DC Health Benefit Exchange Authority (HBX) HI0 Central Purpose Key Facts about HBX

|

|

|

- Everett Reeves

- 8 years ago

- Views:

Transcription

1 DC Health Benefit Exchange Authority (HBX) HI0 Mila Kofman, Executive Director 1225 Eye St. NW, Suite 400 Washington, DC Central Purpose The DC Health Benefit Exchange Authority (HBX) was established as a requirement of Section 3 of the Health Benefit Exchange Authority Establishment Act of 2011, effective March 3, 2012 (D.C. Law ) pursuant to enactment of the federal health reform law: the Patient Protection and Affordable Care Act (ACA). HBX is responsible for implementing a state-based on-line health insurance marketplace under the ACA. The marketplace, called DC Health Link ( enables individuals and small businesses to compare health insurance prices and benefits and to purchase affordable, quality health insurance. For the first time, individual and small business consumers have the purchasing power of large employers and have choices of coverage from multiple insurance companies. Through a no wrong door approach, eligibility for premium reductions through federal tax credits (called advanced premium tax credits) and eligibility for Medicaid is done on-line through DCHealthLink.com. Key Facts about HBX HBX is an independent, quasi-government agency that reports to an 11 member Executive Board -- 7 voting members who are private District residents and 4 ex-officio members who are directors of District Agencies. Prior to creating HBX, the District empowered Department of Health Care Finance, Department of Human Services, Department of Health, and the Department of Insurance Securities and Banking to lead implementation and planning efforts under the ACA for the on-line marketplace. HBX voting Board Members were nominated by the Mayor and confirmed by the Council in the summer of After a national search, the HBX Board hired an Executive Director (January 2013). In January 2013, the District (OCP) entered into an IT services contract to build an online exchange marketplace with Infosys Public Services. DC Health Link opened for business on time on October 1, 2013 for individual and small business customers. Bloomberg News reported that the District was one of only four states that opened on time and was operational all day on October 1. DC Health Link has a Contact Center that provides telephone and help to people. Since opening, the Contact Center has received 150,881 calls total. The average call volume during open enrollment was 14,453 calls per month. The average call volume after the conclusion of open enrollment was 10,676 calls per month. The number is HBX trains and certifies health insurance brokers to provide one-on-one help to small businesses and individuals seeking to purchase health insurance through DC Health Link. HBX supports DC Health Link Assisters to provide one-on-one assistance to customers seeking help. Information for certified brokers and DC Health Link Assisters is available at DCHealthLink.com and on DC Health Link Mobile Device Apps for Individuals and Small Businesses -- both available through Apple App Store and Google Play. In October 2013, the federal government designated the District s small business marketplace as the source of coverage for Members of Congress and their designated staff.

2 In December 2013, President Obama enrolled in coverage through DC Health Link. As of October 22, 2014, DC Health Link has served 62,122 people who chose a health plan or qualified for Medicaid coverage: 15,511 people have enrolled themselves and their families in qualified health plans, 14,632 people have enrolled through their employer, and 31,979 have been determined eligible for Medicaid through DC Health Link. For 2015, four health insurers (Aetna, CareFirst, Kaiser and United) are offering 196 different qualified health plans to small businesses. For 2015, there are 31 qualified health plans for individuals and their families offered by Aetna, CareFirst and Kaiser. Individual and small business plans vary from high deductible health plans to zero deductible options; and include HMO, PPO, and POS plans. HBX policy decisions are made through a stakeholder driven process. In 2013 and 2014 HBX had many working groups and continues to have standing advisory committees in addition to a Standing Advisory Board. The HBX Board has adopted consensus recommendations from working stakeholder groups and committees. All policies adopted through resolutions are available at In 2013, the Council passed legislation called Better Prices, Better Quality, Better Choices for Health Coverage Act of 2013 reflecting policies adopted by HBX: Provide a meaningful choice of health plans. Provide enhanced benefits. Build a competitive private insurance marketplace by not limiting the number of QHPs in the exchange. Require health plans to offer plan options at the bronze, silver and gold metal levels. Create one large marketplace that provides individuals, small businesses and their employees the same leverage as large companies. Defines habilitative services to include treatment of autism. HBX P a g e 2 To date, HBX has used federal grant dollars for establishment and implantation. That will continue through most of The federal grants received by HBX to build DC Health Link s on-line eligibility functionality leverages federal dollars to help the District use one state-of-the-art eligibility system for all social service programs (i.e. food stamps, TANF etc.). Goals/Performance Measures To add functionality to DC Health Link that is required by federal law. Because HBX had only 8 months to develop and deploy a sophisticated online marketplace, only basic functionality for both individual and SHOP was implemented. To improve functionality of DC Health Link in response to customer experience and feedback. This is ongoing. To receive final certification as a State-based exchange marketplace. The District, like all states operating State-based exchange marketplaces, is currently conditionally approved. To continue to find and enroll eligible uninsured people. To advocate on behalf of our individual and small business customers. Programs/Services WEBSITE HEALTH PLAN SHOPPING AND ENROLLMENT: is the online portal for the purchase of health insurance for individuals and small businesses. It allows customers to compare different health insurance products and prices. Customers can enroll on-line in a health plan. ELIGIBILITY DETERMINATIONS FOR REDUCED PREMIUMS AND OTHER FINANCIAL HELP WITH HEALTH INSURANCE: is an on-line portal to help customers determine if they qualify for reduced health insurance premiums, costsharing help, and Medicaid coverage. The online portal verifies income, citizenship status and other eligibility criteria. Based on on-line

are offering 196 different qualified health plans to small businesses.")

3 determinations, a customer can enroll in private coverage on-line or be transferred to an enrollment broker for Medicaid (different city agencies are responsible for Medicaid DHCF and DHS). Premium reductions result in a monthly health insurance premium that is lower than full price; a customer is only responsible for the lower premium amount and the IRS pays the rest directly to the health plan chosen by the customer. DCHealthLink.com also has a cost calculator that enables customers to estimate their premiums before completing an application. MEMBER SERVICES: HBX member services assists customers with technical issues, on-line enrollment, and changes to enrollment. Member services investigates customer complaints and inquiries and works with the IT team and insurers to resolve customer issues. CONTACT CENTER: Provides assistance to customers by phone and . Consumers can call the Contact Center at and complete an application over the phone, get answers to questions about the application process, and receive assistance if they ve run into any technical difficulties. Customers can also the contact center at with questions or to submit documentation. The Contact Center serves individuals, families, small businesses, brokers, and assisters/navigators. DC HEALTH LINK ASSISTERS: Provide in person help to consumers and educate and enroll uninsured and hard to reach people. HBX provides grants to community based organizations and health centers. Some assisters are bi-lingual (Spanish, Amharic and other languages). CERTIFICATION FOR HEALTH INSURANCE BROKERS: HBX trains and certifies health insurance brokers to sell health insurance through DC Health Link. To date there are 362 certified brokers and that number continues to grow. Customers can find information for certified HBX P a g e 3 brokers at The Contact Center will also connect customers to a broker if a person would like expert advice on which health plan is best for them. CERTIFIED APPLICATION COUNSELORS (CACs): Provide in person help to customers, similar to DC Health Link Assisters. HBX does not provide grant funding. HBX provides training and certification. CACs work in community health centers and hospitals with an incoming population that may be uninsured. MOBILE APPS: HBX provides two mobile APPs one for individual and family coverage and another for Small Business coverage. Both can be downloaded from the Apple App Store or Google Play. More information on these APPs can be found here. APPEALS: HBX provides appeal services for customers appealing an eligibility decision, denial of premium reductions, terminations of coverage, etc. Customers can contact the Contact Center to file an appeal or can complete an Appeal Request for Individuals and Families Form and send it by fax, or mail. Our website details this information. PLAN MANAGEMENT: HBX plan management unit works with health plans to ensure that broad coverage options are available to customers and that the benefit and premium information accurately displays for customer shopping and purchase. First Quarter CY2015 Hot Button Issue(s) OVERSIGHT ACTIVITIES: The ACA involves the implementation of significant new insurance standards, the establishment of a new program a transparent on-line health insurance marketplace new tax credits and a tax requirement to have health coverage, and more. As a result, there are significant federal and local oversight activities to which HBX is subject.

