Internal Guideline. Sustainable Mortgage Arrears Solutions

|

|

|

- Agatha Green

- 10 years ago

- Views:

Transcription

1 Internal Guideline Sustainable Mortgage Arrears Solutions Date: 24 September 2013 Updated: 13 June 2014

2 Contents 1. Executive Summary Sustainability Guideline Bank Policies, Procedures, Systems and Controls Assessment of Affordability Assessment of Temporary Arrangements Assessment of Term Extension and Capitalisation Solutions Assessment of Split Mortgage Solutions... 8 a. Treatment of the base loan of a split mortgage... 9 b. Treatment of future increase of income... 9 c. Treatment of term of warehoused part of split mortgage Medium-term restructures Other Requirements and Solutions Mortgage Solutions beyond retirement (updated 13 June 2014) Appendix

... 11 Appendix 1..13 2")

3 1. Executive Summary This paper has been prepared based on internal dialogue and discussion at Financial Stability Committee and provides internal guidance to supervisors as to the important factors to consider when assessing if the modifications provided by lenders are sustainable solutions for mortgage arrears cases. It is for use by Supervisory teams, in conjunction with the principles set out in the Mortgage Arrears Resolution Targets (MART) paper, when auditing the results of targets set in March However measurement of a bank s compliance with the Code of Conduct on Mortgage Arrears (CCMA) falls outside the scope of this document. These are internal guidelines - previously issued guidance to the banks of a more high-level nature remains in force and is attached at appendix 1. Sustainable solutions for both Private Dwelling Houses (PDH s) and Buy-to-let (BTL s) are discussed in this paper. Supervisory teams should find that the guidance provided for the different solutions in Section 2 applies to both PDH s and BTL s (with the possible exception of some elements of the split mortgage solutions related to security of tenure in the personal home). In March 2013 the Central Bank set a series of performance targets for banks in relation to the number of sustainable mortgage arrears solutions that are: proposed to customers in difficulty; concluded with customers; and being met by customers. Those targets will be monitored quarterly from June 2013 onward when the first targets with regard to proposed solutions apply. To provide assurance that the mortgage arrears solutions that banks conclude (and count in their targets) are truly sustainable, a series of supervisory audits are planned to consider the completeness, accuracy and validity of the outcomes reported by the specified credit institutions. This paper is designed to provide those carrying out such audits with additional guidance to determine what constitutes a sustainable solution. As the starting point for assessing solutions proposed by banks, the Central Bank will have regard to: 1. the Mortgage Arrears Resolution Process (MARP) as set out in the CCMA; 2. the Sustainability Guidelines issued to lenders in May 2012 as part of the Mortgage Arrears Resolution Strategy (MARS) project (appendix 1); and 3. the definition of sustainable solution set out in its publication Mortgage Arrears Resolution Targets (MART): a) An arrangement concluded under a bank s MARP in accordance with the CCMA, where the borrower is cooperating under the MARP and the bank has satisfied itself that the arrangement provides a sustainable solution which is likely to enable the customer to meet the original or, as appropriate, the amended terms of the mortgage over the full remaining life of the mortgage, including repayment of the original or an agreed revised principal sum where offered. This may include an interest only or other temporary solution for a period if it is likely that full repayment of the original or revised principal will be achieved over time, or where there is a payment plan to return the account to sustainability through the clearance of arrears. b) A personal insolvency arrangement effected under the Personal Insolvency Act 2012; or 3

falls outside the scope of this document.")

4 c) If an arrangement could not be reached or is not appropriate, that the PDH and BTL property securing the loan has been voluntarily sold or, failing that, any situation where a Specified Credit Institution takes possession of the property including by way of voluntary agreement with the borrower or by Court Order or otherwise Prudential considerations imply that no simple mechanical formula can substitute for a case-bycase approach, despite the fact that such an approach is time-consuming and resourceintensive. While sustainable solutions will therefore be arrived at on a case-by-case basis, there are some fundamental principles and considerations that arise for lenders from this definition: The affordability assessment of the borrower (see section 2.2) needs to be based on both their current and prospective future servicing capacity for all borrowings; assumed prospective future increases in the debt servicing ability of the borrower must be credible and conservative; Lenders need to apply a realistic valuation of the borrower s assets, in particular their property. This also applies to any assumption of potential asset price appreciation, as well as the estimated costs related to a potential foreclosure of property; Lenders need to use an appropriate interest rate when discounting future income flows, which should take account of the lender s cost of funds; Lenders must have adequate policies, procedures, systems and controls to assure itself that the range of solutions it is offering are indeed sustainable for the individual circumstances of the borrower; Lenders need to satisfy themselves that the solution will be effective for the full remaining life of the mortgage and take account not just of capacity to pay interest for an interim period but also to service the (revised) mortgage contract on a lasting basis. A sustainable solution must be likely to enable the customer to meet the original or, as appropriate, the amended terms of the mortgage over the full remaining life of the mortgage, including repayment of the original or an agreed revised principal sum where offered. (This is to be understood to include the specific treatment of the warehoused portion of the split mortgage as outlined above). The revised mortgage servicing terms may be conditional on borrower s income; Lenders therefore need to be able to satisfy themselves and demonstrate to the Central Bank that any temporary term arrangement is part of a sustainable solution because the borrower will have a sufficiently improved capacity to service the debt at the end of the temporary arrangement; In endeavouring to recover mortgage debt owing, lenders should consider the consequences of non-payment of unsecured debt by the borrower, particularly in cases where non-payment of unsecured debt could impact on the employment and earning capacity of the borrower; Each case is different, depending in particular on the circumstance and prospects of the borrower. This means that finding a sustainable solution that fits each case is challenging and time-consuming; no simple mechanical formula can substitute for a case-by-case approach. Yet experience shows that delays in treating loan arrears worsen the outcome for both borrower and lender; It is understood that the process of putting a sustainable solution in place may require a trial period of payment on a revised schedule before all of the elements of the solution are confirmed; and 4

5 Cooperation 1 by the borrower is essential to sustainability of a mortgage. These key considerations have been incorporated into the guidelines set out in section 2. 1 As defined in the CCMA where the mortgage loan of a borrower is secured by their primary residence. 5

6 2. Sustainability Guideline 2.1. Bank Policies, Procedures, Systems and Controls Banks should have adequate policies, procedures, systems and controls documented and available for review by the Central Bank that describe: the types of solutions that are available to borrowers; the criteria that are used to establish whether they are sustainable for an individual borrower s circumstances; and the reasoning used to establish such sustainability. These policies, procedures, systems and controls should also describe how lenders formally review the appropriateness of that solution for the borrower and the review periods for each type of solution available. The Central Bank will rigorously assess banks performance against the targets (including whether genuinely sustainable solutions have been offered). Lenders must maintain an audit trail that captures the inputs; outputs and rationale for option(s) offered to borrowers evidencing that a solution is sustainable. Lenders must document key assumptions in relation to: Current and future income levels including income increases; Current and future expenditure levels; Repayment levels (increases / step-ups etc.) over the life of solutions distinguishing between interest and principal payments; and Future interest rates, foreclosure costs, collateral and other asset valuation and asset appreciation. Lenders should have a consistent approach to such assessments and application of decision trees to support their consideration of a sustainable solution to offer an individual borrower Assessment of Affordability The affordability assessment of the borrower needs to be based on both their current and prospective future servicing capacity for all borrowings. Assumed prospective future increases in the debt servicing ability of the borrower must be credible and conservative. Current affordability assessment should be based on verified borrower income and expenditure levels. Lenders should satisfy themselves, and be able to demonstrate, that appropriate conservatism has been applied in relation to the variable elements of current income that are taken into account. For example, variable elements of pay and/or rental income etc. should be discounted to reflect the possibility that they will not be realised. Any assumptions should be documented in the audit trail. 6

