How To Let A Small Group Plan In Ohio Choose To Choose To Get A Premium For A Health Plan

|

|

|

- Raymond Bishop

- 3 years ago

- Views:

Transcription

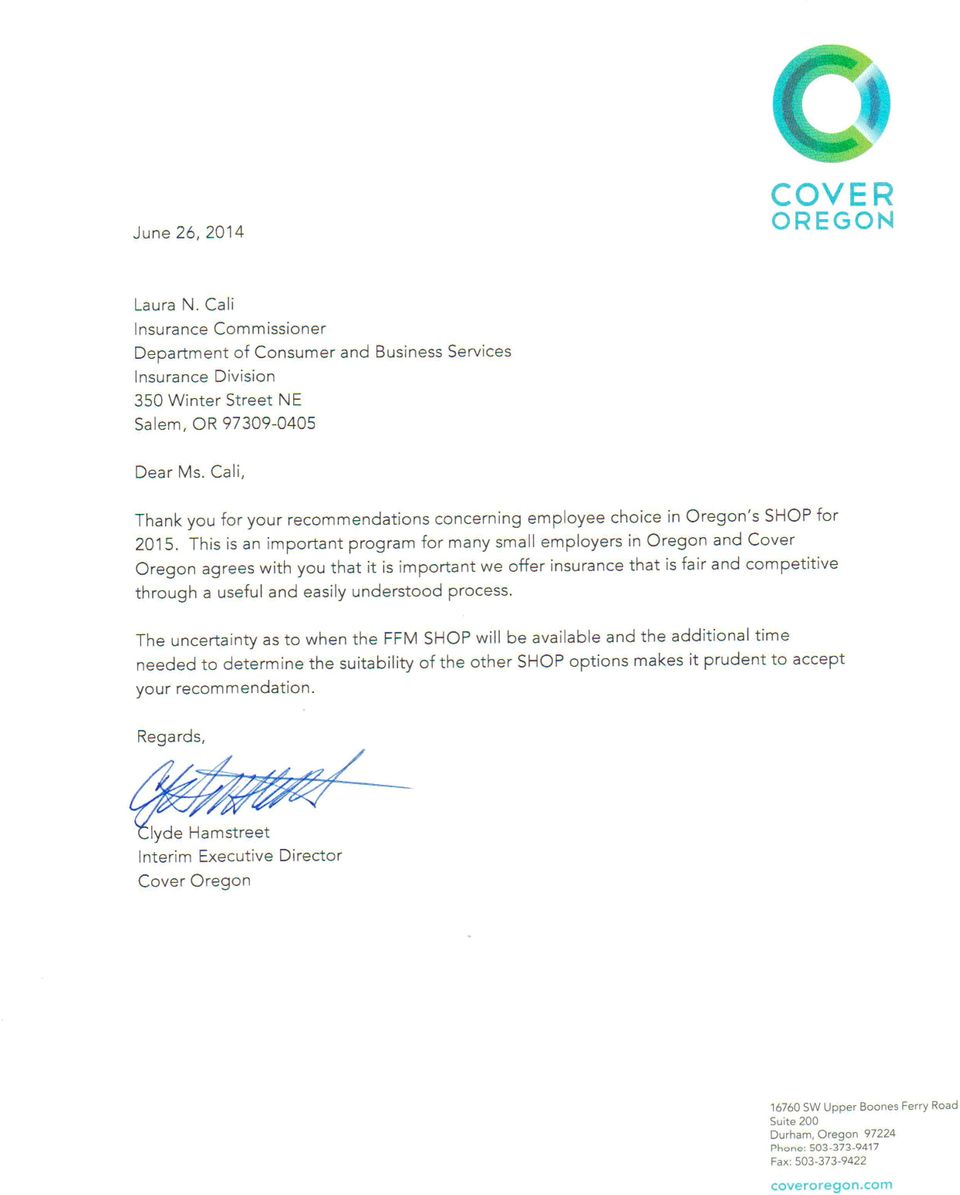

1 June 25, 2014 Mr. Clyde Hamstreet Interim Executive Director Cover Oregon SW Upper Boones Ferry Road, Suite 200 Durham, OR Dear Mr. Hamstreet: The Department of Consumer and Business Services Insurance Division and Cover Oregon share the goal of fostering an insurance market that provides quality, affordable options for consumers. For small employers, this includes providing employees and their dependents with the option of employee choice, and I believe our organizations both remain committed to making this a reality. However, the implementation of employee choice in 2015 will disrupt the small group market and lead to higher premiums. I am writing to you to recommend that Cover Oregon implement a one-year transition to employee choice in its Small Business Health Options Program (SHOP). As you are aware, the Center for Consumer Information and Insurance Oversight (CCIIO) approved Oregon s use of a modified composite rating methodology 1, designed to be applied in conjunction with employee choice and a premium reallocation mechanism to protect against adverse selection. Due to technology challenges, Cover Oregon is currently using a direct enrollment approach to enroll small groups in Qualified Health Plans (QHPs). This approach does not accommodate employee choice but supports Oregon s approved rating methodology, which is key to maintaining stability in small group premiums, facilitating defined employer contributions, and simplifying employee decisions. Without confirmation that the Federally-facilitated SHOP can support composite rating in 2015, offering employee choice in Oregon for 2015 would require use of pure per-member rating. Based on discussions with issuers 2 and consultation with my actuarial staff, an immediate shift from composite to pure per-member rating, combined with employee choice, raises adverse selection concerns and is likely to increase rates and cause significant uncertainty and disruption. Based on our discussions and consultation with issuers, the direct enrollment approach remains the most viable process for enrolling small groups in QHPs during I understand that Cover Oregon is committed to investigating options for a state-based SHOP over the next several months. The continuation of direct enrollment for an additional year will allow for careful consideration of these options and analysis of any resulting modifications to Oregon s rating methodology in consultation with the division, CCIIO, issuers, producers, and small businesses. I recommend that a determination regarding the 2016 SHOP be made no later than December 2014 to provide stakeholders with sufficient 1 See attached brief describing Oregon s small group rating methodology. 2 SHOP issuers consulted include: Atrio Health Plans, Health Republic Insurance Company, Kaiser Foundation Health Plan of the Northwest, Moda Health Plan, Oregon s Health CO-OP, PacificSource Health Plans, Providence Health Plans, and Trillium Community Health Plan. Other small group issuers not participating in SHOP were also contacted, including: Health Net Health Plan of Oregon, LifeWise Health Plan of Oregon, Regence BlueCross BlueShield of Oregon, and UnitedHealthcare Insurance Company.

2 Mr. Clyde Hamstreet June 25, 2014 Page 2 of 2 time to plan and implement any required changes. This critical deliberative process hinges on Cover Oregon s ability to continue direct enrollment in 2015, which will only be possible with a one-year transition to employee choice. In my expert judgment and based on the reasons cited above, it is in the best interest of small employers and their employees and dependents that employee choice be delayed by one year. Given that the division is currently reviewing issuers 2015 rates, a timely response will provide maximum time for the division s actuarial staff to conduct its robust review of small group rates and ensure that they are reasonable for Oregon s small business and their employees and dependents. If you have any questions or wish to discuss this issue further, please do not hesitate to contact me. I appreciate your consideration of my recommendation and look forward to your response. Sincerely, Laura N. Cali Insurance Commissioner Attachment

