Ontario Psychological Association. Accounting for your Private Practice

|

|

|

- Eustacia McKinney

- 8 years ago

- Views:

Transcription

1 Ontario Psychological Association Accounting for your Private Practice Presented by: Regina Baezner, CPA, CA, Partner Andrea Guenther, CPA, CGA, Senior Manager February 19, 2015

2 Agenda Taxation 101 Employee vs. self-employed Incorporation Accounting 101 Record keeping Compliance Levels of assurance

3 Employee vs. Self-employed Employee Advantages: CPP, EI, Income tax and other benefits deducted at source (someone else does the calculations) No compliance record keeping requirement Disadvantages Limited ability to claim professional expenses Minimal control over your work environment Self-employed Advantages Claim professional expenses Control your work environment, whom you work with, hours of work ability to earn more income Disadvantages Requires more record keeping to track professional expenses practice management

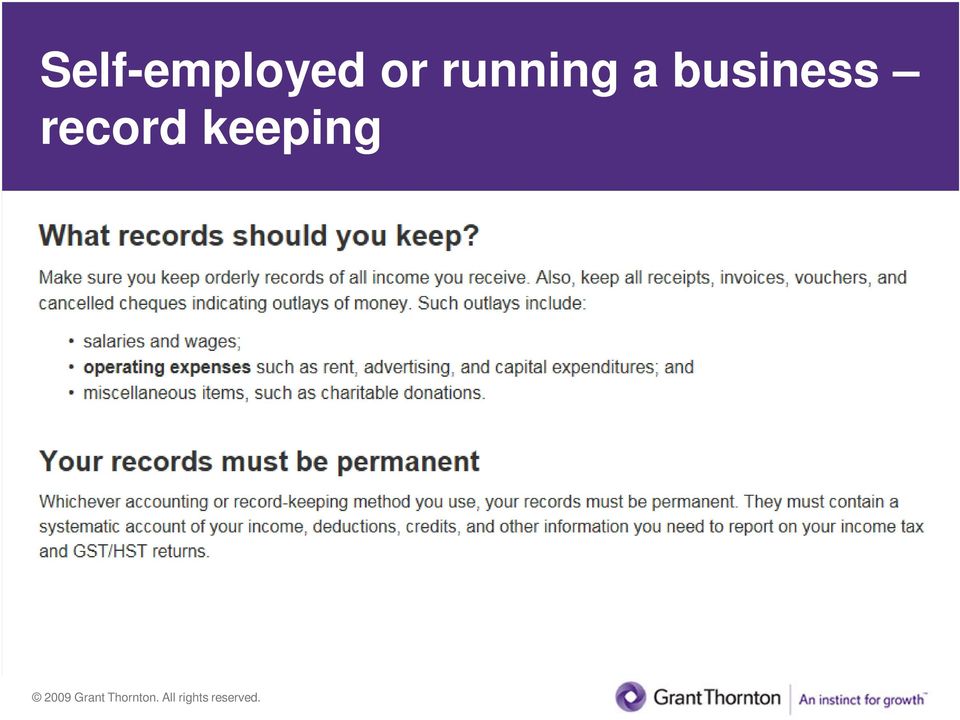

4 Self-employed or running a business record keeping

5 Incorporation Who can incorporate? Health professionals regulated under the Regulated Health Professions Act.

6 Who can incorporate? Regulated Health Professionals in Ontario Acupuncturist/Traditional Chinese Medicine Chiropractors Dental hygienists Dental technologists Dieticians Massage therapists Medical radiation technologists Nurses Opticians Pharmacists Physiotherapists Respiratory therapists Audiologists Chiropodists and Podiatrists Dental surgeons Denturists Kinesiologists Medical laboratory technologists Midwives Occupational therapists Optometrists Physicians and surgeons Psychologists Speech language pathologists

7 Who can incorporate? Regulated Health Professionals in Ontario Professional Corporation shareholder restrictions All of the issued and outstanding shares of the corporation must be owned by one or more members of the same profession. All officers and directors must be shareholders. Specific to dentists and medical doctors Are permitted to have family members own non-voting shares. Spouse must own shares directly. A trust for minor children may own shares. Adult children must own shares directly.

8 Who should incorporate? Establish type of income first Fee for service income - qualifies Employment income does not qualify Factors to consider Age (how many more years will you be practicing?) Family dynamic (do you have a spouse and children?) Not as relevant to psychologists as cannot have family members own shareholders. However can be combined with family income levels and amount of earnings taken out of the corporation in a given year. Lifestyle (what are your personal consumption needs?) Resident status - are you and your fellow shareholders Canadian residents?

Not as relevant to psychologists as cannot have family members own shareholders.")

9 Why should you incorporate? Key benefits 1.Tax-efficient income deferral; 2.Tax-efficient corporate distributions; 3.Limitation of liability (in certain circumstances); and 4.Other benefits

10 Tax-efficient income deferral Ontario Budget changes impacting 2014 planning Introduction of new personal tax brackets in Ontario $136,270 to $150,000 (46.41%) $150,000 to $220,000 (47.97%) $220,000 and above (49.52%) Previously: $136,270 to $514,090 (46.41%) $514,090 and above (49.52%)

$220,000 and above (49.52%) Previously: $136,270 to $514,090 (46.")

11 Example - tax deferral through a corporation Professional earning $500,000 net per year Amount required for personal needs (pre-tax): $300,000 Tax deferral = $67,836 Self-employed Professional Professional Corporation Savings Professional Income $ 500,000 $ 500,000 Corporate tax on $200,000 (15.5%) 31,000 Personal tax on $300,000 salary 122,000 Personal tax on self-employment income 221,000 - Net 279, ,000 Tax on $169,000 dividend (top marginal rate) 67,836 - Net after-tax cash 279, , Tax deferral 67,836

31,000 Personal tax on $300,000 salary 122,000 Personal tax on self-employment income 221,000 - Net 279,000 347,000 Tax on")

12 Tax- efficient corporate distributions Full discretion on future distributions pay dividends in years where family income drops Maternity/Paternity Sickness Fellowships Retirement on retirement - manage distributions with your other sources of retirement income including pensions and RRIF's. On retirement, the professional corporation would be deregistered and used as investment corporation. Can then be used as a vehicle for retirement income.

13 Dividend or Salary All dividend strategy Pros No CPP costs for the health care professional and the professional corporation 2015 Maximum annual cost $2, x 2 = $4, EHT exposure (salaries >$450,000) More cash available for corporate investing/insurance structures Cons individual can no longer contribute to RRSP's Will reduce or eliminate the ability to collect CPP in the future

14 Limitation of Liability Professional Liability No limited liability protection provided by the corporation Voting shareholder(s) and corporation are jointly and severally liable Business liability Limited liability protection is provided by the corporation (assuming no personal guarantees). Examples of business liabilities include: trade liabilities, employment contracts, lease liabilities and nonguaranteed loans.

15 Other Benefits Utilization of cheaper corporate dollars to pay Club/golf memberships with a business purpose Life insurance Meals and entertainment Non deductible penalties and interest Repayment of debt Capital gains exemption (discussed later) Individual Pension Plans (IPP) and Retirement Compensation Arrangements

Individual Pension Plans (IPP) and Retirement Compensation")

16 Costs of incorporation initial set-up There are costs and complexity associated with incorporation. On start-up consider: legal costs to form the corporation application for a certificate of authorization for a Health Profession Corporation and annual renewal consultation with lawyer, accountant and financial advisor before incorporating

17 Costs of incorporation ongoing ongoing legal and accounting fees additional administrative burden, for example: corporation's record keeping and bookkeeping corporate tax installments annual corporate returns need for separate bank accounts corporate minute book upkeep, such as directors' resolutions, annual meetings, etc.

