Washington, DC. A World-Class City for Captive Insurance

|

|

|

- Alfred Simpson

- 10 years ago

- Views:

Transcription

1 Washington, DC A World-Class City for Captive Insurance

2

3 Washington, DC A World-Class City for Captive Insurance The Risk Finance Bureau regulates captive insurance companies, risk retention groups and other kinds of non-traditional risk transfer mechanisms that are licensed by the Department of Insurance, Securities and Banking (DISB). DISB licenses qualified institutions, performs financial analyses and conducts regular financial examinations to ensure financial solvency. DISB provides practical and innovative regulatory responses in a timely manner to captive insurance companies seeking to establish operations or transact business in the District.

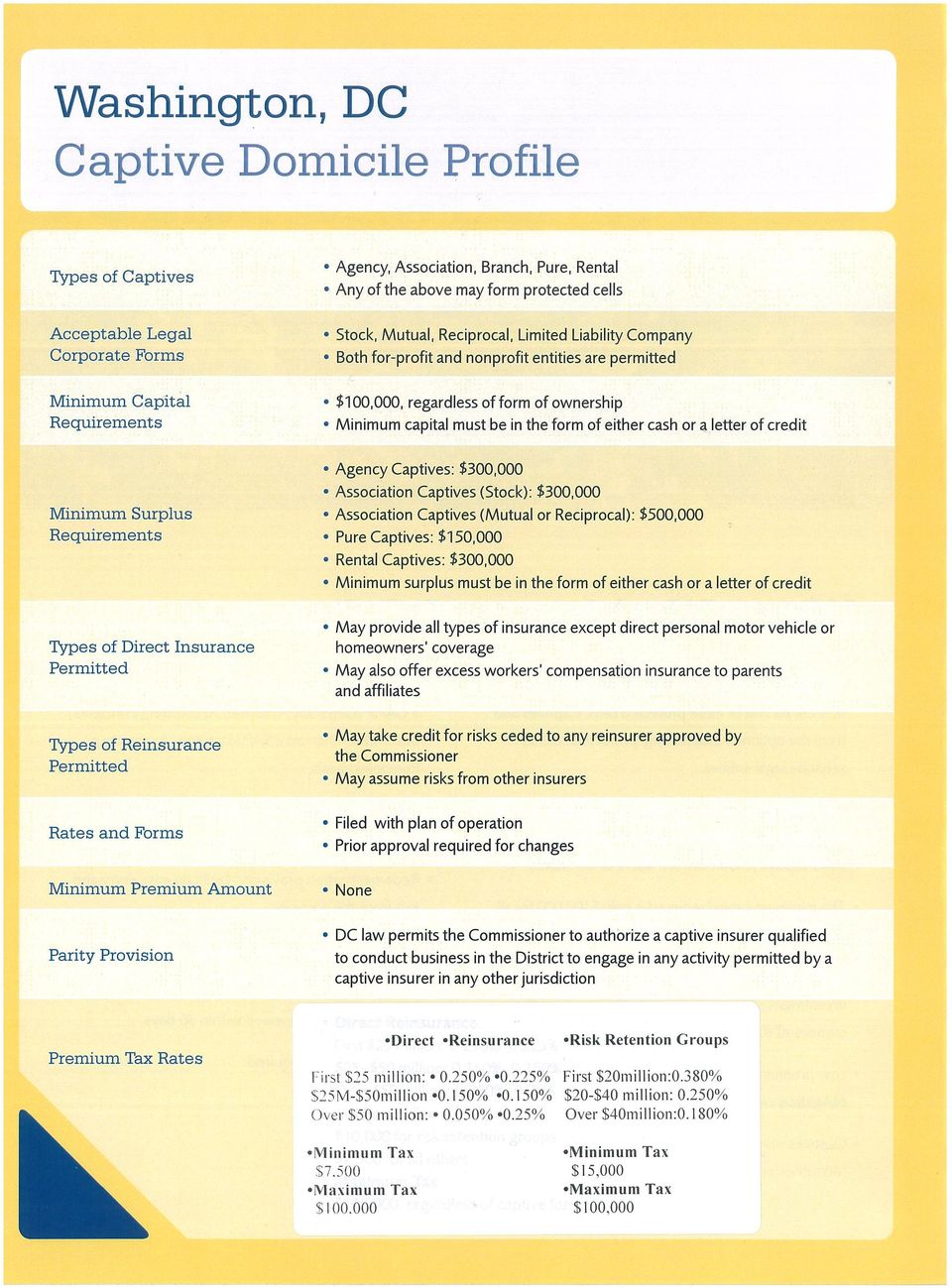

4 Washington, DC Captive Domicile Offers: 1: A modern, progressive captive insurance law that meets the demands of the marketplace and stays current with market trends. 2: Lawmakers who understand the intricacies of balancing sound regulation with the changing nature of the captive insurance market. 3: Experienced and dedicated staff committed to working with risk managers and business owners to provide creative solutions to your risk financing needs. 4: An efficient regulatory process that makes Washington, DC a flexible and innovative captive domicile. 5: The Captive Insurance Council of the District of Columbia (DC s captive insurance trade association), which holds quarterly meetings and an annual conference for captive businesses. 6: Several legal, accounting, actuarial, captive management and investment professionals with extensive expertise establishing and managing captive insurance businesses. 7: A revitalized capital city experiencing an unprecedented economic and cultural renaissance, making it one of the most attractive business destinations. 8: A well-developed transportation infrastructure, making travel to Washington, DC inexpensive and convenient. 9: A prestigious location that reflects influence, connection, reputation and good judgment. 10: A fast-growing domicile that ranks among the leading domiciles in the nation. Call or visit DISB s Web site at

5 Why a Washington, DC Captive? Any type of captive, including risk retention groups, may create one or more protected cells. Captives also have the option of establishing protected cells as separate legal entities. Parity provision will permit a captive to engage in any type of business in Washington that is permitted in any other captive jurisdiction (on-shore or off-shore). The minimum capital required is only $100,000 for all types of captives. Captives have the flexibility of following an investment strategy that meets the needs of the owners of the captive. Premium tax rates have been lowered, and the maximum tax obligation is capped at $100,000. Captives are permitted to file financial statements on a GAAP (Generally Accepted Accounting Principles) basis rather than on a SAP (Statutory Accounting Principles) basis. Captives undergo a financial examination once every five years. Redomestication provisions facilitate easy entry and exit from the domicile. Captive managers are not required to have an office in Washington until they reach critical mass. Applications are reviewed within 30 days. No local director required. Captives may take credit for risks ceded to unauthorized reinsurers.

