Systematic Risk and Crop Insurance in Retrospect and Prospect

|

|

|

- Brooke Sanders

- 8 years ago

- Views:

Transcription

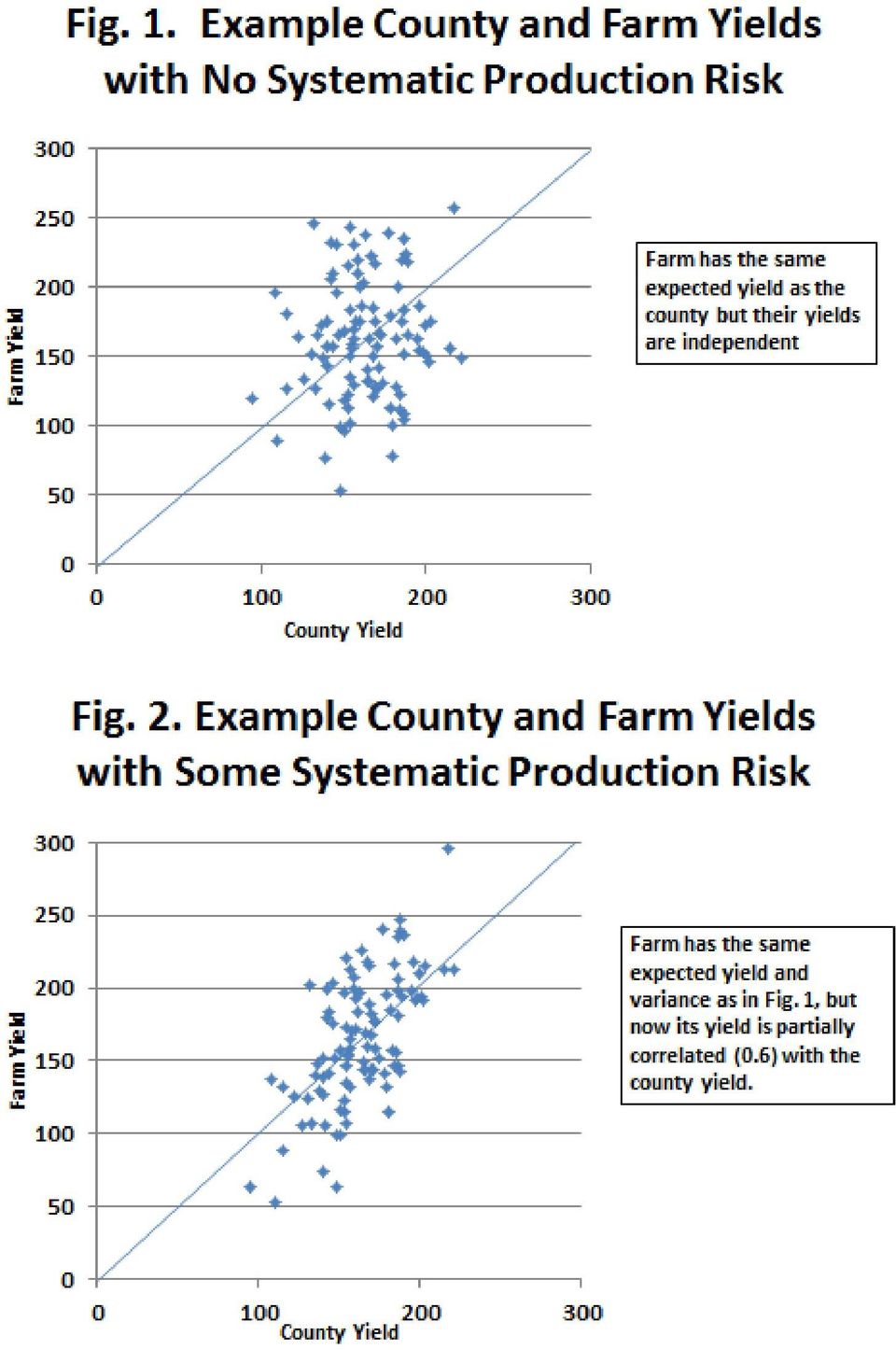

1 Systematic Risk and Crop Insurance in Retrospect and Prospect By Harun Bulut, Frank Schnapp, and Keith Collins, NCIS Systematic risk has been an appealing concept for justifying government involvement in crop insurance markets. It is also the basis for the design of alternative plans of insurance and farm programs. This article revisits the concept by reviewing the related agricultural economics literature. The review focuses on the period since the Federal Crop Insurance Act of 1994 when the crop insurance program went through major changes such as increased participation, the adoption of biotechnology, rating and data improvements and the introduction of revenue plans in crop insurance and farm programs. In the financial economics literature, systematic risk is defined as the portion of a company s risk that is associated with the market portfolio (or risk-pool) and the remaining portion of the risk is defined as the idiosyncratic risk. Systematic risk is also known as undiversifiable risk or market risk. Such a risk may arise due to monetary policy of the Federal Reserve Bank or macroeconomic conditions. On the other hand, idiosyncratic risk is known as diversifiable risk, residual risk, or company-specific risk (Fabozzi and Modigliani). An example may be the unique risk associated with a particular stock in an industry. Investors can diversify or hedge against this risk by holding stocks from another uncorrelated or negatively correlated industry in their portfolio. In crop insurance literature, the term systematic risk (or catastrophic risk) is typically understood as the common portion of underlying risk when losses among insurance units are positively and spatially correlated. 1 Figures 1-3 illustrate no correlation, partial positive correlation and perfect positive correlation between a farmer s and a county s yield. Depending on the level and distribution of positive correlation, a relatively large segment of the insured units may be affected by a common cause of loss, such as widespread adverse weather effects of drought, flood and freeze, as opposed to almost mutually independent events seen in other lines of insurance, such as auto accidents (Miranda and Glauber, 1997; Skees and Black, 1997; Duncan and Myers, 2000; and Chambers and Quiggin, 2002). Price risk also contributes to the insurer s systematic risk due to the high correlation across producers of the same crop. Despite the natural hedge between yield and price movements, in some years, such as 2008, a sharp reduction in price at harvest without major production loss can result in losses on a large number of crop insurance revenue protection policies at the same time. In the next two sections, systematic risk is first considered from the perspective of Approved Insurance Providers (AIPs or insurers) and then from the perspective of farmers. The last section provides concluding comments. 1 The terms systematic risk or systemic risk have been interchangeably used in the literature. In recent years, systemic risk has commonly been used to refer to events that are so severe that they can potentially devastate the entire economy such as a financial meltdown in In referring to non-diversifiable risk, Fabozzi and Modigliani use the term systematic risk, whereas Miranda and Glauber; Mason, Hayes and Lence; Skees and Black use the term systemic risk. Duncan and Myers adopt the term catastrophic risk instead of the term systemic risk. In this article, we choose to use the term systematic risk.

2

3 Systematic Risk from the Insurers Perspective: With very few exceptions, the existence of an insurance market is based on the concept of the law of large numbers. If exposures are independent, the law of large numbers implies that the insurer s risk over its entire book of business is relatively small, with gains on many policies offsetting the losses on a few. On the other hand, if exposures are correlated, then the insurer s risk can be considerable. Simulations conducted by Miranda and Glauber for the 1993 year estimated that the crop insurance portfolios of the ten largest AIPs were 20 to 50 times riskier relative to a hypothetical portfolio consisting of independent crop insurance losses. 2 Facing such a high systematic risk, crop insurance companies would seek reinsurance. The consensus in the literature is that private insurance and reinsurance markets do not provide adequate coverage at a reasonable premium rate for the systematic risk in crop insurance markets. Various proposals have emerged in the literature to address systematic risk in crop insurance markets including: (1) government provided subsidized reinsurance (Duncan and Myers), (2) government provided reinsurance through area insurance (Miranda and Glauber) and (3) options markets, futures markets and forward marketing (Grant, 1985; Chambers and Quiggin). These proposals will be reviewed in the following section. 2 The analysis was done for the 1993 crop year. The authors made simplifying assumptions such as every farmer chose 65 percent coverage with the yield protection policy. They modeled only the joint distribution of farm-level yields and left out modeling of the joint distribution of price and yield. They combined eight years of farm level data with the county level data which went back 30 years from The farm level data covered corn, soybeans and wheat farmers who were enrolled in the program in The sample consisted of 15 percent of the all farmers enrolled in the program in 1993.

