FC United Limited Individual Loan Stock Scheme. You could benefit from Social Investment Tax Relief of 30%!

|

|

|

- Ethelbert Bryant

- 8 years ago

- Views:

Transcription

1 FC United Limited Individual Loan Stock Scheme You could benefit from Social Investment Tax Relief of 30%! In March 2014 FC United launched a Loan Stock Scheme for businesses and organisations as part of our capital fund raising for our community stadium and sports facilities due to open in Moston this autumn. That scheme raised 50,000 (with another 50,000 in the pipeline) and added to our ground-breaking Community Share Scheme, and support from funding partners. Despite this success, the Club are still short of the ambitious capital target that we set ourselves. We are now launching a Loan Stock Scheme for individuals to help bridge that final gap. An announcement by the Chancellor in this year s budget heralded the creation of a new Social Investment Tax Relief which came into force in August This has given us a new focus to complete our capital funding drive. FC United is now launching a Loan Stock Scheme for Individuals. This is a ground-breaking loan stock offer from FC United; the first of its kind to qualify for the new Social Investment Tax Relief (SITR). This means that subject to your own personal circumstances individuals that loan money to the club a minimum of 3 years can claim back 30% of their investment from their income tax liability for the year in which the investment is made. The aim is to raise 200,000 from this scheme. The loan stock will be offered to investors as follows: A minimum investment of 10,000 A maximum investment of 200,000 An optional interest rate payment of 2% Full repayment (whether or not you opt to take the optional 2%) after 4 years February 2019 Qualification of the scheme for Social Investment Tax Relief (SITR) means that, subject to personal circumstances, investors can recoup 30% of what they invest against their tax liability. About FC United FC United Limited is a leading, supporter-owned football club that is democratically run by its 3,000 members. It is currently building a new home ground and community facilities in Moston, north Manchester, which will deliver real and lasting benefit to the area, with new sports and non-sports community facilities. It will also provide a home ground with a 5,000 capacity that will ensure the club s sustainable future. The stadium is due to open in winter 2014.

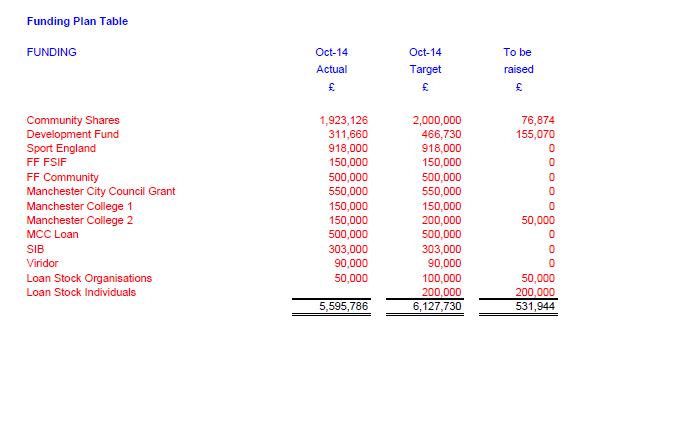

2 Further details about the club and the development can be found at: Invitation to Invest FC United Limited are inviting individuals to lend money to the club to assist this development and help contribute to the significant community benefit outcomes the facility and the club will deliver. FC United has already successfully raised 5.55m needed to build the new facility which has a total project cost of 6.011m. The club s members have raised a phenomenal 1.9m in a landmark Community Share Scheme which qualified for the Enterprise Investment Scheme. The club have also raised over 300,000 in donations and fund raising and over 2.5m in grant funding from Sport England, Football Foundation, Social Investment Business and Manchester City Council. A table showing the funding breakdown is provided at the end of this document. The Loan Stock offer is the last piece in the jigsaw, filling part of required shortfall shortfall in the capital funding target, aiming to raise 200,000: It will benefit the club by providing less expensive borrowing than other options It will benefit the community by allowing resources to be put into our community activities And it will benefit you - by borrowing from our own community, and by being eligible for the SITR, we can enable individuals to share in the success of the club. Business Plan, Project Costs and Funding Potential lenders are encouraged to read the club s Business Plan summary provided in this document and funding plan as at 31 st October Further details are available on request. What is Loan Stock? As a Community Benefit Society (formerly known as Industrial and Provident Society), FC United is a one-member, one-vote organisation. It also has the power to borrow money, in this case in the form of Loan Stock, at a rate and under conditions agreed by its board. The Board has decided to offer loan stock to individuals at an optional 2% interest a year over four years. Other similar societies have raised and repaid loan stock in this way. For example, in 2008/9 Unicorn Grocery raised (and later repaid) around 200,000 loan stock towards buying their Chorlton premises and then their farming land. (More details about the principles of loan stock may be found on pages of Simply Finance What Can You Buy? You can purchase between 10,000 and a maximum of 200,000 of FC United s Loan Stock.

3 Social Investment Tax Relief Individuals making an eligible investment at any time after 6 April 2014 can deduct 30% of the cost of their investment from their income tax liability for 2014/15. The minimum period of investment is 3 years. To make sure new investment is directed to the organisations which need it most and to meet EU regulations, the investment and the organisation receiving it must meet certain criteria. Organisations must have a defined and regulated social purpose. Charities, community interest companies or community benefit societies carrying out a qualifying trade, with fewer than 500 employees and gross assets of no more than 15 million may be eligible. FC United meets these criteria. Individual investors can invest up to 1,000,000 and can invest in more than one social enterprise. This is independent of any investments under Seed Enterprise Investment Scheme and Enterprise Investment Scheme which are subject to their own annual investment limits. It should be noted that: It is possible to claim SITR on this investment even if you have claimed Enterprise Investment Scheme (EIS) tax relief on investment in the FC United Community Shares Scheme. Your ability to claim SITR will be down to your own personal circumstances and FC United cannot comment on your eligibility Further information about SITR is available here: A Financial and Social Return - Why You Should Consider Buying FC United Loan Stock If you have savings in a bank or building society account, it is unlikely that you are earning much more than 1% interest; and even in an ISA it is not likely to exceed 2.5%. If you buy FC United Loan Stock, you will can earn interest AND possibly qualify for SITR which will give you a 30% return against your tax liability. Unlike savings in most banks, you can be assured that FC United is 100% democratically owned by its members. Its constitution specifies that it must deliver benefit to its communities, an obligation directors and members take very seriously. By investing in this scheme you will be supporting a development in an area of North Manchester that is in dire need of new facilities and the work of FC United in the local area to deliver sporting, education, employment and environmental benefit. The Loan Stock offer is based on a robust business plan this has been the basis of FC United s Community Share Scheme, over 2.5m of grant funding and Manchester City

