Materials. Lesson Objectives

|

|

|

- Darcy Jennings

- 8 years ago

- Views:

Transcription

1 70

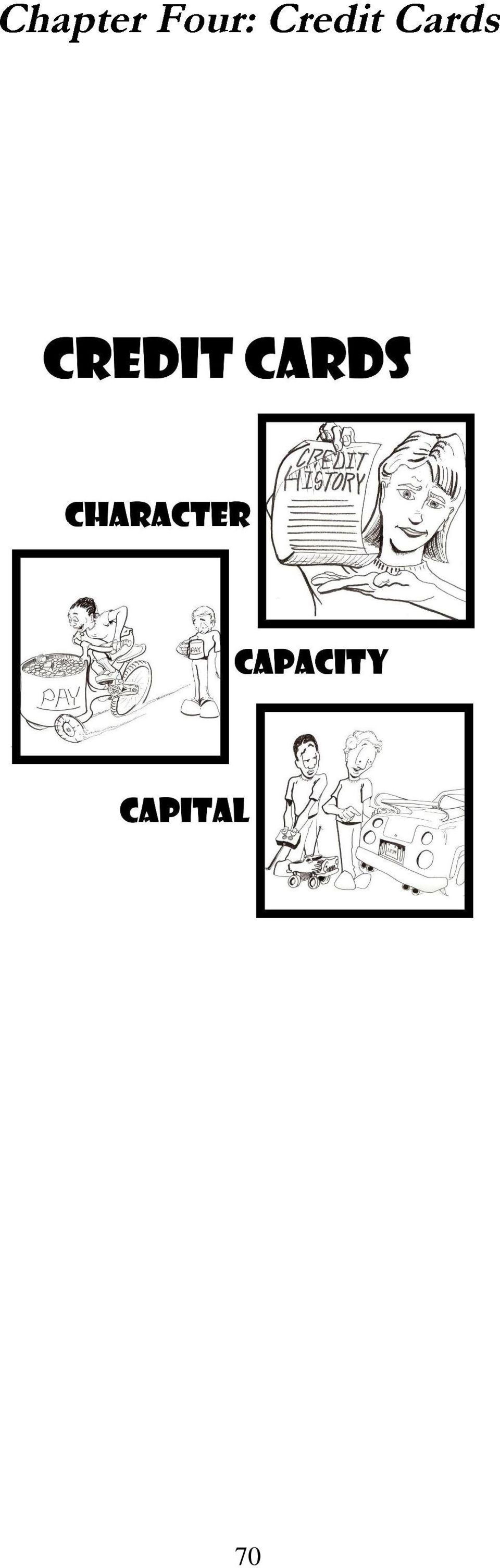

2 Materials 1. Marker or Chalk 2. Chalkboard or Flip Chart 3. Blank piece of white paper 4. Credit Card Vocabulary Sheet 5. Credit Report Answer Key 6. Student Materials Packets Outline 1. KWL 2. Review 3. IEAL 4. Credit Card Ad 5. Fine Print 6. Credit Report 7. APR 8. Three C s of Credit 9. Credit Card Bill 10. Learned Lesson Objectives 1. The student will be able to explain how banks and credit unions make profit from lending money and issuing credit cards. 2. The student will be able to describe how credit card companies decide to give someone credit. 3. The student will be able to define the important terms associated with credit. 4. The student will be able to identify the parts of a Credit Report and what they mean. 5. The student will be able to recognize the interest rate on a credit card offer. Procedure KWL (10 min.) 1. If you worked for a credit card company what questions would you want to ask me before you gave me a credit card? Draw the following diagram on the board and write students answers under matching categories. (see example student answers) Character Capacity Capital Have you paid back loans in the past when you said you would? How much do make? What expenses are you committed to? How much money do you have? What can we take from you if you don t pay us back? 71

3 2. The class will begin a write and toss exercise. Hand a blank piece of paper to the first student. The students will each take turns writing down one question they would ask me before they gave me a credit card. Then the next step is to have them crinkle up the paper and toss it across the room to another student. The next student is to repeat the same process. 3. After a few students have written down responses the teacher should write each question under the appropriate heading on the board. 4. These are the Three C s of Credit (point to the category headings). My answers to these questions will determine how much interest I pay on my credit card or whether I get the card at all. If you are the credit card company you ask these questions because you want to minimize the chances of me not paying you back, or minimize your risk. REVIEW (3 min.) 5. Last class we did a class spending plan and we learned about the two major pieces of a spending plan, what are they? Income and Expenses 6. What was the process we went through to get our spending plan during the last class? First we looked at how much money we had coming in, then we looked at where we were spending. We put it all down on paper and then we looked at where we could cut back. 7. Keep in mind that this is the process you can always use, it is now part of your financial tool kit. IEAL (3 min.) 8. Today the focus is on credit cards. If spending plans fall under the income and expenses boxes, where do you think credit cards would fit on our IEAL chart? Draw this on the board Income Assets Expenses Liabilities 9. Let students answer and record the correct answers on the chart. Your credit card balance would fall under liabilities, you credit card bill would fall under expenses. Be careful to define balance and payment, and explain that we will get a better understanding of them later. 10. So charging money on a credit card would give you more income? NO, credit is not income. Credit is a loan. 72

4 CREDIT CARD ADVERTISEMENT (5 min.) 11. Open the packets to the first page. What do you think this is? It is a credit card advertisement. 12. What is the first number you notice? Zero 13. What do the letters APR mean? They mean Annual Percentage Rate which is a complicated way of saying interest. 14. Write APR = INTEREST on the board 15. Last class we talked about earning interest on your savings and investment accounts. What does it mean to earn interest? The credit union adds some money to your account for keeping your money there. 16. This is the same idea except that when you borrow money on a credit card you pay interest instead of getting it. 17. We are going to go through the process of getting a credit card one step at a time together, that way you will know how it works when you get your own. 18. Write the steps on the board as you go along. 19.! You will get things like this sent to you when you get older but, generally speaking, the card you want to get will not usually find you. You will need to find it. Just like shopping for anything else, you need to go out and compare. Even though the advertisement says 0%, you want to ask yourself- for how long will this be the case? The interest rate can be changed at any time. That information is in the part you do want to pay attention to -- the fine print. Not the big zero on the advertisements, but the APR in the fine print. Customary APR is the regular interest rate, Default APR is what you pay if you miss a payment or make a late payment. Fee is a charge on your account for something. THE FINE PRINT (10 min.) 20. The fine print is on the next page. By law you must be informed about everything included in the fine print before you sign to get the card. I got this from the internet, which can be a good place to compare offers, but once you have chosen your card it is best to go to the credit union or bank and fill out the application in person. 21. The fine print is hard to read and confusing and many times credit card companies put wording in there that allows them to change it all anyway. But let s take a look and 73

5 define some of the terms. Notice that on the next page I have made the fine print into big print for you. 22. Shout out any of the words you want to and we will define them together. 23. After defining the words together (using the Credit Vocabulary Sheet), go over some of the key things that you would find in a good credit card. 24. Can the amount of interest that I am charged change? Yes 25. What APR would I pay if I was late on one payment? 32.4% 26. Can they change the terms of the card at any time? Yes 27.. You will usually find better deals with credit unions than with banks. Credit unions exist to serve their members not to make money, so that means they usually have better terms for loans of all kinds. The card we are looking at right now is from a bank and has some very bad terms. 28. Take a quick look at as a class, noting the information the credit card company collects and questioning why it might want that type of information. 29. You need to know your credit limit so that you don t go over it, and you need to know your interest rate because that is how much you will pay if you carry a balance over from month to month. If you report you card lost/stolen before anybody uses you card then you are not responsible to pay any charges they make. 30. Step five is check your credit report once per year for free from Experian, Equifax, and Transunion at CREDIT REPORT (2 min.) 31. So you send off the application and then what? How does the credit card company decide to give you a card? They check your credit report. 32. Each of you has a copy of my credit report in your packet and a copy of my application. You also have a sheet called et s take a look at that. THREE C S OF CREDIT (15 min.) 33. Take out the sheet in your packets labeled The Three C s of Credit, I will call on one of you to give me a definition of each one. 34. In the boxes at the bottom of the sheet I want you to list one way I can show you my character, capacity, and capital. For example one way to show my character would be to show the open/never late status of all of my accounts, one 74

