REPORT LIFE INSURANCE MARKET DEVELOPMENT IN BALTIC COUNTRIES. By Janis Bokans TABLE OF CONTENTS

|

|

|

- Dwain Walton

- 8 years ago

- Views:

Transcription

1 REPORT LIFE INSURANCE MARKET DEVELOPMENT IN BALTIC COUNTRIES By Janis Bokans TABLE OF CONTENTS Introduction 2 Life insurance market in the Baltic countries overview. 4 Portfolio... 5 Insurance products... 5 Indemnities.. 6 Reinsurance. 6 Insurance companies... 6 Investments. 7 Taxation. 8 Actuaries 10 Life market development prospects.. 10 Private pension funds 11 GRAPHS 13 Comparison of Baltic life insurance market with markets of Hungary, the Czech Republic and Poland.. 13 Life insurance markets of Baltic states. 15 Investments.. 19 Household income / consumption 22 TABLES 23 Number of life companies 23 List of life insurance companies.. 24 Subsidiaries.. 25 Tables by country 26 References 30 1

2 Introduction In , the three Baltic nations: Estonians, Latvians and Lithuanians implemented their dream and established independent countries. Although the period after World War I faced economic hardships and the Depression, the three countries succeeded in developing their economies and they were fullfledged members of Europe. The same applies to insurance. The joint stock company Drosiba, the State Insurance Company, Russian insurance companies Rossija and Salamandra, and also Lloyds of Latvia operated in Latvia. Under the Mutual Insurance Central Union, several hundreds mutual insurance societies were active throughout Latvia. Estonia passed a special law on insurance in The handbook Life Insurance in Estonian language was published in 1938 where one of the authors was Estonian actuary Mr Karl Saare. Lecturer of Lithuanian University Mr S.Feterauskas worked on evaluation of insurance risks and premium rates, he was one of the founders of insurance company Lietuva and State Insurance Company. Upon the start of World War II, the Soviet Union occupied the Baltic countries. Then the invasion by fascist Germany followed but after the war the Baltic countries were incorporated in the USSR. Only state insurance companies Gosstrah and Ingosstrah sold insurance in the USSR. Each Soviet republic had a Gosstrah branch, and each district in the republic had a Gosstrah division. Both property and personal insurance were available. Clearly, this insurance suited the planned economy and operated within its framework. There were about 1 million valid endowment policies in Latvia in the 80s (the population in Latvia was 2.6 million). After 50 years in Estonia, Latvia and Lithuania restored their independence. The separation of the financial system from that of the USSR was one of the very first and most difficult tasks. Estonia, Latvia and Lithuania set up state insurance companies that took over the liabilities of Gosstrah in their territories. Unfortunately, efforts to recover large part of financial resources (related to the liabilities) from Moscow failed. Early 90s were hard years for the Baltic countries. One of the most important steps was the re-introduction of national currencies. In 1992, Estonia re-introduced its Estonian kroon, and in 1993 Latvia re-introduced the Latvian lats and Lithuania - its Lithuanian litas. This is how the hyperinflation was cut it reached nearly 1,000% in The market economy principles were restored, however, legislation required to ensure their implementation was in the process of creation. At the same time, private initiatives developed rapidly. Commercial banks, insurance companies and other financial institutions were set up. First private insurance companies appeared in the Baltic countries in 1991 and in 1992 there were 15 of them in Latvia, 20 in Estonia. Private insurance businesses developed quickly, unfortunately, very often they lacked necessary 2

3 special knowledge and there were also cases of sheer gambling. From 1990 to 1992, Estonia issued licences to 39 insurance companies, 16 of which never started insurance business. To regulate insurance activities, relevant laws were passed in Lithuania in 1990, in Estonia in 1992 and in Latvia in Originally, insurance business was supervised by Ministries of Finance. A permanent insurance supervision authority was set up in Estonia in 1993, in Latvia and Lithuania in Privatisation of the state companies that had taken over the liabilities from Gosstrah was one of the most important problems. In this process was completed successfully in all the Baltic countries. In mid-90s, the Baltic countries were granted considerable assistance within the framework of the EU-Phare project to improve insurance legislation and supervision. New insurance laws were passed in Lithuania in 1996 and in Latvia in Life insurance was separated from non-life insurance in Estonia in 1992, in Latvia - in 1994 and in Lithuania in The solvency control as applied in the EU was introduced. Now insurance accounting complies with EU requirements in Estonia and Latvia. The insurance markets in the Baltic states has been established within a very short period of time only 10 years. Market activities are regulated by legislation that complies with EU requirements and professional supervision authorities have been set up. The fact that nearly 1/3 of life insurance companies in the Baltic countries are owned by foreign insurers demonstrates the stability and potential of the market. 3

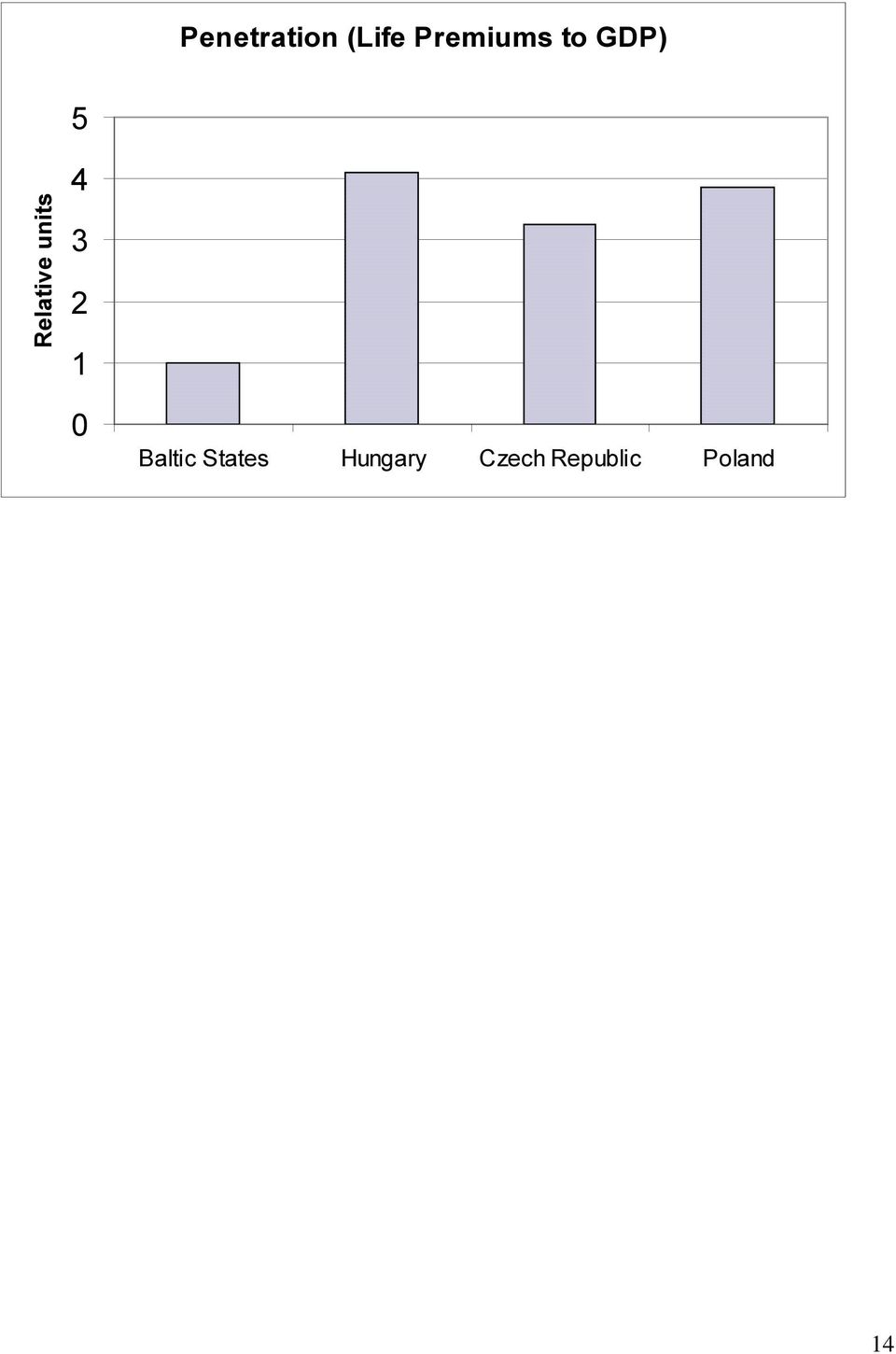

4 Life Insurance market in the Baltic Countries - Overview Although Estonia, Latvia and Lithuania are independent countries, it is useful to view them together and compare the common Baltic market with that of other countries. This approach has a certain historical and economic basis. Firstly, business and business interests spread across borders. Secondly, Baltic countries have many things in common in terms of history and also consumer mentality. The Baltic life insurance market will be compared with markets of Hungary, the Czech Republic and Poland. The total population of the Baltic countries is 7.6 million, while in Hungary there are 10.1 million people and in the Czech Republic 10.3 million, so it is possible to compare them in terms of the number of inhabitants. Comparison is based on data given for 1998/1999. The total gross written premiums of life insurance companies in the Baltic countries were 51 million US$ in This is approximately 9 times less than the amount of premiums written in Hungary or the Czech Republic and 25 times less, compared to Poland. The density (gross life premiums per capita) is only 5 to 7 times less than the respective figure in markets of Poland, Hungary and the Czech Republic. The penetration (life premiums to GDP, adjusted to the purchasing power standards) is approximately 4 times less than the respective figure in Hungary, the Czech Republic and Poland. Insurance premiums written in Latvia and Lithuania in 1999 were approximately the same 18.5 million US$ in each country, the premium volume in Estonia was 14 million US$. Densities differ considerably in Estonia, the density is 9,6 US$ per capita and it is twice as much than in Lithuania (5 US$ per capita). The density in Latvia is in between the two figures 7,6 US$ per capita. The density in Poland in 1998 was 34 US$ per capita, In Hungary 42 US$, in Czech Republic 45 US$, but in France, for example, the density is slightly over 1,000 US$. The share of life insurance as of the total insurance business in the Baltic countries is very low in comparison with the average OECD figure only 10% in Latvia, 16% - in Estonia and 18% in Lithuania. Moreover, in the period from 1996 to 1999 the life share decreased from 21% to 10% in Latvia, and from 29% to 18% in Lithuania. In Estonia, an opposite trend was observed the life insurance share went up from 8% to 16% in In Latvia, the decrease of the life insurance share was determined to a large extent by the introduction of the obligatory motor third party liability insurance which led to a considerable increase in the non-life business volume. From 1996 to 1999, the total premium volume increased 1.5 times in the Baltic countries. The development was different in each country. The biggest premium increase rate was observed in Estonia it reached 100% in 1997 but it was only 5% in The premium increase in Latvia was affected both by the banking crisis in 1995 and considerable changes in tax legislation in However, in 1998 the premium increase was 36%. The development is most 4

