The Use of IFRS for Prudential and Regulatory Purposes

|

|

|

- Howard Hubbard

- 8 years ago

- Views:

Transcription

1 REPARIS A REGIONAL PROGRAM The Use of IFRS for Prudential and Regulatory Purposes IAS 39 Examples Anna Czarniecka Financial Reporting Consultant annaczarniecka@tiscali.co.uk THE ROAD TO EUROPE: PROGRAM OF ACCOUNTING REFORM AND INSTITUTIONAL STRENGTHENING (REPARIS)

2 Classification of Financial Assets! IAS 39.9 has 4 categories of financial assets as follows: Loans and receivables Held-to maturity investments (HTM) Financial assets at fair value through profit or loss (FVTPL) Available-for-sale financial assets (AFS) Disclose categories in balance sheet or notes IFRS 7.8 2

Available-for-sale financial assets (AFS) Disclose")

3 Measurement! Loans and receivables are measured at amortised cost! HTM is measured at amortised cost! FVTPL is measured at fair value! AFS is measured at fair value 3

4 Amortised Cost and Effective Interest Rate (EIR)! IAS 39.9 measurement at initial recognition minus repayments...using the EIR. EIR is defined as the rate that exactly discounts estimated future cash payments or receipts through the expected life of the financial instrument... to the net carrying amount of the financial asset or liability! EIR calculation includes all fees and points paid or received that are an integral part of the EIR 4

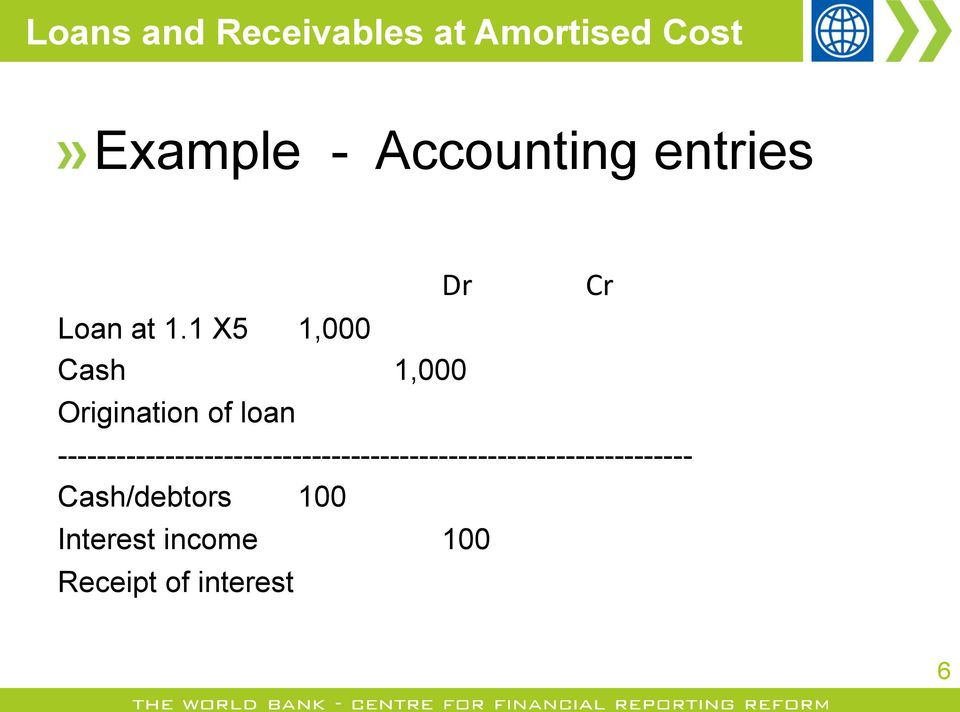

5 Loans and Receivables at Amortised Cost! Example - Fixed interest loan repayable at maturity. No fees or costs.! At 1.1 X5 lend LCY 1,000 for 5 years at 10% Cash inflows Discounted amount X X X X X9 1, Carrying amt 1.1 X5 1,

6 Loans and Receivables at Amortised Cost! Example - Accounting entries Dr Loan at 1.1 X5 1,000 Cash 1,000 Origination of loan Cr Cash/debtors 100 Interest income 100 Receipt of interest 6

7 Loan at Amortised Cost! Example Fixed interest loan repayable at maturity using EIR method of amortisation! At 1.1 X5 lend LCY 1m for 10 years at 7%! Origination fee charged LCY 12,500! Origination costs incurred LCY 25,000! Original EIR 6.823% Loan Principal 1,000,000 Origination fee charged (12,500) Origination costs incurred 25,000 Initial carrying amount 1,012,500 7

8 Carrying Amount of Loan over Period to Maturity Cash inflows Interest income Amor5sa5on of net fees Carrying amount 1.1 X5 70,000 1,012, X5 70,000 69, ,011, X6 70,000 69, ,010, X7 70,000 68,959 1,041 1,009, X8 70,000 68,888 1,112 1,008, X9 70,000 68,812 1,188 1,007,272 8

9 Carrying Amount of Loan over Period to Maturity (Cont d) Cash inflows Interest income Amor5sa5on of net fees Carrying amount Y0 70,000 68,731 1,269 1,006, Y1 70,000 68,644 1,356 1,004, Y2 70,000 68,552 1,448 1,003, Y3 70,000 68,453 1,547 1,001, Y4 70,000 68,348 1,652 1,000, , ,500 12,500 Repayment of loan (1,000,000) 9

9")

10 Loan at Amortised Cost Accounting entries 1.1 X5 Loan account 1,000,000 Cash 1,000,000 Amount lent to borrower X5 Loan account 25,000 Cash 25,000 Origination costs incurred by lender

11 Loan at Amortised Cost (Cont d) 1.1.X5 Cash 12,500 Loan account 12,500 Origination Fees charged to borrower X5 Debtors 70,000 Interest income account 69,083 Loan account 917 Contractual interest accrued at the due date

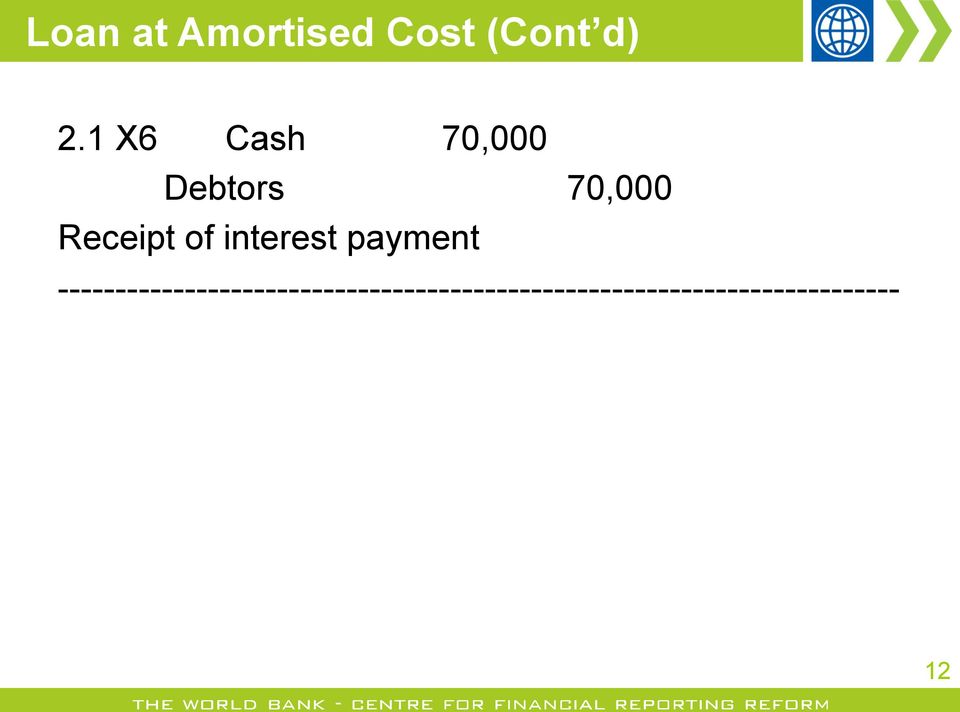

12 Loan at Amortised Cost (Cont d) 2.1 X6 Cash 70,000 Debtors 70,000 Receipt of interest payment

13 Impairment of Financial Assets at Amortised Cost! IAS Objective evidence of impairment includes observable data about the following loss events: Default on payments Lender grants concession because of borrower s financial difficulty Borrower s probable bankruptcy or other financial reorganisation No active market for that financial asset Decrease in estimated cash flows from a group of financial assets indicated by observable data because of: adverse changes in payment status; or economic conditions that correlate with defaults on assets within the group This is an incurred loss model 13

14 Impairment of Financial Assets at Amortised Cost! Financial assets carried at amortised cost! Loans and receivables Amount of the loss is the difference between the carrying amount and present value of estimated future cash flows using original EIR Loss is recognised in profit or loss Interest is recognised on the new carrying amount using original EIR (discount unwind) IFRS 7.20 requires disclosure of these amounts 14

IFRS 7.")