7 Future income increases should only be taken into account where there is good reason to expect that those increases will be realised. Lenders should also satisfy themselves, and be able to demonstrate, that adequate conservatism has been applied in considering the extent to which future increases are taken into account. Unless specific information exists to the contrary, assumed salary increases, bonuses, overtime, career progression, increases in rental income and any other increases should not be out of line with industry/sector/market norms and may need to be discounted to reflect the risk that they will not be fully realised. Assessment of borrower expenditure levels should take account of likely future expenditure increases. At a minimum lenders should be able to demonstrate that increases in line with inflation have been considered but lenders should also be able to demonstrate that increases specific to the borrower and their unique circumstances have been taken into account (for example an increase in dependents or future education costs etc.) Where future and specific expenditure decreases are being taken into account (dependents exiting education and entering the workforce for example) lenders should be able to demonstrate that a conservative approach has been taken in considering those decreases. Where a borrower is required to reduce expenditure levels in order to service mortgage debt repayment, lenders must satisfy themselves, and be able to demonstrate, that those reductions are plausible and practical over the life of the revised solution and that those reductions will not place an unreasonable burden on the borrower. Lenders should ensure, and be able to demonstrate, that, where a revised solution includes increases in amortisation schedule / step-ups in repayment, there is good reason to expect that those increases can be met by the borrower Assessment of Temporary Arrangements Temporary arrangements 2 will only be considered sustainable where the bank has satisfied itself (and can demonstrate to the Central Bank) that the borrower s circumstances are likely to change such that the original (or agreed modified) terms of the mortgage can be fully serviced commencing from the end of the agreed period over the remaining life of the mortgage. Examples of such situations include but are not limited to the borrower/s returning to full-time paid employment form career break, parental leave, long-term sick leave or maternity leave. These situations are likely to involve: An assessment that certain short-term expenses are likely to cease or reduce; and/or An assessment that there is good reason to expect that household income will increase to improve debt serviceability. 3 While such temporary forbearance will be sufficient to assist many borrowers experiencing only temporary difficulties, there are other cases where temporary forbearance is not a sustainable solution and for which a more lasting or permanent 4 solution will be necessary. 2 Temporary solutions are those designed to have a specific term and which will expire at some point in the future, for example a sixmonth interest only restructure 3 This assessment should take account of specific borrower circumstances such as education level, age, length of unemployment and specific skills. Any assumptions used, including assumptions around re-employment, should be realistic and clearly captured in the audit trail by the lender. 4 Permanent restructures are those which are point in time events and can never expire, for example, term extension. 7

8 Some examples of short/medium term forbearance at reduced payment levels which will not be counted towards the sustainable solution targets include: Interest only (or reduced payment) arrangements agreed for short or medium terms where the borrower s level of affordability and repayment capacity at the end of this term has not been assessed; Arrangements in which assessment has not addressed what the borrower s required level of payment at the end of the interest only (or reduced repayment) period will increase to; Arrangements in which assessment has not addressed (on the basis of tangible evidence) the likelihood of a change in the borrowers circumstances which will allow this increased level of payment; and Arrangements in which future increased payments typically dependent on a generic hope that the borrowers situation will improve, without a specific identified factor which can support this Assessment of Term Extension and Capitalisation Solutions The Central Bank will typically consider a term extension or capitalisation solution (or combination of both) to be sustainable only where: For a term extension, the borrower s age has been taken into account. In this regard, if the borrower is subject to a compulsory retirement age, for a mortgage extension beyond that term such extension will only considered sustainable where the lender has assessed and can demonstrate and evidence that the borrower can, through pension or other sources of verified income, service the revised loan repayments to maturity on an affordable basis. An overall ceiling of 70 years of age will apply for the Central Bank to consider a term extension sustainable unless there is firm evidence that an older age limit can apply; For the capitalisation of arrears, the lender has assessed and can evidence that the borrower s verified income and expenditure levels are sufficient to enable them service the revised loan repayment on an affordable basis for the duration of revised repayment schedule and the borrower has been performing against the revised arrangement for 6 months before arrears are capitalised; and For either solution, the lender can demonstrate that the customer has been made fully aware of the implications of a term extension / the capitalisation of arrears in terms of revised repayment, revised loan maturity and any additional interest and charges (above the original loan terms) that will apply. A term extension or capitalisation that includes increases in repayment level over time will not be considered sustainable unless the lender can demonstrate that a verifiable, or otherwise credible and conservative, cause exists to believe that the borrower will be in a position to meet those repayment levels (see section 2.2 Assessment of Affordability) Assessment of Split Mortgage Solutions The Central Bank is concerned that lenders persist in relying on temporary forbearance measures even where a demonstrable ability of the borrower to resume the original contractual 8

the likelihood of a change in the borrowers circumstances which will allow this increased level of payment; and Arrangements in which future increased payments typically dependent")

9 repayments at the conclusion of this forbearance term is unlikely. Therefore, where the borrower is unable to service fully the mortgage payments but where there is some reasonable prospect of the borrower s circumstances improving over a longer term, a split-mortgage solution may be considered as offering a sustainable solution. In the case of PDH loans, a split mortgage can allow the borrower the opportunity to remain in their home, while enabling the lender to recover an additional portion of the loan should the borrower s circumstances improve. A split mortgage divides the sum owed into a base loan ( Part A) and a warehoused loan (Part B). When determining a sustainable solution the lender must attempt to match a solution from the available range that best matches a borrower s current and future affordability. Because of this, various designs of split mortgage may be considered as sustainable solutions by the Central Bank depending on the circumstances of the intended cohort. Sustainability of a split mortgage will be assessed by the Central Bank inter alia with regard both to the affordability of the unwarehoused debt payment schedule and with regard to the treatment of the warehoused loan at maturity. Transparency to a borrower of the terms and conditions of a split mortgage at the outset of such a solution is essential to the sustainability of this solution, in particular how the bank will treat future increase of income and the repayment of the warehoused loan at maturity. a. Treatment of the base loan of a split mortgage The Central Bank will typically consider a split mortgage sustainable if the new term and interest rate on the base loan (Part A) result in a newly contracted payment schedule which leaves the borrower with sufficient funds in line with established norms. In order to reduce the incentive for a borrower to reject a particular offer in the hope of receiving something better through the PIA process, lenders will want to consider how the schedule offered compares (i.e. in terms of monthly disposal income post debt repayment). More generally, for a split mortgage to be considered sustainable, the lender should be able to demonstrate that, given their current and prospective economic circumstances, the borrower will be able to service Part A fully throughout the term or, failing that, will be able to cover any servicing shortfall of Part A from other resources that the lender has a good reason to expect the borrower will possess at the end of term. As the split is designed to help the borrower stay in the family home, in the event of a sale during the term of the mortgage, the lender and borrower will renegotiate the terms of the restructure. b. Treatment of future increase of income The Central Bank will typically only consider a split mortgage to be sustainable if provision is made for any future increase in the borrower s income to be shared in a reasonable proportion between the borrower and the bank. In considering this, the bank should be conscious of how such increase in income would be treated under a Personal Insolvency Agreement. c. Treatment of term of warehoused part of split mortgage In order for a split mortgage to be considered sustainable the lender must inform the borrower regarding the repayment of the unpaid warehoused loan at maturity. The bank must set-out the potential options it may deploy in recovery of the outstanding debt at the maturity of the loan. 9

