The Use of Captive Insurance Companies for Closely Held Businesses

|

|

|

- Gloria Lamb

- 8 years ago

- Views:

Transcription

1 The Use of Captive Insurance Companies for Closely Held Businesses Presented by: Michael F. Amoia, J.D., LL.M., CFP, CLU, ChFC CRUMP LIFE INSURANCE SERVICES Senior Vice President, Advanced Planning and Life Product Bethesda, MD

2 Disclosure This material contains references to concepts that have significant legal, accounting, and tax implications. It is not intended as legal, accounting or tax advice. Clients should always consult their own attorney and/or tax advisor for advice regarding application of these concepts to their particular situation. CIRCULAR 230 DISCLAIMER To ensure compliance with requirements imposed by the IRS, we inform you that, unless expressly stated otherwise, any U.S. federal tax advice contained in this communication (including any attachments) is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter addressed herein.

3 TODAY S DISCUSSION Insure risks otherwise not insurable Managing insurance exposures and expenses Current income tax considerations Estate tax benefits Key employee incentives

4 INSURANCE OPTIONS Captive Insurance Companies Allow Successful Companies to Shift Risk

5

6 Identifying Risk INSURED RISK UNINSURED RISK 6

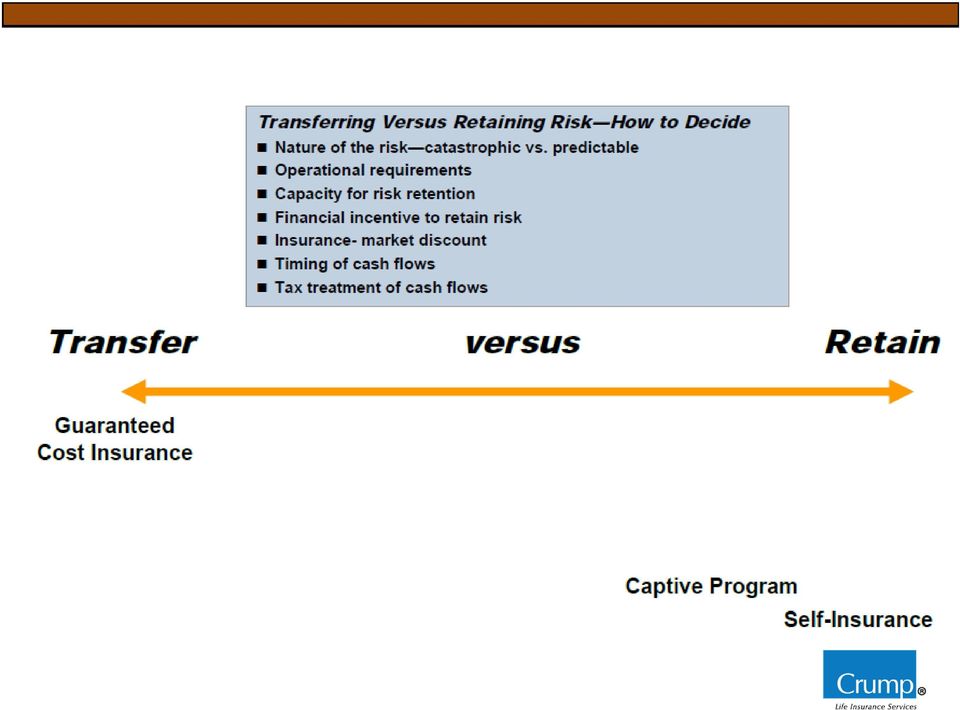

7 To Insure Or Not Insure Balancing between Commercial Insurance and Self Insuring Commercial Insurer Unacceptable Risk Business Manageable Risk Cash Reserve Deduct When Pay Premiums No Deduction Until Claim Paid

8 Analyze the Inefficiencies Pertaining to Your Firms Risk Management Strategy How commercial insurance premiums are calculated 50% of Premium Expected Loss Administration Insurance companies typically price property and casualty insurance at a 50-60% loss ratio Up to 50% is allocated for claims administration, overhead, and profit for the insurer Overhead and Profit 8

9 Captive Insurance Programs How does a captive reduce the net cost of risk? Carefully analyze risk exposure Transfer unacceptable levels of risk to others (via commercial insurance) Incorporate safety and loss prevention measurers Participate in underwriting profits Shareholder Commercial Insurer Unacceptable Risk Sponsor Manageable Risk Captive

10 What is a captive? 10 Private insurance company structured to provide insurance or reinsurance to related entities Captive History First captive believed to have been formed in 1922 (Guernsey) Approximately 10,000 captives in operation Offshore Jurisdictions (Cayman, British Virgin Islands, Bermuda) 1 st On-shore Jurisdiction (Colorado Captive Insurance Act of 1972) Majority of States allow Captive formation Case Law (Humana/Harper Group/UPS) Harvard Medical school was the first domestic captive to manage their med-mal risks IRS guidance Revenue Ruling Safe Harbors

Majority of States allow Captive formation Case Law (Humana/Harper")

11 Potential Insurance Benefits Insurance Costs: Reduced premiums for P&C coverage. Reduced funding for self-insured risks. Adjustment of risk retention levels as needed. Take Advantage of Good Loss Experience Allow Control of the Claims Process Allow Control of Investment of Reserves Access to the Reinsurance Market Estate Planning Opportunities

12 Industries to Consider Builders / Contractors Manufacturers Trucking Franchisees Hotel Chains Private Equity Healthcare

13 What they are and are not Must have a business purpose to it Is not just a tax strategy Is not quick it takes time Is not tax deductible life insurance

14 What is a Captive? Captive Insurance for Qualified Businesses Private Insurance Company Pure captive Association captive Group captive Agency captive Rent-a-captive Protected cell captive Domestic or International 14

15 Captive Insurance Programs Captive Insurance Company (Pure Captive) Shareholder Business Premiums Captive Insurance Policies

16 Income Taxation: Income Tax Issues Deductibility of Premiums. Premiums paid to an insurance company, including a captive, are deductible. Corporate Status. For Federal income tax purposes, an insurance company is a per secorporation. It must pay a corporate level tax and will not receive flow-through or disregarded-entity treatment. Insurance Tax Accounting. If a company qualifies as an insurance company, insurance-tax accounting (under Subchapter L) applies. Favorable Tax Treatment. Insurance tax accounting may provide certain tax benefits to a captive, including: Acceleration of Tax Deductions. A captive can take a current income tax deduction for amounts needed to fund future claims. Self-insured businesses can only deduct claims when paid.

17 Small/Micro Captives 831(b) Captive If premiums less than $1.2 million/year, no tax on premium income However, not a panacea Tax is paid on investment income at corporate rates C-Corporations pay higher capital gains rate than individuals Real estate is generally a poor investment choice Corporate AMT may apply to death benefit paid to a C-Corp Caveat: Beware of captives promoted to buy tax deductible life insurance

18 Federal Income Taxation The IRS and Captives What constitutes insurance? IS NOT an off balance sheet self-insurance structure IS: Bona-fide business purpose Operates as an insurance company Risk shifting» Risk must be transferred Risk distribution» Risk must be spread» The law of large numbers must apply Reasonable premiums Adequate capitalization For Provider Use Only

19 Federal Income Taxation RISK DISTRIBUTION AND SHIFTING What is insurance? Testing for Risk Shifting and Risk Distribution Helveringv. Le Gierse, 312 U.S. 531 (1941) Uninsurable 80-year-old woman purchased a life policy and an annuity policy from the same insurance company one month before death Executor did not report death benefit on estate tax return Supreme Court found no risk shifted because of offsetting positions; this was just an attempted tax avoidance First case to set forth the standard for true insurance as required to have both risk shifting and risk distribution

20 Federal Income Taxation RISK DISTRIBUTION AND SHIFTING Case law developed two theories: Theory 1 (third-party theory): Sufficient third-party premium along with premiums from related entities Courts say 30% third-party insurance is adequate Theory 2 (balance sheet theory): Sufficient number of related party entities insured to create risk distribution and shifting

: Sufficient number of related party entities insured to create risk distribution")

21 Federal Income Taxation RISK DISTRIBUTION AND SHIFTING Revenue Ruling , C.B Service determines it will no longer raise the economic family theory Explicitly acknowledged that no court had fully adopted the economic family theory set forth in Rev. Rul Analysis is now a case-by-case analysis Service promised more challenges based on facts and circumstances Focus is on risk shifting, risk distribution, inadequate capitalization, and parental guarantees

22 Significant IRS Rulings Rev. Rul Third -party Risk (Safe Harbor) Rev. Rul Balance Sheet Theory (Safe Harbor) Rev. Rul Disregarded Entities and More Rev. Rul Cell Captive Rev. Rul Reinsurance and Risk

23 What qualifies as risk shifting and risk distribution? Revenue Ruling Brother/Sister subsidiaries No single Brother/Sister subsidiary can constitute greater than 15% or no less than 5% of the risk Parent Company Each Sub Comprises 5-15% of Risk Sub Sub Sub Sub Sub Sub Sub Sub Sub Sub Sub Sub Captive

24 What qualifies as risk shifting and risk distribution? Revenue Ruling > 50% of risk exposure is derived from unrelated parties 49% of Risk 51% of Risk Parent Company Captive Unrelated Company

25 IRS Revenue Ruling Greater than 50% unrelated risk Parent Company Premium Independent Insurance Company 1 EPLI MGMT PROF LEGAL GEN L BUS CONST Reinsurance Premiums Captive 1 Each Line of Insurance is Pooled in order to Achieve Homogenous Risk Distribution and 3rd Party Risk; 2.5% Pooling Rate