4 Government Provided Reinsurance through the Standard Reinsurance Agreement (SRA) Based on a theoretical model, Duncan and Myers study the question of whether, in the presence of systematic risk, a private crop insurance market can be established so that crop insurance companies obtain an adequate return and farmers obtain adequate coverage levels at affordable premium rates. The authors recognize that the accumulation of risk across a crop insurance portfolio due to systematic risk creates a challenge for the private insurance market since investors generally require a return commensurate with the risk they take. While it might be possible to set the rates at a level that compensates insurers for their high degree of systematic risk, those rates might discourage farmers from participating in the program. If the risk premium is sufficiently high, it may even lead to the complete break-down of the market. They find that reinsurance (private or government provided) will help only if there is a somewhat functioning private crop insurance market to begin with. In case of complete market failure, only subsidized reinsurance can help facilitate the market. In that case, a higher subsidy amount further improves the market outcome in the form of lower premiums, higher coverage and participation levels. Duncan and Myers note that whether the cost of subsidized reinsurance outweighs the resulting benefits is an open question. Consistent with the Duncan and Myers analysis, and to ensure participation of private insurers in crop insurance by limiting their exposure to systematic risk, the U.S. government acted as reinsurer under terms specified in various SRAs since 1981 (U.S. General Accounting Office,1992; Mason, Hayes and Lence, 2001). The SRA is a risk-sharing agreement in which insurers give up a portion of underwriting gains in low loss years in order to be able to transfer a portion of underwriting losses to the government in high loss years. The SRA allows private companies to cede the bulk of the risk to the government on a certain share of policies they sell, while the policies they retain are allocated into different risk-sharing funds with varying exposure to risk. This facilitates the government s objective of making crop insurance available to all eligible producers, including producers who would otherwise find it difficult to obtain coverage in the private market due to their underwriting characteristics, while simultaneously transferring most of the risk of these producers to the government. In the early 1990s, Miranda and Glauber criticized the government-provided reinsurance through the SRA by arguing: (1) it does not provide good incentives to companies to monitor adverse selection and moral hazard problems at the farm level; (2) it provides a rather excessive rate of return on retained premium (above 18 percent). These criticisms were made following a time period, the 1980s and early 1990s, during which the actuarial performance of the crop insurance program had been dismal (Glauber, 2004). The Federal Crop Insurance Act of 1994 and the Agricultural Risk Protection Act of 2002 (ARPA) increased the participation of low risk producers in the program through increased premium subsidies under the expectation that increased participation would lead to less adverse selection and lower, more accurate, premium rates. Consistent with that expectation, the crop insurance program s actuarial performance has improved over time. In regard to the first point raised in Miranda and Glauber, one has to recall that the crop insurance industry is highly regulated compared to other lines of insurance. Private insurers must accept the premium rates and underwriting provisions as set by government. Instead, they compete only in the quality of their service. In addition, once a company decides to operate in a given state, it has to offer all plans of insurance that are approved for sale (except pilot programs) to every farmer in that state (universal service requirement). To mitigate the loss potential due to

5 the universal service requirement, companies can cede a portion of their policies they deem highly risky to the Assigned Risk Fund (ARF), where they retain a relatively lower proportion of the premium and its associated risks compared to other reinsurance funds. Nevertheless, ceding to ARF is done as a proportion of the entire reinsurance fund rather than on an individual contract basis. That is, each company retains at least some liability on every policy it underwrites. This is in contrast to flood insurance where the government takes all the risk and the companies bear none. Since the 1980s, successive SRAs have steadily increased the risk retained by the companies. For example in the SRA, the government assumed 100 percent of the losses for which the loss ratio exceeded In the 2011 SRA, the government assumes 100 percent of the losses for which the loss ratio exceeds 5.0. Because crop insurance companies maintain substantial skin in the game, they have ample incentives to rigorously adjust losses. This incentive has increased over time. In regard to the second point raised in Miranda and Glauber, an historical perspective can be useful. In terms of potential returns, the basic structure of SRA did not change in the late 1990s. The main change between the 1998 SRA and the 2005 SRA was the introduction of net book quota share (NBQS). NBQS requires that companies cede five percent of their cumulative underwriting gains or losses to the Federal Crop Insurance Corporation (FCIC). Because companies obtain underwriting gains more often than losses, the reinsurance provided by NBQS tends to benefit FCIC more so than the companies. Vedenov et al. (2006) find that the expected returns to companies would be decreased due to NBQS by 1.1 percent after adjusting for the companies behavioral response. Another change in the 2005 SRA was an increase in cession limits, but Vedonov et al. calculate that companies would increase gross premiums ceded to the ARF only in a limited number of states. In the 2011 SRA, NBQS is increased to 6.5percent, and if there is an underwriting gain, the additional 1.5 percent is to be distributed back to companies operating in under-served states. Finally, the 2011 SRA introduced alternative risk sharing provisions based on groupings of states to reflect differing underwriting gain potential among states, further decreasing the companies expected returns. The crop insurance industry believes that a fairly negotiated SRA is the foundation of the program. Since the passage of the Federal Crop Insurance Act of 1980, which mandated private and public partnership and private delivery of the program, the crop insurance program has grown to become the centerpiece of the agricultural safety net for crops and currently protects about $110 billion worth of liability. Beyond fulfilling their delivery and service obligations, insurers have contributed to the program by providing input and feedback on the implementation of ever-changing rules and policies and investing in physical and human capital in the form of information technology and specialized skills. The reduction in reinsurance support provided by the government, together with reduced payments for delivery costs, have cut AIP funding. The 2008 farm bill cut total program funding by $6.4 billion over the following 10 years. On top of that, the 2011 SRA took an additional $6 billion out over 10 years, all from the AIPs. In the aftermath of the 2011 SRA, several crop insurance companies were sold to large international reinsurers. Indeed, one year after the 2011 SRA, the President proposed an additional $6.3 billion in cuts to the AIPs over 10 years as part of the Budget Control Act of 2011 deficit reduction process. In addition, a separate proposal to change the way premium rates are determined would further erode the expected returns to AIPs. These actions and proposals are in sharp contrast to the conclusions of the Grant Thornton study of industry profitability, which found that crop insurers are much more efficient at delivering crop insurance than are Property and Casualty (P&C) insurers in general, that they face

6 substantially greater risk than P&C insurers, yet achieve a lower rate of return despite the greater risk (Grant Thornton, LLP, 2010). Government Provided Reinsurance through Area Insurance Plans Instead of reinsurance through the SRA, Miranda and Glauber proposed reinsurance through area yield insurance plans as a solution to the systematic risk problem in crop insurance. The idea is that the government would absorb the systematic risk while companies would retain the residual risk. Area yield insurance would protect against regional yield shortfalls and be rated and sold by the federal government. A separate insurance product could be offered by private companies to protect against a farmer s residual (basis) risk. Private companies could determine the premium rates for such a marginal product and would be entitled to ensuing underwriting gains or losses.. The authors argue that such a design would give AIPs a strong incentive to monitor moral hazard and adverse selection and the actuarial performance of their book of business would improve. Once reinsurance was provided through area plans, they even envisioned the possibility that the federal government could get out of the crop insurance market. The crop insurance industry has considered in the past whether it would be advantageous for the SRA to provide area yield or revenue protection to insurers in place of the existing reinsurance arrangements. But the effectiveness of this concept would depend on the size of the area used to define systematic risk. For example, Miranda and Glauber s analysis compares national versus state level yield options. An insurer might need to be protected against systematic risk at the state level, but the government might be willing to provide protection against systematic risk only at the county level. If we consider the relationship between county and state risk, each county contributes to the statewide risk but has its own idiosyncratic risk. Since insurers like to retain the idiosyncratic risk, it may work to their advantage to get area reinsurance protection at the state level instead. Having statewide area protection would enable insurers to offset losses in one county with gains in another. While one might think that the same argument would imply that insurers ought to prefer area reinsurance protection on a countrywide basis rather than a state basis, the mix of business issue may be the reason why this wouldn t be preferred. In line with Miranda and Glauber s suggestion, area yield or revenue insurance products have been offered to farmers at the county level (albeit through insurers) over the last decade and a half while the government and insurers have shared risk with area plans and the government has continued to provide reinsurance through the SRA. Nevertheless, the experience with the existing area insurance plans identified significant informational and operational issues, which will be reviewed in more detail in the next section. Systematic Risk from the Farmers Perspective The conventional thinking has been that systematic risk lies at the core of farmers risk exposure and it is quite uniform and common across farmers in a given area and even across counties in a given state or region. Such a view has been instrumental for the introduction and development area yield or revenue insurance plans and area revenue farm programs. Area Yield or Revenue Insurance Plans Group Risk Protection (GRP) Insurance and Group Risk Income Protection (GRIP) are area based plans protecting against yield and revenue shortfalls at the county level, respectively. GRP started out as a pilot program for soybeans in 1993 and expanded to other major crops the

