Dear Forum participants, The vision of a target gas pricing model for Europe that I will present today differs from conventional wisdom.

|

|

|

- Dominick Lester

- 8 years ago

- Views:

Transcription

1 1

2 Dear Forum participants, The vision of a target gas pricing model for Europe that I will present today differs from conventional wisdom. The conventional or mainstream belief is that oilindexation in European gas contracts is outdated and will inevitably and fairly soon be replaced by a pricing model based on supply and demand. I will offer you a different perspective that I believe will be of interest to you. If the statement had been made three years ago that the derivatives on U.S. mortgages rated AAA were in actuality pure junk, it would not have been taken as credible. But those who thought that way were proved to be right. The whole world paid an extremely high price for its blind belief in unbounded market liberalization and the invisible hand that allegedly sets everything right. Now it is clear that there are cases when markets cannot perform their balancing functions properly. This is the case in the gas industry. Our research shows that the rationale for the traditional Dutch oil-indexation pricing formula still holds. By way of comparison with gas indexation, I will demonstrate that oil-indexation or, in other words indexation via a third commodity, remains the best pricing mechanism and should therefore retain its dominant role in European contracts. I also need to note that oil indexation is a purely market-based mechanism of price setting. It is true that there are no perfect markets. Perfect markets exist only in textbooks. But in many commodity markets, these real life imperfections could be neglected because they are within acceptable limits. This is not the case for natural gas. In the fully liberalized gas markets of the U.S. and UK, these distortions have acquired a systemic nature and are only getting worse. The outcome of these 2

3 distortions is the lasting inability of price mechanisms based on supply and demand to provide sustainable price signals that support investment in the industry. Continental Europe has developed a unique hybrid pricing system based on the coexistence of oil-indexed contracts and gas-indexed hub prices. Under the existing model, oil-indexed prices play a leading and dominant role, while hub prices play a balancing and subordinate role. Changes in the pricing model that have been proposed for Continental Europe will bring the existing hybrid system to a collapse. These changes will inevitably lead to a termination of the long-term gas supply contracts as these contracts will not be able to protect the investment programs of the exporters. Long-term contracts are a cornerstone of the energy security of the import-dependent Europe and oil-indexation is a hedge against price manipulation by the dominant suppliers. In that sense, the call for absolute use of gas indexation is a recipe for disaster for the European gas industry, an industry that is still comprised of two inseparable parts upstream and downstream. 2

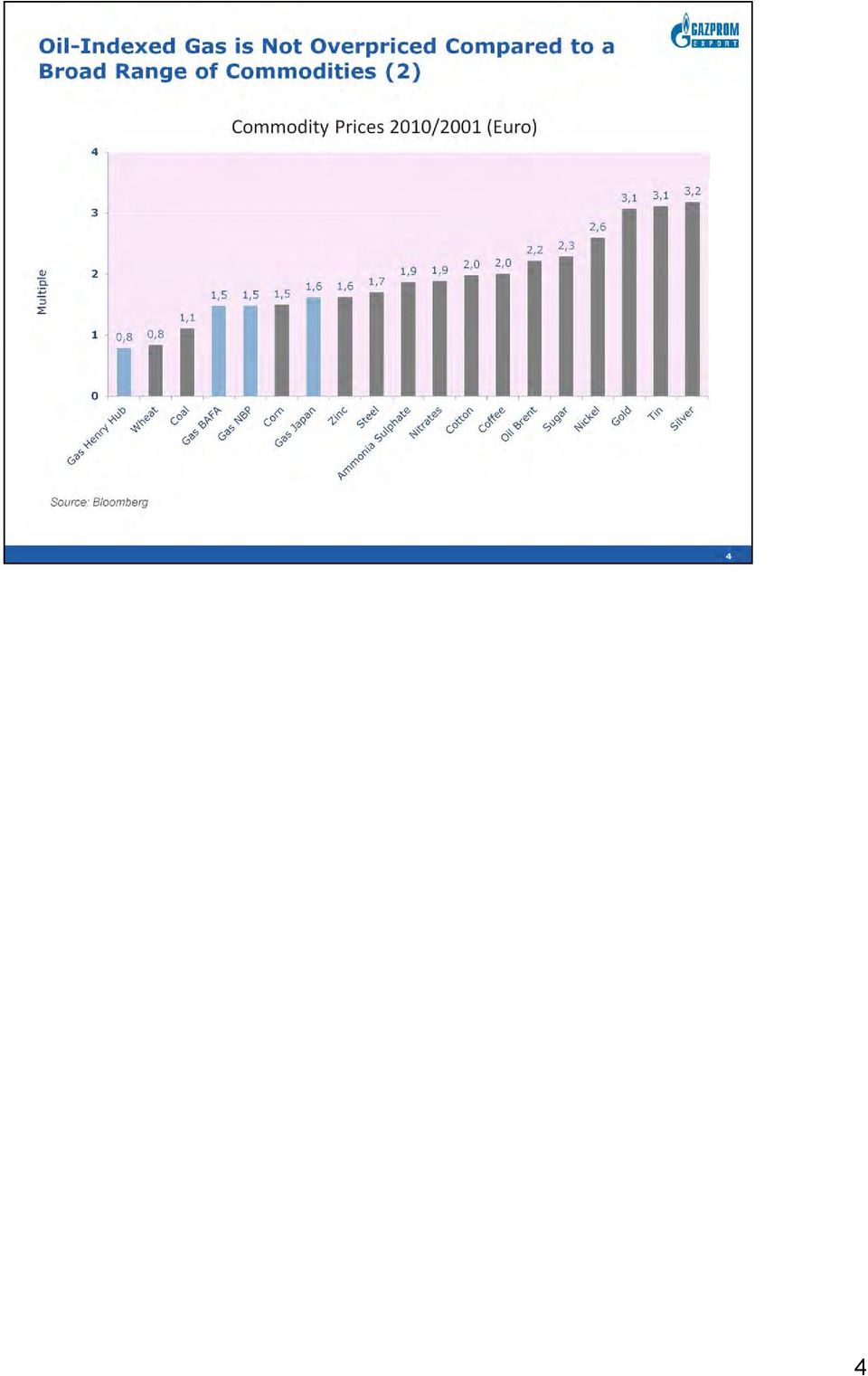

4 Let me begin with a critical evaluation of a popular statement that oil indexation leads to the overpricing of natural gas. Anecdotal evidence does not support this statement. Over the last 10 years, despite their conflicting fundamentals, a broad range of exchange-traded commodities including metals, agricultural and chemical products has grown by 2.5 times in US dollar terms (or about 1.5 times in Euro terms). That is within the same range as the oil-pegged gas price, as shown in the charts on slides 3-4. Is the doubling or nearly tripling of the natural gas oil-indexed price considered fair? There are reasons to believe so. When your own product s pricing dynamics match with those of other raw commodities, it gives you hope that you will be able to launch a new investment cycle without trouble. 3

5 4

6 When measured in calorific terms, oil-indexed gas prices have grown in the same range as energy commodities such as coal and electricity. Let me point your attention to the fact that in the past 10 years oil-indexed prices in Japan and Germany (as represented by the BAFA index) have grown at a rate that is significantly below the 4.4 times multiple seen for oil prices over this period. This is the result of the broad use of the S-curve, caps and lowering coefficients in gas contracts. Since the early 2000s, the Henry Hub gas price has lost 10 percent of its value, while the NBP price has strengthened by only 60 percent in US dollar terms. For comparison purposes, I should mention that 60 percent price growth is on par with the growth seen in The Economist s Big Mac index over the same time period. The major takeaway from these charts is that the oil-indexed gas price is not expensive. Its price growth over the past 10 years is decent compared to the growth of a broad range of exchange-traded commodities. That conclusion is valid because in the early 2000s, there was no concern that the oilindexed price was overblown. 5