10 Any such repayment must consider the circumstances of the borrower at that time and the ability of the borrower to acquire suitable alternative accommodation if required. In particular; The loan arrangements should state the percentage of any lump sums received by the borrower that must be paid towards reduction of the warehouse loan. To be deemed sustainable the cooperating borrower should not be made homeless at the loan maturity. Options for recovery of debt that would be deemed sustainable include: (i) Borrower is required to dispose of the property but permitted to retain borrowings or proceeds sufficient to acquire alternative suitable accommodation (trade down). There should be disclosure regarding the % of value of disposed property that will be available for purchase of trade-down accommodation.(ii) Borrower is provided with right of tenure with recovery of all outstanding debt on disposal of the property e.g. from the borrower s estate after death, if not sold earlier. The lender may determine other suitable sustainable arrangements that fulfil the same principles regarding suitable accommodation such as debt/equity swaps or other structures. A split mortgage solution which does not ensure the sustainable treatment of the warehoused part of the mortgage, as outlined above or with other measures of equivalent effect, will not be counted as a sustainable solution in the context of the targets Medium-term restructures Medium-term Restructures may be created that substantially change the payment structure for a defined period but they will not entirely resolve the borrowers debt position and by itself would not be regarded as a sustainable solution. For such restructures to be regarded as sustainable they must contain clauses to state that at the end of term of the restructure a cooperating borrower will retain the loan (and property), that future payments are matched with borrower affordability and the bank must set-out the potential options it may deploy in recovery of any potential outstanding debt at the maturity of the loan Other Requirements and Solutions Other than for temporary solutions (see section 2.3) forming part of a sustainable solution, revised repayments should be profiled (between interest and capital elements) in the usual manner of mortgage repayments. This requirement applies across the life of the revised mortgage and, therefore, precludes the introduction of repayment step-ups in a long term solution unless the lender, in line with affordability assessment per section 2.2, can demonstrate good reason to expect a future increase in borrower income / reduction in expenditure that would enable a step-up. The lender must also be able to demonstrate that the borrower has been made fully aware of the scale and timing of the step-up(s). In all cases, a solution will only be considered sustainable where the resolution of outstanding / historic arrears is fully addressed. Situations will arise in which lenders determine that borrower expenditure levels are beyond the norm and that the existing mortgage repayment would otherwise be affordable. In such cases lenders will advise borrowers that forbearance has been declined that the borrower must commence meeting current repayments. Such outcomes will be considered sustainable where; 10

Borrower is required to dispose of the property but permitted to retain borrowings or proceeds sufficient to acquire")

11 The lender can demonstrate that it has made an individual determination, based on assessment, of the expenditures that could be reduced and has communicated these to the borrower; and The lender has communicated to the customer an affordable repayment schedule, again based on demonstrable assessment, to resolve any outstanding arrears balance. In such circumstance, should the borrower reject / refuse to comply with that decision (and barring a successful appeal by the borrower), the lender may commence legal proceedings subject to the CCMA provisions. Situations will arise, and notably where a borrower is not cooperating or a sustainable solution (such as those outlined in this document, mortgage-torent, trade-down, debt write-down or other sustainable solutions) cannot be achieved and where voluntary surrender, voluntary sale or legal action for repossession may be required. In the case of voluntary sales or surrenders the lender must clearly state how it will treat the outstanding debt, after the property is sold, and any arrangements proposed for the continued repayment of such debt. For example, clearly stating the borrower will continue to be liable for any shortfall arising (where that is the case), and payments should be based on what the borrower can afford to pay and contingent on the borrower meeting certain agreed hurdles. If a borrower is, inter alia, insolvent then he/she may apply for a Personal Insolvency Arrangement (PIA). These outcomes, while sustainable from the perspective of the targets, should be a last resort and only where the lender has been unable to agree a sustainable loan modification solution or has concluded that one is not appropriate in the circumstances. In all of these cases, the long-term interests of both borrower and lender are better served by determining, agreeing and adhering to a sustainable payment plan. 2.8 Mortgage Solutions beyond retirement (updated 13 June 2014) On 13 June 2014 the Central Bank provided a clarification to the banks covered by the Mortgage Arrears Resolution Targets that there are instances in which sustainable mortgage arrears solutions may extend into the borrower s retirement. Furthermore, borrowers and banks may agree, on a case by case basis, to lifetime tenure of the home in instances in which the anticipated proceeds from the estate are sufficient to pay off the outstanding debt 1. In recent audits of banks mortgage restructuring solutions, the Central Bank noted variations in the interpretation of the guidelines provided by the Central Bank insofar as: 1. Most banks apply an upper age limit rule of 70 on term extensions in accordance with guidelines published by the Central Bank. The guidelines set out the circumstances in which evidence of affordability to service repayments to maturity will be considered sustainable. An older age limit can apply to restructure arrangements in cases where there is appropriate evidence to support it 2. 1 The outstanding debt is the original debt less any amount repaid less any amount agreed by the bank to be written-off now or in the future. The amount of writeoff need not be a specific amount if it refers to a residual balance after disposal of the property at the end of tenure. 2 In cases where both the borrower and the bank are in agreement, a borrower may continue to make payments from on-going pension benefits. 11

12 2. Banks have been reluctant to consider solutions which involve recovery of residual loan balances after the death of a borrower from his/ her estate. The Central Bank is of the view that, where the borrower wishes to remain in his/ her home, long-term payment arrangements with lifetime tenure may be sustainable where the sale of the property provides sufficient surplus funds on death to redeem the outstanding mortgage balance 3. This guidance is issued in the limited context of the resolution of distressed loans, where the Central Bank recognises that, in many instances, banks and borrowers are striving to solve very difficult situations. Moreover, the Central Bank considers that, even in that context, these solutions will apply only in limited circumstances. The Central Bank requires transparency to be provided to the borrower in relation to the terms and conditions at the outset of any such solutions and borrowers must be treated in accordance with the Central Bank s Consumer Protection Code and the Code of Conduct on Mortgage Arrears where applicable. The implications of the solution in terms of payment schedules, stressed interest rate increases, additional interest and charges (above the original loan terms) and future redemption obligations must be clearly communicated in a new contract with the borrower in order for it to be considered sustainable. The lender must also explain the advantages and disadvantages of the offer made by reference to the circumstances of the individual borrower 4. 3 Banks must be able to demonstrate that they have assessed borrowers ability to meet the payments post retirement based on appropriately conservative assumptions. 4 The CCMA provides the process by which a lender is required to establish the appropriate solution for each borrower's individual circumstances. Provision 39 of the CCMA lists a number of alternative repayment arrangement types and recognises interest only repayments on the mortgage for a specified period of time as a solution which may be viable for certain borrowers. Where a lender offers such an arrangement, it must be satisfied of the sustainability and appropriateness of the solution for the borrower over the full term of the mortgage including the borrower s ability to repay the capital outstanding in future. Provision 40 of the CCMA further requires the lender to document its considerations of each option examined, including the reasons why the option is appropriate and sustainable. Under provision 42, a lender must explain in the offer letter the reasons why the alternative arrangement offered is considered to be appropriate and sustainable and must explain the advantages and disadvantages of the offer made together with details of any residual mortgage debt remaining at the end of an alternative repayment arrangement and owed by the borrower. If a lender does not offer a borrower an alternative repayment arrangement, for example, where it is concluded that the mortgage is not sustainable, the lender must provide the reasons for this decision to the borrower in accordance with provision 45 of the CCMA. 12

