FINANCIAL INSTRUCTIONAL BOOKLET ALPHA DELTA KAPPA

|

|

|

- Antonia Pearson

- 10 years ago

- Views:

Transcription

1 FINANCIAL INSTRUCTIONAL BOOKLET ALPHA DELTA KAPPA Revised September 2012

2 Overview FINANCIAL INSTRUCTIONAL BOOKLET TABLE OF CONTENTS I. Internal Revenue Service Exempt Reporting Requirements...1 A. ADK s Reporting Requirements...1 B. State and Chapter Organizations Reporting Requirements...2 (ALSO SEE PAGES FOR 990-N e-postcard INSTRUCTIONS) C. Chapters Reporting Requirements...4 Example of Form 990 EZ Example of Form 990-T II. Alpha Delta Kappa Foundation s Program Efforts...13 A. A K S/P/N Altruistic Fund...13 B. IRS Requirements for Disbanding Chapters...13 III. Organizational Structure...14 A. State Responsibilities...14 B. Reporting Period (Fiscal Year)...14 C. Group Authorization...14 D. Employer/Taxpayer Identification Number (EIN/TIN)...14 E. Bank Accounts and Related Bank Statements...15 IV. States Annual Reporting Requirements to International...15 A. Cash Flow Statement...15 B. Balance Sheet...15 C. Three-Year Gross Receipts Calculation...15 V. State Accounting Reports...15 A. Cash Flow Statement...16 B. Balance Sheet...16 C. Budget...16 VI. Supplementary Materials A. Sample Cash Flow Statement and Notes of Explanation (Report S-1)...18 B. Sample Balance Sheet (Report S-2)...22 C. Sample Three-Year Gross Receipts Calculation and Calculation Procedures (Report S-3)...23 D. Sample Budget (Report S-4)...25 E. IRS Filing Requirements Summary and Determination of Unrelated Business Income, If Any...26 F. Suggested Monthly Planner for State Treasurer...29 G. Suggestions for Setting Up the Treasurers Files...33

...14 C. Group Authorization...14 D. Employer/Taxpayer Identification Number (EIN/TIN)...14 E.")

3 V. Guidelines for State Treasurers A. Guidelines for State Treasurers in Working with Districts, Area Councils, and Chapters on Financial Reporting...34 B. Notes on IRS Forms 990, 990-EZ and 990-T...35 C. Chapter C-1 Tracking Summary...36 D. Sample Single Event Reporting Form for Districts/Area Councils (Report D-1 EZ)...37 E. Sample District/Area Council Annual Cash Flow Statement (Report D-1)...38 VI. Guidelines for Chapter Treasurers A. Guidelines for Chapter Treasurers...39 B. Sample Annual Chapter Reporting Form and Audit (Report C-1)...40 D. Sample Balance Sheet (Report C-2)...41 E. Sample Three-Year Gross Receipts Calculation (Report C-3)...42 C. Sample Budget (Report C-4)...43 VII. VIII. Financial Reporting Information...44 State and Chapter Record Retention Requirements...45 IX. YOU MUST REPORT ANNUALLY TO THE IRS...46 Acknowledgment: Special thanks to Helen Hess, Oregon Rho and Carol Williams, Virginia Delta, for their valuable contributions to this project.

...40 D. Sample Balance Sheet (Report C-2)...41 E. Sample Three-Year Gross Receipts Calculation (Report C-3)...42 C.")

4 OVERVIEW The Executive Board of Alpha Delta Kappa ( A K ) voted to provide instruction and guidance to assist with more accurately collecting and recording financial information. This determination was made after reviewing the results of the State Financial Update Survey received in the summer of The Executive Board believes one of the desired benefits of this educational effort is to ease the burdens of the state/provincial/national treasurer by providing templates for reporting and other helpful organizing information. Another desired benefit is to obtain greater consistency in the organizing and recording of financial information by U.S. states and chapters who must remain compliant with IRS requirements. This educational booklet has been written as a resource to help contribute in achieving these goals. This resource booklet is meant to serve as a how to book regarding the financial matters of your state. It is the first of its kind, and will be revised as feedback is received from state treasurers or other state officers. Therefore, we welcome your questions and comments. Please feel free to contact Headquarters' Executive Administrator if you need an answer to a question or further explanatory information. The Executive Board has approved certain procedural measures for the tracking and reporting of financial information. These procedures also address how the financial activities of the various units under the A K umbrella will be reported. The financial instruction outlined here is merely one recommended way to record financial information. If you are successfully and accurately capturing and recording financial information and can accurately report your year end financial information annually to Headquarters as needed, you do not need to modify your current practices. Accurate reporting essentially means that you are collecting and recording your receipts and making sure your balance sheet balances as well as complying with Headquarters and IRS filing requirements. This booklet is written using the state as the reference point for ease of reading, but general information is also applicable and should be adhered to by all chapters, districts and area councils. This booklet contains a great deal of technical information about accounting and tax compliance. Members of the International Executive Board, the Headquarters Staff and I appreciate the time you will devote to the financial activities of your state to better record its operations. Please call on us to provide any help you may need in this endeavor. Susan L. Worley, CPA

5 I. INTERNAL REVENUE SERVICE EXEMPT ORGANIZATION REPORTING REQUIREMENTS The Alpha Delta Kappa Sorority, Incorporated is a 501 (c) (7) organization under the Internal Revenue Code, while the Alpha Delta Kappa Foundation is a 501 (c) (3) charitable organization. From the member s standpoint, the primary tax difference between the two organizations is that a donation to the Foundation is a charitable contribution, while a donation to International, a state or chapter is not. States, chapters and regions are grouped together under the Sorority s federal tax exemption. This group exemption permits those activities carried on for excellence in education by International, states, chapters and regions to be exempt from federal income tax. This group exemption also means that the regions, states and chapters fall under a different set of regulations than for-profit entities and thus have different reporting responsibilities. Failure to comply with these regulations may jeopardize the Sorority s tax-exempt status. A. The Alpha Delta Kappa Sororit y Incorporated s Reporting Requirements 1. Group Exemption Report a. Annual report which notifies the IRS of all regions, states and chapters to be included in ADK s group exemption relieves each entity from individually filing their own exemption applications and conducting correspondence to IRS on exemption matters. (1) Annual report includes the Employer Identification Number (EIN) for each region, state and chapter as well as the name of each state and chapter president and International Headquarters address. (2) Headquarters completes review of this report (3) Due Date: Annually by March 1 b. Group Exemption Number is Form Return of Organization Exempt From Income Tax a. Reports the financial activities of the Sorority b. Due Date: Annually by October 15 (the fifteenth day of the fifth month following the close of the fiscal year) c. Prepared by a certified public accountant 3. Form 990-T Exempt Organization Business Income Tax Return a. Reports the unrelated business income (UBI) received from regularly carried on income producing activities that are not related to ADK s exempt purposes b. Required if gross income is $1,000 or more c. Includes income from investments and interest for the Sorority. Excludes bequests and contributions (see below for applicable state UBI) d. Due Date: same as Form 990 e. Prepared by a certified public accountant 4. MO Missouri State Corporation Income Tax Return a. Due Date: Same as Form 990 b. Prepared by certified public accountant 5. Estimated Quarterly federal and state tax payments on unrelated business income (UBI) 1

