Guide to IRS Collections. Tax Payment Options and Solutions. Offer in Compromise 4/30/2015

|

|

|

- Nora Wilcox

- 8 years ago

- Views:

Transcription

1 Guide to IRS Collections Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation May 4, 2015 Tax Payment Options and Solutions When to submit an Offer in Compromise Releasing a Federal Tax Lien Installment Agreements when your client would qualify Innocent Spouse issues Offer in Compromise An offer in compromise allows your client to settle your tax debt for less than the full amount they owe It may be a legitimate option if they can't pay the full tax liability, or doing so creates a financial hardship IRS considers your clients unique set of facts and circumstances: Ability to pay; Income; Expenses; and Asset equity. IRS will generally approve an offer in compromise when the amount offered represents the most we can expect to collect within a reasonable period of time 1

2 First Step Explore all other payment options before submitting an offer in compromise The Offer in Compromise program is not for everyone and the application does not ensure the IRS will accept the offer IRS will Evaluate the offer, AND Validate the application information Can the Client Pay Via Installment Agreement Lump sum Generally, if the client can pay by the above means and Offer in Compromise will not be accepted Conditions Doubt as to Liability Doubt as to Collectability Exceptional Circumstances No open bankruptcy proceeding in progress Initial offer payment, unless the client meets the low income certification 2

3 The IRS may accept an OIC based on three grounds: First, the IRS can accept a compromise if there is doubt as to liability. A compromise meets this only when there is a genuine dispute as to the existence or amount of the correct tax debt under the law. Second, the IRS can accept a compromise if there is doubt that the amount owed is fully collectible. Doubt as to collectability exists in any case where the taxpayer's assets and income are less than the full amount of the tax liability. Third, the IRS can accept a compromise based on effective tax administration. An offer may be accepted based on effective tax administration when there is no doubt that the tax is legally owed and that the full amount owed can be collected, but requiring payment in full would either create an economic hardship or would be unfair and inequitable because of exceptional circumstances. Doubt as to Liability A taxpayer submitting an OIC based on doubt as to liability must file a Form 656 L, Offer in Compromise (Doubt as to Liability) Doubt as to Collectability When submitting an OIC based on doubt as to collectability or based on effective tax administration, taxpayers must use the most current version of Form 656, Offer in Compromise Also submit Form 433 A (OIC) (PDF), Collection Information Statement for Wage Earners and Self Employed Individuals And/or Form 433 B (OIC), Collection Information Statement for Businesses 3

4 Cost In general, a taxpayer must submit a $186 application fee with the Form 656. Payment Options Lump Sum Cash: Submit an initial payment of 20 percent of the total offer amount with the application Wait for written acceptance, then pay the remaining balance of the offer in five or fewer payments. Periodic Payment: Submit the initial payment with the application Continue to pay the remaining balance in monthly installments while the IRS considers your offer If accepted, continue to pay monthly until it is paid in full, generally within 24 months Failure to make these payments will cause the offer to be returned Low Income Certification If your client meets the Low Income Certification guidelines chart in instructions Based on family size and where the taxpayer lives Do not send the application fee or the initial payment Do not make monthly installments during the evaluation of the offer See the application package for more details 4

5 Chart Non Refundable Deposit All deposits and fess are non refundable Deposits are applied to the tax due Requirements for Evaluations of the OIC Make sure you are eligible The client must be current with all filing and payment requirements The client is not eligible if they are in an open bankruptcy proceeding Use the Offer in Compromise Pre Qualifier on IRS.GOV to confirm their eligibility and prepare a preliminary proposal 5

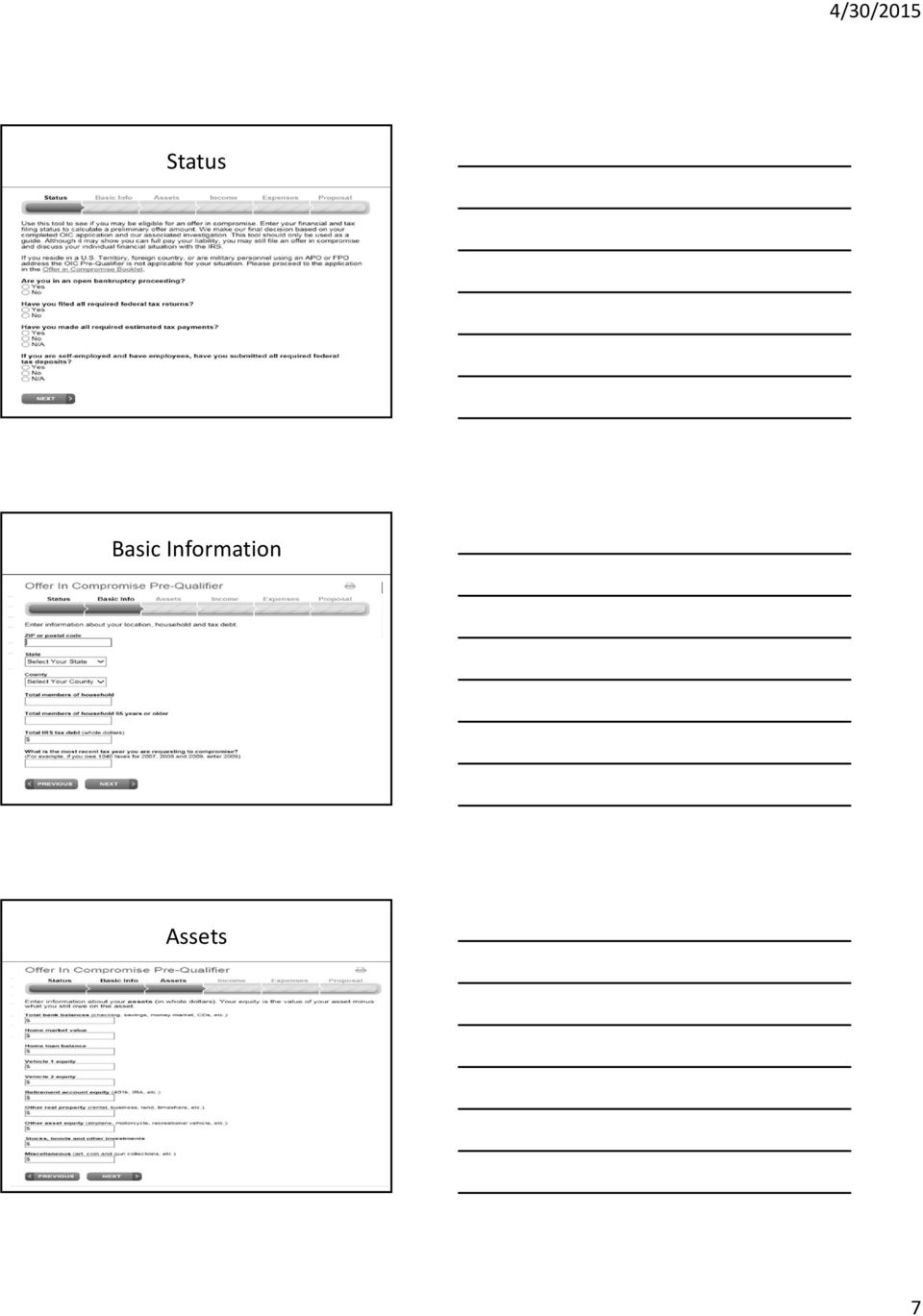

6 Offer In Compromise Pre Qualifier 6 sections need to be completed Status Basic Information Assets Income Expenses Proposal IRS will look at: Ability to Pay Income and Expenses Asset Equity Notice No credit card debt is allowed Full disclosure is required IRS does have means to verify the information IRS can adjust the monthly expenses to allow only for local standards (Drakes and Taylor, T.C. Memo ) Application Generic No personal information of identity is input Have all available information present that is needed to complete the pre qualifier Your client must certify that They have filed all tax returns legally required to be filed They have made all required federal employment tax deposits if applicable They have made all required estimated tax deposits as required 6

