Construction Contractors

|

|

|

- Reginald Harrell

- 8 years ago

- Views:

Transcription

1 Construction Contractors Edward K. Zollars Phoenix, Arizona Resources Website: 1

2 2

3 3

4 4

5 5

6 Day's Outline Accounting and Auditing Tax Issues 6

7 Day's Outline Accounting and Auditing Outline of Accounting & Auditing Accounting and Reporting Issues Example Audit Program Highlights Example Disclosure Checklist Internal Controls Example Statements Issue of Going Concern Day's Outline Income Tax Issues Overview Cost properly allocable to contracts Capitalization of production period interest Methods of Accounting Other than Long-Term Contracts Completed Contract Method Percentage of Completion Method Look-Back Method Adjustment 7

8 Day's Outline Income Tax Issues Changing Accounting Methods AMT Considerations Accounting & Auditing Module 1 8

9 Accounting & Auditing Authoritative Literature Industry Background Accounting for Construction Contractors Other Issues Joint Ventures Tax vs. Book Financial Statement Presentation Homebuilders Issues Auditing Contractors Authoritative Literature ARB No. 45, Long-Term Construction Type Contracts (1955) AICPA Statement of Position 81-1 (1981) AICPA Audit and Accounting Guide: Construction Contractors (2010 Revision) AICPA Audit Risk Alert and Accounting Reporting Alerts (2010) FASB Codification Project ( Section 910 (Effective July 1, 2009) 9

AICPA Audit Risk Alert and Accounting Reporting Alerts (2010) FASB Codification Project (http://asc.fasb.")

10 FASB Codification 605 Revenue Recognition 35 Construction-Type and Production-Type Contracts 00 Status 05 Overview and Background 15 Scope and Scope Exceptions 20 Glossary 25 Recognition 45 Other Presentation Matters 50 Disclosures 55 Implementation Guidance and Illustrations 75 XBRL Elements FASB Codification 910 Contractors Construction 10 Overall 20 Contract Costs 235 Notes to Financial Statements 310 Receivables 330 Inventory 340 Other Assets and Deferred Costs 360 Property, Plant and Equipment 405 Liabilities 605 Revenue Recognition 810 Consolidation 10

11 Construction Industry Background Accounting Standards vs. Reporting Standards Types of Contractors General Contractors Subcontractors Construction Manager Characteristics of Contractors ASC Although the construction industry is difficult to define because of its diversity, certain characteristics are common to entities in the industry. The most basic characteristic is that work is performed under contractual arrangements with customers. A contractor, regardless of the type of construction activity or the type of contractor, typically enters into an agreement with a customer to build or to make improvements on a tangible property to the customer's specification. 11

12 Characteristics of Contractors ASC The contract with the customer specifies the work to be performed, specifies the basis of determining the amount and terms of payment of the contract price, and generally requires total performance before the contractor's obligation is discharged. Unlike the work of many manufacturers, the construction activities of a contractor are usually performed at job sites owned by customers rather than at a central place of business, and each contract usually involves the production of a unique property rather than repetitive production of identical products. Other Characteristics ASC A contractor normally obtains the contracts that generate revenue or sales by bidding or negotiating for specific projects. A contractor bids for or negotiates the initial contract price based on an estimate of the cost to complete the project and the desired profit margin, although the initial price may be changed or renegotiated. A contractor may be exposed to significant risks in the performance of a contract, particularly a fixed-price contract. 12

13 Other Characteristics ASC Customers (usually referred to as owners) frequently require a contractor to post a performance and a payment bond as protection against the contractor's failure to meet performance and payment requirements. The costs and revenues of a contractor are typically accumulated and accounted for by individual contracts or contract commitments extending beyond one accounting period, which complicates the management, accounting, and auditing processes. Other Characteristics ASC The nature of a contractor's risk exposure varies with the type of contract. The several types of contracts used in the construction industry are described in Subtopic The four basic types of contracts used based on their pricing arrangements are fixedprice or lump-sum contracts, unit-price contracts, cost-type contracts, and time-and-materials contracts. 13

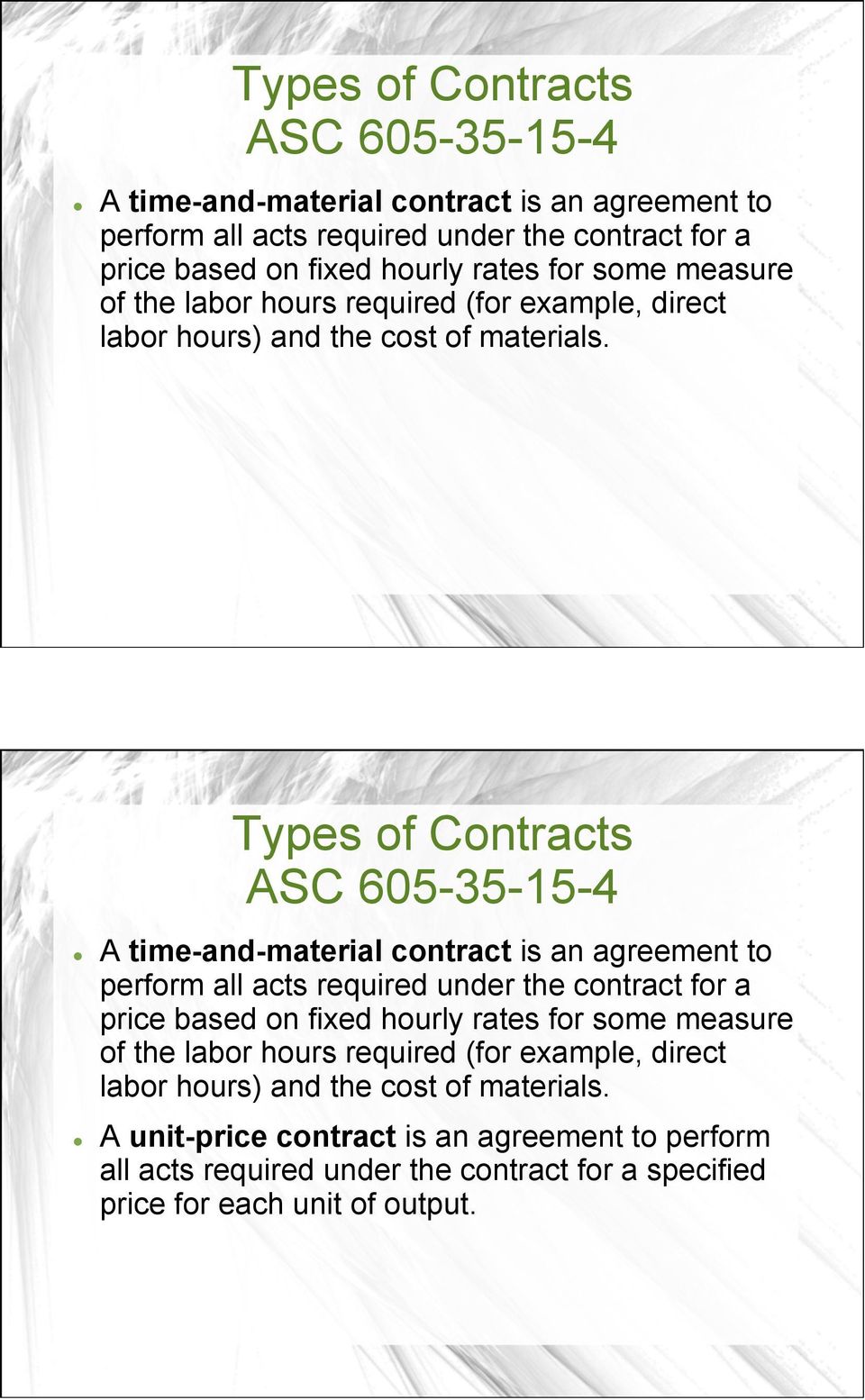

14 Types of Contracts ASC A fixed-price contract is an agreement to perform all acts under the contract for a stated price. Types of Contracts ASC A fixed-price contract is an agreement to perform all acts under the contract for a stated price. A cost-type (including cost-plus) contract is an agreement to perform under a contract for a price determined on the basis of a defined relationship to the costs to be incurred, for example, the costs of all acts required plus a fee, which may be a fixed amount or a fixed percentage of the costs incurred. 14

15 Types of Contracts ASC A time-and-material contract is an agreement to perform all acts required under the contract for a price based on fixed hourly rates for some measure of the labor hours required (for example, direct labor hours) and the cost of materials. Types of Contracts ASC A time-and-material contract is an agreement to perform all acts required under the contract for a price based on fixed hourly rates for some measure of the labor hours required (for example, direct labor hours) and the cost of materials. A unit-price contract is an agreement to perform all acts required under the contract for a specified price for each unit of output. 15

