U.S. SMALL BUSINESS ADMINISTRATION OFFICE OF INSPECTOR GENERAL WASHINGTON, D.C

|

|

|

- Willa Francis

- 8 years ago

- Views:

Transcription

1 U.S. SMALL BUSINESS ADMINISTRATION OFFICE OF INSPECTOR GENERAL WASHINGTON, D.C AUDIT REPORT Issue Date: February 28, 2002 Number: 2-07 To: Robert J. Moffitt Associate Administrator, Office of Surety Guarantees From: Subject: Robert G. Seabrooks Assistant Inspector General for Auditing Audit of Safeco/First National Insurance Company Attached is the audit report on Safeco/First National Insurance Company issued by Cotton & Company LLP. The report discusses the following issues: (1) copies of SBA underwriting form numbers 1624 and 912 were not maintained for one bond, and (2) SBA was not notified of default in a timely manner for one bond. You may release this report to the duly authorized representative of Safeco/First National Insurance Company. The findings included in this report are based on the auditors conclusions. The findings and recommendations are subject to review, management decision, and corrective action by your office in accordance with existing Agency procedures for audit follow-up and resolution. Please provide us your proposed management decision for each recommendation on the attached forms 1824, Recommended Action Sheet, within 80 days. This report may contain proprietary information subject to the provisions of 18 USC Therefore, you should not release this report to the public or another agency without permission of the Office of Inspector General. Should you or your staff have any questions, please contact Robert Hultberg, Business Development Programs Group at (202) Attachments

copies of SBA underwriting form numbers 1624 and 912 were not maintained for one bond, and (2) SBA was not notified of default in a timely manner")

2 INDEPENDENT ACCOUNTANTS REPORT ON THE PERFORMANCE AUDIT OF SAFECO/FIRST NATIONAL INSURANCE COMPANY Performed by: Cotton & Company LLP Certified Public Accountants 333 North Fairfax Street, Suite 401 Alexandria, Virginia 22314

3 November 2, 2001 U.S. Small Business Administration Office of Inspector General BACKGROUND The Small Business Investment Act of 1958, as amended, authorized the U.S. Small Business Administration s (SBA) Surety Bond Guarantee Program (SBG) to assist small, emerging, and minority construction contractors. SBA indemnifies surety companies from potential losses by providing a Government guarantee on bonds issued to such contractors. SBA guarantees up to 90 percent of losses incurred by sureties for contracts not exceeding $1.25 million (increased to $2 million effective January 25, 2001). SBA s Office of Surety Guarantees (OSG) administers the SBG program. OBJECTIVE, SCOPE AND METHODOLOGY SBA s Office of Inspector General (OIG) requested Cotton & Company to conduct a performance audit of Safeco/First National Insurance Company. The primary objectives were to determine if Safeco/First National: 1. Complied with applicable policies and procedures, including SBA s policies and standards generally accepted by the surety industry in issuing SBA-guaranteed bonds. 2. Submitted claims and expenses to SBA that were allowable, allocable, and reasonable. 3. Accurately calculated fees due to SBA and remitted them in a timely manner. We obtained the universe of Safeco/First National bonds for which SBA had paid claims from October 1, 1999, through September 30, This universe contained eight bonds, and we randomly selected two as sample bonds for review. We also randomly selected two additional bonds originally approved in Fiscal Years (FYs) 2000 and 2001 for underwriting review only. Thus, our total sample size was 4 bonds with claims (net of recoveries) totaling $372, [FOIA Ex. 4]. We tested sample bonds for compliance with SBA regulations for underwriting and fees by reviewing underwriting files and Safeco/First National s accounting records. We tested claims incurred under sample bonds from October 1, 1999, through September 30, 2001, by reviewing Safeco/First National s supporting documentation in the claim files and accounting records. We obtained a list of all

administers the SBG program.")

4 SBA-guaranteed final bonds from October 1, 1999, through September 30, 2001, and identified contractors with total bonds exceeding $1.25 million ($2 million for bonds issued after January 25, 2001) for contracts with the same obligee and bond issue dates within several months. We then reviewed project descriptions to determine if the bonds were for a single project divided into more than one contract. We conducted fieldwork during October and November 2001 at Safeco/First National s offices in Redmond, Washington. The audit was conducted in accordance with Government Auditing Standards, 1994 Revision. AUDIT RESULTS AND RECOMMENDATIONS Safeco/First National correctly calculated and remitted all sample bond fees to SBA in a timely manner. Safeco/First National did not always comply with SBA regulations for underwriting and servicing bonds and processing claims. Specifically, Safeco/First National did not maintain copies of SBA underwriting form numbers 1624 and 912 for one of four bonds tested. In addition, it did not notify SBA of default for one bond in a timely manner, as required by SBA regulations. We concluded that management and financial controls were adequate to protect assets and prevent errors and fraud, except as noted below. We concluded that Safeco/First National did not comply in all material aspects with SBA regulations for obtaining and maintaining documents to support proper underwriting of SBA bond guarantees. Also, Safeco/First National did not have procedures in place to ensure timely notification of default to SBA. We conducted an exit conference with Safeco/First National personnel on November 2, They generally agreed with factual aspects of the findings. Our findings and recommendations are discussed in detail below. Record Retention Safeco/First National did not maintain copies of SBA underwriting forms 1624 and 912 for one sample bond, as required by SBA regulations. Additionally, the surety was unable to obtain copies of these documents from their agent. Safeco/First National is required to provide critical underwriting documents that may be necessary to settle existing claims or defend or enhance any litigation actions against indemnitors, obligees, or other claimants. Contractor SBG No. Bond Date Missing Documents [FOIA Ex. 4] SBA Form 1624, 912 Title 13, CFR, Section (b), Audits and Investigations, requires a surety to maintain all documentation submitted by the principal in applying for the bond, for the term of each bond, plus additional time required to settle any claims for reimbursement from SBA and to attempt salvage or other recovery, plus an additional 3 years. Recommendation: We recommend that the OSG Associate Administrator advise Safeco/First National to implement and enforce policies and procedures that would ensure that all required SBA documentation for underwriting and servicing SBA-guaranteed bonds be maintained in accordance with SBA regulations. 2