7 Status Basic Information Assets 7

8 Income Expenses Example 8

9 Proposal Not Qualified for an OIC Business Forms 433 9

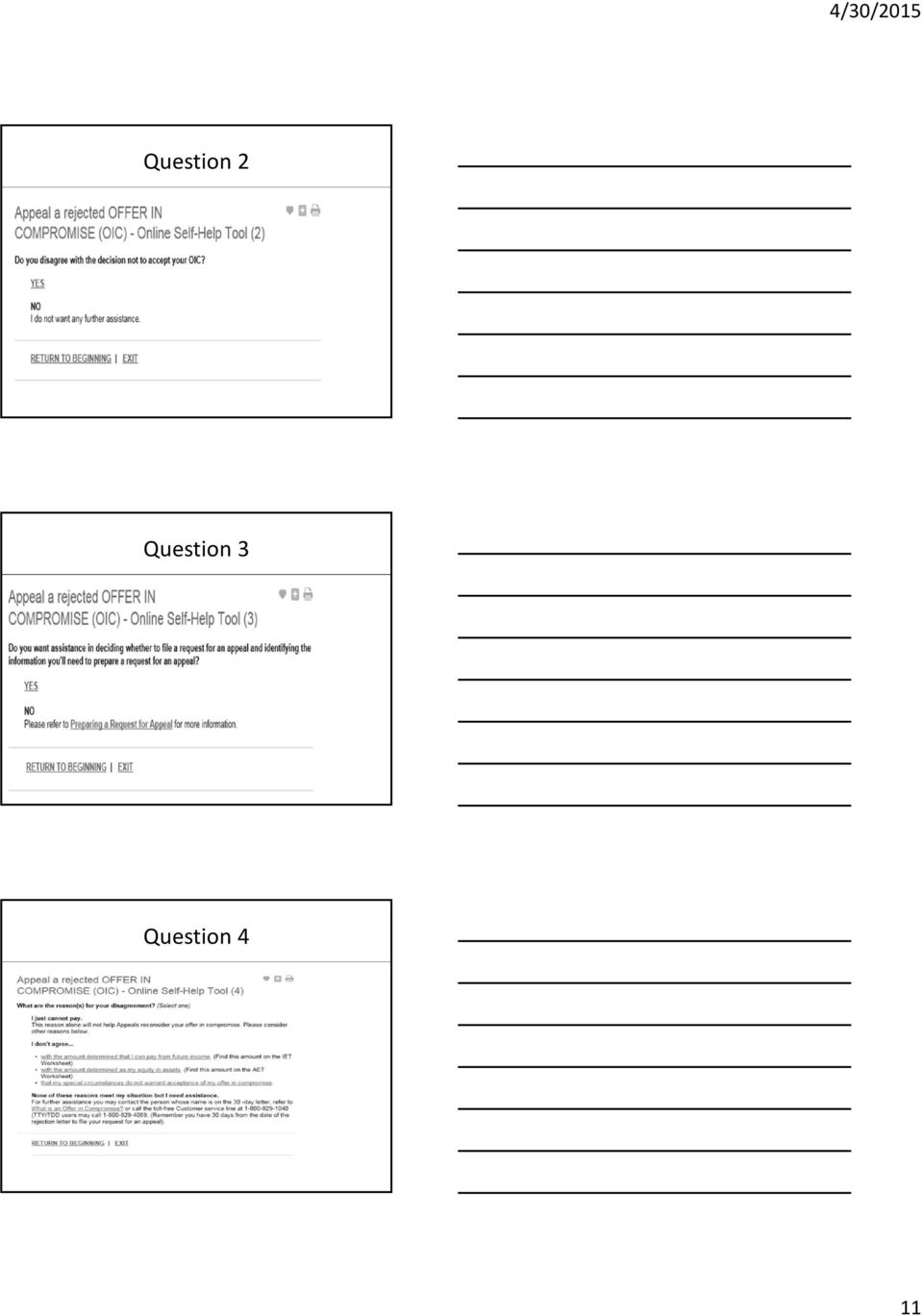

10 Forms 433 Individual Application Rejected Appeal a rejected OFFER IN COMPROMISE (OIC) Online Self Help Tool (START) Before you begin... The tool is for your client if the following statements apply: They received a 30 day letter rejecting an OIC, They are a W 2 wage earner, They do not own rental property, and They are not self employed. Question 1 10

11 Question 2 Question 3 Question 4 11

12 Form If your client received a letter notifying them that the offer was rejected you have 30 days to request an appeal of the decision You can request an Appeals conference by preparing either a Form 13711, Request for Appeal of Offer in Compromise, or a separate letter with the following information included: Name, address, SSN, and daytime telephone number A statement that you want to appeal the IRS findings to the Appeals office A copy of your rejected offer letter Tax period or years involved A list of the specific items you don't agree with and a statement of why you don't agree with each item Any additional information you want Appeals to consider The facts supporting your position on any issue that you do not agree with The law or authority, if any, on which you are relying Sign the written protest, stating this it is true under the penalties of perjury 30 days Must request within the 30 day timeframe Remember you have 30 days from the date of the rejection letter to file your request for an appeal. If you request an appeal and are not able to reach an agreement with the Officer of Appeals, you may be eligible for consideration of post Appeals mediation under Announcement IRS will reject offer if beyond 30 days Be specific in addressing the issues Announcement Test of Procedures for Mediation and Arbitration for Offer in Compromise and Trust Fund Recovery Penalty Cases in Appeals Section 7123 requires the Internal Revenue Service to prescribe procedures by which a taxpayer or the Office of Appeals may request non binding mediation on any issue unresolved at the conclusion of Appeals procedures, or unsuccessful attempts to enter into a closing agreement under section 7121 or a compromise under section 7122 The announcement modifies several other announcements and extended the two year test of the mediation and arbitration procedures for Offer in Compromise (OIC) and Trust Fund Recovery Penalty (TFRP) cases that are under the jurisdiction of the Office of Appeals until December 31,

13 ALERT Revised Offer in Compromise forms and instructions will be available in January 2015 Use the most current revision of Form 656 B in preparing and submitting the offer Use of outdated forms and instructions may cause a delay in the processing of the offer application Scoop Dates for Post Filing Season May 13, 2015 May 27, 2015 UP Coming Tax Law Webinars May 2015 Defense of Marriage Act (DOMA) May 5, Noon to 1:00 An overview of the DOMA decision and how it affects filing status, community property state issues, the marital deduction for same sex couples, fringe benefit issues, gift tax issues and a multitude of other issues directly related to this Supreme Court decision. The class is designed to provide the necessary information to inform your client of their federal tax responsibilities. Free: It s Time for Your Repair Regulations Questions and Concerns May 12, Noon to 2:00 It is time for you to ask the questions you have concerning the new repair regulations. What difficulties did you have during filing season where further clarification is needed? Pose the questions and we will do our best to sort through the facts and get you an answer. We will also update you on any new IRS procedures. 13

14 UP Coming Tax Law Webinars May 2015 Return Preparer Fraud and Remedies for the Client May 26, Noon 1:00 You have a new client and it is evident that serious mistakes have been made and now you, the new tax preparer must fix the mess another person has created. How can you assist this client and what IRS procedures are available for resolving your client s issues, when preparer fraud is present. How the Taxpayer Advocate can assist and what forms the client needs to file to establish they are a victim of fraud will also be discussed. Identity Theft May 27, Noon to 1:00 An overview of the Identity Theft process and how you can assist your client with getting the return processed and the refund issued. New AgLaw Webinars AgLaw Webinar: A Pipeline May Be Coming Through Your Property May 21, Noon to 1:00 A Texas energy company is hoping to build a 1,134 mile underground pipeline to transport crude oil from North Dakota's Bakken oil fields through 18 Iowa counties en route to Illinois. This seminar will discuss the legal issues landowners face, both during negotiations for a voluntary easement or during a possible eminent domain proceeding. We will also discuss the tax implications of granting an easement to a utility company. AgLaw Webinar: Can I Fly an Unmanned Aerial Vehicle Over My Farm? May 13, Noon 1:00 The uses for unmanned aerial vehicles (UAVs) in agricultural operations are numerous. Unfortunately the authorization to begin using this technology has been slow in coming. This webinar will address the legal issues associated with using a UAV in your farming operation and discuss the current status of regulations to govern the commercial use of UAVs. New AgLaw Webinars AgLaw Webinar: What You Need to Know about Ag Liens May 14, Noon to 1:00 This class will review procedures to perfect and collect on a landlord s lien. We will also discuss other agricultural liens and how to respond if your client has a lien against his property. AgLaw Webinar: Establishing an LLC May 28, Noon 1:00 This webinar will provide an introduction to Limited Liability Companies for practitioners. The webinar will discuss when an LLC may be a good choice for your client, what documents you must file at federal and state levels, and other issues related to creating the LLC. This webinar will also link practitioners to helpful forms. 14