26 IRS Revenue Ruling Low $ / high frequency claims (paid by captive) 49% of Risk / Premium Parent Company 1,000,000 Premium Independent Insurance Co 1 EPLI MGMT PROF LEGAL GEN L BUS CONST Reinsurance Contract for this part of risk 477,750 Reinsurance Premiums Captive 250, , ,000 1,000,000 1 net of 2.5% pooling rate

27 IRS Revenue Ruling Low frequency / high $ claims (paid by QS pool) 51% of risk / premium Parent Company 1,000,000 Premium Independent Insurance Co 1 EPLI MGMT PROF LEGAL GEN L BUS CONST Reinsurance Contract for pooled risk 497,250 Reinsurance Premiums Captive 250, , ,000 1,000,000 1 net of 2.5% pooling rate

28 Disregarded Entities Ruling Treatment of disregarded entities (i.e., LLC s) Rev. Rul indicates they are disregarded, risk of a single-member LLC is risk of the parent Inconsistent with the balance sheet theory Inconsistent with treatment IRS wants for partnerships Single member LLC s are respected by the IRS in other contexts 965 repatriation of profits; separate entities for liability for taxes Most importantly, disregarded entities are respected for liability and legal purposes That is what is being transferred in insurance transactions They have separate balance sheets Rev.Rul reads that, even if the insurer is adequately capitalized and completely unrelated, if there are an insufficient number of insureds, you may not have risk distribution, and thus no insurance

29 Other Guidance TAM IRS will not count limited partnerships with a common general partner as separate entities No logic to the IRS s argument that the common general partner bears all risk of loss Rev Rul protected cell captives -IRS requires risk distribution within each cell, not just within the overall organization, as cells are segregated from each other for liability purposes Rev. Rul to determine risk distribution regarding a reinsurance contract, one must look through to the risks of the ultimate insured the primary (underlying) insurance contract Rent-a-Center, 142 T.C. 1 (2014) distinguished cases finding parent guaranty of reinsurance risk results in no risk-shifting; where captive directly insures numerous brother-sister subs, a parent guaranty to the captive does not vitiate risk-shifting

30 Implementation Feasibility study prepared by actuary Choice of domicile Domestic Offshore Corporate formation Underwriting process Policies written Regulatory application/license received Ongoing management costs

31 What Does it Cost?

32 BEYOND THE INSURANCE Creative Business Planning Opportunities

33 Captive Insurance Programs Captive Insurance Company (Pure Captive) Shareholder Business Premiums Captive Insurance Policies

34 Business Planning Opportunities S-Corporation Owners Captive is a C-Corporation, so it is possible to create multiple classes of stock, vesting schedule, liquidation preferences, etc. Key Employee Incentives May be used to help indirectly fund nonqualified deferred comp or Restricted Stock Program Ownership by key employees can be used to incentivize better risk management/create more of an owner mentality for key employees

35 Gross Estate Equals All Assets +Company +Captive "Death may be an avenue of escape from many of the woes of life, but it is no escape from taxes." Estate of Kahrv. Commissioner, 414 F.2d 621, 626 (2d Cir.1969).

36 Captive Insurance Programs Shareholder Shareholder s IDGT Business Premiums Captive Insurance Policies 36

37 Estate Planning Opportunities Potential Transfer Tax Benefits: Reasonable premiums paid by the insured to the captive should not create gift, estate or GST tax exposure to the insured s owner The premiums must constitute full and adequate consideration for insurance coverage (e.g., arm s length and determined in accordance with underwriting standards) When the insured s actual claims are less than actuarially predicted, the captive s reserves will grow If family members directly or indirectly own shares in the captive, they benefit from this increase in value without any transfer tax liability In addition, the captive can distribute unused reserves to the captive shareholders as a dividend (currently taxed at capital gains rates) or as a capital gain distribution on complete liquidation of the captive

38 LEVERAGE, IN A GOOD WAY Split Dollar Offers the Best of All Worlds

39 THE NEED FOR ADVANCED PLANNING TECHNIQUES Estate planning professionals often recommend alternate techniques to fund life insurance policies in ILITs instead of incurring and paying gift taxes. The strategies used most often are: loans from third party lenders, private loans from the client or other family members, or split dollar arrangements employer or client or other family members.

40 SALE OF BUSINESS OR INVESTMENT ASSETS 4/ Client Secured Promissory Note; 9-year interestonly with annual interest based on midterm AFR and a balloon repayment of principal at the end of year 9. (Disregarded for income tax purposes) Sale of Business Assets 6/ Partial Guaranty Independent Party 5/ Irrevocable Grantor Trust Guaranty Annual Fee: Promissory Note Initial Gift Business Assets 4/ The sale would take place after the beneficiary s (Client s) withdrawal right had lapsed 5/ May be an existing irrevocable trust, the creator of the trust, or any other unrelated party who or which has sufficient assets to satisfy the guarantee, if necessary 6/ If the value of assets sold is adjusted by IRS resulting in an unintentional gift, then the beneficiary s testamentary power of appointment would avoid treating that excess as a completed gift. The value is determined by a qualified appraiser. This illustration assumes a 30% discount which is generally considered relatively conservative.

41 Formation of Captive Insurance Company Irrevocable Beneficiary Grantor Trust What is a Captive? Private Insurance Company Types Single Parent / Pure Group Rent-a-Captive Approximately 80% of the S&P 500 Utilize Captives Pure captive: closely held insurance company Provides significant annual savings for qualified business Can lower the net cost of risk Many captives are domestically licensed, state regulated and file Federal tax returns Business Assets Annual deductible insurance premiums Cash flows net of expenses and claims (estimated $1,068,900 in Year 1) Captive 41

42 Hypothetical Example For Discussion Purposes Only CONSOLIDATED CAPTIVE CASH FLOW YEAR 0 YEAR 1 YEAR 2 YEAR 3 YEAR 4 YEAR 10 YR 10 TOTAL Prior Year Balance $0 $175,000 $1,243,900 $2,385,485 $3,604,698 $12,872,307 $0 Initial Capital Contribution (no change) 250, ,000 Formation Fee Expense (75,000) (75,000) Premium Collected (or Taxable Income) 1,200,000 1,200,000 1,200,000 1,200,000 1,200,000 12,000,000 Premium Fee Expense 0 (30,000) (30,000) (30,000) (30,000) (30,000) (300,000) General & Administrative Expense 0 (53,000) (53,000) (53,000) (53,000) (53,000) (530,000) Claims Occurred 0 (60,000) (60,000) (60,000) (60,000) (60,000) (600,000) Gains: Cash Equivalent Assets 0 1,750 12,439 23,855 36, , ,004 Gains: Alternative Investments 0 13,125 93, , , ,423 4,477,527 Income Tax on Realized Investments Gains 0 (2,975) (21,146) (40,553) (61,280) (218,829) (1,014,906) Income Tax NET CASH FLOW $175,000 $1,068,900 $1,141,585 $1,219,213 $1,302,119 $1,932,317 END OF YEAR BALANCE $175,000 $1,243,900 $2,385,485 $3,604,698 $4,906,818 $14,804,624 $14,804,624 COMPARATIVE CASH FLOW -W/O CAPTIVES YEAR 0 YEAR 1 YEAR 2 YEAR 3 YEAR 4 YEAR 10 TOTAL Prior Year Balance $0 $250,000 $951,000 $1,699,668 $2,499,245 $8,577,077 $0 Initial Capital Contribution (no change) 250, ,000 Formation Fee Expense (Premium Collected or) Taxable Income 1,200,000 1,200,000 1,200,000 1,200,000 1,200,000 12,000,000 Premium Fee Expense General & Administrative Expense Claims Occurred 0 (60,000) (60,000) (60,000) (60,000) (60,000) (600,000) Gains: Cash Equivalent Assets 0 2,500 9,510 16,997 24,992 85, ,047 Gains: Alternative Investments 0 18,750 71, , , ,281 3,037,851 Income Tax on Realized Investments Gains 0 (4,250) (16,167) (28,894) (42,487) (145,810) (688,580) Income Tax 0 (456,000) (456,000) (456,000) (456,000) (456,000) (4,560,000) NET CASH FLOW $250,000 $701,000 $748,668 $799,577 $853,949 $1,267,241 END OF YEAR BALANCE $250,000 $951,000 $1,699,668 $2,499,245 $3,353,194 $9,844,318 $9,844,318

43 Option A: ANNUAL ADMINISTRATION OF SALE OF BUSINESS ASSETS AND PURCHASE OF LIFE INSURANCE POLICY Promissory Note Client Initial Gift Annual interest on promissory note (Disregarded for income tax purposes) Income on trust assets taxed to Client 7/ Annual Premiums 8/ Independent Party Guaranty Fee Irrevocable Grantor Trust Life Insurance Company Captive Business assets 7/ Payment of income tax by the beneficiary on trust income is not a gift for gift tax purposes. Additionally, it reduces Client s estate by the amount of income taxes paid, providing a substantial estate tax reduction benefit. 8/ This is not an illustration or a contract for insurance. Costs are estimated and may change based on underwriting.

