PRODUCER S UNDERWRITING GUIDE

|

|

|

- Martina Powers

- 8 years ago

- Views:

Transcription

1 PRODUCER S UNDERWRITING GUIDE CONTENTS A. General Purpose of guide Underwriting philosophy B. Routine underwriting requirements Chart Preparing your client for the exam and/or Tele-Underwriting Interview Preparing your client for the inspection report C. Tips for expediting the underwriting and policy issue process D. Preferred underwriting criteria E. Height and weight table. F. Common medical impairments and possible underwriting actions G. Aviation, avocation, occupation, and military guideline H. Financial underwriting guidelines I. Delivery of the policy J. Large Case Program PURPOSE OF GUIDE The purpose of this guide is to provide Penn Mutual agents with a concise document that provides key underwriting information in a readily available, easy to use format. UNDERWRITING PHILOSOPHY Penn Mutual is committed to providing timely and competitive underwriting service to our agent while meeting the mortality assumptions established for its life products. The Underwriting Department is an integral part of the sales process and is committed to adding value and providing a competitive advantage for our agents. 07/10 Page 1 of 20

2 The Penn Mutual Life Age and Amount Underwriting Requirements Permanent and Term Life Face Amount ,000 to 250,000 A C C C C D-1 F 250,001 to 499,999 B C C C D D-1 F 500,000 to 999,999 B C C D D D-1 F 1,000,000 to 1,499,999 I/C C C D D E-1 F 1,500,000 to 2,499,999 I/C C D D D E-1 F 2,500,000 to 5,000,000 I/C C D D D E-1 F 5,000,001 to 10,000,000 I/C C D D D E-1 F 10,000,001 and higher I/C C D E E E-1 F Chart Key: A Non-Medical B Non-Medical + Urine C Para Med Exam & IRP (Insurance Risk Profile - Blood & Urine specimen) D Para Med Exam, IRP & EKG D-1 Para Med, Sr. Supplement, IRP, EKG E Physician Exam, IRP, EKG E-1 Physician Exam, Sr. Supplement, IRP, EKG F Informal inquiry should be submitted prior to scheduling exam requirements: Physician Exam, Sr. Supplement, IRP, EKG I/C Individual Consideration Senior Supplement Required for all individuals > 70 years old, all amounts Stress EKG Requested by underwriter for cause based on Framingham Cardiac Risk Score Confidential Financial Confidential Financial Statement (CFS) required for all amounts over $2,500,000 for ages 20+ (cover letter and Statement (CFS) supporting documentation, as indicated in the Financial Underwriting Guidelines, still required over $5, ) Inspection Reports Ages to 69 and face amount $10,000,000 and over Ages 70 plus and face amount $5,000,000 and over Survivorship Life Medical Requirements are based on each individual s age and 50% of the face amount,unless one life Requirements uninsurable then the amount will be based on 100% of healthy life. Note: For qualified plans, face amounts under $50,000 at ages require a fully completed application and a Urine. For child riders, any requirements outside of the non-medical form will be at the discretion of Underwriting. Additional requirements may be imposed by underwriting due to medical history, circumstances of the case or facultative reinsurance. Ages Underwriting Requirements as of 07/2010 For Broker/Dealer use only. Not for use in sales situations The Penn Mutual Life Insurance Company, Philadelphia, PA T /13 A0JC

3 All Examination requirements, including physician exams, must be arranged through any of the following paramedical facilities: APPS (American Para Professional Systems Inc.) Portamedic (ASB/Meditest/PSA) Examination Management Services, Inc. (EMSI) Exam One Tele-Underwriting is available from ExamOne, Portamedic, and EMSI. See separate Tele-Underwriting section. These requirements apply to both Penn Mutual and its subsidiaries. Medical requirements are determined by the amount of the new application. When underwriting a case the total amount of amount of coverage both in force and applied for is taken into consideration. We reserve the right to request additional requirements deemed necessary to evaluate the total risk presented. Age 14 and under, examination by either the child s physician or an approved examining facility is acceptable. Insurance Risk Profile (I.R.P.) is an automated chemical analysis of a blood specimen, which includes an H.I.V. antibody test for the A.I.D.S. virus. The blood and urine specimens will be obtained by the examining facility and forwarded to our designated laboratory. 07/10 Page 3 of 20

4 PREPARING YOUR CLIENT FOR THE TELE-UNDERWRITING INTERVIEW 1. They will be contacted, by phone, by a professionally trained interviewer from one of our approved vendors who will conduct the medical history portion the exam by telephone interview. The Process can take approximately minutes. 2. Prior to starting the interview, the tele-underwriter will ask if you are willing to provide a voice signature. This is simply a statement authenticating your identity and the information provided. This replaces the official signature on the medical history and allows Penn Mutual to process the information provided electronically. Using voice signature will significantly speed up the underwriting process. 3. Be prepared to provide names, dosages, and frequency of any present medication. Also, be prepared to provide the correct name, complete address and telephone number of their primary physician as well as any other physician they have seen in the past 5 years and the reason they were seen. 4. At the conclusion of the interview, they will be asked to schedule an appointment to obtain the vitals, fluid draw, and to sign the exam form (signature needed only if voice signature was not applied). If an appointment is not available at that time, the paramedical exam office will contact them to make arrangements for the completion of the requirements. 5. Steps 1 through 10 listed below in Preparing Your Client for the Exam also apply. PREPARING YOUR CLIENT FOR THE EXAM The medical exam is a vital part of the underwriting process and forms the basis on which your client is evaluated. Because detailed questions regarding medical history and a physical examination by an unknown professional examiner can sometimes be unnerving, it is important to prepare your client in the best way possible. To obtain the best possible results, we suggest you advise your client of a few simple steps: 1. If blood testing is required, try to fast at least 4 hours before your examination - an 8-hour fast is preferred. You may drink water. 2. Drink a glass of water one hour or so before the exam as this will facilitate obtaining a urine specimen. 3. Be prepared to provide names, dosages, and frequency of any present medication. Also be prepared to provide any attending physician s correct name, address, zip code, telephone numbers, and dates of visits for the last 5 years and reason seen. 4. AVOID the following as these might adversely affect the results of the exam and give an inaccurate picture of your health condition. Caffeine (coffee, soda, tea) for several hours before the exam Smoking or chewing tobacco for at least one hour prior to your scheduled appointment Alcoholic beverages for at least eight hours before the exam Nasal decongestants 5. Do not engage in strenuous exercise for 24 hours before the exam. 6. Have photo identification available. 7. Schedule the appointment for the least stressful time of the day. Early morning is usually best. 8. Get a good night s rest before the exam. 9. Undressing is not required, but please wear a garment that is short-sleeved, or has sleeves that can be easily rolled up. 10. If you anticipate that your applicant may need a larger blood pressure cuff (for applicants with very large arms) or a large scale (for applicants over 300 lbs.), please alert the examining facility at the time of ordering the requirements. 11. The Senior Exam (for ages 71 and up) requires three brief additional tests (for respiratory capacity, mobility, and cognitive ability) and a few additional questions. 07/10 Page 4 of 20

5 PREPARING YOUR CLIENT FOR THE INSPECTION REPORT An inspection report is routinely required for face amounts of $10,000,000 and above. Underwriting reserves the right to obtain an inspection report on any application; therefore, we recommend that you prepare the applicant for the possibility of an inspection report or an interview being completed on any application. Here are a few simple steps. 1. Inform your client that a representative of a national firm specializing in this type of report may be calling to complete an inspection report or an underwriter may call to conduct a phone interview. 2. Indicate that the inspection report may be required by the insurance company prior to issuing the policy. 3. Your client should be prepared to answer financial questions regarding earned/unearned income, net worth, assets, and liabilities. Your client may be asked to furnish phone numbers of their accountant and/or bank. 4. Be prepared to provide names and addresses of present or past physicians and medications (including exact spelling and dosage) that are presently being taken. 5. Some questions are repetitious of questions on the application or paramedical. This is intended to confirm that information provided is complete. Incomplete answers will only result in delaying the issuance of the policy. 6. If any questions or concerns arise during the inspection reporting process, please advise your client to contact the inspection facility immediately. 07/10 Page 5 of 20

6 TIPS FOR EXPEDITING THE UNDERWRITING PROCESS For the paper exam process, complete the application in its entirety, including the medical questions even if an examination is required. At a minimum, provide the complete name, address, and telephone number of the personal physician and provide the reason and date last seen. For the Tele-Underwriting process, complete all the questions on the application with the exception of the medical questions. Since the Tele-Underwriting interview is more detailed, there is no need to obtain this information from your client. For a Tele-Underwriting case, complete the Producer s Section of the Tele-Underwriting Fax Order Form and submit the order form along with all other required forms with the application, including the VUL supplemental application, Confidential Personal Supplement / Confidential Financial Supplement (as required), avocational questionnaires, etc. to the field office. Submit all required forms with the application, including the VUL supplemental application, Penn Check forms, Confidential Personal Supplement / Confidential Financial Supplement (as required), avocational questionnaires, etc. to the field office. Be sure to clearly state the name and relationship of the Beneficiary to the Insured. Where there are multiple beneficiaries indicate the appropriate percentage share for each. When a Trust is involved, give the complete name, ID number, and date of the Trust as well as the name of the Trustee. When a corporation is the owner and/or beneficiary, the phrase It s successors or assigns should be included. The corporate tax ID number should be included if the corporation is owner or payer. Whenever a correction is necessary (cross-out, write-over, or white-out) be sure to have the Proposed Insured initial the change. We cannot accept the agent s or the owner s initials on a corrected answer. For the paper exam process, schedule the examination when you take the application. Do not schedule the medical evidence requirements when Tele-Underwriting is being used. This will be handled by the field office. Taking money with the application is encouraged, but it must be taken only within the terms of the application. The terms are spelled out in the Temporary Insurance Agreement. Money accepted outside of these terms will be refunded to the applicant. Use a Cover Letter to explain or highlight any unusual aspects of the case. These could be either medical or nonmedical in nature. This will help to expedite your case. On large cases, be prepared to supply documentation of finances. Refer to the Financial Underwriting Guidelines for maximum amounts and specific documentation required. Copies of the past two years Balance Sheets and Income Statements will help to expedite the underwriting process. If an estate plan has been completed, please include a copy with the application. 07/10 Page 6 of 20

