DEALING WITH THE IRS BEFORE FILING BANKRUPTCY

|

|

|

- Theodora French

- 10 years ago

- Views:

Transcription

1 DAVID COFFIN PLLC DEALING WITH THE IRS BEFORE FILING BANKRUPTCY WHAT TO DO WITH YOUR DEBTOR WHO HAS TAX ISSUES David B. Coffin, J.D., C.P.A. November 14, 2011 DAVID COFFIN PLLC 1452 Hughes Rd., Ste. 200 Grapevine, TX (817) (817) (fax) (817) (cell)

410 5709 (817) 410 5710 (fax) (817) 691")

2 DEALING WITH THE IRS BEFORE FILING BANKRUPTCY: WHAT TO DO WITH YOUR DEBTOR WHO HAS TAX ISSUES A. Are Tax Issues Something Bankruptcy Attorneys Will Face? Tax issues can be common in bankruptcy cases. The Small Business Administration, Office of Advocacy, recently commissioned a study resulting in a report published in 2008 entitled Tax Debts of Small Business Owners in Bankruptcy. The study investigated the burden tax obligations imposed on small business owners (both individuals and entities) at the time of their bankruptcy filing. The study was limited to bankruptcies filed between October 17, 2005 and October 16, 2008, in five (5) judicial districts: California, Tennessee, Pennsylvania, Illinois, and Texas. The study found that: 1) Fewer than one quarter of all consumers in bankruptcy reported tax debts, while more than half of individual small business owners reported owing some tax debts. 2) Overall, almost 30 percent of all petitioners in the bankruptcy sample reported owing some kind of tax debts. 3) Individual entrepreneurs reportedly owed tax debts more often than small business entities. 4) Individual small business owners from California and Texas most often reported tax debts (Tennessee was the least often in reporting tax debts). So, the study would indicate that bankruptcy practitioners will probably come across some debtors with tax indebtedness. The purpose of this presentation is to help you implement the steps necessary to address tax issues before filing bankruptcy. B. Rules Regarding Dischargeability Federal taxes, to some extent, are dischargeable. A detail review of the rules regarding dischargeability is beyond the scope of this presentation, but the general rules are listed below: Rule 1: 3 Year Rule due date for the return must be more than 3 years prior to the petition date (11 U.S.C. 507(a)(8)(A)(i)). The first rule requires that the tax return be filed more than 3 years prior to the petition date. Under this rule, a practitioner should identify the tax year for which a discharge is sought, then count three years back from the proposed petition filing date to see if the return was due either within or beyond this time frame. If the return was due beyond this time frame, then the tax for that period David Coffin PLLC 1 Page

judicial districts: California, Tennessee, Pennsylvania, Illinois, and Texas.")

3 passes this test. Note that under this rule, the practitioner is determining when the return was actually due, not when the return was actually filed. Rule 2: 240 day rule The tax must have actually been assessed more than 240 days prior to the petition date. (11 U.S.C. 507(a)(8)(A)(ii)). If the tax year for which the debtor is seeking a discharge passes the 3 year rule, the practitioner must then determine whether the IRS assessed the tax more than 240 days prior to the petition date. This rule asks the bankruptcy practitioner to identify exactly when the tax for a particular tax year was actually assessed, 1 or posted on the IRS books. Typically, the income taxes resulting from a filed tax return are assessed (or put on IRS books) near the time the return is received by the IRS. Be aware that there are times when, such as pursuant to a subsequent IRS audit or examination, the taxes are assessed against the taxpayer well after the return is filed. The IRS may conduct an audit of a particular tax year and assess taxes for that year within 3 years from the date the return is filed. 2 Moreover, this period can be extended. Tax periods and returns that are subject to an IRS audit or examination deserve close scrutiny under this rule. Rule 3: 2 Year rule - The return must have been actually filed more than 2 years prior to the petition date (11 U.S.C. 523(a)(1)(B)). Under this rule, the bankruptcy practitioner should identify the date the Form 1040 was filed with the IRS and make sure that the bankruptcy petition is filed more than 2 years from the date of filing the return. If no return was filed by the debtor, then the tax for that year is not dischargeable. 3 Rule 4 No Fraud: Tax is not dischargeable if the debtor filed a fraudulent return (11 U.S.C. 523(a)(1)(C)). Income taxes for a particular tax year are not dischargeable if the debtor has filed a fraudulent return for that tax year. As a practitioner, this may be very 1 The assessment of a tax is essentially a bookkeeping notation, and is made when the Secretary or his delegate establishes an account against the taxpayer on the tax rolls. In re Hosack, 282 F. App'x. 309, 313 (5th Cir. 2008), citing Laing v. United States, 423 U.S. 161, 170 n. 13, 96 S.Ct. 473, 46 L.Ed.2d 416 (1976). 2 I.R.C. 6501(a). debtor. 3 See discussion below of dischargeability issues when IRS files a substitute return on behalf of the David Coffin PLLC 2 Page

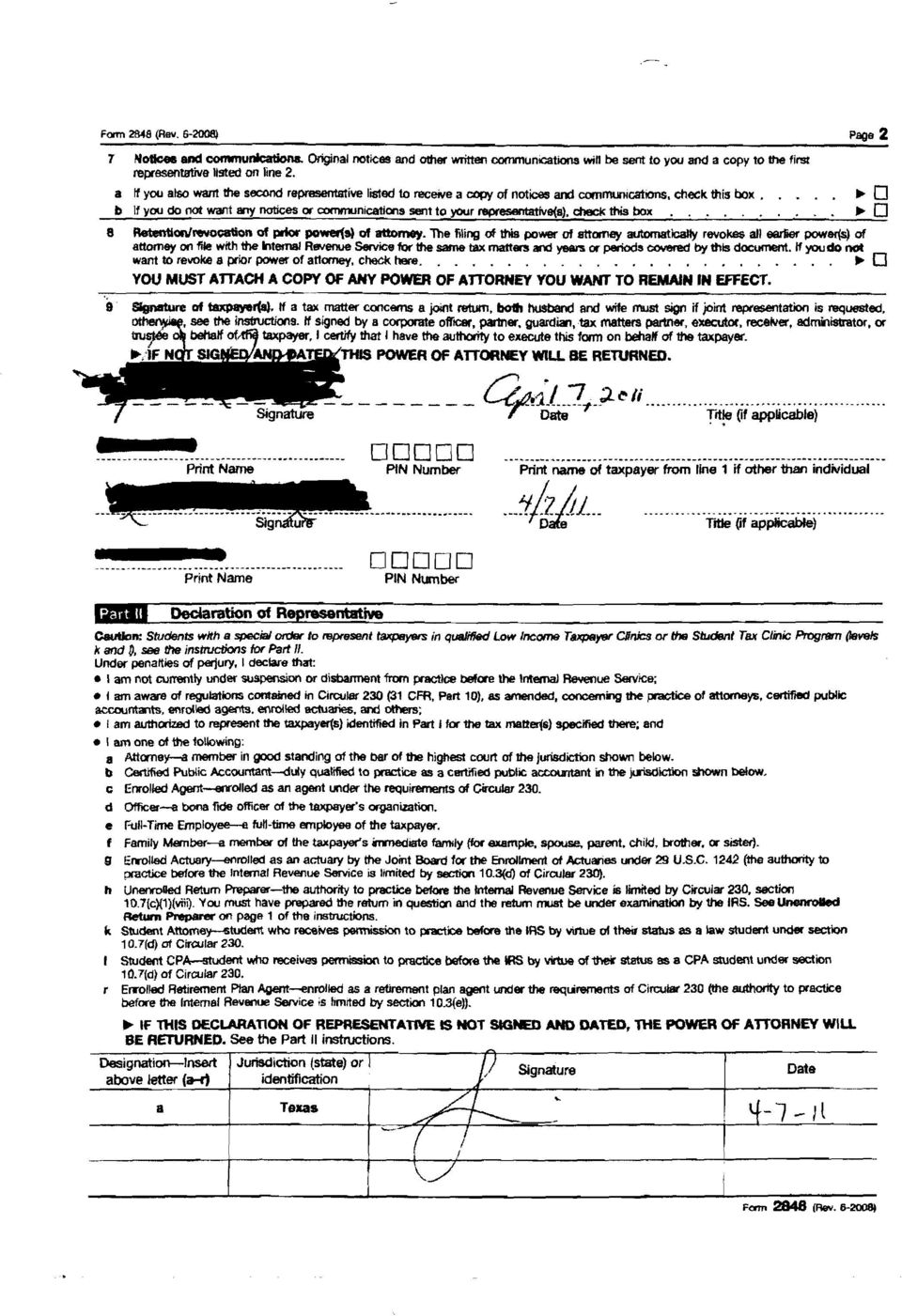

4 difficult to determine. Generally, the practitioner should review the debtor s IRS transcripts (discussed below) and tax returns for any indications of fraud. Rule 5 No Tax Evasion: Taxes are not dischargeable for any year for which the debtor willfully attempted to defeat or evade the tax (11 U.S.C. 523(a)(1)(C)). The debtor s taxes are not dischargeable in bankruptcy when the debtor has attempted to willfully attempt to defeat for evade tax. The statutory phrase willfully attempted to evade means a voluntary, conscious, or intentional attempt to evade a tax, whether the evasion was through overt actions or omissions. Willfully attempting to evade taxes requires the misconduct and an intention to evade. The intention requirement requires that the taxpayer had a duty to pay a tax, knew of the duty, and intentionally and voluntarily evaded such duty. 4 The bankruptcy cases addressing this provision teach that the bankruptcy practitioner must determine whether the debtor fits the mold of the honest debtor. 5 C. What do you when a Debtor with Tax Issues Walks into Your Office So, with all these rules regarding dischargeability, how does the practitioner corral the information needed to make an educated determination as to how the Debtor s tax indebtedness fits into these rules? The key in dealing with tax issues is to develop a series of steps to follow each time a client with tax indebtedness walks into your office. Each practitioner should develop his or her own routine to identify and address the relevant issues surrounding a debtor s tax indebtedness. The steps below provide a good base from which that routine can be developed. Step 1: Get authorization from your Debtor to talk to IRS on their behalf. First, you will want to be able to communicate with the IRS on behalf of your debtor. Before talking with you about your debtor s tax issues, the IRS requires that you present to it a Form 2848, Power of Attorney and Declaration of Representative, which authorizes the IRS to speak with you on the debtor s behalf. It is a good practice to have many copies of the Form 2848 pre-filled with your information so that the document may be completed when the Debtor 4 See e.g., Matter of Bruner, 55 F.3d 195, 200 (5th Cir. 1995). 5 Determining factors include conduct such as (i) understatement of income for more than one year; (ii) implausible or inconsistent behavior; (iii) extensive dealings in cash; (iv) failure to cooperate with the IRS; (v) inadequate record keeping; (vi) transfer[s] of assets to a family member; (vii) transfer[s] of assets for inadequate consideration; (viii) transfer[s] that greatly reduce assets subject to IRS execution; (ix) transfers made in the face of serious financial difficulties; (x) failure to acquire significant assets relative to a debtor s earnings; and (xi) any other conduct that is likely to mislead or conceal. A court may also consider a debtor s lavish lifestyle while concurrently failing to pay taxes, id., or the fact that a debtor has placed assets in the names of others. See Mixon, BJH 7, 2008 WL (Bankr. N.D. Tex. May 13, 2008). David Coffin PLLC 3 Page