44 Option B: ANNUAL ADMINISTRATION OF SALE OF BUSINESS ASSETS AND PURCHASE OF LIFE INSURANCE POLICY Promissory Note Annual Premium 8/ Client Initial Gift Annual interest on promissory note (Disregarded for income tax purposes) Income on trust assets taxed to client 7/ Split Dollar loan repayment Death Benefit (less Split Dollar loan) 8/ Independent Party Guaranty Fee Irrevocable Grantor Trust Life Insurance Company Captive Business assets 7/ Payment of income tax by the beneficiary on trust income is not a gift for gift tax purposes. Additionally, it reduces client s estate by the amount of income taxes paid, providing a substantial estate tax reduction benefit. 8/ This is not an illustration or a contract for insurance. Costs are estimated and may change based on underwriting.

45 COMPLETION OF SALE OF BUSINESS INTERESTS AFTER NOTE TERM (END OF YEAR NINE) Captive Client Repayment of outstanding principal of promissory note and any accrued interest paid in cash and in kind (Disregarded for income tax purposes) Satisfaction of promissory note ( Paid in Full ) Irrevocable Grantor Trust Income Principal and interest payments after 9 years: Total Interest Principal Cash Principal In Kind (shares of Captive Ins. Co.) Initial Gift Business assets

46 FOLLOWING COMPLETION OF SALE OF ASSETS Captive Client Income on trust assets continues to be taxed to Client for life Annual Premium Death Benefit Irrevocable Grantor Trust Income Initial Gift Business assets Life Insurance Company

47 FOLLOWING DEATH OF BENEFICIARY Client s Estate Life Insurance Company Death Benefit Irrevocable Grantor Trust Separate Trusts for Descendants for Life 9/ 9/ (i) Protected from all estate, gift, and GST taxes. (ii) Protected from the trust beneficiaries creditors, including divorcing or dissident spouses, for as long as the property is owned by the trust.

48 Prepared For: Client Trust Values* Prepared By: Agent (1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11) (12) (13) (14) Nominal Beg Yr Beg Yr Cash Asset Captive Loan Interest Loan Loan Repay Insurance EOY Loan Asset Cash Insurance Growth Income Cash Guar. Fee Payment Repay Cash Fund In Kind Death Trust Value Yr Age Payable 2% Gifts 5.5% 3% of 1.01% Cash Balance (Nom. Val.) Benefit Net of Loan 1 54 (7,000,000) 10,200,000 0 (827) (8) 550,000 1,068,900 (42,000) (70,700) 0 1,505, ,000, ,705, (7,000,000) 10,404,000 0 (1,051) 15, ,000 1,141,585 (42,000) (70,700) 0 3,109, ,000, ,513, (7,000,000) 10,612,080 0 (1,361) 31, ,220 1,219,213 (42,000) (70,700) 0 4,817, ,000, ,429, (7,000,000) 10,824,322 0 (1,751) 48, ,664 1,302,119 (42,000) (70,700) 0 6,637, ,000, ,461, (7,000,000) 11,040,808 0 (2,212) 66, ,338 1,390,664 (42,000) (70,700) 0 8,574, ,000, ,615, (7,000,000) 11,261,624 0 (2,715) 85, ,244 1,485,229 (42,000) (70,700) 0 10,637, ,000, ,899, (7,000,000) 11,486,857 0 (3,230) 106, ,389 1,586,224 (42,000) (70,700) 0 12,833, ,000, ,320, (7,000,000) 11,716,594 0 (3,777) 128, ,777 1,694,088 (42,000) (70,700) 0 15,171, ,000, ,887, ,950,926 0 (4,416) 151, ,413 1,809,285 (42,000) (70,700) (7,000,000) 10,659, ,000, ,610, ,189,944 0 (6,500,000) 41, , ,858, ,000, ,048, ,433,743 0 (650,000) 42, , ,920, ,000, ,354, ,682,418 0 (650,000) 42, , ,997, ,000, ,679, ,936,066 0 (650,000) 43, , ,088, ,000, ,024, ,194,788 0 (650,000) 44, , ,194, ,000, ,389, ,458,683 0 (650,000) 45, , ,315, ,000, ,774, ,727,857 0 (650,000) 46, , ,452, ,000, ,180, ,002,414 0 (650,000) 48, , ,605, ,000, ,607, ,282,462 0 (650,000) 49, , ,774, ,000, ,057, ,568,112 0 (650,000) 51, , ,961, ,000, ,529, ,859,474 0 (650,000) 53, , ,166, ,000, ,025,622 * All values are end of year unless otherwise indicated. Not valid wthout Disclosure page.

49 Summary of Results End of Year 1 (Includes Life Insurance Death Benefit) Estate Trust Estate Net to Value Value Taxes Heirs Current Situation 26,875,000 NA (10,750,000) 16,125,000 Proposed Strategy 17,676, ,510,700 (7,070,700) 120,116,750 Difference (9,198,250) - (3,679,300) 103,991,750 End of Year 9 (Includes Life Insurance Death Benefit) Estate Trust Estate Net to Value Value Taxes Heirs Current Situation 46,204,781 NA (18,481,913) 27,722,869 Proposed Strategy 19,448, ,696,208 (7,779,578) 142,365,576 Difference (26,755,836) - (10,702,334) 114,642,707

50 What are the issues to pay attention to DOING IT THE RIGHT WAY

51 Unofficial IRS Captive Audit Considerations 1. Consider whether the risks are garden-variety insurance risks or unique risks that require further investigation into whether the risks are insurance risk. 2. Was a feasibility study performed showing business benefits? The IRS is more likely to find an adjustment with a taxpayer that does not follow good business practice. 3. Assess whether the assuming company has the capacity to assume the risk. Look at the premium to surplus ratio. Are there any parental guarantees? What is the maximum single risk exposure compared to surplus. 51

52 Unofficial IRS Captive Audit Considerations 4. Consider whether the insured is in substantial part paying for their own losses, by comparing the relationship of the largest insured as measured by premiums to total premiums. 5. Consider whether there are sufficient exposure units for risk to be reasonably predictable (law of large numbers). 6. Assess whether the Captive is operating as an independent entity and whether there is insurance in its generally accepted sense. Part of this is the question; could the Captive still function if its largest investment failed? 52

53 Unofficial IRS Captive Audit Considerations 7. Is there a loss portfolio transfer and is there a significant chance of a significant loss as required for GAAP under FASB 113? 8. If parent premiums are deducted, determine whether there is a sufficient amount of unrelated risk assumed by the Captive. 9. Is the taxpayer taking a consistent position by paying excise tax for risk ceded to an offshore insurance company that is not taxed as a U.S. taxpayer? 53

54 Unofficial IRS Captive Audit Considerations 10.Did the Captive enter into a finite risk contract with an offshore reinsurance company that is a non-controlled Foreign Corporation? If so, review the transaction to determine whether there is significant tax avoidance. 11. Are Captive assets used as security or as compensating balance for the liabilities of another entity? 54

Agenda. What is a Captive?

TAKE NO PRISONERS: PITFALLS AND POSSIBILITIES WITH CAPTIVE INSURANCE COMPANIES J. SCOT KIRKPATRICK, ESQ. (404) 658-5421 scot.kirkpatrick@chamberlainlaw.com GEOFF SEAMAN, TEP, MBA, JD (310) 351-5579 geoff.seaman@bnymellon.com

TAKE NO PRISONERS: PITFALLS AND POSSIBILITIES WITH CAPTIVE INSURANCE COMPANIES J. SCOT KIRKPATRICK, ESQ. (404) 658-5421 scot.kirkpatrick@chamberlainlaw.com GEOFF SEAMAN, TEP, MBA, JD (310) 351-5579 geoff.seaman@bnymellon.com

Captive Insurance! Basic Taxation

New Jersey Captive Insurance Association Presents Captive Insurance! Basic Taxation Sponsored by Presented by Christopher J. Ridge, JD, MS (RM)! Manager - Alternative Risk Finance! Perr&Knight! Harborside

New Jersey Captive Insurance Association Presents Captive Insurance! Basic Taxation Sponsored by Presented by Christopher J. Ridge, JD, MS (RM)! Manager - Alternative Risk Finance! Perr&Knight! Harborside

RISK WELL REWARDED CAPTIVE INSURANCE AND ALTERNATIVE RISK SOLUTIONS FOR THE MIDDLE MARKET ARTEX RISK SOLUTIONS, INC

SM RISK WELL REWARDED CAPTIVE INSURANCE AND ALTERNATIVE RISK SOLUTIONS FOR THE MIDDLE MARKET ARTEX RISK SOLUTIONS, INC For many years large corporations have used alternative risk transfer strategies to

SM RISK WELL REWARDED CAPTIVE INSURANCE AND ALTERNATIVE RISK SOLUTIONS FOR THE MIDDLE MARKET ARTEX RISK SOLUTIONS, INC For many years large corporations have used alternative risk transfer strategies to

Captive Insurance Issues and Trends. Michael Mead, Kyle Mrotek and Doug Youngren

Captive Insurance Issues and Trends Michael Mead, Kyle Mrotek and Doug Youngren What is a Captive and What Does it Do? Michael R. Mead, CPCU, M.R. Mead Co. 1 What It Is Not 2 Definition of Captive Insurance

Captive Insurance Issues and Trends Michael Mead, Kyle Mrotek and Doug Youngren What is a Captive and What Does it Do? Michael R. Mead, CPCU, M.R. Mead Co. 1 What It Is Not 2 Definition of Captive Insurance

Growing numbers of publicly traded companies, large and

Captive Insurance Companies: A Growing Alternative Method of Risk Financing PHILLIP ENGLAND, ISAAC E. DRUKER, AND R. MARK KEENAN The authors explain how a captive insurer can serve as a funding or financing

Captive Insurance Companies: A Growing Alternative Method of Risk Financing PHILLIP ENGLAND, ISAAC E. DRUKER, AND R. MARK KEENAN The authors explain how a captive insurer can serve as a funding or financing

Micro Captives: The Insurance Company You Keep

Micro Captives: The Insurance Company You Keep Dallas Bar Association April 4, 2016 Cindy L. Grossman 100 CONGRESS AVENUE, SUITE 1440 AUSTIN, TEXAS 78701 phone 512.767.7100 fax 512.767.7101 WWW.GSRP.COM

Micro Captives: The Insurance Company You Keep Dallas Bar Association April 4, 2016 Cindy L. Grossman 100 CONGRESS AVENUE, SUITE 1440 AUSTIN, TEXAS 78701 phone 512.767.7100 fax 512.767.7101 WWW.GSRP.COM

Captive Insurance Company

Captive Insurance Company Captive Insurance Companies (referred to as Captives) and also known as Closely Held Insurance Companies (CHIC), have become a commonplace form of alternative risk transfer and

Captive Insurance Company Captive Insurance Companies (referred to as Captives) and also known as Closely Held Insurance Companies (CHIC), have become a commonplace form of alternative risk transfer and

*Copyright 2011 by Richard A. Oshins and Lawrence Brody. All Rights Reserved.