6 way to show my capacity would be to show my pay stubs, and my bank statement would show my capital. CREDIT CARD BILL (8 min) 35. Help students as needed then move on to the bill. 36. Let s imagine, I got approved for the credit card. The company will send me the card as soon as the approval is final. 37. As soon as you receive the card, the only thing that protects you from getting into debt is for you to follow the last three steps. 38. For example if your credit limit is $1,000 don t put more than $100-$300 on your card If you follow these steps you will build good credit, and credit reports are becoming more and more important. Landlords, employers, and even insurance companies are now checking them to find out about you, and if you look bad on a credit report it makes it harder to do or get a lot of things. If you can t pay back everything in one month then at least never borrow more then 10% of the credit you have available. If your credit limit is $1,700 don t borrow more than $170 at a time. 42. Let s take a look at my bill and see if I followed the rules. 43. How much do I owe on this card? $ That is my new balance. 45. How much do I have to pay this month? 46. How much interest did I get charged? 47. That is labeled finance charge another fancy word for interest. 48. So if I only pay $15.00 how much am I actually paying on what I owe? $ Did I pay off my whole balance last month? 50. Am I borrowing more then I can pay in one month? 51. How long will it take me to pay this off at $15.00 per month? 75

7 52. I would pay almost in interest for $600 worth of stuff, for a total of almost 53. That is the price you pay for not using credit wisely! LEARNED (3 min) 54. What have we learned about credit today? 55. List responses under L on the board. Note to instructor: We have calculated this at 59 minutes of teaching time. This is the minimum, it can take much longer. Feel free to adjust time according to students needs. 76

8 This sheet is intended for the instructor. While we believe it is important for students to learn some of these terms, we did not do a vocabulary exercise for this lesson because we feel that understanding how credit cards work is more important than understanding all the jargon. In an interview on NPR Harvard law professor Elizabeth Warren was asked by Terry Gross Do you read the fine print and check your APR? No she answered Why should I, they can change the terms anytime they want. Creditor: The person or financial institution from whom you borrow money. Customary APR: The standard Annual Percentage Rate range for a company. Cash Advance: Using your credit card to borrow cash, usually from an ATM. Variable: The rate can change for any reason. Annual Fee: A yearly charge for certain credit cards. Creditworthiness: Your credit score based on your credit report, it has a big impact on the interest rate you pay. Minimum Payment: The smallest amount you can pay per month and still avoid late charges Balance: The amount of money you owe on a credit card. Credit Limit: The largest amount of money you can borrow on your card Default Rate: The highest APR, charged on those who miss a payment on a card or pay late. Finance Charge: A fancy phrase meaning interest and fees. 77