5 with tax indebtedness makes his or her initial appearance in your office. When this happens, have the debtor complete the form by filling in their name, address, social security number, the type of return they file (i.e., 1040). You should then list on the Form the past ten (10) years, plus any other years tax indebtedness exists. Secure the debtor s signature on the back of the Form 2848, execute your signature, and fax the Form 2848 to the CAF Unit of the IRS at (801) (for Texas practitioners). IRS will associate your information with the taxpayer, only for the years and forms listed on the Form IRS will then send you a CAF number, 6 although it may take several weeks for IRS to process the Form 2848 and send it to you. After faxing the Form 2848, place the document in the file. Its use will be discussed below. (See an example Form 2848 at Exhibit 1). Step 2: Get all documents, correspondence, tax returns, etc., from the Debtor. Second, secure copies of all tax returns, IRS correspondence, check copies of payments and other documentation from the debtor related to the tax years at issue. Having as much documented information from the debtor as possible is obviously much more reliable than having them tell you what they recall. Review this information carefully for any matters that may be relevant under the dischargeability rules. Step 3: Get the Account Transcripts from the IRS. Third, the practitioner should secure the account transcripts from the IRS for each and every year that the debtor has tax indebtedness. In fact, it is a good practice to secure the debtor s tax account transcripts for the past 10 years, plus transcripts for any tax years for existing indebtedness falling outside of the 10 years. The debtor may owe taxes for years that they do not recall, so you ll want to get at least the last 10 years transcripts. The fastest method of getting those transcripts is to call the IRS and request that IRS send them to you by facsimile. The IRS has a practitioner s priority service hotline that is available to you: When you make this call, be ready to spend some time on hold. Typically, the best time to call so that you are not on hold for in excess of 15 minutes is either at 8:00 o clock in the morning or 7:00 o clock at night. Make sure you select the menu option allowing you to speak with a representative for questions on your client s individual or business accounts, as the case may be. 6 A CAF number is assigned to a tax practitioner when a Form 2848 is filed with the IRS. This number represents a file that contains information regarding the type of authorization that taxpayers have given representatives for the various modules within their accounts. 7 The Practitioner Priority Service is a toll free, accounts related service for all tax practitioners, nationwide. It is the practitioners first point of contact for assistance regarding taxpayers account related issues. The hours of service are weekdays, 8:00 a.m. until 8:00 p.m. your local time (Alaska and Hawaii follow Pacific Time). David Coffin PLLC 4 Page

620-4249 (for Texas practitioners).")

6 Begin the call by telling the representative that you represent the debtor in their tax matters, that you have a Form 2848 ready to fax to the representative, and that you need to secure account transcripts for the years at issue. The IRS representative will then request the social security number and address of your debtor. The representative will ask you if you have a CAF number and if you do, provide it to the representative. 8 While still on the telephone, the IRS representative will ask that you fax the Form 2848 to the representative. When the IRS representative receives your fax, they will ask you to confirm the items on the Form 2848 to ensure you are the person who faxed the Form to the IRS. When the representative is satisfied with your information, you will be associated with the debtor s tax accounts. Then, the representative may ask for other information about your debtor which you may or may not have, like bank account information, current employment, telephone number, etc. These items are not required to be furnished to the IRS to get the account transcripts. Advise the IRS representative that you need account transcripts and identify the years at issue, and that you would like the IRS to fax the transcripts to you at either the fax number listed on your Form 2848 or another desired number. The representative may ask you if the fax number is secure and once you advise that it is, the representative will process your order for the transcripts. You should receive your transcripts by facsimile within the next several hours. Step 4: Inquire about collection activities. While on the telephone with the IRS representative, ask the representative whether any of the years at issue are in collection status. If the collection of taxes is being handled in ACS or by the Automated Collection Service, 9 then the representative can advise you of any pending collection activities, or whether the commencement of such activities is imminent. The representative can also advise you whether the filing of any liens has occurred, or may be forthcoming. This information may be helpful in determining the timing requirements in filing your client s bankruptcy A CAF number is not required to get the account transcripts, but once you get one, place it on your prefilled Form 2848 s. 9 The Automated Collection System ( ACS ) is a system of phone centers where IRS attempts to establish contact with taxpayers telephonically usually prompted by systemically generated letters and levies. Cases that are not resolved by notices or the ACS are ultimately assigned to the Collection Field function. ACS emphasizes the use of automated enforcement actions as the foundation of its strategy to contact delinquent taxpayers. See National Taxpayer Advocate s Report to Congress 2010, Volume Two; TAS Research and Related Studies, p If the matter is in ACS, the IRS representative will ask if they may transfer you to the ACS representatives, at which point, you have the option to refuse. However, you may want to talk to ACS; see Step 6. David Coffin PLLC 5 Page

7 If collection efforts are being handled locally by a Revenue Officer, however, the IRS representative may not have any information concerning the status of collection activities. If this is the case, the practitioner should conservatively assume that collection activities (levies, liens, etc.) are likely imminent. Step 5: Inquire about the running of the statute of limitations for collection for each year. While the IRS representative is on the telephone, you will want to secure some very important information. Under IRC 6502(a), the IRS enjoys a ten year period from the date the tax is assessed for the collection of taxes, and upon the expiration of that ten year period, the IRS cannot enforce collection. Therefore, the running of the statute of limitations is the best result for a debtor, and it happens more often than you might think. However, there are certain events that toll the running of the ten year collection period, and bankruptcy is one of them. 11 The practitioner would not want to file bankruptcy and interfere with this result, so it is critical to determine the date the collection period expires for each tax year, which can be determined from reviewing the transcripts, but is often difficult. The good news for practitioners is that the IRS representative possesses that information and can provide it to you upon request. Simply ask the representative what the CSED ( collection statute expiration date) is for each year there is existing indebtedness, and be sure and log the information as it will not likely be provided in writing. This piece of information is probably the most important item to have for debtors with older tax liabilities, and a failure to secure such information may put the practitioner at risk of committing significant errors. Step 6: Buy Some Time if Necessary If you discover that the debtor s tax accounts are in ACS with the IRS and that enforcement activities are imminent, you may want to buy some time to allow for sufficient time to assess the debtor s situation. While on the phone with the Practitioner Priority IRS representative, you can request to be transferred to the ACS department, or you can call back later at the same number, and choose the menu option to speak with ACS. 12 You can then advise ACS that your debtor is attempting to resolve his tax issues with the IRS but that you need additional time to assess the debtor s tax situation. The IRS representative is generally cordial, and may give you as much as 30 days before requiring you to call back with an assessment or proposal to resolve the tax issues. 13 If the debtor s tax accounts are in collection status with a 11 Generally, the ten year collection period is tolled the entire time the debtor is in bankruptcy, plus 6 months. See IRC 6503(h)(2). 12 Be advised that in either instance, you will likely need to resubmit by fax your Form 2848, unless the IRS CAF Unit has had sufficient time to process your Form 2848 (usually 2 weeks after you send it). 13 Keeping your promise to call back by a certain date is important in establishing and maintaining credibility with the ACS and generally, the IRS, and also to ensure that the IRS will not resume collection activities like filing liens and serving levies. David Coffin PLLC 6 Page

, the IRS enjoys a ten year period from the date the tax is assessed for the collection of taxes, and upon the expiration of that ten year period, the IRS cannot enforce collection.")