13 Appendix 1 Guidance previously issued to banks on sustainability: Page 1 of 3 13

14 Page 2 of 3 14

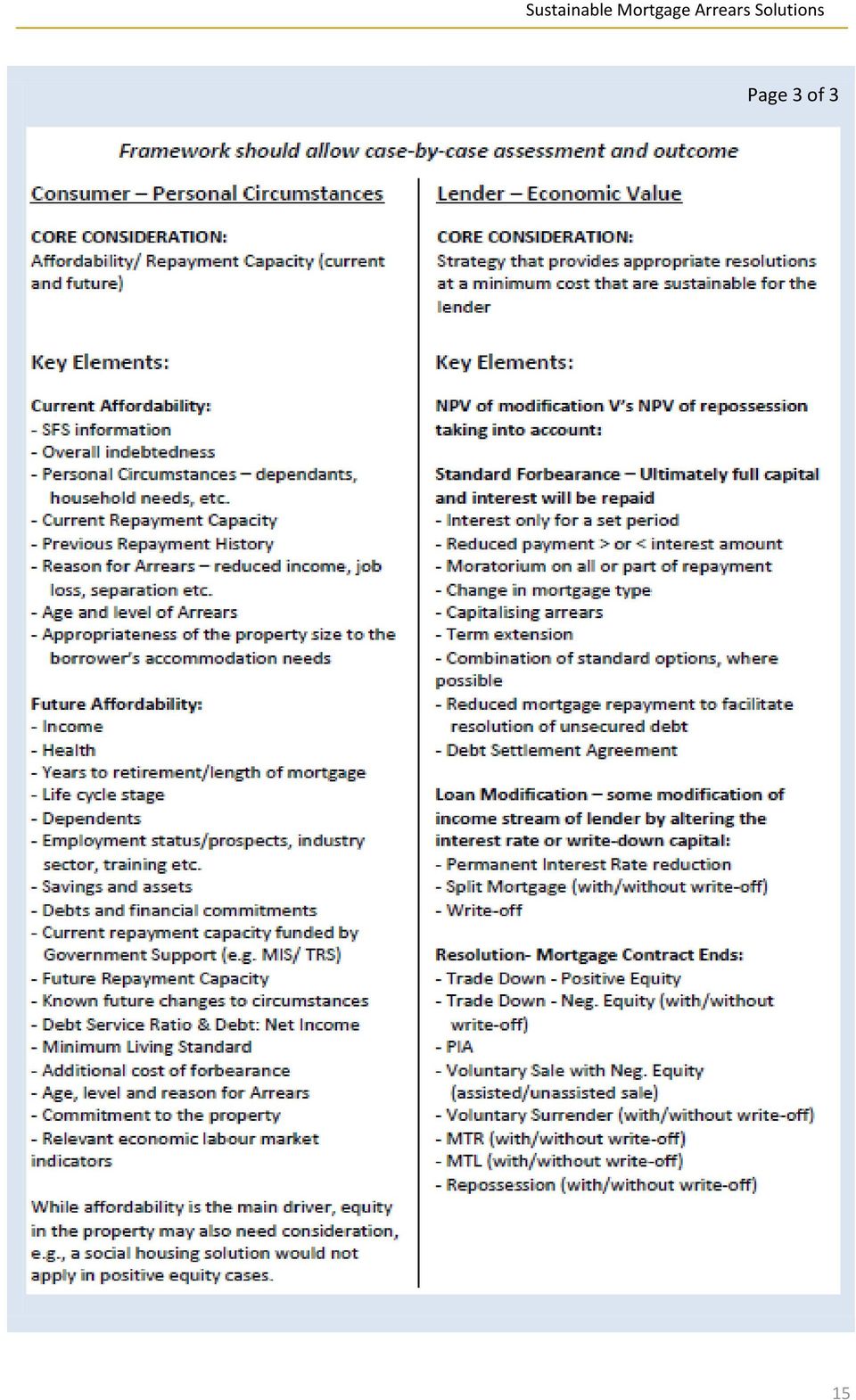

15 Page 3 of 3 15

Mortgage Arrears Resolution Process (MARP) Booklet. Important information for customers experiencing financial difficulties

Booklet. Important information for customers experiencing financial difficulties") Mortgage Arrears Resolution Process (MARP) Booklet Important information for customers experiencing financial difficulties The Mortgage Arrears Resolution Process (MARP) We at Start Mortgages recognise

Mortgage Arrears Resolution Process (MARP) Booklet Important information for customers experiencing financial difficulties The Mortgage Arrears Resolution Process (MARP) We at Start Mortgages recognise

POLICY FOR THE BREATHING SPACE SCHEME

POLICY FOR THE BREATHING SPACE SCHEME PREFACE The Council is participating in a regional scheme called Breathing Space. The scheme facilitates the provision of loans in accordance with powers given under

POLICY FOR THE BREATHING SPACE SCHEME PREFACE The Council is participating in a regional scheme called Breathing Space. The scheme facilitates the provision of loans in accordance with powers given under

M O R T G A G E S E R V I C E S A borrower s guide

M O R T G A G E S E R V I C E S A borrower s guide For most of us, house purchase is our largest financial transaction and the associated mortgage the biggest financial commitment. Repayment of the mortgage

M O R T G A G E S E R V I C E S A borrower s guide For most of us, house purchase is our largest financial transaction and the associated mortgage the biggest financial commitment. Repayment of the mortgage

STANDARD CONDITIONS FOR INDIVIDUAL VOLUNTARY ARRANGEMENTS

Protocol Annex 4 STANDARD CONDITIONS FOR INDIVIDUAL VOLUNTARY ARRANGEMENTS Produced by the IVA FORUM Revised November 2013 For use in Proposals issued on or after 1 January 2014 TABLE OF CONTENTS FOR STANDARD

Protocol Annex 4 STANDARD CONDITIONS FOR INDIVIDUAL VOLUNTARY ARRANGEMENTS Produced by the IVA FORUM Revised November 2013 For use in Proposals issued on or after 1 January 2014 TABLE OF CONTENTS FOR STANDARD

SCHEDULE OF OPTIONS AVAILABLE TO INDIVIDUALS IN FINANCIAL DIFFICULTY

SCHEDULE OF OPTIONS AVAILABLE TO INDIVIDUALS IN FINANCIAL DIFFICULTY The most common options available to individuals who are unable to pay their debts are:- 1 Do nothing. 2 Obtain an unsecured debt consolidation

SCHEDULE OF OPTIONS AVAILABLE TO INDIVIDUALS IN FINANCIAL DIFFICULTY The most common options available to individuals who are unable to pay their debts are:- 1 Do nothing. 2 Obtain an unsecured debt consolidation

Keeping your home: home owners

Keeping your home: home owners What help can I get to pay my mortgage? What should I do if I can t pay my mortgage? Can a lender repossess my home? provided by the Citizens Information Board provided by

Keeping your home: home owners What help can I get to pay my mortgage? What should I do if I can t pay my mortgage? Can a lender repossess my home? provided by the Citizens Information Board provided by

Mortgage Arrears Resolution Process

Mortgage Arrears Resolution Process AIB Mortgage Arrears Resolution Process A practical guide for AIB mortgage customers. Drop in to any branch 1890 252 008 www.aib.ie Working together to find resolutions.

Mortgage Arrears Resolution Process AIB Mortgage Arrears Resolution Process A practical guide for AIB mortgage customers. Drop in to any branch 1890 252 008 www.aib.ie Working together to find resolutions.

Debt Negotiations Loan arrears and the benefit of early and appropriate engagement with banks

Debt Negotiations Loan arrears and the benefit of early and appropriate engagement with banks Paul Kerr 28 th April 2014 First Choice Financial Service Ltd www.firstchoiceltd.ie Introduction Lender with

Debt Negotiations Loan arrears and the benefit of early and appropriate engagement with banks Paul Kerr 28 th April 2014 First Choice Financial Service Ltd www.firstchoiceltd.ie Introduction Lender with

Secured loans - A guide

Secured loans - A guide WHAT IS A SECURED LOAN? A secured loan is a loan in which the borrower pledges some asset such as a car or property as collateral for the loan, which then becomes a secured debt

Secured loans - A guide WHAT IS A SECURED LOAN? A secured loan is a loan in which the borrower pledges some asset such as a car or property as collateral for the loan, which then becomes a secured debt

D1.03: MORTGAGE REPAYMENT OVERVIEW

D1.03: MORTGAGE REPAYMENT OVERVIEW SYLLABUS Repayment mortgages Repayment profile Interest only mortgages Full and low cost endowment mortgages Unit-linked endowment mortgages ISA mortgages Pension mortgages

D1.03: MORTGAGE REPAYMENT OVERVIEW SYLLABUS Repayment mortgages Repayment profile Interest only mortgages Full and low cost endowment mortgages Unit-linked endowment mortgages ISA mortgages Pension mortgages

