Can your choice of Capital Structure add value to the firm?

|

|

|

- Benedict McDonald

- 7 years ago

- Views:

Transcription

1 Can your choice of Capital Structure add value to the firm? 1

2 The firm borrows $4,000 and buys back 200 shares at $20 per share. 2

3 Notice that the expected return on equity is higher for the leveraged company (both debt and equity), but so is the risk -- notice that the range of return for the all equity company is 5% to 25% while the range for the leveraged company is 0% to 40% -- more variability, more volatility, more risk! 3

and one-time catcher for the New York Yankees: It is after a ball game and the pizza man is delivering")

4 decisions will add value to the firm. I ll begin with the quote attributed to Yogi Berra, a noted Manager (not a financial manager) and one-time catcher for the New York Yankees: It is after a ball game and the pizza man is delivering pizza to Yogi. Should I cut it in four slices as usual, Yogi the pizza man asks. No, replies Yogi, Cut it into eight, I m hungry tonight. Can we use this analogy with capital structure? The value of business assets, assuming there is no tax deductibility of interest, is not affected by the capital structure mix of debt and equity. The present value of the cash flows from assets, the value of assets, is equal to the value of securities issued by the business. Changing the mix of securities does not affect the value of the assets. The left-hand side of the balance sheet, assets, determines the size of the pizza; the mix of securities on the right-hand side of the balance sheet determines how the pizza is sliced. The only way to increase the amount of pizza is to increase the value of assets (pizza), not slicing (financing) in a new combination of slices. Good investment decisions are the key to valuation. This theory or idea won Franco Modigliani and Merton Miller (MM) a 4

5 Nobel Prize. Yogi did not even receive honorable mention. 4

6 M&M s world was one of no taxes and perfectly efficient capital markets. 5

7 MM s proposition I (debt irrelevance proposition). Debt policy should not matter to shareholders. It is the assets that count for value. Why should leveraging, or substituting debt for equity in the capital structure, affect the value of assets? Investors do not need businesses to add leverage to their investment portfolio, they can do it themselves. In the example, instead of the firm borrowing, an individual investor can borrow and obtain the same results (in this case borrow $2,000 and buy 100 additional shares). 6

8 MM s proposition I (debt irrelevance proposition). Debt policy should not matter to shareholders. It is the assets that count for value. Why should leveraging, or substituting debt for equity in the capital structure, affect the value of assets? Investors do not need businesses to add leverage to their investment portfolio, they can do it themselves. In the example, instead of the firm borrowing, an individual investor can borrow and obtain the same results (in this case borrow $2,000 and buy 100 additional shares). 7

9 Does substituting lower cost debt for higher cost equity lower the cost of capital? Not without a tax advantage for debt (no taxes for M&M). By adding debt to the firm, the shareholders have additional risk. In the event of liquidation, the bondholders would be paid first. To compensate for the addition financial risk, stockholders will demand a higher return, leaving the overall cost of capital unchanged. 8

10 The WACC or the r assets does not change as debt is added to the capital structure.this concept is MM s proposition II, which states that the expected return on the common stock increases as the debt/equity ratio increases. Why doesn t the WACC change? As more low cost debt is added to the capital structure, the required rate of return on equity increases to offset the advantage of low cost debt. The WACC does not change; the market value of the firm does not change. Debt does not matter in this situation where the deductibility of interest is not a factor. Debt has an explicit cost in the form of an interest rate, and an incidental, implicit cost impact on the required rate of return on equity as debt is added to the capital structure. In the world of MM, any benefits incurred by substituting cheaper debt for more expensive equity are offset by increases in both their costs. Notice that as the cost of debt increases, even the creditors (bondholders) get edgy about sharing the income stream with other bondholders. The default risk increases. The rate of increase in the shareholder s required rate of return begins to slow as bondholders begin to bear a greater share of the risk. The conclusion is the same: the WACC or expected return on assets or the cost of the package of debt and equity (WACC) does not change. Debt does not affect the value of the assets! 9

11 Reality tells us that financial managers are concerned about finding that right mix of capital structure that produces the lowest or optimal cost of capital. This indicates that there are other factors working beyond MM s assumptions. It is unlikely that capital structure is irrelevant in the real world. In spite of this Modigliani and Miller were pioneers in moving capital structure analysis from an environment in which firms picked their debt ratios based upon their peer group and management preferences to one that recognized trade-offs. They drew attention to the fact that good investment decisions comprise the core of valuation for the firm. There are three claims on the operating income of business: creditors, shareholders, and government. The pizza remains the same size, but there is another slice, the government s. MM would still say that the value of the pizza is not changed by slicing, but anything the firm can do to reduce the size of the government s slice will leave more for the others. The deductibility of interest is a tax shield that diverts government taxes to the shareholders. 10

12 In the real world does capital structure matter? Look at the above example. 11

13 Cash flow to investors is $6500 in the all-equity case. 12

14 Case flow to investors (bond holders and stockholders is $7550). Who gets less? The government because of the interest tax shield. 13

15 How can we calculate the value of the interest tax shield? 14

16 The interest tax shield is equal to the amount of debt times the tax rate. The value of the leverage firm equals the value of the all-equity firm plus the present value of the interest tax shield. Thus capital structure can add value to the firm. But there is a serious omission in this argument! (see the following page.) 15

17 What is wrong in this picture? See the next slide for an answer. 16

18 On the cost of capital side, because of the tax advantage, the cost of capital reclines as you add debt to your capital structure (solid green line), unlike M&M s unchanging WACC (dashed green line). But there is a serious omission in this argument. If the value of the firm rises and the cost of capital drops as we add debt, shouldn t the logically conclusion be to have a capital structure that was all debt? Ah, there s the rub. That argument ignores the fact that as the debt/equity ratio rises, the costs of financial distress (possible bankruptcy) increases. 17

19 Now our equation is complete. The market value of the firm equals the all-equity value plus the present value of the interest tax shield minus the present value cost of financial distress. The present value of the cost of financial distress depends both on the probability of distress and the magnitude of the costs encountered if distress occurs. Aside: be sure to read about bankruptcy procedures and financial distortions in your text. As a firm gets into financial hot water it loses suppliers, customers and employees. There are no winners in bankruptcy (except the lawyers). 18

20 The Trade-off Theory says that capital structure matters. At moderate debt levels the probability of financial distress is trivial, and the tax advantages dominate. The added costs of financial distress overtakes the added value of the tax shield at some point and may lower that value of the firm at some high debt/equity ratio. The theoretical optimum capital structure is the debt/equity level in which the PV of the tax shield is just offset by the PV costs of financial distress. This debt/equity level will maximize market value of the business. Notice that this involves a trade-off: between the value of the tax shield and the cost of bankruptcy. 19