7 PREFERRED TOBACCO CRITERIA Tobacco Within the past 12 months Proposed Insured used cigarettes on any basis or used other forms of tobacco on more than an occasional basis, or currently tests positive for nicotine. Not available with flat or table rating based on Penn Mutual s medical underwriting standards. May consider with non-health related flat extra rating. Driving Proposed Insured cannot have a history of a DUI in the past 5 years or any ratable driving criticism. Blood Pressure Proposed Insured cannot have a blood pressure reading greater than 140/90 to age 60 or 150/90 over age 60 on our exam or within the past year. Treatment acceptable if on no more than two medications. Family History Proposed Insured cannot have more than one natural parent or sibling who has died before age 60 from cardiovascular or cerebrovascular disease or cancer. Family History will be discounted if Proposed Insured has reached age 60. Cholesterol Proposed Insured cannot have a Cholesterol/HDL ratio on our IRP, or within the past year, of greater than 6.5 AND Proposed Insured cannot have total Cholesterol on our IRP, or within the past year, of greater than 260. Treatment for cholesterol is acceptable. Drugs and alcohol Proposed Insured cannot have a history of drug or alcohol abuse or treatment within past 7 years. Build Proposed Insured s weight on our exam cannot exceed the maximum listed for their height on the attached chart. NON-TOBACCO PREFERRED CRITERIA Tobacco - Proposed insured cannot have used tobacco/nicotine products of any kind in the last 2 years. We will include very occasional cigar smokers, who admit this on the application and test negative on the nicotine screen. Occasional being defined as no more than 2 cigars per month. Not available with flat or table rating based on Penn Mutual s medical underwriting standards. May consider with non-health related flat extra rating. Driving Proposed Insured cannot have a history of a DUI in the past 5 years or any ratable driving criticism. Blood Pressure Proposed Insured cannot have a blood pressure reading greater than 140/90 to age 60 or 150/90 over age 60 on our exam or within the past year. Treatment acceptable if on no more than two medications. Family History Proposed Insured cannot have more than one natural parent or sibling who has died before age 60 from cardiovascular or cerebrovascular disease or cancer. Family History will be discounted if Proposed Insured has reached age 60. Cholesterol Proposed Insured cannot have a Cholesterol/HDL ratio on our IRP, or within the past year, of greater than 6.5 AND Proposed Insured cannot have total Cholesterol on our IRP, or within the past year, of greater than 260. Treatment for cholesterol is acceptable. Drugs and alcohol Proposed Insured cannot have a history of drug or alcohol abuse or treatment within past 7 years. Build Proposed Insured s weight on our exam cannot exceed the maximum listed for their height on the attached chart. 07/10 Page 7 of 20

8 NON-TOBACCO PREFERRED PLUS CRITERIA Tobacco - Proposed insured cannot have used tobacco/nicotine products of any kind in the last 3 years. We will include very occasional cigar smokers, who admit this on the application and test negative on the nicotine screen. Occasional being defined as no more than 2 cigars per month. Not available with flat or table rating based on Penn Mutual s underwriting standards. Personal History Proposed Insured cannot have a medical history in past 10 years of diabetes, cancer (other than non-melanoma skin cancer), cardiovascular or cerebrovascular disease. Driving Proposed Insured cannot have a history of a DUI in the past 5 years or more than 2 moving violations in past 3 years. Blood Pressure Proposed Insured cannot have a blood pressure reading greater than 140/90 to age 60 or 145/90 over age 60 on our exam or within the past year. Treatment acceptable if on no more than two medications. Family History Proposed Insured cannot have a natural parent or sibling who has died before age 60 from cardiovascular or cerebrovascular disease or cancer. Family History will be discounted if Proposed Insured has reached age 60. Cholesterol Proposed Insured cannot have a Cholesterol/HDL ratio on our IRP, or within the past year, of greater than 5.5 AND Proposed Insured cannot have total Cholesterol on our IRP, or within the past year, of greater than 230. Treatment for cholesterol is acceptable. Drugs and alcohol Proposed Insured cannot have a history of drug or alcohol abuse or treatment within past 10 years. Aviation Proposed Insured cannot participate in private aviation unless IFR, ATP, or Commercial qualified with a minimum of 1500 total flight hours. Aviation activity cannot be ratable. Build Proposed Insured s weight on our exam cannot exceed the maximum listed for their height on the attached chart. NON-TOBACCO PREFERRED BEST CRITERIA (TERM PRODUCT ONLY) Tobacco - Proposed insured cannot have used tobacco/nicotine products of any kind in the last 5 years. Not available with flat or table rating based on Penn Mutual s underwriting standards. Personal History Proposed Insured cannot have a medical history of cardiovascular or cerebrovascular disease, diabetes, or cancer. Proposed Insured must have normal age appropriate routine medical screenings. Driving Proposed Insured cannot have a history of a DUI or more than 1 moving violation in past 3 years. Blood Pressure Proposed Insured cannot have a blood pressure reading greater than 135/85 on our exam or within the past year. No treatment or history of hypertension is acceptable. Family History Proposed Insured cannot have a natural parent or sibling who has been diagnosed before age 60 of cardiovascular or cerebrovascular disease, diabetes, or cancer. Family History will be discounted if Proposed Insured has reached age 60. Cholesterol Proposed Insured cannot have a Cholesterol/HDL ratio on our IRP, or within the past year, of greater than 4.5 AND Proposed Insured cannot have total Cholesterol on our IRP, or within the past year, of greater than 210. Treatment for cholesterol is acceptable. Drugs and alcohol Proposed Insured cannot have a history of drug or alcohol abuse or treatment. Aviation Proposed Insured cannot participate in any private aviation. Build Proposed Insured s weight on our exam cannot exceed the maximum listed for their height on the attached chart. 07/10 Page 8 of 20

, cardiovascular or cerebrovascular disease.")

9 HEIGHT AND WEIGHT TABLE

10 COMMON MEDICAL IMPAIRMENTS/ POSSIBLE UNDERWRITING ACTIONS This is intended to be a guide as to what underwriting action might result with some of the most common medical impairments. Obviously, every case is different and the actual underwriting will depend on the particular details developed through a complete underwriting evaluation. Please note that impairment ratings followed by * MAY qualify for standard rates under our table 3 fold-in program. I Coronary Artery Disease Usual Action 1. Myocardial Infarction (Heart attack) In the first six months Postpone After six months Best case Table 2 * Average case Table 4 2. Coronary Bypass Surgery or Angioplasty In the first six months Postpone After six months Best case Single Vessel Disease Table 2* Average case Table 4 Smoking would be a serious risk factor in applicants with a history of MI, Bypass, or Angioplasty. II Cancer, i.e., Breast, Colon, Prostate With no evidence of metastasis and normal IRP, normal PSA if prostate cancer In the first year After the first year Best case Average case Skin Cancer Non-melanoma Leukemia Postpone $7.50/m for 4 yr. Decline for 3 yr., then rate $10/m for 5 yr. Excised, usually standard Usually decline III Diabetes Mellitus 1. Juvenile Usually decline 2. Insulin dependent - Best case (well-controlled Table 4 without cardiovascular, renal or neurological findings) 3. Adult onset (non-insulin dependent) - Best case Possible standard (Well controlled with no cardiovascular disease; e.g. hypertension, normal build) 07/10 Page 10 of 20

In the first six months Postpone After six months Best case Table 2 * Average case Table 4 2.")

11 IV Hypertension Best case - could be preferred if blood pressure has been normal over one year and controlled with a minimum of medication. Build must be preferred. V. Asthma 1. Children Best case Standard Average case Table In adults who use inhalers only and have no Possible Preferred underlying pulmonary disease or history of frequent infection Use of oral steroids Table 4 6 VI. Peptic Ulcer Best case - healed with adequate treatment With bleeding Chronic Possible Preferred 7.50/m for 2 yr. Table 4 or higher VII. Epilepsy Best case - no medication or seizure for 5 yr. Standard Average case Table 4 6 VIII. Kidney Stones Best case - stone passed, normal urine Present symptoms, abnormal urinalysis Possible Preferred Postpone IX Depression Minor - requiring a minimum of medication and psychotherapy Major - frequent visits for psychotherapy, large doses or multiple medications Possible Preferred Table 4 to Decline X. Chronic Obstructive Pulmonary Disease (i.e.: emphysema) Mild-Best Case Standard - Table 2* Moderate Case Table 2* to Table 4 Severe Table 4 and up 07/10 Page 11 of 20

12 XI. Mitral Valve Prolapse No symptoms, no mitral insufficiency, no serious cardiac arrhythmia With symptoms of fatigue, palpitation, chest pain, continuing treatment History of cardiac arrhythmia Preferred Table 2 and up Table 4 and up XII. Stroke Usually Decline Transient Ischemia Attacks (or mini-strokes) 0-1 year ago Postpone 1-5 years - Best Case Table 2 to Table 6 (Ratings improve with duration from attack) XIII. Osteoarthritis Preferred Rheumatoid Arthritis Under age 40 Best case Table 2* to Table 4 Over age 40 Best case Standard to Table 2 * 07/10 Page 12 of 20

XIII.")