SCHEMATIC Schematic Outline of Planning Benefits Protection, Use, Control Control List Primary /Trustee Controls Office of Trusteeship Circular 230 Disclosure: To ensure compliance with requirements imposed

SCHEMATIC Schematic Outline of Planning Benefits Protection, Use, Control Control List Primary /Trustee Controls Office of Trusteeship Circular 230 Disclosure: To ensure compliance with requirements imposed

Advanced Markets Combining Estate Planning Techniques A Powerful Strategy

Life insurance can help meet many wealth transfer goals. The death benefit could cover estate taxes, for instance, avoiding liquidation of much of the estate to meet the estate tax bill. Even though a

Life insurance can help meet many wealth transfer goals. The death benefit could cover estate taxes, for instance, avoiding liquidation of much of the estate to meet the estate tax bill. Even though a

Insuring your business. Ensuring your future. Private Insurance Companies

Insuring your business. Ensuring your future. Private Insurance Companies Private Insurance Company Basics A Captive Insurance Company provides insurance for its owner. Types of Captive Insurance companies:

Insuring your business. Ensuring your future. Private Insurance Companies Private Insurance Company Basics A Captive Insurance Company provides insurance for its owner. Types of Captive Insurance companies:

Captive Insurance Companies

Captive Insurance Companies Presented to: CPA Manufacturing Services Association Matthew J. Howard, JD, LLM Robert N. Greenberger, CPA/PFS,AEP Moore Ingram Johnson & Steele, LLP Habif Arogeti & Wynne,

Captive Insurance Companies Presented to: CPA Manufacturing Services Association Matthew J. Howard, JD, LLM Robert N. Greenberger, CPA/PFS,AEP Moore Ingram Johnson & Steele, LLP Habif Arogeti & Wynne,

Revenue Ruling 2002-89 states that a Captive that receives 50% of its premiums from unrelated entities will achieve adequate risk distribution.

Captive Insurance: Frequently Asked Questions 1. Q: How is the Captive formed to ensure it is a true insurance arrangement? A: In order to have legitimate Insurance, there must be adequate risk transfer

Captive Insurance: Frequently Asked Questions 1. Q: How is the Captive formed to ensure it is a true insurance arrangement? A: In order to have legitimate Insurance, there must be adequate risk transfer

Sales Strategy Sale to a Grantor Trust (SAGT)

") Estate planners have been using the Irrevocable Life Insurance Trust (ILIT) for many years, to increase wealth and liquidity outside the taxable estate. 1 However, transfers to ILITs One effective technique

Estate planners have been using the Irrevocable Life Insurance Trust (ILIT) for many years, to increase wealth and liquidity outside the taxable estate. 1 However, transfers to ILITs One effective technique

Management Alta s team of professionals set us apart. Our associates are CPAs, attorneys, business, and insurance professionals with the most

Management Alta s team of professionals set us apart. Our associates are CPAs, attorneys, business, and insurance professionals with the most extensive, sophisticated experience in the Captive industry.

Management Alta s team of professionals set us apart. Our associates are CPAs, attorneys, business, and insurance professionals with the most extensive, sophisticated experience in the Captive industry.

The Income Taxation of Employment Split Dollar Loan Arrangements Split Dollar Loan Arrangements

The Income Taxation of Employment Split Dollar Loan Arrangements Split Dollar Loan Arrangements These materials are not intended to be used to avoid tax penalties and were prepared to support the promotion

The Income Taxation of Employment Split Dollar Loan Arrangements Split Dollar Loan Arrangements These materials are not intended to be used to avoid tax penalties and were prepared to support the promotion

CAPTIVE INSURANCE COMPANIES

CAPTIVE INSURANCE COMPANIES Presented By: Domenick R. Lioce, Esquire Nason, Yeager, Gerson, White & Lioce, P.A. 1645 Palm Beach Lakes Boulevard, Suite 1200 West Palm Beach, Florida 33401 Phone: (561) 686-3307

CAPTIVE INSURANCE COMPANIES Presented By: Domenick R. Lioce, Esquire Nason, Yeager, Gerson, White & Lioce, P.A. 1645 Palm Beach Lakes Boulevard, Suite 1200 West Palm Beach, Florida 33401 Phone: (561) 686-3307

ANTHONY M. SARDIS, JD, LLM

YOUR WS+B TEAM ANTHONY M. SARDIS, JD, LLM PRESIDENT, IIAG PROFESSIONAL EXPERIENCE INDUSTRIES Insurance President of Insurance & Investment Advisory Group (IIAG). Consults with individuals and businesses

YOUR WS+B TEAM ANTHONY M. SARDIS, JD, LLM PRESIDENT, IIAG PROFESSIONAL EXPERIENCE INDUSTRIES Insurance President of Insurance & Investment Advisory Group (IIAG). Consults with individuals and businesses

Insights on... WEALTH PLANNING CAPTIVE INSURANCE. What Closely Held Business Owners Need to Know

Insights on... WEALTH PLANNING CAPTIVE INSURANCE What Closely Held Business Owners Need to Know OVERVIEW Risk is a fact of business. Insuring risk is frequently on the minds of business owners. Increasingly

Insights on... WEALTH PLANNING CAPTIVE INSURANCE What Closely Held Business Owners Need to Know OVERVIEW Risk is a fact of business. Insuring risk is frequently on the minds of business owners. Increasingly

Comprehensive Split Dollar

Advanced Markets Client Guide Comprehensive Split Dollar Crafting a plan to meet your needs. John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company New York (John

Advanced Markets Client Guide Comprehensive Split Dollar Crafting a plan to meet your needs. John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company New York (John

Leveraging wealth transfer using private financing

Private Financing Strategy Leveraging wealth transfer using private financing Not a bank or credit union deposit or obligation Not insured by any federal government agency Not FDIC or NCUA/NCUSIF insured

Private Financing Strategy Leveraging wealth transfer using private financing Not a bank or credit union deposit or obligation Not insured by any federal government agency Not FDIC or NCUA/NCUSIF insured

[Collar: 20160216NA] [RMC8271613-001]

![[Collar: 20160216NA] [RMC8271613-001]](/thumbs/35/17306500.jpg "[Collar: 20160216NA] [RMC8271613-001]") [Collar: 20160216NA] [RMC8271613-001] T E C H N I C A L M E M O R A N D U M TO: FROM: RE: Raymond G. Ankner, President Jeffrey I. Bleiweis, Vice President and General Counsel Captive Insurance Companies

[Collar: 20160216NA] [RMC8271613-001] T E C H N I C A L M E M O R A N D U M TO: FROM: RE: Raymond G. Ankner, President Jeffrey I. Bleiweis, Vice President and General Counsel Captive Insurance Companies

memorandum Office of Chief Counsel Internal Revenue Service Number: 201533011 Release Date: 8/14/2015 CC:FIP:B04 POSTF-146000-13

Office of Chief Counsel Internal Revenue Service memorandum Number: 201533011 Release Date: 8/14/2015 CC:FIP:B04 POSTF-146000-13 UILC: 832.00-00, 162.04-03 date: May 06, 2015 to: from: Gwen Schoen Attorney

Office of Chief Counsel Internal Revenue Service memorandum Number: 201533011 Release Date: 8/14/2015 CC:FIP:B04 POSTF-146000-13 UILC: 832.00-00, 162.04-03 date: May 06, 2015 to: from: Gwen Schoen Attorney

INTERNAL REVENUE SERVICE NATIONAL OFFICE FIELD SERVICE ADVICE. DEBORAH A. BUTLER ASSISTANT CHIEF COUNSEL (Field Service) CC:DOM:FS

CC:DOM:FS") DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE WASHINGTON, D.C. 20224 June 12, 2000 Number: 200043011 Release Date: 10/27/2000 CC:DOM:FS:FI&P WTA-N-107454-00 UILC: 162.04-03 INTERNAL REVENUE SERVICE

DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE WASHINGTON, D.C. 20224 June 12, 2000 Number: 200043011 Release Date: 10/27/2000 CC:DOM:FS:FI&P WTA-N-107454-00 UILC: 162.04-03 INTERNAL REVENUE SERVICE

The Journal of Taxation of Investments (Spring 2008 - Vol. 25, No. 3)

") The Journal of Taxation of Investments (Spring 2008 - Vol. 25, No. 3) Captive Insurance Companies Provide Tax and Economic Advantages for Hedge Funds By Gerald Nowotny! This article will outline the how

