Why implement an AML system? 10/9/2014 AML SYSTEMS -- DATA VALIDATION. OceanSystems ECS Verafin. AML Manager. Yellow Hammer BSA

|

|

|

- Sharon Wood

- 10 years ago

- Views:

Transcription

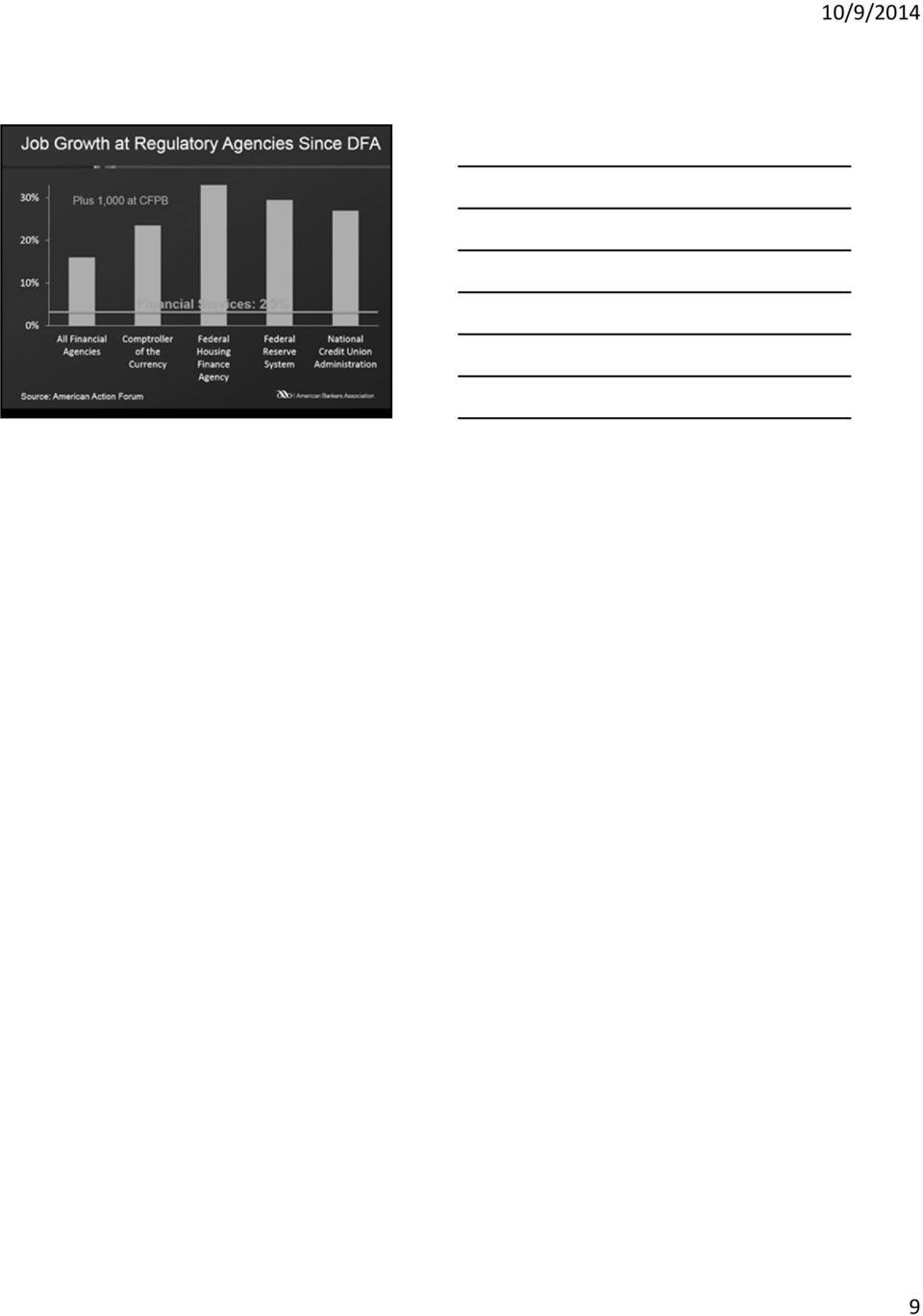

1 AML SYSTEMS -- DATA VALIDATION FLORIDA BANKERS ASSOCIATION OCTOBER 2014 Kristen J. Stogniew, Esq., AAP, Shareholder Saltmarsh, Cleaveland & Gund, CPA s 2 I am nd generation consultant to the industry >19 years consulting in BSA & Regulatory Compliance including audit, monitoring, training, mentoring Attorney - Florida Bar Member since 1995 Member of CFE since 2003; Accredited ACH Professional I am not --- IT person Regulator Vendor representative Why implement an AML system? 3 OceanSystems ECS Verafin AML Manager? Yellow Hammer BSA 1

2 Why implement an AML system? 4 Too much information, not enough time to digest Consistent methodology protects institution Retention of review/conclusions (Almost real time) Risk Rating Comparison of Expected vs. Actual activity Regulators require it 5 Regulatory Expectations on AML/MIS systems, since The Independent Test should address the integrity and accuracy of MIS used in the BSA/AML compliance program. MIS includes reports used to: identify large currency transactions, aggregate daily currency transactions, funds transfer transactions, monetary instrument sales transactions, and analytical and trend reports. The programming of the Bank s monitoring systems should be independently reviewed for reasonable filtering criteria. - April 4, The expanding use of models in all aspects of banking reflects the extent to which models can improve business decisions, but models also come with costs. There is the direct cost of devoting resources to develop and implement models properly. There are also the potential indirect costs of relying on models, such as the possible adverse consequences (including financial loss) of decisions based on models that are incorrect or misused. Those consequences should be addressed by active management of model risk. 2

3 7 Model Risk Processes Conceptual Soundness of model Process Verification / Benchmarking Analyze Model Outcomes 8 Model Risk Processes Prior exams, audits, validations Delegation of responsibilities Risk Assessment/Where does model fit in? Are there risk-appropriate model-related: Policies & procedures Ongoing validation processes Board/ reporting Common Validation Finding: This is not in place. We particularly feel that Board/ reporting (overrides, volume and type of alerts, cases generated) serves as a form of ongoing validation and will help to steer the ship in the right direction... 9 Conceptual Soundness of model Developmental evidence in support of design Came from implementation phase & ongoing validation: Data feeds Tran codes Filters for alerts Points for risk rating Was this carefully considered, using management s judgment, and consistent with sound industry practices? 3

4 Data feeds. 10 Vendors XYZ Bank AML System OFAC ACH Core Systems Originator Beneficiary SEC code/iat Indicator Trust Loan Deposit Brokerage POD Data and Transaction Terminals Fed file & other Wire System(s) Other Side name & address Other side Bank Payment order details International may be different Teller Proprietary ATMs Foreign ATMs POS checkouts Location Purchaser Monetary Payee instrument Method of payment Common Systems Functionalities Rule(s), examples: Cash transactions between $7,000 and $10,000 3 or more wire transfers, each less than $3,000, in a week Wire transfer $5,000 or more in, followed by cash out $5,000 or more ACH credit over $8,000 Rules are IF, THEN.. Common Systems Functionalities Filter(s), apply the rules to Sub-set or Risk Category of accounts Example, Personal accounts Opened less than 3 months Example, Business accounts In high risk industries Newly formed enterprise Beneficial Owners unknown 4

5 Common Systems Functionalities Intelligent systems Review activity in context to other data Adaptive based on historical activity Can compare against peer group Behavior-based norms, fuzzy logic Common Systems Functionalities 14 Risk Rating Applies points to customer information Applies points to transaction activity Total score falls within institution-defined tiers of risk Is this the institution s High Risk list? Expected vs. Actual Transactions OFAC/FSE/PEP, etc. 314(a) CTR and/or SAR filing 15 Cont d Conceptual Soundness of model Is coverage and capabilities in line with risk profile, and intended use? Are there any material gaps? High risk transaction types; products; customers; geographies Is data used representative of portfolio/market? Are parameters/risk weights appropriate? Is the system providing value? Common Findings: (1) One or more high risk areas from institution s Risk Assessment is not being analyzed in System; (2) Parameters or Risk Score too high or low for meaningful ID; (3) Vendor-provided risk settings/keywords have not been updated since install; (4) nature of business is scoring so high on risk rating that all high risk business types score high, even if no activity. 5