18 Accounting 101 Choosing a trusted advisor/accountant Business registration with Canada Revenue Agency (CRA) and your business number(s) Record Keeping Accrual accounting vs. cash basis accounting Accounting Software Compliance Payroll Tax

19 Choosing a trusted advisor Importance of having an accountant you feel comfortable with and trust Advisor should be familiar with and have experience with medical/professional practices depending upon your level of bookkeeping knowledge you may need a bookkeeper as well as an accountant

20 Business Registration with Canada Revenue Agency (CRA) Registration available by mail, phone or Internet Business numbers may be required for the following business accounts: Payroll program account Corporate income tax program account GST/HST program account Annual information returns (i.e. Return of Investment Income (T5))

21 Record Keeping Cash basis accounting Sales are recorded when cash/payment is received. Expenses are recorded when payment is made. Accrual accounting Sales and expenses are recorded when they occur, even if no cash changes hands. Example: Sales are recorded when service is provided; payment for the services may not yet be received.

22 Record Keeping Commonly used Software for record keeping: Excel spreadsheets QuickBooks Simply Accounting

23 Accounting cycle

24 Record Keeping basic monthly processes Monthly reconciliations Bank Credit card(s) Accounts receivable Accounts payable Monthly reasonableness check look for unusual balances in accounts look for unusual amounts on the income statement and balance sheet

25 Record Keeping Other considerations: Outsourcing bookkeeping functions Separate "business" bank account Separate "business" credit cards Corporations Issues related to shareholder advances

26 Compliance Payroll For yourself and your employees Payroll deductions employer costs CPP Maximum pensionable earnings for 2015 is $53,600 Maximum employee contribution for 2015 is $2,479.95; employer required to match CPP contributions

27 Payroll (continued) Employment Insurance (EI) Shareholder's with a percentage interest >40% are EI exempt Employee maximum insurable earning for 2015 is $49,500 Employee maximum annual premiums for 2015 are $930.60; employer match is 1.4 times the employee's premiums Federal and Provincial Tax Deduction based on employee completing form TD1 Form and CRA tax tables

28 Payroll (continued) Remitting Payroll Deductions Based on average monthly withholding amounts (AMWA) Generally, where AMWA are < $25,000 (starting in 2015); remittance are due on or before the 15 th day of the month after the month the employees are paid. Accelerated remittances are required where the AMWA is >$25,000 Threshold 1 - $25,000 - $99,999 Payments due the 25 th of the same month for amounts paid in the first 15 days and 10 th of the following for payroll paid from the 16 th to the end of the month Threshold 2 - $100,000 or more AMWA payments due within 3 days of the payment based on 7 th, 14 th, 21 st and through to the last day of the month

29 Payroll (Continued) Employer Health Tax (EHT) Where annual payroll is >$450,000; requirement to register and file annual return Monthly installments required where annual remuneration is > $600,000 Workplace Safety and Insurance Board (WSIB) Registration required by most businesses Recommend contacting WSIB to determine registration requirement Premiums are paid by the employer Rates based on guidelines set by WSIB 2014 rate for Office of Psychologists = 0.73/$100 of remuneration paid

30 Payroll (continued) Salary vs. Dividend Salary allows for RRSP contributions, whereas dividend payments do not Incorporated practices May want to consider salary/dividend mix, depending on individual cash requirements consult with your professional advisor

31 Compliance Corporations: T2 Corporate Tax Return due 6 months after your year end where there is a balance due, amount to be paid within 3 months of the year-end to avoid non-deductible interest charges Installment payments due quarterly or monthly

32 Compliance Individuals: T1 Personal Tax Return Employee due April 30 th Limited deductions may include membership dues (where not reimbursed; otherwise Form T2200 may be required) Tuition tax credits Self-employed Due June 15 th Where there is a balance due, amounts to be paid by April 30 th to avoid non-deductible interest charges There is a requirement to pay quarterly installments after the first year, based on the prior year taxes payable

33 Compliance Harmonized Sales Tax (HST) Registration required where total taxable sales are > $30,000 Most health, medical, and dental services performed by licensed physicians or dentists for medical reasons are considered exempt services No HST charged and no claim can be made for input tax credits (ITC's) Medical reports are excluded from the exempt supplies Therefore, HST registration required where taxable supply is > $30,000 ITC's claimed must only be related to the writing/producing medical reports; portion of overhead costs may be possible

34 Levels of assurance Auditor's report Review engagement report Compilation report (aka - Notice to Reader)

35 Levels of Assurance Auditor's Report Based on Generally Accepted Auditing Standards (GAAS) Provides highest level of assurance, also the most expensive statements must be prepared in accordance with generally accepted accounting principles. Financial statements include Balance sheet, Income statement, Statement of cash flows and note disclosures Based on materiality A misstatement in financial statements is considered to be material if the decision of a person who is relying on the financial statements would be changed Auditor provides an opinion on whether the financial statements are presented fairly, in all material respects in accordance with the disclosed basis of accounting Notes are included with CRA filings

36 Levels of Assurance Review Engagement Report Negative assurance only no opinion given States only that: Based on my review, nothing has come to my attention that causes me to believe that these financial statements are not, in all material respects, in accordance with Canadian GAAP." Procedures consist primarily of enquiry, analytical review and discussion. Still requires adherence to accounting standards and full financial statements, including notes. Notes are included with CRA filings Often the lowest level of assurance accepted by banks and other lenders

37 Levels of Assurance Compilation Report (Notice to Reader) No assurance provided Readers are cautioned that these financial statements may not be appropriate for their purposes. Acceptable to CRA Can apply accounting standards or not, for example on a cash basis not accrual basis however may result in taxable adjustments if audited by the CRA

38 Can the practice be sold? Sale of Practice More common in dental or other practices, with a large capital investment in equipment and building / leaseholds However may be possible for an established practice, that has a good reputation and good referral sources Sale can also be in whole or in stages as new practitioner shareholders or associates are brought in over time and other shareholders retire Consult with a professional tax advisor Can be selling the shares or the "assets" (i.e. goodwill/customer lists) of the professional practice. Vendors and purchasers are often at cross purposes as to which

39 Sale of shares CRA has stated that shares of a professional corporation will be eligible for the $800,000 exemption providing the small business corporation conditions are met, and the shares are qualifying small business corporation shares and they can be sold for value. Utilization of one individual's capital gains exemption can result in $198,000 in tax savings. This saving is multiplied over the number of shareholders.

40 Sale of shares Capital gains exemption $800,000 on QSBC may qualify for sale of small business corporation rules are complex key is the assets held at time of sale in order to be sure to qualify at the time of sale, practitioners are cautioned to deal with their professional tax advisor well in advance, at least a period of two years or more prior to sale.

41 Disclaimer This material deals with complex matters and may not apply to particular fact situations. As well, this material and the references contained therein reflects laws and practices which are subject to change. For these reasons, the material should not be relied upon as a substitute for specialized professional advice in connection with any particular matter. Although the material has been carefully prepared and reviewed, no persons involved in the preparation of the material accepts any legal responsibility for its contents or for any consequences arising from its use.

