INTRODUCTION v Chapter 6A-1.085, Basic Principles of Internal Fund Accounting.

|

|

|

- Chrystal Cain

- 10 years ago

- Views:

Transcription

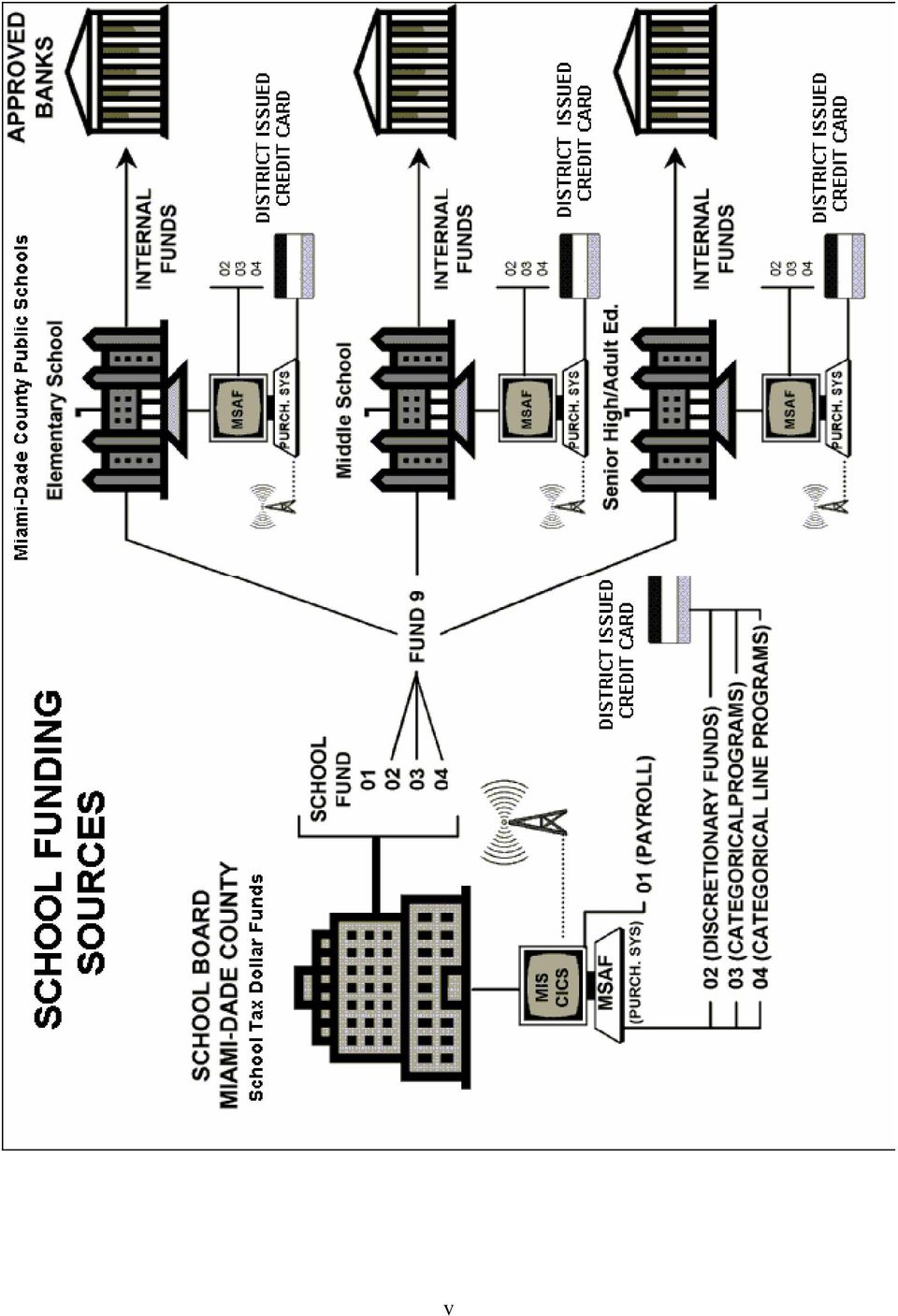

1 INTRODUCTION The programs, activities, and major operations of public schools are funded by different sources. Tax dollars, the main funding source, are allocated annually through the formal budget process and serve to fund the schools educational program and major operating expenses such as staff salaries and plant operations. Grants and federal program dollars are also administered through the budget process and provide funding for federal and district programs, and other educational initiatives. Another source, the schools Internal Fund, consists of revenue generated from student activities at the school site level. Revenue generated from Internal Fund activities is administered separately by each school and is not subject to the budget process. With the exception of the Fund 9 Program within the Internal Fund programs, whose revenue is an advance of school tax-dollar discretionary funds, Internal Fund revenue is unrelated to taxdollar monies. Refer to the diagram presented on page v for a visual overview of these two distinct funding sources. The State of Florida Department of Education has defined and established the responsibility for a school district s Internal Fund through Board of Education Rule Chapter 6A-1.085, Basic Principles of Internal Fund Accounting. As stipulated in this Rule, monies collected and expended within a school shall be used for financing the normal program of school activities not otherwise financed, for providing necessary and proper services and materials for school activities, and for other purposes consistent with the school program as established and approved by the School Board. Accordingly, since the district s School Board is responsible for the management of these funds, its duty shall be to adopt proper, generally recognized accounting policies and procedures to effectively administer the revenue generated from Internal Fund activities. In compliance with these provisions, School Board Rules 6Gx13-3D and 6Gx13-5C and refer to the Manual of Internal Fund Accounting as containing the adopted policies and procedures for Internal Fund activities. The policies and procedures set forth in this manual have taken into account the existing State of Florida Statutes, State Board of Education Rules, and Miami-Dade County School Board Rules. Therefore, they are to be enforced by administrators and school principals when administering and monitoring the schools Internal Fund activities. Principals, treasurers, student activity sponsors and all staff involved with Internal Fund activities must become familiar with this manual since the guidelines established i

2 are the authority for Internal Fund matters and supersede all other publications governing the administration of student activity funds. To avoid duplication of instructions, the manual contains references to other published procedure manuals where appropriate. The reader is directed to refer to these publications as applicable and to contact the district s Internal Fund Accounting Section for clarification, guidance and assistance pertaining to Internal Fund accounting issues. Additionally, administrative directives, memorandums of instruction, or other types of written communications may be issued during the fiscal year in order to institute necessary policies or procedures that relate to the management of Internal Fund activities. These communications will be considered supplementary to this manual and must be adhered to. Consequently, this manual is intended to be updated on an annual basis to incorporate the new or revised policies and procedures that may have resulted from these communications or from changes to School Board Rules. ii

