Lender Expectations and Mortgage Market Dynamics: A Panel Data Study

|

|

|

- Eric Wright

- 8 years ago

- Views:

Transcription

1 Lender Expectations and Mortgage Market Dynamics: A Panel Data Study Natalie Tiernan October 2013 PRELIMINARY AND INCOMPLETE Abstract I create a new Metropolitan Statistical Area (MSA) level database to test the role of lender expectations about housing prices and borrower incomes on the dynamics of housing markets. I employ banks local branching decisions as a proxy for expectations and find that they can explain changes in mortgage application denial rates for small and mid-size banks. Further analysis of this result shows that the banks reacting to positive changes in home prices or borrower incomes by more rapidly expanding their branch network also approve more mortgage applications. I thank RERI for generous financial support. I also thank Abdullah Yavas, Frank Nothaft, Pedro Gete, Rodney Ludema, Sandeep Dahiya, Scott Frame, Bak Ergashev, Jeff Gerlach and Sharon Blei for helpful comments and advice. Ph.D. Candidate, Georgetown University. nlt6@georgetown.edu. Phone: (317)

2 1 Introduction One often-cited cause of the recent U.S. financial crisis is that mortgage lending standards in the pre-crisis years were too lax. Most of the literature so far has focused on the role securitization played in lowering lending standards. For example, Keys et al. (2010) find that loans made to borrowers just above a credit score cutoff, making the loans easier to securitize, default 20% more often than loans with similar risk characteristics just below the cutoff. There is also a new literature that studies the role played by optimistic lender expectations. 1 Foote et al. (2012), for example, argue that overly optimistic beliefs about house prices were a main feature of pre-crisis lending decisions. Understanding both of these channels is important in order to prevent future crises. This paper contributes along the expectations dimension by testing the role of lender expectations about housing prices and borrower incomes on the dynamics of housing markets in the pre-crisis period. I employ a Metropolitan Statistical Area (MSA) level data set that includes individual mortgage loan applications from the Home Mortgage Disclosure Act (HMDA) and bank branching data from the FDIC Summary of Deposits Survey to test whether a proxy for lender expectations can explain changes in lenders mortgage denial rates. A key component of this study is to test whether optimistic lender expectations can be observed in the data and whether this optimism led to overzealous mortgage lending. As lender expectations are diffi cult to measure directly, I employ a proxy to capture them. The proxy I study is the change in the number of lender branch locations. Because new branch locations are costly to open and operate, only lenders that expect favorable lending conditions in an area will choose to open them. Similarly, lenders expecting a deterioration in lending conditions in an area will choose to close branches. My branch location data from the Summary of Deposits Survey and are reported annually as of June 30. I test whether banks 1 See, for example, Brueckner et al. (2012), Cheng et al. (2013), Foote et al. (2012) and Goetzmann et al. (2012). 2

3 opening new branches in an MSA also exhibit lower mortgage denial rates on properties located within that same MSA. Because the timing of the branching data runs from June 30-June 30 and the timing of the denial rate data runs during the calendar year, I am able to rule out reverse-causality. That is, I can rule out that lower denial rates increase borrower demand and generate a need for new branches. 2 A novel feature of my data set is that I am able to exploit the heterogeneity in lenders expectations within the same MSA by comparing the lending behavior of banks that opened new branches to those that did not. That is, I can estimate the response function of individual lenders branching and mortgage denial rate decisions to the same sequence of changes in MSA conditions. My results show that lenders with assets less than $900 million and those with assets between $2 billion and $10 billion that invest in new branches in a particular MSA also lower their denial rates on mortgage loans for properties within that same MSA. When I examine the branching and mortgage denial decisions of these lenders separately, I find that lenders responding to positive movements in house prices and borrower incomes by increasing the number of branch locations in an MSA by more than average are also lowering their mortgage denial rates by more than average. This result suggests that banks that are more optimistic lower their lending standards by more than average, supporting the hypothesis that branch decisions may be a reliable proxy for expectations and that optimistic expectations may be a driver of lower lending standards. To explore the robustness of my results I redo my analysis by lien priority. Loans secured by first liens are inherently less risky, as the lender is first in line to capture the underlying value of the mortgage property should the loan default. Second liens and loans not secured by a lien, on the other hand, carry more risk. One would expect that lender expectations would play a large role in the approval/denial decision of second liens and unsecured loans. However, 2 I will include the results of causality tests in an upcoming version of the paper. 3

4 I find that my expectations proxy does a better job explaining the behavior of lenders first lien approval/denial decisions. There is an existing literature that addresses the relationship between expectations about housing prices and lending standards. Gete and Tiernan (2013) finds using a quantitative model that under imperfect information about the persistence of house price growth, lenders who observe a sequence of positive house price shocks will rationally expect future price growth and lower their lending standards in response. Brueckner et al. (2012) and Goetzmann et al. (2012) provide empirical evidence that lenders extrapolated pre-crisis housing price trends to make subprime lending decisions. Mian and Sufi(2009), however, finds that increased mortgage credit in areas with high levels of subprime lending was driven largely by credit supply factors rather than by housing price expectations. My study is also related to Cheng et al. (2013), Cortes (2012), and Dell Arricia et al. (2008). Cheng et al. (2013) provides evidence that overly optimistic expectations may have negatively influenced lending standards. The paper compares the performance of the personal home transactions of mid-level managers in securitized finance with those of uninformed control groups and finds that the transactions of the securitization agents performed worse. The authors conclude that this result signals distorted beliefs of agents in the mortgage market during the pre-crisis period. My study, in contrast, employs branching decisions to determine whether optimistic lender beliefs were present in the housing market. Cortes (2012) examines the behavior of local lenders, i.e. lenders who operate branches in the same county in which they engage in mortgage lending, in the presence of home price shocks and finds that local lenders have better information about home-price fundamentals than non-local lenders. The author finds that in general, the share of local lending in a market fell as home prices grew rapidly. I only consider local lending in my analysis, but still find evidence of optimism by local lenders due to changes in prices and borrower incomes. Dell Arricia et al. (2008) studies the determinants of denial rates at the MSA level and find that denial rates from fell as home prices, population and average income rose. The authors also find that credit boom 4

and Goetzmann et al.")

