Optimizing Working Capital: New Techniques and Measurements for the Thoughtful Treasurer

|

|

|

- Sydney Wilson

- 8 years ago

- Views:

Transcription

1 Optimizing Working Capital: New Techniques and Measurements for the Thoughtful Treasurer New York Cash Exchange June 1, 2006 Craig A. Jeffery, Strategic Treasurer, Art Lorenz, Hunter Douglas

2 Working Capital is Simple The accounting measure of working capital Current methodologies of managing working capital The impact on the balance sheet and income statement is significant Working capital is easy to understand through the financial statements 2

3 Net working capital is a simple formula... Accounts Receivable + Inventory - Accounts Payable Net Working Capital 3

4 Working Capital Review Cash management: Optimizing an organization s cash Cash, Short term debt, Short term investments Working Capital Management: Optimizing the current assets and liabilities employed in the primary business Accounts receivable, Accounts payable, Inventory 4

5 Working Capital encompasses more than Traditional Cash Management Traditional Cash Mgmt Traditional Cash Mgmt 5

6 Working Capital is Important Cash is king. Working capital has a major impact on cash. These all impact the financial performance and liquidity of the organization Balance Sheet vs. Income Statement 6

7 7

8 8

9 Perspective on managing WC Think in broad terms. Cash management to treasury management. Cash is king. Profit is important. Working capital is a key component of managing your balance sheet and optimizing your profit. Treasury has the pulse on cash in an organization, and managing working capital is an essential contributor 9

10 Working Capital is Tricky Comparing to others o Public financial statements are limited in what they provide Not a clean view of: o History OR the future o Comparison to competitors o Business-mix or customer-type changes. Working Capital is different from liquidity DSO Comparison Retail Retail a fair comparison, right? K-Mart WMT TGT Benchmarking can support bad behaviors and bad activities due to these differences. 10

11 Metrics for Working Capital and Liquidity Traditional Days Inventory: Inventory/CGS x 365 Days Receivable: Accts Receivable/Sales x 365 Days Payable: Accts Payable/CGS x 365 Utilize formula to identify issues in specific working capital area Note: Different denominators makes cross comparison impossible. Alternative Days Inventory: Inventory / Sales x 365 Days Receivable: Accts Receivable / Sales x 365 Days Payable: Accts Payable / Sales x 365 Note: By using sales for all three categories, it is easier to understand the overall cost. Cash Conversion Cycle: Days Inventory +Days Receivable -Days Payable Utilize to understand the overall cost of working capital 11

12 Comparison of formulas Traditional Method Alternate Method Denominator Denominator Accounts Receivable 1, Day Sales 7.5 Day Sales Inventory 10, Day COGS 50.3 Day Sales Accounts Payable 5, Day COGS 28.8 Day Sales Net Working Capital 5, ??? 29.0 Day Sales Sales 73,094 Cost of Goods Sold 47,345 Day sales = / Day COGS 47345/ Alternative method uses sales as a common frame of reference 12

13 Using Historical Data - Same Company (possible to abuse) (15.8) 45.8 (23.4) Net Adjusted Working Capital-HD (Days Sales) (28.6) (29.1) (28.8) (29.1) (31.0) Jan 01 Jan 02 Jan 03 Jan 04 Jan 05 Best Estimated DPO (A/P) Days Inventory DSO (A/R) NAWC 13

Jan 01 Jan 02 Jan 03 Jan 04 Jan 05 Best Estimated 6.2 20.2 6.")

14 Benchmarking: WMT, TGT, K-Mart DSO Comparison Days Inventory Comparison K-Mart WMT TGT K-Mart WMT TGT DPO Comparison NAWC Comparison K-Mart WMT TGT K-Mart WMT TGT Is there a competitive advantage by not financing an additional 20+ days of sales?

15 The impact of electronics is measured differently for liquidity and working capital concerns It is the difference between accounting and treasury and between the Treasurer and Controller DSO Measures are based on financial statements - Cash is recognized at receipt, not availability, for accounting purposes -Cash can only be used when the funds are collected for treasury purposes -Collected vs. ledger 15

16 Float differences (samples for a starting point) Float Direction Type Mail Processing Collection Total Inhouse Lockbox Dropbox Conversion (Dropbox ARC Conversion (Lockbox ARC) Over the counter check Conversion (POP) ACH Inbound Inhouse vs. Lockbox Difference: 5.5 to 3.2 total days of float Difference: Liquidity 2.3 days ( Mail, Processing, Collection) WC 2.0 days ( Mail & Processing) 16

WC 2.0 days (4.0-2.0 Mail & Processing) 16")

17 Balance Sheet Financial Analysis Individual Division(s), Type of Change Paper/Image Sales/Day Paper-Average Current Float Average Current Float % Electronic 300, % Impact Liquidity Impact ,000 Working Captal Impact (accounting measure) ,000 Economic Impact 115,920 Weighted Avg Cost of Capital 12% Impact days differ from the previous slide. The previous slide showed business days. This shows calendar days. Thus, the previous slides numbers are multiplied by the weekend factor of 1.4 to arrive at calendar days. 17

18 Working Capital Must be Optimized It is easy to get out of control Excellent companies manage working capital in a thoughtful manner Cash is king Working capital has a major influence on cash, and is often far more influential in liquidity than cash by itself Companies that do not manage working capital effectively often run into liquidity problems 18

