Product Marketplace Comparison Report

|

|

|

- Collin Hudson

- 8 years ago

- Views:

Transcription

1 Product Marketplace Comparison Report Ownership Insured Carrier Policy Number Type of Policy Sample Trust Owned Bill Tall Lincoln National Indexed Life Prepared By: Michael D Pepe CLU The TOLI Group 2035 Crocker Road Suite 105 Westlake OH mpepe@toligroup.com P: F: /03/2014 Disclosure We believe the sources to be reliable, however, the accuracy and completeness of the information is not guaranteed. In the event of any discrepancy, the carrier's information shall prevail. Performance data represents past performance and does not guarantee future results. The values represented in this report may not reflect the true original cost of the client's initial investment. Calculations and data provided should not be relied upon for tax purposes, use original confirmations and carrier statements instead. The Information contained in these reports is collected from sources believed to be reliable, however the accuracy and completeness of the information is not guaranteed. Always rely on statements you receive directly from the carriers, whose valuation shall prevail in the event of any discrepancy. If you have any questions regarding your report, please call your representative.

2 TABLE OF CONTENTS 1. Policy Summary 2. Performance Guidelines 3. Policy Information 4. Original Structure 5. Current Structure 6. Life Expectancy Analysis 7. Carrier Analysis 8. Premium Gift Analysis 9. Executive Analysis 10. Policy Objectives 11. Policy Design 12. Product Alternatives 13. Product Comparison Analysis 14. Resources Used in This Analysis

3 POLICY SUMMARY Insured Carrier Policy Number Type of Policy Bill Tall Lincoln National Indexed Life This policy analysis has been created to determine the strengths and weaknesses of this life insurance policy based upon your goals, objectives, risk tolerance and personal financial situation. The goal of this report is to provide objective and quantifiable information regarding the existing policy. The analysis is based upon the objective information that has been gathered from the insurance company, your advisors and/or the responses to the TOLI Vault Design Guidelines and Risk Tolerance Questionnaire. POLICY MONITORING GUIDELINES Guideline Desired Acceptable Range Unacceptable Lapse Age Death Benefit $7,000, $6,999, Premium $35, $35, Policy Performance 7.50% 7.49% % 6.74% Carrier Performance Policy Type Indexed Life Carrier Lincoln National LAPSE AGE Age at which coverage may no longer be in force 54 Policy # DEATH BENEFIT The amount of coverage in force $7,000, PREMIUMS The amount and frequency of policy funding $35, POLICY PERFORMANCE Earnings rate of the policy 5.00% CARRIER PERFORMANCE Financial strength and rating of the insurance company 91 Color Key: The performance is as desired -guideline parameters are being met The performance is on track -desired guideline parameters are within the acceptable range The performance is lagging -desired guideline parameters are unacceptable

4 POLICY MONITORING SPECIFICATIONS Insured Lapse Age Death Benefit Premium Policy Performance Carrier Performance Bill Tall POLICY INFORMATION Policy Type IndexedLife Product Name Protector Insurance Carrier Lincoln National STAR Ranking 3 Comdex Rating 91 Policy Number Policy Issue Date 10/23/2009 Policy Anniversary Date 10/23 Owner Sample Trust Owned Trustee Sample Trustee Beneficiary Benny Hill Beneficiary Tony Russo ORIGINAL STRUCTURE Coverage Length Requirement 100 Original Premium $35, Was this policy issued with 1035 exchange money Yes If Yes, How much was the 1035 exchange amount $500, Was this policy issue with a first year unscheduled premium Yes If Yes, How much was the unscheduled premium amount $10, Original Death Benefit $6,000, Guaranteed Credited Interest Rate 2.00% Original Projected Interest Rate 7.50% Guaranteed Lapse Age 90 Policy Riders Estate Liquidity CURRENT STRUCTURE Current Premium $35, Total Premiums Paid $70, Total Current Cash Value $530, Current Cash Surrender Value $450, Cost Basis $575, Total Current Death Benefit $7,000, Current Credited Interest Rate 5.00% Projected Lapse Age 54 Total Amount of Outstanding Loan $0.00 Market Cap 12.00% Index being used S&P 500 Is this Policy a MEC No

5 Is this Policy Collaterally Assigned No Is this Policy part of a Split Dollar Arrangement No Is the Premium for this Policy Premium Financed Yes Loan Number

6 LIFE EXPECTANCY ANALYSIS Client Data Insured Bill Tall Sex M Smoker Y Policy Rating Classification Preferred Current Age 50 Life Expectancy (YEARS) CLIENT(1) Policy # Policy Lapse Age-Guaranteed Basis 90 Probability of Survival at this age 27.16% Policy # Policy Lapse Age-Projected Basis 54 Probability of Survival at this age 98.48% All values are derived from the 2008 VBT Mortality Table

