Econ 2230: Public Economics. Lecture 22: Matching

|

|

|

- Candace Green

- 8 years ago

- Views:

Transcription

1 Econ 2230: Public Economics Lecture 22: Matching

2 Last 1. Tax subsidy a) Characterizing the US deduction for charitable donations b) Optimal subsidy c) Intended and unintended consequences d) Price elasticity of giving e) Salience

Intended and unintended")

3 2. Matching A match typically more salient individuals know what the consequences are Government provided incentives typically provided in the form of deductions. Private incentives in the form of matches Announced by the non-profit Provided by the firm as a employer benefit Outline a. Are rebates and subsidies equivalent? Eckel and Grossman (2003) b. How does the magnitude of the match influence giving? Meier (2007) Karlan and List (2007), Karlan, List, and Shafir (2010) c. Reconciling evidence from experimental and non-experimental data

b. How does the magnitude of the match influence giving?")

4 2.a. Match vs subsidy Eckel and Grossman (2003) investigate how donors respond to variation in their initial income and price of giving (Andreoni & Miller, 2002; Andreoni &Vesterlund, 2001) decision maker allocates money between herself and a charity of her choice (make it more similar to the deductions) International charities (African Christian Relief, Doctors Without Borders, and Feed The Children) National charities (I Have A Dream Foundation); Local organizations (Women s Haven of Tarrant County and American Red Cross, Tarrant County Chapter). Health (AIDS Outreach Center and Cancer Care Services) Environmental (Earth Share Texas) Social service charities (YMCA of Arlington).

.")

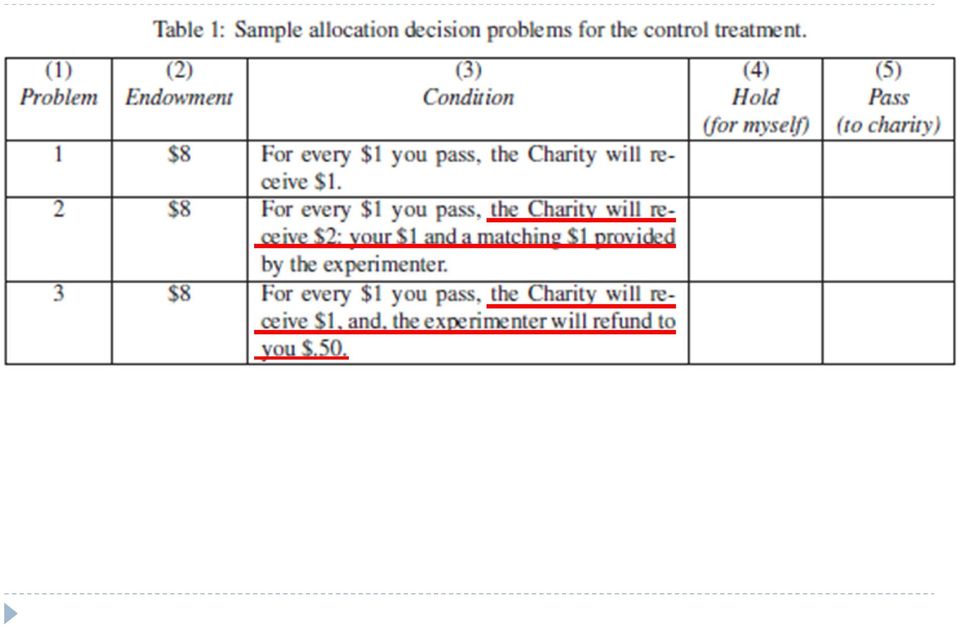

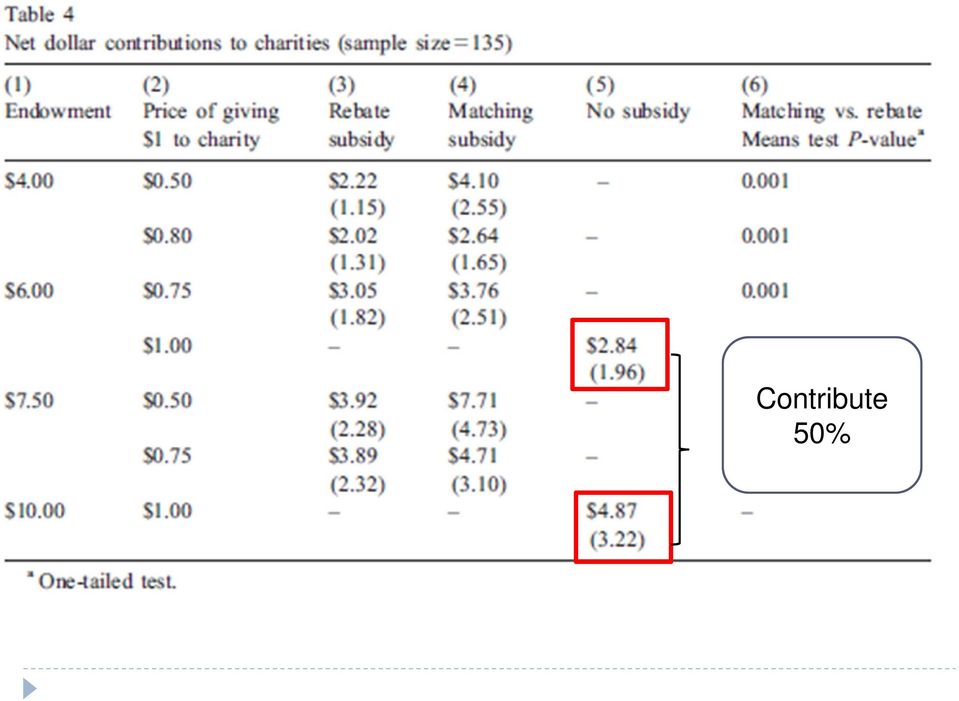

5 2.a. Match vs subsidy Eckel and Grossman (2003) present participants with a series of subsidies and comparable matches Match or subsidy Endowment: 40, 60, 75, or 100 tokens Rebate: 20, 25, and 50% Match rates: 25, 33, and 100%. Cost to the subject of contributing $1 to the charity: $1, $0.80, $0.75, and $0.50

6 Eckel and Grossman, 2003 Equivalent matches and rebates: Rebate, r: Max U(x,g) s.t. x + (1-r) g = w FOC: MRS = 1-r Match, m: Max U(x,(1+m)g) s.t. x + g = w FOC: (1+m) MRS = 1 Contributions are the same under r and m when 1-r = 1/(1+m ) E.g. match of 25 and rebate of 20: 0.8 = 1/1.25

g) s.t.")

