FINANCIAL LITERACY ACCELERATED MATHEMATICS: CHAPTER 13 TOPICS COVERED:

|

|

|

- Neil Stafford

- 9 years ago

- Views:

Transcription

1 ACCELERATED MATHEMATICS: CHAPTER 13 FINANCIAL LITERACY TOPICS COVERED: Checking and savings accounts Credit and debit cards Balancing a checkbook Credit history and credit reports Saving for college Lifetime incomes of different occupations Simple and compound interest Taxes Budgeting Net Worth

2 Financial Literacy Objectives 6 th grade compare features and costs of a checking account and a debit card distinguish between debit and credit cards balance a check register that includes deposits, withdrawals, and transfers describe the information in a credit report and how long it is retained describe the value of credit reports to borrowers and to lenders explain various methods to pay for college (savings, grants, scholarships, student loans, work-study) compare annual salaries of several occupations various levels of education and calculate the effects of the different annual salaries on lifetime income explain why it is important to establish a positive credit history 7 th grade calculate sales tax for a purchase and calculate income tax for earned wages identify the components of a personal budget including: income, savings for college, retirement and emergencies, taxes AND fixed and variable expenses and calculate what percentage each category comprises of the total budget create and organize assets and liabilities and construct a net worth statement use a family budget estimator to determine the budget and wage needed for a family to meet its basic needs in a Texas city calculate and compare simple interest and compound interest earnings analyze and compare monetary incentives, including sales, rebates, and coupons 8 th grade calculate and compare simple interest and compound interest earnings solve real-world problems comparing how interest rate and loan length affect the cost of credit explain how small amounts of money invested regularly, including money saved for college and retirement, grow over time estimate the cost of a two-year and four-year college education, including family contribution, and devise a savings plan for accumulating the money needed to contribute to the total cost of attendance for at least the first year of college calculate the total cost of repaying a loan, including credit cards and easy access loans using an online calculator * Not tested identify and explain the advantages and disadvantages of different payment methods * Not tested analyze situations to determine if they represent financially responsible decisions and identify the benefits of financial responsibility and the costs of financial responsibility * Not tested

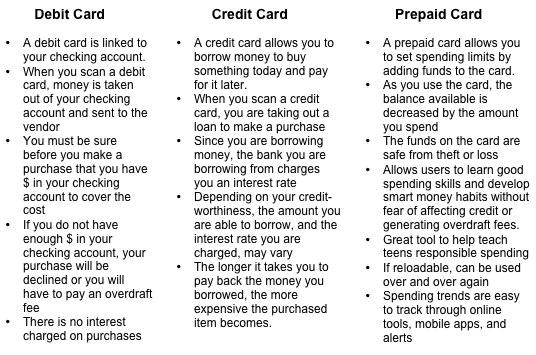

3 Activity 13-1: Bank Accounts A savings account pays interest on the amount of money in the account. A checking account may or may not pay interest, depending on the bank or financial institution. Annual Percentage Yield (APY) is the percentage that is paid to customers based on the account balance in an account for a year. For example, $100 in a savings account at 2% APY will earn $2 at the end of the year. Learning to manage your money is a skill that you will use throughout life. Many different financial institutions offer banking and other financial services, such as savings and investing accounts. Good money management is about three things: earning money, saving money, and borrowing wisely. Financial institutions include banks, credit unions, and savings and loans. Services Checking account, minimum to open, monthly fees Number of free checks per month Interest paid on checking account Mangham Credit Union Underwood Bank Fauatea Savings and Loan $100; $10 monthly fee $150, $5 monthly fee $50; $6 monthly fee No limit $0.10 per check 0.35% No Ten free, $0.15 thereafter 0.4% on balances greater than $500 Debit card No fee No fee No fee ATM fees outside network No fee $2.50 $2.00 Overdraft fee $30 $20 $ Which financial institution has the highest monthly costs for a checking account? Which financial institution has the lowest requirement for opening a checking account? If you wrote 20 checks a month, what fees would you pay to each institution? 4. What is the purpose of a bank?

