Vittorio Corbo: Monetary policy in emerging countries the view from Chile

|

|

|

- Clemence Francis

- 8 years ago

- Views:

Transcription

1 Vittorio Corbo: Monetary policy in emerging countries the view from Chile Speech by Mr Vittorio Corbo, Governor of the Central Bank of Chile, at the Bank of Italy, Rome, 18 June Prepared for presentation at Banca d Italia. I thank Marcelo Ochoa and Ivonne Vera for assistance and Klaus Schmidt-Hebbel and Andrea Tokman for suggestions and comments. * * * Emerging economies have recorded major progress in the conduct and results of monetary policy during the last two decades. This achievement is due to implementation of more robust and transparent monetary regimes, complemented by adoption of flexible exchange rates, sustainable fiscal policies, and stronger financial systems. Among emerging economies, Chile s experience is of particular interest. It shows that monetary stability can be attained as a result of coherent policies, overcoming decades of macroeconomic instability and weak credibility. This presentation documents the improvement of monetary policy conduct and results in emerging economies in general and Chile in particular. Section 1 summarizes the overall trend and specific components of macroeconomic adjustment observed in emerging economies. Chile s transition toward its current monetary policy framework, based on full-fledged inflation targeting, is described next. Section 3 analyzes and documents the results of improved monetary policy in emerging economies and in Chile during the last two decades. Brief conclusions close the presentation. 1. Macroeconomic adjustment in emerging economies Macroeconomic management in emerging markets has improved substantially in the last decade. In particular, the very favorable world economic conditions that have resulted in important terms of trade gains have been associated this time to fiscal prudence, complementing monetary and exchange-rate policies aimed at achieving and maintaining price stability. Four areas of macroeconomic adjustment: Fiscal, monetary and exchange rate policies, and the financial system The main changes that have taken place are in four key areas: (i) adoption of sustainable and responsible fiscal policies, reflected in declining fiscal deficits in most emerging economies (figure 1); (ii) adoption of floating regimes or hard pegs, moving away from intermediate exchange-rate (ER) regimes; (iii) shift of monetary policy (MP) anchors from ERs or monetary aggregates to an inflationtargeting (IT) anchor, particularly in Latin America; and (iv) these changes have been accompanied by the strengthening of regulation and supervision of financial systems, supporting strong financial development. Shift toward more flexible ER regimes The world shift toward more flexible ER regimes has been pronounced. The evidence shows a significant shift away from intermediate regimes. In 1990, nearly 70% of all countries were pursuing some variant of intermediate ER regimes, a share that dropped to 41% by the end of the 1990s, and further to 30% in 2004 (figure 2) 1. Exits from intermediate regimes were more frequently towards floats rather than to hard pegs. The share of floaters increased from 15% in 1990 to 45% in 2004 while, on the other extreme, the share of hard pegs rose from 15% to 26% during the same time span. The latter increase in hard pegs reflects, to some extent, the establishment of the European Monetary Union in The share of countries with crawling pegs a very popular regime among higher-inflation economies dropped from 14% in 1 A new IMF database of de facto ER regimes adopted by IMF member countries allows to classify countries into three broad ER regimes: hard pegs (formal dollarization, currency union, and currency boards), intermediate regimes (conventional fixed pegs, crawling pegs, crawling bands, and tightly managed floats), and floating ER regimes (managed float with no predetermined ER path and independently floating rates). BIS Review 68/2007 1

2 1990 to 6% in In contrast, countries with a crawling band or a tightly managed float rose from 10% at the beginning of the 1990s to 31% by the year Crawling bands offer at least in the short-term more flexibility in coping with volatile capital flows and avoiding extreme ER misalignments, than rigid ER regimes. Tightly managed floats, on the other hand, keep the anchoring role of the exchange rate without committing to any explicit target parity. The transition of ER regimes has come with a shift of MP regimes based on an ER or monetarygrowth anchor to an IT framework, particularly in emerging economies. The number of countries under IT rose from 8 in 1999 to 21 in 2004 (tables 1-2), and many more are considering to adopt IT in the near future. This transition in MP regime has been more pronounced in Latin America. While in 1994 twelve countries in the region had in place an ER anchor, and four others had a monetary growth anchor, by 2004 only three countries remained with an ER anchor. The transition of policy frameworks during led to a significant rise in the number of Latin American countries with a floating regime (from three to twelve countries) and an inflation targeting framework (from one to five countries). 2. Chile s transition to its current monetary policy framework The macroeconomic institutional and policy framework of Chile has been transformed radically in the last 25 years, from one that made stabilization an exceptional result to one that has facilitated achieving price stability. Chile s current macroeconomic framework is based on four pillars: (i) an autonomous Central Bank with the explicit mandate of safeguarding stability of prices and payments; (ii) a low public-debt to GDP ratio and a fiscal policy rule anchored to a structural fiscal surplus; (iii) a robust financial system, with a dynamic, competitive, and well capitalized banking industry, appropriately regulated and supervised; and (iv) a full-fledged inflation targeting monetary framework, complemented by a floating ER regime. Substantial progress was made in CBC autonomy since the 1980s, when autonomy was very weak, even at lower levels than in the average emerging economy. The granting of legal independence in 1989 through constitutional law, led to a much improved position in the international ranking of central bank autonomy. Particularly economic independence of central banks the freedom of taking policy decisions independently of political interference places Chile well above the average level of independence of both emerging and developed economies in Chile has shown a responsible fiscal policy, which has contributed significantly to successful monetary policy. During the 1990s, the fiscal balance averaged a surplus of 1.5% of GDP. The above-mentioned structural fiscal surplus rule stabilizes government spending over time, by linking it explicitly to permanent government revenue. Therefore fiscal dominance of monetary policy is ruled out in Chile, as a result of central bank autonomy and Chile s sound fiscal policy. Public debt has shown a substantial decline since the 1990s, as a result of prudent fiscal policy. The share of consolidated gross public debt has been reduced from 76% of GDP in 1990 to 20% of GDP in 2006, whereas the consolidated net public debt position turned from 34% of GDP in 1990 to -6% in 2006 (figure 3). The successful performance of the fiscal position has been enhanced by the fiscal balance rule applied since 2001 (figure 4). Chile s good growth performance, complemented by a market-based incentive structure, appropriate regulation and sound supervision of the financial system, has resulted in a safe and sound financial system and deep capital markets. As a result of the major banking crisis that came with the deep recession, the 1986 Banking Law enhanced regulation and supervision of the financial system. Since then, the financial system has developed around a well-managed and capitalized banking sector that is both healthy and competitive. This feature also rules out financial dominance of monetary policy in Chile. The CBC shares normative attributions with a specialized public institution, focusing on the formulation of financial regulations applicable to monetary markets. Chile s financial system strength has been acclaimed by international credit rating agencies. Moody s Financial Strength Ranking places Chile s financial strength close to the top of industrial countries (figure 5). 2 BIS Review 68/2007

3 Monetary policy framework: Central Bank charter and its objectives Although the road to CBC autonomy began in the mid-1970s, the 1989 Constitutional Law of the CBC specified the Bank s objectives and granted CBC the necessary instruments to comply with its legal mandate. Since 1989, the CBC is an autonomous, technical institution, governed by the Constitution, with full legal capacity, control of its equity, and of indefinite duration. The constitutional law establishes two objectives for the CBC. The first objective is to preserve the stability of Chile s currency. This means avoiding loss of purchasing power due to inflation. The latter objective is achieved through ensuring that inflation remains low and stable. The second objective of the CBC is to ensure the normal functioning of domestic and external payments, by safeguarding the financial sector s primary functions of credit and savings intermediation, provision of payment services, and proper risk allocation by financial markets. CBC s Constitutional Law prohibits CBC credit to the government. In order to contribute to policy coordination and information sharing, and minimizing potential conflict between fiscal and monetary authorities as a consequence of CBC autonomy, the Constitutional Law mandates participation of the Finance Minister at monetary policy meetings, without voting rights but with the temporary right of suspending a Board decision. Furthermore, the Law states that CBC policy decisions must take into account the government s general economic policy orientation. Overview of the evolution of MP framework The Chilean experience with IT can be split into two periods. The first one from 1991 to 1999 falls short in many aspects of a full-fledged inflation targeting framework. This first phase featured more than one anchor (an ER band, in addition to the inflation target) and low levels of MP transparency and communication. The second phase from 2000 to the present features a single inflation target and an active communication strategy for MP. In the context of reporting the annual monetary program to the Congress, the CBC announcement of an annual inflation target arose as a natural response to the legal mandate for price-level stability. In 1991, the first official target at a 15%-20% annual target range was publicly announced in September 1990 for the Dec Dec rate of annual CPI inflation. From 1990 to 1996, targets were set annually as target ranges in September for the subsequent calendar year, and from 1997 to 1999 as target points (figure 6). Between 1991 and 2001, annual targets were lowered by 1.5 percentage points per year on average. Inflation performance improved considerably during this period, achieving a reduction from 20%-30% annually to low single-digit rates. However, independence and effectiveness of the MP were hindered by conflicts between the exchange-rate-band, annual inflation targets, and capital controls. Transition to a full-fledged IT framework was implemented when inflation was converging to 3%, monetary policy was strengthened by attainment of inflation targets, the ER band was replaced by a floating ER regime, and capital controls were fully abolished. From 2000 to 2006, the target was defined for annual CPI inflation at a range of 2% to 4%, and the monetary policy horizon was defined as 12 to 24 months. Since 2007, the MP objective is to keep annual CPI inflation rate most of the time at around 3%, within a symmetric tolerance range of one percentage point, focused on a policy horizon of around two years. This target redefinition strengthens the 3% level as the nominal anchor of the economy, while recognizing that inflation can temporarily deviate from the 3+/-1% range to accommodate transitory shocks. In parallel, the horizon for monetary policy was extended to around two years. The latter changes were largely an explicit acknowledgment of how monetary policy had been conducted during preceding years. Transparency and communication In the last decade, central banks around the world have significantly improved their communication with the public and the markets. This provides institutional legitimacy and substantive accountability. More transparency and better communication also improve MP effectiveness, contributing to a better understanding of MP by the private sector. MP affects spending decisions, output, and prices more through its effects on market expectations on the future course of monetary policy, rather than through the direct effects of a change in the short-term MPR. BIS Review 68/2007 3