4 P a g e 4 There are five audits through the Department of Health and Human Services Office of Inspector General, the Treasury Inspector General, and various District audits. The federal audits are on all state-based marketplaces. HBX receives requests from the House and Senate oversight committees and is required to respond. Responses include document production. HBX receives and responds to numerous Freedom of Information Act (FOIA) requests from individuals, law firms, and news organizations. HBX receives numerous requests on a monthly basis from other interested parties such as the U.S. Government Accountability Office, research institutions, and consumer advocacy organizations. Facts about the Assessment: 1. Having a broad based assessment ensures all those who benefit from the exchange marketplace contribute to its operation. All health carriers benefit from the exchange marketplace through lower direct claims and a broader marketplace for the sale of supplemental benefit plans such as vision insurance. 2. The assessment is modeled after an existing assessment on insurers in the District to fund the Healthcare Ombudsman Program. 3. The assessment is tied to the budget the DC Council approves for the operation of the marketplace. 4. The Health Benefit Exchange Authority budget, assessment, and expenditures will be reviewed and audited by the Insurance Regulatory Trust Fund Bureau that has been reviewing and auditing the Department of Insurance budget and assessment since FEDERAL GRANT OPPORTUNITY: HBX will be submitting a request for federal grant funds; application is due by November 15, 2014 and requires a letter of support signed by the Mayor and health agencies in the District. FINANCIAL SUSTAINABILITY: A prerequisite for certification as a state-based marketplace, a marketplace must show that it will be self-sustaining. The Council passed emergency and temporary legislation for an assessment of all health carriers operating in the District. The assessment is broad based and includes all health carriers, including those selling plans outside of DC Health Link. This year s assessment was 1% of premiums and carriers were assessed on August 18, Passage of permanent legislation is necessary to meet the financial sustainability requirements of a state based marketplace. SMALL BUSINESS TRANSITION TO ONE BIG MARKETPLACE: In 2013, the Council passed legislation to create one large marketplace in the District that provides individuals, small businesses and their employees the same leverage as large companies. All individual and small group products are sold through DC Health Link. Creating a competitive insurance marketplace where consumers are able to see all prices and products has resulted in real price competition. In 2013, insurers refiled proposed premiums with lower prices. The 2014 rates were also competitive as a result of full transparency by requiring all products to be available to all consumers in one place. The legislation built in a transition to one large marketplace. In 2015 small businesses at renewal will be coming through DC Health Link. HBX has implemented a conversion plan to help with this transition. For the majority of small businesses, their health insurance carrier or broker will manage the transition for them. The conversion

5 P a g e 5 plan was developed with all the health insurers selling through DC Health Link. HEALTH PLAN CERTIFICATION PROCESS: The ACA requires state-based marketplaces to certify health plans. The certification includes consumer protection requirements like ensuring the insurer is licensed and in good standing; a health plan has an adequate network of providers, premium increases are justified and reasonable, a health plan does not discriminate in marketing or benefit design against consumers with high medical needs, etc. In early 2013, HBX s stakeholder working group recommended a certification process, which the Board adopted. Now with two years of experience, the Board s Insurance Committee is reviewing the process in preparing for plan year 2016 and is planning to adopt updated certification requirements in key areas in early Health insurance carriers, consumers have been and will continue to be included in the process and all meetings, deliberations, and decisions are public. IRS REPORTING: As part of the requirements of the ACA, the DC Health Benefit Exchange Authority is required to provide every DC Health Link customer with an IRS-mandated form (called a 1095-A) that provides proof that they had health insurance coverage the preceding year and outlines what, if any, Advanced Premium Tax Credit the individual or family received. To ensure accurate data, HBX relies on enrollment data from the carriers. General questions on how to report this information on tax returns will be most appropriately answered by the IRS help line and HBX will refer people there. However, it will impact our Contact Center as well and it is likely to be a hot topic in early 2015 as people prepare their tax returns. CONGRESS: The ACA requires that Members of Congress and their designated staff obtain coverage through health insurance exchanges. In October 2013, the U.S. Office of Personnel Management designated HBX as the source of coverage for all Members of Congress and their designated staff. The designation occurred after DC Health Link opened for business. HBX coordinated with OPM and House and Senate personnel offices to effectively enroll Members of Congress and their designated staff through DC Health Link in their 2013 open enrollment period, which began on November 11, The 2015 open enrollment period for Congress is November 10 December 8, 2014.

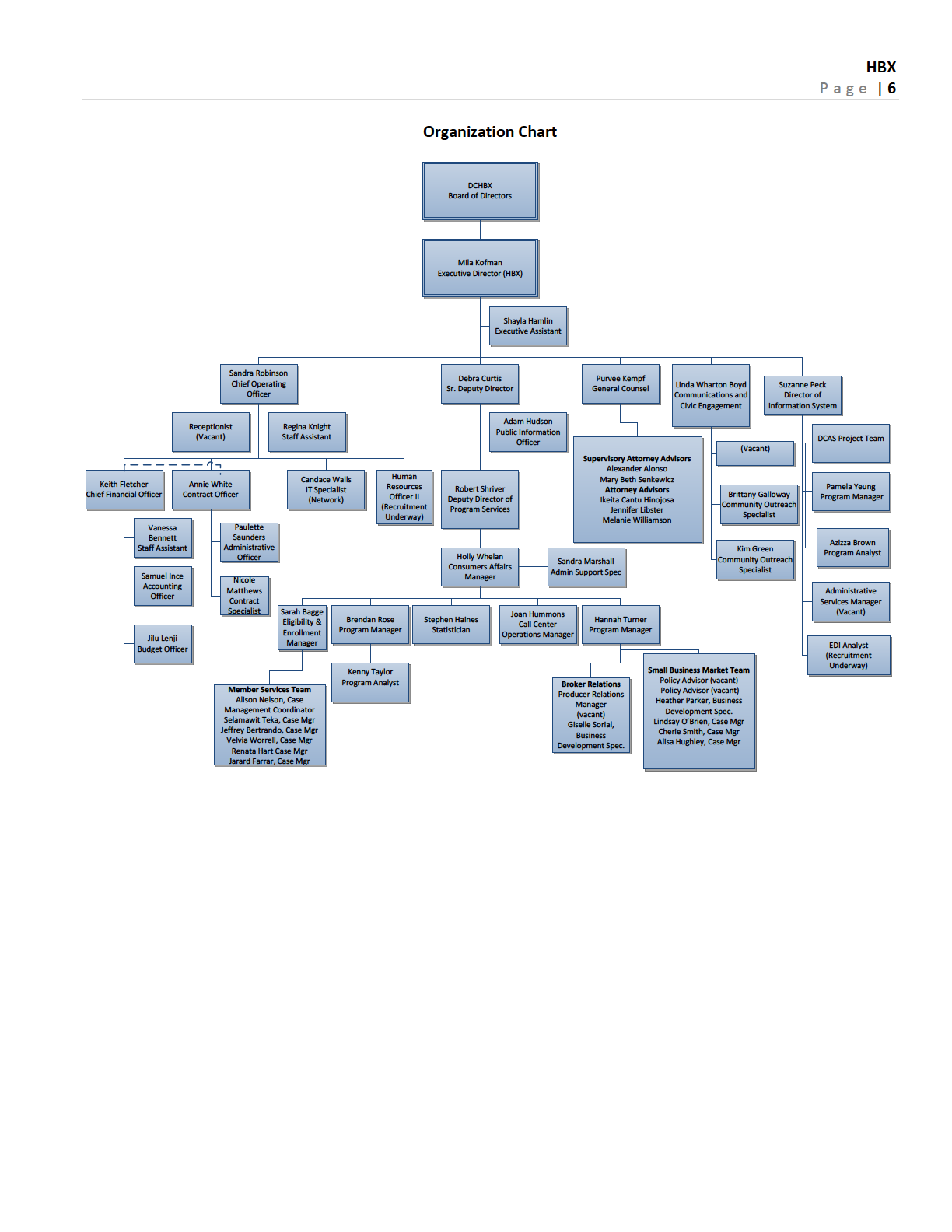

6

7 P a g e 7 Boards and Commissions relevant to the agency (if any) Board Name Name of Chairperson No. of Members District of Columbia Health Benefit Exchange Authority Executive Board Diane C. Lewis 7 voting members of the public 4 ex officio members (District Government Agency Directors) Budget FY2015 Total Budget $ 28,751,244 No. of Employees Current No. of FTEs 54 Union Representation N/A Union(s) Union Representative No. of Members Facility Location(s) Facility Name / ID Address Zip Code Ward Main Phone No. HBX Main Office 1225 Eye Street, NW, # (202) Contact Center 955 L Enfant Plaza, SW, #100P (855) * No Facility ID because we are located in a non-government building* Key Projects/Initiatives Project/Initiative Name Brief Description Delivery Date Open Enrollment for Individuals November 15, 2014 February 15, 2015 is the open enrollment period for coverage in During this window, anyone who is eligible can purchase coverage through DC Health Link s individual marketplace. We have planned enrollment activities and initiatives to inform the public about enrollment opportunities. An abbreviated list of these activities includes: partnerships with government agencies, community and business groups, and Council Members; storefront locations at MLK library, and three other sites; and enrollment events throughout the period. Our calendar at always has our events listed. November 15, 2014 February 15, 2015 Special Enrollment Periods NOTE: People who are found eligible for Medicaid can obtain Medicaid coverage at any time during the year, they are not limited to open enrollment. Small businesses may also apply at any time. Even after open enrollment closes, individuals often become eligible for health insurance coverage by meeting certain qualifying life events like the birth of a child, marriage, loss of minimum essential coverage, or moving to a new jurisdiction. Thus, enrollment continues year-round through DC Health Link. Year -round

