Pensions System In Mauritius & The Private Pension Schemes Act 2012

|

|

|

- Cuthbert Webb

- 8 years ago

- Views:

Transcription

1 1

2 Pensions System In Mauritius & The Private Pension Schemes Act 2012 Presented by: Trisha Dulloo Chief Examiner Surveillance Insurance & Pensions 4 November 2013

3 Retirement System In Mauritius 3

4 Multi-Pillar System 4

5 Legislative Evolution of Pensions 1. Pension Act Employees Superannuation Fund Act 1954 (repealed) 3. Sugar Industry Pension Fund Act National Pensions Act Local Authorities Act National Savings Fund Act Insurance Act Private Pension Scheme Act

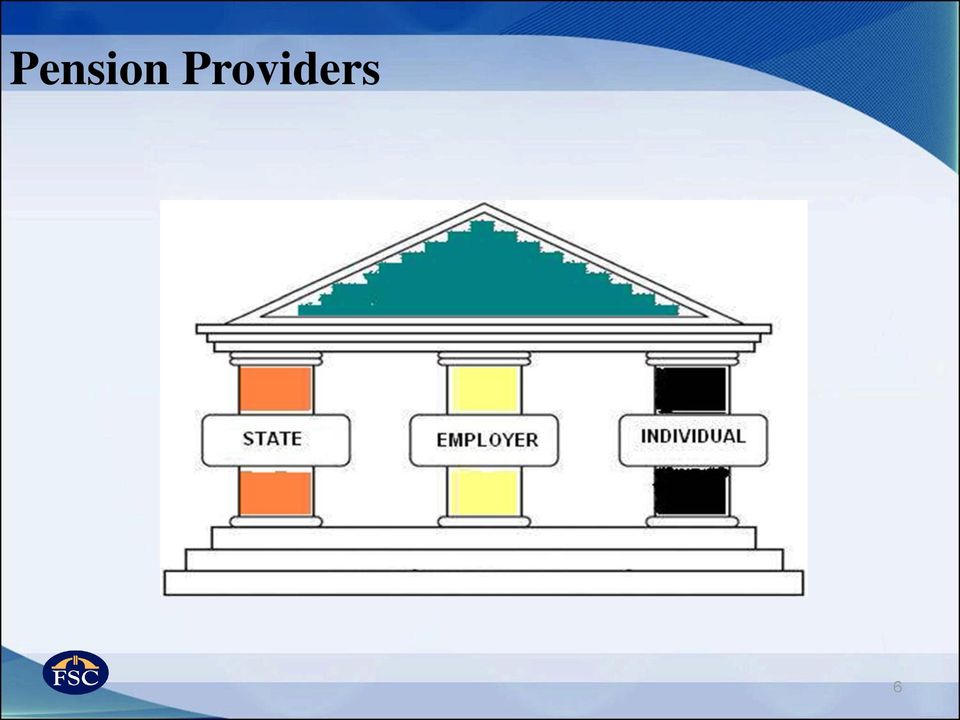

6 Pension Providers 6

7 The Private Pensions Industry In Mauritius 7

8 Fragmented framework The main law for pension schemes established by private companies was the Employees Superannuation Fund Act (1954)- [now repealed] Private occupational pension schemes contracting out to Insurance companies fell under the Insurance Act 2005 Unfortunately, these two Acts do not cover: fully the interests of members and beneficiaries ; the fair, safe and efficient functioning of the private pensions industry 8

9 Fragmented framework Set up of private pension schemes before 1 st November 2012 Vehicle Act Governing Body Insurance Company Insurance Act 2005 Insurance Company Trust Trust Act 2001 Board of Trustees Superannuation Fund Employees Superannuation Fund Act 1954 Management Committee Private occupational pension schemes managed by insurance companies (on contractual basis) fell under the purview of the Insurance Act Rules of occupational pension scheme were required to be approved by Tax Commissioner [Regulation 5 of Income Tax Regulation now revoked] in order to qualify for tax reliefs. Superannuation Funds were registered with the Registrar of Associations. 9

10 Regulatory gaps There were no explicit requirements for: Maintaining a proper funding level to secure scheme benefits Ensuring the safe custody of pension assets Hiring qualified actuaries, auditors & custodians Imposing on actuaries & auditors the responsibility to inform the Regulator of any material breaches of regulations Submitting regular reports to the Regulator Pension schemes to undertake periodical actuarial reviews Investment rules & asset diversification Limiting self-investments in sponsoring employers 10

11 The Private Pension Schemes Act 2012 ( PPSA ) 11

12 PPSA A new dimension Following industry consultations at the drafting stage of the Act, the scope of the legislation has widened to include: A regulatory & supervisory framework for both private occupational & non-occupational pension schemes; Pension schemes to be either licensed or authorised; Self-administration of the pension scheme by the governing body (a common practice in the industry i.r.o. large schemes); Assets of the pension schemes to be managed by a wider range of financial business providers: insurers, investments advisers, asset managers or CIS managers (regulated & supervised under other Acts administered by the FSC); and Safe custody of pension assets by licensed custodians. 12

13 Objectives of PPSA 1. Maintain a fair, safe, stable, efficient private pension industry 2. Maintain the good repute of Mauritius as a sound financial centre through the effective regulation & supervision of the private pension industry 3. Promote confidence among stakeholders 4. Protection & fair treatment to members & beneficiaries 5. Consumer education 6. Combating financial crime 13

14 Main Features 1. Overall Compliance with International Standards (IOPS/OECD) 6. Enforcement with prudential requirements 2. Good governance & business friendly approach 5. Disclosure requirements among stakeholders Objectives of PPSA 3. Licensing requirements for private pension schemes 4. Risk Based Supervision

15 FSC Rules under PPSA Licensing and Authorisation (Operational since 1 Nov 2012) Governance(Operational since 1 Nov 2012) Disclosure (Operational since 1 Jan 2013) Investment (Upcoming) Technical provisions & underfunding (Upcoming) Appointment of the auditor & actuary (Drafting process) Schedules & Returns (Drafting process) Winding up Transfer, compromise or amalgamation Pension scheme administrator Provision in respect of DB & DC schemes General provisions of private pension schemes 15

16 International Principles & Guidelines The PPSA (including operational FSC Rules) adheres to: IOPS Principles of Private Pension Supervision OECD/ IOPS Guidelines on the Licensing of Pension Entities OECD Core Principles of Occupational Pension Regulation OECD Guidelines for pension fund governance 16

17 Pension schemes under PPSA 1. Local (licensed) Occupational/ Nonoccupational Established & regulated in Mauritius 2. External (licensed) Occupational/ Nonoccupational GBC1; Established & regulated in Mauritius 3. Foreign (authorised) Occupational/ Nonoccupational Established & regulated in a foreign jurisdiction 17

Occupational/ Nonoccupational GBC1; Established &")

Investment Managers or Longterm insurer (licence required) Custodian (licence required) 18")

18 Pension schemes stakeholders REGULATOR (FSC) PPS (beneficiaries) Actuary Auditor GOVERNING BODY Pension Scheme Administrator or Long-term Insurer (licence required) Investment Managers or Longterm insurer (licence required) Custodian (licence required) 18

")

19 Pension schemes NOT under PPSA Pension Schemes set up under: National Pensions Act/ National Savings Fund Act Civil Service Family Protection Scheme Act Statutory Bodies Pension Fund Acts Sugar Industry Pension Fund Act Local Authorities (Pensions) Act Individual Pension Plans under the Insurance Act Registrar of Association Act 19

