. own behalf and the fiscally transparent entity should A Form W-8BEN containing a U.S. TIN remains associate the interest holder s Form W-8BEN with a valid for as long as your status and the information Form W-8IMY completed by the entity. relevant to the certifications you make on the form remain unchanged provided at least one payment is reported to An income tax treaty may not apply to reduce the you annually on Form 1042-S.! amount of any tax on an item of income received CAUTION Line 7. If your country of residence for tax purposes has by an entity that is treated as a domestic issued you a tax identifying number, enter it here. For corporation for U.S. tax purposes. Therefore, neither the example, if you are a resident of Canada, enter your domestic corporation nor its shareholders are entitled to Social Insurance Number. the benefits of a reduction of U.S. income tax on an item Line 8. This line may be used by the filer of Form of income received from U.S. sources by the corporation. W-8BEN or by the withholding agent to whom it is To determine whether an entity meets the limitation on provided to include any referencing information that is benefits provisions of a treaty, you must consult the useful to the withholding agent in carrying out its specific provisions or articles under the treaties. Income obligations. For example, withholding agents who are tax treaties are available on the IRS website at required to associate the Form W-8BEN with a particular Form W-8IMY may want to use line 8 for a referencing If you are an entity that derives the income as a number or code that will make the association clear. A TIP resident of a treaty country, you may check this beneficial owner may use line 8 to include the number of box if the applicable income tax treaty does not the account for which he or she is providing the form. A contain a limitation on benefits provision. foreign single owner of a disregarded entity may use line 8 to inform the withholding agent that the account to Line 9d. If you are a foreign corporation claiming treaty which a payment is made or credited is in the name of benefits under an income tax treaty that entered into the disregarded entity (see instructions for line 1 on page force before January 1, 1987 (and has not been 4). renegotiated) on (a) U.S. source dividends paid to you by another foreign corporation or (b) U.S. source interest Part II paid to you by a U.S. trade or business of another foreign corporation, you must generally be a qualified resident Line 9a. Enter the country where you claim to be a of a treaty country. See section 884 for the definition of resident for income tax treaty purposes. For treaty interest paid by a U.S. trade or business of a foreign purposes, a person is a resident of a treaty country if the corporation ( branch interest ) and other applicable rules. person is a resident of that country under the terms of the In general, a foreign corporation is a qualified resident treaty. of a country if any of the following apply. Line 9b. If you are claiming benefits under an income It meets a 50% ownership and base erosion test. tax treaty, you must have a U.S. TIN unless one of the It is primarily and regularly traded on an established exceptions listed in the line 6 instructions above applies. securities market in its country of residence or the United Line 9c. An entity (but not an individual) that is claiming States. a reduced rate of withholding under an income tax treaty It carries on an active trade or business in its country must represent that it: of residence. Derives the item of income for which the treaty benefit It gets a ruling from the IRS that it is a qualified is claimed, and resident. -5-