715-7576 Contact Center 955 L Enfant Plaza, SW, #100P 20024 6 (855) 532-5465 * No Facility ID because we are located in a non-government")

8 P a g e 8 Project/Initiative Name Brief Description Delivery Date IRS Reporting DC Health Benefit Exchange Authority is required by federal law to issue a 1095-A form to people enrolled in health insurance through the individual marketplace; requirement does not apply for group coverage through DC Health Link. The 1095-A provides proof that a person had health insurance coverage the preceding year and outlines what, if any, Advanced Premium Tax Credit the individual or family received. That form will be the basis to determine if a person owes additional taxes or is entitled to additional APTC. The form will also be the basis for determining whether an individual or family had health coverage for the previous year or owes a tax penalty to the IRS. January April 2015 Capital Program(s) Project Name Budget ID Funding Source Project Budget Current Balance Delivery Date N/A Important/Significant Dates Event Brief Description Delivery Date Open Enrollment Open enrollment for private health insurance coverage for individuals and families for plan year 2015: Open enrollment is the window during which any eligible individual can apply for coverage through DC Health Link or change their coverage for the following year. After the open enrollment period, only people who qualify for a Special Enrollment Period can obtain coverage. The two exceptions to this are: November 15, 2014 February 15, 2015 (as required by the Federal government) 1) People found eligible for Medicaid, can always obtain Medicaid coverage at any time of the year; 2) Small businesses may enroll for coverage at any time throughout the year. Congressional Open Enrollment The Office of Personnel Management has ruled that in order for a Member of Congress or their designated staff to receive their employer contribution for health insurance, they are required to enroll in coverage through DC Health Link s small business marketplace. November 10, 2014 December 8, 2014 (dates change slightly each year) Key Contracts Project Name Vendor Name Total Contract Contract Term Value Training Services Whitman Walker $506,215 09/30/2013 thru 05/27/2015 IT Consulting Services Analytica Inc. $1,749,707 10/01/2014 thru 09/30/2015 IT Consulting Services Obverse, Inc. $6,967,052 10/01/2014 thru 09/30/2015 IT Consulting Services The Pittman Group Inc. $6,753,501 10/01/2014 thru 09/30/2015 IT Consulting Services New Light Technologies $2,184,000 04/30/2013 thru 04/29/2014

9 P a g e 9 IT Consulting Services Enlightened Inc. $4,766,117 05/01/2014 thru 04/30/2015 IT Consulting Services Networking for Future $2,537,000 04/30/2013 thru 09/30/2014 Marketing and Weber Shandwick $3,629,067 07/24/2013 thru 07/23/2014 Communication Services Assister Training Families USA $843,885 05/22/2013 thru 05/21/2014 Services Contact Service Center Maximus, Inc. $5,784,204 07/11/2014 thru 07/10/2015 Premium Billing NFP Health $990,000 10/01/2014 thru 09/30/2015 Services EDI Operations Services Secure Exchange Solutions $999,000 10/01/2013 thru 09/30/2014 Staffing Agency Business Strategy Consultants $609,195 10/01/2013 thru 09/30/2014 Key Agreement(s) / Memorandum(s) of Understanding Project Name Brief Description Agreement Term MOA with Department of Human Services- Economic Security Administration To conduct eligibility determinations of individuals who are applying for Advance Payment of Premium Tax Credits and Qualified Health and Dental Plans through DC Health Link. 10/01/ /30/2015 MOA with Office of Administrative Hearings MOA with Department of Insurance, Securities and Banking MOA with DC Department of Human Resources MOA with Department of Human Services MOA with OCTO-DCNET MOA with OCTO-IT Assessment MOA with OCTO- Telecom MOA with Department of General Services To conduct eligibility and enrollment appeals related to Qualified Health Plan, Small Business Options Program and Advanced Payments of Premium Tax Credits. 10/01/ /30/2015 Premium assessment of insurance companies 10/01/ /30/2015 HR services 10/01/ /30/2015 The contract for building the on-line website, DC 10/01/ /30/2015 Health Link, is through DHS and this MOA allows for reimbursement of those IT related expenditures. OCTO-DCNET services associated with the Contact 10/01/ /30/2015 Center relocation. Fixed cost: Enterprise Cloud Information Services, 10/01/ /30/2015 web support, and Enterprise application support Fixed cost: Telephone services 10/01/ /30/2015 Fixed cost: leased space 10/01/ /30/2015 Grant(s) Awarded (or Pending Award) to Agency Grant Name Name of Grantor Total Grant Amount District of Columbia Health Benefit Department of Health and Human Services, Centers for Medicare and Current Grant Grant Balance Expiration $ 25,832,931 $ 25,832,931 12/2015

10 P a g e 10 Exchange Establishment Cooperative Agreement to Support Establishment of the Affordable Care Act s Health Insurance Medicaid Services Department of Health and Human Services, Centers for Medicare and Medicaid Services $42,402,977 $42,402,977 10/2015

11 P a g e 11 Active Litigation(s) Project Name Brief Description Consent Decree(s) Project Name Brief Description Agreement Term N/A

Goals/Performance Measures Enhance consumer financial education in the District.

Department of Insurance, Securities and Banking (DISB) SR0 Chester A. McPherson, Acting Commissioner 801 First St, NE Suite 701 Washington, DC 20002 (202) 727-8000 http://disb.dc.gov/ Central Purpose DISB

Department of Insurance, Securities and Banking (DISB) SR0 Chester A. McPherson, Acting Commissioner 801 First St, NE Suite 701 Washington, DC 20002 (202) 727-8000 http://disb.dc.gov/ Central Purpose DISB

What is a state health insurance exchange (i.e. "American Health Benefit Exchange")?

?") MEMORANDUM DATE: 11/07/2011 TO: Members of the House Appropriation Subcommittee for LARA FROM: Paul Holland, Fiscal Analyst RE: State Health Insurance Exchanges In response to the requirements pertaining

MEMORANDUM DATE: 11/07/2011 TO: Members of the House Appropriation Subcommittee for LARA FROM: Paul Holland, Fiscal Analyst RE: State Health Insurance Exchanges In response to the requirements pertaining

Key Facts. In 2013, the CJCC was designated as a criminal justice agency for purposes of information sharing. (D.C. Code 22-4234)

") Criminal Justice Coordinating Council (CJCC) FJ0 Mannone A. Butler, Executive Director 441 4 th Street, NW, Suite 715N Washington, DC 20001 202.442.9283 http://cjcc.dc.gov/ http://cjcc.resourcelocator.net/

Criminal Justice Coordinating Council (CJCC) FJ0 Mannone A. Butler, Executive Director 441 4 th Street, NW, Suite 715N Washington, DC 20001 202.442.9283 http://cjcc.dc.gov/ http://cjcc.resourcelocator.net/

NOT ALL OF THE COLORADO MARKETPLACE S INTERNAL CONTROLS WERE EFFECTIVE IN ENSURING THAT INDIVIDUALS WERE ENROLLED IN QUALIFIED HEALTH PLANS ACCORDING

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL NOT ALL OF THE COLORADO MARKETPLACE S INTERNAL CONTROLS WERE EFFECTIVE IN ENSURING THAT INDIVIDUALS WERE ENROLLED IN QUALIFIED HEALTH

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL NOT ALL OF THE COLORADO MARKETPLACE S INTERNAL CONTROLS WERE EFFECTIVE IN ENSURING THAT INDIVIDUALS WERE ENROLLED IN QUALIFIED HEALTH

Monday, May 13, 2013 11:00 AM Room 123, John A. Wilson Building. Mila Kofman, J.D. Executive Director Health Benefit Exchange Authority

STATEMENT OF MILA KOFMAN, J.D. EXECUTIVE DIRECTOR OF THE HEALTH BENEFIT EXCHANGE AUTHORITY COUNCIL OF THE DISTRICT OF COLUMBIA COMMITTEE ON HEALTH COUNCILMEMBER YVETTE ALEXANDER, CHAIRPERSON PUBLIC OVERSIGHT

STATEMENT OF MILA KOFMAN, J.D. EXECUTIVE DIRECTOR OF THE HEALTH BENEFIT EXCHANGE AUTHORITY COUNCIL OF THE DISTRICT OF COLUMBIA COMMITTEE ON HEALTH COUNCILMEMBER YVETTE ALEXANDER, CHAIRPERSON PUBLIC OVERSIGHT

The Affordable Care Act. President Obama signed the Affordable Care Act (ACA) into law on March 23, 2010.

into law on March 23, 2010.") The Affordable Care Act President Obama signed the Affordable Care Act (ACA) into law on March 23, 2010. The ACA was enacted to: v Increase quality and affordability of health insurance v Lower the uninsured