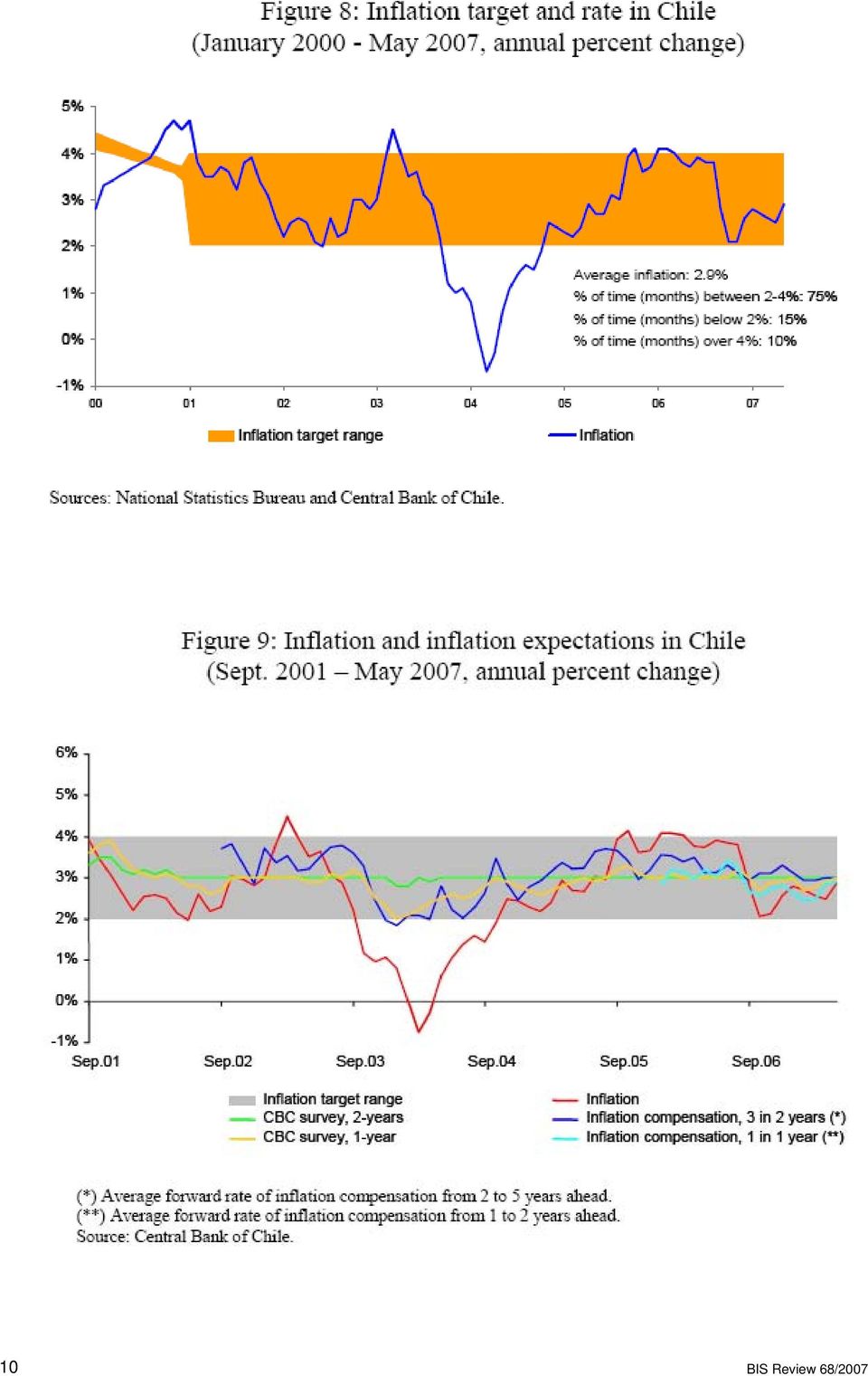

4 Since 2000 the CBC has made a large effort to deliver more and better information to the markets and to explain how its IT regime operates. A series of communication devices were developed, including disclosure of relevant data with a minimum time lag and making information available on the CBC website, a significant number of technical publications, including the Monetary Policy Report (with a four-monthly frequency, since May 2000); the Financial Stability Report (semi-annual, since 2004); the Monetary Policy Framework document (updated in January 2007, previous in May 2000), and Projection Models book (since 2003). The CBC publishes monthly MP meeting dates six months in advance (since 2000), the summary of MP minutes with the Board members voting decisions (since 2000), and background information on MP minutes (since July 2005). The time lag for the release of the minutes was lowered first from 90 to 45 days, and then to five days before the next monthly MP meeting. 3. Monetary policy results in emerging economies and in Chile Convergence of inflation to developed-country levels There are several empirical studies exploring how emerging economies in general, and Chile in particular, have benefited from implementation of an IT regime. The evidence shows that IT has been very helpful in bringing inflation down to low single-digit levels in emerging economies. It has been shown that the adoption of IT has played a leading role in emerging economies successful convergence to inflation levels observed in developed economies (Mishkin and Schmidt-Hebbel, 2007). Small deviations of inflation from target in Chile It has been shown also that IT countries are more successful in attaining their inflation targets than non-it countries (Mishkin and Schmidt-Hebbel, 2007). The introduction of IT has also helped Chile to attain levels of inflation closer to target levels. Albagli and Schmidt-Hebbel (2004) provide an international comparison of inflation performance and deviations from targets for 21 IT countries. They consider the average relative deviation of inflation from targets since the beginning of IT in each country. The results show that Chile is the second most accurate IT country in hitting its inflation target (figure 7). Since adoption of full-fledged IT by Chile in 2000, average annual inflation has been 2.9%, remaining around 75% of the time within the target range. Only 10% of the time did inflation rate rise above the upper target bound, and 15% of the time inflation fell below the lower bound (figure 8). Inflation targeting and credibility Adoption of IT has also contributed to the buildup of credibility of monetary policy in IT countries. Several authors show that the IT regime has helped in anchoring inflation expectations at levels close to inflation targets and inflation expectations are more stable than in the U.S. (Ramos et al., 2007; Gürkaynak et al., 2007). In Chile, the distance of inflation expectations from inflation targets was closed as targets converged toward the stationary 3% level and the Central Bank showed strong commitment to attaining targets (Céspedes and Soto, 2005). During the past five years, inflation expectations have remained close to the mid-point of the inflation target range, reflecting high credibility of the IT regime (figure 9). Inflation targets and stability Emerging economies have experienced reductions in the volatility of both inflation and output (figure 10). However, volatility reductions have been more pronounced in IT countries than in non-it countries. Volatilities of growth and inflation have fallen very significantly in Chile, even in comparison to other IT countries. Two factors explain most of the volatility reduction in IT countries: smaller shocks hitting the economy and improvements in monetary policy efficiency (Mishkin and Schmidt-Hebbel, 2007). Figure 11 depicts the estimated average efficiency frontier of MP for emerging economies before their adoption of IT (orange schedule) and the observed pair of output and inflation volatilities (red point). 4 BIS Review 68/2007

, and Projection Models book (since 2003).")