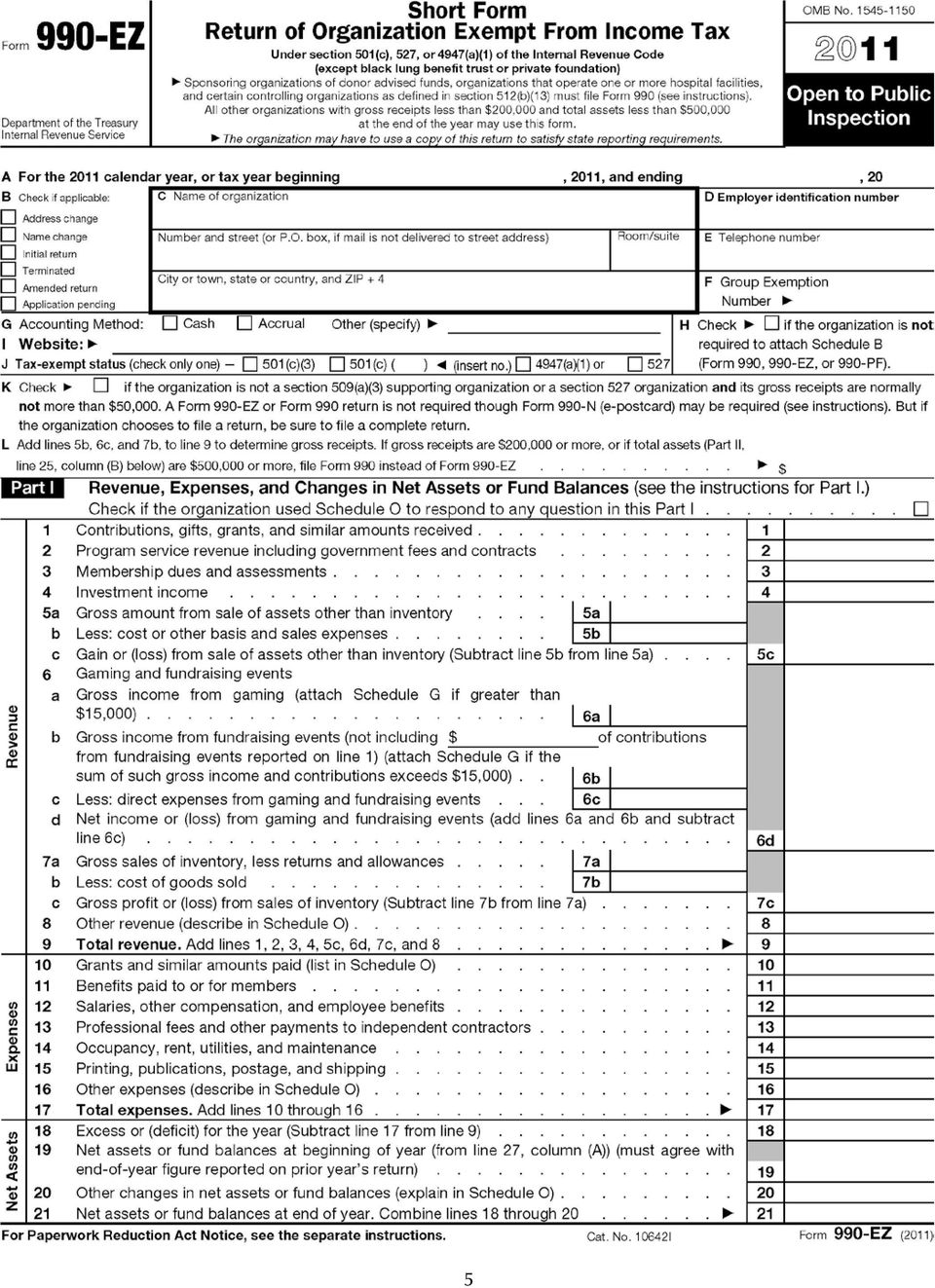

6 B. State and Chapter Organization s Reporting Requirements (See page 26, IRS Filing Requirements) All states and chapters are now required to file an annual report with the IRS. There are two categories for reporting/filing: States and chapters with gross receipts of less than $50,000 must file an annual electronic notice, Form 990-N also known as the e-postcard; States and chapters with gross receipts of $50,000 or more are required to file the more extensive Form 990 or 990-EZ. 1. Form 990-N (See pages for step-by-step instructions.) a. Form must be filed electronically. There is no paper form. b. Due Date: The 990-N (e-postcard) is due every year by the 15th day of the fifth month after the close of your state or chapter s fiscal year. For example, if your fiscal year is June 1 through May 31, you must file after May 31 and before October 15. c. Information Required on the 990-N e-postcard: (1) Your state or chapter s EIN/TIN number. It should be in your permanent files but if not, it is available from Headquarters. (2) Tax year. The 12-month fiscal year used by your state or chapter (Internatioanl Headquarters is making an effort to bring chapters and states fiscal years into alignment with International s, June 1- May 31.) If you don t know your fiscal year, contact your state treasurer. (3) Organization s Legal Name and Mailing Address (The Alpha Delta Kappa Sorority, Inc., 1615 W 92nd St, Kansas City, MO 64114) (4) Any other names your chapter uses (e.g. Missouri Beta Chapter) (5) Name of principle officer (current chapter president) and Headquarters address, above. (6) Organization s website address ( (7) Confirmation that your chapter s annual gross receipts are normally $50,000 or less. (8) If applicable, a statement that your chapter is going out of business. d. Where to File: When you are ready to file, go to e. Penalty: The IRS will revoke the tax-exempt status of a state or chapter who fails to meet the annual filing requirement for three consecutive years and possibly Alpha Delta Kappa s tax-exempt status as well. 2. Form 990 EZ - Short Form Return of Organization Exempt From Income Tax (See the form on page 5 for example) a. If gross receipts for the current year exceed $75,000; OR b. If gross receipts for the current year plus the preceding two years (total of 3 years) exceed $75,000; OR c. If you received a labeled Form 990 or Form 990-EZ from the IRS (1) Call the Executive Administrator at Headquarters for instructions on completing the form d. Due Date: Fifteenth day of the fifth month following the close of the fiscal year 2

is due every year by the 15th day of the fifth month after the close of your state or chapter s fiscal year.")

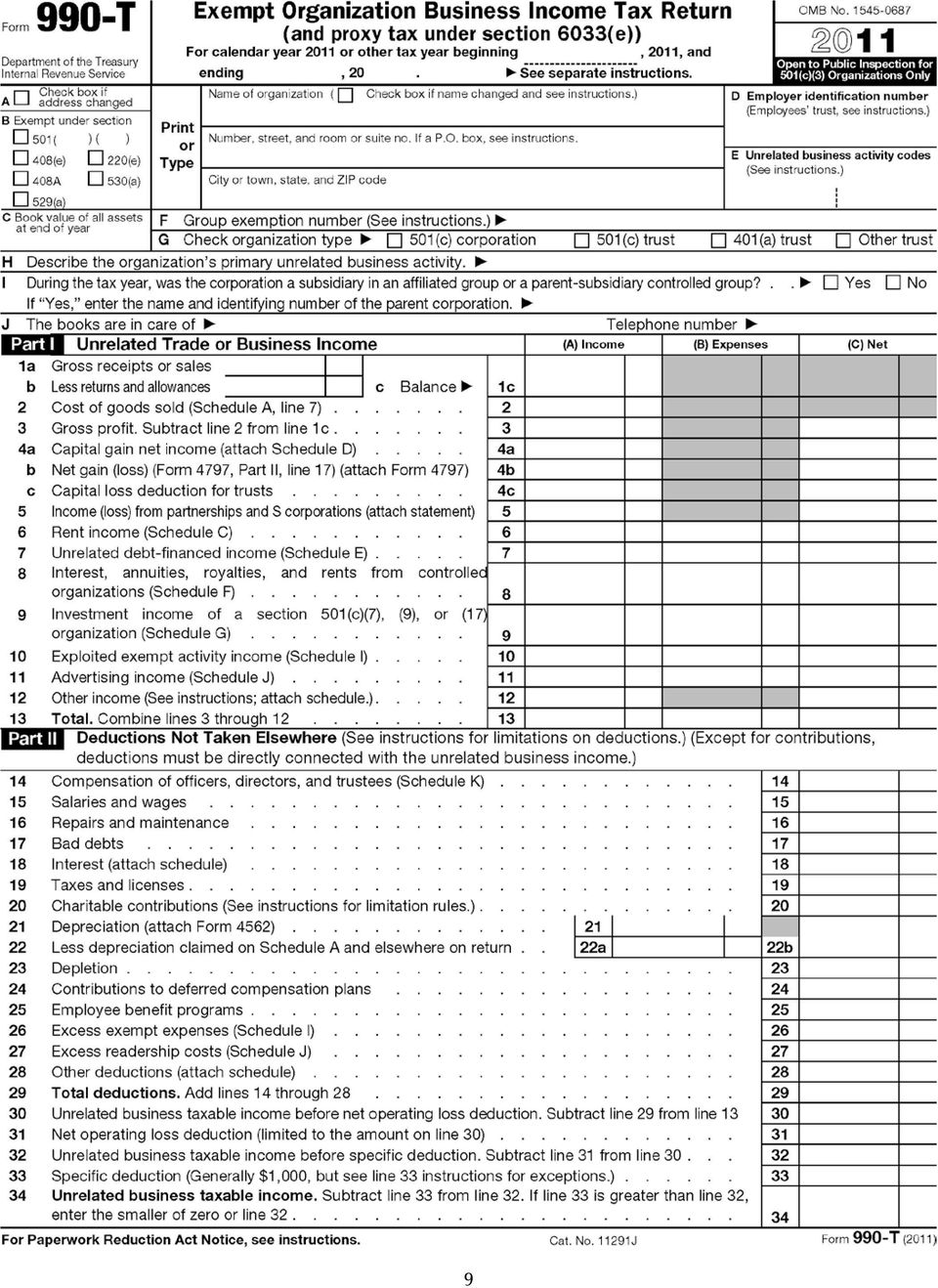

7 3. Form 990-T Exempt Organization Business Income Tax Return (See the four-page form on page 9 for example). a. Not required to file if Unrelated Business Income (UBI) is less than $1,000 b. Required to file if UBI is $1,000 or more. What is UBI? (1) EXCLUDES bequests or contributions (2) EXCLUDES ALL Fundraising efforts directed only to members (3) EXCLUDES all state scholarship fees assessed to members (4) UBI: Includes income from investments, interest income from checking accounts, certificates of deposit or mutual funds (5) Includes gross profits (defined as gross sales less cost of goods sold) from regularly carried on Fundraising activities to the general public (non-members) (a) Example Fundraising program to general public selling t-shirts: Sales Receipts $1,900 Cost of Goods Sold $800 Gross Profits $1,100 (b) If your state has gross profits of $ from regularly carried on Fundraising events to the general public by the end of your third quarter, notify the Headquarters Executive Administrator for guidance. c. Due Date: Same as Form 990 EZ d. Determine federal and state tax liability on your unrelated business income, if any (1) Subtract expenses directly related to that income, for example, investment advisor fees from investment income (2) A specific $1,000 deduction further reduces the amount of taxable income, if any (3) Even if tax liability is reduced to zero, must still complete and file Form 990-T e. Options available to the state in the use of UBI: Goal: To maximize the use of UBI for the state s purposes. Consult your local CPA for assistance. (1) You may set aside or designate net investment income to an A K state scholarship program or a 501 (c) (3) entity of your choosing; thus reducing any potential tax liabilities. (a) Set aside approval should be documented in the executive board s minutes as well as the financial records. (b) Approval must be given annually. (c) Set aside monies need not all be spent each year, but they must be retained in separate bank account. Balances may NOT unreasonably accumulate over time. (2) You may not set aside gross profits from regularly carried on fundraising efforts to the general public. (3) You may use up to $1,000 of UBI on state s operating activities, state scholarship program, or donation to a 501 (c) (3) entity. (4) The use of the amount in excess of $1,000 depends on the source. Consult your local CPA for guidance on your specific case. Example: 3

