New Business Profile Scores Assigned for U.S. Utility and Power Companies; Financial Guidelines Revised

|

|

|

- Maria Lindsay King

- 8 years ago

- Views:

Transcription

1 June 2, 2004 New Business Profile Scores Assigned for U.S. Utility and Power Companies; Financial Guidelines Revised Credit Analyst: Ronald M Barone, New York (1) ; Richard W Cortright, Jr., New York (1) ; Suzanne G Smith, New York (1) ; John W Whitlock, New York (1) ; Andrew Watt, New York (1) ; Arthur F Simonson, New York (1) Table Of Contents New Business Profile Scores and Revised Financial Guidelines Results Business Profile Score Methodology Appendix: U.S. Utility and Power Company Ranking List 1 Standard & Poor's. All rights reserved. No reprint or dissemination without Standard & Poor's permission. See Terms of Use/Disclaimer on the last page

2 New Business Profile Scores Assigned for U.S. Utility and Power Companies; Financial Guidelines Revised Standard & Poor's Ratings Services has assigned new business profile scores to U.S. utility and power companies to better reflect the relative business risk among companies in the sector. Standard & Poor's also has revised its published risk-adjusted financial guidelines. The new business scores and financial guidelines do not represent a change to Standard & Poor's ratings criteria or methodology, and no ratings changes are anticipated from the new business profile scores or revised financial guidelines. New Business Profile Scores and Revised Financial Guidelines Standard & Poor's has always monitored changes in the industry and altered its business risk assessments accordingly. This is the first time since the 10-point business profile scale for U.S. investor-owned utilities was implemented that a comprehensive assessment of the benefits and the application of the methodology has been made. The principal purpose was to determine if the methodology continues to provide meaningful differentiation of business risk. The review indicated that while business profile scoring continues to provide analytical benefits, the complete range of the 10-point scale was not being utilized to the fullest extent. Standard & Poor's has also revised the key financial guidelines that it uses as an integral part of evaluating the credit quality of U.S. utility and power companies. These guidelines were last updated in June The financial guidelines for three principal ratios (funds from operations (FFO) interest coverage, FFO to total debt, and total debt to total capital) have been broadened so as to be more flexible. Pretax interest coverage as a key credit ratio was eliminated. Finally, Standard & Poor's has segmented the utility and power industry into sub-sectors based on the dominant corporate strategy that a company is pursuing. Standard & Poor's has published a new U.S. utility and power company ranking list that reflects these sub-sectors. There are numerous benefits to the reassessment. Fuller utilization of the entire 10-point scale provides a superior relative ranking of qualitative business risk. A simultaneous revision of the financial guidelines supports the goal of not causing rating changes from the recalibration of the business profiles. Classification of companies by sub-sectors will ensure greater comparability and consistency in ratings. The use of industry segmentation will also allow more in-depth statistical analysis of ratings distributions and rating changes. The reassessment does not represent a change to Standard & Poor's criteria or methodology for determining ratings for utility and power companies. Each business profile score should be considered as the assignment of a new score; these scores do not represent improvement or deterioration in our assessment of an individual company's business risk relative to the previously assigned score. The financial guidelines continue to be risk-adjusted based on historical utility and industrial medians. Segmentation into industry sub-sectors does not imply that specific company characteristics will not weigh heavily into the assignment of a company's business profile score. Standard & Poor s RatingsDirect June 2,

3 Results Previously, 83% of U.S. utility and power business profile scores fell between '3' and '6', which clearly does not reflect the risk differentiation that exists in the utility and power industry today. Since the 10-point scale was introduced, the industry has transformed into a much less homogenous industry, where the divergence of business risk--particularly regarding management, strategy, and degree of competitive market exposure--has created a much wider spectrum of risk profiles. Yet over the same period, business profile scores actually converged more tightly around a median score of '4'. The new business profile scores, as of the date of this publication, are shown in Chart 1. The overall median business profile score is now '5'. Chart 1 Table 1 contains the revised financial guidelines. It is important to emphasize that these metrics are only guidelines associated with expectations for various rating levels. Although credit ratio analysis is an important part of the ratings process, these three statistics are by no means the only critical financial measures that Standard & Poor's uses in its analytical process. We also analyze a wide array of financial ratios that do not have published guidelines for each rating category. Table 1 Revised Financial Guidelines Funds from operations/interest coverage (x) Business Profile AA A BBB BB

4 Table 1 Revised Financial Guidelines (cont.) Funds from operation/total debt (%) Business Profile AA A BBB BB Total debt/total capital (%) Business Profile AA A BBB BB Again, ratings analysis is not driven solely by these financial ratios, nor has it ever been. In fact, the new financial guidelines that Standard & Poor's is incorporating for the specified rating categories reinforce the analytical framework whereby other factors can outweigh the achievement of otherwise acceptable financial ratios. These factors include: Effectiveness of liability and liquidity management; Analysis of internal funding sources; Return on invested capital; Standard & Poor s RatingsDirect June 2,

Business Profile AA A BBB BB 1 48 55 55 60 60 70 2 45")

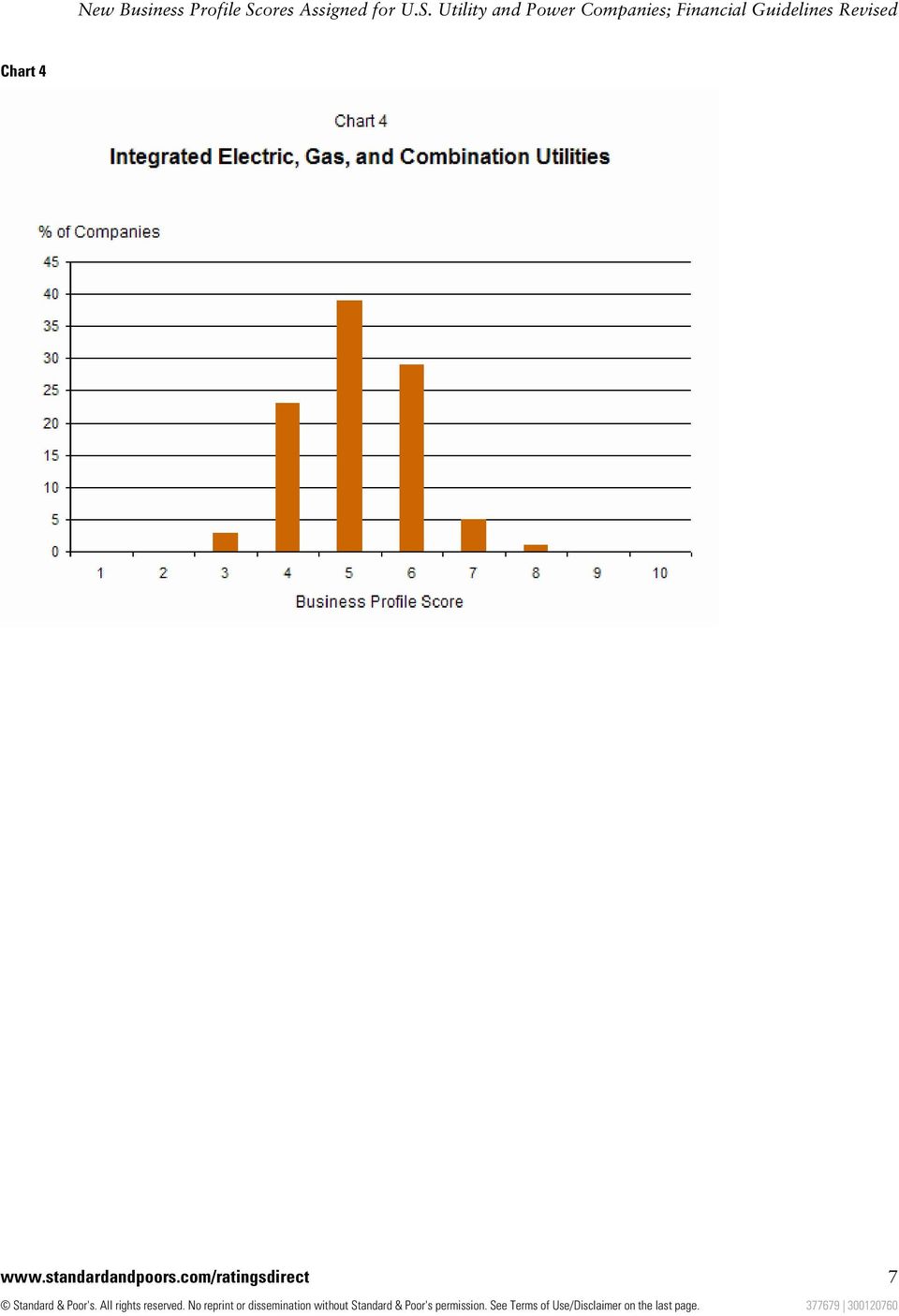

5 The record of execution of stated business strategies; Accuracy of projected performance versus actual results, as well as the trend; Assessment of management's financial policies and attitude toward credit; and Corporate governance practices. Charts 2 through 6 show business profile scores broken out by industry sub-sector. The five industry sub-sectors are: Transmission and distribution--water, gas, and electric; Transmission only--electric, gas, and other; Integrated electric, gas, and combination utilities; Diversified energy and diversified nonenergy; and Energy merchant/power developer/trading and marketing companies. Chart 2 5

6 Chart 3 Standard & Poor s RatingsDirect June 2,

7 Chart 4 7

8 Chart 5 Standard & Poor s RatingsDirect June 2,

9 Chart 6 The average business profile scores for transmission and distribution companies and transmission-only companies are lower on the scale than the previous averages, while the average business profile scores for integrated utilities, diversified energy, and energy merchants and developers are higher. The Appendix provides the company list of business profile scores segmented by industry sub-sector and ranked in order of credit rating, outlook, business profile score, and relative strength. Business Profile Score Methodology Standard & Poor's methodology of determining corporate utility business risk is anchored in the assessment of certain specific characteristics that define the sector. We assign business profile scores to each of the rated companies in the utility and power sector on a 10-point scale, where '1' represents the lowest risk and '10' the highest risk. Business profile scores are assigned to all rated utility and power companies, whether they are holding companies, subsidiaries or stand-alone corporations. For operating subsidiaries and stand-alone companies, the score is a bottom-up assessment. Scores for families of companies are a composite of the operating subsidiaries' scores. The actual credit rating of a company is analyzed, in part, by comparing the business profile score with the risk-adjusted financial guidelines. For most companies, business profile scores are assessed using five categories; specifically, regulation, markets, operations, competitiveness, and management. The emphasis placed on each category may be influenced by the dominant strategy of the company or other factors. For example, for a regulated transmission and distribution 9