3 Oregon Small Group Rating for Health Benefit Plans Issued on or after January 1, 2014 The Oregon Small Group Market For many years, Oregon has required that small group premium be determined on a tiered-composite rating basis. This means that all small group employees pay a premium based on the combined rating characteristics of the entire group, with adjustment factors to each employee s premium to include covered dependents. Oregon s tiered-composite rating methodology ensures that premium is equitably distributed across the small group, simplifies employee decisions, facilitates defined employer contributions, and streamlines overall administration of the small group policy. Because tiered-composite rating is also widely used in the large group market, the use of tiered-composite rates also ensures consistent practices across the entire group market. This consistency will become even more important once the small group market expands to groups with up to 100 employees in Implementation of Federal Market Rules The final federal market rules, as published in the Federal Register on February 27, 2013, require that the total premium charged for small group plans issued on or after January 1, 2014 be derived using a per-member rating methodology. This means that the rating factors (age, geographic area, and tobacco use) must be applied to each covered employee and his/her covered dependents to determine an aggregate group premium. For any one family, no more than the three oldest covered children under age 21 can be considered in determining the aggregate premium. The market rules clarify that the per-member rating methodology does not preclude a state from requiring insurers to offer an average rate per enrollee as long as the total group premium equals the aggregate premium derived by the per-member methodology. In the current Oregon small group market, employees pay an average rate, adjusted by tier factors based on the type of coverage purchased (e.g., employee only, employee + spouse, employee + children, and employee + family). To minimize disruption in the small group market in 2014, Oregon will maintain its tiered-composite rating requirement, both inside and outside of its state-based exchange. The following sections outline the required methodology for developing aggregate small group premiums and allocating these premiums to covered employees and their dependents. Development of Aggregate Small Group Premiums As required by 45 CFR (c)(1) and (3), total premium charged to a small group must be developed using a per-member rating methodology. For each covered employee and his/her covered dependents, the premium must be determined as follows: - For each covered adult age 21 or older: Calculate the rate for each person by multiplying the base rate by the applicable age, geographic area, and tobacco use factors. The tobacco use factor must not be applied if the individual enrolls in a tobacco cessation program. - For each covered child age 0 to 20: Calculate the rate for each of the oldest three children by multiplying the base rate by the applicable age, geographic area, and tobacco use factors. The tobacco use factor must not be applied if the individual enrolls in a tobacco cessation program. Age, geographic area, and tobacco use are determined at the time that coverage is issued to the group. The small group s aggregate premium is equal to the sum of the premiums determined for each covered employee and his/her covered dependents. Allocation of Premium to Small Group Members Once the small group s aggregate premium has been calculated, it must be allocated back to covered employees based on the tier factor applicable to each employee s family composition (e.g., employee only, employee + spouse, employee + children, and employee + family). Oregon will require standard tier definitions and factors for all carriers, in and out of the exchange. The standard tier definitions and factors are as follows: - Employee only = Employee + spouse = Employee + children (including all covered children up to age 26) = Employee + family (including spouse and all covered children up to age 26) = 2.85 Note that all children under age 26 are considered to meet the definition of children for employee + family and employee + children tiers. Page 1 of 2

4 The formula to determine the final premium for each employee is as follows: Page 2 of 2 Final employee premium = [Group aggregate premium] / [Weighted employee count] x [Employee s tier factor] For example, consider the following group of employees: - Employee A: Employee + spouse + 2 children = Employee + family - Employee B: Employee + spouse - Employee C: Employee + spouse + 3 children = Employee + family - Employee D: Employee + 4 children = Employee + children - Employee E: Employee only Using the applicable tier factors and family composition of each employee, the tier-factor weighted employee count is calculated as follows: - Employee A: Employee + family = Employee B: Employee + spouse = Employee C: Employee + family = Employee D: Employee + children = Employee E: Employee only = 1.00 Weighted employee count = 2 x x x = To calculate the final monthly premium for each employee, the aggregate small group premium is divided by the weighted employee count and multiplied by each employee s applicable tier factor. Continuing with the example above, and assuming the total monthly premium for the group is $5,275, each employee s monthly premium is calculated as follows: - Employee A: $5,275 / x 2.85 = $1,425 - Employee B: $5,275 / x 2.00 = $1,000 - Employee C: $5,275 / x 2.85 = $1,425 - Employee D: $5,275 / x 1.85 = $925 - Employee E: $5,275 / x 1.00 = $500 Group total = $5,275 Recalculation of Average Monthly Premiums Throughout a small group s policy period, employees may come and go and employees may qualify for special enrollment periods due to various life events. The methodology described above determines an employee s monthly premium based on a census of employees and their covered dependents at the time the group s policy is issued. The average monthly premium for each of the tiers must remain in effect throughout the entire policy period and may not increase or decrease to reflect changes in the small group s census. The average monthly premium must be recalculated annually, based on the census at the time the policy is rated.

5

2016 Individual Health Benefit Plans - Factors Affecting The Cost

Health Insurance Rate Decisions for 2016 Individual Company Average Rate Request Requested Portland Silver 40 year old rate Rate Decision Portland Silver 40 year old rate ATRIO Health Plans 18.4% 292 18.4%

Health Insurance Rate Decisions for 2016 Individual Company Average Rate Request Requested Portland Silver 40 year old rate Rate Decision Portland Silver 40 year old rate ATRIO Health Plans 18.4% 292 18.4%

Oregon Health Insurance Rates

Kate Brown, Secretary of State Gary Blackmer, Director, Audits Division Oregon Secretary of State 1 Oregon Health Insurance Rates Introduction We conducted preliminary work on the Oregon Insurance Division

Kate Brown, Secretary of State Gary Blackmer, Director, Audits Division Oregon Secretary of State 1 Oregon Health Insurance Rates Introduction We conducted preliminary work on the Oregon Insurance Division

Update: Health Insurance Reforms and Rate Review. Health Insurance Reform Requirements for the Group and Individual Insurance Markets

By Katherine Jett Hayes and Taylor Burke Background Update: Health Insurance Reforms and Rate Review The Patient Protection and Affordable Care Act (ACA) included health insurance market reforms designed

By Katherine Jett Hayes and Taylor Burke Background Update: Health Insurance Reforms and Rate Review The Patient Protection and Affordable Care Act (ACA) included health insurance market reforms designed

How To Reform Health Insurance In The United States

Health Insurance Market Rules, Rate Review Final Rule U.S. DEPARTMENT OF HEALTH AND HUMAN SERVICES (HHS) CENTERS for MEDICARE & MEDICAID SERVICES(CMS) Center for Consumer Information and Insurance Oversight

Health Insurance Market Rules, Rate Review Final Rule U.S. DEPARTMENT OF HEALTH AND HUMAN SERVICES (HHS) CENTERS for MEDICARE & MEDICAID SERVICES(CMS) Center for Consumer Information and Insurance Oversight

A review of the Small Group Health Insurance Market in Maryland March 2015

Creation of the Maryland Health insurance Partnership Senate Bill 6 (SB 6), the Working Families and Small Business Health Coverage Act, (effective July 1, 2008), created the Health Insurance Partnership,

Creation of the Maryland Health insurance Partnership Senate Bill 6 (SB 6), the Working Families and Small Business Health Coverage Act, (effective July 1, 2008), created the Health Insurance Partnership,

Oregon Health Insurance Marketplace Report to the Joint Interim Committee on Ways and Means and Interim Senate and House Committees on Health Care

Oregon Health Insurance Marketplace Report to the Joint Interim Committee on Ways and Means and Interim Senate and House Committees on Health Care November 2015 Department of Consumer and Business Services

Oregon Health Insurance Marketplace Report to the Joint Interim Committee on Ways and Means and Interim Senate and House Committees on Health Care November 2015 Department of Consumer and Business Services

Chapter 14: Instructions for the Rates Table Application Section

Chapter 14: Instructions for the Rates Table Application Section Contents Chapter 14: Instructions for the Rates Table Application Section... 14-1 1. Overview... 14-1 2. Purpose... 14-1 3. Rates Table

Chapter 14: Instructions for the Rates Table Application Section Contents Chapter 14: Instructions for the Rates Table Application Section... 14-1 1. Overview... 14-1 2. Purpose... 14-1 3. Rates Table