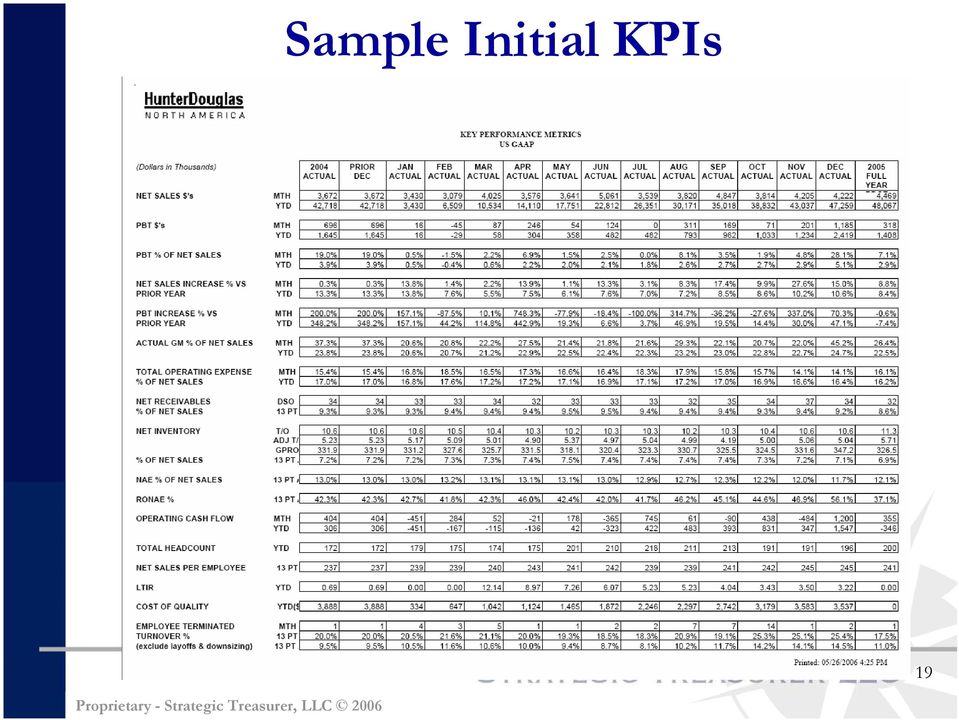

19 Sample Initial KPIs 19

20 Working capital involves many functional areas and is tough to manage Finance is involved in the order-to-pay and order-tocollect processes. o Other business areas are involved. No single person is responsible for all the areas that impact working capital. 20

21 Techniques Then Traditional working capital measures DSO, DPO, DI Now Traditional working capital measures plus Alternative working capital measures Liquidity measurements Income statement and balance sheet metrics Understanding the linkage 21

22 The Treasurer Must Own Working Capital The treasurer sits at the fulcrum point for cash flow The treasurer has key critical insight into the strategic operation of the business and cash and must contribute in that area in order to be strategic The treasurer needs to educate the organization on the value of managing working capital and the interplay between the balance sheet and the income statement The treasurer must report and reward good working capital usage progress reports The treasurer must form a team from the different functional areas and responsibility areas to help optimize working capital 22

23 Cash Conversion Spans the Business, So Must the Treasurer A/P Inventory A/R 23

24 Working Capital Roles Sr. Management: Link working capital goals to overall performance metrics Working Capital and Income Not: Working Capital vs. Income Treasurer: Owner of working capital Chair of the working capital council of the organization Working Capital Council: Educate stakeholders on importance of working capital Communicate drivers of WC and plans Reward and encourage good work that supports balance sheet and income statement goals on an integrated basis 24

25 Developing a Working Capital Council Working Capital Council Steering Committee Chair: Treasurer Operating Committee Manufacturing VP Finance Fabrication VP Finance Manufacturing Fabrication Credit A process that promotes buy-in and understanding across business functions 25

26 Working Capital Perspective 1. The best and most successful firms manage working capital in a thoughtful manner. 2. Working Capital needs to be optimized not minimized. There is a tradeoff between working capital and profitability, and price negotiations, terms and vendor relationship 3. Effective management of working capital requires: A. High level goals/measurements B. Activity goals C. Leadership D. Communication E. Proper rewards structure 26

27 Contact Page Craig A. Jeffery, AAP, CCM, FLMI Managing Director STRATEGIC TREASURER, LLC 500 Westpark Drive, Suite 110 Peachtree City, GA O: C: F: E: Visit the website for web-based training on specific treasury related topics, treasury information resources, and treasury related articles. Website: Art Lorenz, CPA, CTP Assistant Treasurer HUNTERDOUGLAS 2 Parkway Upper Saddle, NJ O: F: E: art.lorenz@hunterdouglas.com Visit the website for information on our services and products. Website: 27

Best Practice Working Capital

Best Practice Working Capital Introduction to bpworkingcapital & Services MacArthur Discussion Group 7 th April 2010 About bpworkingcapital Specialists in Best Practice Working Capital Improvement Focus

Best Practice Working Capital Introduction to bpworkingcapital & Services MacArthur Discussion Group 7 th April 2010 About bpworkingcapital Specialists in Best Practice Working Capital Improvement Focus

Working capital optimization

Working capital optimization Simon Rockcliffe Ernst & Young Background Methodology and approach Canadian Financial Executives Research Foundation (CFERF) Methodology: FEI Executive Survey (November 2012)

Working capital optimization Simon Rockcliffe Ernst & Young Background Methodology and approach Canadian Financial Executives Research Foundation (CFERF) Methodology: FEI Executive Survey (November 2012)

Understanding Working Capital in a Successful Business Acquisition or Where is the Working Capital?

Understanding Working Capital in a Successful Business Acquisition or Where is the Working Capital? Working capital definition- 1. The amount of capital needed to carry on a business. 2. Accounting- current

Understanding Working Capital in a Successful Business Acquisition or Where is the Working Capital? Working capital definition- 1. The amount of capital needed to carry on a business. 2. Accounting- current

Ratio Analysis: Liquidity, Activity & Coverage

Ratio Analysis: Liquidity, Activity & Coverage Quality of Earnings Fraudulent actions Above-average financial risk One-time transactions Borrow from the future/reach into the past Ride the depreciation

Ratio Analysis: Liquidity, Activity & Coverage Quality of Earnings Fraudulent actions Above-average financial risk One-time transactions Borrow from the future/reach into the past Ride the depreciation

Lean Mean Receivables Machine

Lean Mean Receivables Machine Jesse Sandoval, AAP VP, Senior Product Manager Union Bank Nancy Atkinson, CCM Senior Analyst Aite Group Carolyn Swafford, CTP, AAP VP, Treasury Management Solutions Advisor

Lean Mean Receivables Machine Jesse Sandoval, AAP VP, Senior Product Manager Union Bank Nancy Atkinson, CCM Senior Analyst Aite Group Carolyn Swafford, CTP, AAP VP, Treasury Management Solutions Advisor

Freeing cash flow in your business

Working Capital Management Freeing cash flow in your business pwc.com.au/privateclients Executive summary Your company is growing. Sales are skyrocketing, you re taking on new people and you re looking

Working Capital Management Freeing cash flow in your business pwc.com.au/privateclients Executive summary Your company is growing. Sales are skyrocketing, you re taking on new people and you re looking

Welcome to the financial reports topic. 5-1-1

Welcome to the financial reports topic. 5-1-1 We will explore the effect of standard processes in SAP Business One on Financial Reports: such as the Balance Sheet, the Trial Balance, and the Profit and

Welcome to the financial reports topic. 5-1-1 We will explore the effect of standard processes in SAP Business One on Financial Reports: such as the Balance Sheet, the Trial Balance, and the Profit and

SAP Working Capital Analytics Overview. SAP Business Suite Application Innovation January 2014

Overview SAP Business Suite Application Innovation January 2014 Overview SAP Business Suite Application Innovation SAP Working Capital Analytics Introduction SAP Working Capital Analytics Why Using HANA?