4

5 Activity 13-2: Bank Accounts A debit card allows customers to withdraw cash from their accounts at an ATM and pay for purchases at stores. A deposit is money added to an account. A withdrawal is money taken out of an account. A transfer moves money from one account to another; for example, from a savings account to a checking account. Most financial institutions offer free debit cards to their customers. A debit card works much like a check in that money is taken from the account to pay for the withdrawal or purchase immediately. While a debit card is usually free, fees may be charged if a withdrawal is made from another bank s ATM, called an out-of-network withdrawal. Services Checking account, minimum to open, monthly fees Number of free checks per month Interest paid on checking account Mangham Credit Union Underwood Bank Fauatea Savings and Loan $100; $10 monthly fee $150, $5 monthly fee $50; $6 monthly fee No limit $0.10 per check 0.35% No Ten free, $0.15 thereafter 0.4% on balances greater than $500 Debit card No fee No fee No fee ATM fees outside network No fee $2.50 $2.00 Overdraft fee $30 $20 $25 1. Which debit card would you be likely to choose? Why? 2. Compare the features of debit cards offered by each financial institution. 3. Overall, which bank would you choose? Why? Most financial institutions allow you to open both a checking and a savings account. You will receive a monthly statement that shows your beginning and ending balances in your accounts. It shows deposits, withdrawals, transfers, and any interest earned. Keeping track of your deposits and withdrawals allows you to avoid writing a check without enough money in the bank. This is known as an overdraft for which banks charge high fees.

6 Activity 13-3: Checks Use the information in the following check register (this is what you would see on a computer program such as Quicken) to calculate the new account balance. Check Number Date Description Check Amount/ Withdrawal Deposit Balance $ March 1 Allowance $ March 8 New shirt $15.00 March 12 FunLand (debit card) $26.75 March 18 Babysitting $24.00 March 21 Transfer to savings $15.00 March 24 ATM withdrawal $ March 28 Lunch $ March 30 New lunchbox $ How many deposits were made in this month? What was the total amount deposited? 2. How many checks were written? What was the total amount? 3. What was the balance at the beginning of the month? At the end? 4. What mathematical operations do you use to balance a check register? 5. If you have a beginning balance of $ and you write checks for $23.50, $12.80, and $97.26, what will be your ending balance? What fees might the bank charge?

7 Activity 13-4: Credit A credit card allows the user to postpone paying for purchases until receiving a monthly bill. A credit report contains a detailed list of a person s credit history prepared by a credit bureau and used by a lender to determine a loan applicant s creditworthiness. Credit cards offer convenience in buying items. For example, you might not have enough cash with you or you want to buy something and pay for it over a period of months. Credit cards, however, can carry high interest rates. You will need to consider the interest you pay as part of the cost of what you re buying. However, if you pay off your total balance each month, there is no interest to pay. Simple interest formula: I = P R T (Interest = Amount Borrowed times Rate times Time) Interest paid each month: I balance interest rate = 12 A credit score is usually a number between 300 and 850. Scores of 700 or higher are considered good. Scores of 580 and lower are poor or very poor. Three nationwide agencies report on consumer credit. Everyone is entitled to a free credit report once a year. Information on the report includes: Public records such as fines or late payments on bills, taxes, etc. Late payments on loans Unpaid credit card payments Accounts in good standing How can a person build a good credit record? Always pay bills on time. Do not borrow or charge more than you can afford. Open a bank account before trying to get a credit card. Have different types of credit such as a cell phone contract, credit card, and bank account. Information on a credit report is usually kept for 7 years. Information on a bankruptcy may be kept longer You have a credit card balance of $188 and you pay annual interest on the unpaid balance of 18%. If you pay $50 on your balance, how much interest will you pay for the next month on the remaining balance? Which of the following would you expect to see on your credit report: Your birth date, the purchases made with a credit card, the amount of the last check you wrote, your math grade, the fact that you missed a credit card payment, your race, your home value, your employment history, you religion, your current address