Federally-facilitated Marketplace Agent and Broker Training Outline and Summary

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard Baltimore, Maryland 21244-1850 Center for Consumer Information & Insurance Oversight Federally-facilitated

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard Baltimore, Maryland 21244-1850 Center for Consumer Information & Insurance Oversight Federally-facilitated

Patient Protection and Affordable Care Act; HHS Notice of Benefit and Payment

DEPARTMENT OF HEALTH AND HUMAN SERVICES 45 CFR Parts 144, 147, 153, 155, and 156 [CMS-9954-P] RIN 0938-AR89 Patient Protection and Affordable Care Act; HHS Notice of Benefit and Payment Parameters for

DEPARTMENT OF HEALTH AND HUMAN SERVICES 45 CFR Parts 144, 147, 153, 155, and 156 [CMS-9954-P] RIN 0938-AR89 Patient Protection and Affordable Care Act; HHS Notice of Benefit and Payment Parameters for

Department of Health and Human Services. No. 39 February 27, 2013. Part II

Vol. 78 Wednesday, No. 39 February 27, 2013 Part II Department of Health and Human Services 45 CFR Parts 144, 147, 150, et al. Patient Protection and Affordable Care Act; Health Insurance Market Rules;

Vol. 78 Wednesday, No. 39 February 27, 2013 Part II Department of Health and Human Services 45 CFR Parts 144, 147, 150, et al. Patient Protection and Affordable Care Act; Health Insurance Market Rules;

Health Insurance Exchange Proposed Rules

Health Insurance Exchange Proposed Rules Karen Fisher, J.D. 202-862-6140 kfisher@aamc.org Jane Eilbacher 202-828-0896 jeilbacher@aamc.org Will Dardani 202-828-0541 wdardani@aamc.org Exchange Rules Overview

Health Insurance Exchange Proposed Rules Karen Fisher, J.D. 202-862-6140 kfisher@aamc.org Jane Eilbacher 202-828-0896 jeilbacher@aamc.org Will Dardani 202-828-0541 wdardani@aamc.org Exchange Rules Overview

Considerations for a State-based vs. Federally-Facilitated Health Insurance Exchange

C.L. BUTCH OTTER GOVERNOR Considerations for a State-based vs. Federally-Facilitated Health Insurance Exchange MANAGEMENT OF HEALTH PLANS AND COVERAGE OPTIONS IN THE EXCHANGE In a state-based exchange,

C.L. BUTCH OTTER GOVERNOR Considerations for a State-based vs. Federally-Facilitated Health Insurance Exchange MANAGEMENT OF HEALTH PLANS AND COVERAGE OPTIONS IN THE EXCHANGE In a state-based exchange,

Mississippi Health Insurance Exchange Advisory Board. Final Recommendations Employer Participation

Mississippi Health Insurance Exchange Advisory Board Final Recommendations Employer Participation Background The Mississippi Health Insurance Exchange Advisory Board ( Advisory Board ) was formed in order

Mississippi Health Insurance Exchange Advisory Board Final Recommendations Employer Participation Background The Mississippi Health Insurance Exchange Advisory Board ( Advisory Board ) was formed in order

6.0 SMALL BUSINESS HEALTH OPTIONS PROGRAM (SHOP)

") 6.0 SMALL BUSINESS HEALTH OPTIONS PROGRAM (SHOP) Summary Minnesota intends to implement and operate a State-Based Exchange per the requirements of the Affordable Care Act (ACA). This Exchange will meet

6.0 SMALL BUSINESS HEALTH OPTIONS PROGRAM (SHOP) Summary Minnesota intends to implement and operate a State-Based Exchange per the requirements of the Affordable Care Act (ACA). This Exchange will meet

Overview: Final Rule for Health Insurance Market Reforms

Overview: Final Rule for Health Insurance Market Reforms The Centers for Medicare & Medicaid Services (CMS) published a final rule on February 27, 2013 (78 FR 13406) to implement sections 2701, 2702, 2703,

Overview: Final Rule for Health Insurance Market Reforms The Centers for Medicare & Medicaid Services (CMS) published a final rule on February 27, 2013 (78 FR 13406) to implement sections 2701, 2702, 2703,

Small Business Health Options Program (SHOP)

") Small Business Health Options Program (SHOP) Exchange Board Update October 23, 2012 A service of Maryland Health Benefit Exchange SHOP Background States must establish a Small Business Health Options Program

Small Business Health Options Program (SHOP) Exchange Board Update October 23, 2012 A service of Maryland Health Benefit Exchange SHOP Background States must establish a Small Business Health Options Program

June 18, 2012. Submitted Electronically Via ffecomments@cms.hhs.gov. Re: General Guidance on Federally Facilitated Exchanges. Dear Ms.

June 18, 2012 Marilyn Tavenner Acting Administrator Centers for Medicare & Medicaid Services Department of Health and Human Services Room 445-G, Hubert H. Humphrey Building 200 Independence Avenue, SW

June 18, 2012 Marilyn Tavenner Acting Administrator Centers for Medicare & Medicaid Services Department of Health and Human Services Room 445-G, Hubert H. Humphrey Building 200 Independence Avenue, SW

SMALL BUSINESS HEALTH INSURANCE EXCHANGES. Low Initial Enrollment Likely due to Multiple, Evolving Factors

United States Government Accountability Office Report to the Chairman, Committee on Small Business, House of Representatives November 2014 SMALL BUSINESS HEALTH INSURANCE EXCHANGES Low Initial Enrollment

United States Government Accountability Office Report to the Chairman, Committee on Small Business, House of Representatives November 2014 SMALL BUSINESS HEALTH INSURANCE EXCHANGES Low Initial Enrollment

Everything about Exchanges you ve wanted to know... HHS Issues Proposed Rules

This article originally appeared in the July 2011 Quarterly Review. Everything about Exchanges you ve wanted to know... HHS Issues Proposed Rules New Proposed Rules set standards, certify health plans,

This article originally appeared in the July 2011 Quarterly Review. Everything about Exchanges you ve wanted to know... HHS Issues Proposed Rules New Proposed Rules set standards, certify health plans,

SHOP Exchange Technology Enablement Options. March 13, 2012

SHOP Exchange Technology Enablement Options March 13, 2012 Agenda 1. SHOP Overview 2. SHOP Principles 3. Design Options 4. Option Comparisons 5. Timeline and Recommendation - 1 - Overview: Small Business

SHOP Exchange Technology Enablement Options March 13, 2012 Agenda 1. SHOP Overview 2. SHOP Principles 3. Design Options 4. Option Comparisons 5. Timeline and Recommendation - 1 - Overview: Small Business

MINNESOTA HEALTH INSURANCE EXCHANGE PERFORMANCE PROGRESS REPORT

MINNESOTA HEALTH INSURANCE EXCHANGE PERFORMANCE PROGRESS REPORT Submitted to CCIIO September, 2012 Core Area: Legal Authority and Governance Hire full-time staff within the Department of Commerce dedicated

MINNESOTA HEALTH INSURANCE EXCHANGE PERFORMANCE PROGRESS REPORT Submitted to CCIIO September, 2012 Core Area: Legal Authority and Governance Hire full-time staff within the Department of Commerce dedicated

Exchange Final Rule: Indian Provisions

Exchange Final Rule: Indian Provisions DEPARTMENT OF HEALTH AND HUMAN SERVICES CENTERS for MEDICARE & MEDICAID SERVICES Center for Consumer Information and Insurance Oversight Health Insurance Exchange

Exchange Final Rule: Indian Provisions DEPARTMENT OF HEALTH AND HUMAN SERVICES CENTERS for MEDICARE & MEDICAID SERVICES Center for Consumer Information and Insurance Oversight Health Insurance Exchange

