SUN 82 Financial Management: The Path to Profitability. Presenter. Steve L. Wintner, AIA Emeritus. Management Consulting Services The Woodlands, TX

|

|

|

- Rodney Snow

- 8 years ago

- Views:

Transcription

1 SUN 82 Financial Management: The Path to Profitability Presenter Steve L. Wintner, AIA Emeritus Management Consulting Services The Woodlands, TX Copyright Materials This presentation is protected by US and International Copyright laws. Reproduction, distribution, display and use of the presentation without written permission of the speaker is prohibited. The American Society of Landscape Architects 1

2 Learning Objectives Upon completion of this program, attendees will be able to: explain how to develop an annual budget and the metrics that will establish the overhead and break-even rate for every employee. explain how to develop project fee budgets based on value-added service, not just time-to-complete compensation, leading to a fee negotiating strategy that ensures a win-win outcome every time. determine how to set up, interpret, and evaluate the Profit-Loss and Balance Sheet Statement so trends can be recognized, the balance between workload and staff size can be assessed, and overhead more effectively managed and controlled. explain how eleven (11) key financial performance indicators can be calculated. Overview Introduction / Framing Remarks Glossary of Key Accounting Terms Annual Budget Operating Expenses Net Operating Revenue (N.O.R.) / Balancing the Buckets Top Down / Bottom Up Project Fee Budgeting Economic Axioms Value-based Compensation Formulating Billing Rates (overhead, break-even rates) Profit/Loss (Income) Statement P-L Analysis: Component Elements of N.O.R. Seven (7) Key Financial Performance Indicators Balance Sheet Balance Sheet Analysis Four (4) Key Financial Performance Indicators 2

3 The Genesis of Knowledge Knowledge is power. - Sir Francis Bacon The Genesis of Knowledge Knowledge is power. - Sir Francis Bacon is an incomplete statement. 3

4 Glossary of Key Accounting Terms Accounts Payable: Expenses incurred and owed to others, including consultants. Accounts Receivable: Unpaid project invoices previously sent to clients. Aging: 31 to 90+ days. Accrual Basis Accounting: Fees earned, consultant's fees and expenses obligated and/or incurred, whether billed or not; and whether paid or not. Most firms use a modified accrual basis for their Profit-Loss (Income) Statement. This means revenue and expenses are based on invoiced amounts. Accrual accounting should never be used for determining tax liability (see Cash Basis Accounting). Annual Budget: A projection of future financial activity that includes projected revenue, consultant s fees, reimbursable and direct project expenses, salaries and other operating expenses for 12 months (fiscal or calendar year). Backlog: The dollar amount of existing contracts not yet billed, at a given point in time (changes continually). Balance Sheet: The financial status of the firm for a specific period of time (usually the current month and year-to-date). Billing Rate: The dollar amount that your firm charges for an hour of labor spent on projects, including salary, overhead, benefits, and profit. Break-Even Rate: The cost of doing business for every dollar of project labor spent (overhead rate + benefits + salary); also known as Billing Cost. Glossary of Key Accounting Terms Cash Basis Accounting: Actual revenue received and actual salaries and expenses paid (a checkbook approach). This is the basis most commonly used for determining income tax liability. Current: Either an Asset or a Liability that is realized within the next 12 months. Direct Expense: Project-related expenses, not reimbursable. These would also include expenses in Lump Sum Fee basis projects, or those which are not able to be invoiced to the client, per the Contract. Direct Labor: Same as Direct Salary. Represents the salary cost of time charged to projects, whether billed or not. Indirect Expense: Overhead or non-project related operating expenses (includes Indirect Labor). Indirect Labor: Same as Indirect Salary. Represents the salary cost of time spent on non-project related activities (by all members of the firm). Liabilities: Short-term (12-months) and long-term (beyond than 12 months) debt and any other monies owed. Line of Credit: Money extended by a financial institution. Usually collateralized by the firm s Accounts Receivables. 4

.")

5 Glossary of Key Accounting Terms Net Multiplier: The Revenue generated for every $ of Direct Labor. Net Profit: Profit before Distributions & Taxes. Net Operating Revenue: Revenue, including any Mark-Up invoiced, after deducting Project Consultant fees and all project related expenses owed. Overhead Rate: Total Indirect Expenses divided by Total Direct Labor. Proposals Pending: Proposals sent to potential Clients for potential projects. Reimbursable Expenses: Project-related expenses that are invoiced to the client in addition to fees. Appropriately would also include mark-up percentage on those expenses. Mark-Up becomes a part of Net Operating Revenue and adds to profit. Retained Earnings: Cumulative Profit-Loss since the inception of the firm. Retainer: Also referred to as Initial Payment, paid to firm at the outset of the project, per Contract, before work has started. Shown on Balance Sheet as a Liability for Unearned Income and invoiced at end of project. Preparing the Annual Budget 5

6 Preparing the Annual Budget Preparing the Annual Budget 6

7 Maintaining N.O.R. Balancing the Buckets Budget Format: Revenue, Direct Labor, Indirect Expenses 7

8 Budget Format: Revenue, Direct Labor, Indirect Expenses Budget Format: Revenue, Direct Labor, Indirect Expenses 8

9 Summary (Collapsed) Budget Format Annual Profit Plan 400 9

10 Annual Profit Plan Net Operating Revenue Annual Profit Plan Calculating Multipliers 10

11 Project Fee Budgeting Economic Axioms It s unwise to pay too much, but it s worse to pay too little. For when you pay too little, you sometimes lose everything, because what you paid for is incapable of doing what it was bought to do. The common law of business balance prohibits paying a little and getting a lot; it can t be done. If you deal with the lowest bidder, it is wise to add something for the risk you take and if you do that you might as well pay for something better. - John Ruskin, The Price Perspective The bitterness of poor quality lingers long after the sweetness of a cheap price is forgotten. - anonymous 11