Overview SAP Business Suite Application Innovation January 2014 Overview SAP Business Suite Application Innovation SAP Working Capital Analytics Introduction SAP Working Capital Analytics Why Using HANA?

Having cash on hand is costly since you either have to raise money initially (for example, by borrowing from a bank) or, if you retain cash out of

or, if you retain cash out of") 1 Working capital refers to liquid funds used to purchase materials and pay workers. This is in contrast to long term capital such as buildings and machinery. Part of working capital management is cash

1 Working capital refers to liquid funds used to purchase materials and pay workers. This is in contrast to long term capital such as buildings and machinery. Part of working capital management is cash

OBIEE 11g Pre-Built Dashboards from Oracle Courtesy: Oracle OBIEE 11g Deployment on Vision Demo Data FINANCIALS

FINANCIALS General Ledger The General Ledger module provides insight into key financial areas of performance, including balance sheet, cash flow, budget vs. actual, working capital, liquidity. Dashboard

FINANCIALS General Ledger The General Ledger module provides insight into key financial areas of performance, including balance sheet, cash flow, budget vs. actual, working capital, liquidity. Dashboard

Work Capital and the Cash Conversion Cycle

Capital Source Solutions 3115 S. Grand Blvd, Suite 350E St. Louis, MO 63118 Phone: 314-226- 3663 Fax: 314-584- 2085 Web: www.capitalsolutionsstl.com Working Capital Best Practices If you are in business

Capital Source Solutions 3115 S. Grand Blvd, Suite 350E St. Louis, MO 63118 Phone: 314-226- 3663 Fax: 314-584- 2085 Web: www.capitalsolutionsstl.com Working Capital Best Practices If you are in business

Case Study: Automating Healthcare Supplier Payments

Case Study: Automating Healthcare Supplier Payments Robert Raucci, Director-Treasury Operations Thomas Jefferson University June St. John, SVP, CTP Wells Fargo Treasury Management 2 Overview Today s healthcare

Case Study: Automating Healthcare Supplier Payments Robert Raucci, Director-Treasury Operations Thomas Jefferson University June St. John, SVP, CTP Wells Fargo Treasury Management 2 Overview Today s healthcare

Advanced Working Capital Management

Advanced Working Capital Management 2005 Ken Parkinson Treasury Info. Services tisconsulting.com Session #507 1 What is Working Capital Management? Focus on the short term in real time Primary and secondary

Advanced Working Capital Management 2005 Ken Parkinson Treasury Info. Services tisconsulting.com Session #507 1 What is Working Capital Management? Focus on the short term in real time Primary and secondary

Strategies for optimizing your cash management

Part of the Deloitte working capital series Make your working capital work for you Strategies for optimizing your cash management The Deloitte working capital series Strategies for optimizing your accounts

Part of the Deloitte working capital series Make your working capital work for you Strategies for optimizing your cash management The Deloitte working capital series Strategies for optimizing your accounts

Understanding Financial Information for Bankruptcy Lawyers 13-Week Cash Flow Projections

Understanding Financial Information for Bankruptcy Lawyers 13-Week Cash Flow Projections What Are TWCF Projections? One of the most important areas for any business and its management team to deeply understand

Understanding Financial Information for Bankruptcy Lawyers 13-Week Cash Flow Projections What Are TWCF Projections? One of the most important areas for any business and its management team to deeply understand

Working Capital Analytics Overview. SAP Business Suite Application Innovation March 2015

Working Capital Analytics Overview SAP Business Suite Application Innovation March 2015 Abstract As of Smart Financials 1.0 SP02 SAP delivers Working Capital Analytics DSO Analysis Working Capital Analytics

Working Capital Analytics Overview SAP Business Suite Application Innovation March 2015 Abstract As of Smart Financials 1.0 SP02 SAP delivers Working Capital Analytics DSO Analysis Working Capital Analytics

Using dashboard reports. Selecting KPIs

WHITE PAPER When you have accurate, timely and actionable financial information, you re able to make smarter business decisions. Key Performance Indicators (KPIs) can provide a clear picture of your company

WHITE PAPER When you have accurate, timely and actionable financial information, you re able to make smarter business decisions. Key Performance Indicators (KPIs) can provide a clear picture of your company

Southern California AFP Luncheon

Working Capital Unharness your Cash Flow Southern California AFP Luncheon Michael Diekmann Director, Bank of America Merrill Lynch October 10, 2014 Understanding Working Capital Working Capital... = Current

Working Capital Unharness your Cash Flow Southern California AFP Luncheon Michael Diekmann Director, Bank of America Merrill Lynch October 10, 2014 Understanding Working Capital Working Capital... = Current

Integrating Payables and Receivables to Unlock Working Capital

Integrating Payables and Receivables to Unlock Working Capital Approved for 1 CTP / CCM recertification credit by the Association of Financial Professionals May 2009 Introductions David Kunz Treasury Management

Integrating Payables and Receivables to Unlock Working Capital Approved for 1 CTP / CCM recertification credit by the Association of Financial Professionals May 2009 Introductions David Kunz Treasury Management

5 Good Reasons for Ramping up Your Receivables Management

5 Good Reasons for Ramping up Your Receivables Management June 2013 by Mary Ann Rydel, Director Products and Customer Services North America, Hanse Orga International Corp. 5 Good Reasons for Ramping up

5 Good Reasons for Ramping up Your Receivables Management June 2013 by Mary Ann Rydel, Director Products and Customer Services North America, Hanse Orga International Corp. 5 Good Reasons for Ramping up

Chapter Financial Forecasting

Chapter Financial Forecasting PPT 4-2 Chapter 4 - Outline What is Financial Forecasting? 3 Financial Statements for Forecasting Constructing Pro Forma Statements Basis for Sales Projections Steps in a

Chapter Financial Forecasting PPT 4-2 Chapter 4 - Outline What is Financial Forecasting? 3 Financial Statements for Forecasting Constructing Pro Forma Statements Basis for Sales Projections Steps in a

CHAPTER 16 Current Asset Management and Financing

Copyright 2008 by the Foundation of the American College of Healthcare Executives 6/13/07 Version 16-1 CHAPTER 16 Current Asset Management and Financing Investment and financing policies Cash and marketable

Copyright 2008 by the Foundation of the American College of Healthcare Executives 6/13/07 Version 16-1 CHAPTER 16 Current Asset Management and Financing Investment and financing policies Cash and marketable

CHAPTER 26. Working Capital Management. Chapter Synopsis

CHAPTER 26 Working Capital Management Chapter Synopsis 26.1 Overview of Working Capital Any reduction in working capital requirements generates a positive free cash flow that the firm can distribute immediately