42 Thank you Regina Baezner, CPA, CA Partner Grant Thornton LLP Suite Allstate Parkway Markham ON L3R 5B4 Andrea Guenther, CPA, CGA Senior Manager Grant Thornton LLP Suite Allstate Parkway Markham ON L3R 5B4 T F E Regina.Baezner.ca.gt.com W T F E Andrea.Guenther@ca.gt.com W

Accounting For Your Future INCORPORATION OF PROFESSIONALS IN ONTARIO. Details of the Legislation (Ontario Business Corporations Act)

") Accounting For Your Future INCORPORATION OF PROFESSIONALS IN ONTARIO Author: Hugh Faloon, CA, CFP, TEP, Tax Partner Status of Particular Professional Bodies The following professions have been allowed

Accounting For Your Future INCORPORATION OF PROFESSIONALS IN ONTARIO Author: Hugh Faloon, CA, CFP, TEP, Tax Partner Status of Particular Professional Bodies The following professions have been allowed

The Professional s Option Professional Incorporation

The Professional s Option Professional Incorporation Many professionals now have the opportunity to run their business as a professional corporation 1. The ability to incorporate raises a number of planning

The Professional s Option Professional Incorporation Many professionals now have the opportunity to run their business as a professional corporation 1. The ability to incorporate raises a number of planning

Collins Barrow. Chartered Accountants

Income Tax for Small Business Presented by Jason Timmermans, BA, CA Partner KMD Introduction Information package What are you hoping to get out of today s session? Agenda Basics of Canadian income tax

Income Tax for Small Business Presented by Jason Timmermans, BA, CA Partner KMD Introduction Information package What are you hoping to get out of today s session? Agenda Basics of Canadian income tax

Tax Planning Opportunities Involving Professional Corporations

Tax Planning Opportunities Involving Professional Corporations A Discussion Paper Prepared by: Alan Koop, CA Prepared for: The Saskatchewan Provincial Court Judges Association Table of Contents Executive

Tax Planning Opportunities Involving Professional Corporations A Discussion Paper Prepared by: Alan Koop, CA Prepared for: The Saskatchewan Provincial Court Judges Association Table of Contents Executive

Professional Corporations An Attractive Option

Professional Corporations An Attractive Option Recent and planned corporate income tax rate reductions mean that now is a good time for eligible professionals to consider incorporating their practices.

Professional Corporations An Attractive Option Recent and planned corporate income tax rate reductions mean that now is a good time for eligible professionals to consider incorporating their practices.

Incorporating your farm. Is it right for you?

Incorporating your farm Is it right for you? RBC Royal Bank Incorporating your farm 2 The following article was written by RBC Wealth Management Services If you have considered incorporating your farm,

Incorporating your farm Is it right for you? RBC Royal Bank Incorporating your farm 2 The following article was written by RBC Wealth Management Services If you have considered incorporating your farm,

PRIVATE HEALTH SERVICES PLANS

PRIVATE HEALTH SERVICES PLANS REFERENCE GUIDE PHSP OVERVIEW The use of a private health services plan ( PHSP ) provides a tax-efficient method for business owners to offer supplemental health care coverage

PRIVATE HEALTH SERVICES PLANS REFERENCE GUIDE PHSP OVERVIEW The use of a private health services plan ( PHSP ) provides a tax-efficient method for business owners to offer supplemental health care coverage

INCORPORATING YOUR BUSINESS

November 2014 CONTENTS Advantages of incorporation Advantages of an SBC Summary INCORPORATING YOUR BUSINESS If you carry on a business, there are many tax planning opportunities which become available

November 2014 CONTENTS Advantages of incorporation Advantages of an SBC Summary INCORPORATING YOUR BUSINESS If you carry on a business, there are many tax planning opportunities which become available

Introduction to Payroll. Employer, Payer, or Trustee

Introduction to Payroll The Canadian payroll system is a rather complex process, requiring employers to make proper distinctions between workers, collecting deductions from their income, remitting those

Introduction to Payroll The Canadian payroll system is a rather complex process, requiring employers to make proper distinctions between workers, collecting deductions from their income, remitting those

CANADIAN CORPORATE TAXATION. A General Guide January 31, 2011 TABLE OF CONTENTS INCORPORATION OF A BUSINESS 1 POTENTIAL ADVANTAGES OF INCORPORATION 1

CANADIAN CORPORATE TAXATION A General Guide January 31, 2011 TABLE OF CONTENTS PART A PAGE INCORPORATION OF A BUSINESS 1 POTENTIAL ADVANTAGES OF INCORPORATION 1 POTENTIAL DISADVANTAGES OF INCORPORATION

CANADIAN CORPORATE TAXATION A General Guide January 31, 2011 TABLE OF CONTENTS PART A PAGE INCORPORATION OF A BUSINESS 1 POTENTIAL ADVANTAGES OF INCORPORATION 1 POTENTIAL DISADVANTAGES OF INCORPORATION

Owner-Manager Remuneration

Introduction Owner-managers who carry on business through corporations constantly face the dilemma of deciding whether to pay themselves by way of salaries or dividends. On the one hand, a salary is a

Introduction Owner-managers who carry on business through corporations constantly face the dilemma of deciding whether to pay themselves by way of salaries or dividends. On the one hand, a salary is a

Applebaum Commisso Tax Tips

Tax Tips Corporate: Tax information everyone should know: Small business deduction: The effective tax rate for a corporation that is defined as a Canadian Controlled Private Corporation is 15.5% on the

Tax Tips Corporate: Tax information everyone should know: Small business deduction: The effective tax rate for a corporation that is defined as a Canadian Controlled Private Corporation is 15.5% on the

Professional Corporations Is One Right for You?

Professional Corporations Is One Right for You? Recent and planned corporate income tax rate reductions mean that now is a good time for professionals to consider incorporating their practices. The low

Professional Corporations Is One Right for You? Recent and planned corporate income tax rate reductions mean that now is a good time for professionals to consider incorporating their practices. The low

Income Taxes module. After covering the topics in the module booklets or web pages and this workshop, learners will be able to:

Income Taxes module Trainer s Introduction Most people are aware that they must file an income tax return in Canada, if only to claim back any excess taxes that were withheld from their income. Filing

Income Taxes module Trainer s Introduction Most people are aware that they must file an income tax return in Canada, if only to claim back any excess taxes that were withheld from their income. Filing

Federal Budget 2014 by Jamie Golombek

February 11, 2014 Federal Budget 2014 by Jamie Golombek The February 11, 2014 federal budget included various tax measures that will affect individuals, registered plans, employers and trusts. Rather than

February 11, 2014 Federal Budget 2014 by Jamie Golombek The February 11, 2014 federal budget included various tax measures that will affect individuals, registered plans, employers and trusts. Rather than

FACTS & FIGURES. Tax Audit Accounting Consulting

FACTS & FIGURES Tax Audit Accounting Consulting FACTS AND FIGURES FOR TAX PREPARATION AND PLANNING JULY, 2013 CHAPTER 1B PERSONAL INCOME TAX 1.1 Federal Tax Rates - Individuals... 1 1.2 Federal Personal

FACTS & FIGURES Tax Audit Accounting Consulting FACTS AND FIGURES FOR TAX PREPARATION AND PLANNING JULY, 2013 CHAPTER 1B PERSONAL INCOME TAX 1.1 Federal Tax Rates - Individuals... 1 1.2 Federal Personal

Professional Corporations. Presented by Raza Husain, CA

Professional Corporations Presented by Raza Husain, CA Should I Incorporate? Questions: Does the professional practice generate more net income than is needed to meet the lifestyle expenses of the professional?

Professional Corporations Presented by Raza Husain, CA Should I Incorporate? Questions: Does the professional practice generate more net income than is needed to meet the lifestyle expenses of the professional?