15 Loan Impairment! Basic example Loan carried at LCY 100 Collateral of 80 receivable in 1 year EIR 10%! Initial allowance Discounted cash flows 80/1.1 =73 Carrying value of loan LCY 73 Allowance account is LCY 27 (100-73) Interest recognised is LCY 7 (80-73) Recover collateral of LCY 80 at end of year 1 15

")

16 Reversal of Impairment! IAS allows reversal of a loss only if the decrease can be related to an event occurring after the impairment was recognised. For example, an improvement of the borrower s credit rating. 16

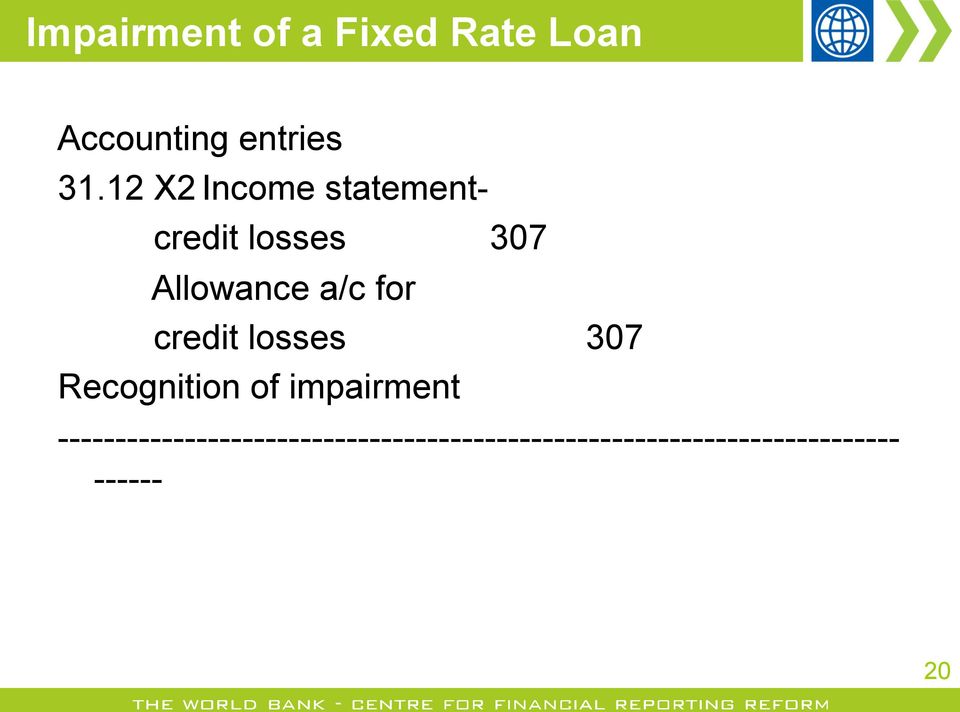

17 Impairment of a Fixed Rate Loan Loan principal at 1.1 X1 1,000 Interest rate 10% Term of loan 5 years At X2 the borrower has financial difficulties. The lender agrees to accept two further payments of LCY 400 at the end of years X3 and X4 17

18 Impairment of a Fixed Rate Loan (Cont d) Carrying amount of loan at: X2 1, X X Cash flows Present values Present value of loan at X2 693 Amount of impairment to profit or loss at X2 307 Gross amount of loan 1,000 18

19 Impairment of a Fixed Rate Loan (Cont d) Interest Income on impaired loan Cash flows Interest Carrying amount at 10%

20 Impairment of a Fixed Rate Loan Accounting entries X2 Income statement- credit losses 307 Allowance a/c for credit losses 307 Recognition of impairment

21 Impairment of a Fixed Rate Loan (Cont d) X3 Cash 400 Interest income 69 Loan account 331 Receipt of first agreed payment X4 Cash 400 Interest income 38 Loan account 362 Final payment

22 Impairment of a Fixed Rate Loan (Cont d) X4 Allowance account 307 Loan account 307 Loan written off

23 Financial Instruments Measured at Fair Value! Fair value is the amount at which an asset could be exchanged, or a liability settled, between knowledgeable, willing parties in an arm s length transaction IAS

24 Held for Trading Example 1.1 X1 Purchase of a bond at X1 Fair value of bond X1 Sell bond for 95 Accounting entries 1.1 X1 Trading assets debt securities 98 Cash 98 Purchase of bond 24

25 Held for Trading (Cont d) 31.3 X1 Net trading profit 2 Trading assets debt securities 2 Loss at next reporting date X1 Cash 95 Net trading profit/loss 1 Trading assets debt securities 96 Sale of bond 25

26 Available for Sale Financial Assets Types of AFS financial assets:! Equity investments! Loans and receivables quoted designated! Quoted debt instruments Focus for investments quoted in an active market should they be classified as fair value through profit or loss or designated as AFS on initial recognition 26

27 AFS Gains and Losses! Gains or losses on AFS financial assets shall be recognised directly in equity through the statement of changes in equity IAS (b)! On derecognition the cumulative gain or loss previously recognised in equity shall be recognised in profit or loss 27

28 Accounting Entries for AFS Equity Investment 1.1 X5 Investment in XYZ 500 Cash 500 Acquisition of equity investment X5 Investment in XYZ 20 Statement of changes in equity 20 Change in FV of investment at balance sheet date Anna Czarniecka Financial ReporOng Consultant 28

29 Accounting Entries for AFS Equity Investment (Cont d) 30.6 X6 Cash 530 Investment on XYZ 520 Gain on sale profit or loss 10 Sale of investment in XYZ X6 Statement of changes in equity 20 Profit or loss 20 Transfer to profit or loss on sale 29

30 AFS Measurement of Impairment! Any decline in fair value due to impairment is moved from equity to profit or loss! A significant or prolonged decline in fair value of an equity investment below cost is evidence of impairment! No reversal of impairment losses for equity investments IAS 39.69! Reversal allowed for debt securities if it relates to an event occurring after recognition of the impairment IAS

31 AFS Measurement of Impairment Example 1.1 X5 Purchase equity investment X5 FV of equity investment X5 FV of equity investment 450 The decline in value is significant and falling. At X5 impairment of 50 would be charged to profit or loss and there would be no reversal. If the fair value increased to 455 at 30.6 X6, 5 would be debited to the investment and credited to equity. 31

Accounting Guidance Note No. 2010/2

Accounting Guidance Note No. 2010/2 Accounting guidance notes are intended for use by Australian Government reporting entities covered by: S49 of the Financial Management and Accountability Act 1997; or

Accounting Guidance Note No. 2010/2 Accounting guidance notes are intended for use by Australian Government reporting entities covered by: S49 of the Financial Management and Accountability Act 1997; or

Accounting for bonds. Accountants and Insurance Companies. Presented by Kabir Okunlola Partner, KPMG professional Services

Accounting for bonds Bond Training i Workshop for Accountants and Insurance Companies Presented by Kabir Okunlola Partner, KPMG professional Services September 2011 Learning objectives At the end of this

Accounting for bonds Bond Training i Workshop for Accountants and Insurance Companies Presented by Kabir Okunlola Partner, KPMG professional Services September 2011 Learning objectives At the end of this

18 BUSINESS ACCOUNTING STANDARD FINANCIAL ASSETS AND FINANCIAL LIABILITIES I. GENERAL PROVISIONS

APPROVED by Resolution No. 11 of 27 October 2004 of the Standards Board of the Public Establishment the Institute of Accounting of the Republic of Lithuania 18 BUSINESS ACCOUNTING STANDARD FINANCIAL ASSETS