9 78

10 79

11 80

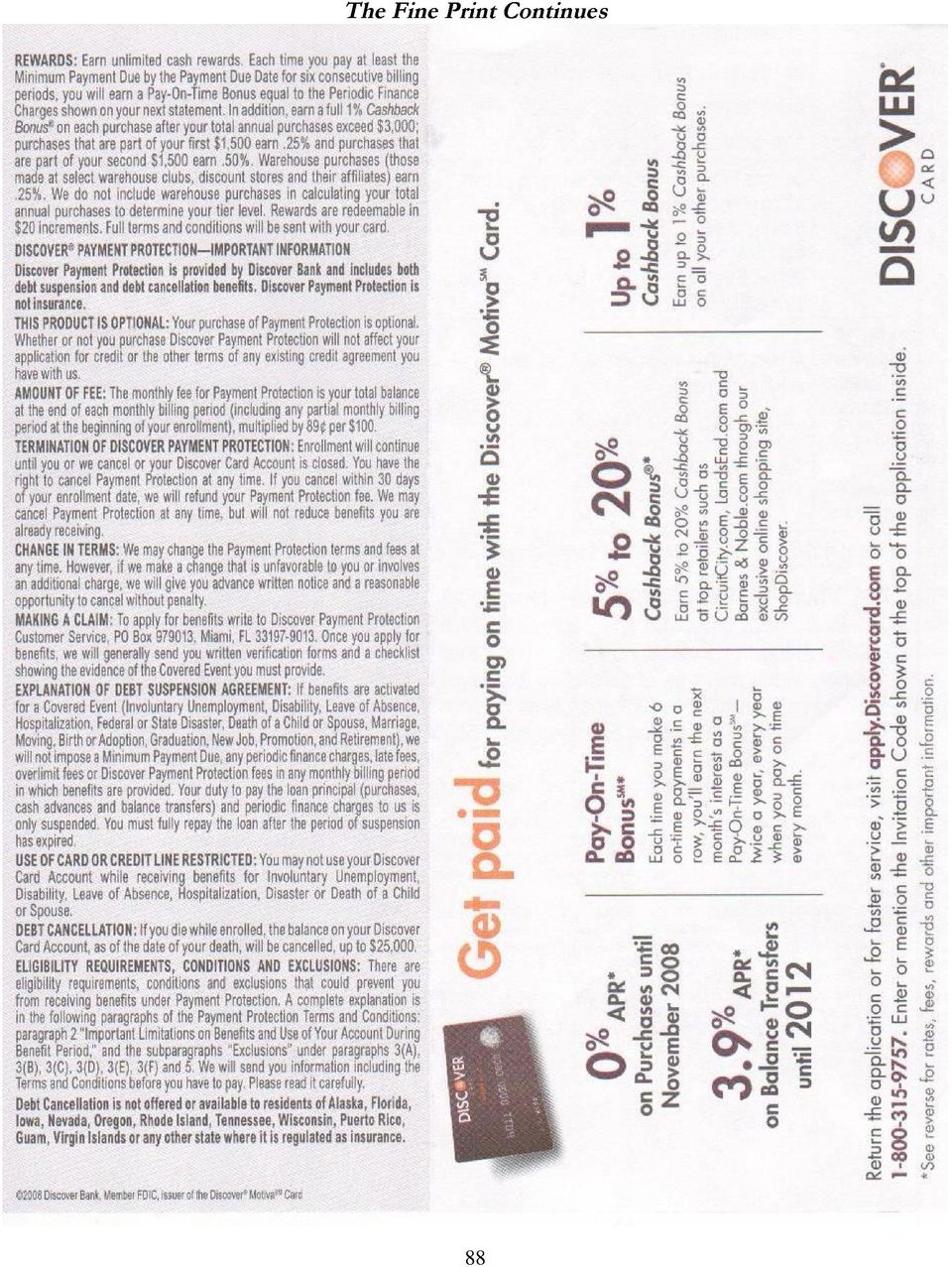

12 81

13 82

14 83

15 84

16 85

17 86

18 87

19 88

20 89

21 90

22 91

23 92

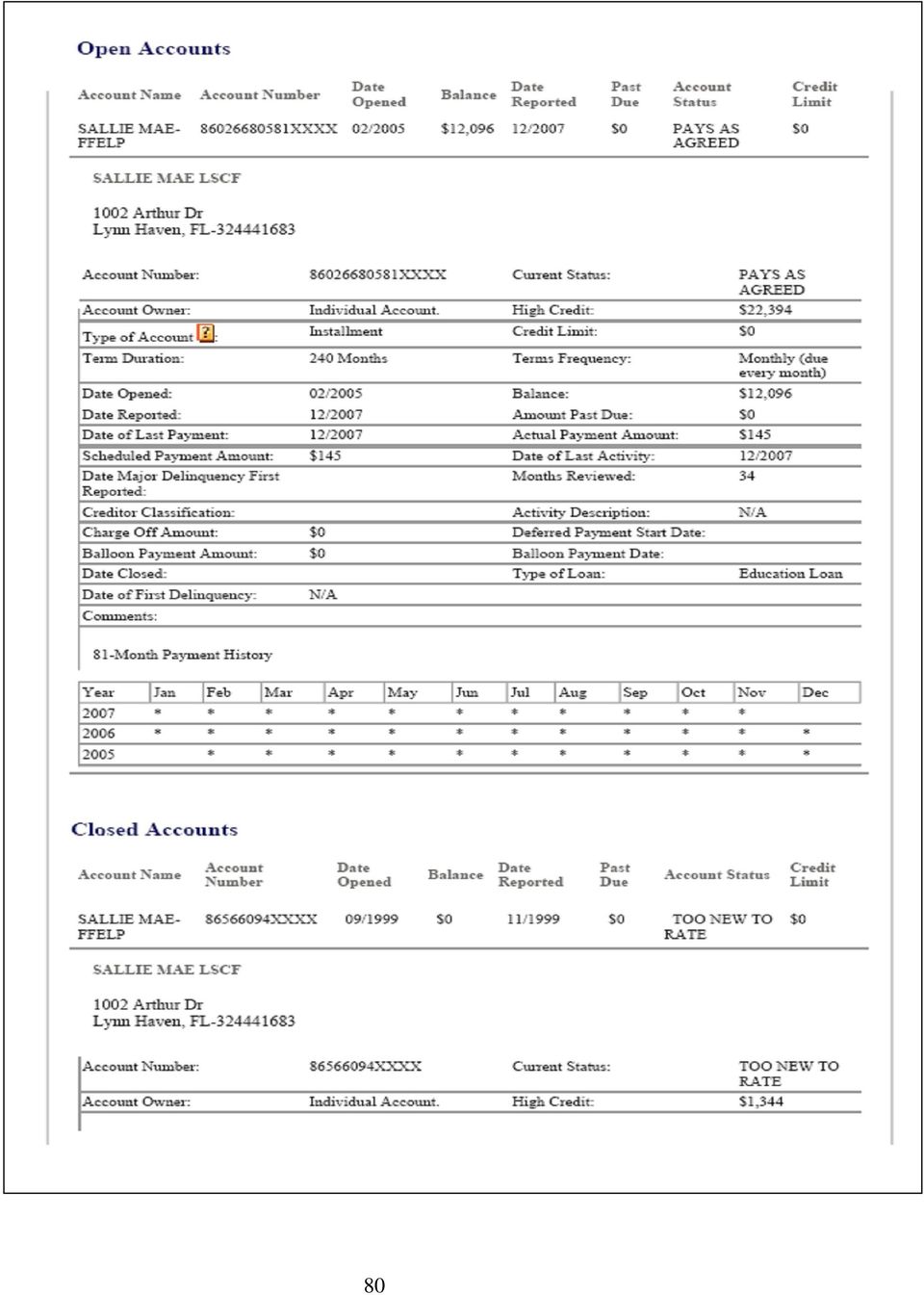

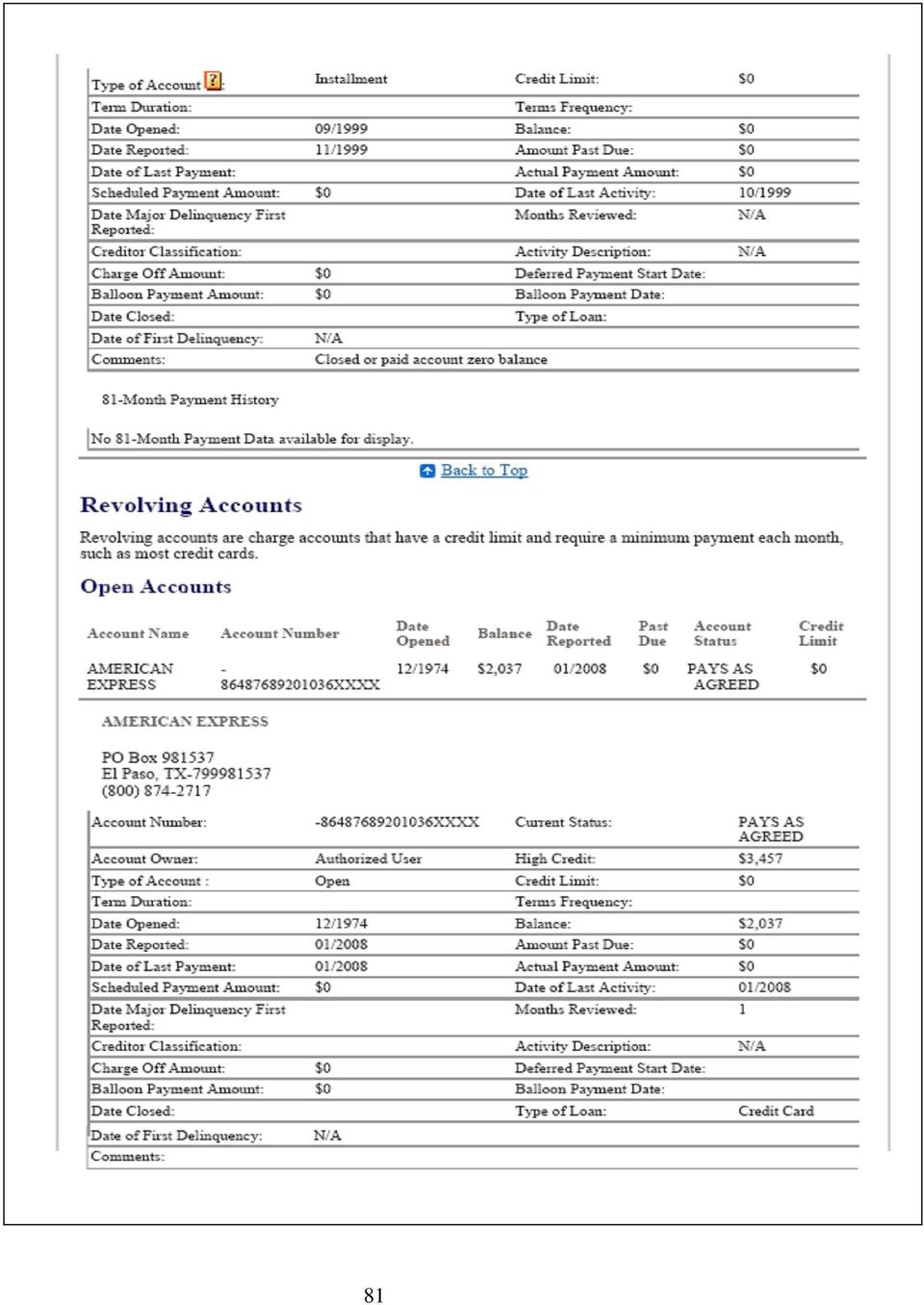

24 93

25 Name Date Explanation: Credit unions, banks, and credit card companies look at three things when they decide if they are going to give you credit and they are Character: This is how a person has paid their bills in the past. Credit card companies find this information about you on your credit report. Capacity: This is how much you can afford to pay every month. Credit Card companies find this our by looking at the application that you filled out. On it you had to write in how much you make in a year, and often what you have pay each month in rent, utilities, and other bills. They want to know that you have enough money left over to pay them each month. Capital: This is what you own (assets) that could be sold to pay them back or money you have in a savings account that could be withdrawn to pay them back. Directions: Put at least one piece of evidence in each box to prove that I either should or shouldn t be approved for a credit card. 94

26 95

27 Name Date Directions We want you to think about the work that you put into this class today. Did you listen and participate? Do you take part in the activities we worked on? How much do you think I should pay you for what you did today? Write out the check below for an amount between one and one hundred dollars depending on how much effort you think you put in today. Thomas Dellwo 6000 Euclid Street Syracuse, NY Date PAY TO THE ORDER OF $ DOLLARS Syracuse Cooperative Federal Credit Union For Eastside Office 723 Westcott Street Syracuse, NY Southside Office 401 South Avenue Syracuse, NY Signature 96

Using Credit to Your Advantage.