4 Council s support of the project. A summary business plan showing repayment of this Loan Stock Offer is attached to this document. Remember you can claim SITR tax relief on this Loan Stock Offer even if you have already claimed EIS on the FCUM Share Scheme (subject to personal circumstances). Risks and Contingencies The Society and the Board accept responsibility for the information contained in this document. To the best of the knowledge of the Society and the Board (who have taken all reasonable care to ensure that such is the case) the information contained in this document is in accordance with the facts and contains no omission likely to affect its substance. Prospective investors should read the whole text of this document and should be aware that the intended outcomes of an investment in the Society are speculative and involve significant risk. Our Loan Stock offer is exempt from the Financial Services and Markets Act 2000 or subsidiary regulations; this means you have no right of complaint to an ombudsman. A community benefit society is registered with but not authorised by the Financial Services Authority and therefore the money you lend in this scheme is not safeguarded by any depositor protection scheme or dispute resolution scheme. As the whole of your investment could carry a risk, please consider it carefully in the context of the complete share offer document, and if needed seek independent advice. This document contains some forward-looking statements that are subject to certain risks and uncertainties. FC United has an obligation to create social dividends and community benefit as well as run sustainably. Its business planning has been undertaken prudently - the robust business plan has been the basis of FC United s Community Share Scheme, over 2.5m of grant funding and Manchester City Council s support of the project. However, the amount of loan stock purchased, and any interest on the loan stock, is not be secured on any assets of FC United. In the event of the social enterprise winding up, you may lose all the money you pay for the loan stock and we may not be able to pay interest on the loan stock purchased. The directors are committed to the prudent financial management of FC s affairs. However you should buy loan stock only with money you can afford to have tied up and without the prospect of any increase in value for several years or longer. The Loan Stock offered ranks below other debts of the enterprise, except other unsecured debt, in the event of the enterprise winding up. The Loan Stock offered ranks equally with the Capital Funding shares issued by FC United of Manchester in the event of the enterprise winding up. This means that the investors in the Loan Stock offered cannot be guaranteed to get their money back before the holders of the Capital Funding Shares or other lenders, as far as is possible, if the social enterprise falls into difficulty or fails.

the information contained in this document is in accordance with the")

5 How Do You Buy Loan Stock? To benefit from FC s loan stock, you simply need to fill in the attached Application Form For any questions or clarifications, please do not hesitate to contact Amanda Tudor FC United s Business Development Manager - amandatudor@fc-utd.co.uk If you require further information about the club, please contact Andy Walsh, General Manager, or Adam Brown, Board Member, at office@fc-utd.co.uk. You can buy between a minimum of 10,000 and a maximum of 200,000 of Loan Stock. Applications must be received between 15 th October 2014 and February 28 th A separate Loan Stock Scheme exists if you want to purchase on behalf of an organisation please contact Amanda Tudor: amandatudor@fc-utd.co.uk Loan stock must be repaid to the lender, in full when it falls due. FC United is not taking money on deposit. Loan stock is not regulated nor guaranteed by the government. What Happens After You Apply FC United Limited will receive your application. We will only take payment once your application has been accepted. You will be issued with a Loan Stock certificate. For further information or to discuss the FC United Individual Loan Stock Offer, please contact Amanda Tudor: amandatudor@fc-utd.co.uk

6 Five Year Forecast P+L Summary and Balance Sheet, November 2014

7

8

Investing in community shares

Investing in community shares Investing in community shares Introduction Give, lend or invest? Have you been invited to buy shares in a community enterprise? Then you are not alone. You are one of thousands

Investing in community shares Investing in community shares Introduction Give, lend or invest? Have you been invited to buy shares in a community enterprise? Then you are not alone. You are one of thousands

The Rangers Community Share Issue

The Rangers Community Share Issue Intro We are asking people to invest in a fund which has the sole purpose of acquiring a significant stake in the Club. Why We believe that the Club is best owned democratically

The Rangers Community Share Issue Intro We are asking people to invest in a fund which has the sole purpose of acquiring a significant stake in the Club. Why We believe that the Club is best owned democratically

Social Investment Tax Relief (SITR) - investors

- investors") Social Investment Tax Relief (SITR) - investors What is SITR - how does it affect me? SITR provides a range of income and capital gains tax reliefs which can be claimed by individual investors for investments

Social Investment Tax Relief (SITR) - investors What is SITR - how does it affect me? SITR provides a range of income and capital gains tax reliefs which can be claimed by individual investors for investments

clubdevelopment Community Shares A better way for Sports Clubs to raise money

clubdevelopment Community Shares A better way for Sports Clubs to raise money 03 Introduction A Club can command a place in the community connecting people like few other things in modern day society,

clubdevelopment Community Shares A better way for Sports Clubs to raise money 03 Introduction A Club can command a place in the community connecting people like few other things in modern day society,

Social Investment Tax Relief

Thompson Taraz Ten things you need to know about: Social Investment Tax Relief September 2014 SITR 2 Background - An introduction Social Investment Tax Relief ( SITR ), launched this year in the UK, aims

Thompson Taraz Ten things you need to know about: Social Investment Tax Relief September 2014 SITR 2 Background - An introduction Social Investment Tax Relief ( SITR ), launched this year in the UK, aims

Social Investment Tax Relief (SITR)

") Social Investment Tax Relief (SITR) The legislation governing SITR will not become law until the Finance Bill receives Royal Assent, expected to be in July 2014. This guidance is based on HM Revenue and

Social Investment Tax Relief (SITR) The legislation governing SITR will not become law until the Finance Bill receives Royal Assent, expected to be in July 2014. This guidance is based on HM Revenue and

Flexible access to short-term finance. Precisely when you need it. Rathbones secured lending facility.

Flexible access to short-term finance. Precisely when you need it. Rathbones secured lending facility. Flexible lending. As a client of Rathbones, there may be occasions when you need to access short to

Flexible access to short-term finance. Precisely when you need it. Rathbones secured lending facility. Flexible lending. As a client of Rathbones, there may be occasions when you need to access short to

Peer-to-peer bad debt relief: proposed technical criteria. Technical Note 24 March 2015

Peer-to-peer bad debt relief: proposed technical criteria Technical Note 24 March 2015 1 Contents Page Chapter 1 Introduction 3 Chapter 2 Summary of Proposed Relief 4 Chapter 3 Amount of Proposed Relief

Peer-to-peer bad debt relief: proposed technical criteria Technical Note 24 March 2015 1 Contents Page Chapter 1 Introduction 3 Chapter 2 Summary of Proposed Relief 4 Chapter 3 Amount of Proposed Relief

Social Investment Tax Relief

Social Investment Tax Relief A BRIEF GUIDE A guide to the first tax incentive of its kind in the world that targets social investors prepared by Social Investment Tax Relief A Brief Guide Table of Questions

Social Investment Tax Relief A BRIEF GUIDE A guide to the first tax incentive of its kind in the world that targets social investors prepared by Social Investment Tax Relief A Brief Guide Table of Questions

Key Features of the Stockmarket Linked Savings Account and Stockmarket Linked Savings Account ISA

Key Features of the Stockmarket Linked Savings Account and Stockmarket Linked Savings Account ISA This is an important document. You need to read this before you open a Stockmarket Linked Savings Account

Key Features of the Stockmarket Linked Savings Account and Stockmarket Linked Savings Account ISA This is an important document. You need to read this before you open a Stockmarket Linked Savings Account

Community Shares Practitioner Training and Licensing

Community Shares Practitioner Training and Licensing January 2016 Contents Introduction... 4 Becoming a licensed practitioner... 4 Other materials... 5 Skills Specification... 6 Functional analysis...