5 stable in Lithuania where the annual premium increase is around 10%. The Russian crisis also had an adverse impact upon the Baltic countries in Portfolio The total number of insurance contracts being in force in life insurance companies was approximate 660 thousand in Baltic Countries at the end of Latvia companies account for the majority of contracts 293 thousand. The largest number of contracts per 1000 inhabitants is found in Latvia 120. In Lithuania this figure is 67 contracts per 1000 inhabitants, in Estonia 86 contracts. These figures should be viewed only as an illustration because the same person can have several insurance contracts. Besides, Lithuanian and Latvian life insurance companies may sell accident and sickness insurance separately from life insurance, while in Estonia only as a rider. It is worth noting that the number of contracts in force decreased almost twice from 1994 to 1998 in Estonia. The number of newly-concluded contracts decreased more than twice from 1997 to 1999 in Lithuania. At the same time, the average sum assured under one contract increased considerably. The old Gosstrah portfolio also had an impact upon the number of contracts in force. Following the hyperinflation in early 90s, these policies lost their value, and policyholders were no more interested in them. In Latvia, the audit of this portfolio was completed by the insurance company Latva (the company that took over the liabilities of Gosstrah) only in The share of surrenders is considerable in Estonia, the ratio of surrenders to contracts in force is 12%, in Lithuania 6%, in Latvia it is around 10%. In Lithuania, the ratio of concluded contracts to cancelled contracts was 1 in 1999, in Estonia 1.6 in Many endowment policies are cancelled in Latvia and Lithuania because people lack financial resources. The reason is similar in Estonia, besides, contracts are cancelled to convert them into pension contracts tax relief s have been applied to them recently. Insurance products Most of premiums apply to the endowment-type insurance. In Estonia, the share is 83%. Annuity contracts account for the remaining 7%, term and whole life contracts - 4%, and accident (supplementary) insurance - 6%. In Latvia, the endowment-type insurance accounts for 61% of premiums, term and whole life contracts - 4%, accident insurance - 31% and sickness insurance - 4%. In Lithuania, 34% of premiums apply to marriage and birth assurance, the remaining 66% apply to other life insurance products and also to accident and sickness insurance. In Estonia it is possible to buy the dread disease cover too. Estonian and Lithuanian insurance companies offer unit-linked insurance polices. In 1997, this insurance product became very popular in Estonia the premium volume reached 1.2 million US$ under unit-linked contracts (13% of all the premiums). 5

6 Later, they became less popular and in 1999 the premium volume was only 56 thousand US$ under unit-linked contracts in Estonia. In Lithuania, the unitlinked business was undertaken in 1999 and the premium volume was 20 thousand US$. Annuity contracts have become very popular in Estonia in 1999 they formed 6% of premiums in Compared to 1997, premiums went up 42 times as much! The increase can be explained by the fact that tax allowances applying to long-term annuity contracts were introduced in Unit linkedpolicies and annuity contracts are not yet sold in Latvia. Long term care contracts are not sold in any of the Baltic countries. Indemnities The ratio of indemnities to insurance premiums tends to decrease in Latvia and Lithuania. In Latvia, the ratio was 60% in 1996 and the figure went down to 30% in In Lithuania, the ratio was 75% in 1996 and 50% - in The ratio is quite stable in Estonia it fluctuated within the limits of 20 30% from 1996 to Surrenders paid in Latvia in 1999 were 37%, in Estonia 58% and in Lithuania 15% of indemnities. Reinsurance Life insurance companies in Lithuania do not really use reinsurance services. The reinsurance share of insurance premiums was only 1% in In Estonia, the reinsurance share was stable 3-4% in the period from 1996 to In Latvia, however, the reinsurance share is quite considerable. In 1996, it accounted for 50% of insurance premiums and for 30% in It is determined by the fact that one insurance company in Latvia pays 91% of insurance premiums to the reinsurer and two other companies pay 60% and 40% respectively. The reinsurance share in the remaining five insurance companies in Latvia is from 0% to 5%. Insurance companies The number of insurance companies stayed nearly the same in the Baltic countries in the period of time from 1996 to In 1996 and 1997 there were 20 insurance companies, in insurance companies. In 1999 there were 19 life insurance companies operating in the Baltic countries. 6 of them are owned by foreign life insurers or insurance groups. The most important investor is Alte Leipziger Europa, Germany, owning insurance companies in all the three Baltic countries. 8 life insurance companies operated in Latvia in Compared to 1996, the number had decreased by 1. One company is a mutual society the only one in Latvia and the Baltic countries. Its members are the Railway Trade Union and railway-related institutions. Estonia had 7 companies in 1996, their number increased up to 9 companies in 1998 but in 1999 fell down to 6. In 1999 licences of two insurance 6

7 companies were withdrawn due to insolvency. The reason for insolvency poor real estate investment policy (newly constructed buildings). One company underwent re-organisation and was taken over by Hansapanga Kindlustus. Lithuania had 5 life insurance companies in On the whole, 9 insurance companies have life insurance portfolios in Lithuania as life and nonlife businesses were separated only in 1997 there. Four companies do not sign any new contracts but they will meet the liabilities until the expiration of contracts signed before 31 July In 1999, life insurance contracts in force in these insurance companies formed 85% of all the insurance contracts in force in Lithuania. The majority of the portfolio 74% - is owned by Lietuvos Draudimas. The market concentration is more explicit in Lithuania and Estonia. In 1999, Lietuvos Draudimas accounted for 57% of premiums in Lithuania, and Hansapanga Kindlustus accounted for 55% of premiums in Estonia. In Latvia, Salamandra Baltik was the leading company with 36% of premiums in 1999, followed by three companies with 17%-12% of premiums. Of the 23 insurance companies that have a life insurance portfolio in the Baltic countries, 8 are controlled directly by foreign insurance companies or insurance groups. In total, these companies have received 33% of all premiums in The respective figure was 13-14% in Latvia and Estonia, while it was much higher in Lithuania - 66%. As said before, Lietuvos Draudimas has the largest life insurance portfolio in Lithuania and its most important shareholder is Codan Insurance Ltd. It should be stressed that links between the banking sector and insurance business are observed. Two life insurance companies are bank subsidiaries in Estonia and Lithuania while in Latvia one of the banks is the subsidiary of a life insurance company. Investments The total investments of life insurance companies were 70 million US$ at the end of % of the investments relate to technical provisions. Life insurance companies in Latvia accounted for investments of 35 million US$. The total investments in Estonia were 24 million US$, and in Lithuania 11 million US$. The Baltic countries have adopted legislation that puts both quality and quantity limitations upon investments. In Latvia and Estonia, quantity limitations apply only to technical provisions, in Lithuania the quantity limitations apply also to the owners equity. Moreover, Lithuania provides that the investment into the state and municipal bonds shall account for not less than 45% of insurance technical provision funds and not less than 20% of authorised capital funds (owners equity). The most important type of investments (about 40% in the Baltic countries) is bonds and other fixed interest securities. It accounts for 77% of 7

8 investments in Lithuania, 25% - in Latvia. Another important investment type is deposits with credit institutions. It accounts for 26% in the Baltic countries. In Latvia it is 32%, and only 5% in Lithuania. In total, shares and other securities account for 8% of investments in the Baltic countries, 11% - in Estonia, 0,1% - in Lithuania. It should be noted that shares and other securities accounted for 28% of investments in Estonia in Obviously, investments in shares and other securities are viewed with slight suspicion as the Baltic stock markets experienced fast growth and equally fast downfall in (the increase was 400% in Estonia, in Latvia it was nearly 1000%). Currently, stock markets in the Baltic countries are rather inactive and small. The official list of the stock markets in Latvia and Estonia quotes only 8 joint stock companies each. Investments in real estate account for the total of 10% in the Baltic countries. In Latvia, insurance companies held considerable amounts in bank accounts or as cash in hand. At the end of 1999 the amount reached approximately 3 million US$. These amounts are small in Estonia and Lithuania. In order to assess the investment volume in each country, one must take into account the different requirements as regards the minimum share capital of life insurance companies. It was 1.7 million US$ in Latvia in 1999, about 0,8 million US$ - in Estonia, about 1 million US$ in Lithuania. In Estonia and Lithuania, the ratio of technical provisions to owners funds is around 2, while in Latvia - around 1. It means that Latvian life insurance companies are rather over-capitalised. Taxation Bearing in mind the social and economic role of life insurance, the establishment of tax incentives is very important part of the overall insurance regulation in a particular country. In Estonia there are no overall tax incentives for life insurance purchasing except for special qualified pension insurance contracts (introduced in 1998). Premiums paid under the pension insurance policy are deductible from the taxable income in respect of the personal income tax, with the ceiling of 15% of the annual income. This is a composite ceiling for pension insurance premiums and purchase of units in a private pension fund. The pension insurance policy must comply with the following requirements: the policyholder and the insured may be only natural persons; the policyholder is obliged to pay premiums until he/she reaches the pension age laid down in the contract; starting from this date, the insurer is obliged to pay the insurance pension as laid down in the contract; 8

9 payments of the insurance pension commence on the due date as laid down in the contract (the pension age) but not before 55 years of age or when the owner of the policy is disabled fully and permanently; insurance pension payments are made on a regular basis, the interval cannot be less than three months, and they continue until the death of the policyholder, unless the contract provides otherwise. The personal income tax at the rate of 10% (instead of the usual rate of 26%) is applied to lump sum benefits paid under the pension insurance policy, but no personal income tax is applied to benefits paid during the person s life (life annuity). There are no tax incentives applied to premiums paid by employers for life insurance policies on behalf of their employees. In Latvia there are no personal income tax incentives for life insurance premiums. There are tax incentives for employers when the employer pays life insurance premiums for the benefit of employees: premiums are not considered as part of the salary and, consequently, the social insurance tax is not applied; this incentive is subject to the ceiling of 10% of the salary; premiums are viewed as business costs and, consequently, the corporate income tax does not apply; this incentive is subject to the ceiling of 10% of the salary. Tax incentives apply only to life insurance contracts lasting more than 5 years. This is a composite incentive for life, sickness and accident insurance premiums and contributions to the private pension funds paid by the employer. Under the Law on Insurance Companies and their Supervision no personal income tax is applied to insurance benefits (except for surrenders paid to employees under contracts where the policy holder is the employer). In Lithuania, the personal income tax does not apply to premiums paid by individuals for life insurance contracts that exceed 10 years. This incentive is subject to the ceiling of the four-fold amount of the minimum monthly salary (set by the Government) per annum. This is a composite incentive for life, accident and sickness insurance premiums. The corporate income tax is not applied to life insurance premiums paid by the employer for the benefit of employees (they are considered to be business costs), provided that the contract period exceeds 10 years. This incentive is subject to the ceiling of the four-fold amount of the minimum monthly salary (set by the Government) per annum for each employee. This is a composite incentive for life, accident and sickness insurance premiums. Received insurance benefits are not subject to tax (Article 58 of the Law on Insurance, Lithuania). 9

is applied to lump sum benefits paid under the pension insurance policy, but no personal income tax is applied to")