Using Credit to Your Advantage. Topic Overview. The Using Credit To Your Advantage topic will provide participants with all the basic information they need to understand credit what it is and how to make

Using Credit to Your Advantage. Topic Overview. The Using Credit To Your Advantage topic will provide participants with all the basic information they need to understand credit what it is and how to make

Materials Lesson Objectives

165 Materials 1. Play money ($2,000 per student) 2. Candy (Different types, 10 per student) 3. Savvy student reward, which is an item perceived by the students to be of greater value than all the candy

165 Materials 1. Play money ($2,000 per student) 2. Candy (Different types, 10 per student) 3. Savvy student reward, which is an item perceived by the students to be of greater value than all the candy

Credit Workshop. What I need to know about credit and lending products of financial institutions. Financial Education Supported by:

Credit Workshop What I need to know about credit and lending products of financial institutions. Financial Education Supported by: Concept Checklist What will I learn today? [ ] What is Credit? [ ] Advantages/

Credit Workshop What I need to know about credit and lending products of financial institutions. Financial Education Supported by: Concept Checklist What will I learn today? [ ] What is Credit? [ ] Advantages/

Using Credit to Your Advantage

Hands on Banking Using Credit to Your Advantage Credit Reports, Credit Scores and Dealing with Debt The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the

Hands on Banking Using Credit to Your Advantage Credit Reports, Credit Scores and Dealing with Debt The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the

Growing Dollars and $ense: Personal Financial Planning Seminar

Growing Dollars and $ense: Personal Financial Planning Seminar The Coalition for Debtor Education Kimberly Allman www.debtoreducati0n.org Email: cde@law.fordham.edu This program is made possible by a grant

Growing Dollars and $ense: Personal Financial Planning Seminar The Coalition for Debtor Education Kimberly Allman www.debtoreducati0n.org Email: cde@law.fordham.edu This program is made possible by a grant

Banking & Budgeting Basics: Making the most of your money

Growing Dollars and $ense Workshops Banking & Budgeting Basics: Making the most of your money Presented by The Coalition for Debtor Education www.debtoreducati0n.org This program is made possible by a

Growing Dollars and $ense Workshops Banking & Budgeting Basics: Making the most of your money Presented by The Coalition for Debtor Education www.debtoreducati0n.org This program is made possible by a

Using Credit Wisely LESSON 14: TEACHERS GUIDE

Using Credit Wisely LESSON 14: TEACHERS GUIDE As teens prepare to enter the financial world, there are many elements for them to consider when it comes to credit. Whether they are off to college in a few

Using Credit Wisely LESSON 14: TEACHERS GUIDE As teens prepare to enter the financial world, there are many elements for them to consider when it comes to credit. Whether they are off to college in a few

Lesson 6: Credit Reports and You Thought Your Report Card Was Important

All About Credit Lesson 6: Credit Reports and You Thought Your Report Card Was Important Standards and Benchmarks (see page C-15) Lesson Description Students read informational text and discuss the advantages

All About Credit Lesson 6: Credit Reports and You Thought Your Report Card Was Important Standards and Benchmarks (see page C-15) Lesson Description Students read informational text and discuss the advantages

SM4-1: Credit Card Application (version 1)

") SM4-1: Credit Card Application (version 1) SM4-1: Credit Card Application (version 1) pg. 1 of 2 SM4-1: Credit Card Application (version 1) continued SM4-1: Credit Card Application (version 1) pg. 2 of

SM4-1: Credit Card Application (version 1) SM4-1: Credit Card Application (version 1) pg. 1 of 2 SM4-1: Credit Card Application (version 1) continued SM4-1: Credit Card Application (version 1) pg. 2 of

How To Understand Credit History

Lesson Description This lesson teaches students why it is important to establish positive credit history; what information can be found on a credit report; how long negative information is retained on

Lesson Description This lesson teaches students why it is important to establish positive credit history; what information can be found on a credit report; how long negative information is retained on

Credit Histories & Credit Scores

Credit Histories & Credit Scores Credit Histories - Definition A continuing record of a borrower s debt commitments and how well they have been honored. (Similar to a transcript) Credit Score - Definition

Credit Histories & Credit Scores Credit Histories - Definition A continuing record of a borrower s debt commitments and how well they have been honored. (Similar to a transcript) Credit Score - Definition

Understanding Credit. Megan Stearns, Credit Counselor

Understanding Credit Megan Stearns, Credit Counselor Obtaining your free credit report will lower your credit score. Closing old accounts can help your credit score. Paying off the balances on your credit

Understanding Credit Megan Stearns, Credit Counselor Obtaining your free credit report will lower your credit score. Closing old accounts can help your credit score. Paying off the balances on your credit

Exercise 4A: What Info Do You Need for a Loan?

Exercise 4A: What Info Do You Need for a Loan? What information do you think is needed to get a loan? Review several samples of loan applications to see what The Cost of Using Credit As mentioned earlier,

Exercise 4A: What Info Do You Need for a Loan? What information do you think is needed to get a loan? Review several samples of loan applications to see what The Cost of Using Credit As mentioned earlier,

What We Need to Know About. Credit Management & Credit Repair for Entrepreneurs

What We Need to Know About. Credit Management & Credit Repair for Entrepreneurs What is Credit? When someone lends you money, and you pay them back with interest, they have extended you credit. Credit

What We Need to Know About. Credit Management & Credit Repair for Entrepreneurs What is Credit? When someone lends you money, and you pay them back with interest, they have extended you credit. Credit

Why Credit is Important

Page 1 Why Credit is Important Page 6 How to Protect Yourself from Identity Theft Page 7 Cosigning and Money Lending Tips Page 8 How to Avoid Credit Card Interest Why Credit is Important Learning to build

Page 1 Why Credit is Important Page 6 How to Protect Yourself from Identity Theft Page 7 Cosigning and Money Lending Tips Page 8 How to Avoid Credit Card Interest Why Credit is Important Learning to build

Credit Cards. and Your Credit Score

Credit Cards and Your Credit Score Introduction Credit Cards and Your Credit Score Learning Objectives Lesson 1 Selecting a Credit Card: The Devil s in the Detail Identify and explain the costs and terms

Credit Cards and Your Credit Score Introduction Credit Cards and Your Credit Score Learning Objectives Lesson 1 Selecting a Credit Card: The Devil s in the Detail Identify and explain the costs and terms

Money Borrowing money

Money Borrowing money Aims: To enable young people to explore ways of borrowing money and the advantages and possible consequences of doing so. Learning Outcomes: By the end of the session the participants

Money Borrowing money Aims: To enable young people to explore ways of borrowing money and the advantages and possible consequences of doing so. Learning Outcomes: By the end of the session the participants

Personal Loans 101: UNDERSTANDING APR

Personal Loans 101: UNDERSTANDING APR In today s world, almost everyone needs access to credit. Whether it is to make a small purchase, pay for an unexpected emergency, repair the car or obtain a mortgage

Personal Loans 101: UNDERSTANDING APR In today s world, almost everyone needs access to credit. Whether it is to make a small purchase, pay for an unexpected emergency, repair the car or obtain a mortgage

The Basics of Building Credit

The Basics of Building Credit This program was developed to help middle school students learn the basics of building credit. At the end of this lesson, you should know about all of the Key Topics below:»

The Basics of Building Credit This program was developed to help middle school students learn the basics of building credit. At the end of this lesson, you should know about all of the Key Topics below:»

Buying with credit lets you purchase something and use it while you are still paying for it.

8) Credit Buying with credit lets you purchase something and use it while you are still paying for it. There are two common types of credit: Credit Cards Offered by credit card companies, department stores

8) Credit Buying with credit lets you purchase something and use it while you are still paying for it. There are two common types of credit: Credit Cards Offered by credit card companies, department stores

3. How to Use Credit

3. How to Use Credit Building a Better Future 103 104 Building a Better Future UNIT 3: HOW TO USE CREDIT Lesson 1: What is Credit? Lesson Objectives: Students will understand why credit is important Students

3. How to Use Credit Building a Better Future 103 104 Building a Better Future UNIT 3: HOW TO USE CREDIT Lesson 1: What is Credit? Lesson Objectives: Students will understand why credit is important Students

Understanding Vehicle Financing

Understanding Vehicle Financing Understanding Vehicle Financing With prices averaging more than $31,000 for a new vehicle and $17,000 for a used model from a dealership, you might consider financing or

Understanding Vehicle Financing Understanding Vehicle Financing With prices averaging more than $31,000 for a new vehicle and $17,000 for a used model from a dealership, you might consider financing or

It lets you pay for expenses you could not afford with cash, such as a college education, a new vehicle, furniture or a home.

