August 15, Dear Chair Record and Board Members,

|

|

|

- Frank Morton

- 8 years ago

- Views:

Transcription

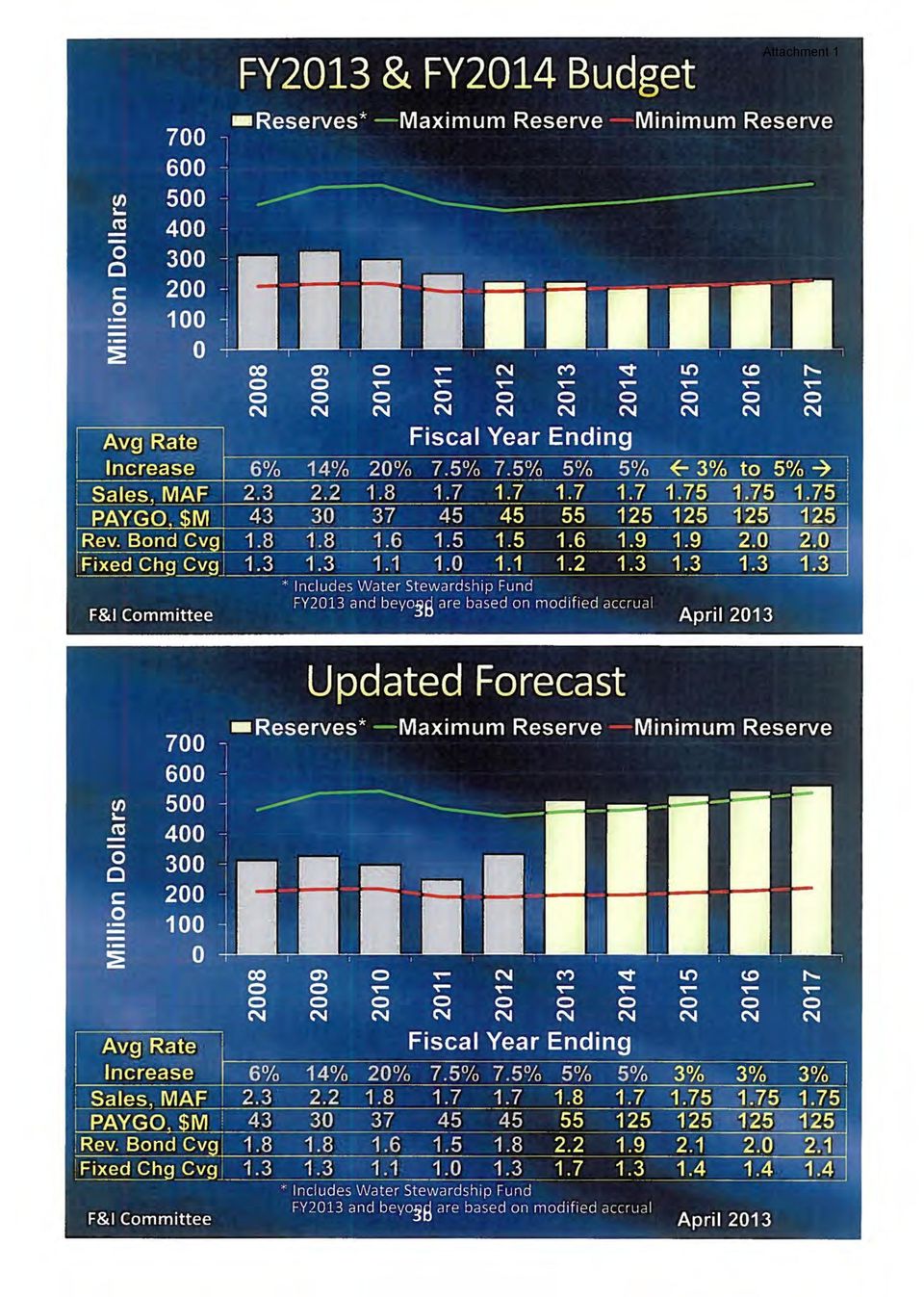

1 August 15, 2015 Randy Record and Members of the Board of s Metropolitan Water District of Southern California P.O. Box Los Angeles, CA RE: Board Memo 5G 2 Adopt (1) the resolution finding that continuing an ad valorem tax rate at the rate levied for fiscal year 2013/14 is essential to Metropolitan's fiscal integrity; and (2) the resolution establishing the tax rate for fiscal year 2014/15 OPPOSE OPTION 1 Dear Chair Record and Board Members, We have reviewed Board Memo 5G 2 and OPPOSE the action recommended to be adopted by the Board of s (i.e., to suspend the tax limitation of Section 124.5, thereby increasing the amount of property tax revenue to be collected by MWD). We have stated our objections previously, each time MWD has proposed to suspend the property tax rate limitations imposed by the Legislature, now embodied in Section of the MWD Act. Copies of our May 14, June 5 and August 16, 2013 letters are attached for your ease of reference (Attachment 1). We SUPPORT adoption of OPTION 2 as described at page one of the Board Memorandum. We OPPOSE the action recommended by staff because MWD has failed to make the requisite factual showing that additional tax revenues are "essential to the fiscal integrity of the District." Such a finding would be impossible to make given that MWD has collected almost $800 million more than necessary to pay the actual expense items included in its adopted budgets over the past three years (even with this spending, MWD still has substantial cash reserves that are nearly at the maximum level prescribed by the Board of s). The fact that the MWD board later chose to spend this rate revenue on unbudgeted expenditures does not change the fact that these revenues were available to the District and therefore the collection of higher taxes was not, and is not necessary, let alone "essential" to the fiscal integrity of the district. MWD has also failed to show why the other fixed revenue options it has available, such as the Readiness to Serve charge and benefit assessments, are not feasible. Indeed, it is clear from the legislative history of SB 1445 that the Legislature intended that MWD would use

.")

2 Chair Record and Members of the Board August 15, 2015 Page 2 these alternatives in lieu of property taxes. See April 21, 1988 Memorandum from MWD's General Counsel to the Subcommittee on Financial Policy (Attachment 2). Board Memorandum 5G 2 is incorrect when it states that MWD's fixed costs, particularly its fixed State Water Contract obligations, are increasing "in ways unforeseen by the Legislature in 1984" (Board Memorandum 5G 2, last paragraph at page 4). To the contrary, MWD's own Report to the California Legislature in Response to AB 322 (March 1984), clearly identified that fixed costs of the State Water Project were expected to increase dramatically (excerpts from the Report Figures 18 and 19 are included as Attachment 3). We also OPPOSE staff recommendation because MWD has failed to provide the public with sufficient information to have a reasonable opportunity to be heard at the public hearing, as required by Section The Board meeting agenda does not even reference the related Committee agenda item. Even if the Board Memorandum is located by a member of the public, it asks them to cull through all of the financial information appearing on MWD's web site, rather than providing an analysis of MWD's current financial condition, demonstrating that increased tax revenues are "essential" to its fiscal integrity within the meaning of the statute passed by the Legislature and signed into law (SB 1445). MWD needs a long range finance plan to address how it will pay for current and anticipated costs of the State Water Project. Revenues from property taxes as one source of revenues, fixed or otherwise should be considered and discussed by the board in the broader context of a plan to ensure MWD s long term fiscal sustainability. Taking action, one year at a time, to increase property tax revenues without a comprehensive long term fiscal strategy and plan does little to assure the public and our ratepayers that MWD is a fiscally prudent and sustainable agency. We would welcome the opportunity to have that dialogue. Sincerely, Michael T. Hogan Keith Lewinger Fern Steiner Yen C. Tu Attachments: 1. Water Authority s Letters to MWD Board (May 14, June 5 and August 16, 2013) 2. Memorandum from MWD's General Counsel to the Subcommittee on Financial Policy (April 21, 1988) 3. MWD Report to California Legislature in Response to AB 322, excerpts Figures 18 and 19 (March 1984)

.")

3 Attachment 1 May 14, 2013 John (Jack) V. Foley and Members of the Board of s Metropolitan Water District of Southern California P.O. Box Los Angeles, CA RE: Board Memo 8 1 Set public hearing to consider suspending Section of the Metropolitan Water District Act to maintain the current ad valorem tax rate Dear Chairman Foley and Members of the Board, We have reviewed Board Memo 8 1 as well as the Legislative History of SB 1445 (Presley), now embodied in Section of the MWD Act. While we support having a long term financing plan to increase MWD s fixed revenues in a manner which is proportional to benefits received by its member agencies, we are troubled by the ad hoc nature of staff s recommendation to schedule a public hearing to suspend tax limitations on the grounds that such action is essential to the fiscal integrity of the district this year. It is particularly difficult to understand the justification for taking this action at the same time MWD is, through its water rates and charges, already collecting hundreds of millions of dollars of revenues far in excess of its actual costs of service. Suspending the tax limitation, in isolation without addressing all of MWD s financial policies, rates, revenues and expenses will only exacerbate the over collection of revenues in FY 2014 beyond what is necessary to meet the agency s expenses. While ad valorem taxes may be an important tool over the long term for ensuring that the cost of MWD s services are shared proportionally by all of those who benefit, Board Memo 8 1 fails to mention other statutory and Constitutional requirements MWD s rates and charges must meet, including but not limited to compliance with Proposition 26. MWD is legally required to align the costs that it incurs with the services it provides. Developing a plan to pay for additional State Water Project costs must be part of that process. A one year suspension of the limitation on the ad valorem tax rate is not a panacea for the hard work and changes that will be needed so that MWD has the funds it needs to pay its future costs from rates that truly represent a fair distribution of its costs. As noted in our letter commenting on the draft Appendix A, we are concerned what the public perception will be of MWD declaring that these ad valorem taxes are essential to the

, now embodied in Section 124.5 of the MWD Act.")