7

8

9

10

11

12

13

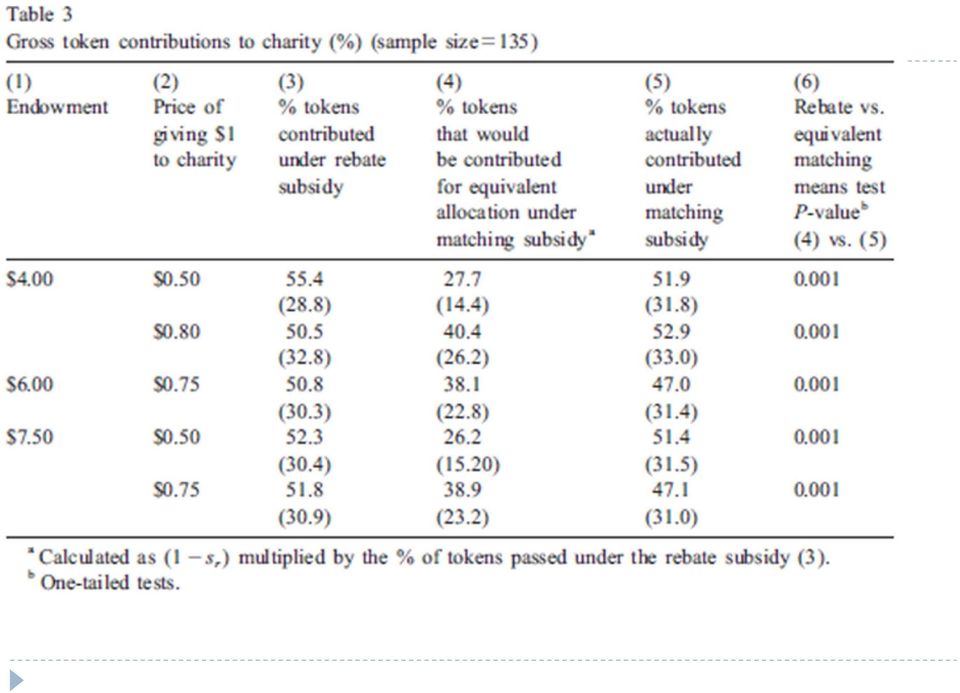

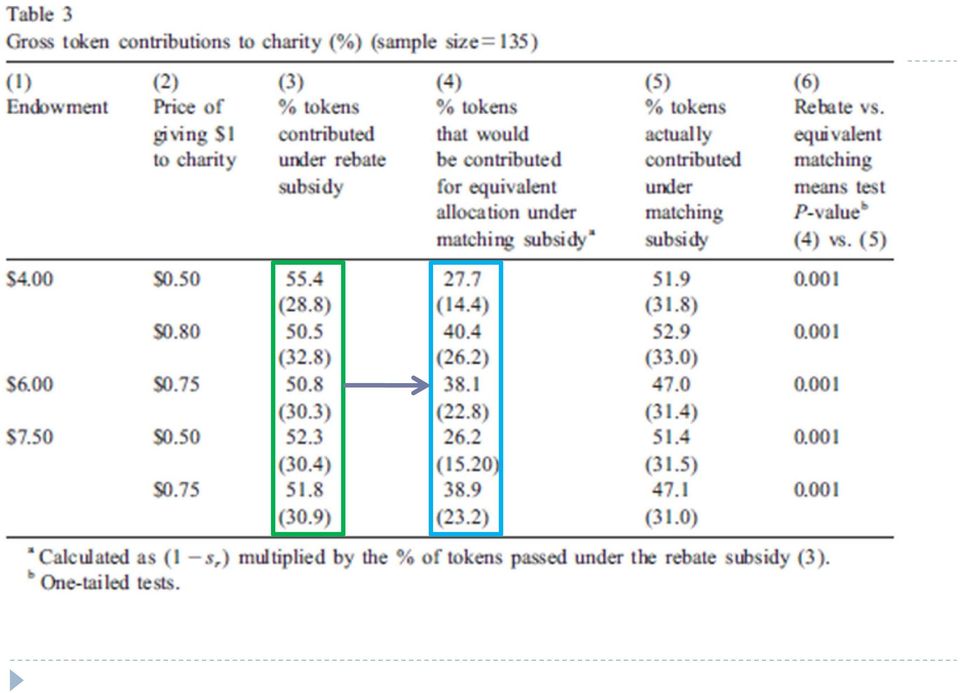

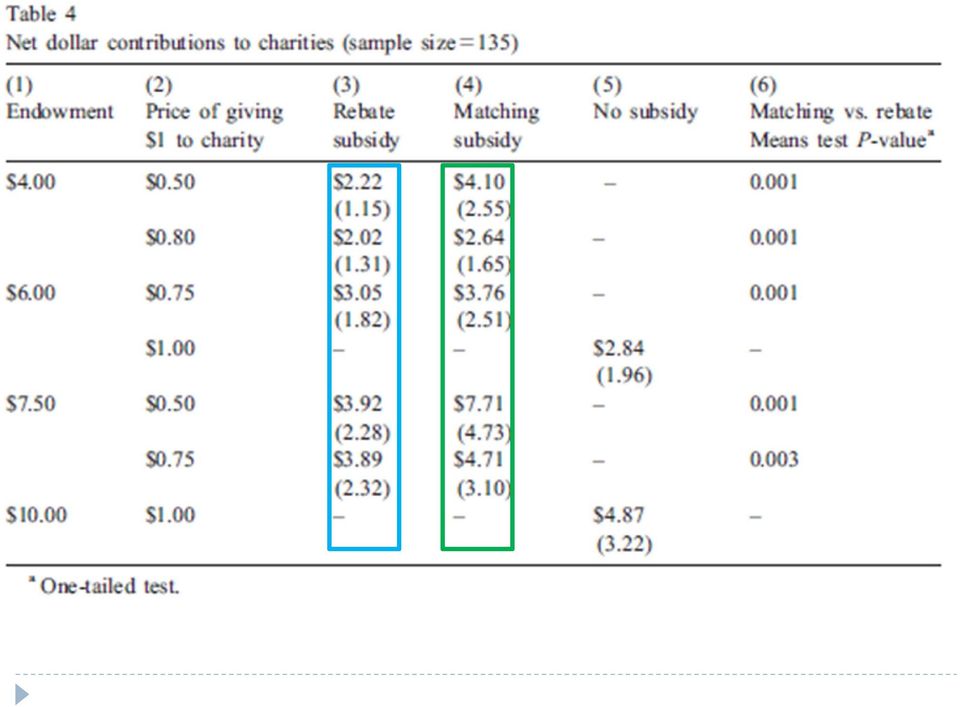

14 Eckel and Grossman, 2003 Match and subsidy not perceived the same Donors presented with a match contribute times more than those presented with the equivalent subsidy Similar results shown by Eckel and Grossman (2006ab), Davis et al. (2005), and Davis and Millner (2005) Davis and Millner (2005): charity receipts were twice as high under the 100% matching subsidy than under the 50% refund condition argue confusion-based-constant pass rule

, and Davis and Millner (2005) Davis and Millner (2005): charity receipts were twice as high under the")

15 Contribute 50% Contribute 50%

16 Match vs. subsidy Going back to our initial question. Does giving respond to salient price changes?

17

18 Contribute 50%

19 Davis (2006): Isolation effect - subjects focus only on their nominal contribution ignoring subsidy Contribute 50%

20 Robust? Eckel and Grossman (2006b) between-subject design to reduce the possibility of subjects confusing the two different subsidy methods. Subjects encounter only one subsidy type. Same result. Eckel and Grossman (2006a) Subjects allowed to choose between a 50 percent rebate subsidy and a 100 percent matching subsidy. Rebate and match equally likely to be picked total donations under the match significantly higher than under the rebate subsidy. Same result Davis, et al. (2005) within-subjects design + tables detailing the consequences of all possible giving alternatives. Same result (smaller difference) Davis and Millner (2005) within-subjects design with private good (chocolate bars) instead of charitable donation). Evidence of constant contribution behavior from the subjects, subjects seem to prefer matching subsidies to rebate subsidies; participants purchased significantly more chocolate bars under the matching sales format.

within-subjects design + tables detailing the consequences of all possible giving alternatives.")

21 Match vs. rebate Preference hypothesis: E.g. Benabou and Tirole (2006) suggest this tendency is consistent with the idea of warm glow effect of giving. Donors prefer a matching subsidy over a rebate because they feel greedy accepting rebates from their donation, and this reduces the utility gained from any donation. Matching subsidies do not have this effect Isolation effect or confusion-based-constant pass rule See also Lukas, Grossman and Eckel (2011)

22 Meier, 2007 Examine long run effects of short term matching incentives Donation to one or two university funds Match offered if contribute to both: If you contribute to both social funds, an anonymous donor matches your contribution with CHF 3 (25%) or CHF 6 (50%) Possible effects after match removed Return to pre-match contribution levels Sustain giving seen under match Decrease giving below pre-match contribution level if match crowds out incentive to give

23 Meier, 2007

24

25

26

27

28

29 - Treatment year: Contribution to two funds increase and contribution to one fund decreases - After treatment: don t return to one fund

30

31

32

33 - After treatment: less likely to make positive contribution - Average contribution lower after treatment

34

35 - Max contributors: Greater decrease for treated group suggest not simply intertemporal substitution.

36 Meier, 2007 Match Has short term positive effects Long term negative effects: negative effect on the participation rate willingness to contribute may be undermined by the temporary incentive to give

37 Karlan and List (2007) large scale natural field experiment involving a capital campaign for a liberal politically-oriented non-profit that focuses on social issues and civil liberties Determine the effect of matching contributions Mail solicitations to 50,000 supporters using different treatments control (no-subsidy) matching subsidies at varying rates $1 for $1 match $2 for $1 match $3 for $1 match

38

39

40

41

42 Karlan and List, 2007 Findings: Matching subsidy significantly increases likelihood of contributing (by 22%) amount given (by 19%). Increasing subsidy amount above the 1:1 match does not further affect contributions. Similar to scaling effect (Kahneman and Knetsch, 1992). Scaling effects may critically undermine willingness to pay elicitations in contingent valuation studies [report the same willingness to pay to clean up Lake Ontario as the entire Great Lakes]

43 Karlan, List, and Shafir (2010) Examine smaller matches (1:1 and 1:3) a liberal organization that focuses on civil justice issues. Although the organization is different, it is of similar spirit to the organization used in Karlan and List (2007). Contacted 20,000 individuals who had previously contributed Findings: Giving patterns are the same across the 1:3 vs 1:1 match Neither match influences giving Warm vs. cold list donor: warm list donors respond more favorably to match funds than cold list agents

44 2.c. Reconciling the difference in experimental and non-experimental data Experimental studies (lab and field) Response to subsidies/rebate smaller than response to matches Response to salient incentives to give rather limited How do we reconcile these findings with the non-experimental evidence that charitable deductions decrease with the price of giving (i.e., marginal tax rate)? Charitable donations may be used for tax evasion of particular concern on non-cash gifts

45 Non-cash gifts Tax deduction may be obtained for donations of property Property types: Securities, art and collectibles, real estate and easements, computers and office equipment and supplies, Vehicles, new and used clothing and household items, food and drugs, inventory property of businesses, intellectual property such as patents and personal papers. Can deduct the fair market value of the donated property Noncash gift (2005) 25.4 million itemizing taxpayers reported $48.1 billion in deductions for noncash charitable contributions, $41.1 billion of the contributions were from the 6.6 million donors who made at least $500 in noncash gifts. These donations resulted in a tax expenditure of over $9 billion for 2005.