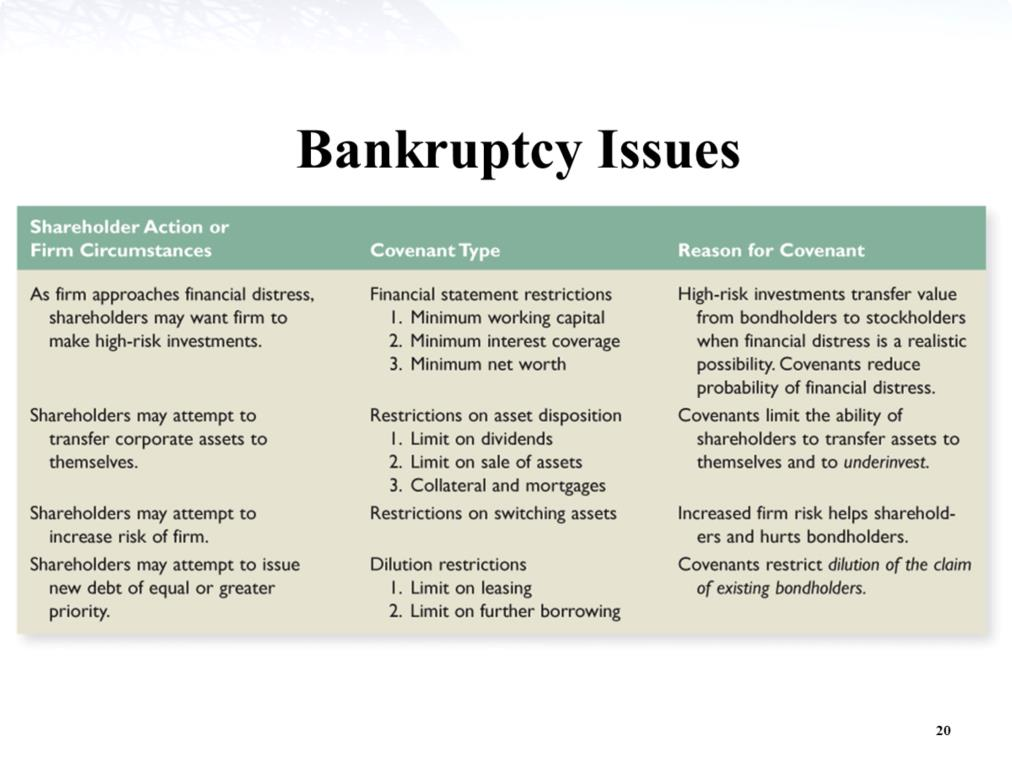

21 20

22 Afterword on the trade-off Theory: Costs of Distress Vary with Type of Asset. Real asset firms tend to lose less value in bankruptcy than firms with significant intangible assets, such as research and development firms who depend upon human capital. If your manufacturing firm is going belly up, the plant and equipment will be around to be liquidated. If a service firm is going belly up, the employees are going to put on their walking shoes and there will be very little to liquidate. Studies have show that sometimes the trade-off theory seems to apply and at other times we see financial sound large companies with little or no debt. It appears they are guided by an alternate theory. (See next page for an explanation of the Pecking Order Theory. 21

23 Businesses prefer to issue debt rather than external equity if internally generated cash flow is insufficient. Use of internally generated funds does not have the signaling effect, positively or negatively, as external funding does. If external funds must be raised, equity will be used reluctantly, reserved as the residual in the finance pecking order. Pecking order is: 1. Internal Equity (Reinvested funds) 2. Debt 3. External Equity (Stock Issue) Under the pecking order theory there is no target debt/equity ratio because there are two kinds of equity: internally generated earnings retained and external stock sales. Internal equity is the first choice for financing ahead of debt, and finally, external equity funding. (See next page.) 22

24 Internal funds are the cheapest and have the least oversight. There are no floatation costs involved. Firms that run out of internal funds turn next to the bond market, where costs are less expensive than in the external equity market. External equity is the most expensive, and as we mentioned earlier in the course, an external stock issue signals the market that the stock is overpriced and is usually followed by a correction. Although the approaches are different, both the Trade-off and Pecking Order Theories conclude that capital structure matters and that the choice of capital structure can add value to the firm (unlike what M&M said). 23

Chapter 15: Debt Policy

FIN 302 Class Notes Chapter 15: Debt Policy Two Cases: Case one: NO TAX All Equity Half Debt Number of shares 100,000 50,000 Price per share $10 $10 Equity Value $1,000,000 $500,000 Debt Value $0 $500,000

FIN 302 Class Notes Chapter 15: Debt Policy Two Cases: Case one: NO TAX All Equity Half Debt Number of shares 100,000 50,000 Price per share $10 $10 Equity Value $1,000,000 $500,000 Debt Value $0 $500,000

CAPITAL STRUCTURE [Chapter 15 and Chapter 16]

![CAPITAL STRUCTURE [Chapter 15 and Chapter 16]](/thumbs/34/17057255.jpg "CAPITAL STRUCTURE [Chapter 15 and Chapter 16]") Capital Structure [CHAP. 15 & 16] -1 CAPITAL STRUCTURE [Chapter 15 and Chapter 16] CONTENTS I. Introduction II. Capital Structure & Firm Value WITHOUT Taxes III. Capital Structure & Firm Value WITH Corporate

Capital Structure [CHAP. 15 & 16] -1 CAPITAL STRUCTURE [Chapter 15 and Chapter 16] CONTENTS I. Introduction II. Capital Structure & Firm Value WITHOUT Taxes III. Capital Structure & Firm Value WITH Corporate

Part 9. The Basics of Corporate Finance

Part 9. The Basics of Corporate Finance The essence of business is to raise money from investors to fund projects that will return more money to the investors. To do this, there are three financial questions

Part 9. The Basics of Corporate Finance The essence of business is to raise money from investors to fund projects that will return more money to the investors. To do this, there are three financial questions

Chapter 17 Capital Structure Limits to the Use of Debt

University of Science and Technology Beijing Dongling School of Economics and management Chapter 17 Capital Structure Limits to the Use of Debt Dec. 2012 Dr. Xiao Ming USTB 1 Key Concepts and Skills Define

University of Science and Technology Beijing Dongling School of Economics and management Chapter 17 Capital Structure Limits to the Use of Debt Dec. 2012 Dr. Xiao Ming USTB 1 Key Concepts and Skills Define

Capital Structure II

Capital Structure II Introduction In the previous lecture we introduced the subject of capital gearing. Gearing occurs when a company is financed partly through fixed return finance (e.g. loans, loan stock

Capital Structure II Introduction In the previous lecture we introduced the subject of capital gearing. Gearing occurs when a company is financed partly through fixed return finance (e.g. loans, loan stock

FIN 413 Corporate Finance. Capital Structure, Taxes, and Bankruptcy

FIN 413 Corporate Finance Capital Structure, Taxes, and Bankruptcy Evgeny Lyandres Fall 2003 1 Relaxing the M-M Assumptions E D T Interest payments to bondholders are deductible for tax purposes while

FIN 413 Corporate Finance Capital Structure, Taxes, and Bankruptcy Evgeny Lyandres Fall 2003 1 Relaxing the M-M Assumptions E D T Interest payments to bondholders are deductible for tax purposes while

MM1 - The value of the firm is independent of its capital structure (the proportion of debt and equity used to finance the firm s operations).