7 6

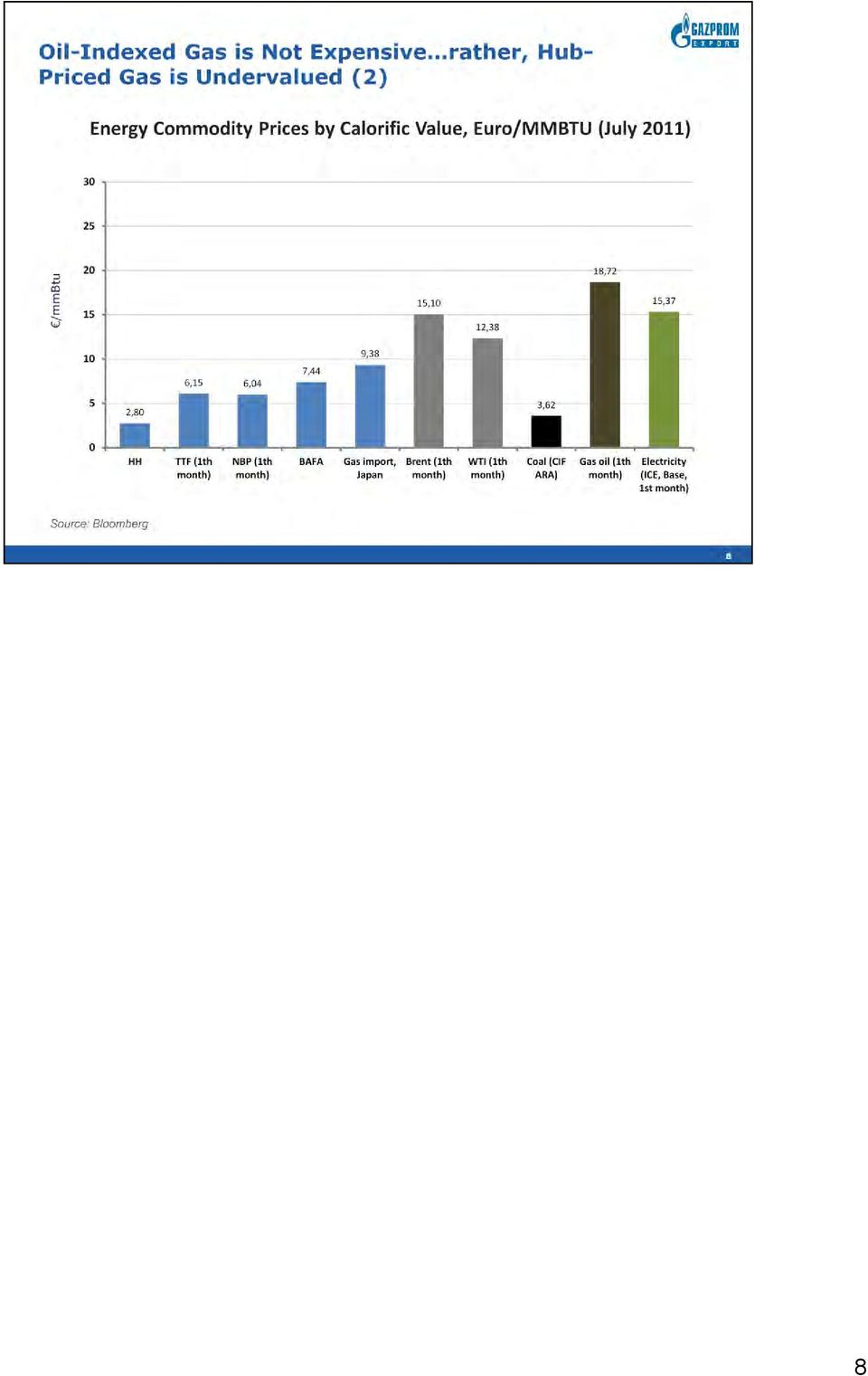

8 What is obvious is that gas-indexed gas is underpriced. Measured by calorific value, the Henry Hub gas price equals only 20 percent of the oil equivalent price, and the NBP price equals only 40 percent of the oil equivalent price. There is no rationale for such a huge discount. Gas has truly come of age and is no longer a little brother of oil. But when it comes to pricing in liberalized markets, it has become an even littler brother of oil. 7

9 8

10 Discounted gas prices put long-term investments in the industry at risk because producers must buy commodities necessary for major investments at the inflated price. The post-crisis behavior of major commodity indexes irrespective of the fundamentals of their own markets shows that these commodities have fully returned to their pre-crisis price levels. But the Henry Hub price is a classic example that a supply and demand pricing mode for natural gas leads to abnormal behavior. 9

11 Only oil-indexed pricing brings gas prices in line with the behavior of other exchange-traded commodities. Producers have good reason to question the quality of price signals that the mature, liberalized markets of the U.S. and UK provide. Hubs in these markets leave an impression that they are designed to hold back gas prices. Hubs in Continental Europe leave the same impression. Does this mean that gas markets cannot function on their own without utilizing a pricing structure based on indexation to a third commodity? Are these failures temporary or are they systemic in nature? Let me make one observation. It is frustrating that producers seem to be the only party interested in finding the right answer to this question. 10

12 In a new Golden Age for Gas Scenario, the International Energy Agency sees global demand rise to 5.1 trillion cubic meters in trillion cubic meters more than today. Obviously, such growth will require huge increases in investments that will need to be made many years in advance of when supply is needed. CERA s recent update of its Upstream Capital Cost Index indicates that cost of gas production has already recovered globally. Henry Hub prices have not. Will lenders give money to gas projects that do not have linkage to oil? Let me repeat it once again. It is frustrating that producers seem to be the only party interested in finding the answer to this question. 11

13 To get an explanation as to why spot prices are depressed and lagging behind the growth of other commodities, we will focus first on developments in the liberalized markets of the U.S. and UK and then tackle Continental Europe. We cannot accept the argument that the abnormal behavior of hub prices is a result of the financial crisis. Other commodities were hit by the crisis but their prices behaved differently. Demand for gas in the U.S. and UK has already topped pre-crisis levels. We think that the abnormal pricing behavior of hub gas prices is due to a factor that emerged in and which has produced strong downward pressure on these prices. This factor is related to the financialization of commodity markets and the emergence of a special breed of financial investors. These investors consider commodities as a safe haven at a time when the major paper currencies are losing their value. A decade ago, commodity markets were a relatively quiet backwater of the global financial markets, where the main participants were almost exclusively producers and consumers who were involved in a routine process of hedging their operational risks. According to Barclays Capital, the combined value of commodity index swaps, exchange-traded commodity products and commodity medium-term notes was just $6 billion at the turn of the millennium in December This picture changed as financial investors seeking hedges against inflation rushed into the market with hundreds of billions of dollars. In the second quarter of 2008, these assets surged to $270 billion. Financial investors are responsible for a commodities bubble that popped in August Although commodity investors reduced their appetite in the face of the global crisis, this appetite subsequently returned with volumes reaching a new peak of $350 billion in the fourth Quarter of 2010 after the announcement of the QE2 program, a second round of quantitative easing, by the U.S. Federal Reserve. Trading in commodities by financial investors is a force that gives its own momentum to pricing structures. Commodity prices are determined not only by fundamentals but by the investments of market participants who are not directly connected with the goods in which they trade. The choice of a commodity as a financial paper asset does not increase its physical demand but does increase its price. The financialization of the energy market would not create any problems if the funds were spread more or less evenly across a broadening spectrum of commodities. However, this has not been, and is not currently, the case. There were darlings of the financial investors as well as Cinderellas. 12

14 Natural gas is treated as the Cinderella of financial markets. Although natural gas exports are only four times lower in US dollar value terms than sales of crude oil, financial markets have disregarded natural gas as an attractive hedging instrument for inflation risk mitigation. Due to this weak interest from financial investors, the gas price is supported largely by the fundamentals of its own market. This support is not sufficient enough to give the hub gas prices momentum comparable to that of the other commodities. There is a reason that natural gas futures have not taken off as an inflation hedge. Commodities chosen as a hedge against inflation must feature a standardized spot price structure in global markets. Natural gas does not fit this description, with its varying degrees of price seasonality in different locations, diverse pricing structures and expensive storage. Natural gas also tends to represent more localized markets as the vast majority of gas is still transported by pipeline. The continued emergence of mobile LNG in transport applications has led to greater correlation between markets but not to the extent that would enable gas to catch up with the broader commodity price trend. There are strong doubts that financial markets will ever appreciate natural gas as an instrument for inflation hedging. It may not happen in the future as commodity investment is becoming more physical amid paper commodity market regulations. Gas will hardly become the darling of exchange-traded physical funds under these circumstances. Storage and insurance costs for gas are much higher than for oil and metals. Commodities are financial instruments that bear no interest profit but at the times of currency wars they are natural, real world hedges against inflation. Additional asset value of this asset class comes from the appreciation of the commodity due to its fundamentals. Predictions of the endless gas glut are not supportive to positioning of gas as a financial markets darling. There is a lot of controversy as to the timing of the glut between the producers and the consumers of gas with many producers claiming that it is already over. The glut in global currencies has led directly to the commodity price boom. Gas, unless it is oilindexed, has not taken and most likely will not take any advantage of this boom. The premise that gas prices should be dictated by spot markets does not give any reassurance to gas producers. 13

15 There are additional depressing factors in addition to the Cinderella factor that affect hubpriced gas prices. In the UK, associated gas deliveries by major natural gas supplier Norway play a secondary or auxiliary role compared to its oil deliveries. Portfolio optimization on the part of Norwegian suppliers to the UK in many instances jeopardizes the value of gas in favor of oil. Cases when prices of gas were negative on NBP are a good example of this depressive factor. The key depressing factor in U.S. markets is shale gas production. Low hub prices are not a result of low shale gas production costs, as is often perceived. In fact, our analysis shows that the all-in costs of major shale gas producers are $2.00/MMBTU higher than the Henry Hub price. Hedging gains in 2008, 2009 and first half of 2010 allowed shale gas companies to continue to drill. Thus, the U.S. shale gas miracle is in fact paid for with the money of the ill-fated financial investors who hold these hedges. Another market distortion that allows shale companies to keep on producing at a time when costs exceed revenues comes from the equity market. The true motive of international oil majors is to book reserves on their balance sheets. Purchasing financially distressed shale companies can make a significant addition to these reserve bookings in an environment where companies are finding it increasingly difficult to book reserves internationally. ExxonMobil s acquisition of XTO Energy last year accounted for 80 percent of the reserves it added in 2010, highlighting the difficulty oil companies are having in finding new sources of crude. ExxonMobil s reserve base increased by 3.5 billion to 24.8 billion oil-equivalent barrels at the end of last year. XTO, a U.S. shale gas producer, accounted for 2.8 billion barrels of these new reserves. 14