46 2.c. Charitable deduction used for tax avoidance Non-cash gifts <$250 no receipt from charity required $250-$500 receipt must be obtained but need not be attached $500+ must submit documentation $5,000 a qualified appraisal needed Ackerman & Auten (2008) Examine characteristics of non-cash gifts

47

48 Can t rule out that people under-report

49 2.c. Charitable deduction used for tax avoidance Ackerman & Auten (2008) Vehicle donations from subset of those reporting noncash donations of at least $500 because (only these taxpayers are required to report detailed information about their donated items). Prior to 2005: taxpayers donating vehicles of less than $5,000 were responsible for assigning the value themselves After 2005: donations in excess of $500 limited to the gross proceeds form the sale

50

51

52 2.c. Charitable deduction used for tax avoidance Ackerman & Auten (2008) Evidence of significant overvaluation of used cars by donors on their tax forms. Yermack (2008) Examine large charitable stock gifts by Chairmen and CEOs of public companies. Examine gifts to family foundations. These gifts (not subject to insider trading law) often occur just before sharp declines in their companies' share prices. Timing is more pronounced when executives donate their shares to their own family foundations

53

54

55 Back dating Yermack Evidence related to reporting delays and seasonal patterns suggests that some CEOs backdate stock gifts to increase personal income tax benefits. CEOs' family foundations hold donated stock for long periods rather than diversifying, permitting CEOs to continue voting the shares. Nixon back dating: The most famous case of a fraudulently backdated charitable gift came to light in the 1974 Congressional investigation of President Richard M. Nixon s personal income tax returns. While serving as president, Nixon donated his vice presidential papers from the Eisenhower administration to the National Archives and claimed that the gift had occurred in early 1969, entitling him to a $576,000 tax deduction. Congressional testimony by a federal archivist later revealed that the true date of the gift was one year later, after an intervening change in federal law had made the deduction worthless. Nixon denied knowledge of the backdating, was ordered to pay restitution to the U.S. Treasury. His tax advisor pleaded guilty to fraud and received a four month jail sentence.

56 Charitable deductions as tax shelter Fack and Landais (2010) Three welfare sufficient statistics necessary to assess tax subsidy optimality Price elasticity of reported contributions Share of contributions that are cheated Price elasticity of cheating contributions Conclude: cheating is a first-order consideration for the design of optimal subsidies Cheating may play a central role in our estimates of price sensitivity Perhaps an explanation for the lower price sensitivity for religious giving?

57 Next: Groups: Norms, Institutions and sorting Elinor Ostrom, Governing the Commons, chapter 3, Governing the Commons: The Evolution of Institutions for Collective Action Theodore Bergstrom, The Uncommon Insight of Elinor Ostrom, Scandinavian Journal of Economics, 2010 Ahn, T.K., Mark Isaac and Timothy C. Salmon. Coming and Going: Experiments on Endogenous Group Sizes for Excludable Public Goods. Journal of Public Economics, Vol. 93, No. 1-2 (2009): Ahn, T.K., Mark Isaac and Timothy C. Salmon.Endogenous Group Formation, Journal of Public Economic Theory, Vol 10. No. 2 (2008) Sutter, Matthias, Stefan D. Haigner, and Martin G. Kocher Choosing the Carrot or the Stick? Endogenous Institutional Choice in Social Dilemma Situations. Cinyabuguma, Matthias, Talbot Page, and Louis Putterman Cooperation under the Threat of Expulsion in a Public Goods Experiment. Journal of Public Economics, 89: Ehrhart, Karl-Martin, and Claudia Keser Mobility and Cooperation: On the Run. Gürerk, Özgür, Bernd Irlenbusch, and Bettina Rockenbach The Competitive Advantage of Sanctioning Institutions. Science, 312(5770):

58 Frey and Meier (AER 2004) Findings: 64% info: 77% contribute to at least one fund 46% info: 74.7% contribute to at least one fund Difference not significant Controlling for past behavior find greater giving in 64% info treatment Conclude: information on other giving increases contributions but mostly for those who have not previously made a contribution decision

59

Tax-Exempt Organizations Alert: Reporting Requirements for Non-Cash Charitable Donations under the Form 990

Tax-Exempt Organizations Alert: Reporting Requirements for Non-Cash Charitable Donations under the Form 990 Introduction In an attempt to improve compliance with the regulations surrounding charitable

Tax-Exempt Organizations Alert: Reporting Requirements for Non-Cash Charitable Donations under the Form 990 Introduction In an attempt to improve compliance with the regulations surrounding charitable

BASIC FACTS ON CHARITABLE GIVING. David Joulfaian US Department of the Treasury

OTA Papers BASIC FACTS ON CHARITABLE GIVING by David Joulfaian US Department of the Treasury OTA Paper 95 June 2005 OTA Papers is an occasional series of reports on the research, models, and data sets

OTA Papers BASIC FACTS ON CHARITABLE GIVING by David Joulfaian US Department of the Treasury OTA Paper 95 June 2005 OTA Papers is an occasional series of reports on the research, models, and data sets

The Price Elasticity of Charitable Giving: Does the Form of Tax Relief Matter?

The Price Elasticity of Charitable Giving: Does the Form of Tax Relief Matter? Kimberley Scharf (University of Warwick and CEPR) Sarah Smith (University of Bristol and IFS) This version: March 2010 Abstract

The Price Elasticity of Charitable Giving: Does the Form of Tax Relief Matter? Kimberley Scharf (University of Warwick and CEPR) Sarah Smith (University of Bristol and IFS) This version: March 2010 Abstract

The price elasticity of charitable giving: does the form of tax relief matter? October 2010 Working Paper No. 10/247

THE CENTRE FOR MARKET AND PUBLIC ORGANISATION The price elasticity of charitable giving: does the form of tax relief matter? Sarah Smith Kim Scharf October 2010 Working Paper No. 10/247 Centre for Market

THE CENTRE FOR MARKET AND PUBLIC ORGANISATION The price elasticity of charitable giving: does the form of tax relief matter? Sarah Smith Kim Scharf October 2010 Working Paper No. 10/247 Centre for Market

The vast majority of Americans make charitable

24 Why Do People Give? LISE VESTERLUND The vast majority of Americans make charitable contributions. In 2000, 90 percent of U.S. households donated on average $1,623 to nonprofit organizations. 1 Why do

24 Why Do People Give? LISE VESTERLUND The vast majority of Americans make charitable contributions. In 2000, 90 percent of U.S. households donated on average $1,623 to nonprofit organizations. 1 Why do

Sarasota Memorial Healthcare Foundation, Inc. Planned Giving Office 1515 South Osprey Avenue, Suite B-4 Sarasota, FL 34239 941-917-1286

Sarasota Memorial Healthcare Foundation, Inc. Planned Giving Office 1515 South Osprey Avenue, Suite B-4 Sarasota, FL 34239 941-917-1286 Charitable Gift Substantiation Requirements by Conrad Teitell, A.B.,

Sarasota Memorial Healthcare Foundation, Inc. Planned Giving Office 1515 South Osprey Avenue, Suite B-4 Sarasota, FL 34239 941-917-1286 Charitable Gift Substantiation Requirements by Conrad Teitell, A.B.,

Church Administration Matters

Church Administration Matters Greg Hickle Minnesota District Secretary/Treasurer Charitable Contribution Receipts Proper receipting of Charitable Contributions by churches is extremely important to those

Church Administration Matters Greg Hickle Minnesota District Secretary/Treasurer Charitable Contribution Receipts Proper receipting of Charitable Contributions by churches is extremely important to those

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Many Taxpayers Are Still Not Complying With Noncash Charitable Contribution Reporting Requirements December 20, 2012 Reference Number: 2013-40-009 This

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Many Taxpayers Are Still Not Complying With Noncash Charitable Contribution Reporting Requirements December 20, 2012 Reference Number: 2013-40-009 This

TAX EXPENDITURES FOR NONCASH CHARITABLE CONTRIBUTIONS

National Tax Journal, June 2011, 64 (2, Part 2), 651 688 TAX EXPENDITURES FOR NONCASH CHARITABLE CONTRIBUTIONS Deena Ackerman and Gerald Auten This paper examines the itemized deduction for donations of