4 Chairman Foley and Members of the Board May 14, 2013 Page 2 Attachment 1 fiscal integrity of the district. Read in the context of the Legislative History of SB 1445, we doubt this is the kind of situation the Legislature envisioned in establishing the limitations of Section Rather than set a public hearing to suspend the tax limitations for one year, we would like to suggest that the board of directors use this time to establish a Fiscal Sustainability Task Force to update MWD s Long Range Finance Plan. The plan would take into account all of MWD s liabilities, and facilities and resource needs and align them to rates and charges including fixed cost recovery that will be proportional to the benefits its member agencies desire and for which they are willing to pay. Sincerely, Keith Lewinger Vincent Mudd Fern Steiner Doug Wilson cc: Jeff Kightlinger, MWD General Manager San Diego County Water Authority Board of s and Member Agencies

5 Attachment 1 June 5, 2013 John (Jack) V. Foley and Members of the Board of s Metropolitan Water District of Southern California P.O. Box Los Angeles, CA June 5, 2013 RE: Board Memo 8 1 Mid cycle Biennial Budget Review and Recommendation for Use of Reserves over Target Water Rate Increases OPPOSE AND REQUEST FOR REFUND TO RATEPAYERS OF EXCESS RESERVES Board Memo 8 2 Suspend the tax rate limitations in Section of the Metropolitan Water District Act to maintain the ad valorem tax rate for fiscal year 2013/14 OPPOSE Dear Chairman Foley and Board Members: In April 2012, this Board voted to raise water rates by 5% for 2013 and 2014 based on the staff s report that limiting water rate increases to no more than 3% would leave MWD unable to pay for critical infrastructure needs on the Colorado River Aqueduct. At that time, MWD staff also represented that the rate increases were based on maintaining reserve levels from 2012 through 2017 at, or close to the board adopted minimum target. As in past years, MWD s estimations of water sales and actual expenditures have proven to be materially different than assumed for budget and rate setting purposes. Far from being unable to pay for critical infrastructure, MWD ended fiscal year 2012 less than three months after adopting rates with an extra $97 million to add to its reserves. According to this month s board report, MWD will, before it ends fiscal year 2013 at the end of this month, add another $217 million to its unrestricted reserves, causing the reserves to exceed the maximum limit by $75 million. In less than 15 months, MWD has collected $314 million more than needed to pay 100% of its budgeted expenditures. Many of the cities we serve are struggling with their own budgets to make ends meet and pay for critical infrastructure. Many of the ratepayers we serve are also struggling to make ends meet during a period of lower incomes and escalating costs. We owe it to our cities and ratepayers to be better stewards of the precious dollars water ratepayers entrust to us when they pay their water bills. We once again call on this Board to establish a Fiscal Sustainability Task Force to develop a long range finance plan and accounting, budget, and rate setting protocols to ensure that every dollar MWD collects is used for its intended purpose, and, that MWD does not collect more money than it really needs.

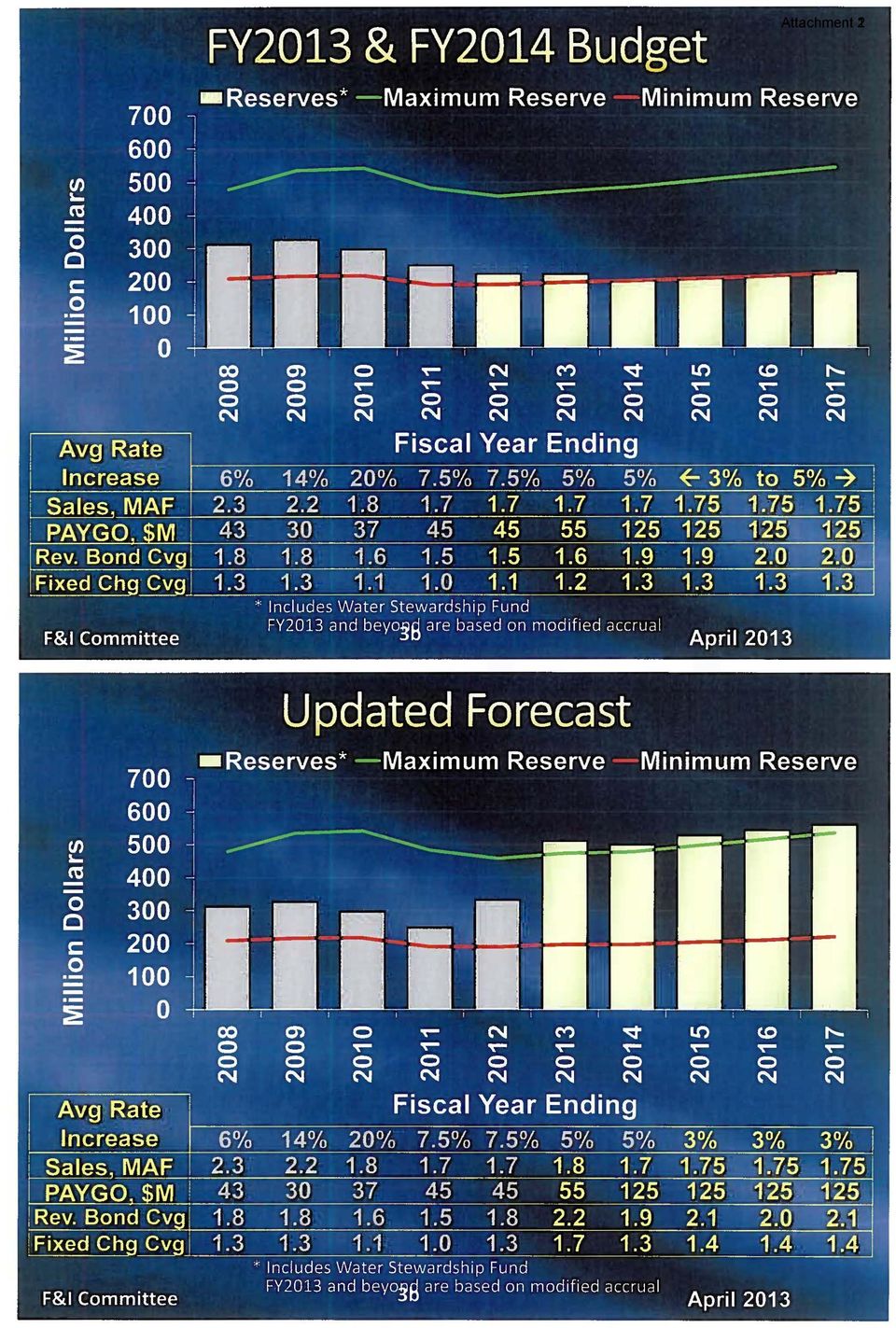

6 Chairman Foley and Members of the Board June 5, 2013 Page 2 Attachment 1 In the meantime, we call on the board to REFUND the $75 million in excess reserves, rather than shift this money to unplanned, unbudgeted expenditures. Attachment 1 to this letter shows approximately 1 how much MWD could refund to each of its member agencies. We also once again call on the Board to act now to REDUCE the planned water rate increase for 2014 from 5% to 3%. Reliance on budget estimates proven to be materially incorrect is unwarranted in the face of the actual facts. For the same reason, we OPPOSE Board Memo 8 2 proposing to suspend the tax rate limitations in Section of the MWD Act. We have reviewed the legislative history of SB We disagree that it was meant to increase Metropolitan s financial flexibility. The clear purpose of the legislation was to limit the imposition of future taxes by MWD, with the ultimate goal that the tax be eliminated. The Legislature instead provided different tools to allow MWD to cover its fixed costs including standby or readiness to serve charges and benefit assessments, as clearly acknowledged in the Board Memo. The fact that MWD has failed to better utilize these and other tools as part of a long range plan to cover its fixed costs does not translate to a need for higher taxes. MWD cannot credibly claim that additional tax revenues of $4.4 million are essential to the fiscal integrity of the District at the very same time it has amassed $549 million in unrestricted cash reserves, exceeding the projected reserve levels forecasted in the adopted biennial budget ($220.8 million) 2 by $328.2 million, and surpassing the board adopted maximum reserve target by $75 million. This issue should also be addressed as part of a long range finance planning process in which all long term costs and sources of revenue may be considered, rather than the ad hoc decision making that is being presented to this board. Finally, there is no factual support for the statements in Board Memo 8 2 that the imposition of a tax increase is necessary to preserve equity across member agencies or that MWD s current rates and charges have been assessed in a manner designed to reflect equity or the actual costs of the services MWD provides. While we support the fiscal objectives as described balance between fixed costs and fixed revenues and equity across member agencies we do not agree that the way to achieve this is to suspend the tax limitation for one year. Instead, MWD should conduct a cost of service study as part of a long range financial planning process in order to ensure accomplishment of these important objectives. Sincerely, Keith Lewinger Vincent Mudd Fern Steiner Attachment 1: Estimated refund of MWD over collection Attachment 2: Comparison of MWD reserves forecast cc: Jeffrey Kightlinger San Diego County Water Authority Board of s 1 Based on 11 months (July 2012 through May 2013) of member agencies payment of rates and charges (data source: MWD WINS). 2 Attachment 2 to this letter shows MWD s projected reserves when the budget was adopted in April 2012 compared to reserves projected in April 2013 (data source: MWD PowerPoint dated 4/8/2013)

7 Estimated Refund of MWD Over Collection Attachment 1 MWD Member Agency Fiscal Year 2013* Total Contribution Rates and Charges (07/12-06/13) Total Contribution (in %) $ 75,000,000 Anaheim $ 14,178, % $ 847,769 Beverly Hills $ 9,133, % $ 546,129 Burbank $ 9,864, % $ 589,832 Calleguas $ 87,186, % $ 5,213,115 Central Basin $ 28,231, % $ 1,688,016 Compton $ 1,364, % $ 81,586 Eastern $ 71,031, % $ 4,247,173 Foothill $ 6,603, % $ 394,817 Fullerton $ 7,611, % $ 455,123 Glendale $ 14,894, % $ 890,597 Inland Empire $ 30,355, % $ 1,815,041 Las Virgenes $ 18,087, % $ 1,081,508 Long Beach $ 25,055, % $ 1,498,148 Los Angeles $ 261,368, % $ 15,627,876 MWDOC $ 149,249, % $ 8,924,009 Pasadena $ 14,646, % $ 875,782 San Diego $ 273,850, % $ 16,374,239 San Fernando $ 72, % $ 4,349 San Marino $ 615, % $ 36,780 Santa Ana $ 8,756, % $ 523,600 Santa Monica $ 5,489, % $ 328,219 Three Valleys $ 47,988, % $ 2,869,350 Torrance $ 13,646, % $ 815,946 Upper San Gabriel $ 8,975, % $ 536,647 West Basin $ 94,668, % $ 5,660,459 Western $ 51,409, % $ 3,073,888 Total $ 1,254,335, % $ 75,000,000 Note: Totals may not foot due to rounding *Based on 11 months (July 2012 through May 2013) of member agencies payment of rates and charges (data source: MWD WINS, June 5, 2013)

8 Attachment 1

9 Attachment 1 August 16, 2013 John (Jack) V. Foley and Members of the Board of s Metropolitan Water District of Southern California P.O. Box Los Angeles, CA RE: Board Memo 5G 2: Adopt resolution maintaining the tax rate for fiscal year 2013/14 OPPOSE Dear Chairman Foley: For the reasons set forth in our letter to you dated June 5, 2013 (copy attached), we OPPOSE the proposed board action to adopt a resolution maintaining the tax rate for fiscal year 2013/14. Among other things, it is clear that this action is not essential to the fiscal integrity of the District, at a time when MWD has amassed hundreds of millions of dollars by overcharging ratepayers utility rates that greatly exceed the costs of the services MWD is providing. MWD has filed a motion for judgment on the pleadings in the Water Authority s litigation challenging its rates, on the grounds that the Constitutional limitations of Proposition 26 do not apply to MWD; that motion is scheduled to be heard September 18. Should MWD not prevail on the motion, we hope that the board of directors will immediately direct staff to conduct a cost of service study as part of a long range financial planning process. This is the right way to ensure accomplishment of the board s objectives, in a manner that is consistent with the legal requirement that MWD charge no more than the proportionate cost of the services it provides to its member agencies. This ad hoc action to suspend the tax rate limitations in Section of the MWD Act for one year is unwarranted, and does nothing to address the long term fiscal challenges confronting MWD. Sincerely, Keith Lewinger Vincent Mudd Fern Steiner Attachment: Water Authority letter to MWD on MWD June 2013 actions re 8 1 and 8 2, dated June 5, 2013