3 OVERVIEW OF THIS MANUAL A committee comprised of school treasurers and personnel from the Internal Fund Accounting Section has prepared this manual. A second committee consisting of school principals, treasurers, and personnel from the Office of the Controller, Office of Management and Compliance Audits and the Office of Athletics, Activities and Accreditation has reviewed the policies and procedures prescribed herein for the management of the schools Internal Fund activities. The revision process was carefully undertaken to evaluate the guidelines in effect, to change the official manual to a more user-friendly format, and to effectuate necessary policy changes to ensure greater internal control. This manual provides specific procedures for long-established but undocumented practices deemed to be in the best interest of Miami-Dade County Public Schools. The contents of this manual are separated into eight (8) major sections denoted by Roman Numerals I thru VIII, with each section containing different chapters addressing pertinent topics. This format was devised to facilitate referencing and the revision process. The Table of Contents depicts the outline of this manual for easy reference. Flow charts, summary tables, sample documents, and other illustrations have been incorporated throughout to provide examples, summarize information that can be disseminated to staff, and facilitate the understanding of policies and procedures. SECTION I INTRODUCTION: The introductory section of this manual provides a summary of general policy pertinent to Internal Fund activities based on School Board Rules and other authoritative sources. To provide a general overview of the different programs and functions used to account for Internal Fund activities, a Quick Reference Guide as well as a brief summary of the codification of Internal Fund accounting structures is included. Additionally, this section contains flowcharts of the different accounting cycles to illustrate and facilitate the understanding of the internal control structure adopted to ensure the accountability of monies generated through Internal Fund activities. iii

4 SECTION II GENERAL ACCOUNTING POLICIES & PROCEDURES: This section sets forth the general accounting policies and procedures applicable to the different accounting cycles, with references to the required documentation that must be completed and maintained for all accounting transactions processed by a school. SECTION III PROGRAM SPECIFIC POLICIES & PROCEDURES: This section sets forth the policies and procedures applicable to the types of transactions that would be recorded under the different programs available in the Internal Fund. Additionally, it provides a description of the programs, some of the functions available under each of them, and the applicable restrictions for the types of transactions processed. SECTION IV ACTIVITY SPECIFIC POLICIES & PROCEDURES: This section establishes policies and procedures specific to major activities conducted and accounted for under the different programs in the schools Internal Fund. SECTION V CLOSING PROCEDURES: This section establishes the policies and procedures for the monthly and year-end closing process, as well as general policy regarding the retention of Internal Fund records. SECTIONS VI - FORMS, VII GLOSSARY OF TERMS, and VIII - INDEX: These sections are mainly for reference purposes. NOTE: Due to the nature of Internal Fund activities, issues may arise that are not addressed in this manual. Additionally, if contradictory information is noted between this manual and other documents issued by other district offices, generally the information in this manual supersedes other manuals, specifically when it relates to financial accounting policy and procedures. Nevertheless, for clarification under either of these circumstances, questions should be directed to the Internal Fund Accounting Section within the Office of the Controller for Miami-Dade County Public Schools. iv

5 v

6 Page 1-1 Chapter 1 General Policies I. POLICY SUMMARY School Board Rules are the adopted policies of the School Board to manage and control the District s operations. The policy for Internal Fund activities is derived mainly from School Board Rules that may be amended from time to time. Consequently, when inconsistencies arise, School Board Rules supersede policy in this manual. For purposes of identifying the School Board rules that directly relate to the administration of Internal Fund activities, references to specific Rules are included throughout this manual. A listing of the more general School Board Rules, along with a brief summary, is provided herein below in chronological order: Board Rule Number 6Gx13-1C-1.05 Policy Summary Acceptance of free materials is discussed. 6Gx13-1C Gx13-1C Gx13-1C Gx13-1C Gx13-1D Gx13-1D Gx13-1D-1.07 The distribution of materials containing advertising from outside of school sources is not permitted without the approval of the Office of the Superintendent of Schools. The employee United Way drive is an authorized fundraiser. The Superintendent may authorize participation with Scholarship Saturdays. Employees should not sell merchandise or services for personal gain. Solicitation in the name of the school without the principal and Region Center Superintendent approval is not permitted. Use of "tag days" is prohibited. Sale of magazines is permitted in high schools with compliance to Board Rule 6Gx13-5C The student United Way drive is an authorized fundraiser. The purpose of this drive is detailed. Student third party fundraising is addressed and its limitations. Exceptions must be transmitted to the Superintendent for School Board review. Guidelines for the use of school facilities for commercial film production are detailed. The terms government and school-allied organizations are defined. School-allied organizations must distinguish their activities from school activities. Procedures for building use are defined. No entertainment for which admission is charged may be held in a school during school hours. Guidelines for school/allied organization sponsored entertainment are detailed. All forms of gambling and games of chance are prohibited.

7 Page 1-2 Chapter 1 General Policies 6Gx13-1F Gx13-3B Gx13-3B Gx13-3B Gx13-3B Gx13-3B Gx13-3B Gx13-3B Gx13-3C Gx13-3C Gx13-3D Gx13-3D Gx13-3D Gx13-3C-1.18 Schools should affiliate in recognized associations because of the various benefits such affiliations provide. All funds available for investment are to be invested where they may earn the maximum possible yield. School fees must be approved annually by the Region Center. Parents must be notified. Non-essential school supplies and novelties can be sold by schools on a 20% mark-up profit basis. Uniforms and physical education equipment must be sold at cost. The sale of snacks and beverages have restrictions during the school day. It is unlawful for any person to sell, serve, vend or otherwise dispose of goods within 500 feet of any Miami-Dade County Public School property unless done so within a secure vending area. Obsolete or worn out items of personal property may only be disposed of by proper review by authorized persons. Schools may not lend, rent, or dispose of equipment without conforming to all regulations. Employees should be guided by the outlined principles and standards adopted by the National Association of Purchasing Management for the acquisition of equipment, supplies, and materials. The district bidding process is discussed. Schools making Internal Fund purchases will adhere to policies as outlined in the Manual of Internal Fund Accounting for Elementary and Secondary Schools. The specific procedures to be followed for internal funds are given in the Manual of Internal Accounting. Petty cash funds are authorized for the purpose of making small expenditures for the operation of schools and administrative units. The amount shall not exceed $ Procedures for the sale of student photographs and the acquisition of a photographer are detailed. Cost limitations relating to expenditures for recognition awards and incentives that may be purchased from school/district funds for students, employees, school volunteers, etc. are established.

8 Page 1-3 Chapter 1 General Policies 6Gx13-3E Gx13-4C Gx13-5B Gx13-5C Gx13-5C Gx13-6A Gx13-6A Gx13-6C The School Board is authorized to collect for damages from the parents of students under 18 who maliciously or willfully destroy school property. The amount of recovery is limited to $2,500. The procedures for collection are outlined. The specific procedures to be followed for travel expenses are given in the Travel Policies and Procedures Manual. Photograph service for senior high school annuals will be contracted on the basis of proper bids. The administration has the responsibility for making all necessary rules for safeguarding, accounting, and auditing of monies received associated with internal fund activities. Solicitations in homes and other fundraising policies are discussed. Field trips for students are permitted which have value in meeting educational objectives, are directly related to the curriculum, or are necessary to the fulfillment of obligations to the interscholastic athletic and activity programs. Field trip guidelines are discussed. Schools may determine student fees within the limitations set in this board rule. Area Vocational-Technical Centers are explained. AVTCs will follow the Manual of Internal Accounting when collecting and expending internal funds.