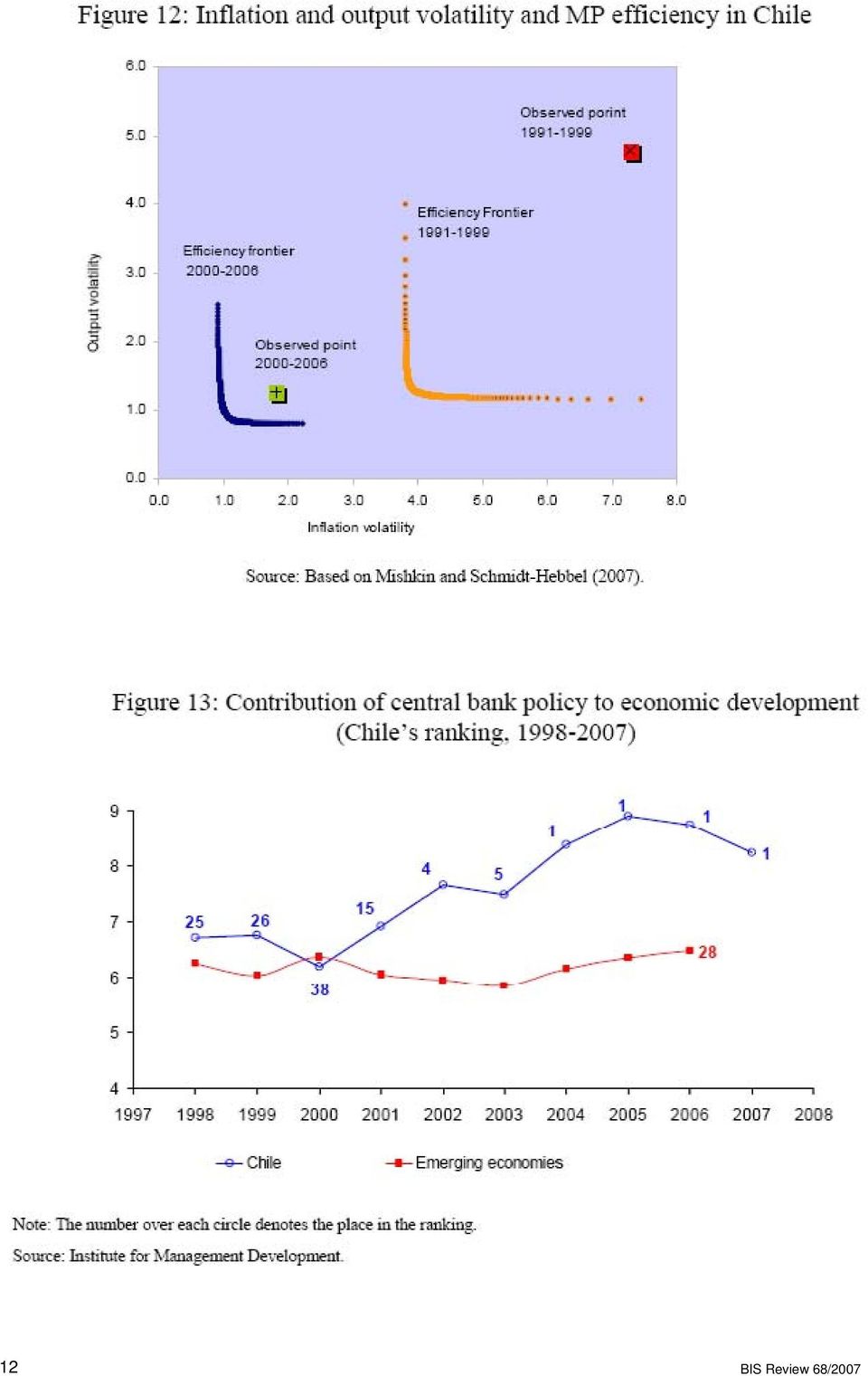

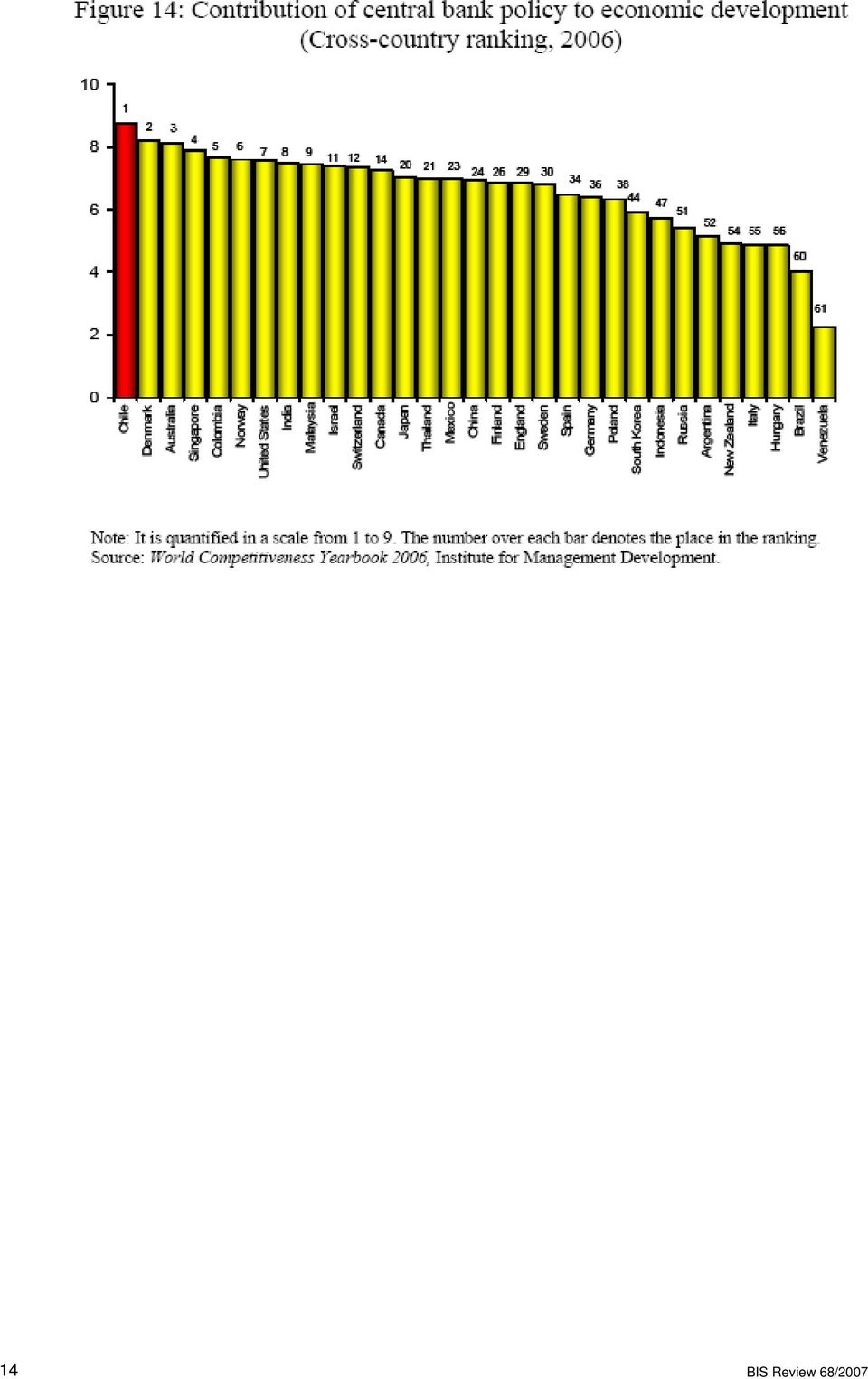

5 The figure also depicts the estimated average efficiency frontier of MP for emerging economies after IT adoption, for the period of stationary inflation targets (blue line) and the observed pair of output and inflation volatilities (green dot). On one hand, the shift of the efficiency frontier toward the origin reflects the smaller shocks faced by emerging economies since they have had stationary IT in place. On the other hand, the observed combination of output and inflation volatilities has moved closer to the efficiency frontier, revealing the corresponding improvement in monetary policy efficiency. In this case, the smaller shocks explain 58% of the current performance, while the improvements in monetary policy explain 42% of the decline in volatilities. Chile also records massive improvements in monetary policy management. Not only does Chile face smaller shocks, as reflected by the inward shift of the MP efficiency frontier, but also MP efficiency has improved significantly, as reflected by the closer position of observed volatilities to the efficiency frontier (see figure 12). Contribution of central bank policy to macroeconomic stability Emerging economies have improved MP practices. However, the contribution of monetary policy to macroeconomic performance still is low. The annual Report on Competitiveness prepared by the Institute for Management Development (IMD) shows that the positions of emerging economies in the country ranking of the contribution of central bank policy to development has not changed significantly since However, Chile has recorded major improvements during the past decade. In 1998, the CBC was ranked 25 among 60 countries, while reaching the first place in the world ranking in 2004, holding this place in the subsequent years (figures 13-14). 4. Conclusions Macroeconomic conditions have improved significantly in emerging economies since the early 1990s. Emerging economies show major progress in fiscal responsibility and sustainability; adoption of a framework of central bank autonomy, monetary regimes based on IT, and larger exchange-rate flexibility; and achievement of financial system strength. Adoption of more flexible exchange rates and an IT regime has contributed to lower output and inflation volatility, and stronger credibility of central bank policies. Macroeconomic stability is often accomplished gradually. Chile adopted the IT regime in two distinct phases and implemented a solid macroeconomic framework based on central bank autonomy with a clear focus on price stability. This was supported by a solvent, responsible, and predictable fiscal policy and a solid and well-regulated financial system. Chile s good record of attaining inflation levels close to the target has strengthened private sector confidence in the CBC and raised MP effectiveness and credibility. Low inflation and a credible monetary policy represent an essential macroeconomic achievement. By improving its policy framework, supported by strong transparency, accountability, and communication, the CBC has laid a major foundation to Chile s macroeconomic stability. Yet the conquest and predictability of inflation are not guaranteed. The CBC will remain vigilant, improving its policy framework as needed to continue delivering high levels of macroeconomic stability. References Albagli, E. and K. Schmidt-Hebbel (2004), By How Much and Why do Inflation Targeters Miss Their Targets?, Mimeo, Central Bank of Chile. Céspedes, L. and C. Soto (2005), Credibility and Inflation Targeting in an Emerging Market: Lessons from the Chilean Experience, International Finance 8 (3): Gürkaynak R., A. Levin, A. Marder and E. Swanson (2007), Inflation Targeting and the Anchoring of Inflation Expectations in the Western Hemisphere, in Monetary Policy Under Inflation Targeting, BIS Review 68/2007 5

6 Series on Central Banking, Analysis, and Economic Policies Vol. XI, edited by K. Schmidt-Hebbel and F. Mishkin, Central Bank of Chile. Institute for Management Development (2006), World Competitiveness Yearbook, several years. International Monetary Fund (2007), International Financial Statistics. Data on CD-ROM, April. Mishkin, Frederic S. and K. Schmidt-Hebbel (2007), Does Inflation Targeting Make a Difference? in Monetary Policy Under Inflation Targeting, Series on Central Banking, Analysis, and Economic Policies Vol. XI, edited by K. Schmidt-Hebbel and F. Mishkin, Central Bank of Chile. Moody s Investors Service (2006), Monthly Ratings List. Bank Credit Research. Ramos-Francia, M., D. Chiquiar, and A. Noriega (2007), A Time Series Approach to Test a Change in Inflation Persistence: The Mexican Experience, Working Paper N , Banco de México. World Bank (2007), World Development Indicators April. 6 BIS Review 68/2007

7 BIS Review 68/2007 7

8 8 BIS Review 68/2007

9 BIS Review 68/2007 9

10 10 BIS Review 68/2007

11 BIS Review 68/

12 12 BIS Review 68/2007

13 BIS Review 68/

14 14 BIS Review 68/2007

Inflation Target Of The Lunda Krona

Inflation Targeting The Swedish Experience Lars Heikensten We in Sweden owe a great debt of thanks to the Bank of Canada for all the help we have received in recent years. We have greatly benefited from

Inflation Targeting The Swedish Experience Lars Heikensten We in Sweden owe a great debt of thanks to the Bank of Canada for all the help we have received in recent years. We have greatly benefited from

INFLATION TARGETING. Frederic S. Mishkin

INFLATION TARGETING by Frederic S. Mishkin Graduate School of Business, Columbia University and National Bureau of Economic Research E-mail: fsm3@columbia.edu July 2001 Prepared for Brian Vane and Howard

INFLATION TARGETING by Frederic S. Mishkin Graduate School of Business, Columbia University and National Bureau of Economic Research E-mail: fsm3@columbia.edu July 2001 Prepared for Brian Vane and Howard

Adjusting to a Changing Economic World. Good afternoon, ladies and gentlemen. It s a pleasure to be with you here in Montréal today.