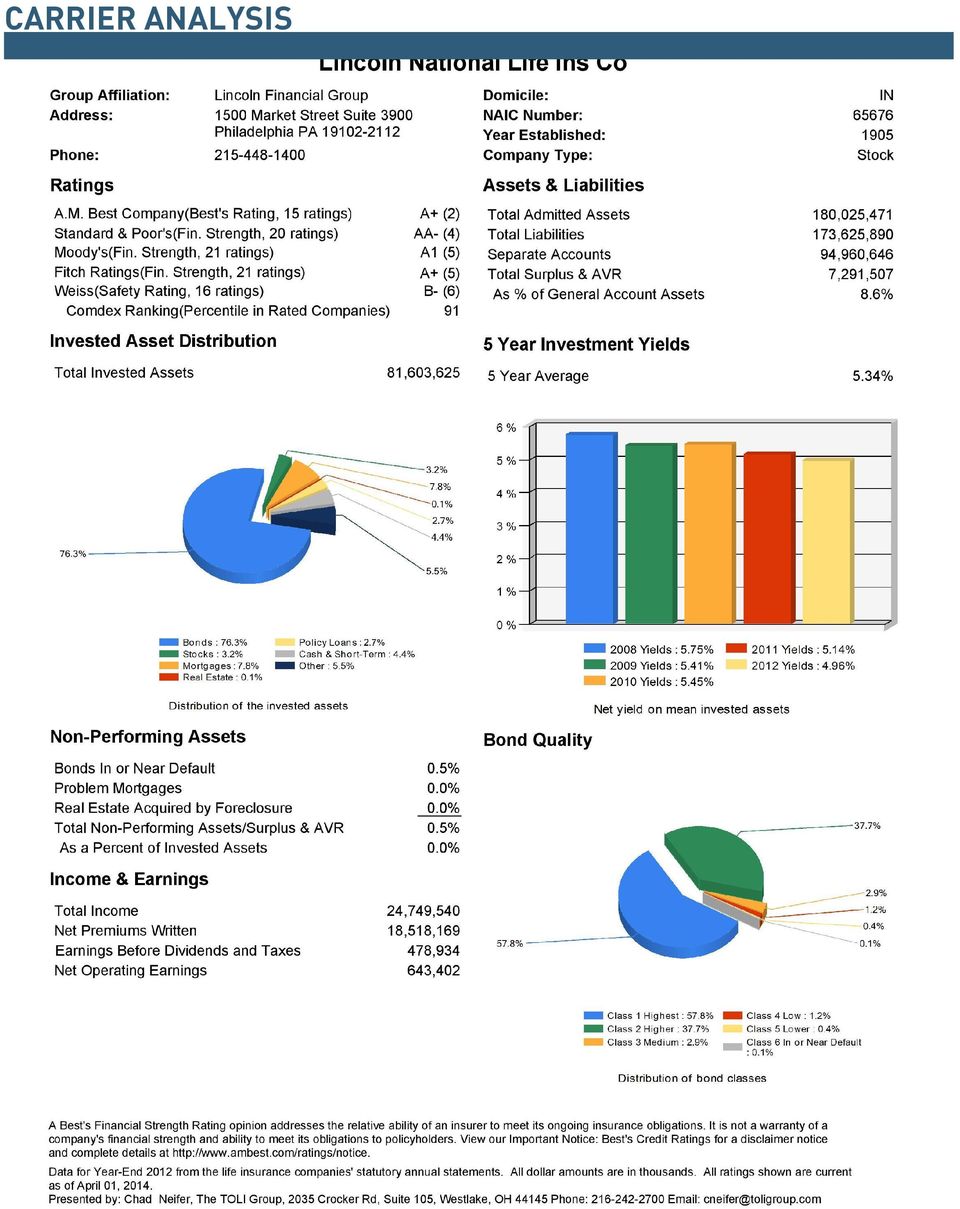

7 CARRIER ANALYSIS

8 EXECUTIVE ANALYSIS Current Product will not achieve your coverage duration goal and the credit rate is below your unacceptable range. PERFORMANCE TRACKING Death Benefit Year Projected Actual +/-% 2014 $6,000,000 $7,000, $7,000,000 $6,000, $7,000,000 $6,000, Cash Value Year Projected Actual +/-% 2014 $0 $530, $0 $530, $0 $530, indicates imported from carrier Premium Projected Actual +/-% $35,000 $35, $35,000 $35, $35,000 $35, Surrender Value Projected Actual +/-% $0 $450, $0 $450, $0 $450, Lapse Age Projected Actual +/-% Credit Rate Projected Actual +/-% Color Key: > 94%: The performance is on track -guideline parameters are being met 94% - 80%: The performance is lagging -monitoring is suggested < 80%: The performance is inadequate -review is recommended Data is incomplete- information is needed

9 POLICY MONITORING GUIDELINES Guideline Desired Acceptable Range Unacceptable Lapse Age Death Benefit $7,000, $6,999, Premium $35, $35, Policy Performance 7.50% 7.49% % 6.74% Carrier Performance Policy Type Indexed Life Carrier Lincoln National LAPSE AGE Age at which coverage may no longer be in force 54 Policy # DEATH BENEFIT The amount of coverage in force $7,000, PREMIUMS The amount and frequency of policy funding $35, POLICY PERFORMANCE Earnings rate of the policy 5.00% CARRIER PERFORMANCE Financial strength and rating of the insurance company 91 Color Key: The performance is as desired -guideline parameters are being met The performance is on track -desired guideline parameters are within the acceptable range The performance is lagging -desired guideline parameters are unacceptable Policy meets some objectives

10 PRODUCT ANALYSIS Product Type: Indexed Life Lowest Premium Lowest Premium Payments Policy Flexibility Ability to alter premium or death benefit Coverage Duration Guarantees Guaranteed Length of Coverage Premium Guarantees Guaranteed Premium Payments Cash Accumulation Building Substantial Cash Value within the Policy Color Key: The Product Type has the desired features The Product Type can produce the desired features The Product Type does not have the desired features Equity Index Universal Life Advantages Disadvantages Not currently registered with the SEC even though returns are Premium flexibility based upon the returns of stock market indices Adjustable death benefit Growth is driven by derivatives Credited return excludes any dividends, which have Unbundled product structure where historically made up 40% of the total return of the S&P 500 pricing components are disclosed Index May require a substantial waiting period to benefit from growth Carrier can limit upside potential through manipulation of caps and participation rates Cash values subject to claims of insurance company creditors Policy meets some design parameters

11 PRODUCT ALTERNATIVES Universal Life with Secondary Guarantees Advantages Disadvantages Lowest guaranteed premium Generally little or no cash values due to high expense loads Premium flexibility, but changes If carrier solvency concerns arise, little cash value available to assist may impact guarantees in a Section 1035 exchange to a different carrier Little upside potential from non-guaranteed elements Cash values subject to claims of insurance company creditors Not available at older ages Variable Universal Life with Guarantees Advantages All expenses are described in prospectus Client controls investment direction of cash values Upside performance potential could be used to abbreviate premium payments, increase death benefit or allow access to policy cash values Policy cash values held in separate account give maximum protection with carrier insolvency Guarantees provide assurance of death benefit coverage Disadvantages Client at risk for having to pay a higher premium Volatility of equities may impact insurance expenses due to changes in net amount at risk Requires client sophistication and commitment to policy management Guarantees are typically more expensive than Universal Life

12 PRODUCT COMPARISON ANALYSIS Variable Universal Life Sample Office Mike Black 02/23/1960 Table D(4) Death Benefit Requirement $1,000, Exchange $35, Premium Payments To Age Coverage Needed To Age 100 No Lapse Protection To Age 100 Carrier Diversification Is Not A Concern Acceptable Comdex Rating Range Premium Comparison Carrier Amount A.M. Best S & P Moody's Fitch Comdex MetLife VUL-G John Hancock VUL-G New York Life VUL-G MassMutual VUL-G Minnesota Life VUL-G $9, A+ AA- Aa3 AA- 95 $10, A+ AA- A1 AA- 93 $11, A++ AA+ Aaa AAA 100 $11, A++ AA+ Aa2 AA+ 98 $12, A+ A+ Aa3 AA- 92

13 RESOURCES USED IN THIS ANALYSIS In reviewing your insurance policy's performance and carrier strength, the following resources were used: - The TOLI Vault - policy monitoring and management software - Vital Signs - key financial reports and ratings from major rating agencies AM Best, Moody's, Fitch, and Standards and Poor's - Life Expectancy Analysis- utilizing the 2008 VBT Mortality Table

InsuranceIQ Bank & Trust. Prepared for: Gregory & Patricia Toppins Insurance Trust Dated 3/15/2007. Policy Owner: InsuranceIQ#: 0001-00010-01

Date Completed: 3/22/2013 Prepared for: InsuranceIQ Bank & Trust Policy Owner: InsuranceIQ#: 0001-00010-01 Prepared for: InsuranceIQ Bank & Trust Branch Code: West 1st Street External Trustee(s): Trustee:

Date Completed: 3/22/2013 Prepared for: InsuranceIQ Bank & Trust Policy Owner: InsuranceIQ#: 0001-00010-01 Prepared for: InsuranceIQ Bank & Trust Branch Code: West 1st Street External Trustee(s): Trustee:

The Life Insurance Design Questionnaire

The Life Insurance Design Questionnaire PREPARED FOR: J OHN Q. SAMPLE PREPARED BY: T HE O NEILL C OMPANY WWW.THEONEILLCO.COM [P] 949.586.8001 [F] 949.454.6543 The Life Insurance Design Questionnaire INTRODUCTION

The Life Insurance Design Questionnaire PREPARED FOR: J OHN Q. SAMPLE PREPARED BY: T HE O NEILL C OMPANY WWW.THEONEILLCO.COM [P] 949.586.8001 [F] 949.454.6543 The Life Insurance Design Questionnaire INTRODUCTION

Life Insurance Review Using Legacy Advantage SUL Insurance Policy

Using Legacy Advantage SUL Insurance Policy Supplemental Illustration Prepared by: MetLife Agent 200 Park Ave. New York, NY 10166 Insurance Products: Not A Deposit Not FDIC-Insured Not Insured By Any Federal

Using Legacy Advantage SUL Insurance Policy Supplemental Illustration Prepared by: MetLife Agent 200 Park Ave. New York, NY 10166 Insurance Products: Not A Deposit Not FDIC-Insured Not Insured By Any Federal

Sample Irrevocable Life Insurance Trust Investment Policy Statement

Sample Irrevocable Insurance Trust Investment Policy Statement Sample Investment Policy Statement This sample has been prepared to show how credible TOLI-specific policy evaluation criteria can be established

Sample Irrevocable Insurance Trust Investment Policy Statement Sample Investment Policy Statement This sample has been prepared to show how credible TOLI-specific policy evaluation criteria can be established

THE CONSTRUCTION OF A SURVIVORSHIP LIFE INSURANCE POLICY

THE CONSTRUCTION OF A SURVIVORSHIP LIFE INSURANCE POLICY PERTINENT INFORMATION Mr. and Mrs. Kugler are considering $1,000,000 of life insurance to provide estate liquidity at the survivor s death to cover

THE CONSTRUCTION OF A SURVIVORSHIP LIFE INSURANCE POLICY PERTINENT INFORMATION Mr. and Mrs. Kugler are considering $1,000,000 of life insurance to provide estate liquidity at the survivor s death to cover

Life Insurance Review

Supplemental Illustration Prepared by: MetLife Agent Financial Services Representative 200 Park Ave. New York, NY 10166 Insurance Products: Not A Deposit Not FDIC-Insured Not Insured By Any Federal Government

Supplemental Illustration Prepared by: MetLife Agent Financial Services Representative 200 Park Ave. New York, NY 10166 Insurance Products: Not A Deposit Not FDIC-Insured Not Insured By Any Federal Government

Whole Life Legacy 10 Pay Basic Life Insurance Illustration

Whole Life Legacy 10 Pay Basic Prepared for: d Client Male, Age 5 Presented by: Michael Fliegelman CLU, ChFC, AEP, RFC Independent Insurance And Financial Consulting 5 Harborfields Ct Greenlawn, NY 11740

Whole Life Legacy 10 Pay Basic Prepared for: d Client Male, Age 5 Presented by: Michael Fliegelman CLU, ChFC, AEP, RFC Independent Insurance And Financial Consulting 5 Harborfields Ct Greenlawn, NY 11740

What You Should Know About Buying. Life Insurance

What You Should Know About Buying Life Insurance Life insurance is the foundation of financial security for you and your family. It protects your financial resources against the uncertainties of life so

What You Should Know About Buying Life Insurance Life insurance is the foundation of financial security for you and your family. It protects your financial resources against the uncertainties of life so

Strength. Product. Relationships

Columbus Life Insurance Company Strength. Product. Relationships For financial professional use only Slide 1 Columbus Life Insurance Company, Cincinnati, Ohio CL 5.XXX (09/12) is licensed in the District

Columbus Life Insurance Company Strength. Product. Relationships For financial professional use only Slide 1 Columbus Life Insurance Company, Cincinnati, Ohio CL 5.XXX (09/12) is licensed in the District

A Guide to Life Insurance for Small Business SUN LIFE FINANCIAL

A Guide to Life Insurance for Small Business SUN LIFE FINANCIAL For a small business owner, group life insurance and qualified plans may not be adequate to protect the business from unforeseen risks or

A Guide to Life Insurance for Small Business SUN LIFE FINANCIAL For a small business owner, group life insurance and qualified plans may not be adequate to protect the business from unforeseen risks or

The Life Insurance Design Questionnaire

HOW TO MATCH YOUR LIFE INSURANCE WITH YOUR NEEDS The Life Insurance Design Questionnaire is an assessment tool that enables your insurance advisor to assist you in the selection, design and purchase of

HOW TO MATCH YOUR LIFE INSURANCE WITH YOUR NEEDS The Life Insurance Design Questionnaire is an assessment tool that enables your insurance advisor to assist you in the selection, design and purchase of

Key Person Insurance. Protecting Your Business From The Loss Of Key Employees. Place Image Here. Prepared For: Valued Company. Presented By:... Tel.:.

Key Person Insurance Protecting Your Business From The Loss Of Key Employees Place Image Here Prepared For: d Company Presented By:.... Tel.:. Insurance products are issued by: Insurance John Hancock products

Key Person Insurance Protecting Your Business From The Loss Of Key Employees Place Image Here Prepared For: d Company Presented By:.... Tel.:. Insurance products are issued by: Insurance John Hancock products

What is included in the life insurance review?

What is the importance of life insurance? Life insurance is a financial instrument owned by many individuals, businesses, and purchased as part of estate plans. It is an asset that is included within a

What is the importance of life insurance? Life insurance is a financial instrument owned by many individuals, businesses, and purchased as part of estate plans. It is an asset that is included within a

Life Insurance Review

Life Insurance Review A thorough evaluation of your life insurance portfolio RELATIONSHIP MANAGEMENT EXPERIENCE PARTNERSHIPS CLIENTSOLUTIONS Purpose Our goal is to provide an objective life insurance policy

Life Insurance Review A thorough evaluation of your life insurance portfolio RELATIONSHIP MANAGEMENT EXPERIENCE PARTNERSHIPS CLIENTSOLUTIONS Purpose Our goal is to provide an objective life insurance policy

Flexible Premium Adjustable Life Insurance Policy Illustration

Flexible Premium Adjustable Life Insurance Policy Illustration Prepared for: d Client Prepared by: Sample Sample MetLife 11225 N Community House Rd Charlotte, North Carolina, 28202 Tel: 5555555555 MetLife

Flexible Premium Adjustable Life Insurance Policy Illustration Prepared for: d Client Prepared by: Sample Sample MetLife 11225 N Community House Rd Charlotte, North Carolina, 28202 Tel: 5555555555 MetLife

Types of Life Insurance Products

Types of Life Insurance Products Page 1 of 16, see disclaimer on final page Table of Contents Term Life Insurance...3 Who should buy term life insurance?...3 Advantages of term life insurance... 3 Disadvantages

Types of Life Insurance Products Page 1 of 16, see disclaimer on final page Table of Contents Term Life Insurance...3 Who should buy term life insurance?...3 Advantages of term life insurance... 3 Disadvantages

