The CFPB and Medical Collections: Unknown Territory in the Face of Sweeping Regulatory Change

|

|

|

- Ernest Wilkerson

- 8 years ago

- Views:

Transcription

1 The CFPB and Medical Collections: Unknown Territory in the Face of Sweeping Regulatory Change Agenda What is the CFPB? Brief chronology of the CFPB CFPB investigations and examinations; the cost of non-compliance CFPB Advanced Notice of Proposed Rulemaking (ANPR) in the debt collection industry CFPB and medical collections What hospitals and providers can do now to get ahead of the regulatory curve 1

in the debt collection industry CFPB and medical")

2 What is the Consumer Financial Protection Bureau? Created in 2010 by President Obama pursuant to the Dodd-Frank Wall Street Reform Act & Consumer Protection Act Our mission is to make markets for consumer financial products and services work for Americans whether they are applying for a mortgage, choosing among credit cards, or using any number of other consumer financial products. UDAAP-Unfair or Deceptive Acts or Practices What is the Consumer Financial Protection Bureau? Independent Federal Agency with broad powers including: Rulemaking 18 Regulations including TILA, FDCPA, FCRA, ECOA Supervision Examinations and Audits Enforcement Consent Orders Fees and Penalties have exceeded $787 million Litigation Similar to FTC Enforcement Education and Public Outreach 2

3 Industries Currently Regulated Bank & Non-Bank Financial Entities Mortgage Industry Banks and Financial Institutions Debt Collection Agencies Pay Day Lenders Debt Relief Services Credit Bureaus Auto Lenders Key Language is consumer product or service as defined by the Dodd-Frank Act 3

4 Brief History of the CFPB 2008 Elizabeth Warren and the Ideology Behind the CFPB; Harvard Magazine- Making Credit Safer But for a growing number of families steered into overpriced credit products and misleading insurance plans, trust in a creditor proves costly. And for families tangled up with truly dangerous financial products, the result can be wipedout savings, lost homes, costlier car insurance, job rejections, troubled marriages, bleak retirements, and broken lives. The effective deregulation of interest rates, coupled with innovations in credit charges including teaser rates, negative amortization, increased use of fees, cross-default clauses, and penalty interest rates have turned ordinary credit transactions into devilishly complex undertakings. Brief History of the CFPB 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act Proposed by Obama Administration in June 2009; Signed into law July 2010 Created the CFPB, Office of Financial Research (OFR) Known as the most comprehensive financial regulatory reform measures taken since the great depression 4

5 Brief History of the CFPB 2011 Fall 2011-releasing first bulletins regarding enforcement, requests for information July 21, Complaint Portal Released Public database administered by the CFPB Pertains to first party and third party consumer related activity Includes complaints related to medical/patient accounts Consumers include their desired resolution which includes Closed with Monetary Relief 5

6 CFPB Complaints by Type 14,328 complaints from July February ,381 complaints were related to medical accounts; more than mortgage and payday loan combined 9.6% of complaints from Texas consumers 6

7 Brief History of the CFPB 2012 Brief History of the CFPB 2012 January Richard Cordray appointed Director of CFPB by President Obama Previously served as Ohio Attorney General Brought suit against AIG, Bank of America and Fannie Mae while AG 7

8 CFPB Supervisory Authority CFPB exams range from 6-8 weeks and cover several modules to determine compliance Onsite auditors review all processes and procedures Reviews company s Compliance Management System ( CMS ) CFPB attempts to identify UDAAP violations Unfair, deceptive, or abusive acts or practices in connection with financial products or services Very broad and abstract Expands potential for practice violations More than $70 million in remediation in non-public examinations CFPB Enforcement Authority Initiated by a Civil Investigative Demand ( CID ) targeting a specific act or practice Must produce millions of documents in incredibly expedited timeframe Interrogatories similar to litigation Investigational hearing similar to deposition; no objections Ending a CFPB Investigation Public Consent Order, litigation, no action 8

9 Cost of a CFPB Investigation Both financial and public relations concerns Third Party Environment - Before and After Before Audits conducted yearly Minimal oversight from clients Agency Guide and FDCPA up to agency to interpret and oversee Financial performance key driver of incentive and relationship status Inadvertent encouragement of UDAAP issues and violations Inconsistency between issuer verticals Marketing based on handshakes and reputation and very little due diligence, in comparison. After Audits conducted as frequently as 7 a year Multi level, microscopic, and in depth Extreme client oversight Scripting Account movement and coding Constant playing field modifications and changing Risk Management, Brand Protection, Customer Experience, and Financial Performance key drivers to incentive and relationship status, respectively. Zero tolerance for UDAAP issues or violations (PPA Example) Consolidation of issuer verticals RFI/RFP due diligence process; opportunistic rate reductions Marketing now keenly based on all of the above Opportunity for organizations that are ahead of the curve and who have embraced the change 9

10 CFPB Compliance Priorities For Debt Collection/Non-Bank Lenders FCRA/Credit Reporting* Validation of Debt (VOD) Time barred debt UDAAP (Unfair Deceptive Acts and Practices) CMS- Compliance Management System Complaint handling procedures Vendor oversight* Executive board review of compliance matters Audits/Remediation CFPB ANPR The CFPB is currently exercising it s rulemaking authority and will soon be issuing new rules in relation to debt collection November 2013: CFPB Released the ANPR 114 Pages, 164 detailed questions Response Deadline: February 28, 2014 Industry does not expect any new rules until Q or Q Covers full gambit of consumer activities 10

