Presentation for Licensed Producers The Affordable Care Act

|

|

|

- Mary Gray

- 8 years ago

- Views:

Transcription

1 Presentation for Licensed Producers The Affordable Care Act Bruce Donaldson, CHC Producer & Stakeholder Specialist Arkansas Insurance Department

2 Affordable Care Act The ACA was passed by Congress and signed into law by President Obama in 2010.

3 What happened next? In 2012 the U.S. Supreme Court upheld the ACA as constitutional. In the same ruling, the court nonetheless ruled that the federal government couldn t force states to expand their Medicaid programs.

4 Why Health Care Reform Is Needed Poor Health Status of Arkansans Ranked 48 th on health indicators (3 rd worst) High rates of chronic disease Health Care Costs Premium care costs have doubled in the past ten years. Many are paying > 10% of income on health care. 25% of adult Arkansans, under age 65, are uninsured (over 500,000) 4

http://www.")

5 The Affordable Care Act The Affordable Care Act of 2010 was created to decrease health costs and improve health outcomes through: Public and Private Coverage Expansions* Change in Benefits and Access to Care Insurance Issuer Market Reforms New Individual Responsibility Establishment of Health Insurance Marketplace 5

6 The Affordable Care Act Individual Responsibility Most must purchase health insurance Reduces the cost for many Assistance is available (premium tax credits) No penalty if not required to file a tax return Public (Medicaid) and Private Coverage Expansions Additional 250,000 could be covered under Medicaid Additional 211,000 likely to obtain Private Coverage in 2014 Billions of dollars will come into Arkansas 6

7 How the Affordable Care Act Has Already Helped Consumers Children can stay on their parents insurance policy until the age of 26. Insurance companies can no longer deny coverage of a child under age 19 due to his/her health conditions. Lifetime benefit limits are eliminated and annual benefit limits on insurance coverage are regulated until Rescinding coverage by insurance companies is prohibited unless due to fraud. Ihttp:// student loans top 1 trillion age 7

8 How the Affordable Care Act Has Already Helped Consumers Recommended preventive services, such as mammograms, colonoscopies, wellness visits, etc. now at no cost to certain consumers. Rebates on health insurance premiums paid if the insurance company does not pay enough on health care claims. Relief for more than a half million Arkansas seniors who hit the Medicare donut hole. Consumer Assistance Program established at AID. 8

9 How the Affordable Care Act Will Help Consumers in the Future Insurance companies cannot deny coverage for anyone due to health conditions or personal health history. No annual or lifetime benefit limits. Begin to close gaps in prescription drug coverage for Medicare (Gaps will be eliminated by 2020). Premiums cannot be increased due to gender, health conditions or personal health history. 9

.")

10 How the Affordable Care Act Will Help Consumers in the Future Premiums can only be increased due to age, geography, tobacco use, and type of coverage. Eligibility determinations are real time. Primary care physicians will be paid no less than 100% of Medicare payment rates for primary care services. 10

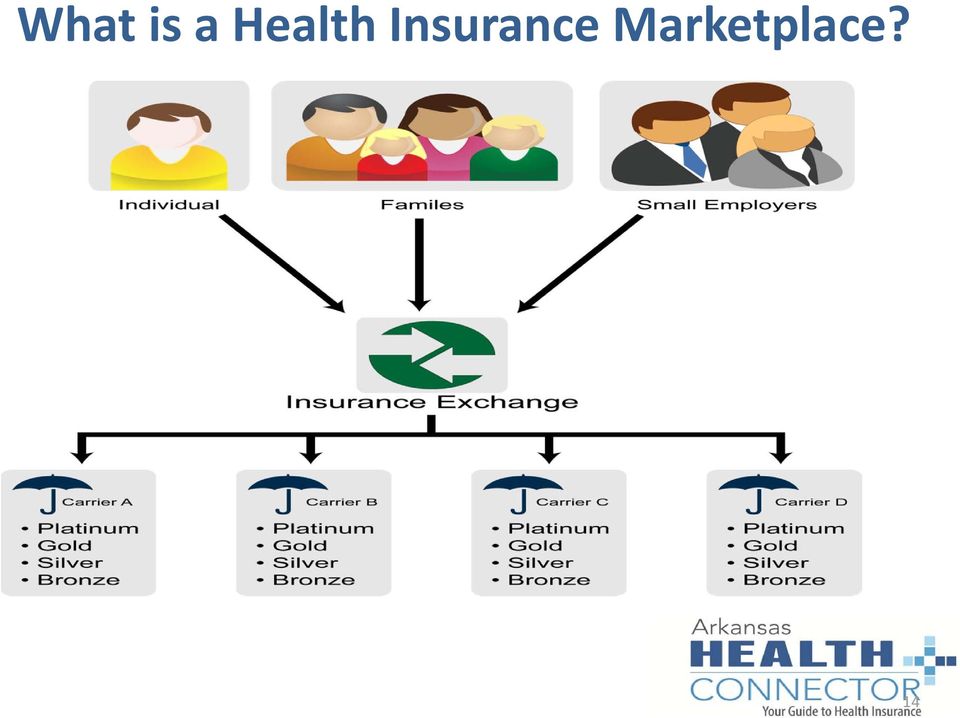

11 What is a Health Insurance Marketplace (Exchange)? Competitive marketplace where individuals, families and small employers can shop for, select and enroll in high quality, affordable private health plans that meet their specific needs at competitive prices. Marketplaces will also help eligible individuals receive premium tax credits and cost sharing reductions or help them enroll in other state or federal public health programs. 11

12 Types of Exchanges (Marketplace) State Based Marketplace (SBM) State is responsible for all functions (QHP, Premium fees, oversight/monitoring, eligibility/enrollment, IT, outreach/education, consumer complaint, In Person assistance and the call center). Partnership Marketplace Marketplace is operated by the federal government, however State retains responsibility for Plan Management and/or Consumer Assistance functions. Federally facilitated Marketplace All functions are the responsibility of the federal government. 12

13 Status of Marketplaces State Based Marketplace Federal Marketplace Partnership Marketplace 13

14 What is a Health Insurance Marketplace? 14

15 Premium Tax Credit Eligibility Household income 138% 400% FPL ($32,499 $94,200 for a family of four). Must be enrolled in a QHP through the Marketplace. Must be lawfully present and not incarcerated. Must not be eligible for other coverage such as Medicare, Medicaid, or employer sponsored insurance. Subsidies are based on the second lowest cost silver plan (actuarial value of 70%) 15

16 Arkansas Benchmark Plan 16

17 Options for AR EHB Benchmark for 2014 One of the three largest federal plans by enrollment One of the three largest state small group plans by enrollment One of the three largest state employee plans by enrollment The largest HMO in State by enrollment If state doesn t choose by September 30, 2012, the federal default plan is the state s largest small group plan by enrollment. 17

18 Arkansas EHB Benchmark Plan for 2014 Commissioner Bradford announced the EHB Benchmark Plan Selection on September 21, Arkansas Blue Cross Blue Shield Health Advantage Point of Service Plan (POS) QualChoice Federal Plan Mental Health and Substance Abuse Benefits for the mental health benefit due to the POS Benefit not being sufficient to meet the requirements under federal law. Arkansas Child Health Insurance Plan (CHIP), AR Kids First for the pediatric dental benefit not provided under the POS plan. Arkansas Blue Cross Blue Shield Federal Pediatric Vision Plan as the POS does not cover pediatric vision benefits and the only supplementation option is the federal plan with the highest enrollment. The EHB was submitted to CCIIO through the HIOS upload on September 26, Details related to each of these plans may be found at 18

19 Qualified Health Plan Benefits (QHPs) All health insurance plans offered on the Marketplace will be Qualified Health Plans, meaning that payments made by the insurance company towards health care costs must meet at least 60% of actuarial value and the following Essential Health Benefits must be provided: 1. Ambulatory Services 2. Hospitalization 3. Emergency Services 4. Maternity and Newborn Care 5. Mental Health and Substance Use Disorder Treatment 6. Prescription Drugs 7. Rehabilitative and Habilitative Services/Devices 8. Laboratory Services 9. Preventive, Wellness, and Chronic Disease Management 10. Pediatric Services, Including Oral and Vision Care 19

20 QHP Levels Allowed on the Marketplace QHP Levels are based on Actuarial Value. The insurance company will pay: Platinum 90% Gold 80% Silver 70% Bronze 60% Catastrophic plans available for adults under 30.

