Pension Saving and Retirement Insecurity: The case of Australia. Mike Rafferty University of Sydney

|

|

|

- Lenard Arnold

- 8 years ago

- Views:

Transcription

1 The New Paradox of Thrift -Mandatory Pension Saving and Retirement Insecurity: The case of Australia Mike Rafferty University of Sydney

2 Outline The GFC, pensions and the vulnerabilities of financialized capitalism The Australian System and Global Pension Reform Lessons from the Australian Experience

3 Paradox of thrift Australia has 9% compulsory pension savings contributions (in privately managed DC schemes) and very generous tax concessions for voluntary contributions, in addition to a PAYG public pension Now more than a trillion dollars in pension assets (more than annual GDP). Yet people are now more anxious and more skeptical than ever about retiring and about the security they will have in retirement This can be seen as part of the wider outcome of the risk transfer/ financialization of labour (Jacob Hacker, Randy Martin) It has included such things as privatization, commercialisation of public services, the increasing use if credit to suppport consumption, and has required increasing the amount of paid labour from households (Warren the Two Income Trap)

It has included such things as privatization, commercialisation of public services, the increasing use if credit to suppport")

4 Australia and the New Global Policy Approach to retirement WB argument was that ageing/fiscal crisis means that old systems approaches won t work. Mandatory pillar the new direction in developing countries need to build retirement around mandatory pillar - Chile and Eastern Europe in developed economies old pension promise needs to be broken, and shift toward private funding - Australia Behind the argument is really the privatisation of an important part of social welfare (Richard Minns, Mitchell Orenstein) and the financialization of everyday life (Randy Martin)

and the financialization of everyday life (Randy")

5 Australia a leader in adoption of World Bank s privatized compulsory super Case of Australia is interesting because since the early 1980s moved a long toward making mandatory contribution ti defined d contribution ti schemes the centre of its pension financing system. Currently a mandatory 9% of all wages and salaries paid into privately managed funds, plus generous tax concessions for voluntary contributions. Now one of few countries with pension assets greater than annual GDP Originally deferred wages to reduce current consumption but promise of greater consumption (better retirement) later Bringing benefits of super from professionals and public servants to all workers Increased national saving Now public pension a safety net and mandatory super the core of retirement financing

later Bringing")

6 Lessons a. disaggregated and b. aggregated 1.a. Agency costs in fund management are significant, and b. so are (foregone) capital stewardship issues 2. a. Reluctant (or conscripted ) fund members don t and won t discipline fund managers, and b. this can only really be done collectively by the state or workers 3. a. GFC revealed the scale of risk transfer in mandatory DC schemes and many of these risks are simply not appropriate for workers to bear, and b. raises issue about whether compulsory DC schemes should be at the centre of a pension financing system 4. a. Compulsory privately managed super a very large and poorly regulated P3 scheme b Danger that Super industry (including union-sponsored funds) becoming a political force in its own right and defining adequacy and how it is funded 13 or 15%, and non or deferred retirement (the new fourth pillar) 5. a. Issue of pension adequacy is complex in light of longevity and future income needs, and b. financial education (the Obama mantra) won t fix things it is about about reinforcing the risk shift and many workers especially low income or with broken work patterns are deferring wages for no future benefit system 6. a. Conflict and compromise at heart of retirement policy (Barr and Diamond, Minns) we need to continually ask what are the objectives that are being targeted, and consequently what is being traded off, and b. what are workers interests? Takeaway Retirement security is complex (involves labour market, health, productivity, household formation, housing, public and private services etc).and so is financing it. More (forced) savings won t necessarily guarantee a more secure and better retirement for all. Pension plans in Australia that began as a way of supplementing the age pension and offered the prospect of labour sharing in the unearned income we produce. After 25 years of compulsory super people living in more financial stress and anxiety, and is also going to asked to pay more (13-15%) and work longer as well.

7 Agency Costs in Fund Management Australia a good natural experiment in fund governance. It has two quite different models: - privately run for profit funds part of large financial conglomerates - employer based government and company schemes run on a not for profit basis - multi-employer funds run on a not for profit basis 1. For profit funds appoint trustees who are typically employees of financial conglomerate 2. Not for profit funds have tustees representing employers and employees

8 Agency costs matter Evidence from range of sources, using different measurement techniques and data all point in ame direction. Representative trustees/nfp status outperform For profit appointed trustee funds. In research we did for the Australian Institute te of Superannuation Trustees (AIST) we found returns between the two types of fund governance were between 1.4 and 2.4% per annum- which would mean significant differences in final pension benefit.

9 But what sort of trustee model? Australia has a system which is complex, and involves lots of hidden conflicts and compromises. One way of thinking about the tensions in fund management is to ask what sort of fund member we have Investor (in a pooled investment vehicle) Beneficiary (of a trust), and Citizen (in a PPP fund charged with delivering retirement financing) The difference between each model is non-trivial Lesson: Agency costs matter and many tensions embedded in system

Beneficiary (of a trust), and Citizen (in a PPP fund charged with delivering retirement")

10 Trusteeship and agency costs In Australia trustees have a fiduciary duty to members, and has produced a very conservative hands off approach to investment, corporate governance, ESG labour and human rights. BUT, funds provide and charge for: Financial advice (including trailing commissions) Insurance (life, income protection TPD) Advertising Other services

")

11 Choice with Reluctant Members Regulatory model In Australia assumes informed and active investors. The job of fund members is to discipline fund managers to deliver for members best risk adjusted returns at lowest cost. Therefore members now have Choice: of fund and fund option. But know that there is very little switching, and research shows very little relationship between performance and fund flows - we found size of fund better predictor of flows than any other factor. Lesson: can t rely on market governance (fund members) to discipline fund managers ie regulation pension design and internal fund governance (trustees etc) becomes critical Financial education won t work - it will as researchers from Austrian Central Bank have argued is about sending a message that risk management is now idnividualised

to discipline fund managers ie regulation pension design and internal fund governance (trustees etc) becomes critical Financial education won t")

12 Labour and Mandatory DC schemes In Australia, trade union were critical to the development of mandatory DC pension system May have begun as a supplement to public system. But now becoming the core of the system. Now with GFC and system maturity projections showing that current system won t deliver better and more secure retirement that public pension Increasing recognition that relying on it to deliver base load retirement power will not work Unions have been leading calls for move mandatory contributions from 9% to 13-15% 15% contributions. More deferred income for the promise of financialized private retirement. AND government has added 4 th tier to retirement policy non- retirement (working age moving up from 65 to 67..to 70.

13 Retirement Policy - Conflict and Compromise. Multiple objectives of any retirement system Consumption smoothing Longevity insurance Production Distribution Labour market Volunteer/care sector Fiscal sustainability? Multiple objectives means tradeoffs or conflicts which need to be recognize (Barr and Diamond 2008) Lesson: Need to ask and answer question what are the objectives being maximised i in the system?