The Affordable Care Act President Obama signed the Affordable Care Act (ACA) into law on March 23, 2010. The ACA was enacted to: v Increase quality and affordability of health insurance v Lower the uninsured

DC Health Benefit Exchange Authority

DC Health Benefit Exchange Authority STAFF PROPOSED BUDGET FY17 1 STAFF PROPOSED BUDGET- FY17 ORGANIZED TO REFLECT FUNCTION AREAS RED IDENTIFIES ACA REQUIRED FUNCTIONS EFFICIENCY: LEVERAGE DC GOV T AGENCIES;

DC Health Benefit Exchange Authority STAFF PROPOSED BUDGET FY17 1 STAFF PROPOSED BUDGET- FY17 ORGANIZED TO REFLECT FUNCTION AREAS RED IDENTIFIES ACA REQUIRED FUNCTIONS EFFICIENCY: LEVERAGE DC GOV T AGENCIES;

DC Office of Cable Television (OCT) CT0 Central Purpose Goals/Performance Measures Key Facts Programs/Services

CT0 Central Purpose Goals/Performance Measures Key Facts Programs/Services") DC Office of Cable Television (OCT) CT0 Eric E. Richardson, Executive Director 1899 9 th Street NE Washington, DC 20018 (202) 671-6600 http://www.oct.dc.gov/ Central Purpose The Office of Cable Television

DC Office of Cable Television (OCT) CT0 Eric E. Richardson, Executive Director 1899 9 th Street NE Washington, DC 20018 (202) 671-6600 http://www.oct.dc.gov/ Central Purpose The Office of Cable Television

6.0 SMALL BUSINESS HEALTH OPTIONS PROGRAM (SHOP)

") 6.0 SMALL BUSINESS HEALTH OPTIONS PROGRAM (SHOP) Summary Minnesota intends to implement and operate a State-Based Exchange per the requirements of the Affordable Care Act (ACA). This Exchange will meet

6.0 SMALL BUSINESS HEALTH OPTIONS PROGRAM (SHOP) Summary Minnesota intends to implement and operate a State-Based Exchange per the requirements of the Affordable Care Act (ACA). This Exchange will meet

CHARTER FOR THE HEALTH BENEFIT EXCHANGE AUTHORITY PREAMBLE ARTICLE I NAME. The District of Columbia Health Benefit Exchange Authority ( Authority).

.") CHARTER FOR THE HEALTH BENEFIT EXCHANGE AUTHORITY PREAMBLE The Health Benefit Exchange Authority of the District of Columbia is an independent authority of the District of Columbia government responsible

CHARTER FOR THE HEALTH BENEFIT EXCHANGE AUTHORITY PREAMBLE The Health Benefit Exchange Authority of the District of Columbia is an independent authority of the District of Columbia government responsible

HHealth HEALTH INSURANCE EXCHANGE FAQs

HHealth HEALTH INSURANCE EXCHANGE FAQs Page 1 TABLE OF CONTENTS Introduction... 3 Background... 3 Health Insurance Exchange FAQs... 4 What is the Patient Protection and Affordable Care Act (PPACA)?...

HHealth HEALTH INSURANCE EXCHANGE FAQs Page 1 TABLE OF CONTENTS Introduction... 3 Background... 3 Health Insurance Exchange FAQs... 4 What is the Patient Protection and Affordable Care Act (PPACA)?...

List of Insurance Terms and Definitions for Uniform Translation

Term actuarial value Affordable Care Act allowed charge Definition The percentage of total average costs for covered benefits that a plan will cover. For example, if a plan has an actuarial value of 70%,

Term actuarial value Affordable Care Act allowed charge Definition The percentage of total average costs for covered benefits that a plan will cover. For example, if a plan has an actuarial value of 70%,

A separate report is also included for the Office of Labor Relations and Collective Bargaining (OLRCB).

.") Office of the City Administrator (OCA) AE0 Allen Y. Lew, City Administrator 1350 Pennsylvania Avenue, NW, Suite 513 Washington, DC 20004 (202) 478-9200 http://oca.dc.gov/ Central Purpose The Office of

Office of the City Administrator (OCA) AE0 Allen Y. Lew, City Administrator 1350 Pennsylvania Avenue, NW, Suite 513 Washington, DC 20004 (202) 478-9200 http://oca.dc.gov/ Central Purpose The Office of

The New Health Law & Small Businesses

The New Health Law & Small Businesses October 2013 1 Goals of the New Health Law Affordable Care Act (ACA) Protect consumers against unfair insurance industry practices Give consumers more insurance options

The New Health Law & Small Businesses October 2013 1 Goals of the New Health Law Affordable Care Act (ACA) Protect consumers against unfair insurance industry practices Give consumers more insurance options

DC Health Link Executive Board Meeting

Health Benefit Exchange Authority Executive Board Meeting Draft Minutes for Wednesday, October 8, 2014 Date: Wednesday, October 8, 2014 Time: 5:30 PM Location: 1100 15 th St. NW, Suite 800 Call- in Number:

Health Benefit Exchange Authority Executive Board Meeting Draft Minutes for Wednesday, October 8, 2014 Date: Wednesday, October 8, 2014 Time: 5:30 PM Location: 1100 15 th St. NW, Suite 800 Call- in Number:

HUMAN RESOURCE EXECUTIVE WEBINAR PREPARING FOR HEALTH CARE EXCHANGES

HUMAN RESOURCE EXECUTIVE WEBINAR PREPARING FOR HEALTH CARE EXCHANGES FEBRUARY 13, 2013 Tracy Watts, Partner Mercer, Washington DC AGENDA FOR TODAY Evolution of health care benefits environment Public Exchanges

HUMAN RESOURCE EXECUTIVE WEBINAR PREPARING FOR HEALTH CARE EXCHANGES FEBRUARY 13, 2013 Tracy Watts, Partner Mercer, Washington DC AGENDA FOR TODAY Evolution of health care benefits environment Public Exchanges

A BILL IN THE COUNCIL OF THE DISTRICT OF COLUMBIA

1 1 1 1 1 1 1 1 0 1 0 1 Chairman Phil Mendelson at the request of the Mayor A BILL IN THE COUNCIL OF THE DISTRICT OF COLUMBIA Chairman Phil Mendelson, at the request of the Mayor, introduced the following

1 1 1 1 1 1 1 1 0 1 0 1 Chairman Phil Mendelson at the request of the Mayor A BILL IN THE COUNCIL OF THE DISTRICT OF COLUMBIA Chairman Phil Mendelson, at the request of the Mayor, introduced the following

Navigator, Agent and Broker Work Group

Minnesota Health Insurance Exchange Navigator, Agent and Broker Work Group Advisory Task Force Meeting October 24, 2012 Advisory Task Force Meeting Navigator, Agent & Broker Work Group October, 2012 Summary

Minnesota Health Insurance Exchange Navigator, Agent and Broker Work Group Advisory Task Force Meeting October 24, 2012 Advisory Task Force Meeting Navigator, Agent & Broker Work Group October, 2012 Summary

Affordable Care Act at 3: How Colorado s insurance exchange is gearing up for 2014

Affordable Care Act at 3: How Colorado s insurance exchange is gearing up for 2014 ISSUE BRIEF First in a series March 23, 2013 George Lyford Health Care Attorney 789 Sherman St. Suite 300 Denver, CO 80203

Affordable Care Act at 3: How Colorado s insurance exchange is gearing up for 2014 ISSUE BRIEF First in a series March 23, 2013 George Lyford Health Care Attorney 789 Sherman St. Suite 300 Denver, CO 80203

District of Columbia Health Benefits Exchange (DC HBX) Insurance Subcommittee FAQ: Small Business Owners and Producers (Insurance Agents & Brokers)

Insurance Subcommittee FAQ: Small Business Owners and Producers (Insurance Agents & Brokers)") District of Columbia Health Benefits Exchange (DC HBX) Insurance Subcommittee FAQ: Small Business Owners and Producers (Insurance Agents & Brokers) 1. Will small businesses be forced into the DC HBX to

District of Columbia Health Benefits Exchange (DC HBX) Insurance Subcommittee FAQ: Small Business Owners and Producers (Insurance Agents & Brokers) 1. Will small businesses be forced into the DC HBX to

Illinois Exchange Background Research and Needs Assessment Final Report and Findings. Governor s Reform Implementation Council October 14, 2011

Illinois Exchange Background Research and Needs Assessment Final Report and Findings Governor s Reform Implementation Council October 14, 2011 Research & Assessment Illinois, using Federal grant money,

Illinois Exchange Background Research and Needs Assessment Final Report and Findings Governor s Reform Implementation Council October 14, 2011 Research & Assessment Illinois, using Federal grant money,