21 QHP Pediatric Dental Plans Stand Alone Pediatric Dental Plans Must demonstrate reasonable annual limitation on cost sharing (without regard to Out of Network) Must demonstrate benefit level 75% 85% (+/ 2%) certified by actuary (may not use AV calculator) note this is different than metal tier AV levels Coverage for Pediatric Dental until age 19

22 Rating Factor Limitations Rates for a particular plan may vary based on the following factors: Whether coverage is for individual or family Geographic Rating Area 7 rating areas in Arkansas Age Tobacco Use Arkansas 20% max rate up (Individual Plans Only) 22

23 Rating Factor Limitations Cont d Uniform Age Bands Child Age Bands Single Age Band 0 to 20 years Adult Age Bands One Year Age bands starting at 21 years and ending at 63 Older Adult Age Bands Single Age Band for individuals from 64 and older 23

24 Rating Factor Limitations Cont d AGE PREMIUM RATIO AGE PREMIUM RATIO AGE PREMIUM RATIO and older

25 Rating Factor Limitations Cont d Individual Marketplace Premiums: In determining the total premium for families, rates would include all the adults and the three oldest covered children who are less than 21 years old. Small group marketplace Premiums: The total premium charged to a small employer group shall be determined by summing the premiums of all plan members based on the same calculation used for the individual market. 25

26 Premiums for Second Lowest Cost Silver Plan From The Washington Post 7/18/13 26

27 Grandfathered Plans Grandfathered and non grandfathered plans: Many health plans that existed before the ACA was passed (March 10, 2010) do not have to implement many aspects of health care reform. These plans are considered to be grandfathered. Plans that do not meet the standards to be considered grandfathered and are, therefore, required to implement all applicable ACA regulations are called nongrandfathered health plans. 27

28 Grandfathered Plans Cont d What Causes an Existing Group Health Plan to Lose Grandfathered Status? Elimination of all or substantially all benefits to diagnose or treat a particular condition. Any increase in a percentage cost sharing requirement (coinsurance) Any increase in fixed dollar cost sharing (deductibles & out of pocket expenses) in excess of the rate of medical inflation since March 23, 2010 plus 15 percentage points. Any increase in co payments in excess of the greater of a) the rate of medical inflation, plus 15% or b) $5.00, increased by medical inflation. Any decrease in employer contributions towards any tier of coverage by more than 5 percent of the contribution rate in effect on March 23, 2010 (cumulative). Certain changes in Annual Benefit Limits 28

29 Individual Marketplace 29

30 Benefits To Using The Marketplace More than half a million Arkansans will be eligible for marketplace coverage beginning January 1, Individual with incomes between 138% 400% of the federal poverty level (FPL) may be eligible for assistance in paying the premium. Individuals with incomes between 0% & 138% of FPL will be eligible for private plans (high level silver plan) with Medicaid funding the premiums. No asset testing is required. Consumer premium cost <9.5% (mostly less) of household income. 30

31 2013 Federal Poverty Guidelines FAMILY SIZE 100% 138% 200% 400% 1 $11,490 $15,856 $22,980 $45,960 2 $15,510 $21,404 $31,020 $62,040 3 $19,530 $26,951 $39,060 $78,120 4 $23,550 $32,499 $47,100 $94,200 5 $27,570 $38,047 $55,140 $110,280 6 $31,590 $43,594 $63,180 $126,360 7 $36,610 $49,142 $71,220 $142,440 8 $39,630 $54,689 $79,260 $158,520 For each Additional person, add $4,020 $5,347 $8,040 $16,080 31

32 Premium Limits Based on Income INCOME PREMIUM LIMIT 0 138% FPL (Medicaid Expansion) % FPL (non Medicaid eligible) 2% of income % FPL 3 4% of income % FPL 4 6.3% of income % FPL % of income % FPL % of income % FPL 9.5% of income 32

33 Examples of Contributions & Tax Credits Coverage Tiers Federal Poverty Level Yearly Income Maximum Premium Contribution Estimated Monthly Premium Consumer Monthly Payment Monthly Tax Subsidy Amount 100% 11,170 2% $466 $19 $447 SELF 200% $22, % $466 $117 $ % $33, % $466 $265 $ % $44, % $466 $353 $ % $23,050 2% $1,308 $38 $1,270 FAMILY OF FOUR 200% $46, % $1,308 $242 $1, % $69, % $1,308 $547 $ % $91, % $1,308 $728 $580 Above numbers are estimated and rounded 33

34 Arkansas Medicaid Expansion April 23, 2013 Health Care Independence Act signed by Governor Beebe. Only State privatizing Medicaid Represents truly private coverage fully integrated within the Marketplace (not a Medicaid product) Expected to add 250,000 or more to the private marketplace 34

35 Health Care Independence Act Medicaid will purchase private, qualified health plan (QHP) coverage on the Marketplace for certain MAGI eligible beneficiaries. Effectuated through a Transition to Market Cost sharing for individuals at % of FPL Additional Medicaid eligible populations will come into the private option 35

36 Private Option Eligible Individuals in 2014 Childless adults ages with incomes below 138% FPL Parents ages with incomes between 17% and 138% FPL Who are not on Medicare Who are not disabled Who have not been determined to be more effectively covered under the standard Medicaid program, such as an individual who is medically frail or other individuals for whom coverage through the Health Insurance Marketplace is determined to be impractical, overly complex or would undermine continuity or effectiveness of care 36

37 Private Option Enrollees Will Enroll in Silver Plans Eligible individuals will be permitted to shop among and enroll in QHPs offered at the Silver metal level in the Marketplace, at the following actuarial value variations: Eligible Individuals with Incomes from 0 100% FPL Year 1: Zero Cost Sharing Silver Plan Variation (100% actuarial value) Year 2: Transition to cost sharing for individuals with incomes from % FPL Eligible Individuals with Incomes from % FPL Years 1 and 2: High Value Silver Plan Variation (94% +/ 1% actuarial value) 37

38 What are Penalties for Not Enrolling? 2014 $95 or 1% of adjusted gross income, whichever is greater, for each adult in the household $325 or 2%, whichever is greater, for each adult in the household $695 or 2.5%, whichever is greater, for each adult in the household. There are limited penalty exemptions. The Congressional Budget Office (CBO), a non partisan agency, estimates that 4 million individuals or 1.2% of the total population will pay penalties to the IRS in

39 Individual Enrollment Open enrollment begins October 1, 2013 through March 31, 2014 first year Subsequent years will be October 15 through December 7 th. (mirrors Medicare) Below 138% continuous enrollment into Private Option 39

40 SHOP (Small Employer Marketplace) 40

41 Benefits To Using The SHOP Marketplace Businesses with less than 25 full time equivalent (FTE) employees may be eligible for tax credits or other cost reductions in 2014 (for any 2 consecutive years). Business Health Care Tax Credit for Small Employers 41

42 What Are Employer Requirements? No requirement to provide insurance for employers with less than 50 FTE employees no requirement to provide insurance for employers with 50 or more Full Time Employees (FTEs 30 or more hours/week) If 50 or more FTE employees, employer must provide affordable insurance options for full time employees (affordable is defined as 9.5% of employee s wages for employee only premium).

43 What are Employer Penalties? 50 full time employees If no offer of minimum coverage to every full time employee and any one employee receives tax subsidized coverage through an individual marketplace, the employer must pay a $2,000 penalty for every full time employee. (The first 30 employees are not counted in determining the penalty.)