The Journal of Taxation of Investments (Spring 2008 - Vol. 25, No. 3) Captive Insurance Companies Provide Tax and Economic Advantages for Hedge Funds By Gerald Nowotny! This article will outline the how

Business Succession Planning. 2011 Morgan Stanley Smith Barney LLC. Member SIPC

2011 Morgan Stanley Smith Barney LLC. Member SIPC 2011-PS-541 Expires: February 2012 Date of First Use: February 2011 Updated/Reviewed: February 2011 Overview Why Succession Planning is Important Common

2011 Morgan Stanley Smith Barney LLC. Member SIPC 2011-PS-541 Expires: February 2012 Date of First Use: February 2011 Updated/Reviewed: February 2011 Overview Why Succession Planning is Important Common

Small Captive Insurance Companies

Small Captive Insurance Companies Presented By: Matthew J. Howard, J.D., LLM & Robert N. Greenberger, CPA/PFS, AEP Presented To: MSA Super Conference Chicago, Illinois August 5, 2011 Small captive insurance

Small Captive Insurance Companies Presented By: Matthew J. Howard, J.D., LLM & Robert N. Greenberger, CPA/PFS, AEP Presented To: MSA Super Conference Chicago, Illinois August 5, 2011 Small captive insurance

A Powerful Way to Plan: The Grantor Retained Annuity Trust

Strategic Thinking A Powerful Way to Plan: The Grantor Retained Annuity Trust According to The Taxpayer Relief Act of 2010, the estate and gift exemption amount has been increased temporarily, for 2011

Strategic Thinking A Powerful Way to Plan: The Grantor Retained Annuity Trust According to The Taxpayer Relief Act of 2010, the estate and gift exemption amount has been increased temporarily, for 2011

Effective Planning with Life Insurance

Effective Planning with Life Insurance The Tax Considerations... Ken Knox, CLU, ChFC Regional Director The Penn Mutual Life Insurance Company 1304529TM_Sept17 Retirement Planning Case Scenario #1... Client

Effective Planning with Life Insurance The Tax Considerations... Ken Knox, CLU, ChFC Regional Director The Penn Mutual Life Insurance Company 1304529TM_Sept17 Retirement Planning Case Scenario #1... Client

Closely held businesses and professionals

Closely Held Business Can Enjoy Captive Insurance Opportunity Although associated with large corporations, captive insurance companies can be available and beneficial to closely held businesses too. BERNARD

Closely Held Business Can Enjoy Captive Insurance Opportunity Although associated with large corporations, captive insurance companies can be available and beneficial to closely held businesses too. BERNARD

Hot Topic!!!! Funding Trust-Owned Life Insurance - Selecting the Best Option.

Executive Capital Resources 5550 W Touhy Ave. Suite 304 Skokie, Illinois 60077 847-673-2677 www.ecrllc.com jeffrey@ecrllc.com Washimgton Report 13-12 Hot Topic!!!! Funding Trust-Owned Life Insurance -

Executive Capital Resources 5550 W Touhy Ave. Suite 304 Skokie, Illinois 60077 847-673-2677 www.ecrllc.com jeffrey@ecrllc.com Washimgton Report 13-12 Hot Topic!!!! Funding Trust-Owned Life Insurance -

Captive Insurance Companies: Current Lay of the Land. Fred Thomas, Deloitte Tax Natasha Ng, Deloitte Tax

Captive Insurance Companies: Current Lay of the Land Fred Thomas, Deloitte Tax Natasha Ng, Deloitte Tax Background What is a captive insurance company? In general, a captive insurance company is an insurance

Captive Insurance Companies: Current Lay of the Land Fred Thomas, Deloitte Tax Natasha Ng, Deloitte Tax Background What is a captive insurance company? In general, a captive insurance company is an insurance

Private Placement Life Insurance

Private Placement Life Insurance Robert W. Chesner, Jr. Leslie C. Giordani 100 CONGRESS AVENUE, SUITE 1440 AUSTIN, TEXAS 78701 phone 512.767.7100 fax 512.767.7101 WWW.GSRP.COM 2009 2015 Giordani, Swanger,

Private Placement Life Insurance Robert W. Chesner, Jr. Leslie C. Giordani 100 CONGRESS AVENUE, SUITE 1440 AUSTIN, TEXAS 78701 phone 512.767.7100 fax 512.767.7101 WWW.GSRP.COM 2009 2015 Giordani, Swanger,

What are Captive Insurance Companies?

What are Captive Insurance Companies? Captives offer unparalleled benefits for the companies that use them. They allow a company to obtain insurance coverage that is tailored to its unique risks, rather

What are Captive Insurance Companies? Captives offer unparalleled benefits for the companies that use them. They allow a company to obtain insurance coverage that is tailored to its unique risks, rather

Many U.S. companies have formed captive insurance companies

Forming a Captive Insurance Company? Understand the Business and Tax Implications By Gary A. Fox and Lynn M. McGuire Many U.S. companies have formed captive insurance companies to achieve significant benefits,

Forming a Captive Insurance Company? Understand the Business and Tax Implications By Gary A. Fox and Lynn M. McGuire Many U.S. companies have formed captive insurance companies to achieve significant benefits,

Captive Insurance Companies in Estate Planning: A Profit Maximization and Risk Reduction Tool

Presenting a live 90-minute webinar with interactive Q&A Captive Insurance Companies in Estate Planning: A Profit Maximization and Risk Reduction Tool Leveraging the Benefits for Asset Protection, Wealth

Presenting a live 90-minute webinar with interactive Q&A Captive Insurance Companies in Estate Planning: A Profit Maximization and Risk Reduction Tool Leveraging the Benefits for Asset Protection, Wealth

Internal Revenue Service

Internal Revenue Service Number: 201429007 Release Date: 7/18/2014 Index Number: 1504.02-00, 832.00-00, 832.06-00 --------------- ------------------------------------------------------------ ------------

Internal Revenue Service Number: 201429007 Release Date: 7/18/2014 Index Number: 1504.02-00, 832.00-00, 832.06-00 --------------- ------------------------------------------------------------ ------------

Number: 200636085 Release Date: 9/8/2006 Internal Revenue Service. Department of the Treasury Washington, DC 20224. Index Number: 162.

Number: 200636085 Release Date: 9/8/2006 Internal Revenue Service Index Number: 162.04-03 ---------------------------- ------------------------------------------------- ---------------------------- -----------------------

Number: 200636085 Release Date: 9/8/2006 Internal Revenue Service Index Number: 162.04-03 ---------------------------- ------------------------------------------------- ---------------------------- -----------------------

Balancing Bet-to Strategies

Balancing Bet-to to-live and Bet-to to-die Strategies Presented By: Robert S. Keebler, CPA, MST, AEP Stephen J. Bigge, CPA CSEP Phone: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com Circular

Balancing Bet-to to-live and Bet-to to-die Strategies Presented By: Robert S. Keebler, CPA, MST, AEP Stephen J. Bigge, CPA CSEP Phone: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com Circular

Wealth Transfer and Charitable Planning Strategies Handbook

Wealth Transfer and Charitable Planning Strategies Handbook This handbook contains 12 core wealth transfer and charitable planning strategies. It also demonstrates how life insurance may enhance the results

Wealth Transfer and Charitable Planning Strategies Handbook This handbook contains 12 core wealth transfer and charitable planning strategies. It also demonstrates how life insurance may enhance the results

16 LC 37 2118ER A BILL TO BE ENTITLED AN ACT BE IT ENACTED BY THE GENERAL ASSEMBLY OF GEORGIA:

Senate Bill 347 By: Senator Bethel of the 54th A BILL TO BE ENTITLED AN ACT 1 2 3 4 5 6 To amend Title 33 of the Official Code of Georgia Annotated, relating to insurance, so as to provide for extensive

Senate Bill 347 By: Senator Bethel of the 54th A BILL TO BE ENTITLED AN ACT 1 2 3 4 5 6 To amend Title 33 of the Official Code of Georgia Annotated, relating to insurance, so as to provide for extensive

Life Insurance: Your blueprint for Wealth Transfer Planning. Private Financing Producer Guide. For agent use only. Not for public distribution.

Life Insurance: Your blueprint for Wealth Transfer Planning Private Financing Producer Guide Private Financing Most people don t object to owning life insurance, they just object to paying the premiums.

Life Insurance: Your blueprint for Wealth Transfer Planning Private Financing Producer Guide Private Financing Most people don t object to owning life insurance, they just object to paying the premiums.