National Tax Journal, June 2011, 64 (2, Part 2), 651 688 TAX EXPENDITURES FOR NONCASH CHARITABLE CONTRIBUTIONS Deena Ackerman and Gerald Auten This paper examines the itemized deduction for donations of

SAMPLE Gift Acceptance Policies and Procedures for Annual Fundraising

SAMPLE Gift Acceptance Policies and Procedures for Annual Fundraising A. Cash Gifts and Pledges 1. Unrestricted Gifts of Cash Gifts given without restriction on the use of the gift. a) Unrestricted gifts

SAMPLE Gift Acceptance Policies and Procedures for Annual Fundraising A. Cash Gifts and Pledges 1. Unrestricted Gifts of Cash Gifts given without restriction on the use of the gift. a) Unrestricted gifts

Substantiation, Recordkeeping and Reporting Requirements for Deduction of Charitable Contributions

Substantiation, Recordkeeping and Reporting Requirements for Deduction of Charitable Contributions Cash Contributions Contributions in cash, check or other monetary form, regardless of amount, are not

Substantiation, Recordkeeping and Reporting Requirements for Deduction of Charitable Contributions Cash Contributions Contributions in cash, check or other monetary form, regardless of amount, are not

Giving Today to Guarantee Tomorrow: Charitable Gifts of Life Insurance

Giving Today to Guarantee Tomorrow: Charitable Gifts of Life Insurance A gift of life insurance can represent a substantial future gift to a favorite charity at relatively little cost to you. Table of

Giving Today to Guarantee Tomorrow: Charitable Gifts of Life Insurance A gift of life insurance can represent a substantial future gift to a favorite charity at relatively little cost to you. Table of

Vehicle Donation, A Donor s Guide to EXEMPT ORGANIZATIONS BEFORE YOU GIVE YOUR VEHICLE TO A CHARITABLE ORGANIZATION: ARE AS A DONOR TO A CHARITY

Tax Exempt and Government Entities EXEMPT ORGANIZATIONS A Donor s Guide to Vehicle Donation, BEFORE YOU GIVE YOUR VEHICLE TO A CHARITABLE ORGANIZATION: n CHECK OUT THE CHARITY, n SEE IF YOU LL GET A TAX

Tax Exempt and Government Entities EXEMPT ORGANIZATIONS A Donor s Guide to Vehicle Donation, BEFORE YOU GIVE YOUR VEHICLE TO A CHARITABLE ORGANIZATION: n CHECK OUT THE CHARITY, n SEE IF YOU LL GET A TAX

Do Subsidies Increase Charitable Giving in the Long Run? Matching Donations in a Field Experiment

No. 06 18 Do Subsidies Increase Charitable Giving in the Long Run? Matching Donations in a Field Experiment Stephan Meier Abstract Offering incentives to promote charitable giving (for example, to encourage

No. 06 18 Do Subsidies Increase Charitable Giving in the Long Run? Matching Donations in a Field Experiment Stephan Meier Abstract Offering incentives to promote charitable giving (for example, to encourage

Step 1 - Determine Eligibility

Step 1 - Determine Eligibility For a car donation to be eligible for a tax deduction, it must be made solely for charitable or public purposes by an individual who will itemize deduction on Schedule A

Step 1 - Determine Eligibility For a car donation to be eligible for a tax deduction, it must be made solely for charitable or public purposes by an individual who will itemize deduction on Schedule A

FAQs on 501(c)(4) Social Welfare Organizations

(4) Social Welfare Organizations") May 20, 2013 FAQs on 501(c)(4) Social Welfare Organizations What are 501(c)(4) social welfare organizations? Section 501(c)(4) social welfare organizations are tax-exempt organizations that have as their

May 20, 2013 FAQs on 501(c)(4) Social Welfare Organizations What are 501(c)(4) social welfare organizations? Section 501(c)(4) social welfare organizations are tax-exempt organizations that have as their

National Capital Gift Planning Council

National Capital Gift Planning Council Nuts and Bolts Session September 16, 2015 Craig Stevens, Aronson LLC www.aronsonllc.com 1 Income Tax and Tax Brackets Calculating Income Tax Gross Income Everything

National Capital Gift Planning Council Nuts and Bolts Session September 16, 2015 Craig Stevens, Aronson LLC www.aronsonllc.com 1 Income Tax and Tax Brackets Calculating Income Tax Gross Income Everything

Does Charity Begin at Home or Overseas?

ISSN 1178-2293 (Online) University of Otago Economics Discussion Papers No. 1504 JUNE 2015 Does Charity Begin at Home or Overseas? Stephen Knowles 1 and Trudy Sullivan 2 Address for correspondence: Stephen

ISSN 1178-2293 (Online) University of Otago Economics Discussion Papers No. 1504 JUNE 2015 Does Charity Begin at Home or Overseas? Stephen Knowles 1 and Trudy Sullivan 2 Address for correspondence: Stephen

Common issues surrounding non-cash contributions

Accepting Unique or Unusual Contributions By Laura J. Kenney and Nancy Murphy * It is not easy to say "thanks, but no thanks" to a donor. In some cases, however, "no thanks" may be the wisest answer for

Accepting Unique or Unusual Contributions By Laura J. Kenney and Nancy Murphy * It is not easy to say "thanks, but no thanks" to a donor. In some cases, however, "no thanks" may be the wisest answer for

Investing in Institutions for Cooperation

Investing in Institutions for Cooperation Alexander Smith Xi Wen September 18, 2014 Abstract We present a public good game experiment on making the tradeoff between investing in contribution productivity

Investing in Institutions for Cooperation Alexander Smith Xi Wen September 18, 2014 Abstract We present a public good game experiment on making the tradeoff between investing in contribution productivity

Overview of the Philanthropic Impact of the American Taxpayer Relief Act of 2012

January 3, 2013 Overview of the Philanthropic Impact of the American Taxpayer Relief Act of 2012 A WHITE PAPER by Robert Sharpe Overview of the Philanthropic Impact of the American Taxpayer Relief Act

January 3, 2013 Overview of the Philanthropic Impact of the American Taxpayer Relief Act of 2012 A WHITE PAPER by Robert Sharpe Overview of the Philanthropic Impact of the American Taxpayer Relief Act

IMPACT. November/December 2014. It s not business, it s personal Personal goodwill offers opportunities for M&A planning

tax November/December 2014 IMPACT It s not business, it s personal Personal goodwill offers opportunities for M&A planning International estate planning: Handle with care Why substantiating your charitable

tax November/December 2014 IMPACT It s not business, it s personal Personal goodwill offers opportunities for M&A planning International estate planning: Handle with care Why substantiating your charitable

FINANCIAL STRATEGIES TRACK DIVERSIFYING REVENUE STREAMS. Funded in part through a Cooperative Agreement with the U.S. Small Business Administration

FINANCIAL STRATEGIES TRACK DIVERSIFYING REVENUE STREAMS Agenda My Non-Profit Experience 15 Revenue Sources 5-Step Revenue Development Process Summary Resources 1 15 Revenue Sources 1. Annual/Sustained

FINANCIAL STRATEGIES TRACK DIVERSIFYING REVENUE STREAMS Agenda My Non-Profit Experience 15 Revenue Sources 5-Step Revenue Development Process Summary Resources 1 15 Revenue Sources 1. Annual/Sustained

Internal Revenue Service

Internal Revenue Service Number: 201027015 Release Date: 7/9/2010 Index Number: 170.01-00 ------------------------------------------------------------ -------- --------------------------- ---------------------------------------

Internal Revenue Service Number: 201027015 Release Date: 7/9/2010 Index Number: 170.01-00 ------------------------------------------------------------ -------- --------------------------- ---------------------------------------

How Can Bill and Melinda Gates Increase Other People s Donations to Fund Public Goods? Dean Karlan and John A. List * January 12, 2014.