.") Teaching Note Miller Modigliani Consider an economy for which the Efficient Market Hypothesis holds and in which all financial assets are possibly traded (abusing words we call this The Complete Markets

Teaching Note Miller Modigliani Consider an economy for which the Efficient Market Hypothesis holds and in which all financial assets are possibly traded (abusing words we call this The Complete Markets

Source of Finance and their Relative Costs F. COST OF CAPITAL

F. COST OF CAPITAL 1. Source of Finance and their Relative Costs 2. Estimating the Cost of Equity 3. Estimating the Cost of Debt and Other Capital Instruments 4. Estimating the Overall Cost of Capital

F. COST OF CAPITAL 1. Source of Finance and their Relative Costs 2. Estimating the Cost of Equity 3. Estimating the Cost of Debt and Other Capital Instruments 4. Estimating the Overall Cost of Capital

Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.)

") Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.) The primary focus of the next two chapters will be to examine the debt/equity choice by firms. In particular,

Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.) The primary focus of the next two chapters will be to examine the debt/equity choice by firms. In particular,

The Debt-Equity Trade Off: The Capital Structure Decision

The Debt-Equity Trade Off: The Capital Structure Decision Aswath Damodaran Stern School of Business Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable

The Debt-Equity Trade Off: The Capital Structure Decision Aswath Damodaran Stern School of Business Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable

Leverage. FINANCE 350 Global Financial Management. Professor Alon Brav Fuqua School of Business Duke University. Overview

Leverage FINANCE 35 Global Financial Management Professor Alon Brav Fuqua School of Business Duke University Overview Capital Structure does not matter! Modigliani & Miller propositions Implications for

Leverage FINANCE 35 Global Financial Management Professor Alon Brav Fuqua School of Business Duke University Overview Capital Structure does not matter! Modigliani & Miller propositions Implications for

EMBA in Management & Finance. Corporate Finance. Eric Jondeau

EMBA in Management & Finance Corporate Finance EMBA in Management & Finance Lecture 4: Capital Structure Limits to the Use of Debt Outline 1. Costs of Financial Distress 2. Description of Costs 3. Can

EMBA in Management & Finance Corporate Finance EMBA in Management & Finance Lecture 4: Capital Structure Limits to the Use of Debt Outline 1. Costs of Financial Distress 2. Description of Costs 3. Can

Chapter 7: Capital Structure: An Overview of the Financing Decision

Chapter 7: Capital Structure: An Overview of the Financing Decision 1. Income bonds are similar to preferred stock in several ways. Payment of interest on income bonds depends on the availability of sufficient

Chapter 7: Capital Structure: An Overview of the Financing Decision 1. Income bonds are similar to preferred stock in several ways. Payment of interest on income bonds depends on the availability of sufficient

CHAPTER 15 Capital Structure: Basic Concepts

Multiple Choice Questions: CHAPTER 15 Capital Structure: Basic Concepts I. DEFINITIONS HOMEMADE LEVERAGE a 1. The use of personal borrowing to change the overall amount of financial leverage to which an

Multiple Choice Questions: CHAPTER 15 Capital Structure: Basic Concepts I. DEFINITIONS HOMEMADE LEVERAGE a 1. The use of personal borrowing to change the overall amount of financial leverage to which an

Chapter 17 Does Debt Policy Matter?

Chapter 17 Does Debt Policy Matter? Multiple Choice Questions 1. When a firm has no debt, then such a firm is known as: (I) an unlevered firm (II) a levered firm (III) an all-equity firm D) I and III only

Chapter 17 Does Debt Policy Matter? Multiple Choice Questions 1. When a firm has no debt, then such a firm is known as: (I) an unlevered firm (II) a levered firm (III) an all-equity firm D) I and III only

cost of capital, 01 technical this measurement of a company s cost of equity THere are two ways of estimating the cost of equity (the return

01 technical cost of capital, THere are two ways of estimating the cost of equity (the return required by shareholders). Can this measurement of a company s cost of equity be used as the discount rate

01 technical cost of capital, THere are two ways of estimating the cost of equity (the return required by shareholders). Can this measurement of a company s cost of equity be used as the discount rate

FNCE 301, Financial Management H Guy Williams, 2006

Stock Valuation Stock characteristics Stocks are the other major traded security (stocks & bonds). Options are another traded security but not as big as these two. - Ownership Stockholders are the owner

Stock Valuation Stock characteristics Stocks are the other major traded security (stocks & bonds). Options are another traded security but not as big as these two. - Ownership Stockholders are the owner

Finding the Right Financing Mix: The Capital Structure Decision. Aswath Damodaran 1

Finding the Right Financing Mix: The Capital Structure Decision Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate

Finding the Right Financing Mix: The Capital Structure Decision Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate

Capital Structure. Itay Goldstein. Wharton School, University of Pennsylvania

Capital Structure Itay Goldstein Wharton School, University of Pennsylvania 1 Debt and Equity There are two main types of financing: debt and equity. Consider a two-period world with dates 0 and 1. At

Capital Structure Itay Goldstein Wharton School, University of Pennsylvania 1 Debt and Equity There are two main types of financing: debt and equity. Consider a two-period world with dates 0 and 1. At

Discounted Cash Flow. Alessandro Macrì. Legal Counsel, GMAC Financial Services

Discounted Cash Flow Alessandro Macrì Legal Counsel, GMAC Financial Services History The idea that the value of an asset is the present value of the cash flows that you expect to generate by holding it

Discounted Cash Flow Alessandro Macrì Legal Counsel, GMAC Financial Services History The idea that the value of an asset is the present value of the cash flows that you expect to generate by holding it

Fundamentals Level Skills Module, Paper F9. Section A. Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6%

![Fundamentals Level Skills Module, Paper F9. Section A. Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6%](/thumbs/40/20831119.jpg "Fundamentals Level Skills Module, Paper F9. Section A. Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6%") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2015 Answers Section A 1 A 2 D 3 D Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6% 4 A 5 D 6 B 7

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2015 Answers Section A 1 A 2 D 3 D Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6% 4 A 5 D 6 B 7

Dividend Policy. Vinod Kothari

Dividend Policy Vinod Kothari Corporations earn profits they do not distribute all of it. Part of profit is ploughed back or held back as retained earnings. Part of the profit gets distributed to the shareholders.

Dividend Policy Vinod Kothari Corporations earn profits they do not distribute all of it. Part of profit is ploughed back or held back as retained earnings. Part of the profit gets distributed to the shareholders.