USING CREDIT WISELY Credit Is An Important Financial Tool It lets you pay for expenses you could not afford with cash, such as a college education, a new vehicle, furniture or a home.

USING CREDIT WISELY Credit Is An Important Financial Tool It lets you pay for expenses you could not afford with cash, such as a college education, a new vehicle, furniture or a home.

Getting Smart about Credit

Getting Smart about Credit LESSON PREPARATION AND TEACHER INFORMATION Lesson Summary: This lesson is intended for high school students during a 40 minute time period. The lesson teaches students about

Getting Smart about Credit LESSON PREPARATION AND TEACHER INFORMATION Lesson Summary: This lesson is intended for high school students during a 40 minute time period. The lesson teaches students about

THEME TWO: SIGNIFICANCE OF LEARNING, EARNING AND SPENDING ON PERSONAL FINANCIAL WELL-BEING

THEME TWO: SIGNIFICANCE OF LEARNING, EARNING AND SPENDING ON PERSONAL FINANCIAL WELL-BEING LESSON TITLE: Theme 2, Lesson 2: Credit: Friend or Foe? Lesson Description: This lesson will help students evaluate

THEME TWO: SIGNIFICANCE OF LEARNING, EARNING AND SPENDING ON PERSONAL FINANCIAL WELL-BEING LESSON TITLE: Theme 2, Lesson 2: Credit: Friend or Foe? Lesson Description: This lesson will help students evaluate

How do I get good credit?

Slide 1 Credit The information provided in this e-course is intended for educational purposes only and does not constitute specific advice for you as an individual. When evaluating your particular needs,

Slide 1 Credit The information provided in this e-course is intended for educational purposes only and does not constitute specific advice for you as an individual. When evaluating your particular needs,

Understanding Credit. The Three C s of Credit. What is a Credit Bureau?

Understanding Credit By definition, the word credit has to do with trust. This is why credit impacts so many financial issues in our lives including the extension of a loan or credit card, how high an

Understanding Credit By definition, the word credit has to do with trust. This is why credit impacts so many financial issues in our lives including the extension of a loan or credit card, how high an

JUST BEGINNING. Your financial life is. I m Buying a Car!

Your financial life is JUST BEGINNING. The decisions you make now will put a steering wheel and a credit card in your hands. But they will also affect your financial future. Your choices may even prevent

Your financial life is JUST BEGINNING. The decisions you make now will put a steering wheel and a credit card in your hands. But they will also affect your financial future. Your choices may even prevent

Keys to Your Financial Future Step 2.5: Credit Repair or Building Plan

46 MODULE 2: Good credit Keys to Your Financial Future Step 2.5: Credit Repair or Building Plan Use the questions to develop your credit repair or building plan. Do you need to repair your credit history?

46 MODULE 2: Good credit Keys to Your Financial Future Step 2.5: Credit Repair or Building Plan Use the questions to develop your credit repair or building plan. Do you need to repair your credit history?

Credit Card Pros and Cons

Program Name Staff Responsible for Lesson Canton City Schools ABLE/ESOL Dodie Jerzyk Date(s) Used Feb. 15-16, 2011 Civics Category Civics Objective Time Frame II Civic Participation 29 Consumer Economics

Program Name Staff Responsible for Lesson Canton City Schools ABLE/ESOL Dodie Jerzyk Date(s) Used Feb. 15-16, 2011 Civics Category Civics Objective Time Frame II Civic Participation 29 Consumer Economics

GL 04/09. How To Improve Your Credit Score

GL 04/09 How To Improve Your Credit Score Table of Contents 1. What is Credit and What is Debt? 2. The 4 C S of Credit 3. Keeping Score With Your Credit 4. The FICO Score Breakdown 5. How to Rebuild Your

GL 04/09 How To Improve Your Credit Score Table of Contents 1. What is Credit and What is Debt? 2. The 4 C S of Credit 3. Keeping Score With Your Credit 4. The FICO Score Breakdown 5. How to Rebuild Your

YOUR FINANCIAL ROAD MAP: WHERE DO YOU WANT TO GO?

YOUR FINANCIAL ROAD MAP: WHERE DO YOU WANT TO GO? DAY: 9 TITLE: YOUR FINANCIAL ROAD MAP Credit: New Rules, Scores & Debt TARGET COMPETENCY: Select strategies to use in handling credit and managing debt

YOUR FINANCIAL ROAD MAP: WHERE DO YOU WANT TO GO? DAY: 9 TITLE: YOUR FINANCIAL ROAD MAP Credit: New Rules, Scores & Debt TARGET COMPETENCY: Select strategies to use in handling credit and managing debt

Remember the Interest

STUDENT MODULE 7.1 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. Remember the Interest Mom, it is not fair. If Bill can

STUDENT MODULE 7.1 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. Remember the Interest Mom, it is not fair. If Bill can

Key points to remember when using this template:

Writing a business plan is hard work. One professional estimates it s as hard as writing a novel. To assist you in preparing your plan, we ve prepared the following Business Plan Questionnaire. Please

Writing a business plan is hard work. One professional estimates it s as hard as writing a novel. To assist you in preparing your plan, we ve prepared the following Business Plan Questionnaire. Please

Lesson 5: Renting vs. Buying Home Sweet Home

Lesson 5: Renting vs. Buying Home Sweet Home All the materials and information included in this presentation is provided for educational and illustrative purposes only and is presented with the express

Lesson 5: Renting vs. Buying Home Sweet Home All the materials and information included in this presentation is provided for educational and illustrative purposes only and is presented with the express

Beginner/Low-Intermediate. Credit Materials. Bad Credit No Loan! Overhead 2-A. Picture Story Bad Credit No Loan!

Beginner & Low-Intermediate Credit Materials Picture Story Bad Credit No Loan! Overhead 2-A Picture Story Bad Credit No Loan! www.valrc.org/courses/moneytalks Beginner/Low-Intermediate Unit II: Planning

Beginner & Low-Intermediate Credit Materials Picture Story Bad Credit No Loan! Overhead 2-A Picture Story Bad Credit No Loan! www.valrc.org/courses/moneytalks Beginner/Low-Intermediate Unit II: Planning

Your Money Matters! Financial Literacy Teacher Guide. Thanks to TD for helping us bring this resource to schools for free.

Your Money Matters! Financial Literacy Teacher Guide 2 Table of Contents: Introduction...3 Toronto Star epaper...4 Financial Awareness Inventory...5 SPENDING To Spend or Not to Spend Activity...6 I Need

Your Money Matters! Financial Literacy Teacher Guide 2 Table of Contents: Introduction...3 Toronto Star epaper...4 Financial Awareness Inventory...5 SPENDING To Spend or Not to Spend Activity...6 I Need

MANAGING CREDIT101 TM %*'9 [[[ EPXEREJGY SVK i

MANAGING CREDIT101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

MANAGING CREDIT101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

Thank you so much for having me. I m really excited to be here today.

Welcome to The Boomer Business Owner. My guest today is Ty Crandall. Ty is an honorary Baby Boomer, internationally known speaker, author, and business credit expert. With over 16 years of financial experience,

Welcome to The Boomer Business Owner. My guest today is Ty Crandall. Ty is an honorary Baby Boomer, internationally known speaker, author, and business credit expert. With over 16 years of financial experience,

What s in My Credit Report?... 1. Taking Care of Your Score... 3. How Do I Get Credit?... 4. Understanding Credit Cards... 5

The Credit 411 Contents What s in My Credit Report?... 1 Taking Care of Your Score... How Do I Get Credit?... 4 Understanding Credit Cards... 5 Protecting Your Credit... Thinking About Filing Bankruptcy?...

The Credit 411 Contents What s in My Credit Report?... 1 Taking Care of Your Score... How Do I Get Credit?... 4 Understanding Credit Cards... 5 Protecting Your Credit... Thinking About Filing Bankruptcy?...