14 See Regulations section for the requirements fellowship income. See Compensation for Dependent that must be met to satisfy each of these tests. Personal Services in the Instructions for Form If you are claiming treaty benefits under an If you are a nonresident alien individual who! income tax treaty entered into force after TIP received noncompensatory scholarship or CAUTION December 31, 1986, do not check box 9d. fellowship income and personal services income Instead, check box 9c. (including compensatory scholarship or fellowship Line 9e. Check this box if you are related to the income) from the same withholding agent, you may use withholding agent within the meaning of section 267(b) or Form 8233 to claim a tax treaty withholding exemption for 707(b) and the aggregate amount subject to withholding part or all of both types of income. received during the calendar year will exceed $500,000. Completing lines 4 and 9a. Most tax treaties that Additionally, you must file Form 8833, Treaty-Based contain an article exempting scholarship or fellowship Return Position Disclosure Under Section 6114 or grant income from taxation require that the recipient be a 7701(b). resident of the other treaty country at the time of, or Line 10 immediately prior to, entry into the United States. Thus, a student or researcher may claim the exemption even if he Line 10 must be used only if you are claiming treaty or she no longer has a permanent address in the other benefits that require that you meet conditions not covered treaty country after entry into the United States. If this is by the representations you make in lines 9a through 9e. the case, you may provide a U.S. address on line 4 and However, this line should always be completed by foreign still be eligible for the exemption if all other conditions students and researchers claiming treaty benefits. See required by the tax treaty are met. You must also identify Scholarship and fellowship grants below for more on line 9a the tax treaty country of which you were a information. resident at the time of, or immediately prior to, your entry The following are additional examples of persons who into the United States. should complete this line. Completing line 10. You must complete line 10 if you Exempt organizations claiming treaty benefits under are a student or researcher claiming an exemption from the exempt organization articles of the treaties with taxation on your scholarship or fellowship grant income Canada, Mexico, Germany, and the Netherlands. under a tax treaty. Foreign corporations that are claiming a preferential rate applicable to dividends based on ownership of a Nonresident alien student or researcher who specific percentage of stock. becomes a resident alien. You must use Form W-9 to Persons claiming treaty benefits on royalties if the claim an exception to a saving clause. See Nonresident treaty contains different withholding rates for different alien who becomes a resident alien on this page for a types of royalties. general explanation of saving clauses and exceptions to them. This line is generally not applicable to claiming treaty benefits under an interest or dividends (other than Example. Article 20 of the U.S.-China income tax dividends subject to a preferential rate based on treaty allows an exemption from tax for scholarship ownership) article of a treaty. income received by a Chinese student temporarily present in the United States. Under U.S. law, this student Nonresident alien who becomes a resident alien. will become a resident alien for tax purposes if his or her Generally, only a nonresident alien individual may use stay in the United States exceeds 5 calendar years. the terms of a tax treaty to reduce or eliminate U.S. tax However, paragraph 2 of the first protocol to the on certain types of income. However, most tax treaties U.S.-China treaty (dated April 30, 1984) allows the contain a provision known as a saving clause. provisions of Article 20 to continue to apply even after the Exceptions specified in the saving clause may permit an Chinese student becomes a resident alien of the United exemption from tax to continue for certain types of States. A Chinese student who qualifies for this exception income even after the recipient has otherwise become a (under paragraph 2 of the first protocol) and is relying on U.S. resident alien for tax purposes. The individual must this exception to claim an exemption from tax on his or use Form W-9 to claim the tax treaty benefit. See the her scholarship or fellowship income would complete instructions for Form W-9 for more information. Also see Form W-9. Nonresident alien student or researcher who becomes a resident alien later for an example. Part III Scholarship and fellowship grants. A nonresident alien student (including a trainee or business apprentice) If you check this box, you must provide the withholding or researcher who receives noncompensatory agent with the required statement for income from a scholarship or fellowship income may use Form W-8BEN notional principal contract that is to be treated as income to claim benefits under a tax treaty that apply to reduce not effectively connected with the conduct of a trade or or eliminate U.S. tax on such income. No Form W-8BEN business in the United States. You should update this is required unless a treaty benefit is being claimed. A statement as often as necessary. A new Form W-8BEN nonresident alien student or researcher who receives is not required for each update provided the form compensatory scholarship or fellowship income must use otherwise remains valid. Form 8233 to claim any benefits of a tax treaty that apply to that income. The student or researcher must use Form Part IV W-4 for any part of such income for which he or she is Form W-8BEN must be signed and dated by the not claiming a tax treaty withholding exemption. Do not beneficial owner of the income, or, if the beneficial owner use Form W-8BEN for compensatory scholarship or is not an individual, by an authorized representative or -6-

