The Office of the State Comptroller (OSC) has identified a flaw in the administration of

|

|

|

- Mitchell Nash

- 8 years ago

- Views:

Transcription

1

2

3 I. Introduction The Office of the State Comptroller (OSC) has identified a flaw in the administration of the Homestead Property Tax Credit program which, if corrected, has the potential to save the State millions of dollars every year. Under this program, certain homeowners are eligible for a reduction to their property taxes. However, this benefit is reduced when the homeowner does not occupy 100 percent of a multi-unit property. For example, the owner of a two-family home who occupies only one of two equally sized units would be entitled to 50 percent of the total Homestead Property Tax Credit. We have determined that the administrator of this program, New Jersey s Division of Taxation (Taxation), currently has no reliable way of verifying the percentage of property that is actually occupied by the program s applicants. While information pertaining to the number of units in a property is readily available locally, it is not required to be reported to Taxation. By simply requiring this information to be reported, Taxation can easily verify the accuracy of a homeowner s representation and could potentially prevent the State from losing millions of dollars. OSC, in fact, utilized such existing information to identify a significant number of homeowners who have incorrectly reported occupying 100 percent of a property, and thus, improperly received the full Homestead Property Tax Credit. OSC has additionally identified two other property tax relief programs that share the same flaw, which can similarly be corrected, potentially saving the State millions of additional dollars. At the conclusion of this report we offer specific recommendations to address the flaw we have identified in these three programs. We also are referring the names of the individuals we have identified as having improperly received a property tax benefit to Taxation for appropriate action. 1

4 II. Background A. Tax Relief Benefit Programs 1. Homestead Property Tax Credit The Homestead Property Tax Credit ( homestead credit ) is provided pursuant to the Homestead Property Tax Credit Act, N.J.S.A. 54: to The Legislature first provided for homestead rebates in 1976 to provide property tax relief to homeowners, first in the form of a rebate check and currently in the form of a credit that reduces total property tax obligations. New Jersey residents who own and occupy a home in New Jersey and meet certain criteria are eligible for this benefit, provided their property taxes were paid for that year and they meet certain income limits. In recent years the income limit has been $150,000 for homeowners aged 65 or older or who are blind or disabled; for homeowners under age 65 and not blind or disabled, the income limit has been $75,000. In 2011, approximately 2,500,000 properties were initially identified by Taxation as eligible to receive the homestead credit. Utilizing a data processing system called MOD-IV and other databases, Taxation prequalified certain residents for the homestead credit and removed from the list those taxpayers who were ineligible to receive the benefit e.g., those who exceed the maximum income limit or who are delinquent in paying their property taxes. Ultimately, for tax year 2011, Taxation sent out approximately 1,600,000 homestead credit applications and approximately 843,000 taxpayers received the credit for that year. The total amount of benefits paid out for tax year 2011 was $395,506,069. Most 2011 benefits were paid to municipalities to apply as a credit to homeowners property tax bills in August The average benefit amount for seniors and disabled homeowners was $515, while the average benefit amount for all other homeowners making less than $75,000 was $405. 2

5 Similar to what occurred for the 2011 homestead credit, the benefit for 2012 is being carried forward into a later tax year. In this case, the 2012 homestead credit will be applied to May 2015 property tax bills. It is expected that average 2012 benefits will roughly mirror those paid out for The Legislature has appropriated $395.2 million for this program in fiscal year Property Tax Reimbursement The Property Tax Reimbursement program, also known as the Senior and Disabled Person s Freeze Act, is an additional program authorized pursuant to N.J.S.A. 54: to This program reimburses senior citizens and disabled persons who meet certain eligibility criteria for property tax increases to their principal residence. From 2009 to 2013, an applicant s annual income could not exceed $70,000 to be eligible for the benefit. The amount of the reimbursement, which is paid in the form of a check, is based on the difference between the property taxes due and paid for the current year and the property taxes due and paid for the first year the applicant met all the eligibility requirements for the program. According to State figures, the average property tax reimbursement for the 2011 tax year was $1,173 per recipient. For fiscal year 2015, the Legislature has appropriated $203.1 million for the property tax reimbursement program. 3. Property Tax Deduction The Property Tax Deduction is authorized by the Property Tax Deduction Act, N.J.S.A. 54A:3A-15 to -22. Under this Act, eligible homeowners and tenants who pay property taxes on their principal residence in New Jersey, either directly or through rent, may qualify for either a tax deduction of up to $10,000 or a refundable credit. This benefit reduces gross income if the taxpayer takes the deduction. For example, a homeowner with $95,000 in gross income can 3

6 deduct the $7,850 he pays in property taxes on his one-unit principal residence from his gross income, thereby yielding an income tax savings of $436. The Legislature has appropriated $542.5 million for the tax deduction benefit program for fiscal year B. Benefit Standards The Homestead Property Tax Credit Act limits the benefit to a homestead that is used as a principal residence. N.J.S.A. 54: to The term homestead is defined, in relevant part, as a dwelling house and the land on which that dwelling house is located. N.J.S.A. 54: Dwelling house is any residential property with four or fewer units, but only one of the units can be used for commercial purposes, and certain types of properties are excluded, such as condominiums. Ibid. To qualify as a principal residence the property must be actually and continually occupied by an applicant as his or her permanent residence, as distinguished from a vacation home, property owned and rented or offered for rent by the claimant, and other secondary real property holdings. Ibid. For multi-unit homesteads, the Act allows only for a homestead credit in an amount that is proportionate to the share of the property taxes assessed and levied against the residential unit occupied as a principal residence. See N.J.S.A. 54:4-8.59(d). The legislation authorizing both the property tax reimbursement and deduction contain similar terms and definitions as used in the legislation for the homestead credit and thus, the percentage of the property that an applicant occupies similarly determines the amount of benefit he or she should receive. Each tax benefit program (homestead credit, property tax reimbursement and property tax deduction) is considered to be a tax preference provision... not to be construed liberally, but instead... strictly interpreted against those claiming the preference. See generally Allied Textile Printers Corp. v. Director of Taxation, 145 N.J. Super. 4

7 456, 461 (App. Div. 1976), certif. denied, 74 N.J. 271 (1977); Vavoulakis v. Director, Div. of Taxation, 12 N.J. Tax 318, 328 (Tax 1992), aff'd, 13 N.J. Tax 322 (App. Div. 1993). In other words, the programs eligibility standards are to be closely followed and firmly enforced. III. Methodology Our investigation began with a complaint alleging that eight homeowners in the Town of Kearny were receiving a larger homestead credit than they were otherwise entitled to because a portion of their multi-unit primary residence was occupied by other tenants. Taxation confirmed that each property owner received 100 percent of the homestead credit for 2011, and information requested from the Kearny tax assessor generally corroborated the complainant s allegations. In order to ascertain whether this was occurring on a statewide basis, we collaborated with Taxation to develop search parameters to aid in identifying other homeowners receiving excess benefits. After excluding residences with multiple filers with the same last name, we focused on properties with two characteristics: Properties receiving 100 percent of the homestead credit in 2011; and Properties with addresses that were listed on more than one State tax return. This search yielded a list of approximately 65,000 addresses (larger list). We refined the search further by extracting from the larger list those properties with secondary address information such as apartment or floor number because it was more likely that such properties contained multiple units. That further refinement yielded a list of over 4,700 addresses (smaller list). We interviewed a municipal tax assessor, a county tax administrator and vendors for Taxation s and tax assessors data collection systems to determine what property tax information is captured by municipal tax assessors and how much of it is being reported to Taxation. We 5