State Roles in Implementing Health Insurance Exchanges

State Roles in Implementing Health Insurance Exchanges By Alex Azarian August 2012 Principal Policy Analyst The Affordable Care Act (ACA) requires states to establish competitive insurance marketplaces,

State Roles in Implementing Health Insurance Exchanges By Alex Azarian August 2012 Principal Policy Analyst The Affordable Care Act (ACA) requires states to establish competitive insurance marketplaces,

PART 1: ENABLING AUTHORITY AND GOVERNANCE

Application for Approval of an American Health Benefit Exchange On March 23, 2010, the President signed into law the Patient Protection and Affordable Care Act (P.L. 111-148). On March 30, 2010, the Health

Application for Approval of an American Health Benefit Exchange On March 23, 2010, the President signed into law the Patient Protection and Affordable Care Act (P.L. 111-148). On March 30, 2010, the Health

HEALTH INSURANCE EXCHANGE FAQS

HEALTH INSURANCE EXCHANGE FAQS 0 TABLE OF CONTENTS INTRODUCTION... 1 BACKGROUND... 1 HEALTH INSURANCE EXCHANGE FAQS... 1 1 INTRODUCTION IN EARLY 2010, CONGRESS PASSED THE PATIENT PROTECTION AND AFFORDABLE

HEALTH INSURANCE EXCHANGE FAQS 0 TABLE OF CONTENTS INTRODUCTION... 1 BACKGROUND... 1 HEALTH INSURANCE EXCHANGE FAQS... 1 1 INTRODUCTION IN EARLY 2010, CONGRESS PASSED THE PATIENT PROTECTION AND AFFORDABLE

Title Here Title Here Title

What You Need to Know about Health Insurance What You Need to Know about Health Insurance Choosing a Health Plan Keeping and Using Health Insurance Title How Here to Keep Title Your Here Marketplace Title

What You Need to Know about Health Insurance What You Need to Know about Health Insurance Choosing a Health Plan Keeping and Using Health Insurance Title How Here to Keep Title Your Here Marketplace Title

Shop. Compare. Choose.

Shop. Compare. Choose. Get access to robust choices on health plans Idaho Statistics Total population: 1,595,728 Median family income: $43,300 per year US Median family income: $50,054 per year Median

Shop. Compare. Choose. Get access to robust choices on health plans Idaho Statistics Total population: 1,595,728 Median family income: $43,300 per year US Median family income: $50,054 per year Median

Presentation for Licensed Producers The Affordable Care Act

Presentation for Licensed Producers The Affordable Care Act Bruce Donaldson, CHC Producer & Stakeholder Specialist Arkansas Insurance Department Affordable Care Act The ACA was passed by Congress and signed

Presentation for Licensed Producers The Affordable Care Act Bruce Donaldson, CHC Producer & Stakeholder Specialist Arkansas Insurance Department Affordable Care Act The ACA was passed by Congress and signed

FINAL BILL REPORT ESHB 1947

FINAL BILL REPORT C 6 L 13 E2 Synopsis as Enacted Brief Description: Concerning the operating expenses of the Washington health benefit exchange. Sponsors: House Committee on Appropriations (originally

FINAL BILL REPORT C 6 L 13 E2 Synopsis as Enacted Brief Description: Concerning the operating expenses of the Washington health benefit exchange. Sponsors: House Committee on Appropriations (originally

For The U.S. House of Representatives Committee on Energy and Commerce Subcommittee on Oversight and Investigations Hearing September 29, 2015

Written Statement For The U.S. House of Representatives Committee on Energy and Commerce Subcommittee on Oversight and Investigations Hearing September 29, 2015 By Patrick Allen, Director Department of

Written Statement For The U.S. House of Representatives Committee on Energy and Commerce Subcommittee on Oversight and Investigations Hearing September 29, 2015 By Patrick Allen, Director Department of

Fact Sheet. AARP Public Policy Institute. Health Reform Changes Insurance Rules

Fact Sheet Health Reform Changes Insurance Rules The Affordable Care Act (ACA) will greatly increase the availability of health insurance and broadly impact the delivery of health care in America. This

Fact Sheet Health Reform Changes Insurance Rules The Affordable Care Act (ACA) will greatly increase the availability of health insurance and broadly impact the delivery of health care in America. This

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE Scott Walker, Governor Theodore K. Nickel, Commissioner Wisconsin.gov 125 South Webster Street P.O. Box 7873 Madison, Wisconsin 53707-7873 Phone:

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE Scott Walker, Governor Theodore K. Nickel, Commissioner Wisconsin.gov 125 South Webster Street P.O. Box 7873 Madison, Wisconsin 53707-7873 Phone:

Department of Legislative Services Maryland General Assembly 2011 Session

Department of Legislative Services Maryland General Assembly 2011 Session HB 166 FISCAL AND POLICY NOTE Revised House Bill 166 (The Speaker, et al.) (By Request - Administration) Health and Government

Department of Legislative Services Maryland General Assembly 2011 Session HB 166 FISCAL AND POLICY NOTE Revised House Bill 166 (The Speaker, et al.) (By Request - Administration) Health and Government

Affordable Care Act HEALTHCARE.GOV. Marketplace Implementation Briefing Virginia Organizing Marketplace Public Forum August 20, 2013

HEALTHCARE.GOV Affordable Care Act Marketplace Implementation Briefing Virginia Organizing Marketplace Public Forum August 20, 2013 Joanne Corte Grossi, MIPP Regional Director U.S. Department of Health

HEALTHCARE.GOV Affordable Care Act Marketplace Implementation Briefing Virginia Organizing Marketplace Public Forum August 20, 2013 Joanne Corte Grossi, MIPP Regional Director U.S. Department of Health

OVERVIEW OF PRIVATE INSURANCE MARKET REFORMS IN THE PATIENT PROTECTION AND AFFORDABLE CARE ACT AND RESOURCES FOR FREQUENTLY ASKED QUESTIONS

OVERVIEW OF PRIVATE INSURANCE MARKET REFORMS IN THE PATIENT PROTECTION AND AFFORDABLE CARE ACT AND RESOURCES FOR FREQUENTLY ASKED QUESTIONS Brief Prepared by MATTHEW COKE Senior Research Attorney LEGISLATIVE

OVERVIEW OF PRIVATE INSURANCE MARKET REFORMS IN THE PATIENT PROTECTION AND AFFORDABLE CARE ACT AND RESOURCES FOR FREQUENTLY ASKED QUESTIONS Brief Prepared by MATTHEW COKE Senior Research Attorney LEGISLATIVE

How To Get Health Care Reform For The United States

Federal Health Care Reform: Implications for New York Division of Coverage and Enrollment Office of Health Insurance Programs Health Bureau Insurance Department June 2010 Federal Health Care Reform: Where

Federal Health Care Reform: Implications for New York Division of Coverage and Enrollment Office of Health Insurance Programs Health Bureau Insurance Department June 2010 Federal Health Care Reform: Where

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS. New York Edition

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS New York Edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM PAGE 2 www.discovermvp.com There s a constant stream of changes and updates related

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS New York Edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM PAGE 2 www.discovermvp.com There s a constant stream of changes and updates related

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE Scott Walker, Governor Theodore K. Nickel, Commissioner Wisconsin.gov 125 South Webster Street P.O. Box 7873 Madison, Wisconsin 53707-7873 Phone:

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE Scott Walker, Governor Theodore K. Nickel, Commissioner Wisconsin.gov 125 South Webster Street P.O. Box 7873 Madison, Wisconsin 53707-7873 Phone:

The Vermont Health Benefit Exchange: An Update for Small Business Owners

The Vermont Health Benefit Exchange: An Update for Small Business Owners Today s Presentation Health Reform Goals Overview of Health Care Reform What is the Exchange? What Does the Exchange Look Like?

The Vermont Health Benefit Exchange: An Update for Small Business Owners Today s Presentation Health Reform Goals Overview of Health Care Reform What is the Exchange? What Does the Exchange Look Like?