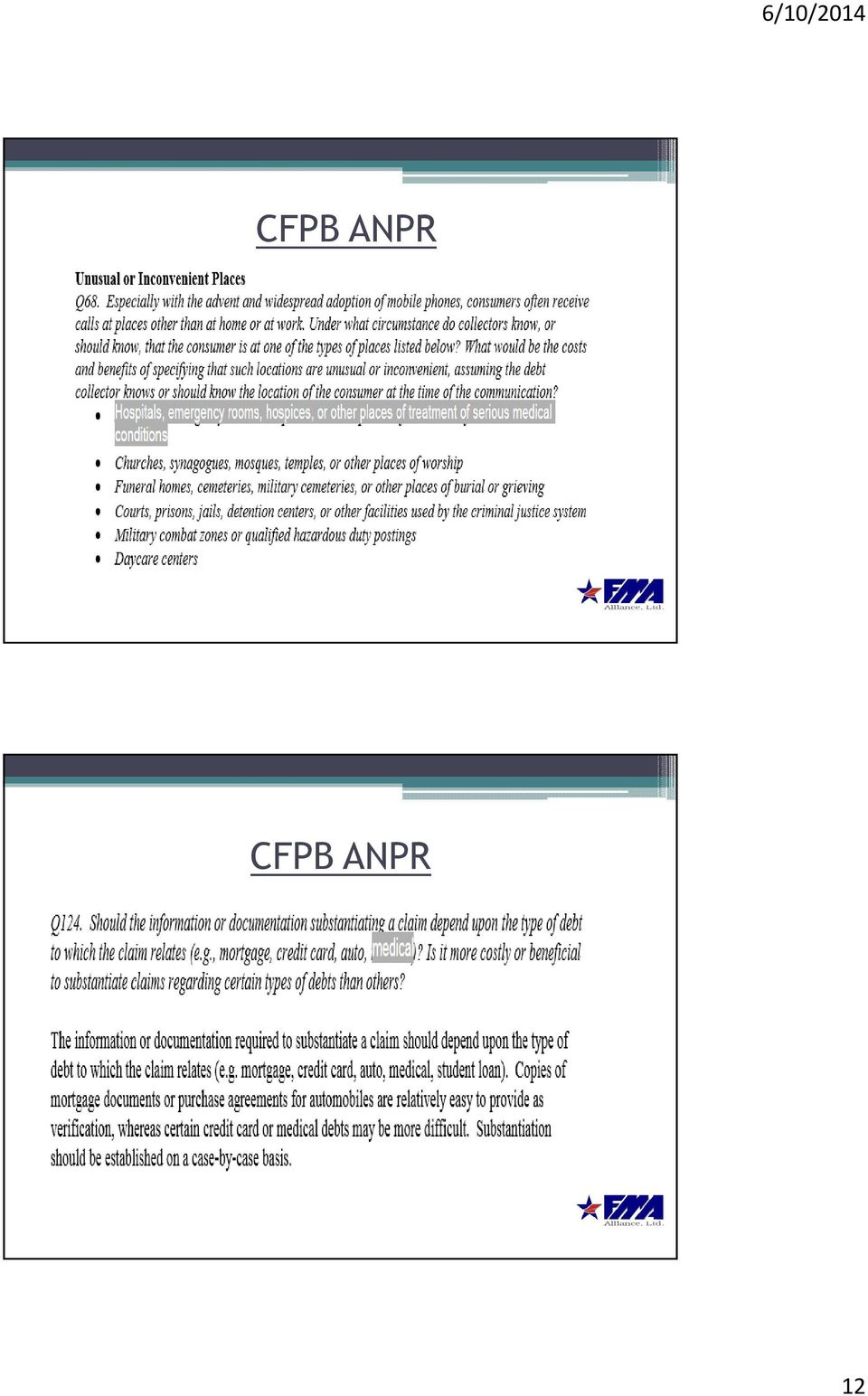

11 CFPB ANPR CFPB ANPR 11

12 CFPB ANPR CFPB ANPR 12

13 Jurisdiction over Medical Debt: Unknown Territory Jurisdiction over Medical Debt: Unknown Territory 13

14 Jurisdiction over Medical Debt: Unknown Territory American Hospital Association stated in response to CFPB: CFPB Readiness Be Ahead of the Curve 14

15 CFPB Enforcement In Healthcare Recent FTC/CFPB Releases: Foreshadowing Regulatory Change 15

16 CFPB Study On Medical Debt & Credit Reporting What Steps Can I Take Now? 1. Look at your internal billing processes and procedures Do you assess interests/fees? Do you have a procedure in place if a patient disputes his bill with the hospital/provider? Are there processes to guarantee all billing codes are entered accurately? Is insurance coverage explained to the patient? 2. Review in-house debt collection practices Do you have a compliance management system in place? What quality control procedures are used? Do you audit your practices? Address patient complaints? 16

17 What Steps Can I Take Now? 3. Assess your third-party debt collection vendors What is your vetting process for vendors? Do you involve your Board of Directors? What audit procedures are in place? What kind of certifications do you require from your vendors? Proof of compliance is key. SSAE-16 ACA PPMS Certification Audited Financials General Counsel/Compliance Team Complaint Procedures Insurance requirements? Questions? 17

CFPB and Medical Collections

CFPB and Medical Collections The Sweeping Regulatory Change Ahead Presented by: Cindy Gagne Legal Disclaimer This information is not intended to be legal advice and may not be used as legal advice. Legal

CFPB and Medical Collections The Sweeping Regulatory Change Ahead Presented by: Cindy Gagne Legal Disclaimer This information is not intended to be legal advice and may not be used as legal advice. Legal

Navigating Consumer Financial Protection Bureau ( CFPB ) Investigations and Enforcement Actions

Investigations and Enforcement Actions") Navigating Consumer Financial Protection Bureau ( CFPB ) Investigations and Enforcement Actions Section of Antitrust Law 2013 Spring Meeting Wednesday, April 10, 2013 Jonathan L. Pompan Partner, Co-Chair

Navigating Consumer Financial Protection Bureau ( CFPB ) Investigations and Enforcement Actions Section of Antitrust Law 2013 Spring Meeting Wednesday, April 10, 2013 Jonathan L. Pompan Partner, Co-Chair

Regulatory Practice Letter January 2013 RPL 13-01

Regulatory Practice Letter January 2013 RPL 13-01 Fair Lending CFPB Annual Report and Supervisory Highlights Executive Summary In December 2012, the Bureau of Consumer Financial Protection ( CFPB or Bureau

Regulatory Practice Letter January 2013 RPL 13-01 Fair Lending CFPB Annual Report and Supervisory Highlights Executive Summary In December 2012, the Bureau of Consumer Financial Protection ( CFPB or Bureau

CFPB Update: Regulatory and Enforcement Developments

CFPB Update: Regulatory and Enforcement Developments December 16, 2014, 12:30 1:30 pm ET American Law Institute Webinar Jonathan L. Pompan Alexandra Megaris 1 Agenda Supervision and Examinations What is

CFPB Update: Regulatory and Enforcement Developments December 16, 2014, 12:30 1:30 pm ET American Law Institute Webinar Jonathan L. Pompan Alexandra Megaris 1 Agenda Supervision and Examinations What is

What Lead Generators Need to Know About the Consumer Financial Protection Bureau (CFPB)

") What Lead Generators Need to Know About the Consumer Financial Protection Bureau (CFPB) LeadsCon March 18, 2013 Mirage Hotel & Casino, Las Vegas, NV Jonathan L. Pompan Venable LLP 1 Agenda for Today What

What Lead Generators Need to Know About the Consumer Financial Protection Bureau (CFPB) LeadsCon March 18, 2013 Mirage Hotel & Casino, Las Vegas, NV Jonathan L. Pompan Venable LLP 1 Agenda for Today What

Client Update CFPB Issues Final Auto Finance Larger Participant Rule and New Auto Finance Examination Procedures

1 Client Update CFPB Issues Final Auto Finance Larger Participant Rule and New Auto Finance Examination Procedures NEW YORK Matthew L. Biben mlbiben@debevoise.com Courtney M. Dankworth cmdankworth@debevoise.com

1 Client Update CFPB Issues Final Auto Finance Larger Participant Rule and New Auto Finance Examination Procedures NEW YORK Matthew L. Biben mlbiben@debevoise.com Courtney M. Dankworth cmdankworth@debevoise.com

Regulatory Practice Letter December 2012 RPL 12-24

Regulatory Practice Letter December 2012 RPL 12-24 CFPB Nonbank Supervision - Larger Participants for Debt Collection and Credit Reporting Final Rules Executive Summary In February 2012, the Bureau of

Regulatory Practice Letter December 2012 RPL 12-24 CFPB Nonbank Supervision - Larger Participants for Debt Collection and Credit Reporting Final Rules Executive Summary In February 2012, the Bureau of

Supervisory Highlights

Supervisory Highlights Spring 2014 Table of contents Table of contents... 2 1. Introduction... 3 2. Supervisory observations... 5 2.1 Consumer reporting... 8 2.2 Debt collection... 11 2.3 Short-term, small-dollar

Supervisory Highlights Spring 2014 Table of contents Table of contents... 2 1. Introduction... 3 2. Supervisory observations... 5 2.1 Consumer reporting... 8 2.2 Debt collection... 11 2.3 Short-term, small-dollar