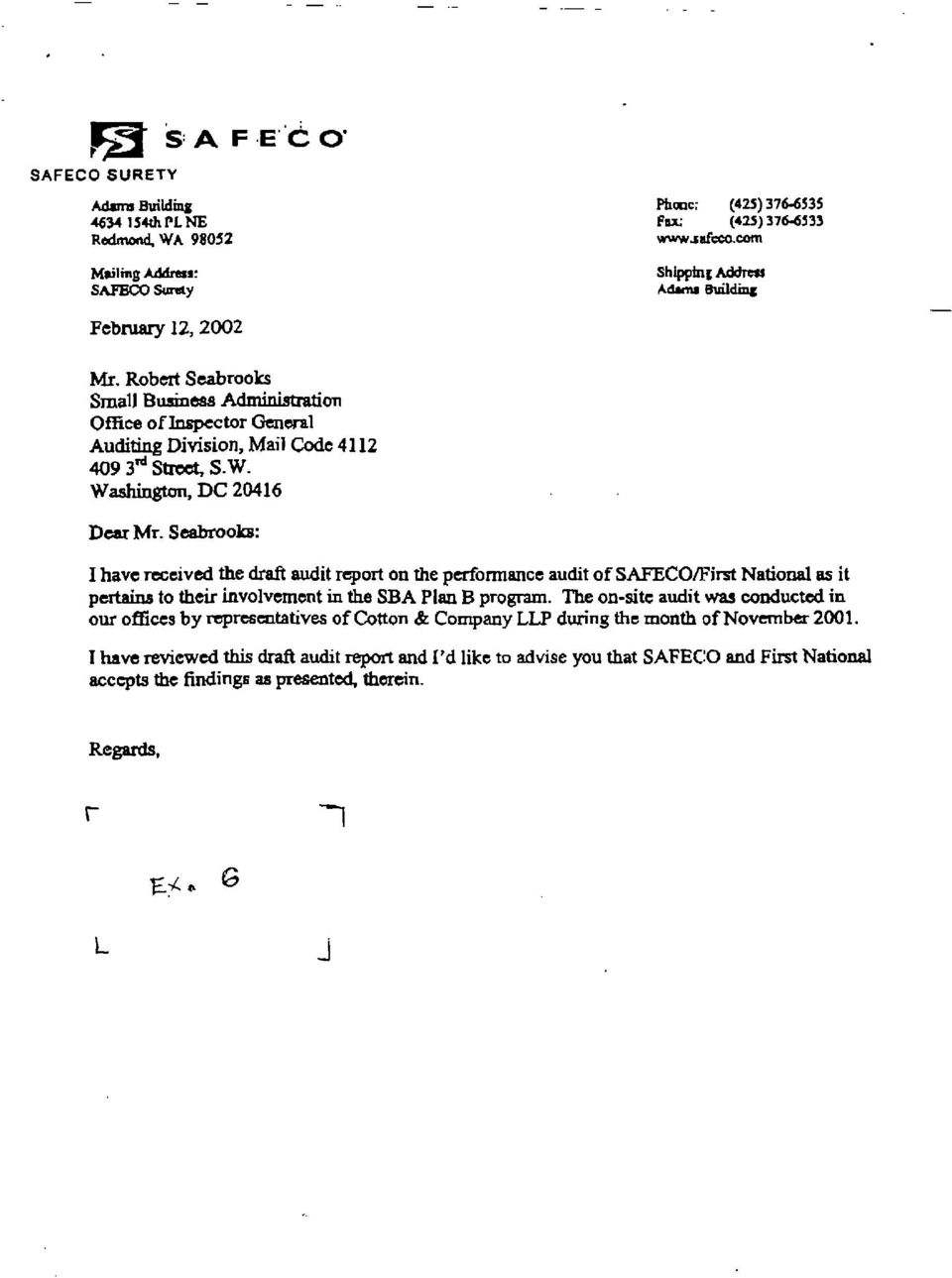

5 Timely Notification of Default Safeco/First National did not notify SBA in a timely manner when the principal for one of the two bonds reviewed with claims activity defaulted. In the default notification letter that Safeco/First National sent to SBA, it acknowledged late notification of default. Safeco indicated that the late notification was the result of a change in personnel handling the file and the new individual was unfamiliar with the SBA reporting requirement. Safeco/First National emphasized, however, that its personnel are aware of the SBA reporting requirement. Contractor SBG No. Bond Default Date Date SBA Notified [FOIA Ex. 4 and 6] September 19, 1998 November 17, 1998 Title 13 CFR (c)(2) defines other events requiring notification as follows: The PSB Surety must notify SBA within 30 calendar days of the name and address of any principal against whom legal action on the bond has been instituted; whenever an obligee has been declared in default; whenever the Surety has established or added to a claim reserve; of the recovery of any amounts on the guaranteed bond; and of any decision by the Surety to bond any such Principal again. Recommendation: We recommend that the OSG Associate Administrator advise Safeco/First National to continue to enforce its policies and procedures to ensure that SBA receives timely notification of default in accordance with SBA regulations. Safeco/First National s Response: Safeco/First National stated that they have reviewed the draft audit report and accept the findings as presented (see appendix). SBA MANAGEMENT S RESPONSE The Associate Administrator, Office of Surety Guarantees, agreed with the recommendations in our draft audit report. He stated that his office will implement the recommendations upon completion of the audit, as appropriate. 3

6 Attachment SAMPLE BONDS Sample No. Surety Bond Guarantee No. Safeco/First National Bond No. Contractor Name Bond Approval Date Bond Default Date 1 [FOIA Ex. 4 and 6] N/A = Sample bond selected for underwriting review only.

7 APPENDIX SAFECO/FIRST NATIONAL INSURANCE COMPANY RESPONSE TO THE DRAFT REPORT

8

9 REPORT DISTRIBUTION Recipient No. of Copies Associate Deputy Administrator for Capital Access...1 General Counsel...2 Office of the Chief Financial Officer Attention: [FOIA Ex. 6]...1 2

INDEPENDENT ACCOUNTANTS REPORT ON THE PERFORMANCE AUDIT OF FARMINGTON CASUALTY COMPANY

INDEPENDENT ACCOUNTANTS REPORT ON THE PERFORMANCE AUDIT OF FARMINGTON CASUALTY COMPANY Performed by: Cotton & Company LLP Certified Public Accountants 333 North Fairfax Street, Suite 401 Alexandria, Virginia

INDEPENDENT ACCOUNTANTS REPORT ON THE PERFORMANCE AUDIT OF FARMINGTON CASUALTY COMPANY Performed by: Cotton & Company LLP Certified Public Accountants 333 North Fairfax Street, Suite 401 Alexandria, Virginia

U.S. SMALL BUSINESS ADMINISTRATION OFFICE OF INSPECTOR GENERAL WASHINGTON, D.C. 20416

U.S. SMALL BUSINESS ADMINISTRATION OFFICE OF INSPECTOR GENERAL WASHINGTON, D.C. 20416 AUDIT REPORT Issue Date: December 27, 2000 Number: 1-02 To: Robert J. Moffitt Associate Administrator, Office of Surety

U.S. SMALL BUSINESS ADMINISTRATION OFFICE OF INSPECTOR GENERAL WASHINGTON, D.C. 20416 AUDIT REPORT Issue Date: December 27, 2000 Number: 1-02 To: Robert J. Moffitt Associate Administrator, Office of Surety

AUDIT OF SBA S EMAIL SYSTEM AUDIT REPORT NUMBER 4-42 SEPTEMBER 10, 2004

AUDIT OF SBA S EMAIL SYSTEM AUDIT REPORT NUMBER 4-42 SEPTEMBER 10, 2004 This report may contain proprietary information subject to the provisions of 18 USC 1905 and must not be released to the public or

AUDIT OF SBA S EMAIL SYSTEM AUDIT REPORT NUMBER 4-42 SEPTEMBER 10, 2004 This report may contain proprietary information subject to the provisions of 18 USC 1905 and must not be released to the public or

U.S. SMALL BUSINESS ADMINISTRATION OFFICE OF INSPECTOR GENERAL Washington, DC 20416

U.S. SMALL BUSINESS ADMINISTRATION OFFICE OF INSPECTOR GENERAL Washington, DC 20416 AUDIT REPORT ISSUE DATE: March 29, 2002 REPORT NUMBER: 2-15 To: Patricia B. Rivera, District Director Colorado District

U.S. SMALL BUSINESS ADMINISTRATION OFFICE OF INSPECTOR GENERAL Washington, DC 20416 AUDIT REPORT ISSUE DATE: March 29, 2002 REPORT NUMBER: 2-15 To: Patricia B. Rivera, District Director Colorado District

AUDIT OF SBA S LOAN APPLICATION TRACKING SYSTEM AUDIT REPORT NUMBER 4-18 APRIL 5, 2004

AUDIT OF SBA S LOAN APPLICATION TRACKING SYSTEM AUDIT REPORT NUMBER 4-18 APRIL 5, 2004 This report may contain proprietary information subject to the provisions of 18 USC 1905 and must not be released

AUDIT OF SBA S LOAN APPLICATION TRACKING SYSTEM AUDIT REPORT NUMBER 4-18 APRIL 5, 2004 This report may contain proprietary information subject to the provisions of 18 USC 1905 and must not be released

ADVISORY MEMORANDUM REPORT ON DEVELOPMENT OF THE LOAN MONITORING SYSTEM ADVISORY REPORT NUMBER A1-03 FEBRUARY 23, 2001

ADVISORY MEMORANDUM REPORT ON DEVELOPMENT OF THE LOAN MONITORING SYSTEM ADVISORY REPORT NUMBER A1-03 FEBRUARY 23, 2001 This report may contain proprietary information subject to the provisions of 18 USC

ADVISORY MEMORANDUM REPORT ON DEVELOPMENT OF THE LOAN MONITORING SYSTEM ADVISORY REPORT NUMBER A1-03 FEBRUARY 23, 2001 This report may contain proprietary information subject to the provisions of 18 USC

REVIEW OF SELECTED SMALL BUSINESS PROCUREMENTS REPORT NUMBER 5-16 MARCH 8, 2005

REVIEW OF SELECTED SMALL BUSINESS PROCUREMENTS REPORT NUMBER 5-16 MARCH 8, 2005 This report may contain proprietary information subject to the provisions of 18 USC 1905 and must not be released to the

REVIEW OF SELECTED SMALL BUSINESS PROCUREMENTS REPORT NUMBER 5-16 MARCH 8, 2005 This report may contain proprietary information subject to the provisions of 18 USC 1905 and must not be released to the

AUDIT OF MONITORING COMPLIANCE WITH 8(A) BUSINESS DEVELOPMENT REGULATIONS DURING 8(A) BUSINESS DEVELOPMENT CONTRACT PERFORMANCE AUDIT REPORT NO.