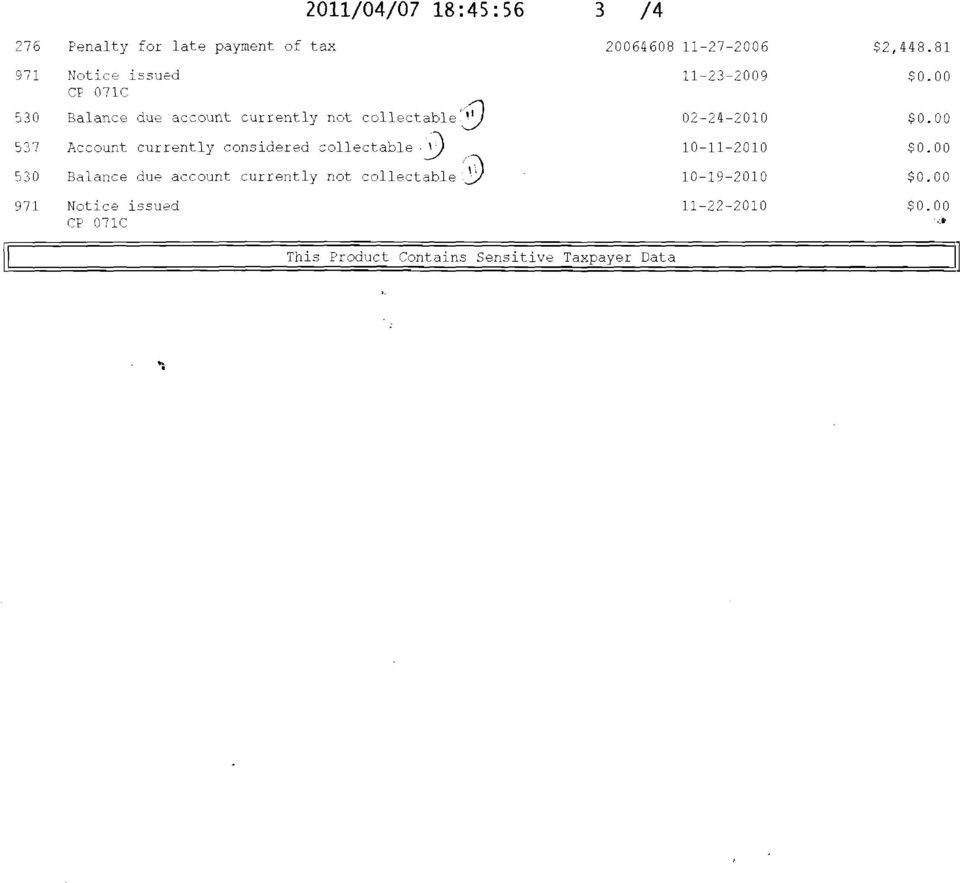

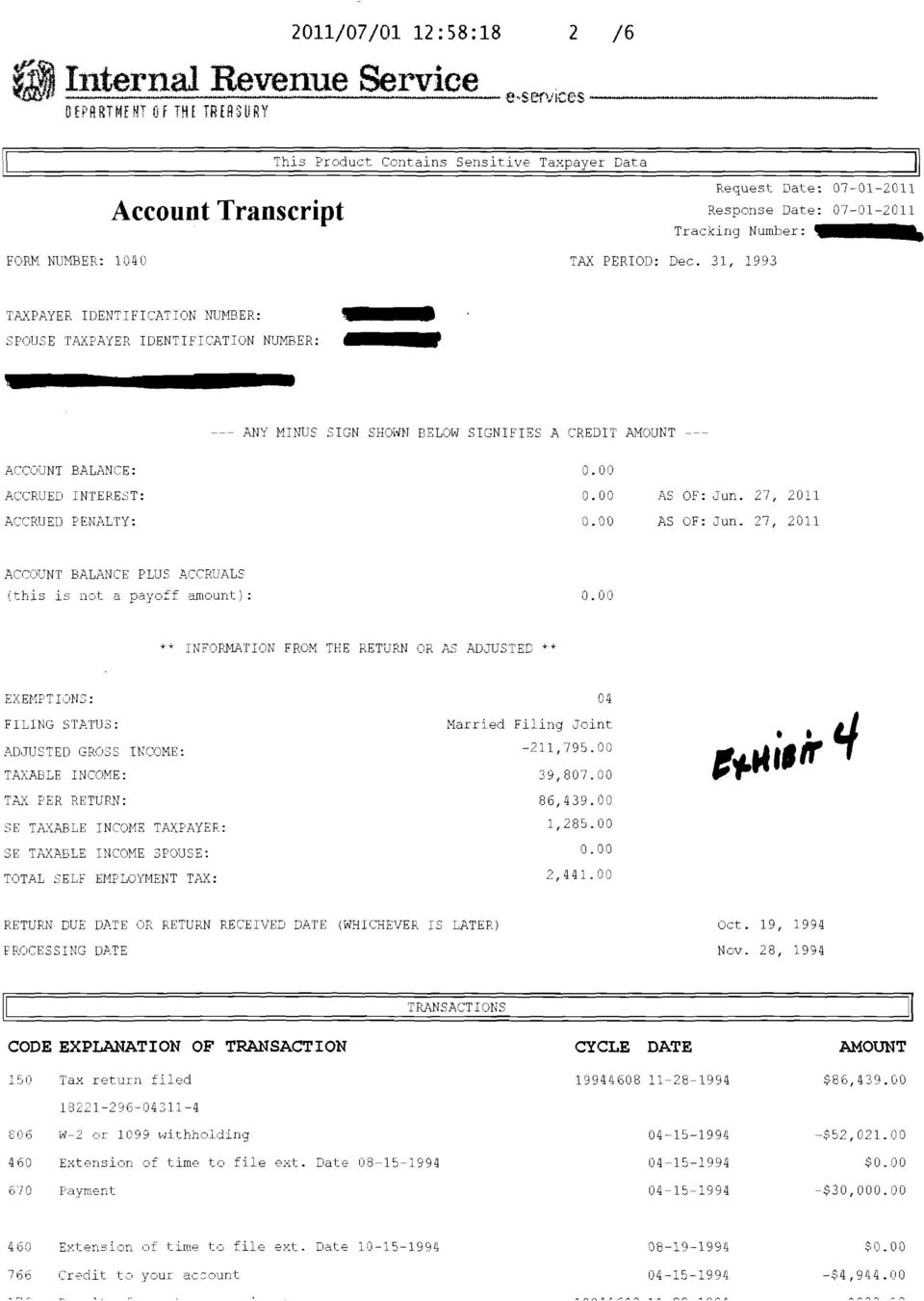

8 local IRS Revenue Officer, however, you should be wary that contacting the Revenue Officer could trigger immediate collection activities. D. Using the Account Transcripts to Assess Debtor s Dischargeability Possibilities. After securing the transcripts and gathering the information described above, the practitioner now should assess the status of the debtor s tax liabilities. There is an abundant amount of information available in the debtor s account transcripts that will help you assess whether the debtor s taxes may be discharged or will require payment in a Chapter 7 or Chapter 13 case. The account transcripts will reveal the amount of the taxes and penalties that were assessed, the date the return was filed, the dates of assessment, and the total amounts owed as of a certain date, with interest. Some of the most important information on the transcripts is provided on the line items displayed on the transcript, with corresponding codes used by the IRS. Below are some of the more critical terms and transaction codes to be aware of when considering whether the debtor should file for bankruptcy protection. Example transcripts as Exhibits are provided following the text of this paper and the line items on the examples are annotated with the corresponding numbers 1-13 below. 1. The words Return Due Date or Return Received Date (Whichever is later) No Code These words and the date that follows provide the date the practitioner should use to determine whether two (2) years has passed from the date the tax return was filed for a particular year. (See dischargeability rule 3 above). 2. The words Tax return filed - Code 150 If the debtor filed his return (as opposed to the IRS filing the return, as discussed below), the practitioner will find these words listed on the transcript. The date accompanying these words reveal the date the tax was assessed by the IRS. As discussed above, the assessment date is critical with regard to the dischargeability rules and also in determining the date the ten year collection statute expires. 3. The words Extension of time to file Code 460 These words indicate that the debtor filed a request for an extension to file their tax return for that particular year, and are typically followed by the extended due date. The bankruptcy significance of this is that under dischargeability rule number 1 above, the practitioner must determine when the tax return was due for the year at issue, and if an extension was requested by the debtor, the extended due date must be used rather than the normal due date of April 15. David Coffin PLLC 7 Page

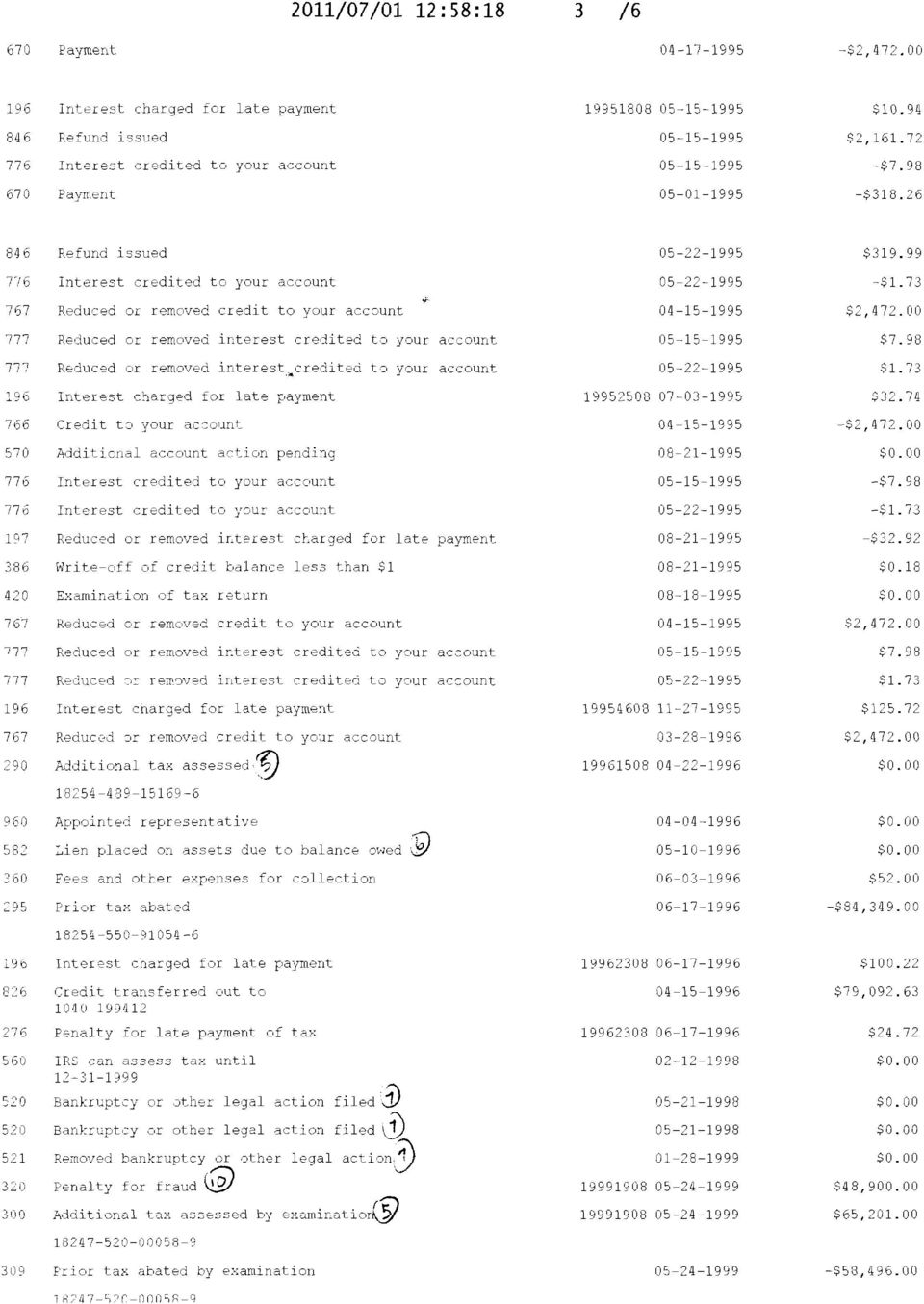

9 4. The words Substitute Return Prepared by IRS - Code 150 This indicates that the IRS has prepared returns on behalf of the debtor because the debtor has failed to file his returns despite several notices from the IRS. The current position of the IRS is that if the IRS has prepared substitute returns on behalf of the debtor, then those taxes will not be dischargeable because the debtor has not actually filed his returns as required by Bankruptcy Code Section 523(a)(1)(B) (see dischargeability rule 3 above). Thus, the IRS believes the debtor will be required to full pay the taxes assessed pursuant to any substitute returns prepared by the IRS, 14 and some bankruptcy cases have supported this position The words Additional tax assessed - Codes 290, 300. These words indicate that an examination occurred on the debtor s tax return for that particular year, resulting in an additional assessment of tax. The corresponding date of that later assessment is listed, and always occurs after the date of the original assessment. The bankruptcy significance of this is that the practitioner must use the later date to determine whether 240 days have passed since the additional tax was assessed, as discussed under dischargeability rule 2 above. 6. The words Lien Placed on Assets - Code 582 This indicates that the IRS has filed a notice of federal tax lien on the debtor s property or rights to property. The relevance of this is that any lien filed by the IRS survives a discharge unless the bankruptcy is a no-asset case, or the related tax liabilities are paid. Therefore, regardless of whether the debtor s tax liability for a particular year meets the 5 tests for dischargeability (discussed above), the indebtedness will still be considered a secured claim in bankruptcy that either has to be paid in a Chapter 13 case, or will survive the discharge in a Chapter 7 case. Of course, the practitioner should secure a copy of the Notice of Federal Tax Lien to ensure that the IRS filed the lien in the proper location. 7. The words Bankruptcy or other legal action filed - Code 520 and the words Removed bankruptcy or other legal action - Code See IRS Chief Counsel Notice CC issued September 10, 2010: A Form 1040 is not disqualified as a return under section 523(a) solely because it was filed late. Regardless of whether a Form 1040 filed after assessment is a return for tax purposes, the portion of a tax that was assessed before the Form 1040 was filed is nondischargeable under section 523(a)(1)(B)(i). 15 See In re Creekmore, 401 B.R. 748 (N.D. Miss. 2008) and In re Cannon, MHM, 2011 WL (Bankr. N.D. Ga. 2011). David Coffin PLLC 8 Page

(1)(B) (see dischargeability rule 3 above).")

