KC 2 Corporate Finance & Risk Management. Suggested Answers and Marking Grid

|

|

|

- Oliver Wilkinson

- 8 years ago

- Views:

Transcription

1 KC 2 Corporate Finance & Risk Management Suggested Answers and Marking Grid

2 Section 1 Question No - 01 A. Learning Outcomes Advise on regulatory implications and procedures on mergers and acquisitions (Companies Act, Securities Exchange Control regulations and other regulatory bodies). 1. As per the Takeovers and Mergers Code, since ABC has acquired 10% of PQR, ABC has to follow the 10% disclosure requirement; i.e. within two market days after acquisition ABC has to inform the management of the target company, the Colombo Stock Exchange (CSE) and the Securities and Exchange Commission (SEC) about the 10% share ownership of PQR. When ABC has acquired ownership of 30% of the voting rights of PQR, it is required to comply with rule 31 of the Takeovers and Mergers Code. A cash offer has to made for the shares held by all remaining shareholders of PQR at the highest market price prevailing during the last 12 months. Any further acquisition equal to or exceeding 2% of the voting rights has to be communicated to the CSE and SEC. The objective of ABC is to acquire controlling interest in PQR with no intention of acquiring 100% of PQR. However, because of the mandatory offer rule, the acquisition looks expensive due to the following reasons: With the announcement of the 10% acquisition, the management of PQR becomes aware of the hostile takeover. Accordingly, PQR may take protective actions which result in the share price of PQR going up and as a result ABC would be compelled to purchase the shares possibly at a higher price than they are worth. In case all or a substantial number of shareholders of PQR accept the offer, ABC has no option than to buy the shares at a higher price. On the other hand, if PQR s shareholders via management collectively decide not to sell further shares, ABC s strategy would become null halfway through the process. If so, an investment has already been made in an asset without generating the expected result. 2

3 Due to these reasons, before taking further actions ABC should carry out a cause and effect analysis under each scenario. ABC has to consider alternative strategies instead of a hostile takeover to acquire PQR s controlling interest and thereby eliminate the possibility of buying PQR at a higher price than it is worth. (10 marks) 2. Learning Outcomes Evaluate business valuation techniques (asset based, earnings based, proxy PE based, cash flow based) for a specific merger or acquisition or divestment. Reasons for undervalues shares The share is unnoticed Companies might sell for less than they're worth because they're under the radar. Small cap shares, foreign shares, and any other shares that aren't in the headlines or aren't household names sometimes offer great potential but don't get the attention they deserve. The stock isn't glamorous Everyone wants to invest in the next big thing or even the current big thing. Not only do investors think they can make a fortune this way, but it's a lot more exciting to say you became a millionaire by purchasing shares of a technology start-up than by purchasing shares of an established consumer durables manufacturer. Media darlings like Microsoft, Apple and Google are more likely to be affected by herd mentality investing than conglomerates like Proctor and Gamble or Johnson and Johnson. A company announces bad news Even good companies face setbacks like litigation and recalls. However, just because a company experiences one negative event doesn't mean that the company isn't still fundamentally valuable or that its shares won't bounce back. Companies with real value can experience a significant drop in share price when something bad happens. However, investors often overreact to the magnitude of the information, opening up buying opportunities for value investors who strictly follow fundamental principles. 3

4 Those who are willing to consider the company's long-term value and ability to recover can turn these setbacks into profit opportunities. One part of the company is underperforming, but other parts are still strong Sometimes a company has an unprofitable division that drags down its performance. If the company sells or closes that division, its financials can improve dramatically. Value investors who see this potential can buy the share while its price is depressed and see gains later. The share doesn't meet analysts' expectations Analysts do not have a great track record for predicting the future, and yet investors often panic and sell when a company announces earnings that are lower than analysts' expectations. This irrational behavior can temporarily depress the share price. The share is cyclical It is common for companies to go through periods of higher and lower profits. The time of year and the overall economy affect consumers' moods and cause them to buy more or less. Their behavior might affect the share price, but it has nothing to do with the company's long term underlying value. (5 marks) 4

5 B. Learning Outcomes Assess various types of financial derivatives (including forward contracts, futures, swaps and options). Alternative 1 - Currency SWAPC is used W1. Total investment cost in LKR 1500 = 75 mn LKR 20 This will be the initial amount being transferred under SWAP agreement W2. The opportunity cost 1000 = 50 X 12% = 6 mn LKR = 25 X 6% = 1.5 mn LKR mn LKR W3. Expected Exchange rates - One year LKR 7%, APC 30% One year forward rate has been calculated based on inflation rates 1 7% %

6 LKR 5%, APC 20% 1 5% % 30 LKR 4%, APC 10% 1 4% % 27.5 W4. Money to be returned to Company back Total contract price 2,000 mn APC Deduct Interest 1000 x 10% (100) mn APC 500 x 5% (25) Less / Principle (1,500) mn APC 375 mn APC Rate APC Mn LKR Mn Less/ Opportunity Cost Net Benefit

7 Expected Value Net Benefit Probability Expected value LKR 7%, APC 30% LKR 5%, APC 20% LKR 4%, APC 10% The expected value under above scenario is 5.50 mn LKR Alternative 2 - Currency SWAPC is not used LKR 7%, APC 30% Mn Initial cost (40.00) In six month (18.00) In one year Opportunity cost (40*12%) + (18*6%) (5.88) net 1.97 LKR 5%, APC 20% Mn Initial cost (40.00) In six month (18.64) In one year Opportunity cost (40*12%)+( 18.64*6%) (5.92) net

In six month 500 mn @ 26.8292683 (18.64) In one year 2000 mn @ 28.5714286 70.")

8 LKR 4%, APC 10% Mn Initial cost (40.00) In six month (19.43) In one year Opportunity cost (40*12%)+( 19.43*6%) (5.97) net Expected Exchange rates - Six months LKR 7%, APC 30% Annual 1 3.5% % LKR 5%, APC 20% Annual 1 2.5% % 27.5 LKR 4%, APC 10% Annual 1 2% %

9 Expected Value Net Benefit Probability Expected value LKR 7%, APC 30% LKR 5%, APC 20% LKR 4%, APC 10% The expected value under above scenario is 4.88 mn LKR Conclusion The following results can be observed from the analysis. ABC enters into a currency SWAP ABC does not enter into a currency SWAP Expected value of 5.50 Mn LKR Expected value of 4.88 Mn LKR The calculations above clearly indicate that ABC will benefit by entering into a currency SWAP. (10 marks) Total 25 marks 9