INCORPORATING YOUR PROFESSIONAL PRACTICE

INCORPORATING YOUR PROFESSIONAL PRACTICE REFERENCE GUIDE Most provinces and professional associations in Canada now permit professionals such as doctors, dentists, lawyers, and accountants to carry on

INCORPORATING YOUR PROFESSIONAL PRACTICE REFERENCE GUIDE Most provinces and professional associations in Canada now permit professionals such as doctors, dentists, lawyers, and accountants to carry on

Working Together on Small Businesses. Joint presentation by the Canada Revenue Agency and the Chartered Professional Accountants of Canada

Working Together on Small Businesses Joint presentation by the Canada Revenue Agency and the Chartered Professional Accountants of Canada Purposes Small business owner/operators are the largest group of

Working Together on Small Businesses Joint presentation by the Canada Revenue Agency and the Chartered Professional Accountants of Canada Purposes Small business owner/operators are the largest group of

Critical Tax and Financial Issues for PEI Business Owners

Critical Tax and Financial Issues for PEI Business Owners While written from the perspective of an entrepreneur starting a business, the financial issues I discuss in this article should be well understood

Critical Tax and Financial Issues for PEI Business Owners While written from the perspective of an entrepreneur starting a business, the financial issues I discuss in this article should be well understood

Business Survival Guide for Family Practice

Business Survival Guide for Family Practice Department of Family Medicine Calgary www.calgaryfamilymedicine.ca Introduction to the Business Survival Guide for Family Practice To encourage those who are

Business Survival Guide for Family Practice Department of Family Medicine Calgary www.calgaryfamilymedicine.ca Introduction to the Business Survival Guide for Family Practice To encourage those who are

HEALTH PROFESSIONALS ADVISORY COMMITTEE (HPAC) TERMS OF REFERENCE

TERMS OF REFERENCE") 975 Alloy Drive, Suite 201 Thunder Bay, ON P7B 5Z8 Tel: 807-684-9425 Fax: 807-684-9533 Toll Free: 1-866-907-5446 975, Alloy Drive, bureau 201 Thunder Bay, ON P7B 5Z8 Tél : 807-684-9425 Téléc : 807-684-9533

975 Alloy Drive, Suite 201 Thunder Bay, ON P7B 5Z8 Tel: 807-684-9425 Fax: 807-684-9533 Toll Free: 1-866-907-5446 975, Alloy Drive, bureau 201 Thunder Bay, ON P7B 5Z8 Tél : 807-684-9425 Téléc : 807-684-9533

Resolving Concerns Within Alberta s Health System

Resolving Concerns Within Alberta s Health System C O N T E N T S Abuse...2 Alberta Blue Cross Drug Plan...3 Alberta Health Care Insurance Plan...3 Alberta s Health System...3 Alberta Ombudsman...4 Ambulance

Resolving Concerns Within Alberta s Health System C O N T E N T S Abuse...2 Alberta Blue Cross Drug Plan...3 Alberta Health Care Insurance Plan...3 Alberta s Health System...3 Alberta Ombudsman...4 Ambulance

Health Human Resources Action Plan

December 2005 Message from the Minister and Deputy Minister of Health Angus MacIsaac, Minister Cheryl Doiron, Deputy Minister In Nova Scotia, we are fortunate to have more than 30,000 dedicated and talented

December 2005 Message from the Minister and Deputy Minister of Health Angus MacIsaac, Minister Cheryl Doiron, Deputy Minister In Nova Scotia, we are fortunate to have more than 30,000 dedicated and talented

This article, prepared by PARO s auditors Rosenswig McRae Thorpe LLP, outlines some points to consider in preparing your income tax returns.

2014 Edition for 2013 Returns This article, prepared by PARO s auditors Rosenswig McRae Thorpe LLP, outlines some points to consider in preparing your income tax returns. Remember that: RRSP Contribution

2014 Edition for 2013 Returns This article, prepared by PARO s auditors Rosenswig McRae Thorpe LLP, outlines some points to consider in preparing your income tax returns. Remember that: RRSP Contribution

The Individual Pension Plan. An opportunity to have your cake and eat it too!

Special Report An introduction to: The Individual Pension Plan An opportunity to have your cake and eat it too! Gerard Hass, CA, CFP, CFA Portfolio Manager Raymond James Ltd. 1 What is an Individual Pension

Special Report An introduction to: The Individual Pension Plan An opportunity to have your cake and eat it too! Gerard Hass, CA, CFP, CFA Portfolio Manager Raymond James Ltd. 1 What is an Individual Pension

CICA National Conference on Income Taxes. Professional Corporations

CICA National Conference on Income Taxes Professional Corporations James A. Hutchinson Miller Thomson LLP 416.597.4381 jhutchinson@millerthomson.com October 14, 2010 Metro Toronto Convention Centre 1 Overview

CICA National Conference on Income Taxes Professional Corporations James A. Hutchinson Miller Thomson LLP 416.597.4381 jhutchinson@millerthomson.com October 14, 2010 Metro Toronto Convention Centre 1 Overview

INCORPORATING YOUR BUSINESS

INCORPORATING YOUR BUSINESS REFERENCE GUIDE If you are carrying on a business through a sole proprietorship or a partnership, it may at some point be appropriate to use a corporation to carry on the business.

INCORPORATING YOUR BUSINESS REFERENCE GUIDE If you are carrying on a business through a sole proprietorship or a partnership, it may at some point be appropriate to use a corporation to carry on the business.

Business Loan Protector

Business Loan Protector Insurance Advisor Guide For advisor use only. PLAN CODE: 958 periodic pay; 958L lump sum PRODUCT TYPE Business protection PURPOSE AND MARKET The Business Loan Protector policy has

Business Loan Protector Insurance Advisor Guide For advisor use only. PLAN CODE: 958 periodic pay; 958L lump sum PRODUCT TYPE Business protection PURPOSE AND MARKET The Business Loan Protector policy has

The Professional Series

The Professional Series INSURANCE ADVISOR GUIDE For advisor use only. PLAN CODE 964 level; 965 step rate PRODUCT TYPE Individual disability income protection SALES TIP Consider offering your client the

The Professional Series INSURANCE ADVISOR GUIDE For advisor use only. PLAN CODE 964 level; 965 step rate PRODUCT TYPE Individual disability income protection SALES TIP Consider offering your client the

Private RRSPs and Small Business Owners - The Canadian Tax Dividend

Private Wealth Management Small Business Report October 19, 2010 April 17, 2007 Rethinking RRSPs for Business Owners: Why Taking a Salary May Not Make Sense by Jamie Golombek Abstract Traditionally, many

Private Wealth Management Small Business Report October 19, 2010 April 17, 2007 Rethinking RRSPs for Business Owners: Why Taking a Salary May Not Make Sense by Jamie Golombek Abstract Traditionally, many

SELF-EMPLOYMENT: IS IT FOR YOU?

July 2015 CONTENTS The advantages and disadvantages of being your own boss Can I become an independent contractor? Improving your chances The tax advantages of being self-employed Deducting expenses Selecting

July 2015 CONTENTS The advantages and disadvantages of being your own boss Can I become an independent contractor? Improving your chances The tax advantages of being self-employed Deducting expenses Selecting

INCORPORATING YOUR FARM BUSINESS

February 2016 CONTENTS Advantages of incorporation Advantages of an SBC and an FFC Other considerations Summary INCORPORATING YOUR FARM BUSINESS If you carry on a farm business, and have significant income,

February 2016 CONTENTS Advantages of incorporation Advantages of an SBC and an FFC Other considerations Summary INCORPORATING YOUR FARM BUSINESS If you carry on a farm business, and have significant income,

Tax Consequences of Providing IT Consulting Services

Tax Consequences of Providing IT Consulting Services Presented By:, CA, CPA And Offices in Toronto & Chicago 1-888- US TAXES Canadian IT Contractors Can Work: As employees; Pros & Cons of Being an Employee

Tax Consequences of Providing IT Consulting Services Presented By:, CA, CPA And Offices in Toronto & Chicago 1-888- US TAXES Canadian IT Contractors Can Work: As employees; Pros & Cons of Being an Employee

RETIREMENT COMPENSATION ARRANGEMENTS

RETIREMENT COMPENSATION ARRANGEMENTS REFERENCE GUIDE A Retirement Compensation Arrangement ( RCA ) can be a valuable planning tool that can effectively provide solutions to retirement planning and, in

RETIREMENT COMPENSATION ARRANGEMENTS REFERENCE GUIDE A Retirement Compensation Arrangement ( RCA ) can be a valuable planning tool that can effectively provide solutions to retirement planning and, in

Income Protection Disability

Income Protection Disability Protecting loved ones from financial hardship in the event of premature death of a primary income earner is usually a high priority for most Canadians. Unfortunately, while

Income Protection Disability Protecting loved ones from financial hardship in the event of premature death of a primary income earner is usually a high priority for most Canadians. Unfortunately, while

Income Splitting CONTENTS

June 2012 CONTENTS The attribution rules Family income splitting Business income splitting Income splitting through corporations Income splitting in retirement Summary Income Splitting With Canada s high

June 2012 CONTENTS The attribution rules Family income splitting Business income splitting Income splitting through corporations Income splitting in retirement Summary Income Splitting With Canada s high

How Can You Reduce Your Taxes?