10 These terms mean that the debtor has previously been involved in a bankruptcy or other proceeding 16 involving the tax indebtedness which prohibited the IRS from collection activities while the matter was pending. When this happens, the dangling paragraph in section 507(a)(8) provides that the time periods under that section are extended for the time the IRS was prohibited from collection activities, plus 90 days. Also, as discussed above, a previous bankruptcy, among other things, tolls the running of the ten year collection period under IRC 6503(h)(2) and is therefore relevant in determining whether bankruptcy should be filed or whether the debtor should patiently wait for the collections period to run. 8. The words Offer in Compromise Received - Code 480; and Offer in Compromise Rejected - Code 481 or Offer in Compromise Withdrawn - Code 482. The IRS allows taxpayers to compromise their tax liabilities through a program called the Offer in Compromise ( OIC ) program. The taxpayer submits the OIC at which point the IRS may or may not consider it to be processable. Once that determination is made by the IRS, all collection on that account for that tax year contained in the offer is restricted. Eventually, the OIC is either accepted or rejected by the IRS, or withdrawn or defaulted upon by the debtor. During the time the OIC is pending, the IRS is prohibited from collecting the tax by levy until one of these events concerning the OIC occurs. Therefore, if the debtor withdraws his OIC or otherwise fails to comply with its terms, and then later attempts to discharge the tax, the bankruptcy practitioner must determine the time that the IRS was prohibited from collecting the tax, and add 90 days to that time period. 9. The words Collection Due Process Request Timely Received - Code 971 followed by Codes 520 and 521. Taxpayers are usually given an appeal opportunity entitled a Collection Due Process Hearing ( CDP hearing ) after the taxes have been assessed but before IRS begins its collection efforts. If the taxpayer requests a CDP hearing, it should be noted on the debtor s account transcript with Collection Due Process Request Timely Received, Code 971, and followed by a Code 520, Bankruptcy or other legal action filed. Similar to a bankruptcy, or and OIC, while a CDP hearing is pending, the IRS is prohibited from collecting the tax at issue, and the Code 520 provides this notice. 17 Under the dangling paragraph in section 507(a)(8), the period the IRS is prohibited from collecting tax (the 16 See discussion of Collection Due Process Appeals below. 17 Contrast this with the words Collection due process equivalent request received, also a Code 971. The IRS is not restricted from collection while these equivalent hearings are pending, and as such, are not followed on the transcript by a 520 transaction code. David Coffin PLLC 9 Page

(2) and is therefore relevant in determining whether")

11 ending date of which is shown by Code 521), plus 90 days, must be added to the applicable time periods in that section (see dischargeability rules 1 and 2 above). 10. The words Penalty for Fraud - Code 320 This means that the debtor has been assessed a penalty for fraud, and the bankruptcy significance of this is that under Section 523(a)(1)(c), the underlying tax will not be dischargeable in bankruptcy, regardless of the time that has passed. 11. The words Balance Due Account Currently Not Collectable - Code 530 and Account Currently Considered Collectable Code 537 The first phrase means that because of the debtor s current financial situation, the IRS considers the debtor s liability to be uncollectable and therefore, the IRS will temporarily not pursue collection. However, once the IRS determines that the debtor has the means to pay the indebtedness, from information provided on the debtor s tax returns, potential employers, or 1099 payers, the IRS will determine that the account is currently collectible, and enforcement actions will resume. The bankruptcy significance of this is that the debtor in not collectable status may have some time to wait before filing for bankruptcy to allow some of the time frames to pass (as discussed in the 5 dischargeability rules) so as to discharge as much tax as possible. Additionally, the debtor might be counseled to just wait until the collection statute runs rather than filing bankruptcy, as long as the IRS is not attempting to collect its debt. 12. The words Miscellaneous Penalty IRC 6672 Trust Fund Recovery Penalty - Code 240 These words indicate that the debtor has been assessed the Trust Fund Recovery Penalty ( TFRP ), which, under Bankruptcy Code 507(a)(8)(C), is not dischargeable. Therefore, unless the TFRP is fully paid in bankruptcy, then the debtor will not be relieved of this liability upon discharge. 13. The words Write-off of balance due Code 608 This means that the ten (10) year collection statute has expired, and the IRS has written the balance off and will no longer pursue collection. E. Assessing Dischargeability With the information pulled from the transcripts, and with the known equity in the debtor s assets, the practitioner can apply that information to the dischargeability rules and make a determination as to whether bankruptcy is a viable option for the debtor. David Coffin PLLC 10 Page

12 Chapter 7 Determinations from the Government After filing the petition, the practitioner can seek a dischargeability determination from the IRS in two ways. For no-asset Chapter 7 cases, the IRS Centralized Insolvency Operation (CIO) in Philadelphia handles dischargeability determinations. Once bankruptcy is filed, debtor s counsel should send a fax to the CIO at with a copy of Form 2848 and request a dischargeability determination. The CIO also has a telephone number of , and following the fax with a phone call may provide the practitioner s with the best approach in getting a determination. Another approach is to file an adversary Complaint to Determine Dischargeability. This may be the quickest approach in that the CIO discussed above usually waits thirty (30) days until after the debtor has been discharged before issuing a written determination. After filing the Complaint to Determine Dischargeability, the practitioner may fax the Complaint, along with the debtor s relevant account transcripts and a draft Order Regarding Dischargeability, to the Department of Justice, Tax Division s Dallas office to get a determination. 18 The practitioner should get a prompt determination and hopefully a signed order from the DOJ s office. For any taxes that are not discharged, there is still administrative relief available to the debtor in the form of the debtor entering into an installment agreement to pay down the remaining tax liability, or seeking an Offer in Compromise with the IRS. A practitioner having a debtor with expected remaining indebtedness should see that the debtor is aware of these options after discharge. Chapter 13 Determinations from the Government After the Chapter 13 case is filed, the IRS will file its proof of claim, which hopefully will come to no surprise to the practitioner. Once the debtor s Chapter 13 plan is filed, approved and completed, the debtor should be free from pre-petition tax indebtedness. F. A Note About Staying Current After filing for bankruptcy relief, debtors, like all taxpayers, have an obligation to stay current on their tax filings. Practitioners would be serving their debtors well by routinely advising them to remain current on their future federal tax filings. Remaining current is important in that if they are not, debtors may not be able to seek relief from the bankruptcy court or administratively, from the IRS. Practitioners could assist in this process by advising debtors of the ramifications of falling behind in their tax filings and obligations. This advice would go a long way in keeping the IRS away from your debtors in the future. 18 Of course, the Complaint and related summons must be properly served upon the Government. David Coffin PLLC 11 Page

13

14

15

16

17

18

19

20

21

22

23

24

25

DETERMINING THE DISCHARGEABILITY OF UNSECURED INCOME TAX DEBTS BREAKING THE CODE OF THE IRS ACCOUNT TRANSCRIPTS

21ST ANNUAL DFW AREA CHAPTER 13 CONFERENCE DETERMINING THE DISCHARGEABILITY OF UNSECURED INCOME TAX DEBTS BREAKING THE CODE OF THE IRS ACCOUNT TRANSCRIPTS David B. Coffin, J.D., CPA October 22, 2012 DAVID

21ST ANNUAL DFW AREA CHAPTER 13 CONFERENCE DETERMINING THE DISCHARGEABILITY OF UNSECURED INCOME TAX DEBTS BREAKING THE CODE OF THE IRS ACCOUNT TRANSCRIPTS David B. Coffin, J.D., CPA October 22, 2012 DAVID

Bankruptcy Filing and Federal Employment Taxes. Bad investments, too great an assumption of risk, circumstances beyond their control.

I. What causes someone to file for bankruptcy? Bad investments, too great an assumption of risk, circumstances beyond their control. II. The options A. Individuals Chapter 7, Chapter 11, i Chapter 13 B.

I. What causes someone to file for bankruptcy? Bad investments, too great an assumption of risk, circumstances beyond their control. II. The options A. Individuals Chapter 7, Chapter 11, i Chapter 13 B.

Discharging Taxes in Bankruptcy and. Avoiding Malpractice in the Process 9/29/2015

Discharging Taxes in Bankruptcy and Avoiding Malpractice in the Process Brought to you by the NACTT Academy A SPECIAL THANK YOU TO OUR PANELISTS Kent Anderson Certified Bankruptcy Specialist, Eugene, OR

Discharging Taxes in Bankruptcy and Avoiding Malpractice in the Process Brought to you by the NACTT Academy A SPECIAL THANK YOU TO OUR PANELISTS Kent Anderson Certified Bankruptcy Specialist, Eugene, OR

Collecting Back Taxes: The IRS Statute of Limitations Explained

Collecting Back Taxes: The IRS Statute of Limitations Explained A Practice Essentials CLE Program Presenter: Benjamin A. Stolz, Esq. 1 Copyright 2011 OnePath Practice Management Advisors, LLC Disclaimer

Collecting Back Taxes: The IRS Statute of Limitations Explained A Practice Essentials CLE Program Presenter: Benjamin A. Stolz, Esq. 1 Copyright 2011 OnePath Practice Management Advisors, LLC Disclaimer

Federal Tax Issues in Bankruptcy A View From Your Friends at the IRS and DOJ

Federal Tax Issues in Bankruptcy A View From Your Friends at the IRS and DOJ Richard Charles Grosenick Office of Chief Counsel IRS Special Assistant United States Attorney 211 W. Wisconsin Ave. Suite 807

Federal Tax Issues in Bankruptcy A View From Your Friends at the IRS and DOJ Richard Charles Grosenick Office of Chief Counsel IRS Special Assistant United States Attorney 211 W. Wisconsin Ave. Suite 807

BANKRUPTCY: THE SILVER BULLET OF TAX DEFENSE. Dennis Brager, Esq.*

Adapted from an article that originally appeared in the California Tax Lawyer, Winter 1997 BANKRUPTCY: THE SILVER BULLET OF TAX DEFENSE Dennis Brager, Esq.* Many individuals, including accountants and