8 Activity 13-5: Credit Cards Simple interest formula: I = P R T (Interest = Amount Borrowed times Rate times Time) Interest paid each month: I balance interest rate = You make a purchase for $290 on your credit card. You make the minimum payment required each month, $15, to pay off the purchase. At the end of 24 months your payments are complete. How much did you spend on interest? John bought a game system for $350 on his credit card. The system ended up costing him $429. How much interest did John pay? 3. What percentage of the game system price did John pay in interest? Calculate the minimum monthly payment for a credit card with a $400 balance and a 2% minimum payment each month. Calculate the minimum monthly payment for a credit card with a $1200 balance and a 3.5% minimum monthly payment. What is the interest rate for the minimum payment if the balance is $4000 and the minimum payment is $100? Credit cards generally charge between 15% and 22% interest per year. Going back to question #5, how much of the minimum payment is being paid in interest each month? How much of the minimum payment is being paid toward the balance each month? Describe a situation where a consumer might choose to use a credit card responsibly. Describe a situation where a consumer could use a credit card irresponsibly. 11. Describe the advantages and disadvantages of debit cards. 12. Describe the advantages and disadvantages of debit cards.

9 Activity 13-6: Planning for the Future One decision that will probably affect the kind of job you have and how much you earn is whether you go to college. College costs can vary greatly depending on the type of school, such as a public or private college, community college, university, or trade school. There are several ways to help pay for college. Savings Many parents start saving for college when their children are small. Children can also start saving early by putting some of their allowance or cash gifts into savings. Grants and scholarships Grants and scholarships are available from several different sources. The federal government provides Pell grants based on financial need, cost to attend school, and status as a full-time or part-time student. Many are available for students with special talents, such as sports or music. Others are given for high grades. Unlike student loans, grants and scholarships do not have to be repaid. Student loans Like other kids of borrowing, student loans must be paid back, with interest. Work-study Once you are in school, many colleges offer work-study jobs. These jobs can give you experience in a field you are interested in. They may be on campus or in private companies What factors can earn you a grant or scholarship to help pay college costs? Explain the difference between taking out a student loan and paying with savings, work-study, and other options. Assume you are ready for college and you plan to go to a local college while living at home. The annual cost for tuition, fees, and books is $14,500. Also assume that you qualify for a Pell grant of $5,500 and scholarships of $1,500. If the rest of your cost must come from savings, how much savings do you need to pay for your first year? If fees and tuition increase by 4% each year, how much money would you need for four years of college? (Round to the nearest whole dollar.) Assume that you work 12 hours a week through a work-study program and earn $7.50 per hour. How much would you earn per week? 6. How much would you earn for two semesters of 16 weeks each? 7. If you work 12 weeks during the summer and earn $9.50 per hour for a 40 hour week, how much would you earn during the summer?

10

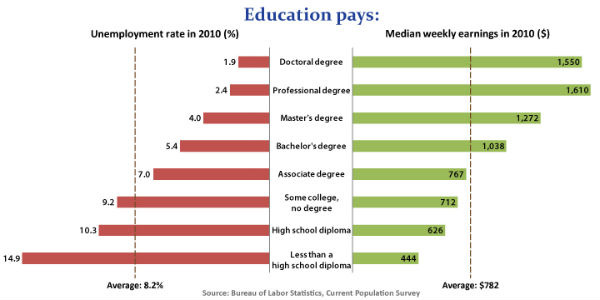

11 Activity 13-7: Different Jobs The table blow shows the median weekly earnings for people with different levels of schooling. Complete the table by determining the increase in weekly income with each additional level of education. Education Level Median Weekly Income Increase Less than a high school diploma $ High school graduate $638 Some college, no diploma $719 Associate degree $768 Bachelor s degree $1053 Master s degree $1263 Doctoral or professional degree $1608 According to the US Census Bureau, someone with a college degree will earn about $1 million more in a lifetime than someone with only a high school diploma. Consider the following statistics: The average total earnings for all people with a bachelor s degree is $2.4 million. Those with a professional degree, such as a doctor or lawyer, may earn about $4 million. Education Level Less than a high school diploma Median Weekly Income $451 High school graduate $638 Some college, no diploma $719 Associate degree $768 Bachelor s degree $1053 Master s degree $1263 Doctoral or professional degree $1608 Median Yearly Income Income over 40 Years 1. What are some reasons that the income of 40 years numbers do not match the average total earnings listed above?