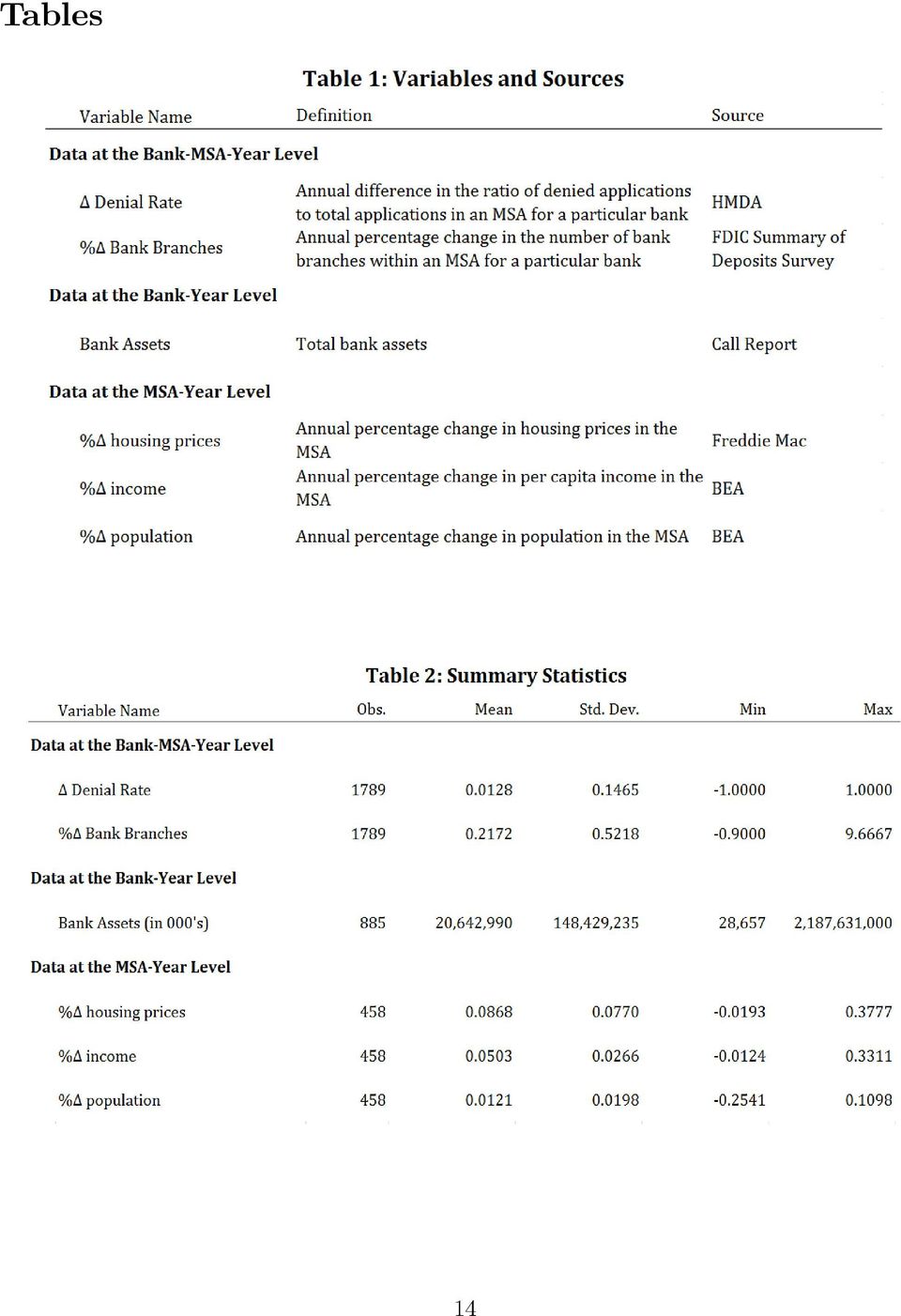

5 conditions and market structure mattered as well. My analysis addresses some of the same denial rate determinants, but approaches the question at the bank-msa level. The remainder of the paper is organized as follows. Section 2 presents the data and Section 3 describes the empirical methodology. Section 4 discusses the empirical results. Section 5 offers robustness checks. Section 6 concludes. 2 Data My principal data sets are publicly available and include U.S. home mortgage application data from the Home Mortgage Disclosure Act and bank branch data from the FDIC Summary of Deposits Survey. My control variables include banking variables from the Consolidated Reports of Condition and Income (Call Reports) collected by U.S. bank regulatory authorities, MSA-level demographic and economic data from the Bureau of Economic Analysis and MSAlevel home price data from Freddie Mac. In what follows, I define a bank or a lender as the regulatory top holder financial institution. That is, where possible I aggregate observations up to the bank holding company level. In addition, because I study year-on-year changes in some of my variables of interest, I also make adjustments for merger and acquisition activity using data available from the Federal Reserve Bank of Chicago. Table 1 contains information about variable definitions and data sources and Table 2 reports summary statistics. 2.1 Home Mortgage Disclosure Act (HMDA) Data The Home Mortgage Disclosure Act was enacted in 1975, and requires mortgage lending institutions to report data on mortgage loan applications to gauge compliance with fair lending laws and to guide public investment in housing. The data coverage includes mortgage applica- 5

collected by U.S.")

6 tions received by depository institutions and mortgage finance companies with branch offi ces in MSAs. The data do not cover mortgage applications received by small or primarily rural depository institutions. HMDA data include characteristics about mortgage loan itself, information regarding whether the loan was approved or denied, borrower demographic and income characteristics, as well as information regarding the underlying property and its location. My sample starts in 2005 and runs through HMDA data cover approximately 95% of the total volume of home mortgage originations in the U.S. in this period. 3 Because my proxy for lender expectations is only available for banks and savings institutions, I restrict my analysis to the application data reported by these institutions. With this restriction, my data account for approximately 40% of the lending activity captured by HMDA. The remaining fraction of lending activity was reported by mortgage finance companies. My primary interest in the HMDA data is computing denial rates by lender in a particular MSA in a particular year. To ensure that my comparison of denial rates across lenders is sensible, I restrict my analysis to applications for conventional home purchase loans where the underlying property is a one-to-four family home that will be owner-occupied. Furthermore, I examine only those applications with clear approval or denial decisions. That is, I include applications where the lender either originated the loan, denied the loan, or the loan was approved but not accepted. 4 My computation of the denial rate will be the total number of applications denied by a lender in a particular MSA in a particular year divided by the total number of applications received by a lender in a particular MSA in a particular year that were classified as either originated, approved, or denied. After all restrictions, my data set includes approximately 12% of the lending activity captured by HMDA. In order to use the HMDA data alongside data from the Summary of Deposits Survey and 3 Dell Ariccia et al. (2008) provide estimates of HMDA coverage rates by year. 4 I exclude applications that were withdrawn by the applicant, application files that were closed due to incompleteness, loans that were purchased by the lender, or any preapproval requests. 6

7 Call Reports, I must link records in the HMDA data to each financial institution s unique RSSD number. To do this, the HMDA data include a unique identifier for each lender based upon the combination of the lender s agency code and HMDA respondent identification number. 5 Those institutions listed as filing with the Offi ce of the Comptroller of the Currency report their charter number as their respondent identification number, those filing with the Federal Reserve System report their RSSD number, those filing with the FDIC report their certificate number and those filing with the Offi ce of Thrift Supervision report their docket number. I match these numbers to the related fields in the Call Report in order to find each institution s RSSD number. 2.2 Summary of Deposits Survey Data The Summary of Deposits Survey contains data on the location and deposits of branch offi ces for all FDIC-insured institutions as of June 30th of each year. To use bank branching decisions as a proxy for expectations, I first compute the total number of branch offi ces in an MSA for each lender in a given year. I then compute the percent change in the total number of branch offi ces for each lender in a given year, accounting for any mergers and acquisitions. 3 Empirical Methodology I first test the relationship between bank branching and denial rate decisions using a simple regression. My hypothesis is that lenders that increase the size of their branch network in a given MSA in a particular year will also lower their mortgage denial rate in that MSA in that year. That is, lenders that invest in opening branches do so because they expect more favorable lending conditions, which will then be reflected in lower mortgage denial rates. My simple 5 The agency code represents the regulatory agency with which the lender files. 7

8 regression takes the following form: denial_rate ikt = β 1 + β 2 % branches ikt + ε ikt (1) where denial_rate ikt represents the difference in the denial rate between years t and t 1 for bank i in MSA k and % branches ikt represents the percent change in the number of branches between years t and t 1 for bank i in MSA k. I run this regression for the full sample of banks as well as for different samples of banks categorized by size. To further analyze the relationships I observe from this simple regression, I explore the effect of different MSA-level factors on the banks decisions about branching and mortgage decisions independently. 6 First, I examine the impact of changes in population, changes in per capita income, and changes in house prices on a bank s decision to open or close its branch locations in a given MSA. 7 In order to capture individual banks reactions to these different MSA conditions, I also include an interaction term in my specification. The coeffi cient on this term will measure the sensitivity of individual banks to changes in either home prices or per capita income in terms of branching decisions. A positive coeffi cient would convey that a particular lender is more optimistic on average. Similarly, a negative coeffi cient would suggest that a lender is more pessimistic on average. My specification takes the following form: % branches ikt = α i D i + β 1 % population k,t 1 + +β 2 % income k,t 1 + +β 3 % prices k,t 2 + (2) +γ i (D i selected_control) + ε ikt where D i is a dummy variable for bank i, % population k,t 1 is the lagged percent change in population in MSA k, % income k,t 1 is the lagged percent change in per capita income in MSA 6 I conduct analyses of the branching and denial decisions separately to avoid issues with multicollinearity. 7 Hannan and Hanweck (2008) find that population and per capita income explain the number of bank branches present in a given MSA. 8

9 k, % prices k,t 2 is the lagged percent change in house prices in MSA k, and selected_control can be either % prices k,t 2 or % income k,t 1. I focus on lagged MSA controls because changes in branches are measured June 30 to June 30, while my controls are measured December 31 to December 31. Second, I examine the impact of the same MSA controls on changes in banks mortgage denial rates. 8 I again include an interaction term with two separate specifications: denial_rate ikt = λ i D i + ψ 1 % population k,t 1 + +ψ 2 % income k,t 1 + +ψ 3 % prices k,t 2 + (3) +θ i (D i selected_control) + ε ikt where the independent variables have the same meaning as in Equation (2) and selected_control can be either % prices k,t 2 or % income k,t 1. As before, the coeffi cient on the interaction term will measure the sensitivity of individual banks to changes in either home prices or per capita income in terms of changes in mortgage denial rates. A positive coeffi cient would imply that a particular bank raises its denial rate more than average in the presence of positive changes in house prices or per capita income. The converse is true for a negative coeffi cient. Because my interest is in measuring lender optimism and examining its effects, I study whether banks that are more sensitive to changes in either home prices or per capita income are opening (closing) branches by more than average while at the same time lowering (raising) their denial rate by more than average. This relationship would show up in a comparison of γ i, my measure for the sensitivity of bank i s branching decisions to changes in MSA conditions, with θ i, my measure for the sensitivity of bank i s denial rate modifications in response to changes in MSA conditions. 8 Dell Ariccia et al. (2008) find that population, average income and house price appreciation can explain mortgage denial rates in an MSA. 9

+θ i (D i")

10 4 Results The first specification of Equation (1) that I test includes all of the banks in my sample, and I find that the relationship between branching decisions and the mortgage denial rate is insignificant. However, when I restrict my sample to banks of certain sizes, I find varying degrees of significance. Table 3 reports these results. Banks with assets less than $900 million, which account for approximately half of the number of banks in my sample, tend to lower mortgage denial rates in MSAs where they are increasing the number of branch locations. A similar relationship emerges for banks with assets between $2 billion and $10 billion. However, smaller mid-size banks and very large banks do not exhibit a significant relationship between branch openings and changes in mortgage denial rates. One could claim that a significant negative relationship between the dependent and independent variables above arises due to reverse causality. That is, a bank lowering its denial rates would experience an increase in borrower demand and open more branches in response. However, the fact that branch openings data begin and end as of June 30, while the approval-denial decisions are measured in a calendar year mitigates this argument somewhat. For example, if Bank A opens a new branch in Miami in June 2005, that opening would be compared to mortgage denial decisions from January-December Because the decision to open that new branch likely occurred with some lead time prior to the branch opening for business, it is likely I am capturing the lender expectations channel as opposed to the borrower demand channel. To further explore the significant negative relationship observed for some of the banks in my sample, I run the regessions in Equations (2) and (3). I want to compare γ i, my measure for the sensitivity of bank i s branching decisions to changes in MSA conditions, with θ i, my measure for the sensitivity of bank i s denial rate modifications in response to changes in MSA conditions. 10