9 Page 2-1 Chapter 2 Codification of Accounting Transactions I. GENERAL OVERVIEW OF INTERNAL FUND ACCOUNTING STRUCTURES Internal Fund account structures have been established in accordance with the guidelines set forth in the Financial and Program Cost Accounting and Reporting for Florida Schools ( Red Book ), to maintain a uniform codification of financial transactions for accounting and reporting purposes. The Internal Fund Chart of Accounts is an all inclusive listing of available account codes for classifying and recording Internal Fund financial transactions and is maintained by the district s Internal Fund Accounting Section. Schools must submit written requests, signed by the principal, to this department to open new account structures, as needed. To activate existing account structures, verbal requests are acceptable. An Internal Fund accounting structure consists of the following elements: 1. Fund (0800) 2. Location (school site) 3. Program 4. Function 5. Object Fund 800 is the fund code for the schools Internal Fund. The following programs, with the respective program numbers (codes), are part of the Internal Fund: Program # Athletic Program 5001 Music Program 5002 Classes and Clubs Program 5003 Trust Program 5004 Property Fund Program 5005 School Store Program 5006 Instructional Fees Program 5007 General Program 5008 Instructional Materials and Educational Support (Fund 9) Program 5009 Adult Education Program 5010

10 Page 2-2 Chapter 2 Codification of Accounting Transactions Program # Community Schools Program 5011 Agriculture Program 5012 Food Service Program 5013 Production/Service Programs 5014 Dental Program 5015 Within the Internal Fund program classifications, function codes are used to classify the activities performed to accomplish the objectives of the school; thereby, function codes refer to the objective or purpose of a revenue or expenditure. A myriad of function numbers (codes) for each program classification are available in the Internal Fund Chart of Accounts to be used accordingly for recording financial transactions. Refer to the Quick Reference Table provided in, Chapter 3 for sample available functions for each program. In addition to the function assigned, object codes are used to classify revenue received and goods or services purchased. The following object names and corresponding codes are applicable for Internal Fund transactions: Revenue Objects Expenditure Objects Object # Object # Sales 4493 Out of County Travel 5331 Dues and Fees 4429 Field Trips 5332 Restricted Revenue 4445 Other Purchased Serv Other (Interest) 4490 Supplies 5510 Items for Re-sale 5595 Equipment 5640 Miscellaneous 5790 All financial transactions must be recorded using the proper structures in accordance with Internal Fund policy set forth in this manual. All schools and centers may obtain an all-inclusive listing of the Internal Fund Chart of Accounts from the district s Internal Fund Accounting Section accordingly. Refer to the following diagrams for a pictorial overview of Internal Fund accounting programs and functions.

for each program classification are available in the Internal Fund Chart of Accounts to be used accordingly for recording financial transactions.")

11 Page 2-3 Chapter 2 Codification of Accounting Transactions

12 Page 2-4 Chapter 2 Codification of Accounting Transactions

13 Page 3-1 Chapter 3 Quick Reference Table for Programs and Functions

14 Page 3-2 Chapter 3 Quick Reference Table for Programs and Functions

15 Page 3-3 Chapter 3 Quick Reference Table for Programs and Functions

16 Page 3-4 Chapter 3 Quick Reference Table for Programs and Functions

17 Date Issued: March 17, 2004 Page 4-3 Chapter 4 Accounting Cycle Flowcharts

18 Date Issued: March 17, 2004 Page 4-3 Chapter 4 Accounting Cycle Flowcharts

19 Date Issued: March 17, 2004 Page 4-3 Chapter 4 Accounting Cycle Flowcharts

SCHOOL BOARD OF BROWARD COUNTY, FL INTERNAL FUNDS ACCOUNTING FUNDRAISING ACTIVITIES

Page 1 of 6 FUNDRAISING ACTIVITIES TOPICS IN BULLETIN: I. FUNDRAISING ACTIVITIES LIMITATIONS II. FUNDRAISING ACTIVITY PROCEDURES III. FINANCIAL REPORT, STUDENT ACTIVITY OPERATING REPORT IV. STATEMENT OF

Page 1 of 6 FUNDRAISING ACTIVITIES TOPICS IN BULLETIN: I. FUNDRAISING ACTIVITIES LIMITATIONS II. FUNDRAISING ACTIVITY PROCEDURES III. FINANCIAL REPORT, STUDENT ACTIVITY OPERATING REPORT IV. STATEMENT OF

PUBLIC AND NON-PUBLIC FUNDS. Public funds - restricted to the same legal requirements as Board funds:

SECTION 1 Page 1 of 2 PUBLIC AND NON-PUBLIC FUNDS The funds maintained at the local schools can generally be divided into two major categories: public and non-public. Various factors must be considered

SECTION 1 Page 1 of 2 PUBLIC AND NON-PUBLIC FUNDS The funds maintained at the local schools can generally be divided into two major categories: public and non-public. Various factors must be considered

SCHOOL BOARD OF BROWARD COUNTY, FL INTERNAL FUNDS ACCOUNTING GENERAL POLICY

Page 1 of 9 GENERAL POLICY TOPICS IN BULLETIN: I. INTERNAL ACCOUNTS POLICIES II. RESPONSIBILITY - PRINCIPAL III. RESPONSIBILITY - BOOKKEEPER IV. EMPLOYEE RESTRICTIONS V. ACCOUNTING FOR STUDENT ACTIVITIES

Page 1 of 9 GENERAL POLICY TOPICS IN BULLETIN: I. INTERNAL ACCOUNTS POLICIES II. RESPONSIBILITY - PRINCIPAL III. RESPONSIBILITY - BOOKKEEPER IV. EMPLOYEE RESTRICTIONS V. ACCOUNTING FOR STUDENT ACTIVITIES

Cobb County Schools Booster Organizations. Resource Guide

Cobb County Schools Booster Organizations 8/22/13 Resource Guide Introduction: On behalf of the Cobb County School District we want to thank you for your service to help provide our students with the best

Cobb County Schools Booster Organizations 8/22/13 Resource Guide Introduction: On behalf of the Cobb County School District we want to thank you for your service to help provide our students with the best

Instructions for Schedule D (Form 990) Supplemental Financial Statements

Supplemental Financial Statements") 2009 Instructions for Schedule D (Form 990) Supplemental Financial Statements Department of the Treasury Internal Revenue Service Section references are to the Internal 1. That is separately identified

2009 Instructions for Schedule D (Form 990) Supplemental Financial Statements Department of the Treasury Internal Revenue Service Section references are to the Internal 1. That is separately identified

THE BOARD OF VISITORS OF VIRGINIA POLYTECHNIC INSTITUTE AND STATE UNIVERSITY POLICY GOVERNING FINANCIAL OPERATIONS AND MANAGEMENT