APPROVED by Resolution No. 11 of 27 October 2004 of the Standards Board of the Public Establishment the Institute of Accounting of the Republic of Lithuania 18 BUSINESS ACCOUNTING STANDARD FINANCIAL ASSETS

The Use of IFRS for Prudential and Regulatory Purposes

REPARIS A REGIONAL PROGRAM The Use of IFRS for Prudential and Regulatory Purposes IASB works - IAS 39 THE ROAD TO EUROPE: PROGRAM OF ACCOUNTING REFORM AND INSTITUTIONAL STRENGTHENING (REPARIS) Background

REPARIS A REGIONAL PROGRAM The Use of IFRS for Prudential and Regulatory Purposes IASB works - IAS 39 THE ROAD TO EUROPE: PROGRAM OF ACCOUNTING REFORM AND INSTITUTIONAL STRENGTHENING (REPARIS) Background

ACCOUNTING POLICY INVESTMENTS AND OTHER FINANCIAL ASSETS

Responsible Officer ACCOUNTING POLICY INVESTMENTS AND OTHER FINANCIAL ASSETS Director, Shared Services and Corporate Finance & Advisory Services Contact Officer Senior Group Statutory Reporting Manager,

Responsible Officer ACCOUNTING POLICY INVESTMENTS AND OTHER FINANCIAL ASSETS Director, Shared Services and Corporate Finance & Advisory Services Contact Officer Senior Group Statutory Reporting Manager,

Resource Management Guide No. 115. Accounting for concessional loans

Resource Management Guide No. 115 Accounting for concessional loans NOVEMBER 2014 Commonwealth of Australia 2014 ISBN: 978-1-922096-97-5 (Online) With the exception of the Commonwealth Coat of Arms and

Resource Management Guide No. 115 Accounting for concessional loans NOVEMBER 2014 Commonwealth of Australia 2014 ISBN: 978-1-922096-97-5 (Online) With the exception of the Commonwealth Coat of Arms and

Explain how the instrument will be initially and subsequently measured.

Example 1 Requirement (i) Explain how the instrument will be initially and subsequently measured. Cumulative preference shares Redeemable on 31 December 2016 Obligations, therefore instrument is a financial

Example 1 Requirement (i) Explain how the instrument will be initially and subsequently measured. Cumulative preference shares Redeemable on 31 December 2016 Obligations, therefore instrument is a financial

Riyadh, 16 October 2012. Agenda

Investment Securities Accounting IFRS and SOCPA ICAP KSA Chapter Riyadh, 16 October 2012 Mansoor Chaudhry Agenda 1. Introduction 2. Initial Recognition & Measurement 3. Trade date vs. Settlement date accounting

Investment Securities Accounting IFRS and SOCPA ICAP KSA Chapter Riyadh, 16 October 2012 Mansoor Chaudhry Agenda 1. Introduction 2. Initial Recognition & Measurement 3. Trade date vs. Settlement date accounting

SSAP 24 STATEMENT OF STANDARD ACCOUNTING PRACTICE 24 ACCOUNTING FOR INVESTMENTS IN SECURITIES

SSAP 24 STATEMENT OF STANDARD ACCOUNTING PRACTICE 24 ACCOUNTING FOR INVESTMENTS IN SECURITIES (Issued April 1999) The standards, which have been set in bold italic type, should be read in the context of

SSAP 24 STATEMENT OF STANDARD ACCOUNTING PRACTICE 24 ACCOUNTING FOR INVESTMENTS IN SECURITIES (Issued April 1999) The standards, which have been set in bold italic type, should be read in the context of

International Accounting Standard 39 Financial Instruments: Recognition and Measurement

EC staff consolidated version as of 18 February 2011 FOR INFORMATION PURPOSES ONLY International Accounting Standard 39 Financial Instruments: Recognition and Measurement Objective 1 The objective of this

EC staff consolidated version as of 18 February 2011 FOR INFORMATION PURPOSES ONLY International Accounting Standard 39 Financial Instruments: Recognition and Measurement Objective 1 The objective of this

Accounting and Reporting Policy FRS 102. Staff Education Note 2 Debt instruments - Amortised cost

Accounting and Reporting Policy FRS 102 Staff Education Note 2 Debt instruments - Amortised cost Disclaimer This Education Note has been prepared by FRC staff for the convenience of users of FRS 102 The

Accounting and Reporting Policy FRS 102 Staff Education Note 2 Debt instruments - Amortised cost Disclaimer This Education Note has been prepared by FRC staff for the convenience of users of FRS 102 The

Illustrative Examples on Financial Instruments We Passionately Develop Quality Programmes

Illustrative Examples on Financial Instruments Date 11 June 2015 Time 18:30 20:30 Venue CPA Australia Office www.zhtraining.com Disclaimer The materials of this seminar are intended only to provide general

Illustrative Examples on Financial Instruments Date 11 June 2015 Time 18:30 20:30 Venue CPA Australia Office www.zhtraining.com Disclaimer The materials of this seminar are intended only to provide general

How To Account In Indian Accounting Standards

Indian Accounting Standard (Ind AS) 39 Financial Instruments: Recognition and Measurement Contents Paragraphs Objective 1 Scope 2 7 Definitions 8 9 Embedded derivatives 10 13 Recognition and derecognition

Indian Accounting Standard (Ind AS) 39 Financial Instruments: Recognition and Measurement Contents Paragraphs Objective 1 Scope 2 7 Definitions 8 9 Embedded derivatives 10 13 Recognition and derecognition

Guideline for the Measurement, Monitoring and Control of Impaired Assets

Guideline for the Measurement, Monitoring and Control of Impaired Assets FINAL TABLE OF CONTENTS 1 INTRODUCTION... 1 2 PURPOSE... 1 3 INTERPRETATION... 2 4 IMPAIRMENT RECOGNITION AND MEASUREMENT POLICY...

Guideline for the Measurement, Monitoring and Control of Impaired Assets FINAL TABLE OF CONTENTS 1 INTRODUCTION... 1 2 PURPOSE... 1 3 INTERPRETATION... 2 4 IMPAIRMENT RECOGNITION AND MEASUREMENT POLICY...

Reclassification of financial assets

Issue 34 / March 2009 Supplement to IFRS outlook Reclassification of financial assets This publication summarises all the recent amendments to IAS 39 Financial Instruments: Recognition and Measurement

Issue 34 / March 2009 Supplement to IFRS outlook Reclassification of financial assets This publication summarises all the recent amendments to IAS 39 Financial Instruments: Recognition and Measurement

Türkiye İş Bankası A.Ş. Separate Financial Statements As at and for the Year Ended 31 December 2015

Türkiye İş Bankası A.Ş. Separate Financial Statements As at and for the Year Ended 2015 29 April 2016 This report includes 93 pages of separate financial statements together with their explanatory notes.

Türkiye İş Bankası A.Ş. Separate Financial Statements As at and for the Year Ended 2015 29 April 2016 This report includes 93 pages of separate financial statements together with their explanatory notes.