Leverage and Capital Structure

Leverage and Capital Structure Ross Chapter 16 Spring 2005 10.1 Leverage Financial Leverage Financial leverage is the use of fixed financial costs to magnify the effect of changes in EBIT on EPS. Fixed

Leverage and Capital Structure Ross Chapter 16 Spring 2005 10.1 Leverage Financial Leverage Financial leverage is the use of fixed financial costs to magnify the effect of changes in EBIT on EPS. Fixed

Corporate Finance & Options: MGT 891 Homework #6 Answers

Corporate Finance & Options: MGT 891 Homework #6 Answers Question 1 A. The APV rule states that the present value of the firm equals it all equity value plus the present value of the tax shield. In this

Corporate Finance & Options: MGT 891 Homework #6 Answers Question 1 A. The APV rule states that the present value of the firm equals it all equity value plus the present value of the tax shield. In this

CHAPTER 13 Capital Structure and Leverage

CHAPTER 13 Capital Structure and Leverage Business and financial risk Optimal capital structure Operating Leverage Capital structure theory 1 What s business risk? Uncertainty about future operating income

CHAPTER 13 Capital Structure and Leverage Business and financial risk Optimal capital structure Operating Leverage Capital structure theory 1 What s business risk? Uncertainty about future operating income

Total shares at the end of ten years is 100*(1+5%) 10 =162.9.

10 =162.9.") FCS5510 Sample Homework Problems Unit04 CHAPTER 8 STOCK PROBLEMS 1. An investor buys 100 shares if a $40 stock that pays a annual cash dividend of $2 a share (a 5% dividend yield) and signs up for the

FCS5510 Sample Homework Problems Unit04 CHAPTER 8 STOCK PROBLEMS 1. An investor buys 100 shares if a $40 stock that pays a annual cash dividend of $2 a share (a 5% dividend yield) and signs up for the

1. What is a recapitalization? Why is this considered a pure capital structure change?

CHAPTER 12 CONCEPT REVIEW QUESTIONS 1. What is a recapitalization? Why is this considered a pure capital structure change? Recapitalization is an alteration of a company s capital structure to change the

CHAPTER 12 CONCEPT REVIEW QUESTIONS 1. What is a recapitalization? Why is this considered a pure capital structure change? Recapitalization is an alteration of a company s capital structure to change the

Chapter 1: The Modigliani-Miller Propositions, Taxes and Bankruptcy Costs

Chapter 1: The Modigliani-Miller Propositions, Taxes and Bankruptcy Costs Corporate Finance - MSc in Finance (BGSE) Albert Banal-Estañol Universitat Pompeu Fabra and Barcelona GSE Albert Banal-Estañol

Chapter 1: The Modigliani-Miller Propositions, Taxes and Bankruptcy Costs Corporate Finance - MSc in Finance (BGSE) Albert Banal-Estañol Universitat Pompeu Fabra and Barcelona GSE Albert Banal-Estañol

optimum capital Is it possible to increase shareholder wealth by changing the capital structure?

78 technical optimum capital RELEVANT TO ACCA QUALIFICATION PAPER F9 Is it possible to increase shareholder wealth by changing the capital structure? The first question to address is what is meant by capital

78 technical optimum capital RELEVANT TO ACCA QUALIFICATION PAPER F9 Is it possible to increase shareholder wealth by changing the capital structure? The first question to address is what is meant by capital

Ch. 18: Taxes + Bankruptcy cost

Ch. 18: Taxes + Bankruptcy cost If MM1 holds, then Financial Management has little (if any) impact on value of the firm: If markets are perfect, transaction cost (TAC) and bankruptcy cost are zero, no

Ch. 18: Taxes + Bankruptcy cost If MM1 holds, then Financial Management has little (if any) impact on value of the firm: If markets are perfect, transaction cost (TAC) and bankruptcy cost are zero, no

Chapter 14 Assessing Long-Term Debt, Equity, and Capital Structure

I. Capital Structure (definitions) II. MM without Taxes (1958) III. MM with Taxes (1963) Chapter 14 Assessing Long-Term Debt, Equity, and Capital Structure IV. Financial Distress V. Business Risk VI. Financial

I. Capital Structure (definitions) II. MM without Taxes (1958) III. MM with Taxes (1963) Chapter 14 Assessing Long-Term Debt, Equity, and Capital Structure IV. Financial Distress V. Business Risk VI. Financial

DUKE UNIVERSITY Fuqua School of Business. FINANCE 351 - CORPORATE FINANCE Problem Set #7 Prof. Simon Gervais Fall 2011 Term 2.

DUKE UNIVERSITY Fuqua School of Business FINANCE 351 - CORPORATE FINANCE Problem Set #7 Prof. Simon Gervais Fall 2011 Term 2 Questions 1. Suppose the corporate tax rate is 40%, and investors pay a tax

DUKE UNIVERSITY Fuqua School of Business FINANCE 351 - CORPORATE FINANCE Problem Set #7 Prof. Simon Gervais Fall 2011 Term 2 Questions 1. Suppose the corporate tax rate is 40%, and investors pay a tax

Value-Based Management

Value-Based Management Lecture 5: Calculating the Cost of Capital Prof. Dr. Gunther Friedl Lehrstuhl für Controlling Technische Universität München Email: gunther.friedl@tum.de Overview 1. Value Maximization

Value-Based Management Lecture 5: Calculating the Cost of Capital Prof. Dr. Gunther Friedl Lehrstuhl für Controlling Technische Universität München Email: gunther.friedl@tum.de Overview 1. Value Maximization

University of Waterloo Midterm Examination

Student number: Student name: ANONYMOUS Instructor: Dr. Hongping Tan Duration: 1.5 hours AFM 371/2 Winter 2011 4:30-6:00 Tuesday, March 1 This exam has 12 pages including this page. Important Information:

Student number: Student name: ANONYMOUS Instructor: Dr. Hongping Tan Duration: 1.5 hours AFM 371/2 Winter 2011 4:30-6:00 Tuesday, March 1 This exam has 12 pages including this page. Important Information:

If you ignore taxes in this problem and there is no debt outstanding: EPS = EBIT/shares outstanding = $14,000/2,500 = $5.60

Problems Relating to Capital Structure and Leverage 1. EBIT and Leverage Money Inc., has no debt outstanding and a total market value of $150,000. Earnings before interest and taxes [EBIT] are projected

Problems Relating to Capital Structure and Leverage 1. EBIT and Leverage Money Inc., has no debt outstanding and a total market value of $150,000. Earnings before interest and taxes [EBIT] are projected

IESE UNIVERSITY OF NAVARRA OPTIMAL CAPITAL STRUCTURE: PROBLEMS WITH THE HARVARD AND DAMODARAN APPROACHES. Pablo Fernández*

IESE UNIVERSITY OF NAVARRA OPTIMAL CAPITAL STRUCTURE: PROBLEMS WITH THE HARVARD AND DAMODARAN APPROACHES Pablo Fernández* RESEARCH PAPER No 454 January, 2002 * Professor of Financial Management, IESE Research

IESE UNIVERSITY OF NAVARRA OPTIMAL CAPITAL STRUCTURE: PROBLEMS WITH THE HARVARD AND DAMODARAN APPROACHES Pablo Fernández* RESEARCH PAPER No 454 January, 2002 * Professor of Financial Management, IESE Research

CHAPTER 16. Financial Distress, Managerial Incentives, and Information. Chapter Synopsis

CHAPTER 16 Financial Distress, Managerial Incentives, and Information Chapter Synopsis In the previous two chapters it was shown that, in an otherwise perfect capital market in which firms pay taxes, the

CHAPTER 16 Financial Distress, Managerial Incentives, and Information Chapter Synopsis In the previous two chapters it was shown that, in an otherwise perfect capital market in which firms pay taxes, the

Chapter 5 Valuing Stocks

Chapter 5 Valuing Stocks MULTIPLE CHOICE 1. The first public sale of company stock to outside investors is called a/an a. seasoned equity offering. b. shareholders meeting. c. initial public offering.