MANAGEMENT AGREEMENT BETWEEN THE COMMONWEALTH OF VIRGINIA AND VIRGINIA POLYTECHNIC INSTITUTE AND STATE UNIVERSITY PURSUANT TO THE RESTRUCTURED HIGHER EDUCATION FINANCIAL AND ADMINISTRATIVE OPERATIONS ACT

MANAGEMENT AGREEMENT BETWEEN THE COMMONWEALTH OF VIRGINIA AND VIRGINIA POLYTECHNIC INSTITUTE AND STATE UNIVERSITY PURSUANT TO THE RESTRUCTURED HIGHER EDUCATION FINANCIAL AND ADMINISTRATIVE OPERATIONS ACT

FLORIDA HIGH SCHOOL FOR ACCELERATED LEARNING - WEST PALM BEACH CAMPUS, INC. d/b/a QUANTUM HIGH SCHOOL

LEARNING - WEST PALM BEACH CAMPUS, INC. Financial Statements with Independent Auditors Reports Thereon June 30, 2015 CONTENTS Page Management s Discussion and Analysis 1 6 Report of Independent Auditors

LEARNING - WEST PALM BEACH CAMPUS, INC. Financial Statements with Independent Auditors Reports Thereon June 30, 2015 CONTENTS Page Management s Discussion and Analysis 1 6 Report of Independent Auditors

1320 DUTIES OF SCHOOL BUSINESS ADMINISTRATOR/ BOARD SECRETARY. 1. A valid certificate as a School Business Administrator.

1320/page 1 of 7 1320 DUTIES OF SCHOOL BUSINESS ADMINISTRATOR/ BOARD SECRETARY Qualifications 1. A valid certificate as a School Business Administrator. 2. Experience in educational administration, school

1320/page 1 of 7 1320 DUTIES OF SCHOOL BUSINESS ADMINISTRATOR/ BOARD SECRETARY Qualifications 1. A valid certificate as a School Business Administrator. 2. Experience in educational administration, school

ASSETS: TRACKING, INVENTORY, AND DISPOSAL OF ASSETS, AND ACQUISITION OF REAL PROPERTY

: TRACKING, INVENTORY, AND DISPOSAL OF, AND ACQUISITION OF REAL PROPERTY As Adopted: March 31, 2008 Amended: March 24, 2010 The Monroe County Airport Authority (Authority) constitutes a public benefit

: TRACKING, INVENTORY, AND DISPOSAL OF, AND ACQUISITION OF REAL PROPERTY As Adopted: March 31, 2008 Amended: March 24, 2010 The Monroe County Airport Authority (Authority) constitutes a public benefit

SCHOOL BOARD OF BROWARD COUNTY, FL INTERNAL FUNDS ACCOUNTING SALES AND USE TAXES

Page 1 of 7 SALES AND USE TAXES TOPICS IN BULLETIN: I. GENERAL INFORMATION EXEMPT ACTIVITIES AND ITEMS I TAXABLE ACTIVITIES AND ITEMS IV. SALES TAX EXEMPTION CERTIFICATE V. SALES TAX COLLECTIONS AND REMITTANCES

Page 1 of 7 SALES AND USE TAXES TOPICS IN BULLETIN: I. GENERAL INFORMATION EXEMPT ACTIVITIES AND ITEMS I TAXABLE ACTIVITIES AND ITEMS IV. SALES TAX EXEMPTION CERTIFICATE V. SALES TAX COLLECTIONS AND REMITTANCES

WORKING DRAFT HOUSE BILL NO. Select Committee on Capital Financing and Investments A BILL. for

00 STATE OF WYOMING 0LSO-0.W WORKING DRAFT HOUSE BILL NO. State building commission repeal. Sponsored by: Select Committee on Capital Financing and Investments A BILL for AN ACT relating to administration

00 STATE OF WYOMING 0LSO-0.W WORKING DRAFT HOUSE BILL NO. State building commission repeal. Sponsored by: Select Committee on Capital Financing and Investments A BILL for AN ACT relating to administration

Burleson Independent School District

Burleson Independent School District PTO/Booster Club Guidelines 11/1/2014 The following guidelines are to be used for student support activity groups (Parent Teacher Organizations, Booster Clubs, etc.)

Burleson Independent School District PTO/Booster Club Guidelines 11/1/2014 The following guidelines are to be used for student support activity groups (Parent Teacher Organizations, Booster Clubs, etc.)

BYLAWS. Robert E. Lee High School. Band Parents Organization. A Texas Non-Profit Corporation

BYLAWS Of Robert E. Lee High School Band Parents Organization A Texas Non-Profit Corporation Of Robert E. Lee High School Band Parents Organization A Texas Non-Profit Corporation ARTICLE I NAME The name

BYLAWS Of Robert E. Lee High School Band Parents Organization A Texas Non-Profit Corporation Of Robert E. Lee High School Band Parents Organization A Texas Non-Profit Corporation ARTICLE I NAME The name

Elements of Local School Accounting II

Elements of Local School Accounting II LSFM Certificate Program March 2015 Bryant Conference Center Tuscaloosa, Alabama 1 Elements of Local School Accounting II Board Policies and Procedures Accounting

Elements of Local School Accounting II LSFM Certificate Program March 2015 Bryant Conference Center Tuscaloosa, Alabama 1 Elements of Local School Accounting II Board Policies and Procedures Accounting

SCHOOL ACTIVITY FUNDS ACCOUNTING MANUAL

SCHOOL ACTIVITY FUNDS ACCOUNTING MANUAL TABLE OF CONTENTS INTRODUCTION Section 1 Section 2 Section 3 Section 4 Section 5 Section 6 Section 7 Section 8 FUND ACCOUNTING DESCRIPTION FUNDS 2.1 Funds 2.2 Restricted

SCHOOL ACTIVITY FUNDS ACCOUNTING MANUAL TABLE OF CONTENTS INTRODUCTION Section 1 Section 2 Section 3 Section 4 Section 5 Section 6 Section 7 Section 8 FUND ACCOUNTING DESCRIPTION FUNDS 2.1 Funds 2.2 Restricted

CARRIAGE MUSEUM OF AMERICA ACCOUNTING POLICIES AND PROCEDURES MANUAL. February 2014

CARRIAGE MUSEUM OF AMERICA ACCOUNTING POLICIES AND PROCEDURES MANUAL February 2014 I. Introduction The purpose of this manual is to describe all accounting policies and procedures currently in use at The

CARRIAGE MUSEUM OF AMERICA ACCOUNTING POLICIES AND PROCEDURES MANUAL February 2014 I. Introduction The purpose of this manual is to describe all accounting policies and procedures currently in use at The

Michigan Public School Accounting Manual presented by Glenda Rader Grand Ledge Public Schools September 23, 2015

Michigan Public School Accounting Manual presented by Glenda Rader Grand Ledge Public Schools September 23, 2015 Introduction Serves as MANDATORY Guide to the uniform classification and recording of accounting

Michigan Public School Accounting Manual presented by Glenda Rader Grand Ledge Public Schools September 23, 2015 Introduction Serves as MANDATORY Guide to the uniform classification and recording of accounting

Title 4 - Codification of Board Policy Statements. Chapter 9 NEVADA SYSTEM OF HIGHER EDUCATION INTERNAL AUDIT, FINANCE AND ADMINISTRATION POLICIES

Title 4 - Codification of Board Policy Statements Chapter 9 NEVADA SYSTEM OF HIGHER EDUCATION INTERNAL AUDIT, FINANCE AND ADMINISTRATION POLICIES A. Internal Audit Department Charter... 2 Section 1. Nature...