16 Bonding Referenced at ASC Principal reason contractors require financial statements with attest reports Post a bond equal to percentage of cost to complete contract Types of Bonds Bid bond Performance bond Payment, or labor-and-materials bond 16

17 Purpose of Bond Protects buyer from certain types of damages from nonperformance Surety provides that assurance to the buyer Investigates the contractor Primary interest is in contractor's ability to fulfill his obligations Sureties place great reliance on the outside accountants' report and abilities Bonding Agents and Sureties Bonding agent works to finds a surety for the contractor CPA can assist by Educate client Job cost system Issuance of financial statements Helping to assure are providing information the surety wants However, watch for EI

18 Analysis of the Statements Looking to determine bonding capacity Looks at maximum per job, and maximum for all jobs Key interest in contractor's net working capital Adjusted current assets less Current liabilities Adjustments to Current Assets Remove assets not recoverable in cash if contractor liquidates Reduce to a (potentially mechanical) estimate of liquidation value for assets not likely to be fully recovered in cash if contractor liquidates 18

estimate of liquidation value for assets not likely to be fully recovered in cash if")

19 Adjustments to Current Assets Assets normally adjusted or removed Receivables from shareholders Receivables from employees Retainage receivable Other receivables over 90 days old Inventories Prepaid expenses Bonding Capacities Rules of thumb Maximum single job bond: times net working capital Maximum total bonding: times adjusted net equity For net equity can look at revaluing other assets Can assist in providing information for calculating adjustments, again subject to EI issues Example worksheets 19

20 Other Items Considered Gross profit in backlog Amount of underbillings Quick ratio of more than 1:1 Liabilities to net worth Interest bearing debt to net worth Debt coverage Overhead to contract revenue Comparison to averages 20

21 Lien Rights Contractor is working on someone else's property State law generally grants lien rights However, must be handled properly Rules vary from state to state (don't presume home state rules) Contractor needs to get this right Contract Changes Change order (ASC to 28) Claim (ASC ) Extras (Contract Option and Addition ASC ) Incentives and penalties (ASC to 31) 21

22 Billing Practices Based on contract terms for specific contract Example billing systems Completion of stages of the contract Costs incurred on the contract Architect/engineer estimates of completion Specific time schedules Quantity measure of unit price Front end loading is a financing technique (and lack of same may be indicative of optimistic accounting) Front End Loading Helps with cash up front Contractor must be aware of dearth of cash at the end of the job Retentions create opposite issues Normally 5-10% of billings Held until specified level of completion Must consider both retentions and front end loading in planning job and related cash needs 22

23 Joint Ventures Regular feature for many construction contractors Business entity owned by a group of businesses Normally LLCs today unless state law has anti-llc bias (California and Texas, for instance) Financial & Tax Reporting Financial statements required Financing Bonding Income tax methods Differ from GAAP Deferred tax issues Different goals for each type of reporting for both users and client 23

24 GAAP/Tax Diffrences Note that in real world both are often compromised Example to illustrate differences even when using the same method ASC Adjustments to the original estimates of the total contract revenue, total contract cost, or extent of progress toward completion are often required as work progresses under the contract and as experience is gained, even though the scope of the work required under the contract may not change. The nature of accounting for contracts is such that refinements of the estimating process for changing conditions and new developments are continuous and characteristic of the process. 24

25 ASC Additional information that enhances and refines the estimating process is often obtained after the balance sheet date but before the financial statements are issued or are available to be issued (as discussed in Section ); except as indicated in paragraph , such information should result in an adjustment of the unissued financial statements. ASC Additional information that enhances and refines the estimating process is often obtained after the balance sheet date but before the Events financial occurring statements after are issued or are the available date of the to financial be issued statements (as discussed in Section ); that are outside except the normal as indicated exposure in paragraph , and risk such aspects information of the contract should shall result in an not be considered refinements of the adjustment of the unissued financial statements. estimating process of the prior year but should be disclosed as subsequent events. 25

26 IRS Notice Q-24: In determining percentage of completion for a particular taxable year, when are total contract costs and total contract revenues to be estimated? A-24: Total contract revenue and total contract costs are to be estimated based on the facts and reasonable estimates as of the last day of the taxable year. Events that occur after the end of the taxable year that were not reasonably subject to estimate as of the last day of the taxable year are not taken into account. 26

27 Construction Industry Operations Preparing Cost Estimate and Bids Entering into a Contract Planning and Starting the Job 27

28 Cost Estimate and Bids Crucial for contractors Overestimate costs and won't get job Underestimate costs and may bankrupt the contractor Influence issues Complexities of the job Labor and material market and supplies Experience doing similar work Reputation of engineer or architect Season, weather and timing Cost Estimate and Bids Influence issues Reputation of the owner Opportunities to add change orders Specifications of the plan Competition and the marketplace Incentive or penalty clauses Anticipated cash flows and ability to front end load billings Unique risk considerations 28

29 Entering Into Contract Owner selects a contractor from the bids received Formal agreement reached Due to change orders, initial agreement represents only starting understanding So must understand this will very likely not be the final outline of what happened Planning & Starting Job Contractor needs to plan the job itself, move equipment into place, order materials, establish job site office, contract with subcontractors and hire labor Job cost system in place Solid estimates documented and in place Control system in place to assure proper job cost capture Consider contractor size and methods of operation exercise judgement 29

30 Accounting For Construction Contractors Main standards came from SOP 81-1 (Now effectively in ASC 910) Very strong preference for Percentage of Completion (ASC ) Types of Contracts Covered Fixed price/lump sum Cost type products (including cost plus) Time and material Unit price Accounting for Construction Contractors Profit Center Accounting Job cost system May combine small contracts or, if reasonable, related contracts Determinations made at individual job level 30

31 Percentage of Completion Method Reasonably Dependable Estimates Hazards of Estimates Control based on reliability of job cost system Need to evaluate how good estimates have been in the past Can find inability to produce estimates as reason not to use percentage of completion (ASC ) ASC Contract revenues and costs are estimated in a wide variety of ways ranging from rudimentary procedures to complex methods and systems. Regardless of the techniques used, a contractor's estimating procedures should provide reasonable assurance of a continuing ability to produce reasonably dependable estimates. The type of estimating procedures appropriate in a particular set of circumstances depends on a careful evaluation of the costs and benefits of developing the procedures. The ability to produce reasonably dependable estimates that would justify the use of the percentage-of-completion method as recommended in paragraph does not depend on the elaborateness of the estimating procedures used. 31

32 Past Accuracy ASC Ability to estimate covers more than the estimating and documentation of contract revenues and costs; it covers a contractor's entire contract administration and management control system. The ability to produce reasonably dependable estimates depends on all the procedures and personnel that provide financial or production information on the status of contracts. It encompasses systems and personnel not only of the accounting department but of all areas of the entity that participate in production control, cost control, administrative control, or accountability for contracts. Previous reliability of a contractor's estimating process is usually an indication of continuing reliability, particularly if the present circumstances are similar to those that prevailed in the past. 32

33 33

34 ASC The percentage-of-completion method is considered preferable as an accounting policy in circumstances in which reasonably dependable estimates can be made and in which all the following conditions exist: 1. Contracts executed by the parties normally include provisions that clearly specify the enforceable rights regarding goods or services to be provided and received by the parties, the consideration to be exchanged, and the manner and terms of settlement. 2. The buyer can be expected to satisfy all obligations under the contract. 3. The contractor can be expected to perform all contractual obligations. 34

35 ASC The percentage-of-completion method is considered preferable as an accounting policy in circumstances in which reasonably dependable estimates can be made and in which all the following conditions exist: 1. Contracts executed by the parties normally include provisions that clearly specify the enforceable rights regarding goods or services to be provided and received by the parties, the consideration to be exchanged, and the manner and terms of settlement. 2. The buyer can be expected to satisfy all obligations under the contract. 3. The contractor can be expected to perform all contractual obligations. ASC The percentage-of-completion method is considered preferable as an accounting policy in circumstances in which reasonably dependable estimates can be made and in which all the following conditions exist: 1. Contracts executed by the parties normally include provisions that clearly specify the enforceable rights regarding goods or services to be provided and received by the parties, the consideration to be exchanged, and the manner and terms of settlement. 2. The buyer can be expected to satisfy all obligations under the contract. 3. The contractor can be expected to perform all contractual obligations. 35