Remarks by David Dodge Governor of the Bank of Canada to the Board of Trade of Metropolitan Montreal Montréal, Quebec 11 February 2004 Adjusting to a Changing Economic World Good afternoon, ladies and

Remarks by David Dodge Governor of the Bank of Canada to the Board of Trade of Metropolitan Montreal Montréal, Quebec 11 February 2004 Adjusting to a Changing Economic World Good afternoon, ladies and

Monetary policy rules and their application in Russia. Economics Education and Research Consortium Working Paper Series ISSN 1561-2422.

Economics Education and Research Consortium Working Paper Series ISSN 1561-2422 No 04/09 Monetary policy rules and their application in Russia Anna Vdovichenko Victoria Voronina This project (02-230) was

Economics Education and Research Consortium Working Paper Series ISSN 1561-2422 No 04/09 Monetary policy rules and their application in Russia Anna Vdovichenko Victoria Voronina This project (02-230) was

The EMU and the debt crisis

The EMU and the debt crisis MONETARY POLICY REPORT FEBRUARY 212 43 The debt crisis in Europe is not only of concern to the individual debt-ridden countries; it has also developed into a crisis for the

The EMU and the debt crisis MONETARY POLICY REPORT FEBRUARY 212 43 The debt crisis in Europe is not only of concern to the individual debt-ridden countries; it has also developed into a crisis for the

The International Crisis and Latin America: Growth Effects and Development Strategies. Vittorio Corbo Klaus Schmidt-Hebbel

::: The International Crisis and Latin America: Growth Effects and Development Strategies Vittorio Corbo Klaus Schmidt-Hebbel World Bank Seminar on Managing Openness: Outward-oriented Growth Strategies

::: The International Crisis and Latin America: Growth Effects and Development Strategies Vittorio Corbo Klaus Schmidt-Hebbel World Bank Seminar on Managing Openness: Outward-oriented Growth Strategies

Naturally, these difficult external conditions have affected the Mexican economy. I would stress in particular three developments in this regard:

REMARKS BY MR. JAVIER GUZMÁN CALAFELL, DEPUTY GOVERNOR AT THE BANCO DE MÉXICO, ON THE MEXICAN ECONOMY IN AN ADVERSE EXTERNAL ENVIRONMENT: CHALLENGES AND POLICY RESPONSE, SANTANDER MEXICO DAY 2016, Mexico

REMARKS BY MR. JAVIER GUZMÁN CALAFELL, DEPUTY GOVERNOR AT THE BANCO DE MÉXICO, ON THE MEXICAN ECONOMY IN AN ADVERSE EXTERNAL ENVIRONMENT: CHALLENGES AND POLICY RESPONSE, SANTANDER MEXICO DAY 2016, Mexico

Mario Draghi: Europe and the euro a family affair

Mario Draghi: Europe and the euro a family affair Keynote speech by Mr Mario Draghi, President of the European Central Bank, at the conference Europe and the euro a family affair, organised by the Bundesverband

Mario Draghi: Europe and the euro a family affair Keynote speech by Mr Mario Draghi, President of the European Central Bank, at the conference Europe and the euro a family affair, organised by the Bundesverband

The following text represents the notes on which Mr. Parry based his remarks. 1998: Issues in Monetary Policymaking

Phoenix Society of Financial Analysts and Arizona State University Business School ASU, Memorial Union - Ventana Room April 24, 1998, 12:30 PM Robert T. Parry, President, FRBSF The following text represents

Phoenix Society of Financial Analysts and Arizona State University Business School ASU, Memorial Union - Ventana Room April 24, 1998, 12:30 PM Robert T. Parry, President, FRBSF The following text represents

Statement by. Janet L. Yellen. Chair. Board of Governors of the Federal Reserve System. before the. Committee on Financial Services

For release at 8:30 a.m. EST February 10, 2016 Statement by Janet L. Yellen Chair Board of Governors of the Federal Reserve System before the Committee on Financial Services U.S. House of Representatives

For release at 8:30 a.m. EST February 10, 2016 Statement by Janet L. Yellen Chair Board of Governors of the Federal Reserve System before the Committee on Financial Services U.S. House of Representatives

New Monetary Policy Challenges

New Monetary Policy Challenges 63 Journal of Central Banking Theory and Practice, 2013, 1, pp. 63-67 Received: 5 December 2012; accepted: 4 January 2013 UDC: 336.74 Alexey V. Ulyukaev * New Monetary Policy

New Monetary Policy Challenges 63 Journal of Central Banking Theory and Practice, 2013, 1, pp. 63-67 Received: 5 December 2012; accepted: 4 January 2013 UDC: 336.74 Alexey V. Ulyukaev * New Monetary Policy

Response on the financing of Employment Insurance and recent measures. Ottawa, Canada October 9, 2014 www.pbo-dpb.gc.ca

Response on the financing of Employment Insurance and recent measures Ottawa, Canada October 9, 20 www.pbo-dpb.gc.ca The mandate of the Parliamentary Budget Officer (PBO) is to provide independent analysis

Response on the financing of Employment Insurance and recent measures Ottawa, Canada October 9, 20 www.pbo-dpb.gc.ca The mandate of the Parliamentary Budget Officer (PBO) is to provide independent analysis

Recent Developments and Outlook for the Mexican Economy Credit Suisse, 2016 Macro Conference April 19, 2016

Credit Suisse, Macro Conference April 19, Outline 1 Inflation and Monetary Policy 2 Recent Developments and Outlook for the Mexican Economy 3 Final Remarks 2 In line with its constitutional mandate, the

Credit Suisse, Macro Conference April 19, Outline 1 Inflation and Monetary Policy 2 Recent Developments and Outlook for the Mexican Economy 3 Final Remarks 2 In line with its constitutional mandate, the

Monetary Policy in Emerging Markets: Indonesia s s Case

Monetary Policy in Emerging Markets: Indonesia s s Case Hartadi A. Sarwono, Deputy Governor Paper presented at The OECD-CCBS CCBS Seminar on Monetary Policy in Emerging Markets,, Paris, 28 February 2007.

Monetary Policy in Emerging Markets: Indonesia s s Case Hartadi A. Sarwono, Deputy Governor Paper presented at The OECD-CCBS CCBS Seminar on Monetary Policy in Emerging Markets,, Paris, 28 February 2007.

MONETARY POLICY IN DOLLARIZED ECONOMIES Karl Driessen*

MONETARY POLICY IN DOLLARIZED ECONOMIES Karl Driessen* Governor and distinguished guests, I am honored to address you on the occasion of the fifth international conference of the Bank of Albania. The topic

MONETARY POLICY IN DOLLARIZED ECONOMIES Karl Driessen* Governor and distinguished guests, I am honored to address you on the occasion of the fifth international conference of the Bank of Albania. The topic

Ignazio Visco: Rebalancing trade and capital flows

Ignazio Visco: Rebalancing trade and capital flows Remarks by Mr Ignazio Visco, Deputy Director General of the Bank of Italy, at the Global Economic Symposium 2010, Istanbul, 29 September 2010. * * * 1.

Ignazio Visco: Rebalancing trade and capital flows Remarks by Mr Ignazio Visco, Deputy Director General of the Bank of Italy, at the Global Economic Symposium 2010, Istanbul, 29 September 2010. * * * 1.

Why a Floating Exchange Rate Regime Makes Sense for Canada

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Chambre de commerce du Montréal métropolitain Montreal, Quebec 4 December 2000 Why a Floating Exchange Rate Regime Makes Sense for Canada

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Chambre de commerce du Montréal métropolitain Montreal, Quebec 4 December 2000 Why a Floating Exchange Rate Regime Makes Sense for Canada

Decomposition of External Capital Inflows and Outflows in the Small Open Transition Economy (The Case Analysis of the Slovak Republic)

") PANOECONOMICUS, 2008, 2, str. 219-231 UDC 330.342(437.6) ORIGINAL SCIENTIFIC PAPER Decomposition of External Capital Inflows and Outflows in the Small Open Transition Economy (The Case Analysis of the

PANOECONOMICUS, 2008, 2, str. 219-231 UDC 330.342(437.6) ORIGINAL SCIENTIFIC PAPER Decomposition of External Capital Inflows and Outflows in the Small Open Transition Economy (The Case Analysis of the

Globalization, IMF and Bulgaria

Globalization, IMF and Bulgaria Presentation by Piritta Sorsa * *, Resident Representative of the IMF in Bulgaria, At the Conference on Globalization and Sustainable Development, Varna Free University,

Globalization, IMF and Bulgaria Presentation by Piritta Sorsa * *, Resident Representative of the IMF in Bulgaria, At the Conference on Globalization and Sustainable Development, Varna Free University,

X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/

1/ X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/ 10.1 Overview of World Economy Latest indicators are increasingly suggesting that the significant contraction in economic activity has come to an end, notably

1/ X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/ 10.1 Overview of World Economy Latest indicators are increasingly suggesting that the significant contraction in economic activity has come to an end, notably

ANNEX 1 - MACROECONOMIC IMPLICATIONS FOR ITALY OF ACHIEVING COMPLIANCE WITH THE DEBT RULE UNDER TWO DIFFERENT SCENARIOS

ANNEX 1 - MACROECONOMIC IMPLICATIONS FOR ITALY OF ACHIEVING COMPLIANCE WITH THE DEBT RULE UNDER TWO DIFFERENT SCENARIOS The aim of this note is first to illustrate the impact of a fiscal adjustment aimed

ANNEX 1 - MACROECONOMIC IMPLICATIONS FOR ITALY OF ACHIEVING COMPLIANCE WITH THE DEBT RULE UNDER TWO DIFFERENT SCENARIOS The aim of this note is first to illustrate the impact of a fiscal adjustment aimed

Lecture 2. Output, interest rates and exchange rates: the Mundell Fleming model.