The future of the Small Business Health Options Program (SHOP) in Maryland. Presentation to the MHBE Stakeholder Advisory Committee December 10, 2015

in Maryland. Presentation to the MHBE Stakeholder Advisory Committee December 10, 2015") The future of the Small Business Health Options Program (SHOP) in Maryland Presentation to the MHBE Stakeholder Advisory Committee December 10, 2015 Historical support for small business Senate Bill 6,

The future of the Small Business Health Options Program (SHOP) in Maryland Presentation to the MHBE Stakeholder Advisory Committee December 10, 2015 Historical support for small business Senate Bill 6,

Department of Health and Human Services. Part II

Vol. 79 Tuesday, No. 47 March 11, 2014 Part II Department of Health and Human Services 45 CFR Parts 144, 147, 153, et al. Patient Protection and Affordable Care Act; HHS Notice of Benefit and Payment Parameters

Vol. 79 Tuesday, No. 47 March 11, 2014 Part II Department of Health and Human Services 45 CFR Parts 144, 147, 153, et al. Patient Protection and Affordable Care Act; HHS Notice of Benefit and Payment Parameters

Connecting with Brokers. Small Business Marketplace Manager Connect for Health Colorado

Connecting with Brokers Small Business Marketplace Manager Connect for Health Colorado Today s Agenda Where are we now? How will C4HC partner with Brokers What will happen on October 1 st? A vision for

Connecting with Brokers Small Business Marketplace Manager Connect for Health Colorado Today s Agenda Where are we now? How will C4HC partner with Brokers What will happen on October 1 st? A vision for

October 31, 2011. Dear Dr. Berwick:

Donald Berwick, M.D., M.P.P. Administrator Centers for Medicare & Medicaid Services Hubert H. Humphrey Building 200 Independence Avenue, S.W. Room 445-G Washington, DC 20201 RE: CMS 9989 P; Patient Protection

Donald Berwick, M.D., M.P.P. Administrator Centers for Medicare & Medicaid Services Hubert H. Humphrey Building 200 Independence Avenue, S.W. Room 445-G Washington, DC 20201 RE: CMS 9989 P; Patient Protection

October 3, 2011. Re: File code CMS-9989-P. Dear Director Larsen,

October 3, 2011 Steve Larsen Director, Center for Consumer Information and Insurance Oversight Centers for Medicare and Medicaid Services Department of Health and Human Services Hubert H. Humphrey Building,

October 3, 2011 Steve Larsen Director, Center for Consumer Information and Insurance Oversight Centers for Medicare and Medicaid Services Department of Health and Human Services Hubert H. Humphrey Building,

Maryland Health Benefit Exchange. Request for Information. SHOP Technology Enablement

+ Maryland Health Benefit Exchange Request for Information SHOP Technology Enablement Issue Date: 3/16/2012 1 MARYLAND HEALTH BENEFIT EXCHANGE KEY INFORMATION SUMMARY SHEET Request for Information SHOP

+ Maryland Health Benefit Exchange Request for Information SHOP Technology Enablement Issue Date: 3/16/2012 1 MARYLAND HEALTH BENEFIT EXCHANGE KEY INFORMATION SUMMARY SHEET Request for Information SHOP

UPDATE TO COVER OREGON BUSINESS PLAN 2014-2015

UPDATE TO COVER OREGON BUSINESS PLAN 2014-2015 PRESENTED TO OREGON STATE LEGISLATURE ON MAY 28, 2014 Cover Oregon 16760 SW Upper Boones Ferry Road, Suite 200 Durham, OR 97224 1-855-CoverOR www.coveroregon.com

UPDATE TO COVER OREGON BUSINESS PLAN 2014-2015 PRESENTED TO OREGON STATE LEGISLATURE ON MAY 28, 2014 Cover Oregon 16760 SW Upper Boones Ferry Road, Suite 200 Durham, OR 97224 1-855-CoverOR www.coveroregon.com

EXPLAINING HEALTH CARE REFORM: Risk Adjustment, Reinsurance, and Risk Corridors

EXPLAINING HEALTH CARE REFORM: Risk Adjustment, Reinsurance, and Risk Corridors As of January 1, 2014, insurers are no longer able to deny coverage or charge higher premiums based on preexisting conditions

EXPLAINING HEALTH CARE REFORM: Risk Adjustment, Reinsurance, and Risk Corridors As of January 1, 2014, insurers are no longer able to deny coverage or charge higher premiums based on preexisting conditions

DEPARTMENT OF HEALTH & HUMAN SERVICES. Centers for Medicare & Medicaid Services. 200 Independence Ave SW Washington, DC 20201

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 200 Independence Ave SW Washington, DC 20201 Date: January 3, 2013 From: Center for Consumer Information and Insurance Oversight

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 200 Independence Ave SW Washington, DC 20201 Date: January 3, 2013 From: Center for Consumer Information and Insurance Oversight

PATIENT PROTECTION AND AFFORDABLE CARE ACT. Status of Federal and State Efforts to Establish Health Insurance Exchanges for Small Businesses

United States Government Accountability Office Report to the Chairman, Committee on Small Business, House of Representatives June 2013 PATIENT PROTECTION AND AFFORDABLE CARE ACT Status of Federal and State

United States Government Accountability Office Report to the Chairman, Committee on Small Business, House of Representatives June 2013 PATIENT PROTECTION AND AFFORDABLE CARE ACT Status of Federal and State

Report to the Massachusetts Division of Insurance:

Report to the Massachusetts Division of Insurance: The Projected Impact on Health Insurance Premiums in the Merged Individual/Small Group Market with the Implementation of Federal Rating Rules that Restrict

Report to the Massachusetts Division of Insurance: The Projected Impact on Health Insurance Premiums in the Merged Individual/Small Group Market with the Implementation of Federal Rating Rules that Restrict

DRAFT FOR PUBLIC COMMENT February 8, 2016

State of Vermont Department of Vermont Health Access [Phone] 802-879-5900 280 State Drive, NOB 1 South Waterbury, VT 05671-1010 http://dvha.vermont.gov Agency of Human Services Vermont s Proposal to Waive

State of Vermont Department of Vermont Health Access [Phone] 802-879-5900 280 State Drive, NOB 1 South Waterbury, VT 05671-1010 http://dvha.vermont.gov Agency of Human Services Vermont s Proposal to Waive

Minnesota Health Insurance Exchange Blueprint Application Documentation. 4.1 Appropriate authority to perform and oversee certification of QHPs

Minnesota Health Insurance Exchange Blueprint Application ation 4.0 PLAN MANAGEMENT Blueprint Application November, 2012 4.1 Appropriate authority to perform and oversee certification of QHPs Federal law

Minnesota Health Insurance Exchange Blueprint Application ation 4.0 PLAN MANAGEMENT Blueprint Application November, 2012 4.1 Appropriate authority to perform and oversee certification of QHPs Federal law

It s the month for shamrocks and a glimpse of spring. We continue to stay busy as you ll see in this latest news from VIM.

THE VIM BULLETIN News from the Clinic MARCH, 2014 It s the month for shamrocks and a glimpse of spring. We continue to stay busy as you ll see in this latest news from VIM. UPDATE ON ACA ENROLLMENT PROGRESS

THE VIM BULLETIN News from the Clinic MARCH, 2014 It s the month for shamrocks and a glimpse of spring. We continue to stay busy as you ll see in this latest news from VIM. UPDATE ON ACA ENROLLMENT PROGRESS

PERS Health Insurance Program. 2015 Fall Plan Change Meetings

PERS Health Insurance Program 2015 Fall Plan Change Meetings Agenda What is the PERS Health Insurance Program (PHIP)? Health Plans (Medicare / Non-Medicare) Providence Health Plans Kaiser Permanente PacificSource

PERS Health Insurance Program 2015 Fall Plan Change Meetings Agenda What is the PERS Health Insurance Program (PHIP)? Health Plans (Medicare / Non-Medicare) Providence Health Plans Kaiser Permanente PacificSource

Presentation for Licensed Producers The Affordable Care Act

Presentation for Licensed Producers The Affordable Care Act Bruce Donaldson, CHC Producer & Stakeholder Specialist Arkansas Insurance Department Affordable Care Act The ACA was passed by Congress and signed

Presentation for Licensed Producers The Affordable Care Act Bruce Donaldson, CHC Producer & Stakeholder Specialist Arkansas Insurance Department Affordable Care Act The ACA was passed by Congress and signed

We recommend CCIIO create instructions and allow $0 experience values for brand new carriers with no previous experience.