10 Attachment 1 June 5, 2013 John (Jack) V. Foley and Members of the Board of s Metropolitan Water District of Southern California P.O. Box Los Angeles, CA June 5, 2013 RE: Board Memo 8 1 Mid cycle Biennial Budget Review and Recommendation for Use of Reserves over Target Water Rate Increases OPPOSE AND REQUEST FOR REFUND TO RATEPAYERS OF EXCESS RESERVES Board Memo 8 2 Suspend the tax rate limitations in Section of the Metropolitan Water District Act to maintain the ad valorem tax rate for fiscal year 2013/14 OPPOSE Dear Chairman Foley and Board Members: In April 2012, this Board voted to raise water rates by 5% for 2013 and 2014 based on the staff s report that limiting water rate increases to no more than 3% would leave MWD unable to pay for critical infrastructure needs on the Colorado River Aqueduct. At that time, MWD staff also represented that the rate increases were based on maintaining reserve levels from 2012 through 2017 at, or close to the board adopted minimum target. As in past years, MWD s estimations of water sales and actual expenditures have proven to be materially different than assumed for budget and rate setting purposes. Far from being unable to pay for critical infrastructure, MWD ended fiscal year 2012 less than three months after adopting rates with an extra $97 million to add to its reserves. According to this month s board report, MWD will, before it ends fiscal year 2013 at the end of this month, add another $217 million to its unrestricted reserves, causing the reserves to exceed the maximum limit by $75 million. In less than 15 months, MWD has collected $314 million more than needed to pay 100% of its budgeted expenditures. Many of the cities we serve are struggling with their own budgets to make ends meet and pay for critical infrastructure. Many of the ratepayers we serve are also struggling to make ends meet during a period of lower incomes and escalating costs. We owe it to our cities and ratepayers to be better stewards of the precious dollars water ratepayers entrust to us when they pay their water bills. We once again call on this Board to establish a Fiscal Sustainability Task Force to develop a long range finance plan and accounting, budget, and rate setting protocols to ensure that every dollar MWD collects is used for its intended purpose, and, that MWD does not collect more money than it really needs.

11 Chairman Foley and Members of the Board June 5, 2013 Page 2 Attachment 1 In the meantime, we call on the board to REFUND the $75 million in excess reserves, rather than shift this money to unplanned, unbudgeted expenditures. Attachment 1 to this letter shows approximately 1 how much MWD could refund to each of its member agencies. We also once again call on the Board to act now to REDUCE the planned water rate increase for 2014 from 5% to 3%. Reliance on budget estimates proven to be materially incorrect is unwarranted in the face of the actual facts. For the same reason, we OPPOSE Board Memo 8 2 proposing to suspend the tax rate limitations in Section of the MWD Act. We have reviewed the legislative history of SB We disagree that it was meant to increase Metropolitan s financial flexibility. The clear purpose of the legislation was to limit the imposition of future taxes by MWD, with the ultimate goal that the tax be eliminated. The Legislature instead provided different tools to allow MWD to cover its fixed costs including standby or readiness to serve charges and benefit assessments, as clearly acknowledged in the Board Memo. The fact that MWD has failed to better utilize these and other tools as part of a long range plan to cover its fixed costs does not translate to a need for higher taxes. MWD cannot credibly claim that additional tax revenues of $4.4 million are essential to the fiscal integrity of the District at the very same time it has amassed $549 million in unrestricted cash reserves, exceeding the projected reserve levels forecasted in the adopted biennial budget ($220.8 million) 2 by $328.2 million, and surpassing the board adopted maximum reserve target by $75 million. This issue should also be addressed as part of a long range finance planning process in which all long term costs and sources of revenue may be considered, rather than the ad hoc decision making that is being presented to this board. Finally, there is no factual support for the statements in Board Memo 8 2 that the imposition of a tax increase is necessary to preserve equity across member agencies or that MWD s current rates and charges have been assessed in a manner designed to reflect equity or the actual costs of the services MWD provides. While we support the fiscal objectives as described balance between fixed costs and fixed revenues and equity across member agencies we do not agree that the way to achieve this is to suspend the tax limitation for one year. Instead, MWD should conduct a cost of service study as part of a long range financial planning process in order to ensure accomplishment of these important objectives. Sincerely, Keith Lewinger Vincent Mudd Fern Steiner Attachment 1: Estimated refund of MWD over collection Attachment 2: Comparison of MWD reserves forecast cc: Jeffrey Kightlinger San Diego County Water Authority Board of s 1 Based on 11 months (July 2012 through May 2013) of member agencies payment of rates and charges (data source: MWD WINS). 2 Attachment 2 to this letter shows MWD s projected reserves when the budget was adopted in April 2012 compared to reserves projected in April 2013 (data source: MWD PowerPoint dated 4/8/2013)

12 Estimated Refund of MWD Over Collection Attachment 1 MWD Member Agency Fiscal Year 2013* Total Contribution Rates and Charges (07/12-06/13) Total Contribution (in %) $ 75,000,000 Anaheim $ 14,178, % $ 847,769 Beverly Hills $ 9,133, % $ 546,129 Burbank $ 9,864, % $ 589,832 Calleguas $ 87,186, % $ 5,213,115 Central Basin $ 28,231, % $ 1,688,016 Compton $ 1,364, % $ 81,586 Eastern $ 71,031, % $ 4,247,173 Foothill $ 6,603, % $ 394,817 Fullerton $ 7,611, % $ 455,123 Glendale $ 14,894, % $ 890,597 Inland Empire $ 30,355, % $ 1,815,041 Las Virgenes $ 18,087, % $ 1,081,508 Long Beach $ 25,055, % $ 1,498,148 Los Angeles $ 261,368, % $ 15,627,876 MWDOC $ 149,249, % $ 8,924,009 Pasadena $ 14,646, % $ 875,782 San Diego $ 273,850, % $ 16,374,239 San Fernando $ 72, % $ 4,349 San Marino $ 615, % $ 36,780 Santa Ana $ 8,756, % $ 523,600 Santa Monica $ 5,489, % $ 328,219 Three Valleys $ 47,988, % $ 2,869,350 Torrance $ 13,646, % $ 815,946 Upper San Gabriel $ 8,975, % $ 536,647 West Basin $ 94,668, % $ 5,660,459 Western $ 51,409, % $ 3,073,888 Total $ 1,254,335, % $ 75,000,000 Note: Totals may not foot due to rounding *Based on 11 months (July 2012 through May 2013) of member agencies payment of rates and charges (data source: MWD WINS, June 5, 2013)

13 Attachment 2 1

14 Attachment 2

15 Attachment 2

16 Attachment 2

17 Attachment 2

18 Attachment 2

19 Attachment 2

20 Attachment 3

21 Attachment 3

22 Attachment 3

$49,645,000 THE METROPOLITAN WATER DISTRICT OF SOUTHERN CALIFORNIA WATERWORKS GENERAL OBLIGATION REFUNDING BONDS, 2014 SERIES A

NEW ISSUE FULL BOOK-ENTRY Ratings: Fitch AAA Moody s Aaa S&P AAA See Ratings herein. In the opinion of Hawkins Delafield & Wood LLP and Alexis S. M. Chiu, Esq., Co-Bond Counsel to Metropolitan, under existing

NEW ISSUE FULL BOOK-ENTRY Ratings: Fitch AAA Moody s Aaa S&P AAA See Ratings herein. In the opinion of Hawkins Delafield & Wood LLP and Alexis S. M. Chiu, Esq., Co-Bond Counsel to Metropolitan, under existing

June 19, 2013. Administrative and Finance Committee

Attention: Administrative and Finance Committee Adopt the Water Authority s rates and charges for calendar year 2014, amend and restate the amounts and requirements of the System Capacity Charge and Water

Attention: Administrative and Finance Committee Adopt the Water Authority s rates and charges for calendar year 2014, amend and restate the amounts and requirements of the System Capacity Charge and Water

Municipal Water District of Orange County. Regional Urban Water Management Plan

Municipal Water District of Orange County Regional Urban Water Management Plan Municipal Water District of Orange County Water Reliability Challenges and Solutions Matt Stone Associate General Manager

Municipal Water District of Orange County Regional Urban Water Management Plan Municipal Water District of Orange County Water Reliability Challenges and Solutions Matt Stone Associate General Manager

Summary of SB 107 (Budget and Fiscal Review) Chapter 325, Statutes of 2015

Chapter 325, Statutes of 2015") Important Dates Summary of SB 107 (Budget and Fiscal Review) Chapter 325, Statutes of 2015 November 1, 2015: Deadline for Successor Agency (SA) for a Redevelopment Agency (RDA) that was not allocated property

Important Dates Summary of SB 107 (Budget and Fiscal Review) Chapter 325, Statutes of 2015 November 1, 2015: Deadline for Successor Agency (SA) for a Redevelopment Agency (RDA) that was not allocated property

SUPERIOR COURT OF THE STATE OF CALIFORNIA FOR THE COUNTY OF SAN FRANCISCO. Respondents and Defendants.