Lecture 2. Output, interest rates and exchange rates: the Mundell Fleming model. Carlos Llano (P) & Nuria Gallego (TA) References: these slides have been developed based on the ones provided by Beatriz

Lecture 2. Output, interest rates and exchange rates: the Mundell Fleming model. Carlos Llano (P) & Nuria Gallego (TA) References: these slides have been developed based on the ones provided by Beatriz

DEVELOPMENTS IN 1990 s

MACROECONOMIC MANAGEMENT WITH OPEN CAPITAL ACCOUNTS: THE TURKISH CASE FAIK OZTRAK Director TUSIAD-Koc University, Economic Research Forum HIGH LEVEL SEMINAR ON CRISIS PREVENTION, SINGAPORE, JULY 1, 26

MACROECONOMIC MANAGEMENT WITH OPEN CAPITAL ACCOUNTS: THE TURKISH CASE FAIK OZTRAK Director TUSIAD-Koc University, Economic Research Forum HIGH LEVEL SEMINAR ON CRISIS PREVENTION, SINGAPORE, JULY 1, 26

Lecture 4: The Aftermath of the Crisis

Lecture 4: The Aftermath of the Crisis 2 The Fed s Efforts to Restore Financial Stability A financial panic in fall 2008 threatened the stability of the global financial system. In its lender-of-last-resort

Lecture 4: The Aftermath of the Crisis 2 The Fed s Efforts to Restore Financial Stability A financial panic in fall 2008 threatened the stability of the global financial system. In its lender-of-last-resort

INFLATION TARGETING IN DEVELOPING COUNTRIES. Ferya KADIOĞLU Nilüfer ÖZDEMİR Gökhan YILMAZ

INFLATION TARGETING IN DEVELOPING COUNTRIES Ferya KADIOĞLU Nilüfer ÖZDEMİR Gökhan YILMAZ THE CENTRAL BANK OF THE REPUBLIC OF TURKEY Research Department Discussion Paper September, 2000 The authors are

INFLATION TARGETING IN DEVELOPING COUNTRIES Ferya KADIOĞLU Nilüfer ÖZDEMİR Gökhan YILMAZ THE CENTRAL BANK OF THE REPUBLIC OF TURKEY Research Department Discussion Paper September, 2000 The authors are

International Monetary and Financial Committee

International Monetary and Financial Committee Twenty-Seventh Meeting April 20, 2013 Statement by Koen Geens, Minister of Finance, Ministere des Finances, Belgium On behalf of Armenia, Belgium, Bosnia

International Monetary and Financial Committee Twenty-Seventh Meeting April 20, 2013 Statement by Koen Geens, Minister of Finance, Ministere des Finances, Belgium On behalf of Armenia, Belgium, Bosnia

Preparation of the Informal Ministerial Meeting of Ministers responsible for Cohesion Policy, Milan 10 October 2014

Preparation of the Informal Ministerial Meeting of Ministers responsible for Cohesion Policy, Milan 10 October 2014 Cohesion Policy and economic governance: complementing each other Background paper September

Preparation of the Informal Ministerial Meeting of Ministers responsible for Cohesion Policy, Milan 10 October 2014 Cohesion Policy and economic governance: complementing each other Background paper September

MACROECONOMIC ANALYSIS OF VARIOUS PROPOSALS TO PROVIDE $500 BILLION IN TAX RELIEF

MACROECONOMIC ANALYSIS OF VARIOUS PROPOSALS TO PROVIDE $500 BILLION IN TAX RELIEF Prepared by the Staff of the JOINT COMMITTEE ON TAXATION March 1, 2005 JCX-4-05 CONTENTS INTRODUCTION... 1 EXECUTIVE SUMMARY...

MACROECONOMIC ANALYSIS OF VARIOUS PROPOSALS TO PROVIDE $500 BILLION IN TAX RELIEF Prepared by the Staff of the JOINT COMMITTEE ON TAXATION March 1, 2005 JCX-4-05 CONTENTS INTRODUCTION... 1 EXECUTIVE SUMMARY...

Reducing public debt: Turkey

Reducing public debt: Turkey Abstract Turkey halved the ratio of public debt to GDP from almost 80 percent in 2001 to less than 40 percent before the global crisis of 2009. Several factors helped. First,

Reducing public debt: Turkey Abstract Turkey halved the ratio of public debt to GDP from almost 80 percent in 2001 to less than 40 percent before the global crisis of 2009. Several factors helped. First,

Research and Statistics Department, Bank of Japan. E-mail: yoshiko.satou@boj.or.jp

&200(176216(66,21, $66(66,1*38%/,&/,$%,/,7,(6

&200(176216(66,21, $66(66,1*38%/,&/,$%,/,7,(6

CHAPTER 11. AN OVEVIEW OF THE BANK OF ENGLAND QUARTERLY MODEL OF THE (BEQM)

") 1 CHAPTER 11. AN OVEVIEW OF THE BANK OF ENGLAND QUARTERLY MODEL OF THE (BEQM) This model is the main tool in the suite of models employed by the staff and the Monetary Policy Committee (MPC) in the construction

1 CHAPTER 11. AN OVEVIEW OF THE BANK OF ENGLAND QUARTERLY MODEL OF THE (BEQM) This model is the main tool in the suite of models employed by the staff and the Monetary Policy Committee (MPC) in the construction

RIA Novosti Press Meeting. Economic Outlook and Policy Challenges for Russia in 2012. Odd Per Brekk Senior Resident Representative.

RIA Novosti Press Meeting Economic Outlook and Policy Challenges for Russia in 2012 Odd Per Brekk Senior Resident Representative January 26, 2012 This morning I will start with introductory remarks on

RIA Novosti Press Meeting Economic Outlook and Policy Challenges for Russia in 2012 Odd Per Brekk Senior Resident Representative January 26, 2012 This morning I will start with introductory remarks on

Chapter 17. Fixed Exchange Rates and Foreign Exchange Intervention. Copyright 2003 Pearson Education, Inc.

Chapter 17 Fixed Exchange Rates and Foreign Exchange Intervention Slide 17-1 Chapter 17 Learning Goals How a central bank must manage monetary policy so as to fix its currency's value in the foreign exchange

Chapter 17 Fixed Exchange Rates and Foreign Exchange Intervention Slide 17-1 Chapter 17 Learning Goals How a central bank must manage monetary policy so as to fix its currency's value in the foreign exchange

Mr Duisenberg discusses the role of capital markets and financing in the euro area Speech by Willem F Duisenberg, President of the European Central

Mr Duisenberg discusses the role of capital markets and financing in the euro area Speech by Willem F Duisenberg, President of the European Central Bank, at the Waarborgfonds Sociale Woningbouw in Utrecht,

Mr Duisenberg discusses the role of capital markets and financing in the euro area Speech by Willem F Duisenberg, President of the European Central Bank, at the Waarborgfonds Sociale Woningbouw in Utrecht,

CHAPTER 3 BALANCE OF PAYMENTS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 3 BALANCE OF PAYMENTS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Define the balance of payments. Answer: The balance of payments (BOP) can be defined

CHAPTER 3 BALANCE OF PAYMENTS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Define the balance of payments. Answer: The balance of payments (BOP) can be defined

THE GREAT DEPRESSION OF FINLAND 1990-1993: causes and consequences. Jaakko Kiander Labour Institute for Economic Research

THE GREAT DEPRESSION OF FINLAND 1990-1993: causes and consequences Jaakko Kiander Labour Institute for Economic Research CONTENTS Causes background The crisis Consequences Role of economic policy Banking

THE GREAT DEPRESSION OF FINLAND 1990-1993: causes and consequences Jaakko Kiander Labour Institute for Economic Research CONTENTS Causes background The crisis Consequences Role of economic policy Banking

Jarle Bergo: Monetary policy and the outlook for the Norwegian economy

Jarle Bergo: Monetary policy and the outlook for the Norwegian economy Speech by Mr Jarle Bergo, Deputy Governor of Norges Bank, at the Capital markets seminar, hosted by Terra-Gruppen AS, Gardermoen,

Jarle Bergo: Monetary policy and the outlook for the Norwegian economy Speech by Mr Jarle Bergo, Deputy Governor of Norges Bank, at the Capital markets seminar, hosted by Terra-Gruppen AS, Gardermoen,

Estonia and the European Debt Crisis Juhan Parts

Estonia and the European Debt Crisis Juhan Parts Estonia has had a quick recovery from the recent recession and its economy is in better shape than before the crisis. It is now much leaner and significantly

Estonia and the European Debt Crisis Juhan Parts Estonia has had a quick recovery from the recent recession and its economy is in better shape than before the crisis. It is now much leaner and significantly

Turkish Experience With Implicit Inflation Targeting. A. Hakan Kara. September 2006. The Central Bank of the Republic of Turkey

Research and Monetary Policy Department Working Paper No:06/03 Turkish Experience With Implicit Inflation Targeting A. Hakan Kara September 2006 The Central Bank of the Republic of Turkey Turkish Experience

Research and Monetary Policy Department Working Paper No:06/03 Turkish Experience With Implicit Inflation Targeting A. Hakan Kara September 2006 The Central Bank of the Republic of Turkey Turkish Experience

Russia s move in exchange rate policy and other monetary policy options

Russia s move in exchange rate policy and other monetary policy options Riikka Nuutilainen, Bank of Finland Institute for Economies in Transition (BOFIT) 77 th East Jour Fixe of the Oesterreichische Nationalbank

Russia s move in exchange rate policy and other monetary policy options Riikka Nuutilainen, Bank of Finland Institute for Economies in Transition (BOFIT) 77 th East Jour Fixe of the Oesterreichische Nationalbank

INTERNATIONAL MONETARY FUND. Russian Federation Concluding Statement for the 2012 Article IV Consultation Mission. Moscow, June 13, 2012

INTERNATIONAL MONETARY FUND Russian Federation Concluding Statement for the 2012 Article IV Consultation Mission Moscow, June 13, 2012 The Russian economy has recovered from the 2008-09 crisis and is now

INTERNATIONAL MONETARY FUND Russian Federation Concluding Statement for the 2012 Article IV Consultation Mission Moscow, June 13, 2012 The Russian economy has recovered from the 2008-09 crisis and is now

THE US DOLLAR, THE EURO, THE JAPANESE YEN AND THE CHINESE YUAN IN THE FOREIGN EXCHANGE MARKET A COMPARATIVE ANALYSIS

THE US DOLLAR, THE EURO, THE JAPANESE YEN AND THE CHINESE YUAN IN THE FOREIGN EXCHANGE MARKET A COMPARATIVE ANALYSIS ORASTEAN Ramona Lucian Blaga University of Sibiu, Romania Abstract: This paper exposes