RON GRAHAM AND ASSOCIATES LTD. 10585 111 Street NW, Edmonton, Alberta, T5M 0L7 Telephone (780) 429-6775 Facsimile (780) 424-0004 Email rgraham@rgafinancial.com How Can You Reduce Your Taxes? Tax Brackets.

RON GRAHAM AND ASSOCIATES LTD. 10585 111 Street NW, Edmonton, Alberta, T5M 0L7 Telephone (780) 429-6775 Facsimile (780) 424-0004 Email rgraham@rgafinancial.com How Can You Reduce Your Taxes? Tax Brackets.

CIFPs 11 th Annual National Conference. Frank Di Pietro, CFA, CFP Director, Tax & Estate Planning. May 2013

Tax & Estate Planning for Business Owners CIFPs 11 th Annual National Conference Frank Di Pietro, CFA, CFP Director, Tax & Estate Planning May 2013 DISCLAIMER The information provided is general in nature

Tax & Estate Planning for Business Owners CIFPs 11 th Annual National Conference Frank Di Pietro, CFA, CFP Director, Tax & Estate Planning May 2013 DISCLAIMER The information provided is general in nature

HEALTH PROFESSIONS ACT

HEALTH PROFESSIONS ACT A new law for regulated health care professionals HEALTH AND WELLNESS Contents 1 Health Professions Act... 3 A new law for regulated health care professionals... 3 2 Why the Health

HEALTH PROFESSIONS ACT A new law for regulated health care professionals HEALTH AND WELLNESS Contents 1 Health Professions Act... 3 A new law for regulated health care professionals... 3 2 Why the Health

For advisor use only. RBC Insurance 2016 Student Savings Program

For advisor use only RBC Insurance 2016 Student Savings Program Contents RBC Insurance 2016 Student Savings Program...3 Eligible Occupations...4 Timing of the 2016 Student Savings Program...4 Student Limits

For advisor use only RBC Insurance 2016 Student Savings Program Contents RBC Insurance 2016 Student Savings Program...3 Eligible Occupations...4 Timing of the 2016 Student Savings Program...4 Student Limits

Financial Information Kit

Financial Information Kit The purpose of this kit is to provide basic information on keeping financial records to facilitate compliance by registered charities with the requirements of the Canada Revenue

Financial Information Kit The purpose of this kit is to provide basic information on keeping financial records to facilitate compliance by registered charities with the requirements of the Canada Revenue

Module 4: Personal And Professional Accounting And Taxation. Financial Practice Living md.cma.ca

Module 4: Personal And Professional Accounting And Taxation Financial Practice Living md.cma.ca MD Physician Services acknowledges the significant contributions of the author of this resource document,

Module 4: Personal And Professional Accounting And Taxation Financial Practice Living md.cma.ca MD Physician Services acknowledges the significant contributions of the author of this resource document,

A Conversation With a Canadian Benefits Attorney

A Conversation With a Canadian Benefits Attorney 28 th Annual National CLE Conference Employee Benefits January 5, 2011 (5:30 6:30 p.m.) Elizabeth M. Brown Hicks Morley Hamilton Stewart Storie LLP Overview

A Conversation With a Canadian Benefits Attorney 28 th Annual National CLE Conference Employee Benefits January 5, 2011 (5:30 6:30 p.m.) Elizabeth M. Brown Hicks Morley Hamilton Stewart Storie LLP Overview

TAX PLANNING FOR CANADIAN FARMERS

April 2014 CONTENTS Annual tax planning issues Income tax deferral Incorporating your farming business Long-term planning issues Taxation of capital gains Maximizing your capital gains exemption claims

April 2014 CONTENTS Annual tax planning issues Income tax deferral Incorporating your farming business Long-term planning issues Taxation of capital gains Maximizing your capital gains exemption claims

Disability benefits in Ontario:

Social Assistance Disability benefits in Ontario: Who can get them How to apply To qualify for assistance from the Ontario Disability Support Program (ODSP) Most people must meet this definition of disability

Social Assistance Disability benefits in Ontario: Who can get them How to apply To qualify for assistance from the Ontario Disability Support Program (ODSP) Most people must meet this definition of disability

Personal income tax organizer

2015 Personal income tax organizer Your Personal tax organizer includes a personal income tax checklist and tracking schedules. It is designed to make it easier to compile information for your tax preparer.

2015 Personal income tax organizer Your Personal tax organizer includes a personal income tax checklist and tracking schedules. It is designed to make it easier to compile information for your tax preparer.

Tax Planning & Personal Investment. Customer Value

Tax Planning & Personal Investment Customer Tax Planning To a great extent, tax planning needs to be customized to the individual. Each individual is strongly advised to consult with a qualified tax planner

Tax Planning & Personal Investment Customer Tax Planning To a great extent, tax planning needs to be customized to the individual. Each individual is strongly advised to consult with a qualified tax planner

THE TAX-FREE SAVINGS ACCOUNT

THE TAX-FREE SAVINGS ACCOUNT The 2008 federal budget introduced the Tax-Free Savings Account (TFSA) for individuals beginning in 2009. The TFSA allows you to set money aside without paying tax on the income

THE TAX-FREE SAVINGS ACCOUNT The 2008 federal budget introduced the Tax-Free Savings Account (TFSA) for individuals beginning in 2009. The TFSA allows you to set money aside without paying tax on the income

MOUNTAIN EQUIPMENT CO-OPERATIVE

Consolidated Financial Statements of MOUNTAIN EQUIPMENT CO-OPERATIVE KPMG LLP PO Box 10426 777 Dunsmuir Street Vancouver BC V7Y 1K3 Canada Telephone (604) 691-3000 Fax (604) 691-3031 Internet www.kpmg.ca

Consolidated Financial Statements of MOUNTAIN EQUIPMENT CO-OPERATIVE KPMG LLP PO Box 10426 777 Dunsmuir Street Vancouver BC V7Y 1K3 Canada Telephone (604) 691-3000 Fax (604) 691-3031 Internet www.kpmg.ca

Financial Statements. Youth Employment Services YES. March 31, 2014

Financial Statements Youth Employment Services YES March 31, 2014 Contents Page Independent Auditor s Report 1-2 Statement of Financial Position 3 Statement of Operations and Changes in Fund Balance -

Financial Statements Youth Employment Services YES March 31, 2014 Contents Page Independent Auditor s Report 1-2 Statement of Financial Position 3 Statement of Operations and Changes in Fund Balance -

Strategies For Dealing With An Early Retirement Package

If you or a member of your family is facing a permanent lay-off, voluntary early retirement or forced early retirement, there are many important decisions to be made decisions that can have a significant

If you or a member of your family is facing a permanent lay-off, voluntary early retirement or forced early retirement, there are many important decisions to be made decisions that can have a significant

Hiring Employees. Entrepreneur s Guide To: Main Office 700 California Avenue, Suite 200 Windsor, Ontario N9B 2Z2 T. 519-253-6900 F.