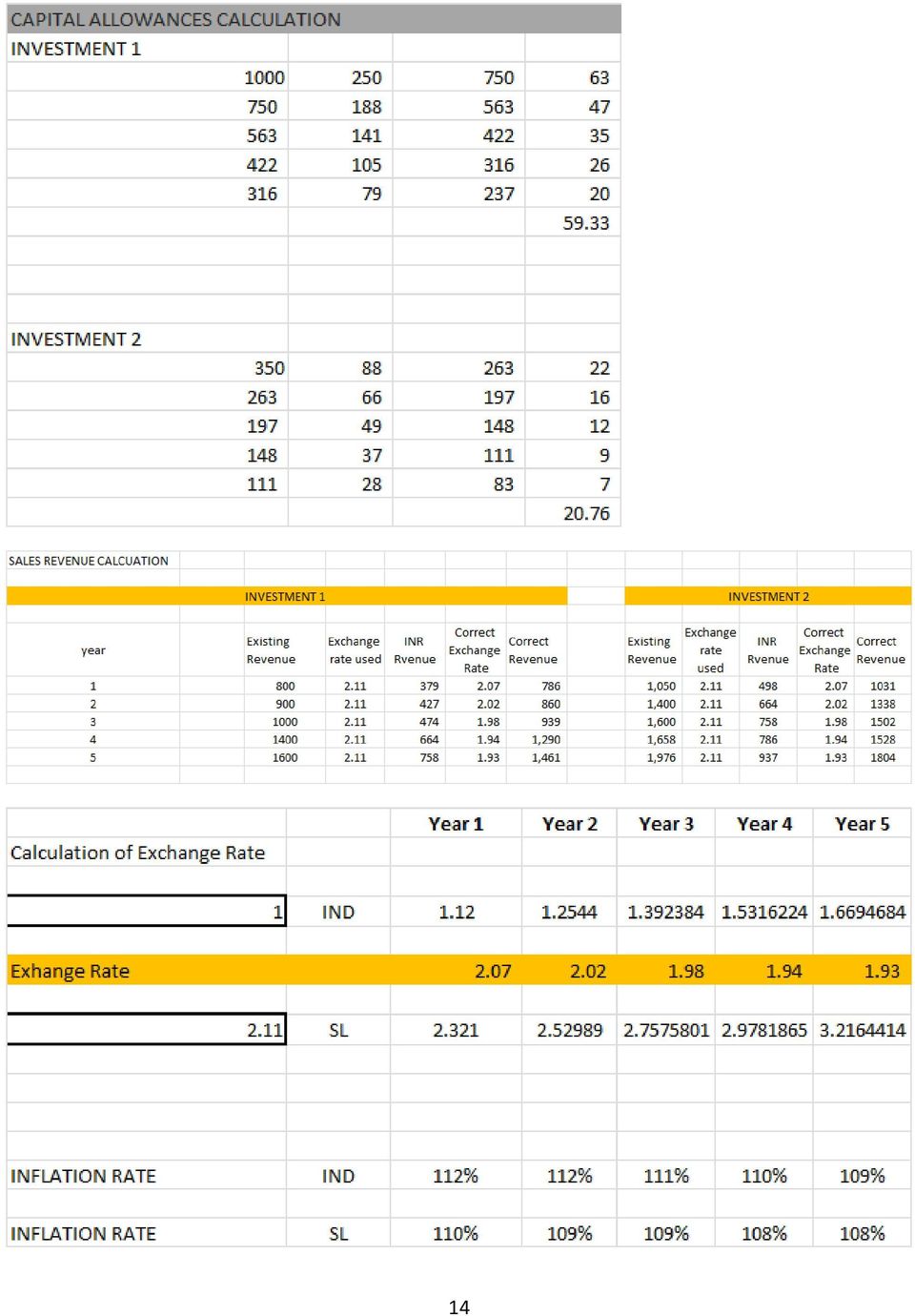

10 Question No 02 Learning Outcomes ( Part 1,2,3 & 4) Evaluate investment projects using discounting factor/non-discounting factor techniques with: - Tax - Inflation (monetary and real method) - Unequal life projects (annual equivalent method only) - Asset replacement - Capital rationing (including multi period capital rationing) - Under uncertainty (certainty equivalent, adjusting discounting factors/payback, using probability and sensitivity analysis) - Foreign investments (using forward exchange rates or country-specific Discounting factors). 10

- Unequal life projects (annual equivalent method only) - Asset replacement - Capital rationing (including multi period capital")

11 1. Three Directors are commenting on three different methods which can be used effectively in appraising projects. Note The question does not indicate for any need to show calculations to support the answer but critically evaluate various options suggested by directors in principal. It is very important for students to read and understand the questions property to avoid time being spent in answering areas which have not been requested to answer. Director A Director A prefers average profits in evaluation of projects. Average profit is a poor criterion to use in investment appraisal. Although readily understood by managers, it fails to take into account the time value of money or the incremental cash flows from the investments. Also the accounting profit would be subject many assumptions and various accounting standards used in financial accounting. There is greater possibility for accountants to go for a window dressing situation in order to show better results or later the results the way they would prefer to see.. The size of the initial outlay of the project is also ignored by this measure. Therefore a resource allocation decision should be based upon cash flows not profit, which is a reporting measure. Director B Director B prefers discounted payback in evaluation of projects. Payback is frequently used as part of investment appraisal, often being argued by management to select less risky investments from among several alternatives. Its major weakness is that it ignores cash flows after the payback period is complete. Such cash flows might be substantial and influence the investment decision where mutually exclusive investments are concerned. Discounted payback has the advantage of taking account of the time value of money, but still ignores cash flows after the discounted payback period. However, if the investment has a discounted payback period within its expected lifespan, it must have a zero or positive net present value, and be considered to be financially viable. If investments are not mutually exclusive, discounted payback will lead to the same decisions as NPV. If, as in this case, investments are mutually exclusive, an investment that does not maximise net present value could result from using discounted payback. A further 11

12 problem is that working capital cash flows are difficult to incorporate within this technique. Therefore one may argue that discounted payback method is comparatively better than the average profit from many aspects. However the discounted payback has its own disadvantages as explained before. Director C Director C has considered only guaranteed income. It indicated that Director C is a risk adverse investor. We cannot simply say that his view point is correct as the risk preference of various people is different. The relationship can be presented below. Low risk preference Lower returns ( example Treasury bills) Medium risk preference Medium returns ( average risk investments) High risk preference Higher Returns ( Ex- Invest to launch a totally new product to the market) The above table indicates a relationship between risk and return. Low risk - Lower returns High risk Higher returns Therefore if the company PQR wisher to be exposed to a greater risk or has the ability to undertake greater risk just investing in risk free investments will not give them maximum return. Therefore they should first decide on their risk preference and invest in such investment to maximize the wealth. In order to incorporate the risk element, they will have to discount each projects by an appropriate discount factor that has considered the risk element of such project and see if there is positive NPV and compare all the options before making a decision. Relationship of discounting rates Lower risk projects lower discount rate High risk projects - Higher discount rates (6 marks) 12

13 2. Payback is normally calculated using after-tax cash flows. 13

14 14

15 The discount rate should be calculated by considering inflation adjustment ( 1+8%) (1+7%) = 15.56% Investment 1 does not have the quicker discounted payback period, as it fails to pay back within its expected life. 3. (4 marks) The project 01 ends up with a negative NPV of 428mn hence should be rejected The project 2 ends up with a positive NPV of 4 mn LKR. As a rule of thumb the project 2 can be accepted due to positive NPV. However the final result depends on the accuracy of estimates made and any slightest error would lead the project to end up with a negative NPV. Therefore the margin for error for project two even is minimal and the management should access the acceptability of estimates and make a conscious decision to choose the second project, if there is no any other viable project to undertake. (10 marks) 15

16 4. Relevant non-financial factors might include: Although the financial appraisal for making an investment is a vital part of the decisionmaking process, non-financial factors can also be very important. Key non-financial factors may include: Meeting the requirements of current and future legislation Environmental factors Speed of delivery and installation of capital equipment Availability of spare parts and servicing (if required). Reliability of capital equipment. which the depreciation allowance can be set. Matching industry standards and good practice Developing the capabilities of business, such as building skills and experience in new areas or strengthening management systems The availability of suitably skilled labour Anticipating and dealing with future threats, such as protecting intellectual property against potential competition For example, a company might need to take into account the environmental impact of a potential investment. To some extent, this may be reflected in financial factors, eg the energy savings offered by new machinery. But other effects - such as the effect on company s reputation will not be considered in financial evaluations. In some cases, non-financial criteria may be essential requirements. For example,a company would not invest in new machinery that breaks health and safety regulations. (5 marks) Total 25 marks 16

. Reliability of capital equipment. which the depreciation allowance can be set.")

17 Section 2 Question (a) Learning Outcomes Analyzed financial results by using trends and ratios [including the DuPont analysis in financial statements across time/different companies/different accounting policies in appraising the short and long-term viability of the organization(working capital issues such as overtrading and solutions to overtrading is expected to be discussed here)]. Financial statement analysis- Du Pont Formulae PROFIT AND LOSS ACCOUNTS Clayhaus Tiles MIGAYA TILES FOR THE YEAR ENDED 31 MARCH Rs.'000 Rs.'000 Rs.'000 Rs.'000 Revenue 1,447,812 1,423,705 4,106,015 3,641,563 Cost of Sales -1,111,299-1,052,600-3,026,511-2,512,679 Gross Profit 336, ,105 1,079,504 1,128,884 Other Income 30,775 9,404 18, ,081 Administrative Expenses -83,624-82, , ,757 Distribution Expenses -88,212-70, , ,914 Other Expenses ,722 Net Finance Costs -68,387-43, , ,562 Profit Before Taxation 126, , , ,732 Income Tax Expenses -26,907-54,999-39, ,820 Profit After Tax 99, ,574 91, ,912 Earnings per share Dividend Per Share (Rs.) Market Value of Shares as at the year end

].")