6

7 Investment Limitations Financial Reporting Requirements Application Process/Fees Other Requirements DC Department of Insurance, Securities and Banking ART Staff A captive may invest its assets in any investment approved by Commissioner Non-risk retention groups must file annual unaudited financials on DC form on GAAP basis Risk retention groups must file annual and quarterly unaudited financials on National Association of Insurance Commissioners (NAIC) Yellow Blank on GAAP basis All captives must file annual audited financials and actuarial certification of loss reserves Application review fee: $500 (non-refundable) Issuance of certificate of authority fee: $300 Annual license renewal fee: $300 Completed applications processed within 30 days of filing Captive must retain qualified manager, attorney, accountant and actuary Captive must hold annual board of directors meeting in DC The DC DISB ART (Alternative Risk Transfer) staff consists of nine full-time employees dedicated to providing reasonable and prompt regulation for DC captives

Issuance of certificate of authority fee: $300 Annual license renewal fee: $300 Completed applications processed within 30 days of filing Captive must retain qualified")

8 Frequently Asked Questions about Captive Insurance Companies and Washington, DC 1: What is a captive? A captive insurance company is generally defined as an insurance company owned and controlled by its insureds. The captive s primary purpose is to insure the risks of its owners. It issues policies, buys reinsurance, pays claims and invests premiums similar to a traditional insurance company. 2: Why should I form a captive? There are many advantages to insuring risks through a captive insurance program as well as disadvantages in terms of risk and commitment. Some commonly cited advantages include: Tailored coverage: the captive can custom-write a policy to fit the needs of its insureds, even when such coverages are unavailable or prohibitively expensive in the commercial market; Pricing stability: stable loss experience results in stable premiums. Since the captive insures only the risks of its owners, broad market conditions that result in fluctuations to premiums may not affect your captive insurance program; Direct access to the reinsurance market: the captive can negotiate directly with the reinsurance market thereby avoiding commissions charged by commercial carriers; Greater control over claims: captive insurance, essentially self-insurance, provides financial

9 incentives to control claims costs through proactive risk management; Accumulation of investment income: the captive receives and invests premium payments until such time when those funds are needed to pay claims, operating expenses or dividends; and Increased insurance capacity: a successful captive will build surplus over time, which will enable the captive to retain more risks. 3: What types of captives can be formed in Washington, DC? Pure captives: a captive insuring only the risks of its parent and affiliated companies; Association captives: a captive that insures the risks of the member organizations of an association and the affiliated companies of those members; Branch captives: an alien (i.e., foreign) captive licensed to transact insurance in the District through a business unit with a principal place of business in the District; Rental captives: a captive formed by an organizer in which the rental captive enters into contractual agreements to insure the risks of policyholders or participants. The rental captive offers some or all of the same benefits of a traditional captive without all of the costs and responsibilities associated with a traditional captive insurance program; and Protected cells: any type of captive insurer may form one or more protected cells to insure the risks of the captive s participants. Each protected cell is capitalized separately, and the assets and liabilities in the protected cells are legally separate from the assets and liabilities in the captive insurer and the other protected cells. Agency captives: a captive that is owned by an insurance agency or brokerage and that only insures risks of policies that are placed by or through the agency or brokerage;

10 Where can I find more information on captive insurance? A variety of good information on captives is available on the Web, including: : What types of insurance can captives write? Captives are generally restricted to writing only commercial lines of coverage, such as commercial property, auto liability, general liability, professional liability and employers liability. Many captives also insure workers compensation; however, this line must generally be written through a commercially licensed insurer and reinsured by the captive. 5: What is a risk retention group (RRG)? A risk retention group is a captive insurance company operating under the federal Liability Risk Retention Act, and organized for the primary purpose of insuring liability risk exposures of its group members. Members of the RRG must be engaged in similar business activities (e.g., doctors seeking medical malpractice insurance). 6: What is a feasibility study? The feasibility study, generally prepared by a consulting actuary, is documentation of how the captive program will operate and is a required element of the captive application. The study is often the pivotal piece of information used to decide whether or not to proceed with the formation of the captive. The study may include both a written summary of the business plan and five years worth of projected financial results. Those interested in forming a captive will need to accumulate three to five years worth of past premium and claims data, as well as prospective information related to the insurance risks the captive is anticipated to write. The cost of the feasibility studies varies with the complexity of the captive program. 7: What involvement will I have in operating the captive? Many of the day-to-day operations of the captive, including accounting, regulatory compliance and routine claims handling, are typically handled by contracted service providers, including an approved captive manager. However, the ultimate responsibility for management rests with the captive s board of directors. Management must provide direction, coordinate the work of contracted services providers, ensure that loss control programs are executed and attend board meetings, among other responsibilities. Appropriate management participation is critical to achieving success in a captive program.

11 8: What is a captive manager? A captive manager is a contracted service provider that specializes in running the day-to-day operations of captive insurers. The captive manager will often perform the accounting function, interface with the Risk Finance Bureau on regulatory issues and provide general consulting assistance. A captive manager can also be helpful in steering management through the captive formation process. Contact DISB for a list of approved captive managers. 9: What services do actuaries perform? An actuary experienced in captive programs can assist in the formation of a captive by preparing a feasibility study, determining the appropriate premium to charge and recommending appropriate reinsurance coverage. The captive must also engage an actuary to perform an annual estimate of the captive s liability for future claims (i.e., reserves). 10: What is a fronting company? or a substantial part of the risk to another carrier, such as a captive. 11: Will my captive have to use a fronting company to issue insurance policies? Possibly. Certain types of coverage require evidence of insurance from admitted insurers. In addition, some insureds may be required to show evidence of insurance from a highly rated carrier. 12: What types of investments are captives allowed to use? As part of its business plan filed with DISB, the captive will document its investment plan, including the proposed types of invested assets to be acquired and held by the captive. DISB will review the proposed investment strategy and may approve the plan as submitted or require revisions. Typically, newly formed captives invest in bank instruments (e.g., money market funds and certificates of deposit) and highly rated marketable securities, including mutual funds. A fronting company is a commercially licensed insurance carrier that issues a policy and reinsures all

12 13: Does the captive get to keep its investment income? Yes. The captive retains all of the income earned on its investments and can use that revenue for any purpose. The captive retains the risk of default and depreciation on its investments as well. 14: Does a captive pay income taxes? Yes and no. A captive insurance company is required to file a federal income tax return but generally is not subject to state income taxes. The federal rules for taxing captive insurance programs are complex, and professional advice is often important for making appropriate tax elections. 15: Can a state guaranty fund assess captives who write business in their state? No. Captives are exempt from state guaranty fund assessments. 16: What information is required to accompany the captive application? The application must include the following: A completed signed application A business plan summary An actuarial feasibility study Articles, by-laws, participation or shareholders agreements Captive manager and other service provider agreements A description of the risk management program A description of the underwriting and claims administration process Five-year financial proformas showing expected and adverse scenarios Biographical affidavits for all officers, directors and key service providers A non-refundable application fee ($500) and certificate of authority fee ($300)

13 Who should I contact at DISB to talk about forming a captive? Your first call should be directly to the Risk Finance Bureau of the Department of Insurance, Securities and Banking at to set up an initial meeting to discuss your captive program. 17: What are the common sources of formation capital? Capital, either in the form of cash or an approved letter of credit, is often funded by the owner(s), but may also be obtained through assessments on the individual insureds. 18: Can I use a letter of credit to capitalize the captive? Yes. The District s Captive Law allows for a letter of credit as evidence of the formation capital. A letter of credit can satisfy both the minimum capital and surplus requirements. 19: What fees are involved in setting up a captive in the District of Columbia? A non-refundable fee of $500 is required with the application and a licensing fee of $300 will be assessed upon approval of the application. DISB will charge the applicant an additional fee (currently $3,200) if it deems it necessary to send the feasibility study to an independent actuary for review. The costs of professional services to complete the application, feasibility study and incorporate the entity can vary significantly based on the type of captive, the nature of the risks and the complexity of the program. In our experience, we have seen organizational costs range from $50,000 to $150, : What is underwriting? Underwriting is the process of selecting and rating (i.e., pricing) the risks to insure. 21: What is reinsurance? Insuring the insurer. A form of insurance whereby one insurer agrees to indemnify another insurer for losses resulting from retained risks. Reinsurance is very common in captive programs and can take a variety of forms including: Quota share reinsurance: the captive and the reinsurer agree to split premiums and losses proportionally (e.g., 50/50 split); and Excess of loss: the reinsurer agrees to reimburse the captive for claims costs over a specified amount (e.g., individual claims over $100,000). 22: What is the difference between gross written premium and net written premium? Gross written premium represents the consideration charged to the insured. When the captive shares risk with a reinsurer, part of the gross premium is paid to the reinsurer. The remaining premium (i.e., gross less reinsurance premium) represents the net written premium.