10 company, regulation may account for 30% to 40% of the business profile score because regulation can be the single-most important credit driver for this type of company. Conversely, competition, which may not exist for a transmission and distribution company, would provide a much lower proportion (e.g., 5% to 15%) of the business profile score. For certain types of companies, such as power generators, power developers, oil and gas exploration and production companies, or nonenergy-related holdings, where these five components may not be appropriate, Standard & Poor's will use other, more appropriate methodologies. Some of these companies are assigned business profile scores that are useful only for relative ranking purposes. As noted above, the business profile score for a parent or holding company is a composite of the business profile scores of its individual subsidiary companies. Again, Standard & Poor's does not apply rigid guidelines for determining the proportion or weighting that each subsidiary represents in the overall business profile score. Instead, it is determined based on a number of factors. Standard & Poor's will analyze each subsidiary's contribution to FFO, forecast capital expenditures, liquidity requirements, and other parameters, including the extent to which one subsidiary has higher growth. The weighting is determined case-by-case. Appendix: U.S. Utility and Power Company Ranking List U.S. Utility and Power Company Ranking List Company Corporate Credit Rating Business Profile 1. Regulated Transmission and Distribution - Electric, Gas, and Water Baton Rouge Water Works Co. (The) AA/Stable/-- 1 Nicor Gas Co. AA/Stable/A-1+ 2 Nicor Inc. AA/Stable/A-1+ 3 Washington Gas Light Co. AA-/Stable/A-1+ 2 WGL Holdings Inc. AA-/Stable/A-1+ 3 New Jersey Natural Gas Co. A+/Stable/A-1 1 Aqua Pennsylvania A+/Stable/-- 2 KeySpan Energy Delivery Long Island A+/Negative/-- 1 KeySpan Energy Delivery New York A+/Negative/-- 1 Elizabethtown Water Co. A+/Negative/-- 2 California Water Service Co. A+/Negative/-- 3 Questar Gas Co. A+/Negative/-- 3 Southern California Gas Co. A/Stable/A-1 1 Boston Edison Co. A/Stable/A-1 1 Commonwealth Electric Co. A/Stable/-- 1 Cambridge Electric Light Co. A/Stable/-- 1 NSTAR A/Stable/A-1 1 Massachusetts Electric Co. A/Stable/A-1 1 Narragansett Electric Co. A/Stable/A-1 1 Northwest Natural Gas Co. A/Stable/A-1 1 Connecticut Water Service Inc. A/Stable/ -- 2 Connecticut Water Co. (The) A/Stable/ -- 2 Standard & Poor s RatingsDirect June 2,

11 U.S. Utility and Power Company Ranking List (cont.) Aquarion Co. A/Stable/-- 2 Aquarion Water Co. of Connecticut A/Stable/-- 2 NSTAR Gas Co. A/Stable/-- 2 Piedmont Natural Gas Co. Inc. A/Stable/A-1 2 National Grid USA A/Stable/A-1 2 Consolidated Edison Co. of New York Inc. A/Stable/A-1 2 Orange and Rockland Utilities Inc. A/Stable/A-1 2 Rockland Electric Co. A/Stable/-- 2 Consolidated Edison Inc. A/Stable/A-1 2 Laclede Gas Co. A/Stable/A-1 3 Laclede Group Inc. A/Stable/-- 3 Atlantic City Sewerage Co. A/Stable/-- 3 Niagara Mohawk Power Corp. A/Stable/-- 3 Central Hudson Gas & Electric Co. A/Stable/-- 3 American Water Capital Corp. A/Negative/ 2 Boston Gas Co. A/Negative/-- 2 Colonial Gas Co. A/Negative/-- 2 Middlesex Water Co. A/Negative/-- 3 York Water Co. (The) A-/Stable/-- 2 Alabama Gas Corp. A-/Stable/-- 2 Atlanta Gas Light Co. A-/Stable/-- 2 Public Service Co. of North Carolina Inc. A-/Stable/A-2 2 Wisconsin Gas Co. A-/Stable/A-2 2 North Shore Gas Co. A-/Stable/A-2 2 Peoples Gas Light & Coke Co. A-/Stable/A-2 2 ONEOK Inc. A-/Stable/A-2 6 Indiana Gas Co. Inc. A-/Negative/-- 1 Southern California Water Co. A-/Negative/-- 3 American States Water Co. A-/Negative/-- 3 United Water New Jersey A-/Negative/-- 4 United Waterworks A-/Negative/-- 4 PPL Electric Utilities Corp. A-/Negative/-- 4 Commonwealth Edison Co. A-/Negative/A-2 4 PECO Energy Co. A-/Negative/A-2 4 Central Illinois Public Service Co. A-/CW-Neg/-- 3 Western Massachusetts Electric Co. BBB+/Stable/-- 1 Cascade Natural Gas Corp. BBB+/Stable/-- 2 South Jersey Gas Co. BBB+/Stable/-- 2 Baltimore Gas & Electric Co. BBB+/Stable/A-2 3 Connecticut Natural Gas Corp. BBB+/Negative/-- 3 Southern Connecticut Gas Co. BBB+/Negative/-- 3 Central Maine Power Co. BBB+/Negative/-- 3 Atlantic City Electric Co. BBB+/Negative/A

12 U.S. Utility and Power Company Ranking List (cont.) Potomac Electric Power Co. BBB+/Negative/A-2 3 Delmarva Power & Light Co. BBB+/Negative/A-2 3 Yankee Gas Services Co. BBB+/Negative/-- 3 Connecticut Light & Power Co. BBB+/Negative/-- 3 UGI Utilities Inc. BBB+/Negative/-- 4 Bay State Gas Co. BBB/Stable/-- 2 AEP Texas Central Co. BBB/Stable/-- 2 AEP Texas North Co. BBB/Stable/-- 2 Southwest Gas Corp. BBB-/Stable/-- 3 Columbus Southern Power Co. BBB/Stable/-- 3 Ohio Power Co. BBB/Stable/-- 3 Public Service Electric & Gas Co. BBB/Stable/A-2 3 Oncor Electric Delivery Co. BBB/Negative/-- 2 Southern Union Co. BBB/Negative/-- 3 Centerpoint Energy Houston Electric LLC BBB/Negative/-- 3 CenterPoint Energy Resources Corp. BBB/Negative/-- 3 Duquesne Light Co. BBB/Negative/ 4 Duquesne Light Holdings Inc. BBB/Negative/ -- 5 TXU Gas Co. BBB/CW-Dev/-- 3 Jersey Central Power & Light Co. BBB-/Stable/-- 4 Metropolitan Edison Co. BBB-/Stable/-- 4 Pennsylvania Electric Co. BBB-/Stable/-- 4 Texas-New Mexico Power Co. BB+/Stable/-- 4 AmeriGas Partners L.P. BB+/Stable/-- 7 NUI Utilities Inc. BB/CW-Dev/-- 4 Suburban Propane Partners L.P. BB-/Stable/-- 8 Star Gas Partners L.P. BB-/Stable/-- 8 SEMCO Energy Inc. BB-/Negative/-- 5 Ferrellgas Partners L.P. BB-/Negative/-- 8 Potomac Edison Co. B/Stable/-- 3 West Penn Power Co. B/Stable/-- 3 Illinova Corp. B/Negative/-- 7 NorthWestern Corp. D/NM/ Transmission Only - Electric, Gas, and Other Questar Pipeline Co. A+/Negative/-- 3 Mid-West Independent Transmission System Operator Inc. A/Stable/-- 1 American Transmission Co. A/Stable/A-1 1 New England Power Co. A/Stable/A-1 1 Colonial Pipeline Co. A/Stable/A-1 3 Dixie Pipeline Co. --/--/A-1 3 Plantation Pipeline Co. --/--/A-1 3 Explorer Pipeline Co. A/Stable/A-1 4 Standard & Poor s RatingsDirect June 2,

13 U.S. Utility and Power Company Ranking List (cont.) Northern Natural Gas Co. A-/Positive/-- 2 Buckeye Partners L.P. A-/Stable/-- 4 Kern River Gas Transmission Co. A-/Negative/-- 3 Northern Border Pipeline Co. A-/CW-Neg/-- 2 Texas Gas Transmission LLC BBB+/Stable/-- 3 Iroquois Gas Transmission System L.P. BBB+/Stable/-- 3 Florida Gas Transmission Co. BBB/Stable/-- 2 International Transmission Co. BBB/Stable 2 ITC Holding Corp. BBB/Stable 2 Texas Eastern Transmission L.P. BBB/Stable/-- 3 PanEnergy Corp. BBB/Stable/-- 3 TE Products Pipeline Co. L.P. BBB/Stable/-- 4 TEPPCO Partners L.P. BBB/Stable/-- 4 Panhandle Eastern Pipeline LLC BBB/Negative/-- 3 Noark Pipeline Finance LLC BBB/Negative/-- 4 Southern Star Central Gas Pipeline Inc. BB/Stable/-- 3 Transwestern Pipeline Co. BB/CW-Dev/-- 4 Transcontinental Gas Pipe Line Corp. B+/Negative/-- 2 Northwest Pipeline Corp. B+/Negative/-- 2 Colorado Interstate Gas Co. B-/Negative/-- 2 Southern Natural Gas Co. B-/Negative/-- 2 ANR Pipeline Co. B-/Negative/-- 3 Tennessee Gas Pipeline Co. B-/Negative/-- 3 El Paso Tennessee Pipeline Co. B-/Negative/-- 3 El Paso Natural Gas Co. B-/Negative/-- 4 Gas Transmission-Northwest Corp. CC/CW-Pos/ Integrated Electric, Gas, and Combination Utilities Wisconsin Public Service Corp. AA-/Stable/A-1+ 4 Madison Gas & Electric Co. AA/Negative/A-1+ 4 Southern Co. A/Stable/A-1 4 Georgia Power Co. A/Stable/A-1 4 Alabama Power Co. A/Stable/A-1 4 Mississippi Power Co. A/Stable/A-1 4 Gulf Power Co. A/Stable/-- 4 Savannah Electric & Power Co. A/Stable/-- 4 San Diego Gas & Electric Co. A/Stable/A-1 5 MidAmerican Energy Co. A/Stable/A-1 5 Questar Corp. --/--/A-1 6 Equitable Resources Inc. A/Stable/A-1 6 Florida Power & Light Co. A/Negative/A-1 4 South Carolina Electric & Gas Co. A-/Stable/A-2 4 SCANA Corp. A-/Stable/