Entrepreneur s Guide To: Hiring Employees Main Office 700 California Avenue, Suite 200 Windsor, Ontario N9B 2Z2 T. 519-253-6900 F. 519-255-9987 Satellite Office 39 Maidstone Avenue East Essex, Ontario

Entrepreneur s Guide To: Hiring Employees Main Office 700 California Avenue, Suite 200 Windsor, Ontario N9B 2Z2 T. 519-253-6900 F. 519-255-9987 Satellite Office 39 Maidstone Avenue East Essex, Ontario

PRIVATE HEALTH SERVICES PLAN (PHSP)

") PRIVATE HEALTH SERVICES PLAN (PHSP) Information Package for All Businesses For more information: Call: 1 (866) 996-7477 or E-Mail: phsp@stratabenefits.ca Administered by: A Private Health Services Plan

PRIVATE HEALTH SERVICES PLAN (PHSP) Information Package for All Businesses For more information: Call: 1 (866) 996-7477 or E-Mail: phsp@stratabenefits.ca Administered by: A Private Health Services Plan

STARTING UP YOUR PRACTICE Lesson 5 Incorporating a Medical Practice

2 INCORPORATING A MEDICAL PRACTICE 3 DIVIDEND VERS SALARY 5 MEDICAL PROFESSIONAL CORPORATIONS ACT 5 STEPS TO INCORPORATE YOUR MEDICAL PRACTICE 6 Digital format created from the original with the permission

2 INCORPORATING A MEDICAL PRACTICE 3 DIVIDEND VERS SALARY 5 MEDICAL PROFESSIONAL CORPORATIONS ACT 5 STEPS TO INCORPORATE YOUR MEDICAL PRACTICE 6 Digital format created from the original with the permission

DC Health Professional Licensing Fees

Profession Description of Service Fees Acupuncturist Application Fee (original, temporary, or reinstatement) 85 Acupuncturist License Fee 145 Acupuncturist Re-Examination 119 Acupuncturist Paid Inactive

Profession Description of Service Fees Acupuncturist Application Fee (original, temporary, or reinstatement) 85 Acupuncturist License Fee 145 Acupuncturist Re-Examination 119 Acupuncturist Paid Inactive

Expert Access Seminar Series: Tax Accounting 101 September 14, 2011

www.pwc.com Expert Access Seminar Series: Tax Accounting 101 September 14, 2011 Introduction to Tax Accounting Robin DarrenCaicco Speake (905) (416) 777-7003 869 2471 Robin.T.Caicco@ca.pwc.com darren.speak@ca.pwc.com

www.pwc.com Expert Access Seminar Series: Tax Accounting 101 September 14, 2011 Introduction to Tax Accounting Robin DarrenCaicco Speake (905) (416) 777-7003 869 2471 Robin.T.Caicco@ca.pwc.com darren.speak@ca.pwc.com

There are no changes to personal federal income tax rates or income brackets for the 2015 tax year.

The 2015 Federal Budget was the first for Finance Minister Joe Oliver, and it tabled a number of proposals that will impact the financial, tax and estate plans of Canadians. The following is a summary

The 2015 Federal Budget was the first for Finance Minister Joe Oliver, and it tabled a number of proposals that will impact the financial, tax and estate plans of Canadians. The following is a summary

Guide to the Determination of Employee/Independent Contractor Status

Employee/Contractor Website Guide to the Determination of Employee/Independent Contractor Status Related Links: Introduction At times, services are provided to the University under arrangements other than

Employee/Contractor Website Guide to the Determination of Employee/Independent Contractor Status Related Links: Introduction At times, services are provided to the University under arrangements other than

DISABILITY TAX INFORMATION

DISABILITY TAX INFORMATION Presentation to Early Intervention Services of York Region January 7, 2004 Introduction Presenter BEN SETO, CA 1981 FCA 2003 Introduction - CHIM & SETO,, LLP York Region Two

DISABILITY TAX INFORMATION Presentation to Early Intervention Services of York Region January 7, 2004 Introduction Presenter BEN SETO, CA 1981 FCA 2003 Introduction - CHIM & SETO,, LLP York Region Two

structuring firms to manage risk

structuring firms to manage risk Time was that if you were going to set up a professional practice, how you organized it was pretty simple. If you were going to practise on your own, you were a sole practitioner,

structuring firms to manage risk Time was that if you were going to set up a professional practice, how you organized it was pretty simple. If you were going to practise on your own, you were a sole practitioner,

2014 Year-End Tax Planning Tips for Seniors, Employees, Families and Students

2014 Year-End Tax Planning Tips for Seniors, Employees, Families and Students While the end of 2014 is approaching, there is still an opportunity for individuals to review their financial situation with

2014 Year-End Tax Planning Tips for Seniors, Employees, Families and Students While the end of 2014 is approaching, there is still an opportunity for individuals to review their financial situation with

assureflex health spending account the evolution of health and dental care benefits

assureflex health spending account the evolution of health and dental care benefits Savings Comparisons Assureflex Corporation Post Office Box 81, Strathroy, Ontario N7G 3J1 telephone: (519) 245-3283 local

assureflex health spending account the evolution of health and dental care benefits Savings Comparisons Assureflex Corporation Post Office Box 81, Strathroy, Ontario N7G 3J1 telephone: (519) 245-3283 local

NEW MEXICO STATE TAX AND CREDIT AND INCENTIVES OVERVIEW FOR HEALTH CARE

NEW MEXICO STATE TAX AND CREDIT AND INCENTIVES OVERVIEW FOR HEALTH CARE Presentation to NMHFMA / NMHA Joint Conference September 29, 2011 MOSS ADAMS LLP 1 AGENDA Gross Receipts Deductible Health Care Service

NEW MEXICO STATE TAX AND CREDIT AND INCENTIVES OVERVIEW FOR HEALTH CARE Presentation to NMHFMA / NMHA Joint Conference September 29, 2011 MOSS ADAMS LLP 1 AGENDA Gross Receipts Deductible Health Care Service

starting up your practice Lesson 4 Personal and Professional Accounting and Taxation

2 INTRODUCTION 3 PHYSICIANS AS EMPLOYEES AND/OR SOLE PROPRIETORS 3 ACCOUNTING BASICS 4 TAXATION BASICS 9 POTENTIAL TAX DEDUCTIONS AND TAX CREDITS 14 SELECTING AN ACCOUNTANT 31 Doctors Nova Scotia acknowledges

2 INTRODUCTION 3 PHYSICIANS AS EMPLOYEES AND/OR SOLE PROPRIETORS 3 ACCOUNTING BASICS 4 TAXATION BASICS 9 POTENTIAL TAX DEDUCTIONS AND TAX CREDITS 14 SELECTING AN ACCOUNTANT 31 Doctors Nova Scotia acknowledges

HealthForceOntario Ontario s Health Human Resources Strategy

HealthForceOntario Ontario s Health Human Resources Strategy Recruit and Retain Conference Thunder Bay, Ontario January, 16, 2014 Jeff Goodyear, Health Workforce Planning Branch Ministry of Health and

HealthForceOntario Ontario s Health Human Resources Strategy Recruit and Retain Conference Thunder Bay, Ontario January, 16, 2014 Jeff Goodyear, Health Workforce Planning Branch Ministry of Health and

Government of Nunavut Department of Finance

Government of Nunavut Department of Finance Taxation Division P.O. Box 2260 Iqaluit, NU X0A 0H0 Telephone: (867) 975-6820 or 1-800-316-3324 Facsimile: (867) 975-5845 E-mail: payrolltax@gov.nu.ca ᑖnᓇ ᑎᑎᕋqᓯᒪᔪq

Government of Nunavut Department of Finance Taxation Division P.O. Box 2260 Iqaluit, NU X0A 0H0 Telephone: (867) 975-6820 or 1-800-316-3324 Facsimile: (867) 975-5845 E-mail: payrolltax@gov.nu.ca ᑖnᓇ ᑎᑎᕋqᓯᒪᔪq

Starting a new Business?