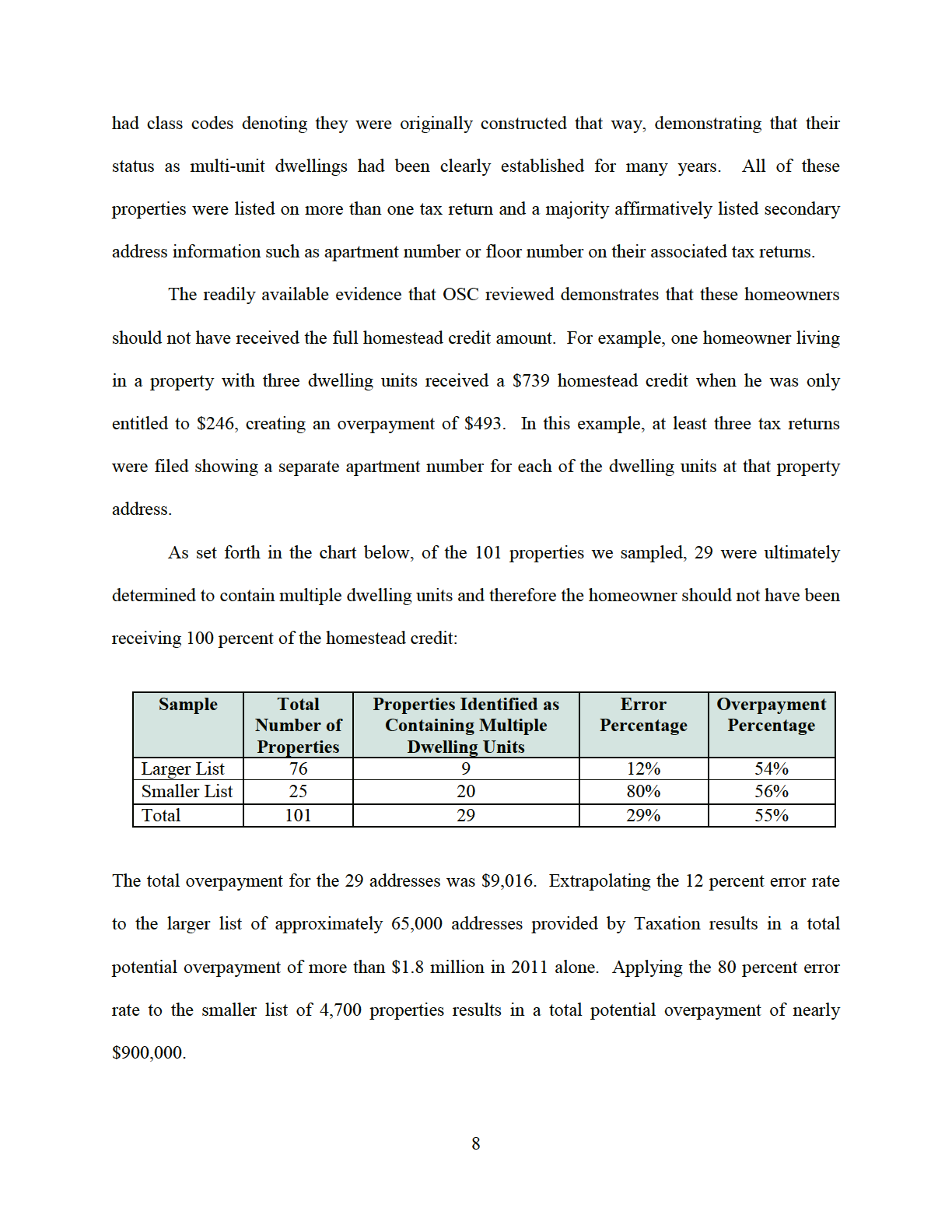

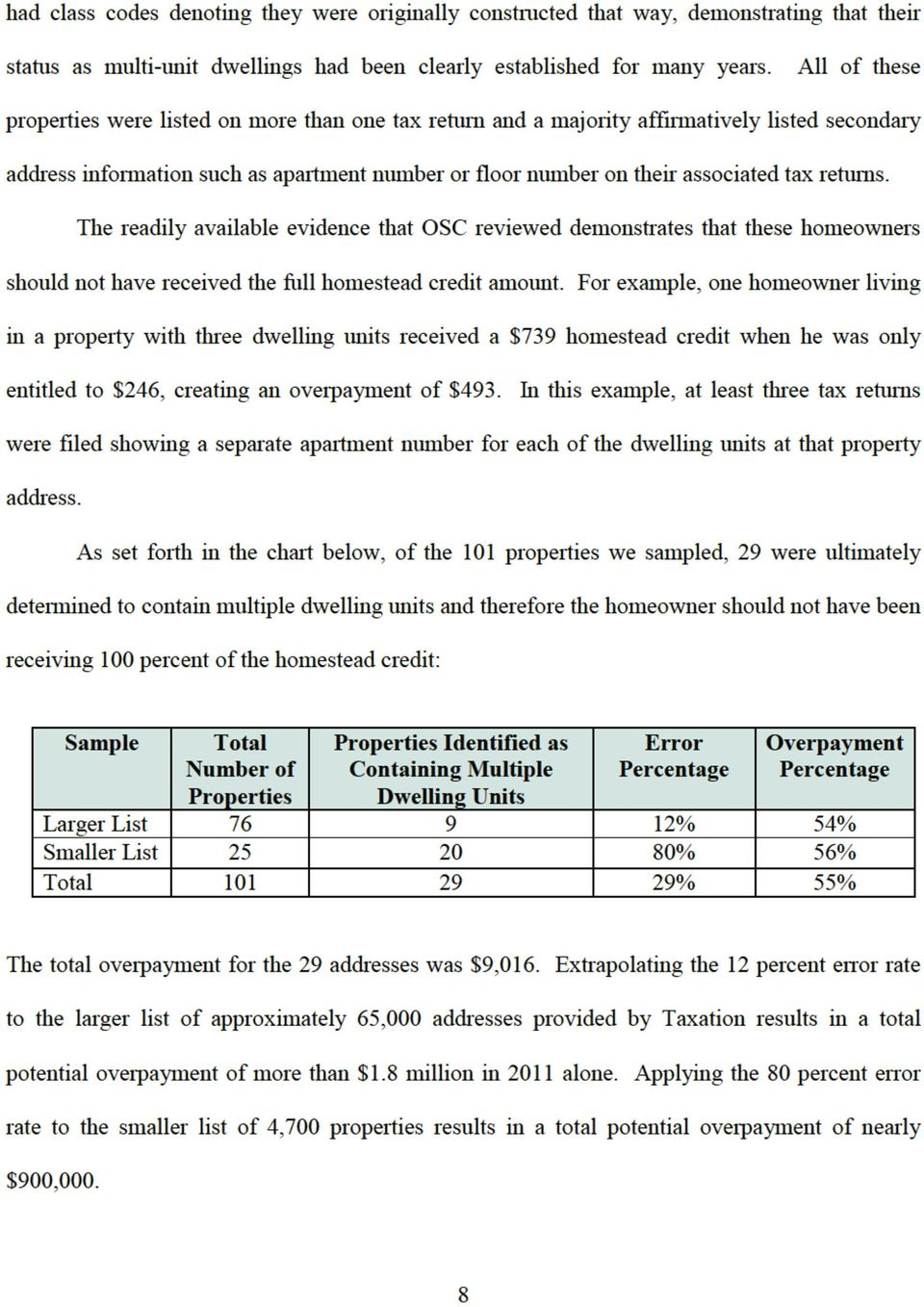

8 then took a random sample of 25 addresses from the smaller list and, to be as comprehensive as possible, we also randomly selected 76 addresses from the larger list, for a total of 101 unique properties for further review. We then requested information from Taxation and from the municipal tax assessors for these 101 properties. Finally, we interviewed Taxation officials to determine whether a potential solution to the deficiency we uncovered was feasible. We sent a draft of this report to Taxation, a vendor for the data collection system, the Kearny tax assessor and another municipal tax assessor who provided background for the report. The responses we received were considered in preparing this final report and were incorporated herein where appropriate. IV. Findings A. Multiple Unit Information is Regularly Recorded at the Local Level Municipal tax assessors should continuously record and maintain individual property data including the type, use and number of dwelling units within a property. This information is used to aid assessors in determining the complete and accurate value of each parcel of real property within a municipality. Many tax assessors record this information on documents known as property record cards. Tax assessors may also record the information in a computer software program called the Computer Assisted Mass Appraisal (CAMA) system, which can produce a computer generated property record card. OSC was told the information recorded in the property record cards, CAMA system or other local records includes the number of units within a property. The Real Property Appraisal Manual for New Jersey Assessors provides a coding system for tax assessors to classify residential structures. Different building class codes exist for single 6

9 family and multi-family residential dwellings from two to four units. These codes are also regularly inputted into the property record cards and CAMA. Thus, information regarding the number of dwelling units within a property is normally noted by tax assessors and generally can be found in property record cards, the CAMA system or other local record. B. Inappropriate Award of Property Tax Credit OSC was able to use the available data collected by local tax assessors to identify properties that contained multiple dwelling units. Information from the Kearny tax assessor listed the number of units within the properties and corroborated the allegation that seven of the eight addresses from the original complaint were multi-unit dwellings in These seven homeowners received a total of $5,485 in homestead credit benefits for 2011 when they were only entitled to $2,588 based on the number of dwelling units in their residences, creating an overpayment of $2,897. Specific examples of these overpayments included one homeowner with a property containing three dwelling units who received the full homestead credit of $925 for his property when, in fact, he was only entitled to receive a homestead credit of $308, resulting in an excess benefit of $616. Two other homeowners with two-unit properties received excess homestead credit amounts of $376 and $424, respectively. The address for each of the seven properties was listed on more than one tax return and there was secondary address information listed on tax forms associated with each property. In all, the seven homeowners were apparently overpaid by approximately 53 percent. As for the 101 properties selected for further review, a significant number had property record cards clearly showing they contained multiple units. In fact, a majority of such properties 7

10

11 For 23 of the 29 properties, the municipal assessor had filled out one or both of two fields (number of dwelling units and building class code) on the property record card that would definitively establish the multi-unit status of those properties. Five of the remaining six properties had property record cards suggesting the existence of multiple units, such as multiple kitchens in addition to multiple structures, living rooms and/or dining rooms. We later confirmed the existence of multiple units within these properties from other public information. 1 Thus, 28 of the 29 property record cards contained information showing multiple units within the property. C. Local Tax Assessors Could Easily Provide Multiple Unit Information to Taxation As noted, information pertaining to the number of units within a property is regularly collected by municipal tax assessors and largely available in property record cards or the CAMA system. These tax assessors are already required to annually report certain information to Taxation and with limited effort they could similarly report on the number of units within a property. Specifically, municipal tax assessors are already required to file information with Taxation showing the assessed value of each property in a municipality. In order to meet that requirement, assessors input certain information into Taxation s MOD-IV system. MOD-IV records a snapshot in time of certain information which Taxation has deemed to be relevant to fulfill its statutory obligations. As such, it contains some but not all of the information relating to a parcel of property that must be maintained by the municipal tax assessor. Taxation has not required assessors to record the number of dwelling units and building class code for each property in the MOD-IV system. 1 According to the tax assessor, one additional property has an illegal apartment above the garage that was not reflected on the property record card. 9