36 ASC The percentage-of-completion method is considered preferable as an accounting policy in circumstances in which reasonably dependable estimates can be made and in which all the following conditions exist: 1. Contracts executed by the parties normally include provisions that clearly specify the enforceable rights regarding goods or services to be provided and received by the parties, the consideration to be exchanged, and the manner and terms of settlement. 2. The buyer can be expected to satisfy all obligations under the contract. 3. The contractor can be expected to perform all contractual obligations. ASC The percentage-of-completion method is considered preferable as an accounting policy in circumstances in which reasonably dependable estimates can be made and in which all the following conditions exist: 1. Contracts executed by the parties normally include provisions that clearly specify the enforceable rights regarding goods or services to be provided and received by the parties, the consideration to be exchanged, and the manner and terms of settlement. 2. The buyer can be expected to satisfy all obligations under the contract. 3. The contractor can be expected to perform all contractual obligations. 36

37 ASC The percentage-of-completion method is considered preferable as an accounting policy in circumstances in which reasonably dependable estimates can be made and in which all the following conditions exist: 1. Contracts executed by the parties normally include provisions that clearly specify the enforceable rights regarding goods or services to be provided and received by the parties, the consideration to be exchanged, and the manner and terms of settlement. 2. The buyer can be expected to satisfy all obligations under the contract. 3. The contractor can be expected to perform all contractual obligations. ASC For entities engaged on a continuing basis in the production and delivery of goods or services under contractual arrangements and for whom contracting represents a significant part of their operations, the presumption is that they have the ability to make estimates that are sufficiently dependable to justify the use of the percentage-of-completion method of accounting. Persuasive evidence to the contrary is necessary to overcome that presumption. The ability to produce reasonably dependable estimates is an essential element of the contracting business. Accordingly, entities with significant contracting operations generally have the ability to produce reasonably dependable estimates and for such entities the percentage-of-completion method of accounting is preferable in most circumstances. 37

38 ASC For entities engaged on a continuing basis in the production and delivery of goods or services under contractual arrangements and for whom contracting represents a significant part of their operations, the presumption is that they have the ability to make estimates that are sufficiently dependable to justify the use of the percentage-of-completion method of accounting. Persuasive evidence to the contrary is necessary to overcome that presumption. The ability to produce reasonably dependable estimates is an essential element of the contracting business. Accordingly, entities with significant contracting operations generally have the ability to produce reasonably dependable estimates and for such entities the percentage-of-completion method of accounting is preferable in most circumstances. ASC For entities engaged on a continuing basis in the production and delivery of goods or services under contractual arrangements and for whom contracting represents a significant part of their operations, the presumption is that they have the ability to make estimates that are sufficiently dependable to justify the use of the percentage-of-completion method of accounting. Persuasive evidence to the contrary is necessary to overcome that presumption. The ability to produce reasonably dependable estimates is an essential element of the contracting business. Accordingly, entities with significant contracting operations generally have the ability to produce reasonably dependable estimates and for such entities the percentage-of-completion method of accounting is preferable in most circumstances. 38

39 ASC An entity using the percentage-of-completion method as its basic accounting policy shall use the completed-contract method for a single contract or a group of contracts for which reasonably dependable estimates cannot be made or for which inherent hazards make estimates doubtful. ASC An entity using the percentage-of-completion method as its basic accounting policy shall use the completed-contract method for a single contract or a group of contracts for which reasonably dependable estimates cannot be made or for which inherent hazards make estimates doubtful. 39

40 ASC An entity using the percentage-of-completion method as its basic accounting policy shall use the completed-contract method for a single contract or a group of contracts for which reasonably dependable estimates cannot be made or for which inherent hazards make estimates doubtful. ASC An entity using the percentage-of-completion method as its basic accounting policy shall use the completed-contract method for a single contract or a group of contracts for which reasonably dependable estimates cannot be made or for which inherent hazards make estimates doubtful. 40

41 Combining Contracts Closely related contracts that represent a single project can be combined for GAAP purposes Presumption of uniform reporting of revenue and profit for combined contracts Requirements to combine (GAAP) ASC (Main) ASC (Production style contracts only) A group of contracts may be combined for accounting purposes if all the following conditions exist: a. The contracts are negotiated as a package in the same economic environment with an overall profit margin objective. Contracts not executed at the same time may be considered to have been negotiated as a package in the same economic environment only if the time period between the commitments of the parties to the individual contracts is reasonably short. The longer the period between the commitments of the parties to the contracts, the more likely it is that the economic circumstances affecting the negotiations have changed. 41

42 A group of contracts may be combined for accounting purposes if all the following conditions exist: b. The contracts constitute in essence an agreement to do a single project. A project for this purpose consists of construction, or related service activity with different elements, phases, or units of output that are closely interrelated or interdependent in terms of their design, technology, and function or their ultimate purpose or use A group of contracts may be combined for accounting purposes if all the following conditions exist: c. The contracts require closely interrelated construction activities with substantial common costs that cannot be separately identified with, or reasonably allocated to, the elements, phases, or units of output. d. The contracts are performed concurrently or in a continuous sequence under the same project management at the same location or at different locations in the same general vicinity. 42

43 A group of contracts may be combined for accounting purposes if all the following conditions exist: e. The contracts constitute in substance an agreement with a single customer. In assessing whether the contracts meet this criterion, the facts and circumstances relating to the other criteria should be considered. In some circumstances different divisions of the same entity would not constitute a single customer if, for example, the negotiations are conducted independently with the different divisions. On the other hand, two or more parties may constitute in substance a single customer if, for example, the negotiations are conducted jointly with the parties to do what in essence is a single project Contracts that meet all of these criteria may be combined for profit recognition and for determining the need for a provision for losses in accordance with paragraphs through The criteria shall be applied consistently to contracts with similar characteristics in similar circumstances. 43

44 Segmenting a Contract Two sets of criteria for other than units of production Normal criteria (ASC ) Special criteria (ASC ) Normal Criteria ASC A project may be segmented if all of the following steps were taken and are documented and verifiable: a. The contractor submitted bona fide proposals on the separate components of the project and on the entire project. b. The customer had the right to accept the proposals on either basis. c. The aggregate amount of the proposals on the separate components approximated the amount of the proposal on the entire project. 44

45 Alternative Criteria A project that does not meet the criteria in the preceding paragraph may be segmented only if it meets all of the following criteria: a. The terms and scope of the contract or project clearly call for separable phases or elements. b. The separable phases or elements of the project are often bid or negotiated separately. c. The market assigns different gross profit rates to the segments because of factors such as different levels of risk or differences in the relationship of the supply and demand for the services provided in different segments. Alternative Criteria A project that does not meet the criteria in the preceding paragraph may be segmented only if it meets all of the following criteria: d. The contractor has a significant history of providing similar services to other customers under separate contracts for each significant segment to which a profit margin higher than the overall profit margin on the project is ascribed. In applying this criterion, values assignable to the segments shall be on the basis of the contractor's normal historical prices and terms of such services to other customers. A contractor shall not segment on the basis of prices charged by other contractors, because it does not follow that those prices could have been obtained by a contractor who has no history in the market. 45

46 Alternative Criteria A project that does not meet the criteria in the preceding paragraph may be segmented only if it meets all of the following criteria: e. The significant history with customers who have contracted for services separately is one that is relatively stable in terms of pricing policy rather than one unduly weighted by erratic pricing decisions (responding, for example, to extraordinary economic circumstances or to unique customer-contractor relationships). Alternative Criteria A project that does not meet the criteria in the preceding paragraph may be segmented only if it meets all of the following criteria: f. The excess of the sum of the prices of the separate elements over the price of the total project is clearly attributable to cost savings incident to combined performance of the contract obligations (for example, cost savings in supervision, overhead, or equipment mobilization). Unless this condition is met, segmenting a contract with a price substantially less than the sum of the prices of the separate phases or elements would be inappropriate even if the other conditions are met. Acceptable price variations shall be allocated to the separate phases or elements in proportion to the prices ascribed to each. In all other situations a substantial difference in price (whether more or less) between the separate elements and the price of the total project is evidence that the contractor has accepted different profit margins. Accordingly, segmenting is not appropriate, and the contracts shall be the profit centers. 46

47 Alternative Criteria A project that does not meet the criteria in the preceding paragraph may be segmented only if it meets all of the following criteria: g. The similarity of services and prices in the contract segments and services and the prices of such services to other customers contracted separately should be documented and verifiable. Segmenting a Contract Again, special unit of production option available Found at ASC The flip side of ASC (not going to cover today except to mention) 47

48 Example of Effects of Combining vs. Segmenting See example Note that results may vary depending on which costs on incurred on which portion of contract (neither one is necessarily always best) Concern if client always makes this call in the way that gives the highest income 48

49 Methods of Measuring Progress ASC Cost to cost Variations of cost to cost Efforts expended Units of delivery Units of work performed Cost to cost most often used Customer Furnished Materials ASC through 24 Generally, if customer furnishes the materials, it should not be counted in the cost or revenue equation Exceptions Contractor responsible for nature, type, characteristics or specification of material or Contractor ultimately responsible for acceptability of performance based on the material Looking only at items to which contractor has risk 49