NEED TO KNOW. IFRS 9 Financial Instruments Impairment of Financial Assets

NEED TO KNOW IFRS 9 Financial Instruments Impairment of Financial Assets 2 IFRS 9 FINANCIAL INSTRUMENTS IMPAIRMENT OF FINANCIAL ASSETS IFRS 9 FINANCIAL INSTRUMENTS IMPAIRMENT OF FINANCIAL ASSETS 3 TABLE

NEED TO KNOW IFRS 9 Financial Instruments Impairment of Financial Assets 2 IFRS 9 FINANCIAL INSTRUMENTS IMPAIRMENT OF FINANCIAL ASSETS IFRS 9 FINANCIAL INSTRUMENTS IMPAIRMENT OF FINANCIAL ASSETS 3 TABLE

Know your standards IFRS 9, Financial Instruments

RELEVANT TO ACCA QUALIFICATION PAPER P2 Know your standards IFRS 9, Financial Instruments The issue of IFRS 9, Financial Instruments is part of the project to replace IAS 39, Financial Instruments Recognition

RELEVANT TO ACCA QUALIFICATION PAPER P2 Know your standards IFRS 9, Financial Instruments The issue of IFRS 9, Financial Instruments is part of the project to replace IAS 39, Financial Instruments Recognition

Related party loans at below-market interest rates

Related party loans at below-market interest rates Our IFRS Viewpoint series provides insights from our global IFRS team on applying IFRSs in challenging situations. Each edition will focus on an area

Related party loans at below-market interest rates Our IFRS Viewpoint series provides insights from our global IFRS team on applying IFRSs in challenging situations. Each edition will focus on an area

International Financial Reporting Standard 7. Financial Instruments: Disclosures

International Financial Reporting Standard 7 Financial Instruments: Disclosures INTERNATIONAL FINANCIAL REPORTING STANDARD AUGUST 2005 International Financial Reporting Standard 7 Financial Instruments:

International Financial Reporting Standard 7 Financial Instruments: Disclosures INTERNATIONAL FINANCIAL REPORTING STANDARD AUGUST 2005 International Financial Reporting Standard 7 Financial Instruments:

IFRS 9 FINANCIAL INSTRUMENTS (2014) INTERNATIONAL FINANCIAL REPORTING BULLETIN 2014/12

INTERNATIONAL FINANCIAL REPORTING BULLETIN 2014/12") IFRS 9 FINANCIAL INSTRUMENTS (2014) INTERNATIONAL FINANCIAL REPORTING BULLETIN 2014/12 Summary On 24 July 2014, the International Accounting Standards Board (IASB) completed its project on financial instruments

IFRS 9 FINANCIAL INSTRUMENTS (2014) INTERNATIONAL FINANCIAL REPORTING BULLETIN 2014/12 Summary On 24 July 2014, the International Accounting Standards Board (IASB) completed its project on financial instruments

different periods sometimes referred to as an accounting mismatch

Matching the change in FV of the hedging instrument and the hedged item in profit or loss for the same period Hedge accounting is only an issue when normal accounting would put the two fair value changes

Matching the change in FV of the hedging instrument and the hedged item in profit or loss for the same period Hedge accounting is only an issue when normal accounting would put the two fair value changes

IFRS Practice Issues for Banks: Loan acquisition accounting

IFRS Practice Issues for Banks: Loan acquisition accounting August 2011 kpmg.com/ifrs Contents 1. Addressing complexity in loan acquisitions 1 2. When should the acquisition of a loan be recognised in

IFRS Practice Issues for Banks: Loan acquisition accounting August 2011 kpmg.com/ifrs Contents 1. Addressing complexity in loan acquisitions 1 2. When should the acquisition of a loan be recognised in

DECISION ON THE METHOD OF VALUATION OF ASSETS FOR INSURANCE COMPANIES

Pursuant to Articles 89 and 177 item 4 of the Law on Insurance (Official Gazette of the Republic of Montenegro 78/06 and 19/07) and Article 6 of the Rulebook on the Manner of Determining and Monitoring

Pursuant to Articles 89 and 177 item 4 of the Law on Insurance (Official Gazette of the Republic of Montenegro 78/06 and 19/07) and Article 6 of the Rulebook on the Manner of Determining and Monitoring

Financial Instruments: Recognition and Measurement

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 39 Financial Instruments: Recognition and Measurement This version of the Statutory Board Financial Reporting Standard does not include amendments that

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 39 Financial Instruments: Recognition and Measurement This version of the Statutory Board Financial Reporting Standard does not include amendments that

HKAS 39 Financial Instruments: Recognition and Measurement

1 Hong Kong Financial Reporting Standards: HKAS 39 Financial Instruments: Recognition and Measurement (Relevant to PBE Paper I Financial Reporting) Lindy W W Yau, ACA, FCCA, FAIA, FCPA and Morris Y M Kwok,

1 Hong Kong Financial Reporting Standards: HKAS 39 Financial Instruments: Recognition and Measurement (Relevant to PBE Paper I Financial Reporting) Lindy W W Yau, ACA, FCCA, FAIA, FCPA and Morris Y M Kwok,

FINANCE POLICY POLICY NO F.6 SIGNIFICANT ACCOUNTING POLICIES. FILE NUMBER FIN 2 ADOPTION DATE 13 June 2002

POLICY NO F.6 POLICY SUBJECT FILE NUMBER FIN 2 ADOPTION DATE 13 June 2002 Shire of Toodyay Policy Manual FINANCE POLICY SIGNIFICANT ACCOUNTING POLICIES LAST REVIEW 22 July 2014 (Council Resolution No 201/07/14)

POLICY NO F.6 POLICY SUBJECT FILE NUMBER FIN 2 ADOPTION DATE 13 June 2002 Shire of Toodyay Policy Manual FINANCE POLICY SIGNIFICANT ACCOUNTING POLICIES LAST REVIEW 22 July 2014 (Council Resolution No 201/07/14)

IFRS Seminar for Regulators Accounting and Regulatory issues

REPARIS A REGIONAL PROGRAM IFRS Seminar for Regulators Accounting and Regulatory issues GDLN Session 2: IAS 39 Financial Instruments: Recognition and Measurement Hedge accounting THE ROAD TO EUROPE: PROGRAM

REPARIS A REGIONAL PROGRAM IFRS Seminar for Regulators Accounting and Regulatory issues GDLN Session 2: IAS 39 Financial Instruments: Recognition and Measurement Hedge accounting THE ROAD TO EUROPE: PROGRAM

Residual carrying amounts and expected useful lives are reviewed at each reporting date and adjusted if necessary.

87 Accounting Policies Intangible assets a) Goodwill Goodwill represents the excess of the cost of an acquisition over the fair value of identifiable net assets and liabilities of the acquired company

87 Accounting Policies Intangible assets a) Goodwill Goodwill represents the excess of the cost of an acquisition over the fair value of identifiable net assets and liabilities of the acquired company

FUBON LIFE INSURANCE CO., LTD. AND SUBSIDIARIES. CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS JUNE 30, 2013 and 2012

FUBON LIFE INSURANCE CO., LTD. AND SUBSIDIARIES CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS JUNE 30, 2013 and 2012 (with Independent Auditors Report Thereon) Address: 14F, No. 108, Sec. 1, Tun

FUBON LIFE INSURANCE CO., LTD. AND SUBSIDIARIES CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS JUNE 30, 2013 and 2012 (with Independent Auditors Report Thereon) Address: 14F, No. 108, Sec. 1, Tun

Technical Accounting Alert

TA ALERT 2009-12 JULY 2009 Technical Accounting Alert Impairment of available-for-sale equity investments Issue This alert provides guidance on the application of IAS 39's impairment rules to investments

TA ALERT 2009-12 JULY 2009 Technical Accounting Alert Impairment of available-for-sale equity investments Issue This alert provides guidance on the application of IAS 39's impairment rules to investments

Area Standard AIFRS impact Management action First time Adoption of Australian Equivalents to IFRS

First time Adoption of Australian Equivalents to IFRS AASB 1 An entity s first Australian-equivalents-to-IFRS (AIFRS) financial report applies for reporting periods beginning on or after 1 January 2005

First time Adoption of Australian Equivalents to IFRS AASB 1 An entity s first Australian-equivalents-to-IFRS (AIFRS) financial report applies for reporting periods beginning on or after 1 January 2005

NOTES TO THE FINANCIAL STATEMENTS

1. Principal activities The Company is an investment holding company and its subsidiaries are principally engaged in the provision of banking and related financial services in Hong Kong. The Company is

1. Principal activities The Company is an investment holding company and its subsidiaries are principally engaged in the provision of banking and related financial services in Hong Kong. The Company is

SHIRE OF CARNARVON POLICY

SHIRE OF CARNARVON POLICY POLICY NO C010 POLICY SIGNIFICANT ACCOUNTING POLICIES RESPONSIBLE DIRECTORATE CORPORATE COUNCIL ADOPTION Date: 27.5.14 Resolution No. FC 5/5/14 REVIEWED/MODIFIED Date: Resolution

SHIRE OF CARNARVON POLICY POLICY NO C010 POLICY SIGNIFICANT ACCOUNTING POLICIES RESPONSIBLE DIRECTORATE CORPORATE COUNCIL ADOPTION Date: 27.5.14 Resolution No. FC 5/5/14 REVIEWED/MODIFIED Date: Resolution