14 U.S. Utility and Power Company Ranking List (cont.) Wisconsin Electric Power Co. A-/Stable/A-2 4 AGL Resources Inc. A-/Stable/A-2 4 Virginia Electric & Power Co. (Dominion Virginia) A-/Stable/A-2 5 Idaho Power Co. A-/Stable/A-2 5 IDACORP Inc. A-/Stable/A-2 5 Energen Corp. A-/Stable/-- 6 Vectren Utility Holdings Inc. A-/Negative/A-2 3 Wisconsin Power & Light Co. A-/Negative/A-2 4 Atmos Energy Corp. A-/Negative/A-2 4 Southern Indiana Gas & Electric Co. A-/Negative/-- 5 Montana-Dakota Utilities Co. A-/Negative/-- 5 PacifiCorp A-/Negative/A-2 5 Northern Border Partners L.P. A-/CW-Neg/-- 4 Central Illinois Light Co. A-/CW-Neg/-- 5 CILCORP A-/CW-Neg/-- 5 Union Electric Co. A-/CW-Neg/A-2 5 Ameren Corp. A-/CW-Neg/A-2 5 Cincinnati Gas & Electric Co. BBB+/Stable/A2-4 Oklahoma Gas & Electric Co. BBB+/Stable/A-2 4 Northern States Power Wisconsin BBB+/Stable /A-2 5 Kentucky Utilities Co. BBB+/Stable/A-2 5 Louisville Gas & Electric Co. BBB+/Stable/A-2 5 Allete Inc. BBB+/Stable/A-2 5 Wisconsin Energy Corp. BBB+/Stable/A-2 5 PSI Energy Inc. BBB+/Stable/A-2 5 Union Light Heat & Power Co. BBB+/Stable/-- 5 Hawaiian Electric Co. Inc. BBB+/Stable/A-2 6 Enogex Inc. BBB+/Stable/-- 6 National Fuel Gas Co. BBB+/Stable/A-2 7 Energy East Corp. BBB+/Negative/--A2 3 RGS Energy Group Inc. BBB+/Negative/-- 4 Rochester Gas & Electric Corp. BBB+/Negative/-- 4 Michigan Consolidated Gas Co. BBB+/Negative/A-2 4 Interstate Power & Light Co. BBB+/Negative/A-2 5 Public Service Co. of New Hampshire BBB+/Negative/-- 5 Kaneb Pipe Line Operating Partnership L.P. BBB+/Negative/-- 5 Consolidated Natural Gas Co. BBB+/Negative/A-2 6 Detroit Edison Co. BBB+/Negative/A-2 6 Questar Market Resources Inc. BBB+/Negative/-- 8 Portland General Electric Co. BBB+/CW-Neg./A-2 5 Columbia Energy Group BBB/Stable/-- 3 NiSource Inc. BBB/Stable/-- 4 Xcel Energy Inc. BBB/Stable/A-2 5 Standard & Poor s RatingsDirect June 2,

15 U.S. Utility and Power Company Ranking List (cont.) Public Service Co. of Colorado BBB/Stable /A-2 5 Northern States Power Co. BBB/Stable /A-2 5 Southwestern Public Service Co. BBB/Stable /A-2 5 Appalachian Power Co. BBB/Stable/-- 5 Kentucky Power Co. BBB/Stable/-- 5 Public Service Co. of Oklahoma BBB/Stable/-- 5 Southwestern Electric Power Co. BBB/Stable/-- 5 Northern Indiana Public Service Co. BBB/Stable/-- 5 Entergy Arkansas Inc. BBB/Stable/-- 5 Entergy Louisiana Inc. BBB/Stable/-- 5 Progress Energy Florida BBB/Stable/-- 5 Progress Energy Carolinas Inc. BBB/Stable/A-2 5 Kansas City Power & Light Co. BBB/Stable/A-2 6 PNM Resources Inc. BBB/Stable/-- 6 Southern California Edison Co. BBB/Stable/A-2 6 Empire District Electric Co. BBB/Stable/A-2 6 Entergy Mississippi Inc. BBB/Stable/-- 6 Entergy New Orleans Inc. BBB/Stable/-- 6 Duke Energy Field Services LLC BBB/Stable/A-2 6 Arizona Public Service Co. BBB/Negative/A-2 5 TXU U.S. Holdings Co. BBB/Negative/-- 5 Pinnacle West Capital Corp. BBB/Negative/A-2 6 Cleco Power LLC BBB/Negative/A-3 6 Puget Sound Energy Inc. BBB-/Positive/A-3 5 Puget Energy Inc. BBB-/Positive/-- 5 Green Mountain Power Corp. BBB-/Stable/-- 5 Public Service Co. of New Mexico BBB-/Stable/A-2 6 Pacific Gas & Electric Co. BBB-/Stable/ -- 6 Cleveland Electric Illuminating Co. BBB-/Stable/-- 6 Ohio Edison Co. BBB-/Stable/-- 6 Toledo Edison Co. BBB-/Stable/-- 6 Pennsylvania Power Co. BBB-/Stable/-- 6 El Paso Electric Co. BBB-/Stable/-- 6 Central Vermont Public Service Corp. BBB-/Stable/-- 6 Entergy Gulf States Inc. BBB-/Stable/-- 6 System Energy Resources Inc. BBB-/Stable/-- 7 Tampa Electric Co. BBB-/Negative/A-3 4 Black Hills Power Inc. BBB-/Negative/-- 6 Westar Energy Inc. BB+/Positive/-- 5 Kansas Gas & Electric Co. BB+/Positive/-- 6 Indianapolis Power & Light Co. BB+/Stable/-- 4 IPALCO Enterprises Inc. BB+/Stable/-- 4 Enterprise Products Operating L.P. BB+/Stable/

16 U.S. Utility and Power Company Ranking List (cont.) Enterprise Products Partners L.P. BB+/Stable/-- 6 GulfTerra Energy Partners L.P. BB+/CW-Neg/-- 6 Consumers Energy Co. BB/Negative/-- 6 Tucson Electric Power Co. BB/CW-Neg/-- 6 Dayton Power & Light Co. BB-/CW-Neg/ - 7 Monongahela Power Co. B/Stable/-- 5 Nevada Power Co. B+/Negative/-- 7 Sierra Pacific Power Co. B+/Negative/-- 7 Sierra Pacific Resources B+/Negative/ Diversified Energy and Diversified Non-Energy WPS Resources Corp. A/Stable/A-1 5 KeySpan Corp. A/Negative/A-1 4 FPL Group Inc. A/Negative/-- 6 Peoples Energy Corp. A-/Stable/A-2 5 Vectren Corp. A-/Negative/-- 4 PacifiCorp Holdings Inc. A-/Negative/-- 5 Exelon Corp. A-/Negative/A-2 7 MDU Resources Group Inc. A-/Negative/A-2 7 Centennial Energy Holdings Inc. A-/Negative/A-2 8 Otter Tail Corp. A-/Negative/-- 8 Kinder Morgan Energy Partners L.P. BBB+/Stable/A-2 4 Northeast Utilities BBB+/Stable/-- 5 OGE Energy Corp. BBB+/Stable/A-2 6 LG&E Energy Corp. BBB+/Stable/-- 6 Cinergy Corp. BBB+/Stable/A-2 6 Constellation Energy Group Inc. BBB+/Stable/A-2 7 Sempra Energy BBB+/Stable/A-2 7 Pepco Holdings Inc. BBB+/Negative/A-2 5 Conectiv BBB+/Negative/-- 5 Alliant Energy Corp. BBB+/Negative/A-2 6 DTE Energy Co. BBB+/Negative/A-2 6 Dominion Resources Inc. BBB+/Negative/A-2 7 Kinder Morgan Inc. BBB/Stable/A-2 5 American Electric Power Co. Inc. BBB/Stable/A-2 6 Entergy Corp. BBB/Stable/-- 6 Hawaiian Electric Industries Inc. BBB/Stable/A-2 6 Progress Energy Inc. BBB/Stable/A-2 6 PPL Corp. BBB/Stable/-- 7 Public Service Enterprise Group Inc. BBB/Stable/A-2 7 Great Plains Energy Inc. BBB/Stable/-- 7 Duke Energy Corp. BBB/Stable/A-2 7 Duke Capital Corp. BBB/Stable/A-2 8 Standard & Poor s RatingsDirect June 2,

17 U.S. Utility and Power Company Ranking List (cont.) TXU Corp. BBB/Negative/-- 5 Centerpoint Energy Inc. BBB/Negative/-- 5 Cleco Corp. BBB/Negative/A-3 6 Potomac Capital Investment Corp. BBB/Negative/-- 8 MidAmerican Energy Holdings Co. BBB-/Positive/-- 5 FirstEnergy Corp. BBB-/Stable/-- 6 TECO Energy Inc. BBB-/Negative/A-3 5 Black Hills Corp. BBB-/Negative/-- 8 Avista Corp. BB+/Stable/-- 6 Edison International BB+/Stable/-- 6 TNP Enterprises BB+/Stable/-- 6 New York Water Service Corp. BB/Stable 7 CMS Energy Corp. BB/Negative/-- 7 DPL Inc. BB- /CW-Neg/-- 8 Williams Companies Inc. (The) B+/Negative/-- 8 Allegheny Energy Inc. B/Stable/-- 7 Dynegy Inc. B/Negative/-- 8 Dynegy Holdings Inc. B/Negative/-- 9 El Paso CGP Corp. B-/Negative/-- 6 Aquila Inc. B-/Negative/-- 8 El Paso Corp. B-/Negative/ Energy Merchants/Power Developers/Trading and Marketing Entergy-Koch L.P. A/Stable/-- 9 KeySpan Generation LLC A/Negative/-- 5 FPL Group Capital A/Negative/A-1 8 Exelon Generation Co. A-/Negative/A-2 8 AmerenEnergy Generating Co. A-/CW-Neg/-- 8 Southern Power Co. BBB+/Stable/-- 6 LG&E Capital Corp. BBB+/Stable/A-2 9 Alliant Energy Resources Inc. BBB+/Negative/-- 9 American Ref-Fuel Co. LLC BBB/Stable/-- 6 PSEG Power LLC BBB/Stable/-- 8 PPL Energy Supply LLC BBB/Stable/-- 8 TXU Energy Co. LLC BBB/Negative/-- 7 Duke Energy Trading and Marketing LLC BBB-/Negative/-- 10 Northeast Generation Company BB+/Negative/-- 9 Cogentrix Energy BB-/Stable/-- 6 PSEG Energy Holdings Inc. BB-/Stable/-- 9 AES Corp. B+/Stable/-- 9 NRG Energy Inc. B+/Stable 9 Allegheny Energy Supply Co. LLC B/Stable/-- 8 Reliant Resources Inc. B/Negative/

B+/Negative/-- 8 Allegheny Energy Inc. B/Stable/-- 7 Dynegy Inc. B/Negative/-- 8 Dynegy Holdings Inc. B/Negative/-- 9 El Paso CGP Corp.")