14 What are the minimum capital and surplus requirements in Washington, DC? The statutory minimum capital and surplus requirements are listed below. Additional capital may be required based on the volume and type of risk to be retained. An actuary or captive manager will be helpful in determining an appropriate level of capital to maintain. Captive Form Paid-In-Capital Surplus Total Pure captive $100,000 $150,000 $250,000 Association captive stock $100,000 $300,000 $400,000 Association captive mutual N/A $500,000 $500,000 Agency or rental captive $100,000 $300,000 $400,000 Protected cells Amount of capital and surplus to be determined by the Commissioner 23: How should I decide what reinsurance programs are appropriate for my captive? It is very important to consult someone experienced in forming captive programs to select an appropriate reinsurance program for your captive. Actuaries and captive managers may be valuable resources in designing the reinsurance program and contracting with reinsurers. 25: How does a captive settle claims? Claims against captive insurance policies are settled essentially in the same manner as commercial policies. Often, captive programs are structured so that the fronting carrier settles the claims. In other cases, the captive may settle claims directly or through use of service providers (i.e., insurance adjustment firms and attorneys). 24: What are premium taxes? Captive domiciles each charge a tax on the amount of premium written by the captive. The District s tax rates can be found at

15 FAQ s prepared by: James A. Murphy, CPA Partner, Johnson Lambert & Co. Courtesy of The Captive Insurance Council of the District of Columbia, Inc.

16 810 First Street NE, Suite 701, Washington, DC p f

16 LC 37 2118ER A BILL TO BE ENTITLED AN ACT BE IT ENACTED BY THE GENERAL ASSEMBLY OF GEORGIA:

Senate Bill 347 By: Senator Bethel of the 54th A BILL TO BE ENTITLED AN ACT 1 2 3 4 5 6 To amend Title 33 of the Official Code of Georgia Annotated, relating to insurance, so as to provide for extensive

Senate Bill 347 By: Senator Bethel of the 54th A BILL TO BE ENTITLED AN ACT 1 2 3 4 5 6 To amend Title 33 of the Official Code of Georgia Annotated, relating to insurance, so as to provide for extensive

FORC QUARTERLY JOURNAL OF INSURANCE LAW AND REGULATION

FORC QUARTERLY JOURNAL OF INSURANCE LAW AND REGULATION Summer 1998 June 20, 1998 Vol. X, Edition II CAPTIVE INSURANCE COMPANIES AND WORKERS COMPENSATION GROUP FUNDS IN THE SOUTHEAST: A COMPARATIVE VIEW

FORC QUARTERLY JOURNAL OF INSURANCE LAW AND REGULATION Summer 1998 June 20, 1998 Vol. X, Edition II CAPTIVE INSURANCE COMPANIES AND WORKERS COMPENSATION GROUP FUNDS IN THE SOUTHEAST: A COMPARATIVE VIEW

ACTION ITEM AMENDMENT TO FORMATION OF A CAPTIVE INSURANCE COMPANY EXECUTIVE SUMMARY

F7 Office of the President TO MEMBERS OF THE COMMITTEE ON FINANCE: For Meeting of November 20, 2015 ACTION ITEM AMENDMENT TO FORMATION OF A CAPTIVE INSURANCE COMPANY EXECUTIVE SUMMARY In May 2012, the

F7 Office of the President TO MEMBERS OF THE COMMITTEE ON FINANCE: For Meeting of November 20, 2015 ACTION ITEM AMENDMENT TO FORMATION OF A CAPTIVE INSURANCE COMPANY EXECUTIVE SUMMARY In May 2012, the

Intermodal Insurance Company, Inc., A Risk Retention Group GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON EXAMINATION Intermodal Insurance Company, Inc., A Risk Retention Group AS OF DECEMBER 31, 2007 NAIC NUMBER

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON EXAMINATION Intermodal Insurance Company, Inc., A Risk Retention Group AS OF DECEMBER 31, 2007 NAIC NUMBER

Captive insurance: An overview of the market today

Once considered to be a cutting edge risk management tool, captive insurance has now found its way into the mainstream of corporate risk planning. Captive insurance companies (generally defined as wholly

Once considered to be a cutting edge risk management tool, captive insurance has now found its way into the mainstream of corporate risk planning. Captive insurance companies (generally defined as wholly

CONTACT: Ted Cooke Debbie Jo Maust (623) 869-2167 (623) 869-2160. Report and Discussion Regarding Captive Domicile Review

869-2167 (623) 869-2160. Report and Discussion Regarding Captive Domicile Review") FAP Agenda Number 5. CONTACT: Ted Cooke Debbie Jo Maust (623) 869-2167 (623) 869-2160 [email protected] [email protected] MEETING DATE: September 18, 2014 AGENDA ITEM: Report and Discussion Regarding Captive

FAP Agenda Number 5. CONTACT: Ted Cooke Debbie Jo Maust (623) 869-2167 (623) 869-2160 [email protected] [email protected] MEETING DATE: September 18, 2014 AGENDA ITEM: Report and Discussion Regarding Captive

Filings: An original hardcopy CARF and other required documents must be filed along with an electronic copy of the completed CARF.

NORTH CAROLINA DEPARTMENT OF INSURANCE Form C-200 Captive Annual Report Form Instructions (All captive insurers except association captive insurers and risk retention groups) A. GENERAL INSTRUCTIONS This

NORTH CAROLINA DEPARTMENT OF INSURANCE Form C-200 Captive Annual Report Form Instructions (All captive insurers except association captive insurers and risk retention groups) A. GENERAL INSTRUCTIONS This

The Rent-A-Captive Alternative

The Rent-A-Captive Alternative This brochure is made available for informational purposes only in support of the insurance relationship between FM Global and its clients. This information does not change

The Rent-A-Captive Alternative This brochure is made available for informational purposes only in support of the insurance relationship between FM Global and its clients. This information does not change

MEDSTAR LIABILITY LIMITED INSURANCE COMPANY, INC., A RISK RETENTION GROUP GOVERNMENT OF THE DISTRICT OF COLUMBIA

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON EXAMINATION MEDSTAR LIABILITY LIMITED INSURANCE COMPANY, INC., A RISK RETENTION GROUP AS OF DECEMBER 31,

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON EXAMINATION MEDSTAR LIABILITY LIMITED INSURANCE COMPANY, INC., A RISK RETENTION GROUP AS OF DECEMBER 31,

Below is a general overview of Captives with particular information regarding Labuan International and Business Financial Centre (Labuan IBFC).