CFPB COMPLIANCE: Interaction Between Compliance Assessments and Systems Issues

CFPB COMPLIANCE: Interaction Between Compliance Assessments and Systems Issues Presented by: Stefanie H. Jackman Consumer Financial Services Group 678.420.9490 jackmans@ballardspahr.com Trevor Salter Consumer

CFPB COMPLIANCE: Interaction Between Compliance Assessments and Systems Issues Presented by: Stefanie H. Jackman Consumer Financial Services Group 678.420.9490 jackmans@ballardspahr.com Trevor Salter Consumer

Regulatory Practice Letter February 2014 RPL 14-05

Regulatory Practice Letter February 2014 RPL 14-05 CFPB Nonbank Supervision of International Money Transfer Providers Proposed Rule Executive Summary The Consumer Financial Protection Bureau (CFPB or Bureau)

Regulatory Practice Letter February 2014 RPL 14-05 CFPB Nonbank Supervision of International Money Transfer Providers Proposed Rule Executive Summary The Consumer Financial Protection Bureau (CFPB or Bureau)

Regulatory Practice Letter January 2014 RPL 14-03

Regulatory Practice Letter January 2014 RPL 14-03 CFPB Nonbank Supervision of Student Loan Servicers Final Rule CFPB Student Loan Ombudsman - Annual Report Executive Summary Effective March 1, 2014, the

Regulatory Practice Letter January 2014 RPL 14-03 CFPB Nonbank Supervision of Student Loan Servicers Final Rule CFPB Student Loan Ombudsman - Annual Report Executive Summary Effective March 1, 2014, the

Consumer Financial Protection Bureau - An Overview

The Consumer Financial Protection Bureau: An Overview for Campus Officials and Their Vendors Prepared by David Stocker Chair, COHEAO CFPB Task Force February 2014 The Consumer Financial Protection Bureau

The Consumer Financial Protection Bureau: An Overview for Campus Officials and Their Vendors Prepared by David Stocker Chair, COHEAO CFPB Task Force February 2014 The Consumer Financial Protection Bureau

What You Need to Know About the CFPB and Why You Should Care

What You Need to Know About the CFPB and Why You Should Care Thomas A. Brooks Jane C. Luxton Joann Needleman (202) 552-2356 (202) 572-8674 (215) 640-8536 tbrooks@ jluxton@ jneedleman@ Leaders of the Consumer

What You Need to Know About the CFPB and Why You Should Care Thomas A. Brooks Jane C. Luxton Joann Needleman (202) 552-2356 (202) 572-8674 (215) 640-8536 tbrooks@ jluxton@ jneedleman@ Leaders of the Consumer

CFPB Focus. Five Questions to Ask Before January 10, 2014

Five Questions to Ask Before January 10, 2014 Courtney H. Gilmer, 615.726.5747, cgilmer@bakerdonelson.com 1. Compliance Procedures. Have you updated your written policies and procedures for each of your

Five Questions to Ask Before January 10, 2014 Courtney H. Gilmer, 615.726.5747, cgilmer@bakerdonelson.com 1. Compliance Procedures. Have you updated your written policies and procedures for each of your

Student Loan Servicing and the CFPB

Regulatory Practice Letter April 2013 RPL 13-09 CFPB Nonbank Supervision Larger Participants for Student Loan Servicing Proposed Rule Executive Summary The Bureau of Consumer Financial Protection (CFPB

Regulatory Practice Letter April 2013 RPL 13-09 CFPB Nonbank Supervision Larger Participants for Student Loan Servicing Proposed Rule Executive Summary The Bureau of Consumer Financial Protection (CFPB

Military Lending Basics

Military Lending Basics ABA Business Law Section Meeting Consumer Financial Services Committee Wednesday, April 15, 2015 Joseph J. Schuster Consumer Financial Services Group 215.864.8614 furlettim@ballardspahr.com

Military Lending Basics ABA Business Law Section Meeting Consumer Financial Services Committee Wednesday, April 15, 2015 Joseph J. Schuster Consumer Financial Services Group 215.864.8614 furlettim@ballardspahr.com

Supervisory Highlights. Summer 2013

Supervisory Highlights Summer 2013 Table of Contents 1. Introduction... 3 2. Supervisory Observations... 5 2.1 Compliance Management Systems... 5 2.2 Mortgage Servicing... 11 2.3 Fair Lending Provision

Supervisory Highlights Summer 2013 Table of Contents 1. Introduction... 3 2. Supervisory Observations... 5 2.1 Compliance Management Systems... 5 2.2 Mortgage Servicing... 11 2.3 Fair Lending Provision

Compliance Bulletin and Policy Guidance: Mortgage Servicing Transfers

1700 G Street, N.W., Washington, DC 20552 Bulletin 2014-01 Date: August 19, 2014 Subject: Compliance Bulletin and Policy Guidance: Mortgage Servicing Transfers The Bureau of Consumer Financial Protection

1700 G Street, N.W., Washington, DC 20552 Bulletin 2014-01 Date: August 19, 2014 Subject: Compliance Bulletin and Policy Guidance: Mortgage Servicing Transfers The Bureau of Consumer Financial Protection

Minimizing Legal and Compliance Risk for Credit Furnishers

Minimizing Legal and Compliance Risk for Credit Furnishers Wednesday, November 18, 2015 2:00 p.m. 3:00 p.m. EST Webinar Speakers Jonathan L. Pompan, Esq., Partner and Co-Chair Consumer Financial Protection

Minimizing Legal and Compliance Risk for Credit Furnishers Wednesday, November 18, 2015 2:00 p.m. 3:00 p.m. EST Webinar Speakers Jonathan L. Pompan, Esq., Partner and Co-Chair Consumer Financial Protection

The CFPB's 'UDAAPification' Of Consumer Protection Law

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com The CFPB's 'UDAAPification' Of Consumer Protection

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com The CFPB's 'UDAAPification' Of Consumer Protection

The Other Side of CFPB Compliance

The Other Side of CFPB Compliance Strengthening your compliance program via vendor management Legal Disclaimer This information is for the use of attendees only. Any distribution, reproduction, copying

The Other Side of CFPB Compliance Strengthening your compliance program via vendor management Legal Disclaimer This information is for the use of attendees only. Any distribution, reproduction, copying

Table of Contents... 1. Chapter 1 Introduction... 5. 1.1 Goals & Objectives... 5 1.2 Required Review... 5 1.3 Applicability...

... 1 Chapter 1 Introduction... 5 1.1 Goals & Objectives... 5 1.2 Required Review... 5 1.3 Applicability... 5 Chapter 2 Company Culture... 6 Chapter 3 Risk Management Governance... 7 3.1 Board of Directors...

... 1 Chapter 1 Introduction... 5 1.1 Goals & Objectives... 5 1.2 Required Review... 5 1.3 Applicability... 5 Chapter 2 Company Culture... 6 Chapter 3 Risk Management Governance... 7 3.1 Board of Directors...