MORGAN LEWIS & BOCKIUS LLP Colin C. West (Bar No. 4095) Thomas S. Hixson (Bar No. 3033) Three Embarcadero Center San Francisco, California 941-4067 Telephone: (415) 393-00 Facsimile: (415) 393-26 QUINN

MORGAN LEWIS & BOCKIUS LLP Colin C. West (Bar No. 4095) Thomas S. Hixson (Bar No. 3033) Three Embarcadero Center San Francisco, California 941-4067 Telephone: (415) 393-00 Facsimile: (415) 393-26 QUINN

VOLUME NO. 49 OPINION NO. 22

VOLUME NO. 49 OPINION NO. 22 BONDS - County water and sewer district general obligation bond payable by levy on real and personal property in district; COUNTIES - County water and sewer district general

VOLUME NO. 49 OPINION NO. 22 BONDS - County water and sewer district general obligation bond payable by levy on real and personal property in district; COUNTIES - County water and sewer district general

San Diego s Voice for Affordable Housing

July 15, 2015 SANDAG Board of Directors, Chair Jack Dale Transportation Committee, Chair Todd Gloria Regional Planning Committee, Chair Lesa Heebner 401 B Street, Suite 800 RE: Draft San Diego Forward:

July 15, 2015 SANDAG Board of Directors, Chair Jack Dale Transportation Committee, Chair Todd Gloria Regional Planning Committee, Chair Lesa Heebner 401 B Street, Suite 800 RE: Draft San Diego Forward:

153 HOSPITALS FOR CHILDREN S HOSPITAL OF ORANGE COUNTY Sorted by City and Name

Alhambra Hospital Medical Center Beds: 144 Alhambra, CA 91801 Gross Revenue: $172254563 Phone: (626) 570-1606 Discharges: 3952 Patient Days: 34712 Anaheim General Hospital Beds: 143 Anaheim, CA 92804 Gross

Alhambra Hospital Medical Center Beds: 144 Alhambra, CA 91801 Gross Revenue: $172254563 Phone: (626) 570-1606 Discharges: 3952 Patient Days: 34712 Anaheim General Hospital Beds: 143 Anaheim, CA 92804 Gross

Orange Unified School District

Orange Unified School District March 14, 2013 Overview of California Education Finance Keygent LLC 999 N. Sepulveda Blvd., Suite 500 El Segundo, CA 90245 (310) 322 4222 Table of Contents Section I. Introduction

Orange Unified School District March 14, 2013 Overview of California Education Finance Keygent LLC 999 N. Sepulveda Blvd., Suite 500 El Segundo, CA 90245 (310) 322 4222 Table of Contents Section I. Introduction

JOHN CHIANG California State Controller

JOHN CHIANG California State Controller August 15, 2013 Michael Gregoryk, Vice President of Administrative Services Mt. San Antonio Community College District 1100 N. Grand Avenue Walnut, CA 91789 Dear

JOHN CHIANG California State Controller August 15, 2013 Michael Gregoryk, Vice President of Administrative Services Mt. San Antonio Community College District 1100 N. Grand Avenue Walnut, CA 91789 Dear

UC DAVIS: ACADEMIC SENATE

UC DAVIS: ACADEMIC SENATE March 25, 2013 Dear Colleagues, We should expect that the California Legislature and the Governor will continue to be strongly interested in online learning as a way to help solve

UC DAVIS: ACADEMIC SENATE March 25, 2013 Dear Colleagues, We should expect that the California Legislature and the Governor will continue to be strongly interested in online learning as a way to help solve

TRUSTS & ESTATES SECTION

TRUSTS & ESTATES SECTION T HE STATE B AR OF CALIFORN IA APPOINTMENT OF COUNSEL FOR A PROPOSED CONSERVATEE WHO MAY LACK THE CAPACITY TO HIRE COUNSEL LEGISLATIVE PROPOSAL (T&E-2010-06) TO: FROM; Saul Bercovitch,

TRUSTS & ESTATES SECTION T HE STATE B AR OF CALIFORN IA APPOINTMENT OF COUNSEL FOR A PROPOSED CONSERVATEE WHO MAY LACK THE CAPACITY TO HIRE COUNSEL LEGISLATIVE PROPOSAL (T&E-2010-06) TO: FROM; Saul Bercovitch,

Proposed Charter City Measure: Frequently Asked Questions

Proposed Charter City Measure: Frequently Asked Questions The City of Rancho Palos Verdes is currently a general law city. The Rancho Palos Verdes City Council voted to hold a special election on March

Proposed Charter City Measure: Frequently Asked Questions The City of Rancho Palos Verdes is currently a general law city. The Rancho Palos Verdes City Council voted to hold a special election on March

SECTION 7 DEBT MANAGEMENT POLICY LAS VEGAS VALLEY WATER DISTRICT FISCAL YEAR 2015-16 OPERATING AND CAPITAL BUDGET

SECTION 7 DEBT MANAGEMENT POLICY LAS VEGAS VALLEY WATER DISTRICT FISCAL YEAR 2015-16 OPERATING AND CAPITAL BUDGET In Accordance With NRS 350.013 June 30, 2015 7-1 Table of Contents Introduction... 7-3

SECTION 7 DEBT MANAGEMENT POLICY LAS VEGAS VALLEY WATER DISTRICT FISCAL YEAR 2015-16 OPERATING AND CAPITAL BUDGET In Accordance With NRS 350.013 June 30, 2015 7-1 Table of Contents Introduction... 7-3

County of Los Angeles School District General Obligation Bonds White Paper

County of Los Angeles School District General Obligation Bonds White Paper California s Coalition for Adequate School Housing s Fall Conference Tuesday, October 18, 2011 Presented by: Donald Field, Esq.

County of Los Angeles School District General Obligation Bonds White Paper California s Coalition for Adequate School Housing s Fall Conference Tuesday, October 18, 2011 Presented by: Donald Field, Esq.

Proposition 172 Facts A Primer on the Public Safety Augmentation Fund

Coleman Advisory Services www.californiacityfinance.com Proposition 172 Facts A Primer on the Public Safety Augmentation Fund Background: A Sales Tax for Public Safety Born Out of ERAF In 1992, facing

Coleman Advisory Services www.californiacityfinance.com Proposition 172 Facts A Primer on the Public Safety Augmentation Fund Background: A Sales Tax for Public Safety Born Out of ERAF In 1992, facing

COUNTY OF SACRAMENTO CALIFORNIA

COUNTY OF SACRAMENTO CALIFORNIA Attachment II For the Agenda of: September 7, 2011 9:30 A.M.. To: From: Subject: Board of Supervisors Department of Human Assistance Proposal For In-Home Supportive Service

COUNTY OF SACRAMENTO CALIFORNIA Attachment II For the Agenda of: September 7, 2011 9:30 A.M.. To: From: Subject: Board of Supervisors Department of Human Assistance Proposal For In-Home Supportive Service

COUNTY OF LOS ANGELES

COUNTY OF LOS ANGELES DEPARTMENT OF PUBLIC WORKS "To Enrich Lives Through Effective and Caring Service" DEAN D. EFST A THIOU, Acting Director 900 SOUTH FREMONT AVENUE ALHAMBRA, CALIFORNIA 91803-133 I Telephone:

COUNTY OF LOS ANGELES DEPARTMENT OF PUBLIC WORKS "To Enrich Lives Through Effective and Caring Service" DEAN D. EFST A THIOU, Acting Director 900 SOUTH FREMONT AVENUE ALHAMBRA, CALIFORNIA 91803-133 I Telephone:

Curriculum Vitae. 1993- Present Center for Enforcement of Family Support, Law Firm, Managing Partner

Raymond R. Goldstein, Esq. 5855 Green Valley Circle Suite 315 Culver City, CA 90230-6969 Tel: (310) 417-4141 Goldstein@EnforceSupport.com Fax: (310) 417-5060 1993- Present Center for Enforcement of Family

Raymond R. Goldstein, Esq. 5855 Green Valley Circle Suite 315 Culver City, CA 90230-6969 Tel: (310) 417-4141 Goldstein@EnforceSupport.com Fax: (310) 417-5060 1993- Present Center for Enforcement of Family

San Gabriel River Discovery Center Authority. Date: July 31, 2015. Governing Board Members. Mark Stanley, Interim Executive Officer

San Gabriel River Discovery Center Authority Date: July 31, 2015 To: From: Governing Board Members Mark Stanley, Interim Executive Officer Subject: Item 8.d. Consideration of a resolution authorizing an

San Gabriel River Discovery Center Authority Date: July 31, 2015 To: From: Governing Board Members Mark Stanley, Interim Executive Officer Subject: Item 8.d. Consideration of a resolution authorizing an

# 14-28: Water Enterprise Plan Development

City of Beverly Hills Public Works Services Department 345Foothill Road Beverly Hills, CA. 90210 # 14-28: Water Enterprise Plan Development Request for Proposal For Professional Planning and Engineering

City of Beverly Hills Public Works Services Department 345Foothill Road Beverly Hills, CA. 90210 # 14-28: Water Enterprise Plan Development Request for Proposal For Professional Planning and Engineering

How To Organize A Nursing Organization In California

CALIFORNIA ORGANIZATION OF ASSOCIATE DEGREE NURSING PROGRAM DIRECTORS BY-LAWS This organization shall be known as the California Organization of Associate Degree Nursing Program Directors. COMPOSITION

CALIFORNIA ORGANIZATION OF ASSOCIATE DEGREE NURSING PROGRAM DIRECTORS BY-LAWS This organization shall be known as the California Organization of Associate Degree Nursing Program Directors. COMPOSITION

EXHIBIT C UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF FLORIDA

EXHIBIT C UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF FLORIDA If you are not a California resident and you purchased Kashi All Natural / 100% Natural /Nothing Artificial Products between May 3, 2008

EXHIBIT C UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF FLORIDA If you are not a California resident and you purchased Kashi All Natural / 100% Natural /Nothing Artificial Products between May 3, 2008

Notice of Public Hearing on Water Rate Increases

Explanation of Water Increases The Lee Water District is proposing an increase for providing water service to your property and other properties serviced by the District. The District is not proposing

Explanation of Water Increases The Lee Water District is proposing an increase for providing water service to your property and other properties serviced by the District. The District is not proposing

DIVISION OF ACCOUNTS AND REPORTS POLICY AND PROCEDURE MANUAL Revision Date 04/03/00 Filing Number 4,271 Date Issued 04/76 Page 1 of 5 Revisions #

Date Issued 04/76 Page 1 of 5 SUBJECT Fund Accounting PURPOSE Financial transactions for all state agencies should be recorded in self-balancing groups of accounts established as funds by law or administrative

Date Issued 04/76 Page 1 of 5 SUBJECT Fund Accounting PURPOSE Financial transactions for all state agencies should be recorded in self-balancing groups of accounts established as funds by law or administrative

The NEVADA PLAN For School Finance An Overview

The NEVADA PLAN For School Finance An Overview Fiscal Analysis Division Legislative Counsel Bureau 2013 Legislative Session Nevada Plan for School Finance I. Overview of Public K-12 Education Finance

The NEVADA PLAN For School Finance An Overview Fiscal Analysis Division Legislative Counsel Bureau 2013 Legislative Session Nevada Plan for School Finance I. Overview of Public K-12 Education Finance

Proposed Staff Recommendation Consent Calendar for November 29, 2012

Proposed Staff Recommendation Consent Calendar for November 29, 2012 ADMINISTRATIVE AND FINANCE COMMITTEE 9-1. Treasurer s report. Note and file the monthly Treasurer s report. 9-2. Vote Entitlement Resolution

Proposed Staff Recommendation Consent Calendar for November 29, 2012 ADMINISTRATIVE AND FINANCE COMMITTEE 9-1. Treasurer s report. Note and file the monthly Treasurer s report. 9-2. Vote Entitlement Resolution

A Citizen s Guide to PARtiCiPAtion

The Budget Process A Citizen s Guide to PARTICIPATION The law does not permit the committee or individual legislators to use public funds to keep constituents updated on items of interest unless specifically