15 CALT Website Tour of the CALT Website CALT Staff Roger A. McEowen CALT Director and is a Leonard Dolezal Professor in Agricultural Law mceowen@iastate.edu Phone: (515) Fax: (515) Kristine A. Tidgren Staff Attorney E mail: ktidgren@iastate.edu Phone: (515) Fax: (515)

16 CALT Staff Kristy S. Maitre Tax Specialist E mail: ksmaitre@iastate.edu Phone: (515) Fax: (515) Tiffany Kayser Program Administrator tlkayser@iastate.edu Phone: (515) Fax: (515)

Federal Income Tax Payment Options

Federal Income Tax Payment Options Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation June 24, 2015 What Has to Happen First? Agenda The tax must be assessed or the client can pre pay

Federal Income Tax Payment Options Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation June 24, 2015 What Has to Happen First? Agenda The tax must be assessed or the client can pre pay

LLC Classification. Tax Law Basics of an LLC Kristy S. Maitre, Tax Specialist Center for Agricultural Law and Taxation

Tax Law Basics of an LLC Kristy S. Maitre, Tax Specialist Center for Agricultural Law and Taxation What is a Limited Liability Company? A creation of an entity based on state law varies from state to state

Tax Law Basics of an LLC Kristy S. Maitre, Tax Specialist Center for Agricultural Law and Taxation What is a Limited Liability Company? A creation of an entity based on state law varies from state to state

GOVERNMENT OF THE DISTRICT OF COLUMBIA OFFICE OF THE CHIEF FINANCIAL OFFICER OFFICE OF TAX AND REVENUE OFFER IN COMPROMISE. Form OTR-10 Booklet

GOVERNMENT OF THE DISTRICT OF COLUMBIA OFFICE OF THE CHIEF FINANCIAL OFFICER OFFICE OF TAX AND REVENUE OFFER IN COMPROMISE Form OTR-10 Booklet Content What is an Offer in Compromise (OIC)? What is the

GOVERNMENT OF THE DISTRICT OF COLUMBIA OFFICE OF THE CHIEF FINANCIAL OFFICER OFFICE OF TAX AND REVENUE OFFER IN COMPROMISE Form OTR-10 Booklet Content What is an Offer in Compromise (OIC)? What is the

Offer in Compromise Program Updates

Offer in Compromise Program Updates Presenter name: Joseph Lewandoski Presenter title: Senior Stakeholder Liaison Small Business/Self-Employed Division Date What is an Offer in Compromise? An agreement

Offer in Compromise Program Updates Presenter name: Joseph Lewandoski Presenter title: Senior Stakeholder Liaison Small Business/Self-Employed Division Date What is an Offer in Compromise? An agreement

ACA Penalties Individual Shared Responsibility Provision. Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 9, 2014

ACA Penalties Individual Shared Responsibility Provision Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 9, 2014 Enrollment period You can generally buy Marketplace health

ACA Penalties Individual Shared Responsibility Provision Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 9, 2014 Enrollment period You can generally buy Marketplace health

Affordable Care Act Exemptions and Affordability Information. Exemptions. Exemption from What? 10/2/2014

Affordable Care Act Exemptions and Affordability Information Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 14, 2014 Exemptions What qualifies for an exemption? How is the

Affordable Care Act Exemptions and Affordability Information Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 14, 2014 Exemptions What qualifies for an exemption? How is the

The Scoop. Agenda. IRS Changes It s Tune 7/1/2015. Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 1, 2015

The Scoop Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 1, 2015 Agenda Refund Problem POA s New Letter to Practitioners Address Changes Electronic Tax Administration Advisory

The Scoop Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 1, 2015 Agenda Refund Problem POA s New Letter to Practitioners Address Changes Electronic Tax Administration Advisory

Partnership Form K 1. Purpose of the Form K 1. Basis Losses 7/8/2015

Partnership Form K 1 Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 8, 2015 Purpose of the Form K 1 The partnership uses Schedule K 1 to report your share of the partnership's

Partnership Form K 1 Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 8, 2015 Purpose of the Form K 1 The partnership uses Schedule K 1 to report your share of the partnership's

Small Business Seminar Offer in Compromise. Felicia Branch August 15, 2015

Small Business Seminar Offer in Compromise Felicia Branch August 15, 2015 Collection Power of the IRS What can they do? For how long? What alternatives does the taxpayer have? Can the taxpayer appeal a

Small Business Seminar Offer in Compromise Felicia Branch August 15, 2015 Collection Power of the IRS What can they do? For how long? What alternatives does the taxpayer have? Can the taxpayer appeal a

The Health Insurance Premium Tax Credit. Topics. What is the Premium Tax Credit? 10/1/2014

The Health Insurance Premium Tax Credit Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 8, 2014 Topics Definitions Premium Tax Credit Basics Determining the amount of the

The Health Insurance Premium Tax Credit Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 8, 2014 Topics Definitions Premium Tax Credit Basics Determining the amount of the

Payment Alternatives When You Owe the IRS

Payment Alternatives When You Owe the IRS Internal Revenue Service Small Business/Self-Employed Division Traci Suiter September 12, 2012 The information contained in this presentation is current as of

Payment Alternatives When You Owe the IRS Internal Revenue Service Small Business/Self-Employed Division Traci Suiter September 12, 2012 The information contained in this presentation is current as of

AGOSTINO & ASSOCIATES, P.C. IRS Collections. Presented by : Frank Agostino

AGOSTINO & ASSOCIATES, P.C. IRS Collections Presented by : Frank Agostino DISCLAIMER: The following materials and accompanying Access MCLE, LLC audio program are for instructional purposes only. Nothing

AGOSTINO & ASSOCIATES, P.C. IRS Collections Presented by : Frank Agostino DISCLAIMER: The following materials and accompanying Access MCLE, LLC audio program are for instructional purposes only. Nothing

Matthew Von Schuch. Tax Attorney and CPA

Matthew Von Schuch Tax Attorney and CPA 7 METHODS TO RESOLVE IRS TAX DEBT Offer in Compromise Settling tax debt for less than owed Installment Agreement A payment plan for tax debts Non- Collectable Status

Matthew Von Schuch Tax Attorney and CPA 7 METHODS TO RESOLVE IRS TAX DEBT Offer in Compromise Settling tax debt for less than owed Installment Agreement A payment plan for tax debts Non- Collectable Status

Offer in Compromise (Doubt as to Liability)

") Form 656-L Offer in Compromise (Doubt as to Liability) CONTENTS What you need to know...2 Important information...2 Form 656-L...5 IRS contact information If you have questions about qualifying for an

Form 656-L Offer in Compromise (Doubt as to Liability) CONTENTS What you need to know...2 Important information...2 Form 656-L...5 IRS contact information If you have questions about qualifying for an

Legal Aid Society of Orange County Low Income Taxpayer Clinic

Legal Aid Society of Orange County Low Income Taxpayer Clinic Presented by: Renato L. Izquieta, Esq. Legal Aid Society of Orange County Presented by: Richard Silva, Paralegal Legal Aid Society of Orange

Legal Aid Society of Orange County Low Income Taxpayer Clinic Presented by: Renato L. Izquieta, Esq. Legal Aid Society of Orange County Presented by: Richard Silva, Paralegal Legal Aid Society of Orange

Offer in Compromise. Worksheets to calculate an acceptable offer amount using Form 433-A and/or 433-B and Publication 1854*

Department of Treasury Internal Revenue Service Form 656 (Rev. 1-97) Catalog Number 16728N Form 656 Offer in Compromise What you should know before submitting an offer in compromise Worksheets to calculate

Department of Treasury Internal Revenue Service Form 656 (Rev. 1-97) Catalog Number 16728N Form 656 Offer in Compromise What you should know before submitting an offer in compromise Worksheets to calculate

This Offer in Compromise package includes: Information you need to know before submitting an offer in compromise

www.irs.gov Form 656 (Rev. 5-2001) Catalog Number 16728N Form 656 Offer in Compromise This Offer in Compromise package includes: Information you need to know before submitting an offer in compromise Instructions

www.irs.gov Form 656 (Rev. 5-2001) Catalog Number 16728N Form 656 Offer in Compromise This Offer in Compromise package includes: Information you need to know before submitting an offer in compromise Instructions

DET710. A Guide to Tax Resolution: Solving IRS Problems - 12 Hours

DET710 A Guide to Tax Resolution: Solving IRS Problems - 12 Hours Course Objectives and Outline Chapter 1 - IRS Overview and Taxpayer Rights 1. List the mission of the IRS. 2. State the role of Taxpayer

DET710 A Guide to Tax Resolution: Solving IRS Problems - 12 Hours Course Objectives and Outline Chapter 1 - IRS Overview and Taxpayer Rights 1. List the mission of the IRS. 2. State the role of Taxpayer

Part III Administrative, Procedural, and Miscellaneous. 26 CFR 601.203: Offers in Compromise (Also Part I, 7122; 301.7122-1) Rev.