Title 4 - Codification of Board Policy Statements Chapter 9 NEVADA SYSTEM OF HIGHER EDUCATION INTERNAL AUDIT, FINANCE AND ADMINISTRATION POLICIES A. Internal Audit Department Charter... 2 Section 1. Nature...

Sample 1023, Application for Recognition of Exemption FILING INSTRUCTIONS

Sample 1023, Application for Recognition of Exemption FILING INSTRUCTIONS Remember, on all attachments to have a heading with your PTA s corporation name and EIN (Employer ID Number). Form 1023 (Rev. 12-2011)

Sample 1023, Application for Recognition of Exemption FILING INSTRUCTIONS Remember, on all attachments to have a heading with your PTA s corporation name and EIN (Employer ID Number). Form 1023 (Rev. 12-2011)

RULES OF THE AUDITOR GENERAL

RULES OF THE AUDITOR GENERAL CHAPTER 10.850 AUDITS OF CHARTER SCHOOLS AND SIMILAR ENTITIES, FLORIDA VIRTUAL SCHOOL, AND VIRTUAL INSTRUCTION PROGRAM PROVIDERS EFFECTIVE 06-30-15 RULES OF THE AUDITOR GENERAL

RULES OF THE AUDITOR GENERAL CHAPTER 10.850 AUDITS OF CHARTER SCHOOLS AND SIMILAR ENTITIES, FLORIDA VIRTUAL SCHOOL, AND VIRTUAL INSTRUCTION PROGRAM PROVIDERS EFFECTIVE 06-30-15 RULES OF THE AUDITOR GENERAL

Chapter 8. School Internal Funds

Chapter 8 School Internal Funds SECTION I PRINCIPLES 1. The district school board shall be responsible for the administration and control of internal funds of the district school system, and in connection

Chapter 8 School Internal Funds SECTION I PRINCIPLES 1. The district school board shall be responsible for the administration and control of internal funds of the district school system, and in connection

Operating Procedures Manual Indiana Natural Resources Foundation

Operating Procedures Manual Indiana Natural Resources Foundation Adopted May 2003 I. GENERAL ORGANIZATIONAL PROCEDURES Subject: Corporate Organization The Indiana Natural Resources Foundation (Foundation)

Operating Procedures Manual Indiana Natural Resources Foundation Adopted May 2003 I. GENERAL ORGANIZATIONAL PROCEDURES Subject: Corporate Organization The Indiana Natural Resources Foundation (Foundation)

WOUNDED WARRIOR PROJECT, INC. (A NOT-FOR-PROFIT ORGANIZATION)

") (A NOT-FOR-PROFIT ORGANIZATION) FINANCIAL REPORT TABLE OF CONTENTS Report of independent certified public accountants 1 Financial statements: Statement of financial position 2 Statement of activities 3

(A NOT-FOR-PROFIT ORGANIZATION) FINANCIAL REPORT TABLE OF CONTENTS Report of independent certified public accountants 1 Financial statements: Statement of financial position 2 Statement of activities 3

WISHES & MORE AUDITED FINANCIAL STATEMENTS DECEMBER 31, 2014

AUDITED FINANCIAL STATEMENTS DECEMBER 31, 2014 SCHLENNER WENNER & CO. Certified Public Accountants & Business Consultants TABLE OF CONTENTS Independent Auditors' Report... 1 Statements of Financial Position...

AUDITED FINANCIAL STATEMENTS DECEMBER 31, 2014 SCHLENNER WENNER & CO. Certified Public Accountants & Business Consultants TABLE OF CONTENTS Independent Auditors' Report... 1 Statements of Financial Position...

RULE 2 EFFECTIVE DATE JULY 7, 2013 (REVISED) NEBRASKA DEPARTMENT OF EDUCATION UNIFORM SYSTEM OF ACCOUNTING FOR NEBRASKA PUBLIC SCHOOL DISTRICTS

NEBRASKA DEPARTMENT OF EDUCATION UNIFORM SYSTEM OF ACCOUNTING FOR NEBRASKA PUBLIC SCHOOL DISTRICTS") NEBRASKA DEPARTMENT OF EDUCATION RULE 2 UNIFORM SYSTEM OF ACCOUNTING FOR NEBRASKA PUBLIC SCHOOL DISTRICTS TITLE 92, NEBRASKA ADMINISTRATIVE CODE, EFFECTIVE DATE JULY 7, 2013 (REVISED) State of Nebraska

NEBRASKA DEPARTMENT OF EDUCATION RULE 2 UNIFORM SYSTEM OF ACCOUNTING FOR NEBRASKA PUBLIC SCHOOL DISTRICTS TITLE 92, NEBRASKA ADMINISTRATIVE CODE, EFFECTIVE DATE JULY 7, 2013 (REVISED) State of Nebraska

5. The administration of the school shall decide how to use student-generated funds to benefit the student body.

SHELBY COUNTY SCHOOLS DIVISION OF INTERNAL AUDIT (DIA) QUICK REFERENCE GUIDE FOR PRINCIPALS The principal of each school shall have the duty of implementing and following the regulations, standards and

SHELBY COUNTY SCHOOLS DIVISION OF INTERNAL AUDIT (DIA) QUICK REFERENCE GUIDE FOR PRINCIPALS The principal of each school shall have the duty of implementing and following the regulations, standards and

IMPLEMENTING GASB STATEMENT NO. 68 ACCOUNTING AND FINANCIAL REPORTING FOR PENSIONS A CCMA WHITE PAPER FOR CALIFORNIA LOCAL GOVERNMENTS

IMPLEMENTING GASB STATEMENT NO. 68 ACCOUNTING AND FINANCIAL REPORTING FOR PENSIONS A CCMA WHITE PAPER FOR CALIFORNIA LOCAL GOVERNMENTS Issued April 2015 PUBLISHED BY THE CALIFORNIA COMMITTEE ON MUNICIPAL

IMPLEMENTING GASB STATEMENT NO. 68 ACCOUNTING AND FINANCIAL REPORTING FOR PENSIONS A CCMA WHITE PAPER FOR CALIFORNIA LOCAL GOVERNMENTS Issued April 2015 PUBLISHED BY THE CALIFORNIA COMMITTEE ON MUNICIPAL

COMMUNITY BLOOD CENTERS OF FLORIDA, INC. AND AFFILIATE

CONSOLIDATED FINANCIAL STATEMENTS CONTENTS Independent Auditors Report...1 Consolidated Financial Statements Statement of Financial Position... 2-3 Statement of Activities and Changes in Net Assets...4

CONSOLIDATED FINANCIAL STATEMENTS CONTENTS Independent Auditors Report...1 Consolidated Financial Statements Statement of Financial Position... 2-3 Statement of Activities and Changes in Net Assets...4

SOS CHILDREN S VILLAGES USA, INC.