The Budget Process A Citizen s Guide to PARTICIPATION The law does not permit the committee or individual legislators to use public funds to keep constituents updated on items of interest unless specifically

E-FILED. Attorneys for Plaintiff, Peter MacKinnon, Jr. SUPERIOR COURT OF CALIFORNIA COUNTY OF SANTA CLARA CASE NO. 111 CV 193767

ADAM J. GUTRIDE (State Bar No. ) adam@gutridesafier.com SETH A. SAFIER (State Bar No. ) seth@gutridesafier.com TODD KENNEDY (State Bar No. 0) todd@gutridesafier.com GUTRIDE SAFIER LLP Douglass Street San

ADAM J. GUTRIDE (State Bar No. ) adam@gutridesafier.com SETH A. SAFIER (State Bar No. ) seth@gutridesafier.com TODD KENNEDY (State Bar No. 0) todd@gutridesafier.com GUTRIDE SAFIER LLP Douglass Street San

ATTORNEY-CLIENT MEDIATION AND ARBITRATION SERVICES VOLUNTEER APPLICATION. I want to be a: I am a:

ATTORNEY-CLIENT MEDIATION AND ARBITRATION SERVICES VOLUNTEER APPLICATION I want to be a: I am a: Arbitrator Attorney Mediator Non-Attorney [ ] Mr. [ ] Mrs. [ ] Ms. [ ] Dr. [ ] Other Title: Name: Firm:

ATTORNEY-CLIENT MEDIATION AND ARBITRATION SERVICES VOLUNTEER APPLICATION I want to be a: I am a: Arbitrator Attorney Mediator Non-Attorney [ ] Mr. [ ] Mrs. [ ] Ms. [ ] Dr. [ ] Other Title: Name: Firm:

Retired Employees Association of Orange County, Inc.

Retired Employees Association of Orange County, Inc. PO Box 11787, Santa Ana, CA 92711-1787 Phone: 714 840-3995 www.reaoc.org Email: reaoc@reaoc.org Officers Linda Robinson Doug Storm Co-Presidents June

Retired Employees Association of Orange County, Inc. PO Box 11787, Santa Ana, CA 92711-1787 Phone: 714 840-3995 www.reaoc.org Email: reaoc@reaoc.org Officers Linda Robinson Doug Storm Co-Presidents June

Item #16-5-3. Capitol Valley Regional Service Authority for Freeways and Expressways Draft Grant Funding Program Framework

SAFE Board of Directors Item #16-5-3 Receive and File May 12, 2016 Capitol Valley Regional Service Authority for Freeways and Expressways Draft Grant Funding Program Framework CVR-SAFE is comprised of

SAFE Board of Directors Item #16-5-3 Receive and File May 12, 2016 Capitol Valley Regional Service Authority for Freeways and Expressways Draft Grant Funding Program Framework CVR-SAFE is comprised of

2005 SCHOOL FINANCE LEGISLATION Funding and Distribution

2005 SCHOOL FINANCE LEGISLATION Funding and Distribution RESEARCH REPORT # 3-05 Legislative Revenue Office State Capitol Building 900 Court Street NE, H-197 Salem, Oregon 97301 (503) 986-1266 http://www.leg.state.or.us/comm/lro/home.htm

2005 SCHOOL FINANCE LEGISLATION Funding and Distribution RESEARCH REPORT # 3-05 Legislative Revenue Office State Capitol Building 900 Court Street NE, H-197 Salem, Oregon 97301 (503) 986-1266 http://www.leg.state.or.us/comm/lro/home.htm

AGENDA ITEM BACKGROUND TO: GOVERNING BOARD ITEM NUMBER C.5

59 replacement page TO: GOVERNING BOARD AGENDA ITEM BACKGROUND DATE FROM: PRESIDENT SUBJECT: Selection of Search Consultant for New Superintendent/President REASON FOR BOARD CONSIDERATION ACTION ITEM NUMBER

59 replacement page TO: GOVERNING BOARD AGENDA ITEM BACKGROUND DATE FROM: PRESIDENT SUBJECT: Selection of Search Consultant for New Superintendent/President REASON FOR BOARD CONSIDERATION ACTION ITEM NUMBER

NOTICE OF CLASS ACTION SETTLEMENT Mirkarimi v. Nevada Property 1 LLC dba The Cosmopolitan of Las Vegas S.D. Cal. Case No. 12-cv-02160-BTM (DHB)

") NOTICE OF CLASS ACTION SETTLEMENT Mirkarimi v. Nevada Property 1 LLC dba The Cosmopolitan of Las Vegas S.D. Cal. Case No. 12-cv-02160-BTM (DHB) PLEASE READ THIS NOTICE CAREFULLY. THIS NOTICE CONTAINS IMPORTANT

NOTICE OF CLASS ACTION SETTLEMENT Mirkarimi v. Nevada Property 1 LLC dba The Cosmopolitan of Las Vegas S.D. Cal. Case No. 12-cv-02160-BTM (DHB) PLEASE READ THIS NOTICE CAREFULLY. THIS NOTICE CONTAINS IMPORTANT

Inventory of the Commission for the Review of the Master Plan for Higher Education Records

http://oac.cdlib.org/findaid/ark:/13030/kt2q2nf168 No online items Higher Education Records Archives Staff and Choquette Marrow California State Archives 1020 "O" Street Sacramento, California 95814 Phone:

http://oac.cdlib.org/findaid/ark:/13030/kt2q2nf168 No online items Higher Education Records Archives Staff and Choquette Marrow California State Archives 1020 "O" Street Sacramento, California 95814 Phone:

5.0 FINANCIAL ANALYSIS AND COMPARISON OF ALTERNATIVES

5.0 FINANCIAL ANALYSIS AND COMPARISON OF ALTERNATIVES 5.1 FINANCIAL ANALYSIS The cost of a transportation investment falls into two categories: capital costs, and operating and maintenance (O&M) costs.

5.0 FINANCIAL ANALYSIS AND COMPARISON OF ALTERNATIVES 5.1 FINANCIAL ANALYSIS The cost of a transportation investment falls into two categories: capital costs, and operating and maintenance (O&M) costs.

Associated Students of the University of California, Merced 2014-2015. Resolution #14. Resolution in Support of the California High-Speed Rail Project

Introduced By: Isaias Rumayor III, ASUCM Senator At-Large Authored By: Michael Lomio, ASUCM Senator At-Large Isaias Rumayor III, ASUCM Senator At-Large Sponsored By: Background: The California High-Speed

Introduced By: Isaias Rumayor III, ASUCM Senator At-Large Authored By: Michael Lomio, ASUCM Senator At-Large Isaias Rumayor III, ASUCM Senator At-Large Sponsored By: Background: The California High-Speed

Limitations on Hospital Billing & Collections

Medical Billing Limitations on Hospital Billing & Collections AB 774 requires hospitals to have written financial assistance policies and caps the charges for hospital services for low-to-moderate-income

Medical Billing Limitations on Hospital Billing & Collections AB 774 requires hospitals to have written financial assistance policies and caps the charges for hospital services for low-to-moderate-income

Senate Bill No. 962 CHAPTER 517

Senate Bill No. 962 CHAPTER 517 An act to amend Section 123371 of, and to add Section 1249 to, the Health and Safety Code, relating to umbilical cord blood. [Approved by Governor October 11, 2007. Filed

Senate Bill No. 962 CHAPTER 517 An act to amend Section 123371 of, and to add Section 1249 to, the Health and Safety Code, relating to umbilical cord blood. [Approved by Governor October 11, 2007. Filed

IRS Administrative Appeals Process Procedures

IRS Administrative Appeals Process Procedures Charles P. Rettig Avoiding litigation is often the best choice for a client. The Administrative Appeals process can make it happen. Charles P. Rettig, a partner

IRS Administrative Appeals Process Procedures Charles P. Rettig Avoiding litigation is often the best choice for a client. The Administrative Appeals process can make it happen. Charles P. Rettig, a partner

TRUSTS & ESTATES SECTION

TRUSTS & ESTATES SECTION T HE STATE B AR OF CALIFORN IA HEARING PROCEDURES IN PROBATE PROCEEDINGS LEGISLATIVE PROPOSAL (T&E-2010-10) TO: FROM: Saul Bercovitch, Legislative Counsel State Bar Office of Governmental

TRUSTS & ESTATES SECTION T HE STATE B AR OF CALIFORN IA HEARING PROCEDURES IN PROBATE PROCEEDINGS LEGISLATIVE PROPOSAL (T&E-2010-10) TO: FROM: Saul Bercovitch, Legislative Counsel State Bar Office of Governmental

Easily compare our California HMO networks

Quality health plans & benefits Healthier living Financial well-being Intelligent solutions Easily compare our California networks As of July 1, 2014 Southern California plan and Golden Empire Managed

Quality health plans & benefits Healthier living Financial well-being Intelligent solutions Easily compare our California networks As of July 1, 2014 Southern California plan and Golden Empire Managed

Easily compare our California HMO networks

Quality health plans & benefits Healthier living Financial well-being Intelligent solutions Easily compare our California networks As of October 1, 2014 Southern California IPA name County deductible plan

Quality health plans & benefits Healthier living Financial well-being Intelligent solutions Easily compare our California networks As of October 1, 2014 Southern California IPA name County deductible plan

CalPERS Budget Policy

California Public Employees Retirement System Agenda Item 6a Attachment 2 Page 1 of 6 CalPERS Budget Policy Purpose This document sets forth the budget policy (Policy) to ensure CalPERS budgeting practices

California Public Employees Retirement System Agenda Item 6a Attachment 2 Page 1 of 6 CalPERS Budget Policy Purpose This document sets forth the budget policy (Policy) to ensure CalPERS budgeting practices

NOTICE OF PROPOSED CLASS ACTION SETTLEMENT

NOTICE OF PROPOSED CLASS ACTION SETTLEMENT Hoover v. Hi Tech Pharmacal Co., Inc. Case No. EDCV 13 00097 JGB (OPx) If you purchased a product manufactured by Hi Tech Pharmacal Co., Inc., called Nasal Ease

NOTICE OF PROPOSED CLASS ACTION SETTLEMENT Hoover v. Hi Tech Pharmacal Co., Inc. Case No. EDCV 13 00097 JGB (OPx) If you purchased a product manufactured by Hi Tech Pharmacal Co., Inc., called Nasal Ease

Report of the Legislation Subcommittee. of the Franchise, Distribution and Licensing Committee. of the

Report of the Legislation Subcommittee of the Franchise, Distribution and Licensing Committee of the New York State Bar Association s Business Law Section November 10, 2009 Subcommittee Members: Thomas

Report of the Legislation Subcommittee of the Franchise, Distribution and Licensing Committee of the New York State Bar Association s Business Law Section November 10, 2009 Subcommittee Members: Thomas