11 I focus my analysis on banks in the size ranges where the results of the simple regression in Equation (1) were significant and I have a suffi cient number of observations to complete my exercise. That is, I focus banks with assets between $2 billion and $10 billion. In Figure 1, I produce a scatter plot of γ i and θ i. Support for the expectations channel is present if in Figure 1 we observe a negative relationship between the two coeffi cients. I interpret such a result as evidence that banks responding to higher house prices or per capita income by opening (closing) more branches are also responding by lowering (raising) their denial rates to a larger degree. Figure 1 indeed shows that the expectations channel with regards to changes in both house prices and per capita income appears to drive the negative relationship between changes in bank branches and changes in bank denial rates. 5 Robustness 5.1 Lien Status As a robustness check, I repeat my analysis by lien status. In the HMDA data, lien status is reported for loan applications and originations as either a first lien, a subordinate lien, or not secured by a lien. Tables 4 and 5 report the results of the simple regression for first lien and subordinate/unsecured liens respectively. The results in Table 4 are very similar to those in Table 3 and show that the change in denial rates of banks with assets less than $900 million and banks with assets between $2 billion and $10 billion is negatively related to branch openings. All results in Table 5 are insignificant, suggesting that branching decisions may not be a reliable proxy for expectations about subordinate and unsecured lien lending prospects. Figure 2 plots the coeffi cients of the interaction terms in the regressions of Equations (2) and (3) for the first lien sample. These results also resemble those from the whole sample. 11

more branches are also responding by lowering (raising) their denial rates")

12 6 Conclusion I examine at the MSA level bank branching decisions as a proxy for lender expectations and test whether this proxy can explain changes in lenders mortgage denial rates. I find a significant negative relationship between this proxy and mortgage denial rates for banks with assets less than $900 million and banks with assets between $2 billion and $10 billion. When I break the sample by lien status, I find a similar relationship for first lien mortgage applications, but find no such relationship for second lien and unsecured applications. I find evidence that optimistic lenders that opened more branches in response to positive changes in home prices and borrower incomes also lowered their mortgage denial rate. This evidence lends support to the effect of an expectations channel on lending standards. 12

13 References Brueckner, J., Calem, P. and Nakamura, L.: 2012, Subprime mortgages and the housing bubble, Journal of Urban Economics 71, Cheng, I. H., Raina, S. and Xiong, W.: 2013, Wall street and the housing bubble. Cortés, K.: 2012, Did local lenders forecast the bust? evidence from the real estate market. Dell Ariccia, G., Igan, D. and Laeven, L.: 2008, Credit booms and lending standards: Evidence from the subprime mortgage market. Foote, C. L., Gerardi, K. S. and Willen, P. S.: 2012, Why did so many people make so many ex post bad decisions? the causes of the foreclosure crisis. Gete, P. and Tiernan, N.: 2013, Macroprudential policy for lending standards in real estate markets under imperfect information. Goetzmann, W., Peng, L. and Yen, J.: 2012, The subprime crisis and house price appreciation, The Journal of Real Estate Finance and Economics 44(1), Hannan, T. and Hanweck, G.: 2008, Recent trends in the number and size of bank branches: an examination of likely determinants. Keys, B. J., Mukherjee, T., Seru, A. and Vig, V.: 2010, Did securitization lead to lax screening? evidence from subprime loans, The Quarterly Journal of Economics 125(1), Mian, A. and Sufi, A.: 2009, The consequences of mortgage credit expansion: Evidence from the us mortgage default crisis, The Quarterly Journal of Economics 124(4),

14 Tables 14

15 Table 3: Simple Regression Results, Full Sample Assets Assets Assets Assets Dependent variable: denial_rate ikt All banks <$0.9B $0.9B-$2B $2B-$10B >$10B % branches ikt * ** (0.007) (0.020) (0.022) (0.017) (0.007) Constant 0.015*** 0.028** * 0.014*** (0.004) (0.012) (0.012) (0.008) (0.004) Observations No. of Banks Notes: Standard errors are in parentheses. * denotes significance at 10%, ** at 5%, and *** at 1%. Table 4: Simple Regression Results, First Liens Only Assets Assets Assets Assets Dependent variable: denial_rate ikt All banks <$0.9B $0.9B-$2B $2B-$10B >$10B % branches ikt * ** (0.008) (0.021) (0.024) (0.018) (0.010) Constant 0.016*** 0.028** *** (0.004) (0.013) (0.013) (0.008) (0.006) Observations No. of Banks Notes: Standard errors are in parentheses. * denotes significance at 10%, ** at 5%, and *** at 1%. 15

16 Table 5: Simple Regression Results, Subordinate and Unsecured Liens Only Assets Assets Assets Assets Dependent variable: denial_rate ikt All banks <$0.9B $0.9B-$2B $2B-$10B >$10B % branches ikt (0.009) (0.044) (0.028) (0.038) (0.010) Constant (0.005) (0.017) (0.016) (0.013) (0.006) Observations No. of Banks Notes: Standard errors are in parentheses. * denotes significance at 10%, ** at 5%, and *** at 1%. 16

Observations 1313 182 164 248 719 No. of Banks 413 157 111 107 47 Notes: Standard errors are in parentheses.")

17 Figures Banks' sensitivity to house price changes in an MSA 100 Corr = θ i γ i 40 Banks' sensitivity to per capita income changes in an MSA Corr = θ i γ i Figure 1: Sensitivity of individual banks branch openings and denial rates in response to changes in MSA conditions. Data shown are for banks with assets between $2 billion and $10 billion. 17

18 Banks' sensitivity to house price changes in an MSA 100 Corr = θ i γ i 60 Banks' sensitiv ity to per capita income changes in an MSA 40 Corr = θ i γ i Figure 2: Sensitivity of individual banks branch openings and denial rates on first lien loan applications in response to changes in MSA conditions. Data shown are for banks with assets between $2 billion and $10 billion. 18

Discussion. Credit Boom and Lending Standard: Evidence from Subprime Mortgage Lending. Satyajit Chatterjee

Credit Boom and Lending Standard: Evidence from Subprime Mortgage Lending Research Department Federal Reserve Bank of Philadelphia September 2008 OBJECTIVES AND FINDINGS Consensus that the source of the

Credit Boom and Lending Standard: Evidence from Subprime Mortgage Lending Research Department Federal Reserve Bank of Philadelphia September 2008 OBJECTIVES AND FINDINGS Consensus that the source of the

Online Appendix. Banks Liability Structure and Mortgage Lending. During the Financial Crisis

Online Appendix Banks Liability Structure and Mortgage Lending During the Financial Crisis Jihad Dagher Kazim Kazimov Outline This online appendix is split into three sections. Section 1 provides further

Online Appendix Banks Liability Structure and Mortgage Lending During the Financial Crisis Jihad Dagher Kazim Kazimov Outline This online appendix is split into three sections. Section 1 provides further

HMDA DATA ON DEMAND FREQUENTLY ASKED QUESTIONS

HMDA DATA ON DEMAND FREQUENTLY ASKED QUESTIONS About the Home Mortgage Disclosure Act (HMDA) One of the most comprehensive sources of publically available application-level information on the single-family

HMDA DATA ON DEMAND FREQUENTLY ASKED QUESTIONS About the Home Mortgage Disclosure Act (HMDA) One of the most comprehensive sources of publically available application-level information on the single-family

Characteristics of Home Mortgage Lending to Racial or Ethnic Groups in Iowa

Characteristics of Home Mortgage Lending to Racial or Ethnic Groups in Iowa Liesl Eathington Dave Swenson Regional Capacity Analysis Program ReCAP Department of Economics, Iowa State University September

Characteristics of Home Mortgage Lending to Racial or Ethnic Groups in Iowa Liesl Eathington Dave Swenson Regional Capacity Analysis Program ReCAP Department of Economics, Iowa State University September

Cream Skimming in Subprime Mortgage Securitizations

Cream-skimming in Subprime Mortgage Securitizations: Which Subprime Mortgage Loans were Sold by Depository Institutions Prior to the Crisis of 2007? Paul Calem, Christopher Henderson, Jonathan Liles Discussion

Cream-skimming in Subprime Mortgage Securitizations: Which Subprime Mortgage Loans were Sold by Depository Institutions Prior to the Crisis of 2007? Paul Calem, Christopher Henderson, Jonathan Liles Discussion

Out of State Non Local Mortgages: Features and Explanation

Out of State Non Local Mortgages: Features and Explanation Yilan Xu yix11@pitt.edu Jipeng Zhang jiz44@pitt.edu Department of Economics University of Pittsburgh Abstract Using a sample from the Home Mortgage

Out of State Non Local Mortgages: Features and Explanation Yilan Xu yix11@pitt.edu Jipeng Zhang jiz44@pitt.edu Department of Economics University of Pittsburgh Abstract Using a sample from the Home Mortgage

What Did Lenders Know? House Price Increases and Previously Rejected Mortgages

What Did Lenders Know? House Price Increases and Previously Rejected Mortgages Peggy Crawford Pepperdine University Joetta Forsyth Pepperdine University We examine whether the incidence of originated mortgages