12 Activity 13-8: Different Jobs To become an attorney you need 7 years of school after high school. You can become a paralegal with 2 years of school after high school. The table below shows the annual salaries for the two occupations. Years After High School Occupation Attorney $0 $0 $97,000 $112,000 $129,000 Paralegal $0 $34,000 $40,000 $46,000 $53, Calculate the lifetime incomes for both occupations 12 years after high school. 2. Calculate the lifetime incomes for both occupations 22 year after high school.

13

14 Activity FL1: Interest When you put money into a savings account your money will earn interest. Interest is the amount the bank pays you for using your money and it is usually expressed as a percentage. There are two main types of interest. Simple interest is a percentage that is paid only on the original principal while compound interest is a percentage that is paid on the principal and interest after each time period. Simple interest is simple to calculate, but compound interest is much more commonly used. Principal is the amount of money upon which interest is paid. It is the amount to initially put in the bank. Compare the amount of simple and compound interest in the table below. Describe the rate of increase for each investment option. Describe the shape of each graph if the total value is plotted as a function of time. Time (years) Total Value with Total Value with simple interest ($) compound interest ($) Jose is saving for his son s college education. Calculate the interest earned from $9000 invested for 18 years in an account that earns 3% simple interest. Year 1: What is 3% of $5000? = 270 Jose will make $270 in interest the first year. Year 2: What is 3% of $5000? = 270 Jose will make $270 in interest the second year. We could keep doing this for 18 years and every year he will earn $270 interest. At the end of 18 years he will have the following: Principal = $9000 Interest = $ = $4860 Total = $ $4860 = $13600 Complete the table to determine the total value of $400 invested at 3% for 4 years in a simple interest account. Time (years) Principal invested ($) Interest earned ($) Balance ($) 1 $ I = (400)(0.03)(1) = $12 $ $ I = 3 I = 4 I =

15 Activity FL2: Simple and Compound Interest Principal (p or P) The principal is the amount of money upon which interest is paid. It is the amount of money at the beginning. Annual Rate of Interest (r) The percentage an investor will earn on an investment each year. Interest (I) For the saver, interest is the price a financial institution pays for using a saver s money and is normally expressed as a percentage of the amount saved. Time (t) The amount of time, in years, that the original money will accumulate interest. Simple Interest The amount of interest earned on the principal only. Compound Interest The interest that is earned on the principal and the interest already earned. Compound interest is always better for people that save and invest their money. Savings that earns compound interest will earn more money over a period of time than with simple interest. Just about all interest you will encounter in real-life is compound interest. Simple Interest I = prt This simple interest formula computes the amount of interest at the end of a period of time. Compound Interest A = P(1 + r) t This compound interest formula computes the total amount you would have (principal + interest) at the end of a period of time

16 Activity FL3: Simple and Compound Interest Simple Interest I = prt Compound Interest A = P(1 + r) t 1. Jessica opened a savings account with a one-time deposit of $100 that will be left in the account for 5 years. The savings account will pay 5% simple interest each year. Calculate the amount of interest she will earn in 5 years. I = prt I = (100)(0.05)(5) I = $25 This is the total interest. Add it to the original $100 for a total of $125. You can also see the simple interest each year in the table below. Year Amount to earn interest Interest Rate Interest Earned Ending Balance 1 $100 5% $5 $105 2 $100 5% $5 $110 3 $100 5% $5 $115 4 $100 5% $5 $120 5 $100 5% $5 $125 Total $25 2. Charles opened a savings account with a one-time deposit of $100 that will be left in the account for 5 years. The savings account will pay 5% compound interest each year. Calculate the amount of interest she will earn in 5 years. A = P(1 + r) A = 100( ) A = 100(1.05) A = 100(1.2761) A = $ t 5 t This is the total amount. For just interest, you would subtract the original $100 ($27.61). You can also see the compound interest each year in the table below. Year Amount to earn interest Interest Rate Interest Earned Ending Balance 1 $100 5% $5 $105 2 $105 5% $5.25 $ $ % $5.51 $ $ % $5.78 $ $ % $6.07 $ Total $27.61