12 The feasibility of making the number of dwelling units and building class fields mandatory in MOD-IV was discussed with the Taxation official responsible for statewide property tax administration. This official told us that making these fields mandatory and requiring the local assessors to populate these fields would not be an issue. In fact, some assessors have voluntarily added this information to the MOD-IV database. The official stated that Taxation would be willing to add the number of dwelling units and building class fields to the list of mandatory fields required to be filled out in MOD-IV. Additionally, multiple unit information that has already been uploaded to the CAMA system could potentially be automatically transferred to Taxation s MOD-IV system. One vendor that we spoke with reported that a program to automatically transfer such information from CAMA to matching fields in MOD-IV is already in existence. The Taxation official told us that she would assess whether the other MOD-IV vendors could similarly transfer the data from the CAMA system. She further told us that her staff could also aid the tax assessors in the manual input of the information, if required. D. The Homestead Credit Application Should Be Clarified The homestead credit application itself may have contributed to some of the inappropriate filings for the full property tax benefit. For example, the instructions to the application use the term principal residence instead of the general term property, which potentially creates ambiguity and confusion. Specifically, Line 15a of the homestead credit application requests homeowners to reveal whether their principal residence consists of more than one residential unit, whereas Line 15b of the application directs homeowners to enter the percentage of the property that they use as their principal residence. Furthermore, the instructions provide only one example in that regard: 10

13 For example, if your property consists of four units of equal size, one commercial unit and three residential units, and you occupy one of the residential units as your principal residence, enter 25% at Line 15b. This is the percentage of the property you occupy. NOTE: (1) If your property consists of more than four units, you do not qualify for the benefit. (2) If your property contains more than one commercial unit, you do not qualify for the benefit. While this example is helpful, the application does not define what specifically constitutes a unit and the instructions do not explicitly state that only a unit that is used as a principal residence will qualify for the homestead credit. The inconsistent use of principal residence and limited instructions could potentially cause confusion in the application process. E. Multiple Unit Information Could be Utilized in Review of Two Other Tax Relief Programs Two other property tax relief programs, the property tax reimbursement and deduction programs identified earlier, are potentially impacted by these findings. Taxation has confirmed that the amount of the benefit for each of these programs is similarly based on the percentage of property the owner occupies as his or her principal residence. Because Taxation does not currently verify the number of units within a property, the potential for inappropriate awards also exists for these programs. To test the impact of our findings on these other programs we checked to see whether any of the 29 property owners we identified as improperly receiving 100 percent of the homestead credit also applied for and inappropriately received the full property tax reimbursement and/or property tax deduction. Four out of the five homeowners who also applied for and received the full property tax reimbursement, and 12 out of the 15 who also claimed and received the full property tax deduction (or roughly 80 percent in each category), once again inaccurately reported 11

14 that they utilized 100 percent of the property as their primary residence and similarly received a greater property tax reimbursement or deduction than they were otherwise permitted. In total, the four homeowners received excess property tax reimbursements of $1,588 and the 12 homeowners received excess property tax deductions of $48,516. For example, our review revealed a property owner who received both a homestead credit and property tax reimbursement in the total amount of $2,374, resulting in an overpayment of $1,187, and another owner who received a homestead credit of $828 and claimed the maximum allowable property tax deduction of $10,000, resulting in a total excess benefit of $5,414. Two other beneficiaries of multiple programs similarly applied for and received the full homestead credit and property tax deduction when in fact their properties contained two dwelling units, resulting in excess benefits of $5,243 and $5,124, respectively. Taxation officials stated that requiring tax assessors to report the number of dwelling units and building class code for each property in MOD-IV would also enable them to verify the percentage of principal residence claimed by a taxpayer in seeking benefits from the property tax reimbursement and deduction programs. *** Taxation officials concurred that in view of the enormity of all three property tax relief programs more than one billion dollars has been budgeted for these programs in fiscal year 2015 the effect of this simple change could result in millions of dollars in annual savings for the State. 12

15 V. Recommendations and Referrals Millions of State dollars can potentially be saved every year by simply requiring municipal tax assessors to provide known information to Taxation. Taxation should immediately require all tax assessors to begin reporting in Taxation s MOD-IV system the number of dwelling units and building class codes for each property in their municipalities. This will enable Taxation to verify the information reported by those seeking the homestead credit, property tax reimbursement and property tax deduction as well as identify those who may be ineligible for the full benefit from the outset. Additionally, Taxation should clarify the instructions for these three tax relief programs. For example, OSC recommends that Taxation consider providing a standard definition of unit for all three programs, as it does for the tenant rebate program. See N.J.A.C. 18: (defining unit of residential rental property as including its own kitchen and bathroom facilities ). OSC notes that one such concise definition is provided by an international building codes organization: A single unit providing complete, independent living facilities for one or more persons, including permanent provisions for living, sleeping, eating, cooking, and sanitation. See 202 of Model Code of Building Officials and Code Administrators International, Inc. (1999). Taxation should also not use the terms property and principal residence interchangeably in the homestead credit application. Specifically, at Line 15a Taxation should clarify that applicants should mark Yes if their property (not principal residence ) has more than one unit. Additionally, the instructions for each program should explicitly state that the tax benefit is available only for the unit used as a principal residence. The instructions should 13

16 also provide additional examples to assist the applicant in determining the total percentage of occupancy. We have referred to Taxation the names of the seven property owners from Kearny and the 29 property owners from our sample who received excess homestead credit amounts in 2011, as well as those who also improperly claimed the property tax reimbursement and deduction, for appropriate action. This action should include the recovery of any amounts paid or credited in error or as a result of misrepresentation. See N.J.S.A. 54:4-8.66c; N.J.S.A. 54A:9-2. As noted above, some assessors have already added multi-unit information to the MOD-IV database and, in response to our investigation, Taxation recently sent letters seeking adjustments of the homestead credit to 3,771 taxpayers who did not claim a multi-unit percentage even though their municipal tax assessors had designated the properties as having multiple units. Taxation anticipates over $1.6 million in savings from this effort. Within the relevant statute of limitations, see N.J.S.A. 54A:9-4, Taxation should also identify all other property owners who have erroneously or improperly claimed or received 100 percent of the homestead credit, property tax reimbursement and property tax deduction under similar circumstances and recover such erroneous or misrepresented benefits. 14

ASSEMBLY, No. 441 STATE OF NEW JERSEY. 211th LEGISLATURE PRE-FILED FOR INTRODUCTION IN THE 2004 SESSION

ASSEMBLY, No. STATE OF NEW JERSEY th LEGISLATURE PRE-FILED FOR INTRODUCTION IN THE 00 SESSION Sponsored by: Assemblyman ANTHONY IMPREVEDUTO District (Bergen and Hudson) Assemblyman NEIL M. COHEN District

ASSEMBLY, No. STATE OF NEW JERSEY th LEGISLATURE PRE-FILED FOR INTRODUCTION IN THE 00 SESSION Sponsored by: Assemblyman ANTHONY IMPREVEDUTO District (Bergen and Hudson) Assemblyman NEIL M. COHEN District

STATE OF NEW JERSEY OFFICE OF THE STATE COMPTROLLER INVESTIGATIVE REPORT INEQUITABLE TAX ASSESSMENTS BOROUGH OF EDGEWATER

STATE OF NEW JERSEY OFFICE OF THE STATE COMPTROLLER INVESTIGATIVE REPORT INEQUITABLE TAX ASSESSMENTS BOROUGH OF EDGEWATER A. Matthew Boxer COMPTROLLER November 15, 2011 TABLE OF CONTENTS I. Introduction

STATE OF NEW JERSEY OFFICE OF THE STATE COMPTROLLER INVESTIGATIVE REPORT INEQUITABLE TAX ASSESSMENTS BOROUGH OF EDGEWATER A. Matthew Boxer COMPTROLLER November 15, 2011 TABLE OF CONTENTS I. Introduction

Comparison of the Executive, Assembly, and Senate Property Tax Relief Proposals FY 2015-2016

Comparison of the Executive, Assembly, and Senate Property Tax Relief Proposals FY 2015-2016 March 23, 2015 The governor s Executive Budget proposal includes a significant new property circuit breaker

Comparison of the Executive, Assembly, and Senate Property Tax Relief Proposals FY 2015-2016 March 23, 2015 The governor s Executive Budget proposal includes a significant new property circuit breaker

Overpayments of Ambulatory Patient Group Claims. Medicaid Program Department of Health

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Overpayments of Ambulatory Patient Group Claims Medicaid Program Department of Health Report

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Overpayments of Ambulatory Patient Group Claims Medicaid Program Department of Health Report

How To Pay For A Home Care Program In Camden

PROPERTY TAX RELIEF FUND CASINO CONTROL FUND CASINO REVENUE FUND GUBERNATORIAL ELECTIONS FUND PROPERTY TAX RELIEF FUND GIA 82. DEPARTMENT OF THE TREASURY 70. GOVERNMENT DIRECTION, MANAGEMENT AND CONTROL

PROPERTY TAX RELIEF FUND CASINO CONTROL FUND CASINO REVENUE FUND GUBERNATORIAL ELECTIONS FUND PROPERTY TAX RELIEF FUND GIA 82. DEPARTMENT OF THE TREASURY 70. GOVERNMENT DIRECTION, MANAGEMENT AND CONTROL

HOUSE BILL NO. HB0037. Senior citizen property tax relief program.