7 following year. GRIP was proposed as a pilot by the private sector in Starting in 2004, GRIP also began to offer the harvest price option (GRIP-HPO), which sets the insurance guarantee at the higher of planting or harvest prices. Farmers have had little demand for GRP and GRIP in most areas, as these plans accounted for less than four percent of the total MPCI program premium in In crop year 2011, the Risk Management Agency (RMA), on behalf of the FCIC, introduced the Common Crop Insurance Policy (Combo Policy) replacing the previous individual insurance plans with the goal of unifying and simplifying the Federal crop insurance program. To bring the area plans in line with the Combo Policy changes, FCIC proposed a rule to replace GRP Insurance, GRIP Insurance, and GRP-HPO Insurance with new plans called Area Yield Protection Insurance (AYP), Area Revenue Protection Insurance with Harvest Price Exclusion (ARP-HPE), and Area Revenue Protection Insurance (ARP), respectively. These new area plans collectively are referred to as ARPI. While the new area plans improve upon GRIP-HPO, GRIP, and GRP by establishing uniform commodity prices across plans, the proposed rule raises issues in other respects, such as the introduction of the total loss factor in the indemnity calculation and the additional burden and cost of reporting production. Despite proposing new plans of insurance for area coverage, some underlying concerns with area plan protection remain. Farmers currently do not report their acreage and production with GRP and GRIP plans. This has kept transaction costs low and provided an advantage over individual insurance plans for which production reporting has been mandatory. Nevertheless, the experience with GRP and GRIP programs has pointed out significant problems with the availability of reliable county yield estimates from the National Agricultural Statistics Service (NASS). RMA discontinued GRP/GRIP programs in 1,062 counties in 2010, which included counties producing corn, soybeans, grain sorghum, and peanuts due to the introduction of revised standards by NASS which resulted in fewer but more reliable county yield estimates. With the new area plan, ARPI, FCIC proposes to require farmers to submit both an acreage report and an annual production report. With the new production reporting requirement, FCIC proposes to build its own database in order to support and maintain area plans. Since FCIC collects more detailed information from a much larger sample of farmers than NASS, its goal may be to rely more heavily on its own data in establishing expected and final county yields. Using the best combination of available data, FCIC intends to release expected county yields on a crop, type, and practice basis. Otherwise, the coverage will not be available. The new ARPI plan proposal maintains the multiplier concept from GRP and GRIP so that farmers with above average yields can get higher protection, and it renames the multiplier as protection factor. This is intended to address the difference in each farmer s own yield as compared to the county average. The maximum protection factor a farmer can select is reduced from 1.5 to 1.2 in the proposal. Also, the proposal introduces a new concept called total loss factor (TLF) which is motivated as accounting for lower county variation compared to an individual farmer s variation. Under the existing area plans, the total policy protection is paid out only if the county experiences a 100 percent loss. In other words, the deductible disappears in its entirety only when a total loss occurs. Under the new plans, due to introduction of TLF, the total policy protection is paid out even in cases where a total loss has not occurred. Moreover, the inclusion of a protection factor that permits the insured potentially to over-insure the crop is problematic. In the aggregate, this could result in total indemnity payments for a county in excess of the total

, on behalf of the FCIC, introduced the Common Crop Insurance Policy (Combo Policy) replacing the previous individual insurance plans with the goal")

8 value of the crop. Given the new requirement for the insured to provide production information, this problem could be mitigated by requiring the insured to support the selected protection factor based on the farmer s own yield in relation to the county yield, just as a farmer needs to support his APH yield to obtain coverage under individual plans of insurance. In summary, the experience with GRP and GRIP plans indicated that area plans can also be prone to moral hazard and adverse selection. Transaction costs with these plans will be increasing due to the acreage and production reporting requirement of the new area insurance, however, the reported data may provide more and better county yield data for RMA to operate the plans. Finally, even if the problems with area plans can be overcome, it has been theoretically shown that individual insurance does a better job in minimizing farmers risk as compared to area insurance (Bulut, Collins, and Zacharias, 2010). Hedging Against Systematic Risk Using Price Options and Futures Contracts An alternative tool for hedging systematic risk is the use of price options, futures contracts, and forward marketing (Grant; Chambers and Quiggin; Barnaby, 2011). However, this idea is dismissed in Miranda and Glauber who reason that the correlation between U.S. output and price has weakened due to increasing international trade. One limitation in Miranda and Glauber s paper is that they assume producers have no control over the idiosyncratic risk they face, which is at odds with the very definition of idiosyncratic risk as being diversifiable risk. In fact, Chambers and Quiggin criticize this assumption and model the producer s choice on the amount of idiosyncratic risk they retain (thereby the amount of idiosyncratic risk they transfer) and the amount of production. Chambers and Quiggin point out that because of the availability of other financial instruments closely related to agriculture (such as options, futures and forward marketing), the role of area insurance in covering systematic risk can be redundant. They even speculate that, under certain conditions, the provision of area insurance may increase the systematic risk. Chambers and Quiggin show that area insurance will be useful to the degree it would reduce the idiosyncratic risk producers are facing rather than protecting against systematic risk. Even then, Chambers and Quiggin question whether the resulting reduction in idiosyncratic risk could justify the cost of introducing area insurance. Grant analyzes the economic decisions of a risk-averse farmer when confronting two types of risk: 1) price risk only, and 2) joint price and quantity risk. If forward contracting is available, and there is only price risk, Grant shows that a farmer can fully hedge risk through forward marketing and the production decision is then independent of the farmer s risk aversion and distribution of price risk. If forward contracting is available, and there is joint output and price risk, then the use of forward marketing does not eliminate all the risk and the choices of production and the forward position are related. Both choices depend on the degree of riskaversion and the joint distribution of price and quantity. The difference in farmers decisions across two risk environments arises from the role of the covariance between quantity and price. Barnaby (2011) points out that a revenue insurance plan, which protects against price risk in either direction, complements forward marketing plans. A producer may be able to hedge a larger share of expected production because insurance provides resources to offset the obligation to deliver in the event of a crop loss. Finally, revenue insurance is more economical than having a separate yield insurance policy and buying put option in futures market. Area Revenue Farm Programs

9 The 2008 Farm Bill emphasized the revenue protection goal for farm programs and introduced new programs such as Supplemental Revenue Assistance Payments (SURE) and Average Crop Revenue Election (ACRE). This was despite the fact that the premium of revenue insurance products which provide protection against revenue shortfalls as a share of total U.S. crop insurance premium is about 80 percent. Farmers have been receiving such protection (individual or county based) since the 1990s. SURE is a whole farm program and makes payments based on individual producer losses over an entire farm. ACRE protects against revenue shortfalls for a crop at the state level. Using a farm level data obtained from Illinois and Kansas Farm Management Associations (for corn, soybeans, and wheat in Illinois and for corn, sorghum, soybeans, and wheat in Kansas) over the time period from 1978 to 2008, Zulauf (2011) finds that the systematic component of the losses appears to be mostly shallow losses, while deeper losses pertain to the idiosyncratic component and that the pattern for shallow versus deep losses differs across states. Zulauf argues that a reason for the introduction of different programs such as ACRE and SURE in addition to crop insurance could be to accommodate different loss patterns in different states. The duplication of coverage and overlap between ACRE and crop insurance appears to be modest (Zulauf, Schnitkey, and Langemeier, 2010). They are separate programs whereas in order to receive a SURE payment, the farmer has to purchase crop insurance. Net crop insurance indemnities are counted against the SURE guarantee which eliminates duplication of payments between the two. Both ACRE and SURE are subject to payment limits while crop insurance is not. The program complexity and slow payment of claims have been major issues for both ACRE and SURE. Overall the participation has been low and selective by region and crop with ACRE. Even though ACRE is optional for all eligible farmers and farmers do not directly pay for it, selection of ACRE has an implicit premium as farmers must give up 20 percent of their direct payment and their entire price-based countercyclical payment along with a 30 percent reduction to their marketing loan rate. This implicit premium does not change with the systematic risk associated with the area and is not based on actuarial or underwriting considerations (Barnaby, 2010). If the implicit premium is mispriced, it may discourage or encourage participation depending on the farmer s risk. Using a theoretical model, Bulut, Collins, and Zacharias (2011) study a risk-averse farmer s relative coverage demand for area versus individual insurance. Assuming that the farmer s losses are imperfectly and positively correlated with area losses, they show that under actuarially fair premium rates, farmers would purchase individual insurance only. In addition, if area-insurance is underpriced while individual insurance is fairly priced, separate area and individual plans are substitutes and demand for area insurance increases whereas demand for individual insurance decreases as the correlation between farmer and area losses increases. Furthermore, whenever individual insurance becomes overpriced while area insurance is fairly priced, some additional demand for area insurance will be created. The model can be useful to explain the pattern of actual coverage in counties where ACRE participation is low or high. From the perspective of a policyholder with crop insurance, whether a loss is due to systematic risk, that is, whether the farmer s loss is correlated to those of other policyholders, or not is irrelevant, so long as these losses can be protected at an affordable premium and the insurer can process and pay for the legitimate claim. Nevertheless, there are two exceptions to this argument.