Southern California Mediation Association 24th Annual Conference Welcome Cocktail Reception and Dinner - November 2, 2012

Southern California Mediation Association 24th Annual Conference Welcome Cocktail Reception and Dinner - November 2, 2012 Roger Wolfson Roger Wolfson is a writer in Los Angeles, California, who currently

Southern California Mediation Association 24th Annual Conference Welcome Cocktail Reception and Dinner - November 2, 2012 Roger Wolfson Roger Wolfson is a writer in Los Angeles, California, who currently

Curriculum Vitae ABOUT SUSAN D. GREEN, M.S., CRC, ABVE, FVE

Curriculum Vitae ABOUT SUSAN D. GREEN, M.S., CRC, ABVE, FVE Susan Green completed her Bachelor of Arts degree in Sociology at Ramapo College in Mahwah, New Jersey in 1974. She received her Master of Science

Curriculum Vitae ABOUT SUSAN D. GREEN, M.S., CRC, ABVE, FVE Susan Green completed her Bachelor of Arts degree in Sociology at Ramapo College in Mahwah, New Jersey in 1974. She received her Master of Science

Using a Receiver to Sell Real Property to Satisfy a Judgment by Patrick Bulmer of California Receivership Services

Making the Case: Using a Receiver to Sell Real Property to Satisfy a Judgment by Patrick Bulmer of California Receivership Services Introduction The statutory remedy of selling real property under a writ

Making the Case: Using a Receiver to Sell Real Property to Satisfy a Judgment by Patrick Bulmer of California Receivership Services Introduction The statutory remedy of selling real property under a writ

SB 878 (LEYVA) WORK HOURS: SCHEDULING OPPOSE JOB KILLER

WORK HOURS: SCHEDULING OPPOSE JOB KILLER") SB 878 (LEYVA) WORK HOURS: SCHEDULING OPPOSE JOB KILLER SB 878 (LEYVA) WORK HOURS: SCHEDULING OPPOSE JOB KILLER April 7, 2016 TO: FROM: Members, Senate Committee on Labor and Industrial Relations California

SB 878 (LEYVA) WORK HOURS: SCHEDULING OPPOSE JOB KILLER SB 878 (LEYVA) WORK HOURS: SCHEDULING OPPOSE JOB KILLER April 7, 2016 TO: FROM: Members, Senate Committee on Labor and Industrial Relations California

BUSINESS LAW SECTION

BUSINESS LAW SECTION CORPORATIONS COMMITTEE T HE STATE BAR OF CALIFORNIA 180 Howard Street San Francisco, CA 94105-1639 http://www.calbar.org/buslaw/corporations STATUTORY CLOSE CORPORATIONS LEGISLATIVE

BUSINESS LAW SECTION CORPORATIONS COMMITTEE T HE STATE BAR OF CALIFORNIA 180 Howard Street San Francisco, CA 94105-1639 http://www.calbar.org/buslaw/corporations STATUTORY CLOSE CORPORATIONS LEGISLATIVE

Small Business Loan Guarantee Program Report

GOVERNOR S OFFICE OF BUSINESS AND ECONOMIC DEVELOPMENT STATE OF CALIFORNIA OFFICE OF GOVERNOR EDMUND G. BROWN JR. Small Business Loan Guarantee Program Report Budget Item # 0509-001-0001 Edmund G. Brown

GOVERNOR S OFFICE OF BUSINESS AND ECONOMIC DEVELOPMENT STATE OF CALIFORNIA OFFICE OF GOVERNOR EDMUND G. BROWN JR. Small Business Loan Guarantee Program Report Budget Item # 0509-001-0001 Edmund G. Brown

PREPARED REBUTTAL TESTIMONY OF LEE SCHAVRIEN SAN DIEGO GAS & ELECTRIC COMPANY

Application No: Exhibit No.: Witness: A.0-0-01 Lee Schavrien In the Matter of the Application of San Diego Gas & Electric Company (U 0 E for Authorization to Recover Unforeseen Liability Insurance Premium

Application No: Exhibit No.: Witness: A.0-0-01 Lee Schavrien In the Matter of the Application of San Diego Gas & Electric Company (U 0 E for Authorization to Recover Unforeseen Liability Insurance Premium

NOTICE OF CLASS ACTION SETTLEMENT GRECO V. SELECTION MANAGEMENT SYSTEMS, INC. San Diego Superior Court Case No. 37-2014-00085074-CU-BT-CTL

NOTICE OF CLASS ACTION SETTLEMENT GRECO V. SELECTION MANAGEMENT SYSTEMS, INC. San Diego Superior Court Case No. 37-2014-00085074-CU-BT-CTL The Superior Court has authorized this notice. This is not a solicitation

NOTICE OF CLASS ACTION SETTLEMENT GRECO V. SELECTION MANAGEMENT SYSTEMS, INC. San Diego Superior Court Case No. 37-2014-00085074-CU-BT-CTL The Superior Court has authorized this notice. This is not a solicitation

PROP. 41 (June, 2014): VETERANS HOUSING AND HOMELESS PREVENTION BOND ACT

: VETERANS HOUSING AND HOMELESS PREVENTION BOND ACT") Board of Directors Policy Committee: Home Ownership Housing Committee (Information only) Level of Government Committee: Legislative Committee (Information Only) May 2, 2014 PROP. 41 (June, 2014): VETERANS

Board of Directors Policy Committee: Home Ownership Housing Committee (Information only) Level of Government Committee: Legislative Committee (Information Only) May 2, 2014 PROP. 41 (June, 2014): VETERANS

Budget Introduction Proposed Budget

Budget Introduction Proposed Budget INTRO - 1 INTRO - 2 Summary of the Budget and Accounting Structure The City of Beverly Hills uses the same basis for budgeting as for accounting. Governmental fund financial

Budget Introduction Proposed Budget INTRO - 1 INTRO - 2 Summary of the Budget and Accounting Structure The City of Beverly Hills uses the same basis for budgeting as for accounting. Governmental fund financial

LOCAL AGENCY FORMATION COMMISSION COUNTY OF SAN BERNARDINO

LOCAL AGENCY FORMATION COMMISSION COUNTY OF SAN BERNARDINO 215 North D Street, Suite 204, San Bernardino, CA 92415-0490 (909) 383-9900 Fax (909) 383-9901 E-MAIL: lafco@lafco.sbcounty.gov www.sbclafco.org

LOCAL AGENCY FORMATION COMMISSION COUNTY OF SAN BERNARDINO 215 North D Street, Suite 204, San Bernardino, CA 92415-0490 (909) 383-9900 Fax (909) 383-9901 E-MAIL: lafco@lafco.sbcounty.gov www.sbclafco.org

4. The legislature envisioned that mediators be paid for their services.

SAN FERNANDO VALLEY BAR ASSOCIATION ALTERNATIVE DISPUTE RESOLUTION SECTION EXECUTIVE COMMITTEE C/O CHARLES B. PARSELLE 14320 VENTURA BLVD., #408 SHERMAN OAKS, CA 91423 Telephone: 818.781.5810 Facsimile:

SAN FERNANDO VALLEY BAR ASSOCIATION ALTERNATIVE DISPUTE RESOLUTION SECTION EXECUTIVE COMMITTEE C/O CHARLES B. PARSELLE 14320 VENTURA BLVD., #408 SHERMAN OAKS, CA 91423 Telephone: 818.781.5810 Facsimile:

Certified Taxation Law Specialist, State Bar of California Board of Legal Specialization, 1991

KNEAVE RIGGALL Tax Law Pasadena, CA 91030 Adjunct Professor, Tax LL.M. Program (taught "Partnership Taxation I", "Corporate Taxation I" and, twice, "Taxation of S Corporations"), Loyola Law School, 2001

KNEAVE RIGGALL Tax Law Pasadena, CA 91030 Adjunct Professor, Tax LL.M. Program (taught "Partnership Taxation I", "Corporate Taxation I" and, twice, "Taxation of S Corporations"), Loyola Law School, 2001

THE STATE EDUCATION DEPARTMENT Room 475 EBA Office of Educational Management Services Albany, NY 12234 (518) 474-6541

474-6541") THE STATE EDUCATION DEPARTMENT Room 475 EBA Office of Educational Management Services Albany, NY 12234 (518) 474-6541 Fund Balance - Reservations and Designations The following Reserve Funds are available

THE STATE EDUCATION DEPARTMENT Room 475 EBA Office of Educational Management Services Albany, NY 12234 (518) 474-6541 Fund Balance - Reservations and Designations The following Reserve Funds are available

Metropolitan Setting l

Metropolitan Setting l GENERAL CHARACTERISTICS Los Angeles lies at the heart of one of the most complex metropolitan regions in the United States. As a major center of commerce, finance, and industry in

Metropolitan Setting l GENERAL CHARACTERISTICS Los Angeles lies at the heart of one of the most complex metropolitan regions in the United States. As a major center of commerce, finance, and industry in

Colantuono & Levin, PC 11406 Pleasant Valley Road Penn Valley, CA 95946-9024 Main: (530) 432-7357 FAX: (530) 432-7356

432-7357 FAX: (530) 432-7356") Michael G. Colantuono MColantuono@CLLAW.US (530) 432-7359 Colantuono & Levin, PC 11406 Pleasant Valley Road Penn Valley, CA 95946-9024 Main: (530) 432-7357 FAX: (530) 432-7356 WWW.CLLAW.US COURT SLIGHTLY

Michael G. Colantuono MColantuono@CLLAW.US (530) 432-7359 Colantuono & Levin, PC 11406 Pleasant Valley Road Penn Valley, CA 95946-9024 Main: (530) 432-7357 FAX: (530) 432-7356 WWW.CLLAW.US COURT SLIGHTLY

2016 SCHEDULED ELECTIONS (As of August 17, 2016)

") COUNTY OF LOS ANGELES REGISTRAR-RECORDER/COUNTY CLERK 2016 SCHEDULED ELECTIONS (As of August 17, 2016) ELECTION INFORMATION AND PREPARATION DIVISION ELECTION RR/CC CLOSE ELECTION CONTESTS PROJECT CONDUCTED

COUNTY OF LOS ANGELES REGISTRAR-RECORDER/COUNTY CLERK 2016 SCHEDULED ELECTIONS (As of August 17, 2016) ELECTION INFORMATION AND PREPARATION DIVISION ELECTION RR/CC CLOSE ELECTION CONTESTS PROJECT CONDUCTED

Submit a Valid Claim Form Deadline: February 12, 2016 Ask to be excluded Deadline: November 24, 2015. Object Deadline: November 24, 2015

NOTICE OF CLASS ACTION SETTLEMENT California Superior Court, County of Los Angeles IF FIRE INSURANCE EXCHANGE APPLIED DEPRECIATION WHEN CALCULATING A PAYMENT MADE TO YOU ON A PROPERTY LOSS INSURANCE CLAIM,