18 Clayhaus Tiles Migaya Tiles AS AT 31 MARCH Rs 000 Rs 000 Rs 000 Rs 000 ASSETS NON CURRENT ASSETS Property, Plant & Equipment 3,272,943 3,111,383 2,971,624 2,654,682 Long term Investment 142, ,742 CURRENT ASSETS Inventories 1,350, ,358 1,919,980 1,565,072 Trade and Other Receivables 787, , , ,773 Other Investments , ,027 Cash and Cash Equivalents 127,546 50,919 35,272 47,462 2,265,493 1,490,151 3,252,956 2,654,334 TOTAL ASSETS 5,538,436 4,601,535 6,367,575 5,503,758 EQUITY AND LIABILITIES Stated Capital 156, ,000 2,289,750 2,096,250 Reserves 525, ,943 77,850 77,850 Retained Earnings 696, , , ,859 1,377,946 1,253,681 2,956,069 2,864, NON CURRENT LIABILITIES Loans and Borrowings 1,257, , , ,499 Employee Benefits 530, , , ,653 1,788,171 1,429, , ,152 CURRENT LIABILITIES Trade and Other Payables 972,588 1,206,349 1,180, ,513 Loans and Borrowings 930, , , ,895 Bank Overdraft (Secured) 469, , , ,239 2,372,319 1,918,800 2,460,819 1,754,647 TOTAL EQUITY AND LIABILITIES 5,538,436 4,601,535 6,367,575 5,503,758 18

19 Clayhaus Tiles MIGAYA TILES Return in Equity (ROE) Rs.'000 Rs.'000 Rs.'000 Rs.'000 Profit After Tax 99, ,574 91, ,912 Total Equity 1,377,946 1,253,681 2,956,069 2,864,959 ROE 7% 10% 3% 15% Decomposed ROE = 'Profit Margin x Total Assests Turnover x Equity Multiplier Profit Margin Net Income 99, ,574 91, ,912 Sales 1,447,812 1,423,705 4,106,015 3,641,563 7% 9% 2% 12% Total Assets Turover Ratio Sales Sales 1,447,812 1,423,705 4,106,015 3,641,563 Assets 5,538,436 4,601,535 6,367,575 5,503,758 26% 31% 64% 66% Equity Multiplier Assets 5,538,436 4,601,535 6,367,575 5,503,758 Total Equity 1,377,946 1,253,681 2,956,069 2,864, ROE TEST 7% 10% 3% 15% 19

20 Share Trading Information Clayhaus Tiles MIGAYA TILES Rs.'000 Rs.'000 Rs.'000 Rs.'000 Long Term Sovency Ratio (Financial Leverage Ratios) Total Debt Ratio Total Assets - Total Equity 4,160,490 3,347,854 3,411,506 2,638,799 Total Assets 5,538,436 4,601,535 6,367,575 5,503,758 Times Debt-equity Ratio Total Debt Total Equity Times Times Interest Earned EBIT 195, , , ,294 Interest 68,387 43, , , Conclusion ROE of both Companies for the recent year has been very unsatisfactory and which is even lower than the risk free rate. Therefore the management should look at the reasons for such a lower ROE. Decomposed ROE = 'Profit Margin x Total Assests Turnover x Equity Multiplier (5 marks) 20

21 (b) Learning Outcomes Analyse financial results by using trends and ratios [including the DuPont analysis in financial statements across time/different companies/different accounting policies in appraising the short and long-term viability of the organisation (working capital issues such as overtrading and solutions to overtrading is expected to be discussed here)]. Net Profit margin The net profit margin for both Companies have been very unsatisfactory. Migaya group has posted a net profit margin of just 2% for the recent where as Clayhaus is reporting it at 7%. Assets Turnover Migaya group is reporting much better assets turnover ratio of about 60% where as Clayhaus is operating at about 28% on average. Equity Multiplier Equity Multiplier is at 4 times for Clayhaue where Migaya reports it at 2 times. This means that Clayhaus is highly geared than Migaya group. In summary, the clear reason for lower ROE is the operational inefficiency displayed by both companies. The gross profit margin for both Companies operates around 26% and the drop in profitability is mainly due to higher admin, distribution and more significantly the finance costs. The Clayhaus is better in terms of finance cost compared their higher gearing and Migaya group profitability has significantly diluted to a massive fiancé cost figure. Solvency Ratio Analysis. The conclusion made above can be established by the solvency ratios as well and Clayhaus is in a critical stage in terms of gearing. However the Migaya group is in a critical stage from interest cover perspective. Therefore the senior management team should make a critical decision of their ability to improve the operational efficiency to come out of the situation and if the reason is due to industry pressure, accruing another company from the same industry creates a clear doubt. (5 marks) 21

22 2. Learning Outcomes Discuss dividend theories such as dividend irrelevancy theory, bird-in-hand theory, tax preference theory, residual theory and packing order theory. This is common question that arises around declaring dividends as opposed to investing within the business: The finance Director s concern is about the dividend policy of the company. Dividend policy is concerned with financial policies regarding paying cash dividend in the present or paying an increased dividend at a later stage. Whether to issue dividends and what amount, is determined mainly on the basis of the company's unappropriated profit (excess cash) and influenced by the company's long-term earning power. When cash surplus exists and is not needed by the firm, then management is expected to pay out some or all of those surplus earnings in the form of cash dividends. The argument of not paying dividends will lead the share price to come down may not be correct if the growth opportunities exists for the company for a return that easily exceeds the cost of capital of shareholders. If there are no NPV positive opportunities, i.e. projects where returns exceed the hurdle rate, and excess cash surplus is not needed, then finance theory suggests management should return some or all of the excess cash to shareholders as dividends. This is the general case, however there are exceptions. For example, shareholders of a "growth stock", expect that the company will, almost by definition, retain most of the excess earnings so as to fund future growth internally. By withholding current dividend payments to shareholders, managers of growth companies are hoping that dividend payments will be increased proportionality higher in the future, to offset the retainment of current earnings and the internal financing of present investment projects. Many firms choose to pay no dividends and these firms sell at positive prices. For example, most Internet firms, such as Amazon.com, Google, and ebay, pay no dividends. Rational shareholders believe that either they will receive dividends at some point or they will receive something just as good. That is, the firm will be acquired in a merger, with the stockholders receiving either cash or shares of stock at that time. Empirical evidence suggests that firms with high growth rates are likely to pay lower dividends, a result consistent with the analysis here. For example, consider McDonald s Corporation. The company started in the 1950s and grew rapidly for many years. It paid its first dividend in 1975, though it was a billion-dollar company (in both sales and market value of stockholders equity) prior to that date. Why did it wait so long to pay a dividend? It waited because it had so many positive growth opportunities (additional locations for new hamburger outlets) to take advantage of. In the Indian context also, there exist a large number of similar examples. The software giant, Infosys Limited, till a few years back, did not pay any dividends ensuring that all the earnings were reinvested for its growth 22

23 opportunities. High growth telecom companies, such as Tata Telecom and Bharti Airtel, are also examples of companies which have avoided paying dividends. 3. Learning Outcomes Calculate Weighted Average Cost of Capital (WACC). (6 marks) Cost of Capital Calculation - Dividend Valuation Model Clayhaus Tiles MIGAYA TILES Stated Capital (Rs,000) 156,000 2,289,750 Number of shares 90,000, ,850,000 Total Equity including Reserves (Rs,000) 1,377,946 2,956,069 Earnings for the year after Tax (Rs,000) 99,811 91,110 ROE 7% 3% DPS Total Dividends Paid (Rs,000) 49,500 0 Share Price Payout Ratio 20% 30% Retention Ratio ( R) 80% 70% Growth Rate (ROE X R) 6% 2% Cost of Capital Calculation R = Div1/Po+g Next Year Earnings 105,595 93,076 Payout (Rs,000) 21,119 27,923 DPS R = Div1/Po+g 8% 3% 23

24 As mentioned earlier we can see that Migaya s cost of capital figure does not seems to be correct calculated based on dividend valuation method and necessary analysis is need to see why the investors are still willing pay a higher price and make necessary adjustments accordingly. Therefore we can look at the CAPM based cost of capital as more accurate valuation which is given below. Cost of Capital Calculation - CAPM Clayhaus Tiles MIGAYA TILES Rsik Free Rate 8% 8% Rsik Premium 6.50% 6.50% Beta Factor re 14.50% 13.14% (6 marks) 24

25 4 (a) Learning Outcomes Assess systematic (market-wide/non-diversifiable) and unsystematic risk (firm specific/diversifiable) and their implications on equity financing, from a company s viewpoint (beta factor and expected return) and an investor s view point (basic fundamentals of a diversified portfolio). Mergers or acquisitions sometimes happen because business firms want diversification. This is the reason why the Director Risk and Governance was not happy about the acquisition. Because he was in the view that a diversification effect is not possible had this target being acquired. Diversification is the reduction of risk through investment decisions. If a large, conglomerate firm thinks that it has too much exposure to risk because it has too much of its business invested in one particular industry, it may buy a business in another industry. That would provide a measure of diversification for the acquiring firm. In other words, the acquiring firm no longer has all its eggs in one basket. There is a parameter to check the diversification effect and his correlation coefficient of was such in determining the same. For example if the correlation coefficient is a positive figure the two stocks are moving is the same direction when the economic changes take place and if the coefficient is negative the return of two stocks will move on the opposition direction under different market conditions. This is the simple reason why he suggested finding a target with negative correlation coefficient to achieve the diversification effect. In other words the diversification reduces the unsystematic risk of an entity. (6 marks) 25