FINANCIAL STATEMENTS AND REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS DECEMBER 31, 2014 AND 2013 TABLE OF CONTENTS REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS 1-2 Page FINANCIAL STATEMENTS

FINANCIAL STATEMENTS AND REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS DECEMBER 31, 2014 AND 2013 TABLE OF CONTENTS REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS 1-2 Page FINANCIAL STATEMENTS

RULES OF THE AUDITOR GENERAL

RULES OF THE AUDITOR GENERAL CHAPTER 10.800 AUDITS OF DISTRICT SCHOOL BOARDS EFFECTIVE 06-30-12 RULES OF THE AUDITOR GENERAL CHAPTER 10.800 TABLE OF CONTENTS Rule Description Page Section No. PREFACE TO

RULES OF THE AUDITOR GENERAL CHAPTER 10.800 AUDITS OF DISTRICT SCHOOL BOARDS EFFECTIVE 06-30-12 RULES OF THE AUDITOR GENERAL CHAPTER 10.800 TABLE OF CONTENTS Rule Description Page Section No. PREFACE TO

SOS CHILDREN S VILLAGES USA, INC.

FINANCIAL STATEMENTS AND REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS DECEMBER 31, 2015 AND 2014 TABLE OF CONTENTS REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS 1-2 Page FINANCIAL STATEMENTS

FINANCIAL STATEMENTS AND REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS DECEMBER 31, 2015 AND 2014 TABLE OF CONTENTS REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS 1-2 Page FINANCIAL STATEMENTS

COMMITTEE CHAIRPERSONS

Program of Activities 2012-2013 COMMITTEE CHAIRPERSONS STUDENT DEVELOPMENT COMMITTEE CHAIRPERSON 1. Awards State Secretary 2. Publicity State Reporter 3. Student Leadership State Vice President 4. State

Program of Activities 2012-2013 COMMITTEE CHAIRPERSONS STUDENT DEVELOPMENT COMMITTEE CHAIRPERSON 1. Awards State Secretary 2. Publicity State Reporter 3. Student Leadership State Vice President 4. State

NATIONAL ENERGY EDUCATION DEVELOPMENT PROJECT, INC. Financial Statements and Supplemental Information

NATIONAL ENERGY EDUCATION DEVELOPMENT PROJECT, INC. Financial Statements and Supplemental Information (With Summarized Financial Information for the Year Ended December 31, 2011) and Report Thereon TABLE

NATIONAL ENERGY EDUCATION DEVELOPMENT PROJECT, INC. Financial Statements and Supplemental Information (With Summarized Financial Information for the Year Ended December 31, 2011) and Report Thereon TABLE

Audit of. G-Star School of the Arts For Motion Pictures and Television

Audit of G-Star School of the Arts For Motion Pictures and Television September 14, 2007 Report 2007-11 Audit of G-Star School of the Arts for Motion Pictures and Television Table of Contents PURPOSE AND

Audit of G-Star School of the Arts For Motion Pictures and Television September 14, 2007 Report 2007-11 Audit of G-Star School of the Arts for Motion Pictures and Television Table of Contents PURPOSE AND

Please see Section IX. for Additional Information:

The Florida Senate BILL ANALYSIS AND FISCAL IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) BILL: CS/SB 972 Prepared By: The

The Florida Senate BILL ANALYSIS AND FISCAL IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) BILL: CS/SB 972 Prepared By: The

SUBCHAPTER XI. GENERAL POLICE REGULATIONS.

SUBCHAPTER XI. GENERAL POLICE REGULATIONS. Article 37. Lotteries, Gaming, Bingo and Raffles. Part 2. Bingo and Raffles. 14-309.5. Bingo. (a) The purpose of the conduct of bingo is to insure a maximum availability

SUBCHAPTER XI. GENERAL POLICE REGULATIONS. Article 37. Lotteries, Gaming, Bingo and Raffles. Part 2. Bingo and Raffles. 14-309.5. Bingo. (a) The purpose of the conduct of bingo is to insure a maximum availability

State of Connecticut REGULATION of

Page 1 of 8 Pages R-39 Rev. 9/2003 IMPORTANT: Read instructions on bottom of Certification Page before completing this form. Failure to comply with instructions may cause disapproval of proposed Regulations

Page 1 of 8 Pages R-39 Rev. 9/2003 IMPORTANT: Read instructions on bottom of Certification Page before completing this form. Failure to comply with instructions may cause disapproval of proposed Regulations

Doral Performing Arts and Entertainment Academy (A charter school under Doral College, Inc.) Doral, Florida

Doral, Florida") (A charter school under Doral College, Inc.) Doral, Florida Financial Statements and Independent Auditors' Report June 30, 2010 TABLE OF CONTENTS General Information....................................

(A charter school under Doral College, Inc.) Doral, Florida Financial Statements and Independent Auditors' Report June 30, 2010 TABLE OF CONTENTS General Information....................................

ATTACHMENT D CHARTER SCHOOLS IN MICHIGAN

ATTACHMENT D CHARTER SCHOOLS IN MICHIGAN Introduction In December of 1993, Michigan became the ninth state to pass charter school legislation. The current charter school statute applicable to this RFP

ATTACHMENT D CHARTER SCHOOLS IN MICHIGAN Introduction In December of 1993, Michigan became the ninth state to pass charter school legislation. The current charter school statute applicable to this RFP

ACCOUNTING POLICIES AND PROCEDURES SAMPLE MANUAL

(Name of Organization & logo) ACCOUNTING POLICIES AND PROCEDURES SAMPLE MANUAL (Date) Note: this sample manual is designed for nonprofit organizations with the following staff involved with accounting

(Name of Organization & logo) ACCOUNTING POLICIES AND PROCEDURES SAMPLE MANUAL (Date) Note: this sample manual is designed for nonprofit organizations with the following staff involved with accounting

Instructions for Schedule D (Form 990)

") 2015 Instructions for Schedule D (Form 990) Supplemental Financial Statements Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted.

2015 Instructions for Schedule D (Form 990) Supplemental Financial Statements Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted.

SCHEDULE "C" to the MEMORANDUM OF UNDERSTANDING BETWEEN ALBERTA HEALTH SERVICES AND THE ALBERTA MEDICAL ASSOCIATION (CMA ALBERTA DIVISION)

") SCHEDULE "C" to the MEMORANDUM OF UNDERSTANDING BETWEEN ALBERTA HEALTH SERVICES AND THE ALBERTA MEDICAL ASSOCIATION (CMA ALBERTA DIVISION) ELECTRONIC MEDICAL RECORD INFORMATION EXCHANGE PROTOCOL (AHS AND

SCHEDULE "C" to the MEMORANDUM OF UNDERSTANDING BETWEEN ALBERTA HEALTH SERVICES AND THE ALBERTA MEDICAL ASSOCIATION (CMA ALBERTA DIVISION) ELECTRONIC MEDICAL RECORD INFORMATION EXCHANGE PROTOCOL (AHS AND

Quality Procedures and Work Instructions Manual

Quality Procedures and Work Instructions Manual Revision Number: (1) ISSUED TO: MANUAL NO: REVISION NO: ISSUE DATE: President Date 1 ii. Table of Contents 1 of 4 0 Section Number Name Revision Date i.