December 4, 2013 Mr. Dennis Yu Actuarial Branch Director, Oversight Group Center for Consumer Information and Insurance Oversight 7500 Security Boulevard Baltimore, MD 21244 Dear Dennis, On behalf of the

December 4, 2013 Mr. Dennis Yu Actuarial Branch Director, Oversight Group Center for Consumer Information and Insurance Oversight 7500 Security Boulevard Baltimore, MD 21244 Dear Dennis, On behalf of the

From: Center for Consumer Information and Insurance Oversight, Centers for Medicare & Medicaid Services

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services Center for Consumer Information & Insurance Oversight 200 Independence Avenue SW Washington, DC 20201 Date: March 14, 2014

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services Center for Consumer Information & Insurance Oversight 200 Independence Avenue SW Washington, DC 20201 Date: March 14, 2014

PPACA/Healthcare Reform CHANGES

PPACA/Healthcare Reform CHANGES beginning in 2014 for small employers A guide to understanding the administrative provisions, benefit changes, new taxes and credits, market reforms and purchasing options

PPACA/Healthcare Reform CHANGES beginning in 2014 for small employers A guide to understanding the administrative provisions, benefit changes, new taxes and credits, market reforms and purchasing options

How To Get A Dental Plan On The Marketplace

2014 Delaware Qualified Health Plans Individual Market Overview October 8, 2013 www.pcghealth.com Topics Overview of QHPs in the Individual Market QHP Issuers Plan Summary Premium Rates and Cost-Sharing

2014 Delaware Qualified Health Plans Individual Market Overview October 8, 2013 www.pcghealth.com Topics Overview of QHPs in the Individual Market QHP Issuers Plan Summary Premium Rates and Cost-Sharing

October 26, 2012. Selection Risks for SHOP Exchange Scenarios. Dear Michael:

4370 La Jolla Village Dr. Suite 700 San Diego, CA 92122 (858) 558-8400 tel (858) 597-0111 fax www.milliman.com Mr. Michael Lujan Director Small Business Health Options Program (SHOP) California Health

4370 La Jolla Village Dr. Suite 700 San Diego, CA 92122 (858) 558-8400 tel (858) 597-0111 fax www.milliman.com Mr. Michael Lujan Director Small Business Health Options Program (SHOP) California Health

One of the more visible changes soon to be brought MONTANA S HEALTH INSURANCE A PREVIEW OF MARKETPLACE

A PREVIEW OF MONTANA S HEALTH INSURANCE MARKETPLACE by Gregg Davis and Christina Goe One of the more visible changes soon to be brought to the forefront by passage of the Affordable Care Act (ACA) is the

A PREVIEW OF MONTANA S HEALTH INSURANCE MARKETPLACE by Gregg Davis and Christina Goe One of the more visible changes soon to be brought to the forefront by passage of the Affordable Care Act (ACA) is the

California Health Benefit Exchange

Board Members Diana S. Dooley, Chair Kimberly Belshé Paul Fearer Susan Kennedy Robert Ross, MD Executive Director Peter V. Lee Qualified Health Plan Policies and Strategies to Improve Care, Prevention

Board Members Diana S. Dooley, Chair Kimberly Belshé Paul Fearer Susan Kennedy Robert Ross, MD Executive Director Peter V. Lee Qualified Health Plan Policies and Strategies to Improve Care, Prevention

HEFFERNAN BENEFIT ADVISORY SERVICES 2014 HEALTH CARE TREND REPORT

HEFFERNAN BENEFIT ADVISORY SERVICES 2014 HEALTH CARE TREND REPORT HEFFERNAN BENEFIT ADVISORY SERVICES TABLE OF CONTENTS What is Trend 1 Medical Trend Projections 2 Historic National Medical Trend 2 Dental

HEFFERNAN BENEFIT ADVISORY SERVICES 2014 HEALTH CARE TREND REPORT HEFFERNAN BENEFIT ADVISORY SERVICES TABLE OF CONTENTS What is Trend 1 Medical Trend Projections 2 Historic National Medical Trend 2 Dental

Oregon Health Insurance Exchange Corporation, dba Cover Oregon Performance Audit

Oregon Health Insurance Exchange Corporation, dba Cover Oregon Performance Audit April 30, 2015 4800 Meadows Rd., Ste. 200 Lake Oswego, OR 97035 P 503.274.2849 F 503.274.2843 www.tkw.com April 30, 2015

Oregon Health Insurance Exchange Corporation, dba Cover Oregon Performance Audit April 30, 2015 4800 Meadows Rd., Ste. 200 Lake Oswego, OR 97035 P 503.274.2849 F 503.274.2843 www.tkw.com April 30, 2015

1. Establishment of SHOPs

Page 1 of 10 Checkpoint Contents Pension & Benefits Library Pension & Benefits Editorial Materials EBIA Benefits Compliance Library Health Care Reform for Employers and Advisors XXI. Exchanges, Qualified

Page 1 of 10 Checkpoint Contents Pension & Benefits Library Pension & Benefits Editorial Materials EBIA Benefits Compliance Library Health Care Reform for Employers and Advisors XXI. Exchanges, Qualified

Financial Management 101

Financial Management 101 DEPARTMENT OF HEALTH AND HUMAN SERVICES CENTERS for MEDICARE & MEDICAID SERVICES Center for Consumer Information and Insurance Oversight State Exchange Grantee Meeting The material

Financial Management 101 DEPARTMENT OF HEALTH AND HUMAN SERVICES CENTERS for MEDICARE & MEDICAID SERVICES Center for Consumer Information and Insurance Oversight State Exchange Grantee Meeting The material

402 Small Business Health Options Program (SHOP) Marketplaces

Marketplaces") Checkpoint Contents Federal Library Federal Editorial Materials PPC's Tax and Financial Planning Library Health Care Reform (PPC) Chapter 4 Health Insurance Marketplaces 402 Small Business Health Options

Checkpoint Contents Federal Library Federal Editorial Materials PPC's Tax and Financial Planning Library Health Care Reform (PPC) Chapter 4 Health Insurance Marketplaces 402 Small Business Health Options

Small Employers Eligible for Health Care Tax Credit

Brought to you by Clark-Mortenson Insurance Small Employers Eligible for Health Care Tax Credit The Affordable Care Act (ACA) created a health care tax credit for eligible small employers that provide

Brought to you by Clark-Mortenson Insurance Small Employers Eligible for Health Care Tax Credit The Affordable Care Act (ACA) created a health care tax credit for eligible small employers that provide

Adopted by the NAIC Health Insurance and Managed Care (B) Committee on June 27, 2012 Intended for Use by the States as Guidance Only

Committee on June 27, 2012 Intended for Use by the States as Guidance Only") Rate Review White Paper The purpose of this white paper is to assist state policymakers with the implementation of the Affordable Care Act (ACA) provisions related to health insurance rating, rate filing

Rate Review White Paper The purpose of this white paper is to assist state policymakers with the implementation of the Affordable Care Act (ACA) provisions related to health insurance rating, rate filing

SMALL BUSINESS HEALTH OPTIONS PROGRAM

SMALL BUSINESS HEALTH OPTIONS PROGRAM This summary provides an overview of what is currently known about the Small Business Health Options Program (commonly referred to as "SHOP"), an aspect of the American