Adapted from an article that originally appeared in the California Tax Lawyer, Winter 1997 BANKRUPTCY: THE SILVER BULLET OF TAX DEFENSE Dennis Brager, Esq.* Many individuals, including accountants and

Discharging Taxes in Bankruptcy

When clients need protection from creditors, tax debts can be resolved as well. by Donald L. Ariail, CPA/CFP Michael M. Smith, Esq., CPA Neil Deininger, Esq., CPA and Reba M. Wingfield, Esq. Discharging

When clients need protection from creditors, tax debts can be resolved as well. by Donald L. Ariail, CPA/CFP Michael M. Smith, Esq., CPA Neil Deininger, Esq., CPA and Reba M. Wingfield, Esq. Discharging

AGOSTINO & ASSOCIATES, P.C. IRS Collections. Presented by : Frank Agostino

AGOSTINO & ASSOCIATES, P.C. IRS Collections Presented by : Frank Agostino DISCLAIMER: The following materials and accompanying Access MCLE, LLC audio program are for instructional purposes only. Nothing

AGOSTINO & ASSOCIATES, P.C. IRS Collections Presented by : Frank Agostino DISCLAIMER: The following materials and accompanying Access MCLE, LLC audio program are for instructional purposes only. Nothing

Taxes and Bankruptcy

Taxes and Bankruptcy Charles S. Parnell Parnell & Associates, P.C. 4891 Independence St., Suite 240 Wheat Ridge, CO 80033 303-234-0574 303-234-1415 fax [email protected] TABLE OF CONTENTS I. INTRODUCTION

Taxes and Bankruptcy Charles S. Parnell Parnell & Associates, P.C. 4891 Independence St., Suite 240 Wheat Ridge, CO 80033 303-234-0574 303-234-1415 fax [email protected] TABLE OF CONTENTS I. INTRODUCTION

How To Discharge A Tax Debt

How to Bankrupt Income Taxes 507 & 523 Attorney Nick C Thompson Louisville KY 40223 800 Stone Creek Parkway Suite 6 Louisville KY 40223 502-429-0057 [email protected] www.bankruptcy-divorce.com

How to Bankrupt Income Taxes 507 & 523 Attorney Nick C Thompson Louisville KY 40223 800 Stone Creek Parkway Suite 6 Louisville KY 40223 502-429-0057 [email protected] www.bankruptcy-divorce.com

ONE-DAY SEMINAR OUTLINE

ONE-DAY SEMINAR OUTLINE A. The Discharge of Indebtedness 8:30 am 9:20 am 1. IRC 61, 108, 1017; and Regulations thereunder. 2. Exclusions. 3. Exceptions. 4. Mortgage Debt Relief Act of 2007. 5. Definition

ONE-DAY SEMINAR OUTLINE A. The Discharge of Indebtedness 8:30 am 9:20 am 1. IRC 61, 108, 1017; and Regulations thereunder. 2. Exclusions. 3. Exceptions. 4. Mortgage Debt Relief Act of 2007. 5. Definition

The Examination Process. The IRS Mission

The IRS Mission Provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all. The Examination

The IRS Mission Provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all. The Examination

Income Tax Discharge Considerations in an Individual Debtor s Chapter 7 Bankruptcy

Income Tax Valuation Insights Income Tax Discharge Considerations in an Individual Debtor s Chapter 7 Bankruptcy Robert F. Reilly, CPA, and Ashley L. Reilly Many professional practitioners and small business

Income Tax Valuation Insights Income Tax Discharge Considerations in an Individual Debtor s Chapter 7 Bankruptcy Robert F. Reilly, CPA, and Ashley L. Reilly Many professional practitioners and small business

SAMPLE BANKRUPTCY DISCHARGE FORM Page 1 of 2

One Division Avenue Room 200 Grand Rapids, MI 49503-3132 Phone : (616) 456-2693 http://www.miwb.uscourts.gov/ WHAT IS CHAPTER 7 BANKRUPTCY? Chapter 7 bankruptcy, sometimes call a straight bankruptcy is

One Division Avenue Room 200 Grand Rapids, MI 49503-3132 Phone : (616) 456-2693 http://www.miwb.uscourts.gov/ WHAT IS CHAPTER 7 BANKRUPTCY? Chapter 7 bankruptcy, sometimes call a straight bankruptcy is

Avoid the IRS Maze When Representing Clients: Know How the IRS Works and What to Do When Representing Clients

Avoid the IRS Maze When Representing Clients: Know How the IRS Works and What to Do When Representing Clients This course looks at the organization of the IRS, including the IRS divisions involved with

Avoid the IRS Maze When Representing Clients: Know How the IRS Works and What to Do When Representing Clients This course looks at the organization of the IRS, including the IRS divisions involved with

IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF IDAHO

IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF IDAHO In re: ALAN GREENWAY, Bankruptcy Case No. 04-04100 dba Greenway Seed Co., Debtor. MEMORANDUM OF DECISION Appearances: D. Blair Clark, RINGERT,

IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF IDAHO In re: ALAN GREENWAY, Bankruptcy Case No. 04-04100 dba Greenway Seed Co., Debtor. MEMORANDUM OF DECISION Appearances: D. Blair Clark, RINGERT,

Collection Bankruptcy Overview

Collection Bankruptcy Overview Small Business/Self-Employed Division January 25, 2011 The information contained in this presentation is current as of the date it was presented. It should not be considered

Collection Bankruptcy Overview Small Business/Self-Employed Division January 25, 2011 The information contained in this presentation is current as of the date it was presented. It should not be considered

UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF FLORIDA TAMPA DIVISION. In re. Case No. 8:04-bk-10201-KRM BACKGROUND KATHY L.

In re UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF FLORIDA TAMPA DIVISION KATHY L. COLE, Case No. 8:04-bk-10201-KRM Debtor. ) KATHY L. COLE, vs. Plaintiff, Adversary No. 04-00361 UNITED STATES OF

In re UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF FLORIDA TAMPA DIVISION KATHY L. COLE, Case No. 8:04-bk-10201-KRM Debtor. ) KATHY L. COLE, vs. Plaintiff, Adversary No. 04-00361 UNITED STATES OF

Bankruptcy or Offer in Compromise? Where the Bankruptcy Code and IRS Policy Meet. By Howard S. Levy

Bankruptcy or Offer in Compromise? Where the Bankruptcy Code and IRS Policy Meet By Howard S. Levy As Published in the Journal of Tax Practice and Procedure February - March, 2000 The choice between a

Bankruptcy or Offer in Compromise? Where the Bankruptcy Code and IRS Policy Meet By Howard S. Levy As Published in the Journal of Tax Practice and Procedure February - March, 2000 The choice between a

Frequently Asked Questions. for. Chapter 7 Debtors

Frequently Asked Questions for Chapter 7 Debtors The information contained in this document is provided as a service to our clients, and does not constitute legal advice. We try to provide quality information,

Frequently Asked Questions for Chapter 7 Debtors The information contained in this document is provided as a service to our clients, and does not constitute legal advice. We try to provide quality information,

Offer in Compromise. Attach Application Fee and Payment (check or money order) here. IRS Received Date. (Rev. May 2012) Section 3

here. IRS Received Date. (Rev. May 2012) Section 3") Form 656 (Rev. May 2012) Department of the Treasury Internal Revenue Service Offer in Compromise Attach Application Fee and Payment (check or money order) here. Section 1 Your Contact Information Your

Form 656 (Rev. May 2012) Department of the Treasury Internal Revenue Service Offer in Compromise Attach Application Fee and Payment (check or money order) here. Section 1 Your Contact Information Your

This Chief Counsel Advice responds to your request for assistance. This advice may not be used or cited as precedent.

Office of Chief Counsel Internal Revenue Service memorandum Number: 201005029 Release Date: 2/5/2010 CC:PA:Br5 POSTN-137568-09 UILC: 09.00.00-00 date: October 21, 2009 to: from: Michael Skeen, Associate

Office of Chief Counsel Internal Revenue Service memorandum Number: 201005029 Release Date: 2/5/2010 CC:PA:Br5 POSTN-137568-09 UILC: 09.00.00-00 date: October 21, 2009 to: from: Michael Skeen, Associate

Case 10-32200 Document 33 Filed in TXSB on 04/21/10 Page 1 of 8 IN THE UNITED STATES BANKRUPTCY COURT FOR THE SOUTHERN DISTRICT OF TEXAS

Case 10-32200 Document 33 Filed in TXSB on 04/21/10 Page 1 of 8 IN THE UNITED STATES BANKRUPTCY COURT FOR THE SOUTHERN DISTRICT OF TEXAS HOUSTON DIVISION ENTERED 04/21/2010 ) IN RE ) ) SOUTHWEST GUARANTY,

Case 10-32200 Document 33 Filed in TXSB on 04/21/10 Page 1 of 8 IN THE UNITED STATES BANKRUPTCY COURT FOR THE SOUTHERN DISTRICT OF TEXAS HOUSTON DIVISION ENTERED 04/21/2010 ) IN RE ) ) SOUTHWEST GUARANTY,

Offer in Compromise Program Updates

Offer in Compromise Program Updates Presenter name: Joseph Lewandoski Presenter title: Senior Stakeholder Liaison Small Business/Self-Employed Division Date What is an Offer in Compromise? An agreement

Offer in Compromise Program Updates Presenter name: Joseph Lewandoski Presenter title: Senior Stakeholder Liaison Small Business/Self-Employed Division Date What is an Offer in Compromise? An agreement

3.1.11.3 STATUTORY AUTHORITY: Section 9-11-6.2 NMSA 1978. [3/15/96; 3.1.11.3 NMAC - Rn, 3 NMAC 1.11.3, 1/15/01]

![3.1.11.3 STATUTORY AUTHORITY: Section 9-11-6.2 NMSA 1978. [3/15/96; 3.1.11.3 NMAC - Rn, 3 NMAC 1.11.3, 1/15/01]](/thumbs/26/9157741.jpg "3.1.11.3 STATUTORY AUTHORITY: Section 9-11-6.2 NMSA 1978. [3/15/96; 3.1.11.3 NMAC - Rn, 3 NMAC 1.11.3, 1/15/01]") TITLE 3: CHAPTER 1: PART 11: TAXATION TAX ADMINISTRATION PENALTIES 3.1.11.1 ISSUING AGENCY: Taxation and Revenue Department, Joseph M. Montoya Building, 1100 South St. Francis Drive, P.O. Box 630, Santa

TITLE 3: CHAPTER 1: PART 11: TAXATION TAX ADMINISTRATION PENALTIES 3.1.11.1 ISSUING AGENCY: Taxation and Revenue Department, Joseph M. Montoya Building, 1100 South St. Francis Drive, P.O. Box 630, Santa