13 AVIATION, AVOCATIONS, OCCUPATIONS AVIATION Aviation risks are generally divided into three broad categories based upon the nature of the aviation activity. These are Commercial (flying for pay), Civilian (flying for pleasure), and Military (flying in conjunction with Military Service). The underlying concerns with all aviation risks are the nature of the flying, amount of experience and amount of annual flying time. The following sample should serve as a guide in evaluating the aviation risk. This is not intended to be an all inclusive listing of aviation activities. Contact your local field office with specifics situations. AVIATION / CIVILIAN Recreational Flying (not for pay) Personal and Business Student Pilots Pilots with < 100 hours SOLO experience...$2.50/m Licensed Pilots Other forms of Recreational Flying / Aircraft Aerobatics Flying Balloonists Hang Gliders - over 1 yr. Experience Hazardous geographical area AVIATION / COMMERCIAL Airlines - Domestic and International, passenger and /or cargo. Scheduled and non-scheduled with at least 1 terminal in the US Business, Corporate - Maintenance and flying conditions Similar to regularly scheduled airlines Others Crop Dusting Conventional planes Helicopter Other forms of commercial aviation $10.00/M STD to $3.50/M $ 2.50/M $ 7.50/M Preferred Preferred $2.50/M $5.00/M $3.50/M $3.00/M - $10.00/M 7/10 Page 13 of 20

14 AVIATION / MILITARY Ratings for Military Aviation are dependent upon Age, Branch of Service, Rank/Rating, Duty Station and type of aircraft flown. In these situations, contact your field office for help. AVOCATION The risks associated with most avocations and hazardous sports relate both to hazards of the avocation or sport itself and to the participant s qualification and abilities to participate in that sport. Key factors such as frequency of activity, location of activity, safety record of activity training and experience of participant all play a role in the decision making process. To list all hazardous avocations and their ratings is beyond the scope of this guide. When confronted with a hazardous sport or avocation, be sure to complete an Hazardous Sports Questionnaire, and/or contact the field office for help. The following examples of some of the more common avocations, their underwriting criteria and likely actions are presented here to give you a general idea as to our approach. SCUBA DIVING: Scuba Divers, Skin Divers 07/10 Page 14 of 20

15 SKY DIVING: Not affiliated with parachute club to 50 jumps per yr. $5.00/M jumps per yr. $7.50/M Affiliated with a parachute club to 15 jumps per yr. $3.50/M 15 or more jumps per yr. $2.50/M MOUNTAIN CLIMBING: Novice climber (less than 2 yrs. climbing experience) United States (lower 48 states) Other Experienced Climber ( 2 full yrs. experience at least 6 climbs) United States (lower 48 states) Alaska (excluding Brooks range) Other locations $3.50/M Usually Decline Usually Standard $ $7.00/M Refer to field office OCCUPATIONS The primary underwriting concern with regard to hazardous occupations is that of accidental death or injury as a result of either direct accident (mine cave-in) or insidious exposure to toxic substances (asbestos). It is important to clarify the exact nature and duties of employment. For example the team manager is not very descriptive and could carry a very different risk profile depending on the industry. A detailed listing of ratable occupations is beyond the scope of this guide. Should you have any questions about whether or not an occupation is ratable, please contact your field office. 07/10 Page 15 of 20

")

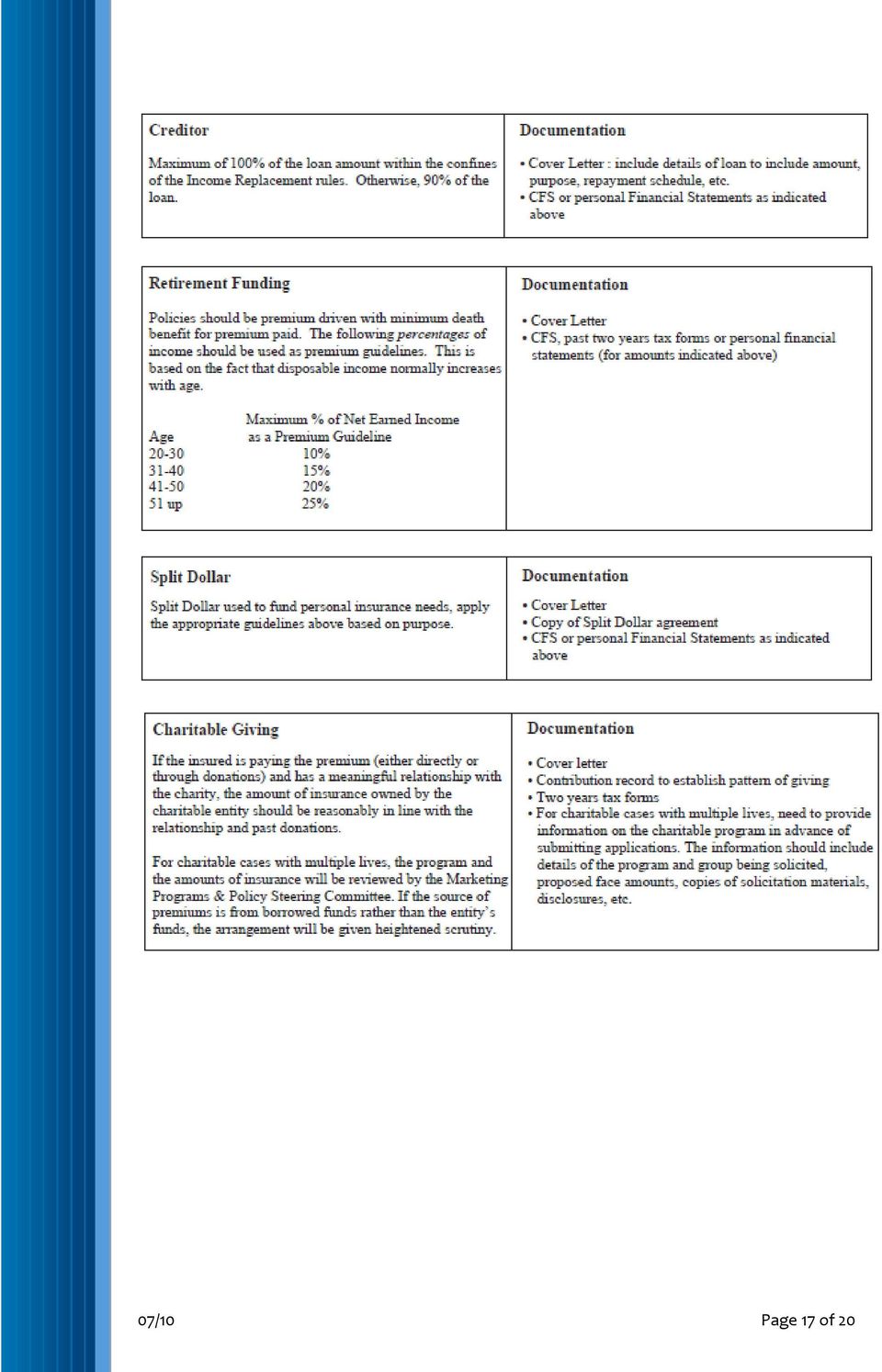

16 Penn Mutual s Financial Underwriting Guidelines Financial underwriting is necessary on all applications to screen for adverse selection and to determine if the amount of insurance is reasonable. The following guidelines are used by the underwriters to determine the maximum amount of coverage that is considered usual for the proposed insured s financial status. If the total face amount (all companies) falls outside of these guidelines, a brief letter from you explaining the purpose of the insurance and how you arrived at the face amount can help to expedite the underwriting process. If annual premium for personal insurance exceeds 25% of the applicant s total income, a cover letter is required explaining how the premium is being funded and why. Below are listed the most common needs for life insurance and the appropriate guidelines for maximum face amount and necessary documentation. Unless indicated otherwise below, all cases require Penn Mutual s Confidential Financial Statement questionnaire (CFS) at $2,500,001 and higher and supporting financial documentation for amounts of $5,000,001 and higher. Supporting financial documents should include past two years tax forms, income statements and balance sheets, etc. The type of supporting documentation depends on the purpose of the insurance (see below). If these items are not available, please provide any available supporting documentation with an explanation. An inspection report (IR) will be requested above $9,999,999. Be sure to prepare your client for the inspection report. 07/10 Page 16 of 20

17 07/10 Page 17 of 20

18 07/10 Page 18 of 20

19 07/10 Page 19 of 20

20 DELIVERY OF THE POLICY Proper delivery of a policy is a very important step in the sales process. To avoid potential free look complications, all policies should be delivered to the owner as promptly as possible and must be delivered within 30 days of receipt by you. When you deliver a life policy, it is imperative to determine if there has been a change in the proposed insured s health, habits, occupation and other facts since the application/exam was taken before delivering the policy. If there has been a change, the policy cannot be delivered without reviewing the changes with Underwriting. Please have the applicant sign a statement as to the changes and submit this to your field office. Underwriting will decide whether the policy can be delivered or the underwriting evaluation must be reopened. When you personally deliver the policy to the owner, both you and the owner should sign and date the policy receipt, and one copy of the duplicate receipt should be left with the owner. The other copy of the policy delivery receipt, amendments, and NAIC illustration, if applicable, should be signed and returned to Penn Mutual s home office within 30 days of the issue date. If the policy is not accepted by the owner, please return it immediately to the home office for cancellation. LARGE CASE PROGRAM Penn Mutual has developed the Large Case Unit, which is a special program for handling your large cases. Major components of the program include: expanded communication, priority handling, and a very competitive underwriting offer. Under terms of this program, a large case is defined as an application for: $100,000 annual premium OR $10,000,000 of face amount Your large case will receive special first-class treatment, which includes: Special case handling, to include: priority processing by both the field office and home office priority attention to attending physician statements aggressive follow-up on all outstanding requirements priority policy issue express-mail service throughout the process Underwriting review We make maximum use of our underwriting expertise in getting your case the best possible offer. Improved communication through your field manager You are encouraged to consult with your general agent or regional director before a Large Case application is taken to discuss any medical or financial underwriting issues. If necessary, your field manager will involve underwriting management at that point. The underwriter will maintain close communication with your field manager at critical decision points. 07/10 Page 20 of 20

renewable term Your Guide to Wawanesa Life s LifeStyle Term Plan

renewable term Your Guide to Wawanesa Life s LifeStyle Term Plan LIFESTYLE TERM What is Wawanesa Life s LifeStyle Term plan? The LifeStyle Term plan consists of 10, 20 or 30-year renewable and convertible

renewable term Your Guide to Wawanesa Life s LifeStyle Term Plan LIFESTYLE TERM What is Wawanesa Life s LifeStyle Term plan? The LifeStyle Term plan consists of 10, 20 or 30-year renewable and convertible