Community Shares Practitioner Training and Licensing January 2016 Contents Introduction... 4 Becoming a licensed practitioner... 4 Other materials... 5 Skills Specification... 6 Functional analysis...

NEWCASTLE BUILDING SOCIETY ANNOUNCES FINANCIAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2013

Stock Exchange Announcement Strictly embargoed until 9.00 a.m. Tuesday 25 th February 2014 NEWCASTLE BUILDING SOCIETY ANNOUNCES FINANCIAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2013 Newcastle Building

Stock Exchange Announcement Strictly embargoed until 9.00 a.m. Tuesday 25 th February 2014 NEWCASTLE BUILDING SOCIETY ANNOUNCES FINANCIAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2013 Newcastle Building

The Help to Buy: equity loan scheme What you need to know before you go ahead

Page 1 of 5 The Help to Buy: equity loan scheme What you need to know before you go ahead What is the Help to Buy: equity loan scheme? The Help to Buy: equity loan scheme is a Government backed programme

Page 1 of 5 The Help to Buy: equity loan scheme What you need to know before you go ahead What is the Help to Buy: equity loan scheme? The Help to Buy: equity loan scheme is a Government backed programme

TOPIC SHEET - COMMUNITY SHARES TOPIC SHEET COMMUNITY SHARES. What are community shares? Purpose. What s involved

Purpose This topic sheet provides you with information about how to raise investment capital from your community to finance enterprising activities that may be identified in a Community Led Plan. Community

Purpose This topic sheet provides you with information about how to raise investment capital from your community to finance enterprising activities that may be identified in a Community Led Plan. Community

Stocks & Shares ISA Key Facts. This is an important document which you should keep.

Stocks & Shares ISA Key Facts! This is an important document which you should keep. 2 Key Facts of the Alliance Trust Savings Stocks & Shares ISA The Financial Conduct Authority is the independent financial

Stocks & Shares ISA Key Facts! This is an important document which you should keep. 2 Key Facts of the Alliance Trust Savings Stocks & Shares ISA The Financial Conduct Authority is the independent financial

The Help to Buy Equity Loan Scheme What you need to know before you go ahead

Page 1 of 6 The Help to Buy Equity Loan Scheme What you need to know before you go ahead What is the Help to Buy Equity Loan scheme? The Help to Buy Equity Loan scheme is a Government backed programme

Page 1 of 6 The Help to Buy Equity Loan Scheme What you need to know before you go ahead What is the Help to Buy Equity Loan scheme? The Help to Buy Equity Loan scheme is a Government backed programme

Secure Trust Bank PLC. 2014 YEAR END RESULTS 19th March 2015

Secure Trust Bank PLC 2014 YEAR END RESULTS 19th March 2015 Introduction PAUL LYNAM Chief Executive Officer Strategy Continues to Deliver Maximise shareholder value by: To maximise shareholder value through

Secure Trust Bank PLC 2014 YEAR END RESULTS 19th March 2015 Introduction PAUL LYNAM Chief Executive Officer Strategy Continues to Deliver Maximise shareholder value by: To maximise shareholder value through

Macquarie Prime Loan Facility

Macquarie Prime Loan Facility Product Disclosure Statement Contents Section 1 - About Macquarie Bank Limited and the Macquarie Prime Loan Facility 1 Section 2 - Benefits of a Macquarie Prime Loan Facility

Macquarie Prime Loan Facility Product Disclosure Statement Contents Section 1 - About Macquarie Bank Limited and the Macquarie Prime Loan Facility 1 Section 2 - Benefits of a Macquarie Prime Loan Facility

Help to Buy. House Builder and Developer Participation Guidance. July 2014. Page 1 of 15

Help to Buy House Builder and Developer Participation Guidance July 2014 Page 1 of 15 Contents Ministerial Foreword page 3 Introduction... page 4 Help to Buy overview... page 5 Help to Buy registration...

Help to Buy House Builder and Developer Participation Guidance July 2014 Page 1 of 15 Contents Ministerial Foreword page 3 Introduction... page 4 Help to Buy overview... page 5 Help to Buy registration...

ISA qualifying investments: consultation on whether to include investment based crowdfunding

Consultation Response ISA qualifying investments: consultation on whether to include investment based crowdfunding September 2015 About Co-operatives UK Co-operatives UK is the network for Britain s thousands

Consultation Response ISA qualifying investments: consultation on whether to include investment based crowdfunding September 2015 About Co-operatives UK Co-operatives UK is the network for Britain s thousands

SIPP Key Facts. This is an important document which you should keep.

SIPP Key Facts! This is an important document which you should keep. 2 Key Facts of the Alliance Trust Savings SIPP The Financial Conduct Authority is the independent financial services regulator. It requires

SIPP Key Facts! This is an important document which you should keep. 2 Key Facts of the Alliance Trust Savings SIPP The Financial Conduct Authority is the independent financial services regulator. It requires

Secure Trust Bank PLC. 2015 INTERIM RESULTS 21st July 2015

Secure Trust Bank PLC 2015 INTERIM RESULTS 21st July 2015 Introduction & business review PAUL LYNAM Chief Executive Officer Strategy continues to deliver Maximise shareholder value: To maximise shareholder

Secure Trust Bank PLC 2015 INTERIM RESULTS 21st July 2015 Introduction & business review PAUL LYNAM Chief Executive Officer Strategy continues to deliver Maximise shareholder value: To maximise shareholder

Enterprise Investment Scheme Compliance Statement

Enterprise Investment Scheme Compliance Statement There is a time limit for sending this form (read note 2 on page 5 for details). Please read the notes before filling in this form. If there is not enough

Enterprise Investment Scheme Compliance Statement There is a time limit for sending this form (read note 2 on page 5 for details). Please read the notes before filling in this form. If there is not enough

Portfolio Investments Key Features

Portfolio Investments Key Features Including the Investments ISA IMPORTANT INFORMATION YOU NEED TO READ AND UNDERSTAND BEFORE YOU INVEST The Financial Conduct Authority is a financial services regulator.