18 U.S. Utility and Power Company Ranking List (cont.) Calpine Corp B/Negative/-- 9 Edison Mission Energy B/Negative/-- 9 Orion Power Holdings Inc B/Negative/-- 9 Reliant Energy Mid-Atlantic Power Holdings LLC B/Negative/-- 9 Mirant Americas Generation Inc. D/--/-- 10 Mirant Americas Energy Marketing L.P. D/--/-- 10 Mirant Corp. D/--/-- 10 NEGT Energy Trading Holdings Corp D/--/-- 10 PG&E National Energy Group D/--/-- 10 USGen New England Inc. D/--/-- 10 Standard & Poor s RatingsDirect June 2,

19 Copyright 2007, Standard & Poor's, a division of The McGraw-Hill Companies, Inc. (S&P). S&P and/or its third party licensors have exclusive proprietary rights in the data or information provided herein. This data/information may only be used internally for business purposes and shall not be used for any unlawful or unauthorized purposes. Dissemination, distribution or reproduction of this data/information in any form is strictly prohibited except with the prior written permission of S&P. Because of the possibility of human or mechanical error by S&P, its affiliates or its third party licensors, S&P, its affiliates and its third party licensors do not guarantee the accuracy, adequacy, completeness or availability of any information and is not responsible for any errors or omissions or for the results obtained from the use of such information. S&P GIVES NO EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. In no event shall S&P, its affiliates and its third party licensors be liable for any direct, indirect, special or consequential damages in connection with subscribers or others use of the data/information contained herein. Access to the data or information contained herein is subject to termination in the event any agreement with a thirdparty of information or software is terminated. Analytic services provided by Standard & Poor's Ratings Services (Ratings Services) are the result of separate activities designed to preserve the independence and objectivity of ratings opinions. The credit ratings and observations contained herein are solely statements of opinion and not statements of fact or recommendations to purchase, hold, or sell any securities or make any other investment decisions. Accordingly, any user of the information contained herein should not rely on any credit rating or other opinion contained herein in making any investment decision. Ratings are based on information received by Ratings Services. Other divisions of Standard & Poor's may have information that is not available to Ratings Services. Standard & Poor's has established policies and procedures to maintain the confidentiality of non-public information received during the ratings process. Ratings Services receives compensation for its ratings. Such compensation is normally paid either by the issuers of such securities or third parties participating in marketing the securities. While Standard & Poor's reserves the right to disseminate the rating, it receives no payment for doing so, except for subscriptions to its publications. Additional information about our ratings fees is available at Any Passwords/user IDs issued by S&P to users are single user-dedicated and may ONLY be used by the individual to whom they have been assigned. No sharing of passwords/user IDs and no simultaneous access via the same password/user ID is permitted. To reprint, translate, or use the data or information other than as provided herein, contact Client Services, 55 Water Street, New York, NY 10041; (1) or by to: research_request@standardandpoors.com. Copyright Standard & Poor's, a division of The McGraw-Hill Companies. All Rights Reserved

J.D. Power Reports: Electric Utilities Achieve Highest Level of Business Customer Satisfaction since 2009

w J.D. Power Reports: Electric Utilities Achieve Highest Level of Business Customer Satisfaction since 2009 Satisfaction Improves for More than 80 Percent of Utilities for Second Consecutive Year WESTLAKE

w J.D. Power Reports: Electric Utilities Achieve Highest Level of Business Customer Satisfaction since 2009 Satisfaction Improves for More than 80 Percent of Utilities for Second Consecutive Year WESTLAKE

Investor-Owned Utility Ratio Comparisons

Investor-Owned Utility Ratio Comparisons 2002 Data Published March 2004 2301 M Street NW Washington, D.C. 20037-1484 202/467-2900 Investor-Owned Utility Ratio Comparisons, 2002 Data APPA provides several

Investor-Owned Utility Ratio Comparisons 2002 Data Published March 2004 2301 M Street NW Washington, D.C. 20037-1484 202/467-2900 Investor-Owned Utility Ratio Comparisons, 2002 Data APPA provides several

J.D. Power Reports: Communicating with Customers and Higher Price Satisfaction Increase Overall Satisfaction for Residential Electric Utilities

w J.D. Power Reports: Communicating with Customers and Higher Price Satisfaction Increase Overall Satisfaction for Residential Electric Utilities Proactive Communication during Power Outages Remains a

w J.D. Power Reports: Communicating with Customers and Higher Price Satisfaction Increase Overall Satisfaction for Residential Electric Utilities Proactive Communication during Power Outages Remains a

National Price Rankings

National Price Rankings The links below provide the latest available electric service price data from a July 1, 2010 survey of more than 150 investor-owned utilities. Data source: Edison Electric Institute.

National Price Rankings The links below provide the latest available electric service price data from a July 1, 2010 survey of more than 150 investor-owned utilities. Data source: Edison Electric Institute.

The Williams Capital Group, L.P. Presentation to National Association of Regulatory Utility Commissioners Summer Committee Meetings.

Presentation to National Association of Regulatory Utility Commissioners Summer Committee Meetings July 18, 2010 WCG Co Manager relationships with Power and Gas utilities Fixed Income Underwriting (Lead

Presentation to National Association of Regulatory Utility Commissioners Summer Committee Meetings July 18, 2010 WCG Co Manager relationships with Power and Gas utilities Fixed Income Underwriting (Lead

UNITED STATES OF AMERICA FEDERAL ENERGY REGULATORY COMMISSION NOTICE. March 9, 2006

UNITED STATES OF AMERICA FEDERAL ENERGY REGULATORY COMMISSION NOTICE March 9, 2006 The following notice of meeting is published pursuant to section 3(a) of the government in the Sunshine Act (PUB. L. No.

UNITED STATES OF AMERICA FEDERAL ENERGY REGULATORY COMMISSION NOTICE March 9, 2006 The following notice of meeting is published pursuant to section 3(a) of the government in the Sunshine Act (PUB. L. No.

Management Salaries in Local Publicly Owned Electric Utilities

2014 Survey of Management Salaries in Local Publicly Owned Electric Utilities 1875 Connecticut Avenue, NW Washington, D.C. 20009-5715 202/467-2900 www.publicpower.org Survey of Management Salaries In Local

2014 Survey of Management Salaries in Local Publicly Owned Electric Utilities 1875 Connecticut Avenue, NW Washington, D.C. 20009-5715 202/467-2900 www.publicpower.org Survey of Management Salaries In Local

Research Update: ArcelorMittal 'BBB+' Ratings Placed On CreditWatch Negative On Weak Operating Results

April 29, 2009 Research Update: ArcelorMittal 'BBB+' Ratings Placed On CreditWatch Negative On Weak Operating Results Primary Credit Analyst: Alex Herbert, London (44) 20-7176-3616;alex_herbert@standardandpoors.com

April 29, 2009 Research Update: ArcelorMittal 'BBB+' Ratings Placed On CreditWatch Negative On Weak Operating Results Primary Credit Analyst: Alex Herbert, London (44) 20-7176-3616;alex_herbert@standardandpoors.com

Research Update: Russian Steel Pipe Maker OAO TMK Outlook Revised To Negative; National Scale Rating Cut To 'rua'

March 2, 2009 Research Update: Russian Steel Pipe Maker OAO TMK Outlook Revised To Negative; National Scale Rating Cut Primary Credit Analyst: Andrey Nikolaev, CFA, Moscow (7) 495-783-4131;andrey_nikolaev@standardandpoors.com

March 2, 2009 Research Update: Russian Steel Pipe Maker OAO TMK Outlook Revised To Negative; National Scale Rating Cut Primary Credit Analyst: Andrey Nikolaev, CFA, Moscow (7) 495-783-4131;andrey_nikolaev@standardandpoors.com

Research Update: Swiss Republic and Canton of Geneva Upgraded To 'A+' On Debt Reduction; Outlook Stable

December 11, 2008 Research Update: Swiss Republic and Canton of Geneva Upgraded To 'A+' On Debt Reduction; Outlook Stable Primary Credit Analyst: Bertrand de Dianous, Paris (33) 1-4420-7371;bertrand_de_dianous@standardandpoors.com

December 11, 2008 Research Update: Swiss Republic and Canton of Geneva Upgraded To 'A+' On Debt Reduction; Outlook Stable Primary Credit Analyst: Bertrand de Dianous, Paris (33) 1-4420-7371;bertrand_de_dianous@standardandpoors.com

Program Update. Sally Rand, EPA May 6, 2014

Program Update Sally Rand, EPA May 6, 2014 SF 6 Emission Reduction Partnership for Electric Power Systems Since 1999, members of the U.S. electric power industry and the U.S. Environmental Protection Agency

Program Update Sally Rand, EPA May 6, 2014 SF 6 Emission Reduction Partnership for Electric Power Systems Since 1999, members of the U.S. electric power industry and the U.S. Environmental Protection Agency

Business Segmentation

Business Segmentation Q4 2010 FINANCIAL UPDATE QUARTERLY REPORT OF THE U.S. SHAREHOLDER-OWNED ELECTRIC UTILITY INDUSTRY About EEI The Edison Electric Institute is the association of U.S. shareholderowned

Business Segmentation Q4 2010 FINANCIAL UPDATE QUARTERLY REPORT OF THE U.S. SHAREHOLDER-OWNED ELECTRIC UTILITY INDUSTRY About EEI The Edison Electric Institute is the association of U.S. shareholderowned

Progress Report: Integrating Enterprise Risk Management Analysis Into Corporate Credit Ratings

July 22, 2009 Progress Report: Integrating Enterprise Risk Management Analysis Into Corporate Credit Ratings Corporate & Gov't Ratings: Steven J Dreyer, Managing Director, New York (1) 212-438-7187; steven_dreyer@standardandpoors.com

July 22, 2009 Progress Report: Integrating Enterprise Risk Management Analysis Into Corporate Credit Ratings Corporate & Gov't Ratings: Steven J Dreyer, Managing Director, New York (1) 212-438-7187; steven_dreyer@standardandpoors.com

Research Update: Nykredit Realkredit A/S Assigned 'A+' L-T Ratings, Outlook Stable; Covered Bonds Rated 'AAA'

November 5, 2008 Research Update: Nykredit Realkredit A/S Assigned 'A+' L-T Ratings, Outlook Stable; Covered Bonds Rated 'AAA' Primary Credit Analyst: Miguel Pintado, Stockholm (46) 8-440-5904;miguel_pintado@standardandpoors.com

November 5, 2008 Research Update: Nykredit Realkredit A/S Assigned 'A+' L-T Ratings, Outlook Stable; Covered Bonds Rated 'AAA' Primary Credit Analyst: Miguel Pintado, Stockholm (46) 8-440-5904;miguel_pintado@standardandpoors.com

Public School Teacher Experience Distribution. Public School Teacher Experience Distribution

Public School Teacher Experience Distribution Lower Quartile Median Upper Quartile Mode Alabama Percent of Teachers FY Public School Teacher Experience Distribution Lower Quartile Median Upper Quartile

Public School Teacher Experience Distribution Lower Quartile Median Upper Quartile Mode Alabama Percent of Teachers FY Public School Teacher Experience Distribution Lower Quartile Median Upper Quartile

Regulatory Trends and the Status of Deregulation in the Natural Gas Business

Regulatory Trends and the Status of Deregulation in the Natural Gas Business ESC Technology and Market Assessment Forum Chicago, Illinois October 27, 2011 Cynthia J. Marple Director, Rates and Regulatory