")

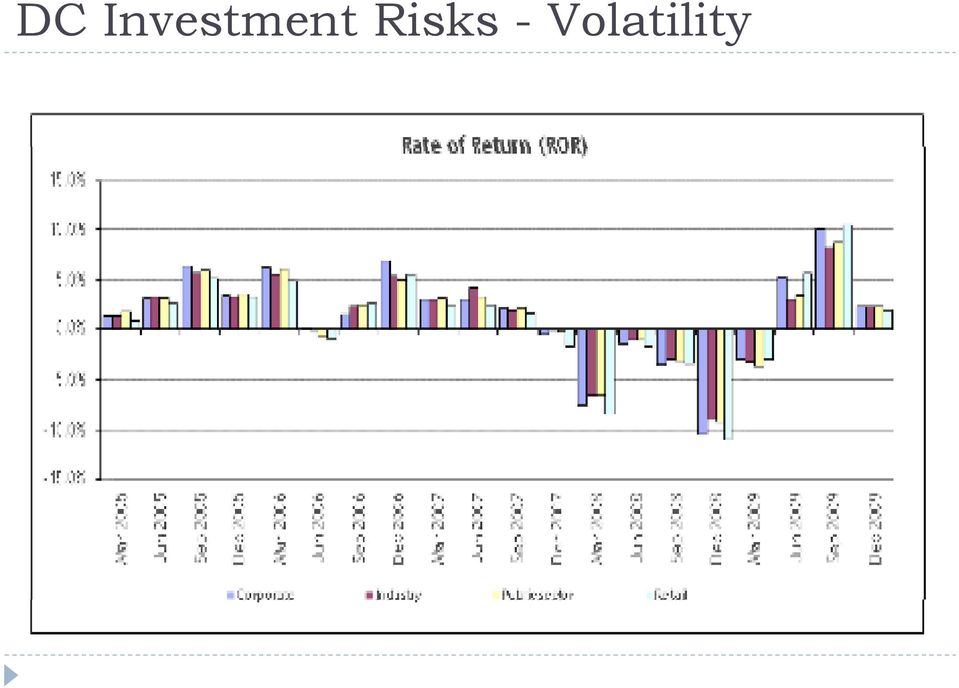

14 DC Investment Risks - Volatility

15

16

Demographics issues and Pension systems. Najat El Mekkaoui de Freitas najat.el-mekkaoui@dauphine.fr. Université Paris Dauphine.

Demographics issues and Pension systems Najat El Mekkaoui de Freitas najat.el-mekkaoui@dauphine.fr Université Paris Dauphine May, 2009 The demographic and economic challenges Over the next decades many

Demographics issues and Pension systems Najat El Mekkaoui de Freitas najat.el-mekkaoui@dauphine.fr Université Paris Dauphine May, 2009 The demographic and economic challenges Over the next decades many

COUNTRY PROFILE - MAURITIUS

COUNTRY PROFILE - MAURITIUS DEMOGRAPHICS AND MACROECONOMICS 2011 2012 Gross Domestic Product (GDP) at market prices (MUR Million) 322,773 344,550 GDP per capita at Market Prices (MUR) 250,924 266,816 Population

COUNTRY PROFILE - MAURITIUS DEMOGRAPHICS AND MACROECONOMICS 2011 2012 Gross Domestic Product (GDP) at market prices (MUR Million) 322,773 344,550 GDP per capita at Market Prices (MUR) 250,924 266,816 Population

The Cypriot Pension System: Adequacy and Sustainability

Cyprus Economic Policy Review, Vol. 6, No. 2, pp. 49-58 (2012) 1450-4561 49 The Cypriot Pension System: Adequacy and Sustainability Philippos Mannaris Aon Hewitt Abstract The fundamental objective of pension

Cyprus Economic Policy Review, Vol. 6, No. 2, pp. 49-58 (2012) 1450-4561 49 The Cypriot Pension System: Adequacy and Sustainability Philippos Mannaris Aon Hewitt Abstract The fundamental objective of pension

Australia: Retirement Income and Annuities Markets. Contractual Savings Conference April 2008 Greg Brunner

Australia: Retirement Income and Annuities Markets Contractual Savings Conference April 2008 Greg Brunner Pension system Age pension in place since 1908, funded on a payas-you go basis Means testing. The

Australia: Retirement Income and Annuities Markets Contractual Savings Conference April 2008 Greg Brunner Pension system Age pension in place since 1908, funded on a payas-you go basis Means testing. The

ASFA Research and Resource Centre

ASFA Research and Resource Centre Employer contributions to superannuation in excess of 9% of wages Results of survey and other research Ross Clare Director of Research March 2010 Association of Superannuation

ASFA Research and Resource Centre Employer contributions to superannuation in excess of 9% of wages Results of survey and other research Ross Clare Director of Research March 2010 Association of Superannuation

An Ageing Australia: Preparing for the Future

An Ageing Australia: Preparing for the Future Mike Woods Deputy Chairman, Productivity Commission COTA National Policy Forum Productivity Commission million 90% confidence interval 95% confidence interval

An Ageing Australia: Preparing for the Future Mike Woods Deputy Chairman, Productivity Commission COTA National Policy Forum Productivity Commission million 90% confidence interval 95% confidence interval

FSC SUPERANNUATION CORPORATE GOVERNANCE POLICY RAISING THE BAR

FSC SUPERANNUATION CORPORATE GOVERNANCE POLICY RAISING THE BAR Australia s pool of managed funds is the fourth largest in the world at $AUD1.8 trillion, of which $1.3 trillion is held in superannuation.

FSC SUPERANNUATION CORPORATE GOVERNANCE POLICY RAISING THE BAR Australia s pool of managed funds is the fourth largest in the world at $AUD1.8 trillion, of which $1.3 trillion is held in superannuation.

Changes to regulatory settings for financial products dealing with longevity

ASFA Research and Resource Centre Changes to regulatory settings for financial products dealing with longevity Ross Clare Director of Research October 2013 ASFA Level 6 66 Clarence Street Sydney NSW 2000

ASFA Research and Resource Centre Changes to regulatory settings for financial products dealing with longevity Ross Clare Director of Research October 2013 ASFA Level 6 66 Clarence Street Sydney NSW 2000

JOHN RALFE CONSULTING

Mr Andrew Lennard Accounting Standards Board Aldwych House 71-91 Aldwych London WC2B 4HN July 14th 2008 Dear Andrew Discussion Paper The Financial Reporting of Pensions January 2008 As you know I was a

Mr Andrew Lennard Accounting Standards Board Aldwych House 71-91 Aldwych London WC2B 4HN July 14th 2008 Dear Andrew Discussion Paper The Financial Reporting of Pensions January 2008 As you know I was a

Australia s Future Tax System Preliminary Submission from the Institute of Actuaries of Australia

21 October 2008 AFTS Secretariat The Treasury Langton Crescent PARKES ACT 2600 Email: AFTS@treasury.gov.au Dear Sir/Madam Purpose Australia s Future Tax System Preliminary Submission from the Institute