15 officer of the beneficial owner. If Form W-8BEN is information. We need it to ensure that you are complying completed by an agent acting under a duly authorized with these laws and to allow us to figure and collect the power of attorney, the form must be accompanied by the right amount of tax. power of attorney in proper form or a copy thereof You are not required to provide the information specifically authorizing the agent to represent the requested on a form that is subject to the Paperwork principal in making, executing, and presenting the form. Reduction Act unless the form displays a valid OMB Form 2848, Power of Attorney and Declaration of control number. Books or records relating to a form or its Representative, may be used for this purpose. The instructions must be retained as long as their contents agent, as well as the beneficial owner, may incur liability may become material in the administration of any Internal for the penalties provided for an erroneous, false, or Revenue law. Generally, tax returns and return fraudulent form. information are confidential, as required by section Broker transactions or barter exchanges. Income The time needed to complete and file this form will from transactions with a broker or a barter exchange is vary depending on individual circumstances. The subject to reporting rules and backup withholding unless estimated average time is: Recordkeeping, 5 hr., Form W-8BEN or a substitute form is filed to notify the 58 min.; Learning about the law or the form, 3 hr., broker or barter exchange that you are an exempt foreign 46 min.; Preparing and sending the form to IRS, 4 hr., person. 2 min. You are an exempt foreign person for a calendar year If you have comments concerning the accuracy of in which: these time estimates or suggestions for making this form You are a nonresident alien individual or a foreign simpler, we would be happy to hear from you. You can corporation, partnership, estate, or trust; us at *taxforms@irs.gov. Please put Forms You are an individual who has not been, and does not Comment on the subject line. Or you can write to plan to be, present in the United States for a total of 183 Internal Revenue Service, Tax Products Coordinating days or more during the calendar year; and Committee, SE:W:CAR:MP:T:T:SP, 1111 Constitution You are neither engaged, nor plan to be engaged Ave. NW, IR-6406, Washington, DC Do not send during the year, in a U.S. trade or business that has Form W-8BEN to this office. Instead, give it to your effectively connected gains from transactions with a withholding agent. broker or barter exchange. Paperwork Reduction Act Notice. We ask for the information on this form to carry out the Internal Revenue laws of the United States. You are required to provide the -7-

MIT U.S. Income Tax Presentation Non US Resident Students

MIT U.S. Income Tax Presentation Non US Resident Students PwC Boston Nabih Daaboul Carol McNeil Rich Wagman 1 Basic U.S. Tax Overview for International Students A foreign national is a person born outside

MIT U.S. Income Tax Presentation Non US Resident Students PwC Boston Nabih Daaboul Carol McNeil Rich Wagman 1 Basic U.S. Tax Overview for International Students A foreign national is a person born outside

Babcock & Brown Infrastructure. Guide for Completing IRS Forms: W-8IMY & W-8BEN

Babcock & Brown Infrastructure Guide for Completing IRS Forms: W-8IMY & W-8BEN GUIDE FOR COMPLETING IRS FORMS: W-8IMY & W-8BEN Contents Introduction...2 Guide for Completing Form W-8IMY...3 Guide for Completing

Babcock & Brown Infrastructure Guide for Completing IRS Forms: W-8IMY & W-8BEN GUIDE FOR COMPLETING IRS FORMS: W-8IMY & W-8BEN Contents Introduction...2 Guide for Completing Form W-8IMY...3 Guide for Completing

Withholding of Tax on Nonresident Aliens and Foreign Entities

Department of the Treasury Internal Revenue Service Publication 515 Cat. No. 15019L Withholding of Tax on Nonresident Aliens and Foreign Entities For use in 2013 Contents What's New... 1 Reminders... 2

Department of the Treasury Internal Revenue Service Publication 515 Cat. No. 15019L Withholding of Tax on Nonresident Aliens and Foreign Entities For use in 2013 Contents What's New... 1 Reminders... 2

Payments Made to Nonresident Aliens

Payments Made to Nonresident Aliens Procedure Manual This Procedures for Payments Made to Nonresident Aliens guide was prepared by Arctic International LLC in connection with Loyola Marymount University

Payments Made to Nonresident Aliens Procedure Manual This Procedures for Payments Made to Nonresident Aliens guide was prepared by Arctic International LLC in connection with Loyola Marymount University

If you do not have all of the above forms, please call Junn De Guzman at (732) 235-9202.