Quality Procedures and Work Instructions Manual Revision Number: (1) ISSUED TO: MANUAL NO: REVISION NO: ISSUE DATE: President Date 1 ii. Table of Contents 1 of 4 0 Section Number Name Revision Date i.

SAMPLE FINANCIAL PROCEDURES MANUAL

SAMPLE FINANCIAL PROCEDURES MANUAL Approved by (organization s) Board of Directors on (date) I. GENERAL 1. The Board of Directors formulates financial policies, delegates administration of the financial

SAMPLE FINANCIAL PROCEDURES MANUAL Approved by (organization s) Board of Directors on (date) I. GENERAL 1. The Board of Directors formulates financial policies, delegates administration of the financial

The accounting system and procedures detailed herein are based on IC 20-41-1-1 et seq..

Revised 2010-1-1 CHAPTER 1 SCHOOL EXTRA-CURRICULAR ACCOUNT - OVERVIEW INTRODUCTION The accounting system and procedures detailed herein are based on IC 20-41-1-1 et seq.. Activity or activities as used

Revised 2010-1-1 CHAPTER 1 SCHOOL EXTRA-CURRICULAR ACCOUNT - OVERVIEW INTRODUCTION The accounting system and procedures detailed herein are based on IC 20-41-1-1 et seq.. Activity or activities as used

Chapter 1 Internal Accounts Overview

Chapter 1 Internal Accounts Overview The District is required to follow the guidelines established by Rule 6A-1.001, Financial and Program Cost Accounting and Reporting for Florida Schools, Chapter 8 School

Chapter 1 Internal Accounts Overview The District is required to follow the guidelines established by Rule 6A-1.001, Financial and Program Cost Accounting and Reporting for Florida Schools, Chapter 8 School

ALAMO COLLEGES FOUNDATION, INC. (A Texas nonprofit Foundation) AUDITED FINANCIAL STATEMENTS. Year Ended December 31, 2012

AUDITED FINANCIAL STATEMENTS. Year Ended December 31, 2012") R. D. Harrison, CPA Certified Public Accountant Member American Institute of Certified Public Accountants Registered with the Public Company Accounting Oversight Board ALAMO COLLEGES FOUNDATION, INC. AUDITED

R. D. Harrison, CPA Certified Public Accountant Member American Institute of Certified Public Accountants Registered with the Public Company Accounting Oversight Board ALAMO COLLEGES FOUNDATION, INC. AUDITED

PINAL COUNTY POLICY AND PROCEDURE 8.8. Replaces Policy Dated: January 12, 1981, and subsequent revisions to date

PINAL COUNTY POLICY AND PROCEDURE 8.8 Subject: CAPITAL ASSETS Date: Effective as of July 1, 2009 Pages: 1 of 6 Replaces Policy Dated: January 12, 1981, and subsequent revisions to date Purpose: The purpose

PINAL COUNTY POLICY AND PROCEDURE 8.8 Subject: CAPITAL ASSETS Date: Effective as of July 1, 2009 Pages: 1 of 6 Replaces Policy Dated: January 12, 1981, and subsequent revisions to date Purpose: The purpose

Financial Statements. August 31, 2013 and 2012. (With Independent Auditors Report Thereon)

") Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Statements of Financial Position 2 Statement of Activities Year ended August 31, 2013

Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Statements of Financial Position 2 Statement of Activities Year ended August 31, 2013

AN ACT relating to sales and use tax incentives. Be it enacted by the General Assembly of the Commonwealth of Kentucky:

AN ACT relating to sales and use tax incentives. Be it enacted by the General Assembly of the Commonwealth of Kentucky: Section 1. KRS 154.32-020 is amended to read as follows: (1) The purposes of this

AN ACT relating to sales and use tax incentives. Be it enacted by the General Assembly of the Commonwealth of Kentucky: Section 1. KRS 154.32-020 is amended to read as follows: (1) The purposes of this

FIVE MANAGEMENT SYSTEM Policies and Procedures Checklist

FIVE MANAGEMENT SYSTEM Procedures Checklist Provided by: Navajo Nation Office of the Auditor General TABLE OF CONTENTS Introduction.........................................1 General Administrative Procedures...............................1

FIVE MANAGEMENT SYSTEM Procedures Checklist Provided by: Navajo Nation Office of the Auditor General TABLE OF CONTENTS Introduction.........................................1 General Administrative Procedures...............................1

2008 Schedule D (Form 990) Instructions - Draft April 7, 2008. Schedule D contains a compilation of various financial statement attachments.

Instructions - Draft April 7, 2008. Schedule D contains a compilation of various financial statement attachments.") Highlights Schedule D contains a compilation of various financial statement attachments. Part I requires information regarding donor advised funds and other similar funds or accounts. This information

Highlights Schedule D contains a compilation of various financial statement attachments. Part I requires information regarding donor advised funds and other similar funds or accounts. This information

President and Board of Trustees Miami University 107 Roudebush Hall Oxford, Ohio 45056

President and Board of Trustees Miami University 107 Roudebush Hall Oxford, Ohio 45056 We have reviewed the Independent Auditors Report of the Miami University, Butler County, prepared by Deloitte & Touche

President and Board of Trustees Miami University 107 Roudebush Hall Oxford, Ohio 45056 We have reviewed the Independent Auditors Report of the Miami University, Butler County, prepared by Deloitte & Touche

ASPIRE CHARTER ACADEMY, INC. A Charter School and Component Unit of the District School Board of Orange County, Florida

Financial Statements with Independent Auditors Reports Thereon June 30, 2015 CONTENTS Page Management s Discussion and Analysis 1 6 Report of Independent Auditors on Basic Financial Statements and Supplementary

Financial Statements with Independent Auditors Reports Thereon June 30, 2015 CONTENTS Page Management s Discussion and Analysis 1 6 Report of Independent Auditors on Basic Financial Statements and Supplementary

Brief Description: Reorganizing and streamlining central service functions, powers, and duties of state government.