Act Individual Pension Plans under the Insurance Act Registrar of")

20 Benefits of PPSA to Jurisdiction The PPSA provides a comprehensive & modern regulatory & supervisory framework for the protection of members & beneficiaries of private pension schemes & soundness of the private pensions industry. It clearly designates the FSC as the Regulator of this industry. All providers of private pensions with a physical presence in Mauritius including overseas providers with an agent-based presence are covered by the Act. 20

21 Benefits of PPSA to Jurisdiction The PPSA has addressed the regulatory gaps that prevailed prior to 1 st November 2012:- fund governance; appropriate funding levels; asset segregation and safe custody; asset valuation and diversification; accounting, auditing and actuarial standards; whistle-blowing provisions; financial reporting; disclosure and transparency; off-site surveillance; on-site inspections; powers of intervention and remedial action. 21

22 Benefits of PPSA to Jurisdiction In supervising private pension schemes, FSC collaborates with governing bodies, auditors, actuaries and custodians to ensure that the schemes are properly administered and their assets properly managed. Hence, protecting the interests of members and beneficiaries. Effective regulation & supervision of the private pensions sector will promote confidence in the industry and encourage savings for retirement. 22

23 Conclusion Overall objective of the new regulatory & supervisory framework for the private pensions industry is to ensure the security of members benefits without overly burdening or discouraging the setting up of private pension schemes in Mauritius. The FSC has a vital role for achieving this. 23

24 Any Questions 24

25 THANK YOU FOR YOUR KIND ATTENTION 25

26 54 Ebene Cybercity Mauritius Tel: (230) Fax: (230)

Implications of the Private pension scheme legislation

Financial Services Commission Mauritius The Anglo-Mauritius Assurance Society Ltd and Pension Consultants & Administrators Ltd workshop Implications of the Private pension scheme legislation Clairette

Financial Services Commission Mauritius The Anglo-Mauritius Assurance Society Ltd and Pension Consultants & Administrators Ltd workshop Implications of the Private pension scheme legislation Clairette

August 10, 2015. Many of these principles will be familiar to U.S. readers, but these are global principles that would be new to many countries.

August 10, 2015 Author: David W. Powell If you have questions, please contact your regular Groom attorney or one of the attorneys listed below: Louis T. Mazawey lmazawey@groom.com (202) 861-6608 David

August 10, 2015 Author: David W. Powell If you have questions, please contact your regular Groom attorney or one of the attorneys listed below: Louis T. Mazawey lmazawey@groom.com (202) 861-6608 David

Fact Sheet Global Business

FS/GB01-14 March 2013 Fact Sheet Global Business Global Business in Mauritius Global Business (GB) is a regime available in Mauritius for resident corporations proposing to conduct business outside Mauritius.

FS/GB01-14 March 2013 Fact Sheet Global Business Global Business in Mauritius Global Business (GB) is a regime available in Mauritius for resident corporations proposing to conduct business outside Mauritius.

Regulation of Private Pension Funds

Flagship Course in Pension Reform March 6 17, 2000 Washington, D.C. Regulation of Private Pension Funds Dimitri Vittas March 13, 2000 The Regulation of Private Pension Funds Dimitri Vittas 2 Outline of

Flagship Course in Pension Reform March 6 17, 2000 Washington, D.C. Regulation of Private Pension Funds Dimitri Vittas March 13, 2000 The Regulation of Private Pension Funds Dimitri Vittas 2 Outline of

COUNTRY PROFILE - MAURITIUS

COUNTRY PROFILE - MAURITIUS DEMOGRAPHICS AND MACROECONOMICS 2011 2012 Gross Domestic Product (GDP) at market prices (MUR Million) 322,773 344,550 GDP per capita at Market Prices (MUR) 250,924 266,816 Population

COUNTRY PROFILE - MAURITIUS DEMOGRAPHICS AND MACROECONOMICS 2011 2012 Gross Domestic Product (GDP) at market prices (MUR Million) 322,773 344,550 GDP per capita at Market Prices (MUR) 250,924 266,816 Population

OECD GUIDELINES FOR PENSION FUND GOVERNANCE

OECD GUIDELINES FOR PENSION FUND GOVERNANCE These Guidelines were approved by the Working Party on Private Pensions on 5 June 2009. OECD GUIDELINES FOR PENSION FUND GOVERNANCE 1 I. GOVERNANCE STRUCTURE

OECD GUIDELINES FOR PENSION FUND GOVERNANCE These Guidelines were approved by the Working Party on Private Pensions on 5 June 2009. OECD GUIDELINES FOR PENSION FUND GOVERNANCE 1 I. GOVERNANCE STRUCTURE

THE LICENSING OF PENSION ENTITIES IN PRIVATE PENSION SYSTEMS

THE LICENSING OF PENSION ENTITIES IN PRIVATE PENSION SYSTEMS July 2007 This comparative report provides background to the OECD-IOPS Guidelines on the Licensing of Pension Entities. For further on this

THE LICENSING OF PENSION ENTITIES IN PRIVATE PENSION SYSTEMS July 2007 This comparative report provides background to the OECD-IOPS Guidelines on the Licensing of Pension Entities. For further on this

SUPERANNUATION SCHEMES REPORT

B30 SUPERANNUATION SCHEMES REPORT 2014 FOR THE YEAR ENDED 30 JUNE Financial Markets Authority www.fma.govt.nz AUCKLAND OFFICE Level 5, Ernst & Young Building 2 Takutai Square, Britomart PO Box 106 672

B30 SUPERANNUATION SCHEMES REPORT 2014 FOR THE YEAR ENDED 30 JUNE Financial Markets Authority www.fma.govt.nz AUCKLAND OFFICE Level 5, Ernst & Young Building 2 Takutai Square, Britomart PO Box 106 672

Introducing the Qatar Financial Centre Regulatory Authority

Introducing the Qatar Financial Centre Regulatory Authority Contents Chapter 1 2 The Qatar Financial Centre Diagram 1: The QFC Structure QFC Permitted Activities Non-Regulated Activities Regulated Activities

Introducing the Qatar Financial Centre Regulatory Authority Contents Chapter 1 2 The Qatar Financial Centre Diagram 1: The QFC Structure QFC Permitted Activities Non-Regulated Activities Regulated Activities

CHAPTER 16 INVESTMENT ENTITIES

CHAPTER 16 INVESTMENT ENTITIES Introduction 16.1 This Chapter sets out the requirements for the listing of the securities of investment entities, which include investment companies, unit trusts, closed-end

CHAPTER 16 INVESTMENT ENTITIES Introduction 16.1 This Chapter sets out the requirements for the listing of the securities of investment entities, which include investment companies, unit trusts, closed-end

GUIDELINES FOR PENSION FUND GOVERNANCE. (OECD Secretariat) JULY 2002

JULY 2002") GUIDELINES FOR PENSION FUND GOVERNANCE (OECD Secretariat) JULY 2002 OECD GUIDELINES FOR PENSION FUND GOVERNANCE 1. Private pension plans function on the basis of agency relationships between plan members

GUIDELINES FOR PENSION FUND GOVERNANCE (OECD Secretariat) JULY 2002 OECD GUIDELINES FOR PENSION FUND GOVERNANCE 1. Private pension plans function on the basis of agency relationships between plan members

Internal controls Guidance for trustees

Regulatory code of practice no. 9 Internal controls Guidance for trustees Contents Paragraph Page 1 Introduction 3 5 The status of codes of practice 3 6 Other regulatory requirements 3 7 Terminology 4