16 As a result of the developments described above, U.S. Henry Hub prices are currently depressed and headed nowhere. If the business model of gas exporters was based on hedging like that of shale producers, they would theoretically be able to keep on selling their gas in the U.S. at any price, be it $1.00 or $ 2.00/MMBTU. When you ask producers to switch to spot pricing you are in fact selling us a clock that nearly always shows the wrong time. Let me remind you of the fact that the necessity of pricing natural gas via a third commodity stems from the fact that the market for natural gas is not perfect enough to function properly and produce quality price signals. This was certainly the case in the early years of the gas industry when gas production required enormous investments and market mechanisms were in their infancy and therefore not in a position to guarantee security of supply and demand. As the gas industry has matured, it seems to have become conventional wisdom that the rationale for oil indexation in Europe no longer holds and that the move to spot prices is a fait accompli. Allow me to take this opportunity to argue that the rationale for oil-indexation does indeed still hold, more than ever before, and that it is now no longer the issue of market immaturity but rather a case of the overmaturity of commodity markets that can no longer be ignored. The effects of financialization on pricing in energy markets should be thoroughly analyzed so that their impacts are sufficiently understood. It is frustrating that producers seem to be the only parties showing interest in analyzing these effects. 15

17 Now let us turn from the mature liberalized markets in the U.S. and UK to markets in Continental Europe that have chosen a liberalization path but are still immature judging by their churn ratio. What I will demonstrate in that part of my presentation is that the Continental market has its own unique organization and is mature enough to perform the functions that it is designed for. In contrast to North America, natural gas pricing at Continental European hubs does not provide a true indication of the supply-demand balance because the Continental European market comprises a complicated structure of long-term and short-term contracts. Therefore, Continental hub pricing is not a function of total supply and demand but a function of something quite different arbitrage of all kinds, between different contract pricing structures, between contract and spot prices, between hubs, between UK and the Continent. In fact, the market in Continental Europe is a platform for arbitrage of all kinds. I ask you to pay special attention to slide 16. The Oxford Institute of Energy Studies will not show you anything of this kind. One important conclusion from this chart is that our clients are not interested in preserving the value of the commodity they are selling. Low spot prices increase revenues from arbitrage and are only limited by take-orpay obligations. 16

18 In contrast to the U.S. Henry Hub, where primary sales account for the bulk of physical trades, European hubs generally play the role of market balancer, and during the most recent crisis served as markets of mistakes in demand assessment rather than as full-fledged price originators. According to our estimates, less than a third of all physical trades in Continental Europe were comprised of direct sales of gas. The remaining amount was comprised of secondary or tertiary volumes sold back and forth. A major contributor to direct sales on Continental hubs is GasTerra. This Dutch company sells half of its domestic output on TTF as it is envisaged by the government decree.

19 The specific character of natural gas price signals in Europe is demonstrated by the extremely low churn ratios at Continental hubs. In order to produce sustainable price signals, the churn ratio has to be at least 15. In Europe, only the NBP meets this condition. Continental markets do not pass this test. Some analysts say that low churn ratios on the Continent are a reflection of the transition phase, and that, as hub markets mature, churn ratios will grow. I am pessimistic in this respect. It is not because of the lack of appetite on the side of European financial institutions to play with the forward curve. It is extremely hard to predict what the price on a balancing market will be in two or three years because these prices are not about supply and demand but rather about arbitrage opportunities. There are too many moving parts in the balancing market that must be taken into consideration. This mission looks impossible for a rational forecast to be made. Churn ratios on Continent hubs are low and do not look likely to increase, as shown in the chart on slide 18. The major conclusion from this chart is that we will not have one global price for gas in the foreseeable future. Prices in the USA are a function of supply and demand. Contract prices in Japan have nothing to do with gas supply and demand. Hub prices on the Continent are a function of all kinds of arbitrage. The market on the Continent is a paradise for the arbitrageurs already. In this sense, it is a mature market by now. In a similar way, it would be wrong to say that that pony is not a fully formed horse. It is simply another beast. 18

20 What we hear from our clients is that they do not care about the specific nature of the European market but believe in gas indexes because these indexes offer lower prices. It is always a wrong approach and in many cases a costly exercise to ignore realities. Let me point out that the growth in hub prices in the third quarter of 2010 came as a great surprise to nearly all market participants. It occurred at a time when the recession was not yet over and Europe was not short on gas; indeed, demand in the third quarter of 2010 was lower than in the third quarter of Expectations of a new wave of LNG, as reflected in the low futures prices seen at the end of 2009, were negatively affecting sentiment in the market, but not the real price curve. The truth of the matter is that additional volumes of Qatari gas reached the European market in the third quarter of But contrary to economic theory and common sense, these volumes have not led to a further decline in the spot price but rather to a major increase in hub prices. Put in other words, the paradox is that the more Qatari LNG comes to Europe, the more the hub-based price increases. It is clear that Continental hub prices are driven by supply and demand only to a limited extent but by arbitrage opportunities that produce unexpected effects on prices. A new development in arbitrage on Continental hubs over the crisis period is the involvement of large volumes of gas under take-or-pay obligations of the short-term contracts. 19

21 Let me make a brief detour into history. The gas year, as you all know, begins on October 1 st. In mid 2008, when new contracts were negotiated, market participants were expecting tight supplies and were demanding as much gas as possible. They were also accepting high prices. The economic crisis came as a major surprise and end-users soon realized that they did not need the amount of gas they had ordered from importers as depicted on the next slide. First-tier wholesalers or importers in their turn were not able to meet their minimum quantity requirements. But there is a fundamental difference in the execution of take-or-pay obligations in the long-term contracts that Gazprom offers its clients and the short-term, one- or two-year contracts that the clients of our clients have. Long-term contracts offer a make-up gas option (not to mention flexible take-orpay terms in some cases). The make up gas option allows customers to take quantities not needed in the current year in later years provided that prepayment is made. End-users and distribution companies in the EU have no right to make-up gas because of the shortterm nature of their contracts. (BKartA in Germany introduced limitations on contract duration beginning October 1, 2007.) End-users and distribution companies have only two options to pay fines for gas that is not taken, or to dump the gas on trading hubs, thus reducing their losses by the revenues they earn from those sales. Gas volumes under take-or-pay obligations dumped on the hubs, in our view, put enormous pressure on spot prices and was the main reason behind the divergence in spot and contract prices. This divergence was wrongly taken by many analysts as signal of a complete divergence of oil-indexed and gas-indexed prices. EU regulations shortened the duration of downstream contracts in order to enhance competition. It had an unintended consequence of depriving end-users and distribution companies of the make-up gas. If the make-up gas opportunity was available, there would be no need to dump take-or-pay gas on the hubs. No major diversion of the hub and contract prices would take place as a result.

22 Let me remind you, take-or-pay obligations exist not only between exporters and first-tier wholesalers but also between wholesalers and end-users. These obligations comprise up to 80 percent of annual contract quantities. 21

23 Let me return to the question of what made prices strong in the third quarter of 2010 prior to the cold winter, the Fukushima accident, and the turbulences in North Africa. The argument that markets anticipated these events does not look persuasive. It was reset of the arrangements under short-term contracts that caused escalation of hub prices in Europe. New short-term contracts came into force starting October 1, End-users and wholesalers tried their best to minimize their contract obligations. The conventional wisdom of the market was: Why should we buy expensive gas from Russia when we can get it cheaper on the spot market whenever we need it? But it is also true that the dumping, or forced sale, of gas at hubs has stopped. This under-contracting led to additional demand for spot gas producing a kind of greenhouse effect on prices. Gazprom s clients responded to the new market situation by increasing their offtake above the Maximum Annual Quantity. Some of them executed the make-up option. So, what are the takeaways from the analysis I ve just presented? Two and a half years of abominably low spot prices in Europe have created the illusion that gas has lost its link to oil once and forever. This is not true and could not happen simply because oil-indexed contract prices serve as the benchmark for arbitrage on the Continental market. The Continental market is adequately supplied with the long-term contracts in place. The existing contracts that Gazprom has with its European clients alone allow for a supply boost of 40 bcm, from the current 150 bcm per annum to 190 bcm. Competition on the Continental market is already tough and gas importers have other supply options available to them. If they prefer to take only 150 bcm of Russian gas, that means that there are other sources of cheaper gas that could be acquired through

24 other long-term contracts or on the hubs. Once the importers exercise their arbitrage option, spot prices settle at a discount to the contract prices adjusted for the transportation costs and the value of flexibility provided by the pipeline suppliers. That is why spot prices are usually lagging behind contract prices. Otherwise, it would be more convenient to use the existing long-term contracts arrangements for gas supply. In the few cases when spot gas is more expensive than contract gas on the Continental market, it is a result of the inadequate development of gas infrastructure at a time of strong demand for gas. The more developed this infrastructure is and the more integrated the EU domestic market is, the rarer will be instances when spot prices are higher than contracted. Gas producers cannot accept a proposal to make contract and spot prices comparable by lowering contract prices. In most cases, spot prices will respond immediately by dropping down further. That is, any further decreases of contract oil-indexed prices would result in a new cycle of spot price downward adjustment. Contract price reduction may have sense if it increases long-term contracts offtake. But this may happen only when there are other suppliers that are hesitant to deliver gas at a reduced price. 22