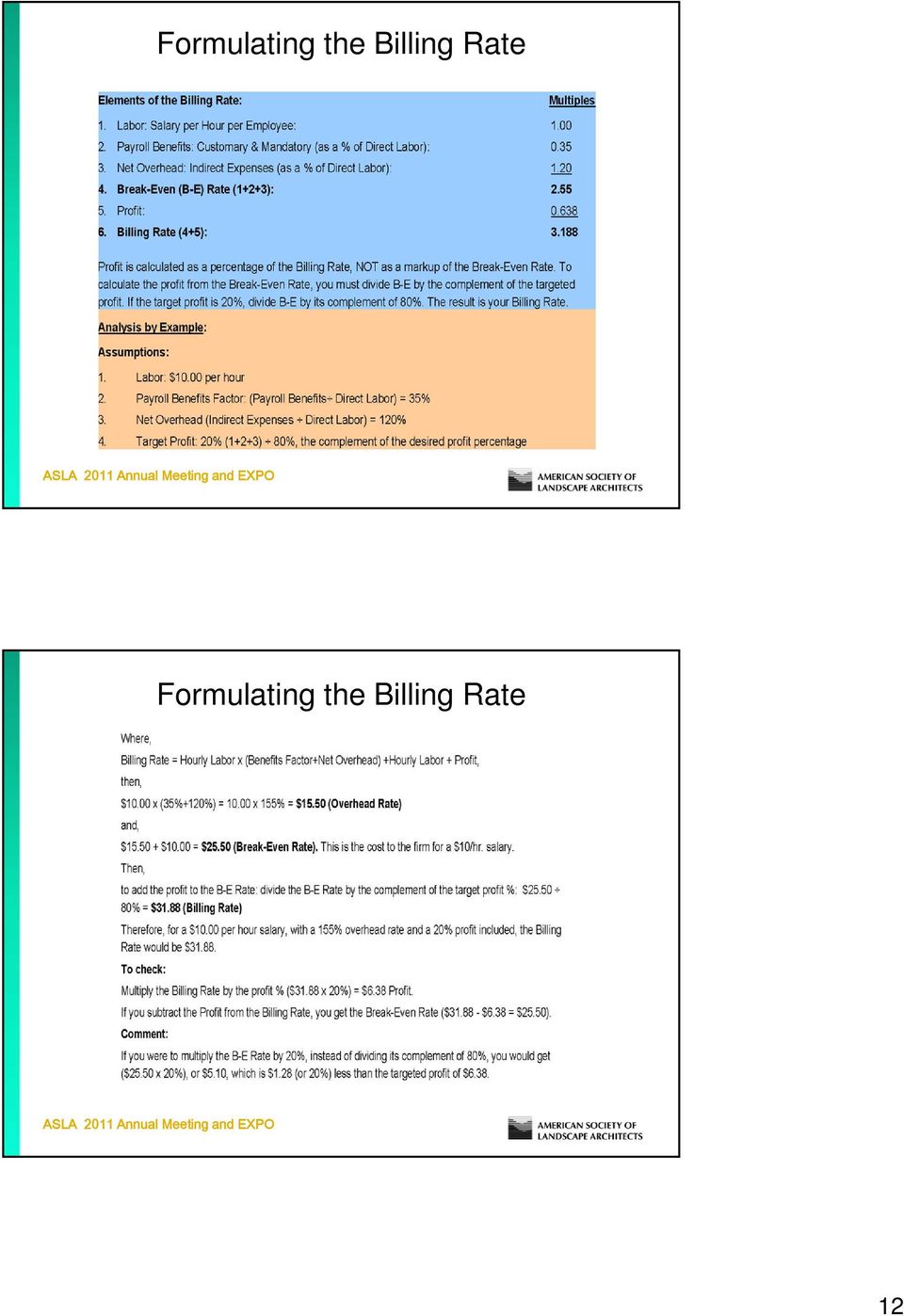

12 Formulating the Billing Rate Formulating the Billing Rate 12

13 Profit-Loss (Income) Statement Profit-Loss (Income) Statement Revenue, Direct Labor 13

14 Profit-Loss (Income) Statement Revenue Components P-L Statement Component of N.O.R. 14

15 Profit-Loss (Income) Statement Expenses & Net Profit Profit-Loss Key Financial Performance Indicators 1. Utilization Rate Time spend on project activities, expressed as a percent of Total Hours worked. NOT a measurement of productivity. This is not necessarily billable time. It is chargeable time, which may or may not be billable. 15

16 Profit-Loss Key Financial Performance Indicators 2. Overhead Rate Measurement of non-project expenses as a percentage of project labor (Direct Labor, in dollars). The overhead rate must be known to properly establish hourly billing rates. Once the overhead rate has been determined, profitability can be determined. Without an accurately determined overhead rate, profit is only an estimate, or worse, a guesstimate. Profit-Loss Key Financial Performance Indicators 3. Break-Even Rate Cost of operations for every dollar of labor. This factor is essential to negotiating a fee which will include a desirable profit margin. Once this factor has been determined, a profit margin can be established and billing rates determined. 16

17 Profit-Loss Key Financial Performance Indicators 4. Net Multiplier Measurement of Revenue as a percentage of Direct Labor. The Net Multiplier indicates the $ Revenue earned for every $ of Direct Labor spent. Profit-Loss Key Financial Performance Indicators 5. Aged Accounts Receivable (A/R) Represents unpaid invoices. An Aged Accounts Receivable Report indicates which invoices, and their amount, that have not been paid. Most reports will indicate the number of days since the invoice was sent. Each firm should establish, as a condition of the Contract, the number of days from the invoice date when the payment is due. Invoices that are unpaid after this period are considered outstanding or aged. 17

18 Profit-Loss Key Financial Performance Indicators 6. Net Revenue Per Employee Represents the Revenue potential generated for each employee. This factor is useful for determining a realistic range for Net Operating Revenue for the budget for the year. Profit-Loss Key Financial Performance Indicators 7. Profit-to-Earnings (P/E) Ratio Since the projects produce a firm s profits, the P-E Ratio indicates a firm s effectiveness in completing projects profitably. 18

19 Balance Sheet - Assets Balance Sheet Liabilities & Stockholder Equity 19

20 Balance Sheet Key Financial Performance Indicators Solvency: Liquidity: Leverage: The ability to pay debt. The ability to convert assets, excluding FF & E, to cash. The ability to manage debt appropriately. Return on equity: The amount of profit produced relative to the money invested to earn it. Balance Sheet Key Financial Performance Indicators Solvency Referred to as the Current Ratio; the ratio between Current Assets and Current Liabilities. Lenders look for a minimum ratio of 1.5:1. Formula: Total Current Assets / Total Current Liabilities Liquidity Referred to as the Quick Ratio or Acid Test. Lenders look for a ratio of 1:1 or better. Formula: Cash + Accts. Receivable + Work-in-Progress / Total Current Liabilities Leverage Referred to as the Debt-to-Equity Ratio. Acceptable ratio: Total Liabilities should not exceed Stockholders Equity by more than 35 percent (ratio should be 1.35 or less). Formula: Total Liabilities / Total Equity Return on Equity Referred to as Owner s or Shareholder s Equity. Formula: (Net Operating Revenue Total Expenses) / Total Equity 20

21 Balance Sheet The Genesis of Knowledge Knowledge is power. - Sir Francis Bacon is an incomplete statement... until it is implemented. - Steve L. Wintner, AIA Emeritus 21

22 Q & A SUN 82 Financial Management: The Path to Profitability Presenter Steve L. Wintner, AIA Emeritus Management Consulting Services The Woodlands, TX 22