General Underwriting Guidelines

General Underwriting Guidelines Old Mutual is the marketing name of OM Financial Life Insurance Company, and in NY only, OM Financial Life Insurance Company of New York, Old Mutual plc companies. Each

General Underwriting Guidelines Old Mutual is the marketing name of OM Financial Life Insurance Company, and in NY only, OM Financial Life Insurance Company of New York, Old Mutual plc companies. Each

Underwriting Guidelines

Underwriting Guidelines Lincoln individual and survivorship products The Lincoln National Life Insurance Company Lincoln Life & Annuity Company of New York Not a deposit Not FDIC-insured May go down in

Underwriting Guidelines Lincoln individual and survivorship products The Lincoln National Life Insurance Company Lincoln Life & Annuity Company of New York Not a deposit Not FDIC-insured May go down in

Examination Requirements Schedule

Examination Requirements Schedule For the purpose of determining exam requirements, the applicant s age at the birthday nearest to the date of the application will be used. In the examination requirements

Examination Requirements Schedule For the purpose of determining exam requirements, the applicant s age at the birthday nearest to the date of the application will be used. In the examination requirements

term life 10, 15, 20, 30

Companion Life Insurance Company A Mutual of Omaha Company term life 10, 15, 20, 30 product and underwriting guide Y6754_1208 For producer use only. Not for use with the general public. Term Life 10, 15,

Companion Life Insurance Company A Mutual of Omaha Company term life 10, 15, 20, 30 product and underwriting guide Y6754_1208 For producer use only. Not for use with the general public. Term Life 10, 15,

General Underwriting Guidelines

General Underwriting Guidelines Fidelity & Guaranty Life is the marketing name of Fidelity & Guaranty Life Insurance Company, and in NY only, Fidelity & Guaranty Life Insurance Company of New York. Each

General Underwriting Guidelines Fidelity & Guaranty Life is the marketing name of Fidelity & Guaranty Life Insurance Company, and in NY only, Fidelity & Guaranty Life Insurance Company of New York. Each

UNDERWRITING GUIDELINES

UNDERWRITING GUIDELINES Western Reserve Life WRL Freedom ChoiceTerm II WRL Freedom Index Universal Life WRL Freedom Global Index Universal Life WRL Freedom Elite Builder II WRL Freedom Asset Advisor For

UNDERWRITING GUIDELINES Western Reserve Life WRL Freedom ChoiceTerm II WRL Freedom Index Universal Life WRL Freedom Global Index Universal Life WRL Freedom Elite Builder II WRL Freedom Asset Advisor For

Life Insurance Medical Underwriting Requirements Requirements are based on age as of nearest birthday

Underwriting. Only Better. Life Insurance Medical Underwriting Requirements Requirements are based on age as of nearest birthday Death Benefit Amount 0 250,000 Non-Medical 250,001 500,000 Non-Medical 500,001

Underwriting. Only Better. Life Insurance Medical Underwriting Requirements Requirements are based on age as of nearest birthday Death Benefit Amount 0 250,000 Non-Medical 250,001 500,000 Non-Medical 500,001

For advisor use only Insurance Advisor Guide

For advisor use only Insurance Advisor Guide Term 10 and Term 20 2 RBC Insurance Many people day work hard at leading a healthy lifestyle. RBC Insurance recognizes that fact and offers insurance products

For advisor use only Insurance Advisor Guide Term 10 and Term 20 2 RBC Insurance Many people day work hard at leading a healthy lifestyle. RBC Insurance recognizes that fact and offers insurance products

Best Class Criteria LIFE UNDERWRITING

LIFE UNDERWRITING Best Class Criteria The following criteria contain key information that can help you estimate whether your life insurance clients will qualify for one of our best risk classes Super Preferred,

LIFE UNDERWRITING Best Class Criteria The following criteria contain key information that can help you estimate whether your life insurance clients will qualify for one of our best risk classes Super Preferred,

Underwriting Guidelines

writing Guidelines Committed to Complete and Professional Risk Selections Table of Contents writing and New Business Overview 3 Contact Information by Department 4 Approved Facilities 4 Connect 24/7 with

writing Guidelines Committed to Complete and Professional Risk Selections Table of Contents writing and New Business Overview 3 Contact Information by Department 4 Approved Facilities 4 Connect 24/7 with

PREFERRED UNDERWRITING CLASSIFICATIONS

PREFERRED UNDERWRITING CLASSIFICATIONS term ADVISOR GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations we ve provided policyholders

PREFERRED UNDERWRITING CLASSIFICATIONS term ADVISOR GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations we ve provided policyholders

Underwriting requirements and preferred guidelines

Individual Life Underwriting requirements and preferred guidelines For BGA use only Requirements for all Symetra Life Insurance Products Face Amount Ages 0-17 Ages 18-40 Ages 41-50 Ages 51-69 Ages 70+

Individual Life Underwriting requirements and preferred guidelines For BGA use only Requirements for all Symetra Life Insurance Products Face Amount Ages 0-17 Ages 18-40 Ages 41-50 Ages 51-69 Ages 70+

JLTexpress APP. How it Works. Carriers Available. Toll Free 800.222.4090

JLTexpress APP The easiest way to sell term life insurance. How it Works The broker completes the JLTexpress APP and submits via email or fax. Depending on the carrier you may have to complete to complete

JLTexpress APP The easiest way to sell term life insurance. How it Works The broker completes the JLTexpress APP and submits via email or fax. Depending on the carrier you may have to complete to complete

SUBSTANDARD UNDERWRITING

H I G H L I G H T E R SUBSTANDARD UNDERWRITING Substandard Marketing Opportunities Tips for Selling Life Insurance in the Substandard Market Recognizing a Substandard Marketing Situation The substandard

H I G H L I G H T E R SUBSTANDARD UNDERWRITING Substandard Marketing Opportunities Tips for Selling Life Insurance in the Substandard Market Recognizing a Substandard Marketing Situation The substandard

Underwriting Guidelines

writing Guidelines Committed to Complete and Professional Risk Selections Table of Contents writing and New Business Overview 3 Contact Information by Department 4 Approved Facilities 4 Connect 24/7 with

writing Guidelines Committed to Complete and Professional Risk Selections Table of Contents writing and New Business Overview 3 Contact Information by Department 4 Approved Facilities 4 Connect 24/7 with

requ i r e m e n t s

GUiDe to initial Un D e rw r i t ing requ i r e m e n t s As of February 2009 International Underwriting Team For producer use only. Not for distribution to the public. Table of Contents Examination Authority

GUiDe to initial Un D e rw r i t ing requ i r e m e n t s As of February 2009 International Underwriting Team For producer use only. Not for distribution to the public. Table of Contents Examination Authority

Term 10 and Term 20. Insurance Advisor Guide. Guaranteed renewable and convertible

FOR INSURANCE ADVISOR USE ONLY. NOT INTENDED FOR CLIENT DISTRIBUTION. Term 10 and Term 20 Guaranteed renewable and convertible Insurance Advisor Guide Many people day work hard at leading a healthy lifestyle.

FOR INSURANCE ADVISOR USE ONLY. NOT INTENDED FOR CLIENT DISTRIBUTION. Term 10 and Term 20 Guaranteed renewable and convertible Insurance Advisor Guide Many people day work hard at leading a healthy lifestyle.

No Lapse Universal Life Product Guide PLATINUM SERIES

PLATINUM SERIES No Lapse Universal Life Product Guide For Producer Use Only. Not for Public Distribution. Sagicor Life Insurance Company is Rated A- (Excellent) by A.M. Best Company 4179 S1000710 TABLE

PLATINUM SERIES No Lapse Universal Life Product Guide For Producer Use Only. Not for Public Distribution. Sagicor Life Insurance Company is Rated A- (Excellent) by A.M. Best Company 4179 S1000710 TABLE

Underwriting Guide PLAG.2807 (10.15) For Financial Professional Use Only. Not for Use With Consumers.