Navigating the Consumer Financial Protection Bureau. kpmg.com

Navigating the Consumer Financial Protection Bureau kpmg.com Contents 01 CFPB examination and enforcement Are you prepared? 02 Everything you need to know about the CFPB 03 Helping your business navigate

Navigating the Consumer Financial Protection Bureau kpmg.com Contents 01 CFPB examination and enforcement Are you prepared? 02 Everything you need to know about the CFPB 03 Helping your business navigate

2014 Financial Services Industry Compliance Benchmark Study

2014 Financial Services Industry Compliance Benchmark Study Presented By: and Executive Summary Beginning in early December 2013, SAI Global Compliance conducted a survey among compliance professionals

2014 Financial Services Industry Compliance Benchmark Study Presented By: and Executive Summary Beginning in early December 2013, SAI Global Compliance conducted a survey among compliance professionals

Payment Systems: Regulatory Interest in Payment Processors, Faster Payments, and Related Consumer Protections

July 2015 RPL15-04 Payment Systems: Regulatory Interest in Payment Processors, Faster Payments, and Related Consumer Protections Executive Summary The expansion of the Internet and the growth in electronic

July 2015 RPL15-04 Payment Systems: Regulatory Interest in Payment Processors, Faster Payments, and Related Consumer Protections Executive Summary The expansion of the Internet and the growth in electronic

The Consumer Financial Protection Bureau (CFPB): Purpose & Function Federal Reserve Bank of Boston 22 March 2011

: Purpose & Function Federal Reserve Bank of Boston 22 March 2011") The Consumer Financial Protection Bureau (CFPB): Purpose & Function Federal Reserve Bank of Boston 22 March 2011 Susanna Montezemolo Center for Responsible Lending susanna.montezemolo@responsiblelending.org

The Consumer Financial Protection Bureau (CFPB): Purpose & Function Federal Reserve Bank of Boston 22 March 2011 Susanna Montezemolo Center for Responsible Lending susanna.montezemolo@responsiblelending.org

Overview of Financial Products and Consumer Protections

Overview of Financial Products and Consumer Protections Presented by the Consumer and Mortgage Lending Division, House Financial Institutions Committee January 23, 2014 Role of the CML Division The Consumer

Overview of Financial Products and Consumer Protections Presented by the Consumer and Mortgage Lending Division, House Financial Institutions Committee January 23, 2014 Role of the CML Division The Consumer

Evolving Legal and Regulatory Landscape for Lead Generation

Evolving Legal and Regulatory Landscape for Lead Generation LeadsCon 2012 February 27, 2012 The Mirage Resort & Casino, Las Vegas, NV Jonathan L. Pompan, Esq. Venable LLP, Washington, DC 1 IMPORTANT INFORMATION

Evolving Legal and Regulatory Landscape for Lead Generation LeadsCon 2012 February 27, 2012 The Mirage Resort & Casino, Las Vegas, NV Jonathan L. Pompan, Esq. Venable LLP, Washington, DC 1 IMPORTANT INFORMATION

The Consumer Financial Protection Bureau - A History

Consumer Financial Protection Bureau Two Years In and Just Beginning the Baby Steps By Thomas J. King, Standing Chapter 13 Trustee for the Eastern District of Wisconsin The Consumer Financial Protection

Consumer Financial Protection Bureau Two Years In and Just Beginning the Baby Steps By Thomas J. King, Standing Chapter 13 Trustee for the Eastern District of Wisconsin The Consumer Financial Protection

Importance of the Consumer Financial Protection Bureau

Importance of the Consumer Financial Protection Bureau The aftermath of the financial crisis affected millions of Americans. The U.S. economy was devastated as companies crumbled, homeowners lost their

Importance of the Consumer Financial Protection Bureau The aftermath of the financial crisis affected millions of Americans. The U.S. economy was devastated as companies crumbled, homeowners lost their

Takeaways From GE Capital's $225M Credit Card Settlement

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com Takeaways From GE Capital's $225M Credit Card Settlement

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com Takeaways From GE Capital's $225M Credit Card Settlement

Fair Lending Report of the Consumer Financial Protection Bureau

Fair Lending Report of the Consumer Financial Protection Bureau April 2015 Message from Richard Cordray Director of the CFPB The Consumer Financial Protection Bureau (the Bureau or CFPB) is the nation

Fair Lending Report of the Consumer Financial Protection Bureau April 2015 Message from Richard Cordray Director of the CFPB The Consumer Financial Protection Bureau (the Bureau or CFPB) is the nation

Collections After Compliance. The Changing Landscape. An Experian Perspective

Collections After Compliance The Changing Landscape An Experian Perspective The current financial situation is a result of many factors, including the actions of both large and small financial institutions,

Collections After Compliance The Changing Landscape An Experian Perspective The current financial situation is a result of many factors, including the actions of both large and small financial institutions,

THE LEAD GENERATION COMPANY: MANAGING THE RISKS. Jonathan Foxx *

THE LEAD GENERATION COMPANY: MANAGING THE RISKS Jonathan Foxx * Generating leads is an important way to reach consumers. It is also fraught with regulatory risk. A lead is consumer information that signals

THE LEAD GENERATION COMPANY: MANAGING THE RISKS Jonathan Foxx * Generating leads is an important way to reach consumers. It is also fraught with regulatory risk. A lead is consumer information that signals

Regulatory Practice Letter May 2014 RPL 14-09

Regulatory Practice Letter May 2014 RPL 14-09 Payday Lending CFPB Data Point Report Executive Summary The Consumer Financial Protection Bureau (CFPB or Bureau) recently released a report presenting the

Regulatory Practice Letter May 2014 RPL 14-09 Payday Lending CFPB Data Point Report Executive Summary The Consumer Financial Protection Bureau (CFPB or Bureau) recently released a report presenting the

COMPLIANCE MANAGEMENT SYSTEM

COMPLIANCE MANAGEMENT SYSTEM Ensuring Your Bank Meets Regulatory Standards Overview of Compliance Exams Examination Purpose: Assess the quality of an institution s compliance management system (CMS) for

COMPLIANCE MANAGEMENT SYSTEM Ensuring Your Bank Meets Regulatory Standards Overview of Compliance Exams Examination Purpose: Assess the quality of an institution s compliance management system (CMS) for

Regulatory Practice Letter May 2013 RPL 13-10

Regulatory Practice Letter May 2013 RPL 13-10 Senior Designations for Financial Advisers- CFPB Report Executive Summary The Bureau of Consumer Financial Protection s (CFPB or Bureau) Office of Financial

Regulatory Practice Letter May 2013 RPL 13-10 Senior Designations for Financial Advisers- CFPB Report Executive Summary The Bureau of Consumer Financial Protection s (CFPB or Bureau) Office of Financial

CFSA Compliance School, Part II: Implementing an Effective Compliance Management System

CFSA Compliance School, Part II: Implementing an Effective Compliance Management System Michelle Hemerley Managing Director FIS Enterprise Governance, Risk & Compliance (EGRC) SoluBon February 2014 Overview

CFSA Compliance School, Part II: Implementing an Effective Compliance Management System Michelle Hemerley Managing Director FIS Enterprise Governance, Risk & Compliance (EGRC) SoluBon February 2014 Overview

VII 4.1. VII. Unfair and Deceptive Practices Third Party Risk. Third Party Risk. Introduction. Background

Third Party Risk Introduction The board of directors and senior management of an insured depository institution (institution) are ultimately responsible for managing activities conducted through third-party

Third Party Risk Introduction The board of directors and senior management of an insured depository institution (institution) are ultimately responsible for managing activities conducted through third-party

Notwithstanding little guidance from the CFPB, expect more UDAAP enforcement actions now that the presidential election is over

Notwithstanding little guidance from the CFPB, expect more UDAAP enforcement actions now that the presidential election is over By Martin J. Bishop and Rebecca R. Hanson Thomson Reuters News & Insight

Notwithstanding little guidance from the CFPB, expect more UDAAP enforcement actions now that the presidential election is over By Martin J. Bishop and Rebecca R. Hanson Thomson Reuters News & Insight