6 16 OCC & FRB Supervisory Guidance on Model Risk Conceptual Soundness / Testing Recalculate risk ratings across a wide range of risk factors Conduct sensitivity analysis determine the impact of small changes in assumptions on model output: Unexpectedly large changes in outputs in response to small changes in inputs can indicate an unstable model, while stress testing responses to a wide range of inputs, including extreme changes, can confirm the model s robustness We work with management during the review if possible to test the impact of changes/prove or disprove our assessment of the theory behind the model. Sometimes this cannot be done during the review and a follow-up visit is often recommended. 17 Process Verification / Benchmarking: Are all model components functioning as intended? Test risk based sample of internal and external data feeds for accuracy and integrity of data capture Review user access controls Review model overrides level and documentation (excessive may compromise model integrity) If available, compare inputs and outputs to estimates from alternative internal or external data (benchmark) E.g., Testing Currency Transactions 18 Deposits & Withdrawals DDA CD IRA Savings Money market ATM Internal bank accounts, on customer s behalf Others Less cash / cash back On us non customer Transit check cashed Batched transactions Savings Withdrawal to Close account Loan payment Monetary instrument purchases General Ledger cash ins Loan disbursements Currency exchanges Cash orders 6

7 Actual Finding on transaction capture: 19 For the days in our sample, the AML system failed to capture the following types of transactions: Miscellaneous cash out; On us non-customer cashed check; Money market withdrawal; Savings withdrawal; and Checking deposit cash in The institution requested the vendor to review the configuration to determine why For the transactions, the cash component was missing in the configuration None of the CTRs thought to have been created and filed during this period were actually sent to FinCEN, as the system s entire filing process was not completed. The BSA Officer can make changes to the parameters without IT or other independent review, and system maintenance reports do not provide a useful audit trail for parameter changes. 20 Analyze Model Outcomes Obtain reportable transactions or high risk accounts from source records and verify whether they alerted as expected (forward-testing), and, conversely, compare alerted activity to source information to verify proper calculations (back-testing). Determine whether alerts and risk changes are being responded to - timely and with adequate documentation. Compare the Bank s customer base of low, moderate, and high risk customers for reasonableness and against the latest risk rating list to identify potential deficiencies. Some Findings on Model Outcome: 21 Foreign wire transfers are not identified and/or scoring properly (some too many, some too few) Accounts rated as Charity, Jewel Dealer, and Non-traditional financial entities are not being assigned added points at account opening DBAs are not being industry-coded Activity subject to review is too short to make a decision; so, it looks like alerts are not being responded timely Deviation thresholds are set so high, suspicious increases are not alerting 7

8 22 Work with & the Vendor as necessary to form conclusions How settings / filters work in the Bank s environment Are there newer parameters available? Provide Effective Challenge a critical analysis by objective third parties who can identify model limitations and assumptions and produce appropriate changes. Deep thoughts on model validation 23 If you can, run parallel before implementing a new system 3-6 months BSA Officer should be involved/aware of all new products and system updates. What is the impact on filters / parameters? Ongoing validation, management reporting Re-do testing where applicable (significant changes, system upgrades) The volume of system alerts should not be tailored solely to meet existing staff levels Talk with your peers join formal or informal user groups. AML Systems Model Validation 24 Questions / Discussion? Kristen J. Stogniew, ext 1030 [email protected] 8

9 Questions / Discussion 25 9

Validating Third Party Software Erica M. Torres, CRCM

Validating Third Party Software Erica M. Torres, CRCM Michigan Bankers Association Risk Management & Compliance Institute September 29, 2014 MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT

Validating Third Party Software Erica M. Torres, CRCM Michigan Bankers Association Risk Management & Compliance Institute September 29, 2014 MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT

FIRST COMMUNITY CREDIT UNION OFAC AND BSA RISK ASSESSMENTS

FIRST COMMUNITY CREDIT UNION OFAC AND BSA RISK ASSESSMENTS I. OFAC RISK ASSESSMENT - APRIL 30, 2006 All Credit Union staff shall be aware of risks involved in conducting daily transactions and shall take

FIRST COMMUNITY CREDIT UNION OFAC AND BSA RISK ASSESSMENTS I. OFAC RISK ASSESSMENT - APRIL 30, 2006 All Credit Union staff shall be aware of risks involved in conducting daily transactions and shall take

FFIEC BSA/AML Examination Manual. Four Key Components of a Suspicious Activity Monitoring Program

FFIEC BSA/AML Examination Manual Four Key Components of a Suspicious Activity Monitoring Program 1 2 IDENTIFICATION OF SUSPICIOUS ACTIVITY 3 Unusual Activity Identification Employee Identification Law

FFIEC BSA/AML Examination Manual Four Key Components of a Suspicious Activity Monitoring Program 1 2 IDENTIFICATION OF SUSPICIOUS ACTIVITY 3 Unusual Activity Identification Employee Identification Law

Department of Financial Services Superintendent s Regulations

Department of Financial Services Superintendent s Regulations Part 504 BANKING DIVISION TRANSACTION MONITORING AND FILTERING PROGRAM REQUIREMENTS AND CERTIFICATIONS (Statutory authority: Banking Law 37(3)(4)

Department of Financial Services Superintendent s Regulations Part 504 BANKING DIVISION TRANSACTION MONITORING AND FILTERING PROGRAM REQUIREMENTS AND CERTIFICATIONS (Statutory authority: Banking Law 37(3)(4)

Bank Secrecy Act Anti-Money Laundering Examination Manual

Bank Secrecy Act Anti-Money Laundering Examination Manual Core Overview - Customer Identification Program Assess the bank's compliance with the statutory and regulatory requirements for the Customer Identification

Bank Secrecy Act Anti-Money Laundering Examination Manual Core Overview - Customer Identification Program Assess the bank's compliance with the statutory and regulatory requirements for the Customer Identification

BSA/AML & OFAC. Volunteer Compliance Training. Agenda

Ideas + Solutions = Success BSA/AML & OFAC Ideas + Solutions = Success Volunteer Compliance Training Presented by Dorie Fitchett HCUL Regulatory Officer April 25, 2013 Agenda 1. Bank Secrecy Act (BSA)

Ideas + Solutions = Success BSA/AML & OFAC Ideas + Solutions = Success Volunteer Compliance Training Presented by Dorie Fitchett HCUL Regulatory Officer April 25, 2013 Agenda 1. Bank Secrecy Act (BSA)

Bank Secrecy Act, Anti-Money Laundering, and Office of Foreign Assets Control

Bank Secrecy Act, Anti-Money Laundering, and Office of Foreign Assets Control Overview The Bank Secrecy Act (BSA) was created in 1970 to assist in criminal, tax, and regulatory investigations. The Financial

Bank Secrecy Act, Anti-Money Laundering, and Office of Foreign Assets Control Overview The Bank Secrecy Act (BSA) was created in 1970 to assist in criminal, tax, and regulatory investigations. The Financial

BANK EXAMINERS MANUAL FOR AML/CFT RBS EXAMINATION

BANK EXAMINERS MANUAL FOR AML/CFT RBS EXAMINATION 1 Contents 1. EXAMINATION PROCEDURES ON SCOPING AND PLANNING 1..1 2. EXAMINATION PROCEDURES OF AML/CFT COMPLIANCE PROGRAM...3.. 3 3. OVERVIEW OF AML/CFT

BANK EXAMINERS MANUAL FOR AML/CFT RBS EXAMINATION 1 Contents 1. EXAMINATION PROCEDURES ON SCOPING AND PLANNING 1..1 2. EXAMINATION PROCEDURES OF AML/CFT COMPLIANCE PROGRAM...3.. 3 3. OVERVIEW OF AML/CFT