23 Steve L. Wintner, AIA Emeritus Founder and principal, Management Consulting Services 55 years of professional experience; 26 years serving a national clientele Co-author, Financial Management for Design Professionals: The Path to Profitability Author of numerous articles on design-firm management in AIA Practice Management Digest, AIA Best Practices, and AIArchitect. Author of Management Tools, monologue of 12 articles on issues of professional design firm management Developer and workshop leader of The Path to Profitability workshop for AIA national, state, and local components Workshop leader of Annual Budgeting for Design Firms, Profit Planning, Project Fee Budgeting, and Project Administration. 23

Understanding Financial Statements. For Your Business

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Architects aspire to financial health. The reason is simple they cannot attain

JWPR065-C08[312-347].qxd 1/24/08 09:05 PM Page 332 Aptara (PPG-Quark) Deltek Vision Deltek Systems, Inc. 100 Cambridge Park Drive, 5th Floor Cambridge, MA 02140-2314 (617) 492-4410 www.deltek.com Peachtree

JWPR065-C08[312-347].qxd 1/24/08 09:05 PM Page 332 Aptara (PPG-Quark) Deltek Vision Deltek Systems, Inc. 100 Cambridge Park Drive, 5th Floor Cambridge, MA 02140-2314 (617) 492-4410 www.deltek.com Peachtree

How To Calculate Financial Leverage Ratio

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

Creating a Successful Financial Plan

Creating a Successful Financial Plan Basic Financial Reports Balance Sheet - Estimates the firm s worth on a given date; built on the accounting equation: Assets = Liabilities + Owner s Equity Income Statement

Creating a Successful Financial Plan Basic Financial Reports Balance Sheet - Estimates the firm s worth on a given date; built on the accounting equation: Assets = Liabilities + Owner s Equity Income Statement

Return on Equity has three ratio components. The three ratios that make up Return on Equity are:

Evaluating Financial Performance Chapter 1 Return on Equity Why Use Ratios? It has been said that you must measure what you expect to manage and accomplish. Without measurement, you have no reference to

Evaluating Financial Performance Chapter 1 Return on Equity Why Use Ratios? It has been said that you must measure what you expect to manage and accomplish. Without measurement, you have no reference to

Understanding A Firm s Financial Statements

CHAPTER OUTLINE Spotlight: J&S Construction Company (http://www.jsconstruction.com) 1 The Lemonade Kids Financial statement (accounting statements) reports of a firm s financial performance and resources,

CHAPTER OUTLINE Spotlight: J&S Construction Company (http://www.jsconstruction.com) 1 The Lemonade Kids Financial statement (accounting statements) reports of a firm s financial performance and resources,

RENAISSANCE ENTREPRENEURSHIP CENTER First Finance Class (FIN-1)

") Finance 1 (FIN-1) RENAISSANCE ENTREPRENEURSHIP CENTER (FIN-1) Learning Outcomes At the conclusion of this class, you should: Know what will be covered in the six finance class sessions. Have reviewed some

Finance 1 (FIN-1) RENAISSANCE ENTREPRENEURSHIP CENTER (FIN-1) Learning Outcomes At the conclusion of this class, you should: Know what will be covered in the six finance class sessions. Have reviewed some

UNDERSTANDING WHERE YOU STAND. A Simple Guide to Your Company s Financial Statements

UNDERSTANDING WHERE YOU STAND A Simple Guide to Your Company s Financial Statements Contents INTRODUCTION One statement cannot diagnose your company s financial health. Put several statements together

UNDERSTANDING WHERE YOU STAND A Simple Guide to Your Company s Financial Statements Contents INTRODUCTION One statement cannot diagnose your company s financial health. Put several statements together

Accounting Basics: The Balance Sheet & Key Performance Indicators

Best Practices page 1 of 8 _ Accounting Basics: The Balance Sheet & Key Performance Indicators Contributed by Michael A. Webber, A/E FINANCE The AIA collects and disseminates Best Practices as a service

Best Practices page 1 of 8 _ Accounting Basics: The Balance Sheet & Key Performance Indicators Contributed by Michael A. Webber, A/E FINANCE The AIA collects and disseminates Best Practices as a service

ESSENTIALS OF ENTREPRENEURSHIP AND SMALL BUSINESS MANAGEMENT 6E

CHAPTER 11 Creating a Successful Financial Plan The Importance of a Financial Plan Financial planning is essential to running a successful business and is not that difficult! Common mistake among business

CHAPTER 11 Creating a Successful Financial Plan The Importance of a Financial Plan Financial planning is essential to running a successful business and is not that difficult! Common mistake among business

Trade Date The date of the previous trading day. Recent Price is the closing price taken from this day.

Definition of Terms Price & Volume Share Related Institutional Holding Ratios Definitions for items in the Price & Volume section Recent Price The closing price on the previous trading day. Trade Date

Definition of Terms Price & Volume Share Related Institutional Holding Ratios Definitions for items in the Price & Volume section Recent Price The closing price on the previous trading day. Trade Date

Financial Ratio Cheatsheet MyAccountingCourse.com PDF

Financial Ratio Cheatsheet MyAccountingCourse.com PDF Table of contents Liquidity Ratios Solvency Ratios Efficiency Ratios Profitability Ratios Market Prospect Ratios Coverage Ratios CPA Exam Ratios to

Financial Ratio Cheatsheet MyAccountingCourse.com PDF Table of contents Liquidity Ratios Solvency Ratios Efficiency Ratios Profitability Ratios Market Prospect Ratios Coverage Ratios CPA Exam Ratios to

Guide to Financial Statements Study Guide

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

Accounting Methods 4 Methods

Accounting Methods 4 Methods WHEN to Recognize (or report) Profit and Loss on Your Income Statement 1: Cash 2: Accrual 3: Completed Contract 4: Percentage of Completion 1 - CASH METHOD: Report Revenues

Accounting Methods 4 Methods WHEN to Recognize (or report) Profit and Loss on Your Income Statement 1: Cash 2: Accrual 3: Completed Contract 4: Percentage of Completion 1 - CASH METHOD: Report Revenues

Creating a Successful Financial Plan

CHAPTER 11 Creating a Successful Financial Plan The Importance of a Financial Plan Financial planning is essential to running a successful business and is not that difficult! Common mistake among business

CHAPTER 11 Creating a Successful Financial Plan The Importance of a Financial Plan Financial planning is essential to running a successful business and is not that difficult! Common mistake among business

Financial Statement and Cash Flow Analysis

Chapter 2 Financial Statement and Cash Flow Analysis Answers to Concept Review Questions 1. What role do the FASB and SEC play with regard to GAAP? The FASB is a nongovernmental, professional standards

Chapter 2 Financial Statement and Cash Flow Analysis Answers to Concept Review Questions 1. What role do the FASB and SEC play with regard to GAAP? The FASB is a nongovernmental, professional standards

Financial Statements and Ratios: Notes

Financial Statements and Ratios: Notes 1. Uses of the income statement for evaluation Investors use the income statement to help judge their return on investment and creditors (lenders) use it to help

Financial Statements and Ratios: Notes 1. Uses of the income statement for evaluation Investors use the income statement to help judge their return on investment and creditors (lenders) use it to help

The BASICS of CONSTRUCTION ACCOUNTING Workshop GLOSSARY

The BASICS of CONSTRUCTION ACCOUNTING Workshop GLOSSARY From Financial Management & Accounting for the Construction Industry, CFMA. 2014 Matthew Bender and Company, Inc., a member of the LexisNexis Group.