21 October 2008 AFTS Secretariat The Treasury Langton Crescent PARKES ACT 2600 Email: AFTS@treasury.gov.au Dear Sir/Madam Purpose Australia s Future Tax System Preliminary Submission from the Institute

Smart strategies for maximising retirement income

Smart strategies for maximising retirement income 2010 Why you need to create a life-long income Australia has one of the highest life expectancies in the world and the average retirement length has increased

Smart strategies for maximising retirement income 2010 Why you need to create a life-long income Australia has one of the highest life expectancies in the world and the average retirement length has increased

Why understanding asset allocation could improve your SMSF returns. By Peter Switzer & Paul Rickard BROUGHT TO YOU BY AMP CAPITAL

Why understanding asset allocation could improve your SMSF returns By Peter Switzer & Paul Rickard WELCOME To put together a comprehensive investment strategy, and maximise the returns of your self-managed

Why understanding asset allocation could improve your SMSF returns By Peter Switzer & Paul Rickard WELCOME To put together a comprehensive investment strategy, and maximise the returns of your self-managed

If you work in Australia, your employer may have to contribute to a superannuation fund for you under the Superannuation Guarantee system if you:

Superannuation is a tax advantaged way of saving for retirement and makes up two of the three pillars of the Government s retirement income policy. The three pillars are: A Government funded means-tested

Superannuation is a tax advantaged way of saving for retirement and makes up two of the three pillars of the Government s retirement income policy. The three pillars are: A Government funded means-tested

Superannuation And Insurance For. People With Cancer (NEW SOUTH WALES EDITION)

") Superannuation And Insurance For People With Cancer (NEW SOUTH WALES EDITION) Prepared by John Berrill John Berrill Maurice Blackburn Lawyers Level 20, 201 Elizabeth Street, Sydney Phone: 1800 810 812

Superannuation And Insurance For People With Cancer (NEW SOUTH WALES EDITION) Prepared by John Berrill John Berrill Maurice Blackburn Lawyers Level 20, 201 Elizabeth Street, Sydney Phone: 1800 810 812

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES AUSTRALIA

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions AUSTRALIA Australia: pension system in 2008

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions AUSTRALIA Australia: pension system in 2008

EXECUTIVE SUMMARY. SUBMISSION 12 March 2014 Final www.industrysuperaustralia.com 2

EXECUTIVE SUMMARY ISA welcomes the opportunity to comment on the Government s Commission of Audit. Australia s superannuation system, which is a key pillar of our retirement income architecture, serves

EXECUTIVE SUMMARY ISA welcomes the opportunity to comment on the Government s Commission of Audit. Australia s superannuation system, which is a key pillar of our retirement income architecture, serves

Retirement income in Australia

Retirement income in Australia The development of adequacy over time Joint research by Towers Watson and The University of Melbourne Presented by John Burnett 7 July 2015 Background Purpose of research

Retirement income in Australia The development of adequacy over time Joint research by Towers Watson and The University of Melbourne Presented by John Burnett 7 July 2015 Background Purpose of research

Project LINK Meeting New York, 20-22 October 2010. Country Report: Australia

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

Australian superannuation funds should be exempt from FATCA withholding obligations on this basis.

7 May 2012 CC:PA:LPD:PR (REG-121647-10) Room 5205 Internal Revenue Service PO Box 7604 Ben Franklin Station Washington D.C. 20044 United States of America Reg-121647-10: Regulations Relating to Information

7 May 2012 CC:PA:LPD:PR (REG-121647-10) Room 5205 Internal Revenue Service PO Box 7604 Ben Franklin Station Washington D.C. 20044 United States of America Reg-121647-10: Regulations Relating to Information

Review into the Governance, Efficiency, Structure and Operation of Australia's Superannuation System

Review into the Governance, Efficiency, Structure and Operation of Australia's Superannuation System ACTU submission on Structure 26 February 2010 D No 01/2010 Introduction The review panel s papers on

Review into the Governance, Efficiency, Structure and Operation of Australia's Superannuation System ACTU submission on Structure 26 February 2010 D No 01/2010 Introduction The review panel s papers on

Demographics, financial crisis & pensions How to help the system?

Demographics, financial crisis & pensions How to help the system? Violeta Ciurel, Regional CEO Greenfields & Business Development - ING Insurance Central Europe European Parliament The Social Impact of

Demographics, financial crisis & pensions How to help the system? Violeta Ciurel, Regional CEO Greenfields & Business Development - ING Insurance Central Europe European Parliament The Social Impact of

Canada s Retirement Security Crisis. National Union of Public and General Employees (NUPGE) Ottawa, Canada: January 2012

Ottawa, Canada: January 2012") Canada s Retirement Security Crisis National Union of Public and General Employees (NUPGE) Ottawa, Canada: January 2012 MYTH1 Most public sector employees have a gold-plated pension. No, in fact the far

Canada s Retirement Security Crisis National Union of Public and General Employees (NUPGE) Ottawa, Canada: January 2012 MYTH1 Most public sector employees have a gold-plated pension. No, in fact the far

The Thrift Savings Plan (TSP): The US Experience with Complementary Pension Funds for Federal Civil Servants

: The US Experience with Complementary Pension Funds for Federal Civil Servants") The Thrift Savings Plan (TSP): The US Experience with Complementary Pension Funds for Federal Civil Servants James Petrick General Counsel Federal Retirement Thrift Investment Board May 6, 2015 1 Outline

The Thrift Savings Plan (TSP): The US Experience with Complementary Pension Funds for Federal Civil Servants James Petrick General Counsel Federal Retirement Thrift Investment Board May 6, 2015 1 Outline

Governance working group

Governance working group Issues paper on trustee and director duties March 2011 PROPOSED REFORM The Government s response to recommendation 2.1 of the Super System Review included in principle support

Governance working group Issues paper on trustee and director duties March 2011 PROPOSED REFORM The Government s response to recommendation 2.1 of the Super System Review included in principle support

Superannuation And Insurance For. People With Blood Cancer (SOUTH AUSTRALIAN EDITION)

") Superannuation And Insurance For People With Blood Cancer (SOUTH AUSTRALIAN EDITION) Prepared by John Berrill John Berrill Maurice Blackburn Lawyers Level 10, 456 Lonsdale Street, Melbourne Phone: 1800

Superannuation And Insurance For People With Blood Cancer (SOUTH AUSTRALIAN EDITION) Prepared by John Berrill John Berrill Maurice Blackburn Lawyers Level 10, 456 Lonsdale Street, Melbourne Phone: 1800

CLIENT FACT SHEET. If you are under age 65 you may make personal contributions to superannuation on your own behalf.