00 STATE OF WYOMING 0LSO-0 HOUSE BILL NO. HB00 Senior citizen property tax relief program. Sponsored by: Representative(s) Hammons, Bagby, Dockstader, Madden and Martin and Senator(s) Aullman, Geis and

00 STATE OF WYOMING 0LSO-0 HOUSE BILL NO. HB00 Senior citizen property tax relief program. Sponsored by: Representative(s) Hammons, Bagby, Dockstader, Madden and Martin and Senator(s) Aullman, Geis and

Rebates and Discounts on Physician-Administered Drugs. Medicaid Program Department of Health

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Rebates and Discounts on Physician-Administered Drugs Medicaid Program Department of Health

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Rebates and Discounts on Physician-Administered Drugs Medicaid Program Department of Health

Improper Payments to a Physical Therapist. Medicaid Program Department of Health

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Improper Payments to a Physical Therapist Medicaid Program Department of Health Report 2013-S-15

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Improper Payments to a Physical Therapist Medicaid Program Department of Health Report 2013-S-15

Vacancy Rebate Verification Program

DATE: April 26,2004 REPORT: Corp/Fin 04-10 TITLE: Vacancy Rebate Verification Program C.A.O. WARD: All Wards FILE: ATTACHMENTS: PREPARED BY: John Morrison DEPARTMENT: Financial Services - Revenue CLEARANCE:

DATE: April 26,2004 REPORT: Corp/Fin 04-10 TITLE: Vacancy Rebate Verification Program C.A.O. WARD: All Wards FILE: ATTACHMENTS: PREPARED BY: John Morrison DEPARTMENT: Financial Services - Revenue CLEARANCE:

DEPARTMENT OF HEALTH MEDICAID OVERPAYMENTS FOR MENTAL HEALTH SERVICES. Report 2006-S-53 OFFICE OF THE NEW YORK STATE COMPTROLLER

Thomas P. DiNapoli COMPTROLLER OFFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE GOVERNMENT ACCOUNTABILITY Audit Objective... 2 Audit Results - Summary... 2 Background... 3 Audit Findings and

Thomas P. DiNapoli COMPTROLLER OFFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE GOVERNMENT ACCOUNTABILITY Audit Objective... 2 Audit Results - Summary... 2 Background... 3 Audit Findings and

TABLE OF CONTENTS. CASINO CONTROL FUND Executive Branch: Department of Law and Public Safety... G-11 Department of the Treasury...

TABLE OF CONTENTS Page Reference Direct State Grants State Services In-Aid Aid PROPERTY TAX RELIEF FUND Executive Branch: Department of Community Affairs... G-2 Department of Education... G-3 Department

TABLE OF CONTENTS Page Reference Direct State Grants State Services In-Aid Aid PROPERTY TAX RELIEF FUND Executive Branch: Department of Community Affairs... G-2 Department of Education... G-3 Department

Targeting Property Tax Relief: A Design to Expand Illinois Circuit Breaker

Targeting Relief: A Design to Expand Illinois Circuit Breaker This paper proposes to expand the current Illinois Circuit Breaker Program and provide property tax credits to up to 4.7 million households

Targeting Relief: A Design to Expand Illinois Circuit Breaker This paper proposes to expand the current Illinois Circuit Breaker Program and provide property tax credits to up to 4.7 million households

INCOME DEFINED "income" "income" "business income" "Married persons income"

INCOME DEFINED N.J.S.A.54:4-8.40(a) defines "income" as all income from whatever source derived including, but not limited to, realized capital gains except for a capital gain resulting from the sale or

INCOME DEFINED N.J.S.A.54:4-8.40(a) defines "income" as all income from whatever source derived including, but not limited to, realized capital gains except for a capital gain resulting from the sale or

UNDERSTANDING PROPERTY TAXES IN COOK COUNTY

UNDERSTANDING PROPERTY TAXES IN COOK COUNTY 1 A PERSPECTIVE COOK COUNTY NEW TRIER TOWNSHIP 2 nd Largest County in U.S. 5.3 Million People 1.8 Million Parcels 1.2 Million Residential Parcels One of Smallest

UNDERSTANDING PROPERTY TAXES IN COOK COUNTY 1 A PERSPECTIVE COOK COUNTY NEW TRIER TOWNSHIP 2 nd Largest County in U.S. 5.3 Million People 1.8 Million Parcels 1.2 Million Residential Parcels One of Smallest

School Tax Relief (STAR) Program

Program") O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability School Tax Relief (STAR) Program 2012-MS-6 Thomas P. DiNapoli Table of Contents

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability School Tax Relief (STAR) Program 2012-MS-6 Thomas P. DiNapoli Table of Contents

Medicaid Payments Made Pursuant to Medicare Part C. Medicaid Program Department of Health

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Medicaid Payments Made Pursuant to Medicare Part C Medicaid Program Department of Health Report

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Medicaid Payments Made Pursuant to Medicare Part C Medicaid Program Department of Health Report

Office of Children and Family Services

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of State Government Accountability Office of Children and Family Services Adoption Subsidy Program Report 2008-S-106 Thomas

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of State Government Accountability Office of Children and Family Services Adoption Subsidy Program Report 2008-S-106 Thomas

Appraisal Districts. Who governs a local county appraisal district? How are directors chosen? How is an appraisal district funded?

Appraisal Districts Who governs a local county appraisal district? A local board of directors governs the appraisal district. How are directors chosen? The governing bodies of the taxing units that vote

Appraisal Districts Who governs a local county appraisal district? A local board of directors governs the appraisal district. How are directors chosen? The governing bodies of the taxing units that vote

Request for Proposals for Professional Services For Affordable Housing Administrative Agent

Request for Proposals for Professional Services For The Township of Harrison, Gloucester County, is seeking proposals for an Affordable Housing Administrative Agent in compliance with the Rules on Affordable

Request for Proposals for Professional Services For The Township of Harrison, Gloucester County, is seeking proposals for an Affordable Housing Administrative Agent in compliance with the Rules on Affordable

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Many Taxpayers Are Still Not Complying With Noncash Charitable Contribution Reporting Requirements December 20, 2012 Reference Number: 2013-40-009 This

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Many Taxpayers Are Still Not Complying With Noncash Charitable Contribution Reporting Requirements December 20, 2012 Reference Number: 2013-40-009 This

New York State Medicaid Program

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of State Government Accountability New York State Medicaid Program Department of Health Under Reporting of Net Available Monthly

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of State Government Accountability New York State Medicaid Program Department of Health Under Reporting of Net Available Monthly

OPIC. Part-Year Residents

New Jersey Division of Taxation TAX OPIC Part-Year Residents Bulletin GIT-6 Contents Introduction 1 Definitions 2 Filing Requirements 3 Filing Status Considerations 6 How Residents and Nonresidents Are

New Jersey Division of Taxation TAX OPIC Part-Year Residents Bulletin GIT-6 Contents Introduction 1 Definitions 2 Filing Requirements 3 Filing Status Considerations 6 How Residents and Nonresidents Are

State Department of Assessments and Taxation

Audit Report State Department of Assessments and Taxation December 2013 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related follow-up correspondence

Audit Report State Department of Assessments and Taxation December 2013 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related follow-up correspondence

815 CMR 9.00: DEBT COLLECTION AND INTERCEPT. Section

815 CMR 9.00: DEBT COLLECTION AND INTERCEPT Section 9.01: Purpose, Application and Authority 9.02: Definitions 9.03: Billing Entity Requirements for Collection of Debts 9.04: Simultaneous Submission of

815 CMR 9.00: DEBT COLLECTION AND INTERCEPT Section 9.01: Purpose, Application and Authority 9.02: Definitions 9.03: Billing Entity Requirements for Collection of Debts 9.04: Simultaneous Submission of

ARTICLE IV. SENIOR CITIZENS TAX ABATEMENT Sec. 220-13. Pilot Program for Senior Citizens Tax Abatement for Fiscal Year 2015/2016.