Broker-Dealer Concepts

Broker-Dealer Concepts Broker-Dealer AML Program Checklist/Gap Analysis Published by the Broker-Dealer & Investment Management Regulation Group September 2011 I. GENERAL REQUIREMENTS AML AML Program Components

Broker-Dealer Concepts Broker-Dealer AML Program Checklist/Gap Analysis Published by the Broker-Dealer & Investment Management Regulation Group September 2011 I. GENERAL REQUIREMENTS AML AML Program Components

FEDERAL DEPOSIT INSURANCE CORPORATION WASHINGTON, D.C. ) ) ) ) ) ) ) )

) ) ) ) ) ) )") FEDERAL DEPOSIT INSURANCE CORPORATION WASHINGTON, D.C. In the Matter of BURKE & HERBERT BANK & TRUST COMPANY ALEXANDRIA, VIRGINIA (Insured State Nonmember Bank CONSENT ORDER FDIC-14-0103b The Federal Deposit

FEDERAL DEPOSIT INSURANCE CORPORATION WASHINGTON, D.C. In the Matter of BURKE & HERBERT BANK & TRUST COMPANY ALEXANDRIA, VIRGINIA (Insured State Nonmember Bank CONSENT ORDER FDIC-14-0103b The Federal Deposit

FEDERAL DEPOSIT INSURANCE CORPORATION WASHINGTON, D.C. CALIFORNIA DEPARTMENT OF FINANCIAL INSTITUTIONS SAN FRANCISCO, CALIFORNIA

FEDERAL DEPOSIT INSURANCE CORPORATION WASHINGTON, D.C. CALIFORNIA DEPARTMENT OF FINANCIAL INSTITUTIONS SAN FRANCISCO, CALIFORNIA ) ) In the Matter of ) ) CONSENT ORDER BANAMEX USA ) CENTURY CITY, CALIFORNIA

FEDERAL DEPOSIT INSURANCE CORPORATION WASHINGTON, D.C. CALIFORNIA DEPARTMENT OF FINANCIAL INSTITUTIONS SAN FRANCISCO, CALIFORNIA ) ) In the Matter of ) ) CONSENT ORDER BANAMEX USA ) CENTURY CITY, CALIFORNIA

Anti-Money Laundering Policy Manual Table of Contents [Sample Client] Table of Contents

![Anti-Money Laundering Policy Manual Table of Contents [Sample Client] Table of Contents](/thumbs/39/20119425.jpg "Anti-Money Laundering Policy Manual Table of Contents [Sample Client] Table of Contents") Table of Contents [ Client] Table of Contents TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 3 1.1 GOALS AND OBJECTIVES... 3 1.2 REQUIRED REVIEW... 3 1.3 APPLICABILITY... 3 1.4 MONEY LAUNDERING DEFINED...

Table of Contents [ Client] Table of Contents TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 3 1.1 GOALS AND OBJECTIVES... 3 1.2 REQUIRED REVIEW... 3 1.3 APPLICABILITY... 3 1.4 MONEY LAUNDERING DEFINED...

FEDERAL DEPOSIT INSURANCE CORPORATION WASHINGTON, D.C. ) CONSENT ORDER. ) FDIC-13-0450b

CONSENT ORDER. ) FDIC-13-0450b") FEDERAL DEPOSIT INSURANCE CORPORATION WASHINGTON, D.C. In the Matter of THE BANK OF PRINCETON PRINCETON, NEW JERSEY (INSURED STATE NONMEMBER BANK) ) ) ) ) CONSENT ORDER ) ) ) FDIC-13-0450b ) The Federal

FEDERAL DEPOSIT INSURANCE CORPORATION WASHINGTON, D.C. In the Matter of THE BANK OF PRINCETON PRINCETON, NEW JERSEY (INSURED STATE NONMEMBER BANK) ) ) ) ) CONSENT ORDER ) ) ) FDIC-13-0450b ) The Federal

Customer Risk Ranking

PROACTIVE VS. REACTIVE IN YOUR INVESTIGATIVE PROCESS / CUSTOMER DUE DILIGENCE Customer Risk Ranking Norberto Molina, VP, BSA/AML Manager Banco Popular de Puerto Rico PUBLIC - 1 Customer Risk Ranking -

PROACTIVE VS. REACTIVE IN YOUR INVESTIGATIVE PROCESS / CUSTOMER DUE DILIGENCE Customer Risk Ranking Norberto Molina, VP, BSA/AML Manager Banco Popular de Puerto Rico PUBLIC - 1 Customer Risk Ranking -

Emerging ACH Issues. Florida Bankers Association 30 th Annual Consumer Compliance Seminar Orlando, Florida April 29- May 1, 2015

1 Emerging ACH Issues Florida Bankers Association 30 th Annual Consumer Compliance Seminar Orlando, Florida April 29- May 1, 2015 Kristen J. Stogniew, Esquire, AAP, CFE, Shareholder [email protected]

1 Emerging ACH Issues Florida Bankers Association 30 th Annual Consumer Compliance Seminar Orlando, Florida April 29- May 1, 2015 Kristen J. Stogniew, Esquire, AAP, CFE, Shareholder [email protected]

HIGH-RISK COUNTRIES IN AML MONITORING

HIGH-RISK COUNTRIES IN AML MONITORING ALICIA CORTEZ TABLE OF CONTENTS I. Introduction 3 II. High-Risk Countries 3 Customers 4 Products 7 Monitoring 8 Audit Considerations 8 III. Conclusion 10 IV. References

HIGH-RISK COUNTRIES IN AML MONITORING ALICIA CORTEZ TABLE OF CONTENTS I. Introduction 3 II. High-Risk Countries 3 Customers 4 Products 7 Monitoring 8 Audit Considerations 8 III. Conclusion 10 IV. References

Product. AML Risk Manager for Life Insurance Complete End-to-End AML Coverage for Life Insurance

Product AML Risk Manager for Life Insurance Complete End-to-End AML Coverage for Life Insurance A Comprehensive Solution for AML Detection, Investigation, Case Management and Reporting Illegal money laundering

Product AML Risk Manager for Life Insurance Complete End-to-End AML Coverage for Life Insurance A Comprehensive Solution for AML Detection, Investigation, Case Management and Reporting Illegal money laundering

Bank Secrecy Act Monitoring Tools

Bank Secrecy Act Monitoring Tools Using CU*BASE Tools to Comply with BSA Requirements also includes Printing Currency Transaction Report (CTR) Forms via CU*BASE INTRODUCTION This book describes the CU*BASE

Bank Secrecy Act Monitoring Tools Using CU*BASE Tools to Comply with BSA Requirements also includes Printing Currency Transaction Report (CTR) Forms via CU*BASE INTRODUCTION This book describes the CU*BASE

WIRE TRANSFER GUIDE. 1 Fedline Advantage/Fedline Web from Federal Reserve Bank 2 Autosolution from Bankers Bank 3 Telephone 4 Other (Internet)

") WIRE TRANSFER GUIDE WIRE TRANSFER METHOD: 1 Fedline Advantage/Fedline Web from Federal Reserve Bank 2 Autosolution from Bankers Bank 3 Telephone 4 Other (Internet) COMPUTER SETTINGS - FEDLINE ADVANTAGE/FEDLINE

WIRE TRANSFER GUIDE WIRE TRANSFER METHOD: 1 Fedline Advantage/Fedline Web from Federal Reserve Bank 2 Autosolution from Bankers Bank 3 Telephone 4 Other (Internet) COMPUTER SETTINGS - FEDLINE ADVANTAGE/FEDLINE

DEVELOPING AN AML (ANTI-MONEY LAUNDERING) PROGRAM:

PROGRAM:") DEVELOPING AN AML (ANTI-MONEY LAUNDERING) PROGRAM: Although the Department of the Treasury has not issued specific rules for hedge funds and hedge fund managers, hedge fund managers should adopt and implement