CLIENT FACT SHEET July 2010 Understanding superannuation and superannuation contributions Superannuation is an investment vehicle designed to assist Australians in saving for their retirement. The Government

CLIENT FACT SHEET July 2010 Understanding superannuation and superannuation contributions Superannuation is an investment vehicle designed to assist Australians in saving for their retirement. The Government

We all have dreams about retirement. Some day you expect to retire, and you

Sustainability, Cost-Effectiveness, Fairness and Value A Primer on Modern Pension Plan Design Dr. Bruce Kennedy, Executive Director BC Public Service Pension Plan May 2013 We all have dreams about retirement.

Sustainability, Cost-Effectiveness, Fairness and Value A Primer on Modern Pension Plan Design Dr. Bruce Kennedy, Executive Director BC Public Service Pension Plan May 2013 We all have dreams about retirement.

Superannuation And Insurance For. People With Huntington s Disease (WESTERN AUSTRALIAN EDITION)

") Superannuation And Insurance For People With Huntington s Disease (WESTERN AUSTRALIAN EDITION) Prepared by Phil Gleeson Phil Gleeson Maurice Blackburn Lawyers Unit 1, 328 Carrington Street, Hamilton Hill

Superannuation And Insurance For People With Huntington s Disease (WESTERN AUSTRALIAN EDITION) Prepared by Phil Gleeson Phil Gleeson Maurice Blackburn Lawyers Unit 1, 328 Carrington Street, Hamilton Hill

R. LITVINOV, PhD student in Law, Kharkiv National University of Internal Affairs,

R. LITVINOV, PhD student in Law, Kharkiv National University of Internal Affairs, SOCIAL SECURITY SYSTEM IN THE USA: GOOD OR BAD EXPERIENCE FOR UKRAINE? Analyzing the process of implementation of the pension

R. LITVINOV, PhD student in Law, Kharkiv National University of Internal Affairs, SOCIAL SECURITY SYSTEM IN THE USA: GOOD OR BAD EXPERIENCE FOR UKRAINE? Analyzing the process of implementation of the pension

Eugene Bland, Texas A&M University Corpus Christi Robert Trimm, Freed-Hardeman University Judson Ruig, Francis Marion University ABSTRACT

An Investigation of the Impact on Retirement Benefits from Changing the Defined Benefit US Social Security System to the Defined Contribution Australian Superannuation System: Data from 1980 through 2010

An Investigation of the Impact on Retirement Benefits from Changing the Defined Benefit US Social Security System to the Defined Contribution Australian Superannuation System: Data from 1980 through 2010

The Canadian Income Security System and Economic Well Being Michael Baker University of Toronto

The Canadian Income Security System and Economic Well Being Michael Baker University of Toronto Much of this material is drawn from the paper Michael Baker and Dwayne Benjamin, The Evolving Retirement

The Canadian Income Security System and Economic Well Being Michael Baker University of Toronto Much of this material is drawn from the paper Michael Baker and Dwayne Benjamin, The Evolving Retirement

MLC MasterKey Super & Pension Fundamentals MLC MasterKey Super & Pension How to Guide

MLC MasterKey Super & Pension Fundamentals MLC MasterKey Super & Pension How to Guide Preparation date 1 July 2015 Issued by The Trustee, MLC Nominees Pty Limited (MLC) ABN 93 002 814 959 AFSL 230702 The

MLC MasterKey Super & Pension Fundamentals MLC MasterKey Super & Pension How to Guide Preparation date 1 July 2015 Issued by The Trustee, MLC Nominees Pty Limited (MLC) ABN 93 002 814 959 AFSL 230702 The

Wellard Superannuation Better Tax Submission

Justification for Superannuation Wellard Superannuation Better Tax Submission It is well documented that Australia has an aging population and consequently less workers will be available to support the

Justification for Superannuation Wellard Superannuation Better Tax Submission It is well documented that Australia has an aging population and consequently less workers will be available to support the

A DIFFERENT KIND OF WEALTH MANAGEMENT FIRM. www.jaswealth.com.au. Superannuation 101. Everything you always wanted to know but were too afraid to ask

A DIFFERENT KIND OF WEALTH MANAGEMENT FIRM www.jaswealth.com.au Superannuation 101 Everything you always wanted to know but were too afraid to ask What is Superannuation? Superannuation 101 Contents What

A DIFFERENT KIND OF WEALTH MANAGEMENT FIRM www.jaswealth.com.au Superannuation 101 Everything you always wanted to know but were too afraid to ask What is Superannuation? Superannuation 101 Contents What

IPPR speech Pension reform in the public services

IPPR speech Pension reform in the public services 23 June 2011 Good morning everybody. Can I start by thanking the IPPR for giving me this opportunity to say a few words about pension reform in the public

IPPR speech Pension reform in the public services 23 June 2011 Good morning everybody. Can I start by thanking the IPPR for giving me this opportunity to say a few words about pension reform in the public

How To Understand The Economic And Social Costs Of Living In Australia

Australia s retirement provision: the decumulation challenge John Piggott Director CEPAR Outline of talk Introduction to Australian retirement policy Issues in Longevity Current retirement products in

Australia s retirement provision: the decumulation challenge John Piggott Director CEPAR Outline of talk Introduction to Australian retirement policy Issues in Longevity Current retirement products in

Prudential Supervision of Insurance in Australia. Chris Lewis Immediate Past President

Prudential Supervision of Insurance in Australia Chris Lewis Immediate Past President REGULATORY FRAMEWORK RBA APRA ASIC ACCC Monetary Policy System Stability Payments System Prudential supervision - banks

Prudential Supervision of Insurance in Australia Chris Lewis Immediate Past President REGULATORY FRAMEWORK RBA APRA ASIC ACCC Monetary Policy System Stability Payments System Prudential supervision - banks

140 Greenhill Road, Unley South Australia 5061 // T: +61 8 8373 5588 // F: +61 8 8373 5933 // E: kennedy@kennedy.com.au. Tax Planning 2014/15

140 Greenhill Road, Unley South Australia 5061 // T: +61 8 8373 5588 // F: +61 8 8373 5933 // E: kennedy@kennedy.com.au Tax Planning 2014/15 30 June 2014 Trust Distributiion Resolutions Tax Rates and Impact

140 Greenhill Road, Unley South Australia 5061 // T: +61 8 8373 5588 // F: +61 8 8373 5933 // E: kennedy@kennedy.com.au Tax Planning 2014/15 30 June 2014 Trust Distributiion Resolutions Tax Rates and Impact

Province of Nova Scotia Department of Finance MECHANISMS FOR ENHANCING THE RETIREMENT INCOME SYSTEM IN CANADA

Province of Nova Scotia Department of Finance MECHANISMS FOR ENHANCING THE RETIREMENT INCOME SYSTEM IN CANADA The Government of Nova Scotia is working with other provinces and territories, and the Government

Province of Nova Scotia Department of Finance MECHANISMS FOR ENHANCING THE RETIREMENT INCOME SYSTEM IN CANADA The Government of Nova Scotia is working with other provinces and territories, and the Government