The BASICS of CONSTRUCTION ACCOUNTING Workshop GLOSSARY From Financial Management & Accounting for the Construction Industry, CFMA. 2014 Matthew Bender and Company, Inc., a member of the LexisNexis Group.

National Black Law Journal UCLA

National Black Law Journal UCLA Peer Reviewed Title: An Introduction to Financial Statements for the Practicing Lawyer Journal Issue: National Black Law Journal, 4(1) Author: Edmonds, Thom Publication

National Black Law Journal UCLA Peer Reviewed Title: An Introduction to Financial Statements for the Practicing Lawyer Journal Issue: National Black Law Journal, 4(1) Author: Edmonds, Thom Publication

In this chapter, we build on the basic knowledge of how businesses

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

Course 1: Evaluating Financial Performance

Excellence in Financial Management Course 1: Evaluating Financial Performance Prepared by: Matt H. Evans, CPA, CMA, CFM This course provides a basic understanding of how to use ratio analysis for evaluating

Excellence in Financial Management Course 1: Evaluating Financial Performance Prepared by: Matt H. Evans, CPA, CMA, CFM This course provides a basic understanding of how to use ratio analysis for evaluating

Bob s Pretty Good Architectural Firm. G Neil Harper

Bob s Pretty Good Architectural Firm G Neil Harper Getting Started On December 31, 2004, Bob opens a bank account, and deposits $10,000 to get his firm started. Balance Sheet 12/31/04 Assets Cash 10,000

Bob s Pretty Good Architectural Firm G Neil Harper Getting Started On December 31, 2004, Bob opens a bank account, and deposits $10,000 to get his firm started. Balance Sheet 12/31/04 Assets Cash 10,000

C&I LOAN EVALUATION UNDERWRITING GUIDELINES. A Whitepaper

C&I LOAN EVALUATION & UNDERWRITING A Whitepaper C&I Lending Commercial and Industrial, or C&I Lending, has long been a cornerstone product for many successful banking institutions. Also known as working

C&I LOAN EVALUATION & UNDERWRITING A Whitepaper C&I Lending Commercial and Industrial, or C&I Lending, has long been a cornerstone product for many successful banking institutions. Also known as working

RAPID REVIEW Chapter Content

RAPID REVIEW BASIC ACCOUNTING EQUATION (Chapter 2) INVENTORY (Chapters 5 and 6) Basic Equation Assets Owner s Equity Expanded Owner s Owner s Assets Equation = Liabilities Capital Drawing Revenues Debit

RAPID REVIEW BASIC ACCOUNTING EQUATION (Chapter 2) INVENTORY (Chapters 5 and 6) Basic Equation Assets Owner s Equity Expanded Owner s Owner s Assets Equation = Liabilities Capital Drawing Revenues Debit

Metric: Operating Profit w/o Bonus/Taxes (% of Net Revenues) Income Total Annual Net Revenues

Income Total Annual Net Revenues") DECK s KPI s & Metrics The following 26 KPI s and metrics are standard inside of Spieker Point s DECK web ecosystem. Deploying DECK to get this information at a customer site is as simple as creating a

DECK s KPI s & Metrics The following 26 KPI s and metrics are standard inside of Spieker Point s DECK web ecosystem. Deploying DECK to get this information at a customer site is as simple as creating a

Measuring Financial Performance: A Critical Key to Managing Risk

Measuring Financial Performance: A Critical Key to Managing Risk Dr. Laurence M. Crane Director of Education and Training National Crop Insurance Services, Inc. The essence of managing risk is making good

Measuring Financial Performance: A Critical Key to Managing Risk Dr. Laurence M. Crane Director of Education and Training National Crop Insurance Services, Inc. The essence of managing risk is making good

Discussion Board Articles Ratio Analysis

Excellence in Financial Management Discussion Board Articles Ratio Analysis Written by: Matt H. Evans, CPA, CMA, CFM All articles can be viewed on the internet at www.exinfm.com/board Ratio Analysis Cash

Excellence in Financial Management Discussion Board Articles Ratio Analysis Written by: Matt H. Evans, CPA, CMA, CFM All articles can be viewed on the internet at www.exinfm.com/board Ratio Analysis Cash

SMALL BUSINESS DEVELOPMENT CENTER RM. 032

SMALL BUSINESS DEVELOPMENT CENTER RM. 032 FINANCING THROUGH COMMERCIAL BANKS Revised January, 2013 Adapted from: National Federation of Independent Business report Steps to Small Business Financing Jeffrey

SMALL BUSINESS DEVELOPMENT CENTER RM. 032 FINANCING THROUGH COMMERCIAL BANKS Revised January, 2013 Adapted from: National Federation of Independent Business report Steps to Small Business Financing Jeffrey

6.3 PROFIT AND LOSS AND BALANCE SHEETS. Simple Financial Calculations. Analysing Performance - The Balance Sheet. Analysing Performance

63 COSTS AND COSTING 6 PROFIT AND LOSS AND BALANCE SHEETS Simple Financial Calculations Analysing Performance - The Balance Sheet Analysing Performance Analysing Financial Performance Profit And Loss Forecast

63 COSTS AND COSTING 6 PROFIT AND LOSS AND BALANCE SHEETS Simple Financial Calculations Analysing Performance - The Balance Sheet Analysing Performance Analysing Financial Performance Profit And Loss Forecast

Performance Review for Electricity Now

Performance Review for Electricity Now For the period ending 03/31/2008 Provided By Mark Dashkewytch 780-963-5783 Report prepared for: Electricity Now Industry: 23821 - Electrical Contractors Revenue:

Performance Review for Electricity Now For the period ending 03/31/2008 Provided By Mark Dashkewytch 780-963-5783 Report prepared for: Electricity Now Industry: 23821 - Electrical Contractors Revenue:

Report Description. Business Counts. Top 10 States (by Business Counts) Page 1 of 16

Page 1 of 16") 5-Year County-Level Financial Profile Industry Report Architectural Services (SIC Code: 8712) in Prince George County, Maryland Sales Range: $500,000 - $999,999 Date: 11/07/08 Report Description This 5-Year

5-Year County-Level Financial Profile Industry Report Architectural Services (SIC Code: 8712) in Prince George County, Maryland Sales Range: $500,000 - $999,999 Date: 11/07/08 Report Description This 5-Year