Regulatory code of practice no. 9 Internal controls Guidance for trustees Contents Paragraph Page 1 Introduction 3 5 The status of codes of practice 3 6 Other regulatory requirements 3 7 Terminology 4

MANAGED CORPORATE SERVICE PROVIDERS

PRACTICE NOTES ON MANAGED CORPORATE SERVICE PROVIDERS (PN-010105) (Issued under section 7(1)(a) of the Financial Services Development Act 2001) Issued on 06 January 2005 CONTENTS Pages 1 Introduction 1-2

PRACTICE NOTES ON MANAGED CORPORATE SERVICE PROVIDERS (PN-010105) (Issued under section 7(1)(a) of the Financial Services Development Act 2001) Issued on 06 January 2005 CONTENTS Pages 1 Introduction 1-2

CONSULTATIVE PAPER ON COMPETENCY STANDARDS FOR INVESTMENT ADVISERS. March 2014

CONSULTATIVE PAPER ON COMPETENCY STANDARDS F INVESTMENT ADVISERS March 2014 Competency Standards Investment Advisers 1 1. Consultation Point 1: Technical Competencies and Minimum Educational Qualifications

CONSULTATIVE PAPER ON COMPETENCY STANDARDS F INVESTMENT ADVISERS March 2014 Competency Standards Investment Advisers 1 1. Consultation Point 1: Technical Competencies and Minimum Educational Qualifications

INFORMATION ON CUSTOMER COMPANY

INFORMATION ON CUSTOMER COMPANY 1 st Floor, The Exchange, 18 Cybercity, Ebene, Mauritius Telephone: - (230) 454 3200 Facsimile: + (230) 454 3202 Date Customer type GBL1 GBL2 Trust Kindly read attached

INFORMATION ON CUSTOMER COMPANY 1 st Floor, The Exchange, 18 Cybercity, Ebene, Mauritius Telephone: - (230) 454 3200 Facsimile: + (230) 454 3202 Date Customer type GBL1 GBL2 Trust Kindly read attached

NOTICE ON OUTSOURCING

CONSULTATION PAPER P018-2014 SEPTEMBER 2014 NOTICE ON OUTSOURCING PREFACE 1 MAS first issued the Guidelines on Outsourcing in 2004 1 ( Guidelines ) to promote sound risk management practices for the outsourcing

CONSULTATION PAPER P018-2014 SEPTEMBER 2014 NOTICE ON OUTSOURCING PREFACE 1 MAS first issued the Guidelines on Outsourcing in 2004 1 ( Guidelines ) to promote sound risk management practices for the outsourcing

OECD GUIDELINES ON PENSION FUND ASSET MANAGEMENT. Recommendation of the Council

DIRECTORATE FOR FINANCIAL AND ENTERPRISE AFFAIRS OECD GUIDELINES ON PENSION FUND ASSET MANAGEMENT Recommendation of the Council These guidelines, prepared by the OECD Insurance and Private Pensions Committee

DIRECTORATE FOR FINANCIAL AND ENTERPRISE AFFAIRS OECD GUIDELINES ON PENSION FUND ASSET MANAGEMENT Recommendation of the Council These guidelines, prepared by the OECD Insurance and Private Pensions Committee

GUIDE TO INVESTMENT FUNDS IN THE CAYMAN ISLANDS

GUIDE TO INVESTMENT FUNDS IN THE CAYMAN ISLANDS CONTENTS PREFACE 1 1. Cayman Islands - Jurisdiction of Choice 2 2. Investment Funds 3 3. Investment Fund Structures 4 4. Investment Fund Vehicles 5 5. Director

GUIDE TO INVESTMENT FUNDS IN THE CAYMAN ISLANDS CONTENTS PREFACE 1 1. Cayman Islands - Jurisdiction of Choice 2 2. Investment Funds 3 3. Investment Fund Structures 4 4. Investment Fund Vehicles 5 5. Director

SIPP operator guidance

Finalised guidance A guide for Self-Invested Personal Pensions (SIPP) operators 8 October 2013 SIPP operator guidance This guidance relates to the following rule(s) in the FCA Handbook Conduct of Business

Finalised guidance A guide for Self-Invested Personal Pensions (SIPP) operators 8 October 2013 SIPP operator guidance This guidance relates to the following rule(s) in the FCA Handbook Conduct of Business

Life Insurance Regulations Everything you need to know*

Life Insurance Regulations Everything you need to know* 13.02.2013 *not really, but hopefully a good start! Agenda Life insurance Life reinsurance PRSAs Other 2 February 13, 2013 Regulations Acts Primary

Life Insurance Regulations Everything you need to know* 13.02.2013 *not really, but hopefully a good start! Agenda Life insurance Life reinsurance PRSAs Other 2 February 13, 2013 Regulations Acts Primary

Annual Statistical Bulletin

Annual Statistical Bulletin 2011 i Disclaimer While all care has been taken in the preparation of this Statistical Bulletin, the Financial Services Commission does not, in any way whatsoever, warrant expressly

Annual Statistical Bulletin 2011 i Disclaimer While all care has been taken in the preparation of this Statistical Bulletin, the Financial Services Commission does not, in any way whatsoever, warrant expressly

Australian superannuation funds should be exempt from FATCA withholding obligations on this basis.

7 May 2012 CC:PA:LPD:PR (REG-121647-10) Room 5205 Internal Revenue Service PO Box 7604 Ben Franklin Station Washington D.C. 20044 United States of America Reg-121647-10: Regulations Relating to Information

7 May 2012 CC:PA:LPD:PR (REG-121647-10) Room 5205 Internal Revenue Service PO Box 7604 Ben Franklin Station Washington D.C. 20044 United States of America Reg-121647-10: Regulations Relating to Information

APRA S FIT AND PROPER REQUIREMENTS

APRA S FIT AND PROPER REQUIREMENTS Consultation Paper Australian Prudential Regulation Authority PREAMBLE APRA was created out of the Government s financial sector reforms that were implemented as a result

APRA S FIT AND PROPER REQUIREMENTS Consultation Paper Australian Prudential Regulation Authority PREAMBLE APRA was created out of the Government s financial sector reforms that were implemented as a result

Guidance Note on Outsourcing/Delegation of Functions

Guidance Note on Outsourcing/Delegation of Functions Supervision Division Financial Supervision Commission 7 May 2002 1 Introduction Guidance Note on Outsourcing/Delegation of Functions This Guidance applies

Guidance Note on Outsourcing/Delegation of Functions Supervision Division Financial Supervision Commission 7 May 2002 1 Introduction Guidance Note on Outsourcing/Delegation of Functions This Guidance applies

Application Processing Monitoring the processing of the application with the regulator, and liaising with the parties involved

Investment Funds The use of foreign companies for investment fund activities is a widely spread practice amongst international investors. Abacus offers a comprehensive solution for investment funds and

Investment Funds The use of foreign companies for investment fund activities is a widely spread practice amongst international investors. Abacus offers a comprehensive solution for investment funds and

Foreign collective investment schemes

REGULATORY GUIDE 178 Foreign collective investment schemes June 2012 About this guide This guide is for operators of foreign collective investment schemes (FCIS) that are authorised in other jurisdictions

REGULATORY GUIDE 178 Foreign collective investment schemes June 2012 About this guide This guide is for operators of foreign collective investment schemes (FCIS) that are authorised in other jurisdictions

A Guide to Understanding Group Risk Insurance

A Guide to Understanding Group Risk Insurance This guide has been produced by Group Risk Development (GRiD) with the support of the Chartered Institute of Procurement and Supply (CIPS). CIPS members can