Includes gross profits (defined as gross sales less cost of goods sold) from regularly carried on")

8 (a) Example 1: Current Year s Gross Profits as defined above. $900 Current Year s Net Investment Income on Scholarship Account $0 Current Year s Net Investment Income on General Account $200 Total $1,100 State executive board must set aside a minimum of $ in net investment income to scholarship account and write a separate check from the operating account to scholarship account. It may however, set aside more to the scholarship account if it so chooses. Once net investment income is transferred to scholarship account, it must remain there. Result: No federal or state tax liability because up to $1,000 in UBI is exempt from tax, and the excess over $1,000 was set aside to state scholarship program or to 501 (c) (3) entity. (b) Example 2: Current Year s Gross Profits as defined above. $2,000 Current Year s Net Investment Income on Scholarship Account $0 Current Year s Net Investment Income on General Account $0 Total $2,000 Result: State will owe federal and state taxes on $1,000 because up to $1,000 is exempt from tax and set aside option is not available for the remaining $1,000 (because the $2,000 does not include an investment income). As IRS reporting can be complicated, International encourages states and chapters to use the services of a certified public accountant to insure accuracy and compliance when filing the 990, 990-EZ or 990-T Forms. C. Chapter Reporting Requirements 1. Same as those of the state 4

9 5

10 6

11 7

12 8

13 9

14 10

15 11

16 12

17 II. ALPHA DELTA KAPPA FOUNDATION S PROGRAM EFFORTS During the biennium, the Foundation s Board of Trustees approved a number of new programs to better serve the needs of our members, states and chapters. A. Alpha Delta Kappa Foundation S/P/N Altruistic Fund 1. States and chapters work with the Foundation to establish their own scholarship program and/or altruistic fund. a. Contribute scholarship and altruistic funds to a named account in the Endowment Fund (e.g. Alabama Altruistic Fund) (1) $5,000 minimum b. Foundation has developed IRS-approved model guidelines, applications and reporting forms for state and chapter use. c. Funds become assets of the Foundation and are invested in accordance with the Foundation s investment policy. d. Investment fees, gains and losses are prorated based on the total amount of the S/P/N Altruistic Fund. e. S/P/N or chapter is responsible for the administration of their scholarship and/or altruistic program. f. Foundation issues checks to the recipients. g. S/P/N or chapter is responsible for submitting personalized scholarship guidelines and names and addresses of judges and recipients to the Foundation. h. Altruistic donations must be made to 501 (c) (3) organizations. i. Advantages (1) Reduces state s or chapter s IRS compliance, as it is now the Foundation s responsibility (2) Reduces liability (3) Future donations to the fund are tax deductible to the donor. (4) Fund qualifies as a charitable set aside for the state s or chapter s unrelated business income, reducing its tax liability. (5) Can eliminate the need to file estimated quarterly federal and state tax payments on investment income (6) Reduces state s or chapter s expenses for attorneys, accounting and investment fees B. IRS Requirements for Disbanding Chapters The IRS requires U.S. chapters that are disbanding to give their remaining monies to a 501 (c) (3) organization 1. In 1998 International Executive Board implemented a policy requiring that lapsing U. S. chapters must: a. Donate any remaining funds to the Foundation; OR b. Distribute any remaining funds between the Foundation and another 501 (c) (3) organization. 2. States are asked to assist with the implementation of this policy by informing chapter officers of the policy when discussing the possibility of disbanding. 13

18 III. ORGANIZATIONAL STRUCTURE A. State Responsibilities 1. Each state is now responsible for receiving and reporting the financial activities of its districts and area councils. 2. Each state is accountable for the accuracy and reliability of financial information provided by its districts and area councils. 3. All state officers, particularly the state treasurer, are accountable for the accuracy and reliability of the subsidiary information provided to them and to Headquarters. B. Reporting Period (Fiscal Year) 1. Alpha Delta Kappa is currently engaged in an effort to bring all states and chapters fiscal years into alignment with International s (June 1 - May 31). Information was mailed in the 2012 supply packets. When fiscal years are aligned, everyone will have the same deadline to file the 990N e-postcard, and Headquarters will be able to remind states and chapters of the deadline. 2. State and its districts and area councils should have the same fiscal year. 3. Fiscal year is composed of 12 months. 4. Starts and ends on the same date, year after year. C. Group Exemption Authorization 1. All states have completed a group exemption authorization, which is on file at Headquarters. 2. Chapters sign a group exemption authorization at the time they form. D. Employer Identification Number (EIN) or Taxpayer Identification Number (TIN) 1. At the time of formation, Headquarters completes a Form SS-4, applying for an EIN for each state and chapter. The IRS uses EIN and TIN interchangeably. It is the same number. 2. IRS notifies the state and/or chapter of its EIN, and the state and/or chapter reports the number to Headquarters. 3. Do not apply for an EIN on your own. 4. If unsure if you have an EIN, or are unsure if you are using the correct one, check with Headquarters. 5. EIN should be a part of your permanent records. 6. Never use an EIN that has not been assigned to your organization. 7. Use the correct EIN and official name when corresponding with the IRS. a. Variation will result in the IRS assigning a new EIN. 14

1. Alpha Delta Kappa is currently engaged in an effort to bring all states and chapters fiscal years into alignment with International s (June 1 - May 31).")

19 E. Bank Accounts and Related Bank Statements 1. States, use your state s EIN to open a bank account. Chapters, use your chapter s EIN to open a bank account. 2. Do not use your personal social security number in application. 3. Districts and area councils may have individual bank accounts, using the state s EIN. a. State treasurer or other officer must be included as a check signer on the bank signature card of district and/or area council account. 4. If an incorrect EIN was used to open a bank account, complete a new bank signature card with the correct EIN as soon as possible. 5. Use personalized checks, imprinted as follows: a. State + Alpha Delta Kappa Sorority (i.e. Florida Alpha Delta Kappa) b. Chapter checks should be personalized with the name of the state + Greek Name (e.g. Florida Beta Nu Chapter) Bank statements should end on the last day of the month. a. If your statement doesn t, request the bank to change the statement cycle to month end. b. Will greatly facilitate preparation of monthly accounting reports 7. Balance all accounts monthly. a. Especially important if there is a high volume of activity IV. STATES ANNUAL REPORTING REQUIREMENTS TO INTERNATIONAL To determine your IRS reporting requirements, International requires that each state complete and submit the following reports to Headquarters: Cash Flow Statement (See page 20, Report S-1) Balance Sheet (See page 22, Report S-2) And if applicable: Three-Year Gross Receipts Calculation (See page 23, Report S-3) If current year s receipts (minus International sustaining members dues and fees) are over $50,000 All reporting forms will be mailed annually to state presidents and are to be completed and mailed to Headquarters no later than eight weeks following the close of the state s fiscal year. V. STATE ACCOUNTING REPORTS The state treasurer (and other appropriate members to aid her if desired) should prepare accounting reports on a regular basis to meet her fiduciary responsibility as a state officer. The state officers should carefully review these financial reports. Whether or not a software package is used to prepare reports is solely up to the state treasurer. For states with a larger volume of activity, a software package such as Quicken may be helpful. For others, Microsoft s Excel spreadsheet or columnar paper will be satisfactory. 15

b. Chapter checks should be personalized with the name of the state + Greek Name (e.g. Florida Beta Nu Chapter)... 6.")

20 A. Cash Flow Statements 1. Show the flow of receipts and disbursements over a specific period of time a. Should end with the last day of a certain month for the designated period (month, quarter or fiscal year) b. Should be detailed enough to know the nature of the disbursement by reading the line item 2. Developed for a 12-month period rather than a two-year period 3. Results may be in the red at the end of year one because of the nature of your state s activities a. This is acceptable from an accountant s perspective b. Does not reflect poor fiscal management c. Merely represents timing differences between receipts and disbursements 4. Results should be in the black at the end of year two a. If not in the black, the statement shows the budget is not serving its purpose and the state is spending in excess of its receipts 5. Notes of explanation and template for a cash flow statement (See page 18, Report S-1) a. Adjust template to meet your needs 6. District and Area Council data a. If they do not have their own bank accounts, their receipts and disbursements will automatically be recorded with the state s cash flow statement through its cash receipts and disbursements. b. If they do have their own accounts, the district and area council information must be included in the state s year end report. c. The district s and area council s activity should determine their frequency of reporting to the state. B. Balance Sheet 1. Shows what the financial position is as of a certain date a. Date corresponds to the last date of the period of time for which you are reporting. 2. Template for a balance sheet and notes of explanation (See page 22, Report S-2) C. Budget 1. Shows projected cash receipts and disbursements for the subsequent year (See page 25, Report S-4) a. Use the current year end projected or actual figures to help you formulate your numbers. b. Include the activities of not only your state, but also districts and area councils. c. Include the prior year s actual numbers and the prior year s budgeted numbers as a means of comparison. 2. The process should permit revisions by fellow officers and members. 3. Prepared on an annual basis 16

21 4. If state convention is held once every two years, the two annual budgets for the biennium should be presented and approved at the state convention. 5. If state convention is held annually, then one year budget should be presented and approved at the state convention. 6. May be amended by the state executive board as needed 7. Executive Board monitors the inflows and outflows reported by the budget. 8. Effective tool for officers to communicate and plan strategically 9. International does not require a copy of the state budget. 10. The accounts on the cash flow statement and the budget mirror one another; changes made to cash flow statement should also be made to the budget. 17