ARTICLE IV. SENIOR CITIZENS TAX ABATEMENT Sec. 220-13. Pilot Program for Senior Citizens Tax Abatement for Fiscal Year 2015/2016. For the fiscal year July 1, 2015 through June 30, 2016 and only said fiscal

ARTICLE IV. SENIOR CITIZENS TAX ABATEMENT Sec. 220-13. Pilot Program for Senior Citizens Tax Abatement for Fiscal Year 2015/2016. For the fiscal year July 1, 2015 through June 30, 2016 and only said fiscal

September 24, 2007. To The Honorable, the City Council:

September 24, 2007 To The Honorable, the City Council: The establishment of the FY08 property tax rate by the Board of Assessors, subject to the approval of the Massachusetts Department of Revenue, is

September 24, 2007 To The Honorable, the City Council: The establishment of the FY08 property tax rate by the Board of Assessors, subject to the approval of the Massachusetts Department of Revenue, is

Property Tax Relief: The $7 Billion Reality

August 2008 Property Tax Relief: The $7 Billion Reality In the spring of 2006, Texas lawmakers passed a massive package of school finance reforms. School tax rates for maintenance and operations were to

August 2008 Property Tax Relief: The $7 Billion Reality In the spring of 2006, Texas lawmakers passed a massive package of school finance reforms. School tax rates for maintenance and operations were to

No one likes paying taxes, especially when they aren t sure how they re figured or where the money goes. For property owners, coming up with that one

No one likes paying taxes, especially when they aren t sure how they re figured or where the money goes. For property owners, coming up with that one or two large payments each year feels more painful

No one likes paying taxes, especially when they aren t sure how they re figured or where the money goes. For property owners, coming up with that one or two large payments each year feels more painful

Glossary of Assessment Terms:

Glossary of Assessment Terms: Abatement A reduction or elimination of a tax or charge imposed by a governmental unit, applicable to property tax bills, motor vehicle excise taxes, fees, charges, and special

Glossary of Assessment Terms: Abatement A reduction or elimination of a tax or charge imposed by a governmental unit, applicable to property tax bills, motor vehicle excise taxes, fees, charges, and special

The Homestead Act. Questions. and Answers. Massachusetts General Laws, Ch. 188, 1-10. William Francis Galvin Secretary of the Commonwealth

Questions and Answers The Homestead Act Massachusetts General Laws, Ch. 188, 1-10 William Francis Galvin Secretary of the Commonwealth updated 8/1/13 William Francis Galvin Secretary of the Commonwealth

Questions and Answers The Homestead Act Massachusetts General Laws, Ch. 188, 1-10 William Francis Galvin Secretary of the Commonwealth updated 8/1/13 William Francis Galvin Secretary of the Commonwealth

Property Tax Real. hio. Taxpayer The tax is paid by all real property owners unless specifically exempt.

108 Property Tax Real Taxpayer The tax is paid by all real property owners unless specifically exempt. Tax Base The tax is based on the assessed value of land and buildings. Assessed value is 35 percent

108 Property Tax Real Taxpayer The tax is paid by all real property owners unless specifically exempt. Tax Base The tax is based on the assessed value of land and buildings. Assessed value is 35 percent

What if Indiana Eliminated Personal Property Taxes? Larry DeBoer Department of Agricultural Economics Purdue University. June 2014

What if Indiana Eliminated Personal Property Taxes? Larry DeBoer Department of Agricultural Economics Purdue University June 2014 Economic Development, Tax Shifts and Revenue Losses Eliminating the personal

What if Indiana Eliminated Personal Property Taxes? Larry DeBoer Department of Agricultural Economics Purdue University June 2014 Economic Development, Tax Shifts and Revenue Losses Eliminating the personal

The State Role in Providing Property Tax Relief

The State Role in Providing Property Tax Relief Andrew Reschovsky Robert M. La Follette School of Public Affairs University of Wisconsin-Madison reschovsky@lafollette.wisc.edu Selected Property Tax Facts

The State Role in Providing Property Tax Relief Andrew Reschovsky Robert M. La Follette School of Public Affairs University of Wisconsin-Madison reschovsky@lafollette.wisc.edu Selected Property Tax Facts

GUIDELINES. For the Michigan Homestead Property Tax Exemption Program

Michigan Department of Treasury 2856, Formerly C-4381 (1-00) GUIDELINES For the Michigan Homestead Property Tax Exemption Program These guidelines are compiled questions and answers from the previous four

Michigan Department of Treasury 2856, Formerly C-4381 (1-00) GUIDELINES For the Michigan Homestead Property Tax Exemption Program These guidelines are compiled questions and answers from the previous four

General Questions and Answers on the Mortgage Recording Taxes

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau General Questions and Answers on the This publication addresses some general questions regarding the

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau General Questions and Answers on the This publication addresses some general questions regarding the

Title 36: TAXATION. Maine Revised Statutes. Chapter 907: MAINE RESIDENTS PROPERTY TAX PROGRAM HEADING: PL 1989, c. 534, Pt.

Maine Revised Statutes Title 36: TAXATION Chapter 907: MAINE RESIDENTS PROPERTY TAX PROGRAM HEADING: PL 1989, c. 534, Pt. A, 1 (rpr) 6201. DEFINITIONS As used in this chapter, unless the context otherwise

Maine Revised Statutes Title 36: TAXATION Chapter 907: MAINE RESIDENTS PROPERTY TAX PROGRAM HEADING: PL 1989, c. 534, Pt. A, 1 (rpr) 6201. DEFINITIONS As used in this chapter, unless the context otherwise

TRANSFER OF PROPERTY TAX BASE FOR PERSONS 55 AND OLDER OR SEVERELY AND PERMANENTLY DISABLED

OFFICE OF ASSESSOR COUNTY OF ALAMEDA 1221 Oak St., County Administration Building Oakland, California 94612-4288 (510) 272-3787 / FAX (510) 272-3803 RON THOMSEN ASSESSOR TRANSFER OF PROPERTY TAX BASE FOR

OFFICE OF ASSESSOR COUNTY OF ALAMEDA 1221 Oak St., County Administration Building Oakland, California 94612-4288 (510) 272-3787 / FAX (510) 272-3803 RON THOMSEN ASSESSOR TRANSFER OF PROPERTY TAX BASE FOR

815 CMR: COMPTROLLER'S DIVISION 815 CMR 9.00: DEBT COLLECTION AND INTERCEPT. Section

815 CMR 9.00: DEBT COLLECTION AND INTERCEPT Section 9.01: Purpose, Application and Authority 9.02: Definitions 9.03: Billing Entity Requirements for Collection of Debts 9.04: Simultaneous Submission of

815 CMR 9.00: DEBT COLLECTION AND INTERCEPT Section 9.01: Purpose, Application and Authority 9.02: Definitions 9.03: Billing Entity Requirements for Collection of Debts 9.04: Simultaneous Submission of

Special Civil Mandatory Attorney s Fees

STATE OF NEW JERSEY NEW JERSEY LAW REVISION COMMISSION Tentative Report Relating to Special Civil Mandatory Attorney s Fees April 20, 2012 This tentative report is distributed to advise interested persons

STATE OF NEW JERSEY NEW JERSEY LAW REVISION COMMISSION Tentative Report Relating to Special Civil Mandatory Attorney s Fees April 20, 2012 This tentative report is distributed to advise interested persons

La Follette School of Public Affairs

Robert M. La Follette School of Public Affairs at the University of Wisconsin-Madison Working Paper Series La Follette School Working Paper No. 2010-003 http://www.lafollette.wisc.edu/publications/workingpapers

Robert M. La Follette School of Public Affairs at the University of Wisconsin-Madison Working Paper Series La Follette School Working Paper No. 2010-003 http://www.lafollette.wisc.edu/publications/workingpapers

Affordable Home Ownership Development Program. Affordable Housing Corporation Homes and Community Renewal

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Affordable Home Ownership Development Program Affordable Housing Corporation Homes and Community

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Affordable Home Ownership Development Program Affordable Housing Corporation Homes and Community

THE CORPORATION OF THE MUNICIPALITY OF POWASSAN BY-LAW NO. 2006-05

THE CORPORATION OF THE MUNICIPALITY OF POWASSAN BY-LAW NO. 2006-05 BEING A BY-LAW TO ESTABLISH A TAX REBATE PROGRAM FOR THE PURPOSES OF PROVIDING RELIEF FROM TAXES OR AMOUNTS PAID ON ACCOUNT OF TAXES ON

THE CORPORATION OF THE MUNICIPALITY OF POWASSAN BY-LAW NO. 2006-05 BEING A BY-LAW TO ESTABLISH A TAX REBATE PROGRAM FOR THE PURPOSES OF PROVIDING RELIEF FROM TAXES OR AMOUNTS PAID ON ACCOUNT OF TAXES ON

How To Get A Disaster Recovery Grant From The Federal Government

Frequently Asked Questions About The Disaster Recovery Action Plan Helping New Jerseyans Understand What The Christie Administration s Community Development Block Grant Disaster Recovery Action Plan Means

Frequently Asked Questions About The Disaster Recovery Action Plan Helping New Jerseyans Understand What The Christie Administration s Community Development Block Grant Disaster Recovery Action Plan Means

Background Paper 79-1 PROPERTY TAX RELIEF

Background Paper 79-1 PROPERTY TAX RELIEF PROPERTY TAX RELIEF Introduction For at least the past decade, demands to reform the property tax have increased in strength and volume. There are several reasons

Background Paper 79-1 PROPERTY TAX RELIEF PROPERTY TAX RELIEF Introduction For at least the past decade, demands to reform the property tax have increased in strength and volume. There are several reasons

A Landlord s Guide to Housing Benefit

A Landlord s Guide to Housing Benefit October 2009 A landlord s guide to Housing Benefit; Table of Contents Introduction...3 Standards Of Service...3 Processing Housing Benefit Claims...3 Changes in circumstances...3

A Landlord s Guide to Housing Benefit October 2009 A landlord s guide to Housing Benefit; Table of Contents Introduction...3 Standards Of Service...3 Processing Housing Benefit Claims...3 Changes in circumstances...3