.") LABUAN CAPTIVES Below is a general overview of Captives with particular information regarding Labuan International and Business Financial Centre (Labuan IBFC). Kensington Trust Labuan Limited is a licensed

LABUAN CAPTIVES Below is a general overview of Captives with particular information regarding Labuan International and Business Financial Centre (Labuan IBFC). Kensington Trust Labuan Limited is a licensed

HEALTH CARE INDUSTRY LIABILITY RECIPROCAL INSURANCE COMPANY, A RISK RETENTION GROUP GOVERNMENT OF THE DISTRICT OF COLUMBIA

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON EXAMINATION HEALTH CARE INDUSTRY LIABILITY RECIPROCAL INSURANCE COMPANY, A RISK RETENTION GROUP AS OF DECEMBER

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON EXAMINATION HEALTH CARE INDUSTRY LIABILITY RECIPROCAL INSURANCE COMPANY, A RISK RETENTION GROUP AS OF DECEMBER

H.198. An act relating to the Legacy Insurance Management Act. It is hereby enacted by the General Assembly of the State of Vermont:

2013 Page 1 of 24 H.198 An act relating to the Legacy Insurance Management Act It is hereby enacted by the General Assembly of the State of Vermont: Sec. 1. TITLE This act shall be known as the Legacy

2013 Page 1 of 24 H.198 An act relating to the Legacy Insurance Management Act It is hereby enacted by the General Assembly of the State of Vermont: Sec. 1. TITLE This act shall be known as the Legacy

RISK WELL REWARDED CAPTIVE INSURANCE AND ALTERNATIVE RISK SOLUTIONS FOR THE MIDDLE MARKET ARTEX RISK SOLUTIONS, INC

SM RISK WELL REWARDED CAPTIVE INSURANCE AND ALTERNATIVE RISK SOLUTIONS FOR THE MIDDLE MARKET ARTEX RISK SOLUTIONS, INC For many years large corporations have used alternative risk transfer strategies to

SM RISK WELL REWARDED CAPTIVE INSURANCE AND ALTERNATIVE RISK SOLUTIONS FOR THE MIDDLE MARKET ARTEX RISK SOLUTIONS, INC For many years large corporations have used alternative risk transfer strategies to

Fairway Physicians Insurance Company, A Risk Retention Group GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON EXAMINATION Fairway Physicians Insurance Company, A Risk Retention Group AS OF DECEMBER 31, 2007 NAIC NUMBER

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON EXAMINATION Fairway Physicians Insurance Company, A Risk Retention Group AS OF DECEMBER 31, 2007 NAIC NUMBER

New Home Warranty Insurance Company, A Risk Retention Group

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON EXAMINATION New Home Warranty Insurance Company, A Risk Retention Group AS OF DECEMBER 31, 2014 NAIC NUMBER

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON EXAMINATION New Home Warranty Insurance Company, A Risk Retention Group AS OF DECEMBER 31, 2014 NAIC NUMBER

REPORT ON EXAMINATION OF THE DELAWARE PROFESSIONAL INSURANCE COMPANY, RISK RETENTION GROUP AS OF DECEMBER 31, 2010

REPORT ON EXAMINATION OF THE DELAWARE PROFESSIONAL INSURANCE COMPANY, RISK RETENTION GROUP AS OF DECEMBER 31, 2010 Table of Contents SALUTATION... 1 SCOPE OF EXAMINATION... 2 SUMMARY OF SIGNIFICNAT FINDINGS...

REPORT ON EXAMINATION OF THE DELAWARE PROFESSIONAL INSURANCE COMPANY, RISK RETENTION GROUP AS OF DECEMBER 31, 2010 Table of Contents SALUTATION... 1 SCOPE OF EXAMINATION... 2 SUMMARY OF SIGNIFICNAT FINDINGS...

All insured's must be owners and likewise all owners must be insured's. Under the LRRA, the membership of the RRG must be relatively homogeneous

What is a Risk Retention Group? A risk retention group (RRG) is a policy issuing liability insurance company that is owned by its member insured's and formed under the Liability Risk Retention Act of 1981,

What is a Risk Retention Group? A risk retention group (RRG) is a policy issuing liability insurance company that is owned by its member insured's and formed under the Liability Risk Retention Act of 1981,

GLOSSARY OF SELECTED INSURANCE AND RELATED FINANCIAL TERMS

In an effort to help our investors and other interested parties better understand our regular SEC reports and other disclosures, we are providing a Glossary of Selected Insurance Terms. Most of the definitions

In an effort to help our investors and other interested parties better understand our regular SEC reports and other disclosures, we are providing a Glossary of Selected Insurance Terms. Most of the definitions

Medical Providers Mutual Insurance Company, A Risk Retention Group

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON EXAMINATION Medical Providers Mutual Insurance Company, A Risk Retention Group AS OF DECEMBER 31, 2011 NAIC

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON EXAMINATION Medical Providers Mutual Insurance Company, A Risk Retention Group AS OF DECEMBER 31, 2011 NAIC

ORGANIZATIONAL EXAMINATION KNIGHT SPECIALTY INSURANCE COMPANY AS OF OCTOBER 18, 2013

ORGANIZATIONAL EXAMINATION OF KNIGHT SPECIALTY INSURANCE COMPANY AS OF OCTOBER 18, 2013 TABLE OF CONTENTS SALUTATION 1 SCOPE OF EXAMINATION 2 HISTORY 2 MANAGEMENT AND CONTROL 2 FIDELITY BOND COVERAGE

ORGANIZATIONAL EXAMINATION OF KNIGHT SPECIALTY INSURANCE COMPANY AS OF OCTOBER 18, 2013 TABLE OF CONTENTS SALUTATION 1 SCOPE OF EXAMINATION 2 HISTORY 2 MANAGEMENT AND CONTROL 2 FIDELITY BOND COVERAGE

January 21, 2015 Memorandum 2015 1C. A. File all documents directly with the Insurance Division, Captive Insurance Branch.

DAVID Y. IGE GOVERNOR SHAN S. TSUTSUI LT. GOVERNOR STATE OF HAW AI`I INSURANCE DIVISION DEPARTMENT OF COMMERCE & CONSUMER AFFAIRS P. O. BOX 3614 HONOLULU, HAWAI`I 968113614 335 MERCHANT STREET, ROOM 13

DAVID Y. IGE GOVERNOR SHAN S. TSUTSUI LT. GOVERNOR STATE OF HAW AI`I INSURANCE DIVISION DEPARTMENT OF COMMERCE & CONSUMER AFFAIRS P. O. BOX 3614 HONOLULU, HAWAI`I 968113614 335 MERCHANT STREET, ROOM 13

Robert H. Katz, Esq. 614.227.2397

OHIO S TAX REFORM OF THE NON-ADMITTED INSURANCE MARKET. Robert H. Katz, Esq. 614.227.2397 As part of a significant and major overhaul of its business taxes, Ohio after a contentious legislative process

OHIO S TAX REFORM OF THE NON-ADMITTED INSURANCE MARKET. Robert H. Katz, Esq. 614.227.2397 As part of a significant and major overhaul of its business taxes, Ohio after a contentious legislative process

A BILL FOR AN ACT ENTITLED: "AN ACT GENERALLY REVISING CAPTIVE INSURANCE LAWS; PROVIDING

SB00.0 SENATE BILL NO. INTRODUCED BY J. COHENOUR BY REQUEST OF THE STATE AUDITOR 0 A BILL FOR AN ACT ENTITLED: "AN ACT GENERALLY REVISING CAPTIVE INSURANCE LAWS; PROVIDING A PENALTY FOR FAILURE TO FILE

SB00.0 SENATE BILL NO. INTRODUCED BY J. COHENOUR BY REQUEST OF THE STATE AUDITOR 0 A BILL FOR AN ACT ENTITLED: "AN ACT GENERALLY REVISING CAPTIVE INSURANCE LAWS; PROVIDING A PENALTY FOR FAILURE TO FILE

PROBUILDERS SPECIALTY INSURANCE COMPANY, RRG One Denver Highlands 10375 East Harvard Avenue, Suite 550 Denver, CO 80231 INFORMATION STATEMENT

PROBUILDERS SPECIALTY INSURANCE COMPANY, RRG One Denver Highlands 10375 East Harvard Avenue, Suite 550 Denver, CO 80231 INFORMATION STATEMENT This Information Statement is furnished in connection with

PROBUILDERS SPECIALTY INSURANCE COMPANY, RRG One Denver Highlands 10375 East Harvard Avenue, Suite 550 Denver, CO 80231 INFORMATION STATEMENT This Information Statement is furnished in connection with