Mortgage Banking. Solutions in Compliance, Transactions, and Defense. Attorney Advertising

Mortgage Banking Solutions in Compliance, Transactions, and Defense Attorney Advertising The mortgage banking industry is changing rapidly. We offer broad regulatory experience, formidable skill in litigation,

Mortgage Banking Solutions in Compliance, Transactions, and Defense Attorney Advertising The mortgage banking industry is changing rapidly. We offer broad regulatory experience, formidable skill in litigation,

GUIDANCE FOR MANAGING THIRD-PARTY RISK

GUIDANCE FOR MANAGING THIRD-PARTY RISK Introduction An institution s board of directors and senior management are ultimately responsible for managing activities conducted through third-party relationships,

GUIDANCE FOR MANAGING THIRD-PARTY RISK Introduction An institution s board of directors and senior management are ultimately responsible for managing activities conducted through third-party relationships,

Consumer Protection and Regulatory Changes in the Dodd-Frank Bill

31 August 2010 Part II of A NERA Insights Series Consumer Protection and Regulatory Changes in the Dodd-Frank Bill By Dr. Ethan Cohen-Cole Summary On 21 July 2010, President Obama signed into law the Dodd-Frank

31 August 2010 Part II of A NERA Insights Series Consumer Protection and Regulatory Changes in the Dodd-Frank Bill By Dr. Ethan Cohen-Cole Summary On 21 July 2010, President Obama signed into law the Dodd-Frank

Short-Term, Small-Dollar Lending

Commonly Known as Payday Lending Exam Date: Prepared By: Reviewer: Docket #: Entity Name: [Click&type] [Click&type] [Click&type] [Click&type] [Click&type] These examination procedures apply to the short-term,

Commonly Known as Payday Lending Exam Date: Prepared By: Reviewer: Docket #: Entity Name: [Click&type] [Click&type] [Click&type] [Click&type] [Click&type] These examination procedures apply to the short-term,

Vendor Risk Management in the New Regulatory Environment. kpmg.com

Vendor Risk Management in the New Regulatory Environment kpmg.com Vendor Risk Management in the New Regulatory Environment 2 Vendor Risk Management in the New Regulatory Environment Background Regulators

Vendor Risk Management in the New Regulatory Environment kpmg.com Vendor Risk Management in the New Regulatory Environment 2 Vendor Risk Management in the New Regulatory Environment Background Regulators

Any business relationship between a bank and another entity, by contract or otherwise

An Overview for Bank Directors Managing the Third Party Relationship Patrick Neuman Boardman & Clark LLP Madison, Wisconsin Any business relationship between a bank and another entity, by contract or otherwise

An Overview for Bank Directors Managing the Third Party Relationship Patrick Neuman Boardman & Clark LLP Madison, Wisconsin Any business relationship between a bank and another entity, by contract or otherwise

Reverse Due Diligence A New Trend In Financial M&A

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com Reverse Due Diligence A New Trend In Financial M&A

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com Reverse Due Diligence A New Trend In Financial M&A

Recent Developments: Consumer Financial Protection Bureau

Recent Developments: Consumer Financial Protection Bureau The Banking Institute University of North Carolina School of Law Center for Banking and Finance March 30, 2012 Reginald J. Brown Eric J. Mogilnicki

Recent Developments: Consumer Financial Protection Bureau The Banking Institute University of North Carolina School of Law Center for Banking and Finance March 30, 2012 Reginald J. Brown Eric J. Mogilnicki

UNFAIR, DECEPTIVE, OR ABUSIVE ACTS OR PRACTICES (UDAAP)

") UNFAIR, DECEPTIVE, OR ABUSIVE ACTS OR PRACTICES (UDAAP) EXAMINATION PROCEDURES Examination Objectives To assess the quality of the credit union s compliance risk management systems, including internal

UNFAIR, DECEPTIVE, OR ABUSIVE ACTS OR PRACTICES (UDAAP) EXAMINATION PROCEDURES Examination Objectives To assess the quality of the credit union s compliance risk management systems, including internal

VII 5.1. VII. Abusive Practices Third Party Procedures. Third Party Risk. Introduction. Background

Third Party Risk Introduction The board of directors and senior management of an insured depository institution (institution) are ultimately responsible for managing activities conducted through third-party

Third Party Risk Introduction The board of directors and senior management of an insured depository institution (institution) are ultimately responsible for managing activities conducted through third-party

First Actions of the Consumer Financial Protection Bureau

2013-2014 DEVELOPMENTS IN BANKING LAW 453 IV. First Actions of the Consumer Financial Protection Bureau A. Introduction The Consumer Financial Protection Bureau ( CFPB ) was formed in 2011, pursuant to

2013-2014 DEVELOPMENTS IN BANKING LAW 453 IV. First Actions of the Consumer Financial Protection Bureau A. Introduction The Consumer Financial Protection Bureau ( CFPB ) was formed in 2011, pursuant to

VII 3.1. VII. Unfair and Deceptive Practices FDCPA. Fair Debt Collection Practices Act. Introduction. Communications Connected with Debt Collection

Fair Debt Collection Practices Act Introduction The Fair Debt Collection Practices Act (FDCPA), effective in 1978, was designed to eliminate abusive, deceptive, and unfair debt collection practices. The

Fair Debt Collection Practices Act Introduction The Fair Debt Collection Practices Act (FDCPA), effective in 1978, was designed to eliminate abusive, deceptive, and unfair debt collection practices. The

The Fair Credit Reporting Act (FCRA) and the Fair Debt Collection Practices Act (FDCPA)

and the Fair Debt Collection Practices Act (FDCPA)") The Fair Credit Reporting Act (FCRA) and the Fair Debt Collection Practices Act (FDCPA) Addressing Medical Debt: Developing Best Practices for Providers and Patients June 18, 2009 Leonard L. Gordon The

The Fair Credit Reporting Act (FCRA) and the Fair Debt Collection Practices Act (FDCPA) Addressing Medical Debt: Developing Best Practices for Providers and Patients June 18, 2009 Leonard L. Gordon The

DOL Whistleblower Rule Will Have Far-Reaching Effects

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com DOL Whistleblower Rule Will Have Far-Reaching Effects

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com DOL Whistleblower Rule Will Have Far-Reaching Effects

Dodd Frank Act Consumer Financial Protection Bureau Mortgage Lending

Dodd Frank Act Consumer Financial Protection Bureau Mortgage Lending A Briefing for the Texas House Investments and Financial Services Committee John C. Fleming Consumer Financial Protection Bureau (CFPB)

Dodd Frank Act Consumer Financial Protection Bureau Mortgage Lending A Briefing for the Texas House Investments and Financial Services Committee John C. Fleming Consumer Financial Protection Bureau (CFPB)

CFPB Examination Procedures

Commonly Known as Payday Lending These examination procedures apply to the short-term, small-dollar credit market, commonly known as payday lending. The procedures are comprised of modules covering a payday

Commonly Known as Payday Lending These examination procedures apply to the short-term, small-dollar credit market, commonly known as payday lending. The procedures are comprised of modules covering a payday

REQUEST FOR PROPOSALS for Authorized Providers of Continuing Education Credits

REQUEST FOR PROPOSALS for Authorized Providers of Continuing Education Credits RFP ISSUANCE: January 22, 2015 PROPOSAL DUE DATE: Open Submittal I. ABOUT DBA INTERNATIONAL DBA International (DBA) is the