CHAPTER 26 Working Capital Management Chapter Synopsis 26.1 Overview of Working Capital Any reduction in working capital requirements generates a positive free cash flow that the firm can distribute immediately

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

The Siburg Company, LLC. Accounts Receivable. Unsecured Loans by a Company. By Daniel R. Siburg, CPA, CVA And Howard W. Fisher

The Siburg Company, LLC Accounts Receivable Unsecured Loans by a Company By Daniel R. Siburg, CPA, CVA And Howard W. Fisher Mergers and Acquisitions Business Development Finance and Operations Account

The Siburg Company, LLC Accounts Receivable Unsecured Loans by a Company By Daniel R. Siburg, CPA, CVA And Howard W. Fisher Mergers and Acquisitions Business Development Finance and Operations Account

It is concerned with decisions relating to current assets and current liabilities

It is concerned with decisions relating to current assets and current liabilities Best Buy Co, NA s largest consumer electronics retailer, has performed extremely well over the past decade. Its stock sold

It is concerned with decisions relating to current assets and current liabilities Best Buy Co, NA s largest consumer electronics retailer, has performed extremely well over the past decade. Its stock sold

Oracle Financial Analytics Accounts Payable Demo Script

Oracle Financial Analytics Accounts Payable Demo Script Last Updated: October 2006 Oracle Systems, Inc. 1 Overview This demo illustrates how Oracle Accounts Payable (A/P) as part of Financial Analytics,

Oracle Financial Analytics Accounts Payable Demo Script Last Updated: October 2006 Oracle Systems, Inc. 1 Overview This demo illustrates how Oracle Accounts Payable (A/P) as part of Financial Analytics,

CAVENDI MANAGEMENT INSIGHT INTRODUCTION TO WORKING CAPITAL

CAVENDI MANAGEMENT INSIGHT INTRODUCTION TO WORKING CAPITAL This paper is an introduction to working capital management and aims at providing the reader with a detailed guide to effective management of

CAVENDI MANAGEMENT INSIGHT INTRODUCTION TO WORKING CAPITAL This paper is an introduction to working capital management and aims at providing the reader with a detailed guide to effective management of

Reference Document Month-End Closing

Overview Each individual company according to their own business practices establishes month end closing procedures. Typically, a company will create a monthly accounting calendar, which sets the dates

Overview Each individual company according to their own business practices establishes month end closing procedures. Typically, a company will create a monthly accounting calendar, which sets the dates

Income Measurement and Profitability Analysis

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

Assessment Questions

Assessment Questions AS-1 ( 1 ) Define accounts receivable. The amount billed to customers and owing from them but not yet collected. AS-2 ( 1 ) Describe the presentation of accounts receivable on the

Assessment Questions AS-1 ( 1 ) Define accounts receivable. The amount billed to customers and owing from them but not yet collected. AS-2 ( 1 ) Describe the presentation of accounts receivable on the

Topic 4 Working Capital Management. 1. Concept of Working Capital 2. Measuring Working Capital and Net Working Capital. 4.

Topic 4 Working Capital Management 1. Concept of Working Capital 2. Measuring Working Capital and Net Working Capital 3. Optimization i i of Working Capital 4. Applications 80 Learning objectives This

Topic 4 Working Capital Management 1. Concept of Working Capital 2. Measuring Working Capital and Net Working Capital 3. Optimization i i of Working Capital 4. Applications 80 Learning objectives This

The Impact of Payment Automation on Bottom-line Savings

The Impact of Payment Automation on Bottom-line Savings In the current recessionary environment, finance professionals have intensified their focus on working capital as well as improving the bottomline

The Impact of Payment Automation on Bottom-line Savings In the current recessionary environment, finance professionals have intensified their focus on working capital as well as improving the bottomline

Treasure Trove The Rising Role of Treasury in Accounts Payable

Treasury and Trade Solutions North America July 30, 2015 Treasure Trove The Rising Role of Treasury in Accounts Payable 2015 Citibank, N.A. All rights reserved Today s Speakers Andrew Bartolini Chief Research

Treasury and Trade Solutions North America July 30, 2015 Treasure Trove The Rising Role of Treasury in Accounts Payable 2015 Citibank, N.A. All rights reserved Today s Speakers Andrew Bartolini Chief Research

PHARMACY BUSINESS NAVIGATOR PROGRAM

PHARMACY BUSINESS NAVIGATOR PROGRAM THE PHARMACY BUSINESS NAVIGATOR PROGRAM As a Pharmacy owner or operator do you truly understand the strategic financial and non-financial indicators for the health of

PHARMACY BUSINESS NAVIGATOR PROGRAM THE PHARMACY BUSINESS NAVIGATOR PROGRAM As a Pharmacy owner or operator do you truly understand the strategic financial and non-financial indicators for the health of

Cash in bank checking account $22,500 U.S. treasury bills 5,000 Cash on hand 1,350 Undeposited customer checks 1,840 Total $30,690 Requirement 2

Chapter 7 Solutions EXERCISES Exercise 7 2 Cash and cash equivalents includes: Cash in bank checking account $22,500 U.S. treasury bills 5,000 Cash on hand 1,350 Undeposited customer checks 1,840 Total

Chapter 7 Solutions EXERCISES Exercise 7 2 Cash and cash equivalents includes: Cash in bank checking account $22,500 U.S. treasury bills 5,000 Cash on hand 1,350 Undeposited customer checks 1,840 Total

How To Be Successful In A Business

A CFO s Perspective on How Supply Chain and Finance can Collaborate to Deliver Value by Joselito Diga CFO, Unilab SUPPLYLINK 2012 CONFERENCE Philippines Institute of Supply Management 19-20 April 2012

A CFO s Perspective on How Supply Chain and Finance can Collaborate to Deliver Value by Joselito Diga CFO, Unilab SUPPLYLINK 2012 CONFERENCE Philippines Institute of Supply Management 19-20 April 2012

Adjustment for Loss from Uncollectible Accounts (accrued expense)

") Adjustment for Loss from Uncollectible Accounts (accrued expense) Objective Explain and illustrate the allowance method of accounting for uncollectible accounts receivable. Cite the advantages and disadvantages

Adjustment for Loss from Uncollectible Accounts (accrued expense) Objective Explain and illustrate the allowance method of accounting for uncollectible accounts receivable. Cite the advantages and disadvantages

WJEC Applied Business A level. ABUS 1 and ABUS 5

1 WJEC Applied Business A level ABUS 1 and ABUS 5 Additional information: formulae, layout and terminology ABUS 1 and ABUS 5 Accounting terminology A number of the terms used in Accounting are changing,