A Guide to Understanding Group Risk Insurance This guide has been produced by Group Risk Development (GRiD) with the support of the Chartered Institute of Procurement and Supply (CIPS). CIPS members can

(Consolidated version with amendments as at 05 October 2013)

") The text below is an internet version of the Regulations made by the Minister under section 154 of the Securities Act 2005 and is for information purposes only. Whilst reasonable care has been taken to

The text below is an internet version of the Regulations made by the Minister under section 154 of the Securities Act 2005 and is for information purposes only. Whilst reasonable care has been taken to

RETAIL FINANCIAL PRODUCT: LIFE ASSURANCE

18.0.14 The Minimum Competency Requirements for Retail Financial Products as detailed under the Minimum Competency Code 2011 RETAIL FINANCIAL PRODUCT: LIFE ASSURANCE SUBJECT MATTER COMPETENCIES 1. THE

18.0.14 The Minimum Competency Requirements for Retail Financial Products as detailed under the Minimum Competency Code 2011 RETAIL FINANCIAL PRODUCT: LIFE ASSURANCE SUBJECT MATTER COMPETENCIES 1. THE

BANKING UNIT BANKING RULES OUTSOURCING BY CREDIT INSTITUTIONS AUTHORISED UNDER THE BANKING ACT 1994

BANKING UNIT BANKING RULES OUTSOURCING BY CREDIT INSTITUTIONS AUTHORISED UNDER THE BANKING ACT 1994 Ref: BR/14/2009 OUTSOURCING BY CREDIT INSTITUTIONS AUTHORISED UNDER THE BANKING ACT 1994 INTRODUCTION

BANKING UNIT BANKING RULES OUTSOURCING BY CREDIT INSTITUTIONS AUTHORISED UNDER THE BANKING ACT 1994 Ref: BR/14/2009 OUTSOURCING BY CREDIT INSTITUTIONS AUTHORISED UNDER THE BANKING ACT 1994 INTRODUCTION

AMP Capital Investors Limited ABN 59 001 777 591 AFSL 232497. AMP Capital Derivatives Risk Statement

AMP Capital Investors Limited ABN 59 001 777 591 AFSL 232497 AMP Capital Derivatives Risk Statement April 2015 Table of Contents 1. Responsible party... 3 2. Objective of the DRS... 3 3. Definition of

AMP Capital Investors Limited ABN 59 001 777 591 AFSL 232497 AMP Capital Derivatives Risk Statement April 2015 Table of Contents 1. Responsible party... 3 2. Objective of the DRS... 3 3. Definition of

Guidance Note AGN 520.1

Guidance Note AGN 520.1 Fit and Proper Requirements Definition of a responsible person 1. The definitions of responsible persons cover those persons whose conduct is most likely to have significant implications

Guidance Note AGN 520.1 Fit and Proper Requirements Definition of a responsible person 1. The definitions of responsible persons cover those persons whose conduct is most likely to have significant implications

Insurance Guidance Note No. 14 System of Governance - Insurance Transition to Governance Requirements established under the Solvency II Directive

Insurance Guidance Note No. 14 Transition to Governance Requirements established under the Solvency II Directive Date of Paper : 31 December 2013 Version Number : V1.00 Table of Contents General governance

Insurance Guidance Note No. 14 Transition to Governance Requirements established under the Solvency II Directive Date of Paper : 31 December 2013 Version Number : V1.00 Table of Contents General governance

IOPS GUIDELINES FOR SUPERVISORY INTERVENTION, ENFORCEMENT AND SANCTIONS

. IOPS GUIDELINES FOR SUPERVISORY INTERVENTION, ENFORCEMENT AND SANCTIONS November 2009 2 IOPS GUIDELINES FOR SUPERVISORY INTERVENTION, ENFORCEMENT AND SANCTIONS Introduction 1. Due to the crucial role

. IOPS GUIDELINES FOR SUPERVISORY INTERVENTION, ENFORCEMENT AND SANCTIONS November 2009 2 IOPS GUIDELINES FOR SUPERVISORY INTERVENTION, ENFORCEMENT AND SANCTIONS Introduction 1. Due to the crucial role

FINANCIAL SERVICE PROVIDERS (REGISTRATION) REGULATIONS

REGULATIONS") 1 OFFICE OF THE MINISTER OF COMMERCE The Chair CABINET ECONOMIC GROWTH AND INFRASTRUCTURE COMMITTEE FINANCIAL SERVICE PROVIDERS (REGISTRATION) REGULATIONS PROPOSAL 1 This paper seeks Cabinet approval for

1 OFFICE OF THE MINISTER OF COMMERCE The Chair CABINET ECONOMIC GROWTH AND INFRASTRUCTURE COMMITTEE FINANCIAL SERVICE PROVIDERS (REGISTRATION) REGULATIONS PROPOSAL 1 This paper seeks Cabinet approval for

BE IT ENACTED by the Queen s Most Excellent Majesty, by

At a Tynwald held in Douglas, Isle of Man, the 21st day of October in the fifty-seventh year of the reign of our Sovereign Lady ELIZABETH THE SECOND by the Grace of God of the United Kingdom of Great Britain

At a Tynwald held in Douglas, Isle of Man, the 21st day of October in the fifty-seventh year of the reign of our Sovereign Lady ELIZABETH THE SECOND by the Grace of God of the United Kingdom of Great Britain

SUPERVISION PROFILE CENTRAL BANK OF TRINIDAD AND TOBAGO CATEGORIES OF FINANCIAL INSTITUTIONS FOR WHICH IT HAS REGULATORY OVERSIGHT: -

SUPERVISION PROFILE CENTRAL BANK OF TRINIDAD AND TOBAGO 1. 1(a) NAME OF SUPERVISORY AGENCY Central Bank of Trinidad & Tobago (CBTT) CATEGORIES OF FINANCIAL INSTITUTIONS FOR WHICH IT HAS REGULATORY OVERSIGHT:

SUPERVISION PROFILE CENTRAL BANK OF TRINIDAD AND TOBAGO 1. 1(a) NAME OF SUPERVISORY AGENCY Central Bank of Trinidad & Tobago (CBTT) CATEGORIES OF FINANCIAL INSTITUTIONS FOR WHICH IT HAS REGULATORY OVERSIGHT:

THE INSURANCE ACT 2005. (Consolidated version with amendments as at 16 July 2011) ARRANGEMENT OF SECTIONS

ARRANGEMENT OF SECTIONS") The text below has been prepared to reflect the text passed by the National Assembly on 25 March 2005, with subsequent amendments, and is for information purpose only. The authoritative version is the

The text below has been prepared to reflect the text passed by the National Assembly on 25 March 2005, with subsequent amendments, and is for information purpose only. The authoritative version is the

A Guide to the Financial Services Regulations

A Guide to the Financial Services Regulations Contents Chapter 1 2 Introduction to the Financial Services Regulations Legislative Background Chapter 2 3 Overview of FSR Regulated Activities Authorisation

A Guide to the Financial Services Regulations Contents Chapter 1 2 Introduction to the Financial Services Regulations Legislative Background Chapter 2 3 Overview of FSR Regulated Activities Authorisation

Objectives and Principles of Securities Regulation

Objectives and Principles of Securities Regulation International Organization of Securities Commissions June 2010 CONTENTS Page Foreword and Executive Summary 3 A Principles Relating to the Regulator 4

Objectives and Principles of Securities Regulation International Organization of Securities Commissions June 2010 CONTENTS Page Foreword and Executive Summary 3 A Principles Relating to the Regulator 4