44 What are Employer Penalties Cont d? 50 full time employees contd. Employee is offered coverage but obtains tax subsidized coverage through the individual marketplace, the employer must pay a $3,000 penalty for each such employee or $2000 per employee after the first 30, whichever is less. (While any employee is free to decline the employer plan and shift to the marketplace, the tax credit is available only if the worker s required contribution to the employer plan for single coverage is more than 9.5 % of the employee s income or the plan pays less than 60 percent of the cost of covered services.) 01/13/13

45 SHOP Marketplace Rules 2014 Small businesses with 2 50 FTEs will be able to shop on the Marketplace. No premium aggregation employer will select one plan for all employees as today Employers will choose a plan & level to determine contributions, employees will have choice among other plans offered on the marketplace for that employer Businesses with up to 100 FTEs will be able to shop on the Marketplace Businesses with over 100 employees at State option. 45

46 Producers in the Marketplace 46

47 Producer Requirements Training & Licensing Producers will be required to take two phases of training and assessments to get their licenses to write business on the Individual & SHOP Marketplace. Federal modules (on line) and pass a test. State modules (on line) and pass a test. When anticipate late August for release of federal on line training, followed by state release. 47

48 Producer Requirements Cont d Commissions Carriers will determine how much commissions producers will receive. ACA requires same commissions to be paid both on and off the Marketplace for same plan. Producers will be paid commissions only from carriers they are appointed with as they do today. Producers must show all QHP plans available to consumers & small group. Producer portals will be available

49 In Person Assister (IPA) Program There will be several types of assisters to help consumers/employers get help in understanding insurance options, determining eligibility, and facilitating enrollment: Navigators Guides Licensed agents and brokers Certified Application Counselors (CACs) All will be trained and certified by the Arkansas Insurance Department. A list of trained and certified assisters, including agents & brokers will be posted on AID website. 49

50 Education & Outreach Campaign 50

51 Campaign Overview Overall Goal to motivate 500,000+ uninsured and underinsured Arkansans to take action. The Arkansas Health Connector website will launch July 1 st to help consumers and small businesses how determine eligibility and enroll into coverage. Statewide media effort, paid media in all 75 counties; air cover will reach the most uninsured and underinsured Arkansans the fastest. Grassroots media including local/community radio, community newspapers & direct mail. 51

52 When? All before September 30 Production of Campaign materials in June AETN Program June 27 to kick off Public awareness efforts for Education & Outreach Campaign launched July 1. ARHealthConnector.org website launched June 27,

53 Summary Cost and quality improvements in Arkansas s healthcare system will benefit all Arkansans. The Affordable Care Act has already resulted in improved coverage for many. More enhancements will become effective January 1, 2014, including access to quality, affordable insurance coverage through the state chosen Health Benefits Exchange model (Open enrollment begins 10/01/13). Increased coverage will help keep health care local. Stay tuned for future updates!

54 Additional Information

55 Questions/Comments 55

The Affordable Care Act What does it mean to Arkansans? Sandra L. Cook, MPA Consumer Assistance Specialist Arkansas Insurance Department

The Affordable Care Act What does it mean to Arkansans? Sandra L. Cook, MPA Consumer Assistance Specialist Arkansas Insurance Department PRESENTATION OBJECTIVES By the end of this presentation, participants

The Affordable Care Act What does it mean to Arkansans? Sandra L. Cook, MPA Consumer Assistance Specialist Arkansas Insurance Department PRESENTATION OBJECTIVES By the end of this presentation, participants

Health Care Reform Update

Small Businesses No Financial Requirements for Small Businesses: The ACA imposes no financial requirements for small businesses to contribute to their employees health insurance. However, beginning in

Small Businesses No Financial Requirements for Small Businesses: The ACA imposes no financial requirements for small businesses to contribute to their employees health insurance. However, beginning in

Health insurance Marketplace. What to expect in 2014

Health insurance Marketplace What to expect in 2014 Overview The Affordable Care Act (ACA) includes several provisions geared to extend greater access to health insurance benefits to more people. Beginning

Health insurance Marketplace What to expect in 2014 Overview The Affordable Care Act (ACA) includes several provisions geared to extend greater access to health insurance benefits to more people. Beginning

Kansas Insurance Department

Kansas Insurance Department A Kansas Guide to Health Insurance Changes Public Policy Session Panel Discussion KAMU Annual Conference Sept. 26, 2013 Sandy Praeger, Commissioner of Insurance 2014 Affordable

Kansas Insurance Department A Kansas Guide to Health Insurance Changes Public Policy Session Panel Discussion KAMU Annual Conference Sept. 26, 2013 Sandy Praeger, Commissioner of Insurance 2014 Affordable

Kansas Insurance Department

Kansas Insurance Department The Affordable Care Act What Happens Now? Kansas Society of CPAs June 5, 2013 Linda J. Sheppard, Special Counsel & Director of Health Care Policy and Analysis 2010 Affordable

Kansas Insurance Department The Affordable Care Act What Happens Now? Kansas Society of CPAs June 5, 2013 Linda J. Sheppard, Special Counsel & Director of Health Care Policy and Analysis 2010 Affordable

Federal Health Reform FAQs

Federal Health Reform FAQs Individuals 1. What is an exchange? An exchange, as created under the Affordable Care Act (ACA), is a place where consumers can purchase subsidized health insurance coverage.

Federal Health Reform FAQs Individuals 1. What is an exchange? An exchange, as created under the Affordable Care Act (ACA), is a place where consumers can purchase subsidized health insurance coverage.

Healthcare Reform Preparedness for Small Businesses

Healthcare Reform Preparedness for Small Businesses Blue KC on Wheels Community awareness initiative Health screenings Wellness information Seminars on healthcare reform, health insurance and wellness

Healthcare Reform Preparedness for Small Businesses Blue KC on Wheels Community awareness initiative Health screenings Wellness information Seminars on healthcare reform, health insurance and wellness

Nebraska Health Insurance Exchange Update

Nebraska Health Insurance Exchange Update Overview of the Affordable Care Act and the Federally Facilitated marketplace. September 2014 AFFORDABLE CARE ACT» The Affordable Care Act: Establishes a Health

Nebraska Health Insurance Exchange Update Overview of the Affordable Care Act and the Federally Facilitated marketplace. September 2014 AFFORDABLE CARE ACT» The Affordable Care Act: Establishes a Health

Understanding the ObamaCare Health Insurance Plans in North Carolina Understanding Insurance and Affordable Care Act Terminology: ACA- Marketplace

Understanding the ObamaCare Health Insurance Plans in North Carolina As a result of the Affordable Care Act (a.k.a. ObamaCare) the following provisions are now in place for health insurance policies with

Understanding the ObamaCare Health Insurance Plans in North Carolina As a result of the Affordable Care Act (a.k.a. ObamaCare) the following provisions are now in place for health insurance policies with

Exchanges and the ACA What You Need to Know for 2014

Exchanges and the ACA What You Need to Know for 2014 How the Affordable Care Act affects the Individual Health Insurance Market This presentation is for informational purposes only and does not constitute

Exchanges and the ACA What You Need to Know for 2014 How the Affordable Care Act affects the Individual Health Insurance Market This presentation is for informational purposes only and does not constitute

Patient Protection and Affordable Care Act (ACA) ACA Guide for Group Employers Employer Information

ACA Guide for Group Employers Employer Information") Patient Protection and Affordable Care Act (ACA) ACA Guide for Group Employers Employer Information DISCLAIMER 2 This information is being provided in an effort to alert you to changes required by the

Patient Protection and Affordable Care Act (ACA) ACA Guide for Group Employers Employer Information DISCLAIMER 2 This information is being provided in an effort to alert you to changes required by the

Legislative Brief: COMPREHENSIVE HEALTH COVERAGE ESSENTIAL HEALTH BENEFITS PACKAGE

Laurus Strategies Legislative Brief: COMPREHENSIVE HEALTH COVERAGE ESSENTIAL HEALTH BENEFITS PACKAGE The Affordable Care Act (ACA) requires non grandfathered health insurance plans in the individual and

Laurus Strategies Legislative Brief: COMPREHENSIVE HEALTH COVERAGE ESSENTIAL HEALTH BENEFITS PACKAGE The Affordable Care Act (ACA) requires non grandfathered health insurance plans in the individual and

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE Scott Walker, Governor Theodore K. Nickel, Commissioner Wisconsin.gov 125 South Webster Street P.O. Box 7873 Madison, Wisconsin 53707-7873 Phone:

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE Scott Walker, Governor Theodore K. Nickel, Commissioner Wisconsin.gov 125 South Webster Street P.O. Box 7873 Madison, Wisconsin 53707-7873 Phone:

Patient Protection and Affordable Care Act (ACA) ACA Guide for Group Employers Agent and Broker Information

ACA Guide for Group Employers Agent and Broker Information") Patient Protection and Affordable Care Act (ACA) ACA Guide for Group Employers Agent and Broker Information DISCLAIMER 2 This information is being provided in an effort to alert you to changes required

Patient Protection and Affordable Care Act (ACA) ACA Guide for Group Employers Agent and Broker Information DISCLAIMER 2 This information is being provided in an effort to alert you to changes required

Affordable Care Act HEALTHCARE.GOV. Marketplace Implementation Briefing Virginia Organizing Marketplace Public Forum August 20, 2013

HEALTHCARE.GOV Affordable Care Act Marketplace Implementation Briefing Virginia Organizing Marketplace Public Forum August 20, 2013 Joanne Corte Grossi, MIPP Regional Director U.S. Department of Health

HEALTHCARE.GOV Affordable Care Act Marketplace Implementation Briefing Virginia Organizing Marketplace Public Forum August 20, 2013 Joanne Corte Grossi, MIPP Regional Director U.S. Department of Health

The Affordable Care Act: Health Coverage Options & Considerations in 2014

The Affordable Care Act: Health Coverage Options & Considerations in 2014 J A C K S O N V I L L E A R E A C H A M B E R O F C O M M E R C E A U G U S T 2 7, 2 0 1 3 L A U R A M I N Z E R E X E C U T I

The Affordable Care Act: Health Coverage Options & Considerations in 2014 J A C K S O N V I L L E A R E A C H A M B E R O F C O M M E R C E A U G U S T 2 7, 2 0 1 3 L A U R A M I N Z E R E X E C U T I

HEALTH CARE REFORM CHECKLIST

HEALTH CARE REFORM CHECKLIST As a small employer, you need to be aware of the new regulations tied to the Affordable Care Act. Refer to this checklist to ensure you understand each one and that you re

HEALTH CARE REFORM CHECKLIST As a small employer, you need to be aware of the new regulations tied to the Affordable Care Act. Refer to this checklist to ensure you understand each one and that you re

The New Health Insurance Marketplace. Choices and Opportunities for Small Groups

The New Health Insurance Marketplace Choices and Opportunities for Small Groups What is the Affordable Care Act? The Patient Protection and Affordable Care Act (ACA) was signed into law on March 23, 2010

The New Health Insurance Marketplace Choices and Opportunities for Small Groups What is the Affordable Care Act? The Patient Protection and Affordable Care Act (ACA) was signed into law on March 23, 2010

Health Insurance Marketplace. vhealth insurance exchanges. What to expect in 2014. What to expect in 2014

vhealth insurance exchanges Health Insurance Marketplace What to expect in 2014 What to expect in 2014 The basics of exchanges As part of the Affordable Care Act (ACA or health care reform law), starting

vhealth insurance exchanges Health Insurance Marketplace What to expect in 2014 What to expect in 2014 The basics of exchanges As part of the Affordable Care Act (ACA or health care reform law), starting

The Vermont Health Benefit Exchange: An Update for Small Business Owners

The Vermont Health Benefit Exchange: An Update for Small Business Owners Today s Presentation Health Reform Goals Overview of Health Care Reform What is the Exchange? What Does the Exchange Look Like?

The Vermont Health Benefit Exchange: An Update for Small Business Owners Today s Presentation Health Reform Goals Overview of Health Care Reform What is the Exchange? What Does the Exchange Look Like?

Health Insurance Marketplace

Health Insurance Marketplace & Arkansas Health Connector Published by the City of Pine Bluff, Human Resources Department ** Federal Mandate ** The Affordable Care Act, a new healthcare law, requires that

Health Insurance Marketplace & Arkansas Health Connector Published by the City of Pine Bluff, Human Resources Department ** Federal Mandate ** The Affordable Care Act, a new healthcare law, requires that

David Lyons Founding Director and Chief Executive Officer

The New Health Insurance Marketplace Changes Impacting Small Employers and the SHOP Opportunity David Lyons Founding Director and Chief Executive Officer CoOportunity Health 10/1/2013 1 Why the Change?

The New Health Insurance Marketplace Changes Impacting Small Employers and the SHOP Opportunity David Lyons Founding Director and Chief Executive Officer CoOportunity Health 10/1/2013 1 Why the Change?

Health Insurance Marketplace 101 1

Affordable Care Act Coverage Accomplishments May 2013 3.1 million young adults have gained insurance through their parents plans 6.1 million people with Medicare through 2012 received $5.7 billion in prescription

Affordable Care Act Coverage Accomplishments May 2013 3.1 million young adults have gained insurance through their parents plans 6.1 million people with Medicare through 2012 received $5.7 billion in prescription

Health Care Reform Frequently Asked Questions (FAQ) Consumers Employers

Consumers Employers") This page provides answers to frequently asked questions (FAQ) regarding The Patient Protection and Affordable Care Act (PPACA; P.L. 111-148) and the Health Care and Education Reconciliation Act of 2010

This page provides answers to frequently asked questions (FAQ) regarding The Patient Protection and Affordable Care Act (PPACA; P.L. 111-148) and the Health Care and Education Reconciliation Act of 2010

Washington Health Benefit Exchange. Leading Age 2014 Annual Conference. Phil Dyer Board Member

Washington Health Benefit Exchange Leading Age 2014 Annual Conference Phil Dyer Board Member DISCLAIMER; The views and information expressed are my personal opinions and perspectives and do not represent

Washington Health Benefit Exchange Leading Age 2014 Annual Conference Phil Dyer Board Member DISCLAIMER; The views and information expressed are my personal opinions and perspectives and do not represent

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE Scott Walker, Governor Theodore K. Nickel, Commissioner Wisconsin.gov 125 South Webster Street P.O. Box 7873 Madison, Wisconsin 53707-7873 Phone:

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE Scott Walker, Governor Theodore K. Nickel, Commissioner Wisconsin.gov 125 South Webster Street P.O. Box 7873 Madison, Wisconsin 53707-7873 Phone:

Find health care options that meet your needs and fit your budget. ctober 2014

O Health Insurance Find health care options that meet your needs and fit your budget. ctober 2014 The Health Care Law In March 2010, President Obama signed the Affordable Care Act into law generally requiring

O Health Insurance Find health care options that meet your needs and fit your budget. ctober 2014 The Health Care Law In March 2010, President Obama signed the Affordable Care Act into law generally requiring

State Roles in Implementing Health Insurance Exchanges

State Roles in Implementing Health Insurance Exchanges By Alex Azarian August 2012 Principal Policy Analyst The Affordable Care Act (ACA) requires states to establish competitive insurance marketplaces,

State Roles in Implementing Health Insurance Exchanges By Alex Azarian August 2012 Principal Policy Analyst The Affordable Care Act (ACA) requires states to establish competitive insurance marketplaces,

The Effect of the Affordable Care Act on Your Small Business. Presented to : Greater Kansas City Chamber Business Class

The Effect of the Affordable Care Act on Your Small Business Presented to : Greater Kansas City Chamber Business Class November 6, 2013 KHN Kaiser Health News Current Headlines October 31- November 4,

The Effect of the Affordable Care Act on Your Small Business Presented to : Greater Kansas City Chamber Business Class November 6, 2013 KHN Kaiser Health News Current Headlines October 31- November 4,

The Affordable Care Act: What Does it Mean for Individuals and Families?

The Affordable Care Act: What Does it Mean for Individuals and Families? FIRM Team Fact Sheet 13-04 Available at http://www.firm.msue.msu.edu David B. Schweikhardt Adam J. Kantrovich Brenda R. Long Michigan

The Affordable Care Act: What Does it Mean for Individuals and Families? FIRM Team Fact Sheet 13-04 Available at http://www.firm.msue.msu.edu David B. Schweikhardt Adam J. Kantrovich Brenda R. Long Michigan

The Affordable Care Act: The Health Insurance Marketplace -- What Does It Mean for Individuals, Families, and Employers?