REQUEST FOR PROPOSALS for Authorized Providers of Continuing Education Credits RFP ISSUANCE: January 22, 2015 PROPOSAL DUE DATE: Open Submittal I. ABOUT DBA INTERNATIONAL DBA International (DBA) is the

Managing specialty finance compliance requirements with a compliance management system

Managing specialty finance compliance requirements with a compliance management system Prepared by: Andrew Amrine, Supervisor, RSM US LLP andrew.amrine@rsmus.com, +1 253 382 2239 September 2013 For over

Managing specialty finance compliance requirements with a compliance management system Prepared by: Andrew Amrine, Supervisor, RSM US LLP andrew.amrine@rsmus.com, +1 253 382 2239 September 2013 For over

Regulatory Impact on Agencies & How They Affect You, The Client

Regulatory Impact on Agencies & How They Affect You, The Client Regulatory Impact on Agencies & How They Affect You, The Client Presented By: Thomas Perrotta, V.P. Collections & Compliance, CCCO Presentation

Regulatory Impact on Agencies & How They Affect You, The Client Regulatory Impact on Agencies & How They Affect You, The Client Presented By: Thomas Perrotta, V.P. Collections & Compliance, CCCO Presentation

Vendor Management: Who the CFPB is Watching and Who They Are Expecting You to be Watching

Vendor Management: Who the CFPB is Watching and Who They Are Expecting You to be Watching John Barnes 713.210.7441 jbarnes@bakerdonelson.com Jessica Hinkie 713.210.7405 jhinkie@bakerdonelson.com Kat Statman

Vendor Management: Who the CFPB is Watching and Who They Are Expecting You to be Watching John Barnes 713.210.7441 jbarnes@bakerdonelson.com Jessica Hinkie 713.210.7405 jhinkie@bakerdonelson.com Kat Statman

Banking Agencies. Federal Banking Agencies

The Consumer Financial Protection Bureau and the State Attorneys General: A Force Multiplier in Consumer Protection Matters, Contri...Page 1 Bloomberg Law Reports May 25, 2011 Banking Agencies Federal

The Consumer Financial Protection Bureau and the State Attorneys General: A Force Multiplier in Consumer Protection Matters, Contri...Page 1 Bloomberg Law Reports May 25, 2011 Banking Agencies Federal

Who s Your Vendor? Secondary Market Compliance and Title Agent Vendor Management

Who s Your Vendor? Secondary Market Compliance and Title Agent Vendor Management 2015 LBA Bank Counsel Conference Marx Sterbcow, Managing Attorney, Sterbcow Law Group The Bureau s Scrutiny of Vendor Management

Who s Your Vendor? Secondary Market Compliance and Title Agent Vendor Management 2015 LBA Bank Counsel Conference Marx Sterbcow, Managing Attorney, Sterbcow Law Group The Bureau s Scrutiny of Vendor Management

The Consumer Financial Protection Bureau:

The Consumer Financial Protection Bureau: The Government s Increased Role in Consumer Protection Laws Andrew C. Sayles Connell Foley LLP 85 Livingston Ave. Roseland, NJ 07068 (973) 535-0500 asayles@connellfoley.com

The Consumer Financial Protection Bureau: The Government s Increased Role in Consumer Protection Laws Andrew C. Sayles Connell Foley LLP 85 Livingston Ave. Roseland, NJ 07068 (973) 535-0500 asayles@connellfoley.com

Washington Update. Payments News from our Nation s Capital. October 2014. Contents. CFPB Finalizes Two Rules Related to International Money Transfers

Washington Update Payments News from our Nation s Capital October 2014 Contents CFPB Finalizes Two Rules Related to International Money Transfers $25 per Issue $200 Annual Subscription Authors: Craig Saperstein

Washington Update Payments News from our Nation s Capital October 2014 Contents CFPB Finalizes Two Rules Related to International Money Transfers $25 per Issue $200 Annual Subscription Authors: Craig Saperstein

Susan Costonis, C.R.C.M. Compliance Training & Consulting for Financial Institutions

The Directors Education Series Fair Lending Training for the Board of Directors Part I Presented by: Susan Costonis, C.R.C.M. Compliance Training & Consulting for Financial Institutions YOUR PRESENTER

The Directors Education Series Fair Lending Training for the Board of Directors Part I Presented by: Susan Costonis, C.R.C.M. Compliance Training & Consulting for Financial Institutions YOUR PRESENTER

VIRGINIA ASSOCIATION OF COMMUNITY BANKS

VIRGINIA ASSOCIATION OF COMMUNITY BANKS Spring Internal Audit / Risk Seminar Presented by Lee G. Lester May 26, 2016 Regulatory Hot Topics > De-Risking > Marketplace Lending > Consumer protection initiatives

VIRGINIA ASSOCIATION OF COMMUNITY BANKS Spring Internal Audit / Risk Seminar Presented by Lee G. Lester May 26, 2016 Regulatory Hot Topics > De-Risking > Marketplace Lending > Consumer protection initiatives

Financial Services Update June 11, 2013

Financial Services Update June 11, 2013 HIGHLIGHTS Federal Regulatory Developments: CFPB Amends Examination Manual State Regulatory Developments: Texas Proposes Constitutional Amendment Regarding Reverse

Financial Services Update June 11, 2013 HIGHLIGHTS Federal Regulatory Developments: CFPB Amends Examination Manual State Regulatory Developments: Texas Proposes Constitutional Amendment Regarding Reverse

To: Our Clients and Friends March 25, 2014

Financial Services Group To: Our Clients and Friends March 25, 2014 A Significant Change Is Occurring Regarding Regulatory Oversight of Banks and Their Third Party Relationships. Both Banks and their Vendors

Financial Services Group To: Our Clients and Friends March 25, 2014 A Significant Change Is Occurring Regarding Regulatory Oversight of Banks and Their Third Party Relationships. Both Banks and their Vendors

Defining Larger Participants of the International Money Transfer Market Docket No. CFPB-2014-0003/RIN 3170-AA25

Robert G. Rowe, III Vice President/Senior Counsel Center for Regulatory Compliance Phone: 202-663-5029 E-mail: rrowe@aba.com April 1, 2014 Monica Jackson Office of the Executive Secretary Bureau of Consumer

Robert G. Rowe, III Vice President/Senior Counsel Center for Regulatory Compliance Phone: 202-663-5029 E-mail: rrowe@aba.com April 1, 2014 Monica Jackson Office of the Executive Secretary Bureau of Consumer

FAQs about ALTA Best Practices for Real Estate Settlement Attorneys and Title Companies

Why do I need to have ALTA Best Practices policies and procedures in place and have a CPA give assurance on my compliance to mortgage lenders? In accordance with Consumer Financial Protection Bureau (CFPB)

Why do I need to have ALTA Best Practices policies and procedures in place and have a CPA give assurance on my compliance to mortgage lenders? In accordance with Consumer Financial Protection Bureau (CFPB)

Fortifying the Three Lines of Defense to Combat Compliance Risk

Fortifying the Three Lines of Defense to Combat Compliance Risk Today s Presenters Thomas Grundy CRCM, Senior Regulatory Consultant, Wolters Kluwer 30 years regulatory/compliance experience: OCC and Federal

Fortifying the Three Lines of Defense to Combat Compliance Risk Today s Presenters Thomas Grundy CRCM, Senior Regulatory Consultant, Wolters Kluwer 30 years regulatory/compliance experience: OCC and Federal

Fair Lending, UDAAP and CRA: Protecting Your Bank from Allegations of Fair and Responsible Lending Violations