235-9202.") To: Non-Resident Aliens Requesting Special Tax Treatment From: Junn De Guzman, Sr. Accountant Payroll Services Date: January 9, 2014 Re: Requirements for Tax Benefits for Calendar Year 2014 Enclosed please

To: Non-Resident Aliens Requesting Special Tax Treatment From: Junn De Guzman, Sr. Accountant Payroll Services Date: January 9, 2014 Re: Requirements for Tax Benefits for Calendar Year 2014 Enclosed please

2015 Publication 4011

01 Publication 4011 Foreign Student and Scholar Volunteer Resource Guide For Use in Preparing Tax Year 01 Returns»» Volunteer Income Tax Assistance (VITA)»» Tax Counseling for the Elderly (TCE) For the

01 Publication 4011 Foreign Student and Scholar Volunteer Resource Guide For Use in Preparing Tax Year 01 Returns»» Volunteer Income Tax Assistance (VITA)»» Tax Counseling for the Elderly (TCE) For the

THE ADVANTAGES OF A UK INTERNATIONAL HOLDING COMPANY

THE ADVANTAGES OF A UK INTERNATIONAL HOLDING COMPANY Ideal Characteristics for the Location of an International Holding Company Laurence Binge +44 (0)1372 471117 laurence.binge@woolford.co.uk www.woolford.co.uk

THE ADVANTAGES OF A UK INTERNATIONAL HOLDING COMPANY Ideal Characteristics for the Location of an International Holding Company Laurence Binge +44 (0)1372 471117 laurence.binge@woolford.co.uk www.woolford.co.uk

Non-Resident Withholding Tax Rates for Treaty Countries 1

Non-Resident Withholding Tax Rates for Treaty Countries 1 firms Non-Resident Withholding Tax Rates for Treaty Countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15%

Non-Resident Withholding Tax Rates for Treaty Countries 1 firms Non-Resident Withholding Tax Rates for Treaty Countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15%

Davy Select Telephone Trading Account (Execution-Only)

") www.davyselect.ie Davy Select Telephone Trading Account (Execution-Only) Application Form Thank you for choosing Davy Select Please read the accompanying Execution-Only Service Terms (and related documentation)

www.davyselect.ie Davy Select Telephone Trading Account (Execution-Only) Application Form Thank you for choosing Davy Select Please read the accompanying Execution-Only Service Terms (and related documentation)

U.S. Tax Treaties. Contents. Future Developments. Reminders. Publication 901. Get forms and other Information faster and easier by: Internet IRS.

Department of the Treasury Internal Revenue Service Publication 901 (Rev. April 2013) Cat. No. 46849F U.S. Tax Treaties Contents Reminders... 1 Introduction... 2 Application of Treaties... 2 Tax Exemptions

Department of the Treasury Internal Revenue Service Publication 901 (Rev. April 2013) Cat. No. 46849F U.S. Tax Treaties Contents Reminders... 1 Introduction... 2 Application of Treaties... 2 Tax Exemptions

BLUM Attorneys at Law

BLUM Attorneys at Law CORPORATE TAXATION SYSTEM IN SWITZERLAND Outline of Swiss Corporate Tax System Levels of Taxation in Switzerland Resident companies are subject to: federal corporate income tax, and

BLUM Attorneys at Law CORPORATE TAXATION SYSTEM IN SWITZERLAND Outline of Swiss Corporate Tax System Levels of Taxation in Switzerland Resident companies are subject to: federal corporate income tax, and

DoD Financial Management Regulation Volume 7B, Chapter 53 + June 2004

SUMMARY OF MAJOR CHANGES TO DOD 7000.14-R, VOLUME 7B, CHAPTER 53 "SURVIVOR BENEFIT PLAN (SBP) - TAXABILITY OF ANNUITIES" Substantive revisions are denoted by a + preceding the section, paragraph, table