THE US DOLLAR, THE EURO, THE JAPANESE YEN AND THE CHINESE YUAN IN THE FOREIGN EXCHANGE MARKET A COMPARATIVE ANALYSIS ORASTEAN Ramona Lucian Blaga University of Sibiu, Romania Abstract: This paper exposes

"Dollarisation in Emerging Market Economies" Part 2: IMPLICATIONS

Part 2: IMPLICATIONS FISCAL IMPLICATIONS OF CURRENCY SUBSTITUTION DOLLARISATION AND FINANCIAL DEEPENING DOLLARISATION AND FINANCIAL FRAGILITY Solvency risk Liquidity risk Liquidity risk and solvency risk

Part 2: IMPLICATIONS FISCAL IMPLICATIONS OF CURRENCY SUBSTITUTION DOLLARISATION AND FINANCIAL DEEPENING DOLLARISATION AND FINANCIAL FRAGILITY Solvency risk Liquidity risk Liquidity risk and solvency risk

CHAPTER 19 CURRENCIES AND FOREIGN EXCHANGE

CHAPTER 19 CURRENCIES AND FOREIGN EXCHANGE MULTIPLE CHOICE 1. A currency becomes hard when a) it is backed by gold b) a government declares that it is an international currency c) it has been around for

CHAPTER 19 CURRENCIES AND FOREIGN EXCHANGE MULTIPLE CHOICE 1. A currency becomes hard when a) it is backed by gold b) a government declares that it is an international currency c) it has been around for

ECON 4311: The Economy of Latin America. Debt Relief. Part 1: Early Initiatives

ECON 4311: The Economy of Latin America Debt Relief Part 1: Early Initiatives The Debt Crisis of 1982 severely hit the Latin American economies for many years to come. Balance of payments deficits and

ECON 4311: The Economy of Latin America Debt Relief Part 1: Early Initiatives The Debt Crisis of 1982 severely hit the Latin American economies for many years to come. Balance of payments deficits and

Inflation targeting in developing countries: perspectives for Russia. Asiya F. Validova

Inflation targeting in developing countries: perspectives for Russia Asiya F. Validova Kazan (Volga region) Federal University, Kremlyovskaya Street, 18, Kazan, 420008, Republic of Tatarstan, Russian Federation

Inflation targeting in developing countries: perspectives for Russia Asiya F. Validova Kazan (Volga region) Federal University, Kremlyovskaya Street, 18, Kazan, 420008, Republic of Tatarstan, Russian Federation

Switzerland 2013 Article for Consultation Preliminary Conclusions Bern, March 18, 2013

Switzerland 2013 Article for Consultation Preliminary Conclusions Bern, March 18, 2013 With the exchange rate floor in place for over a year, the Swiss economy remains stable, though inflation remains

Switzerland 2013 Article for Consultation Preliminary Conclusions Bern, March 18, 2013 With the exchange rate floor in place for over a year, the Swiss economy remains stable, though inflation remains

Monetary Policy Outlook in a Negative Rates Environment Mr. Javier Guzmán Calafell, Deputy Governor, Banco de México J.P. Morgan Investor Seminar

Mr. Javier Guzmán Calafell, Deputy Governor, Banco de México J.P. Morgan Investor Seminar Washington, DC, 15 April 2016 Outline 1 External Conditions 2 Macroeconomic Policy in Mexico 3 Evolution and Outlook

Mr. Javier Guzmán Calafell, Deputy Governor, Banco de México J.P. Morgan Investor Seminar Washington, DC, 15 April 2016 Outline 1 External Conditions 2 Macroeconomic Policy in Mexico 3 Evolution and Outlook

The Balance of Payments, the Exchange Rate, and Trade

Balance of Payments The Balance of Payments, the Exchange Rate, and Trade Policy The balance of payments is a country s record of all transactions between its residents and the residents of all foreign

Balance of Payments The Balance of Payments, the Exchange Rate, and Trade Policy The balance of payments is a country s record of all transactions between its residents and the residents of all foreign

Meeting with Analysts

CNB s New Forecast (Inflation Report IV/) Meeting with Analysts Tibor Hlédik Prague, 7 November, Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

CNB s New Forecast (Inflation Report IV/) Meeting with Analysts Tibor Hlédik Prague, 7 November, Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

2008/09 Financial Management Strategy

2008/09 Financial Management Strategy Report on outcomes For more information visit www.manitoba.ca R e p o r t o n O u t c o m e s / 1 Report on Outcomes Budget 2008 set out the second Financial Management

2008/09 Financial Management Strategy Report on outcomes For more information visit www.manitoba.ca R e p o r t o n O u t c o m e s / 1 Report on Outcomes Budget 2008 set out the second Financial Management

Bank of Finland and Finland s economic internationalization. Turku 16.08.2011

Bank of Finland and Finland s economic internationalization Antti Kuusterä Juha Tarkka Turku 16.08.2011 Early history - towards independent exchange rate policy Monetary reform 1840 - silver standard stabilized

Bank of Finland and Finland s economic internationalization Antti Kuusterä Juha Tarkka Turku 16.08.2011 Early history - towards independent exchange rate policy Monetary reform 1840 - silver standard stabilized

The global economy Banco de Portugal Lisbon, 24 September 2013 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist

The global economy Banco de Portugal Lisbon, 24 September 213 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist Summary of presentation Global economy slowly exiting recession but

The global economy Banco de Portugal Lisbon, 24 September 213 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist Summary of presentation Global economy slowly exiting recession but

Section 2 Evaluation of current account balance fluctuations

Section 2 Evaluation of current account balance fluctuations Key points 1. The Japanese economy and IS balance trends From a macroeconomic perspective, the current account balance weighs the Japanese economy

Section 2 Evaluation of current account balance fluctuations Key points 1. The Japanese economy and IS balance trends From a macroeconomic perspective, the current account balance weighs the Japanese economy

The Mexican Economy: Facts and Opportunities

Manuel Sánchez Santander Global Fixed Income Summit London, England, September 20, 2012 Contents 1 Structural features 2 Recent developments and outlook 3 Inflation and monetary policy 4 Economic challenges

Manuel Sánchez Santander Global Fixed Income Summit London, England, September 20, 2012 Contents 1 Structural features 2 Recent developments and outlook 3 Inflation and monetary policy 4 Economic challenges

Lars Osberg. Department of Economics Dalhousie University 6214 University Avenue Halifax, Nova Scotia B3H 3J5 CANADA Email: Lars.Osberg@dal.

Not Good Enough to be Average? Comments on The Weak Jobs recovery: whatever happened to the great American jobs machine? by Freeman and Rodgers Lars Osberg Department of Economics Dalhousie University

Not Good Enough to be Average? Comments on The Weak Jobs recovery: whatever happened to the great American jobs machine? by Freeman and Rodgers Lars Osberg Department of Economics Dalhousie University

COMMISSION STAFF WORKING DOCUMENT EXECUTIVE SUMMARY OF THE IMPACT ASSESSMENT. Accompanying the document

EUROPEAN COMMISSION Brussels, XXX SWD(2014) 18 /2 COMMISSION STAFF WORKING DOCUMENT EXECUTIVE SUMMARY OF THE IMPACT ASSESSMENT Accompanying the document Proposal for a Decision of the European Parliament

EUROPEAN COMMISSION Brussels, XXX SWD(2014) 18 /2 COMMISSION STAFF WORKING DOCUMENT EXECUTIVE SUMMARY OF THE IMPACT ASSESSMENT Accompanying the document Proposal for a Decision of the European Parliament

The International Monetary Order and the Canadian Economy

Notes for Remarks by David Dodge Governor of the Bank of Canada to the Canada-U.K. Chamber of Commerce London, U.K. 28 June 2005 The International Monetary Order and the Canadian Economy As business people

Notes for Remarks by David Dodge Governor of the Bank of Canada to the Canada-U.K. Chamber of Commerce London, U.K. 28 June 2005 The International Monetary Order and the Canadian Economy As business people

COMPARISON OF CURRENCY CO-MOVEMENT BEFORE AND AFTER OCTOBER 2008

COMPARISON OF CURRENCY CO-MOVEMENT BEFORE AND AFTER OCTOBER 2008 M. E. Malliaris, Loyola University Chicago, 1 E. Pearson, Chicago, IL, mmallia@luc.edu, 312-915-7064 A.G. Malliaris, Loyola University Chicago,

COMPARISON OF CURRENCY CO-MOVEMENT BEFORE AND AFTER OCTOBER 2008 M. E. Malliaris, Loyola University Chicago, 1 E. Pearson, Chicago, IL, mmallia@luc.edu, 312-915-7064 A.G. Malliaris, Loyola University Chicago,

Research. What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields?

Research What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields? The global economy appears to be on the road to recovery and the risk of a double dip recession is receding.

Research What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields? The global economy appears to be on the road to recovery and the risk of a double dip recession is receding.