Part VIII RULES GOVERNING PRACTICE IN THE TAX COURT OF NEW JERSEY TABLE OF CONTENTS

APPENDIX C - New Jersey Tax Court Rules Part VIII RULES GOVERNING PRACTICE IN THE TAX COURT OF NEW JERSEY Rule 8:1. Rule 8:2. Rule 8:3. Rule 8:4. TABLE OF CONTENTS Scope: Applicability Review Jurisdiction

APPENDIX C - New Jersey Tax Court Rules Part VIII RULES GOVERNING PRACTICE IN THE TAX COURT OF NEW JERSEY Rule 8:1. Rule 8:2. Rule 8:3. Rule 8:4. TABLE OF CONTENTS Scope: Applicability Review Jurisdiction

Overview. January, 2009

Information Guide January, 2009 Nebraska Homestead Exemption NOTE: Nebraska Homestead Exemption Application or Certification of Status, Form 458, is mailed to homestead exemption recipients in January,

Information Guide January, 2009 Nebraska Homestead Exemption NOTE: Nebraska Homestead Exemption Application or Certification of Status, Form 458, is mailed to homestead exemption recipients in January,

New Hope Borough Landlord Registration Statement & Application

Landlord s Name: Registration Year: Tax Map Parcel Number 27- Property Address: New Hope Borough Landlord Registration Statement & Application This form must be completed by Landlords, pursuant to Borough

Landlord s Name: Registration Year: Tax Map Parcel Number 27- Property Address: New Hope Borough Landlord Registration Statement & Application This form must be completed by Landlords, pursuant to Borough

Workers Compensation Mandatory Attorney Fees

STATE OF NEW JERSEY NEW JERSEY LAW REVISION COMMISSION Draft Tentative Report Relating to November 7, 2011 This draft tentative report is distributed to advise interested persons of the Commission's tentative

STATE OF NEW JERSEY NEW JERSEY LAW REVISION COMMISSION Draft Tentative Report Relating to November 7, 2011 This draft tentative report is distributed to advise interested persons of the Commission's tentative

New Jersey Department of Community Affairs Division of Codes and Standards Landlord-Tenant Information Service

New Jersey Department of Community Affairs Division of Codes and Standards Landlord-Tenant Information Service GROUNDS FOR AN EVICTION BULLETIN Updated February 2008 An eviction is an actual expulsion

New Jersey Department of Community Affairs Division of Codes and Standards Landlord-Tenant Information Service GROUNDS FOR AN EVICTION BULLETIN Updated February 2008 An eviction is an actual expulsion

Chairman DeFrancisco, Chairman Farrell, and members of the Senate and Assembly:

TESTIMONY 2015-16 Executive Budget Education-Related Tax Policies Senate Finance Committee Assembly Ways and Means Committee February 9, 2015 Chairman DeFrancisco, Chairman Farrell, and members of the

TESTIMONY 2015-16 Executive Budget Education-Related Tax Policies Senate Finance Committee Assembly Ways and Means Committee February 9, 2015 Chairman DeFrancisco, Chairman Farrell, and members of the

Section 12 - TAXATION

Section 12 - TAXATION ORDINANCE PERTAINING TO ELIMINATION OF BOARD OF ASSESSORS AND APPOINTMENT OF PART-TIME ASSESSOR RESOLVED, that the present Board of Assessors of the Town of Deep River be eliminated

Section 12 - TAXATION ORDINANCE PERTAINING TO ELIMINATION OF BOARD OF ASSESSORS AND APPOINTMENT OF PART-TIME ASSESSOR RESOLVED, that the present Board of Assessors of the Town of Deep River be eliminated

Department of Health and Mental Hygiene Department of Human Resources. Medical Assistance Program

Performance Audit Report Department of Health and Mental Hygiene Department of Human Resources Medical Assistance Program Using the Federal Death Master File to Detect and Prevent Medicaid Payments Attributable

Performance Audit Report Department of Health and Mental Hygiene Department of Human Resources Medical Assistance Program Using the Federal Death Master File to Detect and Prevent Medicaid Payments Attributable

Walter Kreher, Director, Multifamily Program Center, 2FHM. Alexander C. Malloy, Regional Inspector General for Audit, 2AGA INTRODUCTION

Issue Date September 27, 2004 Audit Case Number 2004-NY-1005 TO: Walter Kreher, Director, Multifamily Program Center, 2FHM FROM: Alexander C. Malloy, Regional Inspector General for Audit, 2AGA SUBJECT:

Issue Date September 27, 2004 Audit Case Number 2004-NY-1005 TO: Walter Kreher, Director, Multifamily Program Center, 2FHM FROM: Alexander C. Malloy, Regional Inspector General for Audit, 2AGA SUBJECT:

THE SILENT KILLER: What New Jersey attorneys need to know about Chapter 91. By David B. Wolfe 1

THE SILENT KILLER: What New Jersey attorneys need to know about Chapter 91. By David B. Wolfe 1 It is essential that all lawyers who represent real estate owners have a fundamental understanding of N.J.S.A.

THE SILENT KILLER: What New Jersey attorneys need to know about Chapter 91. By David B. Wolfe 1 It is essential that all lawyers who represent real estate owners have a fundamental understanding of N.J.S.A.

Medicaid Claims Processing Activity April 1, 2012 through September 30, 2012 Medicaid Program Department of Health

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Medicaid Claims Processing Activity April 1, 2012 through September 30, 2012 Medicaid Program

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Medicaid Claims Processing Activity April 1, 2012 through September 30, 2012 Medicaid Program

INSTRUCTIONS FOR LEGAL RESIDENCE APPLICATION FOR ANY QUESTIONS CALL THE CHARLESTON COUNTY ASSESSOR S OFFICE AT

INSTRUCTIONS FOR LEGAL RESIDENCE APPLICATION FOR ANY QUESTIONS CALL THE CHARLESTON COUNTY ASSESSOR S OFFICE AT 843 958 4100 Other offices will not be able to answer your questions accurately Call the Assessor

INSTRUCTIONS FOR LEGAL RESIDENCE APPLICATION FOR ANY QUESTIONS CALL THE CHARLESTON COUNTY ASSESSOR S OFFICE AT 843 958 4100 Other offices will not be able to answer your questions accurately Call the Assessor

Table of Contents Section Page #

HOMESTEAD STANDARD DEDUCTION AND OTHER DEDUCTIONS Frequently Asked Questions (FAQs) Revised January 5, 2011 For additional information regarding deductions, please visit http://www.in.gov/dlgf/2344.htm.

HOMESTEAD STANDARD DEDUCTION AND OTHER DEDUCTIONS Frequently Asked Questions (FAQs) Revised January 5, 2011 For additional information regarding deductions, please visit http://www.in.gov/dlgf/2344.htm.

HOWARD JARVIS TAXPAYERS ASSOCIATION. Re: California Homeowners and Renters Tax Relief Act of 2016

HOWARD JARVIS, Founder (1903-1986) JON COUPAL, President TREVOR GRIMM, General Counsel TIMOTHY BITTLE, Director of Legal Affairs Ashley Johansson Initiative Coordinator Attorney General's Office P.O. Box

HOWARD JARVIS, Founder (1903-1986) JON COUPAL, President TREVOR GRIMM, General Counsel TIMOTHY BITTLE, Director of Legal Affairs Ashley Johansson Initiative Coordinator Attorney General's Office P.O. Box

State Property Tax Credits (School Levy, First Dollar, and Lottery and Gaming Credits)

") State Property Tax Credits (School Levy, First Dollar, and Lottery and Gaming Credits) Informational Paper 21 Wisconsin Legislative Fiscal Bureau January, 2013 Wisconsin Legislative Fiscal Bureau January,

State Property Tax Credits (School Levy, First Dollar, and Lottery and Gaming Credits) Informational Paper 21 Wisconsin Legislative Fiscal Bureau January, 2013 Wisconsin Legislative Fiscal Bureau January,

Model Legislation for Short-Term Online Rentals. Menu

Section 1 - Definitions Model Legislation for Short-Term Online Rentals Menu Short-term rental unit means a residential dwelling of any type in the [state/city of ], including, but not limited to, a single-family

Section 1 - Definitions Model Legislation for Short-Term Online Rentals Menu Short-term rental unit means a residential dwelling of any type in the [state/city of ], including, but not limited to, a single-family

New York State Office of Alcoholism and Substance Abuse Services

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE GOVERNMENT ACCOUNTABILITY New York State Office of Alcoholism and Substance Abuse Services Chemical Dependency Program Payments to Selected Contractors

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE GOVERNMENT ACCOUNTABILITY New York State Office of Alcoholism and Substance Abuse Services Chemical Dependency Program Payments to Selected Contractors

FIRST AMENDMENT TO COMMITMENT TO PURCHASE FINANCIAL INSTRUMENT and HFA PARTICIPATION AGREEMENT

FIRST AMENDMENT TO COMMITMENT TO PURCHASE FINANCIAL INSTRUMENT and HFA PARTICIPATION AGREEMENT This First Amendment to Commitment to Purchase Financial Instrument and HFA Participation Agreement (the First

FIRST AMENDMENT TO COMMITMENT TO PURCHASE FINANCIAL INSTRUMENT and HFA PARTICIPATION AGREEMENT This First Amendment to Commitment to Purchase Financial Instrument and HFA Participation Agreement (the First

Seized Assets Program. Division of State Police

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Seized Assets Program Division of State Police Report 2013-S-46 December 2014 Executive Summary

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Seized Assets Program Division of State Police Report 2013-S-46 December 2014 Executive Summary