10 A small portion of systematic risk stemming from market equilibrium risk could be of concern to producers (Zulauf; Schnitkey, 2011). Crop insurance is effective at protecting against within-year price changes but not against price declines which persist over multiple years and might affect the entire farm sector. ACRE is viewed as fulfilling that role through its guarantee based on a 2-year moving average of prices and complements crop insurance in that regard (Schnitkey; Zulauf). Another issue is the imperfect indemnification of shallow losses on individual plans due to the deductible. For example, maximum coverage that can be obtained with revenue or yield protection insurance is 85 percent. Through the deductible, the policyholder has a stake in the outcome, which reduces the moral hazard concern. One way to address the imperfect indemnity or shallow loss issue (albeit indirectly) is via area plans whose indemnities are perceived as being outside of an individual farmer s control. SURE is a more direct approach to addressing shallow losses but may require some modifications in order to be more effective (Schnitkey; Zulauf). Finally, Zuluaf suggests that a farmer s premium subsidies be equal to the systematic risk portion of the farmer s expected loss and argues that current levels of subsidy are higher than the frequencies of actual losses would suggest. Recall that Zulauf s analysis is based on data from Illinois and Kansas for a few major crops. We are unaware of comprehensive U.S. estimates of farm and county yield, loss, or revenue correlations based on individual farm data. Barnett et al. (2005) report estimated average correlations between farm and county yields for corn in 10 states using individual farm data on nearly 67,000 farms during Their correlations varied widely; they were generally high in the heart of the corn belt, ranging from 0.71 in Ohio to 0.82 in Illinois, but fell to 0.49 in Texas and 0.36 in Michigan. These wide correlation differences across regions suggest that county area plans are likely to be of widely differing risk reduction value to producers in various regions. Note that Barnett et al. reported the average estimated correlations between farm and county yields. There is a distribution of the correlation between a farmer s and area losses in a given area, that is, farmers differ in how their yields track the county average yield. That further complicates Zulauf s idea of relating farmer s subsidy to the systematic risk a farmer faces. An alternative explanation for the producer subsidy could be the discrepancy between a farmer s assessment versus government assessment of the risk. Some evidence on farmers overconfidence and bias in underestimating the risk has been reported (Umarov and Sherrick, 2005; Gao et al., 2011). Concluding Comments This article discusses the systematic risk issue in crop insurance markets by reviewing the related agricultural economics literature. After examining the issue from both insurers and farmers perspectives, the review raises the following points. From the insurer s perspective, systematic risk is best addressed through a fairly negotiated SRA agreement. The alternative idea of providing reinsurance through area plans has not been appealing to companies. A fair negotiation must recognize and emphasize the contribution of the private-public partnership in creating the success of the crop insurance program as seen today. The focus of such negotiations should be on whether the program operates effectively and achieves the objectives set for it by Congress by ensuring effective and efficient delivery, creating new insurance opportunities for farmers, keeping premiums affordable, and expanding crop insurance coverage.

11 From the farmers perspective, the risk management needs of the producer are best met with individual crop insurance under actuarially fair rates along with the use of forward marketing. Coverage restrictions imposed in individual insurance against moral hazard concerns can result in a limited indemnity or shallow loss issues. In that context, a partial role for area farm programs or insurance plans to cover deductibles and therefore to improve risk protection is possible. Even then, the individual plan must be the base product while the area plan is stacked on top of individual insurance. Multi-year price risk is a component of systematic risk and can be addressed through actuarially based multiyear insurance policies or farm programs. We argue that the definition of systematic risk should be expanded to include risks associated with climate change and regulations. Climate change has been recognized for increasing risks not only for agricultural insurers but also for other lines of insurance, both catastrophic and non-catastrophic (NAIC, 2008). Even though some resist reacting to the potential risks of climate change, farmers have been adapting to it in various parts of the world such as by changing crop varieties (New York Times, 2011). RMA argues that setting premiums based on actual losses would reflect any additional risk due to climate change. Even though justification can be found for government s role in crop insurance markets as a reinsurer, the funding cuts in the 2008 Farm Bill, the 2011 SRA and the proposals for further cuts to address the Federal budget deficit and premium rate changes have amplified insurers regulatory risk concerns. Regulatory risk adds to the systematic risk companies are facing and further increases the necessary risk-premium for their involvement in crop insurance markets.

12 References: Barnaby, G.A Improved Farm Financial Safety Net Based on Revenue Insurance. Presented at the 2011 Annual Meeting of the Agricultural and Applied Economics Association, July 24-26, 2011, Pittsburgh, Pennsylvania. Barnett, B.J., J.R. Black, Y. Hu, and J.R. Skees Is Area Yield Insurance Competitive with Farm Yield Insurance? Journal of Agricultural and Resource Economics. 30(2): 285: 301. Bulut, H., K. Collins, and T. Zacharias Optimal Coverage Demand with Individual and Area Plans of Insurance. Selected paper for presentation at the 2011 Annual Meeting of the Agricultural and Applied Economics Association, July 24-26, 2011, Pittsburgh, Pennsylvania. Coble, K.H. and B.J.Barnett Implications of Integrated Commodity Programs and Crop Insurance. Journal of Agricultural and Applied Economics. 40(2): Chambers, R.G. and J. Quiggin Optimal Producer Behavior in the Presence of Area- Yield Crop Insurance. American Journal of Agricultural Economics. 84(2): Duncan, J. and R. M. Myers Crop Insurance Under Catastrophic Risk. American Journal of Agricultural Economics. 82 (4) Fabozzi, J.F and F. Modigliani Capital Markets: Institutions and Instruments. 3 rd Edition. Prentize Hall, New Jersey. Glauber, J. W Crop Insurance Reconsidered. American Journal of Agricultural Economics. 86 (5): Gao, X. and C.G. Turvey, R. Nie, L.Wang and R. Kong Crop Insurance Rate Making in the Absence of Crop Yield Data: Subjective Assessments and PERT Distributions in Shaanxi China. Paper presented at SCC-76 Group Annual Meeting, Atlanta, GA, March. Grant, D Theory of the Firm with Joint Price and Output Risk and a Forward Market. American Journal of Agricultural Economics. 67(3): Grant Thornton, LLP Federal Crop Insurance Program: Profitability and Effectiveness Analysis 2010 Update. January 13. Available online at _FINAL.pdf Mahul, O Managing Catastrophic Risk Through Insurance and Securitization. American Journal of Agricultural Economics. 63(3): Mason C., D.J. Hayes and S.H. Lence Systemic Risk in U.S. Crop and Revenue Insurance Programs. CARD Iowa State University Working Paper 01-WP 266.

13 Miranda, M.J. and J.W. Glauber Systemic Risk, Reinsurance, and the Failure of Crop Insurance Markets. American Journal of Agricultural Economics. 79 (1): NAIC The Potential Impact of Climate Change on Insurance Regulation. White Paper. Available at New York Times Article, Farm Groups Step up Interest in Insurance Due to Extreme Weather, but Don t Talk Climate Change. September 14. By Jean Chemnick. Schnitkey, G Farm Commodity Programs Given the Existence of Crop Insurance. Farmdocdaily. Available online at Skees, J.R. and B.J. Black Conceptual and Practical Considerations for Sharing Catastrophic/Systemic Risks. Applied Economic Perspectives and Policy. 21(2): Umarov, A.A. and B. Sherrick Farmers' Subjective Yield Distributions: Calibration and Implications for Crop Insurance Valuation. Presented at the American Agricultural Economics Association Annual Meeting in Providence, RI, July. U.S. General Accounting Office Crop Insurance Program Has Not Fostered Significant Risk Sharing by Insurance Companies. Report to the Chairman, Committee on Agriculture, Nutrition, and Forestry, U.S. Senate, Washington DC, GAO/RCED-92-25, January. Zulauf, C A Coordinated Framework for a 21 st Century Farm Safety Net. Presented at the Agricultural and Applied Economics Association Meeting in Pittsburgh, PA, July. Zulauf, C., G. Schnitkey, and M. Langemeier Average Crop Revenue Election, Crop Insurance, and Supplemental Revenue Assistance: Interactions and Overlap for Illinois and Kansas Farm Program Crops. Journal of Agricultural and Applied Economics, 42(3):

Explaining the Costs

TODAYcrop insurance Explaining the Costs of the Crop Insurance Program By Keith Collins and Frank Schnapp, NCIS This article examines the information typically presented to the public on the costs of the

TODAYcrop insurance Explaining the Costs of the Crop Insurance Program By Keith Collins and Frank Schnapp, NCIS This article examines the information typically presented to the public on the costs of the

Group Risk Income Protection Plan and Group Risk Plans added in New Kansas Counties for 2005 1 Updated 3/12/05

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Risk Management Agency

Risk Management Agency Premium Rate Study Update Questions & Answers November 2012 Q1 Why is RMA examining premium rates and the process for determining them? A1 Section 508(i) of the Federal Crop Insurance

Risk Management Agency Premium Rate Study Update Questions & Answers November 2012 Q1 Why is RMA examining premium rates and the process for determining them? A1 Section 508(i) of the Federal Crop Insurance

Agricultural Outlook Forum For Release: Monday, February 23, 1998 AGRICULTURAL RISK MANAGEMENT AND THE ROLE OF THE PRIVATE SECTOR

Agricultural Outlook Forum For Release: Monday, February 23, 1998 AGRICULTURAL RISK MANAGEMENT AND THE ROLE OF THE PRIVATE SECTOR Joseph W. Glauber Deputy Chief Economist U.S. Department of Agriculture

Agricultural Outlook Forum For Release: Monday, February 23, 1998 AGRICULTURAL RISK MANAGEMENT AND THE ROLE OF THE PRIVATE SECTOR Joseph W. Glauber Deputy Chief Economist U.S. Department of Agriculture

Lower Rates Mean Lower Crop Insurance Cost 1

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Details of the Proposed Stacked Income Protection Plan (STAX) Program for Cotton Producers and Potential Strategies for Extension Education