Rev.") Part III Administrative, Procedural, and Miscellaneous 26 CFR 601.203: Offers in Compromise (Also Part I, 7122; 301.7122-1) Rev. Proc 2003-71 SECTION 1. PURPOSE The purpose of this revenue procedure is

Part III Administrative, Procedural, and Miscellaneous 26 CFR 601.203: Offers in Compromise (Also Part I, 7122; 301.7122-1) Rev. Proc 2003-71 SECTION 1. PURPOSE The purpose of this revenue procedure is

The Scoop. Social Security News 1/20/2016. Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation January 20, 2016

The Scoop Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation January 20, 2016 Social Security News 2015 was a special year for Social Security They launched their very first blog, Social

The Scoop Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation January 20, 2016 Social Security News 2015 was a special year for Social Security They launched their very first blog, Social

BRIEF SUMMARY: The bill would amend the Revenue Act to create an "offer-in-compromise" program with Department of Treasury.

Legislative Analysis OFFER-IN-COMPROMISE TAXPAYER AGREEMENTS House Bill 4003 (reported from committee without amendment) Sponsor: Rep. John Walsh Committee: Tax Policy Mary Ann Cleary, Director Phone:

Legislative Analysis OFFER-IN-COMPROMISE TAXPAYER AGREEMENTS House Bill 4003 (reported from committee without amendment) Sponsor: Rep. John Walsh Committee: Tax Policy Mary Ann Cleary, Director Phone:

The IRS has attempted to balance enforcement

Practice By Charles P. Rettig A Fresh Start for Struggling Taxpayers Charles P. Rettig is a Principal with Hochman, Salkin, Rettig, Toscher & Perez, P.C. in Beverly Hills, California. Mr. Rettig is Chair

Practice By Charles P. Rettig A Fresh Start for Struggling Taxpayers Charles P. Rettig is a Principal with Hochman, Salkin, Rettig, Toscher & Perez, P.C. in Beverly Hills, California. Mr. Rettig is Chair

The Nuts and Bolts of Handling a Pro Bono Tax Controversy Case. Presented by The ABA Section of Taxation

The Nuts and Bolts of Handling a Pro Bono Tax Controversy Case Presented by The ABA Section of Taxation Panelists Caroline Ciraolo - Rosenberg, Martin, Greenberg, LLP, Baltimore, Maryland Catherine Engell

The Nuts and Bolts of Handling a Pro Bono Tax Controversy Case Presented by The ABA Section of Taxation Panelists Caroline Ciraolo - Rosenberg, Martin, Greenberg, LLP, Baltimore, Maryland Catherine Engell

Offer in Compromise. What you need to know... Paying for your offer... How to apply... Completing the application package... 3

Form 656 Booklet Offer in Compromise CONTENTS What you need to know...... 1 Paying for your offer...... 2 How to apply... 3 Completing the application package... 3 Important information... 4 Removable

Form 656 Booklet Offer in Compromise CONTENTS What you need to know...... 1 Paying for your offer...... 2 How to apply... 3 Completing the application package... 3 Important information... 4 Removable

The IRS Resolution Guide for Owner-Operators

The IRS Resolution Guide for Owner-Operators Learn ways to avoid penalties, how the IRS deals with unpaid taxes, the resolution options available, and how to take action to resolve your debt. PRESENTED

The IRS Resolution Guide for Owner-Operators Learn ways to avoid penalties, how the IRS deals with unpaid taxes, the resolution options available, and how to take action to resolve your debt. PRESENTED

Guide to IRS Collections

CPE/CE 1 Credit Hour Guide to IRS Collections Tax Payment Options and Solutions 2012 Tax Year Interactive Self-Study CPE/CE Course Course Overview Program Content: Publication Date: September 2012. Expiration

CPE/CE 1 Credit Hour Guide to IRS Collections Tax Payment Options and Solutions 2012 Tax Year Interactive Self-Study CPE/CE Course Course Overview Program Content: Publication Date: September 2012. Expiration

Offer in Compromise. Attach Application Fee and Payment (check or money order) here. IRS Received Date. (Rev. May 2012) Section 3

here. IRS Received Date. (Rev. May 2012) Section 3") Form 656 (Rev. May 2012) Department of the Treasury Internal Revenue Service Offer in Compromise Attach Application Fee and Payment (check or money order) here. Section 1 Your Contact Information Your

Form 656 (Rev. May 2012) Department of the Treasury Internal Revenue Service Offer in Compromise Attach Application Fee and Payment (check or money order) here. Section 1 Your Contact Information Your

Offer in Compromise Booklet

Georgia Department of Revenue Offer in Compromise Booklet IMPORTANT! THIS BOOKLET CONTAINS INFORMATION AND FORMS THAT YOU NEED IN ORDER TO PREPARE A COMPLETE AND ACCURATE OFFER IN COMPROMISE. PLEASE READ

Georgia Department of Revenue Offer in Compromise Booklet IMPORTANT! THIS BOOKLET CONTAINS INFORMATION AND FORMS THAT YOU NEED IN ORDER TO PREPARE A COMPLETE AND ACCURATE OFFER IN COMPROMISE. PLEASE READ

Successfully Negotiating Offers In Compromise

Successfully Negotiating Offers In Compromise All audio is streamed through your computer speakers. There were several attendance verification questions presented during the LIVE webinar to qualify for

Successfully Negotiating Offers In Compromise All audio is streamed through your computer speakers. There were several attendance verification questions presented during the LIVE webinar to qualify for

Offer in Compromise Application Guide

Offer in Compromise Application Guide How To Avoid The Most Common Reasons For IRS Offer in Compromise Rejection Presented to you by: http://aaataxaccountants.com About Offers in Compromise The Offer in

Offer in Compromise Application Guide How To Avoid The Most Common Reasons For IRS Offer in Compromise Rejection Presented to you by: http://aaataxaccountants.com About Offers in Compromise The Offer in

ONE-DAY SEMINAR OUTLINE

ONE-DAY SEMINAR OUTLINE A. The Discharge of Indebtedness 8:30 am 9:20 am 1. IRC 61, 108, 1017; and Regulations thereunder. 2. Exclusions. 3. Exceptions. 4. Mortgage Debt Relief Act of 2007. 5. Definition

ONE-DAY SEMINAR OUTLINE A. The Discharge of Indebtedness 8:30 am 9:20 am 1. IRC 61, 108, 1017; and Regulations thereunder. 2. Exclusions. 3. Exceptions. 4. Mortgage Debt Relief Act of 2007. 5. Definition

Usually, a low-income taxpayer receives several notices (sometimes as many as

PART III. COLLECTION CASES...1 OVERVIEW:...1 A. REASONABLE COLLECTION POTENTIAL... 1 B. CURRENTLY NOT COLLECTIBLE... 3 C. PARTIAL INSTALLMENT AGREEMENTS.... 3 D. INSTALLMENT AGREEMENTS... 4 E. PREPARING

PART III. COLLECTION CASES...1 OVERVIEW:...1 A. REASONABLE COLLECTION POTENTIAL... 1 B. CURRENTLY NOT COLLECTIBLE... 3 C. PARTIAL INSTALLMENT AGREEMENTS.... 3 D. INSTALLMENT AGREEMENTS... 4 E. PREPARING

Identity Theft: Expanded efforts at IRS protect taxpayers and fight fraud. Ley Mills IRS COSS SL/Field November 12, 2014

Identity Theft: Expanded efforts at IRS protect taxpayers and fight fraud Ley Mills IRS COSS SL/Field November 12, 2014 Identity theft is a serious threat Federal Trade Commission hears from more than

Identity Theft: Expanded efforts at IRS protect taxpayers and fight fraud Ley Mills IRS COSS SL/Field November 12, 2014 Identity theft is a serious threat Federal Trade Commission hears from more than

The IRS Collection Process Keep this publication for future reference Publication 594