New York Addresses Tax Treatment of Premiums Paid to a Captive Insurance Company

Journal of Multistate Taxation and Incentives (Thomson Reuters/Tax & Accounting) Volume 26, Number 3, June 2016 CORPORATE FRANCHISE AND INCOME TAXES New York Addresses Tax Treatment of Premiums Paid to

Journal of Multistate Taxation and Incentives (Thomson Reuters/Tax & Accounting) Volume 26, Number 3, June 2016 CORPORATE FRANCHISE AND INCOME TAXES New York Addresses Tax Treatment of Premiums Paid to

Possibilities and Pitfalls With Captive Insurance Companies

Estate Planning August 2011 CAPTIVE INSURANCE COMPANIES Possibilities and Pitfalls With Captive Insurance Companies Profitable family businesses can use captive insurance companies to manage business risk

Estate Planning August 2011 CAPTIVE INSURANCE COMPANIES Possibilities and Pitfalls With Captive Insurance Companies Profitable family businesses can use captive insurance companies to manage business risk

2012 Estate/Gift Tax Overview

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013 Presented By:, March 20, 2013 Phone: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com Circular 230 Disclosure:

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013 Presented By:, March 20, 2013 Phone: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com Circular 230 Disclosure:

INTERNATIONAL PRIVATE PLACEMENT VARIABLE LIFE INSURANCE. A Fountainhead Forum Fact Sheet

INTERNATIONAL PRIVATE PLACEMENT VARIABLE LIFE INSURANCE A Fountainhead Forum Fact Sheet INTERNATIONAL PRIVATE PLACEMENT VARIABLE LIFE INSURANCE Many high net worth clients have superior investment managers,

INTERNATIONAL PRIVATE PLACEMENT VARIABLE LIFE INSURANCE A Fountainhead Forum Fact Sheet INTERNATIONAL PRIVATE PLACEMENT VARIABLE LIFE INSURANCE Many high net worth clients have superior investment managers,

Hot Topics In Insurance Planning: Private Placement Insurance By Jonathan M. Forster, Michael B. Liebeskind, and Jennifer M. Smith

Hot Topics In Insurance Planning: Private Placement Insurance By Jonathan M. Forster, Michael B. Liebeskind, and Jennifer M. Smith As tax rates increase and investment returns decline, high-net-worth clients

Hot Topics In Insurance Planning: Private Placement Insurance By Jonathan M. Forster, Michael B. Liebeskind, and Jennifer M. Smith As tax rates increase and investment returns decline, high-net-worth clients

IN THIS ISSUE: March, 2011 j Planning with the $5 Million Gift Tax Exemption

IN THIS ISSUE: Federal Gift, Estate and GST Exemptions and Tax Rates New York State Gift & Estate Tax March, 2011 j Planning with the $5 Million Gift Tax Exemption By: Louis W. Pierro, Esq., Philip A.

IN THIS ISSUE: Federal Gift, Estate and GST Exemptions and Tax Rates New York State Gift & Estate Tax March, 2011 j Planning with the $5 Million Gift Tax Exemption By: Louis W. Pierro, Esq., Philip A.

Irrevocable Life Insurance Trusts

Irrevocable Life Insurance Trusts Producer Guide 1 Irrevocable Life Insurance Trusts For producer use only. Not for distribution to the public. An In-Depth Look at the ILIT An irrevocable life insurance

Irrevocable Life Insurance Trusts Producer Guide 1 Irrevocable Life Insurance Trusts For producer use only. Not for distribution to the public. An In-Depth Look at the ILIT An irrevocable life insurance

Internal Revenue Service

Internal Revenue Service Number: 201114015 Release Date: 4/8/2011 Index Number: 832.15-00, 162.04-02, 162.04-03, 263.00-00 ------------------------------- -------------------------------------------------------------

Internal Revenue Service Number: 201114015 Release Date: 4/8/2011 Index Number: 832.15-00, 162.04-02, 162.04-03, 263.00-00 ------------------------------- -------------------------------------------------------------

The Continuing Significance of Non-Qualified Deferred Compensation. From: Louis Lepore TABLE OF CONTENTS

THE PLANNER THE MAY 2010 EDITION Volume 2, Issue 5 A monthly newsletter for Accounting, and Financial Professionals with a focusing on Estate Planning, Elder Law, and Special Needs Persons. The Planner

THE PLANNER THE MAY 2010 EDITION Volume 2, Issue 5 A monthly newsletter for Accounting, and Financial Professionals with a focusing on Estate Planning, Elder Law, and Special Needs Persons. The Planner

What Are the Roles and Responsibilities of a Captive Manager?

Captive Management: What Are the Roles and Responsibilities of a Captive Manager? WWW.CHICAGOLANDRISKFORUM.ORG What Is a Captive Insurance Company? A captive is A separate legal entity created or used

Captive Management: What Are the Roles and Responsibilities of a Captive Manager? WWW.CHICAGOLANDRISKFORUM.ORG What Is a Captive Insurance Company? A captive is A separate legal entity created or used

A Practical Guide to the Final Regs. Governing Split- Dollar Life Insurance

PERSONAL A Practical Guide to the Final Regs. Governing Split- Dollar Life Insurance Author: By Gary Lee and Deborah Walker GARY LEE is National Director of Insurance Consulting Services for Deloitte &

PERSONAL A Practical Guide to the Final Regs. Governing Split- Dollar Life Insurance Author: By Gary Lee and Deborah Walker GARY LEE is National Director of Insurance Consulting Services for Deloitte &

IRS Captive Insurance Ruling Creates Opportunities for Plan Sponsors

July 28, 2014 Authors: Theodore R. Groom Kara M. Soderstrom If you have questions, please contact your regular Groom attorney or one of the attorneys listed below: Theodore R. Groom tgroom@groom.com (202)

July 28, 2014 Authors: Theodore R. Groom Kara M. Soderstrom If you have questions, please contact your regular Groom attorney or one of the attorneys listed below: Theodore R. Groom tgroom@groom.com (202)

PART II GRANTOR RETAINED ANNUITY TRUST (GRAT)

") PART II GRANTOR RETAINED ANNUITY TRUST (GRAT) By Leo J. Cushing, Esq., CPA, LLM Cushing & Dolan, P.C. Attorneys at Law 375 Totten Pond Road, Suite 200 Waltham, MA 02451 I. DESCRIPTION OF TECHNIQUE Donor

PART II GRANTOR RETAINED ANNUITY TRUST (GRAT) By Leo J. Cushing, Esq., CPA, LLM Cushing & Dolan, P.C. Attorneys at Law 375 Totten Pond Road, Suite 200 Waltham, MA 02451 I. DESCRIPTION OF TECHNIQUE Donor

Does the arrangement described below constitute insurance within the meaning

Part I Section 801. Tax Imposed Rev. Rul. 2014-15 ISSUE Does the arrangement described below constitute insurance within the meaning of subchapter L of the Internal Revenue Code? If so, does the issuer

Part I Section 801. Tax Imposed Rev. Rul. 2014-15 ISSUE Does the arrangement described below constitute insurance within the meaning of subchapter L of the Internal Revenue Code? If so, does the issuer

Life Insurance: Business Applications

Life Insurance: Business Applications What is business life insurance? Life insurance is an important part of a business. It may be used as a funding mechanism for your buy-sell agreement and as business

Life Insurance: Business Applications What is business life insurance? Life insurance is an important part of a business. It may be used as a funding mechanism for your buy-sell agreement and as business

Life Insurance Coverage on a Key Employee

Center for Wealth Management Susan A. Myers, CPA, CFP, CLTC Robert J. Moore Justin M. Williamson 755 W. Big Beaver Rd, Ste 600 Troy, MI 48084 248-680-0490 smyers1@metlife.com www.center4wealthmgmt.com

Center for Wealth Management Susan A. Myers, CPA, CFP, CLTC Robert J. Moore Justin M. Williamson 755 W. Big Beaver Rd, Ste 600 Troy, MI 48084 248-680-0490 smyers1@metlife.com www.center4wealthmgmt.com

Private Financing CLIENT GUIDE. Advanced Markets

CLIENT GUIDE Advanced Markets Private Financing John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) Guiding you through life. Private

CLIENT GUIDE Advanced Markets Private Financing John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) Guiding you through life. Private

Qualified Personal Residence Trust (QPRT)

") Qualified Personal Residence Trust (QPRT) Overview A Qualified Personal Residence Trust (QPRT) can allow a homeowner to transfer a residence to other family members at a reduced gift tax cost while retaining

Qualified Personal Residence Trust (QPRT) Overview A Qualified Personal Residence Trust (QPRT) can allow a homeowner to transfer a residence to other family members at a reduced gift tax cost while retaining

White Paper Life Insurance Coverage on a Key Employee

White Paper Life Insurance Coverage on a Key Employee www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC,

White Paper Life Insurance Coverage on a Key Employee www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC,

Benefits Of An Irrevocable Life Insurance Trust

1 Benefits Of An Irrevocable Life Insurance Trust CHAPTER OVERVIEW Life insurance is the only asset that Congress has bestowed with most favored tax status. 1 No other investment provides the potential

1 Benefits Of An Irrevocable Life Insurance Trust CHAPTER OVERVIEW Life insurance is the only asset that Congress has bestowed with most favored tax status. 1 No other investment provides the potential

Irrevocable Life Insurance Trust (ILIT)

") THE WEALTH COUNSELOR LLC Irrevocable Life Insurance Trust (ILIT) What Is the Irrevocable Life Insurance Trust? An irrevocable trust is one in which the grantor completely gives up all rights in the property

THE WEALTH COUNSELOR LLC Irrevocable Life Insurance Trust (ILIT) What Is the Irrevocable Life Insurance Trust? An irrevocable trust is one in which the grantor completely gives up all rights in the property

Thursday, May 7 2015 WRM# 15-16

Thursday, May 7 2015 WRM# 15-16 The WRMarketplace is created exclusively for AALU Members by the AALU staff and Greenberg Traurig, one of the nation s leading tax and wealth management law firms. The WRMarketplace

Thursday, May 7 2015 WRM# 15-16 The WRMarketplace is created exclusively for AALU Members by the AALU staff and Greenberg Traurig, one of the nation s leading tax and wealth management law firms. The WRMarketplace

Understanding the Income Taxation of Life Insurance

A Reference Guide for Individuals and Businesses Understanding the Income Taxation of Life Insurance Answers to Frequently Asked Questions Tax Insights Contents 1 General Questions 4 Non-MEC Policy Questions

A Reference Guide for Individuals and Businesses Understanding the Income Taxation of Life Insurance Answers to Frequently Asked Questions Tax Insights Contents 1 General Questions 4 Non-MEC Policy Questions

INTERNAL REVENUE SERVICE. Number: 200119039 Release Date: 5/11/2001 UIL Nos. 831.03-00 832.00-00. CC:FIP:4 PLR-119217-00 February 8, 2001.