The Patient Protection and Affordable Care Act (ACA) includes provisions that will have significant implications for individuals, families and employers in 2014. These provisions include: The creation

The Patient Protection and Affordable Care Act (ACA) includes provisions that will have significant implications for individuals, families and employers in 2014. These provisions include: The creation

Nebraska Health Insurance Exchange Update

Nebraska Health Insurance Exchange Update Overview of the Affordable Care Act and the Federally Facilitated marketplace. September 2015 AFFORDABLE CARE ACT OVERVIEW» The Affordable Care Act was enacted

Nebraska Health Insurance Exchange Update Overview of the Affordable Care Act and the Federally Facilitated marketplace. September 2015 AFFORDABLE CARE ACT OVERVIEW» The Affordable Care Act was enacted

The Vermont Health Benefit Exchange: An Update

The Vermont Health Benefit Exchange: An Update Today s Discussion Health Reform Goals & Timeline Overview of Health Care Reform What is the Exchange? What Does the Exchange Look Like? Plan Design Enrollment

The Vermont Health Benefit Exchange: An Update Today s Discussion Health Reform Goals & Timeline Overview of Health Care Reform What is the Exchange? What Does the Exchange Look Like? Plan Design Enrollment

This glossary provides simple and straightforward definitions of key terms that are part of the health reform law.

This glossary provides simple and straightforward definitions of key terms that are part of the health reform law. A Affordable Care Act Also known as the ACA. A law that creates new options for people

This glossary provides simple and straightforward definitions of key terms that are part of the health reform law. A Affordable Care Act Also known as the ACA. A law that creates new options for people

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS. Vermont Edition

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS Vermont Edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM There s a constant stream of changes and updates related to health care reform,

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS Vermont Edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM There s a constant stream of changes and updates related to health care reform,

HEALTH BENEFIT EXCHANGE SURVIVAL GUIDE FOR SMALL BUSINESS. New York Edition

HEALTH BENEFIT EXCHANGE SURVIVAL GUIDE FOR SMALL BUSINESS New York Edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM PAGE 2 www.discovermvp.com There s a constant stream of changes and updates related

HEALTH BENEFIT EXCHANGE SURVIVAL GUIDE FOR SMALL BUSINESS New York Edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM PAGE 2 www.discovermvp.com There s a constant stream of changes and updates related

THE AFFORDABLE CARE ACT: THE AFFORDABLE COVERAGE OPTIONS AND CONSIDERATIONS IN 2014 THE NEW HEALTH INSURANCE: MARKETPLACE AND MEDICAID

THE AFFORDABLE CARE ACT: THE AFFORDABLE COVERAGE OPTIONS AND CONSIDERATIONS IN 2014 THE NEW HEALTH INSURANCE: MARKETPLACE AND MEDICAID Deloris Summers Deaf In-Person Counselor Navigator Jacksonville Area

THE AFFORDABLE CARE ACT: THE AFFORDABLE COVERAGE OPTIONS AND CONSIDERATIONS IN 2014 THE NEW HEALTH INSURANCE: MARKETPLACE AND MEDICAID Deloris Summers Deaf In-Person Counselor Navigator Jacksonville Area

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS. New York Edition

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS New York Edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM PAGE 2 www.discovermvp.com There s a constant stream of changes and updates related

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS New York Edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM PAGE 2 www.discovermvp.com There s a constant stream of changes and updates related

OVERVIEW OF PRIVATE INSURANCE MARKET REFORMS IN THE PATIENT PROTECTION AND AFFORDABLE CARE ACT AND RESOURCES FOR FREQUENTLY ASKED QUESTIONS

OVERVIEW OF PRIVATE INSURANCE MARKET REFORMS IN THE PATIENT PROTECTION AND AFFORDABLE CARE ACT AND RESOURCES FOR FREQUENTLY ASKED QUESTIONS Brief Prepared by MATTHEW COKE Senior Research Attorney LEGISLATIVE

OVERVIEW OF PRIVATE INSURANCE MARKET REFORMS IN THE PATIENT PROTECTION AND AFFORDABLE CARE ACT AND RESOURCES FOR FREQUENTLY ASKED QUESTIONS Brief Prepared by MATTHEW COKE Senior Research Attorney LEGISLATIVE

5Want to know more about the health

www. WHAT S INSIDE STEPS TO UNDERSTANDING OBAMACARE Introduction 4 Step 1 Does your current health insurance plan need to change? 6 Step 2 How will you pay for health insurance in 2014? 10 Step 3 What

www. WHAT S INSIDE STEPS TO UNDERSTANDING OBAMACARE Introduction 4 Step 1 Does your current health insurance plan need to change? 6 Step 2 How will you pay for health insurance in 2014? 10 Step 3 What

How To Get A Health Insurance Plan In Texas

Anticipating the Health Insurance Marketplace in Texas HFMA Lone Star Chapter Fall Institute September 16, 2013 1 About Community Health Choice Non-profit Health Maintenance Organization licensed by the

Anticipating the Health Insurance Marketplace in Texas HFMA Lone Star Chapter Fall Institute September 16, 2013 1 About Community Health Choice Non-profit Health Maintenance Organization licensed by the

Health Insurance Marketplaces

Health Insurance Marketplaces 2013 Zywave, Inc. All rights reserved. Presented by Employer Flexible What is Health Care Reform? The Affordable Care Act (ACA) was enacted in March 2010. Biggest overhaul

Health Insurance Marketplaces 2013 Zywave, Inc. All rights reserved. Presented by Employer Flexible What is Health Care Reform? The Affordable Care Act (ACA) was enacted in March 2010. Biggest overhaul

Health care reform for large businesses

FOR PRODUCERS AND EMPLOYERS Health care reform for large businesses A guide to what you need to know now DECEMBER 2013 CONTENTS 2 Introduction Since 2010 when the Affordable Care Act (ACA) was signed into

FOR PRODUCERS AND EMPLOYERS Health care reform for large businesses A guide to what you need to know now DECEMBER 2013 CONTENTS 2 Introduction Since 2010 when the Affordable Care Act (ACA) was signed into

SURVIVAL GUIDE FOR SMALL BUSINESS

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS New York edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM PAGE 2 www.discovermvp.com There s a constant stream of changes and updates related

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS New York edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM PAGE 2 www.discovermvp.com There s a constant stream of changes and updates related

HHealth HEALTH INSURANCE EXCHANGE FAQs

HHealth HEALTH INSURANCE EXCHANGE FAQs Page 1 TABLE OF CONTENTS Introduction... 3 Background... 3 Health Insurance Exchange FAQs... 4 What is the Patient Protection and Affordable Care Act (PPACA)?...

HHealth HEALTH INSURANCE EXCHANGE FAQs Page 1 TABLE OF CONTENTS Introduction... 3 Background... 3 Health Insurance Exchange FAQs... 4 What is the Patient Protection and Affordable Care Act (PPACA)?...

One of the more visible changes soon to be brought MONTANA S HEALTH INSURANCE A PREVIEW OF MARKETPLACE

A PREVIEW OF MONTANA S HEALTH INSURANCE MARKETPLACE by Gregg Davis and Christina Goe One of the more visible changes soon to be brought to the forefront by passage of the Affordable Care Act (ACA) is the

A PREVIEW OF MONTANA S HEALTH INSURANCE MARKETPLACE by Gregg Davis and Christina Goe One of the more visible changes soon to be brought to the forefront by passage of the Affordable Care Act (ACA) is the

The Affordable Care Act. President Obama signed the Affordable Care Act (ACA) into law on March 23, 2010.

into law on March 23, 2010.") The Affordable Care Act President Obama signed the Affordable Care Act (ACA) into law on March 23, 2010. The ACA was enacted to: v Increase quality and affordability of health insurance v Lower the uninsured

The Affordable Care Act President Obama signed the Affordable Care Act (ACA) into law on March 23, 2010. The ACA was enacted to: v Increase quality and affordability of health insurance v Lower the uninsured

HEALTH REFORM AND MULTIEMPLOYER PLAN COVERAGE 2014 AND BEYOND

WWW.BKLAWYERS.COM HEALTH REFORM AND MULTIEMPLOYER PLAN COVERAGE 2014 AND BEYOND ABA SECTION OF LABOR AND EMPLOYMENT LAW EMPLOYEE BENEFITS COMMITTEE MID- WINTER MEETING 201 BLITMAN & KING LLP Franklin Center,