STANDARD CONDITIONS FOR INDIVIDUAL VOLUNTARY ARRANGEMENTS. Produced by the IVA FORUM

Protocol Annex 4 STANDARD CONDITIONS FOR INDIVIDUAL VOLUNTARY ARRANGEMENTS Produced by the IVA FORUM Revised November 2013 For use in proposals issued on or after 1 January 2014 TABLE OF CONTENTS FOR STANDARD

Protocol Annex 4 STANDARD CONDITIONS FOR INDIVIDUAL VOLUNTARY ARRANGEMENTS Produced by the IVA FORUM Revised November 2013 For use in proposals issued on or after 1 January 2014 TABLE OF CONTENTS FOR STANDARD

In Debt? Dealing with your creditors Call: 0800 157 7330 or 01257 251319 www.debtproblemsuk.com

Debtfocus Business Recovery & Insolvency Ltd In Debt? Dealing with your creditors Call: 0800 157 7330 or 01257 251319 www.debtproblemsuk.com Content highlights Before you read this guide in detail, you

Debtfocus Business Recovery & Insolvency Ltd In Debt? Dealing with your creditors Call: 0800 157 7330 or 01257 251319 www.debtproblemsuk.com Content highlights Before you read this guide in detail, you

Guideline for the Measurement, Monitoring and Control of Impaired Assets

Guideline for the Measurement, Monitoring and Control of Impaired Assets FINAL TABLE OF CONTENTS 1 INTRODUCTION... 1 2 PURPOSE... 1 3 INTERPRETATION... 2 4 IMPAIRMENT RECOGNITION AND MEASUREMENT POLICY...

Guideline for the Measurement, Monitoring and Control of Impaired Assets FINAL TABLE OF CONTENTS 1 INTRODUCTION... 1 2 PURPOSE... 1 3 INTERPRETATION... 2 4 IMPAIRMENT RECOGNITION AND MEASUREMENT POLICY...

Mortgage Arrears in Ireland: Introducing the Enhanced Quarterly Statistics

8 Mortgage Arrears in Ireland: Introducing the Jean Goggin * Abstract This article introduces the recently expanded Residential Mortgage Arrears and Repossessions Statistics published by the Central Bank

8 Mortgage Arrears in Ireland: Introducing the Jean Goggin * Abstract This article introduces the recently expanded Residential Mortgage Arrears and Repossessions Statistics published by the Central Bank

Mortgages and Home Finance: Conduct of Business Sourcebook. Chapter 11. Responsible lending, and responsible financing of home purchase plans

Mortgages and Home Finance: Conduct of Business Sourcebook Chapter esponsible lending, and responsible of MCOB : esponsible lending, and responsible of Section.6 : esponsible lending and.6 esponsible lending

Mortgages and Home Finance: Conduct of Business Sourcebook Chapter esponsible lending, and responsible of MCOB : esponsible lending, and responsible of Section.6 : esponsible lending and.6 esponsible lending

Certificate in Regulated Equity Release

Unit 1: Fundamentals of Equity Release Certificate in Regulated Equity Release Attainment Level knowledge of: K1 Definition of a Home Reversion (HR) plan & alternative methods of equity release/capital

Unit 1: Fundamentals of Equity Release Certificate in Regulated Equity Release Attainment Level knowledge of: K1 Definition of a Home Reversion (HR) plan & alternative methods of equity release/capital

Mortgage & Home Equity Reporting Guidelines In Response to Current Financial Conditions

Mortgage & Home Equity Reporting Guidelines In Response to Current Financial Conditions General Reporting Guidelines Report accounts in the standard Metro 2 Format. Refer to the Credit Reporting Resource

Mortgage & Home Equity Reporting Guidelines In Response to Current Financial Conditions General Reporting Guidelines Report accounts in the standard Metro 2 Format. Refer to the Credit Reporting Resource

Mortgages Guide. From http://limetreefs.co.uk 1

Mortgages Guide Mortgages revealed... The explanations below are intended to give you an insight into some of the more common terms associated with the mortgage process. Repaying the Mortgage Whichever

Mortgages Guide Mortgages revealed... The explanations below are intended to give you an insight into some of the more common terms associated with the mortgage process. Repaying the Mortgage Whichever

PIA. Guide to a Personal Insolvency Arrangement

nseirbhís Dócmhainneachta na héirea PIA Guide to a Personal Insolvency Arrangement n Insolvency Service of Ireland A Personal Insolvency Arrangement enables an eligible insolvent debtor to reach agreement

nseirbhís Dócmhainneachta na héirea PIA Guide to a Personal Insolvency Arrangement n Insolvency Service of Ireland A Personal Insolvency Arrangement enables an eligible insolvent debtor to reach agreement

Personal Debt Solutions (Dealing With Debt) An Essential Guide by Debt Advisory Services (Scotland)

An Essential Guide by Debt Advisory Services (Scotland)") Personal Debt Solutions (Dealing With Debt) An Essential Guide by Debt Advisory Services (Scotland) Why you should read this guide Many people living in Scotland, through no fault of their own, are struggling

Personal Debt Solutions (Dealing With Debt) An Essential Guide by Debt Advisory Services (Scotland) Why you should read this guide Many people living in Scotland, through no fault of their own, are struggling

A guide to Repossession

A guide to Repossession A guide explaining how to deal with the threat of Property Repossession Contents Part 1 Overview 4 Guide overview Part 2 Repossession 5 Root causes of property repossession Mortgage

A guide to Repossession A guide explaining how to deal with the threat of Property Repossession Contents Part 1 Overview 4 Guide overview Part 2 Repossession 5 Root causes of property repossession Mortgage

The Straightforward. Consumer IVA Protocol. 2014 version

The Straightforward Consumer IVA Protocol 2014 version Effective from January 2014 1 IVA PROTOCOL Straightforward consumer individual voluntary arrangement hereinafter referred to as a Protocol Compliant

The Straightforward Consumer IVA Protocol 2014 version Effective from January 2014 1 IVA PROTOCOL Straightforward consumer individual voluntary arrangement hereinafter referred to as a Protocol Compliant

Relate. Personal Insolvency Bill 2012. August 2012. New arrangements for dealing with debt. Contents

August 2012 Volume 39: Issue 8 ISSN 0790-4290 Contents Relate The journal of developments in social services, policy and legislation in Ireland Page No. 1 Personal Insolvency Bill 2012 This issue deals

August 2012 Volume 39: Issue 8 ISSN 0790-4290 Contents Relate The journal of developments in social services, policy and legislation in Ireland Page No. 1 Personal Insolvency Bill 2012 This issue deals

Rights of the borrower (mortgagor) Negotiating with the lender. Mortgage rescue schemes. Can I get any help with my mortgage

Negotiating with the lender. Mortgage rescue schemes. Can I get any help with my mortgage") Contents The need to act quickly Available options Rights of the borrower (mortgagor) Negotiating with the lender Going to court Mortgage rescue schemes Secured loans Can I get any help with my mortgage

Contents The need to act quickly Available options Rights of the borrower (mortgagor) Negotiating with the lender Going to court Mortgage rescue schemes Secured loans Can I get any help with my mortgage

Banking & Finance - Bulletin 60 December 2008

Banking & Finance - Bulletin 60 December 2008 In this issue: Breaking a Fixed Rate Loan our approach to break costs Direct Debits on Transaction Accounts Maladministration and Secured Lending Dealing with

Banking & Finance - Bulletin 60 December 2008 In this issue: Breaking a Fixed Rate Loan our approach to break costs Direct Debits on Transaction Accounts Maladministration and Secured Lending Dealing with

BANK OF NEW ZEALAND FACILITY MASTER AGREEMENT. Important information about. Your home loan

BANK OF NEW ZEALAND FACILITY MASTER AGREEMENT Important information about Your home loan Contents PAGE 2 Introduction Agreeing a facility 3 Changes to facilities Insurance 4 Pre-conditions This document