SMALL BUSINESS HEALTH OPTIONS PROGRAM This summary provides an overview of what is currently known about the Small Business Health Options Program (commonly referred to as "SHOP"), an aspect of the American

RE: D.C. Health Benefit Exchange - Dental Workgroup II Minority Report

deltadentalins.com April 18, 2014 SUBMITTED VIA EMAIL Dr. Leighton Ku, Chair Ms. Katherine Stocks, Vice-Chair D.C. Health Benefit Exchange Dental Plan Advisory Working Group II RE: D.C. Health Benefit

deltadentalins.com April 18, 2014 SUBMITTED VIA EMAIL Dr. Leighton Ku, Chair Ms. Katherine Stocks, Vice-Chair D.C. Health Benefit Exchange Dental Plan Advisory Working Group II RE: D.C. Health Benefit

The Transitional Reinsurance Program Operational Guidance: Counting Method Examples for Contributing Entities

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services Center for Consumer Information and Insurance Oversight 200 Independence Avenue SW Washington, DC 20201 Date: July 17, 2014

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services Center for Consumer Information and Insurance Oversight 200 Independence Avenue SW Washington, DC 20201 Date: July 17, 2014

REGULATORY UPDATE Vol. 1 No. 18

REGULATORY UPDATE Vol. 1 No. 18 FAQs on Exchanges August 7, 2013 IN THIS ISSUE FAQs on Exchanges Employer Mandate Delay Transitional Guidance Issued Individual Mandate Final Rules Issued Possible Exchange

REGULATORY UPDATE Vol. 1 No. 18 FAQs on Exchanges August 7, 2013 IN THIS ISSUE FAQs on Exchanges Employer Mandate Delay Transitional Guidance Issued Individual Mandate Final Rules Issued Possible Exchange

Health Insurance Partnership

Health Insurance Partnership Enrollment Update Prepared by the Maryland Health Care Commission January 1, 2015 Introduction During the 2007 Special Session, Governor O Malley proposed and the General Assembly

Health Insurance Partnership Enrollment Update Prepared by the Maryland Health Care Commission January 1, 2015 Introduction During the 2007 Special Session, Governor O Malley proposed and the General Assembly

Submitted via email to OIRA_submission@omb.eop.gov. May 12, 2014. CMS Desk Officer Fax Number (202) 395-5806 OIRA_submission@omb.eop.

395-5806 OIRA_submission@omb.eop.") Submitted via email to OIRA_submission@omb.eop.gov May 12, 2014 CMS Desk Officer Fax Number (202) 395-5806 OIRA_submission@omb.eop.gov RE: Comments on CMS-10320 (OCN: 0938-1086) I write on behalf of the

Submitted via email to OIRA_submission@omb.eop.gov May 12, 2014 CMS Desk Officer Fax Number (202) 395-5806 OIRA_submission@omb.eop.gov RE: Comments on CMS-10320 (OCN: 0938-1086) I write on behalf of the

Maryland Misallocated Millions to Establishment Grants for a Health Insurance Marketplace (A-01-14-02503)

") March 26, 2015 TO: Andrew M. Slavitt Acting Administrator Centers for Medicare & Medicaid Services FROM: /Daniel R. Levinson/ Inspector General SUBJECT: Maryland Misallocated Millions to Establishment

March 26, 2015 TO: Andrew M. Slavitt Acting Administrator Centers for Medicare & Medicaid Services FROM: /Daniel R. Levinson/ Inspector General SUBJECT: Maryland Misallocated Millions to Establishment

Affordable Insurance Exchanges: Plan Management Partnership Guidance

Affordable Insurance Exchanges: Plan Management Partnership Guidance DEPARTMENT OF HEALTH AND HUMAN SERVICES CENTERS for MEDICARE and MEDICAID SERVICES Center for Consumer Information and Insurance Oversight

Affordable Insurance Exchanges: Plan Management Partnership Guidance DEPARTMENT OF HEALTH AND HUMAN SERVICES CENTERS for MEDICARE and MEDICAID SERVICES Center for Consumer Information and Insurance Oversight

Final Regulations on Health Insurance Exchanges

Health Care Reform Legislative Brief Final Regulations on Health Insurance Exchanges Beginning in 2014, individuals and small businesses will be able to purchase private health insurance through state-based

Health Care Reform Legislative Brief Final Regulations on Health Insurance Exchanges Beginning in 2014, individuals and small businesses will be able to purchase private health insurance through state-based

Engaging Small Businesses and Brokers in State SHOPs

Engaging Small Businesses and Brokers in State SHOPs DEPARTMENT OF HEALTH AND HUMAN SERVICES CENTERS for MEDICARE & MEDICAID SERVICES Center for Consumer Information and Insurance Oversight Health Insurance

Engaging Small Businesses and Brokers in State SHOPs DEPARTMENT OF HEALTH AND HUMAN SERVICES CENTERS for MEDICARE & MEDICAID SERVICES Center for Consumer Information and Insurance Oversight Health Insurance

CERTIFIED MEDICAL QUALIFIED HEALTH PLANS (QHP) FOR GROUPS January 1, 2015 December 31, 2015

FOR GROUPS January 1, 2015 December 31, 2015") CERTIFIED MEDICAL QUALIFIED HEALTH PLANS (QHP) FOR GROUPS January 1, 2015 December 31, 2015 METAL TIER ATRIO Oregon Standard Bronze Plan 32536OR0010006 Bronze ATRIO Bronze Pioneer 32536OR0010007 Bronze

CERTIFIED MEDICAL QUALIFIED HEALTH PLANS (QHP) FOR GROUPS January 1, 2015 December 31, 2015 METAL TIER ATRIO Oregon Standard Bronze Plan 32536OR0010006 Bronze ATRIO Bronze Pioneer 32536OR0010007 Bronze

YOUR HEALTH IDAHO 2015 QUALIFIED HEALTH PLAN STANDARDS

C.L. BUTCH OTTER Governor State of Idaho DEPARTMENT OF INSURANCE 700 West State Street, 3rd Floor P.O. Box 83720 Boise, Idaho 83720-0043 Phone (208)334-4250 Fax (208)334-4398 Website: http://www.doi.idaho.gov

C.L. BUTCH OTTER Governor State of Idaho DEPARTMENT OF INSURANCE 700 West State Street, 3rd Floor P.O. Box 83720 Boise, Idaho 83720-0043 Phone (208)334-4250 Fax (208)334-4398 Website: http://www.doi.idaho.gov

SMALL GROUP MARKET HEALTH INSURANCE COVERAGE MODEL REGULATION

SMALL GROUP MARKET HEALTH INSURANCE COVERAGE MODEL REGULATION Section 1. Section 2. Section 3. Section 4. Section 5. Section 6. Section 7. Section 8. Section 9. Section 10. Section 11. Section 12. Section

SMALL GROUP MARKET HEALTH INSURANCE COVERAGE MODEL REGULATION Section 1. Section 2. Section 3. Section 4. Section 5. Section 6. Section 7. Section 8. Section 9. Section 10. Section 11. Section 12. Section

DEPARTMENT OF HEALTH AND HUMAN SERVICES. Patient Protection and Affordable Care Act; Establishment of Exchanges and

This document is scheduled to be published in the Federal Register on 03/11/2013 and available online at http://federalregister.gov/a/2013-04952, and on FDsys.gov DEPARTMENT OF HEALTH AND HUMAN SERVICES

This document is scheduled to be published in the Federal Register on 03/11/2013 and available online at http://federalregister.gov/a/2013-04952, and on FDsys.gov DEPARTMENT OF HEALTH AND HUMAN SERVICES

Request for Information Web Based Entities. Covered California

Request for Information Web Based Entities Covered California Request for Information Covered California August 25, 2015 1. PURPOSE: The purpose of this Request for Information (RFI) is to gather information