17 Activity FL4: Simple and Compound Interest Griffin opened two savings accounts with a one-time deposit of $300 in each account. The first savings account will pay 5% simple interest each year. The second will pay 5% compound interest each year. Use the charts below to calculate the amount of interest he will earn in a 5 year period. 1. SIMPLE INTEREST Year Total Amount to earn interest Interest Rate Interest Earned Ending Balance 2. Complete the formula below to show the total amount of interest earned in #1. I = prt 3. COMPOUND INTEREST Year Total Amount to earn interest Interest Rate Interest Earned Ending Balance (nearest dollar) 4. Complete the formula below to show the total balance at the end of five years of compound interest. A = P(1 + r) t 5. In words, write a comparison of simple interest and compound interest.

18 Activity FL5: Simple and Compound Interest Ella opened two savings accounts with a one-time deposit of $1200 in each account. The first savings account will pay 5% simple interest each year. The second will pay 5% compound interest each year. Use the charts below to calculate the amount of interest she will earn in a 5 year period. 1. SIMPLE INTEREST Year Total Amount to earn interest Interest Rate Interest Earned Ending Balance 2. Complete the formula below to show the total amount of interest earned in #1. I = prt 3. COMPOUND INTEREST Year Total Amount to earn interest Interest Rate Interest Earned Ending Balance (nearest dollar) 4. Complete the formula below to show the total balance at the end of five years of compound interest. A = P(1 + r) t 5. In words, write a comparison of simple interest and compound interest.

19 Activity FL6: Simple and Compound Interest You may use a calculator on this page. If you have savings that earns simple interest the interest earnings are calculated once a year. Remember that the formula for simple interest is I = P r t. 1. Calculate the simple interest on savings of $18,470. Use an annual interest rate of 2.7%. 2. Calculate the simple interest on savings of $9,028 invested for six months at a rate of 3.4%. 3. Analyze the table below which shows the total value over time of $1000 invested in accounts earning 4% interest. What do you notice about simple interest compared to compound interest as the years increase? Number of Years Invested Total Value in Simple Interest 1 $1040 $ $1080 $ $1120 $ $1160 $ $1200 $ $1400 $ $1800 $ $2200 $ Total Value in Compound Interest 4. Use simple interest and compound interest of 3% to compare the earnings on savings of $20,000 invested for two years. 5. Calculate simple interest on $7,000 at 3.2% for a year. 6. Calculate compound interest on $5,400 for 2 years at 4%, compounded annually. 7. Calculate and compare simple interest and compound interest of 5% on the amount of $12,000 for 5 years. 8. Calculate and compare simple and compound interest of 4.2% on savings of $15,000 for 10 years.

20 Activity FL7: Choosing the Better Incentive A monetary incentive is a special offer that reduces the total cost of one or more items, such as buy one, get one free. A coupon is a document offering a reduction in price on a specific item, such as a box of cereal. A rebate is a sales promotion used as an incentive to get buyers to purchase a specific product. When you buy an item on sale or use a discount coupon, you pay less than full price for the item and generally pay tax on the sale price. When you get a rebate, you usually pay full price for the item and the tax on that price, and then get a refund later. Evaluate the pairs of coupons for the eight purchases below and, for each pair, choose the coupon that provides that greater cost savings Book Bag $29.99 (buy one) Snappy Krunch Cereal $2.99 per box (buy three boxes) Super Nutty Peanut Butter 32 oz. jar for $2.56 OR 48 oz. jar for $2.99 (buy two jars of one size) Soccer Shoes $69.95 a pair (buy two pairs) Amusement Park All day admission ticket $45.00 (buy 6 tickets) Scary Movie Festival $8.00 each night for 6 nights (attend all 6 nights) Pizza $18.99 (buy 2 pizzas) Video Game $49.99 (buy 3 games) Coupon 1: 20% off Coupon 2: Save $5.00 Coupon 1: Buy 2, Get 1 Free! Coupon 2: Save $1.50 per box Coupon 1: Buy a 32 oz. jar at regular price, get another free! Coupon 2: Save $0.50 on each 48 oz. jar Coupon 1: Buy one pair, get another at half price! Coupon 2: Two pairs for $ Coupon 1: $5 off each ticket (limit 6) when you buy a case of root beer at $9.99 a case Coupon 2: Buy 5 tickets at regular price, get the 6 th one free Coupon 1: 4 nights at regular price: half price the next 2 nights Coupon 2: 5 nights at regular price 6 th night free Coupon 1: Save $2.00 on each pizza. Limit 2 Coupon 2: Today only 2 pizzas $35.00 Coupon 1: Rebate $14.00 each. Limit two. Coupon 2: Save 20% no limit