Insurance Functions AGENCY LAW INSURANCE OCCUPATIONS. Chapter 5 Page 1

Insurance Functions Chapter 8 1 AGENCY LAW An agent is a person authorized to act on behalf of another person who is the principal Duties of the agent: Loyalty Not to be negligent To obey instructions

Insurance Functions Chapter 8 1 AGENCY LAW An agent is a person authorized to act on behalf of another person who is the principal Duties of the agent: Loyalty Not to be negligent To obey instructions

LABOR AND WORKERS COMPENSATION GROUP SELF-INSURANCE

TITLE 11 CHAPTER 4 PART 9 LABOR AND WORKERS COMPENSATION WORKERS COMPENSATION GROUP SELF-INSURANCE 11.4.9.1 ISSUING AGENCY: Workers Compensation Administration. [8/1/96; 11.4.9.1 NMAC - Rn, 11 NMAC 4.9.1,

TITLE 11 CHAPTER 4 PART 9 LABOR AND WORKERS COMPENSATION WORKERS COMPENSATION GROUP SELF-INSURANCE 11.4.9.1 ISSUING AGENCY: Workers Compensation Administration. [8/1/96; 11.4.9.1 NMAC - Rn, 11 NMAC 4.9.1,

Understanding Captives and Alternative Risk Transfer

Understanding Captives and Alternative Risk Transfer Putting your insurance premiums to work for you Managing risk as you manage your bottom line What do Verizon, Coca-Cola, BP and most Fortune 500 sized

Understanding Captives and Alternative Risk Transfer Putting your insurance premiums to work for you Managing risk as you manage your bottom line What do Verizon, Coca-Cola, BP and most Fortune 500 sized

REPORT ON EXAMINATION OF THE MAKE TRANSPORTATION INSURANCE, INC., A RISK RETENTION GROUP AS OF

REPORT ON EXAMINATION OF THE MAKE TRANSPORTATION INSURANCE, INC., A RISK RETENTION GROUP AS OF DECEMBER 31, 2011 TABLE OF CONTENTS SALUTATION... 1 SCOPE OF EXAMINATION... 1 SUMMARY OF SIGNIFICANT FINDINGS...

REPORT ON EXAMINATION OF THE MAKE TRANSPORTATION INSURANCE, INC., A RISK RETENTION GROUP AS OF DECEMBER 31, 2011 TABLE OF CONTENTS SALUTATION... 1 SCOPE OF EXAMINATION... 1 SUMMARY OF SIGNIFICANT FINDINGS...

Schedule A TERRORISM RISK INSURANCE PROGRAM

Control Number (Treasury use) Schedule A TERRORISM RISK INSURANCE PROGRAM DECLARATION OF DIRECT EARNED PREMIUM AND CALCULATION OF INSURER DEDUCTIBLE UNDER TERRORISM RISK INSURANCE ACT (TRIA) Insurer or

Control Number (Treasury use) Schedule A TERRORISM RISK INSURANCE PROGRAM DECLARATION OF DIRECT EARNED PREMIUM AND CALCULATION OF INSURER DEDUCTIBLE UNDER TERRORISM RISK INSURANCE ACT (TRIA) Insurer or

KENTUCKY EMPLOYERS' MUTUAL INSURANCE AUTHORITY dba KENTUCKY EMPLOYERS' MUTUAL INSURANCE

KENTUCKY EMPLOYERS' MUTUAL INSURANCE AUTHORITY dba KENTUCKY EMPLOYERS' MUTUAL INSURANCE Statutory Basis Financial Statements and Supplementary Information Years Ended December 31, 2010 and 2009 with Independent

KENTUCKY EMPLOYERS' MUTUAL INSURANCE AUTHORITY dba KENTUCKY EMPLOYERS' MUTUAL INSURANCE Statutory Basis Financial Statements and Supplementary Information Years Ended December 31, 2010 and 2009 with Independent

Fairway Physicians Insurance Company, A Risk Retention Group

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON EXAMINATION Fairway Physicians Insurance Company, A Risk Retention Group AS OF DECEMBER 31, 2012 NAIC NUMBER

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON EXAMINATION Fairway Physicians Insurance Company, A Risk Retention Group AS OF DECEMBER 31, 2012 NAIC NUMBER

Revenue Ruling 2002-89 states that a Captive that receives 50% of its premiums from unrelated entities will achieve adequate risk distribution.

Captive Insurance: Frequently Asked Questions 1. Q: How is the Captive formed to ensure it is a true insurance arrangement? A: In order to have legitimate Insurance, there must be adequate risk transfer

Captive Insurance: Frequently Asked Questions 1. Q: How is the Captive formed to ensure it is a true insurance arrangement? A: In order to have legitimate Insurance, there must be adequate risk transfer

Captive Insurance Company

Captive Insurance Company Captive Insurance Companies (referred to as Captives) and also known as Closely Held Insurance Companies (CHIC), have become a commonplace form of alternative risk transfer and

Captive Insurance Company Captive Insurance Companies (referred to as Captives) and also known as Closely Held Insurance Companies (CHIC), have become a commonplace form of alternative risk transfer and

Group Captive Insurance Programs for Property and Casualty Coverages

Group Captive Insurance Programs for Property and Casualty Coverages Duke Niedringhaus, ARM Vice President J.W. Terrill, Inc. April 2013 Group captive insurance programs can be an attractive alternative

Group Captive Insurance Programs for Property and Casualty Coverages Duke Niedringhaus, ARM Vice President J.W. Terrill, Inc. April 2013 Group captive insurance programs can be an attractive alternative

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON ORGANIZATIONAL EXAMINATION

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON ORGANIZATIONAL EXAMINATION GUARDIAN PROPERTY & CASUALTY COMPANY INC. AS OF JUNE 30, 2007 TABLE OF CONTENTS

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON ORGANIZATIONAL EXAMINATION GUARDIAN PROPERTY & CASUALTY COMPANY INC. AS OF JUNE 30, 2007 TABLE OF CONTENTS

Management Alta s team of professionals set us apart. Our associates are CPAs, attorneys, business, and insurance professionals with the most

Management Alta s team of professionals set us apart. Our associates are CPAs, attorneys, business, and insurance professionals with the most extensive, sophisticated experience in the Captive industry.

Management Alta s team of professionals set us apart. Our associates are CPAs, attorneys, business, and insurance professionals with the most extensive, sophisticated experience in the Captive industry.

COMPANION PROPERTY & CASUALTY INSURANCE COMPANY

REPORT ON LIMITED SCOPE EXAMINATION OF COMPANION PROPERTY & CASUALTY INSURANCE COMPANY COLUMBIA, SOUTH CAROLINA OF THE Loss and Loss Expenses, Large Deductible Collateral Reserves and Reinsurance As of

REPORT ON LIMITED SCOPE EXAMINATION OF COMPANION PROPERTY & CASUALTY INSURANCE COMPANY COLUMBIA, SOUTH CAROLINA OF THE Loss and Loss Expenses, Large Deductible Collateral Reserves and Reinsurance As of

State of Idaho DEPARTMENT OF INSURANCE BULLETIN NO. 11-08

C.L. BUTCH OTTER Governor State of Idaho DEPARTMENT OF INSURANCE 700 West State Street, 3rd Floor P.O. Box 83720 Boise, Idaho 83720-0043 Phone (208) 334-4250 FAX (208) 334-4398 http://www.doi.idaho.gov

C.L. BUTCH OTTER Governor State of Idaho DEPARTMENT OF INSURANCE 700 West State Street, 3rd Floor P.O. Box 83720 Boise, Idaho 83720-0043 Phone (208) 334-4250 FAX (208) 334-4398 http://www.doi.idaho.gov

Captive Insurance Companies Risk Financing For Self-Insurance and. Underinsured Risks