IRS Mission: Provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all. What You Should

IRS Mission: Provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all. What You Should

The West Virginia State Treasury. A free publication provided by

TAXES A free publication provided by The West Virginia State Treasury Visit www.wvtreasury.com or Call 1.800.422.7498 From the Office of West Virginia State Treasurer, John D. Perdue TAXES Dear fellow

TAXES A free publication provided by The West Virginia State Treasury Visit www.wvtreasury.com or Call 1.800.422.7498 From the Office of West Virginia State Treasurer, John D. Perdue TAXES Dear fellow

The CNMI Division of Revenue and Tax s Collection Process Keep this publication for future reference

DIVISION OF REVENUE AND TAXATION COMMONWEALTH OF THE NORTHERN MARIANA ISLANDS Post Office Box 5234 CHRB Saipan, MP 96950 Tel. (670) 664-1000 What You Should Know About The CNMI Division of Revenue and

DIVISION OF REVENUE AND TAXATION COMMONWEALTH OF THE NORTHERN MARIANA ISLANDS Post Office Box 5234 CHRB Saipan, MP 96950 Tel. (670) 664-1000 What You Should Know About The CNMI Division of Revenue and

The IRS Collection Process Keep this publication for future reference Publication 594

IRS Mission: Provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all. What You Should

IRS Mission: Provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all. What You Should

The IRS Collection Process

IRS Mission: Provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all. The IRS Collection

IRS Mission: Provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all. The IRS Collection

The Offer In Compromise Program May Offer Tax Relief To Financially Troubled Clients

The Offer In Compromise Program May Offer Tax Relief To Financially Troubled Clients Robert F. Reilly When the taxpayer s loaf is getting thinner and thinner, the IRS may be satisfied with something less

The Offer In Compromise Program May Offer Tax Relief To Financially Troubled Clients Robert F. Reilly When the taxpayer s loaf is getting thinner and thinner, the IRS may be satisfied with something less

The IRS Collection Process Publication 594

The IRS Collection Process Publication 594 Page 1 The IRS Collection Process Publication 594 This publication provides a general description of the IRS collection process. The collection process is a series

The IRS Collection Process Publication 594 Page 1 The IRS Collection Process Publication 594 This publication provides a general description of the IRS collection process. The collection process is a series

REPRESENTING THE CLIENT WITH AN IRS COLLECTION PROBLEM

October 18, 2002 REPRESENTING THE CLIENT WITH AN IRS COLLECTION PROBLEM Robert M. Kane, Jr. LeSourd & Patten, P.S. 2401 One Union Square 600 University Street Seattle, Washington 98101 (206) 624-1040 Bob

October 18, 2002 REPRESENTING THE CLIENT WITH AN IRS COLLECTION PROBLEM Robert M. Kane, Jr. LeSourd & Patten, P.S. 2401 One Union Square 600 University Street Seattle, Washington 98101 (206) 624-1040 Bob

Fresh Start Streamlined Installment Agreements & Offer In Compromise

Fresh Start Streamlined Installment Agreements & Offer In Compromise Fresh Start Initiative Goals Assist taxpayers in meeting their tax obligations Aid taxpayers in the payment of back taxes 2 Fresh Start

Fresh Start Streamlined Installment Agreements & Offer In Compromise Fresh Start Initiative Goals Assist taxpayers in meeting their tax obligations Aid taxpayers in the payment of back taxes 2 Fresh Start

What you need to know... 1. Paying for your offer... 2. How to apply... 3. Completing the application package... 4. Important information...

Form 656 Booklet Offer in Compromise CONTENTS What you need to know... 1 Paying for your offer... 2 How to apply... 3 Completing the application package... 4 Important information... 5 Removable Forms

Form 656 Booklet Offer in Compromise CONTENTS What you need to know... 1 Paying for your offer... 2 How to apply... 3 Completing the application package... 4 Important information... 5 Removable Forms

ROWLAND ALEXANDER Lisa R. Alexander, MSA, RTRP lisa@goraonline.com www.goraonline.com TAX YEAR 2014

ROWLAND ALEXANDER Lisa R. Alexander, MSA, RTRP lisa@goraonline.com www.goraonline.com TAX YEAR 2014 Welcome to the New Year and another tax filing. Hopefully, with a minimal effort on your part, we can

ROWLAND ALEXANDER Lisa R. Alexander, MSA, RTRP lisa@goraonline.com www.goraonline.com TAX YEAR 2014 Welcome to the New Year and another tax filing. Hopefully, with a minimal effort on your part, we can

BRIEF SUMMARY: The bill amended the Revenue Act to create an "offer-in-compromise" program within the Department of Treasury.

Legislative Analysis OFFER-IN-COMPROMISE TAXPAYER AGREEMENTS House Bill 4003 as enacted Public Act 240 of 2014 Sponsor: Rep. John Walsh House Committee: Tax Policy Senate Committee: Finance Mary Ann Cleary,

Legislative Analysis OFFER-IN-COMPROMISE TAXPAYER AGREEMENTS House Bill 4003 as enacted Public Act 240 of 2014 Sponsor: Rep. John Walsh House Committee: Tax Policy Senate Committee: Finance Mary Ann Cleary,

What to Know When You Owe (edited transcript)

") What to Know When You Owe (edited transcript) Sarah Vainer: Hello, and welcome to SB/SE Collection s Nationwide Tax Forum Presentation for this year. I m Sarah Vainer. I m the Collection group manager

What to Know When You Owe (edited transcript) Sarah Vainer: Hello, and welcome to SB/SE Collection s Nationwide Tax Forum Presentation for this year. I m Sarah Vainer. I m the Collection group manager

Taxpayer Bill of Rights Adopted June 10, 2014

1. The Right to Be Informed Taxpayers have the right to know what they need to do to comply with the tax laws. They are entitled to clear explanations of the laws and IRS procedures in all tax forms, instructions,

1. The Right to Be Informed Taxpayers have the right to know what they need to do to comply with the tax laws. They are entitled to clear explanations of the laws and IRS procedures in all tax forms, instructions,

Map to IRS Billing and Collections

Map to IRS Billing and Collections File Tax Return with Receive a Bill From IRS If the first bill is unpaid, one additional bill will be sent. Watch out for penalties and interest If the final bill which

Map to IRS Billing and Collections File Tax Return with Receive a Bill From IRS If the first bill is unpaid, one additional bill will be sent. Watch out for penalties and interest If the final bill which

The Examination Process. The IRS Mission

The IRS Mission Provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all. The Examination

The IRS Mission Provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all. The Examination

TERMS AND CONDITIONS

Disclosure of Consumer Credit File Rights under State and Federal Law: You have a right to dispute inaccurate information in your credit report by contacting the credit bureau directly. However, neither

Disclosure of Consumer Credit File Rights under State and Federal Law: You have a right to dispute inaccurate information in your credit report by contacting the credit bureau directly. However, neither

DRAFT. Offer in Compromise. What you need to know...1. Paying for your offer...2. How to apply...3. Completing the application package...

Form 656 Booklet Offer in Compromise CONTENTS What you need to know...1 Paying for your offer...2 How to apply...3 Completing the application package...3 Important information...4 Removable Forms - Form

Form 656 Booklet Offer in Compromise CONTENTS What you need to know...1 Paying for your offer...2 How to apply...3 Completing the application package...3 Important information...4 Removable Forms - Form

Don't go it alone* The IRS collection process. pwc. *connectedthinking. Introduction. IRS emphasis on increasing tax collection.

IRS Service Team Don't go it alone* The IRS collection process Introduction Taxpayers periodically request assistance with IRS collection matters. IRS collection contacts can appear intimidating, and taxpayers

IRS Service Team Don't go it alone* The IRS collection process Introduction Taxpayers periodically request assistance with IRS collection matters. IRS collection contacts can appear intimidating, and taxpayers

Tax Filing Season Issues for Assisters

Tax Filing Season Issues for Assisters A p r e s e n t a t i o n f o r V e r m o n t h e a l t h c a r e a s s i s t e r s by C h r i s t i n e S p e i d e l S t a f f A t t o r n e y O f f i c e o f t

Tax Filing Season Issues for Assisters A p r e s e n t a t i o n f o r V e r m o n t h e a l t h c a r e a s s i s t e r s by C h r i s t i n e S p e i d e l S t a f f A t t o r n e y O f f i c e o f t

10/29/2012. In any professional service, a member shall maintain objectivity and integrity, shall be free from conflicts of interest.