21 Activity FL8: Taxes As you get older you will start earning money and paying taxes. Among the three major taxes that many people pay are income taxes, sales taxes, and property taxes. An income tax is a percent of earnings paid to federal, state, or local governments. A sales tax is a percent of the cost of a purchase. A property tax is the percent of the value of the property owned. Suppose a family earns total wages of $800 a week and pays state income taxes of 5% on annual earnings. How much will the family pay as state income tax? Suppose the local government taxes income at 1%. How much additional money will the family pay in taxes to the local government? What amount of money is left after taxes are paid? Below is the 2014 Federal income tax table. In addition to this table people pay Social Security tax, which is 6.2% of earnings up to $113,700. In addition to this table people pay Medicare tax, which is 1.45% on all income. If you (single) had a taxable income of $54,000 a year, what tax bracket would you be in? If you (single) earned $10 an hour, how much would you make for a 40-hour week? A year? What federal income taxes would be withheld? If you (single) has a taxable income of $49,400 a year, what amounts of federal taxes would be withheld? The money that is left after taxes are withheld is called take-home pay. Calculate the income taxes, Social Security taxes, and Medicare taxes you would pay on a taxable income of $54,000. What is the take-home pay?

22 Activity FL9: Calculating Withholding Most workers pay yearly federal income tax based on the wages they earn. Employees deduct money called federal withholding from worker s wages and send it to the federal government as partial payment of the worker s yearly income tax. Each year around April 15 workers submit a federal income tax return. At that time they may owe addition taxes or may get a refund depending on several factors, including the amount already paid through withholding. Net Pay = Gross Pay Total Deductions Robert s gross monthly pay is $2,050. Federal withholding is 11.4% of his gross pay. Find Robert s net pay after all deductions. Find the federal withholding = $2050 x = $ Find the total deductions. Gross Pay $ Tax: Federal withholding $ Tax: Social security $ Tax: Medicare $29.73 Total Deductions $ Net Pay $ Anita s monthly gross pay is $4,200. Federal withholding is 16.5% of her pay. Her other deductions total $ Find her net pay. 2. Juan earns a monthly salary of $3,200. Federal withholding is 14.1% of his gross pay. Juan has a total of $ deducted for Social Security and Medicare. Find his net pay. Which is the better buy? 3. The Corner Store sells 4 bottles of Gatorade for $ The Side Store sells 6 bottles for $ You can buy a 2-pound loaf of bread for $2.50 or a 2-pack of 1.5 pound loaves for $ Maria can buy a 6-pack of 15-ounce cans of broth for $11.29 or three 32-ounce containers for $ JD is buying a pizza that costs $ Should he used a $5 off coupon or a 35% off coupon? 7. MasterCard offers a credit card with an annual fee of $50, but gives you a rebate at the end of the year of 2% of your total purchases. Visa offers a card with no annual fee or rebate. If you spend $150 a month, which card is better for you?