22 Alpha Delta Kappa Sorority Accompanying Notes of Explanation to Cash Flow Statement Report S-1 1. Sustaining members International dues and publication fees should be deposited and recorded by the state. When determining what gross receipts are from the IRS standpoint, sustaining members International dues and fees should be excluded. Typically this is not a large amount and will not significantly affect your calculation of gross receipts. Report S-3 on page 23 will guide you through this calculation. 2. All scholarship fees should be deposited in a separate account from the general operating account. Monies from scholarship fees should not be commingled with the operating funds. Interest earned on the separate scholarship bank account should always remain in the scholarship account and be used for scholarship programs. 3. Receipts for your state s altruistic project should be recorded in full, without subtracting any costs associated with it. Those costs should be included in your disbursements section on the next page. 4. Bequests and contributions are an important source of revenues, and must be accounted for in the determination of gross receipts. For example, bequests could occur in the form of cash or real estate. In either form, the state treasurer must monitor the Form 990-EZ reporting requirements for the current year. (See Report S-3 for further help on this). Such a large bequest or gift could change the circumstances so significantly that a state which under normal circumstances would not need to file a 990- EZ will now need to do so with the receipt of the bequest or contribution. Therefore, capturing and recording these sources of receipts is very important. 5. You may wish to add several lines of interest income to reflect the different types of investments for example, money market checking, certificate of deposit, investment income or securities, etc. If this amount totals $1,000 or more, completion of Form 990-T is required. 6. Flow through accounts merely represent the receipt of revenue and the outflow of the associated expense, all within one account. Example 1: A small contribution to Charity X is a receipt and the check written to disburse the contribution is an expense for a net sum of zero. Example 2: Revenue is money collected from members for a meal and the expense is the associated check written to the restaurant for the meals, for a net sum of zero. 7. Because districts and area councils now fall under the state s umbrella, separate lines should occur for their receipts. If your state has numerous districts and the districts DO NOT have their own bank accounts, then you will want a separate line for each district s total receipts and require that each district complete D1-EZ Single Event reporting form for each activity. If, however, your districts DO HAVE their own bank accounts, then they each need to send the state a copy of the cash flow statement (D1) (at a minimum annually) for you to include in your state cash flow statement. 18

23 Alpha Delta Kappa Sorority Accompanying Notes of Explanation to Cash Flow Statement Report S-1 8. If you should have significant Other receipt sources, they should be separately identified. If that is not the case, miscellaneous receipts can fall within this Other category. 9. The disbursement of sustaining members International dues and publication fees merely represents the state acting as an agent in forwarding these amounts to International. Typically this disbursement amount is not significant. 10. International convention disbursements usually occur in the summer of odd numbered years (which occur in the even numbered accounting year if your state has a fiscal year end of May 31.) Comparably, regional conference disbursements usually occur in the summer of the even numbered year, and state convention disbursements perhaps every year. All three have been included on the template because they should be included in the accounting year in which the disbursement is made. For example, let s say your state has a May 31 year end and you book and pay for the officers air fares to International convention in April. The airfares should be recorded on the May 31 financial statements, and the remaining disbursements on the next year s May 31 financial statements. Therefore, include all the applicable line items each year to properly record the timing of disbursements. 11. Fund transfer represents transferring funds from one cash account (savings) to another (checking account) to cover operating disbursements. 19

24 Report S-1 Alpha Delta Kappa Sorority Cash Flow Statement Template (For the 12 Months Ending Your State Year End) If gross receipts were $50,000 or less, state electronically filed the 990-N: qyes qno Date Filed Your State Year End State Receipts (Revenues) International Dues - Sustaining Members 1 Publication Fees - Sustaining Members 1 Dues - State Fees - State Scholarship 2 Fees - Late Fees EIN Subtotal - All Dues and Fees... State Convention Revenue Other Meeting Revenue Fundraising for Altruistic Project (Gross Receipts) 3 Fun Day Sales (Ways and Means) Sales to Members Sales to Non-Members Bequests 4 Contributions 4 Interest Income 5 Flow Through 6 District Receipts 7 Area Council Receipts 7 Other Receipts 8 Funds Transferred from savings Actual For Year End Total Receipts Check: Subtract sustaining members International dues and fees from total receipts. If over $50,000 or your state filed a 990 in either of the two previous years, also complete Report S-3. See accompanying notes of explanation. 20

25 Disbursements (Expenses) International Dues - Sustaining Members Paid to Headquarters 9 Publication Fees - Sustaining Members Paid to Headquarters 9 Altruistic Contribution paid to Charity 3 Altruistic Costs (Non Contribution Expenses/fundraising costs) 3 Professional Services (accounting, legal, consulting) Board Members Expenses - Officers Subsidies Board Expense - Meeting Planning/Accommodations Newsletters/Publications Postage Telephone Historian International Convention 10 State Convention 10 Regional Conference 10 Other Meetings Membership Scholarship Disbursements to recipients District Disbursements 7 Area Council Disbursements 8 Music Courtesy Miscellaneous Fund Transfer to Savings 11 Total Disbursements Total Receipts Less Total Disbursements Please Sign: Actual For Year End Report S-1 Signature Telephone Print Name Date Mailing Address See accompanying notes of explanation. 21

26 Report S-2 Alpha Delta Kappa Sorority Sa m p l e Ba l a n c e Sheet (Yo u m a y a d d lines to t h i s f o r m a s needed.) (As of Your State Year End) Your State Year End ASSETS Cash and Investments Checking Account - Mercantile Bank $ 11,300 Savings Account - Mercantile Bank 4,300 Certificate of Deposit - Commerce Bank 10,000 Total Assets $ 25,600 LIABILITIES AND NET ASSETS Liabilities $ Net Assets $ 25,600 Total Liabilities and Net Assets $ 25, Net assets for a not-for-profit organization are the equivalent of equity for a for-profit organization. Most software packages use the term equity, however. As most states are on the cash basis, they will not record any liabilities. 2. Note that Total Assets must equal Total Liabilities and Net Assets to balance. 22

27 Report S-3 Alpha Delta Kappa Sorority Calculation of Gross Receipts Using IRS Standards Explanatory Note: From the standpoint of the IRS, gross receipts are the total amount received from all sources of funds which your state has control over, without subtracting any costs and expenses. Sustaining members International dues and publication fees should not be included in your state s calculation of gross receipts, because your state has no right to use the funds. Therefore, to determine gross receipts at the state level, complete the attached worksheet for the current year column only. Remember, do not subtract any costs or expenses that may be related to these sources of income. For example, include all of your receipts from Fundraising events and activities without deducting costs or sales expenses. The Fundraising receipts should be recorded at full value (or using accounting lingo, at gross ). The Fundraising costs and expenses should be included separately under the disbursements section of your cash flow statement. Calculation Procedures: 1. What is your total for the current year? Is your total less than or equal to $50,000? If so, no further calculation is required on this worksheet. You do not need to file a Form 990 EZ for the current year. You may skip completing the rest of this worksheet. 2. If your gross receipts are more than $50,000 in the current year, you need to calculate your gross receipts for the remaining two columns on the worksheet and send the completed schedule to Headquarters. 3. Do your totals for the three years exceed $75,000? If NO, you do not need to complete the Form 990 EZ for the current year. However, keep this worksheet in your permanent file for next year, as you will need to refer and use your calculations again. If YES, you will need to complete the IRS filing requirements as outlined on page

28 Report S-3 Alpha Delta Kappa Sorority Three-Year Gross Receipts Calculation If the total under the Current Year column exceeds $50,000 or your state filed a 990 in either of the two previous years, complete the next two columns. Mail the completed form to Headquarters along with your current cash flow statement and balance sheet (Reports S-1 and S-2) no later than eight weeks following the close of your fiscal year. Your State Year End State EIN Current Year One Year Previous to Current Year Two Years Previous to Current Year State Dues Only State Scholarship Fees Only State Late Fees Only State Convention Revenue Other Meeting Revenue Fundraising Altruistic Project Fun Day Sales Bequests Contributions Interest Income/Investment Income District Receipts Area Council Receipts Other Receipts TOTAL Note: Current year is the most recent fully completed accounting period (a total of 12 months). See accompanying note of explanation. 24

29 Report S-4 Alpha Delta Kappa Sorority Sa m p l e Bu d g e t (Yo u m a y a d d lines to t h i s f o r m a s needed.) (For the 12 Months Ending Your State Year End) Current Year s Budget Current Year s Actual Projected Subsequent Year s Budget Prior Year s Actual OPTIONAL Prior Year s Budget Disbursements (Expenses) International Dues - Sustaining Members Paid to Headquarters Publication Fees - Sustaining Members Paid to Headquarters Altruistic Contribution to Charity Altruistic Costs (Non Contribution Expenses) Professional Services (accounting, legal, consulting) Board Members Expenses - Officers Subsidies Board Expense - Meeting Planning/Accommodations Newsletters/Publications Postage Telephone Historian International Convention State Convention Regional Conference Other Meetings Membership Scholarship District Disbursements Area Council Disbursements Music Courtesy Fund Transfer Miscellaneous Total Disbursements 25 Total Receipts Less Total Disbursements