Program for Cotton Producers and Potential Strategies for Extension Education") Journal of Agricultural and Applied Economics, 45,3(August 2013):569 575 Ó 2013 Southern Agricultural Economics Association Details of the Proposed Stacked Income Protection Plan (STAX) Program for Cotton

Journal of Agricultural and Applied Economics, 45,3(August 2013):569 575 Ó 2013 Southern Agricultural Economics Association Details of the Proposed Stacked Income Protection Plan (STAX) Program for Cotton

CROP REVENUE COVERAGE INSURANCE PROVIDES ADDITIONAL RISK MANAGEMENT WHEAT ALTERNATIVES 1

Presented at the 1997 Missouri Commercial Agriculture Crop Institute CROP REVENUE COVERAGE INSURANCE PROVIDES ADDITIONAL RISK MANAGEMENT WHEAT ALTERNATIVES 1 Presented by: Art Barnaby Managing Risk With

Presented at the 1997 Missouri Commercial Agriculture Crop Institute CROP REVENUE COVERAGE INSURANCE PROVIDES ADDITIONAL RISK MANAGEMENT WHEAT ALTERNATIVES 1 Presented by: Art Barnaby Managing Risk With

We have seen in the How

: Examples Using Hedging, Forward Contracting, Crop Insurance, and Revenue Insurance To what extent can hedging, forward contracting, and crop and revenue insurance reduce uncertainty within the year (intrayear)

: Examples Using Hedging, Forward Contracting, Crop Insurance, and Revenue Insurance To what extent can hedging, forward contracting, and crop and revenue insurance reduce uncertainty within the year (intrayear)

Analysis of the STAX and SCO Programs for Cotton Producers

Analysis of the STAX and SCO Programs for Cotton Producers Jody L. Campiche Department of Agricultural Economics Oklahoma State University Selected Paper prepared for presentation at the Agricultural &

Analysis of the STAX and SCO Programs for Cotton Producers Jody L. Campiche Department of Agricultural Economics Oklahoma State University Selected Paper prepared for presentation at the Agricultural &

CHOOSING AMONG CROP INSURANCE PRODUCTS

CHOOSING AMONG CROP INSURANCE PRODUCTS Gary Schnitkey Department of Agricultural and Consumer Economics University of Illinois at Urbana-Champaign Email: schnitke@uiuc.edu, Phone: (217) 244-9595 August

CHOOSING AMONG CROP INSURANCE PRODUCTS Gary Schnitkey Department of Agricultural and Consumer Economics University of Illinois at Urbana-Champaign Email: schnitke@uiuc.edu, Phone: (217) 244-9595 August

Managing Risk With Revenue Insurance

Managing Risk With Revenue Insurance VOLUME 4 ISSUE 5 22 Robert Dismukes, dismukes@ers.usda.gov Keith H. Coble, coble@agecon.msstate.edu Comstock 10 Crop revenue insurance offers farmers a way to manage

Managing Risk With Revenue Insurance VOLUME 4 ISSUE 5 22 Robert Dismukes, dismukes@ers.usda.gov Keith H. Coble, coble@agecon.msstate.edu Comstock 10 Crop revenue insurance offers farmers a way to manage

Group Risk Income Protection Plan added in Kansas for 2006 Wheat (Updated) 1

1") Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

TODAYcrop insurance. Crop Insurance Rate of Return. Issues & Concerns. By Frank Schnapp, NCIS

TODAYcrop insurance Crop Insurance Rate of Return Issues & Concerns By Frank Schnapp, NCIS In recent months, a variety of claims have been aired in the press regarding the cost of delivery of the Federal

TODAYcrop insurance Crop Insurance Rate of Return Issues & Concerns By Frank Schnapp, NCIS In recent months, a variety of claims have been aired in the press regarding the cost of delivery of the Federal

From Catastrophic to Shallow Loss Coverage: An Economist's Perspective of U.S. Crop Insurance Program and Implications for Developing Countries

From Catastrophic to Shallow Loss Coverage: An Economist's Perspective of U.S. Crop Insurance Program and Implications for Developing Countries Robert Dismukes Agricultural Economist Insurance coverage:

From Catastrophic to Shallow Loss Coverage: An Economist's Perspective of U.S. Crop Insurance Program and Implications for Developing Countries Robert Dismukes Agricultural Economist Insurance coverage:

Implications of Crop Insurance as Social Policy

Implications of Crop Insurance as Social Policy Bruce Babcock Iowa State University Presented at the Minnesota Crop Insurance Conference Sept 10, 2014 Mankato, MN Summary of talk 2014 farm bill irrevocably

Implications of Crop Insurance as Social Policy Bruce Babcock Iowa State University Presented at the Minnesota Crop Insurance Conference Sept 10, 2014 Mankato, MN Summary of talk 2014 farm bill irrevocably

The Supplementary Insurance Coverage Option: A New Risk Management Tool for Wyoming Producers

The Supplementary Insurance Coverage Option: A New Risk Management Tool for Wyoming Producers Agricultural Marketing Policy Center Linfield Hall P.O. Box 172920 Montana State University Bozeman, MT 59717-2920

The Supplementary Insurance Coverage Option: A New Risk Management Tool for Wyoming Producers Agricultural Marketing Policy Center Linfield Hall P.O. Box 172920 Montana State University Bozeman, MT 59717-2920

How To Insure A Crop

Materials Prepared for Federation of Southern Cooperatives Epes, Alabama September 11, 2009 Group Risk Crop Insurance by Karen R. Krub Farmers Legal Action Group, Inc. 360 North Robert Street, Suite 500

Materials Prepared for Federation of Southern Cooperatives Epes, Alabama September 11, 2009 Group Risk Crop Insurance by Karen R. Krub Farmers Legal Action Group, Inc. 360 North Robert Street, Suite 500

Understanding the Standard Reinsurance Agreement, Explains Crop Insurance Companies Losses 1,2

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Volume Title: The Intended and Unintended Effects of U.S. Agricultural and Biotechnology Policies

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: The Intended and Unintended Effects of U.S. Agricultural and Biotechnology Policies Volume Author/Editor:

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: The Intended and Unintended Effects of U.S. Agricultural and Biotechnology Policies Volume Author/Editor:

What Percent Level and Type of Crop Insurance Should Winter Wheat Growers Select? 1

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

GAO CROP INSURANCE. Opportunities Exist to Reduce the Costs of Administering the Program. Report to Congressional Requesters

GAO United States Government Accountability Office Report to Congressional Requesters April 2009 CROP INSURANCE Opportunities Exist to Reduce the Costs of Administering the Program GAO-09-445 { April 2009

GAO United States Government Accountability Office Report to Congressional Requesters April 2009 CROP INSURANCE Opportunities Exist to Reduce the Costs of Administering the Program GAO-09-445 { April 2009

Federal Crop Insurance: Background and Issues

Federal Crop Insurance: Background and Issues Dennis A. Shields Specialist in Agricultural Policy December 13, 2010 Congressional Research Service CRS Report for Congress Prepared for Members and Committees

Federal Crop Insurance: Background and Issues Dennis A. Shields Specialist in Agricultural Policy December 13, 2010 Congressional Research Service CRS Report for Congress Prepared for Members and Committees

Crop Insurance as a Tool

Crop Insurance as a Tool By: Chris Bastian University of Wyoming There are several approaches to address income variability associated with production risk. One approach is to produce more than one product

Crop Insurance as a Tool By: Chris Bastian University of Wyoming There are several approaches to address income variability associated with production risk. One approach is to produce more than one product

Crop Insurance for Cotton Producers: Key Concepts and Terminology

Crop Insurance for Cotton Producers: Key Concepts and Terminology With large investments in land, equipment, and technology, cotton producers typically have more capital at risk than producers of other

Crop Insurance for Cotton Producers: Key Concepts and Terminology With large investments in land, equipment, and technology, cotton producers typically have more capital at risk than producers of other

To: Board of Directors September 17, 2001 Federal Crop Insurance Corporation

United States Department of Agriculture Federal Crop Insurance Corporation 1400 Independence Ave, SW Stop 0801 Washington, DC 20250-0801 To: Board of Directors September 17, 2001 Federal Crop Insurance

United States Department of Agriculture Federal Crop Insurance Corporation 1400 Independence Ave, SW Stop 0801 Washington, DC 20250-0801 To: Board of Directors September 17, 2001 Federal Crop Insurance

Audit Report. Risk Management Agency Financial Management Controls Over Reinsured Companies. U.S. Department of Agriculture

U.S. Department of Agriculture Office of Inspector General Great Plains Region Audit Report Risk Management Agency Financial Management Controls Over Reinsured Companies Report No. 05801-3-KC April 2006

U.S. Department of Agriculture Office of Inspector General Great Plains Region Audit Report Risk Management Agency Financial Management Controls Over Reinsured Companies Report No. 05801-3-KC April 2006

Multiple Peril Crop Insurance

Multiple Peril Crop Insurance Multiple Peril Crop Insurance (MPCI) is a broadbased crop insurance program regulated by the U.S. Department of Agriculture and subsidized by the Federal Crop Insurance Corporation

Multiple Peril Crop Insurance Multiple Peril Crop Insurance (MPCI) is a broadbased crop insurance program regulated by the U.S. Department of Agriculture and subsidized by the Federal Crop Insurance Corporation

What Harm is Done by Subsidizing Crop Insurance?