Portfolio Investments Key Features Including the Investments ISA IMPORTANT INFORMATION YOU NEED TO READ AND UNDERSTAND BEFORE YOU INVEST The Financial Conduct Authority is a financial services regulator.

Filling in the Form of Authority. Please ensure you have the lenders name in order to pursue the claim.

Filling in the Form of Authority Please ensure you have the lenders name in order to pursue the claim. 1. Print a claim form for each lender and type of finance. 2. Do not use one claim form for multiple

Filling in the Form of Authority Please ensure you have the lenders name in order to pursue the claim. 1. Print a claim form for each lender and type of finance. 2. Do not use one claim form for multiple

Deduction of income tax from interest: peer-topeer

Deduction of income tax from interest: peer-topeer lending Consultation document Publication date: 15 July 2015 Closing date for comments: 18 September 2015 Subject of this consultation: Scope of this

Deduction of income tax from interest: peer-topeer lending Consultation document Publication date: 15 July 2015 Closing date for comments: 18 September 2015 Subject of this consultation: Scope of this

Corporate Business. Newsletter. GAAR - a whole new world. Winter 2013-14

Newsletter Winter 2013-14 Corporate Business GAAR - a whole new world On 17 July 2013 a new tax rule came into force the general antiabuse rule known as GAAR. This is a fundamental change to the tax planning

Newsletter Winter 2013-14 Corporate Business GAAR - a whole new world On 17 July 2013 a new tax rule came into force the general antiabuse rule known as GAAR. This is a fundamental change to the tax planning

Help to Buy Buyers Guide

Help to Buy Buyers Guide Homes and Communities Agency http://www.homesandcommunities.co.uk/helptobuy Page 1 of 27 Key information Buyers using this scheme must provide security in the form of a second

Help to Buy Buyers Guide Homes and Communities Agency http://www.homesandcommunities.co.uk/helptobuy Page 1 of 27 Key information Buyers using this scheme must provide security in the form of a second

Income and gains generated by ISA investments are exempt from any further UK income tax as well as capital gains tax in the hands of the investor.

What is an ISA? ISA stands for Individual Savings Account. ISAs have been available since 6 April 1999. An ISA is a scheme for investment managed in accordance with the ISA Regulations under terms agreed

What is an ISA? ISA stands for Individual Savings Account. ISAs have been available since 6 April 1999. An ISA is a scheme for investment managed in accordance with the ISA Regulations under terms agreed

The Charity Bank Savings Account

The Charity Bank Savings Account Application form for individuals Please complete in block capitals and return this form to: Charity Bank, Fosse House, 182 High Street, Tonbridge, Kent TN9 1BE FOR OFFICE

The Charity Bank Savings Account Application form for individuals Please complete in block capitals and return this form to: Charity Bank, Fosse House, 182 High Street, Tonbridge, Kent TN9 1BE FOR OFFICE

Debts and Capital Gains Tax

Helpsheet 296 Tax year 6 April 2013 to 5 April 2014 Debts and Capital Gains Tax A Contacts This helpsheet explains: how debts are dealt with for Capital Gains Tax purposes how you may be able to claim

Helpsheet 296 Tax year 6 April 2013 to 5 April 2014 Debts and Capital Gains Tax A Contacts This helpsheet explains: how debts are dealt with for Capital Gains Tax purposes how you may be able to claim

Deduction of income tax from savings income: implementation of the Personal Savings Allowance

Deduction of income tax from savings income: implementation of the Personal Savings Allowance Consultation document Publication date: 15 July 2015 Closing date for comments: 18 September 2015 Subject of

Deduction of income tax from savings income: implementation of the Personal Savings Allowance Consultation document Publication date: 15 July 2015 Closing date for comments: 18 September 2015 Subject of

Close Brothers Close Brothers Finance plc (incorporated with limited liability in England and Wales with registered number 4322721)

") SUPPLEMENTARY PROSPECTUS DATED 9 APRIL Close Brothers Close Brothers Finance plc (incorporated with limited liability in England and Wales with registered number 4322721) 1,000,000,000 Euro Medium Term

SUPPLEMENTARY PROSPECTUS DATED 9 APRIL Close Brothers Close Brothers Finance plc (incorporated with limited liability in England and Wales with registered number 4322721) 1,000,000,000 Euro Medium Term

5. Funding Available for IP-Rich Businesses

20 IP Finance Toolkit 5. Funding Available for IP-Rich Businesses Introduction As the Banking on IP? report notes; SMEs first port of call for finance is often a bank. Figures quoted in the report show

20 IP Finance Toolkit 5. Funding Available for IP-Rich Businesses Introduction As the Banking on IP? report notes; SMEs first port of call for finance is often a bank. Figures quoted in the report show

Investment trusts and companies

Investment trusts and companies INVESTMENT TRUSTS AND COMPANIES Investment trusts and investment companies can provide an excellent way to achieve a diversified portfolio of shares within one simple investment.

Investment trusts and companies INVESTMENT TRUSTS AND COMPANIES Investment trusts and investment companies can provide an excellent way to achieve a diversified portfolio of shares within one simple investment.

NOTE ON LOAN CAPITAL MARKETS

The structure and use of loan products Most businesses use one or more loan products. A company may have a syndicated loan, backstop, line of credit, standby letter of credit, bridge loan, mortgage, or

The structure and use of loan products Most businesses use one or more loan products. A company may have a syndicated loan, backstop, line of credit, standby letter of credit, bridge loan, mortgage, or

how to finance the business

A DV I C E B O O K L E T how to finance the business HOW TO FINANCE THE BUSINESS Getting enough of the right funding is one of the more difficult tasks that you will face as a new entrepreneur. Typically,

A DV I C E B O O K L E T how to finance the business HOW TO FINANCE THE BUSINESS Getting enough of the right funding is one of the more difficult tasks that you will face as a new entrepreneur. Typically,

Financial Regulation. Consultation Paper 13/13: The FCA s regulatory approach to crowdfunding (and similar activities) November 2013

November 2013") Financial Regulation Consultation Paper 13/13: The FCA s regulatory approach to crowdfunding (and similar activities) November 2013 5926 Pinsent Masons Financial Regulation In the Entrepreneurship 2020

Financial Regulation Consultation Paper 13/13: The FCA s regulatory approach to crowdfunding (and similar activities) November 2013 5926 Pinsent Masons Financial Regulation In the Entrepreneurship 2020

ST. JAMES S PLACE UNIT TRUST AND ISA

ST. JAMES S PLACE UNIT TRUST AND ISA SUPPLEMENTARY INFORMATION DOCUMENT PARTNERS IN MANAGING YOUR WEALTH This document sets out terms and conditions which summarise how we will manage your investment.