NOTICE OF CLASS ACTION SETTLEMENT California Superior Court, County of Los Angeles IF FIRE INSURANCE EXCHANGE APPLIED DEPRECIATION WHEN CALCULATING A PAYMENT MADE TO YOU ON A PROPERTY LOSS INSURANCE CLAIM,

SUPERIOR COURT OF THE STATE OF CALIFORNIA COUNTY OF ORANGE ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) )

) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) )") SUPERIOR COURT OF THE STATE OF CALIFORNIA COUNTY OF ORANGE CHRISTOPHER LEVANOFF; ALISON DIAZ; ANDREW GAXIOLA; JENNA STEED; ROES 1 through 25, inclusive, as individuals and on behalf of all similarly situated

SUPERIOR COURT OF THE STATE OF CALIFORNIA COUNTY OF ORANGE CHRISTOPHER LEVANOFF; ALISON DIAZ; ANDREW GAXIOLA; JENNA STEED; ROES 1 through 25, inclusive, as individuals and on behalf of all similarly situated

1st Session 110 483 AUTHORIZING APPROPRIATIONS FOR THE SAN GABRIEL BASIN RESTORATION FUND

110TH CONGRESS REPORT " HOUSE OF REPRESENTATIVES! 1st Session 110 483 AUTHORIZING APPROPRIATIONS FOR THE SAN GABRIEL BASIN RESTORATION FUND DECEMBER 11, 2007. Committed to the Committee of the Whole House

110TH CONGRESS REPORT " HOUSE OF REPRESENTATIVES! 1st Session 110 483 AUTHORIZING APPROPRIATIONS FOR THE SAN GABRIEL BASIN RESTORATION FUND DECEMBER 11, 2007. Committed to the Committee of the Whole House

September 19, 2005. Mr. Edward Cox Chairman State University Construction Fund State University Plaza Albany, New York 12201

ALAN G. HEVESI COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER September 19, 2005 Mr. Edward Cox Chairman State University Construction Fund State

ALAN G. HEVESI COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER September 19, 2005 Mr. Edward Cox Chairman State University Construction Fund State

City of Hercules Agenda Item Transmittal

City of Hercules Agenda Item Transmittal Meeting October 27, 2009 Agenda Item Number: IX.6 Agenda Item Wording: Adopt A Resolution Approving The Form Of And Authorizing The Execution And Delivery Of A

City of Hercules Agenda Item Transmittal Meeting October 27, 2009 Agenda Item Number: IX.6 Agenda Item Wording: Adopt A Resolution Approving The Form Of And Authorizing The Execution And Delivery Of A

INTERNATIONAL ASSOCIATION OF PLUMBING AND MECHANICAL OFFICIALS

INTERNATIONAL ASSOCIATION OF PLUMBING AND MECHANICAL OFFICIALS Codes Department 5001 E. Philadelphia St. Ontario, CA 91761 USA PHONE 800-854-2766 FAX 909-472-4265 http://www.iapmo.org November 23, 2005

INTERNATIONAL ASSOCIATION OF PLUMBING AND MECHANICAL OFFICIALS Codes Department 5001 E. Philadelphia St. Ontario, CA 91761 USA PHONE 800-854-2766 FAX 909-472-4265 http://www.iapmo.org November 23, 2005

(310) 543-9900 (310) 379-3620, (310) 370-5902, (213) 745-6434, (213) 222-1237, (562) 388-7652 info@1736fcc.org

543-9900 (310) 379-3620, (310) 370-5902, (213) 745-6434, (213) 222-1237, (562) 388-7652 info@1736fcc.org") Los Angeles Violence Prevention Resource Directory Domestic Violence Victim/Prevention Services 1736 Family Crisis Center South Bay Office 21707 Hawthorne Blvd., Suite 300 Torrance, CA 90503 (310) 543-9900

Los Angeles Violence Prevention Resource Directory Domestic Violence Victim/Prevention Services 1736 Family Crisis Center South Bay Office 21707 Hawthorne Blvd., Suite 300 Torrance, CA 90503 (310) 543-9900

This Class Action Settlement May Affect Your Rights A Court authorized this Notice. This is not a solicitation from a lawyer.

Garrett Kacsuta, et al., v. Lenovo (United States) Inc. Case No. 13-cv-00316-CJC (RNBx) OWNERS OF CERTAIN MODELS OF LENOVO BRAND ULTRABOOK COMPUTERS MAY CLAIM SETTLEMENT BENEFITS. This Class Action Settlement

Garrett Kacsuta, et al., v. Lenovo (United States) Inc. Case No. 13-cv-00316-CJC (RNBx) OWNERS OF CERTAIN MODELS OF LENOVO BRAND ULTRABOOK COMPUTERS MAY CLAIM SETTLEMENT BENEFITS. This Class Action Settlement

Would These Keywords Help Your Business? divorce lawyer 90254 90254 divorce lawyer divorce lawyer hermosa beach divorce lawyer hermosa beach ca

divorce lawyer 90254 90254 divorce lawyer divorce lawyer hermosa beach divorce lawyer hermosa beach ca divorce lawyer hermosa beach california divorce lawyer in hermosa beach divorce lawyer in hermosa

divorce lawyer 90254 90254 divorce lawyer divorce lawyer hermosa beach divorce lawyer hermosa beach ca divorce lawyer hermosa beach california divorce lawyer in hermosa beach divorce lawyer in hermosa

11-15463-shl Doc 8096 Filed 05/10/13 Entered 05/10/13 11:28:56 Main Document Pg 1 of 8

Pg 1 of 8 UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF NEW YORK ---------------------------------------------------------------x : In re : Chapter 11 Case No. : AMR CORPORATION, et al., : 11-15463

Pg 1 of 8 UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF NEW YORK ---------------------------------------------------------------x : In re : Chapter 11 Case No. : AMR CORPORATION, et al., : 11-15463

Admin 101 Participant Directory 2014

Counselor, Outreach, Degree and Transfer Pasadena City College Associate Director Rancho Santiago CCD Coordinator of Outreach & Recruitment LA City College Business Services Supervisor San Jose City College

Counselor, Outreach, Degree and Transfer Pasadena City College Associate Director Rancho Santiago CCD Coordinator of Outreach & Recruitment LA City College Business Services Supervisor San Jose City College

NINTH JUDICIAL CIRCUIT, IN AND FOR ORANGE AND OSCEOLA COUNTIES, FLORIDA

ADMINISTRATIVE ORDER NO. 2012-03 IN THE CIRCUIT COURT OF THE NINTH JUDICIAL CIRCUIT, IN AND FOR ORANGE AND OSCEOLA COUNTIES, FLORIDA ADMINISTRATIVE ORDER ESTABLISHING NINTH JUDICIAL CIRCUIT COURT CIRCUIT

ADMINISTRATIVE ORDER NO. 2012-03 IN THE CIRCUIT COURT OF THE NINTH JUDICIAL CIRCUIT, IN AND FOR ORANGE AND OSCEOLA COUNTIES, FLORIDA ADMINISTRATIVE ORDER ESTABLISHING NINTH JUDICIAL CIRCUIT COURT CIRCUIT

Superior Court of California County of Los Angeles

ROBERT LEVENTER COURT COMMISSIONER NORTHEAST DISTRICT- PASADENA 300 EAST WALNUT STREET, DEPARTMENT 271 PASADENA, CA 91101 TELEPHONE: (626) 356-5671 RLEVENTE@LASUPERIORCOURT.ORG Superior Court of California

ROBERT LEVENTER COURT COMMISSIONER NORTHEAST DISTRICT- PASADENA 300 EAST WALNUT STREET, DEPARTMENT 271 PASADENA, CA 91101 TELEPHONE: (626) 356-5671 RLEVENTE@LASUPERIORCOURT.ORG Superior Court of California

County of Sonoma Agenda Item Summary Report

County of Sonoma Agenda Item Summary Report Agenda Item Number: 39 (This Section for use by Clerk of the Board Only.) Clerk of the Board 575 Administration Drive Santa Rosa, CA 95403 To: Sonoma County

County of Sonoma Agenda Item Summary Report Agenda Item Number: 39 (This Section for use by Clerk of the Board Only.) Clerk of the Board 575 Administration Drive Santa Rosa, CA 95403 To: Sonoma County

Enrollment 40,211 (as of 8/13/15) Students from over 100 countries. MSI, HSI, and ANAPISI. Largest number of students with disabilities served in US

Students from over 100 countries. MSI, HSI, and ANAPISI. Largest number of students with disabilities served in US") CSU COUNSELORS CONFERENCE 2015 Enrollment 40,211 (as of 8/13/15) Students from over 100 countries MSI, HSI, and ANAPISI Largest number of students with disabilities served in US Academic programs 70 undergraduate

CSU COUNSELORS CONFERENCE 2015 Enrollment 40,211 (as of 8/13/15) Students from over 100 countries MSI, HSI, and ANAPISI Largest number of students with disabilities served in US Academic programs 70 undergraduate

Local Government Bankruptcy in California: Questions and Answers

POLICY BRIEF Local Government Bankruptcy in California: Questions and Answers MAC Taylor Legislative Analyst August 7, 2012 Introduction Unanticipated events or prolonged imbalances between resources and

POLICY BRIEF Local Government Bankruptcy in California: Questions and Answers MAC Taylor Legislative Analyst August 7, 2012 Introduction Unanticipated events or prolonged imbalances between resources and

CITY OF ORANGE PROPOSED INCREASE OF WATER RATES AND CHARGES FREQUENTLY ASKED QUESTIONS (FAQ) REGARDING ORANGE S PROPOSED WATER RATES AND CHARGES

REGARDING ORANGE S PROPOSED WATER RATES AND CHARGES") CITY OF ORANGE PROPOSED INCREASE OF WATER RATES AND CHARGES On Tuesday March 27, 2012, the Orange City Council will hold a public hearing to consider a rate adjustment for water service rates and charges.

CITY OF ORANGE PROPOSED INCREASE OF WATER RATES AND CHARGES On Tuesday March 27, 2012, the Orange City Council will hold a public hearing to consider a rate adjustment for water service rates and charges.

The Rubicon Project, Inc. Corporate Governance Guidelines

The Rubicon Project, Inc. Corporate Governance Guidelines These Corporate Governance Guidelines reflect the corporate governance practices established by the Board of Directors (the Board ) of The Rubicon

The Rubicon Project, Inc. Corporate Governance Guidelines These Corporate Governance Guidelines reflect the corporate governance practices established by the Board of Directors (the Board ) of The Rubicon

Client Assistance Program (CAP) Michael Thomas-Region one Leilani Pfeifer-Region two

Michael Thomas-Region one Leilani Pfeifer-Region two") Client Assistance Program (CAP) Michael Thomas-Region one Leilani Pfeifer-Region two Agenda Overview of the Client Assistance Program 1 2 3 4 Rehabilitation Act of 1973 Vocational Rehabilitation Process

Client Assistance Program (CAP) Michael Thomas-Region one Leilani Pfeifer-Region two Agenda Overview of the Client Assistance Program 1 2 3 4 Rehabilitation Act of 1973 Vocational Rehabilitation Process

An act to amend Section 11836 of the Health and Safety Code, and to amend Section 23103.5 of the Vehicle Code, relating to vehicles.