50 Change Orders ASC through 28 Modification of the original contract that effectively changes the contract without adding new provisions Unpriced change order costs (ASC ) Contract costs when incurred if it is not probable will be recovered through price change If is probable will be recovered, costs deferred and/or equal amount of revenue recognized until pricing agreed upon Change Orders Unpriced change orders If probable will recover in excess of costs and amount can be reliably estimated, adjust contract price when costs are recognized If change orders are in dispute or are unapproved both as to scope and price, treat as a claim 50

51 Contract Option or Addition Treated as separate contract if (ASC ) Delivered item differs significantly from original item Price negotiated without regard to original item or Deliverable similar, but price and cost relationship significantly different If fail tests Combined if meet proper criteria or Treated as change order on original contract Claims ASC Contractor seeks to collect amount in excess of contract price Delays Errors in specifications and designs Contract terminations Disputed change orders Revenue recognized only when Probable claim will result in additional revenue and Amount can be reasonably estimated 51

52 Claims Probability established by existence of all of the following conditions (ASC ) Clear legal basis for the claim Additional costs triggered by events unforeseen at contract date and not due to deficiencies of contractor s performance Costs associated with claim determinable and are reasonable in view of work performed Evidence supporting claim objective and verifiable (management s feel for the situation doesn t qualify) Claims Can decide to record only when claim has been received or awarded Methods of claim recognition should be disclosed in financial statements 52

53 Contract Costs ASC Direct costs incurred Indirect costs (overhead) incurred Estimated remaining costs to complete the job (both direct and indirect) (ASC ) Most significant variable impacting income earned Most vulnerable to manipulation (and it's rather obvious how to manipulate) May be combined with misclassifying costs incurred and/or otherwise overstating costs incurred Must be regularly reviewed Estimated Costs to Complete The estimated cost to complete (the other component of total estimated contract cost) is a significant variable in the process of determining income earned and is thus a significant factor in accounting for contracts. The latest estimate may be determined in a variety of ways and may be the same as the original estimate. The following approaches should be followed: a. Systematic and consistent procedures that are correlated with the cost accounting system should be used to provide a basis for periodically comparing actual and estimated costs. b. In estimating total contract costs, the quantities and prices of all significant elements of cost should be identified. c. The estimating procedures should provide that estimated cost to complete includes the same elements of cost that are included in actual accumulated costs. Also, those elements should reflect expected price increases. d. The effects of future wage and price escalations should be taken into account in cost estimates, especially when the contract performance will be carried out over a significant period of time. Escalation provisions should not be blanket overall provisions but should cover labor, materials, and indirect costs based on percentages or amounts that take into consideration experience and other pertinent data. e. Estimates of cost to complete should be reviewed periodically and revised as appropriate to reflect new information. 53

54 Calculation under PCM Estimate gross profit on entire contract Revenue Cost of Contract Revenue Gross Profit from Contract Estimating Revenue Estimating the revenue on a contract is an involved process that is affected by a variety of uncertainties that depend on the outcome of a series of future events. The estimates must be periodically revised throughout the life of the contract as events occur and as uncertainties are resolved. The major factors that must be considered in determining total estimated revenue include all of the following: 54

55 Estimating Revenue a. The basic contract price b. Contract options c. Change orders d. Claims e. Contract provisions for penalties and incentive payments, including award fees and performance incentives. Estimating Revenue All those factors and other special contract provisions shall be evaluated throughout the life of a contract in estimating total contract revenue to recognize revenues in the periods in which they are earned under the percentage-of completion method of accounting. 55

56 Calculation under PCM Estimates must be constantly revised using the best available information Affects financial reporting Also an important internal management tool 56

57 57

58 58

59 Joint Ventures Be aware of FASB Interpretation No. 46 may require consolidation (post-enron situation) where in the past would not have been consolidated Capital contributions Cash recorded at value contributed Other assets recorded at book value Capital adjusted based on accounting method used (cost, equity or consolidation see reference to ASC provisions on corporate investments in ASC treatment is similar) Joint Ventures Transactions with venture Normally not revenue or income until realized through transaction with 3 rd party, however can be deemed arms length if all of the following met Transaction actually entered into at a verifiable arms length amount (not just an assertion) No substantial uncertainties regarding venturer's ability to perform Venture is creditworthy on its own and has independent financial substance 59

60 Joint Ventures Presentations, depending on size of investment, percentage controlled, ownership interests and Interpretation 46 tests Consolidation (full or partial) Expanded equity Equity method Cost Disclosure issues presented in checklist Accounting/Tax Differences For GAAP, generally only PCM is allowed Income taxes may allow Cash Standard accrual (with or without counting retentions) Percentage of completion (under tax rules) Completed contract Other elective variations of percentage of completion method 60

61 Accounting/Tax Differences Financial statement method may not be allowed for tax purposes (and vice versa) Joint venture is often its own tax reporting entity, with its own elections, methods, etc. Expected losses must be recorded immediately for tax purposes, but not currently deductible in full for income tax purposes Leads to deferred tax issues under SFAS No. 109 (now ASC 740) Financial Statement Presentation Issues Classified vs. Unclassified Balance Sheet Classified preferable for entities with one year or less operating cycle Unclassified preferable for entities with operating cycles in excess of one year If normal cycle is less than a year, but have a few longer contracts, can separately classify the long contracts If operating cycle > one year or use unclassified balance sheet, should disclose liquidation of components (ASC ) 61

62 Classified Balance Sheets Current contract related assets Accounts or retentions receivable Unbilled contract receivables Costs in excess of billings and estimated earnings on uncompleted contracts (underbillings) Other deferred contract costs Equipment specifically purchased for, or expected to be used solely on an individual contract Classified Balance Sheets Current contract related liabilities Accounts and retentions payable Accrued contract costs Billings in excess of costs and estimated earnings on uncompleted contracts (overbillings) Deferred taxes Advanced payments on contracts Obligations on equipment purchased for, or expected to be used solely on an individual contract (regardless of terms) 62

63 Classified Balance Sheets Other Balance Sheet Accounts Retentions receivable or payable not realized or paid within a normal operating cycle should be classified as noncurrent Joint venture investments are normally noncurrent unless venture expected to be completed and liquidated within the operating cycle Equipment that will be consumed during the life of the contract or abandoned at the end of the contract should be a contract cost Classified Balance Sheets Other Balance Sheet Accounts Excess billings Normally classified as work to be performed and classified as current liabilities However, to extent billings exceed total estimated costs at completion of the contract plus contract profits earned to date, such excess should be treated as deferred income 63

64 Offsetting and Netting Generally not allowed unless an actual right of offset exists ASC (big surprise) Do not offset underbillings and overbillings Advances on cost plus contracts not normally offset against costs unless the payment is definitely regarded as a payment on account of work in progress Disclosures in Financial Statements A number of disclosures are required in the financial statements See disclosure checklist Remember, user generally has a right to presume that all required disclosures have been made, so be careful of the implications if a disclosure is overlooked As well, internal accountants have virtually the same exposure as outside accountants 64

65 Homebuilders Contractor vs. Manufacturer Special treatment for those that build home on land it owns If build on customer's land, same treatment as other contracting However, if build on own land, then FASB 67 & 68 apply, and not SOP 81-1 (ASC and & 5) Homebuilder Accounting Deposit Method of Accounting All revenues and costs deferred until closing (ASC ) Note subtle difference from completed contract/tax treatment, where income recognized at substantial completion Accounting policy disclosure should describe deposit method see example disclosure Remember, this applies only if builder is building on his own land otherwise standard contracting rules apply 65

66 Auditing Contractors SAS 107 Audit Risk & Materiality in Conducting an Audit (AU 312, AU-C 320) Special risk areas for contractors Direct contract costs both actual to date and estimated costs to complete Measurement of progress towards completion Contract amounts (contract price, change orders, billings to date and accounts receivable) Expected total gross profit Reliance on estimate of costs to complete Understanding Entity SAS No. 109 Understanding the Entity (AU-C 315) - Requires understanding of internal control - Cannot skip and evaluate at maximum SAS No. 110 Performing Audit Procedures (AU-C 330) - Can internal controls be relied upon to reduce substantive testing? - If not, can substantive testing really provide necessary level of assurance? 66

67 Auditing Contractors Areas of control focus System of internal accounting controls Operating systems and procedures Project management systems Nature of contractor's activity History of performance and profitability Other relevant accounting and operating factors Remember goal is to obtain sufficient evidence to form a reasonable basis for an opinion Auditing Contractors FASB Statement of Financial Accounting Concepts #2 Definition of Materiality the magnitude of an omission or misstatement of accounting information that, in the light of surrounding circumstances, makes it probable that the judgment of a reasonable person relying on the information would have been changed or influenced by the omission or misstatement. Viewpoint of the decision maker reading the statements Involves both qualitative and quantitative issues 67