DEVELOPING AN AML (ANTI-MONEY LAUNDERING) PROGRAM: Although the Department of the Treasury has not issued specific rules for hedge funds and hedge fund managers, hedge fund managers should adopt and implement

Chris Price Compliance Consultant

METAVANTE WHITE PAPER Utilization of s in Anti- Money Laundering Compliance Monitoring Programs Chris Price Compliance Consultant 1-800-822-6758 Utilization of s in Anti-Money Laundering Compliance Monitoring

METAVANTE WHITE PAPER Utilization of s in Anti- Money Laundering Compliance Monitoring Programs Chris Price Compliance Consultant 1-800-822-6758 Utilization of s in Anti-Money Laundering Compliance Monitoring

NATIONAL CREDIT UNION ADMINISTRATION OFFICE OF INSPECTOR GENERAL

NATIONAL CREDIT UNION ADMINISTRATION OFFICE OF INSPECTOR GENERAL OFFICE OF FOREIGN ASSET CONTROL COMPLIANCE REVIEW Report #OIG-06-09 December 18, 2006 William A. DeSarno Inspector General Released By:

NATIONAL CREDIT UNION ADMINISTRATION OFFICE OF INSPECTOR GENERAL OFFICE OF FOREIGN ASSET CONTROL COMPLIANCE REVIEW Report #OIG-06-09 December 18, 2006 William A. DeSarno Inspector General Released By:

Anti-Money Laundering and Economic Sanctions

Anti-Money Laundering and Economic Sanctions 1 Meet Your Instructor Denise Whiting, CAMS Manager, Risk Advisory, Charlotte Uptown 14 years experience in the financial services industry Extensive knowledge

Anti-Money Laundering and Economic Sanctions 1 Meet Your Instructor Denise Whiting, CAMS Manager, Risk Advisory, Charlotte Uptown 14 years experience in the financial services industry Extensive knowledge

PERSONAL ACCOUNT SPECIFICATIONS AND FEE LISTING

PERSONAL ACCOUNT SPECIFICATIONS AND FEE LISTING Account Opening and Usage Sterling Eagle & Club Sterling TM Eagle Checking Minimum balance to open account: $500 Monthly average balance to avoid fee: $500

PERSONAL ACCOUNT SPECIFICATIONS AND FEE LISTING Account Opening and Usage Sterling Eagle & Club Sterling TM Eagle Checking Minimum balance to open account: $500 Monthly average balance to avoid fee: $500

BANK SECRECY ACT POLICY

BANK SECRECY ACT POLICY Policy Statement In compliance with section 748.2 of the NCUA Rules and Regulations, the board of directors of Alternatives Federal Credit Union (AFCU) has adopted the following

BANK SECRECY ACT POLICY Policy Statement In compliance with section 748.2 of the NCUA Rules and Regulations, the board of directors of Alternatives Federal Credit Union (AFCU) has adopted the following

JENNIFER SHASKY CALVERY DIRECTOR FINANCIAL CRIMES ENFORCEMENT NETWORK ABA/ABA MONEY LAUNDERING ENFORCEMENT CONFERENCE NOVEMBER 16, 2015 WASHINGTON, DC

JENNIFER SHASKY CALVERY DIRECTOR FINANCIAL CRIMES ENFORCEMENT NETWORK ABA/ABA MONEY LAUNDERING ENFORCEMENT CONFERENCE NOVEMBER 16, 2015 WASHINGTON, DC Good afternoon. Thank you to the American Bankers

JENNIFER SHASKY CALVERY DIRECTOR FINANCIAL CRIMES ENFORCEMENT NETWORK ABA/ABA MONEY LAUNDERING ENFORCEMENT CONFERENCE NOVEMBER 16, 2015 WASHINGTON, DC Good afternoon. Thank you to the American Bankers

Bank Secrecy Act for Directors. Barb Boyd Content Manager CU Solutions Group

Bank Secrecy Act for Directors Barb Boyd Content Manager CU Solutions Group Agenda What is the Bank Secrecy Act? How to have a successful BSA Compliance Program OFAC responsibilities. Penalties for non-compliance.

Bank Secrecy Act for Directors Barb Boyd Content Manager CU Solutions Group Agenda What is the Bank Secrecy Act? How to have a successful BSA Compliance Program OFAC responsibilities. Penalties for non-compliance.

CONSUMER COMPLIANCE SELF ASSESSMENT GUIDE. Excerpt: Bank Secrecy Act

CONSUMER COMPLIANCE SELF ASSESSMENT GUIDE Excerpt: Bank Secrecy Act A complete copy of the Consumer Compliance Self Assessment Guide is available on the NCUA web site, http://www.ncua.gov/. From the home

CONSUMER COMPLIANCE SELF ASSESSMENT GUIDE Excerpt: Bank Secrecy Act A complete copy of the Consumer Compliance Self Assessment Guide is available on the NCUA web site, http://www.ncua.gov/. From the home

AML & Mortgage Fraud Compliance Program v. 08.2013 ANTI-MONEY LAUNDERING & MORTGAGE FRAUD COMPLIANCE PROGRAM

ANTI-MONEY LAUNDERING & MORTGAGE FRAUD COMPLIANCE PROGRAM Version: 2.0 dated 08.2013 TABLE OF CONTENTS AML & Mortgage Fraud Compliance Program 1.0 PURPOSE AND SCOPE... 3 2.0 APPLICABLE REGULATIONS AND

ANTI-MONEY LAUNDERING & MORTGAGE FRAUD COMPLIANCE PROGRAM Version: 2.0 dated 08.2013 TABLE OF CONTENTS AML & Mortgage Fraud Compliance Program 1.0 PURPOSE AND SCOPE... 3 2.0 APPLICABLE REGULATIONS AND

The FinCEN Currency Transaction Report & Designation of Exempt Persons Report. Introduction & Filing Instructions

The FinCEN Currency Transaction Report & Designation of Exempt Persons Report Introduction & Filing Instructions Agenda Introduction FinCEN CTR The New FinCEN CTR: General Information Features and Advantages

The FinCEN Currency Transaction Report & Designation of Exempt Persons Report Introduction & Filing Instructions Agenda Introduction FinCEN CTR The New FinCEN CTR: General Information Features and Advantages

Customer Identification Program - Overview

. ~ancial/~. "8 ~~. ~~~~~ ~~ ~ ~ ~ ~v ~. ~ : ~~t. Q ion CO Customer Identification Program - Overview Bank Secrecy Act / Anti-Money Laundering Examination Manual Customer Identification Program - Overview

. ~ancial/~. "8 ~~. ~~~~~ ~~ ~ ~ ~ ~v ~. ~ : ~~t. Q ion CO Customer Identification Program - Overview Bank Secrecy Act / Anti-Money Laundering Examination Manual Customer Identification Program - Overview

Designing an Operational Risk Program for a Community Bank Stephan Salvador Managing Director, Risk Management Consulting

Consulting and Professional Services Designing an Operational Risk Program for a Community Bank Stephan Salvador Managing Director, Risk Management Consulting Designing an Operational Risk Program for

Consulting and Professional Services Designing an Operational Risk Program for a Community Bank Stephan Salvador Managing Director, Risk Management Consulting Designing an Operational Risk Program for

BUSINESS BANKING PRICING SCHEDULE EFFECTIVE MAY 1, 2015

BUSINESS BANKING PRICING SCHEDULE EFFECTIVE MAY 1, 2015 A division of ZB, N.A. AMEGY PREMIER BUSINESS RELATIONSHIP PACKAGE * Monthly package maintenance fee $25.00 Balance requirement to avoid package

BUSINESS BANKING PRICING SCHEDULE EFFECTIVE MAY 1, 2015 A division of ZB, N.A. AMEGY PREMIER BUSINESS RELATIONSHIP PACKAGE * Monthly package maintenance fee $25.00 Balance requirement to avoid package

FBAR Background. Reporting Foreign Financial Accounts on the Electronic FBAR

FBAR Background Reporting Foreign Financial Accounts on the Electronic FBAR ROD LUNDQUIST, SENIOR POLICY ANALYST SMALL BUSINESS/SELF-EMPLOYED June 4, 2014 Bank Secrecy Act enacted in 1970 Codified primarily