Chapter 5 Valuing Stocks MULTIPLE CHOICE 1. The first public sale of company stock to outside investors is called a/an a. seasoned equity offering. b. shareholders meeting. c. initial public offering.

Financial Statement and Cash Flow Analysis

Chapter 2 Financial Statement and Cash Flow Analysis Answers to Concept Review Questions 1. What role do the FASB and SEC play with regard to GAAP? The FASB is a nongovernmental, professional standards

Chapter 2 Financial Statement and Cash Flow Analysis Answers to Concept Review Questions 1. What role do the FASB and SEC play with regard to GAAP? The FASB is a nongovernmental, professional standards

Chapter 14 Capital Structure in a Perfect Market

Chapter 14 Capital Structure in a Perfect Market 14-1. Consider a project with free cash flows in one year of $130,000 or $180,000, with each outcome being equally likely. The initial investment required

Chapter 14 Capital Structure in a Perfect Market 14-1. Consider a project with free cash flows in one year of $130,000 or $180,000, with each outcome being equally likely. The initial investment required

A Basic Introduction to the Methodology Used to Determine a Discount Rate

A Basic Introduction to the Methodology Used to Determine a Discount Rate By Dubravka Tosic, Ph.D. The term discount rate is one of the most fundamental, widely used terms in finance and economics. Whether

A Basic Introduction to the Methodology Used to Determine a Discount Rate By Dubravka Tosic, Ph.D. The term discount rate is one of the most fundamental, widely used terms in finance and economics. Whether

E2-2: Identifying Financing, Investing and Operating Transactions?

E2-2: Identifying Financing, Investing and Operating Transactions? Listed below are eight transactions. In each case, identify whether the transaction is an example of financing, investing or operating

E2-2: Identifying Financing, Investing and Operating Transactions? Listed below are eight transactions. In each case, identify whether the transaction is an example of financing, investing or operating

The value of tax shields is NOT equal to the present value of tax shields

The value of tax shields is NOT equal to the present value of tax shields Pablo Fernández * IESE Business School. University of Navarra. Madrid, Spain ABSTRACT We show that the value of tax shields is

The value of tax shields is NOT equal to the present value of tax shields Pablo Fernández * IESE Business School. University of Navarra. Madrid, Spain ABSTRACT We show that the value of tax shields is

Wrap-up of Financing. Katharina Lewellen Finance Theory II March 11, 2003

Wrap-up of Financing Katharina Lewellen Finance Theory II March 11, 2003 Overview of Financing Financial forecasting Short-run forecasting General dynamics: Sustainable growth. Capital structure Describing

Wrap-up of Financing Katharina Lewellen Finance Theory II March 11, 2003 Overview of Financing Financial forecasting Short-run forecasting General dynamics: Sustainable growth. Capital structure Describing

Appendix B Weighted Average Cost of Capital

Appendix B Weighted Average Cost of Capital The inclusion of cost of money within cash flow analyses in engineering economics and life-cycle costing is a very important (and in many cases dominate) contributing

Appendix B Weighted Average Cost of Capital The inclusion of cost of money within cash flow analyses in engineering economics and life-cycle costing is a very important (and in many cases dominate) contributing

TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II + III

SOLUTIONS RE-EXAMS 2014 II + III") TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II III Instructions 1. Only one problem should be treated on each sheet of paper and only one side of the sheet should be used. 2. The solutions folder

TPPE17 Corporate Finance 1(5) SOLUTIONS RE-EXAMS 2014 II III Instructions 1. Only one problem should be treated on each sheet of paper and only one side of the sheet should be used. 2. The solutions folder

Financial Management Sample paper 1

Financial Management Sample paper 1 Time: 3 hours Maxi Mark 100 General Instructions 1. Answers to questions carrying 1 mark may be from one word to one sentence. 2. Answers to questions carrying 3 marks

Financial Management Sample paper 1 Time: 3 hours Maxi Mark 100 General Instructions 1. Answers to questions carrying 1 mark may be from one word to one sentence. 2. Answers to questions carrying 3 marks

- Once we have computed the costs of the individual components of the firm s financing,

WEIGHTED AVERAGE COST OF CAPITAL - Once we have computed the costs of the individual components of the firm s financing, we would assign weight to each financing source according to some standard and then

WEIGHTED AVERAGE COST OF CAPITAL - Once we have computed the costs of the individual components of the firm s financing, we would assign weight to each financing source according to some standard and then

Current and Non-Current Assets as Part of the Regulatory Asset Base. (The Return to Working Capital: Australia Post) R.R.Officer and S.

R.R.Officer and S.") Current and Non-Current Assets as Part of the Regulatory Asset Base. (The Return to Working Capital: Australia Post) R.R.Officer and S.R Bishop 1 4 th October 2007 Overview Initially, the task was to examine

Current and Non-Current Assets as Part of the Regulatory Asset Base. (The Return to Working Capital: Australia Post) R.R.Officer and S.R Bishop 1 4 th October 2007 Overview Initially, the task was to examine

CHAPTER 17 Does Debt Policy Matter?

CHPTR 17 Does Debt Policy Matter? nswers to Practice Questions 1. a. The two firms have equal value; let represent the total value of the firm. Rosencrantz could buy one percent of Company B s equity and

CHPTR 17 Does Debt Policy Matter? nswers to Practice Questions 1. a. The two firms have equal value; let represent the total value of the firm. Rosencrantz could buy one percent of Company B s equity and

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

Chapter 31. Financial Management in Not-for-Profit Businesses

Chapter 31 Financial Management in Not-for-Profit Businesses Topics in Chapter For-profit (investor-owned) vs. not-forprofit businesses Goals of the firm What are the key features of investor-owned firms?

Chapter 31 Financial Management in Not-for-Profit Businesses Topics in Chapter For-profit (investor-owned) vs. not-forprofit businesses Goals of the firm What are the key features of investor-owned firms?