Oklahoma Ad Valorem. 1 of 14. Central Valuation by Oklahoma Tax Commission: All Public Service Corporations (multiple county impact)

") Oklahoma Ad Valorem - Founded Before Statehood And Codified in the 1907 Populist Constitution And Current Laws - Township Assessors in 1894 - County Assessor System Set Up in 1911 - Tax Commission Oversight

Oklahoma Ad Valorem - Founded Before Statehood And Codified in the 1907 Populist Constitution And Current Laws - Township Assessors in 1894 - County Assessor System Set Up in 1911 - Tax Commission Oversight

Pursuant to A.R.S. 12-1831, et seq., plaintiffs allege:

1 1 1 1 MOONEY, WRIGHT & MOORE, PLLC Paul J. Mooney (No. 000) Jim L. Wright (No. 01) Mesa Financial Plaza, Suite 000 South Alma School Road Mesa, Arizona 0-1 Telephone: (0) 1-00 Email: pmooney@azstatetaxlaw.com

1 1 1 1 MOONEY, WRIGHT & MOORE, PLLC Paul J. Mooney (No. 000) Jim L. Wright (No. 01) Mesa Financial Plaza, Suite 000 South Alma School Road Mesa, Arizona 0-1 Telephone: (0) 1-00 Email: pmooney@azstatetaxlaw.com

Minnetonka Independent School District 276 Levy Adoption Taxes Payable in 2012

Minnetonka Independent School District 276 Levy Adoption Taxes Payable in 2012 Public Schools Established by Minnesota Constitution ARTICLE XIII MISCELLANEOUS SUBJECTS Section 1. UNIFORM SYSTEM OF PUBLIC

Minnetonka Independent School District 276 Levy Adoption Taxes Payable in 2012 Public Schools Established by Minnesota Constitution ARTICLE XIII MISCELLANEOUS SUBJECTS Section 1. UNIFORM SYSTEM OF PUBLIC

150-303-405 (Rev. 6-09)

") A Brief History of Oregon Property Taxation 150-303-405-1 (Rev. 6-09) 150-303-405 (Rev. 6-09) To understand the current structure of Oregon s property tax system, it is helpful to view the system in a

A Brief History of Oregon Property Taxation 150-303-405-1 (Rev. 6-09) 150-303-405 (Rev. 6-09) To understand the current structure of Oregon s property tax system, it is helpful to view the system in a

Estimating 2009 Circuit Breaker Credits: A 12-Step Guide for Indiana Local Governments

Estimating 2009 Circuit Breaker Credits: A 12-Step Guide for Indiana Local Governments Larry DeBoer Department of Agricultural Economics Purdue University June 2008 Indiana s 2008 property tax reform complicates

Estimating 2009 Circuit Breaker Credits: A 12-Step Guide for Indiana Local Governments Larry DeBoer Department of Agricultural Economics Purdue University June 2008 Indiana s 2008 property tax reform complicates

DEPARTMENT OF HEALTH DETERMINING MEDICAID ELIGIBILITY. Report 2005-S-42 OFFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE SERVICES

Alan G. Hevesi COMPTROLLER OFFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE SERVICES Audit Objective...2 Audit Results - Summary...2 Background...3 Audit Findings and Recommendations...4 Deceased

Alan G. Hevesi COMPTROLLER OFFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE SERVICES Audit Objective...2 Audit Results - Summary...2 Background...3 Audit Findings and Recommendations...4 Deceased

WISCONSIN VETERANS AND SURVIVING SPOUSES PROPERTY TAX CREDIT

WISCONSIN VETERANS AND SURVIVING SPOUSES PROPERTY TAX CREDIT Information, Request Form, and Instructions Contents Property Tax Credit for Veterans and Surviving Spouses... 2 Procedures... 3 Form Completion

WISCONSIN VETERANS AND SURVIVING SPOUSES PROPERTY TAX CREDIT Information, Request Form, and Instructions Contents Property Tax Credit for Veterans and Surviving Spouses... 2 Procedures... 3 Form Completion

Yavapai County Assessor s Office. Valuing People and Property.

Yavapai County Assessor s Office www.yavapai.us Valuing People and Property. In Prescott: In Cottonwood: 1015 Fair Street 10 S 6th Street Prescott, AZ Cottonwood, AZ (928)771-3220 (928)639-8121 PAMELA

Yavapai County Assessor s Office www.yavapai.us Valuing People and Property. In Prescott: In Cottonwood: 1015 Fair Street 10 S 6th Street Prescott, AZ Cottonwood, AZ (928)771-3220 (928)639-8121 PAMELA

ARTICLE I Tax Relief for the Elderly

Proposed Amendment to Ordinance on Tax Relief: Chapter 57, Article I of the New Canaan Code is hereby amended as follows. Deletions are marked by strikeouts, and new language is marked by underlined italics.

Proposed Amendment to Ordinance on Tax Relief: Chapter 57, Article I of the New Canaan Code is hereby amended as follows. Deletions are marked by strikeouts, and new language is marked by underlined italics.

Maryland Homeowners Association Act

Maryland Homeowners Association Act Table of Contents Maryland Homeowners Association Act 11B-101. Definitions... 1 11B-102. Applicability of title and 11B-105 through 11B-108, and 11B-110... 3 11B-103.

Maryland Homeowners Association Act Table of Contents Maryland Homeowners Association Act 11B-101. Definitions... 1 11B-102. Applicability of title and 11B-105 through 11B-108, and 11B-110... 3 11B-103.

Department of Environmental Conservation

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of State Government Accountability Department of Environmental Conservation Collection of Petroleum Bulk Storage Fees Report

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of State Government Accountability Department of Environmental Conservation Collection of Petroleum Bulk Storage Fees Report

to the Property Tax Relief Department of Revenue August 2014 Legislative Audit Division 14P-02

A Report to the Montana Legisl ature Perform ance Audit Property Tax Relief Department of Revenue August 2014 Legislative Audit Division 14P-02 Legislative Audit Committee Representatives Randy Brodehl,

A Report to the Montana Legisl ature Perform ance Audit Property Tax Relief Department of Revenue August 2014 Legislative Audit Division 14P-02 Legislative Audit Committee Representatives Randy Brodehl,

Social security assessment of the principal home

Social security assessment of the principal home FirstTech Strategic Update By Harry Rips, Technical Analyst The majority of Australians are homeowners, and the principal home is generally a client s most

Social security assessment of the principal home FirstTech Strategic Update By Harry Rips, Technical Analyst The majority of Australians are homeowners, and the principal home is generally a client s most

Overpayments for Services Also Covered by Medicare Part B. Medicaid Program Department of Health

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Overpayments for Services Also Covered by Medicare Part B Medicaid Program Department of Health

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Overpayments for Services Also Covered by Medicare Part B Medicaid Program Department of Health

2007 Property Tax Law Summary. September 2007 Minnesota Legislative Special Session

2007 Property Tax Law Summary September 2007 Minnesota Legislative Special Session Property Tax Division September 2007 2007 Disaster and Emergency Relief Disaster Abatement Appropriation Appropriation

2007 Property Tax Law Summary September 2007 Minnesota Legislative Special Session Property Tax Division September 2007 2007 Disaster and Emergency Relief Disaster Abatement Appropriation Appropriation

STAFF REPORT. March 31, 2004. Administration Committee. Chief Financial Officer and Treasurer. Overpayment of Property Taxes.

STAFF REPORT March 31, 2004 To: From: Subject: Administration Committee Chief Financial Officer and Treasurer Overpayment of Property Taxes Purpose: This report provides information and statistical data

STAFF REPORT March 31, 2004 To: From: Subject: Administration Committee Chief Financial Officer and Treasurer Overpayment of Property Taxes Purpose: This report provides information and statistical data

DISABILITY INSURANCE. Actions Needed to Help Prevent Potential Overpayments to Individuals Receiving Concurrent Federal Workers Compensation

United States Government Accountability Office Report to Congressional Requesters July 2015 DISABILITY INSURANCE Actions Needed to Help Prevent Potential Overpayments to Individuals Receiving Concurrent

United States Government Accountability Office Report to Congressional Requesters July 2015 DISABILITY INSURANCE Actions Needed to Help Prevent Potential Overpayments to Individuals Receiving Concurrent

2008 KANSAS Homestead Claim & Property Tax Relief Claim

2008 KANSAS Homestead Claim & Property Tax Relief Claim Forms and Instructions www.ksrevenue.org Page 1 What s Inside: General Information 3 What is the Homestead Refund? 3 What is a Homestead? 3 What

2008 KANSAS Homestead Claim & Property Tax Relief Claim Forms and Instructions www.ksrevenue.org Page 1 What s Inside: General Information 3 What is the Homestead Refund? 3 What is a Homestead? 3 What

Rochdale MBC Corporate Debt Management Policy. Contents Page. Page

Rochdale MBC Corporate Debt Management Policy Contents Page Page 1. Background and Objectives 1.1 What is a Corporate Debt Management Policy 1 1.2 Introduction 1 1.3 Objectives of the Policy 1 1.4 What

Rochdale MBC Corporate Debt Management Policy Contents Page Page 1. Background and Objectives 1.1 What is a Corporate Debt Management Policy 1 1.2 Introduction 1 1.3 Objectives of the Policy 1 1.4 What