For Financial Professional Use Only. Not for Use With Consumers.") Underwriting Guide PLAG.2807 (10.15) For Financial Professional Use Only. Not for Use With Consumers. Table of Contents Approved Para-Medical Providers Approved Para-Medical Providers...3 Underwriting

Underwriting Guide PLAG.2807 (10.15) For Financial Professional Use Only. Not for Use With Consumers. Table of Contents Approved Para-Medical Providers Approved Para-Medical Providers...3 Underwriting

SBLI Agent Underwriting Guide For Agent Use ONLY. Not intended for Consumer Use. September 2008

SBLI Agent Underwriting Guide For Agent Use ONLY. Not intended for Consumer Use. September 2008 Form M-91 1 SBLI Agent Underwriting Guide Table of Contents SBLI Underwriting Philosophy... 3 Prescreening

SBLI Agent Underwriting Guide For Agent Use ONLY. Not intended for Consumer Use. September 2008 Form M-91 1 SBLI Agent Underwriting Guide Table of Contents SBLI Underwriting Philosophy... 3 Prescreening

life underwriting condensed guide

life underwriting condensed guide For Financial Professional Use Only. Not for Use with, or Distribution to the General Public. AXA Equitable Underwriting Criteria Preferred Guidelines All Applicants Term

life underwriting condensed guide For Financial Professional Use Only. Not for Use with, or Distribution to the General Public. AXA Equitable Underwriting Criteria Preferred Guidelines All Applicants Term

GUIDE. Prepare for Your Phone Interview and Medical Exam.

GUIDE Prepare for Your Phone Interview and Medical Exam. WHAT YOU NEED TO HAVE, KNOW, AND DO. All information gathered during the interview and exam will be shared only with those who need it in order

GUIDE Prepare for Your Phone Interview and Medical Exam. WHAT YOU NEED TO HAVE, KNOW, AND DO. All information gathered during the interview and exam will be shared only with those who need it in order

ING Life Underwriting

ING Life Underwriting Requirements Guide June 2011 1 General Information 2 Medical, Inspection & APS Requirements 3-4 Preferred Criteria 5-6 Financial Requirements/Underwriting Guide LIFE INSURANCE Your

ING Life Underwriting Requirements Guide June 2011 1 General Information 2 Medical, Inspection & APS Requirements 3-4 Preferred Criteria 5-6 Financial Requirements/Underwriting Guide LIFE INSURANCE Your

Completion of a fact finder will accelerate the underwriting process

QUICK FACT-FINDER TOOLS All personal information protected by HIPPA regulations (see HIPPA form attached with supplemental forms) Completion of a fact finder will accelerate the underwriting process Name:

QUICK FACT-FINDER TOOLS All personal information protected by HIPPA regulations (see HIPPA form attached with supplemental forms) Completion of a fact finder will accelerate the underwriting process Name:

UNDERWRITING GUIDELINES

Single Premium Whole Life UNDERWRITING GUIDELINES LifeScape For Agent use only. Product availability, rates and features vary by state. 16-166-01101 (Rev. 9/15/10) n-medical Limits and Examination Requirements

Single Premium Whole Life UNDERWRITING GUIDELINES LifeScape For Agent use only. Product availability, rates and features vary by state. 16-166-01101 (Rev. 9/15/10) n-medical Limits and Examination Requirements

Life Insurance Underwriting Pocket Guide

UW Pocket Guide_ Aug 2010.v2 8/9/2010 3:26 PM Page 1 Life Insurance Underwriting Pocket Guide The Company You Keep Agent use only UW Pocket Guide_ Aug 2010.v2 8/9/2010 3:26 PM Page 2 UW Pocket Guide_ Aug

UW Pocket Guide_ Aug 2010.v2 8/9/2010 3:26 PM Page 1 Life Insurance Underwriting Pocket Guide The Company You Keep Agent use only UW Pocket Guide_ Aug 2010.v2 8/9/2010 3:26 PM Page 2 UW Pocket Guide_ Aug

Commit to Quit Term Life Product Guide

Commit to Term Life Product Guide According to the Department of Health and Human Services Nearly 1 in 5 adults and teenagers smoke CIGARETTES More than16 MILLION people already have at least one smoking-related

Commit to Term Life Product Guide According to the Department of Health and Human Services Nearly 1 in 5 adults and teenagers smoke CIGARETTES More than16 MILLION people already have at least one smoking-related

Underwriting guidelines for life insurance products

Life insurance (R-9/04) Allianz Life Insurance Company of North America guidelines for life insurance products Your client will be contacted to complete a telephone interview (). Please help prepare them

Life insurance (R-9/04) Allianz Life Insurance Company of North America guidelines for life insurance products Your client will be contacted to complete a telephone interview (). Please help prepare them

Underwriting Requirements Guide September 2014

Voya Life Companies Fully Underwritten Life Insurance Underwriting Requirements Guide September 2014 General Information... 2 Medical, Inspection & APS Requirements... 3 Preferred Criteria... 4-5 Financial

Voya Life Companies Fully Underwritten Life Insurance Underwriting Requirements Guide September 2014 General Information... 2 Medical, Inspection & APS Requirements... 3 Preferred Criteria... 4-5 Financial

Life Insurance Underwriting Pocket Guide. The Company You Keep. Agent use only

Life Insurance Underwriting Pocket Guide The Company You Keep Agent use only Table of Contents Page 1 Page 2 Page 3 Page 4 Pages 5-6 Pages 7-8 Page 9 Page 10 Page 11 Page 12 Page 13 Page 14 Page 15 Introduction

Life Insurance Underwriting Pocket Guide The Company You Keep Agent use only Table of Contents Page 1 Page 2 Page 3 Page 4 Pages 5-6 Pages 7-8 Page 9 Page 10 Page 11 Page 12 Page 13 Page 14 Page 15 Introduction

AppAssist. The Agent s Guide to

The Agent s Guide to AppAssist Banner Life s AppAssist program is designed to make it easy for you to facilitate the sale of high-quality, low-cost term life insurance. Now available with LAA1363 (6/08)

The Agent s Guide to AppAssist Banner Life s AppAssist program is designed to make it easy for you to facilitate the sale of high-quality, low-cost term life insurance. Now available with LAA1363 (6/08)

Civil Service Employees Benefit Association 67182-7. Address City State Zip. Place of Birth Home/Cell Phone # Work Phone # E-mail Address

Group Term Life Application for 10-Year or 20-Year Level Term Rate Please complete the entire application. If completing this application in paper format, please print clearly in dark ink and mail to WrightUSA

Group Term Life Application for 10-Year or 20-Year Level Term Rate Please complete the entire application. If completing this application in paper format, please print clearly in dark ink and mail to WrightUSA

Making it easier for you to do business

Making it easier for you to do business Nationwide Life Underwriting Desk Reference For insurance professional use only not for distribution with the public EasyMed or regular underwriting? Determine which

Making it easier for you to do business Nationwide Life Underwriting Desk Reference For insurance professional use only not for distribution with the public EasyMed or regular underwriting? Determine which

AppAssist. The Agent s Guide to

The Agent s Guide to AppAssist Banner Life s AppAssist program is designed to make it easy for you to facilitate the sale of high-quality, low-cost term life insurance. Now available with LAA1363 (4/06)

The Agent s Guide to AppAssist Banner Life s AppAssist program is designed to make it easy for you to facilitate the sale of high-quality, low-cost term life insurance. Now available with LAA1363 (4/06)

Competitive. Flexible. Innovative.

Competitive. Flexible. Innovative. Underwriting Guidelines FOR BROKER/DEALER USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC. Table of Contents Key Benefits 2 Medical Examiners 4 Preferred Vendors

Competitive. Flexible. Innovative. Underwriting Guidelines FOR BROKER/DEALER USE ONLY. THIS MATERIAL MAY NOT BE USED WITH THE PUBLIC. Table of Contents Key Benefits 2 Medical Examiners 4 Preferred Vendors

Underwriting Criteria and Requirements

Underwriting Criteria Underwriting Criteria Preferred Plus Preferred Standard Plus Standard Impairments No personal history of disease or impairment that would affect mortality No personal history of disease

Underwriting Criteria Underwriting Criteria Preferred Plus Preferred Standard Plus Standard Impairments No personal history of disease or impairment that would affect mortality No personal history of disease

For Agent Use ONLY. Not intended for Consumer Use. December 2010

For Agent Use ONLY. Not intended for Consumer Use. December 2010 Form M-91 1 SBLI Agent Underwriting Guide Table of Contents SBLI Underwriting Philosophy... 3 Prescreening of Applicants for Level Term

For Agent Use ONLY. Not intended for Consumer Use. December 2010 Form M-91 1 SBLI Agent Underwriting Guide Table of Contents SBLI Underwriting Philosophy... 3 Prescreening of Applicants for Level Term

Principal Accelerated Underwriting SM. Program Overview

Principal Accelerated Underwriting SM Program Overview Accelerated underwriting from the Principal Financial Group provides you with a streamlined approach that improves the underwriting process through:

Principal Accelerated Underwriting SM Program Overview Accelerated underwriting from the Principal Financial Group provides you with a streamlined approach that improves the underwriting process through:

Informal Inquiry. Name Soc. Sec. # BISYS Agent ID Phone No. Address City State Zip Fax No. Email Address

page 1 of 5 Preliminary Inquiry Not an application for life insurance. This Informal Inquiry form is used exclusively to gather specific information on a proposed insured s medical history and other factors

page 1 of 5 Preliminary Inquiry Not an application for life insurance. This Informal Inquiry form is used exclusively to gather specific information on a proposed insured s medical history and other factors

Group Benefits Evidence of Insurability for Comprehensive Optional Critical Illness Insurance

Group Benefits Evidence of Insurability for Comprehensive Optional Critical Illness Insurance INSTRUCTIONS - Please print all answers If required, retain a photocopy for your files. 1a) Plan contract number(s)

Group Benefits Evidence of Insurability for Comprehensive Optional Critical Illness Insurance INSTRUCTIONS - Please print all answers If required, retain a photocopy for your files. 1a) Plan contract number(s)

Name Firm/Agency. Phone Fax Email. Check one; Single Life case Survivorship (complete 2 apps) 1st to Die (complete 2 apps)