1 WJEC Applied Business A level ABUS 1 and ABUS 5 Additional information: formulae, layout and terminology ABUS 1 and ABUS 5 Accounting terminology A number of the terms used in Accounting are changing,

Teacher Resource Bank

Teacher Resource Bank GCE Accounting Other Guidance: Layouts and Formulae ACCN1: Layouts ACCN2: Layouts and Formulae ACCN4: Layouts and Formulae (Updated July 2012) The Assessment and Qualifications Alliance

Teacher Resource Bank GCE Accounting Other Guidance: Layouts and Formulae ACCN1: Layouts ACCN2: Layouts and Formulae ACCN4: Layouts and Formulae (Updated July 2012) The Assessment and Qualifications Alliance

Statement of Cash Flows

THE CONTENT AND VALUE OF THE STATEMENT OF CASH FLOWS The cash flow statement reconciles beginning and ending cash by presenting the cash receipts and cash disbursements of an enterprise for an accounting

THE CONTENT AND VALUE OF THE STATEMENT OF CASH FLOWS The cash flow statement reconciles beginning and ending cash by presenting the cash receipts and cash disbursements of an enterprise for an accounting

Make Your Working Capital Work

Make Your Working Capital Work Unlocking the value through improving processes Working capital is the amount of daily operating liquidity available with a firm i.e. for day to day operations of the firm.

Make Your Working Capital Work Unlocking the value through improving processes Working capital is the amount of daily operating liquidity available with a firm i.e. for day to day operations of the firm.

Projecting the 3 Statements & 3-Statement Modeling Quiz Questions

Projecting the 3 Statements & 3-Statement Modeling Quiz Questions 1. Let s say that we re creating 3-statement projections for a company, and in its historical filings Depreciation & Amortization and Stock-Based

Projecting the 3 Statements & 3-Statement Modeling Quiz Questions 1. Let s say that we re creating 3-statement projections for a company, and in its historical filings Depreciation & Amortization and Stock-Based

Financial Statements and Ratios: Notes

Financial Statements and Ratios: Notes 1. Uses of the income statement for evaluation Investors use the income statement to help judge their return on investment and creditors (lenders) use it to help

Financial Statements and Ratios: Notes 1. Uses of the income statement for evaluation Investors use the income statement to help judge their return on investment and creditors (lenders) use it to help

The Request for Proposal Process

The Request for Proposal Process Mark K. Webster, CPA, CCM, Partner Daniel L. Blumen, CTP, Partner Treasury Alliance Group LLC Agenda Background Bank Relationship Management Changing banks The RFP Process

The Request for Proposal Process Mark K. Webster, CPA, CCM, Partner Daniel L. Blumen, CTP, Partner Treasury Alliance Group LLC Agenda Background Bank Relationship Management Changing banks The RFP Process

Cash Flow Forecasting & Break-Even Analysis

Cash Flow Forecasting & Break-Even Analysis 1. Cash Flow Cash Flow Projections What is cash flow? Cash flow is an estimate of the timing of when the cash associated with sales will be received and when

Cash Flow Forecasting & Break-Even Analysis 1. Cash Flow Cash Flow Projections What is cash flow? Cash flow is an estimate of the timing of when the cash associated with sales will be received and when

CASH MANAGEMENT 200: Cash Positioning. 2012 CPIM Academy

CASH MANAGEMENT 200: Cash Positioning 2012 CPIM Academy Josh Mandel, State Treasurer of Ohio CASH MANAGEMENT 200 Cash Positioning 2012 CPIM Academy Learning Objectives Understanding Cash Decisions Use

CASH MANAGEMENT 200: Cash Positioning 2012 CPIM Academy Josh Mandel, State Treasurer of Ohio CASH MANAGEMENT 200 Cash Positioning 2012 CPIM Academy Learning Objectives Understanding Cash Decisions Use

The Treasury 3.0 Framework: Deploying a Model of Best Practices. 2013 Treasury Strategies, Inc. All rights reserved.

The Treasury 3.0 Framework: Deploying a Model of Best Practices 2013 Treasury Strategies, Inc. All rights reserved. Agenda Treasury: The Future State Successful Treasury Traits Moving to the Ideal State:

The Treasury 3.0 Framework: Deploying a Model of Best Practices 2013 Treasury Strategies, Inc. All rights reserved. Agenda Treasury: The Future State Successful Treasury Traits Moving to the Ideal State:

Short Term Finance and Planning. Sources and Uses of Cash

Short Term Finance and Planning (Text reference: Chapter 27) Topics sources and uses of cash operating cycle and cash cycle short term financial policy cash budgeting short term financial planning AFM

Short Term Finance and Planning (Text reference: Chapter 27) Topics sources and uses of cash operating cycle and cash cycle short term financial policy cash budgeting short term financial planning AFM

KPI ENCYCLOPEDIA FINANCE. A Comprehensive Collection of KPI Definitions for. www.opsdog.com info@opsdog.com 201.526.1200

KPI ENCYCLOPEDIA A Comprehensive Collection of KPI Definitions for FINANCE www.opsdog.com info@opsdog.com 201.526.1200 Table of Contents KPI Encyclopedia OpsDog Services Overview...2 Metric Definitions....3

KPI ENCYCLOPEDIA A Comprehensive Collection of KPI Definitions for FINANCE www.opsdog.com info@opsdog.com 201.526.1200 Table of Contents KPI Encyclopedia OpsDog Services Overview...2 Metric Definitions....3

Welcome to the course on accounting for the sales and purchasing processes.

Welcome to the course on accounting for the sales and purchasing processes. 1-1 In this topic, we will cover some general accounting conventions and give examples of the automatic journal entries that

Welcome to the course on accounting for the sales and purchasing processes. 1-1 In this topic, we will cover some general accounting conventions and give examples of the automatic journal entries that

Revisited. Working Capital Lines of Credit,

CR Credit Risk Working Capital Lines of Credit, Revisited Avoid the risks of oversized lines of credit by understanding the factors that may create a need for bank financing. 34 October 2012 The RMA Journal

CR Credit Risk Working Capital Lines of Credit, Revisited Avoid the risks of oversized lines of credit by understanding the factors that may create a need for bank financing. 34 October 2012 The RMA Journal

The Hierarchy of Supply Chain Metrics: Diagnosing Your Supply Chain Health

The Hierarchy of Supply Chain Metrics: Diagnosing Your Supply Chain Health Wednesday, February 18, 2004 Debra Hofman The Bottom Line: Companies can assess their supply chain health using just three key

The Hierarchy of Supply Chain Metrics: Diagnosing Your Supply Chain Health Wednesday, February 18, 2004 Debra Hofman The Bottom Line: Companies can assess their supply chain health using just three key