ST. JAMES S PLACE UNIT TRUST AND ISA SUPPLEMENTARY INFORMATION DOCUMENT PARTNERS IN MANAGING YOUR WEALTH This document sets out terms and conditions which summarise how we will manage your investment.

ST. JAMES S PLACE UNIT TRUST GROUP

ST. JAMES S PLACE UNIT TRUST GROUP SUPPLEMENTARY INFORMATION DOCUMENT PARTNERS IN MANAGING YOUR WEALTH This document sets out terms and conditions which summarise how we will manage your investment. Words

ST. JAMES S PLACE UNIT TRUST GROUP SUPPLEMENTARY INFORMATION DOCUMENT PARTNERS IN MANAGING YOUR WEALTH This document sets out terms and conditions which summarise how we will manage your investment. Words

Community Shares. #OwnedByTheCrowd. /crowdfunder @crowdfunderuk communityshares@crowdfunder.co.uk

Community Shares #OwnedByTheCrowd /crowdfunder @crowdfunderuk communityshares@crowdfunder.co.uk Case study Introduction Hastings Pier Hastings Pier changed history with the power of the crowd when they

Community Shares #OwnedByTheCrowd /crowdfunder @crowdfunderuk communityshares@crowdfunder.co.uk Case study Introduction Hastings Pier Hastings Pier changed history with the power of the crowd when they

Company Tax Relief - What is a DLA?

.1. INTRODUCTION (DLA) simply describes the situation where either the company owes a director money or vice versa. Typically, a DLA is first created shortly before a company first starts to trade where

.1. INTRODUCTION (DLA) simply describes the situation where either the company owes a director money or vice versa. Typically, a DLA is first created shortly before a company first starts to trade where

Lend Us a Hand Loan Scheme and Social Investment Tax Relief (SITR).

.") Lend Us a Hand Loan Scheme and Social Investment Tax Relief (SITR). The Jericho Foundation Lend us a Hand loan scheme has now been able to take advantage of new legislation so that any future loans made

Lend Us a Hand Loan Scheme and Social Investment Tax Relief (SITR). The Jericho Foundation Lend us a Hand loan scheme has now been able to take advantage of new legislation so that any future loans made

Insolvency: a glossary of terms

INFORMATION SHEET 41 Insolvency: a glossary of terms This is a brief explanation of some of the terms you may come across in company insolvency proceedings. Please note that this glossary is for general

INFORMATION SHEET 41 Insolvency: a glossary of terms This is a brief explanation of some of the terms you may come across in company insolvency proceedings. Please note that this glossary is for general

LEND A HAND SAVINGS ACCOUNT. Terms and conditions

LEND A HAND SAVINGS ACCOUNT Terms and conditions April 2014 Terms and conditions This Account is not covered by the Lloyds Bank Personal Banking Terms and conditions. All terms relating to this Account

LEND A HAND SAVINGS ACCOUNT Terms and conditions April 2014 Terms and conditions This Account is not covered by the Lloyds Bank Personal Banking Terms and conditions. All terms relating to this Account

So You Want to Borrow Money to Start a Business?

So You Want to Borrow Money to Start a Business? M any small business owners cannot understand why a lending institution would refuse to lend them money. Others have no trouble getting money, but they

So You Want to Borrow Money to Start a Business? M any small business owners cannot understand why a lending institution would refuse to lend them money. Others have no trouble getting money, but they

Residential mortgages general information

Residential mortgages general information Residential mortgages general information 2 Contents Who we are and what we do 2 Forms of security 2 Representative Example 2 Indication of possible further costs

Residential mortgages general information Residential mortgages general information 2 Contents Who we are and what we do 2 Forms of security 2 Representative Example 2 Indication of possible further costs

Debt Service Analysis: Can I Repay?

Purdue Extension Knowledge to Go Debt Service Analysis: Can I Repay? Low prices and incomes have made many farmers and their lenders concerned about the farmers ability to fulfill debt obligations. Lenders

Purdue Extension Knowledge to Go Debt Service Analysis: Can I Repay? Low prices and incomes have made many farmers and their lenders concerned about the farmers ability to fulfill debt obligations. Lenders

Investing for a brighter future. Stocks and Shares ISAs explained 1 STOCKS AND SHARES ISAS EXPLAINED

Investing for a brighter future Stocks and Shares ISAs explained 1 STOCKS AND SHARES ISAS EXPLAINED Contents 03 What is a stocks and shares ISA? 04 How much can I invest? 05 Why invest in a stocks and

Investing for a brighter future Stocks and Shares ISAs explained 1 STOCKS AND SHARES ISAS EXPLAINED Contents 03 What is a stocks and shares ISA? 04 How much can I invest? 05 Why invest in a stocks and

KEY GUIDE. Setting up a new business

KEY GUIDE Setting up a new business The business idea You have a business idea, but can you turn it into a viable enterprise? Is there a market for the goods you will produce or the services you will supply?

KEY GUIDE Setting up a new business The business idea You have a business idea, but can you turn it into a viable enterprise? Is there a market for the goods you will produce or the services you will supply?

Car loans. Richie found it pays to shop around. How do car loans work? Factsheet. August 2011

Factsheet August 2011 Apart from your home, a car is one of the biggest single purchases you re ever likely to make. If you don t have the cash to pay for it upfront, you ll need to borrow money. And,

Factsheet August 2011 Apart from your home, a car is one of the biggest single purchases you re ever likely to make. If you don t have the cash to pay for it upfront, you ll need to borrow money. And,

The bank the business partner you can t do without

The bank the business partner you can t do without Key people are always in demand to help in running a business. Ask any farm owner to list out the key people the look to in the running of the farm would

The bank the business partner you can t do without Key people are always in demand to help in running a business. Ask any farm owner to list out the key people the look to in the running of the farm would

Email swanneyd@methodistchurch.org.uk

Churches Mutual Credit Union MC/14/4 Contact Name and Details Status of Paper Action Required Draft Resolution Alternative Options to Consider, if Any Mr Doug Swanney, Connexional Secretary Email swanneyd@methodistchurch.org.uk

Churches Mutual Credit Union MC/14/4 Contact Name and Details Status of Paper Action Required Draft Resolution Alternative Options to Consider, if Any Mr Doug Swanney, Connexional Secretary Email swanneyd@methodistchurch.org.uk

Helping businesses source finance

SUPPORTING BUSINESS - SOURCING FINANCE Helping businesses source finance Helping businesses source finance These are challenging times for every business. The economic environment has changed and many

SUPPORTING BUSINESS - SOURCING FINANCE Helping businesses source finance Helping businesses source finance These are challenging times for every business. The economic environment has changed and many

Terms of Business. Regulated Activities Our principal business is mortgage lending and this activity is regulated by the Central Bank of Ireland.