BOM/BSD 13/November 2004 BANK OF MAURITIUS. Guideline on Credit Impairment Measurement and Income Recognition

BOM/BSD 13/November 2004 BANK OF MAURITIUS Guideline on Credit Impairment Measurement and Income Recognition November 2004 Revised June 2005 Contents 1.0 INTRODUCTION...1 2.0 INTERPRETATION...1 3.0 IMPAIRMENT

BOM/BSD 13/November 2004 BANK OF MAURITIUS Guideline on Credit Impairment Measurement and Income Recognition November 2004 Revised June 2005 Contents 1.0 INTRODUCTION...1 2.0 INTERPRETATION...1 3.0 IMPAIRMENT

Financial Instruments

Compiled AASB Standard AASB 9 Financial Instruments This compiled Standard applies to annual reporting periods beginning on or after 1 January 2015. Early application is permitted. It incorporates relevant

Compiled AASB Standard AASB 9 Financial Instruments This compiled Standard applies to annual reporting periods beginning on or after 1 January 2015. Early application is permitted. It incorporates relevant

IPSAS 29 FINANCIAL INSTRUMENTS: RECOGNITION AND MEASUREMENT

IPSAS 29 FINANCIAL INSTRUMENTS: RECOGNITION AND MEASUREMENT Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 39,

IPSAS 29 FINANCIAL INSTRUMENTS: RECOGNITION AND MEASUREMENT Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 39,

Derivatives, Measurement and Hedge Accounting

Derivatives, Measurement and Hedge Accounting IAS 39 11 June 2008 Contents Derivatives and embedded derivatives Definition Sample of products Accounting treatment Measurement Active market VS Inactive

Derivatives, Measurement and Hedge Accounting IAS 39 11 June 2008 Contents Derivatives and embedded derivatives Definition Sample of products Accounting treatment Measurement Active market VS Inactive

POLICY MANUAL. Financial Management Significant Accounting Policies (July 2015)

") POLICY 1. Objective To adopt Full Accrual Accounting and all other applicable Accounting Standards. 2. Local Government Reference Local Government Act 1995 Local Government (Financial Management) Regulations

POLICY 1. Objective To adopt Full Accrual Accounting and all other applicable Accounting Standards. 2. Local Government Reference Local Government Act 1995 Local Government (Financial Management) Regulations

0175/00014699/en Half-Yearly Financial Report GLOBAL DIGITAL SERVICES PLC STC. Correction To:0175/00014529

Correction To:0175/00014529 0175/00014699/en Half-Yearly Financial Report GLOBAL DIGITAL SERVICES PLC STC Corrected Consolidated Half Year Financial Report 9th February 2016 Global Digital Services PLC

Correction To:0175/00014529 0175/00014699/en Half-Yearly Financial Report GLOBAL DIGITAL SERVICES PLC STC Corrected Consolidated Half Year Financial Report 9th February 2016 Global Digital Services PLC

FINANCIAL STATEMENTS

ASIA ASSET FINANCE PLC FINANCIAL STATEMENTS 31 MARCH 2013 STATEMENT OF COMPREHENSIVE INCOME Note 2013 2012 Income 626,800,329 435,341,934 Interest Income 4 589,316,038 378,483,748 Interest Expense 5

ASIA ASSET FINANCE PLC FINANCIAL STATEMENTS 31 MARCH 2013 STATEMENT OF COMPREHENSIVE INCOME Note 2013 2012 Income 626,800,329 435,341,934 Interest Income 4 589,316,038 378,483,748 Interest Expense 5

Assurance and accounting A Guide to Financial Instruments for Private

june 2011 www.bdo.ca Assurance and accounting A Guide to Financial Instruments for Private Enterprises and Private Sector t-for-profit Organizations For many entities adopting the Accounting Standards

june 2011 www.bdo.ca Assurance and accounting A Guide to Financial Instruments for Private Enterprises and Private Sector t-for-profit Organizations For many entities adopting the Accounting Standards

Professional Level Essentials Module, Paper P2 (IRL)

") Answers Professional Level Essentials Module, Paper P2 (IRL) Corporate Reporting (Irish) June 2011 Answers 1 (a) (i) Under the Companies Act 1996 and European Communities (Companies: Group Accounts) Regulations,

Answers Professional Level Essentials Module, Paper P2 (IRL) Corporate Reporting (Irish) June 2011 Answers 1 (a) (i) Under the Companies Act 1996 and European Communities (Companies: Group Accounts) Regulations,

Note 2 SIGNIFICANT ACCOUNTING

Note 2 SIGNIFICANT ACCOUNTING POLICIES BASIS FOR THE PREPARATION OF THE FINANCIAL STATEMENTS The consolidated financial statements have been prepared in accordance with International Financial Reporting

Note 2 SIGNIFICANT ACCOUNTING POLICIES BASIS FOR THE PREPARATION OF THE FINANCIAL STATEMENTS The consolidated financial statements have been prepared in accordance with International Financial Reporting

TCS Financial Solutions Australia (Holdings) Pty Limited. ABN 61 003 653 549 Financial Statements for the year ended 31 March 2015

Pty Limited. ABN 61 003 653 549 Financial Statements for the year ended 31 March 2015") TCS Financial Solutions Australia (Holdings) Pty Limited ABN 61 003 653 549 Financial Statements for the year ended 31 March 2015 Contents Page Directors' report 3 Statement of profit or loss and other

TCS Financial Solutions Australia (Holdings) Pty Limited ABN 61 003 653 549 Financial Statements for the year ended 31 March 2015 Contents Page Directors' report 3 Statement of profit or loss and other

Defining Issues. FASB Redeliberates Impairment of Debt Securities and Measurement of Credit Losses. August 2014, No. 14-37.

Defining Issues August 2014, No. 14-37 FASB Redeliberates Impairment of Debt Securities and Measurement of Credit Losses At its August 13 meeting, the FASB continued redeliberations on its proposed standard

Defining Issues August 2014, No. 14-37 FASB Redeliberates Impairment of Debt Securities and Measurement of Credit Losses At its August 13 meeting, the FASB continued redeliberations on its proposed standard

National Mortgage Company Refinancing Credit Organisation CJSC. Financial Statements for the year ended 31 December 2014

National Mortgage Company Refinancing Credit Organisation CJSC Financial Statements for the year ended 31 December Contents Independent Auditors Report... 3 Statement of profit or loss and other comprehensive

National Mortgage Company Refinancing Credit Organisation CJSC Financial Statements for the year ended 31 December Contents Independent Auditors Report... 3 Statement of profit or loss and other comprehensive

International Accounting Standard 28 Investments in Associates

International Accounting Standard 28 Investments in Associates Scope 1 This Standard shall be applied in accounting for investments in associates. However, it does not apply to investments in associates

International Accounting Standard 28 Investments in Associates Scope 1 This Standard shall be applied in accounting for investments in associates. However, it does not apply to investments in associates

STATEMENT OF COMPLIANCE AND BASIS OF MEASUREMENT

Accounting policies REPORTING ENTITY The Waikato Regional Council is a territorial local authority governed by the Local Government Act 2002, and is domiciled in New Zealand. The main purpose of prospective

Accounting policies REPORTING ENTITY The Waikato Regional Council is a territorial local authority governed by the Local Government Act 2002, and is domiciled in New Zealand. The main purpose of prospective

Microfinance Organization Credo LLC Financial statements

LLC Financial statements Year ended 31 December 2015, together with independent auditor s report Financial statements Contents Independent auditors report Financial statements Statement of financial position...

LLC Financial statements Year ended 31 December 2015, together with independent auditor s report Financial statements Contents Independent auditors report Financial statements Statement of financial position...