Maureen Baran SVP Business Development. Kris Bona Business Relationship Officer

Williams College Maureen Baran SVP Business Development Kris Bona Business Relationship Officer Agenda What is credit and why is it so important? Credit reports and credit scores Building credit Comparing

Williams College Maureen Baran SVP Business Development Kris Bona Business Relationship Officer Agenda What is credit and why is it so important? Credit reports and credit scores Building credit Comparing

Your Credit Report. Trade lines. The bulk of a credit report is dedicated to your history of handling credit. It includes:

Your Credit Report The three major credit bureaus in the United States are Experian, TransUnion, and Equifax. These companies acquire data from banks, credit unions, mortgage lenders, and retail establishments.

Your Credit Report The three major credit bureaus in the United States are Experian, TransUnion, and Equifax. These companies acquire data from banks, credit unions, mortgage lenders, and retail establishments.

CREDIT BASICS About your credit score

CREDIT BASICS About your credit score Your credit score influences the credit that s available to you and the terms (interest rate, etc.) that lenders offer you. It s a vital part of your credit health.

CREDIT BASICS About your credit score Your credit score influences the credit that s available to you and the terms (interest rate, etc.) that lenders offer you. It s a vital part of your credit health.

Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money.

TEACHER GUIDE 7.2 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. It Is In Your Interest Priority Academic Student Skills

TEACHER GUIDE 7.2 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. It Is In Your Interest Priority Academic Student Skills

u n i t f i v e Credit: Buy Now, Pay Later To use credit wisely you need to know oming soon to a what s really

Unit Five Credit: Buy Now, Pay Later To use credit wisely you C need to know oming soon to a what s really mailbox near you credit card offers! involved. If you haven t started receiving them already,

Unit Five Credit: Buy Now, Pay Later To use credit wisely you C need to know oming soon to a what s really mailbox near you credit card offers! involved. If you haven t started receiving them already,

Establishing Credit Smart investing@your library Series

4 Establishing Credit Credit is the opportunity to borrow money to use now and then repay over time at an agreed upon cost. It s a convenience and an important financial tool if used wisely. Smart investing@your

4 Establishing Credit Credit is the opportunity to borrow money to use now and then repay over time at an agreed upon cost. It s a convenience and an important financial tool if used wisely. Smart investing@your

How To Get A Credit Report From A Credit Card To A Credit Rating Card

Credit Report Info Packet Information in this Packet What Is a Credit Report?.....................3 What Is a Credit Score?..................... 4 Who Can See Your Credit Report?.............. 5 Ordering

Credit Report Info Packet Information in this Packet What Is a Credit Report?.....................3 What Is a Credit Score?..................... 4 Who Can See Your Credit Report?.............. 5 Ordering

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account.

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account. Account fee the amount charged by a financial institution for the

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account. Account fee the amount charged by a financial institution for the

Lesson Objectives. Procedure

97 Materials 1. Car Advertisements (magazines, downloaded video from the internet, or taped from TV) 2. Deciding What You Want Worksheet 3. Loan Calculations Sheet 4. Don t Abuse Your Credit Story 5. Dry

97 Materials 1. Car Advertisements (magazines, downloaded video from the internet, or taped from TV) 2. Deciding What You Want Worksheet 3. Loan Calculations Sheet 4. Don t Abuse Your Credit Story 5. Dry

A crash course in credit

A crash course in credit Ever get the feeling that you re being watched? That someone s keeping an eye on how you handle your money? Well, you re not just imagining things. Banks, credit card companies,

A crash course in credit Ever get the feeling that you re being watched? That someone s keeping an eye on how you handle your money? Well, you re not just imagining things. Banks, credit card companies,

IMPORTANCE OF CREDIT HISTORY AND SUCCESSFUL SAVING

IMPORTANCE OF CREDIT HISTORY AND SUCCESSFUL SAVING From America Saves and Experian WHAT IS A CREDIT REPORT AND SCORE? A credit score is a three digit number that measures how likely you are to repay a

IMPORTANCE OF CREDIT HISTORY AND SUCCESSFUL SAVING From America Saves and Experian WHAT IS A CREDIT REPORT AND SCORE? A credit score is a three digit number that measures how likely you are to repay a

GET CREDITWISE SM SM

GET CREDITWISE SM SM Table Of Contents October, 2006 Credit Matters 1 An introduction Establishing Credit 3 Begin building a solid financial base Using Credit Wisely 5 Narrowing your options Monitoring

GET CREDITWISE SM SM Table Of Contents October, 2006 Credit Matters 1 An introduction Establishing Credit 3 Begin building a solid financial base Using Credit Wisely 5 Narrowing your options Monitoring

Fun, engaging and effective. Aligned with national financial education and core curriculum requirements.

Building Your Financial Foundation Adult Level Curriculum - Instructors Guide Fun, engaging and effective. Aligned with national financial education and core curriculum requirements. Lessons on: Credit

Building Your Financial Foundation Adult Level Curriculum - Instructors Guide Fun, engaging and effective. Aligned with national financial education and core curriculum requirements. Lessons on: Credit

Business Start-Up Basics II

Business Start-Up Basics II P R E B U S I N E S S P L A N P R E P A R A T I O N Presented by: SBDC Business Advisors Lisa Hutson Ana Badillo Susan Patton Agenda 1. Determine financing needs a. Discuss

Business Start-Up Basics II P R E B U S I N E S S P L A N P R E P A R A T I O N Presented by: SBDC Business Advisors Lisa Hutson Ana Badillo Susan Patton Agenda 1. Determine financing needs a. Discuss

Credit Repair Made Easy

Credit Repair Made Easy A simple self help guide to credit repair By Don Troiano Introduction My name is Don Troiano and I spent over 15 years in the mortgage industry. Knowing how to guide customers in

Credit Repair Made Easy A simple self help guide to credit repair By Don Troiano Introduction My name is Don Troiano and I spent over 15 years in the mortgage industry. Knowing how to guide customers in

Lesson 11 Take Control of Debt: Are You Credit Worthy? Check Your Credit Report

Lesson 11 Take Control of Debt: Are You Credit Worthy? Check Your Credit Report Lesson Description Students take on the role of lender in the introduction to this lesson as they consider the information

Lesson 11 Take Control of Debt: Are You Credit Worthy? Check Your Credit Report Lesson Description Students take on the role of lender in the introduction to this lesson as they consider the information

Credit History and Ratings

Credit History and Ratings Course Title Money Matters Lesson Title Credit History and Ratings Performance Objectives: Understand and manage credit responsibly. Specific Objective : As a result of this

Credit History and Ratings Course Title Money Matters Lesson Title Credit History and Ratings Performance Objectives: Understand and manage credit responsibly. Specific Objective : As a result of this

Personal Credit Recovery Program

Personal Credit Recovery Program Program Benefits Get 24/7 online access to your personal credit report and score Learn at your own pace by working through our self-study credit rebuilding guide Access

Personal Credit Recovery Program Program Benefits Get 24/7 online access to your personal credit report and score Learn at your own pace by working through our self-study credit rebuilding guide Access

Understanding Credit Cards

Understanding Credit Cards INTRODUCTION This brochure can help you understand how credit cards work, become familiar with common terms offered with a credit card, and avoid the dangers of using credit

Understanding Credit Cards INTRODUCTION This brochure can help you understand how credit cards work, become familiar with common terms offered with a credit card, and avoid the dangers of using credit

Solving the Credit Puzzle. L G & W Federal Credit Union

Solving the Credit Puzzle L G & W Federal Credit Union Knowledge Check How much do you already know about credit scoring? Sample Credit Report Credit Bureaus Equifax TransUnion Experian Who Can Pull Your

Solving the Credit Puzzle L G & W Federal Credit Union Knowledge Check How much do you already know about credit scoring? Sample Credit Report Credit Bureaus Equifax TransUnion Experian Who Can Pull Your

YOUR GOOD CREDIT The Importance of Your Credit Report and Your Credit Score Maintain Good Credit Combat Identity Theft FACT Act Rights

YOUR GOOD CREDIT The Importance of Your Credit Report and Your Credit Score Maintain Good Credit Combat Identity Theft FACT Act Rights WHY YOU NEED TO KNOW ABOUT CREDIT REPORTS & CREDIT SCORES Having good