What Did Lenders Know? House Price Increases and Previously Rejected Mortgages Peggy Crawford Pepperdine University Joetta Forsyth Pepperdine University We examine whether the incidence of originated mortgages

ICBA Summary of the Home Mortgage Disclosure Act (HMDA) Revisions to Regulation C

Revisions to Regulation C") ICBA Summary of the Home Mortgage Disclosure Act (HMDA) Revisions to Regulation C November 2015 Month Year Mon Contact: Joe Gormley Assistant Vice President & Regulatory Counsel joseph.gormley@icba.org

ICBA Summary of the Home Mortgage Disclosure Act (HMDA) Revisions to Regulation C November 2015 Month Year Mon Contact: Joe Gormley Assistant Vice President & Regulatory Counsel joseph.gormley@icba.org

Comment On: Reducing Foreclosures by Christopher Foote, Kristopher Gerardi, Lorenz Goette and Paul Willen

Comment On: Reducing Foreclosures by Christopher Foote, Kristopher Gerardi, Lorenz Goette and Paul Willen Atif Mian 1 University of Chicago Booth School of Business and NBER The current global recession

Comment On: Reducing Foreclosures by Christopher Foote, Kristopher Gerardi, Lorenz Goette and Paul Willen Atif Mian 1 University of Chicago Booth School of Business and NBER The current global recession

Competition in mortgage markets: The effect of lender type on loan characteristics

Competition in mortgage markets: The effect of lender type on loan characteristics Richard J. Rosen Introduction and summary The years 1995 through 2007 saw a boom and bust in home prices and purchase

Competition in mortgage markets: The effect of lender type on loan characteristics Richard J. Rosen Introduction and summary The years 1995 through 2007 saw a boom and bust in home prices and purchase

Subprime Lending and the Community Reinvestment Act

Joint Center for Housing Studies Harvard University Subprime Lending and the Community Reinvestment Act Kevin Park November 2008 N08-2 by Kevin Park. All rights reserved. Short sections of text, not to

Joint Center for Housing Studies Harvard University Subprime Lending and the Community Reinvestment Act Kevin Park November 2008 N08-2 by Kevin Park. All rights reserved. Short sections of text, not to

Credit Supply and the Price of Housing

Credit Supply and the Price of Housing Giovanni Favara HEC Lausanne Swiss Finance Institute IMF Jean Imbs HEC Lausanne Swiss Finance Institute CEPR January 2010 Abstract We show that since 1994, branching

Credit Supply and the Price of Housing Giovanni Favara HEC Lausanne Swiss Finance Institute IMF Jean Imbs HEC Lausanne Swiss Finance Institute CEPR January 2010 Abstract We show that since 1994, branching

Subprime Mortgage Defaults and Credit Default Swaps

Subprime Mortgage Defaults and Credit Default Swaps The Journal of Finance Eric Arentsen (TCW) David C. Mauer (IOWA) Brian Rosenlund (TCW) Harold H. Zhang (UTD) Feng Zhao (UTD) Motivation The sharp increase

Subprime Mortgage Defaults and Credit Default Swaps The Journal of Finance Eric Arentsen (TCW) David C. Mauer (IOWA) Brian Rosenlund (TCW) Harold H. Zhang (UTD) Feng Zhao (UTD) Motivation The sharp increase

Home Mortgage Disclosure Act - Regulation C

Home Mortgage Disclosure Act - Regulation C Revised Date: 12/20/2013 Introduction: The Home Mortgage Disclosure Act (HMDA), implemented by Regulation C, provides the members with loan data that can be

Home Mortgage Disclosure Act - Regulation C Revised Date: 12/20/2013 Introduction: The Home Mortgage Disclosure Act (HMDA), implemented by Regulation C, provides the members with loan data that can be

Interstate Non-Local Mortgage Lending: Features and Explanations

Interstate Non-Local Mortgage Lending: Features and Explanations Yilan Xu yix11@pitt.edu Jipeng Zhang jiz44@pitt.edu Department of Economics University of Pittsburgh Abstract The mortgages from out-of-state

Interstate Non-Local Mortgage Lending: Features and Explanations Yilan Xu yix11@pitt.edu Jipeng Zhang jiz44@pitt.edu Department of Economics University of Pittsburgh Abstract The mortgages from out-of-state

FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA. General Background

March 31, 2005 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted by Congress in 1975, requires most mortgage lenders

March 31, 2005 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted by Congress in 1975, requires most mortgage lenders

Home Mortgage Disclosure Act Examination Procedures

Background and Summary The Home Mortgage Disclosure Act (HMDA) was enacted by the Congress in 1975 and is implemented by the Federal Reserve Board s Regulation C (12 CFR Part 203). The period of 1988 through

Background and Summary The Home Mortgage Disclosure Act (HMDA) was enacted by the Congress in 1975 and is implemented by the Federal Reserve Board s Regulation C (12 CFR Part 203). The period of 1988 through

FEDERAL RESERVE SYSTEM. 12 CFR Part 203. [Regulation C; Docket No. R-1001] Home Mortgage Disclosure

![FEDERAL RESERVE SYSTEM. 12 CFR Part 203. [Regulation C; Docket No. R-1001] Home Mortgage Disclosure](/thumbs/37/17826005.jpg "FEDERAL RESERVE SYSTEM. 12 CFR Part 203. [Regulation C; Docket No. R-1001] Home Mortgage Disclosure") FEDERAL RESERVE SYSTEM 12 CFR Part 203 [Regulation C; Docket No. R-1001] Home Mortgage Disclosure AGENCY: Board of Governors of the Federal Reserve System. ACTION: Advance notice of proposed rulemaking.

FEDERAL RESERVE SYSTEM 12 CFR Part 203 [Regulation C; Docket No. R-1001] Home Mortgage Disclosure AGENCY: Board of Governors of the Federal Reserve System. ACTION: Advance notice of proposed rulemaking.

Information regarding Mortgage Lending indicators in NEO CANDO

Mortgage Lending I. Definitions A lending institution is a bank, savings institution, credit union or mortgage company. A bank, savings institution, or credit union is required to report HMDA data if within

Mortgage Lending I. Definitions A lending institution is a bank, savings institution, credit union or mortgage company. A bank, savings institution, or credit union is required to report HMDA data if within

Home Mortgage Disclosure Act 1

Home Mortgage Disclosure Act 1 The Home Mortgage Disclosure Act (HMDA) was enacted by the Congress in 1975 and is implemented by Regulation C (12 CFR Part 1003). 2 The period of 1988 through 1992 saw substantial

Home Mortgage Disclosure Act 1 The Home Mortgage Disclosure Act (HMDA) was enacted by the Congress in 1975 and is implemented by Regulation C (12 CFR Part 1003). 2 The period of 1988 through 1992 saw substantial

Small Banks and Deposit Insurance: The U.S. Experience. Christine E. Blair, Ph.D. Sr. Financial Economist Federal Deposit Insurance Corporation

Insurance: The U.S. Experience Christine E. Blair, Ph.D. Sr. Financial Economist Federal Deposit Insurance Corporation Insurance: The U.S. Experience Outline of presentation Role of the FDIC U.S. banking

Insurance: The U.S. Experience Christine E. Blair, Ph.D. Sr. Financial Economist Federal Deposit Insurance Corporation Insurance: The U.S. Experience Outline of presentation Role of the FDIC U.S. banking

Comparing patterns of default among prime and subprime mortgages

Comparing patterns of default among prime and subprime mortgages Gene Amromin and Anna L. Paulson Introduction and summary We have all heard a lot in recent months about the soaring number of defaults

Comparing patterns of default among prime and subprime mortgages Gene Amromin and Anna L. Paulson Introduction and summary We have all heard a lot in recent months about the soaring number of defaults

FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA. General Background

April 3, 2006 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted by Congress in 1975, requires most mortgage lenders

April 3, 2006 FREQUENTLY ASKED QUESTIONS ABOUT THE NEW HMDA DATA General Background 1. What is the Home Mortgage Disclosure Act (HMDA)? HMDA, enacted by Congress in 1975, requires most mortgage lenders

Reports - Findings from Analysis of Nationwide Summary Statistics for 2013 Community Reinvestment Act Data Fact Sheet (August 2014)

") Reports - Findings from Analysis of Nationwide Summary Statistics for 2013 Community Reinvestment Act Data Fact Sheet (August 2014) This analysis is based on data compiled by the three federal banking

Reports - Findings from Analysis of Nationwide Summary Statistics for 2013 Community Reinvestment Act Data Fact Sheet (August 2014) This analysis is based on data compiled by the three federal banking

Home Mortgage Disclosure Act: CFPB Finalizes Amendments to Regulation C Implementing Significant Changes to HMDA Reporting

December 2015 RPL15-05 Home Mortgage Disclosure Act: CFPB Finalizes Amendments to Regulation C Implementing Significant Changes to HMDA Reporting Executive Summary The Consumer Financial Protection Bureau

December 2015 RPL15-05 Home Mortgage Disclosure Act: CFPB Finalizes Amendments to Regulation C Implementing Significant Changes to HMDA Reporting Executive Summary The Consumer Financial Protection Bureau