BILL NUMBER: AB 2802 CHAPTERED BILL TEXT CHAPTER 103 FILED WITH SECRETARY OF STATE JULY 10, 2008 APPROVED BY GOVERNOR JULY 10, 2008 PASSED THE SENATE JUNE 26, 2008 PASSED THE ASSEMBLY MAY 1, 2008 INTRODUCED

BILL NUMBER: AB 2802 CHAPTERED BILL TEXT CHAPTER 103 FILED WITH SECRETARY OF STATE JULY 10, 2008 APPROVED BY GOVERNOR JULY 10, 2008 PASSED THE SENATE JUNE 26, 2008 PASSED THE ASSEMBLY MAY 1, 2008 INTRODUCED

COURT OF APPEAL, FOURTH APPELLATE DISTRICT DIVISION ONE STATE OF CALIFORNIA

Filed 4/11/13 CERTIFIED FOR PUBLICATION COURT OF APPEAL, FOURTH APPELLATE DISTRICT DIVISION ONE STATE OF CALIFORNIA BATTAGLIA ENTERPRISES, INC., D063076 Petitioner, v. SUPERIOR COURT OF SAN DIEGO COUNTY,

Filed 4/11/13 CERTIFIED FOR PUBLICATION COURT OF APPEAL, FOURTH APPELLATE DISTRICT DIVISION ONE STATE OF CALIFORNIA BATTAGLIA ENTERPRISES, INC., D063076 Petitioner, v. SUPERIOR COURT OF SAN DIEGO COUNTY,

CALIFORNIA INFRASTRUCTURE AND ECONOMIC DEVELOPMENT BANK INVESTMENT POLICY

CALIFORNIA INFRASTRUCTURE AND ECONOMIC DEVELOPMENT BANK INVESTMENT POLICY UPDATED INVESTMENT POLICY DATED February 24, 2015 Section California Infrastructure and Economic Development Bank Investment Policy

CALIFORNIA INFRASTRUCTURE AND ECONOMIC DEVELOPMENT BANK INVESTMENT POLICY UPDATED INVESTMENT POLICY DATED February 24, 2015 Section California Infrastructure and Economic Development Bank Investment Policy

143 FERC 61,246 UNITED STATES OF AMERICA FEDERAL ENERGY REGULATORY COMMISSION

143 FERC 61,246 UNITED STATES OF AMERICA FEDERAL ENERGY REGULATORY COMMISSION Before Commissioners: Jon Wellinghoff, Chairman; Philip D. Moeller, John R. Norris, Cheryl A. LaFleur, and Tony Clark. San

143 FERC 61,246 UNITED STATES OF AMERICA FEDERAL ENERGY REGULATORY COMMISSION Before Commissioners: Jon Wellinghoff, Chairman; Philip D. Moeller, John R. Norris, Cheryl A. LaFleur, and Tony Clark. San

NILA 2015 Region 2 Meeting

REGION 2 NILA 2015 Region 2 Meeting Heidy Arriola, RVP Anthony Becerril, RSR Ricardo Medina, RGR REGION 2 WHOSE HOUSE??!!!!!! TWO S HOUSE!!!!! AGENDA SHPE Mission & Vision Team Introductions Region 2 Overview

REGION 2 NILA 2015 Region 2 Meeting Heidy Arriola, RVP Anthony Becerril, RSR Ricardo Medina, RGR REGION 2 WHOSE HOUSE??!!!!!! TWO S HOUSE!!!!! AGENDA SHPE Mission & Vision Team Introductions Region 2 Overview

NEW AUTHORITY FOR IMPLEMENTING TECHNOLOGY IN DISCOVERY

1 NEW AUTHORITY FOR IMPLEMENTING TECHNOLOGY IN DISCOVERY The challenge to the bench and bar is to use technology to achieve cost effective discovery and litigation. In January, California lawyers and judges

1 NEW AUTHORITY FOR IMPLEMENTING TECHNOLOGY IN DISCOVERY The challenge to the bench and bar is to use technology to achieve cost effective discovery and litigation. In January, California lawyers and judges

WORKERS' COMPENSATION COMMISSION

WORKERS' COMPENSATION COMMISSION Enabling Laws Act 236 of 214 Constitution of Arkansas Amendment 7 Constitution of Arkansas Amendment 26 History and Organization Workers' compensation insurance is directed

WORKERS' COMPENSATION COMMISSION Enabling Laws Act 236 of 214 Constitution of Arkansas Amendment 7 Constitution of Arkansas Amendment 26 History and Organization Workers' compensation insurance is directed

CITY OF MORENO VALLEY, CALIFORNIA COMMUNITY FACILITIES DISTRICT NO. 3

CITY OF MORENO VALLEY, CALIFORNIA COMMUNITY FACILITIES DISTRICT NO. 3 CONTINUING DISCLOSURE REPORT FOR FISCAL YEAR 2012/13 THESE BONDS HAVE BEEN FULLY REDEMED Report Date: March 2014 Prepared by: FINANCIAL

CITY OF MORENO VALLEY, CALIFORNIA COMMUNITY FACILITIES DISTRICT NO. 3 CONTINUING DISCLOSURE REPORT FOR FISCAL YEAR 2012/13 THESE BONDS HAVE BEEN FULLY REDEMED Report Date: March 2014 Prepared by: FINANCIAL

DEBT MANAGEMENT POLICY AND PROPOSED CERTIFICATES OF PARTICIPATION (COPs) TRANSACTION

TRANSACTION") DEBT MANAGEMENT POLICY AND PROPOSED CERTIFICATES OF PARTICIPATION (COPs) TRANSACTION Los Angeles Unified School District Office of the Chief Financial Officer Background Since 1990, District has issued

DEBT MANAGEMENT POLICY AND PROPOSED CERTIFICATES OF PARTICIPATION (COPs) TRANSACTION Los Angeles Unified School District Office of the Chief Financial Officer Background Since 1990, District has issued

As a current or former non-exempt PPG employee, you may be entitled to receive money from a class action settlement.

NOTICE OF PROPOSED CLASS ACTION SETTLEMENT AND HEARING DATE FOR COURT APPROVAL Penaloza, et al., v. PPG Industries, Inc., Case No. BC471369 As a current or former non-exempt PPG employee, you may be entitled

NOTICE OF PROPOSED CLASS ACTION SETTLEMENT AND HEARING DATE FOR COURT APPROVAL Penaloza, et al., v. PPG Industries, Inc., Case No. BC471369 As a current or former non-exempt PPG employee, you may be entitled

Assessment and Collection of Selected Penalties. Workers Compensation Board

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Assessment and Collection of Selected Penalties Workers Compensation Board Report 2011-S-3

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Assessment and Collection of Selected Penalties Workers Compensation Board Report 2011-S-3

AGENDA REGULAR MEETING SERVICE AUTHORITY FOR FREEWAYS AND EXPRESSWAYS

AGENDA REGULAR MEETING SERVICE AUTHORITY FOR FREEWAYS AND EXPRESSWAYS DATE: Thursday, November 20, 2014 3:00 P.M. LOCATION: Board of Supervisors Chambers, 481 Fourth Street, Hollister, CA 95023 DIRECTORS:

AGENDA REGULAR MEETING SERVICE AUTHORITY FOR FREEWAYS AND EXPRESSWAYS DATE: Thursday, November 20, 2014 3:00 P.M. LOCATION: Board of Supervisors Chambers, 481 Fourth Street, Hollister, CA 95023 DIRECTORS:

The IRS has attempted to balance enforcement

Practice By Charles P. Rettig A Fresh Start for Struggling Taxpayers Charles P. Rettig is a Principal with Hochman, Salkin, Rettig, Toscher & Perez, P.C. in Beverly Hills, California. Mr. Rettig is Chair

Practice By Charles P. Rettig A Fresh Start for Struggling Taxpayers Charles P. Rettig is a Principal with Hochman, Salkin, Rettig, Toscher & Perez, P.C. in Beverly Hills, California. Mr. Rettig is Chair

Senate Education Committee. Senator Jack Scott, Chair Wednesday April 13, 2005 hearing State Capitol, Room 4203

Senate Education Committee Senator Jack Scott, Chair Wednesday April 13, 2005 hearing State Capitol, Room 4203 testimony in opposition to SB 724 (Scott) California State University: doctoral degrees Dr.

Senate Education Committee Senator Jack Scott, Chair Wednesday April 13, 2005 hearing State Capitol, Room 4203 testimony in opposition to SB 724 (Scott) California State University: doctoral degrees Dr.

SBA Turf Special Report for Business

12/11/2006 Aggressive Lenders Redrawing SBA Turf SPECIAL REPORT: Overall volume off but targeted programs clicking Scroll down to CDC By HOWARD FINE LOS ANGELES BUSINESS JOURNAL STAFF Hawthorne businessman

12/11/2006 Aggressive Lenders Redrawing SBA Turf SPECIAL REPORT: Overall volume off but targeted programs clicking Scroll down to CDC By HOWARD FINE LOS ANGELES BUSINESS JOURNAL STAFF Hawthorne businessman

Sweetwater Union High School District. Proposition O Bond Fund Performance Audit Report For the Fiscal Year Ended June 30, 2014.

Proposition O Bond Fund Performance Audit Report For the Fiscal Year Ended June 30, 2014 Prepared by: MOSS ADAMS LLP 9665 Granite Ridge Drive, Suite 600 Santa Diego, CA 92123 March 31, 2015 Board of Trustees

Proposition O Bond Fund Performance Audit Report For the Fiscal Year Ended June 30, 2014 Prepared by: MOSS ADAMS LLP 9665 Granite Ridge Drive, Suite 600 Santa Diego, CA 92123 March 31, 2015 Board of Trustees

AGENDA. Liability claims, increase from $4,999.99 to $25,000. Worker s Compensation claims, increase from $4,999.99 to $75,000.

1. CALL TO ORDER AGENDA MEETING OF THE FINANCE COMMITTEE OF THE SANTA BARBARA METROPOLITAN TRANSIT DISTRICT A PUBLIC AGENCY TUESDAY, JULY 28, 2015 10:00 A.M. SANTA BARBARA MTD CONFERENCE ROOM (UPSTAIRS)

1. CALL TO ORDER AGENDA MEETING OF THE FINANCE COMMITTEE OF THE SANTA BARBARA METROPOLITAN TRANSIT DISTRICT A PUBLIC AGENCY TUESDAY, JULY 28, 2015 10:00 A.M. SANTA BARBARA MTD CONFERENCE ROOM (UPSTAIRS)