Service in Public Sector: The pension system in Mauritius and Superannuation

Service in Public Sector: The pension system in Mauritius and Superannuation Namratta B. Becceea The University of Mauritius Reduit, Mauritius Email: namratta28@hotmail.com Le Meridien Hotel, Mauritius,

Service in Public Sector: The pension system in Mauritius and Superannuation Namratta B. Becceea The University of Mauritius Reduit, Mauritius Email: namratta28@hotmail.com Le Meridien Hotel, Mauritius,

IOPS Member country or territory pension system profile: TRINIDAD AND TOBAGO. Update as of 15 February 2013

IOPS Member country or territory pension system profile: TRINIDAD AND TOBAGO Report 1 issued on September 2011, validated by the Central Bank of Trinidad and Tobago Update as of 15 February 2013 1 This

IOPS Member country or territory pension system profile: TRINIDAD AND TOBAGO Report 1 issued on September 2011, validated by the Central Bank of Trinidad and Tobago Update as of 15 February 2013 1 This

Enhancements to ING s diversified investment funds

Enhancements to ING s diversified investment funds Effective 1 November 2005 Our investment managers, ING Investment Management Limited (INGIM), recently conducted a review of ING s diversified investment

Enhancements to ING s diversified investment funds Effective 1 November 2005 Our investment managers, ING Investment Management Limited (INGIM), recently conducted a review of ING s diversified investment

TAX & SUPERANNUATION:

SECURING RETIREMENT INCOMES TAX & SUPERANNUATION: BENCHMARKING AUSTRALIA AGAINST THE WORLD S BEST RETIREMENT SAVINGS SYSTEMS FEBRUARY 2013 CONTENTS 1 Executive Summary 2 Introduction 3 The variety of retirement

SECURING RETIREMENT INCOMES TAX & SUPERANNUATION: BENCHMARKING AUSTRALIA AGAINST THE WORLD S BEST RETIREMENT SAVINGS SYSTEMS FEBRUARY 2013 CONTENTS 1 Executive Summary 2 Introduction 3 The variety of retirement

Designing the Payout Phase: Main Policy Issues and Options Roberto Rocha

Designing the Payout Phase: Main Policy Issues and Options Roberto Rocha 5 th Contractual Savings Conference, The World Bank/IFC Washington DC, January 10, 2012 Structure of the Presentation The Payout

Designing the Payout Phase: Main Policy Issues and Options Roberto Rocha 5 th Contractual Savings Conference, The World Bank/IFC Washington DC, January 10, 2012 Structure of the Presentation The Payout

services system Reports Act 1988 (Cth) Australia has a sophisticated and stable banking and financial services system.

Australia has a sophisticated and stable banking and financial services system.") FINANCIAL SERVICES Australia has a sophisticated and stable banking and financial services system Australia has a sophisticated and stable banking and financial services system. The banking system is prudentially

FINANCIAL SERVICES Australia has a sophisticated and stable banking and financial services system Australia has a sophisticated and stable banking and financial services system. The banking system is prudentially

Super Funds Comparison Fact Sheet

Super Funds Comparison Fact Sheet This fact sheet has been prepared for new and prospective members of. However, it is not relevant to: members who have been issued with a Part Two Information former ESI

Super Funds Comparison Fact Sheet This fact sheet has been prepared for new and prospective members of. However, it is not relevant to: members who have been issued with a Part Two Information former ESI

Making the Most of Your Super

Making the Most of Your Super For many people, super is one of the best ways to accumulate wealth. The Government provides tax benefits to encourage people to fund their own retirement. With more Australians

Making the Most of Your Super For many people, super is one of the best ways to accumulate wealth. The Government provides tax benefits to encourage people to fund their own retirement. With more Australians

AMP to acquire 19.9% of China Life Pension Company

30 October 2014 AMP to acquire 19.9% of China Life Pension Company AMP Limited, Australia and New Zealand s leading independent wealth management business, announced it has agreed to acquire a 19.99 per

30 October 2014 AMP to acquire 19.9% of China Life Pension Company AMP Limited, Australia and New Zealand s leading independent wealth management business, announced it has agreed to acquire a 19.99 per

Reinforcing the Foundations of the Individually Funded Pension System to ensure its Sustainability

Reinforcing the Foundations of the Individually Funded Pension System to ensure its Sustainability Pension Funds Investment Returns and Risk Management Graham Goodhew - Director & Conducting Officer JPMorgan

Reinforcing the Foundations of the Individually Funded Pension System to ensure its Sustainability Pension Funds Investment Returns and Risk Management Graham Goodhew - Director & Conducting Officer JPMorgan

Australian superannuation: an equitable and sustainable arrangement in a post crisis world?

The Association of Superannuation Funds of Australia Limited ABN 29 002 786 290 ASFA Secretariat PO Box 1485, Sydney NSW 2001 p: 02 9264 9300 (1800 812 798 outside Sydney) f: 1300 926 484 w: www.superannuation.asn.au

The Association of Superannuation Funds of Australia Limited ABN 29 002 786 290 ASFA Secretariat PO Box 1485, Sydney NSW 2001 p: 02 9264 9300 (1800 812 798 outside Sydney) f: 1300 926 484 w: www.superannuation.asn.au

Issue Brief. Lessons for Private Sector Retirement Security from Australia, Canada, and the Netherlands

Issue Brief Lessons for Private Sector Retirement Security from Australia, Canada, and the Netherlands By John A. Turner, PhD and Nari Rhee, PhD August 2013 about the authors John A. Turner, PhD, is Director

Issue Brief Lessons for Private Sector Retirement Security from Australia, Canada, and the Netherlands By John A. Turner, PhD and Nari Rhee, PhD August 2013 about the authors John A. Turner, PhD, is Director

HOW TO BUY PROPERTY WITHIN YOUR SELF-MANAGED SUPERANNUATION FUND

HOW TO BUY PROPERTY WITHIN YOUR SELF-MANAGED SUPERANNUATION FUND COPYRIGHT All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or

HOW TO BUY PROPERTY WITHIN YOUR SELF-MANAGED SUPERANNUATION FUND COPYRIGHT All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or

The Aged care Review by the Productivity Commission raises a number of issues which require a response.