Terms of Business Provided in accordance with the Consumer Protection Code 2012 issued by the Central Bank of Ireland and can be found on the Central Bank s website www.centralbank.ie About Us Our legal

Terms of Business Provided in accordance with the Consumer Protection Code 2012 issued by the Central Bank of Ireland and can be found on the Central Bank s website www.centralbank.ie About Us Our legal

MORTGAGE FACTSHEET -1-

MORTGAGE FACTSHEET Choosing and obtaining a mortgage is not a simple task these days - whether you are a first time buyer, moving home, or remortgaging as you reach the end of your current incentive. This

MORTGAGE FACTSHEET Choosing and obtaining a mortgage is not a simple task these days - whether you are a first time buyer, moving home, or remortgaging as you reach the end of your current incentive. This

Payday and Short-term Loans DELIVERING NEW CONSUMER PROTECTIONS

DELIVERING NEW CONSUMER PROTECTIONS On 24 May 2012, the Consumer Finance Association, the Consumer Credit Trade Association, the BCCA and the Finance & Leasing Association agreed to a series of new consumer

DELIVERING NEW CONSUMER PROTECTIONS On 24 May 2012, the Consumer Finance Association, the Consumer Credit Trade Association, the BCCA and the Finance & Leasing Association agreed to a series of new consumer

ABOUT OUR SERVICES AND COSTS AND HOW WE DO BUSINESS WITH YOU

Wesleyan Financial Services Ltd Colmore Circus Birmingham B4 6AR ABOUT OUR SERVICES AND COSTS AND HOW WE DO BUSINESS WITH YOU About this document This document explains the service we offer, how you will

Wesleyan Financial Services Ltd Colmore Circus Birmingham B4 6AR ABOUT OUR SERVICES AND COSTS AND HOW WE DO BUSINESS WITH YOU About this document This document explains the service we offer, how you will

Help to Buy Buyers Guide. Homes and Communities Agency http://www.homesandcommunities.co.uk/helptobuy August 2014

Help to Buy Buyers Guide Homes and Communities Agency http://www.homesandcommunities.co.uk/helptobuy August 2014 What is Help to Buy? Help to Buy is equity loan assistance to home buyers from the Homes

Help to Buy Buyers Guide Homes and Communities Agency http://www.homesandcommunities.co.uk/helptobuy August 2014 What is Help to Buy? Help to Buy is equity loan assistance to home buyers from the Homes

Financial Statements and Ratios: Notes

Financial Statements and Ratios: Notes 1. Uses of the income statement for evaluation Investors use the income statement to help judge their return on investment and creditors (lenders) use it to help

Financial Statements and Ratios: Notes 1. Uses of the income statement for evaluation Investors use the income statement to help judge their return on investment and creditors (lenders) use it to help

first direct Money Market Account Terms and Conditions

first direct Money Market Account Terms and Conditions first direct Money Market Account Terms and Conditions These Money Market Terms and Conditions (the Money Market Terms ) are Additional Conditions

first direct Money Market Account Terms and Conditions first direct Money Market Account Terms and Conditions These Money Market Terms and Conditions (the Money Market Terms ) are Additional Conditions

Insolvency: a guide for shareholders

INFORMATION SHEET 43 Insolvency: a guide for shareholders If a company is in financial difficulty, it can be put under the control of an independent external administrator. The role of the external administrator

INFORMATION SHEET 43 Insolvency: a guide for shareholders If a company is in financial difficulty, it can be put under the control of an independent external administrator. The role of the external administrator

Business borrowing with FundingKnight

Business borrowing with FundingKnight Get the funding you need, with fast decisions, flexible terms and competitive rates www.fundingknight.com Borrowing for growth is a positive decision by any business

Business borrowing with FundingKnight Get the funding you need, with fast decisions, flexible terms and competitive rates www.fundingknight.com Borrowing for growth is a positive decision by any business

SUPPLEMENTARY INFORMATION DOCUMENT THE NFU MUTUAL SELECT INVESTMENT PLAN THE NFU MUTUAL SELECT INDIVIDUAL SAVINGS ACCOUNT (ISA) INVESTMENTS

INVESTMENTS") SUPPLEMENTARY INFORMATION DOCUMENT THE NFU MUTUAL SELECT INVESTMENT PLAN THE NFU MUTUAL SELECT INDIVIDUAL SAVINGS ACCOUNT (ISA) INVESTMENTS SUPPLEMENTARY INFORMATION DOCUMENT The NFU Mutual Select Investment

SUPPLEMENTARY INFORMATION DOCUMENT THE NFU MUTUAL SELECT INVESTMENT PLAN THE NFU MUTUAL SELECT INDIVIDUAL SAVINGS ACCOUNT (ISA) INVESTMENTS SUPPLEMENTARY INFORMATION DOCUMENT The NFU Mutual Select Investment

UK debt and the Scotland independence referendum

UK debt and the Scotland independence referendum The transfer of debt 1.1 In the event of Scottish independence from the United Kingdom (UK), the continuing UK Government would in all circumstances honour

UK debt and the Scotland independence referendum The transfer of debt 1.1 In the event of Scottish independence from the United Kingdom (UK), the continuing UK Government would in all circumstances honour

FSPFC08 Investigate arrears and recover debts

Overview This unit is about identifying arrears in accounts and implementing measures with the customer to put the repayments back on track. You will need to pay attention to details that are critical

Overview This unit is about identifying arrears in accounts and implementing measures with the customer to put the repayments back on track. You will need to pay attention to details that are critical

Cash ISA. Key features of our

Key features of our The Financial Conduct Authority is the independent financial services regulator. It requires us, The Co-operative Bank, to give you this important information to help you decide whether

Key features of our The Financial Conduct Authority is the independent financial services regulator. It requires us, The Co-operative Bank, to give you this important information to help you decide whether

FACT SHEET 11 - MAJOR BUILDER ELIGIBILITY REVIEWS (effective from 1 July 2014)

") FACT SHEET 11 - MAJOR BUILDER ELIGIBILITY REVIEWS (effective from 1 July 2014) The risk management strategy of the Home Warranty (HWIF) for major builders requires that a comprehensive annual review be

FACT SHEET 11 - MAJOR BUILDER ELIGIBILITY REVIEWS (effective from 1 July 2014) The risk management strategy of the Home Warranty (HWIF) for major builders requires that a comprehensive annual review be

Invitation to Invest

Esk Energy (Yorkshire) Limited Invitation to Invest Rev B August 2012 a small-scale hydroelectric project to support community carbon reduction in Whitby and the Esk Valley www.whitbyeskenergy.org.uk The

Esk Energy (Yorkshire) Limited Invitation to Invest Rev B August 2012 a small-scale hydroelectric project to support community carbon reduction in Whitby and the Esk Valley www.whitbyeskenergy.org.uk The

WHAT IS EQUITY RELEASE? WHY CONSIDER EQUITY RELEASE?