A guide to buying insurance

A guide to buying insurance What you should know before you buy Is life insurance right for you? Life insurance policies are designed for people who: Want to replace income that is lost due to death Seek

A guide to buying insurance What you should know before you buy Is life insurance right for you? Life insurance policies are designed for people who: Want to replace income that is lost due to death Seek

PROTECTION PROTECTION SIUL. The pacesetter in affordable, secure protection. For two. CONSUMER GUIDE IM4156CG

CONSUMER GUIDE PROTECTION PROTECTION SIUL The pacesetter in affordable, secure protection. For two. IM4156CG JOHN HANCOCK LIFE INSURANCE COMPANY (U.S.A.) JOHN HANCOCK LIFE INSURANCE COMPANY OF NEW YORK

CONSUMER GUIDE PROTECTION PROTECTION SIUL The pacesetter in affordable, secure protection. For two. IM4156CG JOHN HANCOCK LIFE INSURANCE COMPANY (U.S.A.) JOHN HANCOCK LIFE INSURANCE COMPANY OF NEW YORK

LIFE INSURANCE THE DIVIDEND DIFFERENCE. Adding Value to Your Whole Life Insurance Policy INVEST INSURE RETIRE

LIFE INSURANCE THE DIVIDEND DIFFERENCE Adding Value to Your Whole Life Insurance Policy INVEST INSURE RETIRE NOT A BANK OR A CREDIT UNION DEPOSIT OR OBLIGATION NOT FDIC OR NCUA-INSURED NOT INSURED BY ANY

LIFE INSURANCE THE DIVIDEND DIFFERENCE Adding Value to Your Whole Life Insurance Policy INVEST INSURE RETIRE NOT A BANK OR A CREDIT UNION DEPOSIT OR OBLIGATION NOT FDIC OR NCUA-INSURED NOT INSURED BY ANY

White Paper Equity Indexed Universal Life Insurance

White Paper www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

White Paper www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

Your guide to Canada Life s participating life insurance. Estate Achiever Wealth Achiever

Your guide to Canada Life s participating life insurance Estate Achiever Wealth Achiever This guide provides an overview of key features of participating life insurance products offered by Canada Life.

Your guide to Canada Life s participating life insurance Estate Achiever Wealth Achiever This guide provides an overview of key features of participating life insurance products offered by Canada Life.

Understanding Life Insurance: A Lesson in Life Insurance

Understanding Life : A Lesson in Life If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Questions 3 Types of Term 4 Term Variations

Understanding Life : A Lesson in Life If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Questions 3 Types of Term 4 Term Variations

Like all other permanent (cash value) policies, a whole life policy contains the following features:

policies, a whole life policy contains the following features:") Whole Life What is it? Permanent (cash value) life insurance Whole life insurance is called permanent protection, meaning the coverage (and possibly the premiums) lasts for your entire (whole) life, as

Whole Life What is it? Permanent (cash value) life insurance Whole life insurance is called permanent protection, meaning the coverage (and possibly the premiums) lasts for your entire (whole) life, as

Replacement Questionnaire (RQ)* A Policy Replacement Evaluation Form

* A Policy Replacement Evaluation Form") Replacement Questionnaire (RQ)* A Policy Replacement Evaluation Form Replacing an existing life insurance policy with a new one generally is not in the policyholder s best interest. New sales loads and

Replacement Questionnaire (RQ)* A Policy Replacement Evaluation Form Replacing an existing life insurance policy with a new one generally is not in the policyholder s best interest. New sales loads and

Life Insurance Choices - An Introduction to the Various Options

Life Insurance Choices - An Introduction to the Various Options Gary T. Bottoms, CLU, ChFC gbottoms@thebottomsgroup.com www.thebottomsgroup.com Two Important Questions Once a need is established for cash

Life Insurance Choices - An Introduction to the Various Options Gary T. Bottoms, CLU, ChFC gbottoms@thebottomsgroup.com www.thebottomsgroup.com Two Important Questions Once a need is established for cash

Insurance. Survivorship Life. Insurance. The Company You Keep

Insurance Survivorship Life Insurance The Company You Keep Permanent Life Insurance Protection for Two People You ve built a legacy, but who will be the recipients your heirs or the IRS? 1 Now is the time

Insurance Survivorship Life Insurance The Company You Keep Permanent Life Insurance Protection for Two People You ve built a legacy, but who will be the recipients your heirs or the IRS? 1 Now is the time

Thursday, 12 November 2015 WRM# 15-42

Thursday, 12 November 2015 WRM# 15-42 The WRMarketplace is created exclusively for AALU Members by the AALU staff and Greenberg Traurig, one of the nation s leading tax and wealth management law firms.

Thursday, 12 November 2015 WRM# 15-42 The WRMarketplace is created exclusively for AALU Members by the AALU staff and Greenberg Traurig, one of the nation s leading tax and wealth management law firms.

Understanding Life Insurance

Understanding Life Insurance A Lesson in Traditional and Indexed Life Insurance 2012 VSA, LP Valid only if used prior to January 1, 2013. The information, general principles and conclusions presented in

Understanding Life Insurance A Lesson in Traditional and Indexed Life Insurance 2012 VSA, LP Valid only if used prior to January 1, 2013. The information, general principles and conclusions presented in

Flexible Premium Adjustable Life Insurance Policy Illustration

Flexible Premium Adjustable Life Insurance Policy Illustration Prepared for: d Client Prepared by: Illustration Desk 2801 Townsgate Rd. Suite 350 Westlake Village, California, 91361 Tel: 800-350-2019 License

Flexible Premium Adjustable Life Insurance Policy Illustration Prepared for: d Client Prepared by: Illustration Desk 2801 Townsgate Rd. Suite 350 Westlake Village, California, 91361 Tel: 800-350-2019 License

John and Katie Winters

John and Katie Winters 360 WEALTH MANAGEMENT -LIFE INS. ASSET December 03, 2012 PREPARED BY: William Wilkinson, CFP ChFC, CLU, CASL, AIF 28170 N. Alma School Parkway Suite 208 Scottsdale, AZ 85262 (480)

John and Katie Winters 360 WEALTH MANAGEMENT -LIFE INS. ASSET December 03, 2012 PREPARED BY: William Wilkinson, CFP ChFC, CLU, CASL, AIF 28170 N. Alma School Parkway Suite 208 Scottsdale, AZ 85262 (480)

An Assessment of No Lapse Guarantee Products and Alternatives. Prepared and Researched by

An Assessment of No Lapse Guarantee Products and Alternatives Prepared and Researched by No Lapse Guarantee (NLG) products continue to be very popular with clients, primarily for their low cost and guaranteed

An Assessment of No Lapse Guarantee Products and Alternatives Prepared and Researched by No Lapse Guarantee (NLG) products continue to be very popular with clients, primarily for their low cost and guaranteed

Marsh Private Client Life Insurance Services 10 REASONS TO REVIEW YOUR LIFE INSURANCE TODAY