Regulatory Trends and the Status of Deregulation in the Natural Gas Business ESC Technology and Market Assessment Forum Chicago, Illinois October 27, 2011 Cynthia J. Marple Director, Rates and Regulatory

Winners and Losers in Restructuring: Assessing Electric and Gas Company Financial Performance

Winners and Losers in Restructuring: Assessing Electric and Gas Company Financial Performance James Coyne and Prescott Hartshorne 1 Lexecon, Cambridge, MA Introduction The era of electric and natural gas

Winners and Losers in Restructuring: Assessing Electric and Gas Company Financial Performance James Coyne and Prescott Hartshorne 1 Lexecon, Cambridge, MA Introduction The era of electric and natural gas

I. TRANSMISSION OWNERS

I. TRANSMISSION OWNERS 1. ALLETE, Inc. (for its operating division Minnesota Power, Inc., and its wholly-owned subsidiary, Superior Water, Light and Power Company) 2. Ameren Illinois Company 3. Ameren

I. TRANSMISSION OWNERS 1. ALLETE, Inc. (for its operating division Minnesota Power, Inc., and its wholly-owned subsidiary, Superior Water, Light and Power Company) 2. Ameren Illinois Company 3. Ameren

Research Update: Swedish Public Housing Group Forvaltnings AB Framtiden Rated 'A+/A-1' On Importance To Goteborg; Outlook Stable

September 9, 2009 Research Update: Swedish Public Housing Group Forvaltnings AB Framtiden Rated 'A+/A-1' On Importance To Primary Credit Analyst: Carl Nyrerod, Stockholm (46) 8-440-5919;carl_nyrerod@standardandpoors.com

September 9, 2009 Research Update: Swedish Public Housing Group Forvaltnings AB Framtiden Rated 'A+/A-1' On Importance To Primary Credit Analyst: Carl Nyrerod, Stockholm (46) 8-440-5919;carl_nyrerod@standardandpoors.com

Chex Systems, Inc. does not currently charge a fee to place, lift or remove a freeze; however, we reserve the right to apply the following fees:

Chex Systems, Inc. does not currently charge a fee to place, lift or remove a freeze; however, we reserve the right to apply the following fees: Security Freeze Table AA, AP and AE Military addresses*

Chex Systems, Inc. does not currently charge a fee to place, lift or remove a freeze; however, we reserve the right to apply the following fees: Security Freeze Table AA, AP and AE Military addresses*

Utility Capital Expenditures

Utility Capital Expenditures Jean Reaves Rollins UPMG--Atlanta October 2007 Your Boss Is Wrong You Are In Fact Doing Twice the Work 750,000 Total Investor-Owned Utility Employment 1998-2006 (C Three Analysis)

Utility Capital Expenditures Jean Reaves Rollins UPMG--Atlanta October 2007 Your Boss Is Wrong You Are In Fact Doing Twice the Work 750,000 Total Investor-Owned Utility Employment 1998-2006 (C Three Analysis)

Criteria Financial Institutions Other: Rating Asset Management Companies

March 18, 2004 Criteria Financial Institutions Other: Rating Asset Management Companies Table Of Contents Competitive Position Financial Management Operations www.standardandpoors.com/ratingsdirect 1 Standard

March 18, 2004 Criteria Financial Institutions Other: Rating Asset Management Companies Table Of Contents Competitive Position Financial Management Operations www.standardandpoors.com/ratingsdirect 1 Standard

Significant Mark-To-Market Losses On Credit Derivatives Not Expected To Affect Bond Insurer Ratings

October 31, 2007 Significant Mark-To-Market Losses On Credit Derivatives Not Expected To Affect Bond Insurer Ratings Primary Credit Analyst: Dick P Smith, New York (1) 212-438-2095; dick_smith@standardandpoors.com

October 31, 2007 Significant Mark-To-Market Losses On Credit Derivatives Not Expected To Affect Bond Insurer Ratings Primary Credit Analyst: Dick P Smith, New York (1) 212-438-2095; dick_smith@standardandpoors.com

Brubaker & Associates, Inc. Testimony Filed Since 1999 by Michael Gorman on Cost of Capital Issues

7/24/2009 9134 PACIFICORP, dba PACIFIC POWER Reply OR UE-210 Return on Common Equity Rate of Return The Industrial and The Citizens' Utility Board of Oregon 7/17/2009 9123 INTERSTATE POWER AND LIGHT Direct

7/24/2009 9134 PACIFICORP, dba PACIFIC POWER Reply OR UE-210 Return on Common Equity Rate of Return The Industrial and The Citizens' Utility Board of Oregon 7/17/2009 9123 INTERSTATE POWER AND LIGHT Direct

Operating Pipeline Companies Ohio Valley & Southern States Region by State & Pipeline Company

Operating Pipeline Companies Ohio Valley & Southern States Region by State & Pipeline Company State Alabama Arizona Arkansas Florida Georgia Kentucky Pipeline Company (ENRON) Mobile Bay Pipeline Co. South

Operating Pipeline Companies Ohio Valley & Southern States Region by State & Pipeline Company State Alabama Arizona Arkansas Florida Georgia Kentucky Pipeline Company (ENRON) Mobile Bay Pipeline Co. South

Research Update: U.K.'s Dwr Cymru Debt Ratings Raised On De-Leveraging And Favorable Ownership Structure

December 18, 2007 Research Update: U.K.'s Dwr Cymru Debt Ratings Raised On De-Leveraging And Favorable Ownership Structure Primary Credit Analyst: Tania Tsoneva, London (44) 20-7176-3489;tania_tsoneva@standardandpoors.com

December 18, 2007 Research Update: U.K.'s Dwr Cymru Debt Ratings Raised On De-Leveraging And Favorable Ownership Structure Primary Credit Analyst: Tania Tsoneva, London (44) 20-7176-3489;tania_tsoneva@standardandpoors.com

Three-Year Moving Averages by States % Home Internet Access

Three-Year Moving Averages by States % Home Internet Access Alabama Alaska Arizona Arkansas California Colorado Connecticut Delaware Florida Georgia Hawaii Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana

Three-Year Moving Averages by States % Home Internet Access Alabama Alaska Arizona Arkansas California Colorado Connecticut Delaware Florida Georgia Hawaii Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana

Ratings On Various Royal Bank of Scotland Group Hybrid Securities Lowered

March 24, 2009 Ratings On Various Royal Bank of Scotland Group Hybrid Securities Lowered Primary Credit Analyst: Nigel Greenwood, London (44) 20-7176-7211; nigel_greenwood@standardandpoors.com Secondary

March 24, 2009 Ratings On Various Royal Bank of Scotland Group Hybrid Securities Lowered Primary Credit Analyst: Nigel Greenwood, London (44) 20-7176-7211; nigel_greenwood@standardandpoors.com Secondary

www.standardandpoors.com/ratingsdirect 1

November 17, 2009 Research Update: Energie Oberoesterreich 'A' Rating Affirmed Despite Lower Stand-Alone Credit Profile; Off Watch, Outlook Negative Primary Credit Analyst: Monica Mariani, Milan (39) 02

November 17, 2009 Research Update: Energie Oberoesterreich 'A' Rating Affirmed Despite Lower Stand-Alone Credit Profile; Off Watch, Outlook Negative Primary Credit Analyst: Monica Mariani, Milan (39) 02

DANIEL J. LAWTON LAWTON CONSULTING B.A. ECONOMICS, MERRIMACK COLLEGE M.A. ECONOMICS, TUFTS UNIVERSITY

Page 1 of 9 DANIEL J. LAWTON LAWTON CONSULTING B.A. ECONOMICS, MERRIMACK COLLEGE M.A. ECONOMICS, TUFTS UNIVERSITY Prior to beginning his own consulting practice Diversified Utility Consultants, Inc., in

Page 1 of 9 DANIEL J. LAWTON LAWTON CONSULTING B.A. ECONOMICS, MERRIMACK COLLEGE M.A. ECONOMICS, TUFTS UNIVERSITY Prior to beginning his own consulting practice Diversified Utility Consultants, Inc., in

2015 National Utilization and Compensation Survey Report. Section 3 Billing Rates. Based on Data Collected: 4 th Quarter 2014

2015 National Utilization and Compensation Survey Report Section 3 Billing s Based on Data Collected: 4 th Quarter Copyright 2015 Reproduction of this report or portions thereof without express written

2015 National Utilization and Compensation Survey Report Section 3 Billing s Based on Data Collected: 4 th Quarter Copyright 2015 Reproduction of this report or portions thereof without express written

Psychology NRC Study S Rankings (1 of 6)

") 1 2 3 4 5 6 Princeton U. Harvard U. Stanford U. U. of Wisconsin at Madison Yale U. U. of Rochester U. of Michigan at Ann Arbor San Diego State U. and U. of California at San Diego Columbia U. U. of California

1 2 3 4 5 6 Princeton U. Harvard U. Stanford U. U. of Wisconsin at Madison Yale U. U. of Rochester U. of Michigan at Ann Arbor San Diego State U. and U. of California at San Diego Columbia U. U. of California

Psychology NRC Study R Rankings (1 of 6)

") 1 2 3 4 5 6 7 8 Princeton U. Harvard U. Stanford U. U. of Michigan at Ann Arbor Yale U. U. of Wisconsin at Madison U. of Rochester U. of California at Los Angeles Columbia U. Brown U. U. of Chicago U.

1 2 3 4 5 6 7 8 Princeton U. Harvard U. Stanford U. U. of Michigan at Ann Arbor Yale U. U. of Wisconsin at Madison U. of Rochester U. of California at Los Angeles Columbia U. Brown U. U. of Chicago U.

National Electric Rate Survey

National Electric Rate Survey Ranking of typical residential, commercial and industrial electric bills 2014 Survey 1040 O Street, P.O. Box 80869 Lincoln, NE 68501-0869 p: 402.475.4211 www.les.com Lincoln

National Electric Rate Survey Ranking of typical residential, commercial and industrial electric bills 2014 Survey 1040 O Street, P.O. Box 80869 Lincoln, NE 68501-0869 p: 402.475.4211 www.les.com Lincoln

Credit Ratings Q3 2013 FINANCIAL UPDATE QUARTERLY REPORT OF THE U.S. SHAREHOLDER-OWNED ELECTRIC UTILITY INDUSTRY

Credit Ratings Q3 2013 FINANCIAL UPDATE QUARTERLY REPORT OF THE U.S. SHAREHOLDER-OWNED ELECTRIC UTILITY INDUSTRY About EEI The Edison Electric Institute (EEI) is the association that represents all U.S.

Credit Ratings Q3 2013 FINANCIAL UPDATE QUARTERLY REPORT OF THE U.S. SHAREHOLDER-OWNED ELECTRIC UTILITY INDUSTRY About EEI The Edison Electric Institute (EEI) is the association that represents all U.S.