10 Actuaries Insurance legislation in the Baltic countries provides that life insurance companies must have an appointed actuary. In Lithuania and Estonia, the appointed actuary signs the annual report. In Latvia the appointed actuary produces a separate report describing the methods applied in the calculation of mathematical reserves and matching assets to liabilities. Associations of Actuaries operate in all the Baltic countries (in Lithuania within the framework of the Association of Insurers). In Latvia, only full-fledged members of the Association of Actuaries can work as appointed actuaries. In Estonia, the professional competence of actuaries is assessed by the Insurance Supervisory Authority. In Lithuania, the University of Vilnius provides training for actuaries (basic higher education), in Estonia actuaries are trained at the University of Tartu. Life Market Development Prospects The need for life insurance comes to the front only after certain basic needs have been satisfied. Unfortunately, the level of income is still very low in the Baltic countries. The income per household member per month in Estonia is 137 US$, in Latvia US$, in Lithuania US$. Social transfers are an essential part of income approximately 25% - 30%. Typically, income per household member is higher in the households where there is at least one retired person. Consequently, the state pension is an important source of income for households. Food, housing and clothing account for 60% - 70% of the expenses. Households do not really have disposable income to purchase insurance or make savings. According to UNDP, Baltic countries have only 3% - 5% households that have enough income to make savings. Thus there could be about thousand potential customers in the Baltic countries who could purchase life insurance. If to compare this figure with the number of insurance contracts in force in the Baltic countries, one might conclude that the potential customers have been covered by now. The growth of the market potential depends on the development of economic activities leading to the increase of household income. Unfortunately, the crisis in Russia had an adverse impact on the economies of the Baltic countries many local producers lost the customers in the Russian market. However, there are also positive signs. Projections are that the GDP will grow considerably in the Baltic countries in Inflation is still low. In 1999, the average salary increase in Latvia exceeded the CPI for the first time since It is quite difficult to make any forecasts about the development of economy in the Baltic countries. The scale is quite small and, consequently, external influences may be critical. However, if to follow a prudent optimistic 10

11 development scenario where the GDP increase is 7% annually and life insurance premiums reach 1% of GDP, then the total life insurance premium volume in the Baltic countries could reach 500 million US$ per annum in 10 years. In this case, the density (gross life premiums/population) would be about 100 US$ per capita. It is important to educate customers if we want to expand the market share. Older generations still rely on the state to receive assistance in critical cases (diseases, accidents, breadwinner s death, etc.). The general public does not yet understand it that individuals should protect themselves by purchasing their own covers from insurance companies. Individuals are not yet aware of the option to plan long term tax and estate using life assurance. The survey carried out in Latvia showed that more than a half of the population does not simply trust insurance companies while one third believes that insurance is too expensive. Clearly, promotion requires considerable investments but Baltic insurance companies do not have resources for this purpose. In Latvia in October 2000, advertisement spaces of insurance companies were only 1% in respect of advertisement spaces of commercial banks in the press. However, positive developments are observed here as well one of the insurance companies broadcast a short informative programme (5 minutes) on the Latvian TV. Radio also broadcasts informative commercials. Opening of the market to foreign companies could make the life insurance market much more active. The law adopted by Estonia in 2000 allows foreign insurers to establish branches in Estonia. Latvia plans to allow the same in Private pension funds Within the framework of the pension reform, the Baltic countries have developed legislation that is necessary for the activities of pension funds. Membership in pension funds is voluntary. At the end of 1999 there were 3 pension funds in Latvia, 1 in Estonia. The law on pension funds was effected in Lithuania on 1 January 200. In Latvia and Estonia, pension funds may accumulate only additional pension capital, they do not pay annuities. Upon reaching the age of 55, members may receive the saved capital as a lump sum or purchase annuities from life insurance companies. The legislation in Lithuania provides for an option that the pension fund also pays annuities but the customer may choose to purchase the annuity contract from a life insurance company using the saved capital. Taking into account the fact that pension funds have launched their activities recently, one can expect to have the first customers having sufficient capital to purchase annuities in 5 10 years. Moreover, Latvia and Estonia introduces the pension system second pillar the mandatory funded pension scheme. In Latvia customers will be able to use 11

12 the capital (saved in a mandatory scheme) to purchase annuities from private life insurance companies. It will help increase the annuity market in approximately 20 year time. 12

13 GRAPHS Comparison of Baltic life insurance market with markets of Hungary, the Czech Republic and Poland *URVV/LIH3UHPLXPV 0LOOLRQ86 %DOWLF6WDWHV +XQJDU\ &]HFK 5HSXEOLF 3RODQG 'HQVLW\*URVV/LIH3UHPLXPV3RSXODWLRQ 86SHU,QKDELWDQW %DOWLF6WDWHV +XQJDU\ &]HFK 5HSXEOLF 3RODQG 13

![%DOWLF6WDWHV +XQJDU\ &]HFK 5HSXEOLF 3RODQG](/docs-images/55/8878526/images/page_13.jpg "'HQVLW\*URVV/LIH3UHPLXPV3RSXODWLRQ 86SHU,QKDELWDQW 13")

14 3HQHWUDWLRQ/LIH3UHPLXPVWR*'3 5HODWLYHXQLWV %DOWLF6WDWHV +XQJDU\ &]HFK5HSXEOLF 3RODQG 14

15 Life insurance markets of Baltic states 6KDUHRI5HVSHFWLYH&RXQWU\LQ%DOWLF0DUNHW /LWKXDQLD (VWRQLD /DWYLD 'HQVLW\*URVV/LIH3UHPLXPV3RSXODWLRQ 86SHULQKDELWDQW (VWRQLD /DWYLD /LWKXDQLD 15

16 3HQHWUDWLRQ/LIH3UHPLXPV*'3 (VWRQLD /DWYLD /LWKXDQLD 3UHPLXP'HYHORSPHQW 0LOOLRQ86 (VWRQLD /DWYLD /LWKXDQLD 16

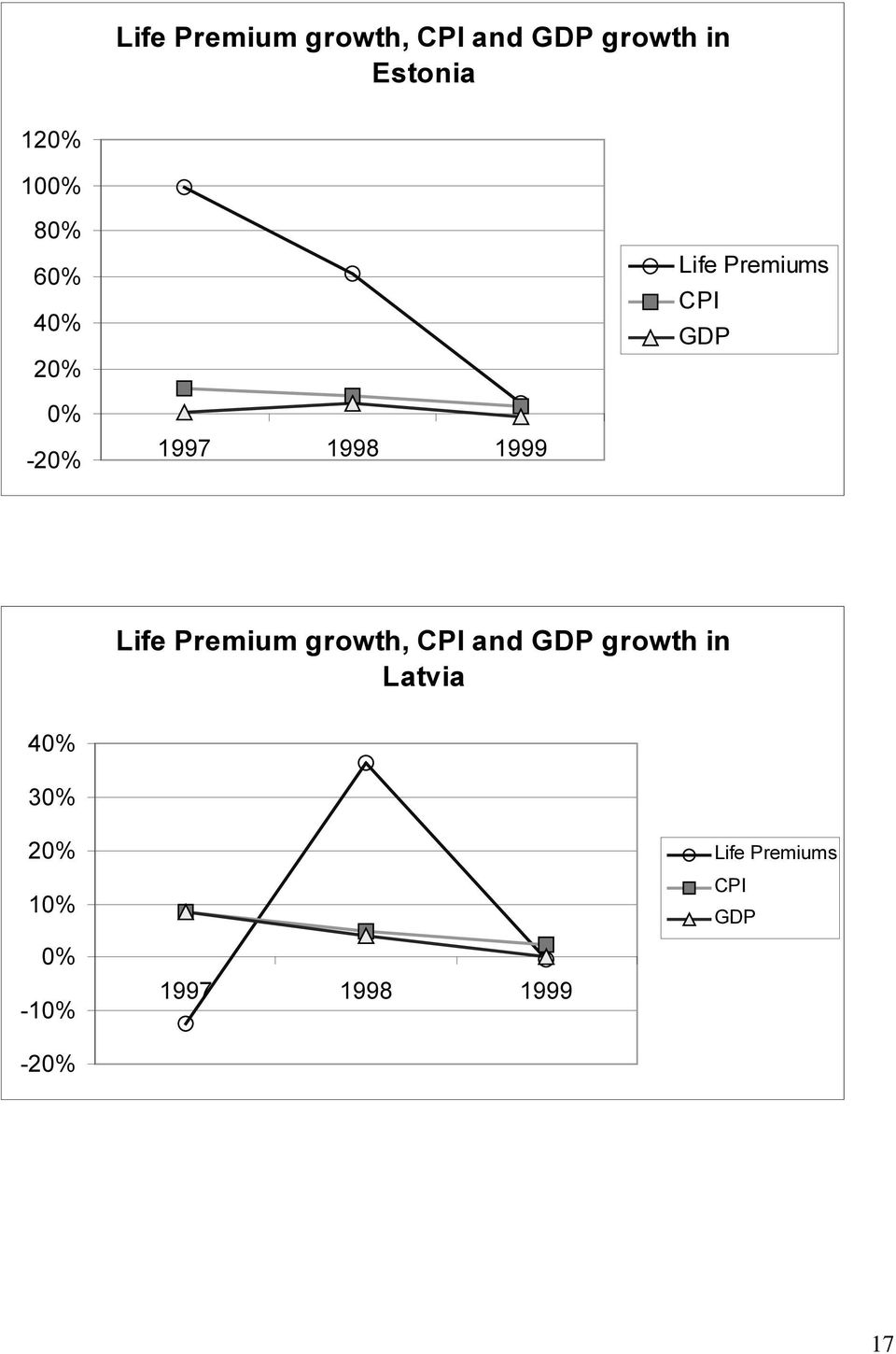

17 /LIH3UHPLXPJURZWK&3,DQG*'3JURZWKLQ (VWRQLD /LIH3UHPLXPV &3, *'3 /LIH3UHPLXPJURZWK&3,DQG*'3JURZWKLQ /DWYLD /LIH3UHPLXPV &3, *'3 17

18 /LIH3UHPLXPJURZWK&3,DQG*'3JURZWKLQ /LWKXDQLD /LIH3UHPLXPV &3, *'3 18

19 Investments 6WUXFWXUHRI,QYHVWPHQWV%DOWLF6WDWHV 2WKHU,QYHVWPHQWV 'HSRVLWVZLWKFUHGLWLQVWLWXWLRQV /RDQVRWKHUWKDQ0RUWJDJH/RDQV 0RUWJDJH/RDQV %RQGV)L[HG,QWHUHVWVHFXULWLHV 6KDUHVDQGRWKHUVHFXULWLHV,QYHVWPHQWVLQDIILOLDWHGFRPSDQLHV 5HDO(VWDWH 6WUXFWXUHRI,QYHVWPHQWV(VWRQLD 2WKHU,QYHVWPHQWV 'HSRVLWVZLWKFUHGLWLQVWLWXWLRQV /RDQVRWKHUWKDQ0RUWJDJH/RDQV 0RUWJDJH/RDQV %RQGV)L[HG,QWHUHVWVHFXULWLHV 6KDUHVDQGRWKHUVHFXULWLHV,QYHVWPHQWVLQDIILOLDWHGFRPSDQLHV 5HDO(VWDWH 19