Marsh Private Client Life Insurance Services 10 REASONS TO REVIEW YOUR LIFE INSURANCE TODAY 1. HAVE YOUR NEEDS CHANGED? Is the original reason you purchased your policies still applicable? Often, the need

Marsh Private Client Life Insurance Services 10 REASONS TO REVIEW YOUR LIFE INSURANCE TODAY 1. HAVE YOUR NEEDS CHANGED? Is the original reason you purchased your policies still applicable? Often, the need

Leverage your accounts receivable. Client overview

Leverage your accounts receivable Client overview Unlock your accounts receivable These strategies funded by life insurance can help professionals like you: Accumulate life insurance cash values in a tax-advantaged

Leverage your accounts receivable Client overview Unlock your accounts receivable These strategies funded by life insurance can help professionals like you: Accumulate life insurance cash values in a tax-advantaged

Nationwide YourLife Survivorship VUL. Product guide. Everyone could use a little balance

Nationwide YourLife Survivorship VUL Product guide Everyone could use a little balance Balance protection and growth potential You like the idea of leaving your family a legacy one day. If you have your

Nationwide YourLife Survivorship VUL Product guide Everyone could use a little balance Balance protection and growth potential You like the idea of leaving your family a legacy one day. If you have your

Advanced Markets Success Strategy Life Insurance in Retirement Planning Plus

Success Strategy Life Insurance in Retirement Planning Plus Life insurance protection is the foundation of a family s future, providing cash to: replace income for surviving family, pay off family debt,

Success Strategy Life Insurance in Retirement Planning Plus Life insurance protection is the foundation of a family s future, providing cash to: replace income for surviving family, pay off family debt,

through life insurance strategies

through life insurance strategies T he purchase of a life insurance policy should go through the same careful analysis that goes into making any investment decision. After a careful examination of your

through life insurance strategies T he purchase of a life insurance policy should go through the same careful analysis that goes into making any investment decision. After a careful examination of your

PolicyEvaluationProgram

program analysis Prepared for: Prepared by: Date: Joseph Client John Producer 01/07/2009 Attach your business card here. Crump Life Insurance Services us not affiliates with the Principal Financial Group

program analysis Prepared for: Prepared by: Date: Joseph Client John Producer 01/07/2009 Attach your business card here. Crump Life Insurance Services us not affiliates with the Principal Financial Group

How to Choose a Life Insurance Company

How to Choose a Life Insurance Company A Guide through Financial Data and Industry Information The Guardian Life Insurance Company of America New York, NY 10004-4025 Table of Contents Page 1. Mutuality...

How to Choose a Life Insurance Company A Guide through Financial Data and Industry Information The Guardian Life Insurance Company of America New York, NY 10004-4025 Table of Contents Page 1. Mutuality...

Private Placement Life Insurance

Private Placement Life Insurance Robert W. Chesner, Jr. Leslie C. Giordani 100 CONGRESS AVENUE, SUITE 1440 AUSTIN, TEXAS 78701 phone 512.767.7100 fax 512.767.7101 WWW.GSRP.COM 2009 2015 Giordani, Swanger,

Private Placement Life Insurance Robert W. Chesner, Jr. Leslie C. Giordani 100 CONGRESS AVENUE, SUITE 1440 AUSTIN, TEXAS 78701 phone 512.767.7100 fax 512.767.7101 WWW.GSRP.COM 2009 2015 Giordani, Swanger,

The Flexibility of Cash Value Life Insurance

Advanced Markets The Flexibility of Cash Value Life Insurance Beyond Protection With today s focus on value and flexibility, cash value life insurance comes into its own. Beyond its main purpose of death

Advanced Markets The Flexibility of Cash Value Life Insurance Beyond Protection With today s focus on value and flexibility, cash value life insurance comes into its own. Beyond its main purpose of death

Variable Universal Life (VUL)

") Variable Universal Life (VUL) What is it? Permanent (cash value) life insurance with maximum flexibility Variable universal life (VUL) is considered the most flexible type of permanent (cash value) life

Variable Universal Life (VUL) What is it? Permanent (cash value) life insurance with maximum flexibility Variable universal life (VUL) is considered the most flexible type of permanent (cash value) life

Update on Mutual Company Dividend Interest Rates for 2013

Update on Mutual Company Dividend Interest Rates for 2013 1100 Kenilworth Ave., Suite 110 Charlotte, NC 28204 704.333.0508 704.333.0510 Fax www.bejs.com Prepared and Researched by June 2013 Near the end

Update on Mutual Company Dividend Interest Rates for 2013 1100 Kenilworth Ave., Suite 110 Charlotte, NC 28204 704.333.0508 704.333.0510 Fax www.bejs.com Prepared and Researched by June 2013 Near the end

VARIABLE UNIVERSAL LIFE YOUR 5-MINUTE GUIDE. You want it all.

VARIABLE UNIVERSAL LIFE YOUR 5-MINUTE GUIDE You want it all. Need more from your life insurance? You need life insurance protection for your family, retirement investments for yourself and your preschooler

VARIABLE UNIVERSAL LIFE YOUR 5-MINUTE GUIDE You want it all. Need more from your life insurance? You need life insurance protection for your family, retirement investments for yourself and your preschooler

DEFINING YOUR NEEDS. Family protection to provide financial security to surviving family members upon the death of the insured person.

DEFINING YOUR NEEDS When you buy life insurance, you want a policy which fits your needs without costing too much. Your first step is to decide how much life insurance you need, how much you can afford

DEFINING YOUR NEEDS When you buy life insurance, you want a policy which fits your needs without costing too much. Your first step is to decide how much life insurance you need, how much you can afford

Guide to buying annuities

Guide to buying annuities Summary of the key points contained in this disclosure document Before you purchase your annuity contract, make sure that you read and understand this guide. While reading this

Guide to buying annuities Summary of the key points contained in this disclosure document Before you purchase your annuity contract, make sure that you read and understand this guide. While reading this

How To Get A Universal Life Insurance Policy

Universal Life What is it? Permanent (cash value life) insurance with flexible premiums Universal life is a form of permanent (cash value) insurance. Your cash value receives a guaranteed minimum interest

Universal Life What is it? Permanent (cash value life) insurance with flexible premiums Universal life is a form of permanent (cash value) insurance. Your cash value receives a guaranteed minimum interest

Variable Universal Life Insurance Policy

May 1, 2015 State Farm Life Insurance Company P R O S P E C T U S Variable Universal Life Insurance Policy prospectus PROSPECTUS DATED MAY 1, 2015 INDIVIDUAL FLEXIBLE PREMIUM VARIABLE UNIVERSAL LIFE INSURANCE

May 1, 2015 State Farm Life Insurance Company P R O S P E C T U S Variable Universal Life Insurance Policy prospectus PROSPECTUS DATED MAY 1, 2015 INDIVIDUAL FLEXIBLE PREMIUM VARIABLE UNIVERSAL LIFE INSURANCE

Life Insurance Education Series

Advanced Planning Life Insurance Education Series Part 5: Life insurance planning for businesses Changes in income- and estate-tax laws as well as volatility in the market may require you to review your