Matthew Von Schuch. Tax Attorney and CPA

Matthew Von Schuch Tax Attorney and CPA 7 METHODS TO RESOLVE IRS TAX DEBT Offer in Compromise Settling tax debt for less than owed Installment Agreement A payment plan for tax debts Non- Collectable Status

Matthew Von Schuch Tax Attorney and CPA 7 METHODS TO RESOLVE IRS TAX DEBT Offer in Compromise Settling tax debt for less than owed Installment Agreement A payment plan for tax debts Non- Collectable Status

HP0868, LD 1187, item 1, 123rd Maine State Legislature An Act To Recoup Health Care Funds through the Maine False Claims Act

PLEASE NOTE: Legislative Information cannot perform research, provide legal advice, or interpret Maine law. For legal assistance, please contact a qualified attorney. Be it enacted by the People of the

PLEASE NOTE: Legislative Information cannot perform research, provide legal advice, or interpret Maine law. For legal assistance, please contact a qualified attorney. Be it enacted by the People of the

Chapter 7 Liquidation Under the Bankruptcy Code

From Administrative Office of the United States Courts, Bankruptcy Basics, Public Information Series. Chapter 7 Liquidation Under the Bankruptcy Code The chapter of the Bankruptcy Code providing for "liquidation,"

From Administrative Office of the United States Courts, Bankruptcy Basics, Public Information Series. Chapter 7 Liquidation Under the Bankruptcy Code The chapter of the Bankruptcy Code providing for "liquidation,"

TAXPAYER RIGHTS ACT OF 2015: SECTION-BY-SECTION SUMMARY

TAXPAYER RIGHTS ACT OF 2015: SECTION-BY-SECTION SUMMARY TAXPAYER RIGHTS Section 101. Statement of Taxpayer Rights. Section 101 requires the Secretary of the Treasury to publish a Taxpayer Bill of Rights

TAXPAYER RIGHTS ACT OF 2015: SECTION-BY-SECTION SUMMARY TAXPAYER RIGHTS Section 101. Statement of Taxpayer Rights. Section 101 requires the Secretary of the Treasury to publish a Taxpayer Bill of Rights

BANKRUPTCY BASICS AND TIPS FOR COLLECTION OF PROPERTY TAXES FROM TAXPAYERS IN BANKRUPTCY

BANKRUPTCY BASICS AND TIPS FOR COLLECTION OF PROPERTY TAXES FROM TAXPAYERS IN BANKRUPTCY by Roy F. Kiplinger Kiplinger Law Firm, P.C. August 5, 2010 We pride ourselves in providing quality legal services

BANKRUPTCY BASICS AND TIPS FOR COLLECTION OF PROPERTY TAXES FROM TAXPAYERS IN BANKRUPTCY by Roy F. Kiplinger Kiplinger Law Firm, P.C. August 5, 2010 We pride ourselves in providing quality legal services

The IRS Collection Process Keep this publication for future reference Publication 594

IRS Mission: Provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all. What You Should

IRS Mission: Provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all. What You Should

Don't go it alone* The IRS collection process. pwc. *connectedthinking. Introduction. IRS emphasis on increasing tax collection.

IRS Service Team Don't go it alone* The IRS collection process Introduction Taxpayers periodically request assistance with IRS collection matters. IRS collection contacts can appear intimidating, and taxpayers

IRS Service Team Don't go it alone* The IRS collection process Introduction Taxpayers periodically request assistance with IRS collection matters. IRS collection contacts can appear intimidating, and taxpayers

REASONS FOR COMMON RECOMMENDATION PROVISIONS RUSSELL BROWN, TRUSTEE

REASONS FOR COMMON RECOMMENDATION PROVISIONS RUSSELL BROWN, TRUSTEE RECOMMENDATION LANGUAGE The principal amount to be paid to [creditor] is to be reduced to the amount stated in the creditor s proof of

REASONS FOR COMMON RECOMMENDATION PROVISIONS RUSSELL BROWN, TRUSTEE RECOMMENDATION LANGUAGE The principal amount to be paid to [creditor] is to be reduced to the amount stated in the creditor s proof of

TOP THINGS TO REMEMBER ABOUT THE TRUSTEE S OFFICE AND YOUR CHAPTER 13 CASE

TOP THINGS TO REMEMBER ABOUT THE TRUSTEE S OFFICE AND YOUR CHAPTER 13 CASE 1. Know your case number. 2. Make your payments. Send your payments in time for the payments to reach the Trustee s office by

TOP THINGS TO REMEMBER ABOUT THE TRUSTEE S OFFICE AND YOUR CHAPTER 13 CASE 1. Know your case number. 2. Make your payments. Send your payments in time for the payments to reach the Trustee s office by

Small Business Seminar Offer in Compromise. Felicia Branch August 15, 2015

Small Business Seminar Offer in Compromise Felicia Branch August 15, 2015 Collection Power of the IRS What can they do? For how long? What alternatives does the taxpayer have? Can the taxpayer appeal a

Small Business Seminar Offer in Compromise Felicia Branch August 15, 2015 Collection Power of the IRS What can they do? For how long? What alternatives does the taxpayer have? Can the taxpayer appeal a

Bankruptcy 101 A Guide to Personal Bankruptcy. Brought to you by Jon Martin, Esq. Http://www.TheSinCityLawyer.com

Bankruptcy 101 A Guide to Personal Bankruptcy Brought to you by Jon Martin, Esq. Http://www.TheSinCityLawyer.com Bankruptcy laws help people who can no longer pay their creditors get a fresh start by liquidating

Bankruptcy 101 A Guide to Personal Bankruptcy Brought to you by Jon Martin, Esq. Http://www.TheSinCityLawyer.com Bankruptcy laws help people who can no longer pay their creditors get a fresh start by liquidating

Offer in Compromise. Worksheets to calculate an acceptable offer amount using Form 433-A and/or 433-B and Publication 1854*

Department of Treasury Internal Revenue Service Form 656 (Rev. 1-97) Catalog Number 16728N Form 656 Offer in Compromise What you should know before submitting an offer in compromise Worksheets to calculate

Department of Treasury Internal Revenue Service Form 656 (Rev. 1-97) Catalog Number 16728N Form 656 Offer in Compromise What you should know before submitting an offer in compromise Worksheets to calculate

BANKRUPTCY TERMINOLOGY

ADVERSARY PROCEEDING BANKRUPTCY TERMINOLOGY A lawsuit arising in or related to a bankruptcy case that is commenced by filing a complaint with the bankruptcy court. ASSUME An agreement to continue performing

ADVERSARY PROCEEDING BANKRUPTCY TERMINOLOGY A lawsuit arising in or related to a bankruptcy case that is commenced by filing a complaint with the bankruptcy court. ASSUME An agreement to continue performing

UNITED STATES BANKRUPTCY COURT DISTRICT OF VIRGINIA Division CHAPTER 13 PLAN AND RELATED MOTIONS

UNITED STATES BANKRUPTCY COURT DISTRICT OF VIRGINIA Division CHAPTER 13 PLAN AND RELATED MOTIONS Name of Debtor(s): Case No: This Plan, dated, is: the first Chapter 13 Plan filed in this case. a modified

UNITED STATES BANKRUPTCY COURT DISTRICT OF VIRGINIA Division CHAPTER 13 PLAN AND RELATED MOTIONS Name of Debtor(s): Case No: This Plan, dated, is: the first Chapter 13 Plan filed in this case. a modified

5/3/2015. Dealing with the IRS Collection Division. Eric L. Green. Discussion Topics

Dealing with the IRS Collection Division Presented by Eric L. Green, Esq. Green & Sklarz LLC www.gs lawfirm.com Eric L. Green Eric is a partner with Green & Sklarz, LLC in Connecticut. The focus is civil

Dealing with the IRS Collection Division Presented by Eric L. Green, Esq. Green & Sklarz LLC www.gs lawfirm.com Eric L. Green Eric is a partner with Green & Sklarz, LLC in Connecticut. The focus is civil

APPENDIX A IN THE UNITED STATES BANKRUPTCY COURT FOR THE EASTERN DISTRICT OF TEXAS

APPENDIX A IN THE UNITED STATES BANKRUPTCY COURT FOR THE EASTERN DISTRICT OF TEXAS In re: MICHELE GRAHAM, Case No.: 02-43262 (Chapter 7 Debtor. FEDERAL TRADE COMMISSION, Plaintiff, v. Adversary Proceeding

APPENDIX A IN THE UNITED STATES BANKRUPTCY COURT FOR THE EASTERN DISTRICT OF TEXAS In re: MICHELE GRAHAM, Case No.: 02-43262 (Chapter 7 Debtor. FEDERAL TRADE COMMISSION, Plaintiff, v. Adversary Proceeding

UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF CALIFORNIA

UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF CALIFORNIA In re: ) FILED September 11, 2012 ) CHAPTER 7 RIGHTS AND ) BANKRUPTCY GENERAL RESPONSIBILITIES and ) ORDER NO. 180 AMENDMENTS TO LOCAL ) BANKRUPTCY

UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF CALIFORNIA In re: ) FILED September 11, 2012 ) CHAPTER 7 RIGHTS AND ) BANKRUPTCY GENERAL RESPONSIBILITIES and ) ORDER NO. 180 AMENDMENTS TO LOCAL ) BANKRUPTCY

The Nuts and Bolts of Handling a Pro Bono Tax Controversy Case. Presented by The ABA Section of Taxation

The Nuts and Bolts of Handling a Pro Bono Tax Controversy Case Presented by The ABA Section of Taxation Panelists Caroline Ciraolo - Rosenberg, Martin, Greenberg, LLP, Baltimore, Maryland Catherine Engell

The Nuts and Bolts of Handling a Pro Bono Tax Controversy Case Presented by The ABA Section of Taxation Panelists Caroline Ciraolo - Rosenberg, Martin, Greenberg, LLP, Baltimore, Maryland Catherine Engell

PRACTICE GUIDELINES MEMORANDUM. RE: Sample Bankruptcy Motions and Orders for Personal Injury Practitioners and Trustees

PRACTICE GUIDELINES MEMORANDUM TO: FROM: Attorneys Practicing Before Me And Other Interested Persons C. Timothy Corcoran, III United States Bankruptcy Judge DATE: January 3, 2000 1 RE: Sample Bankruptcy

PRACTICE GUIDELINES MEMORANDUM TO: FROM: Attorneys Practicing Before Me And Other Interested Persons C. Timothy Corcoran, III United States Bankruptcy Judge DATE: January 3, 2000 1 RE: Sample Bankruptcy

FINDINGS OF FACT AND CONCLUSIONS OF LAW. A. Stipulated Facts

JURISDICTION: - DECISION CITE: 2001-01-25-004 / NOT PRECEDENTIAL ID: P9900093 DATE: 01-25-01 DISPOSITION: DENIED TAX TYPE: INCOME APPEAL: NO APPEAL TAKEN FINDINGS OF FACT AND CONCLUSIONS OF LAW A. Stipulated