STATEMENT OF THE FEDERAL DEPOSIT INSURANCE CORPORATION RICHARD A. BROWN CHIEF ECONOMIST

STATEMENT OF THE FEDERAL DEPOSIT INSURANCE CORPORATION by RICHARD A. BROWN CHIEF ECONOMIST on LESSONS LEARNED FROM THE FINANCIAL CRISIS REGARDING COMMUNITY BANKS before the COMMITTEE ON BANKING, HOUSING,

STATEMENT OF THE FEDERAL DEPOSIT INSURANCE CORPORATION by RICHARD A. BROWN CHIEF ECONOMIST on LESSONS LEARNED FROM THE FINANCIAL CRISIS REGARDING COMMUNITY BANKS before the COMMITTEE ON BANKING, HOUSING,

The Effects of Adjustable Rate Mortgages on House Price Inflation

Abstract The Effects of Adjustable Rate Mortgages on House Price Inflation Albert S. Davies, PhD 1 Middle Tennessee State University Jennings A. Jones College of Business Department of Economics and Finance

Abstract The Effects of Adjustable Rate Mortgages on House Price Inflation Albert S. Davies, PhD 1 Middle Tennessee State University Jennings A. Jones College of Business Department of Economics and Finance

Introduction. Section 203.1 -- Authority, Purpose, and Scope

SUPPLEMENT I TO PART 203 -- STAFF COMMENTARY Introduction 1. Status and citations. The commentary in this supplement is the vehicle by which the Division of Consumer and Community Affairs of the Federal

SUPPLEMENT I TO PART 203 -- STAFF COMMENTARY Introduction 1. Status and citations. The commentary in this supplement is the vehicle by which the Division of Consumer and Community Affairs of the Federal

Fair Lending and HMDA Compliance

Office of Consumer Protection Consumer Compliance Policy & Outreach Fair Lending and HMDA Compliance February 20, 2015 The information contained in this presentation is for informational purposes only

Office of Consumer Protection Consumer Compliance Policy & Outreach Fair Lending and HMDA Compliance February 20, 2015 The information contained in this presentation is for informational purposes only

PUBLIC DISCLOSURE COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

PUBLIC DISCLOSURE January 07, 2014 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Lake Federal, FSB Charter Number 706128 7048 Kennedy Ave Hammond, IN 46323-2212 Office of the Comptroller of the Currency

PUBLIC DISCLOSURE January 07, 2014 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Lake Federal, FSB Charter Number 706128 7048 Kennedy Ave Hammond, IN 46323-2212 Office of the Comptroller of the Currency

GAO RELEASED. October 30, 1990 The Honorable Richard G. LUgar United States Senate

GAO October 30, 1990 The Honorable Richard G. LUgar United States Senate Dear Senator Lugar: RELEASED On October 10, 1990 we briefed your staff on the extent to which adjustable rate mortgages (ARMS) were

GAO October 30, 1990 The Honorable Richard G. LUgar United States Senate Dear Senator Lugar: RELEASED On October 10, 1990 we briefed your staff on the extent to which adjustable rate mortgages (ARMS) were

Bank Consolidation and Small Business Lending: The Role of Community Banks

Bank Consolidation and Small Business Lending: The Role of Community Banks Working Paper 2003-05 Robert B. Avery and Katherine A. Samolyk* October 2003 JEL Classification Codes: L1, L4, G2 * Contact information:

Bank Consolidation and Small Business Lending: The Role of Community Banks Working Paper 2003-05 Robert B. Avery and Katherine A. Samolyk* October 2003 JEL Classification Codes: L1, L4, G2 * Contact information:

Small Bank Comparative Advantages in Alleviating Financial Constraints and Providing Liquidity Insurance over Time

Small Bank Comparative Advantages in Alleviating Financial Constraints and Providing Liquidity Insurance over Time Allen N. Berger University of South Carolina Wharton Financial Institutions Center European

Small Bank Comparative Advantages in Alleviating Financial Constraints and Providing Liquidity Insurance over Time Allen N. Berger University of South Carolina Wharton Financial Institutions Center European

ANALYSIS OF HOME MORTGAGE DISCLOSURE ACT (HMDA) DATA FOR TEXAS, 1999-2001

DATA FOR TEXAS, 1999-2001") LEGISLATIVE REPORT ANALYSIS OF HOME MORTGAGE DISCLOSURE ACT (HMDA) DATA FOR TEXAS, 1999-2001 REPORT PREPARED FOR THE FINANCE COMMISSION OF TEXAS AND THE OFFICE OF CONSUMER CREDIT COMMISSIONER BY THE TEXAS

LEGISLATIVE REPORT ANALYSIS OF HOME MORTGAGE DISCLOSURE ACT (HMDA) DATA FOR TEXAS, 1999-2001 REPORT PREPARED FOR THE FINANCE COMMISSION OF TEXAS AND THE OFFICE OF CONSUMER CREDIT COMMISSIONER BY THE TEXAS

Residential Mortgage Lending in Oregon, CY 2007

Introduction Residential Mortgage Lending in Oregon, CY 2007 By Senate Bill 1064 (2008), the Oregon Legislature required that all mortgage banker and mortgage brokers licensed by the Oregon Division of

Introduction Residential Mortgage Lending in Oregon, CY 2007 By Senate Bill 1064 (2008), the Oregon Legislature required that all mortgage banker and mortgage brokers licensed by the Oregon Division of

Fraudulent Income Overstatement by Home Buyers During the Mortgage Credit Expansion of 2002 to 2005

Fraudulent Income Overstatement by Home Buyers During the Mortgage Credit Expansion of 2002 to 2005 Atif Mian Princeton University NBER Amir Sufi University of Chicago Booth School of Business NBER Mian

Fraudulent Income Overstatement by Home Buyers During the Mortgage Credit Expansion of 2002 to 2005 Atif Mian Princeton University NBER Amir Sufi University of Chicago Booth School of Business NBER Mian

Regression Analysis of Small Business Lending in Appalachia

Regression Analysis of Small Business Lending in Appalachia Introduction Drawing on the insights gathered from the literature review, this chapter will test the influence of bank consolidation, credit

Regression Analysis of Small Business Lending in Appalachia Introduction Drawing on the insights gathered from the literature review, this chapter will test the influence of bank consolidation, credit

Fair Lending Update. 2012 Banker Outreach Program

Fair Lending Update 2012 Banker Outreach Program Fair Lending Discussion Topics: Fair Lending High Risks Areas Pricing and Underwriting Examination Focus and Procedures How to Conduct a Comparative Analysis

Fair Lending Update 2012 Banker Outreach Program Fair Lending Discussion Topics: Fair Lending High Risks Areas Pricing and Underwriting Examination Focus and Procedures How to Conduct a Comparative Analysis

http://www.ritholtz.com/blog/2014/11/housing-market-headwin...

Page 1 of 5 - The Big Picture - http://www.ritholtz.com/blog - Housing Market Headwinds Posted By Guest Author On November 10, 2014 @ 5:00 am In Real Estate,Think Tank 3 Comments Housing Market Headwinds

Page 1 of 5 - The Big Picture - http://www.ritholtz.com/blog - Housing Market Headwinds Posted By Guest Author On November 10, 2014 @ 5:00 am In Real Estate,Think Tank 3 Comments Housing Market Headwinds

Exploratory Study of the Accuracy of Home Mortgage Disclosure Act (HMDA) Data. Final Report. Executive Summary. Contract #C-OPC-5978 Task Order No.

Data. Final Report. Executive Summary. Contract #C-OPC-5978 Task Order No.") Exploratory Study of the Accuracy of Home Mortgage Disclosure Act (HMDA) Data Final Report Cambridge, MA Lexington, MA Hadley, MA Bethesda, MD Washington, DC Chicago, IL Cairo, Egypt Johannesburg, South

Exploratory Study of the Accuracy of Home Mortgage Disclosure Act (HMDA) Data Final Report Cambridge, MA Lexington, MA Hadley, MA Bethesda, MD Washington, DC Chicago, IL Cairo, Egypt Johannesburg, South

The Impact of the Small Business Lending Fund on Community Bank Lending to Small Businesses

The Impact of the Small Business Lending Fund on Community Bank Lending to Small Businesses Dean Amel* Board of Governors of the Federal Reserve System Traci Mach* Board of Governors of the Federal Reserve

The Impact of the Small Business Lending Fund on Community Bank Lending to Small Businesses Dean Amel* Board of Governors of the Federal Reserve System Traci Mach* Board of Governors of the Federal Reserve

Demystifying the Refi-Share Mystery

Demystifying the Refi-Share Mystery Authors Yan Chang and Frank E. Nothaft Abstract The refinance shares reported by Freddie Mac s Primary Mortgage Market Survey (PMMS), the Mortgage Bankers Association

Demystifying the Refi-Share Mystery Authors Yan Chang and Frank E. Nothaft Abstract The refinance shares reported by Freddie Mac s Primary Mortgage Market Survey (PMMS), the Mortgage Bankers Association

Have the GSE Affordable Housing Goals Increased. the Supply of Mortgage Credit?