Secrets of World-Class Accounts Payable Departments

Executive Brief Secrets of World-Class Accounts Payable Departments What the Best-in-Class AP departments do that make them stand out from their peers World-class AP departments know something you don

Executive Brief Secrets of World-Class Accounts Payable Departments What the Best-in-Class AP departments do that make them stand out from their peers World-class AP departments know something you don

How To Grade Your Business

ReportCard TheSmallBusiness Is your business making the grade? This number-crunching study guide has the answer. MasterCard Solutions For Small Business MasterCard Solutions for Small Business encompasses

ReportCard TheSmallBusiness Is your business making the grade? This number-crunching study guide has the answer. MasterCard Solutions For Small Business MasterCard Solutions for Small Business encompasses

BizScore Contractor Example

BizScore Contractor Example For the period ending 12/31/2009 Provided By www.bizscorevaluation.com 919-846-4747 bizscore@gmail.com Page 1 / 11 This report is designed to assist you in your business' development.

BizScore Contractor Example For the period ending 12/31/2009 Provided By www.bizscorevaluation.com 919-846-4747 bizscore@gmail.com Page 1 / 11 This report is designed to assist you in your business' development.

PERFECTION IN DETAIL. WORKING CAPITAL MANAGEMENT

9 PERFECTION IN DETAIL. WORKING CAPITAL MANAGEMENT 2 3 COGON WORKING CAPITAL MANAGEMENT GET MORE OUT OF YOUR IN-HOUSE RESOURCES AND SUSTAINABLY STRENGTHEN YOUR PROCESSES! The key to successfully managing

9 PERFECTION IN DETAIL. WORKING CAPITAL MANAGEMENT 2 3 COGON WORKING CAPITAL MANAGEMENT GET MORE OUT OF YOUR IN-HOUSE RESOURCES AND SUSTAINABLY STRENGTHEN YOUR PROCESSES! The key to successfully managing

Strategies for optimizing your accounts receivable

Part of the Deloitte working capital series Make your working capital work for you Strategies for optimizing your accounts receivable The Deloitte working capital series Strategies for optimizing your

Part of the Deloitte working capital series Make your working capital work for you Strategies for optimizing your accounts receivable The Deloitte working capital series Strategies for optimizing your

Citigroup Global Transaction Services

Citigroup Global Transaction Services Cash Management Trade Services and Finance Securities and Fund Services Uncovering the Hidden Value in Accounts Receivables Olivia Xu Director, NA Trade Sales Kate

Citigroup Global Transaction Services Cash Management Trade Services and Finance Securities and Fund Services Uncovering the Hidden Value in Accounts Receivables Olivia Xu Director, NA Trade Sales Kate

Outdoor Retailer Conference Financial Statement Fraud. August 2, 2010 Derk G. Rasmussen. www.sagefa.com

Outdoor Retailer Conference Financial Statement Fraud August 2, 2010 Derk G. Rasmussen www.sagefa.com About Sage Forensic Accounting Sage Forensic Accounting quantifies damage claims in litigation, determines

Outdoor Retailer Conference Financial Statement Fraud August 2, 2010 Derk G. Rasmussen www.sagefa.com About Sage Forensic Accounting Sage Forensic Accounting quantifies damage claims in litigation, determines

Financial Ratios and Quality Indicators

Financial Ratios and Quality Indicators From U.S. Small Business Administration Online Women's Business Center If you monitor the ratios on a regular basis you'll gain insight into how effectively you

Financial Ratios and Quality Indicators From U.S. Small Business Administration Online Women's Business Center If you monitor the ratios on a regular basis you'll gain insight into how effectively you

Lecture 13 Working Capital Management and Credit Issues

Lecture 13 - Working Capital Management Gross working capital: Net working capital: BASIC DEFINITIONS Total current assets. Net operating working capital (NOWC): Operating CA Operating CL = Current assets

Lecture 13 - Working Capital Management Gross working capital: Net working capital: BASIC DEFINITIONS Total current assets. Net operating working capital (NOWC): Operating CA Operating CL = Current assets

Using T Accounts to post journal entries

Using T Accounts to post journal entries Debits Credits This is a T account which is used to analyze posting of double entry accounting Both the right hand column T and the left must have equal totals.

Using T Accounts to post journal entries Debits Credits This is a T account which is used to analyze posting of double entry accounting Both the right hand column T and the left must have equal totals.

Account Numbering. By separating each account by several numbers, many new accounts can be added between any two while maintaining the logical order.

Chart of Accounts The chart of accounts is a listing of all the accounts in the general ledger, each account accompanied by a reference number. To set up a chart of accounts, one first needs to define

Chart of Accounts The chart of accounts is a listing of all the accounts in the general ledger, each account accompanied by a reference number. To set up a chart of accounts, one first needs to define

How To Finance A Business

SUPPLY CHAIN FINANCE Promoting Sales Growth through Innovative Financing Zurich 19 October 2015 Agenda Presentation 30 min Panel Discussion 30 min Q&A with the Audience 30 min - 2 - Introduction of Panelists

SUPPLY CHAIN FINANCE Promoting Sales Growth through Innovative Financing Zurich 19 October 2015 Agenda Presentation 30 min Panel Discussion 30 min Q&A with the Audience 30 min - 2 - Introduction of Panelists

Taking Care of Business

Taking Care of Business A Publisher s Cash Management Plan Part 2 Managing Your Accounts Receivable 2009 by Daniel R. Siburg, CPA, CVA & Howard W. Fisher Accounts receivable is a topic that every publishing

Taking Care of Business A Publisher s Cash Management Plan Part 2 Managing Your Accounts Receivable 2009 by Daniel R. Siburg, CPA, CVA & Howard W. Fisher Accounts receivable is a topic that every publishing

Xynergy Commercial Capital LLC

Xynergy Commercial Capital LLC How Can Work For You The Problem Short of cash and must pay suppliers, lease, bills and salaries? No need for stress, get your payments in advance for your invoices and pay

Xynergy Commercial Capital LLC How Can Work For You The Problem Short of cash and must pay suppliers, lease, bills and salaries? No need for stress, get your payments in advance for your invoices and pay

Working Capital Improvement through Supplier Finance

Working Capital Improvement through Supplier Finance It s Not Just for Large Corporates Sean Corrigan Senior Vice President Head of Strategic Trade Solutions Wells Fargo International Trade Services 2015

Working Capital Improvement through Supplier Finance It s Not Just for Large Corporates Sean Corrigan Senior Vice President Head of Strategic Trade Solutions Wells Fargo International Trade Services 2015