FSA Note: Summary of Financial Ratio Calculations

FSA Note: Summary of Financial Ratio Calculations This note contains a summary of the more common financial statement ratios. A few points should be noted: Calculations vary in practice; consistency and

FSA Note: Summary of Financial Ratio Calculations This note contains a summary of the more common financial statement ratios. A few points should be noted: Calculations vary in practice; consistency and

Glossary of Accounting Terms Peter Baskerville

Glossary of Accounting Terms Peter Baskerville Account for or 'bring to account': An accounting phrase used to describe the recording of a financial transaction that is required under the generally accepted

Glossary of Accounting Terms Peter Baskerville Account for or 'bring to account': An accounting phrase used to describe the recording of a financial transaction that is required under the generally accepted

Ratio Analysis: Liquidity, Activity & Coverage

Ratio Analysis: Liquidity, Activity & Coverage Quality of Earnings Fraudulent actions Above-average financial risk One-time transactions Borrow from the future/reach into the past Ride the depreciation

Ratio Analysis: Liquidity, Activity & Coverage Quality of Earnings Fraudulent actions Above-average financial risk One-time transactions Borrow from the future/reach into the past Ride the depreciation

Income Measurement and Profitability Analysis

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

ABOUT FINANCIAL RATIO ANALYSIS

ABOUT FINANCIAL RATIO ANALYSIS Over the years, a great many financial analysis techniques have developed. They illustrate the relationship between values drawn from the balance sheet and income statement

ABOUT FINANCIAL RATIO ANALYSIS Over the years, a great many financial analysis techniques have developed. They illustrate the relationship between values drawn from the balance sheet and income statement

Financial Condition Analysis Model

Financial Condition Analysis Model GOVERNMENTAL ACTIVITIES & ENTERPRISE FUNDS Economic resources and accrual basis of accounting Flow Financial Dimension Financial Indicator Interpretation Interperiod

Financial Condition Analysis Model GOVERNMENTAL ACTIVITIES & ENTERPRISE FUNDS Economic resources and accrual basis of accounting Flow Financial Dimension Financial Indicator Interpretation Interperiod

Financial Ratio Analysis A GUIDE TO USEFUL RATIOS FOR UNDERSTANDING YOUR SOCIAL ENTERPRISE S FINANCIAL PERFORMANCE

Financial Ratio Analysis A GUIDE TO USEFUL RATIOS FOR UNDERSTANDING YOUR SOCIAL ENTERPRISE S FINANCIAL PERFORMANCE December 2013 Acknowledgments This guide and supporting tools were developed by Julie

Financial Ratio Analysis A GUIDE TO USEFUL RATIOS FOR UNDERSTANDING YOUR SOCIAL ENTERPRISE S FINANCIAL PERFORMANCE December 2013 Acknowledgments This guide and supporting tools were developed by Julie

Financial Formulas. 5/2000 Chapter 3 Financial Formulas i

Financial Formulas 3 Financial Formulas i In this chapter 1 Formulas Used in Financial Calculations 1 Statements of Changes in Financial Position (Total $) 1 Cash Flow ($ millions) 1 Statements of Changes

Financial Formulas 3 Financial Formulas i In this chapter 1 Formulas Used in Financial Calculations 1 Statements of Changes in Financial Position (Total $) 1 Cash Flow ($ millions) 1 Statements of Changes

Gross Sales (Gross Revenue): the total amount of money received from customers

: the total amount of money received from customers") Chapter 17 Financial Statements and Ratios 17.1: The Income Statement 17.1.1: Learn the terms used with income statements Income Statement: a financial statement used to summarize all income and expenses

Chapter 17 Financial Statements and Ratios 17.1: The Income Statement 17.1.1: Learn the terms used with income statements Income Statement: a financial statement used to summarize all income and expenses

Accounting Basics: The Income Statement & Key Performance Indicators

Best Practices page 1 of 6 The AIA collects and disseminates Best Practices as a service to AIA members without endorsement or recommendation. Appropriate use of the information provided is the responsibility

Best Practices page 1 of 6 The AIA collects and disseminates Best Practices as a service to AIA members without endorsement or recommendation. Appropriate use of the information provided is the responsibility

Developing Financial Statements

New York StartUP! Business Plan Competition Developing Financial Statements Presented by Paisley Demby, CEO PBN Consulting, LLC www.pbnconsulting.com 1 Invitation to Tweet #2015NYStartUp PaisleyDemby Contents

New York StartUP! Business Plan Competition Developing Financial Statements Presented by Paisley Demby, CEO PBN Consulting, LLC www.pbnconsulting.com 1 Invitation to Tweet #2015NYStartUp PaisleyDemby Contents

Financial Terms & Calculations

Financial Terms & Calculations So much about business and its management requires knowledge and information as to financial measurements. Unfortunately these key terms and ratios are often misunderstood

Financial Terms & Calculations So much about business and its management requires knowledge and information as to financial measurements. Unfortunately these key terms and ratios are often misunderstood

Transforming Financial Statements into Management Tools

Accounting Basics for Contractors: Transforming Financial Statements into Management Tools March 2, 2010 John Garofalo General Partner, John N. Garofalo & Associates garofalojohn@yahoo.com; 713-857-9701

Accounting Basics for Contractors: Transforming Financial Statements into Management Tools March 2, 2010 John Garofalo General Partner, John N. Garofalo & Associates garofalojohn@yahoo.com; 713-857-9701

Finance and Accounting For Non-Financial Managers

Finance and Accounting For Non-Financial Managers Accounting/Finance Recording, classifying, and summarizing financial transactions in terms of dollars and their interpretation 1 Key Accounting Terms Accounting

Finance and Accounting For Non-Financial Managers Accounting/Finance Recording, classifying, and summarizing financial transactions in terms of dollars and their interpretation 1 Key Accounting Terms Accounting

LEBANESE ASSOCIATION OF CERTIFIED PUBLIC ACCOUNTANTS MANAGERIAL ACCOUNTING

LEBANESE ASSOCIATION OF CERTIFIED PUBLIC ACCOUNTANTS MANAGERIAL ACCOUNTING JULY 2015 MULTIPLE CHOICE QUESTIONS (37.5%) Choose the correct answer 1. All of the following statements concerning standard costs

LEBANESE ASSOCIATION OF CERTIFIED PUBLIC ACCOUNTANTS MANAGERIAL ACCOUNTING JULY 2015 MULTIPLE CHOICE QUESTIONS (37.5%) Choose the correct answer 1. All of the following statements concerning standard costs

Export Business Plan Guide

Export Business Plan Guide Table of Contents Introduction... 4 SECTION 01: CURRENT SITUATION ANALYSIS... 5 Company Overview... 5 Availability of Resources... 6 SWOT Analysis... 9 SECTION 02: MARKET ANALYSIS...

Export Business Plan Guide Table of Contents Introduction... 4 SECTION 01: CURRENT SITUATION ANALYSIS... 5 Company Overview... 5 Availability of Resources... 6 SWOT Analysis... 9 SECTION 02: MARKET ANALYSIS...