BUSINESS DEVELOPMENT REGULATIONS DURING 8(A) BUSINESS DEVELOPMENT CONTRACT PERFORMANCE AUDIT REPORT NO.") AUDIT OF MONITORING COMPLIANCE WITH 8(A) BUSINESS DEVELOPMENT REGULATIONS DURING 8(A) BUSINESS DEVELOPMENT CONTRACT PERFORMANCE AUDIT REPORT NO. 6-15 MARCH 16, 2006 This report may contain proprietary

AUDIT OF MONITORING COMPLIANCE WITH 8(A) BUSINESS DEVELOPMENT REGULATIONS DURING 8(A) BUSINESS DEVELOPMENT CONTRACT PERFORMANCE AUDIT REPORT NO. 6-15 MARCH 16, 2006 This report may contain proprietary

Surety bonds are almost always written by insurance companies that are licensed by state insurance departments, but they are not like typical

A surety bond is a promise to be liable for the debt, default, or failure of another. A surety bond is a three-party contract by which one party (surety) guarantees the performance of a second party (principal)

A surety bond is a promise to be liable for the debt, default, or failure of another. A surety bond is a three-party contract by which one party (surety) guarantees the performance of a second party (principal)

AUDIT OF SBA S COMPLIANCE WITH JOINT FINANCIAL MANAGEMENT IMPROVEMENT PROGRAM PROPERTY MANAGEMENT SYSTEM REQUIREMENTS AUDIT REPORT NUMBER 3-34

AUDIT OF SBA S COMPLIANCE WITH JOINT FINANCIAL MANAGEMENT IMPROVEMENT PROGRAM PROPERTY MANAGEMENT SYSTEM REQUIREMENTS AUDIT REPORT NUMBER 3-34 JULY 23, 2003 This report may contain proprietary information

AUDIT OF SBA S COMPLIANCE WITH JOINT FINANCIAL MANAGEMENT IMPROVEMENT PROGRAM PROPERTY MANAGEMENT SYSTEM REQUIREMENTS AUDIT REPORT NUMBER 3-34 JULY 23, 2003 This report may contain proprietary information

ASSESSMENT REPORT 09 14 GPO WORKERS COMPENSATION PROGRAM. September 30, 2009

ASSESSMENT REPORT 09 14 GPO WORKERS COMPENSATION PROGRAM September 30, 2009 Date September 30, 2009 To Chief Management Officer Chief, Office of Workers Compensation From Assistant Inspector General for

ASSESSMENT REPORT 09 14 GPO WORKERS COMPENSATION PROGRAM September 30, 2009 Date September 30, 2009 To Chief Management Officer Chief, Office of Workers Compensation From Assistant Inspector General for

AUDIT OF NON-TAX DELINQUENT DEBT WASHINGTON, DC AUDIT REPORT NO. 9-11

AUDIT OF NONTA DELINQUENT DEBT WASHINGTON, DC AUDIT REPORT NO. 911 July 28, 1999 This report may contain proprietary information subject to the provisions of 18 USC 1905 and must nol be released to the

AUDIT OF NONTA DELINQUENT DEBT WASHINGTON, DC AUDIT REPORT NO. 911 July 28, 1999 This report may contain proprietary information subject to the provisions of 18 USC 1905 and must nol be released to the

Close-Out of Complaint on Metropolitan Water Reclamation District of Greater Chicago Incurring Inappropriate Expenses on Recovery Act Projects

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Close-Out of Complaint on Metropolitan Water Reclamation District of Greater Chicago Incurring Inappropriate Expenses on Recovery Act Projects

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Close-Out of Complaint on Metropolitan Water Reclamation District of Greater Chicago Incurring Inappropriate Expenses on Recovery Act Projects

Lawrence County Engineer, Ohio, Generally Accounted For and Expended FEMA Grant Funds Properly

Lawrence County Engineer, Ohio, Generally Accounted For and Expended FEMA Grant Funds Properly June 25, 2015 OIG-15-110-D June 25, 2015 Why We Did This Lawrence County Engineer, Ohio (Lawrence), received

Lawrence County Engineer, Ohio, Generally Accounted For and Expended FEMA Grant Funds Properly June 25, 2015 OIG-15-110-D June 25, 2015 Why We Did This Lawrence County Engineer, Ohio (Lawrence), received

SBA SOP 50 45 3. The Surety Bond Guarantee Program. Office of Surety Guarantees. U.S. Small Business Administration

SBA SOP 50 45 3 The Surety Bond Guarantee Program Office of Surety Guarantees U.S. Small Business Administration August 5, 2015 Effective Date: August 5, 2015 2 TABLE OF CONTENTS Paragraph Page CHAPTER

SBA SOP 50 45 3 The Surety Bond Guarantee Program Office of Surety Guarantees U.S. Small Business Administration August 5, 2015 Effective Date: August 5, 2015 2 TABLE OF CONTENTS Paragraph Page CHAPTER

What You Should Know About General Agreements of Indemnity and Why You Should Know It

What You Should Know About General Agreements of Indemnity and Why You Should Know It Summary When a contractor (for purposes of this discussion, contractor includes subcontractor) first seeks surety credit,

What You Should Know About General Agreements of Indemnity and Why You Should Know It Summary When a contractor (for purposes of this discussion, contractor includes subcontractor) first seeks surety credit,

INTERNATIONAL BUSINESS COLLEGE'S ADMINISTRATION OF TITLE IV STUDENT FINANCIAL ASSISTANCE PROGRAMS

INTERNATIONAL BUSINESS COLLEGE'S ADMINISTRATION OF TITLE IV STUDENT FINANCIAL ASSISTANCE PROGRAMS FINAL AUDIT REPORT Control Number: ED-OIG/A06-A0003 March 2001 Our mission is to promote the efficient

INTERNATIONAL BUSINESS COLLEGE'S ADMINISTRATION OF TITLE IV STUDENT FINANCIAL ASSISTANCE PROGRAMS FINAL AUDIT REPORT Control Number: ED-OIG/A06-A0003 March 2001 Our mission is to promote the efficient

SBA Construction Bonds Up To $250,000

SBA Construction Bonds Up To $250,000 Unable to obtain construction bonds with a standard surety market? Have bad credit? You may apply for construction bonds up to $250,000. To qualify, please complete

SBA Construction Bonds Up To $250,000 Unable to obtain construction bonds with a standard surety market? Have bad credit? You may apply for construction bonds up to $250,000. To qualify, please complete

August 2012 Report No. 12-048

John Keel, CPA State Auditor An Audit Report on The Texas Windstorm Insurance Association Report No. 12-048 An Audit Report on The Texas Windstorm Insurance Association Overall Conclusion The Texas Windstorm

John Keel, CPA State Auditor An Audit Report on The Texas Windstorm Insurance Association Report No. 12-048 An Audit Report on The Texas Windstorm Insurance Association Overall Conclusion The Texas Windstorm

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION The Internal Revenue Service September 14, 2010 Reference Number: 2010-10-115 This report has cleared the Treasury Inspector General for Tax Administration

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION The Internal Revenue Service September 14, 2010 Reference Number: 2010-10-115 This report has cleared the Treasury Inspector General for Tax Administration

FINAL REPORT INSPECTION 2007-11474 REVIEW OF TVA'S WORKERS' COMPENSATION PROGRAM

Memorandum from the Office of the Inspector General March 2, 2009 Phillip L. Reynolds, LP 3A-C FINAL REPORT INSPECTION 2007-11474 REVIEW OF TVA'S WORKERS' COMPENSATION PROGRAM Attached is the subject final

Memorandum from the Office of the Inspector General March 2, 2009 Phillip L. Reynolds, LP 3A-C FINAL REPORT INSPECTION 2007-11474 REVIEW OF TVA'S WORKERS' COMPENSATION PROGRAM Attached is the subject final

2IÀFHRI,QVSHFWRU*HQHUDO

2IÀFHRI,QVSHFWRU*HQHUDO Santa Clara Pueblo, New Mexico, Needs Assistance to Ensure Compliance with FEMA Public Assistance Grant Requirements OIG-14-128-D August 2014 Washington, DC 20528 I www.oig.dhs.gov

2IÀFHRI,QVSHFWRU*HQHUDO Santa Clara Pueblo, New Mexico, Needs Assistance to Ensure Compliance with FEMA Public Assistance Grant Requirements OIG-14-128-D August 2014 Washington, DC 20528 I www.oig.dhs.gov

Gwinnett County, Georgia, Generally Accounted for and Expended FEMA Public Assistance Grant Funds According to Federal Requirements