Advanced Planning Life Insurance Education Series Part 5: Life insurance planning for businesses Changes in income- and estate-tax laws as well as volatility in the market may require you to review your

Understanding Life Insurance: A Lesson in Life Insurance

Understanding Life : A Lesson in Life If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Questions 3 Types of Term 4 Term Variations

Understanding Life : A Lesson in Life If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Questions 3 Types of Term 4 Term Variations

Key Person Coverage. Prepared for: Date: Presented by:

Key Person Coverage Prepared for: Date: Presented by: PURPOSE This presentation is for the purpose of helping you understand how life and disability income insurance can be used to overcome the shock to

Key Person Coverage Prepared for: Date: Presented by: PURPOSE This presentation is for the purpose of helping you understand how life and disability income insurance can be used to overcome the shock to

How To Choose Life Insurance

Life Insurance - An Introduction to the Term or Permanent Question Written by: Gary T. Bottoms, CLU, ChFC gbottoms@thebottomsgroup.com The Question Once a need is established for cash created in the event

Life Insurance - An Introduction to the Term or Permanent Question Written by: Gary T. Bottoms, CLU, ChFC gbottoms@thebottomsgroup.com The Question Once a need is established for cash created in the event

Life insurance solutions for. business owners

Life insurance solutions for business owners Life insurance solutions for business owners What s the best life insurance for business owners? It depends on where you see yourself in the future and at which

Life insurance solutions for business owners Life insurance solutions for business owners What s the best life insurance for business owners? It depends on where you see yourself in the future and at which

Insurance Analysis & Implementation: What CPA Financial Planners Need to Know. Presented by: Dr. Lee Slavutin, MD, CLU

Insurance Analysis & Implementation: What CPA Financial Planners Need to Know Presented by: Dr. Lee Slavutin, MD, CLU Introduction Lee Slavutin, MD, CLU Stern Slavutin 2, Inc. www.sternslavutin.com 2 Caveat

Insurance Analysis & Implementation: What CPA Financial Planners Need to Know Presented by: Dr. Lee Slavutin, MD, CLU Introduction Lee Slavutin, MD, CLU Stern Slavutin 2, Inc. www.sternslavutin.com 2 Caveat

LIFE INSURANCE. Spousal Lifetime Access Trust. Transferring wealth and retaining spousal access

LIFE INSURANCE Spousal Lifetime Access Trust Transferring wealth and retaining spousal access Life. your way SM Strive to live your dreams. Discover the flexibility of life insurance protect, accumulate

LIFE INSURANCE Spousal Lifetime Access Trust Transferring wealth and retaining spousal access Life. your way SM Strive to live your dreams. Discover the flexibility of life insurance protect, accumulate

Wealth Creation Planning

Wealth Creation Planning A better way to own Life Insurance! Life insurance is the most effective way to protect against the financial risk and strain of a premature death. However, large or long term

Wealth Creation Planning A better way to own Life Insurance! Life insurance is the most effective way to protect against the financial risk and strain of a premature death. However, large or long term

Diversified Growth SM Variable Universal Life. Protection and accumulation that adjust with your life. A better way of life

Diversified Growth SM Variable Universal Life Protection and accumulation that adjust with your life A better way of life Add to your peace of mind, while adding to your assets You want and need to protect

Diversified Growth SM Variable Universal Life Protection and accumulation that adjust with your life A better way of life Add to your peace of mind, while adding to your assets You want and need to protect

Flexible Premium Universal Life Insurance with an Indexed Feature A Life Insurance Illustration

Initial Base Face Amount = $ Total Initial Annual Premium = $ About the Universal Life Insurance Policy Phoenix Simplicity Index Life is a single life flexible premium universal life insurance policy with

Initial Base Face Amount = $ Total Initial Annual Premium = $ About the Universal Life Insurance Policy Phoenix Simplicity Index Life is a single life flexible premium universal life insurance policy with

What You Should Know About Buying. Life Insurance

What You Should Know About Buying Life Insurance Life insurance is the foundation of financial security for you and your family. It protects your financial resources against the uncertainties of life so

What You Should Know About Buying Life Insurance Life insurance is the foundation of financial security for you and your family. It protects your financial resources against the uncertainties of life so

Principal Life Insurance Company Des Moines, Iowa 50392-0001 www.principal.com

WE UNDERSTAND WHAT YOU RE WORKING FOR SM Principal Life Insurance Company Des Moines, Iowa 50392-0001 www.principal.com This information is believed to be accurate and authoritative in regard to the subject

WE UNDERSTAND WHAT YOU RE WORKING FOR SM Principal Life Insurance Company Des Moines, Iowa 50392-0001 www.principal.com This information is believed to be accurate and authoritative in regard to the subject

16 General Overview Of Life Insurance Policies

16 General Overview Of Life Insurance Policies CHAPTER OVERVIEW Because the primary asset of an ILIT is life insurance (which can be a very sophisticated financial product), the more an attorney knows

16 General Overview Of Life Insurance Policies CHAPTER OVERVIEW Because the primary asset of an ILIT is life insurance (which can be a very sophisticated financial product), the more an attorney knows

White Paper: Using Cash Value Life Insurance for Retirement Savings

White Paper: Using Cash Value Life Insurance for Retirement Savings www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member

White Paper: Using Cash Value Life Insurance for Retirement Savings www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member

GUIDE TO BUYING ANNUITIES

GUIDE TO BUYING ANNUITIES Buying an Annuity Contract at HD Vest Before you buy any investment, it is important to review your financial situation, investment objectives, risk tolerance, time horizon, diversification

GUIDE TO BUYING ANNUITIES Buying an Annuity Contract at HD Vest Before you buy any investment, it is important to review your financial situation, investment objectives, risk tolerance, time horizon, diversification

MassMutual Whole Life Insurance

A Technical Overview for Clients and their Advisors MassMutual Whole Life Insurance The product design and pricing process Contents 1 Foreword 2 A Brief History of Whole Life Insurance 3 Whole Life Basics

A Technical Overview for Clients and their Advisors MassMutual Whole Life Insurance The product design and pricing process Contents 1 Foreword 2 A Brief History of Whole Life Insurance 3 Whole Life Basics

Spousal Lifetime Access Trust Using Legacy Advantage SUL Insurance Policy

Spousal Lifetime Access Trust Using Insurance Policy Supplemental Illustration Valued Client & Valued Client Prepared by: MetLife Agent 2 Park Ave. New York, NY 1166 Insurance Products: Not A Deposit Not

Spousal Lifetime Access Trust Using Insurance Policy Supplemental Illustration Valued Client & Valued Client Prepared by: MetLife Agent 2 Park Ave. New York, NY 1166 Insurance Products: Not A Deposit Not

Caring for longer than a lifetime

Life insurance Caring for longer than a lifetime Your 5-minute Guide Life goes on prepare for it Your love for your family will live forever. However, we all know we won t live forever. Life insurance

Life insurance Caring for longer than a lifetime Your 5-minute Guide Life goes on prepare for it Your love for your family will live forever. However, we all know we won t live forever. Life insurance