How Can Bill and Melinda Gates Increase Other People s Donations to Fund Public Goods? Dean Karlan and John A. List * January 12, 2014 Abstract We conducted two matching grant experiments with an international

How Can Bill and Melinda Gates Increase Other People s Donations to Fund Public Goods? Dean Karlan and John A. List * January 12, 2014 Abstract We conducted two matching grant experiments with an international

What price charity? Exploring the effect of tax incentives on donation behaviour in the UK: an RDD approach

What price charity? Exploring the effect of tax incentives on donation behaviour in the UK: an RDD approach & Sarah Smith 1 1 Department of Economics and CMPO University of Bristol LCFS User Meeting, March

What price charity? Exploring the effect of tax incentives on donation behaviour in the UK: an RDD approach & Sarah Smith 1 1 Department of Economics and CMPO University of Bristol LCFS User Meeting, March

INSTRUCTIONS FOR BOAT DONATIONS

INSTRUCTIONS FOR BOAT DONATIONS 1. Is the boat worth more than $500? Yes, continue. No, jump to step 7 2. Will the boat be used in the program? Yes, continue. No, jump to step 10 3. Obtain from the Donor

INSTRUCTIONS FOR BOAT DONATIONS 1. Is the boat worth more than $500? Yes, continue. No, jump to step 7 2. Will the boat be used in the program? Yes, continue. No, jump to step 10 3. Obtain from the Donor

Charitable Contributions

STUDENT MODULE 14.1 CHARITABLE GIVING PAGE 1 Standard 14: The student will explain the costs and benefits of charitable giving. Charitable Contributions Hey, Bert. Did you know the band is planning a big

STUDENT MODULE 14.1 CHARITABLE GIVING PAGE 1 Standard 14: The student will explain the costs and benefits of charitable giving. Charitable Contributions Hey, Bert. Did you know the band is planning a big

Instructions for Form 8283 (Rev. December 2014)

") Instructions for Form 8283 (Rev. December 2014) Noncash Charitable Contributions Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise

Instructions for Form 8283 (Rev. December 2014) Noncash Charitable Contributions Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise

Non-cash Donations & Sales. Accounting and IRS Reporting

Non-cash Donations & Sales Accounting and IRS Reporting Contact Information Julie L. Sokolowski, CPA Shareholder Wall, Einhorn & Chernitzer, PC CPAs & Advisors 555 East Main Street, Suite 1600 Norfolk,

Non-cash Donations & Sales Accounting and IRS Reporting Contact Information Julie L. Sokolowski, CPA Shareholder Wall, Einhorn & Chernitzer, PC CPAs & Advisors 555 East Main Street, Suite 1600 Norfolk,

Vehicle Donation, A Charity s Guide to EXEMPT ORGANIZATIONS TYPES OF VEHICLE DONATION PROGRAMS AND THEIR IMPACT ON TAX-EXEMPT STATUS,

Tax Exempt and Government Entities EXEMPT ORGANIZATIONS A Charity s Guide to Vehicle Donation, TYPES OF VEHICLE DONATION PROGRAMS AND THEIR IMPACT ON TAX-EXEMPT STATUS, TAXABLE INCOME, AND DEDUCTIBLE CONTRIBUTIONS

Tax Exempt and Government Entities EXEMPT ORGANIZATIONS A Charity s Guide to Vehicle Donation, TYPES OF VEHICLE DONATION PROGRAMS AND THEIR IMPACT ON TAX-EXEMPT STATUS, TAXABLE INCOME, AND DEDUCTIBLE CONTRIBUTIONS

Charitable Gifts of Life Insurance. in brief

Charitable Gifts of Life Insurance in brief Why Life Insurance? Leverage The greatest advantage of a gift of life insurance is that a donor can make a substantially larger gift to charity by using life

Charitable Gifts of Life Insurance in brief Why Life Insurance? Leverage The greatest advantage of a gift of life insurance is that a donor can make a substantially larger gift to charity by using life

SAMPLE GIFT ACCEPTANCE POLICIES

SAMPLE GIFT ACCEPTANCE POLICIES ABC Charity, a nonprofit organization headquartered in City, State, encourages the solicitation and acceptance of gifts to ABC Charity (hereinafter referred to as ABC) for

SAMPLE GIFT ACCEPTANCE POLICIES ABC Charity, a nonprofit organization headquartered in City, State, encourages the solicitation and acceptance of gifts to ABC Charity (hereinafter referred to as ABC) for

1. The organization mission or most significant activities that you wish to highlight this year:

Form 990 Questionnaire For All Organizations Core Form Heading & Pt I Summary 1. The organization mission or most significant activities that you wish to highlight this year: 2. Total number of volunteers

Form 990 Questionnaire For All Organizations Core Form Heading & Pt I Summary 1. The organization mission or most significant activities that you wish to highlight this year: 2. Total number of volunteers

CHARITABLE FOUNDATIONS: ANOTHER OPTION TO HELP FINANCE SCHOOL ACTIVITIES. Fall 1999

CHARITABLE FOUNDATIONS: ANOTHER OPTION TO HELP FINANCE SCHOOL ACTIVITIES Fall 1999 Written for WASB's Legal Services Membership by Lathrop & Clark LLP School districts continue to be faced with the challenge

CHARITABLE FOUNDATIONS: ANOTHER OPTION TO HELP FINANCE SCHOOL ACTIVITIES Fall 1999 Written for WASB's Legal Services Membership by Lathrop & Clark LLP School districts continue to be faced with the challenge

How To Raise Money For Charity

Fundraising in a nutshell for nonprofit CEOs & development staff: Leveraging charitable giving in the current environment Meg Greene, Esq. Kenleigh Nicoletta, Esq. Amelia Kurtz, Senior Fiduciary Officer

Fundraising in a nutshell for nonprofit CEOs & development staff: Leveraging charitable giving in the current environment Meg Greene, Esq. Kenleigh Nicoletta, Esq. Amelia Kurtz, Senior Fiduciary Officer

c. Restricted Gifts for Existing Activities. A gift, other than an in-kind gift, may be restricted to an existing activity, purpose, or mission of

The mission of is to share the love and grace of Jesus Christ with all people and to invite them to fullness of faith in God. 1. Purpose of the Policy a. To create and sustain positive donor relationships

The mission of is to share the love and grace of Jesus Christ with all people and to invite them to fullness of faith in God. 1. Purpose of the Policy a. To create and sustain positive donor relationships

I.R.S. October 10, 2005 Alan S. Hejnal

I.R.S. October 10, 2005 Alan S. Hejnal Outline Understanding Gifts What is, and what is not, a gift, according to the IRS Key characteristics Common activities that are not gifts Identifying the legal

I.R.S. October 10, 2005 Alan S. Hejnal Outline Understanding Gifts What is, and what is not, a gift, according to the IRS Key characteristics Common activities that are not gifts Identifying the legal

GIFT ACCEPTANCE POLICY

INTRODUCTION The University of Vermont and State Agricultural College Foundation, Inc. (the Foundation ) was incorporated as a Vermont nonprofit corporation on March 14, 2011. The Foundation is exempted

INTRODUCTION The University of Vermont and State Agricultural College Foundation, Inc. (the Foundation ) was incorporated as a Vermont nonprofit corporation on March 14, 2011. The Foundation is exempted

PRIVATE FOUNDATION VERSUS PUBLIC CHARITY (Non Profit Advisory No. 5)

") PRIVATE FOUNDATION VERSUS PUBLIC CHARITY (Non Profit Advisory No. 5) Most nonprofit entities -- and especially their primary donors -- want to insure that they have public charity status for the 50% deduction

PRIVATE FOUNDATION VERSUS PUBLIC CHARITY (Non Profit Advisory No. 5) Most nonprofit entities -- and especially their primary donors -- want to insure that they have public charity status for the 50% deduction

CHAPTER 9 Charitable Giving

CHAPTER 9 Charitable Giving DISCUSSION QUESTIONS 1. What factors must an individual consider before making a charitable gift? A donor needs to consider his charitable objectives and the desired timing

CHAPTER 9 Charitable Giving DISCUSSION QUESTIONS 1. What factors must an individual consider before making a charitable gift? A donor needs to consider his charitable objectives and the desired timing

Gift In Kind Policies. This is the University of Virginia policy for the acceptance, recording and disposition of gifts of personal property.

Gift In Kind Policies This is the University of Virginia policy for the acceptance, recording and disposition of gifts of personal property. Tangible Personal Property Tangible personal property is property,

Gift In Kind Policies This is the University of Virginia policy for the acceptance, recording and disposition of gifts of personal property. Tangible Personal Property Tangible personal property is property,

Report to Congress on Supporting Organizations and Donor Advised Funds

Report to Congress on Supporting Organizations and Donor Advised Funds Department of the Treasury December 2011 Table of Contents Chapter 1: Introduction and Summary... 1 Mandate and Scope of the Study...

Report to Congress on Supporting Organizations and Donor Advised Funds Department of the Treasury December 2011 Table of Contents Chapter 1: Introduction and Summary... 1 Mandate and Scope of the Study...