What Harm is Done by Subsidizing Crop Insurance? Barry K. Goodwin and Vincent H. Smith 1 Agriculture is subject to a wide variety of risks, including many hazards arising from wide-spread natural disasters.

What Harm is Done by Subsidizing Crop Insurance? Barry K. Goodwin and Vincent H. Smith 1 Agriculture is subject to a wide variety of risks, including many hazards arising from wide-spread natural disasters.

Renegotiation of the Standard Reinsurance Agreement (SRA) for Federal Crop Insurance

for Federal Crop Insurance") Renegotiation of the Standard Reinsurance Agreement (SRA) for Federal Crop Insurance Dennis A. Shields Specialist in Agricultural Policy August 12, 2010 Congressional Research Service CRS Report for Congress

Renegotiation of the Standard Reinsurance Agreement (SRA) for Federal Crop Insurance Dennis A. Shields Specialist in Agricultural Policy August 12, 2010 Congressional Research Service CRS Report for Congress

Portfolio Allocation and Alternative Structures of the Standard Reinsurance Agreement

Journal of Agricultural and Resource Economics 3 1(1):57-73 Copyright 2006 Western Agricultural Economics Association Portfolio Allocation and Alternative Structures of the Standard Reinsurance Agreement

Journal of Agricultural and Resource Economics 3 1(1):57-73 Copyright 2006 Western Agricultural Economics Association Portfolio Allocation and Alternative Structures of the Standard Reinsurance Agreement

Understanding Crop Insurance Principles: A Primer for Farm Leaders

Mississippi State University Department of Agricultural Economics Research Report No. 209 February 1999 Understanding Crop Insurance Principles: A Primer for Farm Leaders Barry J. Barnett and Keith H.

Mississippi State University Department of Agricultural Economics Research Report No. 209 February 1999 Understanding Crop Insurance Principles: A Primer for Farm Leaders Barry J. Barnett and Keith H.

CROP INSURANCE. Reducing Subsidies for Highest Income Participants Could Save Federal Dollars with Minimal Effect on the Program

United States Government Accountability Office Report to Congressional Requesters March 2015 CROP INSURANCE Reducing Subsidies for Highest Income Participants Could Save Federal Dollars with Minimal Effect

United States Government Accountability Office Report to Congressional Requesters March 2015 CROP INSURANCE Reducing Subsidies for Highest Income Participants Could Save Federal Dollars with Minimal Effect

Will ARC Allow Farmers to Cancel Their 2014 Crop Insurance (Updated)? 1

? 1") Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Both the House and Senate farm bills include two new supplemental crop insurance programs:

Background Both the House and Senate farm bills include two new supplemental crop insurance programs: Supplemental Coverage Option (SCO) Stacked Income Protection Plan (STAX) for upland cotton Similar

Background Both the House and Senate farm bills include two new supplemental crop insurance programs: Supplemental Coverage Option (SCO) Stacked Income Protection Plan (STAX) for upland cotton Similar

HISTORICAL RATE OF RETURN ANALYSIS

HISTORICAL RATE OF RETURN ANALYSIS Prepared for: Risk Management Agency United States Department of Agriculture Prepared by: Milliman, Inc. David Appel, Ph.D. Philip S. Borba, Ph.D. August 18, 2009 The

HISTORICAL RATE OF RETURN ANALYSIS Prepared for: Risk Management Agency United States Department of Agriculture Prepared by: Milliman, Inc. David Appel, Ph.D. Philip S. Borba, Ph.D. August 18, 2009 The

Title I Programs of the 2014 Farm Bill

Frequently Asked Questions: Title I Programs of the 2014 Farm Bill November 2014 Robin Reid G.A. Art Barnaby Mykel Taylor Extension Associate Extension Specialist Assistant Professor Kansas State University

Frequently Asked Questions: Title I Programs of the 2014 Farm Bill November 2014 Robin Reid G.A. Art Barnaby Mykel Taylor Extension Associate Extension Specialist Assistant Professor Kansas State University

Crop Insurance Plan Explanations and Review

Crop Insurance Plan Explanations and Review Table of Contents Page Information/Insurance Plans 1 Crop Revenue Coverage (CRC) 2 Multiple Peril Crop Insurance (MPCI) 2 Income Protection (IP) 3 Group Risk

Crop Insurance Plan Explanations and Review Table of Contents Page Information/Insurance Plans 1 Crop Revenue Coverage (CRC) 2 Multiple Peril Crop Insurance (MPCI) 2 Income Protection (IP) 3 Group Risk

Cost & Efficiency Analysis of U.S. Crop Insurance Program: Implications of Additional FSA Responsibilities

Cost & Efficiency Analysis of U.S. Crop Insurance Program: Implications of Additional FSA Responsibilities Executive Summary Prepared for: Informa Economics Phone: 901.766.4669 www.informaecon.com September

Cost & Efficiency Analysis of U.S. Crop Insurance Program: Implications of Additional FSA Responsibilities Executive Summary Prepared for: Informa Economics Phone: 901.766.4669 www.informaecon.com September

How Large is the 2012 Crop Insurance Underwriting Loss? 1

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Crop Insurance: Background Statistics on Participation and Results

September 2010 Crop Insurance: Background Statistics on Participation and Results FAPRI MU Report #10 10 Providing objective analysis for more than 25 years www.fapri.missouri.edu This report was prepared

September 2010 Crop Insurance: Background Statistics on Participation and Results FAPRI MU Report #10 10 Providing objective analysis for more than 25 years www.fapri.missouri.edu This report was prepared

Influence of the Premium Subsidy on Farmers Crop Insurance Coverage Decisions

Influence of the Premium Subsidy on Farmers Crop Insurance Coverage Decisions Bruce A. Babcock and Chad E. Hart Working Paper 05-WP 393 April 2005 Center for Agricultural and Rural Development Iowa State

Influence of the Premium Subsidy on Farmers Crop Insurance Coverage Decisions Bruce A. Babcock and Chad E. Hart Working Paper 05-WP 393 April 2005 Center for Agricultural and Rural Development Iowa State

PROPERTY/CASUALTY INSURANCE AND SYSTEMIC RISK

PROPERTY/CASUALTY INSURANCE AND SYSTEMIC RISK Steven N. Weisbart, Ph.D., CLU Chief Economist President April 2011 INTRODUCTION To prevent another financial meltdown like the one that affected the world

PROPERTY/CASUALTY INSURANCE AND SYSTEMIC RISK Steven N. Weisbart, Ph.D., CLU Chief Economist President April 2011 INTRODUCTION To prevent another financial meltdown like the one that affected the world

The Impact of Alternative Farm Bill Designs on the Aggregate Distribution of Farm Program Payments. Keith H. Coble and Barry J.

The Impact of Alternative Farm Bill Designs on the Aggregate Distribution of Farm Program Payments Keith H. Coble and Barry J. Barnett Abstract Several 2007 farm bill proposals focused on reforming commodity

The Impact of Alternative Farm Bill Designs on the Aggregate Distribution of Farm Program Payments Keith H. Coble and Barry J. Barnett Abstract Several 2007 farm bill proposals focused on reforming commodity

Federal Crop Insurance: Background

Dennis A. Shields Specialist in Agricultural Policy August 13, 2015 Congressional Research Service 7-5700 www.crs.gov R40532 Summary The federal crop insurance program began in 1938 when Congress authorized

Dennis A. Shields Specialist in Agricultural Policy August 13, 2015 Congressional Research Service 7-5700 www.crs.gov R40532 Summary The federal crop insurance program began in 1938 when Congress authorized

Federal Crop Insurance: The Basics

Federal Crop Insurance: The Basics Presented by Shawn Wade Director of Communications Plains Cotton Growers, Inc. 4517 West Loop 289 Lubbock, TX 79414 WWW.PLAINSCOTTON.ORG Why Federal Crop Insurance? Every

Federal Crop Insurance: The Basics Presented by Shawn Wade Director of Communications Plains Cotton Growers, Inc. 4517 West Loop 289 Lubbock, TX 79414 WWW.PLAINSCOTTON.ORG Why Federal Crop Insurance? Every

OECD-INEA-FAO Workshop on Agriculture and Adaptation to Climate Change. June 2010

Climate Change and Crop Insurance in the United States OECD-INEA-FAO Workshop on Agriculture and Adaptation to Climate Change June 2010 Outline Overview of U.S. crop insurance program Historical loss experience

Climate Change and Crop Insurance in the United States OECD-INEA-FAO Workshop on Agriculture and Adaptation to Climate Change June 2010 Outline Overview of U.S. crop insurance program Historical loss experience

The 2014 Farm Bill left the farm-level COM-

Current Crop Ag Decision Maker Insurance Policies File A1-48 The 2014 Farm Bill left the farm-level COM- BO products introduced by the Risk Management Agency in 2011 unchanged, but released the Area Risk

Current Crop Ag Decision Maker Insurance Policies File A1-48 The 2014 Farm Bill left the farm-level COM- BO products introduced by the Risk Management Agency in 2011 unchanged, but released the Area Risk