68 Auditing Contractors SAS 107's List of Misstatements (AU-C 450) An inaccuracy in gathering or processing data from which financial statements are prepared A difference between the amount, classification, or presentation of a reported financial statement element, account, or item and the amount, classification, or presentation that would have been reported under generally accepted accounting principles The omission of a financial statement element, account, or item A financial statement disclosure that is not presented in conformity with generally accepted accounting principles Auditing Contractors SAS 107's List of Misstatements The omission of information required to be disclosed in conformity with generally accepted accounting principles An incorrect accounting estimate arising, for example, from an oversight or misinterpretation of facts; and Management s judgements concerning an accounting estimate or the selection or application of accounting policies that the auditor may consider unreasonable or inappropriate. 68

69 Auditing Contractors Remember SAS 99 consideration of possible methods for fraud Manipulation of PCM items would be attractive to someone looking to manipulate the financial statements Auditing Contractors Have Internal Control Checklist beginning at page 9-1 Note that this would be a dream set of controls Evaluate the reasonability given the client's overall size and operation But remember the risks that exist when have a suboptimal system As well, remember that top management always can override the control systems. 69

70 Audit Procedures Consider whether some controls can be relied upon (or the issues if none can) Note that are now required to evaluate internal control Not allow to rubber stamp setting control at maximum and doing only substantive tests since SAS 109/110 In construction, wasn't really a good idea even before changes Consider detailed review of selected job administration files Accounting and Reporting Issues Reporting Issues Accounting Issues 70

71 Reporting Issues Management's Assertions Existence or occurrence Completeness Rights and obligations Valuation or allocation Presentation and disclosure All financial statements embody those assertions CPA duty to disclose knowledge of error in assertions Outside Accountants Reports Nonpublic Companies (SSARS) Audit SSARS Review Compilation (including no report compilations) Other Entities Audit SAS Review (in theory SSARS Review, but...) Unaudited 71

72 Independence Required for review (and essentially for an audit) Ethics Interpretation creates problems Ethics Interpretation Last revised January 27, 2005 Regulates provision of nonattest services, including Other accounting services Tax services Information system consulting (job cost systems) 72

73 Ethics Interpretation Client must agree to Make all management decisions and perform all management functions; Designate an individual who possesses suitable skill, knowledge, and/or experience, preferably within senior management, to oversee the services; Evaluate the adequacy and results of the services performed; Ethics Interpretation Client must agree to Accept responsibility for the results of the services; and Establish and maintain internal controls, including monitoring ongoing activities. 73

74 Ethics Interpretation Must document in writing the understanding on the following with the client: Objectives of the engagement Services to be performed Client's acceptance of its responsibilities Member's responsibilities Any limitations of the engagement Ethics Interpretation Booking activities that would impair independence regardless of agreement Determine or change journal entries, account codings or classification for transactions, or other accounting records without obtaining client approval. Authorize or approve transactions. Prepare source documents. Make changes to source documents without client approval. 74

75 Ethics Interpretation Payroll and disbursement impairment activities that impair regardless of agreement Accept responsibility to authorize payment of client funds, electronically or otherwise, except as specifically provided for with respect to electronic payroll tax payments. Accept responsibility to sign or cosign client checks, even if only in emergency situations. Sign payroll tax return on behalf of client management. Ethics Interpretation As well, watch out not to trip over internal audit restrictions Consulting theory of independence plus Note this has become a very significant issue for peer reviews Also introduces major liability issues 75

76 Level of Reporting Issues GAAP is GAAP regardless of level of assurance CPAs prohibited from being knowingly associated with misleading financial information Active search standard for audits Eyes open standard for compilations and review Reviews necessitate inquiries and analytical review procedures or competent alternative procedures Compilation Standards Must considered stated qualifications of accounting personnel (AR ) in gaining an understanding of entity Is required to consider the need to perform additional accounting work So if client not competent, based on stated qualifications, to be relied upon, you have an issue Can issue an independence modification on report 76

77 Review and Audit Remember EI Issues May find you need another firm involved under current rules Especially when considering the need to first perform a compilation Consider potential implications of SSARS exposure draft on reviews however, won't impact audit issues SOP 94-6 Issues Section 6 of manual Has been around for a while, but still often not picked up Is a hot button area in litigation, since it deals with disclosures of risks and uncertainties Contractors often have such issues 77

78 SOP 94-6 Disclosures Nature of operations Use of estimates Certain significant estimates Concentrations of risk Nature of Operations Description of major products or services Principal markets Location of those markets If more than one line of business, relative importance of each line 78

79 Use of Estimates Explanation of the importance of estimates in financial statements Normally a boilerplate disclosure Significant Estimates Where we tell users which estimates are sensitive in nature Reasonably possible the effect on financial will change in the near term based on confirming events and The effect of the change would be material to the financial statements With PCM, estimates of costs to complete almost always will be this 79

80 Certain Concentrations If all of these facts true, must disclose Concentration exists at balance sheet date Enterprise is vulnerable to a significant short term impact It is reasonably possible an event might occur in the near term Note for some circumstances you must presume it's reasonably possible Example Audit Program Highlights Found in Section 2 of manual Should tailor audit program for specific client not a cookbook system Remember eyes open standard for non-audit attest engagements 80

81 FASB Interpretation 48 Module 3 Income Taxes FIN 48 has been delayed twice for private entities However, almost ended up with it being applied last fall was on, then two weeks later was off Indicated it wants to turn this one on But has also indicated reduced disclosures for nonpublic companies Biggest hitch is uncertain tax positions 81

82 Contingency Special Case Income taxes not governed by FASB 5 Rather, have to use more likely than not test for each tax position Covered Entities Covers all potentially taxable entities S Corporations Built in gains tax Excess passive income Validity of S election State and municipal tax issues, including nexus Applies only to income taxes (sales taxes are FASB 5 issues) 82

Construction Contractors. Resources 1/19/15. Edward K. Zollars Phoenix, Arizona ed@tzlcpas.com www.cperesources.com

Construction Contractors Edward K. Zollars Phoenix, Arizona ed@tzlcpas.com www.cperesources.com Resources Email: ed@tzlpcas.com Website: www.cperesources.com 1 Revenue Recognition ASU 2014-09 FASB Issues

Construction Contractors Edward K. Zollars Phoenix, Arizona ed@tzlcpas.com www.cperesources.com Resources Email: ed@tzlpcas.com Website: www.cperesources.com 1 Revenue Recognition ASU 2014-09 FASB Issues

Accounting for Performance of Construction-Type and Certain Production-Type Contracts

Accounting for Performance of Construction/Production Contracts 18,871 Section 10,330 Statement of Position 81-1 *1 Accounting for Performance of Construction-Type and Certain Production-Type Contracts

Accounting for Performance of Construction/Production Contracts 18,871 Section 10,330 Statement of Position 81-1 *1 Accounting for Performance of Construction-Type and Certain Production-Type Contracts

CHAPTER 11 U.S. GAAP AND INTERNATIONAL ACCOUNTING STANDARDS

CHAPTER 11 U.S. GAAP AND INTERNATIONAL ACCOUNTING STANDARDS CONTENTS Introduction 11.02 Accounting Sources for Construction Contractors 11.03 U.S. GAAP 11.03 IFRS 11.04 Problems with U.S. GAAP for Contractors

CHAPTER 11 U.S. GAAP AND INTERNATIONAL ACCOUNTING STANDARDS CONTENTS Introduction 11.02 Accounting Sources for Construction Contractors 11.03 U.S. GAAP 11.03 IFRS 11.04 Problems with U.S. GAAP for Contractors

CONSTRUCTION CONTRACTORS: CRITICAL ACCOUNTING, AUDITING, AND TAX ISSUES IN TODAY S ENVIRONMENT CONS/14/01

CONSTRUCTION CONTRACTORS: CRITICAL ACCOUNTING, AUDITING, AND TAX ISSUES IN TODAY S ENVIRONMENT CONS/14/01 Table of Contents The Construction Industry An Overview... 1 U.S. GAAP and the Construction Industry...

CONSTRUCTION CONTRACTORS: CRITICAL ACCOUNTING, AUDITING, AND TAX ISSUES IN TODAY S ENVIRONMENT CONS/14/01 Table of Contents The Construction Industry An Overview... 1 U.S. GAAP and the Construction Industry...