MGE#12 The Balance of Payments

MGE#12 The Balance of Payments The Current Account, the Capital Account and the Balance of Payments Introduction to the Foreign Exchange Market Savings, Investment and the Current Account 1 From last session

MGE#12 The Balance of Payments The Current Account, the Capital Account and the Balance of Payments Introduction to the Foreign Exchange Market Savings, Investment and the Current Account 1 From last session

Some Thoughts on the Design of Monetary Policy Strategy and Communications Andrew Levin Resident Scholar, IMF Research Department March 2014

Some Thoughts on the Design of Monetary Policy Strategy and Communications Andrew Levin Resident Scholar, IMF Research Department March 2014 The views expressed are solely my own responsibility and should

Some Thoughts on the Design of Monetary Policy Strategy and Communications Andrew Levin Resident Scholar, IMF Research Department March 2014 The views expressed are solely my own responsibility and should

COMMUNICATION FROM THE COMMISSION. replacing the Communication from the Commission on

EUROPEAN COMMISSION Brussels, 28.10.2014 COM(2014) 675 final COMMUNICATION FROM THE COMMISSION replacing the Communication from the Commission on Harmonized framework for draft budgetary plans and debt

EUROPEAN COMMISSION Brussels, 28.10.2014 COM(2014) 675 final COMMUNICATION FROM THE COMMISSION replacing the Communication from the Commission on Harmonized framework for draft budgetary plans and debt

Expert Group on Debt Redemption Fund and Eurobills Final Report submitted on 31 March 2014 Conclusions

Expert Group on Debt Redemption Fund and Eurobills Final Report submitted on 31 March 2014 Conclusions THE BROADER CONTEXT OF THE DISCUSSION ON JOINT ISSUANCE OF DEBT 1. Schemes of joint issuance of debt,

Expert Group on Debt Redemption Fund and Eurobills Final Report submitted on 31 March 2014 Conclusions THE BROADER CONTEXT OF THE DISCUSSION ON JOINT ISSUANCE OF DEBT 1. Schemes of joint issuance of debt,

Fixed Exchange Rates and Exchange Market Intervention. Chapter 18

Fixed Exchange Rates and Exchange Market Intervention Chapter 18 1. Central bank intervention in the foreign exchange market 2. Stabilization under xed exchange rates 3. Exchange rate crises 4. Sterilized

Fixed Exchange Rates and Exchange Market Intervention Chapter 18 1. Central bank intervention in the foreign exchange market 2. Stabilization under xed exchange rates 3. Exchange rate crises 4. Sterilized

COMPARED EXPERIENCES REGARDING PUBLIC DEBT MANAGEMENT

COMPARED EXPERIENCES REGARDING PUBLIC DEBT MANAGEMENT MIRELA-ANCA POSTOLE, RODICA GHERGHINA, IOANA DUCA, IRINA ZGREABAN ACADEMY OF ECONOMIC SCIENCES, TITU MAIORESCU UNIVERSITY BUCHAREST anca_postole@yahoo.com,

COMPARED EXPERIENCES REGARDING PUBLIC DEBT MANAGEMENT MIRELA-ANCA POSTOLE, RODICA GHERGHINA, IOANA DUCA, IRINA ZGREABAN ACADEMY OF ECONOMIC SCIENCES, TITU MAIORESCU UNIVERSITY BUCHAREST anca_postole@yahoo.com,

Provided in Cooperation with: National Bureau of Economic Research (NBER), Cambridge, Mass.

, Cambridge, Mass.") econstor www.econstor.eu Der Open-Access-Publikationsserver der ZBW Leibniz-Informationszentrum Wirtschaft The Open Access Publication Server of the ZBW Leibniz Information Centre for Economics Mishkin,

econstor www.econstor.eu Der Open-Access-Publikationsserver der ZBW Leibniz-Informationszentrum Wirtschaft The Open Access Publication Server of the ZBW Leibniz Information Centre for Economics Mishkin,

Monetary policy in Russia: Recent challenges and changes

Monetary policy in Russia: Recent challenges and changes Central Bank of the Russian Federation (Bank of Russia) Abstract Increasing trade and financial flows between the world s countries has been a double-edged

Monetary policy in Russia: Recent challenges and changes Central Bank of the Russian Federation (Bank of Russia) Abstract Increasing trade and financial flows between the world s countries has been a double-edged

Financial Market Outlook

ECONOMIC RESEARCH & CORPORATE DEVELOPMENT Financial Market Outlook February 25, 2011 Dr. Michael Heise Euro area sovereign debt road to ruin or salvation? EURO AREA SOVEREIGN DEBT ROAD TO RUIN OR SALVATION?

ECONOMIC RESEARCH & CORPORATE DEVELOPMENT Financial Market Outlook February 25, 2011 Dr. Michael Heise Euro area sovereign debt road to ruin or salvation? EURO AREA SOVEREIGN DEBT ROAD TO RUIN OR SALVATION?

Fixed vs Flexible Exchange Rate Regimes

Fixed vs Flexible Exchange Rate Regimes Review fixed exchange rates and costs vs benefits to devaluations. Exchange rate crises. Flexible exchange rate regimes: Exchange rate volatility. Fixed exchange

Fixed vs Flexible Exchange Rate Regimes Review fixed exchange rates and costs vs benefits to devaluations. Exchange rate crises. Flexible exchange rate regimes: Exchange rate volatility. Fixed exchange

THE RETURN OF CAPITAL EXPENDITURE OR CAPEX CYCLE IN MALAYSIA

PUBLIC BANK BERHAD ECONOMICS DIVISION MENARA PUBLIC BANK 146 JALAN AMPANG 50450 KUALA LUMPUR TEL : 03 2176 6000/666 FAX : 03 2163 9929 Public Bank Economic Review is published bi monthly by Economics Division,

PUBLIC BANK BERHAD ECONOMICS DIVISION MENARA PUBLIC BANK 146 JALAN AMPANG 50450 KUALA LUMPUR TEL : 03 2176 6000/666 FAX : 03 2163 9929 Public Bank Economic Review is published bi monthly by Economics Division,

PROJECTION OF THE FISCAL BALANCE AND PUBLIC DEBT (2012 2027) - SUMMARY

- SUMMARY") PROJECTION OF THE FISCAL BALANCE AND PUBLIC DEBT (2012 2027) - SUMMARY PUBLIC FINANCE REVIEW February 2013 SUMMARY Key messages The purpose of our analysis is to highlight the risks that fiscal policy

PROJECTION OF THE FISCAL BALANCE AND PUBLIC DEBT (2012 2027) - SUMMARY PUBLIC FINANCE REVIEW February 2013 SUMMARY Key messages The purpose of our analysis is to highlight the risks that fiscal policy

THE CURRENT ACCOUNT OF ROMANIA EVOLUTION, FACTORS OF INFLUENCE, FINANCING

THE CURRENT ACCOUNT OF ROMANIA EVOLUTION, FACTORS OF INFLUENCE, FINANCING Abstract Camelia MILEA, PhD The balance of the current account is a tool used to establish the level of economic development of

THE CURRENT ACCOUNT OF ROMANIA EVOLUTION, FACTORS OF INFLUENCE, FINANCING Abstract Camelia MILEA, PhD The balance of the current account is a tool used to establish the level of economic development of

IIb. Weighted Average Interest Rates on New Loans

ECONOMIC BULLETIN VOLUME XIII NO.1 Page 99 IIb. Weighted Average Interest Rates on New Loans Prepared by Tanisha Mitchell and Rekha Sookraj 1 One of the characteristics of the current interest rate environment

ECONOMIC BULLETIN VOLUME XIII NO.1 Page 99 IIb. Weighted Average Interest Rates on New Loans Prepared by Tanisha Mitchell and Rekha Sookraj 1 One of the characteristics of the current interest rate environment

Meeting with Analysts

CNB s New Forecast (Inflation Report II/2015) Meeting with Analysts Petr Král Prague, 11 May, 2015 1 Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

CNB s New Forecast (Inflation Report II/2015) Meeting with Analysts Petr Král Prague, 11 May, 2015 1 Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

(2) Fiscal policy in all countries needs to be cast in a mediumterm FISCAL POLICY IN OIL EXPORTING COUNTRIES AND THE ROLE OF STABILIZATION FUNDS

Fiscal policy in all countries needs to be cast in a mediumterm FISCAL POLICY IN OIL EXPORTING COUNTRIES AND THE ROLE OF STABILIZATION FUNDS") FISCAL POLICY IN OIL EXPORTING COUNTRIES AND THE ROLE OF STABILIZATION FUNDS Ugo Fasano (IMF) U.N. Workshops Bonn, May 2003 (2) Fiscal policy in all countries needs to be cast in a mediumterm framework

FISCAL POLICY IN OIL EXPORTING COUNTRIES AND THE ROLE OF STABILIZATION FUNDS Ugo Fasano (IMF) U.N. Workshops Bonn, May 2003 (2) Fiscal policy in all countries needs to be cast in a mediumterm framework

Governor's Statement No. 34 October 9, 2015. Statement by the Hon. BARRY WHITESIDE, Governor of the Bank and the Fund for the REPUBLIC OF FIJI

Governor's Statement No. 34 October 9, 2015 Statement by the Hon. BARRY WHITESIDE, Governor of the Bank and the Fund for the REPUBLIC OF FIJI Statement by the Hon. Mr. Barry Whiteside, Governor of the

Governor's Statement No. 34 October 9, 2015 Statement by the Hon. BARRY WHITESIDE, Governor of the Bank and the Fund for the REPUBLIC OF FIJI Statement by the Hon. Mr. Barry Whiteside, Governor of the

Statement by the Hon. STEFAN INGVES, Governor of the Fund for SWEDEN, on behalf of the Nordic and Baltic Countries

Governor Statement No. 25 September 23, 2011 Statement by the Hon. STEFAN INGVES, Governor of the Fund for SWEDEN, on behalf of the Nordic and Baltic Countries Statement by the Hon. Stefan Ingves, Governor

Governor Statement No. 25 September 23, 2011 Statement by the Hon. STEFAN INGVES, Governor of the Fund for SWEDEN, on behalf of the Nordic and Baltic Countries Statement by the Hon. Stefan Ingves, Governor

SURVEY ON HOW COMMERCIAL BANKS DETERMINE LENDING INTEREST RATES IN ZAMBIA

BANK Of ZAMBIA SURVEY ON HOW COMMERCIAL BANKS DETERMINE LENDING INTEREST RATES IN ZAMBIA September 10 1 1.0 Introduction 1.1 As Government has indicated its intention to shift monetary policy away from

BANK Of ZAMBIA SURVEY ON HOW COMMERCIAL BANKS DETERMINE LENDING INTEREST RATES IN ZAMBIA September 10 1 1.0 Introduction 1.1 As Government has indicated its intention to shift monetary policy away from

Study Questions (with Answers) Lecture 14 Pegging the Exchange Rate

Lecture 14 Pegging the Exchange Rate") Study Questions (with Answers) Page 1 of 7 Study Questions (with Answers) Lecture 14 the Exchange Rate Part 1: Multiple Choice Select the best answer of those given. 1. Suppose the central bank of Mexico

Study Questions (with Answers) Page 1 of 7 Study Questions (with Answers) Lecture 14 the Exchange Rate Part 1: Multiple Choice Select the best answer of those given. 1. Suppose the central bank of Mexico