Jonathan E. Strouse Holland & Knight LLP 131 S. Dearborn, 30th Floor Chicago, IL 60603 312-715-5741 jonathan.strouse@hklaw.com 1 1. Introduction 2. (No Circular 230 Discussion) 3. ET Section 102 and Interpretation

Jonathan E. Strouse Holland & Knight LLP 131 S. Dearborn, 30th Floor Chicago, IL 60603 312-715-5741 jonathan.strouse@hklaw.com 1 1. Introduction 2. (No Circular 230 Discussion) 3. ET Section 102 and Interpretation

APPEALS. Offers in Compromise Consideration in Appeals

Offers in Compromise Consideration in Appeals 1 APPEALS MISSION To resolve tax controversies, without litigation, on a basis which is fair and impartial to both the Government and the taxpayer in a manner

Offers in Compromise Consideration in Appeals 1 APPEALS MISSION To resolve tax controversies, without litigation, on a basis which is fair and impartial to both the Government and the taxpayer in a manner

IRS Administrative Appeals Process Procedures

IRS Administrative Appeals Process Procedures Charles P. Rettig Avoiding litigation is often the best choice for a client. The Administrative Appeals process can make it happen. Charles P. Rettig, a partner

IRS Administrative Appeals Process Procedures Charles P. Rettig Avoiding litigation is often the best choice for a client. The Administrative Appeals process can make it happen. Charles P. Rettig, a partner

Scheduled for a Public Hearing. Before the SENATE COMMITTEE ON FINANCE. on April 5, 2001. Prepared by the Staff. of the JOINT COMMITTEE ON TAXATION

OVERVIEW OF PRESENT LAW RELATING TO THE INNOCENT SPOUSE, OFFERS-IN-COMPROMISE, INSTALLMENT AGREEMENT, AND TAXPAYER ADVOCATE PROVISIONS OF THE INTERNAL REVENUE CODE Scheduled for a Public Hearing Before

OVERVIEW OF PRESENT LAW RELATING TO THE INNOCENT SPOUSE, OFFERS-IN-COMPROMISE, INSTALLMENT AGREEMENT, AND TAXPAYER ADVOCATE PROVISIONS OF THE INTERNAL REVENUE CODE Scheduled for a Public Hearing Before

Franchise Tax Board 4905BE Booklet Offer In Compromise for Business Entities

State of California Franchise Tax Board 4905BE Booklet Offer In Compromise for Business Entities What you should know before preparing an Offer in Compromise Are you an OIC Candidate? If your business

State of California Franchise Tax Board 4905BE Booklet Offer In Compromise for Business Entities What you should know before preparing an Offer in Compromise Are you an OIC Candidate? If your business

Offers 2007 2008 2009 2010 2011 Received by IRS 46,000 44,000 52,000 57,000 59,000 Accepted by IRS 12, 000 11,000 11,000 14,000 20,000

OIC Policies On May 21, 2012 the Internal Revenue Service announced another expansion of its Fresh Start initiative by offering more flexible terms to its Offer in Compromise (OIC) program. This newest

OIC Policies On May 21, 2012 the Internal Revenue Service announced another expansion of its Fresh Start initiative by offering more flexible terms to its Offer in Compromise (OIC) program. This newest

Sure and Secure IRS Resolution Services

Sure and Secure IRS Resolution Services Enrolled Agent - Representation What is an Enrolled Agent? An Enrolled Agent (EA) is a federally-authorized tax practitioner who has technical expertise in the field

Sure and Secure IRS Resolution Services Enrolled Agent - Representation What is an Enrolled Agent? An Enrolled Agent (EA) is a federally-authorized tax practitioner who has technical expertise in the field

How To Pay Your Federal Taxes

IRS Mission: Provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all. What You Should

IRS Mission: Provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all. What You Should

The IRS Collection Process Keep this publication for future reference Publication 594

IRS Mission: Provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all. What You Should

IRS Mission: Provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all. What You Should

KENTUCKY DEPARTMENT OF REVENUE OFFER IN SETTLEMENT APPLICATION CHECKLIST. Form 12A018 (08/12)

") CHECKLIST I. BEFORE COMPLETING THE APPLICATION, PLEASE VERIFY THAT YOU ARE ELIGIBLE TO SUBMIT AN OFFER IN SETTLEMENT! Check (a) or (b) to each question below. If you check (a), you may proceed to the next

CHECKLIST I. BEFORE COMPLETING THE APPLICATION, PLEASE VERIFY THAT YOU ARE ELIGIBLE TO SUBMIT AN OFFER IN SETTLEMENT! Check (a) or (b) to each question below. If you check (a), you may proceed to the next

DEALING WITH THE IRS

DEALING WITH THE IRS 2 3 DEALING WITH THE IRS More individuals deal with the IRS than any other federal government agency. The IRS processes more than 100 million individual income tax returns every year.

DEALING WITH THE IRS 2 3 DEALING WITH THE IRS More individuals deal with the IRS than any other federal government agency. The IRS processes more than 100 million individual income tax returns every year.

How To Get A Tax Credit From The Irs

IRS Collection: Update and Overlooked Strategies ABA Tax Section May Meeting, 2008 Washington, DC Eric L. Green Gregory Wilson Convicer & Percy, LLP 425 Market Street 41 Hebron Avenue 26 th Floor Glastonbury,

IRS Collection: Update and Overlooked Strategies ABA Tax Section May Meeting, 2008 Washington, DC Eric L. Green Gregory Wilson Convicer & Percy, LLP 425 Market Street 41 Hebron Avenue 26 th Floor Glastonbury,

Low Income Taxpayer Clinics (LITCs) 2012 Interim and Year-End Report General Information

2012 Interim and Year-End Report General Information") Interim and Year-End Report General Information OMB Number -6 Name of clinic University of Washington School oflaw Federal Tax Clinic Reporting Period D Interim Report - January through June!RI Year-End

Interim and Year-End Report General Information OMB Number -6 Name of clinic University of Washington School oflaw Federal Tax Clinic Reporting Period D Interim Report - January through June!RI Year-End

IRS Tax Resolution. Course #5730B/QAS5730B Exam Packet

IRS Tax Resolution Course #5730B/QAS5730B Exam Packet IRS TAX RESOLUTION (COURSE #5730B/QAS5730B) COURSE DESCRIPTION AND INTRODUCTION Tax resolution means providing solutions to businesses and individuals

IRS Tax Resolution Course #5730B/QAS5730B Exam Packet IRS TAX RESOLUTION (COURSE #5730B/QAS5730B) COURSE DESCRIPTION AND INTRODUCTION Tax resolution means providing solutions to businesses and individuals

Presentation Outline

Presentation Outline Saturday 9:00 am 9:45 am A. Debt and the Discharge of Indebtedness 1. IRC 61, 108, 1017; and Regulations thereunder. 2. Exclusions. 3. Exceptions. 4. Mortgage Debt Relief Act of 2007.

Presentation Outline Saturday 9:00 am 9:45 am A. Debt and the Discharge of Indebtedness 1. IRC 61, 108, 1017; and Regulations thereunder. 2. Exclusions. 3. Exceptions. 4. Mortgage Debt Relief Act of 2007.