Gwinnett County, Georgia, Generally Accounted for and Expended FEMA Public Assistance Grant Funds According to Federal Requirements February 20, 2015 HIGHLIGHTS Gwinnett County, Georgia, Generally Accounted

Gwinnett County, Georgia, Generally Accounted for and Expended FEMA Public Assistance Grant Funds According to Federal Requirements February 20, 2015 HIGHLIGHTS Gwinnett County, Georgia, Generally Accounted

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Affordable Care Act: Tracking of Health Insurance Reform Implementation Fund Costs Could Be Improved September 18, 2013 Reference Number: 2013-13-115 This

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Affordable Care Act: Tracking of Health Insurance Reform Implementation Fund Costs Could Be Improved September 18, 2013 Reference Number: 2013-13-115 This

AUDIT OF AN SBA GUARANTEED LOAN TO. [ Exemption 6 ] DBA L & L LEGAL ASSISTANCE. San Francisco, California. Audit Report Number: 7-09

![AUDIT OF AN SBA GUARANTEED LOAN TO. [ Exemption 6 ] DBA L & L LEGAL ASSISTANCE. San Francisco, California. Audit Report Number: 7-09](/thumbs/39/18225327.jpg "AUDIT OF AN SBA GUARANTEED LOAN TO. [ Exemption 6 ] DBA L & L LEGAL ASSISTANCE. San Francisco, California. Audit Report Number: 7-09") AUDIT OF AN SBA GUARANTEED LOAN TO [ Exemption 6 ] DBA L & L LEGAL ASSISTANCE San Francisco, California Audit Report Number: 7-09 January 9, 2007 U.S. SMALL BUSINESS ADMINISTRATION OFFICE OF INSPECTOR

AUDIT OF AN SBA GUARANTEED LOAN TO [ Exemption 6 ] DBA L & L LEGAL ASSISTANCE San Francisco, California Audit Report Number: 7-09 January 9, 2007 U.S. SMALL BUSINESS ADMINISTRATION OFFICE OF INSPECTOR

perform cost settlements to ensure that future final payments for school-based services are based on actual costs.

Page 2 Kerry Weems perform cost settlements to ensure that future final payments for school-based services are based on actual costs. In written comments on our draft report, the State agency concurred

Page 2 Kerry Weems perform cost settlements to ensure that future final payments for school-based services are based on actual costs. In written comments on our draft report, the State agency concurred

U.S. Small Business Administration Surety Bond Guarantee Program. Opening the Door to Bonding

U.S. Small Business Administration Surety Bond Guarantee Program Opening the Door to Bonding What Is a Surety Bond? A three party written agreement between the surety, the contractor and the project owner.

U.S. Small Business Administration Surety Bond Guarantee Program Opening the Door to Bonding What Is a Surety Bond? A three party written agreement between the surety, the contractor and the project owner.

The City of Atlanta, Georgia, Effectively Managed FEMA Public Assistance Grant Funds Awarded for Severe Storms and Flooding in September 2009

The City of Atlanta, Georgia, Effectively Managed FEMA Public Assistance Grant Funds Awarded for Severe Storms and Flooding in September 2009 May 19, 2015 DHS OIG HIGHLIGHTS The City of Atlanta, Georgia,

The City of Atlanta, Georgia, Effectively Managed FEMA Public Assistance Grant Funds Awarded for Severe Storms and Flooding in September 2009 May 19, 2015 DHS OIG HIGHLIGHTS The City of Atlanta, Georgia,

NOT ALL COMMUNITY SERVICES BLOCK GRANT RECOVERY ACT COSTS CLAIMED

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL NOT ALL COMMUNITY SERVICES BLOCK GRANT RECOVERY ACT COSTS CLAIMED ON BEHALF OF THE COMMUNITY ACTION PARTNERSHIP OF NATRONA COUNTY FOR

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL NOT ALL COMMUNITY SERVICES BLOCK GRANT RECOVERY ACT COSTS CLAIMED ON BEHALF OF THE COMMUNITY ACTION PARTNERSHIP OF NATRONA COUNTY FOR

JUt 17 2008. vengriy-- Review offederal Medicaid Claims Made by Inpatient Substance Abuse Treatment Facilities in New Jersey (A-02-07-01005)

") -4 DEPARTMENT (~I'~ ~EHVJC'.e.$ OF HEALTII & HUMAN SERVICES Office of Inspector General '~',,

-4 DEPARTMENT (~I'~ ~EHVJC'.e.$ OF HEALTII & HUMAN SERVICES Office of Inspector General '~',,

AUDIT OF AN SBA GUARANTEED LOAN TO JUST A CUT LAWN CARE, INC. Brunswick, Georgia. Audit Report Number: 7-06

AUDIT OF AN SBA GUARANTEED LOAN TO JUST A CUT LAWN CARE, INC. Brunswick, Georgia Audit Report Number: 7-06 December 28, 2006 U.S. SMALL BUSINESS ADMINISTRATION OFFICE OF INSPECTOR GENERAL WASHINGTON, D.C.

AUDIT OF AN SBA GUARANTEED LOAN TO JUST A CUT LAWN CARE, INC. Brunswick, Georgia Audit Report Number: 7-06 December 28, 2006 U.S. SMALL BUSINESS ADMINISTRATION OFFICE OF INSPECTOR GENERAL WASHINGTON, D.C.

Management Advisory Report. PLP Processing Restrictions for Paying off Existing SBA Debt in a Change of Ownership Transaction

Management Advisory Report PLP Processing Restrictions for Paying off Existing SBA Debt in a Change of Ownership Transaction Report Number 5-27 September 28, 2005 Washington, D.C. The finding in this report

Management Advisory Report PLP Processing Restrictions for Paying off Existing SBA Debt in a Change of Ownership Transaction Report Number 5-27 September 28, 2005 Washington, D.C. The finding in this report

Nelson R. Bregon, General Deputy Assistant Secretary for Community Planning and Development. James D. McKay Regional Inspector General for Audit, 4AGA

Issue Date July 26, 2006 Audit Report Number 2006-AT-1014 TO: Nelson R. Bregon, General Deputy Assistant Secretary for Community Planning and Development FROM: James D. McKay Regional Inspector General

Issue Date July 26, 2006 Audit Report Number 2006-AT-1014 TO: Nelson R. Bregon, General Deputy Assistant Secretary for Community Planning and Development FROM: James D. McKay Regional Inspector General

UPDATED. OIG Guidelines for Evaluating State False Claims Acts

UPDATED OIG Guidelines for Evaluating State False Claims Acts Note: These guidelines are effective March 15, 2013, and replace the guidelines effective on August 21, 2006, found at 71 FR 48552. UPDATED

UPDATED OIG Guidelines for Evaluating State False Claims Acts Note: These guidelines are effective March 15, 2013, and replace the guidelines effective on August 21, 2006, found at 71 FR 48552. UPDATED

MASSACHUSETTS MEDICAID PAYMENTS TO ESSEX PARK REHABILITATION AND NURSING CENTER DID NOT ALWAYS COMPLY WITH FEDERAL AND STATE REQUIREMENTS

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL MASSACHUSETTS MEDICAID PAYMENTS TO ESSEX PARK REHABILITATION AND NURSING CENTER DID NOT ALWAYS COMPLY WITH FEDERAL AND STATE REQUIREMENTS

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL MASSACHUSETTS MEDICAID PAYMENTS TO ESSEX PARK REHABILITATION AND NURSING CENTER DID NOT ALWAYS COMPLY WITH FEDERAL AND STATE REQUIREMENTS

AUDIT REPORT. Federal Energy Regulatory Commission's Fiscal Year 2014 Financial Statement Audit

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections AUDIT REPORT Federal Energy Regulatory Commission's Fiscal Year 2014 Financial Statement Audit OAS-FS-15-05 December

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections AUDIT REPORT Federal Energy Regulatory Commission's Fiscal Year 2014 Financial Statement Audit OAS-FS-15-05 December

AUDIT OF AN SBA GUARANTEED LOAN TO IROM CNC MACHINING, INC. AND IROM IMAGING, INC. Report Number: 7-17

AUDIT OF AN SBA GUARANTEED LOAN TO IROM CNC MACHINING, INC. AND IROM IMAGING, INC. Report Number: 7-17 March 12, 2007 U.S. Small Business Administration Office of Inspector General Memorandum To: From:

AUDIT OF AN SBA GUARANTEED LOAN TO IROM CNC MACHINING, INC. AND IROM IMAGING, INC. Report Number: 7-17 March 12, 2007 U.S. Small Business Administration Office of Inspector General Memorandum To: From:

FEMA Should Disallow over $4 Million Awarded to Mountain View Electric Association, Colorado, for Improper Procurement Practices

FEMA Should Disallow over $4 Million Awarded to Mountain View Electric Association, Colorado, for Improper Procurement Practices July 16, 2015 DHS OIG HIGHLIGHTS FEMA Should Disallow over $4 Million Awarded

FEMA Should Disallow over $4 Million Awarded to Mountain View Electric Association, Colorado, for Improper Procurement Practices July 16, 2015 DHS OIG HIGHLIGHTS FEMA Should Disallow over $4 Million Awarded

Department of Energy Human Resources and Administration Home Page http://www.hr.doe.gov/refshelf.html

U.S. DEPARTMENT OF ENERGY OFFICE OF INSPECTOR GENERAL AUDIT OF DEPARTMENT OF ENERGY'S CONTRACTOR LIABILITY INSURANCE COSTS The Office of Inspector General wants to make the distribution of its reports

U.S. DEPARTMENT OF ENERGY OFFICE OF INSPECTOR GENERAL AUDIT OF DEPARTMENT OF ENERGY'S CONTRACTOR LIABILITY INSURANCE COSTS The Office of Inspector General wants to make the distribution of its reports

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections Audit Report The Department of Energy's Weatherization Assistance Program Funded under the American Recovery and Reinvestment

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections Audit Report The Department of Energy's Weatherization Assistance Program Funded under the American Recovery and Reinvestment

G 7401.5 CHAPTER 8. EMPLOYEE DISHONESTY INSURANCE EXPLANATION AND REQUIREMENTS

G 7401.5 CHAPTER 8. EMPLOYEE DISHONESTY INSURANCE EXPLANATION AND REQUIREMENTS 8-1. EMPLOYEE DISHONESTY. a. Employee dishonesty (sometimes referred to as Fidelity Bonds) should be written on a standard

G 7401.5 CHAPTER 8. EMPLOYEE DISHONESTY INSURANCE EXPLANATION AND REQUIREMENTS 8-1. EMPLOYEE DISHONESTY. a. Employee dishonesty (sometimes referred to as Fidelity Bonds) should be written on a standard

JUl - 2 2008' Review ofmedicaid Claims Made by Freestanding Residential Treatment Facilities in New York State (A-02-06-01021)

") DEPARTMENT OF HEALTH & HUMAN SERVICES Office of Inspector General Washington, D.C. 20201 JUl - 2 2008' TO: FROM: Kerry Weems Acting Administrator Centers for Medicare & Medicaid Services ~ oseph E. Vengrin

DEPARTMENT OF HEALTH & HUMAN SERVICES Office of Inspector General Washington, D.C. 20201 JUl - 2 2008' TO: FROM: Kerry Weems Acting Administrator Centers for Medicare & Medicaid Services ~ oseph E. Vengrin

Department of Homeland Security

FEMA Public Assistance Grant Funds Awarded to South Florida Water Management District Under Hurricane Charley DA-12-23 August 2012 Washington, DC 20528 / www.oig.dhs.gov AUG 2 7 2012 MEMORANDUM FOR: agement

FEMA Public Assistance Grant Funds Awarded to South Florida Water Management District Under Hurricane Charley DA-12-23 August 2012 Washington, DC 20528 / www.oig.dhs.gov AUG 2 7 2012 MEMORANDUM FOR: agement

Department of Rehabilitation

Department of Rehabilitation Audit Services Report Older Individuals who are Blind (OIB) American Recovery and Reinvestment Act (ARRA) Grant #27670A for San Diego Center for the Blind Date: September 20,

Department of Rehabilitation Audit Services Report Older Individuals who are Blind (OIB) American Recovery and Reinvestment Act (ARRA) Grant #27670A for San Diego Center for the Blind Date: September 20,

Controls Over EPA s Compass Financial System Need to Be Improved

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Controls Over EPA s Compass Financial System Need to Be Improved Report No. 13-P-0359 August 23, 2013 Scan this mobile code to learn more

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Controls Over EPA s Compass Financial System Need to Be Improved Report No. 13-P-0359 August 23, 2013 Scan this mobile code to learn more

Department of Homeland Security

Department of Homeland Security National Flood Insurance Program s Management Letter for FY 2011 DHS Consolidated Financial Statements Audit (Redacted) OIG-12-71 April 2012 (Revised) Office of Inspector

Department of Homeland Security National Flood Insurance Program s Management Letter for FY 2011 DHS Consolidated Financial Statements Audit (Redacted) OIG-12-71 April 2012 (Revised) Office of Inspector

Napa County, California, Needs Additional Technical Assistance and Monitoring to Ensure Compliance with Federal Regulations

Napa County, California, Needs Additional Technical Assistance and Monitoring to Ensure Compliance with Federal Regulations OIG-15-135-D August 28, 2015 August 28, 2015 Why We Did This On August 24, 2014,

Napa County, California, Needs Additional Technical Assistance and Monitoring to Ensure Compliance with Federal Regulations OIG-15-135-D August 28, 2015 August 28, 2015 Why We Did This On August 24, 2014,

SUBCONTRACTOR LABOR AND MATERIAL PAYMENT BOND ("Bond") SURETY Address

SURETY Address") Bond # SUBCONTRACTOR LABOR AND MATERIAL PAYMENT BOND ("Bond") KNOW ALL PERSONS BY THESE PRESENTS; that SUBCONTRACTOR as Principal (the "Subcontractor"), and SURETY as Surety or Co-sureties (hereinafter

Bond # SUBCONTRACTOR LABOR AND MATERIAL PAYMENT BOND ("Bond") KNOW ALL PERSONS BY THESE PRESENTS; that SUBCONTRACTOR as Principal (the "Subcontractor"), and SURETY as Surety or Co-sureties (hereinafter

INSPECTION OF PARKS COLLEGE S COMPLIANCE WITH STUDENT FINANCIAL ASSISTANCE REQUIREMENTS

INSPECTION OF PARKS COLLEGE S COMPLIANCE WITH STUDENT FINANCIAL ASSISTANCE REQUIREMENTS FINAL INSPECTION REPORT Control Number ED-OIG/N06-90010 February 2000 Our mission is to promote the efficient and

INSPECTION OF PARKS COLLEGE S COMPLIANCE WITH STUDENT FINANCIAL ASSISTANCE REQUIREMENTS FINAL INSPECTION REPORT Control Number ED-OIG/N06-90010 February 2000 Our mission is to promote the efficient and

Auditor General Procurement Processes Review - Bid Bonds/Performance Bonds

STAFF REPORT June 22, 2005 To: From: Subject: Administration Committee Deputy City Manager and Chief Financial Officer Auditor General Procurement Processes Review - Bid Bonds/Performance Bonds Purpose:

STAFF REPORT June 22, 2005 To: From: Subject: Administration Committee Deputy City Manager and Chief Financial Officer Auditor General Procurement Processes Review - Bid Bonds/Performance Bonds Purpose:

March 28, 2003 Audit Report No. 03-026. Internal Control Over Receivables from Failed Insured Depository Institutions

March 28, 2003 Audit Report No. 03-026 Internal Control Over Receivables from Failed Insured Depository Institutions Federal Deposit Insurance Corporation 801 17th St. NW Washington DC. 20434 Office of

March 28, 2003 Audit Report No. 03-026 Internal Control Over Receivables from Failed Insured Depository Institutions Federal Deposit Insurance Corporation 801 17th St. NW Washington DC. 20434 Office of

Public Assistance Alternative Procedures Pilot Program Guide for Debris Removal (Version 3) June 28, 2015

June 28, 2015") [Type text] Public Assistance Alternative Procedures Pilot Program Guide for Debris Removal (Version 3) June 28, 2015 Federal Emergency Management Agency Department of Homeland Security 500 C Street, S.W.

[Type text] Public Assistance Alternative Procedures Pilot Program Guide for Debris Removal (Version 3) June 28, 2015 Federal Emergency Management Agency Department of Homeland Security 500 C Street, S.W.

Our mission is to promote efficiency, effectiveness, and integrity of the Department s programs and operations.