Fair Lending, UDAAP and CRA: Protecting Your Bank from Allegations of Fair and Responsible Lending Violations Albany, NY April 23, 2015 Legal Counsel to the Financial Services Industry Presented by Warren

Fair Lending, UDAAP and CRA: Protecting Your Bank from Allegations of Fair and Responsible Lending Violations Albany, NY April 23, 2015 Legal Counsel to the Financial Services Industry Presented by Warren

Where Are You? Strategies for Locating Borrowers

Where Are You? Strategies for Locating Borrowers Borrowers that do not have current contact information with the lender/servicer These borrowers cannot always be easily found 50-60% of borrowers who default

Where Are You? Strategies for Locating Borrowers Borrowers that do not have current contact information with the lender/servicer These borrowers cannot always be easily found 50-60% of borrowers who default

The CFPB focuses on mobile phone carrier payment processing If you think you are not a Financial Services Company You may want to think again

www.pwc.com/consumerfinance www.pwcregulatory.com The CFPB focuses on mobile phone carrier payment processing If you think you are not a Financial Services Company You may want to think again January 2015

www.pwc.com/consumerfinance www.pwcregulatory.com The CFPB focuses on mobile phone carrier payment processing If you think you are not a Financial Services Company You may want to think again January 2015

CFPB and Lenders. A presentation on the Consumer Financial Protection Bureau and its impact on the lending industry

CFPB and Lenders A presentation on the Consumer Financial Protection Bureau and its impact on the lending industry What is the Consumer Financial Protection Bureau (CFPB)? Independent agency of the United

CFPB and Lenders A presentation on the Consumer Financial Protection Bureau and its impact on the lending industry What is the Consumer Financial Protection Bureau (CFPB)? Independent agency of the United

Compliance Management Systems (CMS) Division of Depositor and Consumer Protection

Division of Depositor and Consumer Protection") Compliance Management Systems (CMS) What is a Compliance Management System (CMS)? A CMS is how an institution: Learns about its compliance responsibilities Ensures that employees understand these responsibilities

Compliance Management Systems (CMS) What is a Compliance Management System (CMS)? A CMS is how an institution: Learns about its compliance responsibilities Ensures that employees understand these responsibilities

Regulatory Practice Letter September 2012 RPL 12-17

Regulatory Practice Letter September 2012 RPL 12-17 Mortgage Servicing Standards - CFPB Proposed Rule Executive Summary The Bureau of Consumer Financial Protection ( CFBP or Bureau ) released two proposed

Regulatory Practice Letter September 2012 RPL 12-17 Mortgage Servicing Standards - CFPB Proposed Rule Executive Summary The Bureau of Consumer Financial Protection ( CFBP or Bureau ) released two proposed

CFPB BULLETIN 2014-02 Date: September 3, 2014 Subject: Marketing of Credit Card Promotional APR Offers

1700 G Street, N.W., Washington, DC 20552 CFPB BULLETIN 2014-02 Date: September 3, 2014 Subject: Marketing of Credit Card Promotional APR Offers The Consumer Financial Protection Bureau (CFPB or Bureau)

1700 G Street, N.W., Washington, DC 20552 CFPB BULLETIN 2014-02 Date: September 3, 2014 Subject: Marketing of Credit Card Promotional APR Offers The Consumer Financial Protection Bureau (CFPB or Bureau)

Office of Inspector General Evaluation of the Consumer Financial Protection Bureau s Consumer Response Unit

Office of Inspector General Evaluation of the Consumer Financial Protection Bureau s Consumer Response Unit Consumer Financial Protection Bureau September 2012 September 28, 2012 MEMORANDUM TO: FROM: SUBJECT:

Office of Inspector General Evaluation of the Consumer Financial Protection Bureau s Consumer Response Unit Consumer Financial Protection Bureau September 2012 September 28, 2012 MEMORANDUM TO: FROM: SUBJECT:

The Consumer Financial Protection Bureau: What It Is and What to Expect

The Consumer Financial Protection Bureau: What It Is and What to Expect January 2012 On January 4, President Obama, via a recess appointment, installed Richard Cordray as the Director of the Consumer Financial

The Consumer Financial Protection Bureau: What It Is and What to Expect January 2012 On January 4, President Obama, via a recess appointment, installed Richard Cordray as the Director of the Consumer Financial

Short-Term Lenders Face Costly Path To Compliance

Portfolio Media. Inc. 111 West 19 th Street, 5th Floor New York, NY 10011 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com Short-Term Lenders Face Costly Path To Compliance

Portfolio Media. Inc. 111 West 19 th Street, 5th Floor New York, NY 10011 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com Short-Term Lenders Face Costly Path To Compliance

Association of Insurance Compliance Professionals Gulf States Chapter E-Day 2014

Association of Insurance Compliance Professionals Gulf States Chapter E-Day 2014 Consumer Financial Protection Bureau s Encroachment into the Insurance Industry What You Need to Know June 13, 2014 Brian

Association of Insurance Compliance Professionals Gulf States Chapter E-Day 2014 Consumer Financial Protection Bureau s Encroachment into the Insurance Industry What You Need to Know June 13, 2014 Brian

New Loan Origination and Mortgage Servicing Rules

5/15/ New Loan Origination and Mortgage Servicing Rules Personal Finance Seminar for Professionals University of Maryland Extension Presenter: Diane Cipollone, Esq. Director of Training National Fair Housing

5/15/ New Loan Origination and Mortgage Servicing Rules Personal Finance Seminar for Professionals University of Maryland Extension Presenter: Diane Cipollone, Esq. Director of Training National Fair Housing

Fair Debt Collection Practices Act

Fair Debt Collection Practices Act CFPB Annual Report 2014 1 MA R C H 2 0, 2 0 14 Message from Richard Cordray Director of the CFPB On July 21, 2011, the Consumer Financial Protection Bureau was launched

Fair Debt Collection Practices Act CFPB Annual Report 2014 1 MA R C H 2 0, 2 0 14 Message from Richard Cordray Director of the CFPB On July 21, 2011, the Consumer Financial Protection Bureau was launched

Fair Debt Collection Practices Act 1

Fair Debt Collection Practices Act 1 The Fair Debt Collection Practices Act (FDCPA)(15 U.S.C. 1692 et seq.), which became effective March 20, 1978, was designed to eliminate abusive, deceptive, and unfair

Fair Debt Collection Practices Act 1 The Fair Debt Collection Practices Act (FDCPA)(15 U.S.C. 1692 et seq.), which became effective March 20, 1978, was designed to eliminate abusive, deceptive, and unfair

Fair Debt Collection Practices Act

Fair Debt Collection Practices Act CFPB Annual Report 2014 1 MA R C H 2 0, 2 0 14 Message from Richard Cordray Director of the CFPB On July 21, 2011, the Consumer Financial Protection Bureau was launched

Fair Debt Collection Practices Act CFPB Annual Report 2014 1 MA R C H 2 0, 2 0 14 Message from Richard Cordray Director of the CFPB On July 21, 2011, the Consumer Financial Protection Bureau was launched

The final rule has expanded the scope of covered products how does this impact your business?

January 2016 Military Lending Act It s time to get prepared The final rule has expanded the scope of covered products how does this impact your business? Overview A joint point of view by PwC s Consumer

January 2016 Military Lending Act It s time to get prepared The final rule has expanded the scope of covered products how does this impact your business? Overview A joint point of view by PwC s Consumer

CONSUMER COMPLAINT MANAGEMENT: MEETING REGULATORY EXPECTATIONS

Vol. 28 No. 10 October 2012 CONSUMER COMPLAINT MANAGEMENT: MEETING REGULATORY EXPECTATIONS The CFPB has identified consumer complaint data as a valuable tool in informing its consumer protection duties.