Request for Information Web Based Entities Covered California Request for Information Covered California August 25, 2015 1. PURPOSE: The purpose of this Request for Information (RFI) is to gather information

2016: OVERVIEW OF THE HEALTH INSURANCE MARKET IN KANSAS

2016: OVERVIEW OF THE HEALTH INSURANCE MARKET IN KANSAS 2016 Open Enrollment for Individuals and Families The open enrollment period for individual health insurance coverage in Kansas will begin on November

2016: OVERVIEW OF THE HEALTH INSURANCE MARKET IN KANSAS 2016 Open Enrollment for Individuals and Families The open enrollment period for individual health insurance coverage in Kansas will begin on November

Self-insured Plans under Health Care Reform

Brought to you by Good Neighbor Insurance Self-insured Plans under Health Care Reform The Affordable Care Act (ACA) includes numerous reforms affecting the health coverage that employers provide to their

Brought to you by Good Neighbor Insurance Self-insured Plans under Health Care Reform The Affordable Care Act (ACA) includes numerous reforms affecting the health coverage that employers provide to their

SHOP and the Small Group Market Policies

SHOP and the Small Group Market Policies DEPARTMENT OF HEALTH AND HUMAN SERVICES CENTERS for MEDICARE & MEDICAID SERVICES Center for Consumer Information and Insurance Oversight Health Insurance Exchange

SHOP and the Small Group Market Policies DEPARTMENT OF HEALTH AND HUMAN SERVICES CENTERS for MEDICARE & MEDICAID SERVICES Center for Consumer Information and Insurance Oversight Health Insurance Exchange

December 18, 2015. Dear Mr. Slavitt:

Andrew M. Slavitt Acting Administrator Centers for Medicare & Medicaid Services Hubert H. Humphrey Building 200 Independence Avenue, S.W., Room 445-G Washington, DC 20201 RE: Proposed Rule: CMS-9937-P/RIN

Andrew M. Slavitt Acting Administrator Centers for Medicare & Medicaid Services Hubert H. Humphrey Building 200 Independence Avenue, S.W., Room 445-G Washington, DC 20201 RE: Proposed Rule: CMS-9937-P/RIN

For The U.S. House of Representatives Committee on Energy and Commerce Subcommittee on Oversight and Investigations Hearing September 29, 2015

Written Statement For The U.S. House of Representatives Committee on Energy and Commerce Subcommittee on Oversight and Investigations Hearing September 29, 2015 By Patrick Allen, Director Department of

Written Statement For The U.S. House of Representatives Committee on Energy and Commerce Subcommittee on Oversight and Investigations Hearing September 29, 2015 By Patrick Allen, Director Department of

Patient Protection and Affordable Care Act; Health Insurance Market Rules; Rate Review. AGENCY: Centers for Medicare & Medicaid Services (CMS), HHS.

, HHS.") DEPARTMENT OF HEALTH AND HUMAN SERVICES 45 CFR Parts 144, 147, 150, 154 and 156 [CMS-9972-P] RIN 0938-AR40 Patient Protection and Affordable Care Act; Health Insurance Market Rules; Rate Review AGENCY:

DEPARTMENT OF HEALTH AND HUMAN SERVICES 45 CFR Parts 144, 147, 150, 154 and 156 [CMS-9972-P] RIN 0938-AR40 Patient Protection and Affordable Care Act; Health Insurance Market Rules; Rate Review AGENCY:

to Health Care Reform

The Employer s Guide to Health Care Reform What you need to know now to: Consider your choices Decide what s best for you Follow the rules 2013-2014 Health care reform is the law of the land. Some don

The Employer s Guide to Health Care Reform What you need to know now to: Consider your choices Decide what s best for you Follow the rules 2013-2014 Health care reform is the law of the land. Some don

OFFICE OF INSURANCE AND SAFETY FIRE COMMISSIONER

OFFICE OF INSURANCE AND SAFETY FIRE COMMISSIONER RALPH T. HUDGENS COMMISSIONER OF INSURANCE SAFETY FIRE COMMISSIONER INDUSTRIAL LOAN COMMISSIONER SEVENTH FLOOR, WEST TOWER FLOYD BUILDING 2 MARTIN LUTHER

OFFICE OF INSURANCE AND SAFETY FIRE COMMISSIONER RALPH T. HUDGENS COMMISSIONER OF INSURANCE SAFETY FIRE COMMISSIONER INDUSTRIAL LOAN COMMISSIONER SEVENTH FLOOR, WEST TOWER FLOYD BUILDING 2 MARTIN LUTHER

CERTIFIED MEDICAL QUALIFIED HEALTH PLANS (QHP) January 1, 2015 December 31, 2015

January 1, 2015 December 31, 2015") CERTIFIED MEDICAL QUALIFIED HEALTH PLANS (QHP) January 1, 2015 December 31, 2015 ATRIO Oregon Standard Bronze Plan 32536OR0020006 Bronze ATRIO Bronze Pioneer 32536OR0020007 Bronze ATRIO Oregon Standard

CERTIFIED MEDICAL QUALIFIED HEALTH PLANS (QHP) January 1, 2015 December 31, 2015 ATRIO Oregon Standard Bronze Plan 32536OR0020006 Bronze ATRIO Bronze Pioneer 32536OR0020007 Bronze ATRIO Oregon Standard

Puerto Rico Rate Filing Instruction Manual. Version 3.0

Puerto Rico Rate Filing Instruction Manual Version 3.0 1 Table of Contents Overview... 3 Section I: Written Rate Filing Documentation... 4 General Description... 4 Base Period Experience... 4 Capitation

Puerto Rico Rate Filing Instruction Manual Version 3.0 1 Table of Contents Overview... 3 Section I: Written Rate Filing Documentation... 4 General Description... 4 Base Period Experience... 4 Capitation

Department of Health and Human Services. No. 57 March 23, 2012. Part IV

Vol. 77 Friday, No. 57 March 23, 2012 Part IV Department of Health and Human Services 45 CFR Part 153 Patient Protection and Affordable Care Act; Standards Related to Reinsurance, Risk Corridors and Risk

Vol. 77 Friday, No. 57 March 23, 2012 Part IV Department of Health and Human Services 45 CFR Part 153 Patient Protection and Affordable Care Act; Standards Related to Reinsurance, Risk Corridors and Risk

Senate Bill 1025-First Edition

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 00 S 1 SENATE BILL Short Title: Small Business Health Insurance Expansion. (Public) Sponsors: Referred to: Senators Stein; Apodaca, Berger of Franklin, Dorsett,

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 00 S 1 SENATE BILL Short Title: Small Business Health Insurance Expansion. (Public) Sponsors: Referred to: Senators Stein; Apodaca, Berger of Franklin, Dorsett,

PART 1: ENABLING AUTHORITY AND GOVERNANCE

Application for Approval of an American Health Benefit Exchange On March 23, 2010, the President signed into law the Patient Protection and Affordable Care Act (P.L. 111-148). On March 30, 2010, the Health

Application for Approval of an American Health Benefit Exchange On March 23, 2010, the President signed into law the Patient Protection and Affordable Care Act (P.L. 111-148). On March 30, 2010, the Health

Patient Protection and Affordable Care Act Compliance Checklist for Employers

October, 2014 Patient Protection and Affordable Care Act Compliance Checklist for Employers Under the Employer Mandate in the Affordable Care Act, effective January 1, 2015, employers with 50 or more full-time

October, 2014 Patient Protection and Affordable Care Act Compliance Checklist for Employers Under the Employer Mandate in the Affordable Care Act, effective January 1, 2015, employers with 50 or more full-time

Chapter 34 Voluntary Health Insurance Purchasing Alliance Act

Chapter 34 Voluntary Health Insurance Purchasing Alliance Act 31A-34-101 Title. This chapter is known as the "Voluntary Health Insurance Purchasing Alliance Act." 31A-34-102 Purpose and intent -- Legislative

Chapter 34 Voluntary Health Insurance Purchasing Alliance Act 31A-34-101 Title. This chapter is known as the "Voluntary Health Insurance Purchasing Alliance Act." 31A-34-102 Purpose and intent -- Legislative

Health insurance Marketplace. What to expect in 2014

Health insurance Marketplace What to expect in 2014 Overview The Affordable Care Act (ACA) includes several provisions geared to extend greater access to health insurance benefits to more people. Beginning

Health insurance Marketplace What to expect in 2014 Overview The Affordable Care Act (ACA) includes several provisions geared to extend greater access to health insurance benefits to more people. Beginning

This guidance is subject to revision if applicable state or federal laws change.