SUMMARY OF MAJOR CHANGES TO DOD 7000.14-R, VOLUME 7B, CHAPTER 53 "SURVIVOR BENEFIT PLAN (SBP) - TAXABILITY OF ANNUITIES" Substantive revisions are denoted by a + preceding the section, paragraph, table

Perrigo Company Acquisition of Elan Corporation plc Exchange of Perrigo common shares Frequently Asked Questions & Answers

Perrigo Company Acquisition of Elan Corporation plc Exchange of Perrigo common shares Frequently Asked Questions & Answers On November 18, 2013, Perrigo Company ( Perrigo ) announced that its shareholders

Perrigo Company Acquisition of Elan Corporation plc Exchange of Perrigo common shares Frequently Asked Questions & Answers On November 18, 2013, Perrigo Company ( Perrigo ) announced that its shareholders

Instructions for Form 8233 (Rev. June 2011)

") Instructions for Form 8233 (Rev. June 2011) Department of the Treasury Internal Revenue Service (Use with the March 2009 revision of Form 8233.) Exemption From Withholding on Compensation for Independent

Instructions for Form 8233 (Rev. June 2011) Department of the Treasury Internal Revenue Service (Use with the March 2009 revision of Form 8233.) Exemption From Withholding on Compensation for Independent

Davy Select Trading Account (Execution-Only)

") www.davyselect.ie Davy Select Trading Account (Execution-Only) Application Form Thank you for choosing Davy Select The Davy Select Trading Account (Execution- Only) is designed for those who are comfortable

www.davyselect.ie Davy Select Trading Account (Execution-Only) Application Form Thank you for choosing Davy Select The Davy Select Trading Account (Execution- Only) is designed for those who are comfortable

1. All supplier invoices must be emailed as individual attachments to LyndenAPinvoices@Lynden.com. PDF format is preferred.

ATTN: Accounts Receivable/Billing Department/Credit Department As a valued supplier of the Lynden family of companies, please follow the guidelines below to ensure your invoices are processed completely

ATTN: Accounts Receivable/Billing Department/Credit Department As a valued supplier of the Lynden family of companies, please follow the guidelines below to ensure your invoices are processed completely

Instructions for the Requester of Forms W 8BEN, W 8BEN E, W 8ECI, W 8EXP, and W 8IMY (Rev. July 2014)

") Instructions for the Requester of Forms W 8BEN, W 8BEN E, W 8ECI, W 8EXP, and W 8IMY (Rev. July 2014) Section references are to the Internal Revenue Code unless otherwise noted. Future developments. For

Instructions for the Requester of Forms W 8BEN, W 8BEN E, W 8ECI, W 8EXP, and W 8IMY (Rev. July 2014) Section references are to the Internal Revenue Code unless otherwise noted. Future developments. For

International aspects of taxation in the Netherlands

International aspects of taxation in the Netherlands Individuals resident in the Netherlands are subject to income tax on their worldwide income. Companies established in the Netherlands are subject to

International aspects of taxation in the Netherlands Individuals resident in the Netherlands are subject to income tax on their worldwide income. Companies established in the Netherlands are subject to

UPDATED INFORMATION ON USE OF FORM W-8IMY (REVISION DATE FEBRUARY 2006) BEFORE JANUARY 1, 2015

BEFORE JANUARY 1, 2015") UPDATED INFORMATION ON USE OF FORM W-8IMY (REVISION DATE FEBRUARY 2006) BEFORE JANUARY 1, 2015 This Form W-8IMY (revision date April 2014) reflects the changes made in the Foreign Account Tax Compliance

UPDATED INFORMATION ON USE OF FORM W-8IMY (REVISION DATE FEBRUARY 2006) BEFORE JANUARY 1, 2015 This Form W-8IMY (revision date April 2014) reflects the changes made in the Foreign Account Tax Compliance

Application Procedures for Qualified Intermediary Status Under Section 1441; Final Qualified Intermediary Withholding Agreement

Part III Administrative, Procedural, and Miscellaneous Application Procedures for Qualified Intermediary Status Under Section 1441; Final Qualified Intermediary Withholding Agreement Rev. Proc 2000-12

Part III Administrative, Procedural, and Miscellaneous Application Procedures for Qualified Intermediary Status Under Section 1441; Final Qualified Intermediary Withholding Agreement Rev. Proc 2000-12

DISCLAIMER. The information contained in this presentation is current as of the date it was presented. It should not be considered official guidance.