Chapter 002 Financial Statements, Taxes and Cash Flow

Multiple Choice Questions 1. The financial statement summarizing the value of a firm's equity on a particular date is the: a. income statement. B. balance sheet. c. statement of cash flows. d. cash flow

Multiple Choice Questions 1. The financial statement summarizing the value of a firm's equity on a particular date is the: a. income statement. B. balance sheet. c. statement of cash flows. d. cash flow

FI3300 Corporation Finance

Learning Objectives FI3300 Corporation Finance Spring Semester 2010 Dr. Isabel Tkatch Assistant Professor of Finance Explain the objectives of financial statement analysis and its benefits for creditors,

Learning Objectives FI3300 Corporation Finance Spring Semester 2010 Dr. Isabel Tkatch Assistant Professor of Finance Explain the objectives of financial statement analysis and its benefits for creditors,

Completing the Accounting Cycle

C H A P T E R 4 Completing the Accounting Cycle Financial Accounting 14e Warren Reeve Duchac human/istock/360/getty Images Flow of Accounting Information (slide 1 of 5) End-of-Period Spreadsheet (Work

C H A P T E R 4 Completing the Accounting Cycle Financial Accounting 14e Warren Reeve Duchac human/istock/360/getty Images Flow of Accounting Information (slide 1 of 5) End-of-Period Spreadsheet (Work

Workbook 1 Buying and Selling

Contents Highlights... 2 Quick Practice Session on Buying and Selling... 2 Financial Quiz 1 - Buying & Selling... 3 Learning Zone Buying and Selling... 3 Talk the talk... 4 Understand the link between

Contents Highlights... 2 Quick Practice Session on Buying and Selling... 2 Financial Quiz 1 - Buying & Selling... 3 Learning Zone Buying and Selling... 3 Talk the talk... 4 Understand the link between

Your Guide to Profit Guard

Dear Profit Master, Congratulations for taking the next step in improving the profitability and efficiency of your company! Profit Guard will provide you with comparative statistical and graphical measurements

Dear Profit Master, Congratulations for taking the next step in improving the profitability and efficiency of your company! Profit Guard will provide you with comparative statistical and graphical measurements

BACKGROUND KNOWLEDGE for Teachers and Students

Pathway: Business, Marketing, and Computer Education Lesson: BMM C6 4: Financial Statements and Reports Common Core State Standards for Mathematics: N.Q.2 Domain: Quantities Cluster: Reason quantitatively

Pathway: Business, Marketing, and Computer Education Lesson: BMM C6 4: Financial Statements and Reports Common Core State Standards for Mathematics: N.Q.2 Domain: Quantities Cluster: Reason quantitatively

FINANCIAL ANALYSIS CS. Sample Reports. version 2008.x.x

FINANCIAL ANALYSIS CS Sample Reports version 2008.x.x TL 19887 (10/14/2008) Copyright Information Text copyright 2004-2008 by Thomson Reuters/Tax & Accounting. All rights reserved. Video display images

FINANCIAL ANALYSIS CS Sample Reports version 2008.x.x TL 19887 (10/14/2008) Copyright Information Text copyright 2004-2008 by Thomson Reuters/Tax & Accounting. All rights reserved. Video display images

GVEP Workshop Finance 101

GVEP Workshop Finance 101 Nairobi, January 2013 Agenda Introducing business finance Understanding financial statements Understanding cash flow LUNCH Reading and interpreting financial statements Evaluating

GVEP Workshop Finance 101 Nairobi, January 2013 Agenda Introducing business finance Understanding financial statements Understanding cash flow LUNCH Reading and interpreting financial statements Evaluating

Plan and Track Your Finances

Plan and Track Your Finances 9.1 Financing Your Business 9.2 Pro Forma Financial Statements 9.3 Recordkeeping for Businesses Lesson 9.1 Financing Your Business Goals Estimate your startup costs and personal

Plan and Track Your Finances 9.1 Financing Your Business 9.2 Pro Forma Financial Statements 9.3 Recordkeeping for Businesses Lesson 9.1 Financing Your Business Goals Estimate your startup costs and personal

Working Capital Concept & Animation

Working Capital Concept & Animation Meaning A measure of both a company's efficiency and its short-term financial health. The working capital is calculated as: Working Capital = Current Assets Current

Working Capital Concept & Animation Meaning A measure of both a company's efficiency and its short-term financial health. The working capital is calculated as: Working Capital = Current Assets Current

Learning Objectives: Quick answer key: Question # Multiple Choice True/False. 14.1 Describe the important of accounting and financial information.

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

Understanding Financial Information for Bankruptcy Lawyers Understanding Financial Statements

Understanding Financial Information for Bankruptcy Lawyers Understanding Financial Statements In the United States, businesses generally present financial information in the form of financial statements

Understanding Financial Information for Bankruptcy Lawyers Understanding Financial Statements In the United States, businesses generally present financial information in the form of financial statements

Christopher Noble, Negotiating Owner-Architect Agreements: Theory and Practice (revised February 2011)

") Christopher Noble, Negotiating Owner-Architect Agreements: Theory and Practice (revised February 2011) Construction projects are usually complex undertakings with numerous participants, linked by a web

Christopher Noble, Negotiating Owner-Architect Agreements: Theory and Practice (revised February 2011) Construction projects are usually complex undertakings with numerous participants, linked by a web

Financial Planning. Presented by Emma's Garden

+ Financial Planning Presented by Emma's Garden Financial Planning A comprehensive financial plan helps you to forecast and set your financial goals and milestones. Your financial forecasts are an essential

+ Financial Planning Presented by Emma's Garden Financial Planning A comprehensive financial plan helps you to forecast and set your financial goals and milestones. Your financial forecasts are an essential

Xynergy Commercial Capital LLC

Xynergy Commercial Capital LLC How Can Work For You The Problem Short of cash and must pay suppliers, lease, bills and salaries? No need for stress, get your payments in advance for your invoices and pay

Xynergy Commercial Capital LLC How Can Work For You The Problem Short of cash and must pay suppliers, lease, bills and salaries? No need for stress, get your payments in advance for your invoices and pay

Chapter 17: Financial Statement Analysis

FIN 301 Class Notes Chapter 17: Financial Statement Analysis INTRODUCTION Financial ratio: is a relationship between different accounting items that tells something about the firm s activities. Purpose

FIN 301 Class Notes Chapter 17: Financial Statement Analysis INTRODUCTION Financial ratio: is a relationship between different accounting items that tells something about the firm s activities. Purpose

How To Grade Your Business

ReportCard TheSmallBusiness Is your business making the grade? This number-crunching study guide has the answer. MasterCard Solutions For Small Business MasterCard Solutions for Small Business encompasses