20 6WUXFWXUHRI,QYHVWPHQWV/DWYLD 2WKHU,QYHVWPHQWV 'HSRVLWVZLWKFUHGLWLQVWLWXWLRQV /RDQVRWKHUWKDQ0RUWJDJH/RDQV 0RUWJDJH/RDQV %RQGV)L[HG,QWHUHVWVHFXULWLHV 6KDUHVDQGRWKHUVHFXULWLHV,QYHVWPHQWVLQDIILOLDWHGFRPSDQLHV 5HDO(VWDWH 6WUXFWXUHRI,QYHVWPHQWV/LWKXDQLD 2WKHU,QYHVWPHQWV 'HSRVLWVZLWKFUHGLWLQVWLWXWLRQV /RDQVRWKHUWKDQ0RUWJDJH/RDQV 0RUWJDJH/RDQV %RQGV)L[HG,QWHUHVWVHFXULWLHV 6KDUHVDQGRWKHUVHFXULWLHV,QYHVWPHQWVLQDIILOLDWHGFRPSDQLHV 5HDO(VWDWH 20

21 6WRFN0DUNHWLQGLFLHVWUHQGV 5HODWLYHXQLWV (VWRQLD /DWYLD /LWKXDQLD 21

22 Household income / consumption +RXVHKROGLQFRPH /,7+8$1,$ /$79,$ ZDJHV WUDQVIHUV RWKHU (6721,$ 86SHUPRQWK +RXVHKROGFRQVXPSWLRQ /,7+8$1,$ /$79,$ IRRG KRXVLQJ FORWKLQJ RWKHU (6721,$ 86SHUPRQWK 22

23 TABLES Number of life insurance companies LATVIA I half Number of life companies operating at the end of the year Number of new companies licensed in the 1 1 respective year Number of companies where all licenses were revoked in the respective year: - on the subject of self-liquidation on the subject of merger/acquisition - on the subject of insolvency Cases of bankruptcy legally completed in the respective year 1 LITHUANIA I half Number of life companies operating at the end of the year Number of new companies licensed in the respective year Number of companies where all licenses were revoked in the respective year: - on the subject of self-liquidation on the subject of merger/acquisition 1 - on the subject of insolvency Cases of bankruptcy legally completed in the respective year ESTONIA I half Number of life companies operating at the end of the year Number of new companies licensed in the respective year Number of companies where all licenses were revoked in the respective year: - on the subject of self-liquidation 1 - on the subject of merger/acquisition on the subject of insolvency Cases of bankruptcy legally completed in the respective year 2 23

24 List of life insurance companies Share in Market (premiums 1999) Respective country market In respect to the Baltic market ESTONIA 1. Hansapanga Kindlustus 55% 15% 2. Eesti Elukindlustus 1 3. Leks Elukindlustus 8% 2% 4. BICO Elukindlustus 7% 2% 5. SEESAM Elukindlustus 6% 2% 6. Nordika Elukindlustus 3% 1% 7. Uhispanga Elukindlustus 1% 0% 8. AB Elukindlustus 2 10% 3% 9. Polaris-Elu 2 9% 3% 100% 27% 1 - merged with Hansapanga Kindlustus 2 - suspended in 1999 LATVIA 1. Salamandra Baltik 34% 12% 2. Latva 18% 6% 3. Baltikums Dziviba 17% 6% 4. Rigas Fenikss - Dziviba 12% 4% 5. Alterna Viva 8% 3% 6. Estora 7% 2% 7. Sampo Latvija Dziviba 2% 1% 8. Solidaritate 3 3% 1% 100% 36% 3 - mutual company LITHUANIA 1. Lietuvos Draudimo gyvybes draudimas 32% 11% 2. Draudos gyvybes draudimas 9% 3% 3. Lindra - gyvybes draudimas 1% 0% 4. Hermis asmens draudimas 1% 0% 5. VB gyvybes draudimas 1% 0% 6. Lietuvos draudimas 4 57% 21% 7. Preventa 4 0% 0% 8. Hermis-Draudimas 4 0% 0% 9. KDK draudimas 4 0% 0% 100% 36% 4 - is liable for the life insurance contracts concluded before July 31, % 24

25 Life companies subsidiaries of foreign insurers or insurance groups Foreign insurer or insurance group Alte Leipziger Europa, Germany LATVIA ESTONIA LITHUANIA Rigas Fenikss Dziviba (100%) BICO Elukindlustus (65%) Draudos gyvybes draudimas (100%) Pohjola Group, Finland Seesam International Company Sampo Insurance Company, Finland SEESAM Life Latvia (90%) from year 2000 Sampo Latvija Dziviba (100%) SEESAM Elukindlustus (70%) SEESAM Elukindlustus (30%) Sampo Elukindlustus Life companies subsidiaries of banks BANK SUBSIDIARY ESTONIA Uhispank Hansapank Uhispanga elukindlustus Hansapanga Kindlustus LITHUANIA Bank Hermis Vilniaus Bankas Hermis asmens draudimas VB gyvybes draudimas LATVIA

26 Tables by country ESTONIA Monetary unit: Estonia Krona (EEK) NUMBER OF LIFE INSURANCE COMPANIES Domestic Companies 3 Companies with Foreign Participation 3 All Companies PREMIUMS WRITTEN BY LIFE COMPANIES GROSS PREMIUMS Domestic Companies Companies with Foreign Shareholders All Companies Share in the Market 7,8% 11,8% 16,4% 15,7% NET PREMIUMS GROSS CLAIMS PAID BY LIFE INSURANCE COMPANIES GROSS OPERATING EXPENSES OF LIFE INSURANCE COMPANIES ASSETS OF LIFE INSURANCE COMPANIES INVESTMENTS Real Estate Investments in affiliated companies Shares and other securities Bonds, Fixed Interest securities Mortgage Loans Loans other than Mortgage Loans Deposits with credit institutions Other Investments Total of Investments CASH Unit linked investments

27 LATVIA Monetary unit: Latvia Lats (LVL) NUMBER OF LIFE INSURANCE COMPANIES Domestic Companies 6 Companies with Foreign Participation 2 All Companies PREMIUMS WRITTEN BY LIFE COMPANIES GROSS PREMIUMS Domestic Companies Companies with Foreign Shareholders All Companies Share in the Market 20,9% 11,9% 12,6% 10,3% NET PREMIUMS GROSS CLAIMS PAID BY LIFE INSURANCE COMPANIES GROSS OPERATING EXPENSES OF LIFE INSURANCE COMPANIES ASSETS OF LIFE INSURANCE COMPANIES INVESTMENTS Real Estate Investments in affiliated companies Shares and other securities Bonds, Fixed Interest securities Mortgage Loans Loans other than Mortgage Loans Deposits with credit institutions Other Investments Total of Investments CASH

28 LITHUANIA Monetary unit: Lithuania Litas (LTL) NUMBER OF LIFE INSURANCE COMPANIES 1 Domestic Companies 4 Companies with Foreign Participation 1 All Companies PREMIUMS WRITTEN BY LIFE COMPANIES GROSS PREMIUMS Domestic Companies Companies with Foreign Shareholders All Companies Share in the Market 29,4% 23,0% 14,9% 18,2% NET PREMIUMS GROSS CLAIMS PAID BY LIFE INSURANCE COMPANIES GROSS OPERATING EXPENSES OF LIFE INSURANCE COMPANIES na na na na ASSETS OF LIFE INSURANCE COMPANIES 1 INVESTMENTS Real Estate na na na Investments in affiliated companies na na na Shares and other securities na na na Bonds, Fixed Interest securities na na na Mortgage Loans na na na Loans other than Mortgage Loans na na na Deposits with credit institutions na na na Other Investments na na na Total of Investments CASH other 4 non-life companies have life portfolio, concluded before July

29 BALTIC STATES Monetary unit: US$ NUMBER OF LIFE INSURANCE COMPANIES Domestic Companies 13 Companies with Foreign Participation 6 All Companies PREMIUMS WRITTEN BY LIFE COMPANIES GROSS PREMIUMS Domestic Companies Companies with Foreign Shareholders All Companies Share in the Market NET PREMIUMS GROSS CLAIMS PAID BY LIFE INSURANCE COMPANIES ASSETS OF LIFE INSURANCE COMPANIES INVESTMENTS Real Estate Investments in affiliated companies Shares and other securities Bonds, Fixed Interest securities Mortgage Loans Loans other than Mortgage Loans Deposits with credit institutions Other Investments Total of Investments CASH Unit linked investments

30 References Insurance Yearbook 1998, 1997, Estonian Insurance Supervisory Authority. Insurance in Lithuania 1999, 1998, 1997, Lithuania State Insurance Supervisory Authority under the Ministry of Finance. Insurance Yearbook 1997, Latvia Insurance Supervision Inspectorate. Report on the Results of the Household Budget Survey in 1998, Central Statistical Bureau of Latvia. Insurance Statistics Yearbook OECD. Insurance Guidelines for Economies in Transition. OECD, A.Püvi. Insurance Legislation s in the Baltics readiness to become a member of the EU. Proceedings of Fourth Annual International Conference Insurance in the Baltics 2000 ; Riga, September 28-29, Life and health insurance in the emerging markets: assessment, reforms and perspectives. Sigma, No. 1/1998. Swiss Re. Financial difficulties of public pension schemes: market potential for life insurers. Sigma, No. 8/1998. Swiss Re. Estonian Insurance Supervisory Authority Latvia Insurance Supervision Inspectorate State Insurance Supervisory Authority under the Ministry of Finance of the Republic of Lithuania Riga Stock Exchange National Stock Exchange of Lithuania 30

31 Tallinn Stock Exchange Statistical office of Estonia Central Statistical Bureau of Latvia Department of Statistics to the Government of the Republic of Lithuania UNDP National Human Development Reports OECD 31

INSURANCE MARKET DEVELOPMENT

INSURANCE MARKET DEVELOPMENT GENERAL INFORMATION Market participants At end-2009, there were 14 insurance companies operating in Latvia whereof four companies were engaged in life insurance and 10 companies

INSURANCE MARKET DEVELOPMENT GENERAL INFORMATION Market participants At end-2009, there were 14 insurance companies operating in Latvia whereof four companies were engaged in life insurance and 10 companies

LIFE INSURANCE MARKET DEVELOPMENT IN BALTIC COUNTRIES: PENSION REFORMS POTENTIAL MARKET FOR LIFE INSURERS. By Janis Bokans

LIFE INSURANCE MARKET DEVELOPMENT IN BALTIC COUNTRIES: PENSION REFORMS POTENTIAL MARKET FOR LIFE INSURERS By Janis Bokans The process of significant political and economical reforms in the Baltic States

LIFE INSURANCE MARKET DEVELOPMENT IN BALTIC COUNTRIES: PENSION REFORMS POTENTIAL MARKET FOR LIFE INSURERS By Janis Bokans The process of significant political and economical reforms in the Baltic States