Financial Formulas. 5/2000 Chapter 3 Financial Formulas i

Financial Formulas 3 Financial Formulas i In this chapter 1 Formulas Used in Financial Calculations 1 Statements of Changes in Financial Position (Total $) 1 Cash Flow ($ millions) 1 Statements of Changes

Financial Formulas 3 Financial Formulas i In this chapter 1 Formulas Used in Financial Calculations 1 Statements of Changes in Financial Position (Total $) 1 Cash Flow ($ millions) 1 Statements of Changes

Chapter 8. Reporting and Analyzing Receivables

Chapter 8 Reporting and Analyzing Receivables Study Objective 1 - Identify the Different Types of Receivables The term receivables refers to amounts due from individuals and companies. Receivables are

Chapter 8 Reporting and Analyzing Receivables Study Objective 1 - Identify the Different Types of Receivables The term receivables refers to amounts due from individuals and companies. Receivables are

The Receivables Race to Maximize Control and Automation Nina Hanselmann Cheryl Lehotyak. MN AFP April 28, 2015

The Receivables Race to Maximize Control and Automation Nina Hanselmann Cheryl Lehotyak MN AFP April 28, 2015 Every race consists of key milestones 6. Finish 1. Prepare 5. Pit Stops 2. Know the Course

The Receivables Race to Maximize Control and Automation Nina Hanselmann Cheryl Lehotyak MN AFP April 28, 2015 Every race consists of key milestones 6. Finish 1. Prepare 5. Pit Stops 2. Know the Course

Managing Cash Flow on Construction Projects. Alison Sellers October 25, 2012

Managing Cash Flow on Construction Projects Alison Sellers October 25, 2012 1 The material appearing in this presentation is for informational purposes only and is not legal or accounting advice. Communication

Managing Cash Flow on Construction Projects Alison Sellers October 25, 2012 1 The material appearing in this presentation is for informational purposes only and is not legal or accounting advice. Communication

Understanding Cash Flow Statements

Understanding Cash Flow Statements 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Components and Format of the Cash Flow Statement... 3 3. The

Understanding Cash Flow Statements 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Components and Format of the Cash Flow Statement... 3 3. The

Financial Statement Consolidation

Financial Statement Consolidation We will consolidate the previously completed worksheets in this financial plan. In order to complete this section of the plan, you must have already completed all of the

Financial Statement Consolidation We will consolidate the previously completed worksheets in this financial plan. In order to complete this section of the plan, you must have already completed all of the

Consumer Bill Payments Shifts & Strategies

Consumer Bill Payments Shifts & Strategies Jim Gilligan, CTP, FP&A Assistant Treasurer, Great Plains Energy Incorporated Kansas City Power & Light Company Kellie Thomas VP, Product Management, Wells Fargo

Consumer Bill Payments Shifts & Strategies Jim Gilligan, CTP, FP&A Assistant Treasurer, Great Plains Energy Incorporated Kansas City Power & Light Company Kellie Thomas VP, Product Management, Wells Fargo

Inventory Standard Costing. Reference Guide Includes New Features in SedonaOffice 5.1

Inventory Standard Costing Includes New Features in SedonaOffice 5.1 Last Revised: June 18, 2008 About this Guide This Guide is for use by SedonaOffice customers only. This guide is not meant to serve

Inventory Standard Costing Includes New Features in SedonaOffice 5.1 Last Revised: June 18, 2008 About this Guide This Guide is for use by SedonaOffice customers only. This guide is not meant to serve

Cash Flow Management Solutions for Small Business

ThisIsCable for Business Report Series Cash Flow Management Solutions for Small Business White Paper Produced by BizTechReports.com Editorial Director: Lane F. Cooper Research Assistant: Will Frey ThisIsCable

ThisIsCable for Business Report Series Cash Flow Management Solutions for Small Business White Paper Produced by BizTechReports.com Editorial Director: Lane F. Cooper Research Assistant: Will Frey ThisIsCable

Siemens Supply Chain Finance Program

Siemens Supply Chain Finance Program January, 2012 Copyright Siemens AG 2007. All rights reserved. Copyright Siemens AG 2006. All rights reserved. Introduction to the Siemens SCF Program The Siemens SCF

Siemens Supply Chain Finance Program January, 2012 Copyright Siemens AG 2007. All rights reserved. Copyright Siemens AG 2006. All rights reserved. Introduction to the Siemens SCF Program The Siemens SCF

How To Maximize Cash Flow

Working Capital Metrics: What Gets Measured Gets Managed Janine Durbin Director; Working Capital Advisor Phone: 312.992.5185 E-Mail: janine.m.durbin@baml.com Understanding Working Capital Working Capital

Working Capital Metrics: What Gets Measured Gets Managed Janine Durbin Director; Working Capital Advisor Phone: 312.992.5185 E-Mail: janine.m.durbin@baml.com Understanding Working Capital Working Capital

FI3300 Corporation Finance

Learning Objectives FI3300 Corporation Finance Spring Semester 2010 Dr. Isabel Tkatch Assistant Professor of Finance Explain the objectives of financial statement analysis and its benefits for creditors,

Learning Objectives FI3300 Corporation Finance Spring Semester 2010 Dr. Isabel Tkatch Assistant Professor of Finance Explain the objectives of financial statement analysis and its benefits for creditors,

Best E-Commerce Practices

Best E-Commerce Practices Electronic Commerce Defined Segment of a larger business model that allows companies to transact over the internet Can be seen as a mode to collect tax payments, licenses, permit

Best E-Commerce Practices Electronic Commerce Defined Segment of a larger business model that allows companies to transact over the internet Can be seen as a mode to collect tax payments, licenses, permit

Good Business 10/5/2011 @ 5:26 PM

Good Business 10/5/2011 @ 5:26 PM Disclaimer: This report contains sensitive company information. As such, the company / individual for whom this report was prepared is responsible for the management of

Good Business 10/5/2011 @ 5:26 PM Disclaimer: This report contains sensitive company information. As such, the company / individual for whom this report was prepared is responsible for the management of

Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements

Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements TABLE OF CONTENTS 1.0

Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements TABLE OF CONTENTS 1.0

It all Starts with the Invoice

It all Starts with the Invoice Speakers Mel Steals Director of Invoice Automation Solutions PNC Bank Amy Rush Shared Services Controller Courtney Caton Finance Manager Westmoreland Coal Company 1 Agenda

It all Starts with the Invoice Speakers Mel Steals Director of Invoice Automation Solutions PNC Bank Amy Rush Shared Services Controller Courtney Caton Finance Manager Westmoreland Coal Company 1 Agenda