Cash Express, LLC Customer Application PERSONAL INFORMATION Last Name First Name Middle Initial Name Suffix Home Phone # Alternate Phone #

Cash Express, LLC Customer Application PERSONAL INFORMATION Date: Last Name First Name Middle Initial Name Suffix Home Phone # Alternate Phone # Cell Phone # See disclosures below regarding text messages

Cash Express, LLC Customer Application PERSONAL INFORMATION Date: Last Name First Name Middle Initial Name Suffix Home Phone # Alternate Phone # Cell Phone # See disclosures below regarding text messages

Guidelines for Offer in Compromise Program

Guidelines for Offer in Compromise Program Overview of Offer in Compromise Program An Offer in Compromise is a request by a taxpayer for the Michigan Department of Treasury (Treasury) to compromise an

Guidelines for Offer in Compromise Program Overview of Offer in Compromise Program An Offer in Compromise is a request by a taxpayer for the Michigan Department of Treasury (Treasury) to compromise an

Maryland State Tax. Controversy Discussion ANDREW "JAY" MASCHAS, ESQ., ASSISTANT MANAGER, HEARINGS & APPEALS

Maryland State Tax Controversy Discussion ANDREW "JAY" MASCHAS, ESQ., ASSISTANT MANAGER, HEARINGS & APPEALS Overview of Maryland Tax Controversies Where to Find Help Statute of Limitations and Liens Penalty

Maryland State Tax Controversy Discussion ANDREW "JAY" MASCHAS, ESQ., ASSISTANT MANAGER, HEARINGS & APPEALS Overview of Maryland Tax Controversies Where to Find Help Statute of Limitations and Liens Penalty

A Guide to Offers in Settlement

A Guide to Offers in Settlement Frequently Asked Questions Preparing an Offer Department of Revenue Resources Massachusetts Department of Revenue From the Commissioner Dear Taxpayer: A major part of our

A Guide to Offers in Settlement Frequently Asked Questions Preparing an Offer Department of Revenue Resources Massachusetts Department of Revenue From the Commissioner Dear Taxpayer: A major part of our

IRS COLLECTION POLICIES AND PROCEDURES: A PRACTITIONER UDATE ON NEW AND OVERLOOKED IRS COLLECTION IDEAS

IRS COLLECTION POLICIES AND PROCEDURES: A PRACTITIONER UDATE ON NEW AND OVERLOOKED IRS COLLECTION IDEAS Note: This article appeared in Connecticut CPA Magazine, A publication of the Connecticut Society

IRS COLLECTION POLICIES AND PROCEDURES: A PRACTITIONER UDATE ON NEW AND OVERLOOKED IRS COLLECTION IDEAS Note: This article appeared in Connecticut CPA Magazine, A publication of the Connecticut Society

Contents. About This Book How To Use This Book Foreword Acknowledgments About the Author

Contents About This Book How To Use This Book Foreword Acknowledgments About the Author vii ix xi xiii xv Chapter 1 Initial Client Engagement 5 Topical Index 1 1.01 Nature of Federal Tax Law 5 1.02 Role

Contents About This Book How To Use This Book Foreword Acknowledgments About the Author vii ix xi xiii xv Chapter 1 Initial Client Engagement 5 Topical Index 1 1.01 Nature of Federal Tax Law 5 1.02 Role

TAX ISSUES FOR DOMESTIC VIOLENCE SURVIVORS: WHAT ADVOCATES NEED TO KNOW

Susanna Birdsong, Fellow, NWLC TAX ISSUES FOR DOMESTIC VIOLENCE SURVIVORS: WHAT ADVOCATES NEED TO KNOW Shaina Goodman, Policy Manager, National Resource Center on Domestic Violence Jamie Andree, Attorney,

Susanna Birdsong, Fellow, NWLC TAX ISSUES FOR DOMESTIC VIOLENCE SURVIVORS: WHAT ADVOCATES NEED TO KNOW Shaina Goodman, Policy Manager, National Resource Center on Domestic Violence Jamie Andree, Attorney,

Collection Information Statement for Wage Earners and Self-Employed Individuals

Georgia Department of Revenue Collection Information Statement for Wage Earners and SelfEmployed Individuals Form CD14C (June 2012) Use this form if you are An individual who owes income tax on a Form

Georgia Department of Revenue Collection Information Statement for Wage Earners and SelfEmployed Individuals Form CD14C (June 2012) Use this form if you are An individual who owes income tax on a Form

Commissioner. Wage & Investment. Collection Strategy

Commissioner Services & Enforcement Operations Support Small Business- Self Employed Wage & Investment Campus & Call Site Operations Campus & Call Site Operations Field Collection Enterprise Collection

Commissioner Services & Enforcement Operations Support Small Business- Self Employed Wage & Investment Campus & Call Site Operations Campus & Call Site Operations Field Collection Enterprise Collection

Optima Tax Relief Case Study A Look at the Tax Resolution Process

Optima Tax Relief Case Study A Look at the Tax Resolution Process A wide range of client cases were selected encompassing offer in compromises (IOC), installment agreements, wage levies, bank levies, substitute

Optima Tax Relief Case Study A Look at the Tax Resolution Process A wide range of client cases were selected encompassing offer in compromises (IOC), installment agreements, wage levies, bank levies, substitute

PITFALLS IN REPRESENTING A CLIENT BEFORE THE IRS. WSBA Brown Bag CLE September 25, 2008. Robert M. Kane, Jr. LeSourd & Patten, P.S.

PITFALLS IN REPRESENTING A CLIENT BEFORE THE IRS WSBA Brown Bag CLE September 25, 2008 Robert M. Kane, Jr. LeSourd & Patten, P.S. (206) 624-1040 There are numerous pitfalls for the practitioner who represents

PITFALLS IN REPRESENTING A CLIENT BEFORE THE IRS WSBA Brown Bag CLE September 25, 2008 Robert M. Kane, Jr. LeSourd & Patten, P.S. (206) 624-1040 There are numerous pitfalls for the practitioner who represents

Innocent Spouse Relief (And Separation of Liability And Equitable Relief)

") Publication 89 Innocent Spouse Relief (And Separation of Liability And Equitable Relief) Pub 89 (2/15) Note: A Publication is an informational document that addresses a particular topic of interest to

Publication 89 Innocent Spouse Relief (And Separation of Liability And Equitable Relief) Pub 89 (2/15) Note: A Publication is an informational document that addresses a particular topic of interest to

DEPARTMENT OF DEFENSE DEFENSE OFFICE OF HEARINGS AND APPEALS

DEPARTMENT OF DEFENSE DEFENSE OFFICE OF HEARINGS AND APPEALS In the matter of: ) ) ------------------------ ) ISCR Case No. 07-02458 SSN: ----------- ) ) Applicant for Security Clearance ) Appearances

DEPARTMENT OF DEFENSE DEFENSE OFFICE OF HEARINGS AND APPEALS In the matter of: ) ) ------------------------ ) ISCR Case No. 07-02458 SSN: ----------- ) ) Applicant for Security Clearance ) Appearances

Offers in Compromise: Advocating for Victims of Payroll Service Provider Failures

Offers in Compromise: Advocating for Victims of Payroll Service Provider Failures Payroll Service Provider (PSP) A third party that is: Administering payroll and employment taxes on behalf of the employer

Offers in Compromise: Advocating for Victims of Payroll Service Provider Failures Payroll Service Provider (PSP) A third party that is: Administering payroll and employment taxes on behalf of the employer

Tax Related Identity Theft on the Rise

TAX RELATED IDENTITY THEFT ON THE RISE...1 ISSUE 2014-1 WINTER 2014 SIMPLIFIED HOME OFFICE DEDUCTION.... 1 PENALTY FOR PAYING OR REIMBURSING EMPLOYEE INDIVIDUAL HEALTH PLAN PREMIUMS... 2 DEFENSE OF MARRIAGE

TAX RELATED IDENTITY THEFT ON THE RISE...1 ISSUE 2014-1 WINTER 2014 SIMPLIFIED HOME OFFICE DEDUCTION.... 1 PENALTY FOR PAYING OR REIMBURSING EMPLOYEE INDIVIDUAL HEALTH PLAN PREMIUMS... 2 DEFENSE OF MARRIAGE

CONSIDERATIONS AND STRATEGIES WHEN THE TAXPAYER IS ALREADY IN TROUBLE

CONSIDERATIONS AND STRATEGIES WHEN THE TAXPAYER IS ALREADY IN TROUBLE By Leslie Shields Attorney at Law The Shields Law Firm, P.L.L.C. 402 S. Northshore Drive Knoxville, Tennessee 37919 Phone (865) 546-2400

CONSIDERATIONS AND STRATEGIES WHEN THE TAXPAYER IS ALREADY IN TROUBLE By Leslie Shields Attorney at Law The Shields Law Firm, P.L.L.C. 402 S. Northshore Drive Knoxville, Tennessee 37919 Phone (865) 546-2400

Discharging Taxes in Bankruptcy

When clients need protection from creditors, tax debts can be resolved as well. by Donald L. Ariail, CPA/CFP Michael M. Smith, Esq., CPA Neil Deininger, Esq., CPA and Reba M. Wingfield, Esq. Discharging

When clients need protection from creditors, tax debts can be resolved as well. by Donald L. Ariail, CPA/CFP Michael M. Smith, Esq., CPA Neil Deininger, Esq., CPA and Reba M. Wingfield, Esq. Discharging