25 Critics of oil indexation often claim that it is outdated because there is not much demand side substitution between oil and gas nowadays. But demand side substitution has not been the case in Europe for more than 20 years. Residential users that switched once to gas from fuel oil were not keeping a fuel tank in their backyard in order to use it when gas prices become too high. Limited dayto-day substitution or even its absence does not rule out a deep rooted relationship between oil and gas. The days of oil indexation are not over for several reasons apart from its unique role in supporting long-term investments: Gas competes with oil in the residential sector. One third of houses in Germany still use oil products for heating. Gas nearly replaced oil in European power generation 20 year ago. Therefore an argument of the Oxford Institute for Energy Studies that this means there is no longer a rationale for oil indexation is invalid. Even though there is not much demand-side substitution between oil and gas in power generation in Europe, there is still more than a virtual relationship between the two fuels; Merit order puts oil products and gas in the same category of fuels used in peak or semipeak. In that sense, there is a stronger competition with oil products than with coal which is used in base load only. Oil products are a reserve fuel for many power plants and industries if gas supply fails. The oil-gas linkage will only strengthen in the future as a result of direct competition in the transportation sector due to the increasing popularity of natural gas-powered vehicles and the use of LNG as a bunker fuel. Gazprom expects that that European consumption of gas in transportation applications will grow from current 3 billion cubic meters per annum to nearly 100 billion cubic meters in There is a new rationale for oil-indexation that relying on the linkage with oil makes gas inflationindexed. And oil products in the formula perform the function of a universal deflator better than any other man-made price index, be it CPI or PPI. 23

26 The existing market structure on the Continent is at least satisfactory and offers win-win options for both buyers and sellers. But the balancing nature of the Continental market has to be taken into consideration by major players, including reformers. This market is a different beast than the U.S. market. It has to be treated in a way that allows long-term oil-indexed contracts and spot gas to complement each other. Lessons from the crisis have already been taken. Our clients do not believe in the miracle of cheap spot gas anymore. Discount price suppliers with no gas of their own that emerged at a time of financial crisis are not able to keep their promise to deliver cheap gas to their customers. Some of these suppliers have gone bankrupt already (such as TelDaFax). Introducing spot pricing is not an appropriate means of simplifying interactions between market participants on the Continent. The move to gas indexation in longterm contracts is unacceptable to gas producers. This is not only because the low churn ratios at Continental hubs raise doubts as to the quality of their price signals. Transitioning to gas-indexed contracts will not change the balancing nature of the European gas market. It doesn't matter how much lipstick you put on a pig, it still remains a pig. But gas indexation will change the balance of interests in favor of importers; it will create the opportunity for predatory pricing and devalue the entire supply portfolio of natural gas producers. Producers will be running intolerable risk of gas price erosion because there is virtually no force in Europe interested in preserving the value of natural gas. Producers in the EU (Dutch and British) are definitely not interested is selling gas below cost albeit it is lower than for suppliers from the third countries due to their high transportation and liquefaction costs. Indigenous producers have easy access to the hubs and can buy gas to meet their contract obligations when hub prices 24

27 drop too much. Production could be resumed in a swing mode when prices are higher than their costs. Pipeline producers from the third countries do not have easy access to the hubs and that puts them in a disadvantaged position. It is practically not possible for Gazprom to agree with its clients that it will meet its contract requirements with gas bought at the hubs when it is cheaper than contract gas. If the oil-linked benchmark price ceases to exist, exporters will be forced to accept prices irrespective of how low they are without any leverage to influence these prices. Unjustified demands of gas importers that producers should be fully responsible for price risks in long-term contracts change the fragile balance of interests between buyer and seller. Pushing these demands will lead to nothing else but the demolition of long term supply contracts. Indeed, if markets are liquid enough, there is no need for long term supply contracts. But a move to the American model that of hub pricing without long-term contracts and direct sales by natural gas producers is not a suitable option either. As a matter of fact, Europe is increasingly import-dependent and there are oligopolistic structures on both sides of the market that will end up opening a Pandora s Box of endless conflicts. Acrimonious, rather than cooperative, relations are not in the interests of Europeans, as they will undermine the security of supply. Anecdotal experience gives us no evidence that hub pricing is better than traditional Dutch-formula oil-indexed pricing. Transparent, easy to understand, competitive and fair, as liberal determinists say. I strongly doubt that what we get as a result of hub pricing is easy to understand and fair. Markets are not always rational and do not carry an obligation to cover production costs, some argue. But when markets are not rational for too long, it becomes time to help markets to become rational. 24

28 As I have mentioned already, the existing market structure on the Continent is satisfactory and offers win-win options for both buyers and sellers. The basic problem is how to preserve long-term contracts and enhance competition on the internal EU market. One of the major arguments in favor of hub pricing is that lower prices originating on the hubs are transferred throughout the value chain to the benefit of end users of all kinds household, commercial and industrial. Is it really the case? A snapshot of the German gas market for the beginning of April over the last three years provided by national regulator Bundesnetzagentur indicates that it was not the case in 2009 when hub prices reached their bottom. End-user prices were slightly higher in April 1, 2009 compared to April 1, Beneficiaries of lower export prices as measured by the April 2009 BAFA index were not the end users but, taken as a group, domestic wholesalers and distribution companies (stadtwerke). On April 1, 2010, industrial, commercial and household users paid less for natural gas compared to April 1, 2008 by 2, 9, and 5 percent respectively. Exporters were the main losers with an average export price decrease of 14% in April 2010 compared to April The BAFA index price as a share of end user prices suffered a major decrease from 54 percent in 2008 to 47 percent in 2010 (7 percentage points) in the average end-user price for industrial customers. Domestic wholesalers as a group showed mixed results. In absolute terms, their average sales price decreased by 1 percent for household users and by 8 percent for commercial users. But domestic wholesalers margins rose by 20 percent in average sales price to industrial users. Margins of domestic wholesalers in Germany in 2010 on average varied from 0.7 eurocents per kwh for commercial users to 1.15 cents per kwh for households, according to our estimates based on German s regulator s data. In 2010 as in 2009, major beneficiaries of competition between exporters and domestic wholesalers were distribution companies whose share of the margins increased in absolute and relative terms. Distribution companies average prices gained 18 percent in sales to households, 23 percent in sales to commercial users, and 95 percent in sales to industrial users. Snapshots of the German gas market do not support the statement that low hubs prices are transferred throughout the value chain to the benefit of end users. To conclude: the unintended consequence of competition between exporters and importers is the growing margins of distribution companies. 25

29 So far, the competition enhancement policy has only divided European gas market participants. They all got involved in a vigorous fight to preserve their historic margins. That is a positive development, that is how competition works, one may say. But competition does not work if it deprives producers and importers of reasonable margins and brings gas prices below a level that supports the investment cycle in the gas industry. Not to mention when it provides only modest benefits to end users, if any. Reformists should be careful when giving competitive advantages to one group of market participants at the expense of another. They should clearly understand that they are reforming a unique market that is in fact a balancing market. In the old system, the benefits of arbitrage manifesting themselves in lower spot prices were available to a small group of importers. Now these benefits are available to a broad group of market players that have no import contracts and bring no gas to Europe under long-term arrangements. Advantages without responsibilities for this group of players result in unfair competition. What the market reformists have to do is protect long-term contracts and importers, the holders of these contracts, from unfair rules of the game. One solution could be an introduction of a minimum wholesale price for supply tenders initiated by the distribution companies. This price must be no lower than the recent BAFA price plus reasonable costs of storage and transportation to the distribution companies. Importers with long-term contracts, all other terms being equal, would have an advantage over suppliers without imported gas at these tenders. Thank you for your attention. 26

30 27

Dear conference participants, Welcome! My name is Sergei Komlev and I am in charge of contract structuring and pricing for Gazprom Export.

1 Dear conference participants, Welcome! My name is Sergei Komlev and I am in charge of contract structuring and pricing for Gazprom Export. Accordingly, it is understandable that my focus today will be

1 Dear conference participants, Welcome! My name is Sergei Komlev and I am in charge of contract structuring and pricing for Gazprom Export. Accordingly, it is understandable that my focus today will be

The current decoupling of oil and gas prices, where prices of the two commodities move in different directions, negatively affects Gazprom s export

The current decoupling of oil and gas prices, where prices of the two commodities move in different directions, negatively affects Gazprom s export sales by driving up oil-indexed gas prices and leading

The current decoupling of oil and gas prices, where prices of the two commodities move in different directions, negatively affects Gazprom s export sales by driving up oil-indexed gas prices and leading

Gas Pricing Principles for European Gas Markets

Gas Pricing Principles for European Gas Markets A View of Gazprom Export Sergei Komlev Head of Contract Structuring and Price Formation Gazprom Export Eurasia Dialogue. Securing Security of Demand for

Gas Pricing Principles for European Gas Markets A View of Gazprom Export Sergei Komlev Head of Contract Structuring and Price Formation Gazprom Export Eurasia Dialogue. Securing Security of Demand for

Preparing for Changes in Market Design

Preparing for Changes in Market Design EMART Conference Didier Lebout, Strategy and Development Director Gazprom Marketing and Trading France Amsterdam, 21 November 2012 In this presentation GM&T Ltd:

Preparing for Changes in Market Design EMART Conference Didier Lebout, Strategy and Development Director Gazprom Marketing and Trading France Amsterdam, 21 November 2012 In this presentation GM&T Ltd:

Critics of oil indexation often claim that it is outdated because there is not much demand side substitution between oil and gas.