FBAR Background Reporting Foreign Financial Accounts on the Electronic FBAR ROD LUNDQUIST, SENIOR POLICY ANALYST SMALL BUSINESS/SELF-EMPLOYED June 4, 2014 Bank Secrecy Act enacted in 1970 Codified primarily

OPA EFT Payroll Account - Bank Services

OPA EFT Payroll Account - Bank Services ACCOUNT MAINTENANCE AUTOMATIC DOLLAR TRANSF-MAINT ACH Services ACH ADA AUTHORIZED ID ACH EMAIL NOC ACH NOC TRANSMISSION REPORTING ACH RETURN EMAIL NOTIFICATION ADDENDA

OPA EFT Payroll Account - Bank Services ACCOUNT MAINTENANCE AUTOMATIC DOLLAR TRANSF-MAINT ACH Services ACH ADA AUTHORIZED ID ACH EMAIL NOC ACH NOC TRANSMISSION REPORTING ACH RETURN EMAIL NOTIFICATION ADDENDA

Risk Assessments Customer Risk

FIBA Conference 2014 Risk Assessments Customer Risk María de Lourdes Jiménez, Esq Senior Vice President, Popular Inc Customer Risk Ranking Benefits / Features Customer Risk Ranking System based on scoring

FIBA Conference 2014 Risk Assessments Customer Risk María de Lourdes Jiménez, Esq Senior Vice President, Popular Inc Customer Risk Ranking Benefits / Features Customer Risk Ranking System based on scoring

UNITED STATES OF AMERICA BEFORE THE BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D.C.

UNITED STATES OF AMERICA BEFORE THE BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D.C. NEW YORK STATE BANKING DEPARTMENT NEW YORK, NEW YORK Written Agreement by and among BANCO DE LA NACION

UNITED STATES OF AMERICA BEFORE THE BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D.C. NEW YORK STATE BANKING DEPARTMENT NEW YORK, NEW YORK Written Agreement by and among BANCO DE LA NACION

FEDERAL EMPLOYEES CREDIT UNION DES MOINES BSA/AML/OFAC COMPLIANCE RISK ASSESSMENT

FEDERAL EMPLOYEES CREDIT UNION DES MOINES BSA/AML/OFAC COMPLIANCE RISK ASSESSMENT This BSA/AML/OFAC compliance risk assessment is conducted for the purpose of evaluating Federal Employees Credit Union's

FEDERAL EMPLOYEES CREDIT UNION DES MOINES BSA/AML/OFAC COMPLIANCE RISK ASSESSMENT This BSA/AML/OFAC compliance risk assessment is conducted for the purpose of evaluating Federal Employees Credit Union's

HIGH YIELD CHECKING. EXPLANATION OF SOME OF OUR KEY SERVICES AND CHARGES Here are details about High Yield Checking services.

EXPLANATION OF SOME OF OUR KEY SERVICES AND CHARGES Here are details about High Yield Checking services. KEY ACCOUNT TERMS AND CHARGES: Monthly Service Charge: No monthly service charge. Includes free

EXPLANATION OF SOME OF OUR KEY SERVICES AND CHARGES Here are details about High Yield Checking services. KEY ACCOUNT TERMS AND CHARGES: Monthly Service Charge: No monthly service charge. Includes free

RESIDENTIAL MORTGAGE LENDERS & ORIGINATORS L COMPLIANCE PROGRAM

RESIDENTIAL MORTGAGE LENDERS & ORIGINATORS L COMPLIANCE PROGRAM PO Box 760 Prosper, TX 75078 972 347 9921 www.americanhfm.com Contents INTRODUCTION... 6 New FinCEN Rule 31 CFR Parts 1010 and 1029... 6

RESIDENTIAL MORTGAGE LENDERS & ORIGINATORS L COMPLIANCE PROGRAM PO Box 760 Prosper, TX 75078 972 347 9921 www.americanhfm.com Contents INTRODUCTION... 6 New FinCEN Rule 31 CFR Parts 1010 and 1029... 6

Service Charges and Fees

Service Charges and Fees Service Charges and Fees Content 1. Personal Product Types and Service Charges 2. Personal Banking Service Charges and Fees 3. ATM and Debit Card Transaction Charges 4. Business

Service Charges and Fees Service Charges and Fees Content 1. Personal Product Types and Service Charges 2. Personal Banking Service Charges and Fees 3. ATM and Debit Card Transaction Charges 4. Business

1 Copyright 2011, Oracle and/or its affiliates. All rights reserved.

1 Copyright 2011, Oracle and/or its affiliates. All rights Challenges in Implementing the Financial Action Task Force (FATF) recommendations on Risk Based Approach by R. Suresha CAMS 2 Copyright 2011,

1 Copyright 2011, Oracle and/or its affiliates. All rights Challenges in Implementing the Financial Action Task Force (FATF) recommendations on Risk Based Approach by R. Suresha CAMS 2 Copyright 2011,

DCU BULLETIN Division of Credit Unions Washington State Department of Financial Institutions

DCU BULLETIN Division of Credit Unions Washington State Department of Financial Institutions Phone: (360) 902-8701 FAX: (877) 330-6870 January 2, 2014 No. B-14-01 Bank Secrecy Act Guidance and Exam Procedures

DCU BULLETIN Division of Credit Unions Washington State Department of Financial Institutions Phone: (360) 902-8701 FAX: (877) 330-6870 January 2, 2014 No. B-14-01 Bank Secrecy Act Guidance and Exam Procedures

GREAT AMERICAN TITLE OF HOUSTON, LLC D/B/A GREAT AMERICAN TITLE COMPANY EXAMINATION REPORT NOVEMBER 24, 2015

GREAT AMERICAN TITLE OF HOUSTON, LLC D/B/A GREAT AMERICAN TITLE COMPANY EXAMINATION REPORT NOVEMBER 24, 2015 INDEPENDENT ACCOUNTANTS' REPORT To the Board of Directors of Great American Title of Houston,

GREAT AMERICAN TITLE OF HOUSTON, LLC D/B/A GREAT AMERICAN TITLE COMPANY EXAMINATION REPORT NOVEMBER 24, 2015 INDEPENDENT ACCOUNTANTS' REPORT To the Board of Directors of Great American Title of Houston,

FinCEN s Proposed Anti-Money Laundering Compliance Requirements for Investment Advisers: How to Prepare Now

FinCEN s Proposed Anti-Money Laundering Compliance Requirements for Investment Advisers: How to Prepare Now I. INTRODUCTION On August 25, 2015, the Financial Crimes Enforcement Network ( FinCEN ) proposed

FinCEN s Proposed Anti-Money Laundering Compliance Requirements for Investment Advisers: How to Prepare Now I. INTRODUCTION On August 25, 2015, the Financial Crimes Enforcement Network ( FinCEN ) proposed

An Oracle White Paper October 2009. An Integrated Approach to Fighting Financial Crime: Leveraging Investments in AML and Fraud Solutions

An Oracle White Paper October 2009 An Integrated Approach to Fighting Financial Crime: Leveraging Investments in AML and Fraud Solutions Executive Overview Today s complex financial crime schemes pose

An Oracle White Paper October 2009 An Integrated Approach to Fighting Financial Crime: Leveraging Investments in AML and Fraud Solutions Executive Overview Today s complex financial crime schemes pose

NCUA LETTER TO CREDIT UNIONS

NCUA LETTER TO CREDIT UNIONS NATIONAL CREDIT UNION ADMINISTRATION 1775 Duke Street, Alexandria, VA 22314 DATE: June 2005 LETTER NO.: 05-CU-09 TO: SUBJ: ENCL: Federally Insured Credit Unions Bank Secrecy

NCUA LETTER TO CREDIT UNIONS NATIONAL CREDIT UNION ADMINISTRATION 1775 Duke Street, Alexandria, VA 22314 DATE: June 2005 LETTER NO.: 05-CU-09 TO: SUBJ: ENCL: Federally Insured Credit Unions Bank Secrecy

Important Information About Systems Conversion

Important Information About Systems Conversion The conversion from American Bank systems will occur over the weekend of April 22-24, 2016. Please read the following important information and instructions.