DISCLAIMER The information contained in this presentation is current as of the date it was presented. It should not be considered official guidance. 1 INTRODUCTION This webinar is intended to provide basic

DISCLAIMER The information contained in this presentation is current as of the date it was presented. It should not be considered official guidance. 1 INTRODUCTION This webinar is intended to provide basic

Netherlands Country Profile

Netherlands Country Profile EU Tax Centre March 2012 Key factors for efficient cross-border tax planning involving Netherlands EU Member State Yes Double Tax Treaties With: Albania Czech Rep. Jordan Nigeria

Netherlands Country Profile EU Tax Centre March 2012 Key factors for efficient cross-border tax planning involving Netherlands EU Member State Yes Double Tax Treaties With: Albania Czech Rep. Jordan Nigeria

Tax Treaty Benefits for Workers, Trainees, Students, and Researchers

Tax Treaty Benefits for Workers, Trainees, Students, and Researchers By Paula N. Singer, Esq. 1 ONESOURCE NONRESIDENT ALIEN TAXATION As organizations, both large and small, become increasingly more global,

Tax Treaty Benefits for Workers, Trainees, Students, and Researchers By Paula N. Singer, Esq. 1 ONESOURCE NONRESIDENT ALIEN TAXATION As organizations, both large and small, become increasingly more global,

IRS FORM 1099 REPORTING REQUIREMENTS

IRS FORM 1099 REPORTING REQUIREMENTS The Internal Revenue Service (IRS) requires businesses (including not-for-profit organizations) to issue a Form 1099 to any individual or unincorporated business paid

IRS FORM 1099 REPORTING REQUIREMENTS The Internal Revenue Service (IRS) requires businesses (including not-for-profit organizations) to issue a Form 1099 to any individual or unincorporated business paid

ENTERING THE EU BORDERS & VISAS THE SCHENGEN AREA OF FREE MOVEMENT. EU Schengen States. Non-Schengen EU States. Non-EU Schengen States.

ENTERING THE EU BORDERS & VISAS THE SCHENGEN AREA OF FREE MOVEMENT An area without internal borders where EU citizens and non-eu nationals may move freely EU Schengen States Non-Schengen EU States IS Azores

ENTERING THE EU BORDERS & VISAS THE SCHENGEN AREA OF FREE MOVEMENT An area without internal borders where EU citizens and non-eu nationals may move freely EU Schengen States Non-Schengen EU States IS Azores

Greece Country Profile

Greece Country Profile EU Tax Centre March 2013 Key factors for efficient cross-border tax planning involving Greece EU Member State Double Tax Treaties With: Albania Estonia Lithuania Serbia Armenia Finland

Greece Country Profile EU Tax Centre March 2013 Key factors for efficient cross-border tax planning involving Greece EU Member State Double Tax Treaties With: Albania Estonia Lithuania Serbia Armenia Finland

Malta Companies in International Tax Structuring February 2015

INFORMATION SHEET No. 126 Malta in International Tax Structuring February 2015 Introduction Malta is a reputable EU business and financial centre with an attractive tax regime and sound legislative framework.

INFORMATION SHEET No. 126 Malta in International Tax Structuring February 2015 Introduction Malta is a reputable EU business and financial centre with an attractive tax regime and sound legislative framework.