2010 Allocations to States of Volume Cap for Qualified School Construction Bonds

2010 Allocations to States of Volume Cap for Qualified School Construction Bonds Total Dollar Allocation by State/ State/Territory Territory Alabama 140,453,000 Alaska 28,163,000 Arizona 171,115,000 Arkansas

2010 Allocations to States of Volume Cap for Qualified School Construction Bonds Total Dollar Allocation by State/ State/Territory Territory Alabama 140,453,000 Alaska 28,163,000 Arizona 171,115,000 Arkansas

Finance and Accounting Division

Finance and Accounting Division The Business Services and Finance Division is part of EEI s Business Operations Group. This division provides the leadership and management for advocating industry policies,

Finance and Accounting Division The Business Services and Finance Division is part of EEI s Business Operations Group. This division provides the leadership and management for advocating industry policies,

NON-RESIDENT INDEPENDENT, PUBLIC, AND COMPANY ADJUSTER LICENSING CHECKLIST

NON-RESIDENT INDEPENDENT, PUBLIC, AND COMPANY ADJUSTER LICENSING CHECKLIST ** Utilize this list to determine whether or not a non-resident applicant may waive the Oklahoma examination or become licensed

NON-RESIDENT INDEPENDENT, PUBLIC, AND COMPANY ADJUSTER LICENSING CHECKLIST ** Utilize this list to determine whether or not a non-resident applicant may waive the Oklahoma examination or become licensed

Impacts of Sequestration on the States

Impacts of Sequestration on the States Alabama Alabama will lose about $230,000 in Justice Assistance Grants that support law STOP Violence Against Women Program: Alabama could lose up to $102,000 in funds

Impacts of Sequestration on the States Alabama Alabama will lose about $230,000 in Justice Assistance Grants that support law STOP Violence Against Women Program: Alabama could lose up to $102,000 in funds

Owners of Nuclear Power Plants

NUREG/CR-6500, Rev. 1 ORNL/TM-13297/R1 Owners of Nuclear Power Plants Prepared by R. L. Reid, V. S. White Oak Ridge National Laboratory Prepared for U.S. Nuclear Regulatory Commission Washington, D.C.

NUREG/CR-6500, Rev. 1 ORNL/TM-13297/R1 Owners of Nuclear Power Plants Prepared by R. L. Reid, V. S. White Oak Ridge National Laboratory Prepared for U.S. Nuclear Regulatory Commission Washington, D.C.

Workers Compensation State Guidelines & Availability

ALABAMA Alabama State Specific Release Form Control\Release Forms_pdf\Alabama 1-2 Weeks ALASKA ARIZONA Arizona State Specific Release Form Control\Release Forms_pdf\Arizona 7-8 Weeks by mail By Mail ARKANSAS

ALABAMA Alabama State Specific Release Form Control\Release Forms_pdf\Alabama 1-2 Weeks ALASKA ARIZONA Arizona State Specific Release Form Control\Release Forms_pdf\Arizona 7-8 Weeks by mail By Mail ARKANSAS

July 2012 (1) States With Negative Growth 22 States With Positive Growth 25

States With Negative Growth 22 States With Positive Growth 25") Respondent Coverage: 100% July 2012 Current Month Current Month New England 9.5% Connecticut -3.3% Maine 3.6% Massachusetts 24.1% New Hampshire -0.1% Rhode Island 13.3% Vermont -0.3% Middle Atlantic -3.5%

Respondent Coverage: 100% July 2012 Current Month Current Month New England 9.5% Connecticut -3.3% Maine 3.6% Massachusetts 24.1% New Hampshire -0.1% Rhode Island 13.3% Vermont -0.3% Middle Atlantic -3.5%

Tuition and Fees. & Room and Board. Costs 2011-12

National and Regional Comparisons of Tuition and Fees & Room and Board Costs 2011-12 Table of Contents Table of Contents... 1 Comparator Institutions... 3 University of Wyoming Comparator Institutions...

National and Regional Comparisons of Tuition and Fees & Room and Board Costs 2011-12 Table of Contents Table of Contents... 1 Comparator Institutions... 3 University of Wyoming Comparator Institutions...

STATISTICAL BRIEF #435

STATISTICAL BRIEF #435 April 2014 Premiums and Employee Contributions for Employer-Sponsored Health Insurance: Private versus Public Sector, 2012 Karen E. Davis, MA Introduction Employer-sponsored health

STATISTICAL BRIEF #435 April 2014 Premiums and Employee Contributions for Employer-Sponsored Health Insurance: Private versus Public Sector, 2012 Karen E. Davis, MA Introduction Employer-sponsored health

MAINE (Augusta) Maryland (Annapolis) MICHIGAN (Lansing) MINNESOTA (St. Paul) MISSISSIPPI (Jackson) MISSOURI (Jefferson City) MONTANA (Helena)

Maryland (Annapolis) MICHIGAN (Lansing) MINNESOTA (St. Paul) MISSISSIPPI (Jackson) MISSOURI (Jefferson City) MONTANA (Helena)") HAWAII () IDAHO () Illinois () MAINE () Maryland () MASSACHUSETTS () NEBRASKA () NEVADA (Carson ) NEW HAMPSHIRE () OHIO () OKLAHOMA ( ) OREGON () TEXAS () UTAH ( ) VERMONT () ALABAMA () COLORADO () INDIANA

HAWAII () IDAHO () Illinois () MAINE () Maryland () MASSACHUSETTS () NEBRASKA () NEVADA (Carson ) NEW HAMPSHIRE () OHIO () OKLAHOMA ( ) OREGON () TEXAS () UTAH ( ) VERMONT () ALABAMA () COLORADO () INDIANA

SOLAR MARKET GUIDE WHAT S INSIDE OCTOBER 2015. Solar Markets

SOLAR MARKET GUIDE WHAT S INSIDE 2 Our Active Solar Markets 4 Solar Markets 2 3 Rooftop Survey Contract Options 4/ Arizona 4/ Connecticut 5/ California 5/ Delaware 6/ New Hampshire 6/ Maryland 7/ Massachusetts

SOLAR MARKET GUIDE WHAT S INSIDE 2 Our Active Solar Markets 4 Solar Markets 2 3 Rooftop Survey Contract Options 4/ Arizona 4/ Connecticut 5/ California 5/ Delaware 6/ New Hampshire 6/ Maryland 7/ Massachusetts

Standard & Poor's Applies Its Revised Insurance Criteria To 22 Insurance Groups And Their Subsidiaries

Standard & Poor's Applies Its Revised Insurance Criteria 22 Insurance Groups And Their Subsidiaries Primary Credit Analysts: Patrick C Wong, New York (1) 212-438-1936; patrick.wong@standardandpoors.com

Standard & Poor's Applies Its Revised Insurance Criteria 22 Insurance Groups And Their Subsidiaries Primary Credit Analysts: Patrick C Wong, New York (1) 212-438-1936; patrick.wong@standardandpoors.com

BUSINESS DEVELOPMENT OUTCOMES

BUSINESS DEVELOPMENT OUTCOMES Small Business Ownership Description Total number of employer firms and self-employment in the state per 100 people in the labor force, 2003. Explanation Business ownership

BUSINESS DEVELOPMENT OUTCOMES Small Business Ownership Description Total number of employer firms and self-employment in the state per 100 people in the labor force, 2003. Explanation Business ownership

AMI Fact Book 4Q 2009

Synopsis This report is a catalog of current and future AMI and smart meter deployments in the U.S. It includes profiles of utilities, government agencies, and private organizations influencing the development

Synopsis This report is a catalog of current and future AMI and smart meter deployments in the U.S. It includes profiles of utilities, government agencies, and private organizations influencing the development

Compare Your Stats Pharmacy

THE PREMIER SOURCE FOR FUTURE DR. S *Data provided by the American Association of Colleges of Pharmacy **Data based on matriculated students at respective schools entering fall 2010 Compare Your Stats

THE PREMIER SOURCE FOR FUTURE DR. S *Data provided by the American Association of Colleges of Pharmacy **Data based on matriculated students at respective schools entering fall 2010 Compare Your Stats

www.standardandpoors.com/ratingsdirect 1

December 9, 2009 Research Update: Spain Outlook Revised To Negative On Rising Fiscal Deficits And Risks Posed By Macroeconomic Adjustment Primary Credit Analyst: Trevor Cullinan, London (44) 20-7176-7110;trevor_cullinan@standardandpoors.com

December 9, 2009 Research Update: Spain Outlook Revised To Negative On Rising Fiscal Deficits And Risks Posed By Macroeconomic Adjustment Primary Credit Analyst: Trevor Cullinan, London (44) 20-7176-7110;trevor_cullinan@standardandpoors.com

MLGW s Average Residential Utility Bill Ranks the Lowest

MLGW s Average Residential Utility Bill Ranks the Lowest Each year, MLGW strives to deliver the highest quality service at the lowest possible rates. One way that we measure our performance is to examine

MLGW s Average Residential Utility Bill Ranks the Lowest Each year, MLGW strives to deliver the highest quality service at the lowest possible rates. One way that we measure our performance is to examine

Table 1: Advertising, Marketing and Promotional Expense as a Percentage of Net Operating Revenue

Table 1: Advertising, Marketing and Promotional Expense as a Percentage of Net Operating Revenue NAIC Group % Attorney s Title 3.8% Chicago / Fidelity 0.9% Diversified 0.6% First American 2.7% Investors

Table 1: Advertising, Marketing and Promotional Expense as a Percentage of Net Operating Revenue NAIC Group % Attorney s Title 3.8% Chicago / Fidelity 0.9% Diversified 0.6% First American 2.7% Investors

NASPAA s Research Universities Report 3/4/16

NASPAA s Research Universities Report 3/4/16 Data Source: 2014-2015 NASPAA Annual Data Report N= 109 schools, 120 programs 70% of Research Universities Fall 2015 Current Enrollment 15552 students Average

NASPAA s Research Universities Report 3/4/16 Data Source: 2014-2015 NASPAA Annual Data Report N= 109 schools, 120 programs 70% of Research Universities Fall 2015 Current Enrollment 15552 students Average

In-state Tuition & Fees at Flagship Universities by State 2014-15 Rank School State In-state Tuition & Fees Penn State University Park Pennsylvania 1

In-state Tuition & Fees at Flagship Universities by State 2014-15 Rank School State In-state Tuition & Fees Penn State University Park Pennsylvania 1 $18,464 New New Hampshire 2 Hampshire $16,552 3 Vermont

In-state Tuition & Fees at Flagship Universities by State 2014-15 Rank School State In-state Tuition & Fees Penn State University Park Pennsylvania 1 $18,464 New New Hampshire 2 Hampshire $16,552 3 Vermont

Net-Temps Job Distribution Network

Net-Temps Job Distribution Network The Net-Temps Job Distribution Network is a group of 25,000 employment-related websites with a local, regional, national, industry and niche focus. Net-Temps customers'

Net-Temps Job Distribution Network The Net-Temps Job Distribution Network is a group of 25,000 employment-related websites with a local, regional, national, industry and niche focus. Net-Temps customers'

Health Care Service Corp. Outlook Revised To Negative From Stable; Ratings Affirmed

Research Update: Health Care Service Corp. Outlook Revised To Negative From Stable; Ratings Affirmed Primary Credit Analyst: Neal I Freedman, New York (1) 212-438-1274; neal.freedman@standardandpoors.com

Research Update: Health Care Service Corp. Outlook Revised To Negative From Stable; Ratings Affirmed Primary Credit Analyst: Neal I Freedman, New York (1) 212-438-1274; neal.freedman@standardandpoors.com

STATISTICAL BRIEF #273

STATISTICAL BRIEF #273 December 29 Employer-Sponsored Health Insurance for Employees of State and Local Governments, by Census Division, 28 Beth Levin Crimmel, M.S. Introduction Employees of state and

STATISTICAL BRIEF #273 December 29 Employer-Sponsored Health Insurance for Employees of State and Local Governments, by Census Division, 28 Beth Levin Crimmel, M.S. Introduction Employees of state and

Age and Health Insurance: Pricing Out the Decades of Adult Life Looking at the difference in health insurance premiums between ages 20 and 60.