1 Thank you, Mr. Moderator, for an opportunity to address this high-level congress. I work as Head of pricing and contract structuring for Gazprom Export. It is not surprising that a topic of my presentation

1 Thank you, Mr. Moderator, for an opportunity to address this high-level congress. I work as Head of pricing and contract structuring for Gazprom Export. It is not surprising that a topic of my presentation

Gas Pricing Principles for European Gas Markets

Gas Pricing Principles for European Gas Markets A View of Gazprom Export Sergei Komlev Head of Contract Structuring and Price Formation Gazprom Export EU-RUSSIA ENERGY DIALOGUE Gas Advisory Council. Fifth

Gas Pricing Principles for European Gas Markets A View of Gazprom Export Sergei Komlev Head of Contract Structuring and Price Formation Gazprom Export EU-RUSSIA ENERGY DIALOGUE Gas Advisory Council. Fifth

hub Pricing in Europe - An Argument For Gasage

Dear Conference Participants, Dear Mr. Stern and Mr. Rogers! The first thing I would like to do is to apologize for calling you consultants in the research paper I issued on January 11, 2013. In calling

Dear Conference Participants, Dear Mr. Stern and Mr. Rogers! The first thing I would like to do is to apologize for calling you consultants in the research paper I issued on January 11, 2013. In calling

Russian Gas and European Energy Security : Beyond Clichés

Russian Gas and European Energy Security : Beyond Clichés World Energy Council Workshop Energy Vulnerabilities in Europe Didier Lebout, Strategy and Development Director Gazprom Marketing and Trading France

Russian Gas and European Energy Security : Beyond Clichés World Energy Council Workshop Energy Vulnerabilities in Europe Didier Lebout, Strategy and Development Director Gazprom Marketing and Trading France

Hedging Natural Gas Prices

Hedging Natural Gas Prices Luke Miller Assistant Professor of Finance Office of Economic Analysis & Business Research School of Business Administration Fort Lewis College Natural Gas Industry U.S. natural

Hedging Natural Gas Prices Luke Miller Assistant Professor of Finance Office of Economic Analysis & Business Research School of Business Administration Fort Lewis College Natural Gas Industry U.S. natural

How Do Energy Suppliers Make Money? Copyright 2015. Solomon Energy. All Rights Reserved.

Bills for electricity and natural gas can be a very high proportion of a company and household budget. Accordingly, the way in which commodity prices are set is of material importance to most consumers.

Bills for electricity and natural gas can be a very high proportion of a company and household budget. Accordingly, the way in which commodity prices are set is of material importance to most consumers.

LNG Poised to Significantly Increase its Share of Global Gas Market David Wood February 2004 Petroleum Review p.38-39

LNG Poised to Significantly Increase its Share of Global Gas Market David Wood February 2004 Petroleum Review p.38-39 For the past few years LNG has experienced high levels of activity and investment in

LNG Poised to Significantly Increase its Share of Global Gas Market David Wood February 2004 Petroleum Review p.38-39 For the past few years LNG has experienced high levels of activity and investment in

THE GROWING GLOBAL MARKET OF LNG

THE GROWING GLOBAL MARKET OF LNG ISSUES & CHALLENGES Dr Naji Abi-Aad April 2013 The Growing Global Market of LNG Outline Characteristics of Liquefied Natural Gas (LNG) & its Trade Increasing Volumes of

THE GROWING GLOBAL MARKET OF LNG ISSUES & CHALLENGES Dr Naji Abi-Aad April 2013 The Growing Global Market of LNG Outline Characteristics of Liquefied Natural Gas (LNG) & its Trade Increasing Volumes of

NEW TO FOREX? FOREIGN EXCHANGE RATE SYSTEMS There are basically two types of exchange rate systems:

NEW TO FOREX? WHAT IS FOREIGN EXCHANGE Foreign Exchange (FX or Forex) is one of the largest and most liquid financial markets in the world. According to the authoritative Triennial Central Bank Survey

NEW TO FOREX? WHAT IS FOREIGN EXCHANGE Foreign Exchange (FX or Forex) is one of the largest and most liquid financial markets in the world. According to the authoritative Triennial Central Bank Survey

GDF SUEZ. Introduction. Jean-François Cirelli

GDF SUEZ Introduction Jean-François Cirelli Content 1. Focus on gas market dynamics 2. Focus on electricity market dynamics 3. Focus on P&L resilience and sensitivities 4. Focus on synergies and performance

GDF SUEZ Introduction Jean-François Cirelli Content 1. Focus on gas market dynamics 2. Focus on electricity market dynamics 3. Focus on P&L resilience and sensitivities 4. Focus on synergies and performance

Oil and Gas U.S. Industry Outlook

Oil and Gas U.S. Industry Outlook VERSION 01 YEAR 13 OUTLOOK: Positive fundamentals & outlook www.eulerhermes.us Key points WTI Crude is expected to continue to converge to Brent crude prices, narrowing

Oil and Gas U.S. Industry Outlook VERSION 01 YEAR 13 OUTLOOK: Positive fundamentals & outlook www.eulerhermes.us Key points WTI Crude is expected to continue to converge to Brent crude prices, narrowing

Oil Speculation by Jussi Keppo July 8, 2008

Oil Speculation by Jussi Keppo July 8, 2008 The increase in the oil spot price seems to be mainly driven by the global demand. According to the U.S. Energy Information Administration, in 1999 the global

Oil Speculation by Jussi Keppo July 8, 2008 The increase in the oil spot price seems to be mainly driven by the global demand. According to the U.S. Energy Information Administration, in 1999 the global

Creating more Value out of Storage

Creating more Value out of Storage By Gary Howorth, Founder Energy-Redefined Introduction Gas Storage is a complicated business which carries with it large risks and potentially low rewards. Assets can

Creating more Value out of Storage By Gary Howorth, Founder Energy-Redefined Introduction Gas Storage is a complicated business which carries with it large risks and potentially low rewards. Assets can

ICIS Power Index Q1 2015 Global gas oversupply pushes down prices

Highlights l UK wholesale electricity market prices hit their lowest levels since the IPI has been calculated, because of global gas oversupply. l UK markets are now much more influenced by global gas

Highlights l UK wholesale electricity market prices hit their lowest levels since the IPI has been calculated, because of global gas oversupply. l UK markets are now much more influenced by global gas

Price formation in liberalised gas markets. Patrick Heren Heren Energy Ltd

Price formation in liberalised gas markets Patrick Heren Heren Energy Ltd Brief advertisement Publishers of daily gas and power market reports, the Heren Index and European Gas Markets newsletter. Independent

Price formation in liberalised gas markets Patrick Heren Heren Energy Ltd Brief advertisement Publishers of daily gas and power market reports, the Heren Index and European Gas Markets newsletter. Independent

THE EU GAS SUPPLY ENVIRONMENT. An Obstacle to Competition? Dick de Jong, CIEP February 2007

THE EU GAS SUPPLY ENVIRONMENT An Obstacle to Competition? Dick de Jong, CIEP February 2007 Today s Market:Some Observations High gas prices should attract new supplies. Sellers market does not help competition

THE EU GAS SUPPLY ENVIRONMENT An Obstacle to Competition? Dick de Jong, CIEP February 2007 Today s Market:Some Observations High gas prices should attract new supplies. Sellers market does not help competition

Adding fuel to the fire North America s hydrocarbon boom is changing everything. Steven Meersman. Roland Rechtsteiner

Adding fuel to the fire North America s hydrocarbon boom is changing everything Steven Meersman Mark Pellerin Roland Rechtsteiner What if the gasoline that you put in your car came from natural gas instead

Adding fuel to the fire North America s hydrocarbon boom is changing everything Steven Meersman Mark Pellerin Roland Rechtsteiner What if the gasoline that you put in your car came from natural gas instead

Report on Pricing by the Energy Charter. The Report can be downloaded free of charge from: www.encharter.org

Oil and Gas Pricing Mechanisms: Past, Current and Future Trends Dr. Andrey A.Konoplyanik, Consultant to the Board, Gazprombank, and Professor, Russian State Oil & Gas University Presentation at the session

Oil and Gas Pricing Mechanisms: Past, Current and Future Trends Dr. Andrey A.Konoplyanik, Consultant to the Board, Gazprombank, and Professor, Russian State Oil & Gas University Presentation at the session

Contract pricing disputes

Ted Greeno Caroline Kehoe Herbert Smith LLP 1. Introduction Contract pricing disputes in the energy industries typically arise in the context of long-term contracts under which an initial price agreed

Ted Greeno Caroline Kehoe Herbert Smith LLP 1. Introduction Contract pricing disputes in the energy industries typically arise in the context of long-term contracts under which an initial price agreed

Brisbane Mining Club June Lunch 2014 David Knox Managing Director & CEO, Santos Limited

Brisbane Mining Club June Lunch 2014 David Knox Managing Director & CEO, Santos Limited Thursday, 5 June Brisbane Ladies and Gentlemen Thank you for inviting me here today. Today I want to talk to you

Brisbane Mining Club June Lunch 2014 David Knox Managing Director & CEO, Santos Limited Thursday, 5 June Brisbane Ladies and Gentlemen Thank you for inviting me here today. Today I want to talk to you