WWW.BKLAWYERS.COM HEALTH REFORM AND MULTIEMPLOYER PLAN COVERAGE 2014 AND BEYOND ABA SECTION OF LABOR AND EMPLOYMENT LAW EMPLOYEE BENEFITS COMMITTEE MID- WINTER MEETING 201 BLITMAN & KING LLP Franklin Center,

AMERICAN HEALTH BENEFIT EXCHANGES

AMERICAN HEALTH BENEFIT EXCHANGES As we have previously reported, beginning January 1, 2014, the GHLIT will stop offering AVMA members medical insurance. However, members and small employers will be able

AMERICAN HEALTH BENEFIT EXCHANGES As we have previously reported, beginning January 1, 2014, the GHLIT will stop offering AVMA members medical insurance. However, members and small employers will be able

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE Scott Walker, Governor Theodore K. Nickel, Commissioner Wisconsin.gov 125 South Webster Street P.O. Box 7873 Madison, Wisconsin 53707-7873 Phone:

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE Scott Walker, Governor Theodore K. Nickel, Commissioner Wisconsin.gov 125 South Webster Street P.O. Box 7873 Madison, Wisconsin 53707-7873 Phone:

The Affordable Care Act: What Does It Mean for Self-Employed Individuals in Agriculture and Small Business?

FIRM Team Fact Sheet 13-03 Available at http://firm.msue.msu.edu David B. Schweikhardt Adam J. Kantrovich Brenda R. Long Michigan State University Extension October 2013 The Patient Protection and Affordable

FIRM Team Fact Sheet 13-03 Available at http://firm.msue.msu.edu David B. Schweikhardt Adam J. Kantrovich Brenda R. Long Michigan State University Extension October 2013 The Patient Protection and Affordable

An Overview of Arizona Enrollment in the Affordable Care Act (ACA) Marketplace. Presented by: Jaime Perikly, Health Choice

Marketplace. Presented by: Jaime Perikly, Health Choice") An Overview of Arizona Enrollment in the Affordable Care Act (ACA) Marketplace Presented by: Jaime Perikly, Health Choice Affordable Care Act The Patient Protection and Health Care Law of 2010, amended

An Overview of Arizona Enrollment in the Affordable Care Act (ACA) Marketplace Presented by: Jaime Perikly, Health Choice Affordable Care Act The Patient Protection and Health Care Law of 2010, amended

THE AFFORDABLE CARE ACT IN VIRGINIA --THE BASICS-- MARY FRANCES CHARLTON Attorney and ACA Coordinator LEGAL AID JUSTICE CENTER

THE AFFORDABLE CARE ACT IN VIRGINIA --THE BASICS-- MARY FRANCES CHARLTON Attorney and ACA Coordinator LEGAL AID JUSTICE CENTER Overview Affordable Care Act, aka Obamacare Goals Affordable Insurance Coverage

THE AFFORDABLE CARE ACT IN VIRGINIA --THE BASICS-- MARY FRANCES CHARLTON Attorney and ACA Coordinator LEGAL AID JUSTICE CENTER Overview Affordable Care Act, aka Obamacare Goals Affordable Insurance Coverage

SURVIVAL GUIDE FOR SMALL BUSINESS

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS Vermont edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM There s a constant stream of changes and updates related to health care reform,

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS Vermont edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM There s a constant stream of changes and updates related to health care reform,

to Health Care Reform

The Employer s Guide to Health Care Reform What you need to know now to: Consider your choices Decide what s best for you Follow the rules 2013-2014 Health care reform is the law of the land. Some don

The Employer s Guide to Health Care Reform What you need to know now to: Consider your choices Decide what s best for you Follow the rules 2013-2014 Health care reform is the law of the land. Some don

The Impact of Health Care Reform on Community Health Centers in Colorado. Kristen Pieper Policy Manager Colorado Community Health Network

The Impact of Health Care Reform on Community Health Centers in Colorado Kristen Pieper Policy Manager Colorado Community Health Network Presentation Topics Background information on CCHN, Colorado CHCs,

The Impact of Health Care Reform on Community Health Centers in Colorado Kristen Pieper Policy Manager Colorado Community Health Network Presentation Topics Background information on CCHN, Colorado CHCs,

The Health Insurance Marketplace

The Health Insurance Marketplace An Overview of Arizona Enrollment in Medicaid and the Marketplace: Health-e-Arizona Plus update Rural Health Webinar August 7, 2013 What is the Affordable Care Act? The

The Health Insurance Marketplace An Overview of Arizona Enrollment in Medicaid and the Marketplace: Health-e-Arizona Plus update Rural Health Webinar August 7, 2013 What is the Affordable Care Act? The

Health Reform Changes: What s New for 2014? New Hampshire Insurance Department September 11, 2013

Health Reform Changes: What s New for 2014? New Hampshire Insurance Department September 11, 2013 1 New Hampshire Insurance Department Presentation Overview What s New in 2014 Key Questions for Individuals

Health Reform Changes: What s New for 2014? New Hampshire Insurance Department September 11, 2013 1 New Hampshire Insurance Department Presentation Overview What s New in 2014 Key Questions for Individuals

The New Healthcare Law and Its Impact on Small Business

U. S. Small Business Administration Washington Metropolitan Area District Office The New Healthcare Law and Its Impact on Small Business Julie C. Verratti Advisor U.S. Small Business Administration Julie.Verratti@sba.gov

U. S. Small Business Administration Washington Metropolitan Area District Office The New Healthcare Law and Its Impact on Small Business Julie C. Verratti Advisor U.S. Small Business Administration Julie.Verratti@sba.gov

Effective dates for provisions of the PPACA are spread out from 2010 through 2018. This document focuses on 2013 and 2014.

As part of our ongoing initiative to provide added value to our customers, this health care reform summary is being provided on an information only basis. This is NOT a legal document and is not intended

As part of our ongoing initiative to provide added value to our customers, this health care reform summary is being provided on an information only basis. This is NOT a legal document and is not intended

GLOSSARY OF KEY HEALTH INSURANCE CONCEPTS

The Affordable Care Act: A Working Guide for MCH Professionals Module 2 GLOSSARY OF KEY HEALTH INSURANCE CONCEPTS Overview A fundamental first step in accessing health care in the United States is having

The Affordable Care Act: A Working Guide for MCH Professionals Module 2 GLOSSARY OF KEY HEALTH INSURANCE CONCEPTS Overview A fundamental first step in accessing health care in the United States is having

Health Policy Essentials: Private Health Insurance. Bernadette Fernandez, Annie Mach, & Namrata Uberoi February 13, 2015

Health Policy Essentials: Private Health Insurance Bernadette Fernandez, Annie Mach, & Namrata Uberoi February 13, 2015 Briefing Agenda What is the purpose of private health insurance (PHI)? How is PHI

Health Policy Essentials: Private Health Insurance Bernadette Fernandez, Annie Mach, & Namrata Uberoi February 13, 2015 Briefing Agenda What is the purpose of private health insurance (PHI)? How is PHI

Fact Sheet. AARP Public Policy Institute. Health Reform Changes Insurance Rules

Fact Sheet Health Reform Changes Insurance Rules The Affordable Care Act (ACA) will greatly increase the availability of health insurance and broadly impact the delivery of health care in America. This

Fact Sheet Health Reform Changes Insurance Rules The Affordable Care Act (ACA) will greatly increase the availability of health insurance and broadly impact the delivery of health care in America. This

What s in the Healthcare Law for you and your Business

What s in the Healthcare Law for you and your Business How the new law impacts your bottom line Marcia Dávalos Disneyland Hotel - Anaheim, CA October 17, 2013 About Small Business Majority Small business

What s in the Healthcare Law for you and your Business How the new law impacts your bottom line Marcia Dávalos Disneyland Hotel - Anaheim, CA October 17, 2013 About Small Business Majority Small business

THE KANSAS AFFORDABLE CARE ACT IMPLEMENTATION. Linda J. Sheppard November 6, 2014