YOUR GOOD CREDIT The Importance of Your Credit Report and Your Credit Score Maintain Good Credit Combat Identity Theft FACT Act Rights WHY YOU NEED TO KNOW ABOUT CREDIT REPORTS & CREDIT SCORES Having good

Hofstra North Shore-LIJ School of Medicine. Office of Financial Aid

Hofstra North Shore-LIJ School of Medicine Office of Financial Aid Consumer Credit and Your Credit Report Joseph M. Nicolini, MHA Director of Financial Aid What We Will Cover Consumer credit and credit

Hofstra North Shore-LIJ School of Medicine Office of Financial Aid Consumer Credit and Your Credit Report Joseph M. Nicolini, MHA Director of Financial Aid What We Will Cover Consumer credit and credit

Lesson 2: Savings and Financial Institution Knowledge Making the Most of Your Money

Lesson 2: Savings and Financial Institution Knowledge Making the Most of Your Money All the materials and information included in this presentation is provided for educational and illustrative purposes

Lesson 2: Savings and Financial Institution Knowledge Making the Most of Your Money All the materials and information included in this presentation is provided for educational and illustrative purposes

Credit: The Good and the Bad

Managing Your Credit Effectively Credit can be a valuable addition to your financial toolbox if you use it carefully and sensibly. Credit means someone is willing to loan you money called Principal in

Managing Your Credit Effectively Credit can be a valuable addition to your financial toolbox if you use it carefully and sensibly. Credit means someone is willing to loan you money called Principal in

Participant Guide Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum

Charge It Right Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Credit Cards and Debit Cards 1 Other Cards 2 Sample Truth in Lending Disclosure Statement

Charge It Right Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum TABLE OF CONTENTS Page Credit Cards and Debit Cards 1 Other Cards 2 Sample Truth in Lending Disclosure Statement

Familiarize yourself with laws that authorize and regulate vehicle dealership financing and leasing.

W ith prices averaging more than $28,000 for a new vehicle and $15,000 for a used vehicle, most consumers need financing or leasing to acquire a vehicle. In some cases, buyers use direct lending: they

W ith prices averaging more than $28,000 for a new vehicle and $15,000 for a used vehicle, most consumers need financing or leasing to acquire a vehicle. In some cases, buyers use direct lending: they

Life Insurance Buyer's Guide

United of Omaha Life Insurance Company Life Insurance Buyer s Guide Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association

United of Omaha Life Insurance Company Life Insurance Buyer s Guide Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association

DAILY ASSESMENTS: Answer Key

DAILY ASSESMENTS: Answer Key DAY 1: Your Financial Road Map Getting Started 1. Russell Simmons is referred to as an entrepreneur? Provide a definition or example of an entrepreneur. (A: An entrepreneur

DAILY ASSESMENTS: Answer Key DAY 1: Your Financial Road Map Getting Started 1. Russell Simmons is referred to as an entrepreneur? Provide a definition or example of an entrepreneur. (A: An entrepreneur

Life Insurance Buyer s Guide

Life Insurance Buyer s Guide This guide can show you how to save money when you shop for life insurance. It helps you to: - Decide how much life insurance you should buy, - Decide what kind of life insurance

Life Insurance Buyer s Guide This guide can show you how to save money when you shop for life insurance. It helps you to: - Decide how much life insurance you should buy, - Decide what kind of life insurance

Introducing the Credit Card

Introducing the Credit Card This program was designed with high school students in mind. It goes over everything you need to know before you get your first credit card so you can manage it wisely.» Key

Introducing the Credit Card This program was designed with high school students in mind. It goes over everything you need to know before you get your first credit card so you can manage it wisely.» Key

Understanding a Credit Report! April 21, 2011. New York City Department of Consumer Affairs. All rights reserved.

Understanding a Credit Report! Questions to Think About What are the different types of credit and why is credit important? What is a credit report? How does credit impact future financial goals? 3 What

Understanding a Credit Report! Questions to Think About What are the different types of credit and why is credit important? What is a credit report? How does credit impact future financial goals? 3 What

Keeping Score: Why Credit Matters

Keeping Score: Why Credit Matters LESSON 6: TEACHERS GUIDE In the middle of a championship football game, keeping score is the norm. But when it comes to life, many young adults don t realize how important

Keeping Score: Why Credit Matters LESSON 6: TEACHERS GUIDE In the middle of a championship football game, keeping score is the norm. But when it comes to life, many young adults don t realize how important

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

Credit Scoring. 1-800-444-RATE www.gogsf.com

Credit Scoring 1-800-444-RATE www.gogsf.com Your credit score is a major factor that will be considered by the lender when they review your loan application. They want to know what your credit history

Credit Scoring 1-800-444-RATE www.gogsf.com Your credit score is a major factor that will be considered by the lender when they review your loan application. They want to know what your credit history

Financial Literacy. Credit is widely misunderstood and, perhaps even more to the point, widely misused. - Author Unknown. Section V.

Credit is widely misunderstood and, perhaps even more to the point, widely misused. - Author Unknown Section V Credit 113 Credit: Friend or Foe? Families today do not spend much time together talking about

Credit is widely misunderstood and, perhaps even more to the point, widely misused. - Author Unknown Section V Credit 113 Credit: Friend or Foe? Families today do not spend much time together talking about

Introduction The History of Credit Scoring Why Your Credit Score is So Important

Introduction The subject of credit scoring has become an increasingly hot topic, and for good reason. For many years, the general public only associated the concept of credit scoring with the need to purchase

Introduction The subject of credit scoring has become an increasingly hot topic, and for good reason. For many years, the general public only associated the concept of credit scoring with the need to purchase

SHORT SALES Frequently Asked Questions

SHORT SALES Frequently Asked Questions This factsheet is provided for information purposes only. It is not a substitute for advice from legal, accounting, housing, or real estate professionals. Please

SHORT SALES Frequently Asked Questions This factsheet is provided for information purposes only. It is not a substitute for advice from legal, accounting, housing, or real estate professionals. Please

Credit Scoring and Wealth

the Problem In most games, it is wise to understand the rules before you begin to play. What if you weren t aware that you were playing a game? What if you had not choice whether to play or not? Everyone

the Problem In most games, it is wise to understand the rules before you begin to play. What if you weren t aware that you were playing a game? What if you had not choice whether to play or not? Everyone

FINANCIAL LITERACY WORKSHOP 2 Credit and Debt 1 Facilitator Needed Estimated Time: 1 hr 50 min

FINANCIAL LITERACY WORKSHOP 2 Credit and Debt 1 Facilitator Needed Estimated Time: 1 hr 50 min Things to Prepare BEFORE THE WORKSHOP ITEM APPENDIX # PAGE # USED Flip Chart 2-1 A-2-1 2-3 Flip Chart 2-2

FINANCIAL LITERACY WORKSHOP 2 Credit and Debt 1 Facilitator Needed Estimated Time: 1 hr 50 min Things to Prepare BEFORE THE WORKSHOP ITEM APPENDIX # PAGE # USED Flip Chart 2-1 A-2-1 2-3 Flip Chart 2-2

Your Credit Score What It Means to You as a Prospective Home Buyer

Dan L' Altrella Certified Mortgage Planner L'Altrella Lending Group Phone: 203.521.2905 Fax: 203.712.1188 danlaltrella@yahoo.com Your Credit Score What It Means to You as a Prospective Home Buyer Introduction

Dan L' Altrella Certified Mortgage Planner L'Altrella Lending Group Phone: 203.521.2905 Fax: 203.712.1188 danlaltrella@yahoo.com Your Credit Score What It Means to You as a Prospective Home Buyer Introduction

PRACTICAL MONEY GUIDES CREDIT HISTORY. Your credit history and how it affects your future

PRACTICAL MONEY GUIDES CREDIT HISTORY Your credit history and how it affects your future YOUR CREDIT HISTORY THE RECORD OF HOW WELL YOU HANDLE CREDIT To get a glimpse of your financial future, many businesses

PRACTICAL MONEY GUIDES CREDIT HISTORY Your credit history and how it affects your future YOUR CREDIT HISTORY THE RECORD OF HOW WELL YOU HANDLE CREDIT To get a glimpse of your financial future, many businesses