Health Care Reform Frequently Asked Questions (FAQ) Consumers Employers

Consumers Employers") This page provides answers to frequently asked questions (FAQ) regarding The Patient Protection and Affordable Care Act (PPACA; P.L. 111-148) and the Health Care and Education Reconciliation Act of 2010

This page provides answers to frequently asked questions (FAQ) regarding The Patient Protection and Affordable Care Act (PPACA; P.L. 111-148) and the Health Care and Education Reconciliation Act of 2010

12 LC 33 4535 A BILL TO BE ENTITLED AN ACT

Senate Bill 418 By: Senators Orrock of the 36th, Henson of the 41st, Tate of the 38th, Fort of the 39th, Davis of the 22nd and others A BILL TO BE ENTITLED AN ACT 1 2 3 4 5 6 7 8 9 To amend Title 33 of

Senate Bill 418 By: Senators Orrock of the 36th, Henson of the 41st, Tate of the 38th, Fort of the 39th, Davis of the 22nd and others A BILL TO BE ENTITLED AN ACT 1 2 3 4 5 6 7 8 9 To amend Title 33 of

City of Glendale KeenanDirect for Early Retirees Futuris Care for Medicare Eligible Retirees Overview September 3, 2015

City of Glendale KeenanDirect for Early Retirees Futuris Care for Medicare Eligible Retirees Overview September 3, 2015 Enrollment Calendar 2016 Covered California and the Federal Marketplace For Early

City of Glendale KeenanDirect for Early Retirees Futuris Care for Medicare Eligible Retirees Overview September 3, 2015 Enrollment Calendar 2016 Covered California and the Federal Marketplace For Early

American Health Benefit Exchanges Fact Sheet A Provision of the Patient Protection and Affordable Care Act (PPACA)

") American Health Benefit Exchanges Fact Sheet A Provision of the Patient Protection and Affordable Care Act (PPACA) This Fact Sheet reflects the Final Ruling published by the Department of Health and Human

American Health Benefit Exchanges Fact Sheet A Provision of the Patient Protection and Affordable Care Act (PPACA) This Fact Sheet reflects the Final Ruling published by the Department of Health and Human

HEALTH BENEFIT EXCHANGE SURVIVAL GUIDE FOR SMALL BUSINESS. New York Edition

HEALTH BENEFIT EXCHANGE SURVIVAL GUIDE FOR SMALL BUSINESS New York Edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM PAGE 2 www.discovermvp.com There s a constant stream of changes and updates related

HEALTH BENEFIT EXCHANGE SURVIVAL GUIDE FOR SMALL BUSINESS New York Edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM PAGE 2 www.discovermvp.com There s a constant stream of changes and updates related

Arkansas Private Option 1115 Demonstration Waiver

Arkansas Private Option 1115 Demonstration Waiver Quarterly Report October 1, 2014 to December 31, 2014 Arkansas Private Option Quarterly Report October December 2014 Page 1 I. Executive Summary of Significant

Arkansas Private Option 1115 Demonstration Waiver Quarterly Report October 1, 2014 to December 31, 2014 Arkansas Private Option Quarterly Report October December 2014 Page 1 I. Executive Summary of Significant

REGULATORY UPDATE Vol. 1 No. 18

REGULATORY UPDATE Vol. 1 No. 18 FAQs on Exchanges August 7, 2013 IN THIS ISSUE FAQs on Exchanges Employer Mandate Delay Transitional Guidance Issued Individual Mandate Final Rules Issued Possible Exchange

REGULATORY UPDATE Vol. 1 No. 18 FAQs on Exchanges August 7, 2013 IN THIS ISSUE FAQs on Exchanges Employer Mandate Delay Transitional Guidance Issued Individual Mandate Final Rules Issued Possible Exchange

United States Government Accountability Office March 2011 GAO-11-268

GAO United States Government Accountability Office Report to the Secretary of Health and Human Services and the Secretary of Labor March 2011 PRIVATE HEALTH INSURANCE Data on Application and Coverage Denials

GAO United States Government Accountability Office Report to the Secretary of Health and Human Services and the Secretary of Labor March 2011 PRIVATE HEALTH INSURANCE Data on Application and Coverage Denials

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS. Vermont Edition

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS Vermont Edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM There s a constant stream of changes and updates related to health care reform,

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS Vermont Edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM There s a constant stream of changes and updates related to health care reform,

HEALTH INSURANCE REFORM in ILLINOIS

HEALTH INSURANCE REFORM in ILLINOIS Overview of Federal Health Insurance Reform Requirements Illinois Department of Insurance Implementation Planning PAT QUINN Governor MICHAEL T. McRAITH Director May

HEALTH INSURANCE REFORM in ILLINOIS Overview of Federal Health Insurance Reform Requirements Illinois Department of Insurance Implementation Planning PAT QUINN Governor MICHAEL T. McRAITH Director May

A review of the Small Group Health Insurance Market in Maryland March 2015

Creation of the Maryland Health insurance Partnership Senate Bill 6 (SB 6), the Working Families and Small Business Health Coverage Act, (effective July 1, 2008), created the Health Insurance Partnership,

Creation of the Maryland Health insurance Partnership Senate Bill 6 (SB 6), the Working Families and Small Business Health Coverage Act, (effective July 1, 2008), created the Health Insurance Partnership,

Understanding the Health Insurance Marketplace. August 2013

Understanding the Health Insurance Marketplace August 2013 Objectives This session will help you Explain the Health Insurance Marketplace Identify who will benefit Define who is eligible Explain the enrollment

Understanding the Health Insurance Marketplace August 2013 Objectives This session will help you Explain the Health Insurance Marketplace Identify who will benefit Define who is eligible Explain the enrollment

Affordable Care Act: Outreach, Education and Enrollment

Affordable Care Act: Outreach, Education and Enrollment Deepti A. Loharikar Health Policy Analyst Department of Health and Human Services Health Resources and Services Administration What is the Affordable

Affordable Care Act: Outreach, Education and Enrollment Deepti A. Loharikar Health Policy Analyst Department of Health and Human Services Health Resources and Services Administration What is the Affordable

Covering the Uninsured Through DC Health Link: Report on the First Year

Covering the Uninsured Through DC Health Link: Report on the First Year Uninsured rate drops by as much as 43 percent in the District By Leighton Ku, PhD, MPH* December 26, 2014 *This analysis was conducted

Covering the Uninsured Through DC Health Link: Report on the First Year Uninsured rate drops by as much as 43 percent in the District By Leighton Ku, PhD, MPH* December 26, 2014 *This analysis was conducted

The Small Business Health Options Program SHOP. A service of Maryland Health Benefit Exchange

The Small Business Health Options Program SHOP A service of Maryland Health Benefit Exchange What is the SHOP? SHOP = the Small Business Health Options Program The SHOP helps small business owners enroll

The Small Business Health Options Program SHOP A service of Maryland Health Benefit Exchange What is the SHOP? SHOP = the Small Business Health Options Program The SHOP helps small business owners enroll

5Want to know more about the health

www. WHAT S INSIDE STEPS TO UNDERSTANDING OBAMACARE Introduction 4 Step 1 Does your current health insurance plan need to change? 6 Step 2 How will you pay for health insurance in 2014? 10 Step 3 What

www. WHAT S INSIDE STEPS TO UNDERSTANDING OBAMACARE Introduction 4 Step 1 Does your current health insurance plan need to change? 6 Step 2 How will you pay for health insurance in 2014? 10 Step 3 What

One of the more visible changes soon to be brought MONTANA S HEALTH INSURANCE A PREVIEW OF MARKETPLACE

A PREVIEW OF MONTANA S HEALTH INSURANCE MARKETPLACE by Gregg Davis and Christina Goe One of the more visible changes soon to be brought to the forefront by passage of the Affordable Care Act (ACA) is the

A PREVIEW OF MONTANA S HEALTH INSURANCE MARKETPLACE by Gregg Davis and Christina Goe One of the more visible changes soon to be brought to the forefront by passage of the Affordable Care Act (ACA) is the

Small Business Tax Credit

Small Business Tax Credit Effective January 1, 2010 Up to 4 million small businesses are eligible for tax credits to help them provide insurance benefits to their workers. The first phase of this provision

Small Business Tax Credit Effective January 1, 2010 Up to 4 million small businesses are eligible for tax credits to help them provide insurance benefits to their workers. The first phase of this provision

Affordable Care Act: Key Provisions for People with MS

Affordable Care Act: Key Provisions for People with MS October 2013 Why reform healthcare? By 2008, 15% of the U.S. population, or approximately 47 million Americans, lacked health insurance Documented

Affordable Care Act: Key Provisions for People with MS October 2013 Why reform healthcare? By 2008, 15% of the U.S. population, or approximately 47 million Americans, lacked health insurance Documented

INDIVIDUAL HEALTH INSURANCE In Maine

A Consumer s Guide To... INDIVIDUAL HEALTH INSURANCE In Maine Published by: The Maine Bureau of Insurance September 2015 Paul R. LePage Governor Eric A. Cioppa Superintendent Basics of Individual Health

A Consumer s Guide To... INDIVIDUAL HEALTH INSURANCE In Maine Published by: The Maine Bureau of Insurance September 2015 Paul R. LePage Governor Eric A. Cioppa Superintendent Basics of Individual Health

Washington Health Benefit Exchange. Leading Age 2014 Annual Conference. Phil Dyer Board Member

Washington Health Benefit Exchange Leading Age 2014 Annual Conference Phil Dyer Board Member DISCLAIMER; The views and information expressed are my personal opinions and perspectives and do not represent

Washington Health Benefit Exchange Leading Age 2014 Annual Conference Phil Dyer Board Member DISCLAIMER; The views and information expressed are my personal opinions and perspectives and do not represent

Patient Protection and Affordable Care Act (ACA) ACA Guide for Group Employers Employer Information