Capital Structure: Informational and Agency Considerations

Capital Structure: Informational and Agency Considerations The Big Picture: Part I - Financing A. Identifying Funding Needs Feb 6 Feb 11 Case: Wilson Lumber 1 Case: Wilson Lumber 2 B. Optimal Capital Structure:

Capital Structure: Informational and Agency Considerations The Big Picture: Part I - Financing A. Identifying Funding Needs Feb 6 Feb 11 Case: Wilson Lumber 1 Case: Wilson Lumber 2 B. Optimal Capital Structure:

Why banks prefer leverage?

Why banks prefer leverage? By Re i m o Ju k s 1 reimo Juks holds a PhD in finance from the Stockholm School of Economics. He works in the Financial Stability Department of the Riksbank. Introduction The

Why banks prefer leverage? By Re i m o Ju k s 1 reimo Juks holds a PhD in finance from the Stockholm School of Economics. He works in the Financial Stability Department of the Riksbank. Introduction The

Financial Distress EC 1745. Borja Larrain

Financial Distress EC 1745 Borja Larrain Today: 1. Costs of financial distress. 2. Trade-off theory of capital structure. 3. Empirical estimates of the costs of financial distress. 4. Bankruptcy. Readings:

Financial Distress EC 1745 Borja Larrain Today: 1. Costs of financial distress. 2. Trade-off theory of capital structure. 3. Empirical estimates of the costs of financial distress. 4. Bankruptcy. Readings:

CHAPTER 4. FINANCIAL STATEMENTS

CHAPTER 4. FINANCIAL STATEMENTS Accounting standards require statements that show the financial position, earnings, cash flows, and investment (distribution) by (to) owners. These measurements are reported,

CHAPTER 4. FINANCIAL STATEMENTS Accounting standards require statements that show the financial position, earnings, cash flows, and investment (distribution) by (to) owners. These measurements are reported,

Selecting sources of finance for business

Selecting sources of finance for business by Steve Jay 08 Sep 2003 This article considers the practical issues facing a business when selecting appropriate sources of finance. It does not consider the

Selecting sources of finance for business by Steve Jay 08 Sep 2003 This article considers the practical issues facing a business when selecting appropriate sources of finance. It does not consider the

The cost of capital. A reading prepared by Pamela Peterson Drake. 1. Introduction

The cost of capital A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction... 1 2. Determining the proportions of each source of capital that will be raised... 3 3. Estimating the marginal

The cost of capital A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction... 1 2. Determining the proportions of each source of capital that will be raised... 3 3. Estimating the marginal

Fundamentals Level Skills Module, Paper F9

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2009 Answers 1 (a) Weighted average cost of capital (WACC) calculation Cost of equity of KFP Co = 4 0 + (1 2 x (10 5 4 0)) =

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2009 Answers 1 (a) Weighted average cost of capital (WACC) calculation Cost of equity of KFP Co = 4 0 + (1 2 x (10 5 4 0)) =

The Discount Rate: A Note on IAS 36

The Discount Rate: A Note on IAS 36 Sven Husmann Martin Schmidt Thorsten Seidel European University Viadrina Frankfurt (Oder) Department of Business Administration and Economics Discussion Paper No. 246

The Discount Rate: A Note on IAS 36 Sven Husmann Martin Schmidt Thorsten Seidel European University Viadrina Frankfurt (Oder) Department of Business Administration and Economics Discussion Paper No. 246

Chapter 2 Balance sheets - what a company owns and what it owes

Chapter 2 Balance sheets - what a company owns and what it owes SharePad is packed full of useful financial data. This data holds the key to understanding the financial health and value of any company

Chapter 2 Balance sheets - what a company owns and what it owes SharePad is packed full of useful financial data. This data holds the key to understanding the financial health and value of any company

SOLUTIONS. Practice questions. Multiple Choice

Practice questions Multiple Choice 1. XYZ has $25,000 of debt outstanding and a book value of equity of $25,000. The company has 10,000 shares outstanding and a stock price of $10. If the unlevered beta

Practice questions Multiple Choice 1. XYZ has $25,000 of debt outstanding and a book value of equity of $25,000. The company has 10,000 shares outstanding and a stock price of $10. If the unlevered beta

Option Pricing Applications in Valuation!

Option Pricing Applications in Valuation! Equity Value in Deeply Troubled Firms Value of Undeveloped Reserves for Natural Resource Firm Value of Patent/License 73 Option Pricing Applications in Equity

Option Pricing Applications in Valuation! Equity Value in Deeply Troubled Firms Value of Undeveloped Reserves for Natural Resource Firm Value of Patent/License 73 Option Pricing Applications in Equity

6. Debt Valuation and the Cost of Capital

6. Debt Valuation and the Cost of Capital Introduction Firms rarely finance capital projects by equity alone. They utilise long and short term funds from a variety of sources at a variety of costs. No

6. Debt Valuation and the Cost of Capital Introduction Firms rarely finance capital projects by equity alone. They utilise long and short term funds from a variety of sources at a variety of costs. No

On the Applicability of WACC for Investment Decisions

On the Applicability of WACC for Investment Decisions Jaime Sabal Department of Financial Management and Control ESADE. Universitat Ramon Llull Received: December, 2004 Abstract Although WACC is appropriate

On the Applicability of WACC for Investment Decisions Jaime Sabal Department of Financial Management and Control ESADE. Universitat Ramon Llull Received: December, 2004 Abstract Although WACC is appropriate

Fuqua School of Business, Duke University ACCOUNTG 510: Foundations of Financial Accounting

Fuqua School of Business, Duke University ACCOUNTG 510: Foundations of Financial Accounting Lecture Note: Financial Statement Basics, Transaction Recording, and Terminology I. The Financial Reporting Package

Fuqua School of Business, Duke University ACCOUNTG 510: Foundations of Financial Accounting Lecture Note: Financial Statement Basics, Transaction Recording, and Terminology I. The Financial Reporting Package

t = 1 2 3 1. Calculate the implied interest rates and graph the term structure of interest rates. t = 1 2 3 X t = 100 100 100 t = 1 2 3

MØA 155 PROBLEM SET: Summarizing Exercise 1. Present Value [3] You are given the following prices P t today for receiving risk free payments t periods from now. t = 1 2 3 P t = 0.95 0.9 0.85 1. Calculate

MØA 155 PROBLEM SET: Summarizing Exercise 1. Present Value [3] You are given the following prices P t today for receiving risk free payments t periods from now. t = 1 2 3 P t = 0.95 0.9 0.85 1. Calculate

Financial Statement Analysis!