Our mission is to promote efficiency, effectiveness, and integrity of the Department s programs and operations. Our mission is to promote efficiency, effectiveness, and integrity of the Department s programs

Our mission is to promote efficiency, effectiveness, and integrity of the Department s programs and operations. Our mission is to promote efficiency, effectiveness, and integrity of the Department s programs

INTRODUCTION TO BID/PERFORMANCE AND PAYMENT BONDS AND THE SBA BOND GUARANTEE PROGRAM:

INTRODUCTION TO BID/PERFORMANCE AND PAYMENT BONDS AND THE SBA BOND GUARANTEE PROGRAM: U.S. Small Business Administration Phoenix SBA Office March 21, 2013 Mark S. Hewitt, CPCU, AFSB, AIM Western National

INTRODUCTION TO BID/PERFORMANCE AND PAYMENT BONDS AND THE SBA BOND GUARANTEE PROGRAM: U.S. Small Business Administration Phoenix SBA Office March 21, 2013 Mark S. Hewitt, CPCU, AFSB, AIM Western National

U.S. Department of Agriculture Office of Inspector General Midwest Region Audit Report

U.S. Department of Agriculture Office of Inspector General Midwest Region Audit Report Food and Nutrition Service National School Lunch Program Food Service Management Companies Report No. 27601-0027-CH

U.S. Department of Agriculture Office of Inspector General Midwest Region Audit Report Food and Nutrition Service National School Lunch Program Food Service Management Companies Report No. 27601-0027-CH

CHAPTER 179. BE IT ENACTED by the Senate and General Assembly of the State of New Jersey: 1. R.S.34:15-104 is amended to read as follows:

CHAPTER 179 AN ACT concerning the workers' compensation security funds and amending and repealing various sections of chapter 15 of Title 34 of the Revised Statutes. BE IT ENACTED by the Senate and General

CHAPTER 179 AN ACT concerning the workers' compensation security funds and amending and repealing various sections of chapter 15 of Title 34 of the Revised Statutes. BE IT ENACTED by the Senate and General

COSTS CHARGED TO HEAD START PROGRAM ADMINISTERED BY ROCKINGHAM COMMUNITY ACTION,

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL COSTS CHARGED TO HEAD START PROGRAM ADMINISTERED BY ROCKINGHAM COMMUNITY ACTION, INC. DECEMBER 2003 A-01-03-02500 Office of Inspector

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL COSTS CHARGED TO HEAD START PROGRAM ADMINISTERED BY ROCKINGHAM COMMUNITY ACTION, INC. DECEMBER 2003 A-01-03-02500 Office of Inspector

OIG Deployment Activities at FEMA's Joint Field Office in Charleston, West Virginia - Yeager Airport

OIG Deployment Activities at FEMA's Joint Field Office in Charleston, West Virginia - Yeager Airport September 15, 2015 DHS OIG Highlights OIG Deployment Activities at FEMA s Joint Field Office in Charleston,

OIG Deployment Activities at FEMA's Joint Field Office in Charleston, West Virginia - Yeager Airport September 15, 2015 DHS OIG Highlights OIG Deployment Activities at FEMA s Joint Field Office in Charleston,

2IÀFHRI,QVSHFWRU*HQHUDO

2IÀFHRI,QVSHFWRU*HQHUDO FEMA Should Recover $8.0 Million of $26.6 Million in Public Assistance Grant Funds Awarded to St. Stanislaus College Preparatory in Mississippi Hurricane Katrina OIG-14-95-D May

2IÀFHRI,QVSHFWRU*HQHUDO FEMA Should Recover $8.0 Million of $26.6 Million in Public Assistance Grant Funds Awarded to St. Stanislaus College Preparatory in Mississippi Hurricane Katrina OIG-14-95-D May

May 22, 2012. Report Number: A-09-11-02047

May 22, 2012 OFFICE OF AUDIT SERVICES, REGION IX 90-7 TH STREET, SUITE 3-650 SAN FRANCISCO, CA 94103 Report Number: A-09-11-02047 Ms. Patricia McManaman Director Department of Human Services State of Hawaii

May 22, 2012 OFFICE OF AUDIT SERVICES, REGION IX 90-7 TH STREET, SUITE 3-650 SAN FRANCISCO, CA 94103 Report Number: A-09-11-02047 Ms. Patricia McManaman Director Department of Human Services State of Hawaii

Audit of Creighton University s Administration of Its Federal TRIO Projects

Audit of Creighton University s Administration of Its Federal TRIO Projects FINAL AUDIT REPORT. ED-OIG/A07-80027 March 2000 Our mission is to promote the efficient U.S. Department of Education and effective

Audit of Creighton University s Administration of Its Federal TRIO Projects FINAL AUDIT REPORT. ED-OIG/A07-80027 March 2000 Our mission is to promote the efficient U.S. Department of Education and effective

FEMA Should Recover $312,117 of $1.6 Million Grant Funds Awarded to the Pueblo of Jemez, New Mexico

FEMA Should Recover $312,117 of $1.6 Million Grant Funds Awarded to the Pueblo of Jemez, New Mexico March 21, 2016 DHS OIG HIGHLIGHTS FEMA Should Recover $312,117 of $1.6 Million Grant Funds Awarded to

FEMA Should Recover $312,117 of $1.6 Million Grant Funds Awarded to the Pueblo of Jemez, New Mexico March 21, 2016 DHS OIG HIGHLIGHTS FEMA Should Recover $312,117 of $1.6 Million Grant Funds Awarded to

MEMORANDUM FOR: K.J. Brockington, Director, Los Angeles Office of Public Housing, 9DPH

U.S. Department of Housing and Urban Development Office of Inspector General Region IX 611 West Sixth Street, Suite 1160 Los Angeles, CA 90017 Voice (213) 894-8016 Fax (213) 894-8115 Issue Date May 5,

U.S. Department of Housing and Urban Development Office of Inspector General Region IX 611 West Sixth Street, Suite 1160 Los Angeles, CA 90017 Voice (213) 894-8016 Fax (213) 894-8115 Issue Date May 5,

Review of U.S. Coast Guard's FY 2014 Drug Control Performance Summary Report

Review of U.S. Coast Guard's FY 2014 Drug Control Performance Summary Report January 26, 2015 OIG-15-27 HIGHLIGHTS Review of U.S. Coast Guard s FY 2014 Drug Control Performance Summary Report January 26,

Review of U.S. Coast Guard's FY 2014 Drug Control Performance Summary Report January 26, 2015 OIG-15-27 HIGHLIGHTS Review of U.S. Coast Guard s FY 2014 Drug Control Performance Summary Report January 26,

Office of Financial Management's Management Letter for DHS' FY 2014 Financial Statements Audit

Office of Financial Management's Management Letter for DHS' FY 2014 Financial Statements Audit April 16, 2015 OIG-15-70 HIGHLIGHTS Office of Financial Management s Management Letter for DHS FY 2014 Financial

Office of Financial Management's Management Letter for DHS' FY 2014 Financial Statements Audit April 16, 2015 OIG-15-70 HIGHLIGHTS Office of Financial Management s Management Letter for DHS FY 2014 Financial

COLORADO CLAIMED UNALLOWABLE MEDICAID NURSING FACILITY SUPPLEMENTAL PAYMENTS

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL COLORADO CLAIMED UNALLOWABLE MEDICAID NURSING FACILITY SUPPLEMENTAL PAYMENTS Inquiries about this report may be addressed to the Office

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL COLORADO CLAIMED UNALLOWABLE MEDICAID NURSING FACILITY SUPPLEMENTAL PAYMENTS Inquiries about this report may be addressed to the Office

THE FRAUD PREVENTION SYSTEM IDENTIFIED MILLIONS IN MEDICARE SAVINGS, BUT THE DEPARTMENT COULD STRENGTHEN SAVINGS DATA

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL THE FRAUD PREVENTION SYSTEM IDENTIFIED MILLIONS IN MEDICARE SAVINGS, BUT THE DEPARTMENT COULD STRENGTHEN SAVINGS DATA BY IMPROVING ITS

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL THE FRAUD PREVENTION SYSTEM IDENTIFIED MILLIONS IN MEDICARE SAVINGS, BUT THE DEPARTMENT COULD STRENGTHEN SAVINGS DATA BY IMPROVING ITS

February 18, 2016 OIG-16-40-D

Colorado Springs Utilities, Colorado, Has Adequate Policies, Procedures, and Business Practices to Effectively Manage Its FEMA Public Assistance Grant Funding February 18, 2016 OIG-16-40-D DHS OIG HIGHLIGHTS

Colorado Springs Utilities, Colorado, Has Adequate Policies, Procedures, and Business Practices to Effectively Manage Its FEMA Public Assistance Grant Funding February 18, 2016 OIG-16-40-D DHS OIG HIGHLIGHTS