Illustrative Financial Statements Prepared Using the Financial Reporting Framework for Small- and Medium-Entities

Illustrative Financial Statements Prepared Using the Financial Reporting Framework for Small- and Medium-Entities Illustrative Financial Statements This component of the toolkit contains sample financial

Illustrative Financial Statements Prepared Using the Financial Reporting Framework for Small- and Medium-Entities Illustrative Financial Statements This component of the toolkit contains sample financial

SAMPLE CONSTRUCTION COMPANY. FINANCIAL STATEMENT AND SUPPLENTARY INFORMANTION For the Year Ended December 31, 2011

FINANCIAL STATEMENT AND SUPPLENTARY INFORMANTION For the Year Ended December 31, 2011 The financial statement, prepared by an independent Certified Public Accountant, is essential for bonding purposes.

FINANCIAL STATEMENT AND SUPPLENTARY INFORMANTION For the Year Ended December 31, 2011 The financial statement, prepared by an independent Certified Public Accountant, is essential for bonding purposes.

Aerospace & Defense Spotlight The Converged Revenue Recognition Model Has Landed

September 2014 Aerospace & Defense Spotlight The Converged Revenue Recognition Model Has Landed In This Issue: Background Key Accounting Issues Effective Date and Transition Challenges for A&D Entities

September 2014 Aerospace & Defense Spotlight The Converged Revenue Recognition Model Has Landed In This Issue: Background Key Accounting Issues Effective Date and Transition Challenges for A&D Entities

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model No. US2014-01 (supplement) June 11, 2014 What s inside: Overview... 1 Defining the contract...

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model No. US2014-01 (supplement) June 11, 2014 What s inside: Overview... 1 Defining the contract...

Audit Risk and Materiality in Conducting an Audit

Audit Risk and Materiality in Conducting an Audit 1647 AU Section 312 Audit Risk and Materiality in Conducting an Audit (Supersedes SAS No. 47.) Source: SAS No. 107. See section 9312 for interpretations

Audit Risk and Materiality in Conducting an Audit 1647 AU Section 312 Audit Risk and Materiality in Conducting an Audit (Supersedes SAS No. 47.) Source: SAS No. 107. See section 9312 for interpretations

Compilation of Financial Statements: Accounting and Review Services Interpretations of Section 80

Compilation of Financial Statements 2035 AR Section 9080 Compilation of Financial Statements: Accounting and Review Services Interpretations of Section 80 1. Reporting When There Are Significant Departures

Compilation of Financial Statements 2035 AR Section 9080 Compilation of Financial Statements: Accounting and Review Services Interpretations of Section 80 1. Reporting When There Are Significant Departures

International Accounting Standard 11 Construction Contracts

International Accounting Standard 11 Construction Contracts Objective The objective of this Standard is to prescribe the accounting treatment of revenue and costs associated with construction contracts.

International Accounting Standard 11 Construction Contracts Objective The objective of this Standard is to prescribe the accounting treatment of revenue and costs associated with construction contracts.

NEPAL ACCOUNTING STANDARDS ON CONSTRUCTION CONTRACTS

NAS 13 NEPAL ACCOUNTING STANDARDS ON CONSTRUCTION CONTRACTS CONTENTS Paragraphs OBJECTIVE SCOPE 1 2 DEFINITIONS 3 6 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 7 10 CONTRACT REVENUE 11 15 CONTRACT

NAS 13 NEPAL ACCOUNTING STANDARDS ON CONSTRUCTION CONTRACTS CONTENTS Paragraphs OBJECTIVE SCOPE 1 2 DEFINITIONS 3 6 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 7 10 CONTRACT REVENUE 11 15 CONTRACT

The following Accounting Standards Interpretation (ASI) relates to AS 7. ASI 29 Turnover in case of Contractors

relates to AS 7. ASI 29 Turnover in case of Contractors") 108 Accounting Standard (AS) 7 (revised 2002) Construction Contracts Contents OBJECTIVE SCOPE Paragraph 1 DEFINITIONS 2-5 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 6-9 CONTRACT REVENUE 10-14 CONTRACT

108 Accounting Standard (AS) 7 (revised 2002) Construction Contracts Contents OBJECTIVE SCOPE Paragraph 1 DEFINITIONS 2-5 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 6-9 CONTRACT REVENUE 10-14 CONTRACT

SAMPLE CONSTRUCTION FINANCIAL STATEMENT

SAMPLE CONSTRUCTION FINANCIAL STATEMENT Construction Contacts: Tim Klimchock, CPA, CCIFP Manager, AEC Industry Group M. Scott Hursh, CPA, CCIFP Principal, AEC Industry Group 1.800.745.8233 Web Site: www.stambaugh-ness.com

SAMPLE CONSTRUCTION FINANCIAL STATEMENT Construction Contacts: Tim Klimchock, CPA, CCIFP Manager, AEC Industry Group M. Scott Hursh, CPA, CCIFP Principal, AEC Industry Group 1.800.745.8233 Web Site: www.stambaugh-ness.com

Construction Contracts

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 11 Construction Contracts This version of SB-FRS 11 does not include amendments that are effective for annual periods beginning after 1 January 2015.

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 11 Construction Contracts This version of SB-FRS 11 does not include amendments that are effective for annual periods beginning after 1 January 2015.

Inspection Observations Related to PCAOB "Risk Assessment" Auditing Standards (No. 8 through No.15)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org Inspection Observations Related to PCAOB "Risk Assessment" Auditing Standards (No. 8 through

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org Inspection Observations Related to PCAOB "Risk Assessment" Auditing Standards (No. 8 through

How To Calculate Financial Performance For Construction Contractors

Understanding Construction Accounting Understanding Construction Accounting David O Brien, CPA, CGMA Member & Director of Construction Team James F. Weber, CPA, CGMA Managing Member This session is eligible

Understanding Construction Accounting Understanding Construction Accounting David O Brien, CPA, CGMA Member & Director of Construction Team James F. Weber, CPA, CGMA Managing Member This session is eligible

Applicability / Objective

By Rakesh Agarwal Applicability / Objective APPLICABILITY: applicable to all contracts entered into on or after 1-4-2003 and is mandatory in nature from that date. Based on AS 7 (Construction Contracts)

By Rakesh Agarwal Applicability / Objective APPLICABILITY: applicable to all contracts entered into on or after 1-4-2003 and is mandatory in nature from that date. Based on AS 7 (Construction Contracts)

REPORT ON 2007-2010 INSPECTIONS OF DOMESTIC FIRMS THAT AUDIT 100 OR FEWER PUBLIC COMPANIES

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org REPORT ON 2007-2010 INSPECTIONS OF DOMESTIC FIRMS THAT AUDIT 100 OR FEWER PUBLIC COMPANIES PCAOB

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org REPORT ON 2007-2010 INSPECTIONS OF DOMESTIC FIRMS THAT AUDIT 100 OR FEWER PUBLIC COMPANIES PCAOB

Sri Lanka Accounting Standard -LKAS 11. Construction Contracts

Sri Lanka Accounting Standard -LKAS 11 Construction Contracts -405- Sri Lanka Accounting Standard -LKAS 11 Construction Contracts Sri Lanka Accounting Standard LKAS 11 Construction Contracts is set out

Sri Lanka Accounting Standard -LKAS 11 Construction Contracts -405- Sri Lanka Accounting Standard -LKAS 11 Construction Contracts Sri Lanka Accounting Standard LKAS 11 Construction Contracts is set out

Construction Contracts

65 Accounting Standard (AS) 7 Construction Contracts Contents OBJECTIVE SCOPE Paragraph 1 DEFINITIONS 2-5 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 6-9 CONTRACT REVENUE 10-14 CONTRACT COSTS 15-20

65 Accounting Standard (AS) 7 Construction Contracts Contents OBJECTIVE SCOPE Paragraph 1 DEFINITIONS 2-5 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 6-9 CONTRACT REVENUE 10-14 CONTRACT COSTS 15-20

SCHEDULES OF CHAPTER 40B MAXIMUM ALLOWABLE PROFIT FROM SALES AND TOTAL CHAPTER 40B COSTS EXAMINATION PROGRAM

7/30/07 SCHEDULES OF CHAPTER 40B MAXIMUM ALLOWABLE PROFIT FROM SALES AND TOTAL CHAPTER 40B COSTS Instructions: EXAMINATION PROGRAM This Model Program lists the major procedures and steps that should be

7/30/07 SCHEDULES OF CHAPTER 40B MAXIMUM ALLOWABLE PROFIT FROM SALES AND TOTAL CHAPTER 40B COSTS Instructions: EXAMINATION PROGRAM This Model Program lists the major procedures and steps that should be

How To Account For Construction Contracts In Hong Kong Kongsong Accounting Standard 11

HKAS 11 Issued October 2004Revised March 2010 Hong Kong Accounting Standard 11 Construction Contracts COPYRIGHT Copyright 2011 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