26 4(b) Learning Outcomes Assess systematic (market-wide/non-diversifiable) and unsystematic risk (firm specific/diversifiable) and their implications on equity financing, from a company s viewpoint (beta factor and expected return) and an investor s view point (basic fundamentals of a diversified portfolio). Given below are three main reasons why an entity would go for a merger of acquisition. Economies of scale. It is often thought that larger companies have lower unit costs, because fixed costs are spread more thinly. While there are almost certainly some savings to be made, particularly where the companies concerned are in the same industry, it should be remembered that diseconomies of scale are possible. A business may become too large, or a group of businesses too diverse, to be managed effectively. It may also be difficult to bring together two companies in such a way as to obtain all potential economies of scale. Diversification and risk. A group with interests in several different businesses will be less vulnerable to fluctuations in the fortunes of one business than a company which has only one business. Acquisition of existing businesses, which can be left under their existing management so long as performance remains satisfactory, may be the best way to diversify. On the other hand, shareholders can diversify their portfolios themselves, by investing in a wide range of companies each of which has a single business. It is therefore arguable that managers should concentrate on the success of their own businesses, rather than seeking to do the shareholders work for them. Undervalued shares. If a company is really worth more than the price it can be bought at, its purchase would seem to be justified. However, a prospective purchaser should enquire carefully into the true value of the company. Its share price may be low because of justified doubts about its prospects. The reliability of information suggesting that a company is undervalued should be investigated, and one should ask why the market has not taken account of it. If it is because the information is not in the public domain, the risk of prosecution for insider dealing should not be ignored. On the other hand, if the information is public, it is possible that others have not realized its significance, and that the company is indeed undervalued. 26

27 As explained above the acquisition could go ahead even if the diversification effect is not possible but other benefits are bigger enough to compensate for the same. For example the dominance that Mogaya group can get in the tile industry would give them more benefits than the diversification effect. Which could compensate for the additional return that an investor would look for due to higher beta factor with lower diversification. Therefore the decision should not only be made based on the diversification factor. (3 marks) 27

28 5. Learning Outcomes Evaluate post-merger valuation and implications (market values, net asset values, EPS, P/E ratio before and after acquisition or merger), including post-acquisition integration, integration problems which cause merger/acquisition failure. THEORITICAL MARKET PRICE - MIGAYA PLC Clayhaus PLC Rs. '000 Existing Market Capitalization (90 mn x 13.59) 1,223,100 P/E Ratio (298,800 /37,350) = Times Existing equity earnings 99,811 Less/ Earnings from bathware division - 6,000 Net earnings 93,811 20% efficiency 18,762 New annual equity earnings 112,573 New Capitalization (P/E Based) 1,379,490 VRS - 10,000 Sale of bathware division 42,100 1,411,590 Migaya PLC Existing Market Capitalization ( mn x 14.60) 3,107,610 Property Sale 75,200 Less/Reorganization Costs - 21,000 Total Capitalization 3,161,810 The Combined Capitalization Clayhaus PLC 1,411,590 Migaya PLC 3,161,810 4,573,400 Total number of shares after new shares in Company D mn New Shares Prices (Theoretical) Migaya PLC 4,573, ,850 = Rs

29 The market price of Migaya plc and Clayhouse Tiles plc before merger are Rs and Rs respectively. Since the theoretical share price is Rs which is more than the existing market prices of both companies the merger would be beneficial. 6. (8 marks) Learning Outcomes Discuss alternative capital structures (traditional theory, Modigliani and Miller theories without and with tax). Modigliani and Miller, two professors in the 1950s, studied capital-structure theory intensely. From their analysis, they developed the capital-structure irrelevance proposition. Essentially, they hypothesized that in perfect markets, it does not matter what capital structure a company uses to finance its operations. They theorized that the market value of a firm is determined by its earning power and by the risk of its underlying assets, and that its value is independent of the way it chooses to finance its investments or distribute dividends. (Capital-Structure Irrelevance Proposition) Modigliani and Miller's Capital-Structure Irrelevance Proposition The M&M capital-structure irrelevance proposition assumes no taxes and no bankruptcy costs. In this simplified view, the weighted average cost of capital (WACC) should remain constant with changes in the company's capital structure. For example, no matter how the firm borrows, there will be no tax benefit from interest payments and thus no changes or benefits to the WACC. Additionally, since there are no changes or benefits from increases in debt, the capital structure does not influence a company's stock price, and the capital structure is therefore irrelevant to a company's stock price. Therefore the basic M&M proposition is based on the following key assumptions: No taxes No transaction costs No bankruptcy costs Equivalence in borrowing costs for both companies and investors Symmetry of market information, meaning companies and investors have the same information No effect of debt on a company's earnings before interest and taxes However, in the real world, there are taxes, transaction costs, bankruptcy costs, differences in borrowing costs, information asymmetries and effects of debt on earnings. Therefore in the real world there is a greater question to which extent these assumptions can be taken as practical. 29

30 However, as we have stated, taxes and bankruptcy costs do significantly affect a company's stock price. In additional papers, Modigliani and Miller included both the effect of taxes and bankruptcycosts. In summary, the MM I theory without corporate taxes says that a firm's relative proportions of debt and equity don't matter; MM I with corporate taxes says that the firm with the greater proportion of debt is more valuable because of the interest tax shield. (5 marks) 7. Learning Outcomes Identify different types of capital markets (stock market, bond market and money market), advantages and disadvantages of stock market listing, and main stakeholders in the capital market and their functions (including viz., Colombo Stock Exchange, Securities and Exchange Commission, issuing house, brokers,primary dealers, money brokers, Central Depositary System, underwriters). Methods of Raising Capital Issue of Shares It is the most important method. The liability of shareholders is limited to the face value of shares, and they are also easily transferable. A private company cannot invite the general public to subscribe for its share capital and its shares are also not freely transferable. But for public limited companies there are no such restrictions. There are two types of shares :- Equity shares :- the rate of dividend on these shares depends on the profits available and the discretion of directors. Hence, there is no fixed burden on the company. Each share carries one vote. Preference shares :- dividend is payable on these shares at a fixed rate and is payable only if there are profits. Hence, there is no compulsory burden on the company's finances. Such shares do not give voting rights. Issue of Debentures Companies generally have powers to borrow and raise loans by issuing debentures. The rate of interest payable on debentures is fixed at the time of issue and are recovered by a charge on the property or assets of the company, which provide the necessary security for payment. The company is liable to pay interest even if there are no profits. Debentures are mostly issued to finance the long-term requirements of business and do not carry any voting rights. 30

31 Loans from Financial Institutions Long-term and medium-term loans can be secured by companies from financial institutions. Loans from Commercial Banks Medium-term loans can be raised by companies from commercial banks against the security of properties and assets. Funds required for modernisation and renovation of assets can be borrowed from banks. This method of financing does not require any legal formality except that of creating a mortgage on the assets. Reinvestment of Profits Profitable companies do not generally distribute the whole amount of profits as dividend but, transfer certain proportion to reserves. This may be regarded as reinvestment of profits or ploughing back of profits. As these retained profits actually belong to the shareholders of the company, these are treated as a part of ownership capital. Retention of profits is a sort of self financing of business. The reserves built up over the years by ploughing back of profits may be utilised by the company for the following purposes :- Expansion of the undertaking Replacement of obsolete assets and modernisation. Meeting permanent or special working capital requirement. Redemption of old debts. To Finance Short-Term Capital, Companies can use the following Methods :- Trade Credit Companies buy raw materials, components, stores and spare parts on credit from different suppliers. Generally suppliers grant credit for a period of 3 to 6 months, and thus provide short-term finance to the company. Availability of this type of finance is connected with the volume of business. When the production and sale of goods increase, there is automatic increase in the volume of purchases, and more of trade credit is available. Factoring The amounts due to a company from customers, on account of credit sale generally remains outstanding during the period of credit allowed i.e. till the dues are collected from the debtors. The book debts may be assigned to a bank and cash realised in advance from the bank. Thus, the responsibility of collecting the debtors' balance is taken over by the bank on payment of specified charges by the company. This method of raising short-term capital is known as factoring. The bank charges payable for the purpose is treated as the cost of raising funds. 31