Captive Insurance Companies Risk Financing For Self-Insurance and Underinsured Risks Mark Koogler, Partner April 8, 2015 History of Captives Captive Industry Update Retaining Risk vs. Financing Risk A

Captive Insurance Companies Risk Financing For Self-Insurance and Underinsured Risks Mark Koogler, Partner April 8, 2015 History of Captives Captive Industry Update Retaining Risk vs. Financing Risk A

HEALTH MAINTENANCE ORGANIZATION ( HMO ) APPLICATION FOR A NEW CERTIFICATE OF AUTHORITY MEDICARE ONLY INTRODUCTION

APPLICATION FOR A NEW CERTIFICATE OF AUTHORITY MEDICARE ONLY INTRODUCTION") NEW JERSEY DEPARTMENT OF BANKING AND INSURANCE OFFICE OF LIFE AND HEALTH VALUATION BUREAU POST OFFICE BOX 325 20 WEST STATE STREET TRENTON, NEW JERSEY 08625 HEALTH MAINTENANCE ORGANIZATION ( HMO ) APPLICATION

NEW JERSEY DEPARTMENT OF BANKING AND INSURANCE OFFICE OF LIFE AND HEALTH VALUATION BUREAU POST OFFICE BOX 325 20 WEST STATE STREET TRENTON, NEW JERSEY 08625 HEALTH MAINTENANCE ORGANIZATION ( HMO ) APPLICATION

GUIDE TO ESTABLISHING INSURANCE COMPANIES IN GUERNSEY

GUIDE TO ESTABLISHING INSURANCE COMPANIES IN GUERNSEY CONTENTS PREFACE 1 1. Introduction 2 2. Authorisation 2 3. Minimum Criteria for Licensing 2 4. Requirements for Licensing under the Insurance Law 3

GUIDE TO ESTABLISHING INSURANCE COMPANIES IN GUERNSEY CONTENTS PREFACE 1 1. Introduction 2 2. Authorisation 2 3. Minimum Criteria for Licensing 2 4. Requirements for Licensing under the Insurance Law 3

Title 24-A: MAINE INSURANCE CODE

Title 24-A: MAINE INSURANCE CODE Chapter 72-A: MAINE LIABILITY RISK RETENTION ACT HEADING: PL 1987, c. 769, Pt. A, 100 (rpr) Table of Contents Section 6091. SHORT TITLE... 3 Section 6092. PURPOSE... 3

Title 24-A: MAINE INSURANCE CODE Chapter 72-A: MAINE LIABILITY RISK RETENTION ACT HEADING: PL 1987, c. 769, Pt. A, 100 (rpr) Table of Contents Section 6091. SHORT TITLE... 3 Section 6092. PURPOSE... 3

Minnesota Workers' Compensation Assigned Risk Plan. Financial Statements Together with Independent Auditors' Report

Minnesota Workers' Compensation Assigned Risk Plan Financial Statements Together with Independent Auditors' Report December 31, 2012 CONTENTS Page INDEPENDENT AUDITORS' REPORT 1 FINANCIAL STATEMENTS: Balance

Minnesota Workers' Compensation Assigned Risk Plan Financial Statements Together with Independent Auditors' Report December 31, 2012 CONTENTS Page INDEPENDENT AUDITORS' REPORT 1 FINANCIAL STATEMENTS: Balance

Self-Insurance and Captives

Self-Insurance and Captives Basic Concepts Patricia J. (PJ) Kale, CPCU Peter Newman, Jr., PhD 1 Common Goal We are in the same business the risk business. Treasury Operations and Risk Management share

Self-Insurance and Captives Basic Concepts Patricia J. (PJ) Kale, CPCU Peter Newman, Jr., PhD 1 Common Goal We are in the same business the risk business. Treasury Operations and Risk Management share

REPORT ON EXAMINATION HHC INSURANCE COMPANY, INC. AS OF DECEMBER 31, 2009

REPORT ON EXAMINATION OF HHC INSURANCE COMPANY, INC. AS OF DECEMBER 31, 2009 DATE OF REPORT APRIL 6, 2011 EXAMINER BERNARD LOTT TABLE OF CONTENTS ITEM PAGE NO. 1. Scope of examination 2 2. Description

REPORT ON EXAMINATION OF HHC INSURANCE COMPANY, INC. AS OF DECEMBER 31, 2009 DATE OF REPORT APRIL 6, 2011 EXAMINER BERNARD LOTT TABLE OF CONTENTS ITEM PAGE NO. 1. Scope of examination 2 2. Description

ORGANIZATIONAL EXAMINATION GLOBAL HAWK PROPERTY AND CASUALTY INSURANCE COMPANY AS OF FEBRUARY 7, 2014

ORGANIZATIONAL EXAMINATION OF GLOBAL HAWK PROPERTY AND CASUALTY INSURANCE COMPANY AS OF FEBRUARY 7, 2014 TABLE OF CONTENTS SALUTATION 1 SCOPE OF EXAMINATION 2 HISTORY 2 MANAGEMENT AND CONTROL 2 FIDELITY

ORGANIZATIONAL EXAMINATION OF GLOBAL HAWK PROPERTY AND CASUALTY INSURANCE COMPANY AS OF FEBRUARY 7, 2014 TABLE OF CONTENTS SALUTATION 1 SCOPE OF EXAMINATION 2 HISTORY 2 MANAGEMENT AND CONTROL 2 FIDELITY

REGISTERING A CAPTIVE INSURANCE COMPANY IN BRITISH COLUMBIA. The purpose of this bulletin is to provide captive insurance applicants with:

INFORMATION BULLETIN BULLETIN NUMBER: TITLE: LEGISLATION: INS-06-002 REGISTERING A CAPTIVE INSURANCE COMPANY IN BRITISH COLUMBIA INSURANCE (CAPTIVE COMPANY) ACT, INSURANCE (CAPTIVE COMPANY) ACT REGULATION,

INFORMATION BULLETIN BULLETIN NUMBER: TITLE: LEGISLATION: INS-06-002 REGISTERING A CAPTIVE INSURANCE COMPANY IN BRITISH COLUMBIA INSURANCE (CAPTIVE COMPANY) ACT, INSURANCE (CAPTIVE COMPANY) ACT REGULATION,

PART I ARTICLE. apply to all insurers domiciled in this State unless exempt. (b) The purposes of this article shall be to:

The purposes of this article shall be to:") THE SENATE TWENTY-EIGHTH LEGISLATURE, 0 STATE OF HAWAII A BILL FOR AN ACT RELATING TO INSURANCE BE IT ENACTED BY THE LEGISLATURE OF THE STATE OF HAWAII: PART I SECTION. Chapter, Hawaii Revised Statutes,

THE SENATE TWENTY-EIGHTH LEGISLATURE, 0 STATE OF HAWAII A BILL FOR AN ACT RELATING TO INSURANCE BE IT ENACTED BY THE LEGISLATURE OF THE STATE OF HAWAII: PART I SECTION. Chapter, Hawaii Revised Statutes,

SOA 2013 Life & Annuity Symposium May 6-7, 2013. Session 31 PD, Captive Reinsurers for the Small and Medium Insurance Companies

SOA 2013 Life & Annuity Symposium May 6-7, 2013 Session 31 PD, Captive Reinsurers for the Small and Medium Insurance Companies Moderator: Graham W. G. Mackay, FSA, FCIA, MAAA Presenters: Jeffrey N. Altman,

SOA 2013 Life & Annuity Symposium May 6-7, 2013 Session 31 PD, Captive Reinsurers for the Small and Medium Insurance Companies Moderator: Graham W. G. Mackay, FSA, FCIA, MAAA Presenters: Jeffrey N. Altman,

Scaffold Industry Insurance Company Risk Retention Group, Inc. GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON EXAMINATION Scaffold Industry Insurance Company Risk Retention Group, Inc. AS OF DECEMBER 31, 2009 NAIC

GOVERNMENT OF THE DISTRICT OF COLUMBIA DEPARTMENT OF INSURANCE, SECURITIES AND BANKING REPORT ON EXAMINATION Scaffold Industry Insurance Company Risk Retention Group, Inc. AS OF DECEMBER 31, 2009 NAIC

DD&R Reserves For Claims-Made Professional Liability Coverage

DD&R Reserves For Claims-Made Professional Liability Coverage September 2011 Article By: Jessica Lasher, CPA, Senior Manager with Johnson Lambert & Co. LLP and Robert Walling, Principal and Consultant

DD&R Reserves For Claims-Made Professional Liability Coverage September 2011 Article By: Jessica Lasher, CPA, Senior Manager with Johnson Lambert & Co. LLP and Robert Walling, Principal and Consultant

Reinsurance: What? Who? Why? How?