Important Information About Systems Conversion The conversion from American Bank systems will occur over the weekend of April 22-24, 2016. Please read the following important information and instructions.

ACH Welcome Kit. Rev. 10/2014. Member FDIC Page 1 of 8

ACH Welcome Kit Rev. 10/2014 Member FDIC Page 1 of 8 Dear Customer, Thank you for utilizing FirstMerit s ACH services. We have finalized the setup of your ACH product and you may now begin processing ACH

ACH Welcome Kit Rev. 10/2014 Member FDIC Page 1 of 8 Dear Customer, Thank you for utilizing FirstMerit s ACH services. We have finalized the setup of your ACH product and you may now begin processing ACH

AML / CFT Anti-money laundering and countering financing of terrorism

AML / CFT Anti-money laundering and countering financing of terrorism Wire transfers What is a wire transfer? 1. The Anti-Money Laundering and Countering Financing of Terrorism Act 2009 (the Act) contains

AML / CFT Anti-money laundering and countering financing of terrorism Wire transfers What is a wire transfer? 1. The Anti-Money Laundering and Countering Financing of Terrorism Act 2009 (the Act) contains

Managing Regulatory Compliance and AML Risk in a Virtual Currency World

Managing Regulatory Compliance and AML Risk in a Virtual Currency World Issue When you first think of virtual currency (also known as digital currency), the video gaming industry may be what first comes

Managing Regulatory Compliance and AML Risk in a Virtual Currency World Issue When you first think of virtual currency (also known as digital currency), the video gaming industry may be what first comes

B roker-dealers often face a significant challenge

Securities Regulation & Law Report Reproduced with permission from Securities Regulation & Law Report, 44 SRLR 1410, 07/23/2012. Copyright 2012 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com

Securities Regulation & Law Report Reproduced with permission from Securities Regulation & Law Report, 44 SRLR 1410, 07/23/2012. Copyright 2012 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com

INTERAGENCY GUIDANCE ON THE ADVANCED MEASUREMENT APPROACHES FOR OPERATIONAL RISK. Date: June 3, 2011

Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of the Comptroller of the Currency Office of Thrift Supervision INTERAGENCY GUIDANCE ON THE ADVANCED MEASUREMENT

Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of the Comptroller of the Currency Office of Thrift Supervision INTERAGENCY GUIDANCE ON THE ADVANCED MEASUREMENT

How to Build an Effective AML/OFAC Compliance Program

How to Build an Effective AML/OFAC Compliance Program 23 rd Annual ACFE Fraud Conference Orlando, FL June 17 22 Daniel L. Tannebaum Head of Compliance Americas, Travelex Chief Compliance Officer, Travelex

How to Build an Effective AML/OFAC Compliance Program 23 rd Annual ACFE Fraud Conference Orlando, FL June 17 22 Daniel L. Tannebaum Head of Compliance Americas, Travelex Chief Compliance Officer, Travelex

A BSA/AML RISK ASSESSMENT. Page 1 of 35

& A BSA/AML RISK ASSESSMENT Page 1 of 35 TABLE OF CONTENTS PAGE Auditing & Updating a $13 Billion Organization s BSA/AML Risk Assessment...4 Auditing the Existing BSA/AML Risk Assessment..5 Core Components

& A BSA/AML RISK ASSESSMENT Page 1 of 35 TABLE OF CONTENTS PAGE Auditing & Updating a $13 Billion Organization s BSA/AML Risk Assessment...4 Auditing the Existing BSA/AML Risk Assessment..5 Core Components

BANK SECRECY ACT COMPLIANCE PROGRAM AND PROCEDURES. Section I Introduction 2. Appointment of Bank Secrecy Officer and Successor(s)

") BANK SECRECY ACT COMPLIANCE PROGRAM AND PROCEDURES Section Sub- Topic Page Section I Introduction 2. II Appointment of Bank Secrecy Officer and Successor(s) 2 III Currency Transaction Reports 2 IV V Monetary

BANK SECRECY ACT COMPLIANCE PROGRAM AND PROCEDURES Section Sub- Topic Page Section I Introduction 2. II Appointment of Bank Secrecy Officer and Successor(s) 2 III Currency Transaction Reports 2 IV V Monetary

Aetna Anti-Money Laundering and Financial Sanctions Compliance Policy

Aetna AML and Financial Sanctions Compliance Policy Aetna Anti-Money Laundering and Financial Sanctions Compliance Policy Originating Department: Aetna s AML Compliance Office Effective Date: January 1,

Aetna AML and Financial Sanctions Compliance Policy Aetna Anti-Money Laundering and Financial Sanctions Compliance Policy Originating Department: Aetna s AML Compliance Office Effective Date: January 1,

AML Topics Using analytics to get the most from your transaction monitoring system

www.pwc.com AML Topics Using analytics to get the most from your transaction monitoring system March 2011 Contents Components of the AML Compliance Program... 1 Transaction Monitoring... 1 Transaction

www.pwc.com AML Topics Using analytics to get the most from your transaction monitoring system March 2011 Contents Components of the AML Compliance Program... 1 Transaction Monitoring... 1 Transaction

Best Practices: Anti-Money Laundering and Customer Information Selected Requirements

Best Practices: Anti-Money Laundering and Customer Information Selected Requirements INTRODUCTION This document is intended to provide IIUSA members with guidance regarding anti-money laundering (AML),

Best Practices: Anti-Money Laundering and Customer Information Selected Requirements INTRODUCTION This document is intended to provide IIUSA members with guidance regarding anti-money laundering (AML),

Please make extra copies of the blank Independent Review Form and do not use your last blank one.

Section 4 : Independent Review INDEPENDENT REVIEW When you established your Compliance Program and with MoneyGram's approval, you indicated how often you would have an Independent Review of your AML Compliance

Section 4 : Independent Review INDEPENDENT REVIEW When you established your Compliance Program and with MoneyGram's approval, you indicated how often you would have an Independent Review of your AML Compliance

www.pwc.com/modelrisk New supervisory guidance on model Overview, analysis, and next steps

www.pwc.com/modelrisk New supervisory guidance on model risk management: Overview, analysis, and next steps Features of new guidance Issued as supervisory guidance (21 pages) not as a risk bulletin. This

www.pwc.com/modelrisk New supervisory guidance on model risk management: Overview, analysis, and next steps Features of new guidance Issued as supervisory guidance (21 pages) not as a risk bulletin. This

- Cindy Griffin, CEO Northern Hills Federal Credit Union

Services Overview Audit Link as a service has been in business since May 2008. True to its commitment, Audit Link reduces the added work imposed by regulations and compliance. Factors inherent in changing

Services Overview Audit Link as a service has been in business since May 2008. True to its commitment, Audit Link reduces the added work imposed by regulations and compliance. Factors inherent in changing

SAMPLE AUDIT REPORT. Sample Credit Union. Report on Operations. As of Audit Date

Sample Credit Union Report on Operations As of Audit Date GENERAL OVERVIEW Overall, the Credit Union appeared to be well managed and continuing to maintain its financial stability. During the twelve months

Sample Credit Union Report on Operations As of Audit Date GENERAL OVERVIEW Overall, the Credit Union appeared to be well managed and continuing to maintain its financial stability. During the twelve months

Information Technology Audit Considerations When Designing Audit Coverage For AML Applications

Information Technology Audit Considerations When Designing Audit Coverage For AML Applications Peter D. Wild, FCA, CAMS The views expressed in this paper are solely those of the author and do not represent

Information Technology Audit Considerations When Designing Audit Coverage For AML Applications Peter D. Wild, FCA, CAMS The views expressed in this paper are solely those of the author and do not represent