Contents R E V I E W O F L I T H U A N I A S I N S U R A N C E M A R K E T / H 1 2 0 1 5

R E V I E W O F L I T H U A N I A S I N S U R A N C E M A R K E T / H 1 1 1 Contents I. REVIEW OF THE INSURANCE MARKET... 3 II. REVIEW OF THE FINANCIAL PERFORMANCE OF INSURANCE UNDERTAKINGS. III. REVIEW

R E V I E W O F L I T H U A N I A S I N S U R A N C E M A R K E T / H 1 1 1 Contents I. REVIEW OF THE INSURANCE MARKET... 3 II. REVIEW OF THE FINANCIAL PERFORMANCE OF INSURANCE UNDERTAKINGS. III. REVIEW

LIFE INSURANCE. and INVESTMENT

INVESTMENT SAVINGS & INSURANCE ASSOCIATION OF NZ INC GLOSSARY OF LIFE INSURANCE and INVESTMENT TERMS 2 Accident Benefit A benefit payable should death occur as the result of an accident. It may be a stand-alone

INVESTMENT SAVINGS & INSURANCE ASSOCIATION OF NZ INC GLOSSARY OF LIFE INSURANCE and INVESTMENT TERMS 2 Accident Benefit A benefit payable should death occur as the result of an accident. It may be a stand-alone

Act on Insurance. The National Council of the Slovak Republic has adopted the following Act: SECTION I PART ONE GENERAL PROVISIONS

Act on Insurance Full wording of Act No 8/2008 Coll. of 28 November 2007 on Insurance and on amendments and supplements to certain laws, as amended by Act No 270/2008 Coll., Act No 552/2008 Coll., Act

Act on Insurance Full wording of Act No 8/2008 Coll. of 28 November 2007 on Insurance and on amendments and supplements to certain laws, as amended by Act No 270/2008 Coll., Act No 552/2008 Coll., Act

Insurance/Reinsurance - Sweden

Page 1 of 7 Newsletters Law Directory Deals News Conferences Appointments My ILO Home Insurance/Reinsurance - Sweden Overview (March 2006) Contributed by Advokatfirman Vinge March 14 2006 Introduction

Page 1 of 7 Newsletters Law Directory Deals News Conferences Appointments My ILO Home Insurance/Reinsurance - Sweden Overview (March 2006) Contributed by Advokatfirman Vinge March 14 2006 Introduction

MANDATUM LIFE INSURANCE BALTIC SE

MANDATUM LIFE INSURANCE BALTIC SE INTERIM REPORT 1Q/2015 Business name: MANDATUM LIFE INSURANCE BALTIC SE Commercial registry code: 10561490 Address: Viru väljak 2, 10111 Tallinn Telephone: 6812 300 Fax:

MANDATUM LIFE INSURANCE BALTIC SE INTERIM REPORT 1Q/2015 Business name: MANDATUM LIFE INSURANCE BALTIC SE Commercial registry code: 10561490 Address: Viru väljak 2, 10111 Tallinn Telephone: 6812 300 Fax:

BS2551 Money Banking and Finance. Institutional Investors

BS2551 Money Banking and Finance Institutional Investors Institutional investors pension funds, mutual funds and life insurance companies are the main players in securities markets in both the USA and

BS2551 Money Banking and Finance Institutional Investors Institutional investors pension funds, mutual funds and life insurance companies are the main players in securities markets in both the USA and

MANDATUM LIFE INSURANCE BALTIC SE

MANDATUM LIFE INSURANCE BALTIC SE INTERIM REPORT 1-2Q/2015 Business name: MANDATUM LIFE INSURANCE BALTIC SE Commercial registry code: 10561490 Address: Viru väljak 2, 10111 Tallinn Telephone: 6812 300

MANDATUM LIFE INSURANCE BALTIC SE INTERIM REPORT 1-2Q/2015 Business name: MANDATUM LIFE INSURANCE BALTIC SE Commercial registry code: 10561490 Address: Viru väljak 2, 10111 Tallinn Telephone: 6812 300

Annex 7. Fact Sheet Estonia

Annex 7. Fact Sheet Estonia 1. Generalities: Some history of the agricultural risk and crisis management policies, programs and tools. Population: 1, 36 million inhabitants GDP 2004 9,4 billion Euro; Inflation

Annex 7. Fact Sheet Estonia 1. Generalities: Some history of the agricultural risk and crisis management policies, programs and tools. Population: 1, 36 million inhabitants GDP 2004 9,4 billion Euro; Inflation

CIG PANNONIA LIFE INSURANCE PLC.

CIG PANNONIA LIFE INSURANCE PLC. QUARTERLY PROSPECTUS II. QUARTER 2011. 25 August 2011. 1. Summary CIG Pannonia Life Insurance Plc. (hereinafter: Issuer) publishes its quarterly prospectus today. The purpose

CIG PANNONIA LIFE INSURANCE PLC. QUARTERLY PROSPECTUS II. QUARTER 2011. 25 August 2011. 1. Summary CIG Pannonia Life Insurance Plc. (hereinafter: Issuer) publishes its quarterly prospectus today. The purpose

REGULATION ON MEASUREMENT AND ASSESSMENT OF CAPITAL REQUIREMENTS OF INSURANCE AND REINSURANCE COMPANIES AND PENSION COMPANIES

REGULATION ON MEASUREMENT AND ASSESSMENT OF CAPITAL REQUIREMENTS OF INSURANCE AND REINSURANCE COMPANIES AND PENSION COMPANIES Official Gazette of Publication: 19.01.2008 26761 Issued By: Prime Ministry

REGULATION ON MEASUREMENT AND ASSESSMENT OF CAPITAL REQUIREMENTS OF INSURANCE AND REINSURANCE COMPANIES AND PENSION COMPANIES Official Gazette of Publication: 19.01.2008 26761 Issued By: Prime Ministry

DEMOGRAPHICS AND MACROECONOMICS

1 FRANCE DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 1 950 GDP per capita (USD) 44 550 Population (000s) 62 277 Labour force (000s) 28 415 Employment rate 92.6 Population over 65 (%) 16.7 Dependency

1 FRANCE DEMOGRAPHICS AND MACROECONOMICS Nominal GDP (EUR bn) 1 950 GDP per capita (USD) 44 550 Population (000s) 62 277 Labour force (000s) 28 415 Employment rate 92.6 Population over 65 (%) 16.7 Dependency

Luxembourg. Luxembourg Generally Accepted Accounting Principles (GAAP) and the Luxembourg Law dated December 8, 1994.

and the Luxembourg Law dated December 8, 1994.") Luxembourg International Comparison of Insurance * May 2009 Luxembourg General Insurance Definition Definition of property and casualty insurance company A company operating in the following insurance

Luxembourg International Comparison of Insurance * May 2009 Luxembourg General Insurance Definition Definition of property and casualty insurance company A company operating in the following insurance

G E N C S V A L T E R S L A W F I R M B A L T I C T A X C A R D 2 0 1 5

PERSONAL INCOME TAX IN BALTICS Personal Income Tax Rates in Baltics Country Social Tax- employee share Social Tax- employer share Personal Income Tax Latvia 10.50% 23.59% 23% Lithuania 9% 30.98% - 32.6%

PERSONAL INCOME TAX IN BALTICS Personal Income Tax Rates in Baltics Country Social Tax- employee share Social Tax- employer share Personal Income Tax Latvia 10.50% 23.59% 23% Lithuania 9% 30.98% - 32.6%

SCOPE OF APPLICATION AND DEFINITIONS

Unofficial translation No. 398/1995 Act on Foreign Insurance Companies Issued in Helsinki on 17 March 1995 PART I SCOPE OF APPLICATION AND DEFINITIONS Chapter 1. General Provisions Section 1. Scope of

Unofficial translation No. 398/1995 Act on Foreign Insurance Companies Issued in Helsinki on 17 March 1995 PART I SCOPE OF APPLICATION AND DEFINITIONS Chapter 1. General Provisions Section 1. Scope of

MANDATUM LIFE INSURANCE BALTIC SE

MANDATUM LIFE INSURANCE BALTIC SE INTERIM REPORT 1-3Q/2010 Business name: MANDATUM LIFE INSURANCE BALTIC SE Commercial registry code: 10561490 Address: Viru väljak 2, 10111 Tallinn Telephone: 6812 300

MANDATUM LIFE INSURANCE BALTIC SE INTERIM REPORT 1-3Q/2010 Business name: MANDATUM LIFE INSURANCE BALTIC SE Commercial registry code: 10561490 Address: Viru väljak 2, 10111 Tallinn Telephone: 6812 300

INTERIM REPORT 1Q/2010

SE SAMPO LIFE INSURANCE BALTIC INTERIM REPORT 1Q/2010 Business name: SE SAMPO LIFE INSURANCE BALTIC Commercial registry code: 10561490 Address: Viru väljak 2, 10111 Tallinn Telephone: 6812 300 Fax: 6812

SE SAMPO LIFE INSURANCE BALTIC INTERIM REPORT 1Q/2010 Business name: SE SAMPO LIFE INSURANCE BALTIC Commercial registry code: 10561490 Address: Viru väljak 2, 10111 Tallinn Telephone: 6812 300 Fax: 6812

COMPANY INCORPORATION IN LITHUANIA, ESTONIA AND LATVIA

2011 GENCS VALTERS LAW FIRM Mr. Valters Gencs COMPANY INCORPORATION IN LITHUANIA, ESTONIA AND LATVIA [COMPANY INCORPORATION IN LITHUANIA] This memorandum on company incorporation in Lithuania provides

2011 GENCS VALTERS LAW FIRM Mr. Valters Gencs COMPANY INCORPORATION IN LITHUANIA, ESTONIA AND LATVIA [COMPANY INCORPORATION IN LITHUANIA] This memorandum on company incorporation in Lithuania provides

PART 9 LEVIES 2. Page 1 Part 9

PART 9 LEVIES 2 OVERVIEW 2 SECTION 123 CASH CARDS 2 SECTION 123A DEBIT CARDS 2 SECTION 123B CASH, COMBINED AND DEBIT CARDS 2 SECTION 123C PRELIMINARY DUTY: CASH, COMBINED AND DEBIT CARDS 3 SECTION 124

PART 9 LEVIES 2 OVERVIEW 2 SECTION 123 CASH CARDS 2 SECTION 123A DEBIT CARDS 2 SECTION 123B CASH, COMBINED AND DEBIT CARDS 2 SECTION 123C PRELIMINARY DUTY: CASH, COMBINED AND DEBIT CARDS 3 SECTION 124

Definition of Public Interest Entities (PIEs) in Europe

in Europe") Definition of Public Interest Entities (PIEs) in Europe FEE Survey October 2014 This document has been prepared by FEE to the best of its knowledge and ability to ensure that it is accurate and complete.

Definition of Public Interest Entities (PIEs) in Europe FEE Survey October 2014 This document has been prepared by FEE to the best of its knowledge and ability to ensure that it is accurate and complete.