Submission to: Aged Care Review By Margaret Kearney Aged Care Review Cremorne 2090 NSW The Aged care Review by the Productivity Commission raises a number of issues which require a response. The following

Submission to: Aged Care Review By Margaret Kearney Aged Care Review Cremorne 2090 NSW The Aged care Review by the Productivity Commission raises a number of issues which require a response. The following

The Four Pillars and Public Policy Prudential s positions on legislative and regulatory issues impacting retirement security in America

Prudential Financial The Four Pillars and Public Policy Prudential s positions on legislative and regulatory issues impacting retirement security in America Public policy affects many aspects of our everyday

Prudential Financial The Four Pillars and Public Policy Prudential s positions on legislative and regulatory issues impacting retirement security in America Public policy affects many aspects of our everyday

Tax discussion paper submission. May 2015 The Association of Superannuation Funds of Australia (ASFA)

") Tax discussion paper submission May 2015 The Association of Superannuation Funds of Australia (ASFA) Contents Executive summary 3 Key findings 6 Recommendations 7 Objectives of superannuation 8 - Primary

Tax discussion paper submission May 2015 The Association of Superannuation Funds of Australia (ASFA) Contents Executive summary 3 Key findings 6 Recommendations 7 Objectives of superannuation 8 - Primary

Live Long and Prosper? Demographic Change and Europe s Pensions Crisis

10 November 2015, Brussels Live Long and Prosper? Demographic Change and Europe s Pensions Crisis Key Note Speech Dr. Jochen Pimpertz Head of Research Unit Public Finance, Social Security, Income and Wealth

10 November 2015, Brussels Live Long and Prosper? Demographic Change and Europe s Pensions Crisis Key Note Speech Dr. Jochen Pimpertz Head of Research Unit Public Finance, Social Security, Income and Wealth

Pension schemes are integral parts of China s social protection system

Dewen Wang World Bank March 26-27, 2014, Incheon, Republic of Korea Pension schemes are integral parts of China s social protection system SP programs Social Insurance Social Assistance Social Welfare

Dewen Wang World Bank March 26-27, 2014, Incheon, Republic of Korea Pension schemes are integral parts of China s social protection system SP programs Social Insurance Social Assistance Social Welfare

FEDERAL BUDGET 2009 SUMMARY

FEDERAL BUDGET 2009 SUMMARY 13 May 2009 As widely expected, last nightʼs Federal Budget contained a number of proposals that will affect clients. Importantly, the proposals will require passage of legislation

FEDERAL BUDGET 2009 SUMMARY 13 May 2009 As widely expected, last nightʼs Federal Budget contained a number of proposals that will affect clients. Importantly, the proposals will require passage of legislation

Retirement Saving in Australia

Garry Barrett UNSW Yi-Ping Tseng University of Melbourne November 2006 Overview Outline of Presentation 1 Introduction 2 Social Security in Australia 3 Voluntary private retirement saving 4 Mandated private

Garry Barrett UNSW Yi-Ping Tseng University of Melbourne November 2006 Overview Outline of Presentation 1 Introduction 2 Social Security in Australia 3 Voluntary private retirement saving 4 Mandated private

Sustainable & Responsible Investment Policy

Sustainable & Responsible Investment Policy Local Government Superannuation Scheme Effective date: 1/05/2015 Purpose of policy The Local Government Superannuation Scheme (LGS) is established under a multi-division

Sustainable & Responsible Investment Policy Local Government Superannuation Scheme Effective date: 1/05/2015 Purpose of policy The Local Government Superannuation Scheme (LGS) is established under a multi-division

Australia. Qualifying conditions. Benefit calculation. Defined contribution. Key indicators: Australia. Australia: Pension system in 2014

11. PENSIONS AT A GLANCE 215: COUNTRY PROFILES AUSTRALIA Australia Australia: Pension system in 214 Australia s retirement income system has three components: a means-tested Age Pension funded through

11. PENSIONS AT A GLANCE 215: COUNTRY PROFILES AUSTRALIA Australia Australia: Pension system in 214 Australia s retirement income system has three components: a means-tested Age Pension funded through

SUPERANNUATION SUPERANNUATION AN OVERVIEW. Paper 026-001 CONTENTS

SUPERANNUATION SUPERANNUATION AN OVERVIEW CONTENTS Page 1. What Is Superannuation?... 2 2. A History Of Superannuation In Australia... 2 3. Why Implement The Superannuation Guarantee Scheme?... 2 4. How

SUPERANNUATION SUPERANNUATION AN OVERVIEW CONTENTS Page 1. What Is Superannuation?... 2 2. A History Of Superannuation In Australia... 2 3. Why Implement The Superannuation Guarantee Scheme?... 2 4. How

Contributing the Family Home to Super

Contributing the Family Home to Super An innovative proposal designed to assist with the accommodation and income needs of older Australians wishing to remain in their own homes. Abstract There has been

Contributing the Family Home to Super An innovative proposal designed to assist with the accommodation and income needs of older Australians wishing to remain in their own homes. Abstract There has been

1 JULY 2015. Investment Guide INDUSTRY, CORPORATE AND PERSONAL DIVISIONS

1 JULY 2015 Investment Guide INDUSTRY, CORPORATE AND PERSONAL DIVISIONS Your investment choice TWUSUPER was established in 1984 as the Industry SuperFund for people in transport and logistics. By understanding

1 JULY 2015 Investment Guide INDUSTRY, CORPORATE AND PERSONAL DIVISIONS Your investment choice TWUSUPER was established in 1984 as the Industry SuperFund for people in transport and logistics. By understanding

A Guide to Investing in Property Using a Self Managed Super Fund

A Guide to Investing in Property Using a Self Managed Super Fund Why would I consider a SMSF? I already have a super fund. Self Managed Superannuation Funds (SMSF s) are the fastest growing sector of the

A Guide to Investing in Property Using a Self Managed Super Fund Why would I consider a SMSF? I already have a super fund. Self Managed Superannuation Funds (SMSF s) are the fastest growing sector of the

July 2011. IAS 19 - Employee Benefits A closer look at the amendments made by IAS 19R

July 2011 IAS 19 - Employee Benefits A closer look at the amendments made by IAS 19R 2 Contents 1. Introduction 3 2. Executive summary 4 3. General changes made by IAS 19R 6 4. Changes in IAS 19R with

July 2011 IAS 19 - Employee Benefits A closer look at the amendments made by IAS 19R 2 Contents 1. Introduction 3 2. Executive summary 4 3. General changes made by IAS 19R 6 4. Changes in IAS 19R with

Retirement in the 21 st Century- Can you afford it?

Retirement in the 21 st Century- Can you afford it? Dr Peter Winwood Professors Helen and Tony Winefield University of South Australia School of Psychology, Social work and social policy Retirement & Pensions:

Retirement in the 21 st Century- Can you afford it? Dr Peter Winwood Professors Helen and Tony Winefield University of South Australia School of Psychology, Social work and social policy Retirement & Pensions:

The Paradox of Plenty: The Implications of Choice Overload in Retirement Savings?