2014 Farm Bill How does it affect you and your operation? Cotton STAX & SCO

2014 Farm Bill How does it affect you and your operation? Cotton STAX & SCO 1 2014 Farm Bill Cotton Chuck Danehower Extension Area Specialist Farm Management University of Tennessee Extension cdanehow@utk.edu

2014 Farm Bill How does it affect you and your operation? Cotton STAX & SCO 1 2014 Farm Bill Cotton Chuck Danehower Extension Area Specialist Farm Management University of Tennessee Extension cdanehow@utk.edu

Group Risk Income Protection

Group Risk Income Protection James B. Johnson and John Hewlett* Objective Analysis for Informed Agricultural Marketing Policy Paper No. 13 July 2006 Decision Making * University of Wyoming, Extension Educator

Group Risk Income Protection James B. Johnson and John Hewlett* Objective Analysis for Informed Agricultural Marketing Policy Paper No. 13 July 2006 Decision Making * University of Wyoming, Extension Educator

Portfolio Allocation and Alternative Structures of the Standard

Portfolio Allocation and Alternative Structures of the Standard Reinsurance Agreement Dmitry V. Vedenov, Mario J. Miranda, Robert Dismukes, and Joseph W. Glauber 1 Selected Paper presented at AAEA Annual

Portfolio Allocation and Alternative Structures of the Standard Reinsurance Agreement Dmitry V. Vedenov, Mario J. Miranda, Robert Dismukes, and Joseph W. Glauber 1 Selected Paper presented at AAEA Annual

Ratemaking Considerations for Multiple Peril Crop lnsurance

Ratemaking Considerations for Multiple Peril Crop lnsurance Frank F. Schnapp, ACAS, MAAA, James L. Driscoll, Thomas P. Zacharias, and Gary R. Josephson, FCAS, MAAA 159 Ratemaking Considerations for Multiple

Ratemaking Considerations for Multiple Peril Crop lnsurance Frank F. Schnapp, ACAS, MAAA, James L. Driscoll, Thomas P. Zacharias, and Gary R. Josephson, FCAS, MAAA 159 Ratemaking Considerations for Multiple

Crop Insurance Reserving

Carl X. Ashenbrenner Abstract: The crop insurance industry is a private-public partnership, whereby the private companies issue policies and handle claims for multi-peril crop insurance policies, which

Carl X. Ashenbrenner Abstract: The crop insurance industry is a private-public partnership, whereby the private companies issue policies and handle claims for multi-peril crop insurance policies, which

Traditional Products. The two Traditional Crop Insurance Products are: Named Peril Crop Insurance (NPCI) Multi Peril Crop Insurance (MPCI)

Multi Peril Crop Insurance (MPCI)") Traditional Products Traditional crop insurance relies on the principle of indemnity, where losses are measured in the field either after the event (named peril crop insurance) or through yield measurement

Traditional Products Traditional crop insurance relies on the principle of indemnity, where losses are measured in the field either after the event (named peril crop insurance) or through yield measurement

U.S. crop program fiscal costs: Revised estimates with updated participation information

U.S. crop program fiscal costs: Revised estimates with updated participation information June 2015 FAPRI MU Report #02 15 Providing objective analysis for 30 years www.fapri.missouri.edu Published by the

U.S. crop program fiscal costs: Revised estimates with updated participation information June 2015 FAPRI MU Report #02 15 Providing objective analysis for 30 years www.fapri.missouri.edu Published by the

The AIR Multiple Peril Crop Insurance (MPCI) Model For The U.S.

Model For The U.S.") The AIR Multiple Peril Crop Insurance (MPCI) Model For The U.S. According to the National Climatic Data Center, crop damage from widespread flooding or extreme drought was the primary driver of loss in

The AIR Multiple Peril Crop Insurance (MPCI) Model For The U.S. According to the National Climatic Data Center, crop damage from widespread flooding or extreme drought was the primary driver of loss in

CHAPTER 2 AGRICULTURAL INSURANCE: A BACKGROUND 9

CHAPTER 2 AGRICULTURAL INSURANCE: A BACKGROUND 9 Chapter 2: AGRICULTURAL INSURANCE: A BACKGROUND In Chapter 1 we saw that insurance is one of the tools that farmers and other stakeholders can use to manage

CHAPTER 2 AGRICULTURAL INSURANCE: A BACKGROUND 9 Chapter 2: AGRICULTURAL INSURANCE: A BACKGROUND In Chapter 1 we saw that insurance is one of the tools that farmers and other stakeholders can use to manage

GAO CROP INSURANCE. Savings Would Result from Program Changes and Greater Use of Data Mining

GAO March 2012 United States Government Accountability Office Report to the Ranking Member, Permanent Subcommittee on Investigations, Committee on Homeland Security and Governmental Affairs, U.S. Senate

GAO March 2012 United States Government Accountability Office Report to the Ranking Member, Permanent Subcommittee on Investigations, Committee on Homeland Security and Governmental Affairs, U.S. Senate

Designing Crop Insurance to Manage Moral Hazard Costs

Designing Crop Insurance to Manage Moral Hazard Costs R.D. Weaver e-mail: r2w@psu.edu Taeho Kim Paper prepared for presentation at the X th EAAE Congress Exploring Diversity in the European Agri-Food System,

Designing Crop Insurance to Manage Moral Hazard Costs R.D. Weaver e-mail: r2w@psu.edu Taeho Kim Paper prepared for presentation at the X th EAAE Congress Exploring Diversity in the European Agri-Food System,

(Over)reacting to bad luck: low yields increase crop insurance participation. Howard Chong Jennifer Ifft

reacting to bad luck: low yields increase crop insurance participation. Howard Chong Jennifer Ifft") (Over)reacting to bad luck: low yields increase crop insurance participation Howard Chong Jennifer Ifft Motivation Over the last 3 decades, U.S. farms have steadily increased participation in the Federal

(Over)reacting to bad luck: low yields increase crop insurance participation Howard Chong Jennifer Ifft Motivation Over the last 3 decades, U.S. farms have steadily increased participation in the Federal

How Crop Insurance Works. The Basics

How Crop Insurance Works The Basics Behind the Policy Federal Crop Insurance Corporation Board of Directors Approve Policies Policy changes General direction of program Risk Management Agency Administers

How Crop Insurance Works The Basics Behind the Policy Federal Crop Insurance Corporation Board of Directors Approve Policies Policy changes General direction of program Risk Management Agency Administers

THE INVOLVEMENT OF GOVERNMENTS IN THE DEVELOPMENT OF AGRICULTURAL INSURANCE

International Journal of Economics, Commerce and Management United Kingdom Vol. III, Issue 6, June 2015 http://ijecm.co.uk/ ISSN 2348 0386 THE INVOLVEMENT OF GOVERNMENTS IN THE DEVELOPMENT OF AGRICULTURAL

International Journal of Economics, Commerce and Management United Kingdom Vol. III, Issue 6, June 2015 http://ijecm.co.uk/ ISSN 2348 0386 THE INVOLVEMENT OF GOVERNMENTS IN THE DEVELOPMENT OF AGRICULTURAL

Proposals to Reduce Premium Subsidies for Federal Crop Insurance

Proposals to Reduce Premium Subsidies for Federal Crop Insurance Dennis A. Shields Specialist in Agricultural Policy March 20, 2015 Congressional Research Service 7-5700 www.crs.gov R43951 Summary Many

Proposals to Reduce Premium Subsidies for Federal Crop Insurance Dennis A. Shields Specialist in Agricultural Policy March 20, 2015 Congressional Research Service 7-5700 www.crs.gov R43951 Summary Many

Yield Protection Crop Insurance will have the same Yield Coverage as Revenue Protection, but RP is Expected to be the Preferred Choice (Updated) 1

1") Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

JAMAICA. Agricultural Insurance: Scope and Limitations for Weather Risk Management. Diego Arias Economist. 18 June 2009

JAMAICA Agricultural Insurance: Scope and Limitations for Weather Risk Management Diego Arias Economist 18 June 2009 Financed partly by the AAACP EU Support to the Caribbean Agenda The global market Products

JAMAICA Agricultural Insurance: Scope and Limitations for Weather Risk Management Diego Arias Economist 18 June 2009 Financed partly by the AAACP EU Support to the Caribbean Agenda The global market Products

Evaluating Taking Prevented Planting Payments for Corn

May 30, 2013 Evaluating Taking Prevented Planting Payments for Corn Permalink URL http://farmdocdaily.illinois.edu/2013/05/evaluating-prevented-planting-corn.html Due to continuing wet weather, some farmers

May 30, 2013 Evaluating Taking Prevented Planting Payments for Corn Permalink URL http://farmdocdaily.illinois.edu/2013/05/evaluating-prevented-planting-corn.html Due to continuing wet weather, some farmers

THE COMMODITY RISK MANAGEMENT GROUP WORLD BANK

THE COMMODITY RISK MANAGEMENT GROUP WORLD BANK Agricultural Insurance: Scope and Limitations for Rural Risk Management 5 March 2009 Agenda The global market Products Organisation of agricultural insurance