Insurance Supervision Policy Statement No. 7: Fit and Proper Requirements for Insurance Companies and Insurance Brokers in Fiji

Insurance Supervision Policy Statement No. 7: Fit and Proper Requirements for Insurance Companies and Insurance Brokers in Fiji NOTICE TO INSURANCE COMPANIES AND INSURANCE BROKERS LICENSED UNDER THE INSURANCE

Insurance Supervision Policy Statement No. 7: Fit and Proper Requirements for Insurance Companies and Insurance Brokers in Fiji NOTICE TO INSURANCE COMPANIES AND INSURANCE BROKERS LICENSED UNDER THE INSURANCE

protected. As well, the States and Territories undertake to ensure that the exempted

IIEADS OF GOVERNMENT AGREEMENT EXEMPTION OF CERTAIN PUBLIC SECTOR SUPERANNUATION SCHEMES FROM TFre, SUPEk,NNUATION INDASTRY (SUPERVISION) ACT 1993 ^ND THF, SUPEkANNUATION (RESOLATION OF COMPIAINTS) ACT

IIEADS OF GOVERNMENT AGREEMENT EXEMPTION OF CERTAIN PUBLIC SECTOR SUPERANNUATION SCHEMES FROM TFre, SUPEk,NNUATION INDASTRY (SUPERVISION) ACT 1993 ^ND THF, SUPEkANNUATION (RESOLATION OF COMPIAINTS) ACT

A comparison of US and UK pension security systems. David O. Harris Consultant Watson Wyatt Worldwide

A comparison of US and UK pension security systems David O. Harris Consultant Watson Wyatt Worldwide W W W. W A T S O N W Y A T T. C O M International Pensions Seminar 7 June 2001 Brighton, United Kingdom

A comparison of US and UK pension security systems David O. Harris Consultant Watson Wyatt Worldwide W W W. W A T S O N W Y A T T. C O M International Pensions Seminar 7 June 2001 Brighton, United Kingdom

OECD/IOPS Global Forum Session 2 African Pensions Roundtable Mauritius. Ahmad Lallmahomed

OECD/IOPS Global Forum Session 2 African Pensions Roundtable Mauritius Ahmad Lallmahomed PENSION SYSTEM IN MAURITIUS Three-tiered pension system Structured as follows: First tier - a universal non-contributory

OECD/IOPS Global Forum Session 2 African Pensions Roundtable Mauritius Ahmad Lallmahomed PENSION SYSTEM IN MAURITIUS Three-tiered pension system Structured as follows: First tier - a universal non-contributory

Guidance note on Outsourcing/Delegation of Functions and inward outsourcing

Financial Services Rule Book Rules 8.13, 8.9 and 8.9A Guidance note on Outsourcing/Delegation of Functions and inward outsourcing Supervision Division Financial Supervision Commission September 2012 Guidance

Financial Services Rule Book Rules 8.13, 8.9 and 8.9A Guidance note on Outsourcing/Delegation of Functions and inward outsourcing Supervision Division Financial Supervision Commission September 2012 Guidance

March 2014. Guide to the regulation of workplace defined contribution pensions

March 2014 Guide to the regulation of workplace defined contribution pensions The Financial Conduct Authority (FCA) and The Pensions Regulator have jointly developed this guide to provide an overview of

March 2014 Guide to the regulation of workplace defined contribution pensions The Financial Conduct Authority (FCA) and The Pensions Regulator have jointly developed this guide to provide an overview of

BERMUDA INVESTMENT FUNDS ACT 2006 2006 : 37

QUO FA T A F U E R N T BERMUDA INVESTMENT FUNDS ACT 2006 2006 : 37 TABLE OF CONTENTS 1 2 2A 3 4 5 6 6A 6B 7 8 8A 9 9A 10 Short title and commencement PART I PRELIMINARY Interpretation Interpretation Meaning

QUO FA T A F U E R N T BERMUDA INVESTMENT FUNDS ACT 2006 2006 : 37 TABLE OF CONTENTS 1 2 2A 3 4 5 6 6A 6B 7 8 8A 9 9A 10 Short title and commencement PART I PRELIMINARY Interpretation Interpretation Meaning

A GUIDE TO THE OCCUPATIONAL RETIREMENT SCHEMES ORDINANCE

A GUIDE TO THE OCCUPATIONAL RETIREMENT SCHEMES ORDINANCE Issued by THE REGISTRAR OF OCCUPATIONAL RETIREMENT SCHEMES Level 16, International Commerce Centre, 1 Austin Road West, Kowloon, Hong Kong. ORS/C/5

A GUIDE TO THE OCCUPATIONAL RETIREMENT SCHEMES ORDINANCE Issued by THE REGISTRAR OF OCCUPATIONAL RETIREMENT SCHEMES Level 16, International Commerce Centre, 1 Austin Road West, Kowloon, Hong Kong. ORS/C/5

Best practice guidelines for depositary banks in relation to the safekeeping of assets from UCITS funds held through the traditional custody network

Best practice guidelines for depositary banks in relation to the safekeeping of assets from UCITS funds held through the traditional custody network The purpose of the following is to provide general principles

Best practice guidelines for depositary banks in relation to the safekeeping of assets from UCITS funds held through the traditional custody network The purpose of the following is to provide general principles

GUIDELINES ON COMPLIANCE FUNCTION FOR FUND MANAGEMENT COMPANIES

GUIDELINES ON COMPLIANCE FUNCTION FOR FUND MANAGEMENT COMPANIES Issued: 15 March 2005 Revised: 25 April 2014 1 P a g e List of Revision Revision Effective Date 1 st Revision 23 May 2011 2 nd Revision 16

GUIDELINES ON COMPLIANCE FUNCTION FOR FUND MANAGEMENT COMPANIES Issued: 15 March 2005 Revised: 25 April 2014 1 P a g e List of Revision Revision Effective Date 1 st Revision 23 May 2011 2 nd Revision 16

CHAPTER 46:08 NON-BANK FINANCIAL INSTITUTIONS REGULATORY AUTHORITY ARRANGEMENT OF SECTIONS SECTION

CHAPTER 46:08 NON-BANK FINANCIAL INSTITUTIONS REGULATORY AUTHORITY ARRANGEMENT OF SECTIONS SECTION 1. Short title 2. Interpretation 3. Subsidiaries 4. Controllers 5. Republic, etc. to be bound PART I Preliminary

CHAPTER 46:08 NON-BANK FINANCIAL INSTITUTIONS REGULATORY AUTHORITY ARRANGEMENT OF SECTIONS SECTION 1. Short title 2. Interpretation 3. Subsidiaries 4. Controllers 5. Republic, etc. to be bound PART I Preliminary

Australian Prudential Regulation Authority. Protecting Australia s depositors, insurance policyholders and superannuation fund members

Australian Prudential Regulation Authority Protecting Australia s depositors, insurance policyholders and superannuation fund members APRA s vision is to be a world-class integrated prudential supervisor

Australian Prudential Regulation Authority Protecting Australia s depositors, insurance policyholders and superannuation fund members APRA s vision is to be a world-class integrated prudential supervisor

Risk management systems of responsible entities

Attachment to CP 263: Draft regulatory guide REGULATORY GUIDE 000 Risk management systems of responsible entities July 2016 About this guide This guide is for Australian financial services (AFS) licensees

Attachment to CP 263: Draft regulatory guide REGULATORY GUIDE 000 Risk management systems of responsible entities July 2016 About this guide This guide is for Australian financial services (AFS) licensees