Guide to completing W-8BEN-E entity US tax forms

Guide to completing W-8BEN-E entity US tax forms Applicable to Companies, Trusts, Self-Managed Superannuation Funds and Deceased Estates Macquarie Wrap 1 macquarie.com Contents 1 General information 01

Guide to completing W-8BEN-E entity US tax forms Applicable to Companies, Trusts, Self-Managed Superannuation Funds and Deceased Estates Macquarie Wrap 1 macquarie.com Contents 1 General information 01

Missouri Lottery Winner Claim Form Official Missouri Lottery Claim Form

[ STAPLE TICKET HERE ] Missouri Lottery Winner Claim Form Official Missouri Lottery Claim Form A B C PLEASE PRINT your name, address and phone number on the back of your ticket - YOU MUST SIGN YOUR TICKET.

[ STAPLE TICKET HERE ] Missouri Lottery Winner Claim Form Official Missouri Lottery Claim Form A B C PLEASE PRINT your name, address and phone number on the back of your ticket - YOU MUST SIGN YOUR TICKET.

International Call Services

International Call Services Affordable rates for business calls. Wherever you are in the world. We ve got plenty to say when it comes to staying in touch when you re overseas. We have agreements with 443

International Call Services Affordable rates for business calls. Wherever you are in the world. We ve got plenty to say when it comes to staying in touch when you re overseas. We have agreements with 443

Customer Tax Guide - U.S.A. Debt Securities Equities Withholding Tax Capital Gains Tax Stamp Duty

Customer Tax Guide - U.S.A. Debt Securities Equities Withholding Tax Capital Gains Tax Stamp Duty March 2013 Customer Tax Guide - U.S.A. March 2013 edition Document No. US6065 This document is the property

Customer Tax Guide - U.S.A. Debt Securities Equities Withholding Tax Capital Gains Tax Stamp Duty March 2013 Customer Tax Guide - U.S.A. March 2013 edition Document No. US6065 This document is the property

World Consumer Income and Expenditure Patterns

World Consumer Income and Expenditure Patterns 2014 14th edi tion Euromonitor International Ltd. 60-61 Britton Street, EC1M 5UX TableTypeID: 30010; ITtableID: 22914 Income Algeria Income Algeria Income

World Consumer Income and Expenditure Patterns 2014 14th edi tion Euromonitor International Ltd. 60-61 Britton Street, EC1M 5UX TableTypeID: 30010; ITtableID: 22914 Income Algeria Income Algeria Income

Supported Payment Methods

Supported Payment Methods Global In the global payments market, credit cards are the most popular payment method. However, BlueSnap expands the payment selection by including not only the major credit

Supported Payment Methods Global In the global payments market, credit cards are the most popular payment method. However, BlueSnap expands the payment selection by including not only the major credit

CONTRACTOR APPLICATION HOUSING REHABILITATION PROGRAM

CITY OF GALVESTON GRANTS & HOUSING DEPARTMENT P.O. Box 779 Galveston, Texas 77553 Office (409) 797 3820 Fax (409) 797 3888 CONTRACTOR APPLICATION HOUSING REHABILITATION PROGRAM CONTRACTOR APPLICATION HOUSING

CITY OF GALVESTON GRANTS & HOUSING DEPARTMENT P.O. Box 779 Galveston, Texas 77553 Office (409) 797 3820 Fax (409) 797 3888 CONTRACTOR APPLICATION HOUSING REHABILITATION PROGRAM CONTRACTOR APPLICATION HOUSING

Supported Payment Methods

Sell Globally in a Snap Supported Payment Methods Global In the global payments market, credit cards are the most popular payment method. However, BlueSnap expands the payment selection by including not

Sell Globally in a Snap Supported Payment Methods Global In the global payments market, credit cards are the most popular payment method. However, BlueSnap expands the payment selection by including not

Consolidated International Banking Statistics in Japan

Total (Transfer Consolidated cross-border claims in all currencies and local claims in non-local currencies Up to and including one year Maturities Over one year up to two years Over two years Public Sector