WHAT IS EQUITY RELEASE? Equity Release can free some of the capital tied up in your home, while you continue to live there. This money can be in the form of a tax-free lump sum, a regular income or a combination

WHAT IS EQUITY RELEASE? Equity Release can free some of the capital tied up in your home, while you continue to live there. This money can be in the form of a tax-free lump sum, a regular income or a combination

NISAs a simple explanation

NISAs a simple explanation A NISA is a New Individual Savings Account. As the name suggests, these are accounts that can be accessed by individuals (you cannot have a NISA in joint names). ISAs were introduced

NISAs a simple explanation A NISA is a New Individual Savings Account. As the name suggests, these are accounts that can be accessed by individuals (you cannot have a NISA in joint names). ISAs were introduced

Accounting and Reporting Policy FRS 102. Staff Education Note 14 Credit unions - Illustrative financial statements

Accounting and Reporting Policy FRS 102 Staff Education Note 14 Credit unions - Illustrative financial statements Disclaimer This Education Note has been prepared by FRC staff for the convenience of users

Accounting and Reporting Policy FRS 102 Staff Education Note 14 Credit unions - Illustrative financial statements Disclaimer This Education Note has been prepared by FRC staff for the convenience of users

Mortgages and Home Finance: Conduct of Business Sourcebook. Chapter 11. Responsible lending, and responsible financing of home purchase plans

Mortgages and Home Finance: Conduct of Business Sourcebook Chapter esponsible lending, and responsible of MCOB : esponsible lending, and responsible of Section.6 : esponsible lending and.6 esponsible lending

Mortgages and Home Finance: Conduct of Business Sourcebook Chapter esponsible lending, and responsible of MCOB : esponsible lending, and responsible of Section.6 : esponsible lending and.6 esponsible lending

6 % Information booklet. Retail Bond Offer fi xed to December 2020. The Paragon Group of Companies PLC. www.paragon-group.co.uk/group/retail-bond

Information booklet The Paragon Group of Companies PLC 13 February 2013 6 % Retail Bond Offer fi xed to December 2020 Lead Manager and Offeror Canaccord Genuity Limited Authorised Offerors Barclays Stockbrokers

Information booklet The Paragon Group of Companies PLC 13 February 2013 6 % Retail Bond Offer fi xed to December 2020 Lead Manager and Offeror Canaccord Genuity Limited Authorised Offerors Barclays Stockbrokers

VIRGIN STOCKS & SHARES ISA CONDITIONS

VIRGIN STOCKS & SHARES ISA CONDITIONS 1 PLEASE MAKE SURE YOU READ THESE CONDITIONS AS THEY CONTAIN INFORMATION YOU NEED TO KNOW This agreement is governed by the Individual Savings Account Regulations

VIRGIN STOCKS & SHARES ISA CONDITIONS 1 PLEASE MAKE SURE YOU READ THESE CONDITIONS AS THEY CONTAIN INFORMATION YOU NEED TO KNOW This agreement is governed by the Individual Savings Account Regulations

Plan and Track Your Finances

Chapter 9 Plan and Track Your Finances 9.1 Finance Your Business 9.2 Pro Forma Financial Statements 9.3 Record Keeping for Businesses Ideas in Action Electronic Safekeeping Katelin Shea addressed the unmet

Chapter 9 Plan and Track Your Finances 9.1 Finance Your Business 9.2 Pro Forma Financial Statements 9.3 Record Keeping for Businesses Ideas in Action Electronic Safekeeping Katelin Shea addressed the unmet

Will your investment or savings plan pay off your mortgage? why you need to review your investment or savings plan regularly;

April 2006 FSA Factsheet Will your investment or savings plan pay off your mortgage? Financial Services Authority This factsheet is for you if: you are using an investment or savings plan such as an endowment

April 2006 FSA Factsheet Will your investment or savings plan pay off your mortgage? Financial Services Authority This factsheet is for you if: you are using an investment or savings plan such as an endowment

Current liabilities and payroll

Chapter 12 Current liabilities and payroll Current liabilities are obligations that the business has to discharge within 12 months or its operating cycle if longer than one year. Obligations that are due

Chapter 12 Current liabilities and payroll Current liabilities are obligations that the business has to discharge within 12 months or its operating cycle if longer than one year. Obligations that are due

Quasi-Equity. Case study in using Revenue Participation Agreements. Venturesome

Quasi-Equity Case study in using Revenue Participation Agreements Venturesome 2 Venturesome is a social investment fund, an initiative of the Charities Aid Foundation (CAF). Venturesome provides capital

Quasi-Equity Case study in using Revenue Participation Agreements Venturesome 2 Venturesome is a social investment fund, an initiative of the Charities Aid Foundation (CAF). Venturesome provides capital

Keystart Home Loan Product Guide Dated February 2013

Keystart Home Loan Product Guide Dated February 2013 Keystart Loans Ltd ABN 27 009 427 034 Australian Credit Licence 381437 1 Contents About this booklet 3 Keystart Home Loan 4 SharedStart Home Loan 6

Keystart Home Loan Product Guide Dated February 2013 Keystart Loans Ltd ABN 27 009 427 034 Australian Credit Licence 381437 1 Contents About this booklet 3 Keystart Home Loan 4 SharedStart Home Loan 6

Financing UK Microhydro

Financing UK Microhydro What are the options available? raising the finance on hydro projects is slow, tedious, and uncertain unlike on wind and AD etc, where they can see brand names, quick installation

Financing UK Microhydro What are the options available? raising the finance on hydro projects is slow, tedious, and uncertain unlike on wind and AD etc, where they can see brand names, quick installation

Access to Finance Guide: 1. Bank Finance Options

Access to Finance Guide: 1. Bank Finance Options Overdrafts An overdraft is a flexible way for you to manage short-term borrowing requirements. Business overdrafts are traditionally easy to arrange and

Access to Finance Guide: 1. Bank Finance Options Overdrafts An overdraft is a flexible way for you to manage short-term borrowing requirements. Business overdrafts are traditionally easy to arrange and

Important information about your savings account

Important information about your savings account Important information about your savings account 1 Thank you for opening a Kent Reliance savings account. This leaflet contains information to help you

Important information about your savings account Important information about your savings account 1 Thank you for opening a Kent Reliance savings account. This leaflet contains information to help you

BUSINESS PLANS. . The best part of this is that it is free!