World Energy Outlook 2009. Presentation to the Press London, 10 November 2009

World Energy Outlook 29 Presentation to the Press London, 1 November 29 The context The worst economic slump since the 2 nd World War & signs of recovery but how fast? An oil price collapse & then a rebound

World Energy Outlook 29 Presentation to the Press London, 1 November 29 The context The worst economic slump since the 2 nd World War & signs of recovery but how fast? An oil price collapse & then a rebound

Deutsche Bank UK Banks Conference 07 April 2011 Chris Lucas, Group Finance Director

Deutsche Bank UK Banks Conference 07 April 2011 Chris Lucas, Group Finance Director Slide: Name Slide Thanks very much, it s a great pleasure to be here today and I d like to thank our hosts Deutsche Bank

Deutsche Bank UK Banks Conference 07 April 2011 Chris Lucas, Group Finance Director Slide: Name Slide Thanks very much, it s a great pleasure to be here today and I d like to thank our hosts Deutsche Bank

BUSM 411: Derivatives and Fixed Income

BUSM 411: Derivatives and Fixed Income 2. Forwards, Options, and Hedging This lecture covers the basic derivatives contracts: forwards (and futures), and call and put options. These basic contracts are

BUSM 411: Derivatives and Fixed Income 2. Forwards, Options, and Hedging This lecture covers the basic derivatives contracts: forwards (and futures), and call and put options. These basic contracts are

for Analysing Listed Private Equity Companies

8 Steps for Analysing Listed Private Equity Companies Important Notice This document is for information only and does not constitute a recommendation or solicitation to subscribe or purchase any products.

8 Steps for Analysing Listed Private Equity Companies Important Notice This document is for information only and does not constitute a recommendation or solicitation to subscribe or purchase any products.

Natural Gas Prices and LNG's Dirty Little Secret

Natural Gas Prices and LNG's Dirty Little Secret by G. Allen Brooks Parks Paton Hoepfl & Brown Musings from the Oil Patch Optimism about the ending of the U.S. recession and its impact on future demand

Natural Gas Prices and LNG's Dirty Little Secret by G. Allen Brooks Parks Paton Hoepfl & Brown Musings from the Oil Patch Optimism about the ending of the U.S. recession and its impact on future demand

The 2024 prospects for EU agricultural markets: drivers and uncertainties. Tassos Haniotis

1. Introduction The 2024 prospects for EU agricultural markets: drivers and uncertainties Tassos Haniotis Director of Economic Analysis, Perspectives and Evaluations; Communication DG Agriculture and Rural

1. Introduction The 2024 prospects for EU agricultural markets: drivers and uncertainties Tassos Haniotis Director of Economic Analysis, Perspectives and Evaluations; Communication DG Agriculture and Rural

Oil Market Outlook. March 2016. Compiled by Dr Jeremy Wakeford

Oil Market Outlook March 2016 Compiled by Dr Jeremy Wakeford Highlights Oil prices have remained very weak in recent months, with the Brent benchmark averaging $31/bbl in January and $32/bbl in February

Oil Market Outlook March 2016 Compiled by Dr Jeremy Wakeford Highlights Oil prices have remained very weak in recent months, with the Brent benchmark averaging $31/bbl in January and $32/bbl in February

Project LINK Meeting New York, 20-22 October 2010. Country Report: Australia

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

Energy Prices. Presented by: John Heffernan

Global Wholesale Energy Prices Presented by: John Heffernan Energy in 2012 In 2012, the growth in Energy consumption slowed in 2012 90% of this growth came from China & India Consumption & production of

Global Wholesale Energy Prices Presented by: John Heffernan Energy in 2012 In 2012, the growth in Energy consumption slowed in 2012 90% of this growth came from China & India Consumption & production of

Which Is Better: Fixed or Floating Electricity Prices?

Which Is Better: Fixed or Floating Electricity Prices? Which Is Better: Fixed or Floating Electricity Prices? We tend to disparage monopoly power. But if utility distribution systems were not subject to

Which Is Better: Fixed or Floating Electricity Prices? Which Is Better: Fixed or Floating Electricity Prices? We tend to disparage monopoly power. But if utility distribution systems were not subject to

Introduction to Futures Contracts

Introduction to Futures Contracts September 2010 PREPARED BY Eric Przybylinski Research Analyst Gregory J. Leonberger, FSA Director of Research Abstract Futures contracts are widely utilized throughout

Introduction to Futures Contracts September 2010 PREPARED BY Eric Przybylinski Research Analyst Gregory J. Leonberger, FSA Director of Research Abstract Futures contracts are widely utilized throughout

Federal Reserve Monetary Policy

Federal Reserve Monetary Policy To prevent recession, earlier this decade the Federal Reserve s monetary policy pushed down the short-term interest rate to just 1%, the lowest level for many decades. Long-term

Federal Reserve Monetary Policy To prevent recession, earlier this decade the Federal Reserve s monetary policy pushed down the short-term interest rate to just 1%, the lowest level for many decades. Long-term

How LNG Promises to Change Natural Gas Markets and how the markets are already changing LNG!

How LNG Promises to Change Natural Gas Markets and how the markets are already changing LNG! LNG Opportunities Seminar, DnB markets and the Canadian Embassy Oslo 4 th December 2014 Karen Sund Full-picture

How LNG Promises to Change Natural Gas Markets and how the markets are already changing LNG! LNG Opportunities Seminar, DnB markets and the Canadian Embassy Oslo 4 th December 2014 Karen Sund Full-picture

Is Gold Worth Its Weight in a Portfolio?

Is Gold Worth Its Weight in a Portfolio? During a weak global economy and uncertain financial markets, many investors tout the benefits of holding gold. Some proponents claim that gold deserves a significant

Is Gold Worth Its Weight in a Portfolio? During a weak global economy and uncertain financial markets, many investors tout the benefits of holding gold. Some proponents claim that gold deserves a significant

Chapter 16: Financial Risk Management

Chapter 16: Financial Risk Management Introduction Overview of Financial Risk Management in Treasury Interest Rate Risk Foreign Exchange (FX) Risk Commodity Price Risk Managing Financial Risk The Benefits

Chapter 16: Financial Risk Management Introduction Overview of Financial Risk Management in Treasury Interest Rate Risk Foreign Exchange (FX) Risk Commodity Price Risk Managing Financial Risk The Benefits

Oil and Gas - Ukraine, a Case Study

Policy Briefing Series [PB/05/2011] Economic cost of cheap Russian gas Analysis and Policy Recommendations Ricardo Giucci, Georg Zachmann Germany Advisory Group Ukraine Berlin/Kyiv, April 2011 Motivation

Policy Briefing Series [PB/05/2011] Economic cost of cheap Russian gas Analysis and Policy Recommendations Ricardo Giucci, Georg Zachmann Germany Advisory Group Ukraine Berlin/Kyiv, April 2011 Motivation

Adjusting to a Changing Economic World. Good afternoon, ladies and gentlemen. It s a pleasure to be with you here in Montréal today.

Remarks by David Dodge Governor of the Bank of Canada to the Board of Trade of Metropolitan Montreal Montréal, Quebec 11 February 2004 Adjusting to a Changing Economic World Good afternoon, ladies and

Remarks by David Dodge Governor of the Bank of Canada to the Board of Trade of Metropolitan Montreal Montréal, Quebec 11 February 2004 Adjusting to a Changing Economic World Good afternoon, ladies and

Statement by Dean Baker, Co-Director of the Center for Economic and Policy Research (www.cepr.net)

") Statement by Dean Baker, Co-Director of the Center for Economic and Policy Research (www.cepr.net) Before the U.S.-China Economic and Security Review Commission, hearing on China and the Future of Globalization.

Statement by Dean Baker, Co-Director of the Center for Economic and Policy Research (www.cepr.net) Before the U.S.-China Economic and Security Review Commission, hearing on China and the Future of Globalization.

Exchange-traded Funds

Mitch Kosev and Thomas Williams* The exchange-traded fund (ETF) industry has grown strongly in a relatively short period of time, with the industry attracting greater attention as it grows in size. The

Mitch Kosev and Thomas Williams* The exchange-traded fund (ETF) industry has grown strongly in a relatively short period of time, with the industry attracting greater attention as it grows in size. The

Investment insight. Fixed income the what, when, where, why and how TABLE 1: DIFFERENT TYPES OF FIXED INCOME SECURITIES. What is fixed income?