HKAS 11 Issued October 2004Revised March 2010 Hong Kong Accounting Standard 11 Construction Contracts COPYRIGHT Copyright 2011 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

Communicating Internal Control Related Matters Identified in an Audit

Communicating Internal Control 1843 AU Section 325 Communicating Internal Control Related Matters Identified in an Audit (Supersedes SAS No. 112.) Source: SAS No. 115. Effective for audits of financial

Communicating Internal Control 1843 AU Section 325 Communicating Internal Control Related Matters Identified in an Audit (Supersedes SAS No. 112.) Source: SAS No. 115. Effective for audits of financial

SPECIAL REPORT: Comprehensive Coverage of the New U.S. GAAP Revenue Recognition Requirements

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Accounting and Financial Statements (US GAAP) Accounting and Auditing Update 2014-18 (June 2014): SPECIAL REPORT: Comprehensive

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Accounting and Financial Statements (US GAAP) Accounting and Auditing Update 2014-18 (June 2014): SPECIAL REPORT: Comprehensive

GOVERNMENT OF MALAYSIA

GOVERNMENT OF MALAYSIA Malaysian Public Sector Accounting Standards MPSAS 11 Construction Contracts March 2015 MPSAS 11 Construction Contracts Acknowledgment The Malaysian Public Sector Accounting Standard

GOVERNMENT OF MALAYSIA Malaysian Public Sector Accounting Standards MPSAS 11 Construction Contracts March 2015 MPSAS 11 Construction Contracts Acknowledgment The Malaysian Public Sector Accounting Standard

Management Representations

Management Representations 1941 AU Section 333 Management Representations (Supersedes SAS No. 19.) Source: SAS No. 85; SAS No. 89; SAS No. 99; SAS No. 113. See section 9333 for interpretations of this

Management Representations 1941 AU Section 333 Management Representations (Supersedes SAS No. 19.) Source: SAS No. 85; SAS No. 89; SAS No. 99; SAS No. 113. See section 9333 for interpretations of this

CHAPTER 18. Revenue Recognition ASSIGNMENT CLASSIFICATION TABLE. Brief Exercises Exercises Problems Cases

CHAPTER 18 Revenue Recognition ASSIGNMENT CLASSIFICATION TABLE Topics *1. Realization and recognition; sales transactions; high rates of return. Questions 1, 2, 3, 4, 5, 6, 22 Brief Exercises Exercises

CHAPTER 18 Revenue Recognition ASSIGNMENT CLASSIFICATION TABLE Topics *1. Realization and recognition; sales transactions; high rates of return. Questions 1, 2, 3, 4, 5, 6, 22 Brief Exercises Exercises

Auditing Derivative Instruments, Hedging Activities, and Investments in Securities 1

Auditing Derivative Instruments 1915 AU Section 332 Auditing Derivative Instruments, Hedging Activities, and Investments in Securities 1 (Supersedes SAS No. 81.) Source: SAS No. 92. See section 9332 for

Auditing Derivative Instruments 1915 AU Section 332 Auditing Derivative Instruments, Hedging Activities, and Investments in Securities 1 (Supersedes SAS No. 81.) Source: SAS No. 92. See section 9332 for

SSARS 21 Review, Compilation, and Preparation of Financial Statements

SSARS 21 Review, Compilation, and Preparation of Financial Statements Course Objectives Provide background information that resulted in SSARS 21 Introduce new Preparation Standard Compare the Compilation

SSARS 21 Review, Compilation, and Preparation of Financial Statements Course Objectives Provide background information that resulted in SSARS 21 Introduce new Preparation Standard Compare the Compilation

Review of Financial Statements

Review of Financial Statements 2055 AR Section 90 Review of Financial Statements Issue date, unless otherwise indicated: December 2009 See section 9090 for interpretations of this section. Source: SSARS

Review of Financial Statements 2055 AR Section 90 Review of Financial Statements Issue date, unless otherwise indicated: December 2009 See section 9090 for interpretations of this section. Source: SSARS

1 Supplement: IAS 11 Construction contracts

1 Supplement: IAS 11 Construction contracts Introduction In this section we introduce construction contracts. We will look at the required treatments and disclosures under IAS 11. Make sure that you work

1 Supplement: IAS 11 Construction contracts Introduction In this section we introduce construction contracts. We will look at the required treatments and disclosures under IAS 11. Make sure that you work

310-10-00 Status. General

Checkpoint Contents Accounting, Audit & Corporate Finance Library Standards and Regulations FASB Codification Codification Assets 310 Receivables 310-10 Overall 310-10-00 Status Copyright 2014 by Financial

Checkpoint Contents Accounting, Audit & Corporate Finance Library Standards and Regulations FASB Codification Codification Assets 310 Receivables 310-10 Overall 310-10-00 Status Copyright 2014 by Financial

The Auditor s Communication With Those Charged With Governance

The Auditor s Communication With Governance 2083 AU Section 380 The Auditor s Communication With Those Charged With Governance (Supersedes SAS No. 61.) Source: SAS No. 114. Effective for audits of financial

The Auditor s Communication With Governance 2083 AU Section 380 The Auditor s Communication With Those Charged With Governance (Supersedes SAS No. 61.) Source: SAS No. 114. Effective for audits of financial

The Auditor s Consideration of the Internal Audit Function in an Audit of Financial Statements

Auditor s Consideration of Internal Audit Function 1805 AU Section 322 The Auditor s Consideration of the Internal Audit Function in an Audit of Financial Statements (Supersedes SAS No. 9.) Source: SAS

Auditor s Consideration of Internal Audit Function 1805 AU Section 322 The Auditor s Consideration of the Internal Audit Function in an Audit of Financial Statements (Supersedes SAS No. 9.) Source: SAS

Framework for Performing and Reporting on Compilation and Review Engagements

Compilation and Review Engagements 1999 AR Section 60 Framework for Performing and Reporting on Compilation and Review Engagements Issue date, unless otherwise indicated: December 2009 Source: SSARS No.

Compilation and Review Engagements 1999 AR Section 60 Framework for Performing and Reporting on Compilation and Review Engagements Issue date, unless otherwise indicated: December 2009 Source: SSARS No.

AICPA Technical Hotline's Top A&A Issues Facing CPAs

AICPA Technical Hotline's Top A&A Issues Facing CPAs Kristy L. Illuzzi, CPA Frances S. McClintock, CPA Kristy L. Illuzzi, CPA Kristy Illuzzi moved to North Carolina and joined the AICPA in May 2007 as

AICPA Technical Hotline's Top A&A Issues Facing CPAs Kristy L. Illuzzi, CPA Frances S. McClintock, CPA Kristy L. Illuzzi, CPA Kristy Illuzzi moved to North Carolina and joined the AICPA in May 2007 as

Visit CCHGroup.com/AASolutions for an overview of our complete set of Accounting and Audit solutions.

CCH brings you... Chapter 3: Accounting for contractors, home builders, and developers Chapter 6: Completed contract method from: Construction Guide: Accounting and Knowledge-Based Audits (Chapter 3);

CCH brings you... Chapter 3: Accounting for contractors, home builders, and developers Chapter 6: Completed contract method from: Construction Guide: Accounting and Knowledge-Based Audits (Chapter 3);

How To Read The Financial Results Of 20Xx And 200X

Name SAMPLE Financial Statements December 31, 20XX CPA Accounting Firm Name Table of Contents Page Accountant s Review Report 1 Financial Statements Balance Sheet 2 Income Statement 3 Schedule of General

Name SAMPLE Financial Statements December 31, 20XX CPA Accounting Firm Name Table of Contents Page Accountant s Review Report 1 Financial Statements Balance Sheet 2 Income Statement 3 Schedule of General

ACCOUNTING FOR CONSTRUCTION CONTRACT AS7 (Revised-2002) Applied in accounting for construction contracts in the financial statements of contractors.

Applied in accounting for construction contracts in the financial statements of contractors.") ACCOUNTING FOR CONSTRUCTION CONTRACT AS7 (Revised-2002) 1) Applicability of the Standard Applied in accounting for construction contracts in the financial statements of contractors. Where a Construction

ACCOUNTING FOR CONSTRUCTION CONTRACT AS7 (Revised-2002) 1) Applicability of the Standard Applied in accounting for construction contracts in the financial statements of contractors. Where a Construction

Audit Evidence. AU Section 326. Introduction. Concept of Audit Evidence AU 326.03

Audit Evidence 1859 AU Section 326 Audit Evidence (Supersedes SAS No. 31.) Source: SAS No. 106. See section 9326 for interpretations of this section. Effective for audits of financial statements for periods

Audit Evidence 1859 AU Section 326 Audit Evidence (Supersedes SAS No. 31.) Source: SAS No. 106. See section 9326 for interpretations of this section. Effective for audits of financial statements for periods

NEPAL ACCOUNTING STANDARDS ON BUSINESS COMBINATIONS

NAS 21 NEPAL ACCOUNTING STANDARDS ON BUSINESS COMBINATIONS CONTENTS Paragraphs OBJECTIVE 1 SCOPE 2-14 Identifying a business combination 5-10 Business combinations involving entities under common control

NAS 21 NEPAL ACCOUNTING STANDARDS ON BUSINESS COMBINATIONS CONTENTS Paragraphs OBJECTIVE 1 SCOPE 2-14 Identifying a business combination 5-10 Business combinations involving entities under common control

Audit Documentation 2029. See section 9339 for interpretations of this section.