Financial Statement Analysis! The raw data for investing Aswath Damodaran! 1! Questions we would like answered! Assets Liabilities What are the assets in place? How valuable are these assets? How risky

Financial Statement Analysis! The raw data for investing Aswath Damodaran! 1! Questions we would like answered! Assets Liabilities What are the assets in place? How valuable are these assets? How risky

Introduction to Profit and Loss Accounts and Balance Sheets

W J E C B U S I N E S S S T U D I E S A L E V E L R E S O U R C E S. 2008 Spec Issue 2 Sept 2012 Page 1 Introduction to Profit and Loss Accounts and Balance Sheets Specification Requirement -Understand

W J E C B U S I N E S S S T U D I E S A L E V E L R E S O U R C E S. 2008 Spec Issue 2 Sept 2012 Page 1 Introduction to Profit and Loss Accounts and Balance Sheets Specification Requirement -Understand

CHAPTER 18 Dividend and Other Payouts

CHAPTER 18 Dividend and Other Payouts Multiple Choice Questions: I. DEFINITIONS DIVIDENDS a 1. Payments made out of a firm s earnings to its owners in the form of cash or stock are called: a. dividends.

CHAPTER 18 Dividend and Other Payouts Multiple Choice Questions: I. DEFINITIONS DIVIDENDS a 1. Payments made out of a firm s earnings to its owners in the form of cash or stock are called: a. dividends.

7 CAPITAL STRUCTURE AND FINANCIAL LEVERAGE

7 CAPITAL STRUCTURE AND FINANCIAL LEVERAGE Capital structure refers to the way a corporation finances its assets through some combination of equity and debt. A firm's capital structure is then the composition

7 CAPITAL STRUCTURE AND FINANCIAL LEVERAGE Capital structure refers to the way a corporation finances its assets through some combination of equity and debt. A firm's capital structure is then the composition

Chapter 002 Financial Statements, Taxes and Cash Flow

Multiple Choice Questions 1. The financial statement summarizing the value of a firm's equity on a particular date is the: a. income statement. B. balance sheet. c. statement of cash flows. d. cash flow

Multiple Choice Questions 1. The financial statement summarizing the value of a firm's equity on a particular date is the: a. income statement. B. balance sheet. c. statement of cash flows. d. cash flow

There was no evidence of time pressure in this exam and the majority of candidates were able to attempt all questions within the time limit.

Examiner s General Comments Performance on F3 in May was a distinct improvement over some previous diets. This improvement was evident in both home and overseas centres although there were significant

Examiner s General Comments Performance on F3 in May was a distinct improvement over some previous diets. This improvement was evident in both home and overseas centres although there were significant

Practice Exam (Solutions)

") Practice Exam (Solutions) June 6, 2008 Course: Finance for AEO Length: 2 hours Lecturer: Paul Sengmüller Students are expected to conduct themselves properly during examinations and to obey any instructions

Practice Exam (Solutions) June 6, 2008 Course: Finance for AEO Length: 2 hours Lecturer: Paul Sengmüller Students are expected to conduct themselves properly during examinations and to obey any instructions

Test3. Pessimistic Most Likely Optimistic Total Revenues 30 50 65 Total Costs -25-20 -15

Test3 1. The market value of Charcoal Corporation's common stock is $20 million, and the market value of its riskfree debt is $5 million. The beta of the company's common stock is 1.25, and the market

Test3 1. The market value of Charcoal Corporation's common stock is $20 million, and the market value of its riskfree debt is $5 million. The beta of the company's common stock is 1.25, and the market

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 6 Introduction to Corporate Bonds

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 6 Introduction to Corporate Bonds Today: I. Equity is a call on firm value II. Senior Debt III. Junior Debt IV. Convertible Debt V. Variance

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 6 Introduction to Corporate Bonds Today: I. Equity is a call on firm value II. Senior Debt III. Junior Debt IV. Convertible Debt V. Variance

Discount rates for project appraisal

Discount rates for project appraisal We know that we have to discount cash flows in order to value projects We can identify the cash flows BUT What discount rate should we use? 1 The Discount Rate and

Discount rates for project appraisal We know that we have to discount cash flows in order to value projects We can identify the cash flows BUT What discount rate should we use? 1 The Discount Rate and

Mutual Fund Expense Information on Quarterly Shareholder Statements

June 2005 Mutual Fund Expense Information on Quarterly Shareholder Statements You may have noticed that beginning with your March 31 quarterly statement from AllianceBernstein, two new sections have been

June 2005 Mutual Fund Expense Information on Quarterly Shareholder Statements You may have noticed that beginning with your March 31 quarterly statement from AllianceBernstein, two new sections have been

The Modigliani-Miller Theorem The New Palgrave Dictionary of Economics Anne P. Villamil, University of Illinois

The Modigliani-Miller Theorem The New Palgrave Dictionary of Economics Anne P. Villamil, University of Illinois The Modigliani-Miller Theorem is a cornerstone of modern corporate finance. At its heart,

The Modigliani-Miller Theorem The New Palgrave Dictionary of Economics Anne P. Villamil, University of Illinois The Modigliani-Miller Theorem is a cornerstone of modern corporate finance. At its heart,

COST OF CAPITAL. Please note that in finance, we are concerned with MARKET VALUES (unlike accounting, which is concerned with book values).

.") COST OF CAPITAL Cost of capital calculations are a very important part of finance. To value a project, it is important to discount the cash flows using a discount rate that incorporates the debt-equity

COST OF CAPITAL Cost of capital calculations are a very important part of finance. To value a project, it is important to discount the cash flows using a discount rate that incorporates the debt-equity

Use the table for the questions 18 and 19 below.

Use the table for the questions 18 and 19 below. The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of face value): Maturity (years) 1 3 4 5 Price

Use the table for the questions 18 and 19 below. The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of face value): Maturity (years) 1 3 4 5 Price

CHAPTER 20. Hybrid Financing: Preferred Stock, Warrants, and Convertibles

CHAPTER 20 Hybrid Financing: Preferred Stock, Warrants, and Convertibles 1 Topics in Chapter Types of hybrid securities Preferred stock Warrants Convertibles Features and risk Cost of capital to issuers

CHAPTER 20 Hybrid Financing: Preferred Stock, Warrants, and Convertibles 1 Topics in Chapter Types of hybrid securities Preferred stock Warrants Convertibles Features and risk Cost of capital to issuers

Real Estate Investment Newsletter July 2004

The Case for Selling Real Estate in California This month I am writing the newsletter for those investors who currently own rental properties 1 in California. In any type of investing, be it real estate,

The Case for Selling Real Estate in California This month I am writing the newsletter for those investors who currently own rental properties 1 in California. In any type of investing, be it real estate,

Chapter 7. . 1. component of the convertible can be estimated as 1100-796.15 = 303.85.