ACA Guide for Group Employers Employer Information") Patient Protection and Affordable Care Act (ACA) ACA Guide for Group Employers Employer Information DISCLAIMER 2 This information is being provided in an effort to alert you to changes required by the

Patient Protection and Affordable Care Act (ACA) ACA Guide for Group Employers Employer Information DISCLAIMER 2 This information is being provided in an effort to alert you to changes required by the

An Overview. James L. Sugden, CLU Small Business Health Plan Manager

An Overview James L. Sugden, CLU Small Business Health Plan Manager What is Connect for Health Colorado An open, competitive marketplace for individuals and small employers to: Compare information regarding

An Overview James L. Sugden, CLU Small Business Health Plan Manager What is Connect for Health Colorado An open, competitive marketplace for individuals and small employers to: Compare information regarding

Guide to Health Care Reform

Guide to Health Care Reform 2 0 1 5 Navigating the changing landscape The first year of health care reform may be over but it may have left you with more questions than ever. You probably want to know

Guide to Health Care Reform 2 0 1 5 Navigating the changing landscape The first year of health care reform may be over but it may have left you with more questions than ever. You probably want to know

WE RE HERE TO HELP YOU TRANSITION TO THE NEW HEALTH BENEFIT EXCHANGE

HEALTH CARE REFORM: INFORMATION VERMONTERS NEED TO KNOW The Federal Affordable Care Act means new health insurance products, new rules and new systems for purchasing plans beginning in 2013. Blue Cross

HEALTH CARE REFORM: INFORMATION VERMONTERS NEED TO KNOW The Federal Affordable Care Act means new health insurance products, new rules and new systems for purchasing plans beginning in 2013. Blue Cross

Key Facts About the Small Business Health Options Program (SHOP) Marketplace

Marketplace") Key Facts About the Small Business Health Options Program (SHOP) Marketplace The Small Business Health Options Program (SHOP) Marketplace is now open and ready to help you get health coverage for your

Key Facts About the Small Business Health Options Program (SHOP) Marketplace The Small Business Health Options Program (SHOP) Marketplace is now open and ready to help you get health coverage for your

Covered California Participant Guide Course Name: Covered California for Small Business Version 4.0 1. COURSE OBJECTIVES... 3

Covered California Participant Guide Course Name: Covered California for Small Business Covered California for Small Business Participant Guide Version 4.0 Version 4.0 TABLE CONTENTS 1. COURSE OBJECTIVES...

Covered California Participant Guide Course Name: Covered California for Small Business Covered California for Small Business Participant Guide Version 4.0 Version 4.0 TABLE CONTENTS 1. COURSE OBJECTIVES...

Affordable Insurance Exchanges: Choices, Competition and Clout for States

Page 1 of 5 Newsroom Affordable Insurance Exchanges: Choices, Competition and Clout for States On March 12, 2012, the U.S. Department of Health and Human Services (HHS) published a final rule on Affordable

Page 1 of 5 Newsroom Affordable Insurance Exchanges: Choices, Competition and Clout for States On March 12, 2012, the U.S. Department of Health and Human Services (HHS) published a final rule on Affordable

Utah s Marketplace Approach

Utah s Marketplace Approach Utah s approach to health care reform preserves Utah s state based, private market solution. Under Governor Gary R. Herbert s plan, the state will continue to operate Avenue

Utah s Marketplace Approach Utah s approach to health care reform preserves Utah s state based, private market solution. Under Governor Gary R. Herbert s plan, the state will continue to operate Avenue

Patient Protection and Affordable Care Act (ACA) ACA Guide for Group Employers Agent and Broker Information

ACA Guide for Group Employers Agent and Broker Information") Patient Protection and Affordable Care Act (ACA) ACA Guide for Group Employers Agent and Broker Information DISCLAIMER 2 This information is being provided in an effort to alert you to changes required

Patient Protection and Affordable Care Act (ACA) ACA Guide for Group Employers Agent and Broker Information DISCLAIMER 2 This information is being provided in an effort to alert you to changes required

David Lyons Founding Director and Chief Executive Officer

The New Health Insurance Marketplace Changes Impacting Small Employers and the SHOP Opportunity David Lyons Founding Director and Chief Executive Officer CoOportunity Health 10/1/2013 1 Why the Change?

The New Health Insurance Marketplace Changes Impacting Small Employers and the SHOP Opportunity David Lyons Founding Director and Chief Executive Officer CoOportunity Health 10/1/2013 1 Why the Change?

Federal Health Reform FAQs

Federal Health Reform FAQs Individuals 1. What is an exchange? An exchange, as created under the Affordable Care Act (ACA), is a place where consumers can purchase subsidized health insurance coverage.

Federal Health Reform FAQs Individuals 1. What is an exchange? An exchange, as created under the Affordable Care Act (ACA), is a place where consumers can purchase subsidized health insurance coverage.

Health Care Reform. Overview of Federal Health Insurance Reform Requirements and TDI Implementation Planning

Health Care Reform Overview of Federal Health Insurance Reform Requirements and TDI Implementation Planning Presentation to House Select Committee on Federal Legislation April 22, 2010 Mike Geeslin, Commissioner

Health Care Reform Overview of Federal Health Insurance Reform Requirements and TDI Implementation Planning Presentation to House Select Committee on Federal Legislation April 22, 2010 Mike Geeslin, Commissioner

New York Health Benefit Exchange & Small Business Health Options Program (SHOP) Frequently Asked Questions for Agents and Brokers

Frequently Asked Questions for Agents and Brokers") New York Health Benefit Exchange & Small Business Health Options Program (SHOP) Frequently Asked Questions for Agents and Brokers May 9, 2013 Carrier Participation in the Exchange 1. Q: What carriers have

New York Health Benefit Exchange & Small Business Health Options Program (SHOP) Frequently Asked Questions for Agents and Brokers May 9, 2013 Carrier Participation in the Exchange 1. Q: What carriers have

SURVIVAL GUIDE FOR SMALL BUSINESS

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS New York edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM PAGE 2 www.discovermvp.com There s a constant stream of changes and updates related

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS New York edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM PAGE 2 www.discovermvp.com There s a constant stream of changes and updates related

INDIVIDUAL HEALTH INSURANCE GUIDE. Introduction. What is the Health Insurance Marketplace?

INDIVIDUAL HEALTH INSURANCE GUIDE Introduction On November 15th, 2014, the second annual Open Enrollment Period for Individual Health Insurance begins. The Affordable Care Act (ACA) requires all US citizens

INDIVIDUAL HEALTH INSURANCE GUIDE Introduction On November 15th, 2014, the second annual Open Enrollment Period for Individual Health Insurance begins. The Affordable Care Act (ACA) requires all US citizens

Illinois Exchange Needs Assessment Final Report and Findings

Illinois Exchange Needs Assessment Final Report and Findings Illinois Health Benefits Exchange Legislative Study Committee September 21, 2011 Illinois Exchange Planning Project The HMA Team Health Management

Illinois Exchange Needs Assessment Final Report and Findings Illinois Health Benefits Exchange Legislative Study Committee September 21, 2011 Illinois Exchange Planning Project The HMA Team Health Management

Mississippi Insurance Department. 1001 Woolfolk State Office Building 501 North West Street Jackson, Mississippi 39201

Mississippi Insurance Department 1001 Woolfolk State Office Building 501 North West Street Jackson, Mississippi 39201 1 What is an Exchange? Essentially, an Exchange is a marketplace for major medical

Mississippi Insurance Department 1001 Woolfolk State Office Building 501 North West Street Jackson, Mississippi 39201 1 What is an Exchange? Essentially, an Exchange is a marketplace for major medical

The New Health Insurance Marketplace. Choices and Opportunities for Small Groups

The New Health Insurance Marketplace Choices and Opportunities for Small Groups What is the Affordable Care Act? The Patient Protection and Affordable Care Act (ACA) was signed into law on March 23, 2010

The New Health Insurance Marketplace Choices and Opportunities for Small Groups What is the Affordable Care Act? The Patient Protection and Affordable Care Act (ACA) was signed into law on March 23, 2010

PRIVATE HEALTH INSURANCE. Early Effects of Medical Loss Ratio Requirements and Rebates on Insurers and Enrollees

United States Government Accountability Office Report to the Chairman, Committee on Commerce, Science, and Transportation, U.S. Senate July 2014 PRIVATE HEALTH INSURANCE Early Effects of Medical Loss Ratio

United States Government Accountability Office Report to the Chairman, Committee on Commerce, Science, and Transportation, U.S. Senate July 2014 PRIVATE HEALTH INSURANCE Early Effects of Medical Loss Ratio

Healthcare Reform and California Small Businesses

Healthcare Reform and California Small Businesses How the new law impacts your bottom line David Chase March 26, 2013 Lancaster, California About Small Business Majority Small business advocacy organization