KEY FACTS 2015. UK Insurance & Long Term Savings. Key Facts 2015. Follow us on Twitter @BritishInsurers

KEY FACTS 2015 UK Insurance & Long Term Savings Key Facts 2015 @BritishInsurers Follow us on Twitter @BritishInsurers ASSOCIATION OF BRITISH INSURERS The UK insurance and long term savings industry is

KEY FACTS 2015 UK Insurance & Long Term Savings Key Facts 2015 @BritishInsurers Follow us on Twitter @BritishInsurers ASSOCIATION OF BRITISH INSURERS The UK insurance and long term savings industry is

MANDATUM LIFE INSURANCE BALTIC SE

MANDATUM LIFE INSURANCE BALTIC SE INTERIM REPORT 1-3Q/2014 Business name: MANDATUM LIFE INSURANCE BALTIC SE Commercial registry code: 10561490 Address: Viru väljak 2, 10111 Tallinn Telephone: 6812 300

MANDATUM LIFE INSURANCE BALTIC SE INTERIM REPORT 1-3Q/2014 Business name: MANDATUM LIFE INSURANCE BALTIC SE Commercial registry code: 10561490 Address: Viru väljak 2, 10111 Tallinn Telephone: 6812 300

Insurance corporations and pension funds in OECD countries

Insurance corporations and pension funds in OECD countries Massimo COLETTA (Bank of Italy) Belén ZINNI (OECD) UNECE, Expert Group on National Accounts, Geneva - 3 May 2012 Outline Motivations Insurance

Insurance corporations and pension funds in OECD countries Massimo COLETTA (Bank of Italy) Belén ZINNI (OECD) UNECE, Expert Group on National Accounts, Geneva - 3 May 2012 Outline Motivations Insurance

IOPS Member country or territory pension system profile: TRINIDAD AND TOBAGO. Update as of 15 February 2013

IOPS Member country or territory pension system profile: TRINIDAD AND TOBAGO Report 1 issued on September 2011, validated by the Central Bank of Trinidad and Tobago Update as of 15 February 2013 1 This

IOPS Member country or territory pension system profile: TRINIDAD AND TOBAGO Report 1 issued on September 2011, validated by the Central Bank of Trinidad and Tobago Update as of 15 February 2013 1 This

Ministry of Labour and Social Policy LAW ON VOLUNTARY FULLY FUNDED PENSION INSURANCE (189347.11)

") Ministry of Labour and Social Policy LAW ON VOLUNTARY FULLY FUNDED PENSION INSURANCE 1 Table of Contents CHAPTER 1 GENERAL PROVISIONS... 3 CHAPTER 2 VOLUNTARY PENSION FUNDS... 7 CHAPTER 3 PENSION COMPANIES

Ministry of Labour and Social Policy LAW ON VOLUNTARY FULLY FUNDED PENSION INSURANCE 1 Table of Contents CHAPTER 1 GENERAL PROVISIONS... 3 CHAPTER 2 VOLUNTARY PENSION FUNDS... 7 CHAPTER 3 PENSION COMPANIES

MANDATUM LIFE INSURANCE BALTIC SE

MANDATUM LIFE INSURANCE BALTIC SE INTERIM REPORT 1-4Q/2011 Business name: MANDATUM LIFE INSURANCE BALTIC SE Commercial registry code: 10561490 Address: Viru väljak 2, 10111 Tallinn Telephone: 6812 300

MANDATUM LIFE INSURANCE BALTIC SE INTERIM REPORT 1-4Q/2011 Business name: MANDATUM LIFE INSURANCE BALTIC SE Commercial registry code: 10561490 Address: Viru väljak 2, 10111 Tallinn Telephone: 6812 300

ACT ON COLLECTIVE INVESTMENT

ACT ON COLLECTIVE INVESTMENT The full wording of Act No. 594/2003 Coll. on collective investment, as amended by Act No. 635/2003 Coll., Act No. 747/2004 Coll., Act No. 213/2006 Coll., Act No. 209/2007

ACT ON COLLECTIVE INVESTMENT The full wording of Act No. 594/2003 Coll. on collective investment, as amended by Act No. 635/2003 Coll., Act No. 747/2004 Coll., Act No. 213/2006 Coll., Act No. 209/2007

Non-life insurance* Estonian Financial Supervision Authority, 21 March 2005. (thousand kroons) January 2005. Seesam Kindlustus. If Eesti Kindlustus

January 2005. Seesam Kindlustus. If Eesti Kindlustus") Estonian Financial Supervision Authority, 21 March 2005 Non-life * (thousand kroons) January 2005 ETIF** Motor TPL PR 22 943 32 705 5 618 5 592 12 889 3 945 143 83 835 incl membership fee to ETIF PR 644

Estonian Financial Supervision Authority, 21 March 2005 Non-life * (thousand kroons) January 2005 ETIF** Motor TPL PR 22 943 32 705 5 618 5 592 12 889 3 945 143 83 835 incl membership fee to ETIF PR 644

UK INSURANCE KEY FACTS 2014. UK Insurance KEY FACTS. Follow us on Twitter @BritishInsurers

UK INSURANCE KEY FACTS 2014 UK Insurance KEY FACTS 2014 3 @BritishInsurers Follow us on Twitter @BritishInsurers ASSOCIATION OF BRITISH INSURERS About the ABI The Association of British Insurers is the

UK INSURANCE KEY FACTS 2014 UK Insurance KEY FACTS 2014 3 @BritishInsurers Follow us on Twitter @BritishInsurers ASSOCIATION OF BRITISH INSURERS About the ABI The Association of British Insurers is the

Eagle Star Personal Pensions & Associated Policies

Eagle Star Personal Pensions & Associated Policies Freedom in Retirement Plan - Personal & Personal (Rebate) Single Contribution Pension Plan - Personal & Income Protection Plan Customer Guide Introduction

Eagle Star Personal Pensions & Associated Policies Freedom in Retirement Plan - Personal & Personal (Rebate) Single Contribution Pension Plan - Personal & Income Protection Plan Customer Guide Introduction

A guide to unit-linked investments

A guide to unit-linked investments Introduction This guide covers NFU Mutual s unit-linked investments. These are policies in which your money is used to purchase units in a particular fund or combination

A guide to unit-linked investments Introduction This guide covers NFU Mutual s unit-linked investments. These are policies in which your money is used to purchase units in a particular fund or combination

SURVEY OF INVESTMENT REGULATION OF PENSION FUNDS. OECD Secretariat

SURVEY OF INVESTMENT REGULATION OF PENSION FUNDS OECD Secretariat Methodological issues The information collected concerns all forms of quantitative portfolio restrictions applied to pension funds in OECD

SURVEY OF INVESTMENT REGULATION OF PENSION FUNDS OECD Secretariat Methodological issues The information collected concerns all forms of quantitative portfolio restrictions applied to pension funds in OECD

CHAPTER 4 - TAX PREFERENCES FOR SUPERANNUATION AND LIFE INSURANCE SAVINGS

45 CHAPTER 4 - TAX PREFERENCES FOR SUPERANNUATION AND LIFE INSURANCE SAVINGS 4.1 Introduction In general, superannuation and life insurance have not been subject to the normal income tax treatment for

45 CHAPTER 4 - TAX PREFERENCES FOR SUPERANNUATION AND LIFE INSURANCE SAVINGS 4.1 Introduction In general, superannuation and life insurance have not been subject to the normal income tax treatment for

Dwelling prices, total. Apartment prices. House prices. Net wages

Macro Research Macro Research - The Estonian Economy 22 September, 215 The Estonian Economy Newsletter Risks at the housing market Growth of house prices one of the fastest in Europe House prices have

Macro Research Macro Research - The Estonian Economy 22 September, 215 The Estonian Economy Newsletter Risks at the housing market Growth of house prices one of the fastest in Europe House prices have

ESTONIA REVIEW OF THE INSURANCE SYSTEM

ESTONIA REVIEW OF THE INSURANCE SYSTEM October 2011 ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT The OECD is a unique forum where governments work together to address the economic, social and

ESTONIA REVIEW OF THE INSURANCE SYSTEM October 2011 ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT The OECD is a unique forum where governments work together to address the economic, social and

Savings and life insurance in Finland

Savings and life insurance in Finland Federation of Finnish Financial Services CONTENTS Life market... 1 Premium volumes hold steady... 2 Life insurance assets post steady growth... 2 Insurance as a savings

Savings and life insurance in Finland Federation of Finnish Financial Services CONTENTS Life market... 1 Premium volumes hold steady... 2 Life insurance assets post steady growth... 2 Insurance as a savings

Operative Account 2011. Collective life insurance.

Operative Account 2011. Collective life insurance. 2 011 So simple. Just ask us. T 058 280 1000 (24 h), www.helvetia.ch 2011: A year marked by consolidation, expansion and innovation. for other reasons.

Operative Account 2011. Collective life insurance. 2 011 So simple. Just ask us. T 058 280 1000 (24 h), www.helvetia.ch 2011: A year marked by consolidation, expansion and innovation. for other reasons.

Rating Methodology for Domestic Life Insurance Companies

Rating Methodology for Domestic Life Insurance Companies Introduction ICRA Lanka s Claim Paying Ability Ratings (CPRs) are opinions on the ability of life insurance companies to pay claims and policyholder

Rating Methodology for Domestic Life Insurance Companies Introduction ICRA Lanka s Claim Paying Ability Ratings (CPRs) are opinions on the ability of life insurance companies to pay claims and policyholder

Guaranteed Growth Funds and Offshore With-Profits With-profits summary (Hong Kong)

") Guaranteed Growth Funds and Offshore With-Profits With-profits summary (Hong Kong) Clerical Medical closed to new business in Hong Kong on 1 January 2005. This document has been produced in accordance

Guaranteed Growth Funds and Offshore With-Profits With-profits summary (Hong Kong) Clerical Medical closed to new business in Hong Kong on 1 January 2005. This document has been produced in accordance

4 Distribution of Income, Earnings and Wealth

4 Distribution of Income, Earnings and Wealth Indicator 4.1 Indicator 4.2a Indicator 4.2b Indicator 4.3a Indicator 4.3b Indicator 4.4 Indicator 4.5a Indicator 4.5b Indicator 4.6 Indicator 4.7 Income per

4 Distribution of Income, Earnings and Wealth Indicator 4.1 Indicator 4.2a Indicator 4.2b Indicator 4.3a Indicator 4.3b Indicator 4.4 Indicator 4.5a Indicator 4.5b Indicator 4.6 Indicator 4.7 Income per

POLICY CONDITIONS Approved Minimum Retirement Fund (PC AM5 02/11)

") POLICY CONDITIONS Approved Minimum Retirement Fund (PC AM5 02/11) Section 1 Section 2 Section 3 Section 4 Section 5 Section 6 Contract and definitions Contributions The funds Unit linking Benefits & Options

POLICY CONDITIONS Approved Minimum Retirement Fund (PC AM5 02/11) Section 1 Section 2 Section 3 Section 4 Section 5 Section 6 Contract and definitions Contributions The funds Unit linking Benefits & Options

The Hungarian Insurance Market in an International Comparison

Authors: Molnár Tamás, Rácz István, Regős Gábor Editor: Banyár József The Hungarian Insurance Market in an International Comparison Executive Summary The following analysis attempts to review the domestic

Authors: Molnár Tamás, Rácz István, Regős Gábor Editor: Banyár József The Hungarian Insurance Market in an International Comparison Executive Summary The following analysis attempts to review the domestic

OECD INSURANCE STATISTICS

ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT ORGANISATION DE COOPÉRATION ET DE DÉVELOPPEMENT ÉCONOMIQUES DIRECTION DES AFFAIRES FINANCIÈRES ET DES ENTREPRISES DIRECTORATE FOR FINANCIAL AND ENTERPRISE

ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT ORGANISATION DE COOPÉRATION ET DE DÉVELOPPEMENT ÉCONOMIQUES DIRECTION DES AFFAIRES FINANCIÈRES ET DES ENTREPRISES DIRECTORATE FOR FINANCIAL AND ENTERPRISE

ITALIAN INSURANCE IN FIGURES. Year 2015

ITALIAN INSURANCE IN FIGURES Year 2015 The Italian insurance industry gives a significant contribution to the economy and to the society, offering a wide range of services aiming at risk protection: from

ITALIAN INSURANCE IN FIGURES Year 2015 The Italian insurance industry gives a significant contribution to the economy and to the society, offering a wide range of services aiming at risk protection: from

Netherlands. Croatia. Malta. Slovenia. Greece. Czech Republic. Portugal. Compulsory. households actual. social contributions.