Annual Assessments and You! Presented by: Stacey O Day, Allen County Assessor & Laura Boltz Rental Specialist

Annual Assessments and You! Presented by: Stacey O Day, Allen County Assessor & Laura Boltz Rental Specialist Data & Information provided also by: Department of Local Government Finance; The Annual Adjustment

Annual Assessments and You! Presented by: Stacey O Day, Allen County Assessor & Laura Boltz Rental Specialist Data & Information provided also by: Department of Local Government Finance; The Annual Adjustment

Page 1. October 1, 2012. To The Honorable, the City Council:

To The Honorable, the City Council: October 1, 2012 The establishment of the FY13 property tax rate by the Board of Assessors, subject to the approval of the Massachusetts Department of Revenue, is the

To The Honorable, the City Council: October 1, 2012 The establishment of the FY13 property tax rate by the Board of Assessors, subject to the approval of the Massachusetts Department of Revenue, is the

Performance Audit Report. Department of Human Resources The Maryland Energy Assistance Program and the Electric Universal Service Program

Performance Audit Report Department of Human Resources The Maryland Energy Assistance Program and the Electric Universal Service Program Accounting Records Cannot Be Relied Upon to Provide Accurate Expenditure

Performance Audit Report Department of Human Resources The Maryland Energy Assistance Program and the Electric Universal Service Program Accounting Records Cannot Be Relied Upon to Provide Accurate Expenditure

FINANCE. Annual Fiscal Plan. Original. Actual

FINANCE Description The Director of Finance is charged by State law with all duties mandated for the constitutional offices of the Treasurer and Commissioner of Revenue as prescribed by the Code of Virginia

FINANCE Description The Director of Finance is charged by State law with all duties mandated for the constitutional offices of the Treasurer and Commissioner of Revenue as prescribed by the Code of Virginia

Paper to be delivered at the Law Society of Upper Canada Six-Minute Commercial Leasing Lawyer 2007

PROPERTY TAX UPDATE: CURRENT ISSUES AND DISPUTES Paper to be delivered at the Law Society of Upper Canada Six-Minute Commercial Leasing Lawyer 2007 By: Michael Steinberg February 2007 Michael S. Steinberg

PROPERTY TAX UPDATE: CURRENT ISSUES AND DISPUTES Paper to be delivered at the Law Society of Upper Canada Six-Minute Commercial Leasing Lawyer 2007 By: Michael Steinberg February 2007 Michael S. Steinberg

D Approved for Exemption on: D 60% of value but not less than $60,000. D Approved for Refund by Assessor: D Aooroved for Refund by Treasurer:

Senior Citizen and Disabled Persons Exemption from Real Property Taxes Chapter 84.36 RCW Complete both sides of this form and file the application packet with your County Assessor. For assistance, contact

Senior Citizen and Disabled Persons Exemption from Real Property Taxes Chapter 84.36 RCW Complete both sides of this form and file the application packet with your County Assessor. For assistance, contact

Payments for Inmate Health Care Services. Department of Corrections and Community Supervision

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Payments for Inmate Health Care Services Department of Corrections and Community Supervision

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Payments for Inmate Health Care Services Department of Corrections and Community Supervision

TOOLKIT FOR TENANTS LIVING IN FORECLOSED PROPERTIES

TOOLKIT FOR TENANTS LIVING IN FORECLOSED PROPERTIES Department of the Public Advocate Division of Public Interest Advocacy 240 West State Street Trenton, NJ 08625 March 2010 TABLE OF CONTENTS INTRODUCTION...

TOOLKIT FOR TENANTS LIVING IN FORECLOSED PROPERTIES Department of the Public Advocate Division of Public Interest Advocacy 240 West State Street Trenton, NJ 08625 March 2010 TABLE OF CONTENTS INTRODUCTION...

Rhode Island Department of Human Services SUPPLEMENTAL SECURITY INCOME (SSI) AND STATE SUPPLEMENTAL PAYMENT (SSP) PROGRAM

AND STATE SUPPLEMENTAL PAYMENT (SSP) PROGRAM") Rhode Island Department of Human Services SUPPLEMENTAL SECURITY INCOME (SSI) AND STATE SUPPLEMENTAL PAYMENT (SSP) PROGRAM January 2014 Rhode Island Department of Human Services Supplemental Security Income

Rhode Island Department of Human Services SUPPLEMENTAL SECURITY INCOME (SSI) AND STATE SUPPLEMENTAL PAYMENT (SSP) PROGRAM January 2014 Rhode Island Department of Human Services Supplemental Security Income

An explanation of. 2011 Edition ARIZONA CAPITOL TIMES. Arizona Tax Research Association ARIZONA TAX RESEARCH ASSOCIATION 1814 W WASHINGTON STREET

NON-PROFIT ORG. U.S. POSTAGE P A I D PHOENIX, AZ PERMIT #2184 An explanation of ARIZONA TAX RESEARCH ASSOCIATION 1814 W WASHINGTON STREET PHOENIX AZ 85007 2011 Edition ARIZONA CAPITOL TIMES Arizona Tax

NON-PROFIT ORG. U.S. POSTAGE P A I D PHOENIX, AZ PERMIT #2184 An explanation of ARIZONA TAX RESEARCH ASSOCIATION 1814 W WASHINGTON STREET PHOENIX AZ 85007 2011 Edition ARIZONA CAPITOL TIMES Arizona Tax

IMPROPER PAYMENTS FOR EVALUATION AND MANAGEMENT SERVICES COST MEDICARE BILLIONS

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL IMPROPER PAYMENTS FOR EVALUATION AND MANAGEMENT SERVICES COST MEDICARE BILLIONS IN 2010 Daniel R. Levinson Inspector General May 2014

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL IMPROPER PAYMENTS FOR EVALUATION AND MANAGEMENT SERVICES COST MEDICARE BILLIONS IN 2010 Daniel R. Levinson Inspector General May 2014

CHAPTER 9. Employment Insurance Overpayments Human Resources and Skills Development Canada

CHAPTER 9 Employment Insurance Overpayments Human Resources and Skills Development Canada Performance audit reports This report presents the results of a performance audit conducted by the Office of the

CHAPTER 9 Employment Insurance Overpayments Human Resources and Skills Development Canada Performance audit reports This report presents the results of a performance audit conducted by the Office of the

ATTACHMENT II: SUMMARY OF GENERAL FUND RECEIPTS

ATTACHMENT II: SUMMARY OF SUMMARY OF GENERAL FUND REVENUE AND TRANSFERS IN Over the Category Percent Change Real Estate Taxes - Current and Delinquent $1,783,844,578 $1,892,239,118 $1,896,564,376 $1,893,919,994

ATTACHMENT II: SUMMARY OF SUMMARY OF GENERAL FUND REVENUE AND TRANSFERS IN Over the Category Percent Change Real Estate Taxes - Current and Delinquent $1,783,844,578 $1,892,239,118 $1,896,564,376 $1,893,919,994

TARRANT COUNTY HISTORIC SITE TAX EXEMPTION POLICY

TARRANT COUNTY HISTORIC SITE TAX EXEMPTION POLICY A. General Purpose and Objectives The purpose of this Policy is to encourage the rehabilitation and restoration of certain historic properties within Tarrant

TARRANT COUNTY HISTORIC SITE TAX EXEMPTION POLICY A. General Purpose and Objectives The purpose of this Policy is to encourage the rehabilitation and restoration of certain historic properties within Tarrant

SENIORS Clauses 41, 41B, 41C, 41C½

Mark E. Nunnelly Commissioner of Revenue Sean R. Cronin Senior Deputy Commissioner TAXPAYER S GUIDE TO LOCAL PROPERTY TAX EXEMPTIONS SENIORS Clauses 41, 41B, 41C, 41C½ The Department of Revenue (DOR) has

Mark E. Nunnelly Commissioner of Revenue Sean R. Cronin Senior Deputy Commissioner TAXPAYER S GUIDE TO LOCAL PROPERTY TAX EXEMPTIONS SENIORS Clauses 41, 41B, 41C, 41C½ The Department of Revenue (DOR) has

ANNUAL TAXPAYER ADVOCATE REPORT

2015 ANNUAL TAXPAYER ADVOCATE REPORT Calendar Year 2014Activity January 15, 2015 Vermont Department of Taxes 133 State Street PO Box 429 Montpelier, VT 05633-1401 Tel: 802-828-6848 Fax: 802-828-5787 Agency

2015 ANNUAL TAXPAYER ADVOCATE REPORT Calendar Year 2014Activity January 15, 2015 Vermont Department of Taxes 133 State Street PO Box 429 Montpelier, VT 05633-1401 Tel: 802-828-6848 Fax: 802-828-5787 Agency

RENT CONTROL. Chapter 169 RENT CONTROL. Establishment of Rent Leveling Board, Members, Appointments, and Terms.

RENT CONTROL Chapter 169 RENT CONTROL & 169-1. & 169-2. & 169-3. & 169-4. Definitions. Establishment of Rent Leveling Board, Members, Appointments, and Terms. Vacancies: Removal for Cause. Rent Leveling

RENT CONTROL Chapter 169 RENT CONTROL & 169-1. & 169-2. & 169-3. & 169-4. Definitions. Establishment of Rent Leveling Board, Members, Appointments, and Terms. Vacancies: Removal for Cause. Rent Leveling