Washington State House of Representatives Office of Program Research Ways & Means Committee BILL ANALYSIS Brief Description: Reorganizing and streamlining central service functions, powers, and duties

Washington State House of Representatives Office of Program Research Ways & Means Committee BILL ANALYSIS Brief Description: Reorganizing and streamlining central service functions, powers, and duties

Supersedes: CAPR 173-4, 26 December 2012. Distribution: National CAP website. Pages: 7

NATIONAL HEADQUARTERS CIVIL AIR PATROL CAP REGULATION 173-4 16 DECEMBER 2014 Finance FUND RAISING/DONATIONS This regulation covers fund raising activities and donations to Civil Air Patrol (CAP) at the

NATIONAL HEADQUARTERS CIVIL AIR PATROL CAP REGULATION 173-4 16 DECEMBER 2014 Finance FUND RAISING/DONATIONS This regulation covers fund raising activities and donations to Civil Air Patrol (CAP) at the

Department of Education

State of Tennessee Department of Education Office of Local Finance Effective July 2011 Tennessee Internal School Uniform Accounting Policy ANUAL Table of Contents Preface... ii-1 Section 1: Introduction

State of Tennessee Department of Education Office of Local Finance Effective July 2011 Tennessee Internal School Uniform Accounting Policy ANUAL Table of Contents Preface... ii-1 Section 1: Introduction

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY 1. Purpose The Dixon Montessori Charter School Board of Directors ( Board ) has reviewed and adopted the following policies and procedures to ensure

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY 1. Purpose The Dixon Montessori Charter School Board of Directors ( Board ) has reviewed and adopted the following policies and procedures to ensure

BYLAWS OF Brownsboro Education Foundation Revised May 2014 ARTICLE I. - GENERAL

BYLAWS OF Brownsboro Education Foundation Revised May 2014 ARTICLE I. - GENERAL 1.1 Purpose. Brownsboro, Texas, Independent School District (ISD) Education Foundation is a public charity and is connected

BYLAWS OF Brownsboro Education Foundation Revised May 2014 ARTICLE I. - GENERAL 1.1 Purpose. Brownsboro, Texas, Independent School District (ISD) Education Foundation is a public charity and is connected

15-213. Procurement practices of school districts and charter schools; definitions

ARIZONA AUTHORITY 15-213. Procurement practices of school districts and charter schools; definitions A. The state board of education shall adopt rules prescribing procurement practices for all school districts

ARIZONA AUTHORITY 15-213. Procurement practices of school districts and charter schools; definitions A. The state board of education shall adopt rules prescribing procurement practices for all school districts

STANDARD CHART OF ACCOUNTS FOR ASSOCIATIONS

STANDARD CHART OF ACCOUNTS FOR ASSOCIATIONS (Developed by the ASAE Finance and Administration Section Council) INTRODUCTION For an association to carry out its purpose and meet its fiscal responsibility,

STANDARD CHART OF ACCOUNTS FOR ASSOCIATIONS (Developed by the ASAE Finance and Administration Section Council) INTRODUCTION For an association to carry out its purpose and meet its fiscal responsibility,

FORT MYERS PREPARATORY AND FITNESS ACADEMY, INC. A CHARTER SCHOOL AND COMPONENT UNIT OF THE DISTRICT SCHOOL BOARD OF LEE COUNTY, FLORIDA

THE DISTRICT SCHOOL BOARD OF LEE COUNTY, FLORIDA FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR S REPORTS THEREON JUNE 30, 2013 CONTENTS Page Management s Discussion and Analysis 1-7 Report of Independent

THE DISTRICT SCHOOL BOARD OF LEE COUNTY, FLORIDA FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR S REPORTS THEREON JUNE 30, 2013 CONTENTS Page Management s Discussion and Analysis 1-7 Report of Independent

United Cerebral Palsy, Inc. Financial Report September 30, 2013

Financial Report September 30, 2013 Contents Independent Auditor s Report 1 2 Financial Statements Statement Of Financial Position 3 Statement Of Activities 4 Statement Of Functional Expenses 5 Statement

Financial Report September 30, 2013 Contents Independent Auditor s Report 1 2 Financial Statements Statement Of Financial Position 3 Statement Of Activities 4 Statement Of Functional Expenses 5 Statement

The Children's Museum of Memphis, Inc. Financial Statements June 30, 2015 and 2014

The Children's Museum of Memphis, Inc. Financial Statements June 30, 2015 and 2014 Table of Contents June 30, 2015 and 2014 Page Independent Auditor s Report... 3 Financial Statements Statements of Financial

The Children's Museum of Memphis, Inc. Financial Statements June 30, 2015 and 2014 Table of Contents June 30, 2015 and 2014 Page Independent Auditor s Report... 3 Financial Statements Statements of Financial

RANDALL COUNTY FIXED ASSET POLICY April 2002 Revised 5/20/2014

RANDALL COUNTY FIXED ASSET POLICY April 2002 Revised 5/20/2014 Fixed Asset Policy 1 I. INTRODUCTION The Taxpayers of Randall County have an enormous investment in our county buildings, land, furnishings,

RANDALL COUNTY FIXED ASSET POLICY April 2002 Revised 5/20/2014 Fixed Asset Policy 1 I. INTRODUCTION The Taxpayers of Randall County have an enormous investment in our county buildings, land, furnishings,

SAFE Credit Underwriting Guidelines for Non-Profit Lending. Organization Type: NON-PROFIT ORGANIZATIONS. Bridge Loan Guidelines.

Introduction The Credit Underwriting Guidelines (CUG) manual is designed for use with products delivered to faith-based and non-profit organizations. The guidelines herein govern the granting of credit

Introduction The Credit Underwriting Guidelines (CUG) manual is designed for use with products delivered to faith-based and non-profit organizations. The guidelines herein govern the granting of credit

Independent School District of Boise City. Elementary Checking Account Procedures

Independent School District of Boise City Elementary Checking Account Procedures Printed March 2012 TABLE OF CONTENTS ELEMENTARY SCHOOL FUNDS... 1 I. INTRODUCTION... 1 II. DESCRIPTION OF ACCOUNTS... 2

Independent School District of Boise City Elementary Checking Account Procedures Printed March 2012 TABLE OF CONTENTS ELEMENTARY SCHOOL FUNDS... 1 I. INTRODUCTION... 1 II. DESCRIPTION OF ACCOUNTS... 2

CALIFORNIA INFRASTRUCTURE AND ECONOMIC DEVELOPMENT BANK INVESTMENT POLICY

CALIFORNIA INFRASTRUCTURE AND ECONOMIC DEVELOPMENT BANK INVESTMENT POLICY UPDATED INVESTMENT POLICY DATED February 24, 2015 Section California Infrastructure and Economic Development Bank Investment Policy

CALIFORNIA INFRASTRUCTURE AND ECONOMIC DEVELOPMENT BANK INVESTMENT POLICY UPDATED INVESTMENT POLICY DATED February 24, 2015 Section California Infrastructure and Economic Development Bank Investment Policy

UNIVERSITY OF MASSACHUSETTS RECORD MANAGEMENT, RETENTION AND DISPOSITION POLICY

DOC. T99-061 Passed by the BoT 8/4/99 UNIVERSITY OF MASSACHUSETTS RECORD MANAGEMENT, RETENTION AND DISPOSITION POLICY The President of the University shall adopt guidelines to require that each campus

DOC. T99-061 Passed by the BoT 8/4/99 UNIVERSITY OF MASSACHUSETTS RECORD MANAGEMENT, RETENTION AND DISPOSITION POLICY The President of the University shall adopt guidelines to require that each campus