BANK OF NEW ZEALAND FACILITY MASTER AGREEMENT Important information about Your home loan Contents PAGE 2 Introduction Agreeing a facility 3 Changes to facilities Insurance 4 Pre-conditions This document

A GUIDE ON FINANCIAL LEASING I. INTRODUCTION

NATIONAL BANK OF SERBIA A GUIDE ON FINANCIAL LEASING I. INTRODUCTION The purpose of this Guide is to provide basic information on financial leasing as a way to finance purchase of equipment and other fixed

NATIONAL BANK OF SERBIA A GUIDE ON FINANCIAL LEASING I. INTRODUCTION The purpose of this Guide is to provide basic information on financial leasing as a way to finance purchase of equipment and other fixed

Debt Options Information guide

Debt Options Information guide Debt & Money Advice Support CIC (DMAS CIC) is authorised and regulated by the Financial Conduct Authority FRN: 631799. A company registered in England & Wales 9203918. 1

Debt Options Information guide Debt & Money Advice Support CIC (DMAS CIC) is authorised and regulated by the Financial Conduct Authority FRN: 631799. A company registered in England & Wales 9203918. 1

IVA PROTOCOL Straightforward consumer individual voluntary arrangement

IVA PROTOCOL Straightforward consumer individual voluntary arrangement Purpose of the protocol 1.1 The purpose of the protocol is to facilitate the efficient handling of straightforward consumer individual

IVA PROTOCOL Straightforward consumer individual voluntary arrangement Purpose of the protocol 1.1 The purpose of the protocol is to facilitate the efficient handling of straightforward consumer individual

PRA Retail Credit Risk Non-UK Portfolio Quality Return January 2015

PRA Retail Credit Risk Non-UK Portfolio Quality Return January 2015 Guidance Notes Purpose of the Template The purpose of this template is to provide the PRA with a consistent dataset to help form an assessment

PRA Retail Credit Risk Non-UK Portfolio Quality Return January 2015 Guidance Notes Purpose of the Template The purpose of this template is to provide the PRA with a consistent dataset to help form an assessment

The Standard Debt Settlement Arrangement. Protocol. July 2014 version

The Standard Debt Settlement Arrangement Protocol July 2014 version Effective from 14 July 2014 TABLE OF CONTENTS Purpose and scope of the Protocol 3 1. Background and purpose of the Protocol 3 2. Scope

The Standard Debt Settlement Arrangement Protocol July 2014 version Effective from 14 July 2014 TABLE OF CONTENTS Purpose and scope of the Protocol 3 1. Background and purpose of the Protocol 3 2. Scope

DSA. Guide to a Debt Settlement Arrangement

nseirbhís Dócmhainneachta na héirea DSA Guide to a Debt Settlement Arrangement n Insolvency Service of Ireland A Debt Settlement Arrangement enables an eligible insolvent debtor to reach agreement with

nseirbhís Dócmhainneachta na héirea DSA Guide to a Debt Settlement Arrangement n Insolvency Service of Ireland A Debt Settlement Arrangement enables an eligible insolvent debtor to reach agreement with

WEYBRIDGE FINANCIAL SERVICES EQUITY RELEASE QUESTIONNAIRE

WEYBRIDGE FINANCIAL SERVICES EQUITY RELEASE QUESTIONNAIRE PERSONAL DETAILS Title: Mr/Mrs/Miss/Ms/Other Surname First Name(s) Date of Birth Nationality Marital Status Previous/Former (e.g. Maiden) Name

WEYBRIDGE FINANCIAL SERVICES EQUITY RELEASE QUESTIONNAIRE PERSONAL DETAILS Title: Mr/Mrs/Miss/Ms/Other Surname First Name(s) Date of Birth Nationality Marital Status Previous/Former (e.g. Maiden) Name

Tax & Duty Manual. Procedures for Personal Insolvency Caseworking. Collector-General s Office

Tax & Duty Manual Procedures for Personal Insolvency Caseworking Collector-General s Office Updated November 2015 Table of Contents 1. Background Legislation...4 2. Procedures for Dealing with Personal

Tax & Duty Manual Procedures for Personal Insolvency Caseworking Collector-General s Office Updated November 2015 Table of Contents 1. Background Legislation...4 2. Procedures for Dealing with Personal

Considerations for Troubled Debt Restructuring Identification of Loans August 2011

Considerations for Troubled Debt Restructuring Identification of Loans August 2011 Introduction This document is intended to provide examiners with a general overview of the judgments required by an institution

Considerations for Troubled Debt Restructuring Identification of Loans August 2011 Introduction This document is intended to provide examiners with a general overview of the judgments required by an institution

HOME LOAN GENERAL OFFER CONDITIONS (Mortgage Broker Introduction) with effect from 14th March 2016

with effect from 14th March 2016") These Conditions apply to Your Loan. Other terms and conditions are in the Loan Security. When reading these Conditions You will notice the use of technical and legal words that can be identified by their

These Conditions apply to Your Loan. Other terms and conditions are in the Loan Security. When reading these Conditions You will notice the use of technical and legal words that can be identified by their

Principles for the Reporting of Arrears, Arrangements and Defaults at Credit Reference Agencies

Principles for the Reporting of Arrears, Arrangements and Defaults at Credit Reference Agencies Foreword by the Information Commissioner s Office The Information Commissioner s Office (ICO) published Data

Principles for the Reporting of Arrears, Arrangements and Defaults at Credit Reference Agencies Foreword by the Information Commissioner s Office The Information Commissioner s Office (ICO) published Data

Debt Solution Overview 2

Contents Debt Solution Overview 2 Debt Management What is a Debt Management Plan? 3 What are the benefits of a Debt Management Plan? 3 How does it work? 3 What debts can be included in a plan? 4 What debts

Contents Debt Solution Overview 2 Debt Management What is a Debt Management Plan? 3 What are the benefits of a Debt Management Plan? 3 How does it work? 3 What debts can be included in a plan? 4 What debts

Your Mortgage Guide. The Exchange. Property Services Mortgage Services Letting & Management Services Conveyancing Services

The Exchange Property Services Mortgage Services Letting & Management Services Conveyancing Services Your Mortgage Guide Contents: Introduction... 3 The Financial Services Authority (FCA)... 3 What is

The Exchange Property Services Mortgage Services Letting & Management Services Conveyancing Services Your Mortgage Guide Contents: Introduction... 3 The Financial Services Authority (FCA)... 3 What is

STATES OF JERSEY PENSION INCREASE DEBT: OPTIONS FOR EARLY REPAYMENT STATES GREFFE

STATES OF JERSEY PENSION INCREASE DEBT: OPTIONS FOR EARLY REPAYMENT Presented to the States on 18th June 2013 by the Minister for Treasury and Resources STATES GREFFE 2013 Price code: B R.63 2 REPORT Background

STATES OF JERSEY PENSION INCREASE DEBT: OPTIONS FOR EARLY REPAYMENT Presented to the States on 18th June 2013 by the Minister for Treasury and Resources STATES GREFFE 2013 Price code: B R.63 2 REPORT Background

Home Loan. This document sets out your loan s terms and conditions. Some key information about your loan. Terms and Conditions

Home Loan Terms and Conditions This document sets out your loan s terms and conditions In this document we ve explained the terms and conditions applying to your ANZ Home Loan. It includes key information

Home Loan Terms and Conditions This document sets out your loan s terms and conditions In this document we ve explained the terms and conditions applying to your ANZ Home Loan. It includes key information

Equity Release. Standards for Appropriate Examinations. AES3/011206 Financial Services Skills Council 2006 1

Equity Release Standards for Appropriate Examinations AES3/011206 Financial Services Skills Council 2006 1 The Standards The Standards contain the following information: 1. The learning outcomes that must

Equity Release Standards for Appropriate Examinations AES3/011206 Financial Services Skills Council 2006 1 The Standards The Standards contain the following information: 1. The learning outcomes that must