1st to Die (complete 2 apps)") Insurance Designers, LLC and it s Partner and Affiliate offices comprise a full service brokerage organization committed to comprehensive insurance analysis for clients. Our on-site underwriting program

Insurance Designers, LLC and it s Partner and Affiliate offices comprise a full service brokerage organization committed to comprehensive insurance analysis for clients. Our on-site underwriting program

CIGI Direct Insurance Services, Inc. QUICK QUOTE CORONARY ANGIOPLASTY/CORONARY BYPASS

QUICK QUOTE CORONARY ANGIOPLASTY/CORONARY BYPASS Amount of Insurance $ Type of Insurance 1. Has patient had: Date of last symptom, list date (or dates if more than one ) Angina pectoris (heart pain)? r

QUICK QUOTE CORONARY ANGIOPLASTY/CORONARY BYPASS Amount of Insurance $ Type of Insurance 1. Has patient had: Date of last symptom, list date (or dates if more than one ) Angina pectoris (heart pain)? r

Underwriting Requirements Guide February 2015

Voya Life Companies Fully Underwritten Life Insurance Underwriting Requirements Guide February 2015 General Information... 2 Medical, Inspection & APS Requirements... 3 Preferred Criteria... 4-5 Financial

Voya Life Companies Fully Underwritten Life Insurance Underwriting Requirements Guide February 2015 General Information... 2 Medical, Inspection & APS Requirements... 3 Preferred Criteria... 4-5 Financial

UNDERWRITING GUIDE. LifeScape Single Premium Whole Life Insurance

LifeScape Single Premium Whole Life Insurance UNDERWRITING GUIDE FOR AGENT USE ONLY. t for use with consumers. Product rates, availability and features may vary by state. 16-250-01101 (4/14) Underwriting

LifeScape Single Premium Whole Life Insurance UNDERWRITING GUIDE FOR AGENT USE ONLY. t for use with consumers. Product rates, availability and features may vary by state. 16-250-01101 (4/14) Underwriting

Sun Life and Health Insurance Company (U.S.)

") Sun Life and Health Insurance Company (U.S.) One Sun Life Executive Park, Wellesley Hills, MA 02481] [800-247-6875 Evidence of Insurability Cover Page Employer Instructions Complete this cover page and

Sun Life and Health Insurance Company (U.S.) One Sun Life Executive Park, Wellesley Hills, MA 02481] [800-247-6875 Evidence of Insurability Cover Page Employer Instructions Complete this cover page and

NO EXAM or LABS; To Age 60, $1,000,000 (4/22/14)

") NO EXAM or LABS; To Age 60, $1,000,000 (4/22/14) Accelerated Underwriting from Principal Financial may enable your preferred and super preferred clients to avoid exams and APS's and receive prompt underwriting

NO EXAM or LABS; To Age 60, $1,000,000 (4/22/14) Accelerated Underwriting from Principal Financial may enable your preferred and super preferred clients to avoid exams and APS's and receive prompt underwriting

Hartford Term 10, 15, 20, 30

INDIVIDUAL LIFE INSURANCE Hartford Term 10, 15, 20, 30 Product Details, Underwriting Classifications, Sample Rates and Height/ Charts INSURANCE PRODUCTS: NOT INSURED BY FDIC OR ANY MAY LOSE NOT A DEPOSIT

INDIVIDUAL LIFE INSURANCE Hartford Term 10, 15, 20, 30 Product Details, Underwriting Classifications, Sample Rates and Height/ Charts INSURANCE PRODUCTS: NOT INSURED BY FDIC OR ANY MAY LOSE NOT A DEPOSIT

PREFERRED UNDERWRITING

PREFERRED UNDERWRITING For Solution 10 & Solution 20 Criteria Guide 2015 FOR ADVISOR USE ONLY Contents About this guide...1 Preferred underwriting...1 Availability...1 Risk classifications...1 Standard

PREFERRED UNDERWRITING For Solution 10 & Solution 20 Criteria Guide 2015 FOR ADVISOR USE ONLY Contents About this guide...1 Preferred underwriting...1 Availability...1 Risk classifications...1 Standard

Life Insurance. Underwriting Guide. Product issued by National Life Insurance Company 60111 MK1200(0212) TC66099(0212)

TC66099(0212)") Life Insurance Underwriting Guide Product issued by National Life Insurance Company Last Updated February 2012 For Agent Use Only Not For Use With The Public 30 % 60111 MK1200(0212) TC66099(0212) Our Philosophy

Life Insurance Underwriting Guide Product issued by National Life Insurance Company Last Updated February 2012 For Agent Use Only Not For Use With The Public 30 % 60111 MK1200(0212) TC66099(0212) Our Philosophy

INTERNATIONAL AND SPECIAL USE TERM LIFE INSURANCE

INTERNATIONAL AND SPECIAL USE TERM LIFE INSURANCE FOR U.S. Dollar Term Life Insurance for use when there is an international insurable interest involved. USES Employees of Foreign National Firms International

INTERNATIONAL AND SPECIAL USE TERM LIFE INSURANCE FOR U.S. Dollar Term Life Insurance for use when there is an international insurable interest involved. USES Employees of Foreign National Firms International

TimeSaver. A proven solution for your impaired risk cases

TimeSaver TM A proven solution for your impaired risk cases The Crump TimeSaverTM is the most widely accepted preliminary inquiry in the industry. This powerful tool helps identify the right solution for

TimeSaver TM A proven solution for your impaired risk cases The Crump TimeSaverTM is the most widely accepted preliminary inquiry in the industry. This powerful tool helps identify the right solution for

Please print in black ink. TO BE COMPLETED BY APPLICANT Applicant's Name DOB Sex Last First MI Month/Day/Year

Application for Short-Term Disability Insurance (A-57400 Series) Application to American Family Life Assurance Company of Columbus (AFLAC) Worldwide Headquarters: Columbus, Georgia 31999 New Conversion

Application for Short-Term Disability Insurance (A-57400 Series) Application to American Family Life Assurance Company of Columbus (AFLAC) Worldwide Headquarters: Columbus, Georgia 31999 New Conversion

Client Information Name Male Female SSN - - Address (City, State, Zip Code)

") Quick Quoter Informal Inquiry t an application for Life or Disability insurance This Quick Quoter from is used exclusively to gather specific information on a proposed insured s medical history and other

Quick Quoter Informal Inquiry t an application for Life or Disability insurance This Quick Quoter from is used exclusively to gather specific information on a proposed insured s medical history and other

Royal Advantage Term. 10, 20, 30-Year Level Premium Term Life Insurance. Agent Training Guide Not for public distribution

Royal Advantage Term 10, 20, 30-Year Level Premium Term Life Insurance Agent Training Guide Not for public distribution Royal Advantage Term Description Level Premium Term to Age 95 Form series 200711A

Royal Advantage Term 10, 20, 30-Year Level Premium Term Life Insurance Agent Training Guide Not for public distribution Royal Advantage Term Description Level Premium Term to Age 95 Form series 200711A

NEURO-OPHTHALMIC QUESTIONNAIRE NAME: AGE: DATE OF EXAM: CHART #: (Office Use Only)

") PAGE 1 NEURO-OPHTHALMIC QUESTIONNAIRE NAME: AGE: DATE OF EXAM: CHART #: (Office Use Only) 1. What is the main problem that you are having? (If additional space is required, please use the back of this

PAGE 1 NEURO-OPHTHALMIC QUESTIONNAIRE NAME: AGE: DATE OF EXAM: CHART #: (Office Use Only) 1. What is the main problem that you are having? (If additional space is required, please use the back of this

APPLICATION FOR TERM CONVERSION (with Riders or Extra Benefits) OR POLICY REISSUE

OR POLICY REISSUE") 72954101 APPLICATION FOR TERM CONVERSION (with Riders or Extra Benefits) OR POLICY REISSUE Liberty National Life Insurance Company P.O. Box 2612 Birmingham, AL 35202 A Nebraska Stock Company PART 1 Section

72954101 APPLICATION FOR TERM CONVERSION (with Riders or Extra Benefits) OR POLICY REISSUE Liberty National Life Insurance Company P.O. Box 2612 Birmingham, AL 35202 A Nebraska Stock Company PART 1 Section

Presents: Insider tips for the life insurance medical exam. Know what they are testing for--and how to get the best results.