Age and Health Insurance: Pricing Out the Decades of Adult Life Looking at the difference in health insurance premiums between ages 20 and 60. Contents 2 3 3 4 4 5 6 7 7 8 9 10 11 12 13 14 Table of Contents

Age and Health Insurance: Pricing Out the Decades of Adult Life Looking at the difference in health insurance premiums between ages 20 and 60. Contents 2 3 3 4 4 5 6 7 7 8 9 10 11 12 13 14 Table of Contents

Verizon Wireless Ranks Highest in Wireless Network Quality Performance in Five Regions; AT&T Ranks Highest in One Region

Reports: Tablet and Mobile Broadband Devices Generate Increased Data Quality Issues as Usage Patterns and Customer Expectations Impact Problem Incidence Ranks Highest in Wireless Network Quality Performance

Reports: Tablet and Mobile Broadband Devices Generate Increased Data Quality Issues as Usage Patterns and Customer Expectations Impact Problem Incidence Ranks Highest in Wireless Network Quality Performance

STATE-SPECIFIC ANNUITY SUITABILITY REQUIREMENTS

Alabama Alaska Arizona Arkansas California This jurisdiction has pending annuity training legislation/regulation Annuity Training Requirement Currently Effective Initial 8-Hour Annuity Training Requirement:

Alabama Alaska Arizona Arkansas California This jurisdiction has pending annuity training legislation/regulation Annuity Training Requirement Currently Effective Initial 8-Hour Annuity Training Requirement:

Centers of Excellence

Centers of Excellence A program of the NMSDC to enhance corporate minority supplier development through knowledge sharing and excellence in implementing NMSDC best practices. Centers of Excellence enhances

Centers of Excellence A program of the NMSDC to enhance corporate minority supplier development through knowledge sharing and excellence in implementing NMSDC best practices. Centers of Excellence enhances

Research Update: Ratings Lowered On Netherlands-Based SNS REAAL N.V. Group And Core Subs On Slower Recovery Prospects; Outlook Stable

March 1, 2012 Research Update: Ratings Lowered On Netherlands-Based SNS REAAL N.V. Group And Core Subs On Slower Recovery Prospects; Outlook Stable Primary Credit Analysts: Alexandre Birry, London 44 (0)

March 1, 2012 Research Update: Ratings Lowered On Netherlands-Based SNS REAAL N.V. Group And Core Subs On Slower Recovery Prospects; Outlook Stable Primary Credit Analysts: Alexandre Birry, London 44 (0)

State Specific Annuity Suitability Requirements updated 10/10/11

Alabama Alaska Ai Arizona Arkansas California This jurisdiction has pending annuity training legislation/regulation Initial 8 Hour Annuity Training Requirement: Prior to selling annuities in California,

Alabama Alaska Ai Arizona Arkansas California This jurisdiction has pending annuity training legislation/regulation Initial 8 Hour Annuity Training Requirement: Prior to selling annuities in California,

US Department of Health and Human Services Exclusion Program. Thomas Sowinski Special Agent in Charge/ Reviewing Official

US Department of Health and Human Services Exclusion Program Thomas Sowinski Special Agent in Charge/ Reviewing Official Overview Authority to exclude individuals and entities from Federal Health Care

US Department of Health and Human Services Exclusion Program Thomas Sowinski Special Agent in Charge/ Reviewing Official Overview Authority to exclude individuals and entities from Federal Health Care

University System of Georgia Enrollment Trends and Projections to 2018

University System of Georgia Enrollment Trends and Projections to 2018 Introduction: Projections of USG Headcount Enrollment Enrollment projections use past trends and information on other variables to

University System of Georgia Enrollment Trends and Projections to 2018 Introduction: Projections of USG Headcount Enrollment Enrollment projections use past trends and information on other variables to

Englishinusa.com Positions in MSN under different search terms.

Englishinusa.com Positions in MSN under different search terms. Search Term Position 1 Accent Reduction Programs in USA 1 2 American English for Business Students 1 3 American English for Graduate Students

Englishinusa.com Positions in MSN under different search terms. Search Term Position 1 Accent Reduction Programs in USA 1 2 American English for Business Students 1 3 American English for Graduate Students

SCHOOL SCHOOL S WEB ADDRESS. HOURS Tempe Arizona Ph.D. 4-5 54-84 January 15 $60 Not given 550/213

SCHOOL SCHOOL S WEB ADDRESS 1 Arizona State University http://wpcarey.asu.edu/acc/doctoral.cfm 2 Baruch College CUNY http://zicklin.baruch.cuny.edu/programs/doctoral/areas-of-study/accounting 3 Bentley

SCHOOL SCHOOL S WEB ADDRESS 1 Arizona State University http://wpcarey.asu.edu/acc/doctoral.cfm 2 Baruch College CUNY http://zicklin.baruch.cuny.edu/programs/doctoral/areas-of-study/accounting 3 Bentley

Construction Initiative: Distribution of $24.8 Billion In Bonding Authority Initial Estimates for H.R. 4094

Alabama Alaska Arizona Arkansas California SEA Allocation 208,207 Birmingham City 33,463 Mobile County 51,654 Montgomery County 21,960 QZABS 39,638 Total 354,922 SEA Allocation 47,418 Total 53,398 SEA

Alabama Alaska Arizona Arkansas California SEA Allocation 208,207 Birmingham City 33,463 Mobile County 51,654 Montgomery County 21,960 QZABS 39,638 Total 354,922 SEA Allocation 47,418 Total 53,398 SEA

J.D. Power Reports: Strong Network Quality Performance Is Key to Higher Customer Retention for Wireless Carriers

Kw J.D. Power Reports: Strong Network Quality Performance Is Key to Higher Customer Retention for Wireless Carriers Ranks Highest in Wireless Network Quality Performance in All Six Regions WESTLAKE VILLAGE,

Kw J.D. Power Reports: Strong Network Quality Performance Is Key to Higher Customer Retention for Wireless Carriers Ranks Highest in Wireless Network Quality Performance in All Six Regions WESTLAKE VILLAGE,

State-Specific Annuity Suitability Requirements

Alabama Alaska Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Effective 10/16/11: Producers holding a life line of authority on or before 10/16/11 who sell or wish to sell

Alabama Alaska Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Effective 10/16/11: Producers holding a life line of authority on or before 10/16/11 who sell or wish to sell

HECM MIC Endorsement Report WELLS FARGO BANK NA As of July 2010

WELLS FARGO BANK NA As of July 2010 Table of Contents Industry Overview... pg. 3 Top 10 Lenders... pg. 3 Regional Overview... pg. 3 National Lender Stats... National Top 10... pg. 4 pg. 5 Regional Top

WELLS FARGO BANK NA As of July 2010 Table of Contents Industry Overview... pg. 3 Top 10 Lenders... pg. 3 Regional Overview... pg. 3 National Lender Stats... National Top 10... pg. 4 pg. 5 Regional Top

Licensure Resources by State

Licensure Resources by State Alabama Alabama State Board of Social Work Examiners http://socialwork.alabama.gov/ Alaska Alaska Board of Social Work Examiners http://commerce.state.ak.us/dnn/cbpl/professionallicensing/socialworkexaminers.as

Licensure Resources by State Alabama Alabama State Board of Social Work Examiners http://socialwork.alabama.gov/ Alaska Alaska Board of Social Work Examiners http://commerce.state.ak.us/dnn/cbpl/professionallicensing/socialworkexaminers.as

2010 Utility Bill Comparisons for Selected U.S. Cities

Memphis Light, Gas and Water 2010 Utility Bill Comparisons for Selected U.S. Cities Electricity Natural Gas Water Wastewater The information in this book has been compiled to ensure maximum accuracy at

Memphis Light, Gas and Water 2010 Utility Bill Comparisons for Selected U.S. Cities Electricity Natural Gas Water Wastewater The information in this book has been compiled to ensure maximum accuracy at

Association of American Medical College-Affiliated, Liaison Committee on Medical Education-

Supplemental Digital Appendix 1 Association of American Medical College-Affiliated, Liaison Committee on Medical Education- Accredited U.S. Medical Schools Included in an Assessment of Clerkship Grading

Supplemental Digital Appendix 1 Association of American Medical College-Affiliated, Liaison Committee on Medical Education- Accredited U.S. Medical Schools Included in an Assessment of Clerkship Grading

Hosted and Cloud-Based VoIP and UC Services Template

1. Do you offer consumer services? 2. Do you offer business services? (If not, we'll save you the trouble of seeing the questions about business services.) 3. What size range(s) of customers are a best

1. Do you offer consumer services? 2. Do you offer business services? (If not, we'll save you the trouble of seeing the questions about business services.) 3. What size range(s) of customers are a best

J.D. Power and Associates Reports: Overall Wireless Network Problem Rates Differ Considerably Based on Type of Usage Activity

Reports: Overall Wireless Network Problem Rates Differ Considerably Based on Type of Usage Activity Ranks Highest in Wireless Network Quality Performance in Five Regions WESTLAKE VILLAGE, Calif.: 25 August

Reports: Overall Wireless Network Problem Rates Differ Considerably Based on Type of Usage Activity Ranks Highest in Wireless Network Quality Performance in Five Regions WESTLAKE VILLAGE, Calif.: 25 August

DOW JONES UTILITY AVERAGE

DOW JONES UTILITY AVERAGE Historical Components The Dow Jones Utility Average is the youngest of the three Dow Jones Averages, first appearing in January 1929. According to analysts who study the averages,

DOW JONES UTILITY AVERAGE Historical Components The Dow Jones Utility Average is the youngest of the three Dow Jones Averages, first appearing in January 1929. According to analysts who study the averages,