Knowledge. Experience. Performance. THE POWER OF INSIGHT. sm Life Reinsurance Rejean Besner, FSA, MAAA, FCIA, FASSA Vice President & Chief Actuary, International Division Presented to the Conference on

Knowledge. Experience. Performance. THE POWER OF INSIGHT. sm Life Reinsurance Rejean Besner, FSA, MAAA, FCIA, FASSA Vice President & Chief Actuary, International Division Presented to the Conference on

UNIVERSITY OF FLORIDA SELF-INSURANCE PROGRAM AND HEALTHCARE EDUCATION INSURANCE COMPANY COMBINING FINANCIAL STATEMENTS JUNE 30, 2013

UNIVERSITY OF FLORIDA SELF-INSURANCE PROGRAM AND HEALTHCARE COMBINING FINANCIAL STATEMENTS UNIVERSITY OF FLORIDA SELF-INSURANCE PROGRAM AND HEALTHCARE TABLE OF CONTENTS Page(s) Independent Auditors Report

UNIVERSITY OF FLORIDA SELF-INSURANCE PROGRAM AND HEALTHCARE COMBINING FINANCIAL STATEMENTS UNIVERSITY OF FLORIDA SELF-INSURANCE PROGRAM AND HEALTHCARE TABLE OF CONTENTS Page(s) Independent Auditors Report

DISTRICT OF COLUMBIA OFFICIAL CODE

DISTRICT OF COLUMBIA OFFICIAL CODE TITLE 31. INSURANCE AND SECURITIES. CHAPTER 50B. TITLE INSURANCE PRODUCERS. 2001 Edition DISTRICT OF COLUMBIA OFFICIAL CODE CHAPTER 50B. TITLE INSURANCE PRODUCERS. TABLE

DISTRICT OF COLUMBIA OFFICIAL CODE TITLE 31. INSURANCE AND SECURITIES. CHAPTER 50B. TITLE INSURANCE PRODUCERS. 2001 Edition DISTRICT OF COLUMBIA OFFICIAL CODE CHAPTER 50B. TITLE INSURANCE PRODUCERS. TABLE

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2015 SESSION LAW 2015-99 HOUSE BILL 163

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2015 SESSION LAW 2015-99 HOUSE BILL 163 AN ACT TO MAKE VARIOUS CLARIFYING AND TECHNICAL CHANGES TO THE NORTH CAROLINA CAPTIVE INSURANCE ACT. The General Assembly

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2015 SESSION LAW 2015-99 HOUSE BILL 163 AN ACT TO MAKE VARIOUS CLARIFYING AND TECHNICAL CHANGES TO THE NORTH CAROLINA CAPTIVE INSURANCE ACT. The General Assembly

The Story of Non-admitted Insurance in California

The Surplus Line Association Of California CA The Story of Non-admitted Insurance in California The Story of Non-Admitted Insurance in California It is vital an innovative and imaginative insurance marketplace

The Surplus Line Association Of California CA The Story of Non-admitted Insurance in California The Story of Non-Admitted Insurance in California It is vital an innovative and imaginative insurance marketplace

DESCRIPTION OF THE PLAN

DESCRIPTION OF THE PLAN PURPOSE 1. What is the purpose of the Plan? The purpose of the Plan is to provide eligible record owners of common stock of the Company with a simple and convenient means of investing

DESCRIPTION OF THE PLAN PURPOSE 1. What is the purpose of the Plan? The purpose of the Plan is to provide eligible record owners of common stock of the Company with a simple and convenient means of investing

Property and Liability Insurance Accounting (Passing grade for this exam is 60)

") Supplemental Background Material NAIC Examiner Project Course AFE 4 Property and Liability Insurance Accounting (Passing grade for this exam is 60) Please note that this study guide is a tool for learning

Supplemental Background Material NAIC Examiner Project Course AFE 4 Property and Liability Insurance Accounting (Passing grade for this exam is 60) Please note that this study guide is a tool for learning

Statutory Financial Statements and Report of Independent Certified Public Accountants. Massachusetts Catholic Self-Insurance Group, Inc.

Statutory Financial Statements and Report of Independent Certified Public Accountants Massachusetts Catholic Self-Insurance Group, Inc. Contents Page Report of Independent Certified Public Accountants

Statutory Financial Statements and Report of Independent Certified Public Accountants Massachusetts Catholic Self-Insurance Group, Inc. Contents Page Report of Independent Certified Public Accountants

Captive Insurance Issues and Trends. Michael Mead, Kyle Mrotek and Doug Youngren

Captive Insurance Issues and Trends Michael Mead, Kyle Mrotek and Doug Youngren What is a Captive and What Does it Do? Michael R. Mead, CPCU, M.R. Mead Co. 1 What It Is Not 2 Definition of Captive Insurance

Captive Insurance Issues and Trends Michael Mead, Kyle Mrotek and Doug Youngren What is a Captive and What Does it Do? Michael R. Mead, CPCU, M.R. Mead Co. 1 What It Is Not 2 Definition of Captive Insurance

Captive Reinsurance. An Innovative Approach to U.S. Employee Benefits

Captive Reinsurance An Innovative Approach to U.S. Employee Benefits The Prudential Insurance Company of America 751 Broad Street, Newark, NJ 0221709-00002-00 Introduction An important corporate function

Captive Reinsurance An Innovative Approach to U.S. Employee Benefits The Prudential Insurance Company of America 751 Broad Street, Newark, NJ 0221709-00002-00 Introduction An important corporate function

R590-238-5. Risk Limitation. (1) The commissioner may limit the net amount of risk a captive insurance company retains for a single risk after

The commissioner may limit the net amount of risk a captive insurance company retains for a single risk after") R590. Insurance, Administration. R590-238. Captive Insurance Companies. (Effective 8-25-08) R590-238-1. Authority. This rule is promulgated pursuant to the general rulemaking authority granted the insurance

R590. Insurance, Administration. R590-238. Captive Insurance Companies. (Effective 8-25-08) R590-238-1. Authority. This rule is promulgated pursuant to the general rulemaking authority granted the insurance

Compensation Agreement. The Redevelopment Agency of the City of Hercules & Arthur J. Gallagher & Co. Insurance Brokers of CA, Inc.