Presents: Insider tips for the life insurance medical exam. Know what they are testing for--and how to get the best results. Copyright 2012 TheLifeInsuranceInsider.com The material Information presented

Presents: Insider tips for the life insurance medical exam. Know what they are testing for--and how to get the best results. Copyright 2012 TheLifeInsuranceInsider.com The material Information presented

Underwriting Guidelines

Underwriting Guidelines Agent Guide to basic underwriting information and requirements for American National Insurance Company & American National Life Insurance Company of New York For Agent Use Only;

Underwriting Guidelines Agent Guide to basic underwriting information and requirements for American National Insurance Company & American National Life Insurance Company of New York For Agent Use Only;

EVIDENCE OF INSURABILITY COVERAGE DETAIL

EVIDENCE OF INSURABILITY COVERAGE DETAIL This application consists of two parts: The Evidence of Insurability Coverage Detail form and Medical & Lifestyle Questionnaire. INSTRUCTIONS Plan Administrator:

EVIDENCE OF INSURABILITY COVERAGE DETAIL This application consists of two parts: The Evidence of Insurability Coverage Detail form and Medical & Lifestyle Questionnaire. INSTRUCTIONS Plan Administrator:

HELP PROVIDE SECURITY AT AFFORDABLE RATES

US Airways Pilots Association (USAPA) Group Term Life Insurance 10-Year Level Premium Administered by: For Association Members and Their Families Issued by ReliaStar Life Insurance Company, a member of

US Airways Pilots Association (USAPA) Group Term Life Insurance 10-Year Level Premium Administered by: For Association Members and Their Families Issued by ReliaStar Life Insurance Company, a member of

Disability Income Insurance Application

www.inalco.com Disability Income Insurance Application A PARTNER YOU CAN TRUST. F7A (08-08) PDF POLICY NO. Application no. D PROPOSED INSURED AND APPLICANT Last and first name Last name WRITE LEGIBLY IN

www.inalco.com Disability Income Insurance Application A PARTNER YOU CAN TRUST. F7A (08-08) PDF POLICY NO. Application no. D PROPOSED INSURED AND APPLICANT Last and first name Last name WRITE LEGIBLY IN

American General Life Insurance Company Houston, Texas

Application for Life Insurance American General Life Insurance Company Houston, Texas Administrative Office: Mail Stop 6-G2, P.O. Box 4373, Houston, TX 77210-9739 Phone: 866-242-2737 Fax: 713-831-3249

Application for Life Insurance American General Life Insurance Company Houston, Texas Administrative Office: Mail Stop 6-G2, P.O. Box 4373, Houston, TX 77210-9739 Phone: 866-242-2737 Fax: 713-831-3249

application for survivorship joint life insurance Part 1

AMERITAS LIFE INSURANCE CORP. (ALIC) LINCOLN, NEBRASKA 68501 INFORMATION REGARDING INSURED A 1.A. Name: Last First Middle application for survivorship joint life insurance Part 1 Male Female INFORMATION

AMERITAS LIFE INSURANCE CORP. (ALIC) LINCOLN, NEBRASKA 68501 INFORMATION REGARDING INSURED A 1.A. Name: Last First Middle application for survivorship joint life insurance Part 1 Male Female INFORMATION

ScotiaLife Critical Illness Insurance Application

ScotiaLife Critical Illness Insurance Application Group Policy Number: 50184 PO Box 215, Stn Waterloo, Waterloo, ON N2J 3Z9 Simply complete, sign and return this Application Form. NO NEED TO SEND MONEY

ScotiaLife Critical Illness Insurance Application Group Policy Number: 50184 PO Box 215, Stn Waterloo, Waterloo, ON N2J 3Z9 Simply complete, sign and return this Application Form. NO NEED TO SEND MONEY

INTERNATIONAL AND SPECIAL USE TERM LIFE INSURANCE

INTERNATIONAL AND SPECIAL USE TERM LIFE INSURANCE FOR U.S. Dollar Term Life Insurance for use when there is an international insurable interest involved. USES Employees of Foreign National Firms International

INTERNATIONAL AND SPECIAL USE TERM LIFE INSURANCE FOR U.S. Dollar Term Life Insurance for use when there is an international insurable interest involved. USES Employees of Foreign National Firms International

1 MEMBER INFORMATION Policy No. MZ0909533H0000A

Group Term Life Insurance Application Underwritten by Monumental Life Insurance Company, Cedar Rapids, IA Please complete the entire application. Print clearly in dark ink and mail to: Group Term Life

Group Term Life Insurance Application Underwritten by Monumental Life Insurance Company, Cedar Rapids, IA Please complete the entire application. Print clearly in dark ink and mail to: Group Term Life

U.S. FINANCIAL LIFE INSURANCE COMPANY REQUEST FOR POLICY REINSTATEMENT FOR POLICY #

U.S. FINANCIAL LIFE INSURANCE COMPANY REQUEST FOR POLICY REINSTATEMENT FOR POLICY # POLICY OWNER HOME PHONE INSURED HEIGHT WEIGHT DATE OF BIRTH SOCIAL SECURITY NO. WORK PHONE PLEASE NOTE ANY CHANGE OF

U.S. FINANCIAL LIFE INSURANCE COMPANY REQUEST FOR POLICY REINSTATEMENT FOR POLICY # POLICY OWNER HOME PHONE INSURED HEIGHT WEIGHT DATE OF BIRTH SOCIAL SECURITY NO. WORK PHONE PLEASE NOTE ANY CHANGE OF

Life Insurance Underwriting Guide

Life Insurance Company of the Southwest Life Insurance Underwriting Guide 62770 MK2295(0407) TC34081(0407) For Agent Use Only - Not For Use with the Public Life Underwriting Requirements Underwriting Issue

Life Insurance Company of the Southwest Life Insurance Underwriting Guide 62770 MK2295(0407) TC34081(0407) For Agent Use Only - Not For Use with the Public Life Underwriting Requirements Underwriting Issue

AIS CARFAGNO INSURANCE SERVICES - Trial Submission Datasheet Instructions on how to get the most out of your Informal Inquiries:

AIS Instructions on how to get the most out of your Informal Inquiries: 1.) 2.) 3.) 4.) In addition to the completed datasheet, all inquiries and cases that are to be shopped Informally by Carfagno Insurance

AIS Instructions on how to get the most out of your Informal Inquiries: 1.) 2.) 3.) 4.) In addition to the completed datasheet, all inquiries and cases that are to be shopped Informally by Carfagno Insurance

U.S. FINANCIAL LIFE INSURANCE COMPANY REQUEST FOR POLICY REINSTATEMENT FOR POLICY #

U.S. FINANCIAL LIFE INSURANCE COMPANY REQUEST FOR POLICY REINSTATEMENT FOR POLICY # POLICY OWNER HOME PHONE INSURED HEIGHT WEIGHT DATE OF BIRTH SOCIAL SECURITY NO. WORK PHONE PLEASE NOTE ANY CHANGE OF

U.S. FINANCIAL LIFE INSURANCE COMPANY REQUEST FOR POLICY REINSTATEMENT FOR POLICY # POLICY OWNER HOME PHONE INSURED HEIGHT WEIGHT DATE OF BIRTH SOCIAL SECURITY NO. WORK PHONE PLEASE NOTE ANY CHANGE OF

KEY PERSON INSURANCE (Accident & Sickness) PROPOSAL FORM

PROPOSAL FORM") KEY PERSON INSURANCE (Accident & Sickness) PROPOSAL FORM E.U. DISCLOSURE CLAUSE (UK) tice to the Proposer/Insured The Parties are free to choose the law applicable to this insurance Contract. Unless specifically

KEY PERSON INSURANCE (Accident & Sickness) PROPOSAL FORM E.U. DISCLOSURE CLAUSE (UK) tice to the Proposer/Insured The Parties are free to choose the law applicable to this insurance Contract. Unless specifically

Please print in black ink. TO BE COMPLETED BY APPLICANT Applicant's Name DOB Sex Last First MI Month/Day/Year

Application for Accident Insurance (A-34000 Series) with disability riders Application to American Family Life Assurance Company of Columbus (AFLAC) Worldwide Headquarters: Columbus, Georgia 31999 New

Application for Accident Insurance (A-34000 Series) with disability riders Application to American Family Life Assurance Company of Columbus (AFLAC) Worldwide Headquarters: Columbus, Georgia 31999 New

Informal Inquiry. Name Male Female SSN. Address City State Zip. Date of Birth Age Height. Monthly Earned Income $

Informal Inquiry Preliminary Inquiry Not an application for life insurance. This informal inquiry form is used exclusively to gather specific information on a proposed insured s medical history and other

Informal Inquiry Preliminary Inquiry Not an application for life insurance. This informal inquiry form is used exclusively to gather specific information on a proposed insured s medical history and other

AIA International Limited Personal Life & Medical Insurance Program For Members of Hong Kong Institute of Certified Public Accountants Application

AIA International Limited Personal Life & Medical Insurance Program For Members of Hong Kong Institute of Certified Public Accountants Application Form Personal Details of Insured Person Member Accountant

AIA International Limited Personal Life & Medical Insurance Program For Members of Hong Kong Institute of Certified Public Accountants Application Form Personal Details of Insured Person Member Accountant

Group Critical Illness Insurance Provides lump-sum cash benefits that can help with daily expenses

What can living with a critical illness mean to you? Daily out-of-pocket expenses for fighting the disease while still paying your bills! GROCERIES CAR HOME PRESCRIPTIONS Benefit coverage for A Plus Benefits

What can living with a critical illness mean to you? Daily out-of-pocket expenses for fighting the disease while still paying your bills! GROCERIES CAR HOME PRESCRIPTIONS Benefit coverage for A Plus Benefits

P.O. Box 91120, MS 295 Seattle, WA 98111-9220 1-800-290-1278 Fax: 425-918-5278

Oregon Medicare Supplement Enrollment Application for Plans A, F, High Deductible F and N P.O. Box 91120, MS 295 Seattle, WA 98111-9220 1-800-290-1278 Fax: 425-918-5278 You are eligible to apply for a

Oregon Medicare Supplement Enrollment Application for Plans A, F, High Deductible F and N P.O. Box 91120, MS 295 Seattle, WA 98111-9220 1-800-290-1278 Fax: 425-918-5278 You are eligible to apply for a

Simple, Affordable & SAFE!