The Paradox of Plenty: The Implications of Choice Overload in Retirement Savings? Associate Professor Hazel Bateman Centre for Pensions and Superannuation UNSW, Sydney Outline Choice in retirement savings

The Paradox of Plenty: The Implications of Choice Overload in Retirement Savings? Associate Professor Hazel Bateman Centre for Pensions and Superannuation UNSW, Sydney Outline Choice in retirement savings

Financial performance of Australia's superannuation products. Financial Services Council

Financial performance of Australia's superannuation products Financial Services Council August 2014 Contents Executive Summary... i 1 Background... 3 1.1 Characteristics of pension schemes... 3 1.2 Factors

Financial performance of Australia's superannuation products Financial Services Council August 2014 Contents Executive Summary... i 1 Background... 3 1.1 Characteristics of pension schemes... 3 1.2 Factors

An update on the level and distribution of retirement savings

ASFA Research and Resource Centre An update on the level and distribution of retirement savings Ross Clare Director of Research March 2014 The Association of Superannuation Funds of Australia Limited (ASFA)

ASFA Research and Resource Centre An update on the level and distribution of retirement savings Ross Clare Director of Research March 2014 The Association of Superannuation Funds of Australia Limited (ASFA)

New tendencies in the European Pension Fund systems

New tendencies in the European Pension Fund systems Portfolio optimization through low volatility stocks Laurens Swinkels, PhD Robeco Quantitative Strategies Erasmus University Rotterdam Robeco Employees

New tendencies in the European Pension Fund systems Portfolio optimization through low volatility stocks Laurens Swinkels, PhD Robeco Quantitative Strategies Erasmus University Rotterdam Robeco Employees

Home Ownership and Superannuation White Paper

Home Ownership and Superannuation White Paper This paper contains general advice about our superannuation products and has been prepared without taking account of your objectives, financial situation or

Home Ownership and Superannuation White Paper This paper contains general advice about our superannuation products and has been prepared without taking account of your objectives, financial situation or

Investment options and risk

Investment options and risk Issued 1 November 2013 The information in this document forms part of the Product Disclosure Statement for the Commonwealth Superannuation Scheme (CSS), sixth edition, issued

Investment options and risk Issued 1 November 2013 The information in this document forms part of the Product Disclosure Statement for the Commonwealth Superannuation Scheme (CSS), sixth edition, issued

Super Funds Comparison Worksheet

Super Funds Comparison Worksheet This worksheet has been prepared for new and prospective Defined Contribution members of. However, it is NOT relevant to Income Stream, Market Linked Pension or Defined

Super Funds Comparison Worksheet This worksheet has been prepared for new and prospective Defined Contribution members of. However, it is NOT relevant to Income Stream, Market Linked Pension or Defined

Global Retirement Indexes Illustrate Widespread Employee Benefit System Challenges

BP 2015-2 March 6, 2015 The American Benefits Institute is the education and research affiliate of the American Benefits Council. The Institute conducts research on both domestic and international employee

BP 2015-2 March 6, 2015 The American Benefits Institute is the education and research affiliate of the American Benefits Council. The Institute conducts research on both domestic and international employee

The Benefits of Simplified Superannuation Reform

The Benefits of Simplified Superannuation Reform Prafula Fernandez School of Business Law Curtin University of Technology Abstract This paper considers the recent Superannuation tax reforms in the Tax

The Benefits of Simplified Superannuation Reform Prafula Fernandez School of Business Law Curtin University of Technology Abstract This paper considers the recent Superannuation tax reforms in the Tax

PENSION INSURANCE IN REPUBLIC OF CROATIA 2008, progress and improvements

PENSION INSURANCE IN REPUBLIC OF CROATIA 2008, progress and improvements Snježana Baloković Ministry of Economy, Labour and Entrepreneurship JIM Conference, Zagreb, 31 March 2009 1 PENSION REFORM Started

PENSION INSURANCE IN REPUBLIC OF CROATIA 2008, progress and improvements Snježana Baloković Ministry of Economy, Labour and Entrepreneurship JIM Conference, Zagreb, 31 March 2009 1 PENSION REFORM Started

Australia s lost superannuation (retirement saving) accounts*

accounts*") Australia s lost superannuation (retirement saving) accounts* August 2008 Associate Professor Hazel Bateman Director, Centre for Pensions and Superannuation The University of New South Wales Sydney, Australia

Australia s lost superannuation (retirement saving) accounts* August 2008 Associate Professor Hazel Bateman Director, Centre for Pensions and Superannuation The University of New South Wales Sydney, Australia

SPEECH Address to the SMSF Association Melbourne 20 February 2015

The Hon Josh Frydenberg MP Federal Member for Kooyong Assistant Treasurer SPEECH Address to the SMSF Association Melbourne 20 February 2015 E&OE. Thank you Andrea for that kind introduction, and to Peter

The Hon Josh Frydenberg MP Federal Member for Kooyong Assistant Treasurer SPEECH Address to the SMSF Association Melbourne 20 February 2015 E&OE. Thank you Andrea for that kind introduction, and to Peter

Your guide to a total solution Ascend self managed super

Your guide to a total solution Ascend self managed super The big picture ISSUE 2 - SEPTEMBER 2009 Components of an SMSF If one member only If 2 to 4 members What is a self managed super fund? Member trustee

Your guide to a total solution Ascend self managed super The big picture ISSUE 2 - SEPTEMBER 2009 Components of an SMSF If one member only If 2 to 4 members What is a self managed super fund? Member trustee

Contact us. Hoa Bui T: + 61 (02) 9335 8938 E: hbui@kpmg.com.au. Briallen Cummings T: + 61 (02) 9335 7940 E: bcummings01@kpmg.com.au. www.kpmg.com.

9335 8938 E: hbui@kpmg.com.au. Briallen Cummings T: + 61 (02) 9335 7940 E: bcummings01@kpmg.com.au. www.kpmg.com.") Contact us Hoa Bui T: + 61 (02) 9335 8938 E: hbui@kpmg.com.au Briallen Cummings T: + 61 (02) 9335 7940 E: bcummings01@kpmg.com.au www.kpmg.com.au No reliance This report should not be regarded as suitable

Contact us Hoa Bui T: + 61 (02) 9335 8938 E: hbui@kpmg.com.au Briallen Cummings T: + 61 (02) 9335 7940 E: bcummings01@kpmg.com.au www.kpmg.com.au No reliance This report should not be regarded as suitable

SALARY PACKAGING SUPERANNUATION GUIDE TO EMPLOYEES

SALARY PACKAGING SUPERANNUATION GUIDE TO EMPLOYEES Superannuation Introducing Salary Packaging Salary packaging has been made available to all staff of the University through the Enterprise Agreement process.

SALARY PACKAGING SUPERANNUATION GUIDE TO EMPLOYEES Superannuation Introducing Salary Packaging Salary packaging has been made available to all staff of the University through the Enterprise Agreement process.