STUDENT MODULE 8.1 ONLINE SHOPPING AND CREDIT CARDS PAGE 1

STUDENT MODULE 8.1 ONLINE SHOPPING AND CREDIT CARDS PAGE 1 Standard 8: The student will describe and explain interest, credit cards, and online commerce. Credit Cards: More Than Plastic Austin receives

STUDENT MODULE 8.1 ONLINE SHOPPING AND CREDIT CARDS PAGE 1 Standard 8: The student will describe and explain interest, credit cards, and online commerce. Credit Cards: More Than Plastic Austin receives

Budgeting for Home Ownership

A HOME FOR YOUR FAMILY 7 Budgeting for Home Ownership Perhaps you are just beginning to think about buying a home sometime in the future. Or maybe you have already found a home you would like to buy. Whether

A HOME FOR YOUR FAMILY 7 Budgeting for Home Ownership Perhaps you are just beginning to think about buying a home sometime in the future. Or maybe you have already found a home you would like to buy. Whether

In July 2010, credit card rules will change. In the meantime, here is a guide to current rules, with information about the changes to come, to help

2 In July 2010, credit card rules will change. In the meantime, here is a guide to current rules, with information about the changes to come, to help you when you consider which credit card offer you might

2 In July 2010, credit card rules will change. In the meantime, here is a guide to current rules, with information about the changes to come, to help you when you consider which credit card offer you might

Teacher's Guide. Lesson Six. Banking Services 04/09

Teacher's Guide $ Lesson Six Banking Services 04/09 banking services websites Students will make wise choices about their banking services once they understand such fundamentals as: selecting and managing

Teacher's Guide $ Lesson Six Banking Services 04/09 banking services websites Students will make wise choices about their banking services once they understand such fundamentals as: selecting and managing

HOW TO BOOST YOUR CREDIT IN 30 DAYS OR LESS

HOW TO BOOST YOUR CREDIT IN 30 DAYS OR LESS By The Arizona Credit Law Group, PLLC A consumer rights law firm Learn how to improve your credit using 5 simple rules No tricks, no gimmicks, just facts. The

HOW TO BOOST YOUR CREDIT IN 30 DAYS OR LESS By The Arizona Credit Law Group, PLLC A consumer rights law firm Learn how to improve your credit using 5 simple rules No tricks, no gimmicks, just facts. The

The AFI Resource Center is pleased to provide this presentation about credit reports.

The AFI Resource Center is pleased to provide this presentation about credit reports. This is one of several presentations developed for AFI grantees on a variety of financial education topics, including

The AFI Resource Center is pleased to provide this presentation about credit reports. This is one of several presentations developed for AFI grantees on a variety of financial education topics, including

This page intentionally left blank.

This page intentionally left blank. CreditSmart Module 6: Understanding Credit Scoring Table of Contents Welcome to Freddie Mac s CreditSmart Initiative... 4 Program Structure... 4 Using the Instructor

This page intentionally left blank. CreditSmart Module 6: Understanding Credit Scoring Table of Contents Welcome to Freddie Mac s CreditSmart Initiative... 4 Program Structure... 4 Using the Instructor

The ABCs of Credit Credit Scores Establishing Credit Maintaining Good Credit Credit Cards Managing Credit Challenges

The ABCs of Credit Credit Scores Establishing Credit Maintaining Good Credit Credit Cards Managing Credit Challenges CREDIT DEFINITIONS Credit Trust given to another person for future payment of a loan,

The ABCs of Credit Credit Scores Establishing Credit Maintaining Good Credit Credit Cards Managing Credit Challenges CREDIT DEFINITIONS Credit Trust given to another person for future payment of a loan,

BIZ KID$ Program 115: Credit (The Good, the Bad, and the Ugly)

") BIZ KID$ Program 115: (The Good, the Bad, and the Ugly) Introduction Explain that Biz Kid$ is a program to help people become financially educated, learn work-readiness skills, and to even become entrepreneurs

BIZ KID$ Program 115: (The Good, the Bad, and the Ugly) Introduction Explain that Biz Kid$ is a program to help people become financially educated, learn work-readiness skills, and to even become entrepreneurs

Improve Your Credit Put Bad Credit Behind You

Improve Your Credit Put Bad Credit Behind You Improve your credit While it s possible to get by without credit, access to credit is essential for buying a home, financing a car or getting a credit card.

Improve Your Credit Put Bad Credit Behind You Improve your credit While it s possible to get by without credit, access to credit is essential for buying a home, financing a car or getting a credit card.

Part 4: Borrowing Money and Using Credit

Part 4: Borrowing Money and Using Credit CHAPTER 11: Borrowing Money Let s discuss... $ Why people borrow more money today than in the past $ Why people borrow money $ Types of debt/credit $ The cost

Part 4: Borrowing Money and Using Credit CHAPTER 11: Borrowing Money Let s discuss... $ Why people borrow more money today than in the past $ Why people borrow money $ Types of debt/credit $ The cost

Using Credit to Your Advantage Credit Cards and Loans Participant Guide

Hands on Banking Using Credit to Your Advantage The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the program anytime at www.handsonbanking.org & www.elfuturoentusmanos.org

Hands on Banking Using Credit to Your Advantage The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the program anytime at www.handsonbanking.org & www.elfuturoentusmanos.org

Tracking Your Credit History By Mark Schug

By Mark Schug Financial institutions (banks, savings and loan associations, credit unions, and consumer finance companies) are private, profit seeking businesses. They expect to be paid back most of the

By Mark Schug Financial institutions (banks, savings and loan associations, credit unions, and consumer finance companies) are private, profit seeking businesses. They expect to be paid back most of the

Personal Money Management. Why and How we spend money and potential impacts to personal credit.

Personal Money Management Why and How we spend money and potential impacts to personal credit. Presentation Objectives Understanding Your Financial Personality Personal Credit Scores, impacts, tips, your

Personal Money Management Why and How we spend money and potential impacts to personal credit. Presentation Objectives Understanding Your Financial Personality Personal Credit Scores, impacts, tips, your

GOD S SOLUTION TO DEBT

GOD S SOLUTION TO DEBT KEY VERSE: Let no debt remain outstanding, except the continuing debt to love one another, for he who loves his fellowman has fulfilled the law. (Romans 13:8 NIV) Pay all your debts

GOD S SOLUTION TO DEBT KEY VERSE: Let no debt remain outstanding, except the continuing debt to love one another, for he who loves his fellowman has fulfilled the law. (Romans 13:8 NIV) Pay all your debts

Take control of your credit score

Take control of your credit score A guide to understanding and improving your credit. What is a credit score? Your credit score is a number between 300 and 850, assigned to you by a credit bureau, that

Take control of your credit score A guide to understanding and improving your credit. What is a credit score? Your credit score is a number between 300 and 850, assigned to you by a credit bureau, that

Credit arrangements can be formal or informal. The three most common types of credit used by consumers are described below.

1-888-842-6328 For toll-free numbers when overseas, visit Collect internationally 1-703-255-8837 TDD for hearing impaired 1-888-869-5863 Credit Wise Credit: a Useful Tool Most of us use consumer credit

1-888-842-6328 For toll-free numbers when overseas, visit Collect internationally 1-703-255-8837 TDD for hearing impaired 1-888-869-5863 Credit Wise Credit: a Useful Tool Most of us use consumer credit

Understanding Credit

Understanding Credit Topics covered: Establishing Credit Credit Scores Repairing Credit Why is credit necessary? Applying for a loan Applying for a credit card Applying for a mortgage Renting an apartment/house

Understanding Credit Topics covered: Establishing Credit Credit Scores Repairing Credit Why is credit necessary? Applying for a loan Applying for a credit card Applying for a mortgage Renting an apartment/house

The Better Business Bureau. Student Assistance Foundation present. Common $ense. Tips to make college successful

The Better Business Bureau & Student Assistance Foundation present Common $ense Tips to make college successful You will leave so smart in these areas: Credit Identity Theft On Your Own Budgeting Let s

The Better Business Bureau & Student Assistance Foundation present Common $ense Tips to make college successful You will leave so smart in these areas: Credit Identity Theft On Your Own Budgeting Let s