32 Discounting Bills of Exchange This method is widely used by companies for raising short-term finance. When the goods are sold on credit, bills of exchange are generally drawn for acceptance by the buyers of goods. Instead of holding the bills till the date of maturity, companies can discount them with commercial banks on payment of a charge known as bank discount. The rate of discount to be charged by banks is prescribed by the Reserve Bank of India from time to time. The amount of discount is deducted from the value of bills at the time of discounting. The cost of raising finance by this method is the discount charged by the bank. Bank Overdraft and Cash Credit It is a common method adopted by companies for meeting short-term financial requirements. Cash credit refers to an arrangement whereby the commercial bank allows money to be drawn as advances from time to time within a specified limit. This facility is granted against the security of goods in stock, or promissory notes bearing a second signature, or other marketable instruments like Government bonds. Overdraft is a temporary arrangement with the bank which permits the company to overdraw from its current deposit account with the bank up to a certain limit. The overdraft facility is also granted against securities. The rate of interest charged on cash credit and overdraft is relatively much higher than the rate of interest on bank deposits ( 6 marks ) (Total 50 mark) 32

Fundamentals Level Skills Module, Paper F9

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2008 Answers 1 (a) Calculation of weighted average cost of capital (WACC) Cost of equity Cost of equity using capital asset

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2008 Answers 1 (a) Calculation of weighted average cost of capital (WACC) Cost of equity Cost of equity using capital asset

Fundamentals Level Skills Module, Paper F9

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2008 Answers 1 (a) Rights issue price = 2 5 x 0 8 = $2 00 per share Theoretical ex rights price = ((2 50 x 4) + (1 x 2 00)/5=$2

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2008 Answers 1 (a) Rights issue price = 2 5 x 0 8 = $2 00 per share Theoretical ex rights price = ((2 50 x 4) + (1 x 2 00)/5=$2

Fundamentals Level Skills Module, Paper F9

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2009 Answers 1 (a) Weighted average cost of capital (WACC) calculation Cost of equity of KFP Co = 4 0 + (1 2 x (10 5 4 0)) =

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2009 Answers 1 (a) Weighted average cost of capital (WACC) calculation Cost of equity of KFP Co = 4 0 + (1 2 x (10 5 4 0)) =

Paper F9. Financial Management. Fundamentals Pilot Paper Skills module. The Association of Chartered Certified Accountants

Fundamentals Pilot Paper Skills module Financial Management Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Do NOT open this paper

Fundamentals Pilot Paper Skills module Financial Management Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Do NOT open this paper

1 (a) Calculation of net present value (NPV) Year 1 2 3 4 5 6 $000 $000 $000 $000 $000 $000 Sales revenue 1,600 1,600 1,600 1,600 1,600

Calculation of net present value (NPV) Year 1 2 3 4 5 6 $000 $000 $000 $000 $000 $000 Sales revenue 1,600 1,600 1,600 1,600 1,600") Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2011 Answers 1 (a) Calculation of net present value (NPV) Year 1 2 3 4 5 6 $000 $000 $000 $000 $000 $000 Sales revenue 1,600

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2011 Answers 1 (a) Calculation of net present value (NPV) Year 1 2 3 4 5 6 $000 $000 $000 $000 $000 $000 Sales revenue 1,600

Cash flow before tax 1,587 1,915 1,442 2,027 Tax at 28% (444) (536) (404) (568)

(536) (404) (568)") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2014 Answers 1 (a) Calculation of NPV Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 5,670 6,808 5,788 6,928 Variable

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2014 Answers 1 (a) Calculation of NPV Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 5,670 6,808 5,788 6,928 Variable

Fundamental Analysis Ratios

Fundamental Analysis Ratios Fundamental analysis ratios are used to both measure the performance of a company relative to other companies in the same market sector and to value a company. There are three

Fundamental Analysis Ratios Fundamental analysis ratios are used to both measure the performance of a company relative to other companies in the same market sector and to value a company. There are three

Institute of Chartered Accountant Ghana (ICAG) Paper 2.4 Financial Management

Paper 2.4 Financial Management") Institute of Chartered Accountant Ghana (ICAG) Paper 2.4 Financial Management Final Mock Exam 1 Marking scheme and suggested solutions DO NOT TURN THIS PAGE UNTIL YOU HAVE COMPLETED THE MOCK EXAM ii Financial

Institute of Chartered Accountant Ghana (ICAG) Paper 2.4 Financial Management Final Mock Exam 1 Marking scheme and suggested solutions DO NOT TURN THIS PAGE UNTIL YOU HAVE COMPLETED THE MOCK EXAM ii Financial

CFS. Syllabus. Certified Finance Specialist. International benchmark in Finance profession

CFS Certified Finance Specialist Syllabus International benchmark in Finance profession Certified Finance Specialist Summary: This award will provide candidates the opportunity to gain advanced level knowledge

CFS Certified Finance Specialist Syllabus International benchmark in Finance profession Certified Finance Specialist Summary: This award will provide candidates the opportunity to gain advanced level knowledge

Paper F9. Financial Management. Specimen Exam applicable from December 2014. Fundamentals Level Skills Module

Fundamentals Level Skills Module Financial Management Specimen Exam applicable from December 2014 Time allowed Reading and planning: 15 minutes Writing: 3 hours This paper is divided into two sections:

Fundamentals Level Skills Module Financial Management Specimen Exam applicable from December 2014 Time allowed Reading and planning: 15 minutes Writing: 3 hours This paper is divided into two sections:

Indicative Content. 1.1.1 The main types of corporate form. 1.1.2 The regulatory framework for companies. 1.1.6 Shareholder Value Analysis.

Unit Title: Corporate Finance Unit Reference Number: L/601/3900 Guided Learning Hours: 210 Level: Level 6 Number of Credits: 25 Learning Outcome 1 The learner will: Understand the role of the Corporate

Unit Title: Corporate Finance Unit Reference Number: L/601/3900 Guided Learning Hours: 210 Level: Level 6 Number of Credits: 25 Learning Outcome 1 The learner will: Understand the role of the Corporate

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION OCTOBER 2006 Table of Contents 1. INTRODUCTION... 3 2. FINANCIAL RATIOS FOR COMPANIES (INDUSTRY - COMMERCE - SERVICES) 4 2.1 Profitability Ratios...4 2.2 Viability

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION OCTOBER 2006 Table of Contents 1. INTRODUCTION... 3 2. FINANCIAL RATIOS FOR COMPANIES (INDUSTRY - COMMERCE - SERVICES) 4 2.1 Profitability Ratios...4 2.2 Viability

How To Understand The Financial System

E. BUSINESS FINANCE 1. Sources of, and raising short-term finance 2. Sources of, and raising long-term finance 3. Internal sources of finance and dividend policy 4. Gearing and capital structure considerations

E. BUSINESS FINANCE 1. Sources of, and raising short-term finance 2. Sources of, and raising long-term finance 3. Internal sources of finance and dividend policy 4. Gearing and capital structure considerations

for Analysing Listed Private Equity Companies

8 Steps for Analysing Listed Private Equity Companies Important Notice This document is for information only and does not constitute a recommendation or solicitation to subscribe or purchase any products.

8 Steps for Analysing Listed Private Equity Companies Important Notice This document is for information only and does not constitute a recommendation or solicitation to subscribe or purchase any products.

Question 1. Marking scheme. F9 ACCA June 2013 Exam: BPP Answers

Question 1 Text references. NPV is covered in Chapter 8 and real or nominal terms in Chapter 9. Financial objectives are covered in Chapter 1. Top tips. Part (b) requires you to explain the different approaches.

Question 1 Text references. NPV is covered in Chapter 8 and real or nominal terms in Chapter 9. Financial objectives are covered in Chapter 1. Top tips. Part (b) requires you to explain the different approaches.

Fundamentals Level Skills Module, Paper F9. Section A. Monetary value of return = $3 10 x 1 197 = $3 71 Current share price = $3 71 $0 21 = $3 50

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2014 Answers Section A 1 A Monetary value of return = $3 10 x 1 197 = $3 71 Current share price = $3 71 $0 21 = $3 50 2

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2014 Answers Section A 1 A Monetary value of return = $3 10 x 1 197 = $3 71 Current share price = $3 71 $0 21 = $3 50 2

Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.)

") Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.) The primary focus of the next two chapters will be to examine the debt/equity choice by firms. In particular,

Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.) The primary focus of the next two chapters will be to examine the debt/equity choice by firms. In particular,

Diploma in Financial Management Examination Module B Paper DB1 incorporating subject areas: Financial Strategy; Risk Management

Answers Diploma in Financial Management Examination Module B Paper DB1 incorporating subject areas: Financial Strategy; Risk Management June 2005 Answers 1 D Items 2, 3 and 4 are correct. Item 1 relates

Answers Diploma in Financial Management Examination Module B Paper DB1 incorporating subject areas: Financial Strategy; Risk Management June 2005 Answers 1 D Items 2, 3 and 4 are correct. Item 1 relates

How To Calculate Financial Leverage Ratio

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

1 (a) Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084 6,327 6,580 6,844

Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084 6,327 6,580 6,844") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2013 Answers 1 (a) Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2013 Answers 1 (a) Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084

Financial Decision Making Sample paper

Financial Decision Making Sample paper s Important notice When reading these answers, please note that they are not intended to be viewed as a definitive model answer, as in many instances there are several

Financial Decision Making Sample paper s Important notice When reading these answers, please note that they are not intended to be viewed as a definitive model answer, as in many instances there are several

Chapter 1 The Scope of Corporate Finance

Chapter 1 The Scope of Corporate Finance MULTIPLE CHOICE 1. One of the tasks for financial managers when identifying projects that increase firm value is to identify those projects where a. marginal benefits

Chapter 1 The Scope of Corporate Finance MULTIPLE CHOICE 1. One of the tasks for financial managers when identifying projects that increase firm value is to identify those projects where a. marginal benefits

Practice Bulletin No. 2

Practice Bulletin No. 2 INTERNATIONAL GLOSSARY OF BUSINESS VALUATION TERMS To enhance and sustain the quality of business valuations for the benefit of the profession and its clientele, the below identified

Practice Bulletin No. 2 INTERNATIONAL GLOSSARY OF BUSINESS VALUATION TERMS To enhance and sustain the quality of business valuations for the benefit of the profession and its clientele, the below identified

Contribution 787 1,368 1,813 983. Taxable cash flow 682 1,253 1,688 858 Tax liabilities (205) (376) (506) (257)

(376) (506) (257)") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2012 Answers 1 (a) Calculation of net present value (NPV) As nominal after-tax cash flows are to be discounted, the nominal

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2012 Answers 1 (a) Calculation of net present value (NPV) As nominal after-tax cash flows are to be discounted, the nominal

Selecting sources of finance for business

Selecting sources of finance for business by Steve Jay 08 Sep 2003 This article considers the practical issues facing a business when selecting appropriate sources of finance. It does not consider the

Selecting sources of finance for business by Steve Jay 08 Sep 2003 This article considers the practical issues facing a business when selecting appropriate sources of finance. It does not consider the

Chapters 3 and 13 Financial Statement and Cash Flow Analysis

Chapters 3 and 13 Financial Statement and Cash Flow Analysis Balance Sheet Assets Cash Inventory Accounts Receivable Property Plant Equipment Total Assets Liabilities and Shareholder s Equity Accounts

Chapters 3 and 13 Financial Statement and Cash Flow Analysis Balance Sheet Assets Cash Inventory Accounts Receivable Property Plant Equipment Total Assets Liabilities and Shareholder s Equity Accounts

Equity Analysis and Capital Structure. A New Venture s Perspective

Equity Analysis and Capital Structure A New Venture s Perspective 1 Venture s Capital Structure ASSETS Short- term Assets Cash A/R Inventories Long- term Assets Plant and Equipment Intellectual Property

Equity Analysis and Capital Structure A New Venture s Perspective 1 Venture s Capital Structure ASSETS Short- term Assets Cash A/R Inventories Long- term Assets Plant and Equipment Intellectual Property

Financial Management

Different forms business organization Financial Management Sole proprietorship Partnership Cooperative society Company Private limited Vs Public limited company Private co min- two and max fifty, Pub Ltd

Different forms business organization Financial Management Sole proprietorship Partnership Cooperative society Company Private limited Vs Public limited company Private co min- two and max fifty, Pub Ltd

SOLUTIONS. Practice questions. Multiple Choice

Practice questions Multiple Choice 1. XYZ has $25,000 of debt outstanding and a book value of equity of $25,000. The company has 10,000 shares outstanding and a stock price of $10. If the unlevered beta

Practice questions Multiple Choice 1. XYZ has $25,000 of debt outstanding and a book value of equity of $25,000. The company has 10,000 shares outstanding and a stock price of $10. If the unlevered beta

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows

7 Statement of Cash Flows") Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Examiner s report F9 Financial Management June 2013

Examiner s report F9 Financial Management June 2013 General Comments The examination consisted of four compulsory questions, each worth 25 marks. Most candidates attempted all four questions and there

Examiner s report F9 Financial Management June 2013 General Comments The examination consisted of four compulsory questions, each worth 25 marks. Most candidates attempted all four questions and there

Chapter 17: Financial Statement Analysis

FIN 301 Class Notes Chapter 17: Financial Statement Analysis INTRODUCTION Financial ratio: is a relationship between different accounting items that tells something about the firm s activities. Purpose

FIN 301 Class Notes Chapter 17: Financial Statement Analysis INTRODUCTION Financial ratio: is a relationship between different accounting items that tells something about the firm s activities. Purpose

Net revenue 785 25 1,721 05 5,038 54 3,340 65 Tax payable (235 58) (516 32) (1,511 56) (1,002 20)

(516 32) (1,511 56) (1,002 20)") Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2013 Answers 1 (a) Calculating the net present value of the investment project using a nominal terms approach requires the

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2013 Answers 1 (a) Calculating the net present value of the investment project using a nominal terms approach requires the

International Glossary of Business Valuation Terms*

40 Statement on Standards for Valuation Services No. 1 APPENDIX B International Glossary of Business Valuation Terms* To enhance and sustain the quality of business valuations for the benefit of the profession

40 Statement on Standards for Valuation Services No. 1 APPENDIX B International Glossary of Business Valuation Terms* To enhance and sustain the quality of business valuations for the benefit of the profession

Using the FRR to rate Project Business Success

Using the FRR to rate Project Business Success The purpose of this note is to explain the calculation of the financial rate of return (FRR), with a view, firstly to clarify the FRR concept and its determination,

Using the FRR to rate Project Business Success The purpose of this note is to explain the calculation of the financial rate of return (FRR), with a view, firstly to clarify the FRR concept and its determination,

Financial ratio analysis

Financial ratio analysis A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction 2. Liquidity ratios 3. Profitability ratios and activity ratios 4. Financial leverage ratios 5. Shareholder

Financial ratio analysis A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction 2. Liquidity ratios 3. Profitability ratios and activity ratios 4. Financial leverage ratios 5. Shareholder

MGT201 Solved MCQs(500) By

By") MGT201 Solved MCQs(500) By http://www.vustudents.net Why companies invest in projects with negative NPV? Because there is hidden value in each project Because there may be chance of rapid growth Because

MGT201 Solved MCQs(500) By http://www.vustudents.net Why companies invest in projects with negative NPV? Because there is hidden value in each project Because there may be chance of rapid growth Because

6. Debt Valuation and the Cost of Capital

6. Debt Valuation and the Cost of Capital Introduction Firms rarely finance capital projects by equity alone. They utilise long and short term funds from a variety of sources at a variety of costs. No

6. Debt Valuation and the Cost of Capital Introduction Firms rarely finance capital projects by equity alone. They utilise long and short term funds from a variety of sources at a variety of costs. No

There are two types of returns that an investor can expect to earn from an investment.

Benefits of investing in the Stock Market There are many benefits to investing in shares and we will explore how this common form of investment can be an effective way to make money. We will discuss some

Benefits of investing in the Stock Market There are many benefits to investing in shares and we will explore how this common form of investment can be an effective way to make money. We will discuss some

Business Finance. Theory and Practica. Eddie McLaney PEARSON

Business Finance Theory and Practica Eddie McLaney PEARSON Harlow, England London New York Boston San Francisco Toronto Sydney Auckland Singapore Hong Kong Tokyo Seoul Taipei New Delhi Cape Town Säo Paulo

Business Finance Theory and Practica Eddie McLaney PEARSON Harlow, England London New York Boston San Francisco Toronto Sydney Auckland Singapore Hong Kong Tokyo Seoul Taipei New Delhi Cape Town Säo Paulo

Financial statements aim at providing financial

Accounting Ratios 5 LEARNING OBJECTIVES After studying this chapter, you will be able to : explain the meaning, objectives and limitations of accounting ratios; identify the various types of ratios commonly

Accounting Ratios 5 LEARNING OBJECTIVES After studying this chapter, you will be able to : explain the meaning, objectives and limitations of accounting ratios; identify the various types of ratios commonly

Part 9. The Basics of Corporate Finance

Part 9. The Basics of Corporate Finance The essence of business is to raise money from investors to fund projects that will return more money to the investors. To do this, there are three financial questions

Part 9. The Basics of Corporate Finance The essence of business is to raise money from investors to fund projects that will return more money to the investors. To do this, there are three financial questions

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions Chapter 3 Interpreting Financial Ratios Concept Check 3.1 1. What are the different motivations that

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions Chapter 3 Interpreting Financial Ratios Concept Check 3.1 1. What are the different motivations that

Module 1: Corporate Finance and the Role of Venture Capital Financing TABLE OF CONTENTS

1.0 FINANCING PRINCIPLES Module 1: Corporate Finance and the Role of Venture Capital Financing Financing Principles 1.01 Introduction to Financing Principles 1.02 Capitalization of a Business 1.03 Capital

1.0 FINANCING PRINCIPLES Module 1: Corporate Finance and the Role of Venture Capital Financing Financing Principles 1.01 Introduction to Financing Principles 1.02 Capitalization of a Business 1.03 Capital

Interpretation of Financial Statements

Interpretation of Financial Statements Author Noel O Brien, Formation 2 Accounting Framework Examiner. An important component of most introductory financial accounting programmes is the analysis and interpretation

Interpretation of Financial Statements Author Noel O Brien, Formation 2 Accounting Framework Examiner. An important component of most introductory financial accounting programmes is the analysis and interpretation

performance of a company?