Starting a new Business? Here s how to get started. 1.) Business Plan a. Using words and numbers to identify what you want and what you need to get there. b. Summary of mission, mandate, market and methods.

Starting a new Business? Here s how to get started. 1.) Business Plan a. Using words and numbers to identify what you want and what you need to get there. b. Summary of mission, mandate, market and methods.

Taxation of Retirement Income

Taxation of Retirement Income TAXATION OF RETIREMENT INCOME As our population ages, the need to fund a comfortable retirement becomes a priority for more and more Canadians. Many Canadians planning for

Taxation of Retirement Income TAXATION OF RETIREMENT INCOME As our population ages, the need to fund a comfortable retirement becomes a priority for more and more Canadians. Many Canadians planning for

The Great Divide: Income splitting strategies can lower your family s taxes by Jamie Golombek

March 2015 The Great Divide: Income splitting strategies can lower your family s taxes by Jamie Golombek While the new Family Tax Cut credit, which provides a form of income splitting, has been getting

March 2015 The Great Divide: Income splitting strategies can lower your family s taxes by Jamie Golombek While the new Family Tax Cut credit, which provides a form of income splitting, has been getting

FRISSE & BREWSTER LAW OFFICES

FRISSE & BREWSTER LAW OFFICES ADVANTAGES AND DISADVANTAGES OF VARIOUS BUSINESS ENTITIES SOLE PROPRIETORSHIP A sole proprietorship is simple to establish and operate; little ongoing documentation is needed.

FRISSE & BREWSTER LAW OFFICES ADVANTAGES AND DISADVANTAGES OF VARIOUS BUSINESS ENTITIES SOLE PROPRIETORSHIP A sole proprietorship is simple to establish and operate; little ongoing documentation is needed.

BENEFITS AT A GLANCE FACULTY & ADMINISTRATORS

BENEFITS AT A GLANCE FACULTY & ADMINISTRATORS Emily Carr University is pleased to provide employees a comprehensive benefit package. The benefits plans are designed with the continuing health and well-being

BENEFITS AT A GLANCE FACULTY & ADMINISTRATORS Emily Carr University is pleased to provide employees a comprehensive benefit package. The benefits plans are designed with the continuing health and well-being

TEN COMMON TAX MISTAKES What are the most common areas where Canada Revenue Agency auditors find errors that they can assess?

September 2014 TEN COMMON TAX MISTAKES What are the most common areas where Canada Revenue Agency auditors find errors that they can assess? Here are some of the most common tax problems or mistakes that

September 2014 TEN COMMON TAX MISTAKES What are the most common areas where Canada Revenue Agency auditors find errors that they can assess? Here are some of the most common tax problems or mistakes that

How To Manage A Corporation

Western Climate Initiative, Inc. Accounting Policies and Procedures Adopted May 8, 2013 WESTERN CLIMATE INITIATIVE, INC ACCOUNTING POLICIES AND PROCEDURES Adopted May 8, 2013 Table of Contents I. Introduction...

Western Climate Initiative, Inc. Accounting Policies and Procedures Adopted May 8, 2013 WESTERN CLIMATE INITIATIVE, INC ACCOUNTING POLICIES AND PROCEDURES Adopted May 8, 2013 Table of Contents I. Introduction...

Small Business Start Up Kit

INTRODUCTION: Getting your new business started off on the right foot can be a daunting task. Whether you are an entrepreneur starting from scratch, or leaving the workforce to enjoy the autonomy and challenge

INTRODUCTION: Getting your new business started off on the right foot can be a daunting task. Whether you are an entrepreneur starting from scratch, or leaving the workforce to enjoy the autonomy and challenge

GST/HST Technical Information Bulletin

GST/HST Technical Information Bulletin B-105 February 2011 Changes to the Definition of Financial Service NOTE: This GST/HST Technical Information Bulletin replaces the publications listed under Cancelled

GST/HST Technical Information Bulletin B-105 February 2011 Changes to the Definition of Financial Service NOTE: This GST/HST Technical Information Bulletin replaces the publications listed under Cancelled

inc client Dramatic tax savings can be achieved when clients incorporate their businesses.

client inc Dramatic tax savings can be achieved when clients incorporate their businesses. l ast summer, we taught you the basics behind advisors incorporating their practices (August 2006, page 18). But

client inc Dramatic tax savings can be achieved when clients incorporate their businesses. l ast summer, we taught you the basics behind advisors incorporating their practices (August 2006, page 18). But

Includes Tips & Tricks that could save you substantial $$$ and help make sure your claims get paid.

Includes Tips & Tricks that could save you substantial $$$ and help make sure your claims get paid. WHAT IS INSURANCE? It s simply the transference of a risk from yourself to the Insurer. By paying the

Includes Tips & Tricks that could save you substantial $$$ and help make sure your claims get paid. WHAT IS INSURANCE? It s simply the transference of a risk from yourself to the Insurer. By paying the

PROJECTING YOUR CASH FLOW

THE BUSINESS ENTERPRISE CENTRE S GUIDE TO PROJECTING YOUR CASH FLOW The Business Enterprise Centre is a member of Last updated 16 Jan 2015 TD Page 1 of 26 Preface A cash flow statement reports the outflow

THE BUSINESS ENTERPRISE CENTRE S GUIDE TO PROJECTING YOUR CASH FLOW The Business Enterprise Centre is a member of Last updated 16 Jan 2015 TD Page 1 of 26 Preface A cash flow statement reports the outflow

S Corporation vs. LLC in California Here is an overview of the differences between doing business as an S corporation or as an LLC.

S Corporation vs. LLC in California Here is an overview of the differences between doing business as an S corporation or as an LLC. After you have read this article, we can discuss in detail what would

S Corporation vs. LLC in California Here is an overview of the differences between doing business as an S corporation or as an LLC. After you have read this article, we can discuss in detail what would

TAX, RETIREMENT & ESTATE PLANNING SERVICES. Clawback calculator user guide

TAX, RETIREMENT & ESTATE PLANNING SERVICES Clawback calculator user guide Table of contents Introduction... 3 Fully taxable and investment income Fully taxable income... 4 Investment income... 5 Deductions

TAX, RETIREMENT & ESTATE PLANNING SERVICES Clawback calculator user guide Table of contents Introduction... 3 Fully taxable and investment income Fully taxable income... 4 Investment income... 5 Deductions

Early Retirement Strategies

If you or a member of your family is facing a permanent lay-off, voluntary early retirement or forced early retirement, there are many important decisions to be made decisions that can have a significant

If you or a member of your family is facing a permanent lay-off, voluntary early retirement or forced early retirement, there are many important decisions to be made decisions that can have a significant

Ontario introduces recaptured input tax credit rules

Ontario introduces recaptured input tax credit rules March 17, 2010 When the new HST rules were first introduced, it was noted that large businesses generally, those making taxable supplies of more than

Ontario introduces recaptured input tax credit rules March 17, 2010 When the new HST rules were first introduced, it was noted that large businesses generally, those making taxable supplies of more than

Small Business Tax Planning

Small Business Tax Planning Ellis Orlan, CPA (IL), CGMA Andy Yap, CPA, CA Introduction by Ellis Orlan Topics for Discussion Andy Yap 1. Why incorporate? 2. Tax planning with an incorporated business 3.