A Guide to the Mortgage to Rent Scheme

a government initiative A Guide to the Mortgage to Rent Scheme The Mortgage to Rent Scheme is a government initiative to help homeowners who are at risk of losing their home. Contents 1. What is the Mortgage

a government initiative A Guide to the Mortgage to Rent Scheme The Mortgage to Rent Scheme is a government initiative to help homeowners who are at risk of losing their home. Contents 1. What is the Mortgage

Mortgage Conditions and Explanations

Mortgage Conditions and Explanations 1 Mortgage Conditions and Explanations Bath Building Society ( the Society ) The paragraphs headed Introduction and Membership Rights below are included purely for

Mortgage Conditions and Explanations 1 Mortgage Conditions and Explanations Bath Building Society ( the Society ) The paragraphs headed Introduction and Membership Rights below are included purely for

A Guide to the Mortgage to Rent Scheme

a government initiative A Guide to the Mortgage to Rent Scheme A Guide for Applicants Contents 1. What is the Mortgage to Rent Scheme? 3 2. What are the benefits of the Scheme? 3 3. Who provides the Scheme?

a government initiative A Guide to the Mortgage to Rent Scheme A Guide for Applicants Contents 1. What is the Mortgage to Rent Scheme? 3 2. What are the benefits of the Scheme? 3 3. Who provides the Scheme?

Application form Residential and buy-to-let secured loans

Together is a trading style of Blemain Finance Limited Application form Residential and buy-to-let secured loans Section 1: Loan details Loan Details Repayment type: (capital & Interest or interest only)

Together is a trading style of Blemain Finance Limited Application form Residential and buy-to-let secured loans Section 1: Loan details Loan Details Repayment type: (capital & Interest or interest only)

Buy-to-Let Mortgage Arrears: Measures Needed to Protect Homes of Tenants and Stability of Private Rented Sector

Buy-to-Let Mortgage Arrears: Measures Needed to Protect Homes of Tenants and Stability of Private Rented Sector Submission to Joint Oireachtas Committee on Finance, Public Expenditure and Reform April

Buy-to-Let Mortgage Arrears: Measures Needed to Protect Homes of Tenants and Stability of Private Rented Sector Submission to Joint Oireachtas Committee on Finance, Public Expenditure and Reform April

BANKERS GUIDE TO SECURE LENDING

BANKERS GUIDE TO SECURE LENDING WAREHOUSE RECEIPTS, ORDER OR STRAIGHT BILLS OF LADING, OTHER NEGOTIABLE AND NON-NEGOTIABLE DOCUMENTS OF TITLE, INCLUDING WAREHOUSE AND BAILEE OR DOCK RECEIPTS Lending Rationale

BANKERS GUIDE TO SECURE LENDING WAREHOUSE RECEIPTS, ORDER OR STRAIGHT BILLS OF LADING, OTHER NEGOTIABLE AND NON-NEGOTIABLE DOCUMENTS OF TITLE, INCLUDING WAREHOUSE AND BAILEE OR DOCK RECEIPTS Lending Rationale

In Debt. Dealing with your creditors

In Debt Dealing with your creditors 0 This guide has been produced by the Insolvency Service with the help and support of the IVA Standing Committee. The Insolvency Service would like to thank the members

In Debt Dealing with your creditors 0 This guide has been produced by the Insolvency Service with the help and support of the IVA Standing Committee. The Insolvency Service would like to thank the members

General Mortgage Conditions

General Mortgage Conditions 2015 (England and Wales) 0800 298 5714 precisemortgages-customers.co.uk Contents Condition Number Page Number Part 1: Understanding These Conditions 4 1 Definitions 4 Part 2:

General Mortgage Conditions 2015 (England and Wales) 0800 298 5714 precisemortgages-customers.co.uk Contents Condition Number Page Number Part 1: Understanding These Conditions 4 1 Definitions 4 Part 2:

Opinion of the European Banking Authority on Good Practices for the Treatment of Borrowers in Mortgage Payment Difficulties

EBA-Op-2013-03 13 June 2013 Repealed on 21 March 2016 Opinion of the European Banking Authority on Good Practices for the Treatment of Borrowers in Mortgage Payment Difficulties Table of Contents Abbreviations

EBA-Op-2013-03 13 June 2013 Repealed on 21 March 2016 Opinion of the European Banking Authority on Good Practices for the Treatment of Borrowers in Mortgage Payment Difficulties Table of Contents Abbreviations

Residential mortgages general information

Residential mortgages general information Residential mortgages general information 2 Contents Who we are and what we do 2 Forms of security 2 Representative Example 2 Indication of possible further costs

Residential mortgages general information Residential mortgages general information 2 Contents Who we are and what we do 2 Forms of security 2 Representative Example 2 Indication of possible further costs

LEEDS CITY COUNCIL CORPORATE DEBT POLICY

LEEDS CITY COUNCIL CORPORATE DEBT POLICY ( Draft Version 5 ) Summary of policy : This policy details the principles to be adopted by the Council when undertaking the collection of debt in the City of Leeds

LEEDS CITY COUNCIL CORPORATE DEBT POLICY ( Draft Version 5 ) Summary of policy : This policy details the principles to be adopted by the Council when undertaking the collection of debt in the City of Leeds

NEED TO KNOW. IFRS 9 Financial Instruments Impairment of Financial Assets

NEED TO KNOW IFRS 9 Financial Instruments Impairment of Financial Assets 2 IFRS 9 FINANCIAL INSTRUMENTS IMPAIRMENT OF FINANCIAL ASSETS IFRS 9 FINANCIAL INSTRUMENTS IMPAIRMENT OF FINANCIAL ASSETS 3 TABLE

NEED TO KNOW IFRS 9 Financial Instruments Impairment of Financial Assets 2 IFRS 9 FINANCIAL INSTRUMENTS IMPAIRMENT OF FINANCIAL ASSETS IFRS 9 FINANCIAL INSTRUMENTS IMPAIRMENT OF FINANCIAL ASSETS 3 TABLE

GN8: Additional Guidance on valuation of long-term insurance business

GN8: Additional Guidance on valuation of long-term insurance business Classification Practice Standard MEMBERS ARE REMINDED THAT THEY MUST ALWAYS COMPLY WITH THE PROFESSIONAL CONDUCT STANDARDS (PCS) AND

GN8: Additional Guidance on valuation of long-term insurance business Classification Practice Standard MEMBERS ARE REMINDED THAT THEY MUST ALWAYS COMPLY WITH THE PROFESSIONAL CONDUCT STANDARDS (PCS) AND

Lump Sum Lifetime Mortgage Terms and Conditions. Version 1

Lump Sum Lifetime Mortgage Terms and Conditions Version 1 INTRODUCTION Thank you for choosing Hodge Lifetime. We hope that your lifetime mortgage makes a positive difference during your retirement. This

Lump Sum Lifetime Mortgage Terms and Conditions Version 1 INTRODUCTION Thank you for choosing Hodge Lifetime. We hope that your lifetime mortgage makes a positive difference during your retirement. This

CREDIT UNION PRIVATE EDUCATION LINE OF CREDIT AGREEMENT AND DISCLOSURE

CREDIT UNION PRIVATE EDUCATION LINE OF CREDIT AGREEMENT AND DISCLOSURE In this Private Education Line of Credit Agreement and Disclosure ( Agreement ) the terms I, me, my and mine mean each person who

CREDIT UNION PRIVATE EDUCATION LINE OF CREDIT AGREEMENT AND DISCLOSURE In this Private Education Line of Credit Agreement and Disclosure ( Agreement ) the terms I, me, my and mine mean each person who

Equity Release. A guide to our Lifetime Mortgage products

Equity Release A guide to our Lifetime Mortgage products Introducing Retirement Advantage Previously known as MGM Advantage and Stonehaven, we are a well-established company that can trace its roots back