30 Exhibit A Alpha Delta Kappa Sorority IRS Filing Requirements Summary Note: Based on your answers on Report S-3, you have determined that you need to file a Form 990 EZ or Form PART I: IRS Submission Requirements Deadline IRS Reporting Requirements Headquarters Submission Requirements Headquarters Filing Requirements If... Go to: No later than the fifteenth day of the fifth month following the close of your fiscal year Electronically file form 990-N e-postcard S-1 and S-2 Submit the S-1 and S-2 reports to Headquarters eight weeks after the fiscal year-end. Gross receipts for the current year are less than $50,000 Submit completed tax returns to: IRS Ogden, UT Form 990 EZ or Form 990 must be filed no later than the fifteenth day of the 5th month following the close of your fiscal year*. Your CPA may file an extension to avoid penalties for not reporting. The extension must be filed by the 15th day of the 5th month following the close of your fiscal year. File a Form 990 EZ or Form 990 One copy of Accounting Review and Form 990 EZ or Form 990 State treasurer submits a Cash Flow (Report S-1), Balance Sheet (Report S-2) and Calculation of Gross Receipts (Report S-3) to Headquarters eight weeks after fiscal year end. Headquarters reviews and confirms results. State treasurer engages a local CPA to complete accounting review and Form 990 or 990 EZ to meet IRS filing requirements. Gross receipts for the current year exceed $75, See above. See above. File a Form 990 EZ or Form 990 One copy of completed Form 990 EZ or Form 990 State treasurer submits a Cash Flow (Report S-1) and Balance Sheet (Report S-2) to Headquarters eight weeks after fiscal year end, for the current year plus the preceding two years. State treasurer submits completed Report S-3, calculating gross receipts. Headquarters reviews and confirms results. State treasurer engages a local CPA to complete Form 990 or 990 EZ. Gross receipts for the current year plus the preceding two years (total of three years) exceed $75,000 *If your fiscal year end is May 31, your return is due no later than October 15. If your fiscal year end is December 31, the return is due by May 15th. However, you should give your Certified Public Accountant ample time to prepare the Form 990 EZ or Form 990.

31 Exhibit A PART II: IRS and State Submission Requirements Deadline IRS Reporting Requirements and State Reporting Requirements Headquarters Submission Requirements Headquarters Filing Requirements If... CPA will provide instructions on the federal and state filing requirements and estimated payment requirements, if any. Form 990-T must be filed no later than the 15th day of the fifth (5th) month following the close of your fiscal year.** Your CPA may file an extension to avoid penalties for not reporting. The extension must be filed by the 15th day of the fifth (5th) month following the close of your fiscal year. Estimated federal and state payments, if required, need to be paid on a quarterly basis. CPA to file a Form 990-T and state corporation income tax return. Quarterly estimated federal and state tax payments may also be required. One copy of Form 990-T and state corporation return. Forward Xerox copies of quarterly tax payments made for federal and state tax liabilities, if any. State treasurer submits the Cash Flow Report (S-1), with a list of names and addresses of sources of interest income and investment earnings. Detail of gross profits from regularly carried on Fundraising activities to general public is also included if applicable. Headquarters reviews and confirms results. State treasurer engages a local CPA to complete the Form 990-T and state corporation income tax return. Quarterly estimated federal and state payments may be required on gross profits from regularly carried on public Fundraising activities. UBI* equals or exceeds $1,000 in the current year *UBI is composed of investment earnings, dividends, capital gains and interest income from bank accounts, certificates of deposit and mutual funds. It is also gross profits of Fundraising activities regularly carried on to the general public. Gross profits are total sales receipts minus cost of goods sold. **If your fiscal year end is May 31, your return is due no later than October 15. If your fiscal year end is December 31, the return is due by May 15th. However, you should give your Certified Public Accountant ample time to prepare the Form 990-T.

32 Alpha Delta Kappa Sorority Determination of Unrelated Business Income Does your state have $1,000 or more of UBI from (add all that apply): 1. Investment earnings, dividends, capital gains and interest income from bank accounts and certificates of deposit and mutual funds. 2. Gross profits of substantial Fundraising efforts regularly carried on to the general public. (Exclude all Fundraising efforts directed solely to members.) Gross profits are defined as total sales receipts minus cost of goods sold. Engage a CPA to complete Form 990-T and your state corporation return. You are not required to file Form 990 EZ. To minimize the federal and state tax liability, consult your local CPA for guidance. In general, however, for the excess over $1,000: If available to do so, set aside net investment income to state ADK scholarship program or to a 501(c)(3) entity. If net investment income is set aside for state ADK scholarship program, carefully follow procedures to transfer amount to scholarship account. If no net investment income was earned in the current year and excess over $1,000 composed solely from gross profits from regularly carried on Fundraising activities to the general public, consult your local CPA for calculation of federal and state tax liabilities and completion of Form 990-T. You may spend the first $1,000 of UBI as you choose, including for the use of state s operational needs. Engage a CPA to complete the above PLUS Form 990 EZ. All of the above issues regarding the disposition of UBI also apply. YES and gross receipts of less than or equal to $50,000 YES and gross receipts of greater than $50, NO and gross receipts of less than or equal to $50,000 NO and gross receipts of greater than $50,000 Only file 990N e-postcard. Form 990-T (Exempt Organizations Business Income Tax Return) and Form 990 EZ do not need to be completed. You may designate the use of the UBI as you choose. Engage a CPA to complete Form 990 EZ only. You may designate the use of the UBI as you choose.

33 ALPHA DELTA KAPPA SORORITY Suggested Monthly Planner for State Treasurers Developed For May 31 Year End Duties Performed by Outgoing Treasurer: Month 1 After Your State Year End 1. As soon as all checks have cleared the bank (verified by the latest bank statement), close books and prepare year end financial statements. 2. Turn the books over for a review by a committee or certified public accountant. 3. Obtain and complete a new bank signature card for each account, with the name, address and signature of the newly elected treasurer. It is not necessary to change banks. (Note: The signature cards should also carry the name, address and signature of the newly elected president in the event the treasurer could not carry on the duties of her office.) 4. Meet with the newly elected treasurer to review and turn over all files, including bank statements, cancelled checks, the checkbook, deposit slip book, ledger, all reimbursements and receipts all documents of your job as treasurer, including a copy of the latest state budget. (These documents contain vital tax information, if called upon to fill out IRS Form 990 EZ or Form 990, or in the event of an IRS audit.) Duties Performed by the Treasurer with the Assistance of the Immediate Past Treasurer: Month 2 5. Review and Observe Record Retention Requirements. A. Indefinitely: 1) EIN Number (assigned by the IRS), any correspondence from the IRS, copy of any reports to the IRS, copy of correspondence from Headquarters regarding the IRS. 2) Any filed tax returns, including work papers 3) Audit reports and financial statements, cancelled checks for taxes, cash books 4) Financial ledgers, journals and reports 5) IRS determination letter stating that Alpha Delta Kappa is a non-profit organization, designated 501(c)(7) by the IRS. (The IRS letter and your state s EIN will be necessary in opening a new bank account.) B. Retain for eight years: 1) Bank reconciliations and bank statements Retain for three years: 1) petty cash vouchers, general correspondence, other cancelled checks, expense reports, paid bills and monthly trial balances. 6. Prepare and submit Cash Flow Statement (Report S-1) and the Balance Sheet (Report S-2) to Headquarters prior to eight weeks following the close of your fiscal year. 7. If gross receipts are greater than $50,000 in the fiscal year just ended, submit Reports S-1, S-2 and S-3 (Three-Year Gross Receipts Calculation) to Headquarters for review. 29

34 8. If Report S-3 shows that the fiscal year just ended and the preceding two years gross receipts exceed $75,000, engage a certified public accountant to complete IRS Form 990 EZ. 9. If gross receipts are greater than $75,000 for the fiscal year just ended, engage a certified public accountant to complete an accounting review and complete IRS Form 990 EZ. Duties Assumed by Treasurer: Month Make certain the CPA has all necessary information for review and completion of IRS Form 990 EZ, if required. 11. Prepare monthly bank reconciliations and maintain a record of the name, address and telephone number of each bank where your state accounts are held. 12. Gather Treasurer s supplies and take to every state executive board meeting: A. Money pouch with cash for change, calculator, checks, deposit slips, current budget, expense vouchers, check endorsement stamp (optional), return address labels, ledger, note pads, paper clips or stapler. 13. Prepare your treasurer s report for the state executive board meeting. (The report may be no more than the balances on hand since you may not have transacted any business yet.) Month Throughout your term, attend state executive board meetings and present treasurer s reports. 15. Throughout your term, distribute expense vouchers for all requests for reimbursement. Collect completed vouchers substantiated by appropriate receipts and write reimbursement checks. 16. Pay all bills by check as the check doubles as your receipt and is verifiable. Record on the lower left-hand portion of each check, the purpose of the check. 17. If food is catered for lunch, determine the amount owed by each member, collect the amount from each member, pay the bill for the lunch (and any meeting room rental) and deposit the money in the state s checking account as soon as possible. 18. Record an entry in your ledger/register for each transaction for which you wrote a check. 19. Monitor your budget carefully. If you have problems, consult the state president and immediate past treasurer for assistance. Month Assemble the required information for filing Form 990-N e-postcard if you have gross receipts of $50,000 or less. (See pages 2, 23, 46-48) 30