THE KANSAS AFFORDABLE CARE ACT IMPLEMENTATION Linda J. Sheppard November 6, 2014 The Kansas Market Approximately 348,000 Kansans are uninsured - 12.3% of the state s population 44,130 are children, but

THE KANSAS AFFORDABLE CARE ACT IMPLEMENTATION Linda J. Sheppard November 6, 2014 The Kansas Market Approximately 348,000 Kansans are uninsured - 12.3% of the state s population 44,130 are children, but

Presented by South Dakota Community Action Partnership

Presented by South Dakota Community Action Partnership The project described was supported by Funding Opportunity Number CA-NAV-13-001 from the U.S Department of Health and Human Services, Centers for

Presented by South Dakota Community Action Partnership The project described was supported by Funding Opportunity Number CA-NAV-13-001 from the U.S Department of Health and Human Services, Centers for

It goes by many names: Patient Protection and Affordable Care Act (PPACA) or ACA or Obama Care or simply Healthcare Reform.

or ACA or Obama Care or simply Healthcare Reform.") WHAT IS HEALTHCARE REFORM? Healthcare Reform (HCR) is a law passed by Congress that provides many different requirements. A very important aspect of the law is that it is designed to provide individuals

WHAT IS HEALTHCARE REFORM? Healthcare Reform (HCR) is a law passed by Congress that provides many different requirements. A very important aspect of the law is that it is designed to provide individuals

HEALTH INSURANCE EXCHANGE FAQS

HEALTH INSURANCE EXCHANGE FAQS 0 TABLE OF CONTENTS INTRODUCTION... 1 BACKGROUND... 1 HEALTH INSURANCE EXCHANGE FAQS... 1 1 INTRODUCTION IN EARLY 2010, CONGRESS PASSED THE PATIENT PROTECTION AND AFFORDABLE

HEALTH INSURANCE EXCHANGE FAQS 0 TABLE OF CONTENTS INTRODUCTION... 1 BACKGROUND... 1 HEALTH INSURANCE EXCHANGE FAQS... 1 1 INTRODUCTION IN EARLY 2010, CONGRESS PASSED THE PATIENT PROTECTION AND AFFORDABLE

The Affordable Care Act in New Hampshire

The State of New Hampshire Insurance Department 21 South Fruit Street, Suite 14 Concord, NH 03301 (603) 271-2261 Fax (603) 271-1406 TDD Access: Relay NH 1-800-735-2964 The Affordable Care Act in New Hampshire

The State of New Hampshire Insurance Department 21 South Fruit Street, Suite 14 Concord, NH 03301 (603) 271-2261 Fax (603) 271-1406 TDD Access: Relay NH 1-800-735-2964 The Affordable Care Act in New Hampshire

THE HEALTH INSURANCE MARKETPLACE

THE HEALTH INSURANCE MARKETPLACE Presented by Raffa Financial Services Source: Centers for Medicare & Medicaid Services Design 2013 Zywave, Inc. All rights reserved. OBJECTIVES This session will help you:

THE HEALTH INSURANCE MARKETPLACE Presented by Raffa Financial Services Source: Centers for Medicare & Medicaid Services Design 2013 Zywave, Inc. All rights reserved. OBJECTIVES This session will help you:

How The Affordable Care Act will Affect You and Your Business. Logo

How The Affordable Care Act will Affect You and Your Business. AFFORDABLE CARE ACT (ACA) DISCLOSURE The information provided is to be used as a guide. Since the ACA is still a work in progress, changes

How The Affordable Care Act will Affect You and Your Business. AFFORDABLE CARE ACT (ACA) DISCLOSURE The information provided is to be used as a guide. Since the ACA is still a work in progress, changes

TO UNDERSTANDING THE AFFORDABLE CARE ACT

3 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 20 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT

3 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT What s Inside Step 1: What Understand what you re buying 4 Step 2: How How can you buy health insurance? 20 STEPS TO UNDERSTANDING THE AFFORDABLE CARE ACT

HEALTH INSURANCE MARKETPLACES FACT SHEET

HEALTH INSURANCE MARKETPLACES FACT SHEET INFORMED ON REFORM Overview A Health Insurance Marketplace, also known as a Health Insurance Exchange, is available in every state as a public option for individuals

HEALTH INSURANCE MARKETPLACES FACT SHEET INFORMED ON REFORM Overview A Health Insurance Marketplace, also known as a Health Insurance Exchange, is available in every state as a public option for individuals

Update. Director of Policy and National Health Care Reform Coordinator. Roni Mansur Chief Operating Officer. Board of Directors Meeting March 8, 2012

National Health Care Reform Update Kaitlyn Kenney Director of Policy and National Health Care Reform Coordinator Roni Mansur Chief Operating Officer Board of Directors Meeting March 8, 2012 Agenda Update

National Health Care Reform Update Kaitlyn Kenney Director of Policy and National Health Care Reform Coordinator Roni Mansur Chief Operating Officer Board of Directors Meeting March 8, 2012 Agenda Update

The Patient Protection and Affordable Care Act What Employers need to know

The Patient Protection and Affordable Care Act What Employers need to know Presented by: Misty Baker mbake@iiat.org 800-880-7428 This update is based on the known provisions of the PPACA. This is not to

The Patient Protection and Affordable Care Act What Employers need to know Presented by: Misty Baker mbake@iiat.org 800-880-7428 This update is based on the known provisions of the PPACA. This is not to

Health Insurance Marketplace 101. Find health care options that meet your needs and fit your budget.

Health Insurance Marketplace 101 Find health care options that meet your needs and fit your budget. March 2014 The Health Care Law In March 2010, President Obama signed the Affordable Care Act into law

Health Insurance Marketplace 101 Find health care options that meet your needs and fit your budget. March 2014 The Health Care Law In March 2010, President Obama signed the Affordable Care Act into law

Understanding the Impact of Health Care Reform

Understanding the Impact of Health Care Reform Esteban López, MD, MBA Regional President Disclaimer: The content contained within this presentation is for general informational purposes only and does not

Understanding the Impact of Health Care Reform Esteban López, MD, MBA Regional President Disclaimer: The content contained within this presentation is for general informational purposes only and does not

Guide to Health Care Reform

Guide to Health Care Reform 2 0 1 5 Navigating the changing landscape The first year of health care reform may be over but it may have left you with more questions than ever. You probably want to know

Guide to Health Care Reform 2 0 1 5 Navigating the changing landscape The first year of health care reform may be over but it may have left you with more questions than ever. You probably want to know

AFFORDABLE CARE ACT AND MAINE S HEALTH INSURANCE MARKET

1 AFFORDABLE CARE ACT AND MAINE S HEALTH INSURANCE MARKET 2 Source: Social Security Advisory Board, 2009 Where We Are Today: Nationally 4 MAINE S HEALTH INSURANCE MARKET 5 Mainers with Health Coverage

1 AFFORDABLE CARE ACT AND MAINE S HEALTH INSURANCE MARKET 2 Source: Social Security Advisory Board, 2009 Where We Are Today: Nationally 4 MAINE S HEALTH INSURANCE MARKET 5 Mainers with Health Coverage

Review of Market Rules for the Commercial Market

Review of Market Rules for the Commercial Market What Makes up the Commercial Market? Individual Market Through MNSure and from carriers directly ( Off-Exchange ) Small Group Market Through MNSure s SHOP

Review of Market Rules for the Commercial Market What Makes up the Commercial Market? Individual Market Through MNSure and from carriers directly ( Off-Exchange ) Small Group Market Through MNSure s SHOP

AFFORDABLE CARE ACT FAQ

AFFORDABLE CARE ACT FAQ What is the Healthcare Insurance Marketplace? The Marketplace is a new way to find quality health coverage. It can help if you don t have coverage now or if you have it but want

AFFORDABLE CARE ACT FAQ What is the Healthcare Insurance Marketplace? The Marketplace is a new way to find quality health coverage. It can help if you don t have coverage now or if you have it but want

MODULE 16: MEDICARE AND THE HEALTH INSURANCE MARKETPLACES

MODULE 16: MEDICARE AND THE HEALTH INSURANCE MARKETPLACES Objective This module will educate HIICAP counselors about how Medicare is affected (and not affected) by the health insurance Marketplaces. What