Structure and development of tax revenues Table EL.: Revenue (% of GDP) 2004 2005 2006 2007 2008 2009 200 20 202 203 I. Indirect taxes : : 2.3 2.7 2.7.8 2.6 3.5 3. 3.4 VAT : : 6.8 7. 7.0 6.3 7. 7.2 7.

Structure and development of tax revenues Table EL.: Revenue (% of GDP) 2004 2005 2006 2007 2008 2009 200 20 202 203 I. Indirect taxes : : 2.3 2.7 2.7.8 2.6 3.5 3. 3.4 VAT : : 6.8 7. 7.0 6.3 7. 7.2 7.

A company operating in the following insurance branches:

International comparison omparison of insurance taxation Luxembourg General insurance overview verview Definition Definition of property and casualty insurance company A company operating in the following

International comparison omparison of insurance taxation Luxembourg General insurance overview verview Definition Definition of property and casualty insurance company A company operating in the following

Taiwan Life Insurance Report 2011

一 Business Overview of the Industry ( 一 )Business Overview Taiwan Life Insurance Report 2011 The Taiwan life insurance sector reported TWD 2,198.2 billion in premium income in 2011, down by 4.96% when

一 Business Overview of the Industry ( 一 )Business Overview Taiwan Life Insurance Report 2011 The Taiwan life insurance sector reported TWD 2,198.2 billion in premium income in 2011, down by 4.96% when

/ Insurance. Regional Highlights * Bosnia and Herzegovina. karanovic/nikolic. /March 2015/

/ Insurance Regional Highlights * /March 2015/ The insurance sector in South Eastern Europe has undergone considerable change in recent years, marked by Croatia s accession to the EU, amendments to legislation

/ Insurance Regional Highlights * /March 2015/ The insurance sector in South Eastern Europe has undergone considerable change in recent years, marked by Croatia s accession to the EU, amendments to legislation

BRIEFING NOTE. With-Profits Policies

BRIEFING NOTE With-Profits Policies This paper has been prepared by The Actuarial Profession to explain how withprofits policies work. It considers traditional non-pensions endowment policies in some detail

BRIEFING NOTE With-Profits Policies This paper has been prepared by The Actuarial Profession to explain how withprofits policies work. It considers traditional non-pensions endowment policies in some detail

How To Understand The Irish Insurance Market

Fact File INSURANCE IRELAND About Us As the voice of insurance actively promoting the highest standards, Insurance Ireland represents 95% of the domestic market and 70% of Ireland s International life

Fact File INSURANCE IRELAND About Us As the voice of insurance actively promoting the highest standards, Insurance Ireland represents 95% of the domestic market and 70% of Ireland s International life

Italy. Italy General Insurance. International Comparison of Insurance Taxation* May 2009. *connectedthinking. Definition Accounting Taxation

Italy International Comparison of Insurance * May 2009 Italy General Insurance Definition Definition of property and casualty insurance company There is not a specific definition of property and casualty

Italy International Comparison of Insurance * May 2009 Italy General Insurance Definition Definition of property and casualty insurance company There is not a specific definition of property and casualty

Data Compilation Financial Data

Data Compilation Financial Data CONTENTS 1. Transition of Significant Management Indicators, etc. Japan Post Group (Consolidated) 122 Japan Post Holdings Co., Ltd. (Non-consolidated) 122 Japan Post Co.,

Data Compilation Financial Data CONTENTS 1. Transition of Significant Management Indicators, etc. Japan Post Group (Consolidated) 122 Japan Post Holdings Co., Ltd. (Non-consolidated) 122 Japan Post Co.,

DARREN LEIGH Managing Director Baltics Market

DARREN LEIGH Managing Director Baltics Market Market Overview Population 6.9m Languages Estonian, Latvian, Lithuanian, Russian Currencies Euro and Euro pegged Lat and Lita Capital Cities Tallinn, Riga,

DARREN LEIGH Managing Director Baltics Market Market Overview Population 6.9m Languages Estonian, Latvian, Lithuanian, Russian Currencies Euro and Euro pegged Lat and Lita Capital Cities Tallinn, Riga,

Luxembourg Life Assurance for International Investors

Luxembourg Life Assurance for International Investors 2 3 CONTENTS 4 Luxembourg Life Assurance for International Investors 4 A truly international focus 6 Maximum protection 8 Solutions designed for sophisticated

Luxembourg Life Assurance for International Investors 2 3 CONTENTS 4 Luxembourg Life Assurance for International Investors 4 A truly international focus 6 Maximum protection 8 Solutions designed for sophisticated

IRISH FEDERATION FACTFILE INSURANCE. Irish Insurance Federation Factfile 2010 1

IRISH INSURANCE FEDERATION 10 FACTFILE Irish Insurance Federation Factfile 2010 1 Who are we? The Irish Insurance Federation (IIF) is the representative body for insurance companies in Ireland representing

IRISH INSURANCE FEDERATION 10 FACTFILE Irish Insurance Federation Factfile 2010 1 Who are we? The Irish Insurance Federation (IIF) is the representative body for insurance companies in Ireland representing

Law On State Funded Pensions

Disclaimer: The English language text below is provided by the Translation and Terminology Centre for information only; it confers no rights and imposes no obligations separate from those conferred or

Disclaimer: The English language text below is provided by the Translation and Terminology Centre for information only; it confers no rights and imposes no obligations separate from those conferred or

Gains on foreign life insurance policies

Helpsheet 321 Tax year 6 April 2013 to 5 April 2014 Gains on foreign life insurance policies A Contacts Introduction Page 2 Part 1 Types of policy Page 3 What sort of policy do you have? Page 3 When will

Helpsheet 321 Tax year 6 April 2013 to 5 April 2014 Gains on foreign life insurance policies A Contacts Introduction Page 2 Part 1 Types of policy Page 3 What sort of policy do you have? Page 3 When will

CHAPTER 26.1-35 STANDARD VALUATION LAW

CHAPTER 26.1-35 STANDARD VALUATION LAW 26.1-35-00.1. (Contingent effective date - See note) Definitions. In this chapter, the following definitions apply on or after the operative date of the valuation

CHAPTER 26.1-35 STANDARD VALUATION LAW 26.1-35-00.1. (Contingent effective date - See note) Definitions. In this chapter, the following definitions apply on or after the operative date of the valuation

How Can You Reduce Your Taxes?

RON GRAHAM AND ASSOCIATES LTD. 10585 111 Street NW, Edmonton, Alberta, T5M 0L7 Telephone (780) 429-6775 Facsimile (780) 424-0004 Email rgraham@rgafinancial.com How Can You Reduce Your Taxes? Tax Brackets.

RON GRAHAM AND ASSOCIATES LTD. 10585 111 Street NW, Edmonton, Alberta, T5M 0L7 Telephone (780) 429-6775 Facsimile (780) 424-0004 Email rgraham@rgafinancial.com How Can You Reduce Your Taxes? Tax Brackets.

This guide is for you, if you have a traditional with-profits pension policy with either

This guide is for you, if you have a traditional with-profits pension policy with either Guardian Assurance Ltd or Countrywide Assured 1 of 15 CONTENTS 1 What is this guide for? 2 Background to Guardian

This guide is for you, if you have a traditional with-profits pension policy with either Guardian Assurance Ltd or Countrywide Assured 1 of 15 CONTENTS 1 What is this guide for? 2 Background to Guardian

Information Canada s Financial Services Sector

Property and Casualty Insurance in Canada Overview Information Canada s Financial Services Sector The property and casualty (P&C) insurance industry in Canada provides coverage for all risks other than

Property and Casualty Insurance in Canada Overview Information Canada s Financial Services Sector The property and casualty (P&C) insurance industry in Canada provides coverage for all risks other than

ACCOUNTING FOR INSURANCE

lt:\oslo\lifeos..doc 28.10.96 ACCOUNTING FOR INSURANCE Joanne Horton and Richard Macve University of Bristol and LSE OECD Seminar on Accounting Reform In the Baltic Rim Oslo, 13 th -15 th November 1996

lt:\oslo\lifeos..doc 28.10.96 ACCOUNTING FOR INSURANCE Joanne Horton and Richard Macve University of Bristol and LSE OECD Seminar on Accounting Reform In the Baltic Rim Oslo, 13 th -15 th November 1996

186 ACT. of 24 April 2009

186 ACT of 24 April 2009 on Financial Intermediation and Financial Counselling and on amendments and supplements to certain laws The National Council of the Slovak Republic has adopted the following Act:

186 ACT of 24 April 2009 on Financial Intermediation and Financial Counselling and on amendments and supplements to certain laws The National Council of the Slovak Republic has adopted the following Act:

MANDATUM LIFE INSURANCE BALTIC SE

MANDATUM LIFE INSURANCE BALTIC SE INTERIM REPORT 1Q/2012 Business name: MANDATUM LIFE INSURANCE BALTIC SE Commercial registry code: 10561490 Address: Viru väljak 2, 10111 Tallinn Telephone: 6812 300 Fax:

MANDATUM LIFE INSURANCE BALTIC SE INTERIM REPORT 1Q/2012 Business name: MANDATUM LIFE INSURANCE BALTIC SE Commercial registry code: 10561490 Address: Viru väljak 2, 10111 Tallinn Telephone: 6812 300 Fax:

INSURANCE ACT ZAKON O OSIGURANJU

EU-projekt: Podrška Pravosudnoj akademiji: Razvoj sustava obuke za buduće suce i državne odvjetnike EU-project: Support to the Judicial Academy: Developing a training system for future judges and prosecutors

EU-projekt: Podrška Pravosudnoj akademiji: Razvoj sustava obuke za buduće suce i državne odvjetnike EU-project: Support to the Judicial Academy: Developing a training system for future judges and prosecutors