Financial Instruments: Disclosures

Compiled Accounting Standard AASB 7 Financial Instruments: Disclosures This compiled Standard applies to annual reporting periods beginning on or after 1 July 2007 but before 1 January 2009 that end on

Compiled Accounting Standard AASB 7 Financial Instruments: Disclosures This compiled Standard applies to annual reporting periods beginning on or after 1 July 2007 but before 1 January 2009 that end on

Accounting Standard (AS) 30 Financial Instruments: Recognition and Measurement

30 Financial Instruments: Recognition and Measurement") Accounting Standard (AS) 30 Financial Instruments: Recognition and Measurement Limited Revisions to AS 2, AS 11 (revised 2003), AS 21, AS 23, AS 26, AS 27, AS 28 and AS 29 Issued by The Institute of Chartered

Accounting Standard (AS) 30 Financial Instruments: Recognition and Measurement Limited Revisions to AS 2, AS 11 (revised 2003), AS 21, AS 23, AS 26, AS 27, AS 28 and AS 29 Issued by The Institute of Chartered

128 SU 3: Financial Accounting I

128 SU 3: Financial Accounting I 3.5 FINANCIAL ASSETS AND LIABILITIES Definitions 1. Financial assets include cash, equity instruments of other entities (e.g., preference shares), contract rights to receive

128 SU 3: Financial Accounting I 3.5 FINANCIAL ASSETS AND LIABILITIES Definitions 1. Financial assets include cash, equity instruments of other entities (e.g., preference shares), contract rights to receive

Financial Instruments: Recognition and Measurement

Compiled AASB Standard AASB 139 Financial Instruments: Recognition and Measurement This compiled Standard applies to annual reporting periods beginning on or after 1 January 2011 but before 1 January 2013.

Compiled AASB Standard AASB 139 Financial Instruments: Recognition and Measurement This compiled Standard applies to annual reporting periods beginning on or after 1 January 2011 but before 1 January 2013.

Acerinox, S.A. and Subsidiaries. Consolidated Annual Accounts 31 December 2014. Consolidated Directors' Report 2014. (With Auditors Report Thereon)

") Acerinox, S.A. and Subsidiaries Consolidated Annual Accounts 31 December 2014 Consolidated Directors' Report 2014 (With Auditors Report Thereon) (Free translation from the original in Spanish. In the event

Acerinox, S.A. and Subsidiaries Consolidated Annual Accounts 31 December 2014 Consolidated Directors' Report 2014 (With Auditors Report Thereon) (Free translation from the original in Spanish. In the event

Financial Instruments on Display. Illustrative Disclosures and Guidance on IFRS 7 September 2009

Financial Instruments on Display Illustrative Disclosures and Guidance on IFRS 7 September 2009 Financial Instruments on Display 3 Introduction IFRS 7 Financial Instruments: Disclosures (IFRS 7) is not

Financial Instruments on Display Illustrative Disclosures and Guidance on IFRS 7 September 2009 Financial Instruments on Display 3 Introduction IFRS 7 Financial Instruments: Disclosures (IFRS 7) is not

III. Loan Loss Provisioning

III. Loan Loss Provisioning 35 35 Agenda» Loan Loss Provisioning a key to a true and fair view in bank accounting and prudent banking supervision» Incurred Loss Model of IAS 39 The Model Shortcomings»

III. Loan Loss Provisioning 35 35 Agenda» Loan Loss Provisioning a key to a true and fair view in bank accounting and prudent banking supervision» Incurred Loss Model of IAS 39 The Model Shortcomings»

Accounting and Reporting Policy FRS 102. Staff Education Note 16 Financing transactions

Accounting and Reporting Policy FRS 102 Staff Education Note 16 Financing transactions Disclaimer This Education Note has been prepared by FRC staff for the convenience of users of FRS 102 The Financial

Accounting and Reporting Policy FRS 102 Staff Education Note 16 Financing transactions Disclaimer This Education Note has been prepared by FRC staff for the convenience of users of FRS 102 The Financial

Ind AS 32 and Ind AS 109 - Financial Instruments Classification, recognition and measurement. June 2015

Ind AS 32 and Ind AS 109 - Financial Instruments Classification, recognition and measurement June 2015 Contents Executive summary Standards dealing with financial instruments under Ind AS Financial instruments

Ind AS 32 and Ind AS 109 - Financial Instruments Classification, recognition and measurement June 2015 Contents Executive summary Standards dealing with financial instruments under Ind AS Financial instruments

DRAFT DRAFT GUIDANCE: CORPORATION TAX TREATMENT OF INTEREST-FREE LOANS AND OTHER NON- MARKET LOANS

DRAFT GUIDANCE: CORPORATION TAX TREATMENT OF INTEREST-FREE LOANS AND OTHER NON- MARKET LOANS Terminology There currently exists a suite of accounting standards in the UK. Subject to certain restrictions

DRAFT GUIDANCE: CORPORATION TAX TREATMENT OF INTEREST-FREE LOANS AND OTHER NON- MARKET LOANS Terminology There currently exists a suite of accounting standards in the UK. Subject to certain restrictions

International Accounting Standard 32 Financial Instruments: Presentation

EC staff consolidated version as of 21 June 2012, EN EU IAS 32 FOR INFORMATION PURPOSES ONLY International Accounting Standard 32 Financial Instruments: Presentation Objective 1 [Deleted] 2 The objective

EC staff consolidated version as of 21 June 2012, EN EU IAS 32 FOR INFORMATION PURPOSES ONLY International Accounting Standard 32 Financial Instruments: Presentation Objective 1 [Deleted] 2 The objective

How To Write A Budget For The Council

FP5 SIGNIFICANT ACCOUNTING POLICIES - BUDGET Adopted: Audit Committee 20 June 2013 Committee Decision No. 10 Audit Committee Minutes endorsed by Council OMC 18 July 2013 Council Decision No. 2753 AASB

FP5 SIGNIFICANT ACCOUNTING POLICIES - BUDGET Adopted: Audit Committee 20 June 2013 Committee Decision No. 10 Audit Committee Minutes endorsed by Council OMC 18 July 2013 Council Decision No. 2753 AASB

EXPLANATORY NOTES. 1. Summary of accounting policies

1. Summary of accounting policies Reporting Entity Taranaki Regional Council is a regional local authority governed by the Local Government Act 2002. The Taranaki Regional Council group (TRC) consists

1. Summary of accounting policies Reporting Entity Taranaki Regional Council is a regional local authority governed by the Local Government Act 2002. The Taranaki Regional Council group (TRC) consists

Kilikia Universal Credit Organization LLC. Financial Statements for the year ended 31 December 2014

Financial Statements for the year ended 31 December Contents Independent Auditors Report... 3 Statement of profit or loss and other comprehensive income... 4 Statement of financial position... 5 Statement

Financial Statements for the year ended 31 December Contents Independent Auditors Report... 3 Statement of profit or loss and other comprehensive income... 4 Statement of financial position... 5 Statement

Investments in Associates

Indian Accounting Standard (Ind AS) 28 Investments in Associates Investments in Associates Contents Paragraphs SCOPE 1 DEFINITIONS 2-12 Significant Influence 6-10 Equity Method 11-12 APPLICATION OF THE

Indian Accounting Standard (Ind AS) 28 Investments in Associates Investments in Associates Contents Paragraphs SCOPE 1 DEFINITIONS 2-12 Significant Influence 6-10 Equity Method 11-12 APPLICATION OF THE

INFORMATION FOR OBSERVERS

30 Cannon Street, London EC4M 6XH, United Kingdom Tel: +44 (0)20 7246 6410 Fax: +44 (0)20 7246 6411 E-mail: iasb@iasb.org Website: www.iasb.org International Accounting Standards Board This document is

30 Cannon Street, London EC4M 6XH, United Kingdom Tel: +44 (0)20 7246 6410 Fax: +44 (0)20 7246 6411 E-mail: iasb@iasb.org Website: www.iasb.org International Accounting Standards Board This document is

The Wawanesa Life Insurance Company. Financial Statements December 31, 2011

The Wawanesa Life Insurance Company Financial Statements February 21, 2012 Appointed Actuary s Report To the Shareholder and Policyholders of The Wawanesa Life Insurance Company I have valued the insurance

The Wawanesa Life Insurance Company Financial Statements February 21, 2012 Appointed Actuary s Report To the Shareholder and Policyholders of The Wawanesa Life Insurance Company I have valued the insurance

How To Account For A Church In A Hedgebook

Diocesan Finance & Registrar s Conference July 2005 Michael Codling 1 Overview Background First time adoption Investment properties Property, Plant & Equipment Financial instruments main principles loans

Diocesan Finance & Registrar s Conference July 2005 Michael Codling 1 Overview Background First time adoption Investment properties Property, Plant & Equipment Financial instruments main principles loans