BANK SECRECY ACT POLICY

BANK SECRECY ACT POLICY The purpose of this policy is to ensure that the Credit Union is in full compliance with the Treasury Department regulation governing Currency Transaction reporting for any cash

BANK SECRECY ACT POLICY The purpose of this policy is to ensure that the Credit Union is in full compliance with the Treasury Department regulation governing Currency Transaction reporting for any cash

The rise of third party relationships means rise in risk and regulation. Non-compliance is risky business for financial institutions

The rise of third party relationships means rise in risk and regulation Non-compliance is risky business for financial institutions Increasing dependency on third parties by banks has resulted in mandatory

The rise of third party relationships means rise in risk and regulation Non-compliance is risky business for financial institutions Increasing dependency on third parties by banks has resulted in mandatory

Avoiding Buyer s Remorse with AML Monitoring Software. Implementing Effective and Efficient AML Transaction Monitoring Systems

Avoiding Buyer s Remorse with AML Monitoring Software Implementing Effective and Efficient AML Transaction Monitoring Systems Overview A well-designed transaction monitoring program is an important pillar

Avoiding Buyer s Remorse with AML Monitoring Software Implementing Effective and Efficient AML Transaction Monitoring Systems Overview A well-designed transaction monitoring program is an important pillar

M-Aud. Comptroller of the Currency Administrator of National Banks. Internal and External Audits. Comptroller s Handbook. April 2003.

M-Aud Comptroller of the Currency Administrator of National Banks Internal and External Audits Comptroller s Handbook April 2003 M Management Internal and External Audits Table of Contents Introduction...1

M-Aud Comptroller of the Currency Administrator of National Banks Internal and External Audits Comptroller s Handbook April 2003 M Management Internal and External Audits Table of Contents Introduction...1

NEW ACCOUNT INTERVIEW CHECKLIST (BUSINESS/NON-PROFIT/CHARITIES) Business, Non-Profit, & Charities Account Information Sheet

Business, Non-Profit, & Charities Account Information Sheet") NEW ACCOUNT INTERVIEW CHECKLIST (BUSINESS/NON-PROFIT/CHARITIES) Business, Non-Profit, & Charities Account Information Sheet Corporation (For Profit) Partnership (General) Partnership (Limited) FOR BANK

NEW ACCOUNT INTERVIEW CHECKLIST (BUSINESS/NON-PROFIT/CHARITIES) Business, Non-Profit, & Charities Account Information Sheet Corporation (For Profit) Partnership (General) Partnership (Limited) FOR BANK

NUCSOFT. Asset Liability Management

NUCSOFT Asset Liability Management ALM Overview Forecasting, Budgeting & Planning Tool for Advanced Liquidity Management & ALM Analysis & Monitoring of Liquidity Buffers, Key Regulatory Ratios such as

NUCSOFT Asset Liability Management ALM Overview Forecasting, Budgeting & Planning Tool for Advanced Liquidity Management & ALM Analysis & Monitoring of Liquidity Buffers, Key Regulatory Ratios such as

Fee Schedule for Business Accounts A Guide to Your Webster Account

Fee Schedule for Business Accounts A Guide to Your Webster Account At Webster, we re committed to helping you find the right account to meet your needs. We ve prepared the following Account Guide to make

Fee Schedule for Business Accounts A Guide to Your Webster Account At Webster, we re committed to helping you find the right account to meet your needs. We ve prepared the following Account Guide to make

Background. FIN-2010-G001 Issued: March 5, 2010 Subject: Guidance on Obtaining and Retaining Beneficial Ownership Information

Joint Release Financial Crimes Enforcement Network Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation National Credit Union Administration Office of the Comptroller

Joint Release Financial Crimes Enforcement Network Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation National Credit Union Administration Office of the Comptroller

Disclosure of Account Terms

Disclosure of Account Terms Account Type Min. to open Daily Min Balance to obtain yield Basic Checking $0 N/A Choice Checking $0 N/A Premium Checking $0 N/A Statement Savings, Holiday Clubs $50 $300-24,999

Disclosure of Account Terms Account Type Min. to open Daily Min Balance to obtain yield Basic Checking $0 N/A Choice Checking $0 N/A Premium Checking $0 N/A Statement Savings, Holiday Clubs $50 $300-24,999

FinCEN Issues Notice of Proposed Rulemaking that Would Extend AML Requirements to Registered Investment Advisers

FinCEN Issues Notice of Proposed Rulemaking that Would Extend AML Requirements to Registered Investment Advisers On August 25, 2015, the Financial Crimes Enforcement Network (FinCEN), a bureau of the US

FinCEN Issues Notice of Proposed Rulemaking that Would Extend AML Requirements to Registered Investment Advisers On August 25, 2015, the Financial Crimes Enforcement Network (FinCEN), a bureau of the US

Guidance. FIN-2014-G001 Issued: February 14, 2014 Subject: BSA Expectations Regarding Marijuana-Related Businesses

Guidance FIN-2014-G001 Issued: February 14, 2014 Subject: BSA Expectations Regarding Marijuana-Related Businesses The Financial Crimes Enforcement Network ( FinCEN ) is issuing guidance to clarify Bank

Guidance FIN-2014-G001 Issued: February 14, 2014 Subject: BSA Expectations Regarding Marijuana-Related Businesses The Financial Crimes Enforcement Network ( FinCEN ) is issuing guidance to clarify Bank

BUSINESS BANKING PRICING SCHEDULE EFFECTIVE MAY 2, 2016

BUSINESS BANKING PRICING SCHEDULE EFFECTIVE MAY 2, 2016 A division of ZB, N.A. We offer a wide variety of banking services to meet your needs. For more information, regarding specialized services not shown,

BUSINESS BANKING PRICING SCHEDULE EFFECTIVE MAY 2, 2016 A division of ZB, N.A. We offer a wide variety of banking services to meet your needs. For more information, regarding specialized services not shown,

SCHEDULES OF CHAPTER 40B MAXIMUM ALLOWABLE PROFIT FROM SALES AND TOTAL CHAPTER 40B COSTS EXAMINATION PROGRAM

7/30/07 SCHEDULES OF CHAPTER 40B MAXIMUM ALLOWABLE PROFIT FROM SALES AND TOTAL CHAPTER 40B COSTS Instructions: EXAMINATION PROGRAM This Model Program lists the major procedures and steps that should be

7/30/07 SCHEDULES OF CHAPTER 40B MAXIMUM ALLOWABLE PROFIT FROM SALES AND TOTAL CHAPTER 40B COSTS Instructions: EXAMINATION PROGRAM This Model Program lists the major procedures and steps that should be

Service Charges and Fees

Service Charges and Fees 1. Personal Banking Service Charges 1 2. Sabadell Online Banking Service Charges 4 3. Electronic Banking Transaction Charges 5 4. Business Banking Service Charges 7 5. International

Service Charges and Fees 1. Personal Banking Service Charges 1 2. Sabadell Online Banking Service Charges 4 3. Electronic Banking Transaction Charges 5 4. Business Banking Service Charges 7 5. International

Webster Opportunity Checking. $16.95 (or $11.95 with Direct Deposit 2 )

") Fee Schedule for Consumer Accounts A Guide to Your Account At, we re committed to helping you find the right account to meet your needs. We ve prepared the following Account Guide to make sure you understand

Fee Schedule for Consumer Accounts A Guide to Your Account At, we re committed to helping you find the right account to meet your needs. We ve prepared the following Account Guide to make sure you understand

Webster Opportunity Checking. $16.95 (or $11.95 with Direct Deposit 2 )

") Fee Schedule for Consumer Accounts A Guide to Your Account At, we re committed to helping you find the right account to meet your needs. We ve prepared the following Account Guide to make sure you understand

Fee Schedule for Consumer Accounts A Guide to Your Account At, we re committed to helping you find the right account to meet your needs. We ve prepared the following Account Guide to make sure you understand

The 2006 FFIEC Bank Secrecy Act/Anti-Money Laundering Examination Manual:

The 2006 FFIEC Bank Secrecy Act/Anti-Money Laundering Examination Manual: Knowing the Risks Is It Possible to Keep Pace and Manage Them All? By: Carmina Hughes, Executive Director and Patricia McKeown,

The 2006 FFIEC Bank Secrecy Act/Anti-Money Laundering Examination Manual: Knowing the Risks Is It Possible to Keep Pace and Manage Them All? By: Carmina Hughes, Executive Director and Patricia McKeown,

FIS Virtual Back-Office. Dean H. Scholl

FIS Virtual Back-Office Dean H. Scholl FIS Virtual Back-Office Overview FIS Virtual Back-Office is an end to end outsourced delivery model FIS Virtual Back-Office can help mitigate variable costs FIS Virtual

FIS Virtual Back-Office Dean H. Scholl FIS Virtual Back-Office Overview FIS Virtual Back-Office is an end to end outsourced delivery model FIS Virtual Back-Office can help mitigate variable costs FIS Virtual

Identifying Key Risk Indicator

PUERTO RICO PAYMENTS SYMPOSIUM Identifying Key Risk Indicator EPOCPR Services Agenda for Today Background History Regulators & Risk Management Let s have fun Regulators & Risk Assessment ACH Risks Categories

PUERTO RICO PAYMENTS SYMPOSIUM Identifying Key Risk Indicator EPOCPR Services Agenda for Today Background History Regulators & Risk Management Let s have fun Regulators & Risk Assessment ACH Risks Categories

Getting to know your Account the basics

This Deposit Account Disclosure and Bank Fee Schedule and the Deposit Account Agreement for Personal and Business Accounts ( Agreement ) are part of the Deposit Account Agreement that governs your Account

This Deposit Account Disclosure and Bank Fee Schedule and the Deposit Account Agreement for Personal and Business Accounts ( Agreement ) are part of the Deposit Account Agreement that governs your Account

MMC MORTGAGE EXAMINATION MANUAL. Bank Secrecy Act / Anti-Money Laundering Program and Suspicious Activity Report Filing Requirements

MMC MORTGAGE EXAMINATION MANUAL Bank Secrecy Act / Anti-Money Laundering Program and Suspicious Activity Report Filing Requirements MULTI-STATE MORTGAGE COMMITTEE 1129 20 th Street, NW, Ninth Floor Washington,

MMC MORTGAGE EXAMINATION MANUAL Bank Secrecy Act / Anti-Money Laundering Program and Suspicious Activity Report Filing Requirements MULTI-STATE MORTGAGE COMMITTEE 1129 20 th Street, NW, Ninth Floor Washington,

Monthly Service Charge: $8.95 Includes free Debit Cards, usage of Capital One Bank image-enabled ATMs, and access to our extensive Branch Network.

EXPLANATION OF VARIOUS KEY SERVICES AND CHARGES Here are some details about Regular Checking services. KEY ACCOUNT TERMS AND CHARGES: Monthly Service $8.95 Includes free Debit Cards, usage of Capital One

EXPLANATION OF VARIOUS KEY SERVICES AND CHARGES Here are some details about Regular Checking services. KEY ACCOUNT TERMS AND CHARGES: Monthly Service $8.95 Includes free Debit Cards, usage of Capital One

Outsourcing Technology Services A Management Decision

Outsourcing Technology Services A Management Decision A Telephone Seminar for National Banks Tuesday, July 20, 2004 And again on Wednesday, July 21, 2004 Agenda Outsourcing activities and relationships

Outsourcing Technology Services A Management Decision A Telephone Seminar for National Banks Tuesday, July 20, 2004 And again on Wednesday, July 21, 2004 Agenda Outsourcing activities and relationships

POTENTIAL MONEY LAUNDERING WARNING SIGNS POTENTIAL ABUSIVE ACTS - CUSTOMER ACTIVITY WARNING SIGNS

POTENTIAL MONEY LAUNDERING WARNING SIGNS POTENTIAL ABUSIVE ACTS - CUSTOMER ACTIVITY WARNING SIGNS Activity Inconsistent with the Customer s Business A customer opens several accounts for the type of business

POTENTIAL MONEY LAUNDERING WARNING SIGNS POTENTIAL ABUSIVE ACTS - CUSTOMER ACTIVITY WARNING SIGNS Activity Inconsistent with the Customer s Business A customer opens several accounts for the type of business

Bank Secrecy Act E-Filing. Privacy Impact Assessment (PIA) Bank Secrecy Act E-Filing. Version 1.5

Bank Secrecy Act E-Filing. Version 1.5") Bank Secrecy Act E-Filing Privacy Impact Assessment (PIA) Bank Secrecy Act E-Filing Version 1.5 August13, 2014 E-Filing Privacy Impact Assessment Revision Number Change Effective Date Revision History

Bank Secrecy Act E-Filing Privacy Impact Assessment (PIA) Bank Secrecy Act E-Filing Version 1.5 August13, 2014 E-Filing Privacy Impact Assessment Revision Number Change Effective Date Revision History

EURIBOR - CODE OF OBLIGATIONS OF PANEL BANKS

D2725D-2013 EURIBOR - CODE OF OBLIGATIONS OF PANEL BANKS Version: 1 October 2013 1. Objectives The European Money Markets Institute EMMI previously known as Euribor-EBF, as Administrator for the Euribor

D2725D-2013 EURIBOR - CODE OF OBLIGATIONS OF PANEL BANKS Version: 1 October 2013 1. Objectives The European Money Markets Institute EMMI previously known as Euribor-EBF, as Administrator for the Euribor

FIN-2014-A007 August 11, 2014

FIN-2014-A007 August 11, 2014 Advisory to U.S. Financial Institutions on Promoting a Culture of Compliance BSA/AML shortcomings have triggered recent civil and criminal enforcement actions FinCEN seeks

FIN-2014-A007 August 11, 2014 Advisory to U.S. Financial Institutions on Promoting a Culture of Compliance BSA/AML shortcomings have triggered recent civil and criminal enforcement actions FinCEN seeks

International ACH Transactions (IAT) Frequently Asked Questions Corporate Customers. Contents

Frequently Asked Questions Corporate Customers. Contents") International ACH Transactions (IAT) Frequently Asked Questions Corporate Customers IAT changes were made for regulatory compliance The first step is to understand and recognize OFAC requirements - corporates

International ACH Transactions (IAT) Frequently Asked Questions Corporate Customers IAT changes were made for regulatory compliance The first step is to understand and recognize OFAC requirements - corporates

Compliance: A Self-Assessment Guide

Consumer Compliance Self Assessment Guide M4017/8023 Revised December 2004 Compliance: A Self-Assessment Guide Contents A. Introduction Using This Guide B. Key Elements of an Effective Compliance Review

Consumer Compliance Self Assessment Guide M4017/8023 Revised December 2004 Compliance: A Self-Assessment Guide Contents A. Introduction Using This Guide B. Key Elements of an Effective Compliance Review

Presented By Greg Baldwin

ANTI-MONEY LAUNDERING COMPLIANCE OFFICER TRAINING Presented By Greg Baldwin THE ANTI-MONEY LAUNDERING COMPLIANCE OFFICER We re going to cover: Basis for the requirement to have a Compliance Officer The

ANTI-MONEY LAUNDERING COMPLIANCE OFFICER TRAINING Presented By Greg Baldwin THE ANTI-MONEY LAUNDERING COMPLIANCE OFFICER We re going to cover: Basis for the requirement to have a Compliance Officer The

FinCEN Currency Transaction Report (FinCEN CTR) Electronic Filing Requirements

Electronic Filing Requirements") FinCEN Currency Transaction Report (FinCEN CTR) Electronic Filing Requirements Release Date July 2013 Version 1.2 DEPARTMENT OF THE TREASURY Financial Crimes Enforcement Network (FinCEN) Table of Contents

FinCEN Currency Transaction Report (FinCEN CTR) Electronic Filing Requirements Release Date July 2013 Version 1.2 DEPARTMENT OF THE TREASURY Financial Crimes Enforcement Network (FinCEN) Table of Contents