23 Activity FL10: Calculating Income Tax/Budgets Federal income taxes are based on an individual s taxable income. Taxable income is the total amount of income minus deductions. Taxable Income = Gross Income Total Deductions Taxpayers may take a standard deduction set by the IRS or they may itemize deductions such as property taxes or medical expenses. Income tax is the product of the tax rate and the taxable income. Many taxpayers use a tax table provided by the IRS. John s taxable income is $26,318. John has already paid $4,059 in federal withholding. Use the tax table to find the amount of tax owed on $26,318. Then compare the tax due with the tax withheld to determine whether he will have to pay an additional amount or will get a refund. If line 43 (taxable income is - And you are single, At least But less than your tax is Glenda s taxable income is $26,222. She paid $2,640 in federal withholding. Find the tax due on Glenda s income. Then tell whether she will have to pay an additional amount or will get a refund. Use the tax table above. 2. Liz s taxable income is $26,380. She paid $2,940 in federal withholding. Determine whether she will have to pay an additional amount or will get a refund. Use the tax table above. Identifying components of a personal budget Income the money you earn Expenses the money you spend Income is added to the total amount available and expenses are subtracted from the total amount available. Expenses include planned savings for college, retirement, emergencies, and taxes. Expenses can be fixed or variable. Fixed expenses, such as car and house payments, occur regularly and do not change from month to month. Variable expenses, such as purchases of food and gas, occurs regularly and is necessary for living, but you have some control over the amount. Which of these would be fixed expenses? Snacks, weekly flute lesson, saving for a new flute, entertainment, savings for college, monthly bus pass Mr. Underwood has a net monthly income of $4,000. If he allocates 5% of his money to an emergency fund, how much goes to the fund each month? How much goes to clothing if he spends 8% of his money on clothing? What percentage is allocated to housing if he pays $1,400 for his mortgage each month?

24 Activity FL11: Budget Many people create a budget to manage current income and expenses, while also planning ahead for long-term financial goals. A budget is an estimate of expected income and expenses. A fixed expense is one that does not change over a period time. A variable expense occurs regularly and is necessary, but you have some control over the amount. Monthly Budget Income (annual take home pay of $64,646) Salary/wages (take-home pay) 5388 Other (bank account interest) 60 Total monthly income 5448 Expenses Housing (mortgage/rent) % F Property tax 385 F Insurance (home, car, life) 200 F Food 970 V Utilities (water, gas, electricity) 230 V Cell phones 128 F Cable/internet 145 F Gasoline 210 V Child care 400 F Pet expenses 0 V Credit card charges 410 V Entertainment costs 300 V Gifts/charities 100 V Other 0 V Total expenses 4558 Savings Emergency fund 100 Retirement savings 340 College savings 450 Total savings 890 Fixed/Variable 1. What is the amount of total monthly income? 2. What is the amount of total expenses? 3. For each expense calculate its percentage of total expenses. Round to the nearest whole percent. 4. Which expenses take up the largest share of the budget? 5. What percentage of total take-home pay is saved by this family?

25 Activity FL12: Budget A family budget is a financial plan based on the amount of money needed to live. In general, the total family income must meet or exceed the total family expenses. The number of children, employment benefits such as insurance, and where the family lives all affect the budget. Below is an example of the minimum monthly expenses for the Jones family, who live in Beaumont. There are two parents and two children. Jones Family s Monthly Expenses Description Expenses in Beaumont ($) Housing $697 Expenses in Dallas-FW-Arlington ($) Food $731 Child Care $548 Medical Costs $508 Transportation $494 Other Necessities $309 Total Monthly Expenses $3,287 Federal Taxes $285 Federal Tax Credits (-$267) Total Monthly Income Needed $3,591 Household Hourly Wage $16 Living in different parts of the country or state can mean different budgets for even the same family. The Jones family is considering a move to the Dallas-Ft. Worth area. Use to complete the table for the Dallas expenses. Remember it is a family of 4. Assume their employer pays part of their premium and that they are saving for emergencies, retirement, and college.

26 Activity FL13: Net Worth Net worth is the difference between what is owned and what is owed. Assets are items owned. They include a house, a car, savings, and investments. Liabilities are amounts owed. They include a mortgage, credit card debt, and any other loans. Net Worth of Katniss Everdeen Assets House 238,000 General savings 48,000 College fund 28,000 Retirement fund 72,000 Total assets $386,000 Liabilities Mortgage owed 110,000 Credit card debt 1,800 Balance on student loans 23,000 Equity loan for home improvement 25,000 Total liabilities $159,800 NET WORTH $226, Calculate the net worth of someone with assets of $198,000 and liabilities of $154, What is the value of assets if someone has a net worth of $142,500 and liabilities of $87,400? 3. What is the value of liabilities if total assets are $204,800 and net worth is $128,900? Determine whether each item is an asset or a liability. Money in checking Credit cards Savings Student loans Investments Retirement money Car loans Mortgage Home equity loan Vehicles Your home Personal loans Mr. Mangham s accounts are shown below: Checking account: $2876 Student loan: $9560 Credit card: $ (k) account: $14,432 Car loan: $18,680 Savings account: $5500 Place Mr. Mangham s account into the table below and determine Mr. Mangham s net worth. Assets Liabilities Type Amount Type Amount TOTAL Net Worth TOTAL