South African Trade-Offs among Depreciation, Inflation, and Unemployment. Alex Diamond Stephanie Manning Jose Vasquez Erin Whitaker

South African Trade-Offs among Depreciation, Inflation, and Unemployment Alex Diamond Stephanie Manning Jose Vasquez Erin Whitaker April 16, 2003 Introduction South Africa has one of the most unique histories

South African Trade-Offs among Depreciation, Inflation, and Unemployment Alex Diamond Stephanie Manning Jose Vasquez Erin Whitaker April 16, 2003 Introduction South Africa has one of the most unique histories

The role of the G20. Central Bank of Argentina. Miguel Angel Pesce Deputy Governor, BCRA CEMLA. Cartagena, Colombia. 5-6 May 2011

The role of the G20 Central Bank of Argentina Miguel Angel Pesce Deputy Governor, BCRA CEMLA. Cartagena, Colombia. 5-6 May 2011 Agenda Agenda 1. G20 Objectives for 2011 a) Macroeconomic Policy Coordination

The role of the G20 Central Bank of Argentina Miguel Angel Pesce Deputy Governor, BCRA CEMLA. Cartagena, Colombia. 5-6 May 2011 Agenda Agenda 1. G20 Objectives for 2011 a) Macroeconomic Policy Coordination

Session 12. Aggregate Supply: The Phillips curve. Credibility

Session 12. Aggregate Supply: The Phillips curve. Credibility v Potential Output and v Okun s law v The Role of Expectations and the Phillips Curve v Oil Prices and v US Monetary Policy and World Real

Session 12. Aggregate Supply: The Phillips curve. Credibility v Potential Output and v Okun s law v The Role of Expectations and the Phillips Curve v Oil Prices and v US Monetary Policy and World Real

SECTOR ASSESSMENT (SUMMARY): FINANCE 1. 1. Sector Performance, Problems, and Opportunities

: FINANCE 1. 1. Sector Performance, Problems, and Opportunities") Country Partnership Strategy: Bangladesh, 2011 2015 SECTOR ASSESSMENT (SUMMARY): FINANCE 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities 1. The finance sector in Bangladesh is diverse,

Country Partnership Strategy: Bangladesh, 2011 2015 SECTOR ASSESSMENT (SUMMARY): FINANCE 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities 1. The finance sector in Bangladesh is diverse,

SUMMARY OF COUNTRY PRACTICES

I SUMMARY OF COUNTRY PRACTICES 1 Introduction 16. This document has been developed to accompany the Guidelines for Foreign Exchange Reserve Management that were approved by the Executive Board of the International

I SUMMARY OF COUNTRY PRACTICES 1 Introduction 16. This document has been developed to accompany the Guidelines for Foreign Exchange Reserve Management that were approved by the Executive Board of the International

Guidelines. on the applicable notional discount rate for variable remuneration EBA/GL/2014/01. 27 March 2014

GUIDELINES ON THE APPLICABLE NOTIONAL DISCOUNT RATE FOR VARIABLE REMUNERATION EBA/GL/2014/01 27 March 2014 Guidelines on the applicable notional discount rate for variable remuneration Contents 1. Executive

GUIDELINES ON THE APPLICABLE NOTIONAL DISCOUNT RATE FOR VARIABLE REMUNERATION EBA/GL/2014/01 27 March 2014 Guidelines on the applicable notional discount rate for variable remuneration Contents 1. Executive

Dr Andreas Dombret Member of the Board of Deutsche Bundesbank. The euro area Prospects and challenges

Dr Andreas Dombret Member of the Board of Deutsche Bundesbank The euro area Prospects and challenges Speech at the Fundacao Getulio Vargas in Sao Paulo Monday, 5 October 2015 Seite 1 von 12 Inhalt 1 Introduction...

Dr Andreas Dombret Member of the Board of Deutsche Bundesbank The euro area Prospects and challenges Speech at the Fundacao Getulio Vargas in Sao Paulo Monday, 5 October 2015 Seite 1 von 12 Inhalt 1 Introduction...

Ensuring Sound Monetary Policy in the Aftermath of Crisis

Ensuring Sound Monetary Policy in the Aftermath of Crisis U.S. Monetary Policy Forum The Initiative on Global Markets University of Chicago Booth School of Business New York, New York February 27, 2009

Ensuring Sound Monetary Policy in the Aftermath of Crisis U.S. Monetary Policy Forum The Initiative on Global Markets University of Chicago Booth School of Business New York, New York February 27, 2009

East Midlands Development Agency/Bank of England Dinner, Leicester 14 October 2003

1 Speech given by Mervyn King, Governor of the Bank of England East Midlands Development Agency/Bank of England Dinner, Leicester 14 October 2003 All speeches are available online at www.bankofengland.co.uk/publications/pages/speeches/default.aspx

1 Speech given by Mervyn King, Governor of the Bank of England East Midlands Development Agency/Bank of England Dinner, Leicester 14 October 2003 All speeches are available online at www.bankofengland.co.uk/publications/pages/speeches/default.aspx

Money and Public Finance

Money and Public Finance By Mr. Letlet August 1 In this anxious market environment, people lose their rationality with some even spreading false information to create trading opportunities. The tales about

Money and Public Finance By Mr. Letlet August 1 In this anxious market environment, people lose their rationality with some even spreading false information to create trading opportunities. The tales about

Latin America s Debt crisis 1980 s

Latin America s Debt crisis 1980 s The LATAM Debt Crisis of the 80 s Why the region accumulated an unmanageable external debt? What factors precipitated the crisis? How sovereignties and international

Latin America s Debt crisis 1980 s The LATAM Debt Crisis of the 80 s Why the region accumulated an unmanageable external debt? What factors precipitated the crisis? How sovereignties and international

WHY IS THE FISCAL POLICY IMPOSED BY IMF PRO-CYCLIC?

WHY IS THE FISCAL POLICY IMPOSED BY IMF PRO-CYCLIC? Marinaş Marius-Corneliu Academy of Economic Studies, Department of Economics, Bucharest marinasmarius@yahoo.fr Telephone: 0721/32.62.97 The economies

WHY IS THE FISCAL POLICY IMPOSED BY IMF PRO-CYCLIC? Marinaş Marius-Corneliu Academy of Economic Studies, Department of Economics, Bucharest marinasmarius@yahoo.fr Telephone: 0721/32.62.97 The economies

FUNDS TM. G10 Currencies: White Paper. A Monetary Policy Analysis FUNDS. The Authority on Currencies

FUNDS White Paper The Authority on Currencies Merk Investments LLC Research MAY 2012 G10 Currencies: A Monetary Policy Analysis Merk Monetary Score favors currencies of, and Canada; disfavors currencies

FUNDS White Paper The Authority on Currencies Merk Investments LLC Research MAY 2012 G10 Currencies: A Monetary Policy Analysis Merk Monetary Score favors currencies of, and Canada; disfavors currencies

Chapter 17. Preview. Introduction. Fixed Exchange Rates and Foreign Exchange Intervention

Chapter 17 Fixed Exchange Rates and Foreign Exchange Intervention Slides prepared by Thomas Bishop Copyright 2009 Pearson Addison-Wesley. All rights reserved. Preview Balance sheets of central banks Intervention

Chapter 17 Fixed Exchange Rates and Foreign Exchange Intervention Slides prepared by Thomas Bishop Copyright 2009 Pearson Addison-Wesley. All rights reserved. Preview Balance sheets of central banks Intervention

State budget borrowing requirements financing plan and its background

Public Debt Department State budget borrowing requirements financing plan and its background September 2014 THE MOST IMPORTANT INFORMATION Monthly issuance calendar... 2 MoF comment... 8 Rating agencies

Public Debt Department State budget borrowing requirements financing plan and its background September 2014 THE MOST IMPORTANT INFORMATION Monthly issuance calendar... 2 MoF comment... 8 Rating agencies

Implementing Inflation Targeting: Institutional Arrangements, Target Design, and Communications

WP/06/278 Implementing Inflation Targeting: Institutional Arrangements, Target Design, and Communications Geoffrey Heenan, Marcel Peter, and Scott Roger 2006 International Monetary Fund WP/06/278 IMF

WP/06/278 Implementing Inflation Targeting: Institutional Arrangements, Target Design, and Communications Geoffrey Heenan, Marcel Peter, and Scott Roger 2006 International Monetary Fund WP/06/278 IMF

The history of the Bank of Russia s exchange rate policy

The history of the Bank of Russia s exchange rate policy Central Bank of the Russian Federation Abstract During the post-soviet period of 1992 98, the monetary policy of the Bank of Russia was essentially

The history of the Bank of Russia s exchange rate policy Central Bank of the Russian Federation Abstract During the post-soviet period of 1992 98, the monetary policy of the Bank of Russia was essentially

Q1 1990 Q1 1996 Q1 2002 Q1 2008 Q1

August 2015 Canada s debt burden By Richard J. Wylie, CFA Vice-President, Investment Strategy, Assante Wealth Management Much ink has been spilled over the past several years regarding the extent of the

August 2015 Canada s debt burden By Richard J. Wylie, CFA Vice-President, Investment Strategy, Assante Wealth Management Much ink has been spilled over the past several years regarding the extent of the

Managing Systemic Banking Crises. David S. Hoelscher Assistant Director Money and Credit Markets Department

Managing Systemic Banking Crises David S. Hoelscher Assistant Director Money and Credit Markets Department 2 Introduction Systemic banking crises of unprecedented scale: Argentina, East Asia, Ecuador,

Managing Systemic Banking Crises David S. Hoelscher Assistant Director Money and Credit Markets Department 2 Introduction Systemic banking crises of unprecedented scale: Argentina, East Asia, Ecuador,

Sergio Silva Alcalde Beachhead Advisor South America. Presentation to Latin America New Zealand Business Council

Sergio Silva Alcalde Beachhead Advisor South America Presentation to Latin America New Zealand Business Council Stable economy: The good performance of the Chilean economy is one of the major qualities

Sergio Silva Alcalde Beachhead Advisor South America Presentation to Latin America New Zealand Business Council Stable economy: The good performance of the Chilean economy is one of the major qualities