Equity Release A guide to our Lifetime Mortgage products Introducing Retirement Advantage Previously known as MGM Advantage and Stonehaven, we are a well-established company that can trace its roots back

BANK OF NEW ZEALAND FACILITY MASTER AGREEMENT. Important information about. Your home loan

BANK OF NEW ZEALAND FACILITY MASTER AGREEMENT Important information about Your home loan Contents PAGE 2 Introduction Agreeing a facility 3 Changes to facilities Insurance 4 Pre-conditions This document

BANK OF NEW ZEALAND FACILITY MASTER AGREEMENT Important information about Your home loan Contents PAGE 2 Introduction Agreeing a facility 3 Changes to facilities Insurance 4 Pre-conditions This document

Trouble Debt Restructuring & OREO Accounting

Session Objectives Trouble Debt Restructuring & OREO Accounting Chris Vallez, CPA, CICA, MBA, Partner Ellen Vargo, CPA, CFE, FCPA, NCCO Partner Nearman, Maynard, Vallez, CPA s Identify accounting guidance

Session Objectives Trouble Debt Restructuring & OREO Accounting Chris Vallez, CPA, CICA, MBA, Partner Ellen Vargo, CPA, CFE, FCPA, NCCO Partner Nearman, Maynard, Vallez, CPA s Identify accounting guidance

September 2015. Scenario 9 & 10. PIA comparison with Bankruptcy. Page 1 of 21

September 2015 Scenario 9 & 10 PIA comparison with Bankruptcy Page 1 of 21 The case studies contained within this publication are primarily designed to assist Personal Insolvency Practitioners (PIPs) prepare

September 2015 Scenario 9 & 10 PIA comparison with Bankruptcy Page 1 of 21 The case studies contained within this publication are primarily designed to assist Personal Insolvency Practitioners (PIPs) prepare

Sixth Statutory Managers Report

Sixth Statutory Managers Report Aorangi Securities Limited 4 March 2011 Sixth Statutory Managers Report for Aorangi Securities Limited March 2011 2 Introduction History On 20 June 2010, Richard Grant Simpson

Sixth Statutory Managers Report Aorangi Securities Limited 4 March 2011 Sixth Statutory Managers Report for Aorangi Securities Limited March 2011 2 Introduction History On 20 June 2010, Richard Grant Simpson

Tabletop Exercises: Allowance for Loan and Lease Losses and Troubled Debt Restructurings

Tabletop Exercises: Allowance for Loan and Lease Losses and Troubled Debt Restructurings Index Measuring Impairment Example 1: Present Value of Expected Future Cash Flows Method (Unsecured Loan)... - 1

Tabletop Exercises: Allowance for Loan and Lease Losses and Troubled Debt Restructurings Index Measuring Impairment Example 1: Present Value of Expected Future Cash Flows Method (Unsecured Loan)... - 1

Combined Home Loan. This document sets out your loan or facility s terms and conditions. Some key information about your loan or facility

Combined Home Loan Terms and Conditions This document sets out your loan or facility s terms and conditions In this document we ve explained the terms and conditions applying to your ANZ Home Loan or ANZ

Combined Home Loan Terms and Conditions This document sets out your loan or facility s terms and conditions In this document we ve explained the terms and conditions applying to your ANZ Home Loan or ANZ

Business Loan. This document sets out your loan s terms and conditions. Contents of these terms and conditions. Terms and Conditions

Business Loan Terms and Conditions This document sets out your loan s terms and conditions In this document we ve explained the terms and conditions applying to your ANZ Business Loan. It includes key

Business Loan Terms and Conditions This document sets out your loan s terms and conditions In this document we ve explained the terms and conditions applying to your ANZ Business Loan. It includes key

DRN. Guide to a Debt Relief Notice

nseirbhís Dócmhainneachta na héirea DRN Guide to a Debt Relief Notice n Insolvency Service of Ireland A Debt Relief Notice enables an eligible insolvent debtor with limited disposable income and assets

nseirbhís Dócmhainneachta na héirea DRN Guide to a Debt Relief Notice n Insolvency Service of Ireland A Debt Relief Notice enables an eligible insolvent debtor with limited disposable income and assets

This guide has been produced by the Insolvency Service with the help and support of the IVA Standing Committee. The Insolvency Service would like to

This guide has been produced by the Insolvency Service with the help and support of the IVA Standing Committee. The Insolvency Service would like to thank the members of the IVA Standing Committee for

This guide has been produced by the Insolvency Service with the help and support of the IVA Standing Committee. The Insolvency Service would like to thank the members of the IVA Standing Committee for

Business and Agri Loan Terms and Conditions

October 2012 Thank you for choosing an ANZ loan. When you take out a loan, various terms and conditions apply to it. These are covered in this Terms and Conditions document and in your loan agreement.

October 2012 Thank you for choosing an ANZ loan. When you take out a loan, various terms and conditions apply to it. These are covered in this Terms and Conditions document and in your loan agreement.

STELLENBOSCH MUNICIPALITY

STELLENBOSCH MUNICIPALITY APPENDIX 9 BORROWING POLICY 203/204 TABLE OF CONTENTS. PURPOSE... 3 2. OBJECTIVES... 3 3. DEFINITIONS... 3 4. SCOPE OF THE POLICY... 4 5. LEGISLATIVE FRAMEWORK AND DELEGATION

STELLENBOSCH MUNICIPALITY APPENDIX 9 BORROWING POLICY 203/204 TABLE OF CONTENTS. PURPOSE... 3 2. OBJECTIVES... 3 3. DEFINITIONS... 3 4. SCOPE OF THE POLICY... 4 5. LEGISLATIVE FRAMEWORK AND DELEGATION

Dealing with debt - toolkit Information from Southampton City Council. Step 5. Tackle the most important debts first

Dealing with debt - toolkit Information from Southampton City Council Step 5. Tackle the most important debts first Step 5. Tackle the most important debts first priority creditors. Some debts are more

Dealing with debt - toolkit Information from Southampton City Council Step 5. Tackle the most important debts first Step 5. Tackle the most important debts first priority creditors. Some debts are more

Glossary of Mortgage Terms. Also known as: Mortgage Payment Protection Insurance (MPPI).

.") Glossary of Mortgage Terms Italics denote a cross-referenced entry Accident, Sickness and Unemployment Insurance (ASU): In the event of an accident, sickness or involuntary unemployment befalling a borrower,

Glossary of Mortgage Terms Italics denote a cross-referenced entry Accident, Sickness and Unemployment Insurance (ASU): In the event of an accident, sickness or involuntary unemployment befalling a borrower,

NAB Equity Lending. Facility Terms

NAB Equity Lending Facility Terms This document contains important information regarding the terms and conditions which will apply to your NAB Equity Lending Facility. You should read this document carefully

NAB Equity Lending Facility Terms This document contains important information regarding the terms and conditions which will apply to your NAB Equity Lending Facility. You should read this document carefully

MORE CHOICE MORTGAGE CENTRE MORTGAGE GUIDE

MORE CHOICE MORTGAGE CENTRE MORTGAGE GUIDE All you need to know about buying and protecting your home THE FSA More Choice Financial Ltd, The Rufus Centre, Steppingley Road, Flitwick Beds MK45 1AH is authorised

MORE CHOICE MORTGAGE CENTRE MORTGAGE GUIDE All you need to know about buying and protecting your home THE FSA More Choice Financial Ltd, The Rufus Centre, Steppingley Road, Flitwick Beds MK45 1AH is authorised

Help to Buy Buyers Guide

Help to Buy Buyers Guide Homes and Communities Agency http://www.homesandcommunities.co.uk/helptobuy Page 1 of 27 Key information Buyers using this scheme must provide security in the form of a second

Help to Buy Buyers Guide Homes and Communities Agency http://www.homesandcommunities.co.uk/helptobuy Page 1 of 27 Key information Buyers using this scheme must provide security in the form of a second