Dumfries Mutual Insurance Company Financial Statements For the year ended December 31, 2010

Dumfries Mutual Insurance Company Financial Statements For the year ended December 31, 2010 Contents Independent Auditors' Report 2 Financial Statements Balance Sheet 3 Statement of Operations and Unappropriated

Dumfries Mutual Insurance Company Financial Statements For the year ended December 31, 2010 Contents Independent Auditors' Report 2 Financial Statements Balance Sheet 3 Statement of Operations and Unappropriated

ASPE AT A GLANCE Section 3856 Financial Instruments

ASPE AT A GLANCE Section 3856 Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial instruments

ASPE AT A GLANCE Section 3856 Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial instruments

Introduction 1. Executive summary 2

The KPMG Guide: FRS 139, Financial Instruments: Recognition and Measurement i Contents Introduction 1 Executive summary 2 1. Scope of FRS 139 1.1 Financial instruments outside the scope of FRS 139 3 1.2

The KPMG Guide: FRS 139, Financial Instruments: Recognition and Measurement i Contents Introduction 1 Executive summary 2 1. Scope of FRS 139 1.1 Financial instruments outside the scope of FRS 139 3 1.2

G8 Education Limited ABN: 95 123 828 553. Accounting Policies

G8 Education Limited ABN: 95 123 828 553 Accounting Policies Table of Contents Note 1: Summary of significant accounting policies... 3 (a) Basis of preparation... 3 (b) Principles of consolidation... 3

G8 Education Limited ABN: 95 123 828 553 Accounting Policies Table of Contents Note 1: Summary of significant accounting policies... 3 (a) Basis of preparation... 3 (b) Principles of consolidation... 3

Financial Instruments: Disclosures

STATUTORY BOARD SB-FRS 107 FINANCIAL REPORTING STANDARD Financial Instruments: Disclosures This version of the Statutory Board Financial Reporting Standard does not include amendments that are effective

STATUTORY BOARD SB-FRS 107 FINANCIAL REPORTING STANDARD Financial Instruments: Disclosures This version of the Statutory Board Financial Reporting Standard does not include amendments that are effective

IRAS e-tax Guide INCOME TAX IMPLICATIONS ARISING FROM THE ADOPTION OF FRS 39 FINANCIAL INSTRUMENTS: RECOGNITION & MEASUREMENT

IRAS e-tax Guide INCOME TAX IMPLICATIONS ARISING FROM THE ADOPTION OF FRS 39 FINANCIAL INSTRUMENTS: RECOGNITION & MEASUREMENT Published by Inland Revenue Authority of Singapore Revised on 16 Mar 2015 First

IRAS e-tax Guide INCOME TAX IMPLICATIONS ARISING FROM THE ADOPTION OF FRS 39 FINANCIAL INSTRUMENTS: RECOGNITION & MEASUREMENT Published by Inland Revenue Authority of Singapore Revised on 16 Mar 2015 First

(Amounts in millions of Canadian dollars except for per share amounts and where otherwise stated. All amounts stated in US dollars are in millions.

Notes to the Consolidated Financial Statements (Amounts in millions of Canadian dollars except for per share amounts and where otherwise stated. All amounts stated in US dollars are in millions.) 1. Significant

Notes to the Consolidated Financial Statements (Amounts in millions of Canadian dollars except for per share amounts and where otherwise stated. All amounts stated in US dollars are in millions.) 1. Significant

DBS BANK LTD (Incorporated in Singapore. Registration Number: 196800306E) AND ITS SUBSIDIARIES

AND ITS SUBSIDIARIES") DBS BANK LTD (Incorporated in Singapore. Registration Number: 196800306E) AND ITS SUBSIDIARIES FINANCIAL STATEMENTS For the financial year ended 31 December 2013 Financial Statements Table of Contents

DBS BANK LTD (Incorporated in Singapore. Registration Number: 196800306E) AND ITS SUBSIDIARIES FINANCIAL STATEMENTS For the financial year ended 31 December 2013 Financial Statements Table of Contents

Fundamentals of Financial Instrument. Hedge Accounting. Sajid Shafiq, ACA

Financial Instruments Fundamentals of Financial Instrument De recognition Hedge Accounting Sajid Shafiq, ACA Fundamentals Financial assets, liabilities and Classification of equity instruments ts Financial

Financial Instruments Fundamentals of Financial Instrument De recognition Hedge Accounting Sajid Shafiq, ACA Fundamentals Financial assets, liabilities and Classification of equity instruments ts Financial

TREASURER S DIRECTIONS ACCOUNTING ASSETS Section A2.7 : Receivables

TREASURER S DIRECTIONS ACCOUNTING ASSETS Section A2.7 : Receivables STATEMENT OF INTENT Agency receivables require efficient and effective management as they represent future claims to cash. This Section

TREASURER S DIRECTIONS ACCOUNTING ASSETS Section A2.7 : Receivables STATEMENT OF INTENT Agency receivables require efficient and effective management as they represent future claims to cash. This Section

EXPLOREX RESOURCES INC.

EXPLOREX RESOURCES INC. INTERIM FINANCIAL STATEMENTS (Expressed in Canadian Dollars) SEPTEMBER 30, 2015 (Unaudited Prepared by Management) NOTICE OF NO AUDITOR REVIEW OF CONSOLIDATED INTERIM FINANCIAL

EXPLOREX RESOURCES INC. INTERIM FINANCIAL STATEMENTS (Expressed in Canadian Dollars) SEPTEMBER 30, 2015 (Unaudited Prepared by Management) NOTICE OF NO AUDITOR REVIEW OF CONSOLIDATED INTERIM FINANCIAL

Practical guide to IFRS

pwc.com/ifrs Practical guide to IFRS IASB completes first phase of IFRS 9 accounting for financial instruments At a glance The IASB completed part of the first phase of this project on financial assets

pwc.com/ifrs Practical guide to IFRS IASB completes first phase of IFRS 9 accounting for financial instruments At a glance The IASB completed part of the first phase of this project on financial assets

ANNUAL FINANCIAL RESULTS FOR THE YEAR ENDED 31 JULY 2014 FONTERRA ANNUAL FINANCIAL RESULTS 2014 A

ANNUAL FINANCIAL RESULTS FOR THE YEAR ENDED 31 JULY 2014 FONTERRA ANNUAL FINANCIAL RESULTS 2014 A CONTENTS DIRECTORS STATEMENT 1 INCOME STATEMENT 2 STATEMENT OF COMPREHENSIVE INCOME 3 STATEMENT OF FINANCIAL

ANNUAL FINANCIAL RESULTS FOR THE YEAR ENDED 31 JULY 2014 FONTERRA ANNUAL FINANCIAL RESULTS 2014 A CONTENTS DIRECTORS STATEMENT 1 INCOME STATEMENT 2 STATEMENT OF COMPREHENSIVE INCOME 3 STATEMENT OF FINANCIAL

Consolidated financial statements at 30 June 2014

- 2 - CONTENTS CONSOLIDATED FINANCIAL STATEMENTS 4 PROFIT AND LOSS ACCOUNT FOR THE FIRST HALF OF 2014 4 STATEMENT OF NET INCOME AND CHANGES IN ASSETS AND LIABILITIES RECOGNISED 5 DIRECTLY IN EQUITY BALANCE

- 2 - CONTENTS CONSOLIDATED FINANCIAL STATEMENTS 4 PROFIT AND LOSS ACCOUNT FOR THE FIRST HALF OF 2014 4 STATEMENT OF NET INCOME AND CHANGES IN ASSETS AND LIABILITIES RECOGNISED 5 DIRECTLY IN EQUITY BALANCE

SEF International Universal Credit Organization LLC. Financial Statements for the Year Ended 31 December 2009

SEF International Universal Credit Organization LLC Financial Statements for the Year Ended 31 December Contents Independent Auditors Report... 3 Statement of comprehensive income... 5 Statement of financial

SEF International Universal Credit Organization LLC Financial Statements for the Year Ended 31 December Contents Independent Auditors Report... 3 Statement of comprehensive income... 5 Statement of financial