Budgeting For the Emerging Company How to Develop Operational Plans that Improve Financial Performance

Budgeting For the Emerging Company How to Develop Operational Plans that Improve Financial Performance EXECUTIVE SUMMARY Budgeting is a difficult task for operators of emerging businesses. Many don't do

Budgeting For the Emerging Company How to Develop Operational Plans that Improve Financial Performance EXECUTIVE SUMMARY Budgeting is a difficult task for operators of emerging businesses. Many don't do

Study Unit 6. Managing Current Assets

Study Unit 6 Managing Current Assets SU- 6.1 Working Capital What is working capital and types of capital policies What all is included in working capital? Net working capital = What is used to acquire

Study Unit 6 Managing Current Assets SU- 6.1 Working Capital What is working capital and types of capital policies What all is included in working capital? Net working capital = What is used to acquire

B2B Payments New World

The Essentials of Procure-to-Pay Pay Patrick S. Lyons Vice President, Spend & Payment Solutions BMO Financial Group B2B Payments New World Trend: Payment Strategies now include all three Payments (ACH,

The Essentials of Procure-to-Pay Pay Patrick S. Lyons Vice President, Spend & Payment Solutions BMO Financial Group B2B Payments New World Trend: Payment Strategies now include all three Payments (ACH,

E-Commerce, Merchant Processing, EMV and General Best Practices for Municipalities

E-Commerce, Merchant Processing, EMV and General Best Practices for Municipalities T.C. Kennedy. CTP Senior Vice President Treasury & Payment Solutions SunTrust Bank Electronic Commerce Defined Segment

E-Commerce, Merchant Processing, EMV and General Best Practices for Municipalities T.C. Kennedy. CTP Senior Vice President Treasury & Payment Solutions SunTrust Bank Electronic Commerce Defined Segment

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions Chapter 6 Working Capital Management Concept Check 6.1 1. What is the meaning of the terms working

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions Chapter 6 Working Capital Management Concept Check 6.1 1. What is the meaning of the terms working

CHAPTER 21. Working Capital Management

CHAPTER 21 Working Capital Management 1 Topics in Chapter Alternative working capital policies Cash, inventory, and A/R management Accounts payable management Short-term financing policies Bank debt and

CHAPTER 21 Working Capital Management 1 Topics in Chapter Alternative working capital policies Cash, inventory, and A/R management Accounts payable management Short-term financing policies Bank debt and

Reconciling Tax Receivables Course #364

Reconciling Tax Receivables Course #364 MCTA Annual School August, 2011 Presented by John J. Sullivan & Patrice Squillante, CPA Melanson Heath & Company, P.C. (slides courtesy of Jean Berg, Collector/Treasurer,

Reconciling Tax Receivables Course #364 MCTA Annual School August, 2011 Presented by John J. Sullivan & Patrice Squillante, CPA Melanson Heath & Company, P.C. (slides courtesy of Jean Berg, Collector/Treasurer,

Options Are Good. A Treasury Perspective on Driving Value from Payments. Jody L. Lutz Senior Vice President PNC Treasury Consulting Group

Options Are Good A Treasury Perspective on Driving Value from Payments Presented to: April 20, 2015 Jody L. Lutz Senior Vice President PNC Treasury Consulting Group (412) 768-2364 Jody.Lutz@pnc.com Traditional

Options Are Good A Treasury Perspective on Driving Value from Payments Presented to: April 20, 2015 Jody L. Lutz Senior Vice President PNC Treasury Consulting Group (412) 768-2364 Jody.Lutz@pnc.com Traditional

Glossary of Accounting Terms Peter Baskerville

Glossary of Accounting Terms Peter Baskerville Account for or 'bring to account': An accounting phrase used to describe the recording of a financial transaction that is required under the generally accepted

Glossary of Accounting Terms Peter Baskerville Account for or 'bring to account': An accounting phrase used to describe the recording of a financial transaction that is required under the generally accepted

TM Forum Your trusted online source for Treasury Management news

In this issue: Fall 2014 Integrated Receivables nextgeneration platform addresses processing challenges Bank partnership key to building a robust e-payables program Integrated Receivables nextgeneration

In this issue: Fall 2014 Integrated Receivables nextgeneration platform addresses processing challenges Bank partnership key to building a robust e-payables program Integrated Receivables nextgeneration

Accounts Payable Automation Benefits

w h i t e pa p e r Accounts Payable Automation Benefits Facts and best practices by leading analysts Purchase to Pay by Medius, Powered by ReadSoft Author: ReadSoft, August 2011 Edited: Medius, June 2012

w h i t e pa p e r Accounts Payable Automation Benefits Facts and best practices by leading analysts Purchase to Pay by Medius, Powered by ReadSoft Author: ReadSoft, August 2011 Edited: Medius, June 2012

Financial Closing Process Best Practices: Improve and Accelerate

Financial Closing Process Best Practices: Improve and Accelerate Chris Doxey, CAPP, CCSA, CICA, CPC Management Consultant and Executive Director of IOFM s Controller Certification Program chris@chrisdoxey.com

Financial Closing Process Best Practices: Improve and Accelerate Chris Doxey, CAPP, CCSA, CICA, CPC Management Consultant and Executive Director of IOFM s Controller Certification Program chris@chrisdoxey.com

When Treasury Meets Trade Trade finance as a key working capital optimization tool.

FEBRUARY 2012 When Treasury Meets Trade Trade finance as a key working capital optimization tool. Chris Bozek, Managing Director, Head of Global Trade and Supply Chain Products, Bank of America Merrill

FEBRUARY 2012 When Treasury Meets Trade Trade finance as a key working capital optimization tool. Chris Bozek, Managing Director, Head of Global Trade and Supply Chain Products, Bank of America Merrill

SMALL BUSINESS QUARTERLY PULSE CHECK

SMALL BUSINESS QUARTERLY PULSE CHECK To make your business #CPAPOWERED, call today and let s get started. 16733-312_CPAPowered_Quarterly Pulse_Check Checklist_final.indd 1 Sound planning is one of the

SMALL BUSINESS QUARTERLY PULSE CHECK To make your business #CPAPOWERED, call today and let s get started. 16733-312_CPAPowered_Quarterly Pulse_Check Checklist_final.indd 1 Sound planning is one of the

Cash is King. cash flow is less likely to be affected

Reading 27: Understanding Cash Flow Statements Relevance of Cash Flow The primary purpose of the statement of cash flows (SCF) is to provide: Info about a firm s cash receipts & cash payments during an

Reading 27: Understanding Cash Flow Statements Relevance of Cash Flow The primary purpose of the statement of cash flows (SCF) is to provide: Info about a firm s cash receipts & cash payments during an