BUSINESS PLANS A business plan is absolutely essential to the creation of a new business entity as well as the continued profitable operation of an established business. The conduct of a business in the

BUSINESS PLANS A business plan is absolutely essential to the creation of a new business entity as well as the continued profitable operation of an established business. The conduct of a business in the

General Conditions for Bank of Cyprus UK CharityBonds (April 2013)

") General Conditions for Bank of Cyprus UK CharityBonds (April 2013) Bank of Cyprus UK Limited ( we/our/us ), trading as Bank of Cyprus UK, incorporated in England and Wales as company number 04728421, a

General Conditions for Bank of Cyprus UK CharityBonds (April 2013) Bank of Cyprus UK Limited ( we/our/us ), trading as Bank of Cyprus UK, incorporated in England and Wales as company number 04728421, a

Tax Reliefs for Community Energy Who Qualifies; How to Apply

Tax Reliefs for Community Energy Who Qualifies; How to Apply Presented by Mark Ward Senior Tax Manager, BDO LLP 30 March 2015 Budget 2015 From EIS to SITR ALL tax subsidised power and heat generation to

Tax Reliefs for Community Energy Who Qualifies; How to Apply Presented by Mark Ward Senior Tax Manager, BDO LLP 30 March 2015 Budget 2015 From EIS to SITR ALL tax subsidised power and heat generation to

Cash ISA Application Form

Your Information i) We may send your details to credit reference agencies and/or fraud prevention agencies who will supply us with information for the purpose of verifying your identity, including information

Your Information i) We may send your details to credit reference agencies and/or fraud prevention agencies who will supply us with information for the purpose of verifying your identity, including information

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

personal savings accounts

Important information about personal savings accounts STANDARD LIFE CASH SAVINGS A DIVISION OF BARCLAYS 152970.indd 1 06/07/2010 08:07 152970.indd 2 06/07/2010 08:07 Changes to the interest rates on our

Important information about personal savings accounts STANDARD LIFE CASH SAVINGS A DIVISION OF BARCLAYS 152970.indd 1 06/07/2010 08:07 152970.indd 2 06/07/2010 08:07 Changes to the interest rates on our

Saving and Investing in ISAs

Saving and Investing in ISAs ISAs are often referred to as tax wrappers. This means that you pay no tax, or less tax than usual, on the income you earn or on the profits you may make on your investments.

Saving and Investing in ISAs ISAs are often referred to as tax wrappers. This means that you pay no tax, or less tax than usual, on the income you earn or on the profits you may make on your investments.

REPORTING INSTRUCTIONS FOR INVESTMENT FUNDS

REPORTING INSTRUCTIONS FOR INVESTMENT FUNDS 1. Reporting policies & procedures 1.1 The Excel file Investment Funds Returns (FORM STAT 001) - contains three sheets (Assets, Liabilities and Memorandum Items).

REPORTING INSTRUCTIONS FOR INVESTMENT FUNDS 1. Reporting policies & procedures 1.1 The Excel file Investment Funds Returns (FORM STAT 001) - contains three sheets (Assets, Liabilities and Memorandum Items).

HOW DO SMALL BUSINESSES OPERATE

HOW DO SMALL BUSINESSES OPERATE Sources of Finance and Advice N4 BUSINESS IN ACTION N5 UNDERSTANDING BUSINESS LEARNING INTENTIONS AND LEARNING INTENTION: I understand the SUCCESS CRITERIA different sources

HOW DO SMALL BUSINESSES OPERATE Sources of Finance and Advice N4 BUSINESS IN ACTION N5 UNDERSTANDING BUSINESS LEARNING INTENTIONS AND LEARNING INTENTION: I understand the SUCCESS CRITERIA different sources

Truly Bespoke, Truly Independent

Financial Planning Group Truly Bespoke, Truly Independent Cottons Financial Planning Group Ltd is a specialist business; providing financial services and advice to both individuals and companies all over

Financial Planning Group Truly Bespoke, Truly Independent Cottons Financial Planning Group Ltd is a specialist business; providing financial services and advice to both individuals and companies all over

Customer Guide. to lifetime mortgages. more 2 choose a range of lifetime mortgage plans to suit every need

Customer Guide to lifetime mortgages more 2 choose a range of lifetime mortgage plans to suit every need From one of the UK s largest retirement lending specialists Please speak to your adviser for further

Customer Guide to lifetime mortgages more 2 choose a range of lifetime mortgage plans to suit every need From one of the UK s largest retirement lending specialists Please speak to your adviser for further

Stocks & Shares ISA Transfer form Cazenove Investment Fund Company - B Class shares

Stocks & Shares ISA Transfer form Cazenove Investment Fund Company - B Class shares For your own benefit and protection you should read carefully Cazenove Investment Fund Company s Key Investor Information

Stocks & Shares ISA Transfer form Cazenove Investment Fund Company - B Class shares For your own benefit and protection you should read carefully Cazenove Investment Fund Company s Key Investor Information

Junior ISA key features

SIPP ISA Dealing Junior ISA Junior ISA key features The Financial Conduct Authority is the independent financial services regulator. It requires us, AJ Bell Securities Limited, to give you this important

SIPP ISA Dealing Junior ISA Junior ISA key features The Financial Conduct Authority is the independent financial services regulator. It requires us, AJ Bell Securities Limited, to give you this important

Saffron Building Society Mortgages Savings Investments Insurance Loans. Residential mortgage conditions. www.saffronbs.co.

Saffron Building Society Mortgages Savings Investments Insurance Loans Residential mortgage conditions www.saffronbs.co.uk 0800 072 1100 Saffron Building Society Residential Mortgage Conditions (England

Saffron Building Society Mortgages Savings Investments Insurance Loans Residential mortgage conditions www.saffronbs.co.uk 0800 072 1100 Saffron Building Society Residential Mortgage Conditions (England

Investment Funds. Supplementary Information Document (SID) Provided by RBS Collective Investment Funds Limited

Provided by RBS Collective Investment Funds Limited") Investment Funds Supplementary Information Document (SID) Provided by RBS Collective Investment Funds Limited About this document This document is designed to provide you with information about Investment

Investment Funds Supplementary Information Document (SID) Provided by RBS Collective Investment Funds Limited About this document This document is designed to provide you with information about Investment

SUPPORTER SHARE OWNERSHIP:

SUPPORTER SHARE OWNERSHIP: Recommendations on how to increase supporter ownership in football Jim Brown Baker Brown Associates Dr. Adam Brown Substance Tom Hall Supporters Direct 2 Contents 1. INTRODUCTION

SUPPORTER SHARE OWNERSHIP: Recommendations on how to increase supporter ownership in football Jim Brown Baker Brown Associates Dr. Adam Brown Substance Tom Hall Supporters Direct 2 Contents 1. INTRODUCTION

Interest is paid tax-free^

Account Name Interest rates (AER*) Summary Box Key Product Information for our Savings Account(s) smile Cash ISA 0.50% tax-free^/aer* variable if you are a smile current account customer. 0.31% tax-free^/aer*

Account Name Interest rates (AER*) Summary Box Key Product Information for our Savings Account(s) smile Cash ISA 0.50% tax-free^/aer* variable if you are a smile current account customer. 0.31% tax-free^/aer*