35 21. If gross receipts are less than $50,000, electronically file Form 990-N e-postcard by the fifteenth day of the fifth month following the end of your fiscal year. 22. If gross receipts are $50,000-$200,000 and filing is required, mail your completed IRS Form 990 EZ by October 15 (the fifteenth day of the fifth month following the close of your fiscal year) if your fiscal year end is May 31. If your fiscal year end is other than May 31, calculate date of filing. 23. If filing is required, send a copy of your completed IRS Form 990 EZ to Headquarters and keep a copy in your permanent files. Month Receive H-138 Membership Dues Billing for Sustaining Members from Headquarters. 25. Notify sustaining members of the amount of their state and International membership dues, the due date of January 1 and late fee for missing the January 31 payment postmark deadline. Enclose a self-addressed envelope for sustaining members to remit their dues to you. 26. As sustaining member dues arrive, record the amount paid on the billing form (H- 138) and send the form and a state check for the total amount of dues collected to Headquarters. Dues are due January I and become delinquent after January 31. All delinquent dues require an additional $5.00 per member late fee paid to International. If postmarked after January 31, mail directly to International Headquarters, not the PO Box. 27. Mail membership cards to sustaining members soon after receiving their dues. 28. Receive and record all state dues collected from chapters. 29. Deposit all dues checks in the state s checking account as soon as they are received. Month Continue as for Months 6 & For each interest-bearing account, you will receive a bank statement of interest earned the prior year. 32. Meet with the state budget committee, taking several copies of the previous year s budget and actual figures as well as the current year s year-to-date figures. Be prepared to share financial information to determine whether or not sufficient or insufficient funds were budgeted for each line item and whether or not specific line items would be increased, if needed, based on the year s past income. 31

36 The budget committee develops two annual budgets (one for the even numbered year and one for the odd) and compiles the two budgets into a proposed budget for the biennium. The budget committee chairman prepares copies of the budgets to present to the state executive board meeting. The board may revise the budgets before recommending they be presented to the state convention; or, if the convention doesn t meet in the second year, before approval of the board. The budget committee chairman then prepares copies of the proposed budget for each convention registration packet, or if a convention is not held in the second year, for the executive board packet. Month Prepare financial statements for presentation to the state executive board. Have details ready on key issues and comparisons. 32. Pay any reimbursement requests, room rental and lunch fees associated with the state executive board meeting. 33. Inform the executive board of any interest earned on bank accounts the past year, discuss which altruistic organization or scholarship to contribute it to, and make the appropriate motion to do so. (As soon as possible thereafter, write the check to disburse the funds.) This is to reduce tax liability on unrelated business income (UBI). Month Prepare and present a report at the state convention. 35. At the close of the state convention, receive and deposit advance money, and any overage after the convention committee has paid its bills. 36. Prepare executive board report and complete financial statements. Present budget revisions to board if a convention is not held in the second year. Month Make certain all deposits and expense reimbursements have been completed by the month end so the transactions correspond with the current fiscal year. 38. Clean and order files according to record retention requirements (See page 45, #5.) 39. Review Month 1 and 2 of the Monthly Planner for Duties Performed by Outgoing Treasurer or with the Assistance of the Immediate Past Treasurer. NOTE: Document may be modified to meet your state s activities. Acknowledgment: Thank you to Helen Hess and her colleagues in Oregon Alpha Delta Kappa for providing the information in the monthly planner and organization of the treasurer s files. 32

37 Alpha Delta Kappa Sorority Suggestions for Setting Up the Treasurers Files (Use expanding folder or file box for present use and future storage.) A. Treasurer s Duties/Guidelines B. Budget C. Expense Voucher D. Forms H-119/H-133 (With running membership tally) E. IRS and EIN* (Permanent File) F. Audit Reports (Permanent File) G. Financial Statements (Permanent File) H. Directory (With chapter treasurers contact information) I. Members Dues J. Financial Reports K. Bank Statements/Reconciliations L. Receipts/Cancelled Checks (Stapled to Expense Vouchers) M. Scholarship & Altruistic Project (Addresses/Amounts Funded) N. Miscellaneous *United States Only States and Chapters 33

38 GUIDELINES FOR STATE TREASURERS IN WORKING WITH DISTRICTS, AREA COUNCILS AND CHAPTERS ON FINANCIAL REPORTING Districts/Area Councils: 1. Decide which district form works best for your state s record keeping (D-1 EZ Single Event Reporting Form or D-1 Annual District/Area Council Cash Flow Statement). 2. Complete the due date and fiscal year blanks on the appropriate form, copy the form and distribute them to your districts and area councils, preferably during training session. 3. Follow up, making certain you receive completed financial reports from each district and area council by the deadline. 4. Incorporate district/area council reports into the state s financial records and reports. Chapters: 1. Complete the due date and fiscal year blanks on the C-1 Annual Chapter Reporting Form and Audit. 2. Copy the C-1 and C-4 forms, the Guidelines for Chapter Treasurers and the You Must Report to the IRS document (page 46) and distribute these to chapter treasurers, preferably during a training session. 3. Follow up, making certain you receive a completed financial report C-1 from each chapter by the deadline. (Chapter C-1 Tracking Summary provided.) 4. Analyze each C-1 report. If the gross receipts were less than $50,000, did the chapter electronically file Form 990-N e-postcard? If the total adjusted receipts are $50,000 or more and/or Ways & Means - Sales to Non-Members and Interest equal $1,000 or more, contact the chapter president to make certain a copy of the C-1 report was forwarded to International Headquarters. After receiving the C-1 report, Headquarters will send the chapter treasurer forms C-2 and C-3 for completion. 5. If the C-1 report shows that the chapter filed an IRS 990-EZ in the previous year, remind the chapter president that the chapter will receive a packet from the IRS for the current year. REQUEST THAT THE CHAPTER PRESIDENT CONTACT INTERNATIONAL HEADQUARTERS FOR FILING INSTRUCTIONS WHEN THE PACKET IS RECEIVED. 34

39 IN A NUT SHELL... IRS Form 990 or 990-EZ Key Term Gross Receipts = All receipts which your state has control over, without subtracting costs and expenses. This includes bequests and contributions. Key Amount $75,000 Key Date The 15th day of the fifth month following the close of the fiscal year (5/31 = 10/15). Key Concepts 1. File if a. Gross receipts for current year exceed $75,000, or b. Gross receipts for current year plus preceding two years exceed $75,000, or c. You received a labeled form in the mail from the IRS. 2. A large bequest could make it necessary for a state or chapter which normally never has to think about filing to file a 990 or 990-EZ. 3. If required to file, consult a CPA. 35 IRS Form 990- T Key Terms Unrelated Business Income (UBI) = Any income that does not relate to one of the purposes of Alpha Delta Kappa. UBI includes net interest income from bank accounts, CDs and mutual funds; investment earnings, dividends and capital gains. It also includes gross profits from sales activities regularly carried on to the general public. Dues, sales to members, Fundraising for charitable projects including scholarships, scholarship fees assessed to members, bequests and contributions are not considered Unrelated Business Income as they relate directly to the purposes of Alpha Delta Kappa. Gross Profits = Total sales receipts minus cost of goods sold. Net Investment Income = Subtract expenses directly related such as investment advisor fees from investment income. Key Amount $1,000 of UBI Key Date The 15th day of the fifth month following the close of the fiscal year (5/31 = 10/15). Key Concepts 1. Subtract all expenses directly related to UBI (cost of goods, investment advisor fees, etc.) 2. If UBI equals $1,000 or more, you must file, even if the amount taxable is zero. 3. Subtract a $1,000 deduction from total UBI. 4. Net investment income may be set aside or designated to a state scholarship program or a 501(c)(3) entity to reduce tax liability. 5. Gross profits from sales may not be set aside. 6. Up to $1,000 of UBI may be used for operating expenses. 7. If required to file, consult a CPA who has other non-profit clients.

40 Chapter C-1 Tracking Summary State Year Chapter Name Attended Training Date Fiscal Year Ends If Interest + If Gross Non-Member Receipts = Ways $50,000 or & Means = more $1,000 or more $ $ Filed 990-N NOTE: Retain in state treasurer s file and send a copy to Headquarters by August

41 REPORT D-1 EZ SINGLE EVENT REPORTING FORM FOR DISTRICTS/AREA COUNCILS For use by districts/area councils having only one or two events per year. Complete a form D-1EZ for each event. The completed form is due to state treasurer four weeks following the event. Send this report, expense receipts and check (if applicable) to your state treasurer for inclusion in the state financial records. Fiscal Year to. District/Area Council Function State Date Receipts: Income Received From the Event $ Income Received for Dues/Assessments Other Income Received Total Income Received (Line A) $ Expenses: Food $ Services (Room Rental, AV, Tips, etc.) Program (Entertainment, Speaker, etc.) Printing and Postage Decorations and Favors Miscellaneous Deposit Proceeds in State: General Fund/District Altruistic Fund Scholarship Fund Total Expenses (Line B) $ Financial Results (Line A minus Line B) $ Submitted by: Phone Title 37 Date

42 REPORT D-1 DISTRICT/AREA COUNCIL ANNUAL CASH FLOW STATEMENT For use by districts/area councils that have extensive year-round activity. Complete and submit to state treasurer four weeks following the close of the state s fiscal year. Fiscal Year to. Due Date: District/Area Council Receipts (Revenues): District Dues $ District Fees Fundraising Altruistic Project Sales to Members Sales to Non-Members Contributions Scholarship Contributions Interest Other Transfers from Savings Flow Through* TOTAL RECEIPTS $ State *Flow Through accounts merely represent the receipt of revenue and the outflow of the associated expense, all within one account. Example 1: A small contribution to Charity X is a receipt and the check written to disburse the contribution is an expense for a net sum of zero. Example 2: Revenue is money collected from members for a meal and the expense is the associated check written to the restaurant for the meals, for a net sum of zero. Disbursements: Altruistic Contributions to Charity $ Altruistic Costs Professional Services Meeting Expenses Communication (Postage, Newsletter, etc.) Historian International Convention Regional Conference State Convention Other Meetings Membership Scholarship Courtesy Miscellaneous Transfers to Savings/Investments TOTAL DISBURSEMENTS $ TOTAL RECEIPTS LESS TOTAL DISBURSEMENTS $ Submitted by: Title Phone 38 Date