Vol. 28 No. 10 October 2012 CONSUMER COMPLAINT MANAGEMENT: MEETING REGULATORY EXPECTATIONS The CFPB has identified consumer complaint data as a valuable tool in informing its consumer protection duties.

Privacy of Consumer Financial Information

Background and Overview Introduction Title V, Subtitle A of the Gramm-Leach-Bliley Act ( GLBA ) 1 governs the treatment of nonpublic personal information about consumers by financial institutions. Section

Background and Overview Introduction Title V, Subtitle A of the Gramm-Leach-Bliley Act ( GLBA ) 1 governs the treatment of nonpublic personal information about consumers by financial institutions. Section

Consumer Financial Protection Bureau Strategic Plan

April 2013 Consumer Financial Protection Bureau Strategic Plan FY 2013 - FY 2017 Table of Contents Table of Contents... 2 Overview of the CFPB... 4 Plan Overview... 8 Goal 1... 9 Outcome 1.1: Create, adopt,

April 2013 Consumer Financial Protection Bureau Strategic Plan FY 2013 - FY 2017 Table of Contents Table of Contents... 2 Overview of the CFPB... 4 Plan Overview... 8 Goal 1... 9 Outcome 1.1: Create, adopt,

DODD-FRANK AND THE FUTURE ROLE OF STATE SUPERVISION

DODD-FRANK AND THE FUTURE ROLE OF STATE SUPERVISION WHITE PAPER AUGUST 2010 CONFERENCE OF STATE BANK SUPERVISORS 1155 Connecticut Ave., NW, 5 th Floor Washington DC 20036-4306 (202) 296-2840 www.csbs.org

DODD-FRANK AND THE FUTURE ROLE OF STATE SUPERVISION WHITE PAPER AUGUST 2010 CONFERENCE OF STATE BANK SUPERVISORS 1155 Connecticut Ave., NW, 5 th Floor Washington DC 20036-4306 (202) 296-2840 www.csbs.org

Page 1 of 6 Bassford Bulletin FDCPA/FCRA/ TCPA/CFPB January 22, 2014 Bassford Remele, P.A. 33 South Sixth Street, Suite 3800 Minneapolis, Minnesota 55402 612.333.3000 www.bassford.com Greetings! Welcome

Page 1 of 6 Bassford Bulletin FDCPA/FCRA/ TCPA/CFPB January 22, 2014 Bassford Remele, P.A. 33 South Sixth Street, Suite 3800 Minneapolis, Minnesota 55402 612.333.3000 www.bassford.com Greetings! Welcome

Third-Party Risk Management: Busting Myths and Telling Truths

Third-Party Risk Management: Busting Myths and Telling Truths Richik Sarkar, Esq. McDonald Hopkins LLC 600 Superior Avenue, East, Suite 2100 Cleveland, OH 44114 (216) 430-2009 rsarkar@mcdonaldhopkins.com

Third-Party Risk Management: Busting Myths and Telling Truths Richik Sarkar, Esq. McDonald Hopkins LLC 600 Superior Avenue, East, Suite 2100 Cleveland, OH 44114 (216) 430-2009 rsarkar@mcdonaldhopkins.com

Goldman Sachs Residential Mortgage Servicing Vendor Management Policy Addendum U.S.-Based Program

Goldman Sachs Residential Mortgage Servicing Vendor Management Policy Addendum U.S.-Based Program Effective Date: January 27, 2014 Vendor Management Policy Addendum TABLE OF CONTENTS 1. INTRODUCTION...

Goldman Sachs Residential Mortgage Servicing Vendor Management Policy Addendum U.S.-Based Program Effective Date: January 27, 2014 Vendor Management Policy Addendum TABLE OF CONTENTS 1. INTRODUCTION...

UNITED STATES OF AMERICA CONSUMER FINANCIAL PROTECTION BUREAU. The Consumer Financial Protection Bureau ( Bureau ), through its examiners and other

, through its examiners and other") UNITED STATES OF AMERICA CONSUMER FINANCIAL PROTECTION BUREAU In the Matter of Dealers Financial Services, LLC, Lexington, Kentucky ADMINISTRATIVE PROCEEDING File No. 2013-CFPB-0004 CONSENT ORDER The Consumer

UNITED STATES OF AMERICA CONSUMER FINANCIAL PROTECTION BUREAU In the Matter of Dealers Financial Services, LLC, Lexington, Kentucky ADMINISTRATIVE PROCEEDING File No. 2013-CFPB-0004 CONSENT ORDER The Consumer

Putting the Management Back in Vendor Management February 20, 2014

Putting the Management Back in Vendor Management February 20, 2014 Moderator: Brian O Reilly The Collingwood Group, LLC Panelists: Calvin Hagins, CFPB Ken Markison, MBA Jonathan McKernan, Wilmer Hale Dan

Putting the Management Back in Vendor Management February 20, 2014 Moderator: Brian O Reilly The Collingwood Group, LLC Panelists: Calvin Hagins, CFPB Ken Markison, MBA Jonathan McKernan, Wilmer Hale Dan

CONSUMER FINANCIAL PROTECTION BUREAU THE BASICS

CONSUMER FINANCIAL PROTECTION BUREAU THE BASICS George K. Fogg March 5, 2012 CONSUMER FINANCIAL PROTECTION BUREAU ( CFPB ) Created by Consumer Financial Protection Act of 2010 (Article X of Dodd-Frank)

CONSUMER FINANCIAL PROTECTION BUREAU THE BASICS George K. Fogg March 5, 2012 CONSUMER FINANCIAL PROTECTION BUREAU ( CFPB ) Created by Consumer Financial Protection Act of 2010 (Article X of Dodd-Frank)

SUMMARY OF THE CFPB NOTICE

COMMENTS OF THE TAX PROBLEM RESOLUTION SERVICES COALITION TO THE BUREAU OF CONSUMER FINANCIAL PROTECTION IN CONSIDERATION OF DOCKET NUMBER CFPB-HQ-2011-2 FOR DEFINING LARGER PARTICIPANTS IN CERTAIN CONSUMER

COMMENTS OF THE TAX PROBLEM RESOLUTION SERVICES COALITION TO THE BUREAU OF CONSUMER FINANCIAL PROTECTION IN CONSIDERATION OF DOCKET NUMBER CFPB-HQ-2011-2 FOR DEFINING LARGER PARTICIPANTS IN CERTAIN CONSUMER

Transforming collections operations while maintaining strict regulatory compliance

Transforming collections operations while maintaining strict regulatory compliance A constantly changing regulatory environment makes working with the right technology partner on debt collection and compliance

Transforming collections operations while maintaining strict regulatory compliance A constantly changing regulatory environment makes working with the right technology partner on debt collection and compliance

Guide to Fair Mortgage Lending and Home Preservation

Guide to Fair Mortgage Lending and Home Preservation Fair Housing Legal Support Center & Clinic Guide to Fair Mortgage Lending and Home Preservation What does this guide cover? What is Fair Lending? What

Guide to Fair Mortgage Lending and Home Preservation Fair Housing Legal Support Center & Clinic Guide to Fair Mortgage Lending and Home Preservation What does this guide cover? What is Fair Lending? What