ReportCard TheSmallBusiness Is your business making the grade? This number-crunching study guide has the answer. MasterCard Solutions For Small Business MasterCard Solutions for Small Business encompasses

TMX TRADING SIMULATOR QUICK GUIDE. Reshaping Canada s Equities Trading Landscape

TMX TRADING SIMULATOR QUICK GUIDE Reshaping Canada s Equities Trading Landscape OCTOBER 2014 Markets Hours All market data in the simulator is delayed by 15 minutes (except in special situations as the

TMX TRADING SIMULATOR QUICK GUIDE Reshaping Canada s Equities Trading Landscape OCTOBER 2014 Markets Hours All market data in the simulator is delayed by 15 minutes (except in special situations as the

Top Ten Financial Measurement s for a Healthcare Organization

Top Ten Financial Measurement s for a Healthcare Organization If you can t measure it, you can t manage it. By Sheri Blaho 5272 S. LEWIS, SUITE 100 TULSA, OK 74105 918.496.1600 TOLL FREE: 877.496.1600

Top Ten Financial Measurement s for a Healthcare Organization If you can t measure it, you can t manage it. By Sheri Blaho 5272 S. LEWIS, SUITE 100 TULSA, OK 74105 918.496.1600 TOLL FREE: 877.496.1600

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions Chapter 3 Interpreting Financial Ratios Concept Check 3.1 1. What are the different motivations that

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions Chapter 3 Interpreting Financial Ratios Concept Check 3.1 1. What are the different motivations that

Overview of Financial Solutions

Overview of Financial Solutions The Etra Advisory Group provides solutions to businesses for growth, expansion, cash flow, refinance and acquisition. We cover the world of business financing that banks

Overview of Financial Solutions The Etra Advisory Group provides solutions to businesses for growth, expansion, cash flow, refinance and acquisition. We cover the world of business financing that banks

Business Ratios and Formulas. A Comprehensive Guide. 3rd Edition. Wiley Corporate F&A

Brochure More information from http://www.researchandmarkets.com/reports/2213049/ Business Ratios and Formulas. A Comprehensive Guide. 3rd Edition. Wiley Corporate F&A Description: A complete appraisal

Brochure More information from http://www.researchandmarkets.com/reports/2213049/ Business Ratios and Formulas. A Comprehensive Guide. 3rd Edition. Wiley Corporate F&A Description: A complete appraisal

STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

Financial Statement Analysis: An Introduction

Financial Statement Analysis: An Introduction 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Scope of Financial Statement Analysis... 3 3. Major

Financial Statement Analysis: An Introduction 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Scope of Financial Statement Analysis... 3 3. Major

Chapter Twelve. Current Liabilities. Current Liabilities for Competing Companies

Chapter Twelve Current Liabilities and Contingencies 1. Define current liabilities & identify common CL 2. Account for accruals 3. Account for deferrals 4. Account for compensated absences 5. How to report

Chapter Twelve Current Liabilities and Contingencies 1. Define current liabilities & identify common CL 2. Account for accruals 3. Account for deferrals 4. Account for compensated absences 5. How to report

Using dashboard reports. Selecting KPIs

WHITE PAPER When you have accurate, timely and actionable financial information, you re able to make smarter business decisions. Key Performance Indicators (KPIs) can provide a clear picture of your company

WHITE PAPER When you have accurate, timely and actionable financial information, you re able to make smarter business decisions. Key Performance Indicators (KPIs) can provide a clear picture of your company

Components of a Business Model Core Strategy 1-5 Strategic 1-5 Partnership 1-5 Customer 1-5 Resources Network Interface

ENGI 8607: Business Planning and Strategy in an Entrepreneurial Environment ZipCar Dr. Amy Hsiao Lecture 5 Memorial University of Newfoundland ZipCar Components of a Business Model How It Works http://www.zipcar.com/cambridge/findcars?zipfleet_id=94396

ENGI 8607: Business Planning and Strategy in an Entrepreneurial Environment ZipCar Dr. Amy Hsiao Lecture 5 Memorial University of Newfoundland ZipCar Components of a Business Model How It Works http://www.zipcar.com/cambridge/findcars?zipfleet_id=94396

Construction Economics & Finance. Module 6. Lecture-1

Construction Economics & Finance Module 6 Lecture-1 Financial management: Financial management involves planning, allocation and control of financial resources of a company. Financial management is essential

Construction Economics & Finance Module 6 Lecture-1 Financial management: Financial management involves planning, allocation and control of financial resources of a company. Financial management is essential

Topic 4 Working Capital Management. 1. Concept of Working Capital 2. Measuring Working Capital and Net Working Capital. 4.

Topic 4 Working Capital Management 1. Concept of Working Capital 2. Measuring Working Capital and Net Working Capital 3. Optimization i i of Working Capital 4. Applications 80 Learning objectives This

Topic 4 Working Capital Management 1. Concept of Working Capital 2. Measuring Working Capital and Net Working Capital 3. Optimization i i of Working Capital 4. Applications 80 Learning objectives This

Financial Statements

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

Preparing a Successful Financial Plan

Topic 9 Preparing a Successful Financial Plan LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Describe the overview of accounting methods; 2. Prepare the three major financial statements

Topic 9 Preparing a Successful Financial Plan LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Describe the overview of accounting methods; 2. Prepare the three major financial statements

FINANCIAL STATEMENTS AND RATIO ANALYSIS

In following we will be demonstrating the use of ratios to help examine the health of a firm. Ratios allow managers evaluate to a firm's financial statements in order to point out the strengths and weaknesses

In following we will be demonstrating the use of ratios to help examine the health of a firm. Ratios allow managers evaluate to a firm's financial statements in order to point out the strengths and weaknesses

BSM Connection elearning Course

BSM Connection elearning Course Basics of Medical Practice Finance: Part 2 2009, BSM Consulting All rights reserved. Table of Contents OVERVIEW... 1 PRACTICE PERFORMANCE RATIOS... 1 UNDERSTANDING THE CONCEPT

BSM Connection elearning Course Basics of Medical Practice Finance: Part 2 2009, BSM Consulting All rights reserved. Table of Contents OVERVIEW... 1 PRACTICE PERFORMANCE RATIOS... 1 UNDERSTANDING THE CONCEPT

E2-2: Identifying Financing, Investing and Operating Transactions?

E2-2: Identifying Financing, Investing and Operating Transactions? Listed below are eight transactions. In each case, identify whether the transaction is an example of financing, investing or operating

E2-2: Identifying Financing, Investing and Operating Transactions? Listed below are eight transactions. In each case, identify whether the transaction is an example of financing, investing or operating

Study Guide - Final Exam Accounting I

Study Guide - Final Exam Accounting I True/False Indicate whether the sentence or statement is true or false. 1. Entries in a sales journal affect account balances in both the accounts receivable ledger

Study Guide - Final Exam Accounting I True/False Indicate whether the sentence or statement is true or false. 1. Entries in a sales journal affect account balances in both the accounts receivable ledger

Financial Ratios and Quality Indicators

Financial Ratios and Quality Indicators From U.S. Small Business Administration Online Women's Business Center If you monitor the ratios on a regular basis you'll gain insight into how effectively you

Financial Ratios and Quality Indicators From U.S. Small Business Administration Online Women's Business Center If you monitor the ratios on a regular basis you'll gain insight into how effectively you

Understanding Financial Statements: What do they say about your business?