SAMPLE REPORT. Competitive Landscape for Wholesale Distribution: Electronics $295.95 RESEARCHED & PRODUCED BY:

$295.95 2015 Competitive Landscape for Wholesale Distribution: Electronics ANNUAL MARKET DATA, TRENDS AND ANALYSIS FOR THE NORTH AMERICAN WHOLESALE DISTRIBUTION INDUSTRY 2015 by Gale Media, Inc. All rights

$295.95 2015 Competitive Landscape for Wholesale Distribution: Electronics ANNUAL MARKET DATA, TRENDS AND ANALYSIS FOR THE NORTH AMERICAN WHOLESALE DISTRIBUTION INDUSTRY 2015 by Gale Media, Inc. All rights

BENCHMARKING AIR EMISSIONS

BENCHMARKING AIR EMISSIONS OF THE 1 LARGEST ELECTRIC POWER PRODUCERS IN THE UNITED STATES JULY 215 BENCHMARKING AIR EMISSIONS OF THE 1 LARGEST ELECTRIC POWER PRODUCERS IN THE UNITED STATES JULY 215 1

BENCHMARKING AIR EMISSIONS OF THE 1 LARGEST ELECTRIC POWER PRODUCERS IN THE UNITED STATES JULY 215 BENCHMARKING AIR EMISSIONS OF THE 1 LARGEST ELECTRIC POWER PRODUCERS IN THE UNITED STATES JULY 215 1

High Risk Health Pools and Plans by State

High Risk Health Pools and Plans by State State Program Contact Alabama Alabama Health 1-866-833-3375 Insurance Plan 1-334-263-8311 http://www.alseib.org/healthinsurance/ahip/ Alaska Alaska Comprehensive

High Risk Health Pools and Plans by State State Program Contact Alabama Alabama Health 1-866-833-3375 Insurance Plan 1-334-263-8311 http://www.alseib.org/healthinsurance/ahip/ Alaska Alaska Comprehensive

American C.E. Requirements

American C.E. Requirements Alaska Board of Nursing Two of the following: 30 contact hours 30 hours of professional nursing activities 320 hours of nursing employment Arizona State Board of Nursing Arkansas

American C.E. Requirements Alaska Board of Nursing Two of the following: 30 contact hours 30 hours of professional nursing activities 320 hours of nursing employment Arizona State Board of Nursing Arkansas

Vertical Market Selling Guide. Security Systems Services

Vertical Market Selling Guide Security Systems Services Purpose This guide is provided to you at no charge to create awareness for the needs of a payment terminal solution within a specific vertical market

Vertical Market Selling Guide Security Systems Services Purpose This guide is provided to you at no charge to create awareness for the needs of a payment terminal solution within a specific vertical market

2014 INCOME EARNED BY STATE INFORMATION

BY STATE INFORMATION This information is being provided to assist in your 2014 tax preparations. The information is also mailed to applicable Columbia fund non-corporate shareholders with their year-end

BY STATE INFORMATION This information is being provided to assist in your 2014 tax preparations. The information is also mailed to applicable Columbia fund non-corporate shareholders with their year-end

Universities classified as "very high research activity"

Universities classified as "very high research activity" 108 institutions classified as "RU/VH: Research Universities (very high research activity)" in the 2010 Carnegie Classification of Institutions

Universities classified as "very high research activity" 108 institutions classified as "RU/VH: Research Universities (very high research activity)" in the 2010 Carnegie Classification of Institutions

A/B MAC Jurisdiction 1 Original Medicare Claims Processor

A/B MAC Jurisdiction 1 Jurisdiction 1 - American Samoa, California, Guam, Hawaii, Nevada and Northern Mariana Islands Total Number of Fee-For-Service Beneficiaries: 3,141,183 (as of Total Number of Beneficiaries

A/B MAC Jurisdiction 1 Jurisdiction 1 - American Samoa, California, Guam, Hawaii, Nevada and Northern Mariana Islands Total Number of Fee-For-Service Beneficiaries: 3,141,183 (as of Total Number of Beneficiaries

Research Update: Empresa de Energia de Bogotá S.A. E.S.P. 'BB+' Corporate Credit Rating Affirmed; Outlook Remains Stable.

June 21, 2011 Research Update: Empresa de Energia de Bogotá S.A. E.S.P. 'BB+' Corporate Credit Rating Affirmed; Outlook Primary Credit Analyst: Carolina Duran, Mexico City 52-55-5081-4417;carolina_duran@standardandpoors.com

June 21, 2011 Research Update: Empresa de Energia de Bogotá S.A. E.S.P. 'BB+' Corporate Credit Rating Affirmed; Outlook Primary Credit Analyst: Carolina Duran, Mexico City 52-55-5081-4417;carolina_duran@standardandpoors.com

Information About Filing a Case in the United States Tax Court. Attached are the forms to use in filing your case in the United States Tax Court.

Information About Filing a Case in the United States Tax Court Attached are the forms to use in filing your case in the United States Tax Court. It is very important that you take time to carefully read

Information About Filing a Case in the United States Tax Court Attached are the forms to use in filing your case in the United States Tax Court. It is very important that you take time to carefully read

Sirius International Group Outlook Revised To Stable On Plans To Retain Its Strategy Post Acquisition; Ratings Affirmed

Research Update: Sirius International Group Outlook Revised To Stable On Plans To Retain Its Strategy Post Acquisition; Ratings Affirmed Primary Credit Analyst: Anvar Gabidullin, CFA, London (44) 20-7176-7047;

Research Update: Sirius International Group Outlook Revised To Stable On Plans To Retain Its Strategy Post Acquisition; Ratings Affirmed Primary Credit Analyst: Anvar Gabidullin, CFA, London (44) 20-7176-7047;

BenefitsMonitor National Higher Education Participants. Mercer Health & Benefits 20

BenefitsMonitor National Higher Education Participants Arizona State University Austin Peay State University Bates College Baylor College of Medicine Baylor University Boston University Bowling Green State

BenefitsMonitor National Higher Education Participants Arizona State University Austin Peay State University Bates College Baylor College of Medicine Baylor University Boston University Bowling Green State

2009-10 STATE AND LOCAL GOVERNMENT TAX AND REVENUE RANKINGS. By Jacek Cianciara

2009-10 STATE AND LOCAL GOVERNMENT TAX AND REVENUE RANKINGS By Jacek Cianciara Wisconsin Department of Revenue Division of Research and Policy December 12, 2012 TABLE OF CONTENTS Key Findings 3 Introduction

2009-10 STATE AND LOCAL GOVERNMENT TAX AND REVENUE RANKINGS By Jacek Cianciara Wisconsin Department of Revenue Division of Research and Policy December 12, 2012 TABLE OF CONTENTS Key Findings 3 Introduction

Core Entities Of German Insurance Group W&W Affirmed At 'A-' On Improved Enterprise Risk Management; Outlook Stable

Research Update: Core Entities Of German Insurance Group W&W Affirmed At 'A-' On Improved Enterprise Risk Primary Credit Analysts: Silke Longoni, Frankfurt (49) 69-33-999-195; silke.longoni@standardandpoors.com

Research Update: Core Entities Of German Insurance Group W&W Affirmed At 'A-' On Improved Enterprise Risk Primary Credit Analysts: Silke Longoni, Frankfurt (49) 69-33-999-195; silke.longoni@standardandpoors.com

LPSC Renewable Energy Pilot y RFPs issued by Utility Companies by Order of Commission, November 2010

Renewable Energy LPSC Renewable Energy Pilot y RFPs issued by Utility Companies by Order of Commission, November 2010 y Searching for various forms of renewable energy and their actual cost in Louisiana

Renewable Energy LPSC Renewable Energy Pilot y RFPs issued by Utility Companies by Order of Commission, November 2010 y Searching for various forms of renewable energy and their actual cost in Louisiana

J.D. Power Reports: Satisfaction Rebounds for Gas Utility Companies Driven by Proactive Communication

w J.D. Power Reports: Satisfaction Rebounds for Gas Utility Companies Driven by Proactive Communication MidAmerican Energy; Oklahoma Natural Gas; Southern California Gas Company; and Washington Gas Rank

w J.D. Power Reports: Satisfaction Rebounds for Gas Utility Companies Driven by Proactive Communication MidAmerican Energy; Oklahoma Natural Gas; Southern California Gas Company; and Washington Gas Rank

NIH 2009* Total $ Awarded. NIH 2009 Rank

Organization Name (Schools of Nursing) 2009* Total $ Awarded 2009 2008 Total $ Awarded 2008 2007 UNIVERSITY OF PENNSYLVANIA $10,908,657 1 $7,721,221 2 4 5 UNIVERSITY OF CALIFORNIA SAN FRANCISCO $8,780,469

Organization Name (Schools of Nursing) 2009* Total $ Awarded 2009 2008 Total $ Awarded 2008 2007 UNIVERSITY OF PENNSYLVANIA $10,908,657 1 $7,721,221 2 4 5 UNIVERSITY OF CALIFORNIA SAN FRANCISCO $8,780,469

STATE DATA CENTER. District of Columbia MONTHLY BRIEF

District of Columbia STATE DATA CENTER MONTHLY BRIEF N o v e m b e r 2 0 1 2 District Residents Health Insurance Coverage 2000-2010 By Minwuyelet Azimeraw Joy Phillips, Ph.D. This report is based on data

District of Columbia STATE DATA CENTER MONTHLY BRIEF N o v e m b e r 2 0 1 2 District Residents Health Insurance Coverage 2000-2010 By Minwuyelet Azimeraw Joy Phillips, Ph.D. This report is based on data

CMS Establishes PDP and MA Regions

Washington New York San Francisco London Brussels Health Care Reimbursement Client Alert: Medicare Part D December 2004 CMS Establishes PDP and MA Regions The Centers for Medicare and Medicaid Services

Washington New York San Francisco London Brussels Health Care Reimbursement Client Alert: Medicare Part D December 2004 CMS Establishes PDP and MA Regions The Centers for Medicare and Medicaid Services

A Study About Identity Theft

A Study About Identity Theft Prepared For: The National Foundation for Credit Counseling Prepared By: Harris Interactive Inc. Public Relations Research 1 INTRODUCTION AND METHODOLOGY This Identity Theft

A Study About Identity Theft Prepared For: The National Foundation for Credit Counseling Prepared By: Harris Interactive Inc. Public Relations Research 1 INTRODUCTION AND METHODOLOGY This Identity Theft

Overview of Takaful Insurance from a credit perspective

Overview of Takaful Insurance from a credit perspective Ali Karakuyu Associate Director Financial Institutions Ratings Istanbul 13 November 2012 Copyright 2011 Standard & Poor s Financial Services LLC,

Overview of Takaful Insurance from a credit perspective Ali Karakuyu Associate Director Financial Institutions Ratings Istanbul 13 November 2012 Copyright 2011 Standard & Poor s Financial Services LLC,