MODULE 16: MEDICARE AND THE HEALTH INSURANCE MARKETPLACES Objective This module will educate HIICAP counselors about how Medicare is affected (and not affected) by the health insurance Marketplaces. What

PPACA/Healthcare Reform CHANGES

PPACA/Healthcare Reform CHANGES beginning in 2014 for small employers A guide to understanding the administrative provisions, benefit changes, new taxes and credits, market reforms and purchasing options

PPACA/Healthcare Reform CHANGES beginning in 2014 for small employers A guide to understanding the administrative provisions, benefit changes, new taxes and credits, market reforms and purchasing options

American Health Benefit Exchanges Fact Sheet A Provision of the Patient Protection and Affordable Care Act (PPACA)

") American Health Benefit Exchanges Fact Sheet A Provision of the Patient Protection and Affordable Care Act (PPACA) This Fact Sheet reflects the Final Ruling published by the Department of Health and Human

American Health Benefit Exchanges Fact Sheet A Provision of the Patient Protection and Affordable Care Act (PPACA) This Fact Sheet reflects the Final Ruling published by the Department of Health and Human

The Health Benefit Exchange and the Commercial Insurance Market

The Health Benefit Exchange and the Commercial Insurance Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges, that

The Health Benefit Exchange and the Commercial Insurance Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges, that

The Affordable Care Act (ACA) in Wisconsin

in Wisconsin") The Affordable Care Act (ACA) in Wisconsin Caroline B. Gomez, MSW, Healthcare Outreach Specialist, Covering Kids & Families, Healthcare Outreach Specialist Nancy Crevier, Marinette County Family Living

The Affordable Care Act (ACA) in Wisconsin Caroline B. Gomez, MSW, Healthcare Outreach Specialist, Covering Kids & Families, Healthcare Outreach Specialist Nancy Crevier, Marinette County Family Living

Health Reform and the AAP: What the New Law Means for Children and Pediatricians

Health Reform and the AAP: What the New Law Means for Children and Pediatricians Throughout the health reform process, the American Academy of Pediatrics has focused on three fundamental priorities for

Health Reform and the AAP: What the New Law Means for Children and Pediatricians Throughout the health reform process, the American Academy of Pediatrics has focused on three fundamental priorities for

The Health Insurance Marketplace 101. July 2013

The July 2013 The Problem Insurance companies could turn away the 129 million Americans with pre-existing conditions Premiums had more than doubled over the last decade, while insurance company profits

The July 2013 The Problem Insurance companies could turn away the 129 million Americans with pre-existing conditions Premiums had more than doubled over the last decade, while insurance company profits

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE Scott Walker, Governor Theodore K. Nickel, Commissioner Wisconsin.gov 125 South Webster Street P.O. Box 7873 Madison, Wisconsin 53707-7873 Phone:

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE Scott Walker, Governor Theodore K. Nickel, Commissioner Wisconsin.gov 125 South Webster Street P.O. Box 7873 Madison, Wisconsin 53707-7873 Phone:

A Consumer s Guide to the Affordable Care Act

A Consumer s Guide to the Affordable Care Act The Affordable Care Act was designed to help make health care affordable for everyone. This guide will help you understand how the ACA affects individuals

A Consumer s Guide to the Affordable Care Act The Affordable Care Act was designed to help make health care affordable for everyone. This guide will help you understand how the ACA affects individuals

Introduction. Affordable Care Act Overview of Changes

Introduction Affordable Care Act Overview of Changes Presented by: Tim Dillingham, CLU Benefit Resource Group, Inc. 201 E Broad Street, Suite 1 Linden, MI 48451 810-735-6500 810-735-6610 (fax) tim@benefitresourcegroup.net

Introduction Affordable Care Act Overview of Changes Presented by: Tim Dillingham, CLU Benefit Resource Group, Inc. 201 E Broad Street, Suite 1 Linden, MI 48451 810-735-6500 810-735-6610 (fax) tim@benefitresourcegroup.net

Simple answers to health reform s complex issues facing every employer, and what you can do now to protect your business and your future.

Simple answers to health reform s complex issues facing every employer, and what you can do now to protect your business and your future. If you have any questions, please contact: Health Reform: A Guide

Simple answers to health reform s complex issues facing every employer, and what you can do now to protect your business and your future. If you have any questions, please contact: Health Reform: A Guide

The Affordable Care Act and American Indian and Alaska Natives. Frequently Asked Questions

The Affordable Care Act and American Indian and Alaska Natives Frequently Asked Questions 1. Is IHS coverage going away under the Affordable Care Act? No. The IHS, Tribal and urban Indian health programs

The Affordable Care Act and American Indian and Alaska Natives Frequently Asked Questions 1. Is IHS coverage going away under the Affordable Care Act? No. The IHS, Tribal and urban Indian health programs

SHIBA. Statewide Health Insurance Benefits Advisors. Medicare, Health Insurance, & the Affordable Care Act Updates for Summer 2013

SHIBA Statewide Health Insurance Benefits Advisors Medicare, Health Insurance, & the Affordable Care Act Updates for Summer 2013 Liz Mercer Regional Trainer Sponsored by the: 8/8/2013 1 Today s overview

SHIBA Statewide Health Insurance Benefits Advisors Medicare, Health Insurance, & the Affordable Care Act Updates for Summer 2013 Liz Mercer Regional Trainer Sponsored by the: 8/8/2013 1 Today s overview

The Affordable Care Act and People with Disabilities

The Affordable Care Act and People with Disabilities The Arc of Texas envisions a world where people with disabilities are included in their communities and neighborhoods and where quality supports and

The Affordable Care Act and People with Disabilities The Arc of Texas envisions a world where people with disabilities are included in their communities and neighborhoods and where quality supports and

HCR 101: Your Guide to Understanding Healthcare Reform

HCR 101: Your Guide to Understanding Healthcare Reform Are You Ready for Healthcare Reform? By now, you ve probably been hearing a lot about the Affordable Care Act (also known as healthcare reform or

HCR 101: Your Guide to Understanding Healthcare Reform Are You Ready for Healthcare Reform? By now, you ve probably been hearing a lot about the Affordable Care Act (also known as healthcare reform or

Health Care Reform: Policy Implications for the Future

Health Care Reform: Policy Implications for the Future Michigan Primary Care Association Douglas M. Paterson, MPA Director of State Policy Promoting, supporting, and developing comprehensive, accessible,

Health Care Reform: Policy Implications for the Future Michigan Primary Care Association Douglas M. Paterson, MPA Director of State Policy Promoting, supporting, and developing comprehensive, accessible,

The ACA and Healthcare Exchanges

The ACA and Healthcare Exchanges 1 Key Healthcare Exchange Dates April 12, 2012 - Governor Cuomo issued Executive Order #42 to establish Exchanges. December 14, 2012 - New York Receives Conditional Approval

The ACA and Healthcare Exchanges 1 Key Healthcare Exchange Dates April 12, 2012 - Governor Cuomo issued Executive Order #42 to establish Exchanges. December 14, 2012 - New York Receives Conditional Approval

How the Affordable Care Act Affects Medical Support Orders in Oklahoma Frequently Asked Questions Spring, 2014 1

How the Affordable Care Act Affects Medical Support Orders in Oklahoma Frequently Asked Questions Spring, 2014 1 General 1. Did Oklahoma expand Medicaid? No, Oklahoma did not expand Medicaid. 2. Who is

How the Affordable Care Act Affects Medical Support Orders in Oklahoma Frequently Asked Questions Spring, 2014 1 General 1. Did Oklahoma expand Medicaid? No, Oklahoma did not expand Medicaid. 2. Who is

AFFORDABLE CARE ACT LARGE EMPLOYER HEALTH REFORM CHECKLIST. Edition: October 2015

AFFORDABLE CARE ACT Employers that offer health care coverage to employees are responsible for complying with many of the provisions of the Affordable Care Act (ACA). Most health reform changes apply regardless

AFFORDABLE CARE ACT Employers that offer health care coverage to employees are responsible for complying with many of the provisions of the Affordable Care Act (ACA). Most health reform changes apply regardless