The Value of Whole Life Insurance

Page 1 of 6 A MassMutual Illustration Presentation The Value of Whole Life Insurance A life insurance illustration summary Prepared for: Prepared by: Valued Client Michael Fliegelman. CLU, ChFC, AEP RFC

Page 1 of 6 A MassMutual Illustration Presentation The Value of Whole Life Insurance A life insurance illustration summary Prepared for: Prepared by: Valued Client Michael Fliegelman. CLU, ChFC, AEP RFC

Life Insurance and Supplemental Income

supplemental income using life insurance supplement your retirement income maintain your lifestyle Investment and Insurance Products: Are Not Deposits of Any Bank Are Not FDIC Insured Are Not Insured By

supplemental income using life insurance supplement your retirement income maintain your lifestyle Investment and Insurance Products: Are Not Deposits of Any Bank Are Not FDIC Insured Are Not Insured By

Nationwide YourLife Indexed UL. Give clients a balanced life FOR INSURANCE PROFESSIONAL USE ONLY NOT FOR DISTRIBUTION WITH THE PUBLIC

advisor GUIDE Nationwide YourLife Indexed UL Give clients a balanced life FOR INSURANCE PROFESSIONAL USE ONLY NOT FOR DISTRIBUTION WITH THE PUBLIC Preparing for the future can be stressful for your clients.

advisor GUIDE Nationwide YourLife Indexed UL Give clients a balanced life FOR INSURANCE PROFESSIONAL USE ONLY NOT FOR DISTRIBUTION WITH THE PUBLIC Preparing for the future can be stressful for your clients.

Your guide to Great-West Life Participating life insurance

Your guide to Great-West Life Participating life insurance This guide provides a high-level overview of key features of Great-West Life participating life insurance. After you review this guide, talk with

Your guide to Great-West Life Participating life insurance This guide provides a high-level overview of key features of Great-West Life participating life insurance. After you review this guide, talk with

How to Choose a Life Insurance Company *YP½PPMRK 4VSQMWIW A 2014 GUIDE THROUGH RELEVANT INDUSTRY INFORMATION

How to Choose a Life Insurance Company *YP½PPMRK 4VSQMWIW A 2014 GUIDE THROUGH RELEVANT INDUSTRY INFORMATION Because the most important people in your life will car, or computer, most people are completely

How to Choose a Life Insurance Company *YP½PPMRK 4VSQMWIW A 2014 GUIDE THROUGH RELEVANT INDUSTRY INFORMATION Because the most important people in your life will car, or computer, most people are completely

ANICO. Indexed Universal Life. A Universal Life Insurance Policy Issued By American National Insurance Company Galveston, TX

ANICO Indexed Universal Life A Universal Life Insurance Policy Issued By American National Insurance Company Galveston, TX ANICO Indexed Universal Life Financial security isn t just about growing a nest

ANICO Indexed Universal Life A Universal Life Insurance Policy Issued By American National Insurance Company Galveston, TX ANICO Indexed Universal Life Financial security isn t just about growing a nest

Understanding the Income Taxation of Life Insurance

A Reference Guide for Individuals and Businesses Understanding the Income Taxation of Life Insurance Answers to Frequently Asked Questions Tax Insights Contents 1 General Questions 4 Non-MEC Policy Questions

A Reference Guide for Individuals and Businesses Understanding the Income Taxation of Life Insurance Answers to Frequently Asked Questions Tax Insights Contents 1 General Questions 4 Non-MEC Policy Questions

Life Insurer Financial Profile

Life Insurer Financial Profile Company New York Life Ins Northwestern Massachusetts John Hancock Life Mutual of Omaha Lincoln National Pacific Life Ins Co Genworth Life Ins Co Long Term Care Mutual Life

Life Insurer Financial Profile Company New York Life Ins Northwestern Massachusetts John Hancock Life Mutual of Omaha Lincoln National Pacific Life Ins Co Genworth Life Ins Co Long Term Care Mutual Life

Sales Strategy Life Insurance in Retirement Planning Plus

Sales Strategy Life Insurance in Retirement Planning Plus Life insurance protection is the foundation of a family s future, providing cash to: replace income for surviving family, pay off family debt,

Sales Strategy Life Insurance in Retirement Planning Plus Life insurance protection is the foundation of a family s future, providing cash to: replace income for surviving family, pay off family debt,

Understanding Fixed Indexed Annuities

Fact Sheet for Consumers: Understanding Fixed Indexed Annuities PRESENTED BY Insured Retirement Institute Fact Sheet for Consumers: Understanding Fixed Indexed Annuities Put simply, a Fixed Indexed Annuity

Fact Sheet for Consumers: Understanding Fixed Indexed Annuities PRESENTED BY Insured Retirement Institute Fact Sheet for Consumers: Understanding Fixed Indexed Annuities Put simply, a Fixed Indexed Annuity

Understanding fixed index universal life insurance

Allianz Life Insurance Company of North America Understanding fixed index universal life insurance Protection, wealth accumulation potential, and tax advantages in one policy M-3959 Understanding fixed

Allianz Life Insurance Company of North America Understanding fixed index universal life insurance Protection, wealth accumulation potential, and tax advantages in one policy M-3959 Understanding fixed

Variable universal life insurance. Quick reference. You want it all.

Variable universal life insurance Quick reference You want it all. Need more from your life insurance? You need life insurance protection for your family, retirement investments for yourself and your preschooler

Variable universal life insurance Quick reference You want it all. Need more from your life insurance? You need life insurance protection for your family, retirement investments for yourself and your preschooler

Estate Planner s View of Life Insurance and Annuities

Estate Planner s View of Life Insurance and Annuities for Medium-size Estates Michael F. Amoia, JD, LLM (Tax), CFP, CLU, ChFC Vice President, Advanced Sales Crump Life Insurance Services For Training Purposes

Estate Planner s View of Life Insurance and Annuities for Medium-size Estates Michael F. Amoia, JD, LLM (Tax), CFP, CLU, ChFC Vice President, Advanced Sales Crump Life Insurance Services For Training Purposes

Protect your business, your family, and your legacy.