Non-Financial Assets Tax and Other Special Rules

Wealth Strategy Report Non-Financial Assets Tax and Other Special Rules OVERVIEW Because unique attributes distinguish them from other asset classes, nonfinancial assets may offer you valuable financial

Wealth Strategy Report Non-Financial Assets Tax and Other Special Rules OVERVIEW Because unique attributes distinguish them from other asset classes, nonfinancial assets may offer you valuable financial

Donating a Used Vehicle to Charity

Donating a Used Vehicle to Charity KLR Not-for-Profit Services Group May 2015 www.kahnlitwin.com Boston Cambridge Newport Providence Shanghai Waltham 888-KLR-8557 TrustedAdvisors@KahnLitwin.com Donating

Donating a Used Vehicle to Charity KLR Not-for-Profit Services Group May 2015 www.kahnlitwin.com Boston Cambridge Newport Providence Shanghai Waltham 888-KLR-8557 TrustedAdvisors@KahnLitwin.com Donating

RESPONSIBILITIES OF DIRECTORS AND OFFICERS OF CALIFORNIA NONPROFIT PUBLIC BENEFIT CORPORATIONS

RESPONSIBILITIES OF DIRECTORS AND OFFICERS OF CALIFORNIA NONPROFIT PUBLIC BENEFIT CORPORATIONS William C. Staley Attorney www.staleylaw.com 818 936-3490 Los Angeles June 16, 2005 RESPONSIBILITIES OF DIRECTORS

RESPONSIBILITIES OF DIRECTORS AND OFFICERS OF CALIFORNIA NONPROFIT PUBLIC BENEFIT CORPORATIONS William C. Staley Attorney www.staleylaw.com 818 936-3490 Los Angeles June 16, 2005 RESPONSIBILITIES OF DIRECTORS

How To Be A Good Fundraiser

A Legal Checklist for Not-for-Profit Organizations This 10-point checklist is written to help busy charitable organizations stay on top of today s regulatory compliance requirements. For further information,

A Legal Checklist for Not-for-Profit Organizations This 10-point checklist is written to help busy charitable organizations stay on top of today s regulatory compliance requirements. For further information,

IRS Rules & Regs Presented by: Catherine K. Spickard Director of Development Services University of Michigan CASE Gift Processing Workshop 1 Topics of the Day All about Gifts What is a gift and what is

IRS Rules & Regs Presented by: Catherine K. Spickard Director of Development Services University of Michigan CASE Gift Processing Workshop 1 Topics of the Day All about Gifts What is a gift and what is

Frequently asked Questions

Frequently asked Questions By NONPROFITS About Taxes (2014 Revised Edition) ANSWERS* TO QUESTIONS FREQUENTLY ASKED ABOUT - COMPENSATION & BENEFITS We heard that our pastor is both an employee and an independent

Frequently asked Questions By NONPROFITS About Taxes (2014 Revised Edition) ANSWERS* TO QUESTIONS FREQUENTLY ASKED ABOUT - COMPENSATION & BENEFITS We heard that our pastor is both an employee and an independent

Investing in Institutions for Cooperation

Investing in Institutions for Cooperation Alexander Smith Xi Wen March 20, 2015 Abstract We present a voluntary contribution mechanism public good game experiment on investing in contribution productivity

Investing in Institutions for Cooperation Alexander Smith Xi Wen March 20, 2015 Abstract We present a voluntary contribution mechanism public good game experiment on investing in contribution productivity

EXECUTIVE SUMMARY M S I - S T A T E W I D E S U R V E Y O N I N S U R A N C E F R A U D

EXECUTIVE SUMMARY The majority of Virginians believe you should obey the law without question but also suggest that right and wrong are ultimately determined by the individual. Nearly three out of five

EXECUTIVE SUMMARY The majority of Virginians believe you should obey the law without question but also suggest that right and wrong are ultimately determined by the individual. Nearly three out of five

CHARITABLE CONTRIBUTIONS SUBSTANTIATION AND DISCLOSURE REQUIREMENTS

CHARITABLE CONTRIBUTIONS SUBSTANTIATION AND DISCLOSURE REQUIREMENTS This document explains the federal tax law for organizations such as charities and churches that receive tax deductible charitable contributions

CHARITABLE CONTRIBUTIONS SUBSTANTIATION AND DISCLOSURE REQUIREMENTS This document explains the federal tax law for organizations such as charities and churches that receive tax deductible charitable contributions

Charitable Giving. James Andreoni UCSD and NBER. A. Abigail Payne McMaster University

Charitable Giving James Andreoni UCSD and NBER A. Abigail Payne McMaster University For the Handbook of Public Economics, Alan Auerbach, Raj Chetty, Martin Feldstein, Emmanuel Saez, editors December 2011

Charitable Giving James Andreoni UCSD and NBER A. Abigail Payne McMaster University For the Handbook of Public Economics, Alan Auerbach, Raj Chetty, Martin Feldstein, Emmanuel Saez, editors December 2011

Substantiation and Acknowledgment of Gifts A Practical Guide

Substantiation and Acknowledgment of Gifts A Practical Guide Ellis M. Carter, J.D., LL.M. in Taxation Carter Law Group, P.C. 849 N. 3 rd. Avenue Phoenix, Arizona 85003 Ph. 602.456.0071 Fax 602.296.0415

Substantiation and Acknowledgment of Gifts A Practical Guide Ellis M. Carter, J.D., LL.M. in Taxation Carter Law Group, P.C. 849 N. 3 rd. Avenue Phoenix, Arizona 85003 Ph. 602.456.0071 Fax 602.296.0415

DOCUMENT RETENTION AND DESTRUCTION POLICY

DOCUMENT RETENTION AND DESTRUCTION POLICY I. Purpose This policy provides for the systematic review, retention, and destruction of documents received or created by [ORGANIZATION NAME] in connection with

DOCUMENT RETENTION AND DESTRUCTION POLICY I. Purpose This policy provides for the systematic review, retention, and destruction of documents received or created by [ORGANIZATION NAME] in connection with

Nonprofit Fundraising 2010 - Change in the Number of Companies

The 2010 Nonprofit Fundra aising Survey Funds Raised in 20100 Compared with 2009 March 2011 The Nonprof fit Research Collaborative With special thanks to the representatives of 1,845 charitable organizations

The 2010 Nonprofit Fundra aising Survey Funds Raised in 20100 Compared with 2009 March 2011 The Nonprof fit Research Collaborative With special thanks to the representatives of 1,845 charitable organizations

501(c)(3) Organizations: Fundraising, the IRS and State Law

(3) Organizations: Fundraising, the IRS and State Law") Improving the lives of women and girls through programs leading to social and economic empowerment. SOROPTIMIST INTERNATIONAL OF THE AMERICAS 501(c)(3) Organizations: Fundraising, the IRS and State Law

Improving the lives of women and girls through programs leading to social and economic empowerment. SOROPTIMIST INTERNATIONAL OF THE AMERICAS 501(c)(3) Organizations: Fundraising, the IRS and State Law

How To Write A Budget Plan For 2012

Administration's Fiscal Year 2012 Budget Provides Incentives for Innovation, Infrastructure, and Education; Middle-Class Tax Relief; a Responsible and Credible Plan for Deficit Reduction; and an Improved

Administration's Fiscal Year 2012 Budget Provides Incentives for Innovation, Infrastructure, and Education; Middle-Class Tax Relief; a Responsible and Credible Plan for Deficit Reduction; and an Improved

Charitable Organizations. Stephan J. Lipskis, Esq., Wolcott Rivers Gates

Receiving an Appropriate Charitable Deduction for Donations of Tangible Personal Property to Charitable Organizations Stephan J. Lipskis, Esq., Wolcott Rivers Gates Estate and gift counsel encounter the

Receiving an Appropriate Charitable Deduction for Donations of Tangible Personal Property to Charitable Organizations Stephan J. Lipskis, Esq., Wolcott Rivers Gates Estate and gift counsel encounter the

Using Statistical Modeling to Increase

White Paper Using Statistical Modeling to Increase Donations Executive Summary Nonprofits increasingly rely on statistical modeling to help them target their best prospects and strengthen their fundraising

White Paper Using Statistical Modeling to Increase Donations Executive Summary Nonprofits increasingly rely on statistical modeling to help them target their best prospects and strengthen their fundraising

The 2014 U.S. Trust Study of High Net Worth Philanthropy Conducted in partnership with the Indiana University Lilly Family School of Philanthropy

KEY FINDINGS The 2014 U.S. Trust Study of High Net Worth Philanthropy Conducted in partnership with the Indiana University Lilly Family School of Philanthropy The 2014 U.S. Trust Study of High Net Worth

KEY FINDINGS The 2014 U.S. Trust Study of High Net Worth Philanthropy Conducted in partnership with the Indiana University Lilly Family School of Philanthropy The 2014 U.S. Trust Study of High Net Worth

An Analysis of Canadian Philanthropic Support for International Development and Relief. Don Embuldeniya David Lasby Larry McKeown

An Analysis of Canadian Philanthropic Support for International Development and Relief Don Embuldeniya David Lasby Larry McKeown An Analysis of Canadian Philanthropic Support for International Development

An Analysis of Canadian Philanthropic Support for International Development and Relief Don Embuldeniya David Lasby Larry McKeown An Analysis of Canadian Philanthropic Support for International Development

GIFT ACCEPTANCE POLICY

GIFT ACCEPTANCE POLICY Nutrition Science Initiative, a California public benefit corporation ("NuSI") located in San Diego, California, encourages the solicitation and acceptance of gifts to NuSI for purposes