Fixed income investments make up a large proportion of the investment universe and can form a significant part of a diversified portfolio but investors are often much less familiar with how fixed income

Fixed income investments make up a large proportion of the investment universe and can form a significant part of a diversified portfolio but investors are often much less familiar with how fixed income

CONTRACTS FOR DIFFERENCE

CONTRACTS FOR DIFFERENCE Contracts for Difference (CFD s) were originally developed in the early 1990s in London by UBS WARBURG. Based on equity swaps, they had the benefit of being traded on margin. They

CONTRACTS FOR DIFFERENCE Contracts for Difference (CFD s) were originally developed in the early 1990s in London by UBS WARBURG. Based on equity swaps, they had the benefit of being traded on margin. They

Russian energy price subsidies

И.А. Башмаков Центр по эффективному использованию энергии www.cenef.ru 8(499) 120-92-09 Russian energy price subsidies The effectiveness of energy pricing policy is very much determined by energy demand

И.А. Башмаков Центр по эффективному использованию энергии www.cenef.ru 8(499) 120-92-09 Russian energy price subsidies The effectiveness of energy pricing policy is very much determined by energy demand

ECONOMIC OUTLOOK. Quantifying the Shale Gas Revolution s Impact on U.S. Industrial Energy Consumption MAY 2014

MAY ECONOMIC OUTLOOK Quantifying the Shale Gas Revolution s Impact on U.S. Industrial Energy Consumption THE CARLYLE GROUP 1001 PENNSYLVANIA AVENUE, NW WASHINGTON, DC 20004-2505 202-729-5626 WWW.CARLYLE.COM

MAY ECONOMIC OUTLOOK Quantifying the Shale Gas Revolution s Impact on U.S. Industrial Energy Consumption THE CARLYLE GROUP 1001 PENNSYLVANIA AVENUE, NW WASHINGTON, DC 20004-2505 202-729-5626 WWW.CARLYLE.COM

FLEXIBLE EXCHANGE RATES

FLEXIBLE EXCHANGE RATES Along with globalization has come a high degree of interdependence. Central to this is a flexible exchange rate system, where exchange rates are determined each business day by

FLEXIBLE EXCHANGE RATES Along with globalization has come a high degree of interdependence. Central to this is a flexible exchange rate system, where exchange rates are determined each business day by

2015 Oil Outlook. january 21, 2015

MainStay Investments is pleased to provide the following investment insights from Epoch Investment Partners, Inc., a premier institutional manager and subadvisor to a number of MainStay Investments products.

MainStay Investments is pleased to provide the following investment insights from Epoch Investment Partners, Inc., a premier institutional manager and subadvisor to a number of MainStay Investments products.

The Argument for Corporate Debt December 2008

The Argument for Corporate Debt December 2008 This past quarter the US economy has experienced what appears to be the crescendo of a credit crisis that has been building for well over a year. The causes

The Argument for Corporate Debt December 2008 This past quarter the US economy has experienced what appears to be the crescendo of a credit crisis that has been building for well over a year. The causes

An Alternative Way to Diversify an Income Strategy

Senior Secured Loans An Alternative Way to Diversify an Income Strategy Alternative Thinking Series There is no shortage of uncertainty and risk facing today s investor. From high unemployment and depressed

Senior Secured Loans An Alternative Way to Diversify an Income Strategy Alternative Thinking Series There is no shortage of uncertainty and risk facing today s investor. From high unemployment and depressed

What do rising rates mean for equities?

What do rising rates mean for equities? Faced with the choice between changing one's mind and proving that there is no need to do so, almost everyone gets busy on the proof. - John Kenneth Galbraith Wall

What do rising rates mean for equities? Faced with the choice between changing one's mind and proving that there is no need to do so, almost everyone gets busy on the proof. - John Kenneth Galbraith Wall

INTEREST RATES: WHAT GOES UP MUST COME DOWN

3 INTEREST RATES: WHAT GOES UP MUST COME DOWN John M. Petersen Melvin Mark Capital Group, LLC What an interesting time to be asked to write something about interest rates! Our practice emphasis is commercial

3 INTEREST RATES: WHAT GOES UP MUST COME DOWN John M. Petersen Melvin Mark Capital Group, LLC What an interesting time to be asked to write something about interest rates! Our practice emphasis is commercial

www.citizenshipteacher.co.uk 2011 16228 1

The stock market www.citizenshipteacher.co.uk 2011 16228 1 Lesson objectives I will understand what a stock market is. I will identify what caused the downturn in the American Stock Market. www.citizenshipteacher.co.uk

The stock market www.citizenshipteacher.co.uk 2011 16228 1 Lesson objectives I will understand what a stock market is. I will identify what caused the downturn in the American Stock Market. www.citizenshipteacher.co.uk

REGULATION OF THE GAS SUPPLY MARKET FREQUENTLY ASKED QUESTIONS

REGULATION OF THE GAS SUPPLY MARKET FREQUENTLY ASKED QUESTIONS Why is it necessary to regulate gas supply in a free market? Manx Gas has a natural monopoly in the Isle of Man gas supply market. Given the

REGULATION OF THE GAS SUPPLY MARKET FREQUENTLY ASKED QUESTIONS Why is it necessary to regulate gas supply in a free market? Manx Gas has a natural monopoly in the Isle of Man gas supply market. Given the

Chapter Two FINANCIAL AND ECONOMIC INDICATORS

Chapter Two FINANCIAL AND ECONOMIC INDICATORS 1. Introduction In Chapter One we discussed the concept of risk and the importance of protecting a portfolio from losses. Managing your investment risk should

Chapter Two FINANCIAL AND ECONOMIC INDICATORS 1. Introduction In Chapter One we discussed the concept of risk and the importance of protecting a portfolio from losses. Managing your investment risk should

Fifty years of Australia s trade

Fifty years of Australia s trade Introduction This edition of Australia s Composition of Trade marks the publication s 50th anniversary. In recognition of this milestone, this article analyses changes

Fifty years of Australia s trade Introduction This edition of Australia s Composition of Trade marks the publication s 50th anniversary. In recognition of this milestone, this article analyses changes

Short Selling Tutorial

Short Selling Tutorial http://www.investopedia.com/university/shortselling/ Thanks very much for downloading the printable version of this tutorial. As always, we welcome any feedback or suggestions. http://www.investopedia.com/investopedia/contact.asp

Short Selling Tutorial http://www.investopedia.com/university/shortselling/ Thanks very much for downloading the printable version of this tutorial. As always, we welcome any feedback or suggestions. http://www.investopedia.com/investopedia/contact.asp

Today s bond market is riskier and more volatile than in several generations. As

Fixed Income Approach 2014 Volume 1 Executive Summary Today s bond market is riskier and more volatile than in several generations. As interest rates rise so does the anxiety of fixed income investors

Fixed Income Approach 2014 Volume 1 Executive Summary Today s bond market is riskier and more volatile than in several generations. As interest rates rise so does the anxiety of fixed income investors

NPH Fixed Income Research Update. Bob Downing, CFA. NPH Senior Investment & Due Diligence Analyst

White Paper: NPH Fixed Income Research Update Authored By: Bob Downing, CFA NPH Senior Investment & Due Diligence Analyst National Planning Holdings, Inc. Due Diligence Department National Planning Holdings,

White Paper: NPH Fixed Income Research Update Authored By: Bob Downing, CFA NPH Senior Investment & Due Diligence Analyst National Planning Holdings, Inc. Due Diligence Department National Planning Holdings,

Main Street. Economic information. By Jason P. Brown, Economist, and Andres Kodaka, Research Associate

THE Main Street ECONOMIST: ECONOMIST Economic information Agricultural for the and Cornhusker Rural Analysis State S e Issue p t e m b2, e r 214 2 1 Feed de er ra al l RR e es se er rv ve e BBa an nk k

THE Main Street ECONOMIST: ECONOMIST Economic information Agricultural for the and Cornhusker Rural Analysis State S e Issue p t e m b2, e r 214 2 1 Feed de er ra al l RR e es se er rv ve e BBa an nk k

Fundamentals Level Skills Module, Paper F9

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2008 Answers 1 (a) Rights issue price = 2 5 x 0 8 = $2 00 per share Theoretical ex rights price = ((2 50 x 4) + (1 x 2 00)/5=$2

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2008 Answers 1 (a) Rights issue price = 2 5 x 0 8 = $2 00 per share Theoretical ex rights price = ((2 50 x 4) + (1 x 2 00)/5=$2

The impact of Ukraine-Russia crisis on the European gas market. www.sundenergy.com

The impact of Ukraine-Russia crisis on the European gas market Sergiu Maznic Vienna, 11 March 2015 Full-picture perspective Sund Energy helps navigate into the energy future Energy Economics Environment

The impact of Ukraine-Russia crisis on the European gas market Sergiu Maznic Vienna, 11 March 2015 Full-picture perspective Sund Energy helps navigate into the energy future Energy Economics Environment

The Risk/Reward Properties of Bull Spreads

The Risk/Reward Properties of Bull Spreads ThE RiSk/REWaRD PRoPERTiES of BUll SPREaDS Bull Spreads are versatile instruments. They can be used to trade direction, to trade volatility or, in conjunction

The Risk/Reward Properties of Bull Spreads ThE RiSk/REWaRD PRoPERTiES of BUll SPREaDS Bull Spreads are versatile instruments. They can be used to trade direction, to trade volatility or, in conjunction

The Impact of Gold Trading

The Impact of Gold Trading By: Dan Edward, Market Analyst: FOREXYARD Date: December 2010 In this Issue: I. Introduction A brief history of gold trading II. What affects commodity prices? III. The Global

The Impact of Gold Trading By: Dan Edward, Market Analyst: FOREXYARD Date: December 2010 In this Issue: I. Introduction A brief history of gold trading II. What affects commodity prices? III. The Global

Using Currency Futures to Hedge Currency Risk

Using Currency Futures to Hedge Currency Risk By Sayee Srinivasan & Steven Youngren Product Research & Development Chicago Mercantile Exchange Inc. Introduction Investment professionals face a tough climate.

Using Currency Futures to Hedge Currency Risk By Sayee Srinivasan & Steven Youngren Product Research & Development Chicago Mercantile Exchange Inc. Introduction Investment professionals face a tough climate.