An Educational Guide for Business Owners Protect your business, your family, and your legacy. Take a closer look at buy-sell agreements. Needs-based Strategies Your business is probably your single largest

An Educational Guide for Business Owners Protect your business, your family, and your legacy. Take a closer look at buy-sell agreements. Needs-based Strategies Your business is probably your single largest

How to Choose a Life Insurance Company. Fulfilling Promises

How to Choose a Life Insurance Company Fulfilling Promises A 2014 Guide Through Relevant Industry Information Because the most important people in your life will depend on it, life insurance is one of

How to Choose a Life Insurance Company Fulfilling Promises A 2014 Guide Through Relevant Industry Information Because the most important people in your life will depend on it, life insurance is one of

CHAPTER 10 ANNUITIES

CHAPTER 10 ANNUITIES are contracts sold by life insurance companies that pay monthly, quarterly, semiannual, or annual income benefits for the life of a person (the annuitant), for the lives of two or

CHAPTER 10 ANNUITIES are contracts sold by life insurance companies that pay monthly, quarterly, semiannual, or annual income benefits for the life of a person (the annuitant), for the lives of two or

Secure Lifetime GUL 3 Guaranteed Universal Life Insurance Information for Financial Professionals

Secure Lifetime GUL 3 Guaranteed Universal Life Insurance Information for Financial Professionals Our commitment to your clients is stronger than ever before! Policies issued by American General Life Insurance

Secure Lifetime GUL 3 Guaranteed Universal Life Insurance Information for Financial Professionals Our commitment to your clients is stronger than ever before! Policies issued by American General Life Insurance

Guide to buying annuities

Guide to buying annuities Summary of the key points contained in this disclosure document Before you purchase your annuity contract, make sure that you read and understand this guide. While reading this

Guide to buying annuities Summary of the key points contained in this disclosure document Before you purchase your annuity contract, make sure that you read and understand this guide. While reading this

UNDERSTANDING PARTICIPATING WHOLE LIFE INSURANCE

UNDERSTANDING PARTICIPATING WHOLE LIFE INSURANCE equimax CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations we ve provided

UNDERSTANDING PARTICIPATING WHOLE LIFE INSURANCE equimax CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations we ve provided

003.05 Net Cash Surrender Value. "Net cash surrender value" means the maximum amount payable to the policyowner upon surrender.

Title 210 - NEBRASKA DEPARTMENT OF INSURANCE Chapter 40 - UNIVERSAL LIFE INSURANCE 001. Statutory authority. This regulation is promulgated under the authority of NEB. REV. STAT. 44-101.01 and is operative

Title 210 - NEBRASKA DEPARTMENT OF INSURANCE Chapter 40 - UNIVERSAL LIFE INSURANCE 001. Statutory authority. This regulation is promulgated under the authority of NEB. REV. STAT. 44-101.01 and is operative

Life Insurance Policy Valuations

Life Insurance Policy Valuations New Challenges Bring New Opportunities Presented by: Martin Financial Group 315 Commercial Drive, Suite A4 Savannah, GA 31406 DISCLAIMER All rights reserved. No part of

Life Insurance Policy Valuations New Challenges Bring New Opportunities Presented by: Martin Financial Group 315 Commercial Drive, Suite A4 Savannah, GA 31406 DISCLAIMER All rights reserved. No part of

Guide to Buying Annuities

Guide to Buying Annuities Buying an Annuity Contract at H.D. Vest Before you buy any investment, it is important to review your financial situation, investment objectives, risk tolerance, time horizon,

Guide to Buying Annuities Buying an Annuity Contract at H.D. Vest Before you buy any investment, it is important to review your financial situation, investment objectives, risk tolerance, time horizon,

Canada Life 2013 participating policyowner dividend scale announcement

Nov. 8, 2012 Canada Life 2013 participating policyowner dividend scale announcement New dividend scale effective Jan. 1, 2013 Why the decrease for 2013 Detailed information important for advisors Updated

Nov. 8, 2012 Canada Life 2013 participating policyowner dividend scale announcement New dividend scale effective Jan. 1, 2013 Why the decrease for 2013 Detailed information important for advisors Updated

flexible life insurance protection enhanced cash value accumulation potential

AXA Equitable Life Insurance Company Athena Indexed Universal Life SM flexible life insurance protection enhanced cash value accumulation potential your changing protection and financial needs Life never

AXA Equitable Life Insurance Company Athena Indexed Universal Life SM flexible life insurance protection enhanced cash value accumulation potential your changing protection and financial needs Life never

Participating Policy Fact Sheet

Participating Policy Fact Sheet This Fact Sheet helps you better understand the factors that may affect the Reversionary Bonus and Terminal Bonus of your Fortune Guard Life Insurance 1 and/or Fortune Protector

Participating Policy Fact Sheet This Fact Sheet helps you better understand the factors that may affect the Reversionary Bonus and Terminal Bonus of your Fortune Guard Life Insurance 1 and/or Fortune Protector

How to Choose a Life Insurance Company

How to Choose a Life Insurance Company Fulfilling Promises A Guide Through Relevant Industry Information Because the most important people in your life will depend on it, life insurance is one of the most

How to Choose a Life Insurance Company Fulfilling Promises A Guide Through Relevant Industry Information Because the most important people in your life will depend on it, life insurance is one of the most

Life Insurer Financial Profile

Life Insurer Financial Profile Company Ratings A.M. Best Company (Best's Rating, 15 ratings) Standard & Poor's (Financial Strength, 20 ratings) Moody's (Financial Strength, 21 ratings) Fitch Ratings(Financial

Life Insurer Financial Profile Company Ratings A.M. Best Company (Best's Rating, 15 ratings) Standard & Poor's (Financial Strength, 20 ratings) Moody's (Financial Strength, 21 ratings) Fitch Ratings(Financial

White Paper Tax Planning with Life Insurance

White Paper www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

White Paper www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

Understanding Universal Life Insurance

Understanding Universal Life Insurance Universal life insurance has been around for over two decades. Original proponents hailed it as the most revolutionary concept in the insurance industry. Critics

Understanding Universal Life Insurance Universal life insurance has been around for over two decades. Original proponents hailed it as the most revolutionary concept in the insurance industry. Critics

Life Insurance Review. Ensuring life insurance coverage meets today s goals. Life. your way

Life Insurance Review Ensuring life insurance coverage meets today s goals Life. your way SM Life. your way Strive to live your dream and plan for the if in life. Discover the flexibility of life insurance

Life Insurance Review Ensuring life insurance coverage meets today s goals Life. your way SM Life. your way Strive to live your dream and plan for the if in life. Discover the flexibility of life insurance

Variable Universal Life Insurance

A Flexible Approach to Life s Challenges Variable Universal Life Insurance Variable Annuities offered by: Western Reserve Life Assurance Co. of Ohio MS430795-0506 What are your financial goals in life?

A Flexible Approach to Life s Challenges Variable Universal Life Insurance Variable Annuities offered by: Western Reserve Life Assurance Co. of Ohio MS430795-0506 What are your financial goals in life?

Life Insurance. A Consumer s Guide to INSURANCE FACTS. for Pennsylvania Consumers. 1-877-881-6388 Toll-free Automated Consumer Line

INSURANCE FACTS for Pennsylvania Consumers A Consumer s Guide to Life Insurance 1-877-881-6388 Toll-free Automated Consumer Line www.insurance.state.pa.us Pennsylvania Insurance Department Website Buying

INSURANCE FACTS for Pennsylvania Consumers A Consumer s Guide to Life Insurance 1-877-881-6388 Toll-free Automated Consumer Line www.insurance.state.pa.us Pennsylvania Insurance Department Website Buying

SAMPLE. is equal to the Death Benefit less the Account Value of your policy.

DEFINITIONS EquiLife Limited Pay UL (Joint first-to-die) The following are definitions of some of the terms used in your EquiLife Joint First-to-Die policy. If you need additional information or clarification

DEFINITIONS EquiLife Limited Pay UL (Joint first-to-die) The following are definitions of some of the terms used in your EquiLife Joint First-to-Die policy. If you need additional information or clarification