INTERNAL REVENUE SERVICE Number: 200119039 Release Date: 5/11/2001 UIL Nos. 831.03-00 832.00-00 CC:FIP:4 PLR-119217-00 February 8, 2001 Taxpayer = Parent = Subsidiary = Commercial IC = State = Date A =

INTERNAL REVENUE SERVICE Number: 200119039 Release Date: 5/11/2001 UIL Nos. 831.03-00 832.00-00 CC:FIP:4 PLR-119217-00 February 8, 2001 Taxpayer = Parent = Subsidiary = Commercial IC = State = Date A =

The Right Prescription? Should Your Company's Medical Benefits Be Insured Through a Captive Insurance Company?

The Right Prescription? Should Your Company's Medical Benefits Be Insured Through a Captive Insurance Company? Kevin G. Fitzgerald and J. Michael Davis, Foley & Lardner LLP; and Troy M. Filipek and Travis

The Right Prescription? Should Your Company's Medical Benefits Be Insured Through a Captive Insurance Company? Kevin G. Fitzgerald and J. Michael Davis, Foley & Lardner LLP; and Troy M. Filipek and Travis

DOWNLOAD THE VCIA CONFERENCE APP!

DOWNLOAD THE VCIA CONFERENCE APP! http://m.core-apps.com/vcia_ac2014 vcia vcia2014 Download the App Plug in our Username: vcia And Password: vcia2014 View App Captives 102 -Tax Fundamentals Panelists:

DOWNLOAD THE VCIA CONFERENCE APP! http://m.core-apps.com/vcia_ac2014 vcia vcia2014 Download the App Plug in our Username: vcia And Password: vcia2014 View App Captives 102 -Tax Fundamentals Panelists:

Non-Equity Collateral Assignment Split Dollar for Estate Liquidity

Non-Equity Collateral Assignment Split Dollar for Estate Liquidity Using Life Insurance Presented by

Non-Equity Collateral Assignment Split Dollar for Estate Liquidity Using Life Insurance Presented by

Notice 97-34, 1997-1 CB 422, 6/02/1997, IRC Sec(s). 6048

. 6048") Notice 97-34, 1997-1 CB 422, 6/02/1997, IRC Sec(s). 6048 Returns of foreign trusts foreign gift reporting requirements tax This notice provides guidance regarding the new foreign trust and foreign gift

Notice 97-34, 1997-1 CB 422, 6/02/1997, IRC Sec(s). 6048 Returns of foreign trusts foreign gift reporting requirements tax This notice provides guidance regarding the new foreign trust and foreign gift

Estate Tax Concepts. for Edward and Tina Collins

Estate Tax Concepts for Edward and Tina Collins Joseph Davis, CLU, ChFC 215 Broad Street Charlotte, North Carolina 26292 Phone: 704-927-5555 Mobile Phone: 704-549-5555 Fax: 704-549-6666 Email: joseph.davis@aol.com

Estate Tax Concepts for Edward and Tina Collins Joseph Davis, CLU, ChFC 215 Broad Street Charlotte, North Carolina 26292 Phone: 704-927-5555 Mobile Phone: 704-549-5555 Fax: 704-549-6666 Email: joseph.davis@aol.com

Sales to Intentionally Defective Grantor Trusts (IDGT)

") Sales to Intentionally Defective Grantor Trusts (IDGT) A sale to an Intentionally Defective Grantor Trust ( IDGT ) is a sophisticated estate planning strategy that can provide substantial benefits to wealthy

Sales to Intentionally Defective Grantor Trusts (IDGT) A sale to an Intentionally Defective Grantor Trust ( IDGT ) is a sophisticated estate planning strategy that can provide substantial benefits to wealthy

Life Insurance and Estate Planning for Retirement Plans

Reynolds Financial Group LLC A Registered Investment Advisory Firm 216 Chaucer Drive Irwin, PA 15642 724-863-5005 Phone 724-863-8031 Fax wendyl@reynoldsfinancialgroup.net Life Insurance and Estate Planning

Reynolds Financial Group LLC A Registered Investment Advisory Firm 216 Chaucer Drive Irwin, PA 15642 724-863-5005 Phone 724-863-8031 Fax wendyl@reynoldsfinancialgroup.net Life Insurance and Estate Planning

BARBER EMERSON, L.C. MEMORANDUM ESTATE FREEZING THROUGH THE USE OF INTENTIONALLY DEFECTIVE GRANTOR TRUSTS

BARBER EMERSON, L.C. MEMORANDUM ESTATE FREEZING THROUGH THE USE OF INTENTIONALLY DEFECTIVE GRANTOR TRUSTS I. INTRODUCTION AND CIRCULAR 230 NOTICE A. Introduction. This Memorandum discusses how an estate

BARBER EMERSON, L.C. MEMORANDUM ESTATE FREEZING THROUGH THE USE OF INTENTIONALLY DEFECTIVE GRANTOR TRUSTS I. INTRODUCTION AND CIRCULAR 230 NOTICE A. Introduction. This Memorandum discusses how an estate

IN THIS ISSUE: July, 2011 j Income Tax Planning Concepts in Estate Planning

IN THIS ISSUE: Goals of Income Tax Planning Basic Estate Planning Has No Income Tax Impact Advanced Estate Planning Can Have Income Tax Implications Taxation of Corporations, LLCs, Partnerships and Non-

IN THIS ISSUE: Goals of Income Tax Planning Basic Estate Planning Has No Income Tax Impact Advanced Estate Planning Can Have Income Tax Implications Taxation of Corporations, LLCs, Partnerships and Non-

Advanced Wealth Transfer Strategies

Family Limited Partnerships (FLPS) Advanced Wealth Transfer Strategies The American Taxpayer Relief Act of 2012 established a permanent gift and estate tax exemption of $5 million, which is adjusted annually

Family Limited Partnerships (FLPS) Advanced Wealth Transfer Strategies The American Taxpayer Relief Act of 2012 established a permanent gift and estate tax exemption of $5 million, which is adjusted annually

Thursday, July 30 2015 WRM# 15-28

! Thursday, July 30 2015 WRM# 15-28 The WRMarketplace is created exclusively for AALU Members by the AALU staff and Greenberg Traurig, one of the nation s leading tax and wealth management law firms. The

! Thursday, July 30 2015 WRM# 15-28 The WRMarketplace is created exclusively for AALU Members by the AALU staff and Greenberg Traurig, one of the nation s leading tax and wealth management law firms. The

Incentive Stock Options

JPH Advisory Group Curtis Hearn, CFP 600 Galleria Pkwy Ste 1600 Atlanta, GA 30339 770-859-0076 curtis@jphadvisory.com www.jphadvisory.com Incentive Stock Options Page 1 of 6, see disclaimer on final page

JPH Advisory Group Curtis Hearn, CFP 600 Galleria Pkwy Ste 1600 Atlanta, GA 30339 770-859-0076 curtis@jphadvisory.com www.jphadvisory.com Incentive Stock Options Page 1 of 6, see disclaimer on final page

Wealth Transfer Planning in a Low Interest Rate Environment

Wealth Transfer Planning in a Low Interest Rate Environment MLINY0508088997 1 of 44 Did You Know 1/3 of affluent households over the age of 50 do not have an estate plan in place 31% of households with

Wealth Transfer Planning in a Low Interest Rate Environment MLINY0508088997 1 of 44 Did You Know 1/3 of affluent households over the age of 50 do not have an estate plan in place 31% of households with

The Rise of Captive Insurance Companies: Are They also an Opportunity to Address Obamacare?

The Rise of Captive Insurance Companies: Are They also an Opportunity to Address Obamacare? Moderator: Ken Levinson, Partner Faegre Baker Daniels Jeff Brimer, COO Alexius, LLC Kaya Bromley, General Counsel

The Rise of Captive Insurance Companies: Are They also an Opportunity to Address Obamacare? Moderator: Ken Levinson, Partner Faegre Baker Daniels Jeff Brimer, COO Alexius, LLC Kaya Bromley, General Counsel

The Evolution of Taxation of Split Dollar Life Insurance. by Christopher D. Scott. I. Introduction

The Evolution of Taxation of Split Dollar Life Insurance by Christopher D. Scott I. Introduction The federal government recently published final regulations and issued a revenue ruling that changes the

The Evolution of Taxation of Split Dollar Life Insurance by Christopher D. Scott I. Introduction The federal government recently published final regulations and issued a revenue ruling that changes the

GETTING THE MOST OUT OF YOUR ESOP

GETTING THE MOST OUT OF YOUR ESOP Michael G. Keeley Hunton & Williams LLP 1445 Ross Avenue Suite 3700 Dallas, Texas 75202 (214) 468-3345 mkeeley@hunton.com Traditional Sources of Capital for Community

GETTING THE MOST OUT OF YOUR ESOP Michael G. Keeley Hunton & Williams LLP 1445 Ross Avenue Suite 3700 Dallas, Texas 75202 (214) 468-3345 mkeeley@hunton.com Traditional Sources of Capital for Community

Estate planning strategies using life insurance in a trust Options for handling distributions, rollovers and conversions

Estate planning strategies using life insurance in a trust Options for handling distributions, rollovers and conversions Life s better when we re connected Table of contents Find your questions review

Estate planning strategies using life insurance in a trust Options for handling distributions, rollovers and conversions Life s better when we re connected Table of contents Find your questions review

Harry's Goals and Objectives: After meeting with his team of advisors, Harry has defined his goals and objectives as: From Randall Fisher

Transferring Business Interests to Family Members: Sale of Non- Voting Stock Interests to Grantor Dynasty Trusts Volume 5, Issue 9 Some of my clients have family-owned or closely held business interests

Transferring Business Interests to Family Members: Sale of Non- Voting Stock Interests to Grantor Dynasty Trusts Volume 5, Issue 9 Some of my clients have family-owned or closely held business interests

How To Earn A Pension From A Pension Trust

Todd M. Villarrubia Attorney at Law, LL.M. in Taxation Board Certified Expert in Estate Planning 101 W. Robert E. Lee Blvd., Suite 404, New Orleans, LA 70124 Tel 504.212.3440 Fax 504.324.0936 estateplanning@lawealthplan.com

Todd M. Villarrubia Attorney at Law, LL.M. in Taxation Board Certified Expert in Estate Planning 101 W. Robert E. Lee Blvd., Suite 404, New Orleans, LA 70124 Tel 504.212.3440 Fax 504.324.0936 estateplanning@lawealthplan.com

WHAT IS PREMIUM HOW DOES PREMIUM FINANCING? FINANCING WORK?