Small Business Tax Planning Ellis Orlan, CPA (IL), CGMA Andy Yap, CPA, CA Introduction by Ellis Orlan Topics for Discussion Andy Yap 1. Why incorporate? 2. Tax planning with an incorporated business 3.

Working with CPAs As part of your team of professionals that you work with to help you improve your business, a CPA is a valuable resource for you and your business. It is important to know how someone

Working with CPAs As part of your team of professionals that you work with to help you improve your business, a CPA is a valuable resource for you and your business. It is important to know how someone

ELECTRICAL CONTRACTING LIMITED (AUDIT EXEMPT COMPANY*) DIRECTORS REPORT & FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2013. Registered No.

DIRECTORS REPORT & FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2013. Registered No.") (AUDIT EXEMPT COMPANY*) DIRECTORS REPORT & FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2013 Registered No. xxxx * Electrical Contracting Limited is a small company as defined by the Companies (Amendment)

(AUDIT EXEMPT COMPANY*) DIRECTORS REPORT & FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2013 Registered No. xxxx * Electrical Contracting Limited is a small company as defined by the Companies (Amendment)

DEDUCTING EXPENSES AS AN EMPLOYEE

DEDUCTING EXPENSES AS AN EMPLOYEE Employees are very limited in the expenses that they can deduct in calculating the tax they owe to the Canada Revenue Agency ( CRA ). Self-employed individuals have much

DEDUCTING EXPENSES AS AN EMPLOYEE Employees are very limited in the expenses that they can deduct in calculating the tax they owe to the Canada Revenue Agency ( CRA ). Self-employed individuals have much

Registered No. xxxx. * Electrical Contracting Limited is a small company as defined by Section 350 of the Companies Act 2014.

(SMALL COMPANY*) DIRECTORS REPORT & FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2014 Registered No. xxxx * Electrical Contracting Limited is a small company as defined by Section 350 of the Companies Act

(SMALL COMPANY*) DIRECTORS REPORT & FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2014 Registered No. xxxx * Electrical Contracting Limited is a small company as defined by Section 350 of the Companies Act

BEING FINANCIALLY PREPARED FOR RETIREMENT The Scary Facts! $1.00 item in 1972, costs $3.78 today At the average rate of inflation, the price you pay for an item today will be double in 20 years almost

BEING FINANCIALLY PREPARED FOR RETIREMENT The Scary Facts! $1.00 item in 1972, costs $3.78 today At the average rate of inflation, the price you pay for an item today will be double in 20 years almost

Total Financial Solutions. Practical Perspectives on Tax Planning

TM Trademark used under authorization and control of The Bank of Nova Scotia. ScotiaMcLeod is a division of Scotia Capital Inc., Member CIPF. All insurance products are sold through ScotiaMcLeod Financial

TM Trademark used under authorization and control of The Bank of Nova Scotia. ScotiaMcLeod is a division of Scotia Capital Inc., Member CIPF. All insurance products are sold through ScotiaMcLeod Financial

SECTION 1. Chapter 671, Hawaii Revised Statutes, is. amended by adding five new sections to be appropriately

A BILL FOR AN ACT NO. \32S RELATING TO TORTS. BE IT ENACTED BY THE LEGISLATURE OF THE STATE OF HAWAII: SECTION 1. Chapter 671, Hawaii Revised Statutes, is amended by adding five new sections to be appropriately

A BILL FOR AN ACT NO. \32S RELATING TO TORTS. BE IT ENACTED BY THE LEGISLATURE OF THE STATE OF HAWAII: SECTION 1. Chapter 671, Hawaii Revised Statutes, is amended by adding five new sections to be appropriately

Ontario Disability Support Program - Income Support Directives

Ontario Disability Support Program - Income Support Directives 9.12 - Mandatory Special Necessities Summary of Legislation The costs of the following items can be covered for members of the benefit unit

Ontario Disability Support Program - Income Support Directives 9.12 - Mandatory Special Necessities Summary of Legislation The costs of the following items can be covered for members of the benefit unit

REMUNERATION. - List B - Benefits and allowances that are not remuneration and therefore are not subject to tax.

BULLETIN NO. HE 002 Issued June 2000 Revised August 2014 THE HEALTH AND POST SECONDARY EDUCATION TAX LEVY ACT REMUNERATION This bulletin will help employers understand what kind of payments, made to or

BULLETIN NO. HE 002 Issued June 2000 Revised August 2014 THE HEALTH AND POST SECONDARY EDUCATION TAX LEVY ACT REMUNERATION This bulletin will help employers understand what kind of payments, made to or

THE PENSION PLAN FOR PROFESSIONAL STAFF OF THE UNIVERSITY OF GUELPH. For the Year Ended September 30, 2005

THE PENSION PLAN FOR PROFESSIONAL STAFF OF THE UNIVERSITY OF GUELPH December 9, 2005 PricewaterhouseCoopers LLP Chartered Accountants 55 King Street West, Suite 900 Kitchener, Ontario Canada N2G 4W1 Telephone

THE PENSION PLAN FOR PROFESSIONAL STAFF OF THE UNIVERSITY OF GUELPH December 9, 2005 PricewaterhouseCoopers LLP Chartered Accountants 55 King Street West, Suite 900 Kitchener, Ontario Canada N2G 4W1 Telephone

ELECTRICAL CONTRACTING LIMITED (AUDIT EXEMPT COMPANY*) DIRECTORS REPORT & FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2014. Registered No.

DIRECTORS REPORT & FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2014. Registered No.") (AUDIT EXEMPT COMPANY*) DIRECTORS REPORT & FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2014 Registered No. xxxx * Electrical Contracting Limited is a small company as defined by the Companies Act 2014

(AUDIT EXEMPT COMPANY*) DIRECTORS REPORT & FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2014 Registered No. xxxx * Electrical Contracting Limited is a small company as defined by the Companies Act 2014

Provinces and territories also impose income taxes on individuals in addition to federal taxes

Worldwide personal tax guide 2013 2014 Canada Local information Tax Authority Website Tax Year Tax Return due date Is joint filing possible Are tax return extensions possible Canada Revenue Agency (CRA)

Worldwide personal tax guide 2013 2014 Canada Local information Tax Authority Website Tax Year Tax Return due date Is joint filing possible Are tax return extensions possible Canada Revenue Agency (CRA)

Business Insurance Part 1

Business Insurance Part 1 Working with Business Owners A PARTNER YOU CAN TRUST. Jorge Ramos, CFP,CLU Director of Advanced Marketing 1 Business Structures and Taxation A PARTNER YOU CAN TRUST. 1 Business

Business Insurance Part 1 Working with Business Owners A PARTNER YOU CAN TRUST. Jorge Ramos, CFP,CLU Director of Advanced Marketing 1 Business Structures and Taxation A PARTNER YOU CAN TRUST. 1 Business

Key Person Protector INSURANCE ADVISOR GUIDE. For advisor use only. PLAN CODE PRODUCT TYPE PURPOSE AND MARKET

Key Person Protector INSURANCE ADVISOR GUIDE For advisor use only. PLAN CODE 933 PRODUCT TYPE Business protection PURPOSE AND MARKET RBC Insurance has developed the Key Person Protector to provide coverage

Key Person Protector INSURANCE ADVISOR GUIDE For advisor use only. PLAN CODE 933 PRODUCT TYPE Business protection PURPOSE AND MARKET RBC Insurance has developed the Key Person Protector to provide coverage

The Compensation Conundrum: Will it be salary or dividends? by Jamie Golombek

December 2013 The Compensation Conundrum: Will it be salary or dividends? by Jamie Golombek With the year-end for most businesses fast approaching, owner-managers once again will begin to ponder the age-old

December 2013 The Compensation Conundrum: Will it be salary or dividends? by Jamie Golombek With the year-end for most businesses fast approaching, owner-managers once again will begin to ponder the age-old