Have the GSE Affordable Housing Goals Increased the Supply of Mortgage Credit? Brent W. Ambrose * Professor of Finance and Director Center for Real Estate Studies Gatton College of Business and Economics

Have the GSE Affordable Housing Goals Increased the Supply of Mortgage Credit? Brent W. Ambrose * Professor of Finance and Director Center for Real Estate Studies Gatton College of Business and Economics

Home-Mortgage Lending Trends in New England in 2010

January 212 No. 212-1 Home-Mortgage Lending Trends in New England in 21 Ana Patricia Muñoz The views expressed in this paper are solely those of the author and do not necessarily represent those of the

January 212 No. 212-1 Home-Mortgage Lending Trends in New England in 21 Ana Patricia Muñoz The views expressed in this paper are solely those of the author and do not necessarily represent those of the

CHAPTER 3: LENDER APPROVAL 7 CFR 3555.51

3.1 INTRODUCTION CHAPTER 3: LENDER APPROVAL 7 CFR 3555.51 A lender is defined as an entity that originates, services, or holds a loan guaranteed by the Agency. The SFHGLP is not intended to promote risky

3.1 INTRODUCTION CHAPTER 3: LENDER APPROVAL 7 CFR 3555.51 A lender is defined as an entity that originates, services, or holds a loan guaranteed by the Agency. The SFHGLP is not intended to promote risky

Home Mortgage Disclosure

Regulation C Home Mortgage Disclosure Background Regulation C (12 CFR 203) implements the Home Mortgage Disclosure Act (HMDA), which was enacted by Congress in 1975. The period 1988 through 1992 saw substantial

Regulation C Home Mortgage Disclosure Background Regulation C (12 CFR 203) implements the Home Mortgage Disclosure Act (HMDA), which was enacted by Congress in 1975. The period 1988 through 1992 saw substantial

CCE Consumer Compliance Examination. Home Mortgage Disclosure. Comptroller s Handbook. February 2010 CCE-HMDA

CCE-HMDA Comptroller of the Currency Administrator of National Banks Home Mortgage Disclosure Comptroller s Handbook February 2010 CCE Consumer Compliance Examination Home Mortgage Disclosure Table of

CCE-HMDA Comptroller of the Currency Administrator of National Banks Home Mortgage Disclosure Comptroller s Handbook February 2010 CCE Consumer Compliance Examination Home Mortgage Disclosure Table of

Professor Chris Mayer (Columbia Business School; NBER; Visiting Scholar, Federal Reserve Bank of New York)

") Professor Chris Mayer (Columbia Business School; NBER; Visiting Scholar, Federal Reserve Bank of New York) Lessons Learned from the Crisis: Housing, Subprime Mortgages, and Securitization THE PAUL MILSTEIN

Professor Chris Mayer (Columbia Business School; NBER; Visiting Scholar, Federal Reserve Bank of New York) Lessons Learned from the Crisis: Housing, Subprime Mortgages, and Securitization THE PAUL MILSTEIN

Low- and Moderate-Income Home Financing: What Are the Trends in Kansas City?

Low- and Moderate-Income Home Financing: What Are the Trends in Kansas City? James Harvey and Kenneth Spong James Harvey is a senior examiner and policy economist and Kenneth Spong is a senior policy economist

Low- and Moderate-Income Home Financing: What Are the Trends in Kansas City? James Harvey and Kenneth Spong James Harvey is a senior examiner and policy economist and Kenneth Spong is a senior policy economist

Discussion of Credit Growth and the Financial Crisis: A New Narrative, by Albanesi et al.

Discussion of Credit Growth and the Financial Crisis: A New Narrative, by Albanesi et al. Atif Mian Princeton University and NBER March 4, 2016 1 / 24 Main result high credit growth attributed to low credit

Discussion of Credit Growth and the Financial Crisis: A New Narrative, by Albanesi et al. Atif Mian Princeton University and NBER March 4, 2016 1 / 24 Main result high credit growth attributed to low credit

Did the Community Reinvestment Act (CRA) Lead to Risky Lending?

Lead to Risky Lending?") Did the Community Reinvestment Act (CRA) Lead to Risky Lending? Sumit Agarwal (School of Business, National University of Singapore) Efraim Benmelech (Kellogg School of Management, Northwestern University,

Did the Community Reinvestment Act (CRA) Lead to Risky Lending? Sumit Agarwal (School of Business, National University of Singapore) Efraim Benmelech (Kellogg School of Management, Northwestern University,

DISCUSSION ISSUES FOR SMALL ENTITY REPRESENTATIVES

SMALL BUSINESS REVIEW PANEL AND COST OF CREDIT CONSULTATION FOR HOME MORTGAGE DISCLOSURE ACT (HMDA) RULEMAKING DISCUSSION ISSUES FOR SMALL ENTITY REPRESENTATIVES To help frame the small entity representatives

SMALL BUSINESS REVIEW PANEL AND COST OF CREDIT CONSULTATION FOR HOME MORTGAGE DISCLOSURE ACT (HMDA) RULEMAKING DISCUSSION ISSUES FOR SMALL ENTITY REPRESENTATIVES To help frame the small entity representatives

Real Estate Investors and the Boom and Bust of the US Housing Market

Real Estate Investors and the Boom and Bust of the US Housing Market Zhenyu Gao Wenli Li September 2012 (Preliminary and Comments Welcome) Abstract This paper studies residential real estate investors

Real Estate Investors and the Boom and Bust of the US Housing Market Zhenyu Gao Wenli Li September 2012 (Preliminary and Comments Welcome) Abstract This paper studies residential real estate investors

Mortgage Market Concentration, Foreclosures and House Prices

Mortgage Market Concentration, Foreclosures and House Prices Giovanni Favara Board of Governors of the Federal Reserve System giovanni.favara@frb.gov Mariassunta Giannetti Stockholm School of Economics,

Mortgage Market Concentration, Foreclosures and House Prices Giovanni Favara Board of Governors of the Federal Reserve System giovanni.favara@frb.gov Mariassunta Giannetti Stockholm School of Economics,

Small Business Lending in Local Markets Due to Mergers and Consolidation

Bank Consolidation and the Provision of Banking Services: The Case of Small Commercial Loans by Robert B. Avery and Katherine Samolyk* December 2000 Robert B. Avery Federal Reserve Board Washington, DC

Bank Consolidation and the Provision of Banking Services: The Case of Small Commercial Loans by Robert B. Avery and Katherine Samolyk* December 2000 Robert B. Avery Federal Reserve Board Washington, DC

CFPB Proposal Would Make 'HMDites' Of Us All

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com CFPB Proposal Would Make 'HMDites' Of Us All Law360,

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com CFPB Proposal Would Make 'HMDites' Of Us All Law360,

ABL Step 1 An Introduction. How SIPPA can change the Lending Environment and Access to Credit

ABL Step 1 An Introduction How SIPPA can change the Lending Environment and Access to Credit Traditional Bank vs ABL Bank Focused on Credit Status Over reliance on Real Estate Vulnerable to Economic Cycles

ABL Step 1 An Introduction How SIPPA can change the Lending Environment and Access to Credit Traditional Bank vs ABL Bank Focused on Credit Status Over reliance on Real Estate Vulnerable to Economic Cycles

Measuring Mortgage Credit Availability Using Ex-Ante Probability of Default

HOUSING AND HOUSING FINANCE RESEARCH REPORT Measuring Mortgage Credit Availability Using Ex-Ante Probability of Default Wei Li Laurie Goodman November 2014 ABOUT THE URBAN INSTITUTE The nonprofit Urban

HOUSING AND HOUSING FINANCE RESEARCH REPORT Measuring Mortgage Credit Availability Using Ex-Ante Probability of Default Wei Li Laurie Goodman November 2014 ABOUT THE URBAN INSTITUTE The nonprofit Urban

February 27, 2014. Travis Wilbert Travis.wilbert@occ.treas.gov One Financial Place, Suite 2700 440 South LaSalle Street Chicago, IL 60605

February 27, 2014 Travis Wilbert Travis.wilbert@occ.treas.gov One Financial Place, Suite 2700 440 South LaSalle Street Chicago, IL 60605 RE: U.S. Bank National Association Acquisition of RBS Citizens Charter

February 27, 2014 Travis Wilbert Travis.wilbert@occ.treas.gov One Financial Place, Suite 2700 440 South LaSalle Street Chicago, IL 60605 RE: U.S. Bank National Association Acquisition of RBS Citizens Charter

Behavior Model to Capture Bank Charge-off Risk for Next Periods Working Paper

1 Behavior Model to Capture Bank Charge-off Risk for Next Periods Working Paper Spring 2007 Juan R. Castro * School of Business LeTourneau University 2100 Mobberly Ave. Longview, Texas 75607 Keywords:

1 Behavior Model to Capture Bank Charge-off Risk for Next Periods Working Paper Spring 2007 Juan R. Castro * School of Business LeTourneau University 2100 Mobberly Ave. Longview, Texas 75607 Keywords:

(i) To help determine whether financial institutions are serving the housing needs of their communities;

To help determine whether financial institutions are serving the housing needs of their communities;") PART 203 HOME MORTGAGE DISCLOSURE (REGULATION C) Contents 203.1 Authority, purpose, and scope. 203.2 Definitions. 203.3 Exempt institutions. 203.4 Compilation of loan data. 203.5 Disclosure and reporting.

PART 203 HOME MORTGAGE DISCLOSURE (REGULATION C) Contents 203.1 Authority, purpose, and scope. 203.2 Definitions. 203.3 Exempt institutions. 203.4 Compilation of loan data. 203.5 Disclosure and reporting.