Life Insurance Premium Financing 1 of 5 WHAT IS PREMIUM FINANCING? Premium financing allows individuals who have a life insurance need to defer using their liquid assets to fund a life insurance policy.

Life Insurance Premium Financing 1 of 5 WHAT IS PREMIUM FINANCING? Premium financing allows individuals who have a life insurance need to defer using their liquid assets to fund a life insurance policy.

Split Dollar Insurance And Premium Financing Planning (Part 2)

") Split Dollar Insurance And Premium Financing Planning (Part 2) Donald O. Jansen C. Loans To Finance Premiums 1. Concept a. Why Use Loans To Finance Premiums? i. Reduces Gifts To Trust. If the premium exceeds

Split Dollar Insurance And Premium Financing Planning (Part 2) Donald O. Jansen C. Loans To Finance Premiums 1. Concept a. Why Use Loans To Finance Premiums? i. Reduces Gifts To Trust. If the premium exceeds

ADVISING CLIENTS ABOUT LIFE INSURANCE: A PRIMER 1. By Andrew J. Willms, J.D. LL.M. John C. Zimdars, Jr., CLU ChFC. Introduction

ADVISING CLIENTS ABOUT LIFE INSURANCE: A PRIMER 1 By Andrew J. Willms, J.D. LL.M. John C. Zimdars, Jr., CLU ChFC Introduction Over the last several years, tax reform has made tax planning increasingly

ADVISING CLIENTS ABOUT LIFE INSURANCE: A PRIMER 1 By Andrew J. Willms, J.D. LL.M. John C. Zimdars, Jr., CLU ChFC Introduction Over the last several years, tax reform has made tax planning increasingly

Presented By: Jeffrey R. Matsen, J.D. David B. Liptz, CPA. March 2010 by Jeffrey R. Matsen

CAPTIVES AND WEALTH TRANSFER AND ESTATE PLANNING Presented By: Jeffrey R. Matsen, J.D. David B. Liptz, CPA March 2010 by Jeffrey R. Matsen +,-,. ") ) /#!! " #"! $%& $ '$ ( $ ( ) %'!" *!! 0 1 (, 2 ( 3 3%)

CAPTIVES AND WEALTH TRANSFER AND ESTATE PLANNING Presented By: Jeffrey R. Matsen, J.D. David B. Liptz, CPA March 2010 by Jeffrey R. Matsen +,-,. ") ) /#!! " #"! $%& $ '$ ( $ ( ) %'!" *!! 0 1 (, 2 ( 3 3%)

Understanding Captives and Alternative Risk Transfer

Understanding Captives and Alternative Risk Transfer Putting your insurance premiums to work for you Managing risk as you manage your bottom line What do Verizon, Coca-Cola, BP and most Fortune 500 sized

Understanding Captives and Alternative Risk Transfer Putting your insurance premiums to work for you Managing risk as you manage your bottom line What do Verizon, Coca-Cola, BP and most Fortune 500 sized

Table of Contents. 1. Company description 1-1 1.1 Organization structure 1-1

Clal Insurance Enterprises Holdings Ltd Financial Statements As At September 30,, 2014 Board of Directors' Report..11 Condensed consolidated interim financial statements....21 Financial data from the consolidated

Clal Insurance Enterprises Holdings Ltd Financial Statements As At September 30,, 2014 Board of Directors' Report..11 Condensed consolidated interim financial statements....21 Financial data from the consolidated

IMPACT. May/June 2014. Capturing the benefits of captive insurance. How defined-value gifts can help limit your tax exposure

tax May/June 2014 IMPACT Capturing the benefits of captive insurance How defined-value gifts can help limit your tax exposure Undisclosed foreign accounts: Handle with care Tax Tips Hire your kids to save

tax May/June 2014 IMPACT Capturing the benefits of captive insurance How defined-value gifts can help limit your tax exposure Undisclosed foreign accounts: Handle with care Tax Tips Hire your kids to save

Split-Dollar Insurance and the Closely Held Business By: Larry Brody, Esq., Richard Harris, CLU and Martin M. Shenkman, Esq.

Split-Dollar Insurance and the Closely Held Business By: Larry Brody, Esq., Richard Harris, CLU and Martin M. Shenkman, Esq. Introduction Split-dollar is a mechanism for owning and paying for life insurance

Split-Dollar Insurance and the Closely Held Business By: Larry Brody, Esq., Richard Harris, CLU and Martin M. Shenkman, Esq. Introduction Split-dollar is a mechanism for owning and paying for life insurance

Survivorship Builder. An indexed survivorship life policy AS2000 (04-15)

") Survivorship Builder An indexed survivorship life policy AS2000 (04-15) Accordia Life believes in the essence of family. Your family may be a traditional one. It may be a group of people who care for

Survivorship Builder An indexed survivorship life policy AS2000 (04-15) Accordia Life believes in the essence of family. Your family may be a traditional one. It may be a group of people who care for

CRT with assets that, if sold by you, would generate a long-term capital gain, your CHARITABLE REMAINDERTRUSTS

The Charitable Remainder Unitrust CRT ) can be an effective means for diversifying highly appreciated assets while avoiding or postponing capital gains tax, increasing cash flow during your lifetime, obtaining

The Charitable Remainder Unitrust CRT ) can be an effective means for diversifying highly appreciated assets while avoiding or postponing capital gains tax, increasing cash flow during your lifetime, obtaining

Captive Insurance Companies

Monthly White Paper Series November, 2012 Captive Insurance Companies This month focuses on a well established, but often underutilized tool for business owners in managing risks and providing added tax

Monthly White Paper Series November, 2012 Captive Insurance Companies This month focuses on a well established, but often underutilized tool for business owners in managing risks and providing added tax

Divorce and Estate Planning

ATTORNEYS AT LAW THE ANDERSEN FIRM A PROFESSIONAL CORPORATION Divorce and Estate Planning 866.230.2206 www.theandersenfirm.com South Florida Office West Florida Office Florida Keys Office Tennessee Office

ATTORNEYS AT LAW THE ANDERSEN FIRM A PROFESSIONAL CORPORATION Divorce and Estate Planning 866.230.2206 www.theandersenfirm.com South Florida Office West Florida Office Florida Keys Office Tennessee Office

4.76.23 Small Insurance Companies or Associations IRC 501(c)(15)

(15)") US Captive Insurance Company Income Tax Audit Guidelines, Captive Foreign Corporation Tax Audit Guidelines, and Captive Liquidation Tax Audit Guidelines Issued by the IRS (offered by Tom Cifelli, data

US Captive Insurance Company Income Tax Audit Guidelines, Captive Foreign Corporation Tax Audit Guidelines, and Captive Liquidation Tax Audit Guidelines Issued by the IRS (offered by Tom Cifelli, data

UTILIZATION OF CAPTIVES TODAY

UTILIZATION OF CAPTIVES TODAY The Oklahoma Captive Conference April 30, 2014 Ellyn Casazza Senior Vice President Marsh Captive Solutions Group Utilization of Captives Today Objectives of Discussion 1.

UTILIZATION OF CAPTIVES TODAY The Oklahoma Captive Conference April 30, 2014 Ellyn Casazza Senior Vice President Marsh Captive Solutions Group Utilization of Captives Today Objectives of Discussion 1.

Fundamentals of Captive Insurance Companies

Fundamentals of Captive Insurance Companies Bridgebay Consulting & Northern Trust Company Corporate Treasurers Seminar Tuesday, March 22, 2005 Hyatt Regency San Francisco Airport Thomas M. Jones, Partner

Fundamentals of Captive Insurance Companies Bridgebay Consulting & Northern Trust Company Corporate Treasurers Seminar Tuesday, March 22, 2005 Hyatt Regency San Francisco Airport Thomas M. Jones, Partner

Insurance. Survivorship Life. Insurance. The Company You Keep

Insurance Survivorship Life Insurance The Company You Keep Permanent Life Insurance Protection for Two People You ve built a legacy, but who will be the recipients your heirs or the IRS? 1 Now is the time

Insurance Survivorship Life Insurance The Company You Keep Permanent Life Insurance Protection for Two People You ve built a legacy, but who will be the recipients your heirs or the IRS? 1 Now is the time