Total (Transfer Consolidated cross-border claims in all currencies and local claims in non-local currencies Up to and including one year Maturities Over one year up to two years Over two years Public Sector

FOREIGNERS DOING BUSINESS IN THE UNITED STATES U.S. Taxation Overview

FOREIGNERS DOING BUSINESS IN THE UNITED STATES U.S. Taxation Overview The U.S. economic activities of foreign individuals and entities are classified as inbound transactions while the foreign economic

FOREIGNERS DOING BUSINESS IN THE UNITED STATES U.S. Taxation Overview The U.S. economic activities of foreign individuals and entities are classified as inbound transactions while the foreign economic

Global Dialing Comment. Telephone Type. AT&T Direct Number. Access Type. Dial-In Number. Country. Albania Toll-Free 00-800-0010 888-426-6840

Below is a list of Global Access Numbers, in order by country. If a Country has an AT&T Direct Number, the audio conference requires two-stage dialing. First, dial the AT&T Direct Number. Second, dial

Below is a list of Global Access Numbers, in order by country. If a Country has an AT&T Direct Number, the audio conference requires two-stage dialing. First, dial the AT&T Direct Number. Second, dial

US Tax Issues for Foreign Partners: US Withholding Taxes & Tax Treaties

US Tax Issues for Foreign Partners: US Withholding Taxes & Tax Treaties Hope P. Krebs January 2015 2015 Duane Morris LLP. All Rights Reserved. Duane Morris is a registered service mark of Duane Morris

US Tax Issues for Foreign Partners: US Withholding Taxes & Tax Treaties Hope P. Krebs January 2015 2015 Duane Morris LLP. All Rights Reserved. Duane Morris is a registered service mark of Duane Morris

Starting a Business in Israel

Starting a Business in Israel Inspiration Invention Innovation Content: Page 1. Business Entities....... 2 a. Company...... 2 b. Foreign Company (e.g. a branch)...... 2 c. Partnership...... 3 d. Self Employed......

Starting a Business in Israel Inspiration Invention Innovation Content: Page 1. Business Entities....... 2 a. Company...... 2 b. Foreign Company (e.g. a branch)...... 2 c. Partnership...... 3 d. Self Employed......

Information Reporting Forms 1099. Sponsored by Office of Financial Management and Internal Revenue Service December 12, 2012

Information Reporting Forms 1099 Sponsored by Office of Financial Management and Internal Revenue Service December 12, 2012 Information Reporting Form Code Section 1098 6050H 1098-E 6050S 1098-T 6050S

Information Reporting Forms 1099 Sponsored by Office of Financial Management and Internal Revenue Service December 12, 2012 Information Reporting Form Code Section 1098 6050H 1098-E 6050S 1098-T 6050S

SunGard Best Practice Guide

SunGard Best Practice Guide What Number Should I Use? www.intercalleurope.com Information Hotline 0871 7000 170 +44 (0)1452 546742 conferencing@intercalleurope.com Reservations 0870 043 4167 +44 (0)1452

SunGard Best Practice Guide What Number Should I Use? www.intercalleurope.com Information Hotline 0871 7000 170 +44 (0)1452 546742 conferencing@intercalleurope.com Reservations 0870 043 4167 +44 (0)1452

41 T Korea, Rep. 52.3. 42 T Netherlands 51.4. 43 T Japan 51.1. 44 E Bulgaria 51.1. 45 T Argentina 50.8. 46 T Czech Republic 50.4. 47 T Greece 50.

Overall Results Climate Change Performance Index 2012 Table 1 Rank Country Score** Partial Score Tendency Trend Level Policy 1* Rank Country Score** Partial Score Tendency Trend Level Policy 21 - Egypt***

Overall Results Climate Change Performance Index 2012 Table 1 Rank Country Score** Partial Score Tendency Trend Level Policy 1* Rank Country Score** Partial Score Tendency Trend Level Policy 21 - Egypt***

TD F 90-22.1 (Rev. January 2012) Department of the Treasury