RECOGNIZE, RECORD, REPORT: THE LATEST DEVELOPMENTS IN THE HOME MORTGAGE DISCLOSURE ACT

RECOGNIZE, RECORD, REPORT: THE LATEST DEVELOPMENTS IN THE HOME MORTGAGE DISCLOSURE ACT Module 1 Learning Objectives In Module 1, students will: Explore an overview of the Home Mortgage Disclosure Act,

RECOGNIZE, RECORD, REPORT: THE LATEST DEVELOPMENTS IN THE HOME MORTGAGE DISCLOSURE ACT Module 1 Learning Objectives In Module 1, students will: Explore an overview of the Home Mortgage Disclosure Act,

FRBSF ECONOMIC LETTER

FRBSF ECONOMIC LETTER 2012-25 August 20, 2012 Consumer Debt and the Economic Recovery BY JOHN KRAINER A key ingredient of an economic recovery is a pickup in household spending supported by increased consumer

FRBSF ECONOMIC LETTER 2012-25 August 20, 2012 Consumer Debt and the Economic Recovery BY JOHN KRAINER A key ingredient of an economic recovery is a pickup in household spending supported by increased consumer

national community investment fund

national community investment fund May 17, 2013 Legislative and Regulatory Activities Division Office of the Comptroller of the Currency Mail Stop 9W-11 400 7th street, SW Washington DC 20219 Docket ID

national community investment fund May 17, 2013 Legislative and Regulatory Activities Division Office of the Comptroller of the Currency Mail Stop 9W-11 400 7th street, SW Washington DC 20219 Docket ID

The Consequences of Mortgage Credit Expansion: Evidence from the 2007 Mortgage Default Crisis

Working Paper No. 15 The Consequences of Mortgage Credit Expansion: Evidence from the 2007 Mortgage Default Crisis Atif Mian University of Chicago Graduate School of Business and NBER Amir Sufi University

Working Paper No. 15 The Consequences of Mortgage Credit Expansion: Evidence from the 2007 Mortgage Default Crisis Atif Mian University of Chicago Graduate School of Business and NBER Amir Sufi University

Overview of Mortgage Lending

Chapter 1 Overview of Mortgage Lending 1 Chapter Objectives Identify historical events affecting today s mortgage industry. Contrast the primary mortgage market and secondary mortgage market. Identify

Chapter 1 Overview of Mortgage Lending 1 Chapter Objectives Identify historical events affecting today s mortgage industry. Contrast the primary mortgage market and secondary mortgage market. Identify

STATE OF NEW YORK BANKING DEPARTMENT ONE STATE STREET NEW YORK, NY

STATE OF NEW YORK BANKING DEPARTMENT ONE STATE STREET NEW YORK, NY 10004-1417 www.banking.state.ny.us RICHARD H. NEIMAN Superintendent of Banks August 6, 2010 Jennifer J. Johnson, Secretary Board of Governors

STATE OF NEW YORK BANKING DEPARTMENT ONE STATE STREET NEW YORK, NY 10004-1417 www.banking.state.ny.us RICHARD H. NEIMAN Superintendent of Banks August 6, 2010 Jennifer J. Johnson, Secretary Board of Governors

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class * Manuel Adelino, Duke. Antoinette Schoar, MIT and NBER

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class * Manuel Adelino, Duke Antoinette Schoar, MIT and NBER Felipe Severino, Dartmouth Current version: June, 15 First version:

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class * Manuel Adelino, Duke Antoinette Schoar, MIT and NBER Felipe Severino, Dartmouth Current version: June, 15 First version:

What Role Did Piggyback Lending Play in the Housing Bubble. and Mortgage Collapse?

What Role Did Piggyback Lending Play in the Housing Bubble and Mortgage Collapse? Contact Author: Michael LaCour-Little College of Business and Economics California State University at Fullerton Fullerton,

What Role Did Piggyback Lending Play in the Housing Bubble and Mortgage Collapse? Contact Author: Michael LaCour-Little College of Business and Economics California State University at Fullerton Fullerton,

Mortgage Bankers Association of Central Florida

Mortgage Bankers Association of Central Florida Real Estate Appreciation in Single-Family Homes in the Orlando MSA: March 2015 Update (February 26, 2015) Stanley D. Smith Professor of Finance University

Mortgage Bankers Association of Central Florida Real Estate Appreciation in Single-Family Homes in the Orlando MSA: March 2015 Update (February 26, 2015) Stanley D. Smith Professor of Finance University

HUD s AFFORDABLE LENDING GOALS FOR FANNIE MAE AND FREDDIE MAC

Issue Brief HUD s AFFORDABLE LENDING GOALS FOR FANNIE MAE AND FREDDIE MAC Fannie Mae and Freddie Mac, government-sponsored enterprises (GSEs) in the secondary mortgage market, are the two largest sources

Issue Brief HUD s AFFORDABLE LENDING GOALS FOR FANNIE MAE AND FREDDIE MAC Fannie Mae and Freddie Mac, government-sponsored enterprises (GSEs) in the secondary mortgage market, are the two largest sources

A Guide to HMDA Reporting

A Guide to HMDA Reporting Mary-Ann Boaz, CRCM December 8, 2015 MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2010 Wolf & Company, P.C. Before we get started Today s presentation

A Guide to HMDA Reporting Mary-Ann Boaz, CRCM December 8, 2015 MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2010 Wolf & Company, P.C. Before we get started Today s presentation

University of Pennsylvania Law School

University of Pennsylvania Law School ILE INSTITUTE FOR LAW AND ECONOMICS A Joint Research Center of the Law School, the Wharton School, and the Department of Economics in the School of Arts and Sciences

University of Pennsylvania Law School ILE INSTITUTE FOR LAW AND ECONOMICS A Joint Research Center of the Law School, the Wharton School, and the Department of Economics in the School of Arts and Sciences

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class * Manuel Adelino, Duke. Antoinette Schoar, MIT and NBER

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class * Manuel Adelino, Duke Antoinette Schoar, MIT and NBER Felipe Severino, Dartmouth Current version: September 15 First

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class * Manuel Adelino, Duke Antoinette Schoar, MIT and NBER Felipe Severino, Dartmouth Current version: September 15 First

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class * Manuel Adelino, Duke. Antoinette Schoar, MIT and NBER

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class * Manuel Adelino, Duke Antoinette Schoar, MIT and NBER Felipe Severino, Dartmouth Current version: June, 15 First version:

Loan Originations and Defaults in the Mortgage Crisis: The Role of the Middle Class * Manuel Adelino, Duke Antoinette Schoar, MIT and NBER Felipe Severino, Dartmouth Current version: June, 15 First version:

PUBLIC DISCLOSURE. January 31, 2011 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

O LARGE BANK Comptroller of the Currency Administrator of National Banks Washington, DC 20219 PUBLIC DISCLOSURE January 31, 2011 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION South Carolina Bank &

O LARGE BANK Comptroller of the Currency Administrator of National Banks Washington, DC 20219 PUBLIC DISCLOSURE January 31, 2011 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION South Carolina Bank &

WHO RECEIVES A MORTGAGE MODIFICATION? RACE AND INCOME DIFFERENTIALS IN LOAN WORKOUTS

WHO RECEIVES A MORTGAGE MODIFICATION? RACE AND INCOME DIFFERENTIALS IN LOAN WORKOUTS J. MICHAEL COLLINS University of Wisconsin Loan modifications offer one strategy to prevent mortgage foreclosures by

WHO RECEIVES A MORTGAGE MODIFICATION? RACE AND INCOME DIFFERENTIALS IN LOAN WORKOUTS J. MICHAEL COLLINS University of Wisconsin Loan modifications offer one strategy to prevent mortgage foreclosures by

PUBLIC DISCLOSURE. January 3, 2011 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION. First National Bank of Omaha Charter Number: 209

O LARGE BANK Comptroller of the Currency Administrator of National Banks Washington, DC 20219 PUBLIC DISCLOSURE January 3, 2011 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION First National Bank of

O LARGE BANK Comptroller of the Currency Administrator of National Banks Washington, DC 20219 PUBLIC DISCLOSURE January 3, 2011 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION First National Bank of

Regulatory Practice Letter February 2013 RPL 13-07

Regulatory Practice Letter February 2013 RPL 13-07 High Cost Mortgages and Homeownership Counseling; Escrow Requirements - CFPB Final Rules Executive Summary The Bureau of Consumer Financial Protection

Regulatory Practice Letter February 2013 RPL 13-07 High Cost Mortgages and Homeownership Counseling; Escrow Requirements - CFPB Final Rules Executive Summary The Bureau of Consumer Financial Protection

PUBLIC DISCLOSURE COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

Small Bank Performance Evaluation PUBLIC DISCLOSURE November 30, 1998 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Guaranty National Bank of Tallahassee Charter Number 21162 111 South Monroe Street

Small Bank Performance Evaluation PUBLIC DISCLOSURE November 30, 1998 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Guaranty National Bank of Tallahassee Charter Number 21162 111 South Monroe Street

Online Appendix: Bank Competition, Risk Taking and Their Consequences

Online Appendix: Bank Competition, Risk Taking and Their Consequences Xiaochen (Alan) Feng Princeton University - Not for Pulication- This version: Novemer 2014 (Link to the most updated version) OA1.

Online Appendix: Bank Competition, Risk Taking and Their Consequences Xiaochen (Alan) Feng Princeton University - Not for Pulication- This version: Novemer 2014 (Link to the most updated version) OA1.