February 6, 2015 TO: RE: Carriers Offering Transitional Plans Small Group and Individual Transitional Health Benefit Plans In conjunction with Senate Bill 1582 (2014), the division issued regulatory requirements

February 6, 2015 TO: RE: Carriers Offering Transitional Plans Small Group and Individual Transitional Health Benefit Plans In conjunction with Senate Bill 1582 (2014), the division issued regulatory requirements

Office of Personnel Management

United States Office of Personnel Management The Federal Government s Human Resources Agency Multi-State Plan Program Issuer Letter Number: 2014-002 Date: February 4, 2014 Subject: Multi-State Plan Program

United States Office of Personnel Management The Federal Government s Human Resources Agency Multi-State Plan Program Issuer Letter Number: 2014-002 Date: February 4, 2014 Subject: Multi-State Plan Program

Chapter 15: Instructions for Stand-Alone Dental Plan Application

Chapter 15: Instructions for Stand-Alone Dental Plan Application Contents 1. Purpose... 15-1 2. Overview... 15-2 2.1 Key Template Updates... 15-2 3. Data Requirements... 15-3 4. Application Instructions...

Chapter 15: Instructions for Stand-Alone Dental Plan Application Contents 1. Purpose... 15-1 2. Overview... 15-2 2.1 Key Template Updates... 15-2 3. Data Requirements... 15-3 4. Application Instructions...

Small Business Service Bureau Extension (VOTE)

") Small Business Service Bureau Extension (VOTE) RONI MANSUR Deputy Executive Director & Chief Operating Officer BRIAN SCHUETZ Senior Manager, ACA Implementation Board of Directors Meeting, November 14,

Small Business Service Bureau Extension (VOTE) RONI MANSUR Deputy Executive Director & Chief Operating Officer BRIAN SCHUETZ Senior Manager, ACA Implementation Board of Directors Meeting, November 14,

DEPARTMENT OF HEALTH & HUMAN SERVICES. Centers for Medicare & Medicaid Services. 200 Independence Avenue SW Washington, DC 20201

1 DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 200 Independence Avenue SW Washington, DC 20201 Date: May 1, 2013 From: Center for Consumer Information and Insurance Oversight

1 DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 200 Independence Avenue SW Washington, DC 20201 Date: May 1, 2013 From: Center for Consumer Information and Insurance Oversight

April 2, 2012. Dear Mr. Bertko,

April 2, 2012 Mr. John Bertko, FSA, MAAA Director, Office of Special Initiatives and Pricing Center for Consumer Information and Insurance Oversight Centers for Medicare and Medicaid Services U.S. Department

April 2, 2012 Mr. John Bertko, FSA, MAAA Director, Office of Special Initiatives and Pricing Center for Consumer Information and Insurance Oversight Centers for Medicare and Medicaid Services U.S. Department

DRAFT. Final Report. Wisconsin Department of Health Services Division of Health Care Access and Accountability

Final Report Wisconsin Department of Health Services Division of Health Care Access and Accountability Wisconsin s Small Group Insurance Market March 2009 Table of Contents 1 INTRODUCTION... 3 2 EMPLOYER-BASED

Final Report Wisconsin Department of Health Services Division of Health Care Access and Accountability Wisconsin s Small Group Insurance Market March 2009 Table of Contents 1 INTRODUCTION... 3 2 EMPLOYER-BASED

Nebraska Health Insurance Exchange Update

Nebraska Health Insurance Exchange Update State of Nebraska s Health Insurance Exchange A Presentation to the Public September, 2012 TODAY'S AGENDA Section 1: Overview of Health Insurance Exchanges Section

Nebraska Health Insurance Exchange Update State of Nebraska s Health Insurance Exchange A Presentation to the Public September, 2012 TODAY'S AGENDA Section 1: Overview of Health Insurance Exchanges Section

Proposed Rule OAR 836-053-0008; Request for Comments on Provisions in Health Reform Proposed Rule Regarding 24-Month Transplant Waiting Period

December 6, 2013 Laura Cali Insurance Commissioner Oregon Department of Consumer Business Services 350 Winter St NE Salem, OR 97301-3883 Re: Proposed Rule OAR 836-053-0008; Request for Comments on Provisions

December 6, 2013 Laura Cali Insurance Commissioner Oregon Department of Consumer Business Services 350 Winter St NE Salem, OR 97301-3883 Re: Proposed Rule OAR 836-053-0008; Request for Comments on Provisions

The New Health Law & Small Businesses

The New Health Law & Small Businesses October 2013 1 Goals of the New Health Law Affordable Care Act (ACA) Protect consumers against unfair insurance industry practices Give consumers more insurance options

The New Health Law & Small Businesses October 2013 1 Goals of the New Health Law Affordable Care Act (ACA) Protect consumers against unfair insurance industry practices Give consumers more insurance options

Employer Reporting of Health Coverage Code Sections 6055 & 6056

Brought to you by Hickok & Boardman HR Intelligence Employer Reporting of Health Coverage Code Sections 6055 & 6056 The Affordable Care Act (ACA) created new reporting requirements under Internal Revenue

Brought to you by Hickok & Boardman HR Intelligence Employer Reporting of Health Coverage Code Sections 6055 & 6056 The Affordable Care Act (ACA) created new reporting requirements under Internal Revenue

New York State Department of Financial Services

New York State Department of Financial Services Instructions for the Submission of Individual and Small Business Standalone Dental Plans offered Inside and Outside the New York State of Health (NYSOH)

New York State Department of Financial Services Instructions for the Submission of Individual and Small Business Standalone Dental Plans offered Inside and Outside the New York State of Health (NYSOH)

EMPLOYER & EMPLOYEE CHOICE IN THE SMALL BUSINESS HEALTH OPTIONS PROGRAM (SHOP) EXCHANGE

EXCHANGE") EMPLOYER & EMPLOYEE CHOICE IN THE SMALL BUSINESS HEALTH OPTIONS PROGRAM (SHOP) EXCHANGE Background Analysis for Colorado Health Benefit Exchange (COHBE) This paper outlines some important considerations

EMPLOYER & EMPLOYEE CHOICE IN THE SMALL BUSINESS HEALTH OPTIONS PROGRAM (SHOP) EXCHANGE Background Analysis for Colorado Health Benefit Exchange (COHBE) This paper outlines some important considerations

October 1, 2015. Internal Revenue Service 1111 Constitution Avenue NW Washington, DC 20044. Re: Notice 2015-52. To Whom It May Concern:

October 1, 2015 Internal Revenue Service 1111 Constitution Avenue NW Washington, DC 20044 Re: Notice 2015-52 To Whom It May Concern: On behalf of the American Academy of Actuaries 1 Active Benefits Subcommittee,

October 1, 2015 Internal Revenue Service 1111 Constitution Avenue NW Washington, DC 20044 Re: Notice 2015-52 To Whom It May Concern: On behalf of the American Academy of Actuaries 1 Active Benefits Subcommittee,