43 GUIDELINES FOR CHAPTER TREASURERS I. Receipts: A. Record cash and checks received in a ledger, identifying source (from whom) and item or service for which money was received. B. List each check separately on deposit ticket and deposit checks and cash in the bank. C. Record deposit on check register. II. Disbursements: A. Pay all invoices by check. Keep a receipt for each expenditure. B. An expense must be authorized by an approved budget. If not budgeted, an approved purchase order or expense voucher signed by the president should be issued authorizing the expenditure. C. Two persons should sign checks exceeding a designated amount (amount is determined by the chapter). Usually the treasurer and the president are the authorized check signers. III. Bank Statements: A. Use your chapter s EIN to open a bank account. B. Monthly bank statements must be reconciled to the checkbook register each month. C. Obtain the president s initials on each bank statement, indicating that she has reviewed the statement and verifies the reconciliation. D. Scholarship funds must be retained in a separate bank account. They cannot be commingled with the general fund. IV. Financial Reports: A. Treasurer s report or financial statement should be prepared in writing each month. B. An annual statement should be prepared. C. Form C-1 Annual Chapter Reporting Form and Audit should be prepared and sent to state treasurer with a copy to the audit committee by the deadline listed on the form. D. If the chapter s gross receipts are less than $50,000, electronically file Form 990-N e-postcard with the IRS at by the fifteenth day of the fifth month following the end of the chapter s fiscal year. E. If the chapter s adjusted receipts are $50,000 and/or Ways & Means - Sales to Non- Members and/or Interest equals $1,000 or more, submit a copy to International Headquarters as well as to your state treasurer. Headquarters will send the chapter treasurer forms C-2 and C-3 for completion. V. Audit of Treasurer s Books: A. Present the Audit Committee with all financial records so that they may do the following: 1. Verify the figures on the C-1 report. 2. Verify the C-1 report was mailed to the state treasurer by the deadline and a copy was forwarded to International Headquarters, if required (IV. D. above). 3. Determine all deposits have been accurately recorded. 4. Determine all disbursements have a receipt. 5. Verify that the checkbook/ledger balances monthly with the bank statement. 6. Review a list of outstanding checks. 7. Compare expenditures with budget. Review written explanation for any overages. 8. Review the written annual treasurer s report. B. Audit Committee submits written report to the chapter president. 39

44 Report C-1 ANNUAL CHAPTER REPORTING FORM AND AUDIT Report due to State Treasurer on Fiscal Year to Date of Audit Report (12 month period) State Chapter EIN# Beginning Balance (Cash Accounts) as of (date) $ (1) Receipts (Revenues): International Dues and Fees $ State Dues and Fees $ District Dues/Assessments $ Initiation Fees $ Membership Badge Costs $ Subtotal of Non-Chapter Receipts $ (2) Chapter Dues $ Fundraising (Gross Amounts) For Chapter Operations (Ways & Means) $ from Members $ $ from Non-Members $ For Altruism $ from Members $ $ from Non-Members $... Altruistic Contributions $ Meals/Luncheons $ Convention/Conferences/Meetings $ Interest $ Other $ Transfers from Savings $ All profit was used for altruism and scholarships or deposited in separate scholarship account: yes no Subtotal Chapter Receipts $ (3) TOTAL RECEIPTS (Add lines 1, 2 and 3) $ (4) Disbursements (Expenses): International Dues and Fees $ State Dues and Fees $ District Dues/Assessments $ Initiation Fees $ Membership Badge Costs $ Altruistic Donations to Charity $ Fundraising Costs: For Chapter Operations (combined) $... Member Non-Member For Altruistic Projects (combined) $... Member Non-Member Scholarships $ Courtesy $ Communications (postage, phone, printing) $ Officers Expenses $ Meals/Luncheons $ Conventions/Conferences/Meetings $ Membership $ Archives Book $ Yearbook $ Other $ Transfers to Savings $ TOTAL DISBURSEMENTS $ (5) TOTAL RECEIPTS LESS TOTAL DISBURSEMENTS: (Line 4 minus Line 5) $ (6) Has chapter filed 990-N e-postcard? yes no date Has chapter filed an IRS 990-EZ form in the previous two years? yes no If yes, date Year End Checking Account Balance as of $ Treasurer s Ledger Balance as of $ Signature of Treasurer Phone Signature of President Phone Signature of Audit Committee Chairman 40 NOTE: If Line 3 is $50,000 or more and/or Fundraising for Chapter Operations from Non-Members and/or interest earned is $1,000 or more, chapter treasurer must submit a copy of this form to: A K Headquarters, 1615 W 92nd St, Kansas City, MO as well as to your state treasurer.

45 Report C-2 Sample form: Headquarters will mail to chapters after receiving Report C-1, if more information is required. Alpha Delta Kappa Sorority Sa m p l e Ba l a n c e Sheet (Yo u m a y a d d lines to t h i s f o r m a s needed.) As of (Your Chapter Year End) ASSETS Cash and Investments Checking Account - Mercantile Bank $ 300 Savings Account - Mercantile Bank 500 Certificate of Deposit - Commerce Bank 1,000 Total Assets $ 1,800 LIABILITIES AND NET ASSETS Liabilities $ Net Assets 1,800 Total Liabilities and Net Assets $ 1, Net assets for a not-for-profit organization are the equivalent of equity for a for-profit organization. Most software packages use the term equity, however. As most states are on the cash basis, they will not record any liabilities. 2. Note that Total Assets must equal Total Liabilities and Net Assets to balance. 41

46 Report C-3 Sample form: Headquarters will mail to chapters after receiving Report C-1, if more information is required. Alpha Delta Kappa Sorority Three-Year Gross Receipts Calculation (You may add lines to this form as needed.) If the total under the Current Year column exceeds $50,000 or your chapter filed a 990 in either of the two previous years, complete the next two columns. Mail completed form to Headquarters along with your balance sheet (Report C-2) no later than. Your Chapter Year End State Chapter EIN Chapter Dues Current Year (See C-1, Chapter Receipts Section) One Year Previous to Current Year Two Years Previous to Current Year Ways & Means $ from Members Ways & Means $ from Non-Members Altruistic Contributions Meals/Luncheons Conventions/Conferences/Meetings Interest Other Receipts Transfer from Savings TOTAL Note: Current year is the most fully completed accounting period (a total of 12 months). 42

47 For Chapter Use Only. Do Not Mail. Report C-4 Alpha Delta Kappa Sorority Sa m p l e Bu d g e t (Yo u m a y a d d lines to t h i s f o r m a s needed.) For the 12 Months Ended (Your Chapter Year End) State Chapter EIN# Receipts (Revenues): Chapter Dues Fundraising (Gross Amounts) For Chapter Operations (Ways & Means) $ from Members $ from Non-Members For Altruism $ from Members $ from Non-Members Altruistic Contributions Meals/Luncheons Conventions/Conferences/Meetings Interest Receipts Transfer from Savings Total Receipts Disbursements (Expenses): Altruistic Donations to Charity Fundraising Costs: For Chapter Operations For Altruistic Projects Scholarships Courtesy Communications (postage, phone, printing) Officers Expenses Meals/Luncheons Conventions/Conferences/Meetings Membership Archives Book Yearbook Other Transfer to Savings Total Disbursements Total Receipts Less Total Disbursements 43 Current Year s Budget Prior Year s Actual Prior Year s Budget

48 FINANCIAL REPORTING INFORMATION Altruistic/Scholarship Fundraising: Sales to raise money for scholarships and/ or other charitable programs. All money must be used for the advertised purpose. Fundraising for scholarships and altruistic projects is not considered Unrelated Business Income. Ways and Means: Sales to raise money for the S/P/N or chapter operating/general account. Sales to non-members are Unrelated Business Income (UBI). Sales to members are not Unrelated Business Income (UBI). Unrelated Business Income (UBI) Gross profits from Ways and Means sales to NON-MEMBERS (Total sales receipts minus cost of goods sold) Net interest and investment earnings (Total interest or earnings minus investment fees) If UBI is $1,000 or more, consult a CPA to file a 990-T. A maximum of $1,000 of UBI may be used for operating/general expenses. Separate Scholarship Accounts Interest and net investment income may be designated to a separate scholarship account to reduce UBI tax liability. Interest earned in a separate scholarship account may not be transferred to the operating/general account. August

49 State and Chapter Record Retention Requirements President 1. Retain in Permanent Files: Charter (Fidelis Scroll, if Fidelis Chapter) Ceremonies Books Minutes of Meetings and Bylaws Proceedings of International Conventions (states only) Names of Initiated Members and Initiation Dates Written History Correspondence on any Legal Matters 2. Retain 4 years: Forms and Correspondence (for the current and immediate past biennia). Treasurer 1. Retain in Permanent Files: EIN Number (assigned by the Internal Revenue Service), any correspondence from the IRS, copy of any reports to the IRS, copy of correspondence from Headquarters regarding the IRS. Filed tax returns, including working papers. Audit reports and financial statements, cancelled checks for taxes, cash books. Financial ledgers and journals. 2. Retain 8 years: Bank reconciliations and bank statements 3. Retain 3 years: Petty cash vouchers, general correspondence, other cancelled checks, expense reports, paid bills and monthly trial balances. 45