IFRS 9: A Complete Package for Investors

Investor Perspectives July 2014 IFRS 9: A Complete Package for Investors Sue Lloyd, a member of the IASB, discusses the new accounting standard for financial instruments. IFRS 9 completes our main response

Investor Perspectives July 2014 IFRS 9: A Complete Package for Investors Sue Lloyd, a member of the IASB, discusses the new accounting standard for financial instruments. IFRS 9 completes our main response

International Financial Reporting Standard 7 Financial Instruments: Disclosures

EC staff consolidated version as of 21 June 2012, EN EU IFRS 7 FOR INFORMATION PURPOSES ONLY International Financial Reporting Standard 7 Financial Instruments: Disclosures Objective 1 The objective of

EC staff consolidated version as of 21 June 2012, EN EU IFRS 7 FOR INFORMATION PURPOSES ONLY International Financial Reporting Standard 7 Financial Instruments: Disclosures Objective 1 The objective of

ANNUAL FINANCIAL RESULTS

ANNUAL FINANCIAL RESULTS For the year ended 31 July 2013 ANNUAL FINANCIAL RESULTS 2013 FONTERRA CO-OPERATIVE GROUP LIMITED Contents: DIRECTORS STATEMENT... 1 INCOME STATEMENT... 2 STATEMENT OF COMPREHENSIVE

ANNUAL FINANCIAL RESULTS For the year ended 31 July 2013 ANNUAL FINANCIAL RESULTS 2013 FONTERRA CO-OPERATIVE GROUP LIMITED Contents: DIRECTORS STATEMENT... 1 INCOME STATEMENT... 2 STATEMENT OF COMPREHENSIVE

IFRS AT A GLANCE IAS 39 Financial Instruments: Recognition and Measurement

IFRS AT A GLANCE IAS 39 Financial Instruments: Recognition and Measurement As at 1 July 2015 IAS 39 Financial Instruments: Recognition and Measurement Page 1 of 4 Also refer: IFRIC 9 Reassessment of Embedded

IFRS AT A GLANCE IAS 39 Financial Instruments: Recognition and Measurement As at 1 July 2015 IAS 39 Financial Instruments: Recognition and Measurement Page 1 of 4 Also refer: IFRIC 9 Reassessment of Embedded

Updated statement of financial position

ASX Announcement By e-lodgement ASX Code: CXZ 26 August 2014 Updated statement of financial position Attached is an updated statement of financial position based on the actual amount of funds raised pursuant

ASX Announcement By e-lodgement ASX Code: CXZ 26 August 2014 Updated statement of financial position Attached is an updated statement of financial position based on the actual amount of funds raised pursuant

ALTICE FINANCING S.A.

Financial statements as at and for the year ended December 31, 2013 and report of the Réviseur d'entreprises Agréé 3, boulevard Royal L - 2449 LUXEMBOURG R.C.S. Luxembourg: B171.162 Issued capital: EUR

Financial statements as at and for the year ended December 31, 2013 and report of the Réviseur d'entreprises Agréé 3, boulevard Royal L - 2449 LUXEMBOURG R.C.S. Luxembourg: B171.162 Issued capital: EUR

Financial Statements of NATIONAL BUILDING SOCIETY OF CAYMAN. March 31, 2015

CAYMAN ISLANDS Supplement No. 1 published with Extraordinary Gazette No. 61 dated 14 August 2015. Financial Statements of NATIONAL BUILDING SOCIETY OF CAYMAN Financial Statements of NATIONAL BUILDING SOCIETY

CAYMAN ISLANDS Supplement No. 1 published with Extraordinary Gazette No. 61 dated 14 August 2015. Financial Statements of NATIONAL BUILDING SOCIETY OF CAYMAN Financial Statements of NATIONAL BUILDING SOCIETY

Guidance on Implementing Financial Instruments: Recognition and Measurement

STATUTORY BOARD SB-FRS 39 FINANCIAL REPORTING STANDARD Guidance on Implementing Financial Instruments: Recognition and Measurement CONTENTS SECTION A SCOPE A.1 Practice of settling net: forward contract

STATUTORY BOARD SB-FRS 39 FINANCIAL REPORTING STANDARD Guidance on Implementing Financial Instruments: Recognition and Measurement CONTENTS SECTION A SCOPE A.1 Practice of settling net: forward contract

Notes to the consolidated financial statements continued

144 www.ocadogroup.com Stock Code: OCDO to the consolidated financial statements continued 4.5 instruments Accounting policies assets and financial liabilities are recognised on the balance sheet when

144 www.ocadogroup.com Stock Code: OCDO to the consolidated financial statements continued 4.5 instruments Accounting policies assets and financial liabilities are recognised on the balance sheet when

Financial Instruments A Chief Financial Officer's guide to avoiding the traps

Financial Instruments A Chief Financial Officer's guide to avoiding the traps An introduction to IAS 39 Financial Instruments: Recognition and Measurement April 2009 Contents Page 1 Introduction 1 2 Scope

Financial Instruments A Chief Financial Officer's guide to avoiding the traps An introduction to IAS 39 Financial Instruments: Recognition and Measurement April 2009 Contents Page 1 Introduction 1 2 Scope

Practical guide to IFRS

pwc.com/ifrs Practical guide to IFRS Financial reporting considerations arising from current market conditions in Europe Background There continue to be significant economic concerns in some European countries

pwc.com/ifrs Practical guide to IFRS Financial reporting considerations arising from current market conditions in Europe Background There continue to be significant economic concerns in some European countries

Financial Instruments: Recognition and Measurement

HKAS 39 Revised July November 2014 Hong Kong Accounting Standard 39 Financial Instruments: Recognition and Measurement HKAS 39 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants

HKAS 39 Revised July November 2014 Hong Kong Accounting Standard 39 Financial Instruments: Recognition and Measurement HKAS 39 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants

BetaShares Geared U.S. Equity Fund - Currency Hedged (hedge fund) ASX code: GGUS

ASX code: GGUS") BetaShares Geared U.S. Equity Fund - Currency Hedged (hedge fund) ASX code: GGUS ARSN 602 666 615 Annual Financial Report for the period 10 November 2014 to 30 June 2015 BetaShares Geared U.S. Equity Fund

BetaShares Geared U.S. Equity Fund - Currency Hedged (hedge fund) ASX code: GGUS ARSN 602 666 615 Annual Financial Report for the period 10 November 2014 to 30 June 2015 BetaShares Geared U.S. Equity Fund

IBM Finans Norge AS. Condensed Interim Financial Statements. 31 March 2015

Condensed Interim Financial Statements Condensed Interim Financial Statements For the Quarter Ended Contents Page Condensed Interim Statement of Comprehensive Income 2 Condensed Interim Statement of Financial

Condensed Interim Financial Statements Condensed Interim Financial Statements For the Quarter Ended Contents Page Condensed Interim Statement of Comprehensive Income 2 Condensed Interim Statement of Financial

[7] Accounting policies

![[7] Accounting policies](/thumbs/39/20265557.jpg "[7] Accounting policies") 121 [7] Accounting policies The Group financial statements have been prepared under the historical cost convention, with the exception of derivative financial instruments, available-for-sale financial

121 [7] Accounting policies The Group financial statements have been prepared under the historical cost convention, with the exception of derivative financial instruments, available-for-sale financial

Financial Instruments: Recognition and Measurement

International Public Sector Accounting Standards Board IPSAS 29 January 2010 Financial Instruments: Recognition and Measurement International Public Sector Accounting Standards Board International Federation

International Public Sector Accounting Standards Board IPSAS 29 January 2010 Financial Instruments: Recognition and Measurement International Public Sector Accounting Standards Board International Federation

AO UniCredit Bank. Consolidated Financial Statements Year ended 31 December 2014

AO UniCredit Bank Consolidated Financial Statements Year ended 31 December 2014 CONTENTS Page STATEMENT OF MANAGEMENT S RESPONSIBILITIES FOR THE PREPARATION AND APPROVAL OF THE CONSOLIDATED FINANCIAL STATEMENTS

AO UniCredit Bank Consolidated Financial Statements Year ended 31 December 2014 CONTENTS Page STATEMENT OF MANAGEMENT S RESPONSIBILITIES FOR THE PREPARATION AND APPROVAL OF THE CONSOLIDATED FINANCIAL STATEMENTS