JURISDICTION: - DECISION CITE: 2001-01-25-004 / NOT PRECEDENTIAL ID: P9900093 DATE: 01-25-01 DISPOSITION: DENIED TAX TYPE: INCOME APPEAL: NO APPEAL TAKEN FINDINGS OF FACT AND CONCLUSIONS OF LAW A. Stipulated

Taxpayer Bill of Rights Adopted June 10, 2014

1. The Right to Be Informed Taxpayers have the right to know what they need to do to comply with the tax laws. They are entitled to clear explanations of the laws and IRS procedures in all tax forms, instructions,

1. The Right to Be Informed Taxpayers have the right to know what they need to do to comply with the tax laws. They are entitled to clear explanations of the laws and IRS procedures in all tax forms, instructions,

IN THE UNITED STATES BANKRUPTCY COURT FOR THE WESTERN DISTRICT OF MISSOURI

MOW 2016-1.3 (5/22/07) IN THE UNITED STATES BANKRUPTCY COURT FOR THE WESTERN DISTRICT OF MISSOURI IN RE: ) ) ) Case No. ) ) Debtors. ) RIGHTS AND RESPONSIBILITIES AGREEMENT BETWEEN CHAPTER 7 DEBTORS AND

MOW 2016-1.3 (5/22/07) IN THE UNITED STATES BANKRUPTCY COURT FOR THE WESTERN DISTRICT OF MISSOURI IN RE: ) ) ) Case No. ) ) Debtors. ) RIGHTS AND RESPONSIBILITIES AGREEMENT BETWEEN CHAPTER 7 DEBTORS AND

STUDENT BANKRUPTCY AND THE PERMISSIBILITY OF TRADITIONAL CAMPUS COLLECTION MEASURES

TOPIC: STUDENT BANKRUPTCY AND THE PERMISSIBILITY OF TRADITIONAL CAMPUS COLLECTION MEASURES INTRODUCTION: While some economic indicators signal the end of the recession, the fact remains that consumer bankruptcy

TOPIC: STUDENT BANKRUPTCY AND THE PERMISSIBILITY OF TRADITIONAL CAMPUS COLLECTION MEASURES INTRODUCTION: While some economic indicators signal the end of the recession, the fact remains that consumer bankruptcy

The IRS Collection Process Publication 594

The IRS Collection Process Publication 594 Page 1 The IRS Collection Process Publication 594 This publication provides a general description of the IRS collection process. The collection process is a series

The IRS Collection Process Publication 594 Page 1 The IRS Collection Process Publication 594 This publication provides a general description of the IRS collection process. The collection process is a series

KENTUCKY DEPARTMENT OF REVENUE OFFER IN SETTLEMENT APPLICATION CHECKLIST. Form 12A018 (08/12)

") CHECKLIST I. BEFORE COMPLETING THE APPLICATION, PLEASE VERIFY THAT YOU ARE ELIGIBLE TO SUBMIT AN OFFER IN SETTLEMENT! Check (a) or (b) to each question below. If you check (a), you may proceed to the next

CHECKLIST I. BEFORE COMPLETING THE APPLICATION, PLEASE VERIFY THAT YOU ARE ELIGIBLE TO SUBMIT AN OFFER IN SETTLEMENT! Check (a) or (b) to each question below. If you check (a), you may proceed to the next

The CNMI Division of Revenue and Tax s Collection Process Keep this publication for future reference

DIVISION OF REVENUE AND TAXATION COMMONWEALTH OF THE NORTHERN MARIANA ISLANDS Post Office Box 5234 CHRB Saipan, MP 96950 Tel. (670) 664-1000 What You Should Know About The CNMI Division of Revenue and

DIVISION OF REVENUE AND TAXATION COMMONWEALTH OF THE NORTHERN MARIANA ISLANDS Post Office Box 5234 CHRB Saipan, MP 96950 Tel. (670) 664-1000 What You Should Know About The CNMI Division of Revenue and

Offer in Compromise (Doubt as to Liability)

") Form 656-L Offer in Compromise (Doubt as to Liability) CONTENTS What you need to know...2 Important information...2 Form 656-L...5 IRS contact information If you have questions about qualifying for an

Form 656-L Offer in Compromise (Doubt as to Liability) CONTENTS What you need to know...2 Important information...2 Form 656-L...5 IRS contact information If you have questions about qualifying for an

UNITED STATES BANKRUPTCY COURT EASTERN DISTRICT OF WISCONSIN. In re Case No. 13-23483 JANICE RENEE PUGH, Chapter 13 Debtor.

UNITED STATES BANKRUPTCY COURT EASTERN DISTRICT OF WISCONSIN In re Case No. 13-23483 JANICE RENEE PUGH, Chapter 13 Debtor. MEMORANDUM DECISION ON DEBTOR S OBJECTION TO INTERNAL REVENUE SERVICE S MOTION

UNITED STATES BANKRUPTCY COURT EASTERN DISTRICT OF WISCONSIN In re Case No. 13-23483 JANICE RENEE PUGH, Chapter 13 Debtor. MEMORANDUM DECISION ON DEBTOR S OBJECTION TO INTERNAL REVENUE SERVICE S MOTION

INTRODUCTION TO BANKRUPTCY CODE REMEDIES. 101 Overview...1. 115 Glossary...2. 125 Advantages and Disadvantages of Tax Remedies...6

INTRODUCTION TO BANKRUPTCY CODE REMEDIES 101 Overview...1 115 Glossary...2 125 Advantages and Disadvantages of Tax Remedies...6.01 Tax Code remedy: statute of limitation on collection.6.02 Tax Code remedy:

INTRODUCTION TO BANKRUPTCY CODE REMEDIES 101 Overview...1 115 Glossary...2 125 Advantages and Disadvantages of Tax Remedies...6.01 Tax Code remedy: statute of limitation on collection.6.02 Tax Code remedy:

Section 362(c)(3): Does It Terminate The Entire Automatic Stay? Michael Aryeh, J.D. Candidate 2015

(3): Does It Terminate The Entire Automatic Stay? Michael Aryeh, J.D. Candidate 2015") 2014 Volume VI No. 2 Section 362(c)(3): Does It Terminate The Entire Automatic Stay? Michael Aryeh, J.D. Candidate 2015 Cite as: Section 362(c)(3): Does It Terminate The Entire Automatic Stay?, 6 ST. JOHN

2014 Volume VI No. 2 Section 362(c)(3): Does It Terminate The Entire Automatic Stay? Michael Aryeh, J.D. Candidate 2015 Cite as: Section 362(c)(3): Does It Terminate The Entire Automatic Stay?, 6 ST. JOHN

Determining Tax Liability Under Section 505(a) of the Bankruptcy Code

of the Bankruptcy Code") Determining Tax Liability Under Section 505(a) of the Bankruptcy Code Section 505(a) of the Bankruptcy Code (the Code ) provides the means by which a debtor or trustee in bankruptcy may seek a determination

Determining Tax Liability Under Section 505(a) of the Bankruptcy Code Section 505(a) of the Bankruptcy Code (the Code ) provides the means by which a debtor or trustee in bankruptcy may seek a determination

CHAPTER 9 Municipality Bankruptcy

U.S. COURTS HTTP://WWW.USCOURTS.GOV/FEDERALCOURTS/BANKRUPTCY/BANKRUPTCY BASICS/CHAPTER9.ASPX CHAPTER 9 Municipality Bankruptcy The chapter of the Bankruptcy Code providing for reorganization of municipalities

U.S. COURTS HTTP://WWW.USCOURTS.GOV/FEDERALCOURTS/BANKRUPTCY/BANKRUPTCY BASICS/CHAPTER9.ASPX CHAPTER 9 Municipality Bankruptcy The chapter of the Bankruptcy Code providing for reorganization of municipalities

Tax Refund Interception on Account of Discharged Debt

Tip of the Month January 2012 Tax Refund Interception on Account of Discharged Debt Submitted by Christopher Wilcox AmeriCorps VISTA Attorney at Volunteer Lawyers Network Often, debtors that file for bankruptcy

Tip of the Month January 2012 Tax Refund Interception on Account of Discharged Debt Submitted by Christopher Wilcox AmeriCorps VISTA Attorney at Volunteer Lawyers Network Often, debtors that file for bankruptcy

Notice to Delinquent Taxpayers

Notice to Delinquent Taxpayers Department of the Treasury Alcohol and Tobacco Tax and Trade Bureau TTB P 5610.1 (1/04) Previous Editions are Obsolete NOTICE TO DELINQUENT TAXPAYERS INTRODUCTION When you

Notice to Delinquent Taxpayers Department of the Treasury Alcohol and Tobacco Tax and Trade Bureau TTB P 5610.1 (1/04) Previous Editions are Obsolete NOTICE TO DELINQUENT TAXPAYERS INTRODUCTION When you

AN ACT IN THE COUNCIL OF THE DISTRICT OF COLUMBIA

AN ACT IN THE COUNCIL OF THE DISTRICT OF COLUMBIA To amend the District of Columbia Procurement Practices Act of 1985 to make the District s false claims act consistent with federal law and thereby qualify

AN ACT IN THE COUNCIL OF THE DISTRICT OF COLUMBIA To amend the District of Columbia Procurement Practices Act of 1985 to make the District s false claims act consistent with federal law and thereby qualify

The state's collection procedures are detailed in the State Administrative Manual. Collection steps may include some or all of the following:

This report is submitted to meet the provisions of Government Code (GC) Section 13292.5, requiring annual reporting by the Department of Finance to the Legislature on the status of delinquent receivables

This report is submitted to meet the provisions of Government Code (GC) Section 13292.5, requiring annual reporting by the Department of Finance to the Legislature on the status of delinquent receivables

UNITED STATES BANKRUPTCY APPELLATE PANEL OF THE NINTH CIRCUIT

Case: 13-1313 Document: 10 Filed: 09/09/2013 Page: 1 of 12 Edward A. Murphy MURPHY LAW OFFICES, PLLC P.O. Box 2639 Missoula, MT 59806 Phone: (406)728-2671 Email: [email protected] Bar No. 201108

Case: 13-1313 Document: 10 Filed: 09/09/2013 Page: 1 of 12 Edward A. Murphy MURPHY LAW OFFICES, PLLC P.O. Box 2639 Missoula, MT 59806 Phone: (406)728-2671 Email: [email protected] Bar No. 201108

U.S. Department of Education Employer s Garnishment Handbook Revised February 10, 2009

U.S. Department of Education Employer s Garnishment Handbook Revised February 10, 2009 Table of Content Introduction Overview... 3 Legislative Authority... 4 Under This Authority:... 4 Sec. 34.19 Amounts

U.S. Department of Education Employer s Garnishment Handbook Revised February 10, 2009 Table of Content Introduction Overview... 3 Legislative Authority... 4 Under This Authority:... 4 Sec. 34.19 Amounts

LOCAL BANKRUPTCY FORM 4001-1.1 [Caption as in Bankruptcy Official Form 16A]

![LOCAL BANKRUPTCY FORM 4001-1.1 [Caption as in Bankruptcy Official Form 16A]](/thumbs/26/7327530.jpg "LOCAL BANKRUPTCY FORM 4001-1.1 [Caption as in Bankruptcy Official Form 16A]") LOCAL BANKRUPTCY FORM 4001-1.1 NOTICE OF MOTION FOR RELIEF FROM STAY AND OPPORTUNITY FOR HEARING PURSUANT TO 11 U.S.C. 362(d) OBJECTION DEADLINE: (month/day/year). YOU ARE HEREBY NOTIFIED that a Motion

LOCAL BANKRUPTCY FORM 4001-1.1 NOTICE OF MOTION FOR RELIEF FROM STAY AND OPPORTUNITY FOR HEARING PURSUANT TO 11 U.S.C. 362(d) OBJECTION DEADLINE: (month/day/year). YOU ARE HEREBY NOTIFIED that a Motion

The individual or husband and wife must be engaged in a farming operation or a commercial fishing operation.