Metropolitan Community College s Administration of the Title IV Programs FINAL AUDIT REPORT

Metropolitan Community College s Administration of the Title IV Programs FINAL AUDIT REPORT ED-OIG/A07K0003 May 2012 Our mission is to promote the efficiency, effectiveness, and integrity of the Department's

Metropolitan Community College s Administration of the Title IV Programs FINAL AUDIT REPORT ED-OIG/A07K0003 May 2012 Our mission is to promote the efficiency, effectiveness, and integrity of the Department's

SUMMARY: The Small Business Administration (SBA) proposes to add a new system

proposes to add a new system") This document is scheduled to be published in the Federal Register on 10/27/2015 and available online at http://federalregister.gov/a/2015-27257, and on FDsys.gov Billing Code: 8025-01 SMALL BUSINESS ADMINISTRATION

This document is scheduled to be published in the Federal Register on 10/27/2015 and available online at http://federalregister.gov/a/2015-27257, and on FDsys.gov Billing Code: 8025-01 SMALL BUSINESS ADMINISTRATION

The Environmental Careers Organization Reported Outlays for Five EPA Cooperative Agreements

OFFICE OF INSPECTOR GENERAL Attestation Report Catalyst for Improving the Environment The Environmental Careers Organization Reported Outlays for Five EPA Cooperative Agreements Report No. 2007-4-00065

OFFICE OF INSPECTOR GENERAL Attestation Report Catalyst for Improving the Environment The Environmental Careers Organization Reported Outlays for Five EPA Cooperative Agreements Report No. 2007-4-00065

AGENCY FOR HEALTHCARE RESEARCH AND QUALITY: MONITORING PATIENT SAFETY GRANTS

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL AGENCY FOR HEALTHCARE RESEARCH AND QUALITY: MONITORING PATIENT SAFETY GRANTS Daniel R. Levinson Inspector General June 2006 OEI-07-04-00460

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL AGENCY FOR HEALTHCARE RESEARCH AND QUALITY: MONITORING PATIENT SAFETY GRANTS Daniel R. Levinson Inspector General June 2006 OEI-07-04-00460

DEPARTMENT OF HEALTH AND HUMAN SERVICES OFFICE OF AUDIT SERVICES 233 NORTH MICHIGAN AVENUE CHICAGO, ILLINOIS 60601. April 23,2002

DEPARTMENT OF HEALTH AND HUMAN SERVICES OFFICE OF AUDIT SERVICES 233 NORTH MICHIGAN AVENUE CHICAGO, ILLINOIS 60601 REGION V OFFICE OF INSPECTOR GENERAL UN: A-05-0 l-00044 April 23,2002 Mr. Michael O Keefe

DEPARTMENT OF HEALTH AND HUMAN SERVICES OFFICE OF AUDIT SERVICES 233 NORTH MICHIGAN AVENUE CHICAGO, ILLINOIS 60601 REGION V OFFICE OF INSPECTOR GENERAL UN: A-05-0 l-00044 April 23,2002 Mr. Michael O Keefe

Audit of Controls Over Contract Payments FINAL AUDIT REPORT

Audit of Controls Over Contract Payments FINAL AUDIT REPORT ED-OIG/A07-A0015 March 2001 Our mission is to promote the efficient U.S. Department of Education and effective use of taxpayer dollars Office

Audit of Controls Over Contract Payments FINAL AUDIT REPORT ED-OIG/A07-A0015 March 2001 Our mission is to promote the efficient U.S. Department of Education and effective use of taxpayer dollars Office

OAIG-AUD (ATTN: AFTS Audit Suggestions) Inspector General, Department of Defense 400 Army Navy Drive (Room 801) Arlington, VA 22202-2884

Inspector General, Department of Defense 400 Army Navy Drive (Room 801) Arlington, VA 22202-2884") Additional Copies To obtain additional copies of this report, contact the Secondary Reports Distribution Unit of the Audit Followup and Technical Support Directorate at (703) 604-8937 (DSN 664-8937) or

Additional Copies To obtain additional copies of this report, contact the Secondary Reports Distribution Unit of the Audit Followup and Technical Support Directorate at (703) 604-8937 (DSN 664-8937) or

ARKANSAS GENERALLY SUPPORTED ITS CLAIM FOR FEDERAL MEDICAID REIMBURSEMENT

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL ARKANSAS GENERALLY SUPPORTED ITS CLAIM FOR FEDERAL MEDICAID REIMBURSEMENT Inquiries about this report may be addressed to the Office

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL ARKANSAS GENERALLY SUPPORTED ITS CLAIM FOR FEDERAL MEDICAID REIMBURSEMENT Inquiries about this report may be addressed to the Office

United States Department of Agriculture. OFFICE OF INSPECTOR GENERAl

United States Department of Agriculture OFFICE OF INSPECTOR GENERAl Risk Management Agency National Program Operations Reviews 05601-0001-22 April 2015 10401-0001-22 Risk Management Agency National Program

United States Department of Agriculture OFFICE OF INSPECTOR GENERAl Risk Management Agency National Program Operations Reviews 05601-0001-22 April 2015 10401-0001-22 Risk Management Agency National Program

PERFORMANCE BONDS AND LABOUR AND MATERIAL PAYMENT BONDS: WHAT THE CONSTRUCTION INDUSTRY SHOULD KNOW

PERFORMANCE BONDS AND LABOUR AND MATERIAL PAYMENT BONDS: WHAT THE CONSTRUCTION INDUSTRY SHOULD KNOW Deborah E. Palter, B.A., LL.B., J.D. What is a Bond? A bond is a three party written agreement. The three

PERFORMANCE BONDS AND LABOUR AND MATERIAL PAYMENT BONDS: WHAT THE CONSTRUCTION INDUSTRY SHOULD KNOW Deborah E. Palter, B.A., LL.B., J.D. What is a Bond? A bond is a three party written agreement. The three

Report Number: A-03-04-002 13

DEPARTMENT OF HEALTH & HUMAN SERVICES OFFICE OF INSPECTOR GENERAL OFFICE OF AUDIT SERVICES 150 S. INDEPENDENCE MALL WEST SUITE 3 16 PHILADELPHIA, PENNSYLVANIA 19 106-3499 Report Number: A-03-04-002 13

DEPARTMENT OF HEALTH & HUMAN SERVICES OFFICE OF INSPECTOR GENERAL OFFICE OF AUDIT SERVICES 150 S. INDEPENDENCE MALL WEST SUITE 3 16 PHILADELPHIA, PENNSYLVANIA 19 106-3499 Report Number: A-03-04-002 13

Office of Inspector General

Audit Report OIG-07-043 GENERAL MANAGEMENT: Departmental Offices Did Not Have An Effective Workers Compensation Program July 13, 2007 Office of Inspector General Department of the Treasury Contents Audit

Audit Report OIG-07-043 GENERAL MANAGEMENT: Departmental Offices Did Not Have An Effective Workers Compensation Program July 13, 2007 Office of Inspector General Department of the Treasury Contents Audit

Expedited Dispute Resolution Bond (P3 Form)

") Expedited Dispute Resolution Bond (P3 Form) Bond No. KNOW ALL WHO SHALL SEE THESE PRESENTS: THAT WHEREAS, (the "Owner") has awarded to (the "Obligee"), a Public-Private Agreement (the PPA ) for a project

Expedited Dispute Resolution Bond (P3 Form) Bond No. KNOW ALL WHO SHALL SEE THESE PRESENTS: THAT WHEREAS, (the "Owner") has awarded to (the "Obligee"), a Public-Private Agreement (the PPA ) for a project

ARTICLE I General. These Procedures are being adopted by the School District board of education as debt issuance disclosure best practices.