Article from: The Actuary. December 2011 Volume 8 Issue 6

Article from: The Actuary December 2011 Volume 8 Issue 6 16 The Actuary December 2011/January 2012 Life Insurance And The Actuarial Profession In India A Decade After Liberalization The actuarial profession

Article from: The Actuary December 2011 Volume 8 Issue 6 16 The Actuary December 2011/January 2012 Life Insurance And The Actuarial Profession In India A Decade After Liberalization The actuarial profession

Glossary of insurance terms

Glossary of insurance terms I. Insurance Products Annuity is a life insurance policy where an insurance company pays an income stream to an individual, usually until death, in exchange for the payment

Glossary of insurance terms I. Insurance Products Annuity is a life insurance policy where an insurance company pays an income stream to an individual, usually until death, in exchange for the payment

The Insurance Industry in British Virgin Islands, Key Trends and Opportunities to 2017

The Insurance Industry in British Virgin Islands, Key Trends and Opportunities to 2017 Market Intelligence Report Reference code: IS0259MR Published: April 2013 www.timetric.com Timetric John Carpenter

The Insurance Industry in British Virgin Islands, Key Trends and Opportunities to 2017 Market Intelligence Report Reference code: IS0259MR Published: April 2013 www.timetric.com Timetric John Carpenter

No. 63 Page 1 of 71 2015

No. 63 Page 1 of 71 No. 63. An act relating to principle-based valuation for life insurance reserves and a standard nonforfeiture law for life insurance policies. (H.482) It is hereby enacted by the General

No. 63 Page 1 of 71 No. 63. An act relating to principle-based valuation for life insurance reserves and a standard nonforfeiture law for life insurance policies. (H.482) It is hereby enacted by the General

Central Bank Survey. General Provisions

Summary Methodology Central Bank Survey, Credit Institutions Survey, Banking System Survey, Other Financial Institutions Survey, Financial Sector Survey Central Bank Survey, Credit Institutions Survey,

Summary Methodology Central Bank Survey, Credit Institutions Survey, Banking System Survey, Other Financial Institutions Survey, Financial Sector Survey Central Bank Survey, Credit Institutions Survey,

OPEN JOINT STOCK COMPANY AGENCY FOR HOUSING MORTGAGE LENDING. Agency for Housing Mortgage Lending OJSC INFORMATION POLICY GUIDELINES.

OPEN JOINT STOCK COMPANY AGENCY FOR HOUSING MORTGAGE LENDING APPROVED: by decision of the Supervisory Council (minutes No 09 of 21 December 2007) Agency for Housing Mortgage Lending OJSC INFORMATION POLICY

OPEN JOINT STOCK COMPANY AGENCY FOR HOUSING MORTGAGE LENDING APPROVED: by decision of the Supervisory Council (minutes No 09 of 21 December 2007) Agency for Housing Mortgage Lending OJSC INFORMATION POLICY

G E N C S V A L T E R S L A W F I R M B A L T I C T A X C A R D 2 0 1 5

CORPORATE INCOME TAX IN BALTICS Corporate Income Tax Rates in Baltics Country Standard rate Decreased rate Transfer of loses to next periods Latvia 15% 11% microenterprises Unlimited Lithuania 15% Estonia

CORPORATE INCOME TAX IN BALTICS Corporate Income Tax Rates in Baltics Country Standard rate Decreased rate Transfer of loses to next periods Latvia 15% 11% microenterprises Unlimited Lithuania 15% Estonia

Answers to the Questionnaire on the Supervisory Structures for Pension Funds

Answers to the Questionnaire on the Supervisory Structures for Pension Funds Social Welfare Agency, Ministry of Social Welfare and Labour of Mongolia www.mswl.gov.mn A private pension system is not well

Answers to the Questionnaire on the Supervisory Structures for Pension Funds Social Welfare Agency, Ministry of Social Welfare and Labour of Mongolia www.mswl.gov.mn A private pension system is not well

LIFE INSURANCE KEY FACTS

GENERAL INSURANCE CONCEPTS LIFE INSURANCE KEY FACTS A condition that could result in a loss is known as an EXPOSURE. An insurer is responsible for all acts of their agents as long as the agent operates

GENERAL INSURANCE CONCEPTS LIFE INSURANCE KEY FACTS A condition that could result in a loss is known as an EXPOSURE. An insurer is responsible for all acts of their agents as long as the agent operates

The Personal Portfolios Retirement Annuity Fund

The Personal Portfolios Retirement Annuity Fund What is the purpose of the Fund? Sanlam Investment Management ( SIM ) provides an solution within the Sanlam Investment Management Retirement Plan. This

The Personal Portfolios Retirement Annuity Fund What is the purpose of the Fund? Sanlam Investment Management ( SIM ) provides an solution within the Sanlam Investment Management Retirement Plan. This

INSURANCE REGULATION AND SUPERVISION IN OECD COUNTRIES, ASIAN ECONOMIES AND CEEC AND NIS COUNTRIES

INSURANCE REGULATION AND SUPERVISION IN OECD COUNTRIES, ASIAN ECONOMIES AND CEEC AND NIS COUNTRIES INSURANCE REGULATION AND SUPERVISION IN OECD COUNTRIES, ASIAN ECONOMIES AND CEEC AND NIS COUNTRIES...6

INSURANCE REGULATION AND SUPERVISION IN OECD COUNTRIES, ASIAN ECONOMIES AND CEEC AND NIS COUNTRIES INSURANCE REGULATION AND SUPERVISION IN OECD COUNTRIES, ASIAN ECONOMIES AND CEEC AND NIS COUNTRIES...6

INSURANCE DICTIONARY

INSURANCE DICTIONARY Actuary An actuary is a professional who uses statistical data to assess risk and calculate dividends, financial reserves, and insurance premiums for a business or insurer. Agent An

INSURANCE DICTIONARY Actuary An actuary is a professional who uses statistical data to assess risk and calculate dividends, financial reserves, and insurance premiums for a business or insurer. Agent An

Actuarial Report. On the Proposed Transfer of the Life Insurance Business from. Asteron Life Limited. Suncorp Life & Superannuation Limited

Actuarial Report On the Proposed Transfer of the Life Insurance Business from Asteron Life Limited to Suncorp Life & Superannuation Limited Actuarial Report Page 1 of 47 1. Executive Summary 1.1 Background

Actuarial Report On the Proposed Transfer of the Life Insurance Business from Asteron Life Limited to Suncorp Life & Superannuation Limited Actuarial Report Page 1 of 47 1. Executive Summary 1.1 Background

INVESTMENT SAVINGS & INSURANCE ASSOCIATION OF NZ INC ISI QUARTERLY STATISTICS GUIDELINE FOR COMPLETING RETURNS

INVESTMENT SAVINGS & INSURANCE ASSOCIATION OF NZ INC ISI QUARTERLY STATISTICS GUIDELINE FOR COMPLETING RETURNS REVISED SEPTEMBER 2009 REVISION - September 2009 ISI Quarterly Statistics Guidelines for Completing

INVESTMENT SAVINGS & INSURANCE ASSOCIATION OF NZ INC ISI QUARTERLY STATISTICS GUIDELINE FOR COMPLETING RETURNS REVISED SEPTEMBER 2009 REVISION - September 2009 ISI Quarterly Statistics Guidelines for Completing

SEESAM INSURANCE AS Annual report 2013

SEESAM INSURANCE AS Annual report 2013 ANNUAL REPORT Commercial registry number: 10055752 Financial year: 01.01.2013-31.12.2013 Legal address: Vambola 6 10114 Tallinn Republic of Estonia Telephone 6 281

SEESAM INSURANCE AS Annual report 2013 ANNUAL REPORT Commercial registry number: 10055752 Financial year: 01.01.2013-31.12.2013 Legal address: Vambola 6 10114 Tallinn Republic of Estonia Telephone 6 281

NN Group N.V. 30 June 2015 Condensed consolidated interim financial information

Interim financial information 5 August NN Group N.V. Condensed consolidated interim financial information Condensed consolidated interim financial information contents Condensed consolidated interim

Interim financial information 5 August NN Group N.V. Condensed consolidated interim financial information Condensed consolidated interim financial information contents Condensed consolidated interim

LITHUANIAN PENSION SCHEMES

LITHUANIAN PENSION SCHEMES Audrius Bitinas Vice-minister Ministry of Social protection and labour I. STATUTORY MANDATORY SOCIAL INSURANCE P-A-Y-G PENSION SCHEME (DB) About 96 % of the employed population

LITHUANIAN PENSION SCHEMES Audrius Bitinas Vice-minister Ministry of Social protection and labour I. STATUTORY MANDATORY SOCIAL INSURANCE P-A-Y-G PENSION SCHEME (DB) About 96 % of the employed population

LIFE ASSURANCE BUSINESS - REVENUE ACCOUNT FORM 1. Ark Life Assurance Company Limited. Reporting Institution: Written In Ireland - Irish Risk

LIFE ASSURANCE BUSINESS - REVENUE ACCOUNT FORM 1 Written In Ireland - Irish Risk Items to be shown net of reinsurance ceded Premiums receivable (less rebates and refunds) 1 114,030 Investment income receivable

LIFE ASSURANCE BUSINESS - REVENUE ACCOUNT FORM 1 Written In Ireland - Irish Risk Items to be shown net of reinsurance ceded Premiums receivable (less rebates and refunds) 1 114,030 Investment income receivable

Survey on Gender Differentiation in Insurance

GROUPE CONSULTATIF ACTUARIEL EUROPEEN EUROPEAN ACTUARIAL CONSULTATIVE GROUP Survey on Gender Differentiation in Insurance Prepared on behalf of Groupe Consultatif s Insurance Committee Editor: Manuel Peraita

GROUPE CONSULTATIF ACTUARIEL EUROPEEN EUROPEAN ACTUARIAL CONSULTATIVE GROUP Survey on Gender Differentiation in Insurance Prepared on behalf of Groupe Consultatif s Insurance Committee Editor: Manuel Peraita

Doing Business in Russia

Doing Business in Russia www.bakertillyinternational.com Contents 1 Fact Sheet 2 2 Business Entities and Accounting 4 2.1 Companies 4 2.2 Partnerships 5 2.3 Branches and Representative Offices 6 2.4 Individual

Doing Business in Russia www.bakertillyinternational.com Contents 1 Fact Sheet 2 2 Business Entities and Accounting 4 2.1 Companies 4 2.2 Partnerships 5 2.3 Branches and Representative Offices 6 2.4 Individual

Standard Life Investment Funds Limited

Standard Life Investment Funds Limited Annual FSA Insurance Returns for the financial year ended 31 December 2011 Prepared in accordance with the Accounts and Statements Rules (Appendices 9.3, and 9.6)

Standard Life Investment Funds Limited Annual FSA Insurance Returns for the financial year ended 31 December 2011 Prepared in accordance with the Accounts and Statements Rules (Appendices 9.3, and 9.6)

INSTRUCTIONS FOR COMPLETING INSURANCE COMPANY FINANCIAL STATEMENTS