Compensation Agreement The Redevelopment Agency of the City of Hercules & Arthur J. Gallagher & Co. Insurance Brokers of CA, Inc. AGREEMENT THIS COMPENSATION AGREEMENT is made and entered into and effective

Compensation Agreement The Redevelopment Agency of the City of Hercules & Arthur J. Gallagher & Co. Insurance Brokers of CA, Inc. AGREEMENT THIS COMPENSATION AGREEMENT is made and entered into and effective

New York Credit For Reinsurance Rule

New York Credit For Reinsurance Rule 11 NYCRR 125.4 11 N.Y. Comp. Codes R. & Regs. 125.4 OFFICIAL COMPILATION OF CODES, RULES AND REGULATIONS OF THE STATE OF NEW YORK TITLE 11. INSURANCE DEPARTMENT CHAPTER

New York Credit For Reinsurance Rule 11 NYCRR 125.4 11 N.Y. Comp. Codes R. & Regs. 125.4 OFFICIAL COMPILATION OF CODES, RULES AND REGULATIONS OF THE STATE OF NEW YORK TITLE 11. INSURANCE DEPARTMENT CHAPTER

Tennessee Department of Commerce & Insurance

Tennessee Department of Commerce & Insurance Captive Insurance Department Tennessee Captive Insurance Association December 7, 2011 TDCI s Focus Two primary objectives: 1. Monitoring the solvency and standards

Tennessee Department of Commerce & Insurance Captive Insurance Department Tennessee Captive Insurance Association December 7, 2011 TDCI s Focus Two primary objectives: 1. Monitoring the solvency and standards

Medical Malpractice Insurance Crisis

Medical Malpractice Insurance Crisis Alternative Risk Transfer Solutions JOHN J. O BRIEN, JD, CLU, CPCU Vice President and Director, Client Services Wilmington Trust SP Services (South Carolina), Inc.

Medical Malpractice Insurance Crisis Alternative Risk Transfer Solutions JOHN J. O BRIEN, JD, CLU, CPCU Vice President and Director, Client Services Wilmington Trust SP Services (South Carolina), Inc.

ST. JOHNS INSURANCE COMPANY, INC.

REPORT ON EXAMINATION OF ST. JOHNS INSURANCE COMPANY, INC. ORLANDO, FLORIDA AS OF DECEMBER 31, 2006 BY THE OFFICE OF INSURANCE REGULATION TABLE OF CONTENTS LETTER OF TRANSMITTAL...- SCOPE OF EXAMINATION...

REPORT ON EXAMINATION OF ST. JOHNS INSURANCE COMPANY, INC. ORLANDO, FLORIDA AS OF DECEMBER 31, 2006 BY THE OFFICE OF INSURANCE REGULATION TABLE OF CONTENTS LETTER OF TRANSMITTAL...- SCOPE OF EXAMINATION...

Article 21. Surplus Lines Act. 58-21-1. Short title. This Article shall be known and may be cited as the "Surplus Lines Act". (1985, c. 688, s. 1.

Article 21. Surplus Lines Act. 58-21-1. Short title. This Article shall be known and may be cited as the "Surplus Lines Act". (1985, c. 688, s. 1.) 58-21-2. Relationship to other insurance laws. Unless

Article 21. Surplus Lines Act. 58-21-1. Short title. This Article shall be known and may be cited as the "Surplus Lines Act". (1985, c. 688, s. 1.) 58-21-2. Relationship to other insurance laws. Unless

Marsh Canada Limited The Captive Concept

Marsh Canada Limited The Captive Concept A preliminary insight into the rationale behind the formation of a captive insurance company 2 The Captive Concept Marsh Canada Limited What is a Captive? A captive

Marsh Canada Limited The Captive Concept A preliminary insight into the rationale behind the formation of a captive insurance company 2 The Captive Concept Marsh Canada Limited What is a Captive? A captive

North Carolina Insurance Underwriting Association

North Carolina Insurance Underwriting Association Statutory Financial Statements and Supplemental Schedules (With Independent Auditor s Report Thereon) December 31, 2014 and 2013 Contents Independent Auditor

North Carolina Insurance Underwriting Association Statutory Financial Statements and Supplemental Schedules (With Independent Auditor s Report Thereon) December 31, 2014 and 2013 Contents Independent Auditor

PROSPECTUS. Aflac Incorporated Worldwide Headquarters 1932 Wynnton Road Columbus, Georgia 31999 1.800.227.4756-706.596.3589

PROSPECTUS Aflac Incorporated Worldwide Headquarters 1932 Wynnton Road Columbus, Georgia 31999 1.800.227.4756-706.596.3589 AFL Stock Plan A Direct Stock Purchase and Dividend Reinvestment Plan We are offering

PROSPECTUS Aflac Incorporated Worldwide Headquarters 1932 Wynnton Road Columbus, Georgia 31999 1.800.227.4756-706.596.3589 AFL Stock Plan A Direct Stock Purchase and Dividend Reinvestment Plan We are offering

News from The Chubb Corporation

News from The Chubb Corporation The Chubb Corporation 15 Mountain View Road P.O. Box 1615 Warren, New Jersey 07061-1615 Telephone: 908-903-2000 FOR IMMEDIATE RELEASE Chubb Reports Second Quarter Net Income

News from The Chubb Corporation The Chubb Corporation 15 Mountain View Road P.O. Box 1615 Warren, New Jersey 07061-1615 Telephone: 908-903-2000 FOR IMMEDIATE RELEASE Chubb Reports Second Quarter Net Income

LICENSING PROCEDURES FOR MANAGING GENERAL AGENTS TO OBTAIN AUTHORITY IN VIRGINIA

LICENSING PROCEDURES FOR MANAGING GENERAL AGENTS TO OBTAIN AUTHORITY IN VIRGINIA October 2005 GENERAL INFORMATION The 1992 Virginia General Assembly passed legislation requiring the licensing of managing

LICENSING PROCEDURES FOR MANAGING GENERAL AGENTS TO OBTAIN AUTHORITY IN VIRGINIA October 2005 GENERAL INFORMATION The 1992 Virginia General Assembly passed legislation requiring the licensing of managing

What Are the Roles and Responsibilities of a Captive Manager?

Captive Management: What Are the Roles and Responsibilities of a Captive Manager? WWW.CHICAGOLANDRISKFORUM.ORG What Is a Captive Insurance Company? A captive is A separate legal entity created or used

Captive Management: What Are the Roles and Responsibilities of a Captive Manager? WWW.CHICAGOLANDRISKFORUM.ORG What Is a Captive Insurance Company? A captive is A separate legal entity created or used

DELAWARE'S NEW CAPTIVE INSURANCE STATUTE

DELAWARE'S NEW CAPTIVE INSURANCE STATUTE (FORC Journal: Vol. 18 Edition 1 - Spring 2007) Michael W. Teichman, Esq. (302) 594-3331 Hoping to capitalize on its well established reputation as a center for

DELAWARE'S NEW CAPTIVE INSURANCE STATUTE (FORC Journal: Vol. 18 Edition 1 - Spring 2007) Michael W. Teichman, Esq. (302) 594-3331 Hoping to capitalize on its well established reputation as a center for

Why investing money for captive insurance companies is different and the role of an Investment Advisor

Why investing money for captive insurance companies is different and the role of an Investment Advisor Ronnie Dennis Merrill Lynch Why investing money for captive insurance companies is different Regulatory

Why investing money for captive insurance companies is different and the role of an Investment Advisor Ronnie Dennis Merrill Lynch Why investing money for captive insurance companies is different Regulatory

CHAPTER 26.1-31.1 REINSURANCE INTERMEDIARIES

CHAPTER 26.1-31.1 REINSURANCE INTERMEDIARIES 26.1-31.1-01. Definitions. As used in this chapter: 1. "Actuary" means a person who is a member in good standing of the American academy of actuaries. 2. "Controlling

CHAPTER 26.1-31.1 REINSURANCE INTERMEDIARIES 26.1-31.1-01. Definitions. As used in this chapter: 1. "Actuary" means a person who is a member in good standing of the American academy of actuaries. 2. "Controlling