California State Firefighters Employee Welfare Benefits Corporation Simple, Affordable & SAFE! Limited Time Simplified Issue Offer Group Term Life Insurance Application (10-Year Level Term Rate) C2 ReliaStar

California State Firefighters Employee Welfare Benefits Corporation Simple, Affordable & SAFE! Limited Time Simplified Issue Offer Group Term Life Insurance Application (10-Year Level Term Rate) C2 ReliaStar

Disability Underwriting Requirements Guide

D I S A B IL I N T YE IONFCBOUMSEI NI N ESS URANCE Disability Underwriting Requirements Guide FOR PRODUCER USE ONLY. NOT FOR USE WITH THE PUBLIC. INVEST INSURE RETIRE Age and Amount Underwriting Requirement

D I S A B IL I N T YE IONFCBOUMSEI NI N ESS URANCE Disability Underwriting Requirements Guide FOR PRODUCER USE ONLY. NOT FOR USE WITH THE PUBLIC. INVEST INSURE RETIRE Age and Amount Underwriting Requirement

Mailing Address: PO Box 696700 San Antonio, TX 78269-6700

Application for Individual Life Insurance Policy Issued by One Moody Plaza, Galveston, TX 77550-7947 Phone Number: 877-862-0759 *APP* page 1 of 6 Mailing Address: PO Box 696700 San Antonio, TX 78269-6700

Application for Individual Life Insurance Policy Issued by One Moody Plaza, Galveston, TX 77550-7947 Phone Number: 877-862-0759 *APP* page 1 of 6 Mailing Address: PO Box 696700 San Antonio, TX 78269-6700

Individual Health Insurance Application

Individual Health Insurance Application The Insurer retains the right to contact the applicant if any question is not explained in detail or if additional information is required. New policy Additional

Individual Health Insurance Application The Insurer retains the right to contact the applicant if any question is not explained in detail or if additional information is required. New policy Additional

Voluntary Benefits Employee Enrollment and Change Form

LifeMap Assurance Company TM P.O. Box 1271, MS E-3A Portland, OR 97207-1271 (503) 721-7161 (800) 794-5390 Voluntary Benefits Employee Enrollment and Change Form For residents of Oregon and Washington,

LifeMap Assurance Company TM P.O. Box 1271, MS E-3A Portland, OR 97207-1271 (503) 721-7161 (800) 794-5390 Voluntary Benefits Employee Enrollment and Change Form For residents of Oregon and Washington,

FAIRBANKS PHYSICAL THERAPY

REGISTRATION PAPERWORK CHECKLIST If you wish, you can save time and simplify the registration process by completing the registration paperwork before you arrive. This checklist will help make sure you

REGISTRATION PAPERWORK CHECKLIST If you wish, you can save time and simplify the registration process by completing the registration paperwork before you arrive. This checklist will help make sure you

VOLUNTARY GROUP TERM LIFE INSURANCE Application to: American Family Life Assurance Company of Columbus (AFLAC) Worldwide Headquarters

Worldwide Headquarters") VOLUNTARY GROUP TERM LIFE INSURANCE Application to: American Family Life Assurance Company of Columbus (AFLAC) Worldwide Headquarters Policy Number Columbus, Georgia 31999 Please Print In Black Ink - To

VOLUNTARY GROUP TERM LIFE INSURANCE Application to: American Family Life Assurance Company of Columbus (AFLAC) Worldwide Headquarters Policy Number Columbus, Georgia 31999 Please Print In Black Ink - To

Enrollment Form for Assurant Cancer and Heart/Stroke Fixed Indemnity Insurance

Enrollment Form for Assurant Cancer and Heart/Stroke Fixed Indemnity Insurance PLEASE PRINT IN BLACK INK PERSONS TO BE INSURED Attach a separate sheet, signed and dated, if additional space is needed.

Enrollment Form for Assurant Cancer and Heart/Stroke Fixed Indemnity Insurance PLEASE PRINT IN BLACK INK PERSONS TO BE INSURED Attach a separate sheet, signed and dated, if additional space is needed.

Birth date MM/DD/YYYY Social Security # Height Weight. Resident Address Street City State ZIP

APPLICATION FORM FOR SHORT-TERM DISABILITY INSURANCE WITH OPTIONAL RIDERS PLEASE PRINT IN BLACK INK TYPE OF ACTIVITY New Change Reinstatement Policy Number PERSON(S) PROPOSED TO BE INSURED Last Name First

APPLICATION FORM FOR SHORT-TERM DISABILITY INSURANCE WITH OPTIONAL RIDERS PLEASE PRINT IN BLACK INK TYPE OF ACTIVITY New Change Reinstatement Policy Number PERSON(S) PROPOSED TO BE INSURED Last Name First

EVIDENCE OF INSURABILITY COVERAGE DETAIL

EVIDENCE OF INSURABILITY COVERAGE DETAIL This application consists of two parts: The Evidence of Insurability Coverage Detail form and Medical & Lifestyle Questionnaire. INSTRUCTIONS Plan Administrator:

EVIDENCE OF INSURABILITY COVERAGE DETAIL This application consists of two parts: The Evidence of Insurability Coverage Detail form and Medical & Lifestyle Questionnaire. INSTRUCTIONS Plan Administrator:

Life Underwriting. March 2015 AGT-0191AO-WG (03/2015)

") Life Underwriting March 2015 AGT-0191AO-WG (03/2015) Agenda ipipeline Organizational Update Field Underwriting Processing Tips Underwriting Programs Case Study Foreign Travel & International Risk Case

Life Underwriting March 2015 AGT-0191AO-WG (03/2015) Agenda ipipeline Organizational Update Field Underwriting Processing Tips Underwriting Programs Case Study Foreign Travel & International Risk Case

For intermediary use only not for use with your clients. Medical condition guide

For intermediary use only not for use with your clients Medical condition guide Introduction Listed in this guide are the most common medical disclosures we are asked about. You will find an explanation

For intermediary use only not for use with your clients Medical condition guide Introduction Listed in this guide are the most common medical disclosures we are asked about. You will find an explanation

Last name First name Middle initial Social Security number (required)

") Alaska Medicare Supplement Enrollment Application for Plans A, F, High Deductible F and N 2550 Denali St., Suite 1404 Anchorage, AK 99503 1-888-669-2583 Fax: 907-258-1619 ou are eligible to apply for a

Alaska Medicare Supplement Enrollment Application for Plans A, F, High Deductible F and N 2550 Denali St., Suite 1404 Anchorage, AK 99503 1-888-669-2583 Fax: 907-258-1619 ou are eligible to apply for a

PATIENT / VISIT INFORMATION PATIENT INFORMATION

PATIENT / VISIT INFORMATION PATIENT INFORMATION Name of Patient: Date of Birth: Date of Visit: VISIT INFORMATION Please complete this form in its entirety, and present it to the registration desk when

PATIENT / VISIT INFORMATION PATIENT INFORMATION Name of Patient: Date of Birth: Date of Visit: VISIT INFORMATION Please complete this form in its entirety, and present it to the registration desk when

SBLI UNDERWRITING GUIDE

SBLI UNDERWRITING GUIDE NO NONSENSE. LIKE YOU. New guidelines effective as of February 11, 2014 Coming together is a beginning. Keeping together is progress. Working together is success. -- Henry Ford

SBLI UNDERWRITING GUIDE NO NONSENSE. LIKE YOU. New guidelines effective as of February 11, 2014 Coming together is a beginning. Keeping together is progress. Working together is success. -- Henry Ford

Voluntary Benefits Employee Enrollment and Change Form

Voluntary Benefits Employee Enrollment and Change Form LifeMap Assurance Company TM For residents of Oregon and Washington, the definition of a Spouse includes your legal husband or wife or your State

Voluntary Benefits Employee Enrollment and Change Form LifeMap Assurance Company TM For residents of Oregon and Washington, the definition of a Spouse includes your legal husband or wife or your State

P.O. Box 91120, MS 295 Seattle, WA 98111-9220 1-800-752-6663 Fax: 425-918-5278

Washington Medicare Supplement Enrollment Application for Plans A, F, High Deductible F and N P.O. Box 91120, MS 295 Seattle, WA 98111-9220 1-800-752-6663 Fax: 425-918-5278 ou are eligible to apply for

Washington Medicare Supplement Enrollment Application for Plans A, F, High Deductible F and N P.O. Box 91120, MS 295 Seattle, WA 98111-9220 1-800-752-6663 Fax: 425-918-5278 ou are eligible to apply for

Life Insurance 101. Everything You Wanted to Know About Life Insurance* * But were afraid to ask

or Everything You Wanted to Know About Life Insurance* * But were afraid to ask Contents Pre-Existing Conditions and Life Insurance 3 How Long Does It Take to Get a Term Life Insurance Policy 5 Insurance

or Everything You Wanted to Know About Life Insurance* * But were afraid to ask Contents Pre-Existing Conditions and Life Insurance 3 How Long Does It Take to Get a Term Life Insurance Policy 5 Insurance

Life Insurance Application

Life Insurance Application Product Name Type of Enrollment / Change: (check all that apply) New Application Increase Reinstatement Other ReliaStar Life Insurance Company Home Office: Minneapolis, Minnesota

Life Insurance Application Product Name Type of Enrollment / Change: (check all that apply) New Application Increase Reinstatement Other ReliaStar Life Insurance Company Home Office: Minneapolis, Minnesota

LOW T NATION TESTOSTERONE INTAKE FORM NAME: DATE: ADDRESS: CITY: STATE: ZIP: CELL #: HOME #: SOC SECURITY #: DATE OF BIRTH:

LOW T NATION TESTOSTERONE INTAKE FORM NAME: DATE: ADDRESS: CITY: STATE: ZIP: CELL #: HOME #: SOC SECURITY #: DATE OF BIRTH: DRIVERS LICENSE NUMBER: STATE: EMAIL ADDRESS: MARITAL STATUS: ( ) SINGLE ( )

LOW T NATION TESTOSTERONE INTAKE FORM NAME: DATE: ADDRESS: CITY: STATE: ZIP: CELL #: HOME #: SOC SECURITY #: DATE OF BIRTH: DRIVERS LICENSE NUMBER: STATE: EMAIL ADDRESS: MARITAL STATUS: ( ) SINGLE ( )