GIFT ACCEPTANCE POLICY Nutrition Science Initiative, a California public benefit corporation ("NuSI") located in San Diego, California, encourages the solicitation and acceptance of gifts to NuSI for purposes

Tax Tips & Calculators Tips from H&R Block

Tax Tips & Calculators Tips from H&R Block Overview You can deduct your contributions to charitable (non-profit) organizations only if you itemize your deductions. You can't deduct the value of your time

Tax Tips & Calculators Tips from H&R Block Overview You can deduct your contributions to charitable (non-profit) organizations only if you itemize your deductions. You can't deduct the value of your time

Charitable giving and tax policy: a historical and comparative perspective

Charitable giving and tax policy: a historical and comparative perspective Conference Volume CEPR conference May 2012 Paris School of Economics Editors Gabrielle Fack and Camille Landais Organized by CEPR

Charitable giving and tax policy: a historical and comparative perspective Conference Volume CEPR conference May 2012 Paris School of Economics Editors Gabrielle Fack and Camille Landais Organized by CEPR

Wisconsin Land Trusts

Wisconsin Land Trusts What is a Land Trust? Conservation land is essential to the health and beauty of Wisconsin. Land trusts are non-profit organizations that help protect land for public benefit. There

Wisconsin Land Trusts What is a Land Trust? Conservation land is essential to the health and beauty of Wisconsin. Land trusts are non-profit organizations that help protect land for public benefit. There

FIRST UNITED METHODIST CHURCH OF FORT WORTH

FIRST UNITED METHODIST CHURCH OF FORT WORTH Fort Worth, Texas Consolidated Financial Statements Years Ended December 31, 2012 and 2011 Consolidated Financial Statements Years Ended December 31, 2012 and

FIRST UNITED METHODIST CHURCH OF FORT WORTH Fort Worth, Texas Consolidated Financial Statements Years Ended December 31, 2012 and 2011 Consolidated Financial Statements Years Ended December 31, 2012 and

Charity, Publicity and the Donation Registry

Berkeley Law From the SelectedWorks of Robert Cooter June, 2005 Charity, Publicity and the Donation Registry Robert D. Cooter Brian J. Broughman Available at: http://works.bepress.com/robert_cooter/102/

Berkeley Law From the SelectedWorks of Robert Cooter June, 2005 Charity, Publicity and the Donation Registry Robert D. Cooter Brian J. Broughman Available at: http://works.bepress.com/robert_cooter/102/

Energy Taxation and Renewable Energy: Testing for Incentives, Framing Effects and Perceptions of Justice in Experimental Settings

PD Dr. Roland Menge International Institute for Manageme Energy Taxation and Renewable Energy: Testing for Incentives, Framing Effects and Perceptions of Justice in Experimental Settings Roland Menges

PD Dr. Roland Menge International Institute for Manageme Energy Taxation and Renewable Energy: Testing for Incentives, Framing Effects and Perceptions of Justice in Experimental Settings Roland Menges

Social Influences and the Designation of Charitable Contributions: Evidence from the Workplace

Social Influences and the Designation of Charitable Contributions: Evidence from the Workplace Katherine Grace Carman Harvard University November, 2004 This paper investigates factors that influence an

Social Influences and the Designation of Charitable Contributions: Evidence from the Workplace Katherine Grace Carman Harvard University November, 2004 This paper investigates factors that influence an

A Charity s Guide to. Types of car donation programs and their impact on tax-exempt status, taxable income, and deductible contributions

A Charity s Guide to Types of car donation programs and their impact on tax-exempt status, taxable income, and deductible contributions Internal Revenue Service Tax Exempt and Government Entities Exempt

A Charity s Guide to Types of car donation programs and their impact on tax-exempt status, taxable income, and deductible contributions Internal Revenue Service Tax Exempt and Government Entities Exempt

THE IRS AND APPRAISALS OF GIFTS AND DONATIONS Appraisers are encouraged to keep current on IRS rulings and requirements. All IRS forms and related

THE IRS AND APPRAISALS OF GIFTS AND DONATIONS Appraisers are encouraged to keep current on IRS rulings and requirements. All IRS forms and related materials are posted on the IRS web site (http://www.irs.gov).

THE IRS AND APPRAISALS OF GIFTS AND DONATIONS Appraisers are encouraged to keep current on IRS rulings and requirements. All IRS forms and related materials are posted on the IRS web site (http://www.irs.gov).

A Basic Guide to Corporate Philanthropy

A Basic Guide to Corporate Philanthropy Stephanie L. Petit November 2009 A business has reached a point where it wants to give back. It s had a year better than it expected in this economy, and it knows

A Basic Guide to Corporate Philanthropy Stephanie L. Petit November 2009 A business has reached a point where it wants to give back. It s had a year better than it expected in this economy, and it knows

Providing Disaster Relief

Providing Disaster Relief As New York City s nonprofit sector mobilizes in response to Hurricane Sandy Lawyers Alliance is ready to assist. With over 10 years of disaster relief experience Lawyers Alliance

Providing Disaster Relief As New York City s nonprofit sector mobilizes in response to Hurricane Sandy Lawyers Alliance is ready to assist. With over 10 years of disaster relief experience Lawyers Alliance

Executive Summary Planned Giving and Endowment Policies (For Donors and Donors Advisors)

") Appendix B Authority for Gift Acceptance Policies Executive Summary Planned Giving and Endowment Policies (For Donors and Donors Advisors) Independence Institute encourages and solicits outright and deferred

Appendix B Authority for Gift Acceptance Policies Executive Summary Planned Giving and Endowment Policies (For Donors and Donors Advisors) Independence Institute encourages and solicits outright and deferred

charitable contributions

charitable contributions Your ability to control when and how you make charitable contributions can lower your income tax bill, effectively reducing the actual cost of any gift you make, while fulfilling

charitable contributions Your ability to control when and how you make charitable contributions can lower your income tax bill, effectively reducing the actual cost of any gift you make, while fulfilling

2013 Year-End Tax Planning Advice

2013 Year-End Tax Planning Advice To Our Clients and Friends, As we approach year-end, it s again time to focus on last-minute moves you can make to save taxes both on your 2013 return and in future years.

2013 Year-End Tax Planning Advice To Our Clients and Friends, As we approach year-end, it s again time to focus on last-minute moves you can make to save taxes both on your 2013 return and in future years.

A Charity s Guide to. Types of car donation programs and their impact on tax-exempt status, taxable income, and deductible contributions

A Charity s Guide to Types of car donation programs and their impact on tax-exempt status, taxable income, and deductible contributions Internal Revenue Service Tax Exempt and Government Entities Exempt

A Charity s Guide to Types of car donation programs and their impact on tax-exempt status, taxable income, and deductible contributions Internal Revenue Service Tax Exempt and Government Entities Exempt

ALTERNATIVE FUNDING STRATEGIES FOR THE SUPPORT OF REGIONAL CULTURAL FACILITIES IN SOUTHEAST MICHIGAN. This project was funded in part by grants from:

ALTERNATIVE FUNDING STRATEGIES FOR THE SUPPORT OF REGIONAL CULTURAL FACILITIES IN SOUTHEAST MICHIGAN This project was funded in part by grants from: McGregor Fund The Skillman Foundation Matilda R. Wilson

ALTERNATIVE FUNDING STRATEGIES FOR THE SUPPORT OF REGIONAL CULTURAL FACILITIES IN SOUTHEAST MICHIGAN This project was funded in part by grants from: McGregor Fund The Skillman Foundation Matilda R. Wilson

Effects of Regulation on Donations to Charitable Foundations

Effects of Regulation on Donations to Charitable Foundations Ben Marx 9 March 2012 - PRELIMINARY DRAFT Abstract To curb tax avoidance and evasion through charitable foundations, the Tax Reform Act of 1969

Effects of Regulation on Donations to Charitable Foundations Ben Marx 9 March 2012 - PRELIMINARY DRAFT Abstract To curb tax avoidance and evasion through charitable foundations, the Tax Reform Act of 1969

National Conference on Philanthropic Planning

National Conference on Philanthropic Planning October 4-6, 2011 San Antonio, Texas Conference Presentation Paper Partnership for Philanthropic Planning 2011. All rights reserved. The Model Standards after

National Conference on Philanthropic Planning October 4-6, 2011 San Antonio, Texas Conference Presentation Paper Partnership for Philanthropic Planning 2011. All rights reserved. The Model Standards after

www.pwc.com/ie Charitable giving guide

www.pwc.com/ie Charitable giving guide Helping to maximise donations to the wider community March 2012 Contents Introduction 2 Relief from income tax and corporation tax on donations to eligible charities

www.pwc.com/ie Charitable giving guide Helping to maximise donations to the wider community March 2012 Contents Introduction 2 Relief from income tax and corporation tax on donations to eligible charities

Internal Revenue Service Tax Exempt and Government Entities Exempt Organizations. Applying for 501(c)(3) Tax-Exempt Status

(3) Tax-Exempt Status") Internal Revenue Service Tax Exempt and Government Entities Exempt Organizations Applying for 501(c)(3) Tax-Exempt Status 01 Why apply for 501(c)(3) status?... 2 Who is eligible for 501(c)(3) status?....