Understanding insurance

Version 4.2 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to. Important information This document has been published

Version 4.2 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to. Important information This document has been published

RICE WARNER VALUE OF DIFFERENT MODELS OF FINANCIAL ADVICE

RICE WARNER VALUE OF DIFFERENT MODELS OF FINANCIAL ADVICE Fee for service (time based/hourly rate) financial advice, such as that provided by Industry Fund Financial Planning (IFFP), delivers up to 6 times

RICE WARNER VALUE OF DIFFERENT MODELS OF FINANCIAL ADVICE Fee for service (time based/hourly rate) financial advice, such as that provided by Industry Fund Financial Planning (IFFP), delivers up to 6 times

Ceridian Futures Retirement Plan

Ceridian Futures Retirement Plan Summary of Benefits Summary of Benefits Ceridian Futures Retirement Plan 1 Summary of Benefits Introduction Who is eligible? How the Plan works Contributions The Ceridian

Ceridian Futures Retirement Plan Summary of Benefits Summary of Benefits Ceridian Futures Retirement Plan 1 Summary of Benefits Introduction Who is eligible? How the Plan works Contributions The Ceridian

THE HON JOSH FRYDENBERG MP Assistant Treasurer SPEECH FINANCIAL SERVICES COUNCIL BT FINANCIAL GROUP BREAKFAST SYDNEY 15 APRIL 2015

THE HON JOSH FRYDENBERG MP Assistant Treasurer SPEECH FINANCIAL SERVICES COUNCIL BT FINANCIAL GROUP BREAKFAST SYDNEY 15 APRIL 2015 **CHECK AGAINST DELIVERY** Introductory remarks Good morning. Thank you

THE HON JOSH FRYDENBERG MP Assistant Treasurer SPEECH FINANCIAL SERVICES COUNCIL BT FINANCIAL GROUP BREAKFAST SYDNEY 15 APRIL 2015 **CHECK AGAINST DELIVERY** Introductory remarks Good morning. Thank you

American Bankers Association. Sample Glossary of Collective Investment Fund Terms for Disclosures to Retirement Plan Participants

American Bankers Association Sample Glossary of Collective Investment Fund Terms for Disclosures to Retirement Plan Participants January 5, 2012 2 PART 1 Frequently Asked Questions (FAQs) About Collective

American Bankers Association Sample Glossary of Collective Investment Fund Terms for Disclosures to Retirement Plan Participants January 5, 2012 2 PART 1 Frequently Asked Questions (FAQs) About Collective

Public Consultation Package

Public Consultation Package Request for Comments Retirement Income Adequacy in Canada Yukon Finance March 2010 Whitehorse, Yukon March 2010 Message from the Premier and Minister of Finance The Yukon Government

Public Consultation Package Request for Comments Retirement Income Adequacy in Canada Yukon Finance March 2010 Whitehorse, Yukon March 2010 Message from the Premier and Minister of Finance The Yukon Government

GBK lkahair - Australia

- GBK lkahair - Australia Executive Summary This paper outlines the major changes which have occurred in the past 3 years to the regulatory environment governing superannuation funds in Australia, and

- GBK lkahair - Australia Executive Summary This paper outlines the major changes which have occurred in the past 3 years to the regulatory environment governing superannuation funds in Australia, and

Structuring & Tax. Ensuring your plans for your super become a reality. By Ben Andreou Partner Head of Structuring & Tax

Structuring & Tax Ensuring your plans for your super become a reality By Ben Andreou Partner Head of Structuring & Tax December 2015 Table of Contents Page Why should you read this paper?... 3 Background...

Structuring & Tax Ensuring your plans for your super become a reality By Ben Andreou Partner Head of Structuring & Tax December 2015 Table of Contents Page Why should you read this paper?... 3 Background...

GSK Pension Scheme ( the Scheme ) Statement of Investment Principles

Statement of Investment Principles") GSK Pension Scheme ( the Scheme ) Statement of Investment Principles This Statement of Investment Principles (SIP) covers the defined benefit and the defined contribution sections of the Scheme. It is

GSK Pension Scheme ( the Scheme ) Statement of Investment Principles This Statement of Investment Principles (SIP) covers the defined benefit and the defined contribution sections of the Scheme. It is

Understanding Superannuation

Understanding Superannuation Client Fact Sheet July 2012 Superannuation is an investment vehicle designed to assist Australians save for retirement. The Federal Government encourages saving through superannuation

Understanding Superannuation Client Fact Sheet July 2012 Superannuation is an investment vehicle designed to assist Australians save for retirement. The Federal Government encourages saving through superannuation

Superannuation requirements are different for New Zealand and Australia.

SUPERANNUATION Superannuation requirements are different for New Zealand and Australia. New Zealand see: http://www.ird.govt.nz/kiwisaver Australia see: http://www.ato.gov.au/superfunds P A Y T Y P E S

SUPERANNUATION Superannuation requirements are different for New Zealand and Australia. New Zealand see: http://www.ird.govt.nz/kiwisaver Australia see: http://www.ato.gov.au/superfunds P A Y T Y P E S

Review into the governance, efficiency, structure and operation of Australia s superannuation system: Phase one governance

19 October 2009 Mr Jeremy Cooper Chairman Super System Review GPO Box 9827 MELBOURNE VIC 3001 By email: info@supersystemreview.gov.au Dear Chairman and Commissioners Review into the governance, efficiency,

19 October 2009 Mr Jeremy Cooper Chairman Super System Review GPO Box 9827 MELBOURNE VIC 3001 By email: info@supersystemreview.gov.au Dear Chairman and Commissioners Review into the governance, efficiency,

Super Funds Comparison Worksheet

Super Funds Comparison Worksheet This worksheet has been prepared for new and prospective Defined Contribution members of. However, it is NOT relevant to Income Stream, Market Linked Pension or Defined

Super Funds Comparison Worksheet This worksheet has been prepared for new and prospective Defined Contribution members of. However, it is NOT relevant to Income Stream, Market Linked Pension or Defined

Super Spouse Accounts - A member Perspective

Current Issues in Superannuation A member perspective This presentation has been prepared without taking into account any of your objectives, financial situation or needs. You must therefore assess whether

Current Issues in Superannuation A member perspective This presentation has been prepared without taking into account any of your objectives, financial situation or needs. You must therefore assess whether

Pension Systems for Public Sector Employees in the Republic of Korea

International Workshop on Civil Service and Military Pension Arrangements in Selected Countries of the Asia-Pacific, Tokyo, Japan, 20-21 January 2011. Pension Systems for Public Sector Employees in the

International Workshop on Civil Service and Military Pension Arrangements in Selected Countries of the Asia-Pacific, Tokyo, Japan, 20-21 January 2011. Pension Systems for Public Sector Employees in the

Superannuation adequacy with voluntary contributions: a comparison of living standards

Superannuation adequacy with voluntary contributions: a comparison of living standards Marcia Keegan, Gabriela D Souza and Rebecca Cassells National Centre for Social and Economic Modelling, University

Superannuation adequacy with voluntary contributions: a comparison of living standards Marcia Keegan, Gabriela D Souza and Rebecca Cassells National Centre for Social and Economic Modelling, University

Health & the economic crisis: the Australian case

Health & the economic crisis: the Australian case Country: Australia Partner Institute: Centre for Health, Economics Research and Evaluation (CHERE), University of Technology, Sydney Survey no: (14) 2009

Health & the economic crisis: the Australian case Country: Australia Partner Institute: Centre for Health, Economics Research and Evaluation (CHERE), University of Technology, Sydney Survey no: (14) 2009