How to deal with questions on assessing the performance of a company? (Relevant to ATE Paper 7 Advanced Accounting) Dr. M H Ho This article provides guidance for candidates in dealing with examination

How to deal with questions on assessing the performance of a company? (Relevant to ATE Paper 7 Advanced Accounting) Dr. M H Ho This article provides guidance for candidates in dealing with examination

INVESTMENT DICTIONARY

INVESTMENT DICTIONARY Annual Report An annual report is a document that offers information about the company s activities and operations and contains financial details, cash flow statement, profit and

INVESTMENT DICTIONARY Annual Report An annual report is a document that offers information about the company s activities and operations and contains financial details, cash flow statement, profit and

Paper F9. Financial Management. Friday 6 June 2014. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants.

Fundamentals Level Skills Module Financial Management Friday 6 June 2014 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Fundamentals Level Skills Module Financial Management Friday 6 June 2014 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Capital budgeting & risk

Capital budgeting & risk A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction 2. Measurement of project risk 3. Incorporating risk in the capital budgeting decision 4. Assessment of

Capital budgeting & risk A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction 2. Measurement of project risk 3. Incorporating risk in the capital budgeting decision 4. Assessment of

CHAPTER 20 LONG TERM FINANCE: SHARES, DEBENTURES AND TERM LOANS

CHAPTER 20 LONG TERM FINANCE: SHARES, DEBENTURES AND TERM LOANS Q.1 What is an ordinary share? How does it differ from a preference share and debenture? Explain its most important features. A.1 Ordinary

CHAPTER 20 LONG TERM FINANCE: SHARES, DEBENTURES AND TERM LOANS Q.1 What is an ordinary share? How does it differ from a preference share and debenture? Explain its most important features. A.1 Ordinary

Fundamentals Level Skills Module, Paper F9. Section B

Answers Fundamentals Level Skills Module, Paper F9 Financial Management September/December 2015 Answers Section B 1 (a) Market value of equity = 15,000,000 x 3 75 = $56,250,000 Market value of each irredeemable

Answers Fundamentals Level Skills Module, Paper F9 Financial Management September/December 2015 Answers Section B 1 (a) Market value of equity = 15,000,000 x 3 75 = $56,250,000 Market value of each irredeemable

TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II + III

SOLUTIONS RE-EXAMS 2014 II + III") TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II III Instructions 1. Only one problem should be treated on each sheet of paper and only one side of the sheet should be used. 2. The solutions folder

TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II III Instructions 1. Only one problem should be treated on each sheet of paper and only one side of the sheet should be used. 2. The solutions folder

Sri Lanka Accounting Standard-LKAS 7. Statement of Cash Flows

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

INSTITUTE OF ACTUARIES OF INDIA. CT2 Finance and Financial Reporting MAY 2009 EXAMINATION INDICATIVE SOLUTION

INSTITUTE OF ACTUARIES OF INDIA CT2 Finance and Financial Reporting MAY 2009 EXAMINATION INDICATIVE SOLUTION General guidelines to markers: The solutions provided here are indicative ones. Please award

INSTITUTE OF ACTUARIES OF INDIA CT2 Finance and Financial Reporting MAY 2009 EXAMINATION INDICATIVE SOLUTION General guidelines to markers: The solutions provided here are indicative ones. Please award

MCQ on Financial Management

MCQ on Financial Management 1. "Shareholder wealth" in a firm is represented by: a) the number of people employed in the firm. b) the book value of the firm's assets less the book value of its liabilities

MCQ on Financial Management 1. "Shareholder wealth" in a firm is represented by: a) the number of people employed in the firm. b) the book value of the firm's assets less the book value of its liabilities

Advanced Financial Management

Progress Test 2 Advanced Financial Management P4AFM-PT2-Z14-A Answers & Marking Scheme 2014 DeVry/Becker Educational Development Corp. Tutorial note: the answers below are more comprehensive than would

Progress Test 2 Advanced Financial Management P4AFM-PT2-Z14-A Answers & Marking Scheme 2014 DeVry/Becker Educational Development Corp. Tutorial note: the answers below are more comprehensive than would

Leverage. FINANCE 350 Global Financial Management. Professor Alon Brav Fuqua School of Business Duke University. Overview

Leverage FINANCE 35 Global Financial Management Professor Alon Brav Fuqua School of Business Duke University Overview Capital Structure does not matter! Modigliani & Miller propositions Implications for

Leverage FINANCE 35 Global Financial Management Professor Alon Brav Fuqua School of Business Duke University Overview Capital Structure does not matter! Modigliani & Miller propositions Implications for

Copyright 2009 Pearson Education Canada

The consequence of failing to adjust the discount rate for the risk implicit in projects is that the firm will accept high-risk projects, which usually have higher IRR due to their high-risk nature, and

The consequence of failing to adjust the discount rate for the risk implicit in projects is that the firm will accept high-risk projects, which usually have higher IRR due to their high-risk nature, and

Construction Economics & Finance. Module 6. Lecture-1

Construction Economics & Finance Module 6 Lecture-1 Financial management: Financial management involves planning, allocation and control of financial resources of a company. Financial management is essential

Construction Economics & Finance Module 6 Lecture-1 Financial management: Financial management involves planning, allocation and control of financial resources of a company. Financial management is essential

Chapter 7. . 1. component of the convertible can be estimated as 1100-796.15 = 303.85.

Chapter 7 7-1 Income bonds do share some characteristics with preferred stock. The primary difference is that interest paid on income bonds is tax deductible while preferred dividends are not. Income bondholders

Chapter 7 7-1 Income bonds do share some characteristics with preferred stock. The primary difference is that interest paid on income bonds is tax deductible while preferred dividends are not. Income bondholders

CIS September 2013 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Level 2

CIS September 2013 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Level 2 SECTION A: MULTIPLE CHOICE QUESTIONS Corporate Finance (1

CIS September 2013 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Level 2 SECTION A: MULTIPLE CHOICE QUESTIONS Corporate Finance (1

NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

BetaShares Geared U.S. Equity Fund - Currency Hedged (hedge fund) ASX code: GGUS

ASX code: GGUS") BetaShares Geared U.S. Equity Fund - Currency Hedged (hedge fund) ASX code: GGUS ARSN 602 666 615 Annual Financial Report for the period 10 November 2014 to 30 June 2015 BetaShares Geared U.S. Equity Fund

BetaShares Geared U.S. Equity Fund - Currency Hedged (hedge fund) ASX code: GGUS ARSN 602 666 615 Annual Financial Report for the period 10 November 2014 to 30 June 2015 BetaShares Geared U.S. Equity Fund

TYPES OF FINANCIAL RATIOS

TYPES OF FINANCIAL RATIOS In the previous articles we discussed how to invest in the stock market and unit trusts. When investing in the stock market an investor should have a clear understanding about

TYPES OF FINANCIAL RATIOS In the previous articles we discussed how to invest in the stock market and unit trusts. When investing in the stock market an investor should have a clear understanding about

Actuarial Society of India

Actuarial Society of India EXAMINATIONS November 2004 SUBJECT - 108: Finance and Financial Reporting Indicative Solution S-108 Page 1 of 7 1 D 2 C 3 B 4 D 5 D 6 A 7 B 8 C 9 B 10 D 11 Trade credit is short-term

Actuarial Society of India EXAMINATIONS November 2004 SUBJECT - 108: Finance and Financial Reporting Indicative Solution S-108 Page 1 of 7 1 D 2 C 3 B 4 D 5 D 6 A 7 B 8 C 9 B 10 D 11 Trade credit is short-term

How To Understand The Financial Philosophy Of A Firm

1. is concerned with the acquisition, financing, and management of assets with some overall goal in mind. A. Financial management B. Profit maximization C. Agency theory D. Social responsibility 2. Jensen