Living the Dream -Live E-Seminar / Conference Call

September 15, 2010 Living the Dream -Live E-Seminar / Conference Call Fighting Battles: Partners, Potential Foreclosure and The IRS Host: Mat Sorensen, Attorney at Law Special Guests: Mark Kohler, CPA,

September 15, 2010 Living the Dream -Live E-Seminar / Conference Call Fighting Battles: Partners, Potential Foreclosure and The IRS Host: Mat Sorensen, Attorney at Law Special Guests: Mark Kohler, CPA,

Form 2000-4. Arkansas Department of Finance and Administration Settlement or Compromise of Tax Liability

Form 2000-4 Arkansas Department of Finance and Administration Settlement or Compromise of Tax Liability Submit this Form and other items listed in the checklist on page 6 via postal mail to the following

Form 2000-4 Arkansas Department of Finance and Administration Settlement or Compromise of Tax Liability Submit this Form and other items listed in the checklist on page 6 via postal mail to the following

November 2014 Seminar IRS UPDATES. Oklahoma City Chapter OSCPA. Miscellaneous Topics. Anita Douglas Senior Stakeholder Liaison November 13, 2014

Oklahoma City Chapter OSCPA November 2014 Seminar Anita Douglas Senior Stakeholder Liaison November 13, 2014 1 IRS UPDATES 2 Miscellaneous Topics Same Sex Couples: Guidance for Employers Form 8822-B -

Oklahoma City Chapter OSCPA November 2014 Seminar Anita Douglas Senior Stakeholder Liaison November 13, 2014 1 IRS UPDATES 2 Miscellaneous Topics Same Sex Couples: Guidance for Employers Form 8822-B -

THE FOREIGN INVESTMENT IN REAL PROPERTY TAX ACT (FIRPTA)

") THE FOREIGN INVESTMENT IN REAL PROPERTY TAX ACT (FIRPTA) FIRPTA s is to ensure non-resident aliens file U.S. income tax returns and pay taxes on profits generated in the U.S. FIRPTA requires 10% of the

THE FOREIGN INVESTMENT IN REAL PROPERTY TAX ACT (FIRPTA) FIRPTA s is to ensure non-resident aliens file U.S. income tax returns and pay taxes on profits generated in the U.S. FIRPTA requires 10% of the

Special Report: IRS Tax Lien

Special Report: IRS Tax Lien TAX PLANNING AND IRS DEFENSE C a l l T o d a y! 540-438- 5344 What an IRS Tax Lien is and How it Works What is Inside? Why the IRS Files a Notice of Federal Tax Lien IRS Tax

Special Report: IRS Tax Lien TAX PLANNING AND IRS DEFENSE C a l l T o d a y! 540-438- 5344 What an IRS Tax Lien is and How it Works What is Inside? Why the IRS Files a Notice of Federal Tax Lien IRS Tax

A persistent threat to taxpayers. IRS Identity Theft Efforts and 2013 Filing Season Improvements 4/10/2013. The most misused SSN of all time

IRS Identity Theft Efforts and 2013 Filing Season Improvements Ley Mills IRS CSO SL/Field herbert.mills@irs.gov 804-448-2723 April 2013 The most misused SSN of all time Happened more than 70 years ago

IRS Identity Theft Efforts and 2013 Filing Season Improvements Ley Mills IRS CSO SL/Field herbert.mills@irs.gov 804-448-2723 April 2013 The most misused SSN of all time Happened more than 70 years ago

TAX PROCEDURE (DN 893) ASSIGNMENT 28 - - - SETTLEMENT AGREEMENTS WITH THE IRS (DRAFT DATE - DECEMBER 8,, 2014) Table Of Contents

ASSIGNMENT 28 - - - SETTLEMENT AGREEMENTS WITH THE IRS (DRAFT DATE - DECEMBER 8,, 2014) Table Of Contents") TAX PROCEDURE (DN 893) ASSIGNMENT 28 - - - SETTLEMENT AGREEMENTS WITH THE IRS (DRAFT DATE - DECEMBER 8,, 2014) Table Of Contents Table Of Contents... -1- Assignment 28 - - - Settlement Agreements With

TAX PROCEDURE (DN 893) ASSIGNMENT 28 - - - SETTLEMENT AGREEMENTS WITH THE IRS (DRAFT DATE - DECEMBER 8,, 2014) Table Of Contents Table Of Contents... -1- Assignment 28 - - - Settlement Agreements With

IRS Payroll Topics. Alan Gregerson. VOH to Hires Act of 2011. Qualified Veteran WOTC. March 15, 2012

IRS Payroll Topics Alan Gregerson March 15, 2012 VOH to Hires Act of 2011 Qualified Veteran WOTC 1 The New Voluntary Classification Settlement Program (VCSP) No Expiration VCSP Advantages The application

IRS Payroll Topics Alan Gregerson March 15, 2012 VOH to Hires Act of 2011 Qualified Veteran WOTC 1 The New Voluntary Classification Settlement Program (VCSP) No Expiration VCSP Advantages The application

IRS Penalty Abatement Letters. Quick Start Guide & Appeals Manual

IRS Penalty Abatement Letters Quick Start Guide & Appeals Manual IRS Penalty Abatement Criteria The primary IRS penalty abatement reasonable cause criteria center around natural disasters, loss or destruction

IRS Penalty Abatement Letters Quick Start Guide & Appeals Manual IRS Penalty Abatement Criteria The primary IRS penalty abatement reasonable cause criteria center around natural disasters, loss or destruction

Texas Security Freeze Law

Texas Security Freeze Law BUSINESS & COMMERCE CODE CHAPTER 20. REGULATION OF CONSUMER CREDIT REPORTING AGENCIES 20.01. DEFINITIONS. In this chapter: (1) "Adverse action" includes: (A) the denial of, increase

Texas Security Freeze Law BUSINESS & COMMERCE CODE CHAPTER 20. REGULATION OF CONSUMER CREDIT REPORTING AGENCIES 20.01. DEFINITIONS. In this chapter: (1) "Adverse action" includes: (A) the denial of, increase

DOMA- Introduction to the Federal Tax Issues of Legally Married Same Sex Couples after the Windsor Supreme Court Case Decision

DOMA- Introduction to the Federal Tax Issues of Legally Married Same Sex Couples after the Windsor Supreme Court Case Decision Speakers Paul La Monaca, MST, CPA, Director of Education, National Society

DOMA- Introduction to the Federal Tax Issues of Legally Married Same Sex Couples after the Windsor Supreme Court Case Decision Speakers Paul La Monaca, MST, CPA, Director of Education, National Society

METLAW LEGAL SERVICES PLAN FACT SHEET

METLAW LEGAL SERVICES PLAN FACT SHEET HOW TO GET LEGAL SERVICES To use your Legal Plan, visit our web site at www.legalplans.com or call Hyatt Legal Plans' Client Service Center at 1-800-821-6400. Be prepared

METLAW LEGAL SERVICES PLAN FACT SHEET HOW TO GET LEGAL SERVICES To use your Legal Plan, visit our web site at www.legalplans.com or call Hyatt Legal Plans' Client Service Center at 1-800-821-6400. Be prepared

211 CMR 123.00: DIRECT PAYMENT OF MOTOR VEHICLE COLLISION AND COMPREHENSIVE COVERAGE CLAIMS AND REFERRAL REPAIR SHOP PROGRAMS

211 CMR 123.00: DIRECT PAYMENT OF MOTOR VEHICLE COLLISION AND COMPREHENSIVE COVERAGE CLAIMS AND REFERRAL REPAIR SHOP PROGRAMS Section 123.01: Authority 123.02: Purpose and Scope 123.03: Definitions 123.04:

211 CMR 123.00: DIRECT PAYMENT OF MOTOR VEHICLE COLLISION AND COMPREHENSIVE COVERAGE CLAIMS AND REFERRAL REPAIR SHOP PROGRAMS Section 123.01: Authority 123.02: Purpose and Scope 123.03: Definitions 123.04:

Building the Strongest Position for Withstanding an IRS Audit

Building the Strongest Position for Withstanding an IRS Audit Broadcast Date: August 15, 2012 Copyright 2012 All-Star Tax Series, LLC 2011 IRS Data Book: Fiscal Year 2011 Collected: $2.4 trillion Collections

Building the Strongest Position for Withstanding an IRS Audit Broadcast Date: August 15, 2012 Copyright 2012 All-Star Tax Series, LLC 2011 IRS Data Book: Fiscal Year 2011 Collected: $2.4 trillion Collections