THE COMMODITY RISK MANAGEMENT GROUP WORLD BANK Agricultural Insurance: Scope and Limitations for Rural Risk Management 5 March 2009 Agenda The global market Products Organisation of agricultural insurance

DAIRY MARKETS And POLICY

DAIRY MARKETS And POLICY ISSUES AND OPTIONS P-10 May 1993 CCC DAIRY COMMODITY LOANS AS AN ALTERNATIVE TO THE PURCHASE PROGRAM Ronald D. Knutson and Edward G. Smith * The dairy price support program operates

DAIRY MARKETS And POLICY ISSUES AND OPTIONS P-10 May 1993 CCC DAIRY COMMODITY LOANS AS AN ALTERNATIVE TO THE PURCHASE PROGRAM Ronald D. Knutson and Edward G. Smith * The dairy price support program operates

Agricultural Reinsurance

Issues Barry K. Goodwin North Carolina State University October 7, 2013 AAEA Crop Insurance and The Farm Bill Symposium Louisville, Kentucky Introduction Reinsurance is simply insurance taken by insurers

Issues Barry K. Goodwin North Carolina State University October 7, 2013 AAEA Crop Insurance and The Farm Bill Symposium Louisville, Kentucky Introduction Reinsurance is simply insurance taken by insurers

Comparing LRP to a Put Option

Comparing LRP to a Put Option Dr. G. A. Art Barnaby, Jr Kansas State University Phone: (785) 532-1515 Email: abarnaby@agecon.ksu.edu Check out our WEB at: AgManager.info 1 Livestock Risk Protection (LRP)

Comparing LRP to a Put Option Dr. G. A. Art Barnaby, Jr Kansas State University Phone: (785) 532-1515 Email: abarnaby@agecon.ksu.edu Check out our WEB at: AgManager.info 1 Livestock Risk Protection (LRP)

U.S. Farm Policy: Overview and Farm Bill Update. Jason Hafemeister 12 June 2014. Office of the Chief Economist. Trade Bureau

U.S. Farm Policy: Office of the Chief Economist Trade Bureau Overview and Farm Bill Update Jason Hafemeister 12 June 2014 Agenda Background on U.S. Agriculture area, output, inputs, income Key Elements

U.S. Farm Policy: Office of the Chief Economist Trade Bureau Overview and Farm Bill Update Jason Hafemeister 12 June 2014 Agenda Background on U.S. Agriculture area, output, inputs, income Key Elements

WEATHER DERIVATIVES AND SPECIFIC EVENT RISK. Calum G. Turvey

WEATHER DERIVATIVES AND SPECIFIC EVENT RISK By Calum G. Turvey Associate Professor Department of Agricultural Economics and Business Faculty of Management University of Guelph Guelph Ontario Canada Paper

WEATHER DERIVATIVES AND SPECIFIC EVENT RISK By Calum G. Turvey Associate Professor Department of Agricultural Economics and Business Faculty of Management University of Guelph Guelph Ontario Canada Paper

Crop Insurance Rates and the Laws of Probability

Crop Insurance Rates and the Laws of Probability Bruce A. Babcock, Chad E. Hart, and Dermot J. Hayes Working Paper 02-WP 298 April 2002 Center for Agricultural and Rural Development Iowa State University

Crop Insurance Rates and the Laws of Probability Bruce A. Babcock, Chad E. Hart, and Dermot J. Hayes Working Paper 02-WP 298 April 2002 Center for Agricultural and Rural Development Iowa State University

U.S. Livestock Insurance

TODAYcrop insurance The State of U.S. Livestock Insurance By, Dr. Keith Collins, NCIS Editor s Note: Dr. Collins made a presentation on the state of U.S. livestock insurance products at the Congress of

TODAYcrop insurance The State of U.S. Livestock Insurance By, Dr. Keith Collins, NCIS Editor s Note: Dr. Collins made a presentation on the state of U.S. livestock insurance products at the Congress of

ACTUARIAL FAIRNESS OF CROP INSURANCE RATES

ACTUARIAL FAIRNESS OF CROP INSURANCE RATES WITH CONSTANT RATE RELATIVITIES BRUCE A. BABCOCK,CHAD E. HART, AND DERMOT J. HAYES Increased availability and demand for low-deductible crop insurance policies

ACTUARIAL FAIRNESS OF CROP INSURANCE RATES WITH CONSTANT RATE RELATIVITIES BRUCE A. BABCOCK,CHAD E. HART, AND DERMOT J. HAYES Increased availability and demand for low-deductible crop insurance policies

Crop Tariff Models For Farmers Insurance

Rationality of Choices in Subsidized Crop Insurance Markets HONGLI FENG, IOWA STATE UNIVERSITY XIAODONG (SHELDON) DU, UNIVERSITY OF WISCONSIN-MADISON DAVID HENNESSY, IOWA STATE UNIVERSITY Plan of talk

Rationality of Choices in Subsidized Crop Insurance Markets HONGLI FENG, IOWA STATE UNIVERSITY XIAODONG (SHELDON) DU, UNIVERSITY OF WISCONSIN-MADISON DAVID HENNESSY, IOWA STATE UNIVERSITY Plan of talk

Understanding Crop Insurance Principles: A Primer for Farm Leaders

Understanding Crop Insurance Principles: A Primer for arm Leaders Barry J. Barnett Assistant Professor MSU Agricultural Economics Department Keith H. Coble Assistant Professor MSU Agricultural Economics

Understanding Crop Insurance Principles: A Primer for arm Leaders Barry J. Barnett Assistant Professor MSU Agricultural Economics Department Keith H. Coble Assistant Professor MSU Agricultural Economics

AFBF Comparison of Senate and House Committee passed Farm Bills May 16, 2013

CURRENT LAW SENATE AG COMMITTEE (S. 954) HOUSE AG COMMITTEE (HR 1947) Reported out of Committee 15 5 Reported out of Committee 36 10 Cost $979.7 billion over the 10 years before sequester reductions of

CURRENT LAW SENATE AG COMMITTEE (S. 954) HOUSE AG COMMITTEE (HR 1947) Reported out of Committee 15 5 Reported out of Committee 36 10 Cost $979.7 billion over the 10 years before sequester reductions of

Common Crop Insurance Policy (CCIP) DR. G. A. ART BARNABY, JR. Kansas State University 4B Agricultural Consultants

DR. G. A. ART BARNABY, JR. Kansas State University 4B Agricultural Consultants") Common Crop Insurance Policy (CCIP) DR. G. A. ART BARNABY, JR. Kansas State University 4B Agricultural Consultants Phone: 785-532-1515 EMAIL: barnaby@ksu.edu Check out our WEB page at http://www.agmanager.info

Common Crop Insurance Policy (CCIP) DR. G. A. ART BARNABY, JR. Kansas State University 4B Agricultural Consultants Phone: 785-532-1515 EMAIL: barnaby@ksu.edu Check out our WEB page at http://www.agmanager.info

Evaluating the Impact of Proposed Farm Bill Programs with Crop Insurance for Southern Crops. Todd D. Davis * John D. Anderson Nathan B.

Evaluating the Impact of Proposed Farm Bill Programs with Crop Insurance for Southern Crops Todd D. Davis * John D. Anderson Nathan B. Smith Selected Paper prepared for presentation at the Southern Agricultural

Evaluating the Impact of Proposed Farm Bill Programs with Crop Insurance for Southern Crops Todd D. Davis * John D. Anderson Nathan B. Smith Selected Paper prepared for presentation at the Southern Agricultural

THREE ESSAYS ON CROP INSURANCE: RMA S RULES AND PARTICIPATION, AND PERCEPTIONS ALISHER UMAROV

THREE ESSAYS ON CROP INSURANCE: RMA S RULES AND PARTICIPATION, AND PERCEPTIONS BY ALISHER UMAROV B.S., North Dakota State University, 2000 M.S., North Dakota State University, 2003 DISSERTATION Submitted

THREE ESSAYS ON CROP INSURANCE: RMA S RULES AND PARTICIPATION, AND PERCEPTIONS BY ALISHER UMAROV B.S., North Dakota State University, 2000 M.S., North Dakota State University, 2003 DISSERTATION Submitted

Farm Programs and Crop Insurance

Evaluating the Interaction between Farm Programs with Crop Insurance and Producers Risk Preferences Todd D. Davis John D. Anderson Robert E. Young Senior Economist Deputy Chief Economist Chief Economist

Evaluating the Interaction between Farm Programs with Crop Insurance and Producers Risk Preferences Todd D. Davis John D. Anderson Robert E. Young Senior Economist Deputy Chief Economist Chief Economist

1. Prices now 2. TA APH yield endorsement 3. Re-rating 4. Suggestions

Crop Insurance Update Gary Schnitkey University of Illinois Topics 1. Prices now 2. TA APH yield endorsement 3. Re-rating 4. Suggestions 2 1 Combo Product and Old Products Type COMBO Product Old Product

Crop Insurance Update Gary Schnitkey University of Illinois Topics 1. Prices now 2. TA APH yield endorsement 3. Re-rating 4. Suggestions 2 1 Combo Product and Old Products Type COMBO Product Old Product