Oil & Gas Industry Recent Developments

Oil & Gas Industry Recent Developments By Dr. Hilmar R. Zeissig Houston International Business Corp. For RIAS BERLIN COMMISSION U.S. Energy Program in Texas Houston, Texas, April 27, 2015 Typical Downstream

Oil & Gas Industry Recent Developments By Dr. Hilmar R. Zeissig Houston International Business Corp. For RIAS BERLIN COMMISSION U.S. Energy Program in Texas Houston, Texas, April 27, 2015 Typical Downstream

Fixed Income Strategy Quarterly April 2015

Doucet Asset Management Fixed Income Strategy Quarterly April 2015 The first quarter of 2015 was a fairly uneventful one. Across the world, the pullback in yields we witnessed in 2014 continued; however,

Doucet Asset Management Fixed Income Strategy Quarterly April 2015 The first quarter of 2015 was a fairly uneventful one. Across the world, the pullback in yields we witnessed in 2014 continued; however,

Developments in the Traded Market:

PatrickHeatherConsultancy Developments in the Traded Market: The Evolution of European Traded Gas Hubs Eurogas Conference on Central and Eastern Europe Ljubljana, 15 th December, 2015 The contents of this

PatrickHeatherConsultancy Developments in the Traded Market: The Evolution of European Traded Gas Hubs Eurogas Conference on Central and Eastern Europe Ljubljana, 15 th December, 2015 The contents of this

CHAPTER 12 CHAPTER 12 FOREIGN EXCHANGE

CHAPTER 12 CHAPTER 12 FOREIGN EXCHANGE CHAPTER OVERVIEW This chapter discusses the nature and operation of the foreign exchange market. The chapter begins by describing the foreign exchange market and

CHAPTER 12 CHAPTER 12 FOREIGN EXCHANGE CHAPTER OVERVIEW This chapter discusses the nature and operation of the foreign exchange market. The chapter begins by describing the foreign exchange market and

LEE BUSI N ESS SCHOOL UNITED STATES QUARTERLY ECONOMIC FORECAST. U.S. Economic Growth to Accelerate. Chart 1. Growth Rate of U.S.

CENTER FOR BUSINESS & ECONOMIC RESEARCH LEE BUSI N ESS SCHOOL UNITED STATES QUARTERLY ECONOMIC FORECAST O U.S. Economic Growth to Accelerate ver the past few years, U.S. economic activity has remained

CENTER FOR BUSINESS & ECONOMIC RESEARCH LEE BUSI N ESS SCHOOL UNITED STATES QUARTERLY ECONOMIC FORECAST O U.S. Economic Growth to Accelerate ver the past few years, U.S. economic activity has remained

(c) 2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author.

2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author.") The futures markets Introduction and Mechanics, using Natural Gas as the example (c) 2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author. Forward

The futures markets Introduction and Mechanics, using Natural Gas as the example (c) 2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author. Forward

The Commodity Price Roller Coaster

The Commodity Price Roller Coaster Jayati Ghosh For most of the past year, as global prices in oil and other commodity markets zoomed to stratospheric levels, we were told that it had nothing to do with

The Commodity Price Roller Coaster Jayati Ghosh For most of the past year, as global prices in oil and other commodity markets zoomed to stratospheric levels, we were told that it had nothing to do with

Note No. 137 March 1998. Countries in Asia, Europe, and North and South America are introducing reforms to boost

Privatesector P U B L I C P O L I C Y F O R T H E Note No. 137 March 1998 Competition in the Natural Gas Industry The emergence of spot, financial, and pipeline capacity markets Andrej Juris Countries

Privatesector P U B L I C P O L I C Y F O R T H E Note No. 137 March 1998 Competition in the Natural Gas Industry The emergence of spot, financial, and pipeline capacity markets Andrej Juris Countries

Forward exchange rates

Forward exchange rates The forex market consists of two distinct markets - the spot foreign exchange market (in which currencies are bought and sold for delivery within two working days) and the forward

Forward exchange rates The forex market consists of two distinct markets - the spot foreign exchange market (in which currencies are bought and sold for delivery within two working days) and the forward

Spectra Energy Builds a Business

» Introducing Spectra Energy Builds a Business CEO Fowler on Challenges Ahead By Martin Rosenberg Natural gas once again looms as an important fuel for electricity generation, given a spate of cancellations

» Introducing Spectra Energy Builds a Business CEO Fowler on Challenges Ahead By Martin Rosenberg Natural gas once again looms as an important fuel for electricity generation, given a spate of cancellations

ICIS Power Index Q2 2015 UK energy prices hit five-year lows

Highlights l Wholesale UK gas and electricity market prices are at their lowest quarterly average in five years, according to the ICIS Power Index and the ICIS price for gas to be delivered over the next

Highlights l Wholesale UK gas and electricity market prices are at their lowest quarterly average in five years, according to the ICIS Power Index and the ICIS price for gas to be delivered over the next

Hedging Strategies Using Futures. Chapter 3

Hedging Strategies Using Futures Chapter 3 Fundamentals of Futures and Options Markets, 8th Ed, Ch3, Copyright John C. Hull 2013 1 The Nature of Derivatives A derivative is an instrument whose value depends

Hedging Strategies Using Futures Chapter 3 Fundamentals of Futures and Options Markets, 8th Ed, Ch3, Copyright John C. Hull 2013 1 The Nature of Derivatives A derivative is an instrument whose value depends

Note No. 138 March 1998. Natural Gas Markets in the U.K.

Privatesector P U B L I C P O L I C Y F O R T H E Note No. 138 March 1998 Competition, industry structure, and market power of the incumbent Andrej Juris The deregulation of the U.K. natural gas industry

Privatesector P U B L I C P O L I C Y F O R T H E Note No. 138 March 1998 Competition, industry structure, and market power of the incumbent Andrej Juris The deregulation of the U.K. natural gas industry

UK Gas Security Policy

www.eprg.group.cam.ac.uk UK Gas Security Policy and international gas markets Dr Pierre Noël EPRG, University of Cambridge pn243 [at] cam.ac.uk London, 15 th February 2012 EPRG, University of Cambridge

www.eprg.group.cam.ac.uk UK Gas Security Policy and international gas markets Dr Pierre Noël EPRG, University of Cambridge pn243 [at] cam.ac.uk London, 15 th February 2012 EPRG, University of Cambridge

About Hedge Funds. What is a Hedge Fund?

About Hedge Funds What is a Hedge Fund? A hedge fund is a fund that can take both long and short positions, use arbitrage, buy and sell undervalued securities, trade options or bonds, and invest in almost

About Hedge Funds What is a Hedge Fund? A hedge fund is a fund that can take both long and short positions, use arbitrage, buy and sell undervalued securities, trade options or bonds, and invest in almost

Strategy Monthly. Unfixed Income. May 26, 2015

Strategy Monthly Unfixed Income The yield on traditional fixed income this year has been anything but fixed. From a low of. % on the last day of January, the yield to maturity on the ten year Treasury

Strategy Monthly Unfixed Income The yield on traditional fixed income this year has been anything but fixed. From a low of. % on the last day of January, the yield to maturity on the ten year Treasury

Forecasting Chinese Economy for the Years 2013-2014

Forecasting Chinese Economy for the Years 2013-2014 Xuesong Li Professor of Economics Deputy Director of Institute of Quantitative & Technical Economics Chinese Academy of Social Sciences Email: xsli@cass.org.cn

Forecasting Chinese Economy for the Years 2013-2014 Xuesong Li Professor of Economics Deputy Director of Institute of Quantitative & Technical Economics Chinese Academy of Social Sciences Email: xsli@cass.org.cn

Displacement of Coal with Natural Gas to Generate Electricity

Displacement of Coal with Natural Gas to Generate Electricity The American Coalition for Clean Coal Electricity (ACCCE) supports a balanced energy strategy that will ensure affordable and reliable energy,

Displacement of Coal with Natural Gas to Generate Electricity The American Coalition for Clean Coal Electricity (ACCCE) supports a balanced energy strategy that will ensure affordable and reliable energy,

Price developments on the EU retail markets for electricity and gas 1998 2011

Price developments on the EU retail markets for electricity and gas 1998 2011 The Market Observatory for Energy has analysed price developments on the retail markets for electricity and natural gas (domestic

Price developments on the EU retail markets for electricity and gas 1998 2011 The Market Observatory for Energy has analysed price developments on the retail markets for electricity and natural gas (domestic

Time! Our clients give us the responsibility to grow those funds. The problem is that a

Time! January 27, 2015 It takes time to grow an investment portfolio. Most of our clients need to build and maintain an investment portfolio that, when combined with Social Security, pensions, and potential

Time! January 27, 2015 It takes time to grow an investment portfolio. Most of our clients need to build and maintain an investment portfolio that, when combined with Social Security, pensions, and potential

Secondary and short term natural gas markets International experiences

Secondary and short term natural gas markets International experiences Bogotá, 13 th May 2011 Presented by: Dan Harris Principal The Brattle Group Copyright 2011 The Brattle Group, Inc. www.brattle.com

Secondary and short term natural gas markets International experiences Bogotá, 13 th May 2011 Presented by: Dan Harris Principal The Brattle Group Copyright 2011 The Brattle Group, Inc. www.brattle.com