1. is concerned with the acquisition, financing, and management of assets with some overall goal in mind. A. Financial management B. Profit maximization C. Agency theory D. Social responsibility 2. Jensen

Source of Finance and their Relative Costs F. COST OF CAPITAL

F. COST OF CAPITAL 1. Source of Finance and their Relative Costs 2. Estimating the Cost of Equity 3. Estimating the Cost of Debt and Other Capital Instruments 4. Estimating the Overall Cost of Capital

F. COST OF CAPITAL 1. Source of Finance and their Relative Costs 2. Estimating the Cost of Equity 3. Estimating the Cost of Debt and Other Capital Instruments 4. Estimating the Overall Cost of Capital

Overview of Financial Management

Overview of Financial Management Uwadiae Oduware FCA Akintola Williams Deloitte 1-1 Definition Financial Management entails planning for the future for a person or a business enterprise to ensure a positive

Overview of Financial Management Uwadiae Oduware FCA Akintola Williams Deloitte 1-1 Definition Financial Management entails planning for the future for a person or a business enterprise to ensure a positive

Transition to International Financial Reporting Standards

Transition to International Financial Reporting Standards Topps Tiles Plc In accordance with IFRS 1, First-time adoption of International Financial Reporting Standards ( IFRS ), Topps Tiles Plc, ( Topps

Transition to International Financial Reporting Standards Topps Tiles Plc In accordance with IFRS 1, First-time adoption of International Financial Reporting Standards ( IFRS ), Topps Tiles Plc, ( Topps

1 (a) NPV calculation Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales revenue 5,614 7,214 9,015 7,034. Contribution 2,583 3,283 3,880 2,860

NPV calculation Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales revenue 5,614 7,214 9,015 7,034. Contribution 2,583 3,283 3,880 2,860") Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2012 Answers 1 (a) NPV calculation Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales revenue 5,614 7,214 9,015 7,034 Variable

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2012 Answers 1 (a) NPV calculation Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales revenue 5,614 7,214 9,015 7,034 Variable

DUKE UNIVERSITY Fuqua School of Business. FINANCE 351 - CORPORATE FINANCE Problem Set #7 Prof. Simon Gervais Fall 2011 Term 2.

DUKE UNIVERSITY Fuqua School of Business FINANCE 351 - CORPORATE FINANCE Problem Set #7 Prof. Simon Gervais Fall 2011 Term 2 Questions 1. Suppose the corporate tax rate is 40%, and investors pay a tax

DUKE UNIVERSITY Fuqua School of Business FINANCE 351 - CORPORATE FINANCE Problem Set #7 Prof. Simon Gervais Fall 2011 Term 2 Questions 1. Suppose the corporate tax rate is 40%, and investors pay a tax

CIMA Strategic Level F3 FINANCIAL STRATEGY (REVISION SUMMARIES)

") CIMA Strategic Level F3 FINANCIAL STRATEGY (REVISION SUMMARIES) Chapter Title Page number 1 Introduction to financial strategy 3 2 Analysing performance 7 3 Planning and forecasting 11 4 Long term finance

CIMA Strategic Level F3 FINANCIAL STRATEGY (REVISION SUMMARIES) Chapter Title Page number 1 Introduction to financial strategy 3 2 Analysing performance 7 3 Planning and forecasting 11 4 Long term finance

Bond Valuation. What is a bond?

Lecture: III 1 What is a bond? Bond Valuation When a corporation wishes to borrow money from the public on a long-term basis, it usually does so by issuing or selling debt securities called bonds. A bond

Lecture: III 1 What is a bond? Bond Valuation When a corporation wishes to borrow money from the public on a long-term basis, it usually does so by issuing or selling debt securities called bonds. A bond

THE STOCK MARKET GAME GLOSSARY

THE STOCK MARKET GAME GLOSSARY Accounting: A method of recording a company s financial activity and arranging the information in reports that make the information understandable. Accounts payable: The

THE STOCK MARKET GAME GLOSSARY Accounting: A method of recording a company s financial activity and arranging the information in reports that make the information understandable. Accounts payable: The

Chapter 7: Capital Structure: An Overview of the Financing Decision

Chapter 7: Capital Structure: An Overview of the Financing Decision 1. Income bonds are similar to preferred stock in several ways. Payment of interest on income bonds depends on the availability of sufficient

Chapter 7: Capital Structure: An Overview of the Financing Decision 1. Income bonds are similar to preferred stock in several ways. Payment of interest on income bonds depends on the availability of sufficient

CHAPTER 15 Capital Structure: Basic Concepts

Multiple Choice Questions: CHAPTER 15 Capital Structure: Basic Concepts I. DEFINITIONS HOMEMADE LEVERAGE a 1. The use of personal borrowing to change the overall amount of financial leverage to which an

Multiple Choice Questions: CHAPTER 15 Capital Structure: Basic Concepts I. DEFINITIONS HOMEMADE LEVERAGE a 1. The use of personal borrowing to change the overall amount of financial leverage to which an

Monika Goel Online Classes FINANCIAL, TREASURY AND FOREX MANAGEMENT Module II (C.S Professional Course)

") Monika Goel Online Classes FINANCIAL, TREASURY AND FOREX MANAGEMENT Module II (C.S Professional Course) Session Plan Day Date Time Topics- to be covered 14 h July, Nature and Scope of Financial Management

Monika Goel Online Classes FINANCIAL, TREASURY AND FOREX MANAGEMENT Module II (C.S Professional Course) Session Plan Day Date Time Topics- to be covered 14 h July, Nature and Scope of Financial Management

9901_1. A. 74.19 days B. 151.21 days C. 138.46 days D. 121.07 days E. 84.76 days

1. A stakeholder is: 9901_1 Student: A. a creditor to whom a firm currently owes money. B. any person who has voting rights based on stock ownership of a corporation. C. any person or entity other than

1. A stakeholder is: 9901_1 Student: A. a creditor to whom a firm currently owes money. B. any person who has voting rights based on stock ownership of a corporation. C. any person or entity other than

Achievement of Market-Friendly Initiatives and Results Program (AMIR 2.0 Program) Funded by U.S. Agency for International Development

Funded by U.S. Agency for International Development") Achievement of Market-Friendly Initiatives and Results Program (AMIR 2.0 Program) Funded by U.S. Agency for International Development Equity Analysis, Portfolio Management, and Real Estate Practice Quizzes

Achievement of Market-Friendly Initiatives and Results Program (AMIR 2.0 Program) Funded by U.S. Agency for International Development Equity Analysis, Portfolio Management, and Real Estate Practice Quizzes

You have learnt about the financial statements

Analysis of Financial Statements 4 You have learnt about the financial statements (Income Statement and Balance Sheet) of companies. Basically, these are summarised financial reports which provide the

Analysis of Financial Statements 4 You have learnt about the financial statements (Income Statement and Balance Sheet) of companies. Basically, these are summarised financial reports which provide the

Test3. Pessimistic Most Likely Optimistic Total Revenues 30 50 65 Total Costs -25-20 -15

Test3 1. The market value of Charcoal Corporation's common stock is $20 million, and the market value of its riskfree debt is $5 million. The beta of the company's common stock is 1.25, and the market

Test3 1. The market value of Charcoal Corporation's common stock is $20 million, and the market value of its riskfree debt is $5 million. The beta of the company's common stock is 1.25, and the market

STUDENT CAN HAVE ONE LETTER SIZE FORMULA SHEET PREPARED BY STUDENT HIM/HERSELF. FINANCIAL CALCULATOR/TI-83 OR THEIR EQUIVALENCES ARE ALLOWED.

Test III-FINN3120-090 Fall 2009 (2.5 PTS PER QUESTION. MAX 100 PTS) Type A Name ID PRINT YOUR NAME AND ID ON THE TEST, ANSWER SHEET AND FORMULA SHEET. TURN IN THE TEST, OPSCAN ANSWER SHEET AND FORMULA

Test III-FINN3120-090 Fall 2009 (2.5 PTS PER QUESTION. MAX 100 PTS) Type A Name ID PRINT YOUR NAME AND ID ON THE TEST, ANSWER SHEET AND FORMULA SHEET. TURN IN THE TEST, OPSCAN ANSWER SHEET AND FORMULA

Business Studies - Financial Planning and Management Study Notes. Financial Planning and Management Study Notes:

Business Studies - Financial Planning and Management Study Notes Financial Planning and Management Study Notes: The Role of Financial Planning: The strategic role of financial management: Organisational

Business Studies - Financial Planning and Management Study Notes Financial Planning and Management Study Notes: The Role of Financial Planning: The strategic role of financial management: Organisational