Healthcare Reform and California Small Businesses How the new law impacts your bottom line David Chase March 26, 2013 Lancaster, California About Small Business Majority Small business advocacy organization

Gary Cohen, CMS Deputy Administrator and Director Center for Consumer Information and Insurance Oversight (CCIIO)

") DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services Room 352-G 200 Independence Avenue, SW Washington, DC 20201 Date: July 12, 2013 From: Subject: Gary Cohen, CMS Deputy Administrator

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services Room 352-G 200 Independence Avenue, SW Washington, DC 20201 Date: July 12, 2013 From: Subject: Gary Cohen, CMS Deputy Administrator

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE Scott Walker, Governor Theodore K. Nickel, Commissioner Wisconsin.gov 125 South Webster Street P.O. Box 7873 Madison, Wisconsin 53707-7873 Phone:

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE Scott Walker, Governor Theodore K. Nickel, Commissioner Wisconsin.gov 125 South Webster Street P.O. Box 7873 Madison, Wisconsin 53707-7873 Phone:

Nevada Silver State Exchange QHP Issuer Onboarding Meeting. May 22, 2013

Nevada Silver State Exchange QHP Issuer Onboarding Meeting May 22, 2013 Customer Service Meeting Objectives Introductions Customer Assistance Options Producers Exchange Enrollment Facilitators (EEFs) Customer

Nevada Silver State Exchange QHP Issuer Onboarding Meeting May 22, 2013 Customer Service Meeting Objectives Introductions Customer Assistance Options Producers Exchange Enrollment Facilitators (EEFs) Customer

U.S. Department of Health and Human Services Office of Consumer Information and Insurance Oversight

U.S. Department of Health and Human Services Office of Consumer Information and Insurance Oversight Cooperative Agreement to Support Establishment of State-Operated Health Insurance Exchanges New Announcement

U.S. Department of Health and Human Services Office of Consumer Information and Insurance Oversight Cooperative Agreement to Support Establishment of State-Operated Health Insurance Exchanges New Announcement

Kansas Insurance Department

Kansas Insurance Department A Kansas Guide to Health Insurance Changes Public Policy Session Panel Discussion KAMU Annual Conference Sept. 26, 2013 Sandy Praeger, Commissioner of Insurance 2014 Affordable

Kansas Insurance Department A Kansas Guide to Health Insurance Changes Public Policy Session Panel Discussion KAMU Annual Conference Sept. 26, 2013 Sandy Praeger, Commissioner of Insurance 2014 Affordable

Final Regulations on Health Insurance Exchanges

Health Care Reform Legislative Brief Final Regulations on Health Insurance Exchanges Beginning in 2014, individuals and small businesses will be able to purchase private health insurance through state-based

Health Care Reform Legislative Brief Final Regulations on Health Insurance Exchanges Beginning in 2014, individuals and small businesses will be able to purchase private health insurance through state-based

Nebraska Health Insurance Exchange Update

Nebraska Health Insurance Exchange Update State of Nebraska s Health Insurance Exchange A Presentation to Advocacy Groups August 2012 TODAY'S AGENDA Section 1: Overview of Health Insurance Exchanges Section

Nebraska Health Insurance Exchange Update State of Nebraska s Health Insurance Exchange A Presentation to Advocacy Groups August 2012 TODAY'S AGENDA Section 1: Overview of Health Insurance Exchanges Section

State of Oregon Health Insurance Market - Plans for 2015

Oregon Health Insurance Marketplace Report to the Joint Interim Committee on Ways and Means and Interim Senate and House Committees on Health Care September 2015 Department of Consumer and Business Services

Oregon Health Insurance Marketplace Report to the Joint Interim Committee on Ways and Means and Interim Senate and House Committees on Health Care September 2015 Department of Consumer and Business Services

SHOP and the Small Group Market Policies

SHOP and the Small Group Market Policies DEPARTMENT OF HEALTH AND HUMAN SERVICES CENTERS for MEDICARE & MEDICAID SERVICES Center for Consumer Information and Insurance Oversight Health Insurance Exchange

SHOP and the Small Group Market Policies DEPARTMENT OF HEALTH AND HUMAN SERVICES CENTERS for MEDICARE & MEDICAID SERVICES Center for Consumer Information and Insurance Oversight Health Insurance Exchange

Eligibility and Enrollment for Small Business Health Option Program (SHOP) Participant Guide. Version 2.0

Participant Guide. Version 2.0") Eligibility and Enrollment for Small Business Health Option Program (SHOP) Participant Guide Version 2.0 Course Name: Eligibility and Enrollment for SHOP Version 2.0 TABLE OF CONTENTS 1 INTRODUCTION...

Eligibility and Enrollment for Small Business Health Option Program (SHOP) Participant Guide Version 2.0 Course Name: Eligibility and Enrollment for SHOP Version 2.0 TABLE OF CONTENTS 1 INTRODUCTION...

Health Insurance Marketplace. vhealth insurance exchanges. What to expect in 2014. What to expect in 2014

vhealth insurance exchanges Health Insurance Marketplace What to expect in 2014 What to expect in 2014 The basics of exchanges As part of the Affordable Care Act (ACA or health care reform law), starting

vhealth insurance exchanges Health Insurance Marketplace What to expect in 2014 What to expect in 2014 The basics of exchanges As part of the Affordable Care Act (ACA or health care reform law), starting

B. Justification. 1. Need and Legal Basis

Supporting Statement for Data Collection to Support Eligibility Determinations for and Enrollment through Affordable Exchanges, Medicaid and Children s Health Program Agencies A. Background On March 23,

Supporting Statement for Data Collection to Support Eligibility Determinations for and Enrollment through Affordable Exchanges, Medicaid and Children s Health Program Agencies A. Background On March 23,

Health Care Reform & The Health Insurance Marketplace. Presented by Mikal A Jeffries, CEBS Account Manager

Health Care Reform & The Health Insurance Marketplace Presented by Mikal A Jeffries, CEBS Account Manager 1 Health Care Reform Review Goals of Health Care Reform Increase number of Americans with health

Health Care Reform & The Health Insurance Marketplace Presented by Mikal A Jeffries, CEBS Account Manager 1 Health Care Reform Review Goals of Health Care Reform Increase number of Americans with health

Nebraska Health Insurance Exchange Update

Nebraska Health Insurance Exchange Update Overview of the Affordable Care Act and the Federally Facilitated marketplace. September 2015 AFFORDABLE CARE ACT OVERVIEW» The Affordable Care Act was enacted

Nebraska Health Insurance Exchange Update Overview of the Affordable Care Act and the Federally Facilitated marketplace. September 2015 AFFORDABLE CARE ACT OVERVIEW» The Affordable Care Act was enacted

AmeriCorps State and National Member Health Care Q & A

1 General AmeriCorps State and National Member Health Care Q & A Q1: Previously CNCS shared that they will not be changing the FY 2014 grant provisions with respect to the healthcare grantees are required

1 General AmeriCorps State and National Member Health Care Q & A Q1: Previously CNCS shared that they will not be changing the FY 2014 grant provisions with respect to the healthcare grantees are required

The District of Columbia

The District of Columbia Health Benefits Exchange Proposal October 2012 Questions and Answers For Residents and Small Businesses Q. What is the Health Benefits Exchange? A. The Health Benefits Exchange

The District of Columbia Health Benefits Exchange Proposal October 2012 Questions and Answers For Residents and Small Businesses Q. What is the Health Benefits Exchange? A. The Health Benefits Exchange

SHOP Exchange Technology Enablement Options. March 13, 2012

SHOP Exchange Technology Enablement Options March 13, 2012 Agenda 1. SHOP Overview 2. SHOP Principles 3. Design Options 4. Option Comparisons 5. Timeline and Recommendation - 1 - Overview: Small Business

SHOP Exchange Technology Enablement Options March 13, 2012 Agenda 1. SHOP Overview 2. SHOP Principles 3. Design Options 4. Option Comparisons 5. Timeline and Recommendation - 1 - Overview: Small Business

Small Business Guide to. A resource for users of the DC Health Link Small Business Marketplace, including employers and their brokers.

Small Business Guide to A resource for users of the DC Health Link Small Business Marketplace, including employers and their brokers. Table of Contents 1 What is DC Health Link?... 4 1.1 Who Can Participate

Small Business Guide to A resource for users of the DC Health Link Small Business Marketplace, including employers and their brokers. Table of Contents 1 What is DC Health Link?... 4 1.1 Who Can Participate

Oregon Health Insurance Marketplace Report to the Joint Interim Committee on Ways and Means and Interim Senate and House Committees on Health Care

Oregon Health Insurance Marketplace Report to the Joint Interim Committee on Ways and Means and Interim Senate and House Committees on Health Care November 2015 Department of Consumer and Business Services

Oregon Health Insurance Marketplace Report to the Joint Interim Committee on Ways and Means and Interim Senate and House Committees on Health Care November 2015 Department of Consumer and Business Services