Chapter 7 7-1 Income bonds do share some characteristics with preferred stock. The primary difference is that interest paid on income bonds is tax deductible while preferred dividends are not. Income bondholders

Chapter 7 7-1 Income bonds do share some characteristics with preferred stock. The primary difference is that interest paid on income bonds is tax deductible while preferred dividends are not. Income bondholders

Fundamentals Level Skills Module, Paper F9

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2008 Answers 1 (a) Calculation of weighted average cost of capital (WACC) Cost of equity Cost of equity using capital asset

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2008 Answers 1 (a) Calculation of weighted average cost of capital (WACC) Cost of equity Cost of equity using capital asset

Shares Mutual funds Structured bonds Bonds Cash money, deposits

FINANCIAL INSTRUMENTS AND RELATED RISKS This description of investment risks is intended for you. The professionals of AB bank Finasta have strived to understandably introduce you the main financial instruments

FINANCIAL INSTRUMENTS AND RELATED RISKS This description of investment risks is intended for you. The professionals of AB bank Finasta have strived to understandably introduce you the main financial instruments

CHAPTER FOUR Cash Accounting, Accrual Accounting, and Discounted Cash Flow Valuation

CHAPTER FOUR Cash Accounting, Accrual Accounting, and Discounted Cash Flow Valuation Concept Questions C4.1. There are difficulties in comparing multiples of earnings and book values - the old techniques

CHAPTER FOUR Cash Accounting, Accrual Accounting, and Discounted Cash Flow Valuation Concept Questions C4.1. There are difficulties in comparing multiples of earnings and book values - the old techniques

Fundamentals Level Skills Module, Paper F9

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2008 Answers 1 (a) Rights issue price = 2 5 x 0 8 = $2 00 per share Theoretical ex rights price = ((2 50 x 4) + (1 x 2 00)/5=$2

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2008 Answers 1 (a) Rights issue price = 2 5 x 0 8 = $2 00 per share Theoretical ex rights price = ((2 50 x 4) + (1 x 2 00)/5=$2

THE COST OF CAPITAL THE EFFECT OF CHANGES IN GEARING

December 2015 Examinations Chapter 19 Free lectures available for - click here THE COST OF CAPITAL THE EFFECT OF CHANGES IN GEARING 103 1 Introduction In this chapter we will look at the effect of gearing

December 2015 Examinations Chapter 19 Free lectures available for - click here THE COST OF CAPITAL THE EFFECT OF CHANGES IN GEARING 103 1 Introduction In this chapter we will look at the effect of gearing

THE FINANCING DECISIONS BY FIRMS: IMPACT OF CAPITAL STRUCTURE CHOICE ON VALUE

IX. THE FINANCING DECISIONS BY FIRMS: IMPACT OF CAPITAL STRUCTURE CHOICE ON VALUE The capital structure of a firm is defined to be the menu of the firm's liabilities (i.e, the "right-hand side" of the

IX. THE FINANCING DECISIONS BY FIRMS: IMPACT OF CAPITAL STRUCTURE CHOICE ON VALUE The capital structure of a firm is defined to be the menu of the firm's liabilities (i.e, the "right-hand side" of the

Accepted 4 October, 2011

Vol. 7(22), pp. 2079-2085, 14 June, 2013 DOI: 10.5897/AJBM11.1853 ISSN 1993-8233 2013 Academic Journals http://www.academicjournals.org/ajbm African Journal of Business Management Review How to get correct

Vol. 7(22), pp. 2079-2085, 14 June, 2013 DOI: 10.5897/AJBM11.1853 ISSN 1993-8233 2013 Academic Journals http://www.academicjournals.org/ajbm African Journal of Business Management Review How to get correct

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION OCTOBER 2006 Table of Contents 1. INTRODUCTION... 3 2. FINANCIAL RATIOS FOR COMPANIES (INDUSTRY - COMMERCE - SERVICES) 4 2.1 Profitability Ratios...4 2.2 Viability

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION OCTOBER 2006 Table of Contents 1. INTRODUCTION... 3 2. FINANCIAL RATIOS FOR COMPANIES (INDUSTRY - COMMERCE - SERVICES) 4 2.1 Profitability Ratios...4 2.2 Viability

Examiner s report F9 Financial Management June 2011

Examiner s report F9 Financial Management June 2011 General Comments Congratulations to candidates who passed Paper F9 in June 2011! The examination paper looked at many areas of the syllabus and a consideration

Examiner s report F9 Financial Management June 2011 General Comments Congratulations to candidates who passed Paper F9 in June 2011! The examination paper looked at many areas of the syllabus and a consideration

INTERVIEWS - FINANCIAL MODELING

420 W. 118th Street, Room 420 New York, NY 10027 P: 212-854-4613 F: 212-854-6190 www.sipa.columbia.edu/ocs INTERVIEWS - FINANCIAL MODELING Basic valuation concepts are among the most popular technical

420 W. 118th Street, Room 420 New York, NY 10027 P: 212-854-4613 F: 212-854-6190 www.sipa.columbia.edu/ocs INTERVIEWS - FINANCIAL MODELING Basic valuation concepts are among the most popular technical

Often stock is split to lower the price per share so it is more accessible to investors. The stock split is not taxable.

Reading: Chapter 8 Chapter 8. Stock: Introduction 1. Rights of stockholders 2. Cash dividends 3. Stock dividends 4. The stock split 5. Stock repurchases and liquidations 6. Preferred stock 7. Analysis

Reading: Chapter 8 Chapter 8. Stock: Introduction 1. Rights of stockholders 2. Cash dividends 3. Stock dividends 4. The stock split 5. Stock repurchases and liquidations 6. Preferred stock 7. Analysis

Cost of Capital, Valuation and Strategic Financial Decision Making

Cost of Capital, Valuation and Strategic Financial Decision Making By Dr. Valerio Poti, - Examiner in Professional 2 Stage Strategic Corporate Finance The financial crisis that hit financial markets in

Cost of Capital, Valuation and Strategic Financial Decision Making By Dr. Valerio Poti, - Examiner in Professional 2 Stage Strategic Corporate Finance The financial crisis that hit financial markets in

UNIVERSITY OF WAH Department of Management Sciences

BBA-330: FINANCIAL MANAGEMENT UNIVERSITY OF WAH COURSE DESCRIPTION/OBJECTIVES The module aims at building competence in corporate finance further by extending the coverage in Business Finance module to

BBA-330: FINANCIAL MANAGEMENT UNIVERSITY OF WAH COURSE DESCRIPTION/OBJECTIVES The module aims at building competence in corporate finance further by extending the coverage in Business Finance module to

Copyright 2009 Pearson Education Canada

The consequence of failing to adjust the discount rate for the risk implicit in projects is that the firm will accept high-risk projects, which usually have higher IRR due to their high-risk nature, and

The consequence of failing to adjust the discount rate for the risk implicit in projects is that the firm will accept high-risk projects, which usually have higher IRR due to their high-risk nature, and

Chapter 1 The Scope of Corporate Finance

Chapter 1 The Scope of Corporate Finance MULTIPLE CHOICE 1. One of the tasks for financial managers when identifying projects that increase firm value is to identify those projects where a. marginal benefits

Chapter 1 The Scope of Corporate Finance MULTIPLE CHOICE 1. One of the tasks for financial managers when identifying projects that increase firm value is to identify those projects where a. marginal benefits