Internal Revenue Service Tax Exempt and Government Entities Exempt Organizations Applying for 501(c)(3) Tax-Exempt Status 01 Why apply for 501(c)(3) status?... 2 Who is eligible for 501(c)(3) status?....

Bridgepoint Health Foundation

POLICY: Gifts to the Foundation must align with the Mission, Vision, Values and priorities of the Foundation and the Hospital. The Foundation reserves the right to decline a gift that does not meet these

POLICY: Gifts to the Foundation must align with the Mission, Vision, Values and priorities of the Foundation and the Hospital. The Foundation reserves the right to decline a gift that does not meet these

Nonprofit Fundraising Study

Nonprofit Fundraising Study Covering Charitable Receipts at U.S. Nonprofit Organizations in 2011 April 2012 Nonprofit Research Collaborative Acknowledgements The Nonprofit Research Collaborative (NRC)

Nonprofit Fundraising Study Covering Charitable Receipts at U.S. Nonprofit Organizations in 2011 April 2012 Nonprofit Research Collaborative Acknowledgements The Nonprofit Research Collaborative (NRC)

CHAPTER 3 Tax Law INTRODUCTION GENERAL PRINCIPLES THE ABILITY TO TAX TAX ASSESSMENTS, RATES, AND SCHEDULES

CHAPTER 3 Tax Law INTRODUCTION If any business wishes to operate, it must have revenue. Taxes are the source of government revenue. In order for government to operate on a day-to-day basis and provide

CHAPTER 3 Tax Law INTRODUCTION If any business wishes to operate, it must have revenue. Taxes are the source of government revenue. In order for government to operate on a day-to-day basis and provide

Columbus Metropolitan Library Foundation Gift Acceptance Policy. Introduction

Columbus Metropolitan Library Foundation Gift Acceptance Policy Introduction Columbus Metropolitan Library Foundation (the Foundation ) is an organization recognized as exempt from federal income taxation

Columbus Metropolitan Library Foundation Gift Acceptance Policy Introduction Columbus Metropolitan Library Foundation (the Foundation ) is an organization recognized as exempt from federal income taxation

Nonprofit ACH Payment Processing. The Ins and Outs of Direct Debit Payments

Nonprofit ACH Payment Processing The Ins and Outs of Direct Debit Payments Table of Contents 01 02 03 05 06 Introduction Growth Trends in ACH Payments Benefits of ACH for Nonprofits Potential Weaknesses

Nonprofit ACH Payment Processing The Ins and Outs of Direct Debit Payments Table of Contents 01 02 03 05 06 Introduction Growth Trends in ACH Payments Benefits of ACH for Nonprofits Potential Weaknesses

INSTRUCTIONS. (3) Condition (4) Dollars in MPC to PASS to the Charity

Condition (4) Dollars in MPC to PASS to the Charity") INSTRUCTIONS Introduction: This is a decision-making experiment. Funding for this project has been provided by the National Science Foundation and various other public funding agencies. Instructions are

INSTRUCTIONS Introduction: This is a decision-making experiment. Funding for this project has been provided by the National Science Foundation and various other public funding agencies. Instructions are

PRE-BUDGET REPORT: REVIEW OF CHARITY TAXATION

PRE-BUDGET REPORT: REVIEW OF CHARITY TAXATION Sarah Tanner THE INSTITUTE FOR FISCAL STUDIES Briefing Note No. 2 Published by The Institute for Fiscal Studies 7 Ridgmount Street London WC1E 7AE Tel 020

PRE-BUDGET REPORT: REVIEW OF CHARITY TAXATION Sarah Tanner THE INSTITUTE FOR FISCAL STUDIES Briefing Note No. 2 Published by The Institute for Fiscal Studies 7 Ridgmount Street London WC1E 7AE Tel 020

Charitable Gifts By Subchapter S Corporations And By Shareholders Of S Corporation Stock

Charitable Gifts By Subchapter S Corporations And By Shareholders Of S Corporation Stock Christopher R. Hoyt A. The Big Picture There Are Usually Two Potential Donors: The Corporation And The Shareholder

Charitable Gifts By Subchapter S Corporations And By Shareholders Of S Corporation Stock Christopher R. Hoyt A. The Big Picture There Are Usually Two Potential Donors: The Corporation And The Shareholder

THE UNIVERSITY CORPORATION, SAN FRANCISCO STATE

THE UNIVERSITY CORPORATION, SAN FRANCISCO STATE GIFT ACCEPTANCE POLICY Issued: Revision: January 2016 BACKGROUND The purpose of this policy is to outline the process for the review and acceptance of gifts

THE UNIVERSITY CORPORATION, SAN FRANCISCO STATE GIFT ACCEPTANCE POLICY Issued: Revision: January 2016 BACKGROUND The purpose of this policy is to outline the process for the review and acceptance of gifts

Charitable contribution rules and requirements

Charitable contribution rules and requirements October 30, 2013 In brief Contributing to charity is an integral component of the American culture. One reason for charitable giving is the income tax benefit

Charitable contribution rules and requirements October 30, 2013 In brief Contributing to charity is an integral component of the American culture. One reason for charitable giving is the income tax benefit

ATTORNEY GENERAL S SUMMARY OF CHARITABLE SOLICITATIONS BY COMMERCIAL FUND-RAISERS

ATTORNEY GENERAL S SUMMARY OF CHARITABLE SOLICITATIONS BY COMMERCIAL FUND-RAISERS SUPPLEMENTAL REPORT: DONATIONS OF PERSONAL PROPERTY (THRIFT STORES, VEHICLE DONATION PROGRAMS, ETC.) (Government Code 12599)

ATTORNEY GENERAL S SUMMARY OF CHARITABLE SOLICITATIONS BY COMMERCIAL FUND-RAISERS SUPPLEMENTAL REPORT: DONATIONS OF PERSONAL PROPERTY (THRIFT STORES, VEHICLE DONATION PROGRAMS, ETC.) (Government Code 12599)

Before you give your car to a charitable organization:

A Donor s Guide to Before you give your car to a charitable organization: check out the charity see if you ll get a tax benefit check the value of your car see what your responsibilities are as a donor

A Donor s Guide to Before you give your car to a charitable organization: check out the charity see if you ll get a tax benefit check the value of your car see what your responsibilities are as a donor

How to Use a Schwab Charitable Donor-Advised Fund

A better way to give. What is Schwab Charitable? A Schwab Charitable donor-advised fund account is a simple, tax-smart investment solution for charitable giving. You can open a Schwab Charitable account

A better way to give. What is Schwab Charitable? A Schwab Charitable donor-advised fund account is a simple, tax-smart investment solution for charitable giving. You can open a Schwab Charitable account

ATLANTA COMMUNITY FOOD BANK, INC.

FINANCIAL STATEMENTS FOR THE YEAR ENDED TABLE OF CONTENTS INDEPENDENT AUDITORS REPORT 1 FINANCIAL STATEMENTS Statements of Financial Position 3 Statement of Activities 5 Statement of Functional Expenses

FINANCIAL STATEMENTS FOR THE YEAR ENDED TABLE OF CONTENTS INDEPENDENT AUDITORS REPORT 1 FINANCIAL STATEMENTS Statements of Financial Position 3 Statement of Activities 5 Statement of Functional Expenses

tax planning strategies

tax planning strategies In addition to saving income taxes for the current and future years, effective tax planning can reduce eventual estate taxes, maximize the amount of funds you will have available

tax planning strategies In addition to saving income taxes for the current and future years, effective tax planning can reduce eventual estate taxes, maximize the amount of funds you will have available

Voluntary Provision of a Public Good

Classroom Games Voluntary Provision of a Public Good Charles A. Holt and Susan K. Laury * Abstract: This paper describes a simple public goods game, implemented with playing cards in a classroom setup.

Classroom Games Voluntary Provision of a Public Good Charles A. Holt and Susan K. Laury * Abstract: This paper describes a simple public goods game, implemented with playing cards in a classroom setup.

Prospectus. The Demographics Of American Charitable Donors

Prospectus The Demographics Of American Charitable Donors Results Of 35,619 In-Person Interviews Households: Those Who Give; Those Who Don t Correlations: Donation Amounts Based On Financial & Non-Financial

Prospectus The Demographics Of American Charitable Donors Results Of 35,619 In-Person Interviews Households: Those Who Give; Those Who Don t Correlations: Donation Amounts Based On Financial & Non-Financial