Understanding Financial Statements: What do they say about your business? This workbook is not designed to be your only guide to understanding financial statements. A much wider range of resources is available

Understanding Financial Statements: What do they say about your business? This workbook is not designed to be your only guide to understanding financial statements. A much wider range of resources is available

Portfolio Management FMI Skema Paris campus Contrôle continu 2 2 April 2014 O. Williams

Portfolio Management FMI Skema Paris campus Contrôle continu 2 2 April 2014 O. Williams 1. The comparisons with which ratios should be made include the following, except: a. The firm's own past performance

Portfolio Management FMI Skema Paris campus Contrôle continu 2 2 April 2014 O. Williams 1. The comparisons with which ratios should be made include the following, except: a. The firm's own past performance

QuickBooks. Reports List 2013. Enterprise Solutions 14.0

QuickBooks Reports List 2013 Enterprise Solutions 14.0 Table of Contents Complete List of Reports... 5 Company & Financial Reports... 6 Profit & Loss... 6 Income & Expenses... 7 Balance Sheet & Net Worth...

QuickBooks Reports List 2013 Enterprise Solutions 14.0 Table of Contents Complete List of Reports... 5 Company & Financial Reports... 6 Profit & Loss... 6 Income & Expenses... 7 Balance Sheet & Net Worth...

Basic Accounting Principles

Basic Accounting Principles Basic Accounting Model The basic accounting model represents the relationship between assets (what the company owns), liabilities (what the company owes), and owner s equity

Basic Accounting Principles Basic Accounting Model The basic accounting model represents the relationship between assets (what the company owns), liabilities (what the company owes), and owner s equity

FINANCIAL ACCOUNTING TOPIC: FINANCIAL ANALYSIS

SYLLABUS Compulsory part Basic ratio analysis 1. State the general functions of accounting ratios. 2. Calculate and interpret the following ratios: a. working capital/current ratio, quick/liquid/acid test

SYLLABUS Compulsory part Basic ratio analysis 1. State the general functions of accounting ratios. 2. Calculate and interpret the following ratios: a. working capital/current ratio, quick/liquid/acid test

CONTACT THE COORDINATOR

In today's business world, when every manager is held accountable for the bottom line, you have to be finance savvy. During challenging economic times, financial acumen is expected at every organizational

In today's business world, when every manager is held accountable for the bottom line, you have to be finance savvy. During challenging economic times, financial acumen is expected at every organizational

CASH FLOW STATEMENT & BALANCE SHEET GUIDE

CASH FLOW STATEMENT & BALANCE SHEET GUIDE The Agriculture Development Council requires the submission of a cash flow statement and balance sheet that provide annual financial projections for the business

CASH FLOW STATEMENT & BALANCE SHEET GUIDE The Agriculture Development Council requires the submission of a cash flow statement and balance sheet that provide annual financial projections for the business

ISS Governance Services Proxy Research. Company Financials Compustat Data Definitions

ISS Governance Services Proxy Research Company Financials Compustat Data Definitions June, 2008 TABLE OF CONTENTS Data Page Overview 3 Stock Snapshot 1. Closing Price 3 2. Common Shares Outstanding 3 3.

ISS Governance Services Proxy Research Company Financials Compustat Data Definitions June, 2008 TABLE OF CONTENTS Data Page Overview 3 Stock Snapshot 1. Closing Price 3 2. Common Shares Outstanding 3 3.

Key Metrics to Run Your Law Firm Profitably

Key Metrics to Run Your Law Firm Profitably December 1, 2011 Presented by: K. Jennie Kinnevy Feeley & Driscoll, P.C. www.fdcpa.com Neil F. Scullion Feeley & Driscoll, P.C. www.fdcpa.com Agenda Introduction

Key Metrics to Run Your Law Firm Profitably December 1, 2011 Presented by: K. Jennie Kinnevy Feeley & Driscoll, P.C. www.fdcpa.com Neil F. Scullion Feeley & Driscoll, P.C. www.fdcpa.com Agenda Introduction

Accounting Principles Critical to Success Presented By: C. P. Krishnan. www.cakintl.com

Accounting Principles Critical to Success Presented By: C. P. Krishnan Basic Accounting You Need to Know Assets, Liabilities, Equity, Income, & Expenses Assets Includes what you have and what people owe

Accounting Principles Critical to Success Presented By: C. P. Krishnan Basic Accounting You Need to Know Assets, Liabilities, Equity, Income, & Expenses Assets Includes what you have and what people owe

A Simple Model. Introduction to Financial Statements

Introduction to Financial Statements NOTES TO ACCOMPANY VIDEOS These notes are intended to supplement the videos on ASimpleModel.com. They are not to be used as stand alone study aids, and are not written

Introduction to Financial Statements NOTES TO ACCOMPANY VIDEOS These notes are intended to supplement the videos on ASimpleModel.com. They are not to be used as stand alone study aids, and are not written

Financial/Accounting Analysis Ratios Excel Calculator

User Guide Financial/Accounting Analysis Ratios Excel Calculator Dec 2008 Version 2 copyright 2008 Business Tools Templates Financial/Accounting Analysis Ratios Excel Calculator Financial Analysis Ratios

User Guide Financial/Accounting Analysis Ratios Excel Calculator Dec 2008 Version 2 copyright 2008 Business Tools Templates Financial/Accounting Analysis Ratios Excel Calculator Financial Analysis Ratios

Intuit QuickBooks Enterprise Solutions 10.0 Complete List of Reports

Intuit QuickBooks Enterprise Solutions 10.0 Complete List of Reports Intuit QuickBooks Enterprise Solutions, for growing businesses, is the most powerful QuickBooks product. It has the capabilities and

Intuit QuickBooks Enterprise Solutions 10.0 Complete List of Reports Intuit QuickBooks Enterprise Solutions, for growing businesses, is the most powerful QuickBooks product. It has the capabilities and

YOUR SMALL BUSINESS SCORECARD. Your Small Business Scorecard. David Oetken, MBA CPM

Your Small Business Scorecard David Oetken, MBA CPM 1 Being a successful entrepreneur takes a unique mix of skills and practices. You need to generate exciting ideas, deliver desirable products or services,

Your Small Business Scorecard David Oetken, MBA CPM 1 Being a successful entrepreneur takes a unique mix of skills and practices. You need to generate exciting ideas, deliver desirable products or services,