Municipal Finance Disclosure and Continuing Disclosure Policies and Procedures ARTICLE I General Section 1.1. Purpose The purpose of the Chenango Valley Central School District Municipal Finance Disclosure

Municipal Finance Disclosure and Continuing Disclosure Policies and Procedures ARTICLE I General Section 1.1. Purpose The purpose of the Chenango Valley Central School District Municipal Finance Disclosure

AN ACT IN THE COUNCIL OF THE DISTRICT OF COLUMBIA

AN ACT IN THE COUNCIL OF THE DISTRICT OF COLUMBIA To amend the District of Columbia Procurement Practices Act of 1985 to make the District s false claims act consistent with federal law and thereby qualify

AN ACT IN THE COUNCIL OF THE DISTRICT OF COLUMBIA To amend the District of Columbia Procurement Practices Act of 1985 to make the District s false claims act consistent with federal law and thereby qualify

COLORADO CLAIMED UNALLOWABLE MEDICAID INPATIENT SUPPLEMENTAL PAYMENTS

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL COLORADO CLAIMED UNALLOWABLE MEDICAID INPATIENT SUPPLEMENTAL PAYMENTS Inquiries about this report may be addressed to the Office of Public

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL COLORADO CLAIMED UNALLOWABLE MEDICAID INPATIENT SUPPLEMENTAL PAYMENTS Inquiries about this report may be addressed to the Office of Public

REPORT ON INDEPENDENT EVALUATION AND ASSESSMENT OF INTERNAL CONTROL FOR CONTRACT OVERSIGHT

REPORT ON INDEPENDENT EVALUATION AND ASSESSMENT OF INTERNAL CONTROL FOR CONTRACT OVERSIGHT SUBMITTED TO THE U.S. SECURITIES AND EXCHANGE COMMISSION OFFICE OF INSPECTOR GENERAL Cotton & Company LLP Auditors

REPORT ON INDEPENDENT EVALUATION AND ASSESSMENT OF INTERNAL CONTROL FOR CONTRACT OVERSIGHT SUBMITTED TO THE U.S. SECURITIES AND EXCHANGE COMMISSION OFFICE OF INSPECTOR GENERAL Cotton & Company LLP Auditors

Los Angeles County Metropolitan Transportation Authority Office of the Inspector General Medicare Part B Reimbursements to Retirees

Los Angeles County Metropolitan Transportation Authority Medicare Part B Reimbursements to Retirees Several procedural refinements are needed to ensure that reimbursements are discontinued for deceased

Los Angeles County Metropolitan Transportation Authority Medicare Part B Reimbursements to Retirees Several procedural refinements are needed to ensure that reimbursements are discontinued for deceased

GAO FEDERAL STUDENT LOAN PROGRAMS. Opportunities Exist to Improve Audit Requirements and Oversight Procedures. Report to Congressional Committees

GAO United States Government Accountability Office Report to Congressional Committees July 2010 FEDERAL STUDENT LOAN PROGRAMS Opportunities Exist to Improve Audit Requirements and Oversight Procedures

GAO United States Government Accountability Office Report to Congressional Committees July 2010 FEDERAL STUDENT LOAN PROGRAMS Opportunities Exist to Improve Audit Requirements and Oversight Procedures

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION The Office of Disclosure Continued to Improve Compliance With the Freedom of Information Act Requirements August 29, 2008 Reference Number: 2008-30-164

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION The Office of Disclosure Continued to Improve Compliance With the Freedom of Information Act Requirements August 29, 2008 Reference Number: 2008-30-164

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL BACKGROUND

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL AUDIT SERVICES March 25, 2016 Control Number ED-OIG/A19P0007 Ruth Neild Delegated Duties of the Director Institute of Education Sciences

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL AUDIT SERVICES March 25, 2016 Control Number ED-OIG/A19P0007 Ruth Neild Delegated Duties of the Director Institute of Education Sciences

AUDIT REPORT THE ADMINISTRATION OF CONTRACTS AND AGREEMENTS FOR LINGUISTIC SERVICES BY THE DRUG ENFORCEMENT ADMINISTRATION AUGUST 2002 02-33

AUDIT REPORT THE ADMINISTRATION OF CONTRACTS AND AGREEMENTS FOR LINGUISTIC SERVICES BY THE DRUG ENFORCEMENT ADMINISTRATION AUGUST 2002 02-33 THE ADMINISTRATION OF CONTRACTS AND AGREEMENTS FOR LINGUISTIC

AUDIT REPORT THE ADMINISTRATION OF CONTRACTS AND AGREEMENTS FOR LINGUISTIC SERVICES BY THE DRUG ENFORCEMENT ADMINISTRATION AUGUST 2002 02-33 THE ADMINISTRATION OF CONTRACTS AND AGREEMENTS FOR LINGUISTIC

EVALUATION REPORT. Weaknesses Identified During the FY 2014 Federal Information Security Management Act Review. March 13, 2015 REPORT NUMBER 15-07

EVALUATION REPORT Weaknesses Identified During the FY 2014 Federal Information Security Management Act Review March 13, 2015 REPORT NUMBER 15-07 EXECUTIVE SUMMARY Weaknesses Identified During the FY 2014

EVALUATION REPORT Weaknesses Identified During the FY 2014 Federal Information Security Management Act Review March 13, 2015 REPORT NUMBER 15-07 EXECUTIVE SUMMARY Weaknesses Identified During the FY 2014

JAMS Dispute Resolution Rules for Surety Bond Disputes

JAMS Dispute Resolution Rules for Surety Bond Disputes Effective February 2015 JAMS DISPUTE RESOLUTION RULES FOR SURETY BOND DISPUTES JAMS provides arbitration and mediation services worldwide. We resolve

JAMS Dispute Resolution Rules for Surety Bond Disputes Effective February 2015 JAMS DISPUTE RESOLUTION RULES FOR SURETY BOND DISPUTES JAMS provides arbitration and mediation services worldwide. We resolve

Security Concerns with Federal Emergency Management Agency's egrants Grant Management System

Security Concerns with Federal Emergency Management Agency's egrants Grant Management System November 19, 2015 OIG-16-11 DHS OIG HIGHLIGHTS Security Concerns with Federal Emergency Management Agency s

Security Concerns with Federal Emergency Management Agency's egrants Grant Management System November 19, 2015 OIG-16-11 DHS OIG HIGHLIGHTS Security Concerns with Federal Emergency Management Agency s

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Fiscal Year 2015 Statutory Review of Restrictions on Directly Contacting Taxpayers July 7, 2015 Reference Number: 2015-30-061 This report has cleared the

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Fiscal Year 2015 Statutory Review of Restrictions on Directly Contacting Taxpayers July 7, 2015 Reference Number: 2015-30-061 This report has cleared the

EPA Has Improved Its Response to Freedom of Information Act Requests But Further Improvement Is Needed

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Public Liaison Report Catalyst for Improving the Environment EPA Has Improved Its Response to Freedom of Information Act Requests But Further

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Public Liaison Report Catalyst for Improving the Environment EPA Has Improved Its Response to Freedom of Information Act Requests But Further

U.S. Small Business Administration Surety Bond Guarantee Program. Opening the Door to Bonding

U.S. Small Business Administration Surety Bond Guarantee Program Opening the Door to Bonding What Is a Surety Bond? A three party written agreement between the surety, the contractor and the project owner.

U.S. Small Business Administration Surety Bond Guarantee Program Opening the Door to Bonding What Is a Surety Bond? A three party written agreement between the surety, the contractor and the project owner.

U.S. Chemical Safety and Hazard Investigation Board Should Determine the Cost Effectiveness of Performing Improper Payment Recovery Audits

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL U.S. Chemical Safety and Hazard Investigation Board Should Determine the Cost Effectiveness of Performing Improper Payment Recovery Audits

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL U.S. Chemical Safety and Hazard Investigation Board Should Determine the Cost Effectiveness of Performing Improper Payment Recovery Audits

4. A copy of the surety bond required by Rule 6.05, if applicable; investment adviser representatives in Mississippi, and

Rule 6.05 Application for Investment Adviser Registration. A. Initial Application. The application for initial registration as an investment adviser pursuant to Section 75-71-403(a) of the Act shall be

Rule 6.05 Application for Investment Adviser Registration. A. Initial Application. The application for initial registration as an investment adviser pursuant to Section 75-71-403(a) of the Act shall be

In order to adjudicate an appeal, OPM requires claimants or their authorized representatives to submit the following information:

SYSTEM NAME: Health Claims Disputes External Review Services. SYSTEM LOCATION: Office of Personnel Management, 1900 E Street NW., Washington, DC 20415. CATEGORIES OF INDIVIDUALS COVERED BY THE SYSTEM:

SYSTEM NAME: Health Claims Disputes External Review Services. SYSTEM LOCATION: Office of Personnel Management, 1900 E Street NW., Washington, DC 20415. CATEGORIES OF INDIVIDUALS COVERED BY THE SYSTEM:

Congressionally Requested Inquiry Into EPA s Handling of Freedom of Information Act Requests

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Special Report Catalyst for Improving the Environment Congressionally Requested Inquiry Into EPA s Handling of Freedom of Information Act

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Special Report Catalyst for Improving the Environment Congressionally Requested Inquiry Into EPA s Handling of Freedom of Information Act