Audit Documentation 2029 AU Section 339 Audit Documentation (Supersedes SAS No. 96.) Source: SAS No. 103. See section 9339 for interpretations of this section. Effective for audits of financial statements

Audit Documentation 2029 AU Section 339 Audit Documentation (Supersedes SAS No. 96.) Source: SAS No. 103. See section 9339 for interpretations of this section. Effective for audits of financial statements

Auditing Accounting Estimates

Auditing Accounting Estimates 2057 AU Section 342 Auditing Accounting Estimates Source: SAS No. 57; SAS No. 113. See section 9342 for interpretations of this section. Effective for audits of financial

Auditing Accounting Estimates 2057 AU Section 342 Auditing Accounting Estimates Source: SAS No. 57; SAS No. 113. See section 9342 for interpretations of this section. Effective for audits of financial

Roche Capital Market Ltd Financial Statements 2009

R Roche Capital Market Ltd Financial Statements 2009 1 Roche Capital Market Ltd, Financial Statements Reference numbers indicate corresponding Notes to the Financial Statements. Roche Capital Market Ltd,

R Roche Capital Market Ltd Financial Statements 2009 1 Roche Capital Market Ltd, Financial Statements Reference numbers indicate corresponding Notes to the Financial Statements. Roche Capital Market Ltd,

Construction Contracts

Compiled Accounting Standard AASB 111 Construction Contracts This compiled Standard applies to annual reporting periods beginning on or after 1 January 2009 that end on or after 30 June 2009. Early application

Compiled Accounting Standard AASB 111 Construction Contracts This compiled Standard applies to annual reporting periods beginning on or after 1 January 2009 that end on or after 30 June 2009. Early application

Revenue Recognition (Topic 605)

") Proposed Accounting Standards Update (Revised) Issued: November 14, 2011 and January 4, 2012 Comments Due: March 13, 2012 Revenue Recognition (Topic 605) Revenue from Contracts with Customers (including

Proposed Accounting Standards Update (Revised) Issued: November 14, 2011 and January 4, 2012 Comments Due: March 13, 2012 Revenue Recognition (Topic 605) Revenue from Contracts with Customers (including

Investor Sub Advisory Group GOING CONCERN CONSIDERATIONS AND RECOMMENDATIONS. March 28, 2012

PCAOB Investor Sub Advisory Group GOING CONCERN CONSIDERATIONS AND RECOMMENDATIONS March 28, 2012 Auditing standards requiring auditors to issue going concern opinions have existed for several decades.

PCAOB Investor Sub Advisory Group GOING CONCERN CONSIDERATIONS AND RECOMMENDATIONS March 28, 2012 Auditing standards requiring auditors to issue going concern opinions have existed for several decades.

Financial Statements Years Ended September 30, 2012 and 2011. LB&B Associates Inc.

Financial Statements Years Ended September 30, 2012 and 2011 LB&B Associates Inc. LB&B Associates Inc. Contents Page Report of Independent Auditors 1 Financial Statements Balance Sheets 2 Statements of

Financial Statements Years Ended September 30, 2012 and 2011 LB&B Associates Inc. LB&B Associates Inc. Contents Page Report of Independent Auditors 1 Financial Statements Balance Sheets 2 Statements of

BIOQUAL, INC. AND SUBSIDIARY AUDITED CONSOLIDATED FINANCIAL STATE:MENTS MAY 31, 2014 AND 2013

BIOQUAL, INC. AND SUBSIDIARY AUDITED CONSOLIDATED FINANCIAL STATE:MENTS MAY 31, 2014 AND 2013 Table of Contents Page Independent Auditor's Report 1-2 Audited Consolidated Financial Statements Consolidated

BIOQUAL, INC. AND SUBSIDIARY AUDITED CONSOLIDATED FINANCIAL STATE:MENTS MAY 31, 2014 AND 2013 Table of Contents Page Independent Auditor's Report 1-2 Audited Consolidated Financial Statements Consolidated

10-1. Auditing Business Process. Objectives Understand the Auditing of the Enteties Business. Process

10-1 Auditing Business Process Auditing Business Process Objectives Understand the Auditing of the Enteties Business Process Identify the types of transactions in different Business Process Asses Control

10-1 Auditing Business Process Auditing Business Process Objectives Understand the Auditing of the Enteties Business Process Identify the types of transactions in different Business Process Asses Control

How To Write A Financial Audit

Overall Objectives of the Independent Auditor 77 AU-C Section 200 Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance With Generally Accepted Auditing Standards Source:

Overall Objectives of the Independent Auditor 77 AU-C Section 200 Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance With Generally Accepted Auditing Standards Source:

The BASICS of CONSTRUCTION ACCOUNTING Workshop GLOSSARY

The BASICS of CONSTRUCTION ACCOUNTING Workshop GLOSSARY From Financial Management & Accounting for the Construction Industry, CFMA. 2014 Matthew Bender and Company, Inc., a member of the LexisNexis Group.

The BASICS of CONSTRUCTION ACCOUNTING Workshop GLOSSARY From Financial Management & Accounting for the Construction Industry, CFMA. 2014 Matthew Bender and Company, Inc., a member of the LexisNexis Group.

Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement

Understanding the Entity and Its Environment 1667 AU Section 314 Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement (Supersedes SAS No. 55.) Source: SAS No. 109.

Understanding the Entity and Its Environment 1667 AU Section 314 Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement (Supersedes SAS No. 55.) Source: SAS No. 109.

Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained

Performing Audit Procedures in Response to Assessed Risks 1781 AU Section 318 Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained (Supersedes SAS No. 55.)

Performing Audit Procedures in Response to Assessed Risks 1781 AU Section 318 Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained (Supersedes SAS No. 55.)

Consideration of Fraud in a Financial Statement Audit

Consideration of Fraud in a Financial Statement Audit 1719 AU Section 316 Consideration of Fraud in a Financial Statement Audit (Supersedes SAS No. 82.) Source: SAS No. 99; SAS No. 113. Effective for audits

Consideration of Fraud in a Financial Statement Audit 1719 AU Section 316 Consideration of Fraud in a Financial Statement Audit (Supersedes SAS No. 82.) Source: SAS No. 99; SAS No. 113. Effective for audits

No. 2014-09 May 2014. Revenue from Contracts with Customers (Topic 606) An Amendment of the FASB Accounting Standards Codification

An Amendment of the FASB Accounting Standards Codification") No. 2014-09 May 2014 Revenue from Contracts with Customers (Topic 606) An Amendment of the FASB Accounting Standards Codification The FASB Accounting Standards Codification is the source of authoritative

No. 2014-09 May 2014 Revenue from Contracts with Customers (Topic 606) An Amendment of the FASB Accounting Standards Codification The FASB Accounting Standards Codification is the source of authoritative

STOCKCROSS FINANCIAL SERVICES, INC. REPORT ON AUDIT OF STATEMENT OF FINANCIAL CONDITION DECEMBER 31, 2012

REPORT ON AUDIT OF STATEMENT OF FINANCIAL CONDITION Filed in accordance with Rule 17a-5(e)(3) as a PUBLIC DOCUMENT UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 ANNUAL AUDITED

REPORT ON AUDIT OF STATEMENT OF FINANCIAL CONDITION Filed in accordance with Rule 17a-5(e)(3) as a PUBLIC DOCUMENT UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 ANNUAL AUDITED

Roche Capital Market Ltd Financial Statements 2012

R Roche Capital Market Ltd Financial Statements 2012 1 Roche Capital Market Ltd - Financial Statements 2012 Roche Capital Market Ltd, Financial Statements Reference numbers indicate corresponding Notes

R Roche Capital Market Ltd Financial Statements 2012 1 Roche Capital Market Ltd - Financial Statements 2012 Roche Capital Market Ltd, Financial Statements Reference numbers indicate corresponding Notes

For today s contractor to achieve

CHOOSING A CPA FOR YOUR CONSTRUCTION A contractor can qualify a potential CPA by focusing on specific criteria. COMPANY MASON BRUGH, CPA, CCFP AND CHAD MADDOX, CPA, CVA, CCFP For today s contractor to