Chapter 1 GENERAL INTERPRETATION

Chapter 1 GENERAL CHAPTER 1 INTERPRETATION For the avoidance of doubt, the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited apply only to matters related to those securities

Chapter 1 GENERAL CHAPTER 1 INTERPRETATION For the avoidance of doubt, the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited apply only to matters related to those securities

IOPS Member country or territory pension system profile: TRINIDAD AND TOBAGO. Update as of 15 February 2013

IOPS Member country or territory pension system profile: TRINIDAD AND TOBAGO Report 1 issued on September 2011, validated by the Central Bank of Trinidad and Tobago Update as of 15 February 2013 1 This

IOPS Member country or territory pension system profile: TRINIDAD AND TOBAGO Report 1 issued on September 2011, validated by the Central Bank of Trinidad and Tobago Update as of 15 February 2013 1 This

REPUBLIC OF SOUTH AFRICA DRAFT INSURANCE BILL --------------------------------

REPUBLIC OF SOUTH AFRICA DRAFT INSURANCE BILL -------------------------------- (As introduced in the National Assembly (proposed section 75); explanatory summary of Bill published in Government Gazette

REPUBLIC OF SOUTH AFRICA DRAFT INSURANCE BILL -------------------------------- (As introduced in the National Assembly (proposed section 75); explanatory summary of Bill published in Government Gazette

FINANCIAL MARKETS BILL

REPUBLIC OF SOUTH AFRICA FINANCIAL MARKETS BILL (As introduced in the National Assembly (proposed section 7); explanatory summary of Bill published in Government Gazette No. 22 of 7 February 12) (The English

REPUBLIC OF SOUTH AFRICA FINANCIAL MARKETS BILL (As introduced in the National Assembly (proposed section 7); explanatory summary of Bill published in Government Gazette No. 22 of 7 February 12) (The English

CONSULTATION PAPER. Insurance (Fees) Regulations 2013 Registered Schemes Administrators (Fees) Order 2013

Regulations 2013 Registered Schemes Administrators (Fees) Order 2013") CONSULTATION PAPER Insurance (Fees) Regulations 2013 Registered Schemes Administrators (Fees) Order 2013 This document is relevant to all entities regulated by the Insurance and Pensions Authority under

CONSULTATION PAPER Insurance (Fees) Regulations 2013 Registered Schemes Administrators (Fees) Order 2013 This document is relevant to all entities regulated by the Insurance and Pensions Authority under

OPEN ENDED FUND COMPANIES CONSULTATION PAPER. Financial Services and the Treasury Bureau

OPEN ENDED FUND COMPANIES CONSULTATION PAPER Financial Services and the Treasury Bureau March 2014 ABOUT THIS DOCUMENT 1. This consultation paper is published by the Financial Services and the Treasury

OPEN ENDED FUND COMPANIES CONSULTATION PAPER Financial Services and the Treasury Bureau March 2014 ABOUT THIS DOCUMENT 1. This consultation paper is published by the Financial Services and the Treasury

FINANCIAL SERVICES BOARD

FINANCIAL SERVICES BOARD MANUAL ON ACCESS TO INFORMATION HELD BY THE FINANCIAL SERVICES BOARD Compiled in terms of section 14 of the Promotion of Access to Information Act, 2 of 2000 1. The functions of

FINANCIAL SERVICES BOARD MANUAL ON ACCESS TO INFORMATION HELD BY THE FINANCIAL SERVICES BOARD Compiled in terms of section 14 of the Promotion of Access to Information Act, 2 of 2000 1. The functions of

Assist Members in developing their own national arrangements through being able to draw on and hence benefit from the experience of other members;

Introduction IFIAR is an organization of independent audit regulators (hereinafter, audit regulators ). The organization s primary aim is to enable its Members to share information regarding the audit

Introduction IFIAR is an organization of independent audit regulators (hereinafter, audit regulators ). The organization s primary aim is to enable its Members to share information regarding the audit

Question number. Question for discussion. Response by CIPQ

Response by Construction Income Protection Limited to discussion paper options for law reform - Royal Commission into Trade Union Governance and Corruption The responses of Construction Income Protection

Response by Construction Income Protection Limited to discussion paper options for law reform - Royal Commission into Trade Union Governance and Corruption The responses of Construction Income Protection

Mauritius Investment Funds

Mauritius Investment Funds Foreword This memorandum has been prepared for the assistance of those who are considering the formation and regulation of Mauritius investment funds. It deals in broad terms

Mauritius Investment Funds Foreword This memorandum has been prepared for the assistance of those who are considering the formation and regulation of Mauritius investment funds. It deals in broad terms

Pooled Registered Pension Plans in Ontario - What the Canadian Banks Have to Offer

Framework for Pooled Registered Pension Plans CBA Submission to the Ontario Ministry of Finance January 23, 2014 EXPERTISE CANADA BANKS ON LA RÉFÉRENCE BANCAIRE AU CANADA Framework for Pooled Registered

Framework for Pooled Registered Pension Plans CBA Submission to the Ontario Ministry of Finance January 23, 2014 EXPERTISE CANADA BANKS ON LA RÉFÉRENCE BANCAIRE AU CANADA Framework for Pooled Registered

Board Notices Raadskennisgewings

158 Long-term Insurance Act (52/1998): Registrar Of Long-term Insurance And Short-term Insurance 39095 4 No. 39095 GOVERNMENT GAZETTE, 14 AUGUST 2015 Board Notices Raadskennisgewings BOARD NOTICE [ -]

158 Long-term Insurance Act (52/1998): Registrar Of Long-term Insurance And Short-term Insurance 39095 4 No. 39095 GOVERNMENT GAZETTE, 14 AUGUST 2015 Board Notices Raadskennisgewings BOARD NOTICE [ -]

April 2005 Overview of Korean Retirement Pension Plan

April 2005 Overview of Korean Retirement Pension Plan Myoung Jin Koh Chief of Pension Supervision Team Financial Supervisory Service of Korea Major Contents - Overview of current pension systems in Korea

April 2005 Overview of Korean Retirement Pension Plan Myoung Jin Koh Chief of Pension Supervision Team Financial Supervisory Service of Korea Major Contents - Overview of current pension systems in Korea

Life Insurance Regulations

Life Insurance Regulations Everything you need to know* Presented by Andrew Kay and Eamonn Phelan December 13, 2011 *not really, but hopefully a good start! Agenda Life insurance Life reinsurance PRSAs

Life Insurance Regulations Everything you need to know* Presented by Andrew Kay and Eamonn Phelan December 13, 2011 *not really, but hopefully a good start! Agenda Life insurance Life reinsurance PRSAs

Self managed superannuation funds. A Financial Planning Technical Guide

Self managed superannuation funds A Financial Planning Technical Guide 2 Self managed superannuation funds What is a self managed 4 superannuation fund (SMSF)? What are the benefits? 4 What are the risks?

Self managed superannuation funds A Financial Planning Technical Guide 2 Self managed superannuation funds What is a self managed 4 superannuation fund (SMSF)? What are the benefits? 4 What are the risks?

Banking Guidance Note No. 1 Outsourcing of Services or Functions by Gibraltar- Licensed Banks. Date of Paper : 31 January 2000 Version Number : 1.

No. 1 of Services or Functions by Gibraltar- Licensed Banks Date of Paper : 31 January 2000 Version Number : 1.00 Table of Contents Introduction... 3 Submissions to FSC... 3 Assessment of Proposals...