50 WARNING!!! The IRS Will Revoke Your Chapter s Non-Profit Status Unless You File the 990-N e-postcard! Since 2008 the IRS has required all states and chapters to file an annual report. There are two categories for reporting/filing: 1. States and chapters with gross receipts of less than $50,000 will file an annual electronic notice, Form 990-N also known as the e-postcard; 2. States and chapters with gross receipts of $50,000 or more are required to file the more extensive Form 990 or 990-EZ. The 990-N (e-postcard) must be filed electronically. There is no paper form. If the chapter treasurer or chapter president does not have Internet access, she will need to use the Internet connection at a school, library or the home of another chapter member. Filing Deadline: The e-postcard is due every year by the 15th day of the fifth month after the close of your state or chapter s fiscal year. For example, if your fiscal year is June 1 through May 31, your e-postcard must be filed after May 31 and before October 15. If your fiscal year is July 1 through June 30, your e-postcard must be filed after June 30 and before November 15. Penalty: The IRS will revoke the tax-exempt status of a state or chapter who fails to meet the annual filing requirement for three consecutive years and possibly Alpha Delta Kappa s tax-exempt status. Required Information: Completing the e-postcard will require you to provide the following information: 1. Your state or chapter s EIN/TIN number. It should be in your permanent files but if not, it is available from Headquarters. 2. Tax year. The 12-month fiscal year used by your state or chapter (June 1- May 31 or any 12-month period you choose.) If you don t know your fiscal year, contact your state treasurer. 3. Organization s Legal Name and Mailing Address (The Alpha Delta Kappa Sorority, Inc., 1615 W 92nd St, Kansas City, MO 64114) 4. Any other names your chapter uses (e.g. Missouri Beta Chapter) 5. Name of principle officer (current chapter president) and Headquarters address 6. Organization s website address 7. Confirmation that your chapter s annual gross receipts are normally $50,000 or less. 8. If applicable, a statement that your chapter is going out of business. 46

51 How to File the 990-N (E-Postcard) Go to 1. The top of the screen should read e-postcard: file your electronic IRS Form 990-N a. Read the three steps. If you don t have your login ID from last year, click on the underlined part of Step 1. (If you do have it, click on the underlined part of Step 2.) 2. The top of the screen should read Request Login ID a. Read and click Next>> 3. The top of the screen should read Request Login ID a. Login ID Type Fill in box with Exempt Organization b. Organization EIN Type in your EIN c. Click on the print icon on your toolbar to print this screen d. Click Next>> 4. The top of the screen should read Request Login ID a. Create a password if you don t have one from previous years. Using your state abbreviation and chapter name is recommended. Example: ALBETAGAMMA is recommended for Alabama Beta Gamma b. Retype your password. c. Complete the rest of the screen with your name, your address and your phone number. d. Click on the print icon on the toolbar and then click Next 5. If done correctly, the top of the next screen will say Request Login ID Success. a. Click on the print icon on the toolbar b. Close out of the program and wait for an from [email protected] 6. The should arrive within 15 minutes. Read and follow the directions in the , click on the link and proceed. 7. The top of the screen should read Activate Login ID a. Type in the password you created in Step 4 a. b. Click on the print icon on the toolbar and then click Next 8. The top of the screen should read Activate Login ID (Success) a. Click on the print icon on the toolbar and then click Create your Form 990-N (e-postcard) Now 9. The top of the screen should read Electronic Notice Form 990-N (e-postcard) Organization Information. a. Line A Type in your chapter s fiscal year (12 month tax period). The box may be filled and you will not be able to change it. If the fiscal year is not correct, see item 12 in these instructions. b. Line B Click on the arrow in the top box and select No. and in the bottom box click on the arrow and select Yes c. Line C Line 1 The box will say ALPHA DELTA KAPPA SORORITY. Leave the second box in Line 2 blank. d. Line D Type in your EIN number, using the hyphen after the first two digits e. Click on the print icon on the toolbar and then click Next Page 10. This screen is asking for the organization address and principal officer information. a. Click on Save Changes box 47

52 b. In the first box, type your state and chapter. Example: Iowa Alpha Lambda Chapter c. Skip the second box. d. In Care of Name box, type in your name e. United States should appear in the next box. f. Line 1 of mailing address, type in 1615 W 92nd Street g. Skip the next box. h. In City or town box, type Kansas City i. In State box, type in Missouri j. In Zip Code box, type in k. In Line E, type in l. Line F, click on box arrow and select Person m. In Person Name box, type in your current chapter president s name n. In the following address boxes, repeat the information exactly as it appears in the section above, providing Headquarters full address. o. Click on the print icon on the toolbar and then click Save Changes and finally, click on Submit Filing to IRS. 11. This screen will say Form 990-N (e-postcard) Submitted a. Click on the print icon on the toolbar and then click on Go To Filing Status Page. b. Click on the print icon on the toolbar and then exit the program. c. Within 30 minutes you should receive an from the IRS, indicating whether your e-postcard was accepted or rejected. Print this confirmation. If accepted, you are finished for the year. Notify your state treasurer that your 990-N has been accepted by the IRS and file all copies of the screen prints and s in your permanent file. If rejected, the will contain instructions on how to correct the problem. 12. If your tax period (See Item 9.) was incorrect, there is one more step to the process. You must write the IRS a letter stating your name and chapter office, your chapter name and EIN number and say that in filing the 990-N the incorrect fiscal year was listed for your chapter and request that the fiscal year be changed to June 1 to May 31 or whatever 12-month period your chapter uses. Send the letter to: IRS ATTN: EO Entity MS Ogden, UT Or FAX it to (801) Questions: If you have questions, call Headquarters at If you have technical problems, call the IRS service provider toll free at

PTA Treasurer s Training. Being Accountable and Transparent

PTA Treasurer s Training Being Accountable and Transparent Duties of the PTA Treasurer Maintain accurate, detailed financial records Help prepare the PTA Budget Receive & disburse funds Present a Treasurer

PTA Treasurer s Training Being Accountable and Transparent Duties of the PTA Treasurer Maintain accurate, detailed financial records Help prepare the PTA Budget Receive & disburse funds Present a Treasurer

Instructions for Form 990-N and 990-EZ. For Additional Information Contact [email protected]

Instructions for Form 990-N and 990-EZ For Additional Information Contact [email protected] Table of Contents Frequently Asked Questions... 2 E-Postcard 990 N... 4 Required Information... 4 Form 990-N: Step

Instructions for Form 990-N and 990-EZ For Additional Information Contact [email protected] Table of Contents Frequently Asked Questions... 2 E-Postcard 990 N... 4 Required Information... 4 Form 990-N: Step

Burleson Independent School District

Burleson Independent School District PTO/Booster Club Guidelines 11/1/2014 The following guidelines are to be used for student support activity groups (Parent Teacher Organizations, Booster Clubs, etc.)

Burleson Independent School District PTO/Booster Club Guidelines 11/1/2014 The following guidelines are to be used for student support activity groups (Parent Teacher Organizations, Booster Clubs, etc.)

INTRODUCTION RESPONSIBILITIES OF THE TREASURER

TREASURER 2014-2015 INTRODUCTION The treasurer is the authorized custodian of the funds of the association. However, the president, who bears full responsibility for the affairs of the unit, and board

TREASURER 2014-2015 INTRODUCTION The treasurer is the authorized custodian of the funds of the association. However, the president, who bears full responsibility for the affairs of the unit, and board

Associates of Vietnam Veterans of America, Inc.

I. ACCOUNTING: Policy and Procedures A. PURPOSE: to establish a policy and a set of procedures for the proper handling, recording, reporting, and safeguarding of the Corporation s assets. B. RESPONSIBILITY:

I. ACCOUNTING: Policy and Procedures A. PURPOSE: to establish a policy and a set of procedures for the proper handling, recording, reporting, and safeguarding of the Corporation s assets. B. RESPONSIBILITY:

Note: Page 1 of 6 Instructions for Form CHAR500 (rev. 2010)

") New York State Department of Law (Office of the Attorney General) Charities Bureau - Registration Section Instructions for Form CHAR500 Annual Filing for Charitable Organizations www.charitiesnys.com Contents:

New York State Department of Law (Office of the Attorney General) Charities Bureau - Registration Section Instructions for Form CHAR500 Annual Filing for Charitable Organizations www.charitiesnys.com Contents:

Form 1023-EZ Streamlined Application for Reinstatement of Tax-Exempt Status For Organizations within 15 months of Revocation

Form 1023-EZ Streamlined Application for Reinstatement of Tax-Exempt Status For Organizations within 15 months of Revocation Dear PTA Leader: The IRS has released their new Form 1023-EZ to facilitate the

Form 1023-EZ Streamlined Application for Reinstatement of Tax-Exempt Status For Organizations within 15 months of Revocation Dear PTA Leader: The IRS has released their new Form 1023-EZ to facilitate the

2012-2013 PTA Money Matters Quick-Reference Guide Table of Contents. Welcome... 4

1 Table of Contents Table of Contents Welcome... 4 The PTA Treasurer... 5 First Steps... 5 Duties of the Treasurer... 6 Contents of the Treasurer s File... 7 Records Retention Schedule... 8 Treasurer s

1 Table of Contents Table of Contents Welcome... 4 The PTA Treasurer... 5 First Steps... 5 Duties of the Treasurer... 6 Contents of the Treasurer s File... 7 Records Retention Schedule... 8 Treasurer s

UNIT TREASURER DUTIES GLENDALE COUNCIL PTA

UNIT TREASURER DUTIES GLENDALE COUNCIL PTA Usha Archer, Council Treasurer 2011 Topics Mission Statement Board Responsibilities Sources of information Duties & Responsibilities Treasurers File Check Signers

UNIT TREASURER DUTIES GLENDALE COUNCIL PTA Usha Archer, Council Treasurer 2011 Topics Mission Statement Board Responsibilities Sources of information Duties & Responsibilities Treasurers File Check Signers

Income Tax Issues Affecting Small Nonprofit Organizations