The Home Mortgage Disclosure Act History, Evolution, and Limitations Joseph M. Kolar Buckley Kolar LLP March 14, 2005 Washington, DC History of HMDA Enacted 30 years ago, HMDA s purposes and requirements

The Home Mortgage Disclosure Act History, Evolution, and Limitations Joseph M. Kolar Buckley Kolar LLP March 14, 2005 Washington, DC History of HMDA Enacted 30 years ago, HMDA s purposes and requirements

TILA Escrow Requirements for High Priced Mortgage Loans (12 CFR 1026.35)

") TILA Escrow Requirements for High Priced Mortgage Loans (12 CFR 1026.35) The Consumer Financial Protection Bureau s (CFPB) mortgage rules include new escrow account requirements for higher-priced mortgage

TILA Escrow Requirements for High Priced Mortgage Loans (12 CFR 1026.35) The Consumer Financial Protection Bureau s (CFPB) mortgage rules include new escrow account requirements for higher-priced mortgage

Spotlight on the Housing Market in the Orlando-Kissimmee-Sanford, FL MSA

Spotlight on in Orlando-Kissimmee-Sanford, FL MSA The Orlando-Kissimmee-Sanford, FL Metropolitan Statistical Area (Orlando MSA) is located in central Florida and includes four counties: Lake, Orange, Osceola,

Spotlight on in Orlando-Kissimmee-Sanford, FL MSA The Orlando-Kissimmee-Sanford, FL Metropolitan Statistical Area (Orlando MSA) is located in central Florida and includes four counties: Lake, Orange, Osceola,

Public Disclosure. Community Reinvestment Act Performance Evaluation

Comptroller of the Currency Administrator of National Banks LARGE BANK Public Disclosure September 20, 1999 Community Reinvestment Act Performance Evaluation Community Bank, N.A. Charter Number: 8531 45-49

Comptroller of the Currency Administrator of National Banks LARGE BANK Public Disclosure September 20, 1999 Community Reinvestment Act Performance Evaluation Community Bank, N.A. Charter Number: 8531 45-49

The State of Mortgage Lending in New York City

The State of Mortgage Lending in New York City Mortgage lending trends provide an important window into the housing market and the changing availability of credit, both of which have been profoundly affected

The State of Mortgage Lending in New York City Mortgage lending trends provide an important window into the housing market and the changing availability of credit, both of which have been profoundly affected

Arkansas Banks vs. Florida Banks and the Subprime Mortgage Crisis

Arkansas Banks vs. Florida Banks and the Subprime Mortgage Crisis Alex Fayman University of Central Arkansas In the wake of the Great Recession, Arkansas banks found themselves across the negotiating table

Arkansas Banks vs. Florida Banks and the Subprime Mortgage Crisis Alex Fayman University of Central Arkansas In the wake of the Great Recession, Arkansas banks found themselves across the negotiating table

Principal Lending Manager Education Curriculum Outline 40 Hours

Principal Lending Manager Education Curriculum Outline 40 Hours Utah Division of Real Estate PO Box 146711 Salt Lake City, UT 84114-6711 Subject Matter Number of Hours 1. General Mortgage Industry Knowledge

Principal Lending Manager Education Curriculum Outline 40 Hours Utah Division of Real Estate PO Box 146711 Salt Lake City, UT 84114-6711 Subject Matter Number of Hours 1. General Mortgage Industry Knowledge

Appendix A: Description of the Data

Appendix A: Description of the Data This data release presents information by year of origination on the dollar amounts, loan counts, and delinquency experience through year-end 2009 of single-family mortgages

Appendix A: Description of the Data This data release presents information by year of origination on the dollar amounts, loan counts, and delinquency experience through year-end 2009 of single-family mortgages

NATIONAL DELINQUENCY SURVEY: FACTS

NATIONAL DELINQUENCY SURVEY: FACTS The NDS is a voluntary survey of over 120 mortgage lenders, including mortgage banks, commercial banks, thrifts, savings and loan associations, subservicers and life

NATIONAL DELINQUENCY SURVEY: FACTS The NDS is a voluntary survey of over 120 mortgage lenders, including mortgage banks, commercial banks, thrifts, savings and loan associations, subservicers and life

PUBLIC DISCLOSURE. Evaluation Period: June 2, 2009 - March 31, 2012 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

O LARGE BANK Comptroller of the Currency Administrator of National Banks Washington, DC 20219 PUBLIC DISCLOSURE Evaluation Period: June 2, 2009 - March 31, 2012 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

O LARGE BANK Comptroller of the Currency Administrator of National Banks Washington, DC 20219 PUBLIC DISCLOSURE Evaluation Period: June 2, 2009 - March 31, 2012 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

COMMUNITY REINVESTMENT ACT

COMMUNITY REINVESTMENT ACT EXAMINATION PROCEDURES FOR LARGE INSTITUTIONS Examination Scope For institutions (interstate and intrastate) with more than one assessment area, identify assessment areas for

COMMUNITY REINVESTMENT ACT EXAMINATION PROCEDURES FOR LARGE INSTITUTIONS Examination Scope For institutions (interstate and intrastate) with more than one assessment area, identify assessment areas for

The Effect of Mortgage Securitization on Foreclosure. and Modification

The Effect of Mortgage Securitization on Foreclosure and Modification Samuel Kruger January 2014 Harvard University Department of Economics and Harvard Business School. Wyss House, Harvard Business School,

The Effect of Mortgage Securitization on Foreclosure and Modification Samuel Kruger January 2014 Harvard University Department of Economics and Harvard Business School. Wyss House, Harvard Business School,

Small Business Review Panel for HMDA Rulemaking

Submitted electronically June 11, 2014 The Honorable Richard Cordray Director Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC 20552 Re: Small Business Review Panel for HMDA Rulemaking

Submitted electronically June 11, 2014 The Honorable Richard Cordray Director Consumer Financial Protection Bureau 1700 G Street, NW Washington, DC 20552 Re: Small Business Review Panel for HMDA Rulemaking

Vol 2015, No. 2. Abstract

House price volatility: The role of different buyer types Dermot Coates, Reamonn Lydon & Yvonne McCarthy 1 Economic Letter Series Vol 1, No. Abstract This Economic Letter examines the link between house

House price volatility: The role of different buyer types Dermot Coates, Reamonn Lydon & Yvonne McCarthy 1 Economic Letter Series Vol 1, No. Abstract This Economic Letter examines the link between house

A Banker s Quick Reference Guide to CRA

Federal Reserve Bank of Dallas A Banker s Quick Reference Guide to CRA As amended effective September 1, 2005 This publication is a guide to the CRA regulation and examination procedures. It is intended

Federal Reserve Bank of Dallas A Banker s Quick Reference Guide to CRA As amended effective September 1, 2005 This publication is a guide to the CRA regulation and examination procedures. It is intended

EXAMINATION PROCEDURES FOR LARGE INSTITUTIONS... 2 EXAMINATION SCOPE... 2 PERFORMANCE CONTEXT... 3 ASSESSMENT AREA... 4

TABLE OF CONTENTS EXAMINATION PROCEDURES FOR LARGE INSTITUTIONS... 2 EXAMINATION SCOPE... 2 PERFORMANCE CONTEXT... 3 ASSESSMENT AREA... 4 LENDING, INVESTMENT, AND SERVICE TESTS FOR LARGE RETAIL INSTITUTIONS...

TABLE OF CONTENTS EXAMINATION PROCEDURES FOR LARGE INSTITUTIONS... 2 EXAMINATION SCOPE... 2 PERFORMANCE CONTEXT... 3 ASSESSMENT AREA... 4 LENDING, INVESTMENT, AND SERVICE TESTS FOR LARGE RETAIL INSTITUTIONS...

Using Big Data to Improve the Mortgage Industry Operating Model

Using Big Data to Improve the Mortgage Industry Operating Model Overview of the HMDA S B A Score By David K. Moffat Mortgage TrueView December 2014 Copyright 2014 Mortgage TrueView Inc. All Rights Reserved

Using Big Data to Improve the Mortgage Industry Operating Model Overview of the HMDA S B A Score By David K. Moffat Mortgage TrueView December 2014 Copyright 2014 Mortgage TrueView Inc. All Rights Reserved

Elena Loutskina University of Virginia, Darden School of Business. Philip E. Strahan Boston College, Wharton Financial Institutions Center & NBER

INFORMED AND UNINFORMED INVESTMENT IN HOUSING: THE DOWNSIDE OF DIVERSIFICATION Elena Loutskina University of Virginia, Darden School of Business & Philip E. Strahan Boston College, Wharton Financial Institutions

INFORMED AND UNINFORMED INVESTMENT IN HOUSING: THE DOWNSIDE OF DIVERSIFICATION Elena Loutskina University of Virginia, Darden School of Business & Philip E. Strahan Boston College, Wharton Financial Institutions

Data Drives the Movement for Economic Justice! Archana Pradhan, Senior Research Analyst, NCRC. March 20, 2013

Data Drives the Movement for Economic Justice! Archana Pradhan, Senior Research Analyst, NCRC March 20, 2013 Why data? 2 To uncover the trend Ø Who is lending in your community? Ø Are they equitably originating

Data Drives the Movement for Economic Justice! Archana Pradhan, Senior Research Analyst, NCRC March 20, 2013 Why data? 2 To uncover the trend Ø Who is lending in your community? Ø Are they equitably originating