No. 1 of Services or Functions by Gibraltar- Licensed Banks Date of Paper : 31 January 2000 Version Number : 1.00 Table of Contents Introduction... 3 Submissions to FSC... 3 Assessment of Proposals...

IOPS GOOD PRACTICES IN RISK MANAGEMENT OF ALTERNATIVE INVESTMENTS BY PENSION FUNDS

. IOPS GOOD PRACTICES IN RISK MANAGEMENT OF ALTERNATIVE INVESTMENTS BY PENSION FUNDS June 2010 1 GOOD PRACTICES IN RISK MANAGEMENT OF ALTERNATIVE INVESTMENTS BY PENSION FUNDS 1 Introduction 1. The objective

. IOPS GOOD PRACTICES IN RISK MANAGEMENT OF ALTERNATIVE INVESTMENTS BY PENSION FUNDS June 2010 1 GOOD PRACTICES IN RISK MANAGEMENT OF ALTERNATIVE INVESTMENTS BY PENSION FUNDS 1 Introduction 1. The objective

Peer Review on Supervisory Practices in respect of Article 9 of Directive 2003/41/EC ( Conditions of operation ) Final Report

Final Report") EIOPA-BoS-14/262 12 March 2015 Peer Review on Supervisory Practices in respect of Article 9 of Directive 2003/41/EC ( Conditions of operation ) Final Report EIOPA Westhafen Tower, Westhafenplatz 1-60327

EIOPA-BoS-14/262 12 March 2015 Peer Review on Supervisory Practices in respect of Article 9 of Directive 2003/41/EC ( Conditions of operation ) Final Report EIOPA Westhafen Tower, Westhafenplatz 1-60327

SCOPE OF APPLICATION AND DEFINITIONS

Unofficial translation No. 398/1995 Act on Foreign Insurance Companies Issued in Helsinki on 17 March 1995 PART I SCOPE OF APPLICATION AND DEFINITIONS Chapter 1. General Provisions Section 1. Scope of

Unofficial translation No. 398/1995 Act on Foreign Insurance Companies Issued in Helsinki on 17 March 1995 PART I SCOPE OF APPLICATION AND DEFINITIONS Chapter 1. General Provisions Section 1. Scope of

International Monetary Fund Washington, D.C.

2007 International Monetary Fund May 2007 IMF Country Report No. 07/156 Gibraltar: Detailed Report of Observance of the Insurance Core Principles This Detailed Report of Observance of the Insurance Core

2007 International Monetary Fund May 2007 IMF Country Report No. 07/156 Gibraltar: Detailed Report of Observance of the Insurance Core Principles This Detailed Report of Observance of the Insurance Core

RETIREMENT ANNUITY TRUST SCHEMES (RATS)

") FACT SHEET RETIREMENT ANNUITY TRUST SCHEMES (RATS) With only a limited number of retirement annuity contracts (RAC) and personal pension schemes (PPS) available in Guernsey, the popularity of RATS is growing

FACT SHEET RETIREMENT ANNUITY TRUST SCHEMES (RATS) With only a limited number of retirement annuity contracts (RAC) and personal pension schemes (PPS) available in Guernsey, the popularity of RATS is growing

Official Journal of the European Union

L 235/10 23.9.2003 DIRECTIVE 2003/41/EC OF THE EUROPEAN PARLIAMT AND OF THE COUNCIL of 3 June 2003 on the activities and supervision of institutions for occupational retirement provision THE EUROPEAN PARLIAMT

L 235/10 23.9.2003 DIRECTIVE 2003/41/EC OF THE EUROPEAN PARLIAMT AND OF THE COUNCIL of 3 June 2003 on the activities and supervision of institutions for occupational retirement provision THE EUROPEAN PARLIAMT

Understanding Self Managed Superannuation Funds Version 5.0

Understanding Self Managed Superannuation Funds Version 5.0 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to

Understanding Self Managed Superannuation Funds Version 5.0 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to

6. Supporting the financial services industry and looking to the future

6. Supporting the financial services industry and looking to the future 6.1. Issues raised outside the scope of this project The NRFSB Law and FinTech / Digital Finance (DP 6.1.1 6.1.4) 6.1.1. The Commission

6. Supporting the financial services industry and looking to the future 6.1. Issues raised outside the scope of this project The NRFSB Law and FinTech / Digital Finance (DP 6.1.1 6.1.4) 6.1.1. The Commission

GUIDANCE NOTE DECISION-MAKING PROCESS

GUIDANCE NOTE DECISION-MAKING PROCESS This document is intended as a general guide to the way in which the Jersey Financial Services Commission (the Commission ), normally approaches the exercise of its

GUIDANCE NOTE DECISION-MAKING PROCESS This document is intended as a general guide to the way in which the Jersey Financial Services Commission (the Commission ), normally approaches the exercise of its

This Statement of Investment Principles is produced to meet the requirements of the Pensions Act 2004 and to reflect the Government s voluntary code

This Statement of Investment Principles is produced to meet the requirements of the Pensions Act 2004 and to reflect the Government s voluntary code the Myners Principles. The Trustee also complies with

This Statement of Investment Principles is produced to meet the requirements of the Pensions Act 2004 and to reflect the Government s voluntary code the Myners Principles. The Trustee also complies with

Department: Corporate Secretariat

RESPONSIBLE PERSON POLICY Department: Corporate Secretariat 1 Contents Overview 3 General Principles 4 Fitness 4 Propriety 4 Policies: 4 Entity needs and fitness analysis 4 Identifying responsible person

RESPONSIBLE PERSON POLICY Department: Corporate Secretariat 1 Contents Overview 3 General Principles 4 Fitness 4 Propriety 4 Policies: 4 Entity needs and fitness analysis 4 Identifying responsible person

Code of Practice. Overall. A1.2 Segregation, identification and safeguarding of trust assets is paramount.

Code of Practice A Overall A1. Integrity A TACT member must conduct its business with integrity. A1.1 Members will ensure that their key persons and officers work with the highest integrity at all times

Code of Practice A Overall A1. Integrity A TACT member must conduct its business with integrity. A1.1 Members will ensure that their key persons and officers work with the highest integrity at all times

NSW Self Insurance Corporation Amendment (Home Warranty Insurance) Act 2010 No 30

Act 2010 No 30") New South Wales NSW Self Insurance Corporation Amendment (Home Warranty Insurance) Contents Page 1 Name of Act 2 2 Commencement 2 Schedule 1 Amendment of NSW Self Insurance Corporation Act 2004 No 106

New South Wales NSW Self Insurance Corporation Amendment (Home Warranty Insurance) Contents Page 1 Name of Act 2 2 Commencement 2 Schedule 1 Amendment of NSW Self Insurance Corporation Act 2004 No 106

INVESTMENT FUNDS ACT 2006 BERMUDA 2006 : 37 INVESTMENT FUNDS ACT 2006

BERMUDA 2006 : 37 INVESTMENT FUNDS ACT 2006 Date of Assent: 28 December 2006 Operative Date: 7 March 2007 ARRANGEMENT OF PARAGRAPHS PART I PRELIMINARY 1 Short title and commencement Interpretation 2 Interpretation

BERMUDA 2006 : 37 INVESTMENT FUNDS ACT 2006 Date of Assent: 28 December 2006 Operative Date: 7 March 2007 ARRANGEMENT OF PARAGRAPHS PART I PRELIMINARY 1 Short title and commencement Interpretation 2 Interpretation