Chapter 12 Background: Chapter 12 is designed for "family farmers" or "family fishermen" with "regular annual income." It enables financially distressed family farmers and fishermen to propose and carry

Chapter 12 Background: Chapter 12 is designed for "family farmers" or "family fishermen" with "regular annual income." It enables financially distressed family farmers and fishermen to propose and carry

UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF FLORIDA TAMPA DIVISION

UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF FLORIDA TAMPA DIVISION In re: Case No. 99-14794-8G7 WILLIAM O'CALLAGHAN, Debtor. Chapter 7 WILLIAM O'CALLAGHAN, Plaintiff, vs. Adv. No. 99-589 UNITED STATES

UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF FLORIDA TAMPA DIVISION In re: Case No. 99-14794-8G7 WILLIAM O'CALLAGHAN, Debtor. Chapter 7 WILLIAM O'CALLAGHAN, Plaintiff, vs. Adv. No. 99-589 UNITED STATES

The Announcement provides an overview of the IRS s use of private collection agencies (PCAs) in 2006

in 2006") Part IV- Items of General Interest The Announcement provides an overview of the IRS s use of private collection agencies (PCAs) in 2006 ANNOUNCEMENT 2006-63 Section 881 of the American Jobs Creation Act,

Part IV- Items of General Interest The Announcement provides an overview of the IRS s use of private collection agencies (PCAs) in 2006 ANNOUNCEMENT 2006-63 Section 881 of the American Jobs Creation Act,

REG-152166-05 Taxpayer Assistance Orders

DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 301 REG-152166-05 Taxpayer Assistance Orders RIN 1545-BF33 AGENCY: Internal Revenue Service (IRS), Treasury. ACTION: Withdrawal of notice

DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 301 REG-152166-05 Taxpayer Assistance Orders RIN 1545-BF33 AGENCY: Internal Revenue Service (IRS), Treasury. ACTION: Withdrawal of notice

Contents. About This Book How To Use This Book Foreword Acknowledgments About the Author

Contents About This Book How To Use This Book Foreword Acknowledgments About the Author vii ix xi xiii xv Chapter 1 Initial Client Engagement 5 Topical Index 1 1.01 Nature of Federal Tax Law 5 1.02 Role

Contents About This Book How To Use This Book Foreword Acknowledgments About the Author vii ix xi xiii xv Chapter 1 Initial Client Engagement 5 Topical Index 1 1.01 Nature of Federal Tax Law 5 1.02 Role

Important Information for Chapter 13 Participants

Important Information for Chapter 13 Participants Keep this book for reference thoughout your plan. INTRODUCTION. Chapter 13 is one way under the Bankruptcy Code to obtain relief from your creditors while

Important Information for Chapter 13 Participants Keep this book for reference thoughout your plan. INTRODUCTION. Chapter 13 is one way under the Bankruptcy Code to obtain relief from your creditors while

IN THE UNITED STATES BANKRUPTCY COURT FOR THE SOUTHERN DISTRICT OF TEXAS HOUSTON DIVISION

IN THE UNITED STATES BANKRUPTCY COURT FOR THE SOUTHERN DISTRICT OF TEXAS HOUSTON DIVISION DUTIES AND RESPONSIBILITIES OF A DEBTOR UNDER CHAPTER 7 AND ATTENDANCE AT THE 341 MEETING OF CREDITORS In either

IN THE UNITED STATES BANKRUPTCY COURT FOR THE SOUTHERN DISTRICT OF TEXAS HOUSTON DIVISION DUTIES AND RESPONSIBILITIES OF A DEBTOR UNDER CHAPTER 7 AND ATTENDANCE AT THE 341 MEETING OF CREDITORS In either

UNITEDSTATESTAX COURT

UNITEDSTATESTAX COURT (FIRST) (MIDDLE) (LAST) 2014 Allgreens LLC (PLEASE TYPE OR PRINT) v. Petition Docket No. COMMISSIONER OF INTERNAL REVENUE, Respondent PETITION 1. Please check the appropriate box(es)

UNITEDSTATESTAX COURT (FIRST) (MIDDLE) (LAST) 2014 Allgreens LLC (PLEASE TYPE OR PRINT) v. Petition Docket No. COMMISSIONER OF INTERNAL REVENUE, Respondent PETITION 1. Please check the appropriate box(es)

51ST LEGISLATURE - STATE OF NEW MEXICO - FIRST SESSION, 2013

SENATE BILL 1ST LEGISLATURE - STATE OF NEW MEXICO - FIRST SESSION, INTRODUCED BY Joseph Cervantes 1 ENDORSED BY THE COURTS, CORRECTIONS AND JUSTICE COMMITTEE AN ACT RELATING TO CIVIL ACTIONS; CLARIFYING

SENATE BILL 1ST LEGISLATURE - STATE OF NEW MEXICO - FIRST SESSION, INTRODUCED BY Joseph Cervantes 1 ENDORSED BY THE COURTS, CORRECTIONS AND JUSTICE COMMITTEE AN ACT RELATING TO CIVIL ACTIONS; CLARIFYING

Claims Submitted to the IRS Whistleblower Office under Section 7623. This Notice provides guidance to the public on how to file claims under Internal

Part III Administrative, Procedural, and Miscellaneous Claims Submitted to the IRS Whistleblower Office under Section 7623 Notice 2008-4 SECTION 1. PURPOSE This Notice provides guidance to the public on

Part III Administrative, Procedural, and Miscellaneous Claims Submitted to the IRS Whistleblower Office under Section 7623 Notice 2008-4 SECTION 1. PURPOSE This Notice provides guidance to the public on

Chapter 13 Handbook. David Burchard Chapter 13 Trustee Santa Rosa Division. (707) 544-5500 * Fax (707) 544-0475 www.burchardtrustee.

544-5500 * Fax (707) 544-0475 www.burchardtrustee.") Chapter 13 Handbook David Burchard Chapter 13 Trustee Santa Rosa Division (707) 544-5500 * Fax (707) 544-0475 www.burchardtrustee.com TABLE OF CONTENTS I. Disclaimer.....1 II. Introduction.......2 III.

Chapter 13 Handbook David Burchard Chapter 13 Trustee Santa Rosa Division (707) 544-5500 * Fax (707) 544-0475 www.burchardtrustee.com TABLE OF CONTENTS I. Disclaimer.....1 II. Introduction.......2 III.

United States Bankruptcy Court Central District of California

6:12-15990 #51.00 Confirmation of Plan Also #15 EH Docket #: Tentative Ruling: On March 9, 2012, Debtors filed a voluntary Petition. On the same day, Debtors filed their Plan (the Plan ). The Plan included

6:12-15990 #51.00 Confirmation of Plan Also #15 EH Docket #: Tentative Ruling: On March 9, 2012, Debtors filed a voluntary Petition. On the same day, Debtors filed their Plan (the Plan ). The Plan included

ROSE KRAIZA : SUPERIOR COURT. v. : JUDICIAL DISTRICT OF : NEW BRITAIN COMMISSIONER OF REVENUE SERVICES STATE OF CONNECTICUT : FEBRUARY 2, 2009

NO. CV 04 4002676 ROSE KRAIZA : SUPERIOR COURT : TAX SESSION v. : JUDICIAL DISTRICT OF : NEW BRITAIN COMMISSIONER OF REVENUE SERVICES STATE OF CONNECTICUT : FEBRUARY 2, 2009 MEMORANDUM OF DECISION ON MOTION

NO. CV 04 4002676 ROSE KRAIZA : SUPERIOR COURT : TAX SESSION v. : JUDICIAL DISTRICT OF : NEW BRITAIN COMMISSIONER OF REVENUE SERVICES STATE OF CONNECTICUT : FEBRUARY 2, 2009 MEMORANDUM OF DECISION ON MOTION

TARBOX LAW, P.C. 2301 Broadway Lubbock, Texas 79401 Phone - (806) 686-4448 Fax - (806) 368-9785

686-4448 Fax - (806) 368-9785") TARBOX LAW, P.C. 2301 Broadway Lubbock, Texas 79401 Phone - (806) 686-4448 Fax - (806) 368-9785 1. Type of Bankruptcy. CONTRACT FOR CHAPTER 7 BANKRUPTCY SERVICES Debtor retains attorney to file a Chapter

TARBOX LAW, P.C. 2301 Broadway Lubbock, Texas 79401 Phone - (806) 686-4448 Fax - (806) 368-9785 1. Type of Bankruptcy. CONTRACT FOR CHAPTER 7 BANKRUPTCY SERVICES Debtor retains attorney to file a Chapter

App-1 Definitions Accrual of Action. For debt collection, this is the point in time after which a legal action may be brought against a debtor.

APPENDIX 1 1900.25 REV-4 App-1 Definitions Accrual of Action. For debt collection, this is the point in time after which a legal action may be brought against a debtor. Generally, this is recognized as

APPENDIX 1 1900.25 REV-4 App-1 Definitions Accrual of Action. For debt collection, this is the point in time after which a legal action may be brought against a debtor. Generally, this is recognized as

UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF MICHIGAN SOUTHERN DIVISION

2:14-cv-10511-RHC-MAR Doc # 1 Filed 02/04/14 Pg 1 of 9 Pg ID 1 UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF MICHIGAN SOUTHERN DIVISION UNITED STATES OF AMERICA, ) ) Plaintiff, ) Civil No. 2:14-cv-10511

2:14-cv-10511-RHC-MAR Doc # 1 Filed 02/04/14 Pg 1 of 9 Pg ID 1 UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF MICHIGAN SOUTHERN DIVISION UNITED STATES OF AMERICA, ) ) Plaintiff, ) Civil No. 2:14-cv-10511