COLLECTIVE INVESTMENT LAW DIFC LAW No. 2 of 2010

---------------------------------------------------------------------------------------------- COLLECTIVE INVESTMENT LAW DIFC LAW No. 2 of 2010 ----------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------- COLLECTIVE INVESTMENT LAW DIFC LAW No. 2 of 2010 ----------------------------------------------------------------------------------------------

Fit and Proper Assessment Best Practice

Fit and Proper Assessment Best Practice Final Report EMERGING MARKETS COMMITTEE OF THE INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS DECEMBER 2009 CONTENTS Chapter Page 1 Introduction 3 1.1 Objectives

Fit and Proper Assessment Best Practice Final Report EMERGING MARKETS COMMITTEE OF THE INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS DECEMBER 2009 CONTENTS Chapter Page 1 Introduction 3 1.1 Objectives

Strategy for regulating defined contribution pension schemes

Strategy for regulating defined contribution pension schemes From April 2015, new pensions legislation came into force which directly affects this strategy. We will consult on any proposed revisions to

Strategy for regulating defined contribution pension schemes From April 2015, new pensions legislation came into force which directly affects this strategy. We will consult on any proposed revisions to

Financial Services Guidance Note Outsourcing

Financial Services Guidance Note Issued: April 2005 Revised: August 2007 Table of Contents 1. Introduction... 3 1.1 Background... 3 1.2 Definitions... 3 2. Guiding Principles... 5 3. Key Risks of... 14

Financial Services Guidance Note Issued: April 2005 Revised: August 2007 Table of Contents 1. Introduction... 3 1.1 Background... 3 1.2 Definitions... 3 2. Guiding Principles... 5 3. Key Risks of... 14

Objective and key requirements of this Prudential Standard

Prudential Standard CPS 520 Fit and Proper Objective and key requirements of this Prudential Standard This Prudential Standard sets out minimum requirements for APRA-regulated institutions in determining

Prudential Standard CPS 520 Fit and Proper Objective and key requirements of this Prudential Standard This Prudential Standard sets out minimum requirements for APRA-regulated institutions in determining

APRA and PHIAC - Interdependence

Memorandum of Understanding between PRIVATE HEALTH INSURANCE ADMINISTRATION COUNCIL and AUSTRALIAN PRUDENTIAL REGULATION AUTHORITY 2 MEMORANDUM OF UNDERSTANDING BETWEEN THE AUSTRALIAN PRUDENTIAL REGULATION

Memorandum of Understanding between PRIVATE HEALTH INSURANCE ADMINISTRATION COUNCIL and AUSTRALIAN PRUDENTIAL REGULATION AUTHORITY 2 MEMORANDUM OF UNDERSTANDING BETWEEN THE AUSTRALIAN PRUDENTIAL REGULATION

FUND MANAGER CODE OF CONDUCT

FUND MANAGER CODE OF CONDUCT First Edition pursuant to the Securities and Futures Ordinance (Cap. 571) April 2003 Securities and Futures Commission Hong Kong TABLE OF CONTENTS Page INTRODUCTION 1 I. ORGANISATION

FUND MANAGER CODE OF CONDUCT First Edition pursuant to the Securities and Futures Ordinance (Cap. 571) April 2003 Securities and Futures Commission Hong Kong TABLE OF CONTENTS Page INTRODUCTION 1 I. ORGANISATION

GUIDE TO CAPTIVE INSURANCE COMPANIES IN THE CAYMAN ISLANDS

GUIDE TO CAPTIVE INSURANCE COMPANIES IN THE CAYMAN ISLANDS CONTENTS PREFACE 1 1. Cayman Islands Jurisdiction of Choice 2 2. Reasons for Establishing an Insurance Captive 3 3. Establishment and Licensing

GUIDE TO CAPTIVE INSURANCE COMPANIES IN THE CAYMAN ISLANDS CONTENTS PREFACE 1 1. Cayman Islands Jurisdiction of Choice 2 2. Reasons for Establishing an Insurance Captive 3 3. Establishment and Licensing

Objective and key requirements of this Prudential Standard

Prudential Standard GPS 001 Definitions Objective and key requirements of this Prudential Standard The purpose of this Prudential Standard is to define key terms referred to in other Prudential Standards

Prudential Standard GPS 001 Definitions Objective and key requirements of this Prudential Standard The purpose of this Prudential Standard is to define key terms referred to in other Prudential Standards

Australian Charities and Not-for-profits Commission: Regulatory Approach Statement

Australian Charities and Not-for-profits Commission: Regulatory Approach Statement This statement sets out the regulatory approach of the Australian Charities and Not-for-profits Commission (ACNC). It

Australian Charities and Not-for-profits Commission: Regulatory Approach Statement This statement sets out the regulatory approach of the Australian Charities and Not-for-profits Commission (ACNC). It

Agenda. Professionalism and Governance of the Profession. Yves Guérard, Secretary General. Challenges for the Profession. The IAA Priorities

The Fifth International Professional Meeting of Leaders of the Actuarial Profession and Actuarial Educators in Asia and the Pacific Agenda Professionalism, an IAA priority since the restructure What is

The Fifth International Professional Meeting of Leaders of the Actuarial Profession and Actuarial Educators in Asia and the Pacific Agenda Professionalism, an IAA priority since the restructure What is

New Bermuda Company Formation Documents

NEW CLIENT DOCUMENTATION PACKAGE Find enclosed herewith our company formation questionnaire and related documentation required to commence a business relationship with St. George s Services Limited. This

NEW CLIENT DOCUMENTATION PACKAGE Find enclosed herewith our company formation questionnaire and related documentation required to commence a business relationship with St. George s Services Limited. This

COMPLIANCE FRAMEWORK AND REPORTING GUIDELINES

COMPLIANCE FRAMEWORK AND REPORTING GUIDELINES DRAFT FOR CONSULTATION June 2015 38 Cavenagh Street DARWIN NT 0800 Postal Address GPO Box 915 DARWIN NT 0801 Email: utilities.commission@nt.gov.au Website:

COMPLIANCE FRAMEWORK AND REPORTING GUIDELINES DRAFT FOR CONSULTATION June 2015 38 Cavenagh Street DARWIN NT 0800 Postal Address GPO Box 915 DARWIN NT 0801 Email: utilities.commission@nt.gov.au Website:

Outsourcing. FSA Regulated firms (including offshore outsourcing) Contents. March 2004

Contents. March 2004") Outsourcing FSA Regulated firms (including offshore outsourcing) March 2004 Contents 2. Introduction 2. How do the regulations impact an outsourcing? 3. Prudential Sourcebooks 4. Service Level Agreements

Outsourcing FSA Regulated firms (including offshore outsourcing) March 2004 Contents 2. Introduction 2. How do the regulations impact an outsourcing? 3. Prudential Sourcebooks 4. Service Level Agreements

Submission in response to the Life Insurance and Advice Working Group Interim Report on Retail Life Insurance

30 January 2015 Mr John Trowbridge Chairman Life Insurance and Advice Working Group Email: submissions@trowbridge.com.au Dear Mr Trowbridge, Submission in response to the Life Insurance and Advice Working

30 January 2015 Mr John Trowbridge Chairman Life Insurance and Advice Working Group Email: submissions@trowbridge.com.au Dear Mr Trowbridge, Submission in response to the Life Insurance and Advice Working

MLC Derivatives Policy

MLC Derivatives Policy 1 Overview The purpose of this policy is to provide guiding principles and policy directives for the use and oversight of derivatives used within the products, investment portfolios

MLC Derivatives Policy 1 Overview The purpose of this policy is to provide guiding principles and policy directives for the use and oversight of derivatives used within the products, investment portfolios