27 Activity FL14: Net Worth Assets are things you own. They have a positive cash value. Examples of assets are goods that are paid for and owned, such as houses, cars or bicycles, positive bank accounts, and savings bonds. Liabilities are debts you owe. They have a negative cash value. Examples of liabilities are car loans, house mortgages, credit card debt, or student loans. The Johnsen family has two adults and two young children. Both parents work full-time jobs; one child is in day care all day and the other child is in first grade and in after-school care. They own a house and two cars and carry some credit card debt. Complete a net worth statement for this family. Remember that not all monthly expenses are liabilities. The house is valued at $95,000 with a mortgage balance of $45,000. First car is worth $12,000. The family owes $5,000 on their auto loan. Second car is worth $10,000 which is paid in full. Child care costs are $600 per month. Retirement accounts are valued at $15,000. Balance on credit cards total $2,000. Checking account has a balance of $500. Savings account has a balance of $1,200. They have $75 in cash. The value of their furniture is approximately $4,500 which is paid in full. The miscellaneous household items are valued at $1,200 which is paid in full. Mrs. Johnsen s jewelry is valued at $900; this was paid with her credit card and is included above. Assets Liabilities Type Amount Type Amount TOTAL Net Worth TOTAL

28 Activity FL15: Credit Cards 1. What is the minimum payment for this statement? 2. How does this credit card statement show financial responsibility by the credit card holder? 3. What is the Annual Percentage Rate (APR) for purchases? 4. What is the new balance? 5. What is the previous balance? 6. How many charges were made during the billing cycle? 7. How many payments were made during this billing cycle? 8. What is the total amount of the credit line? 9. What is the total amount of available credit? 10. What is the Annual Percentage Rate (APR) for cash advances? 11. What is the date for the next payment?

29 Activity FL16: Saving for College Saving for college or retirement are long-term goals for many people. To help determine a savings plan, it is important to know approximately what your college costs will be or the amount of money you will need for retirement. Both require regular savings and wise money management. Choose four schools you think you might like to attend. One two-year school, such as a community college One four-year public, state-supported university in Texas One four-year public, state-supported university outside Texas One private college or university Research the estimated costs for tuition, room and board, and other expenses at each of the three schools. Then make a plan for at least your first year. When researching online you may want to include College Board as part of your search as they have information you may find useful in estimating costs. COSTS Tuition Room/board Other/fees Totals Two-year college Texas public university Out-of-state public university Private college

Personal Financial Literacy

Personal Financial Literacy 7 Unit Overview Being financially literate means taking responsibility for learning how to manage your money. In this unit, you will learn about banking services that can help

Personal Financial Literacy 7 Unit Overview Being financially literate means taking responsibility for learning how to manage your money. In this unit, you will learn about banking services that can help

Lesson Description. Texas Essential Knowledge and Skills (Target standards) Skills (Prerequisite standards) National Standards (Supporting standards)

Skills (Prerequisite standards) National Standards (Supporting standards)") Lesson Description The students are presented with real life situations in which young people have to make important decisions about their future. Students use an online tool to examine how the cost of

Lesson Description The students are presented with real life situations in which young people have to make important decisions about their future. Students use an online tool to examine how the cost of

It Is In Your Interest

STUDENT MODULE 7.2 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. It Is In Your Interest Jason did not understand how it

STUDENT MODULE 7.2 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. It Is In Your Interest Jason did not understand how it

Using Credit. SSEPF4.a, SSEPF4.b, SSEPF4.c

Using Credit SSEPF4.a, SSEPF4.b, SSEPF4.c Loans and Credit Cards: Buy Now, Pay Later The U.S. economy runs on credit. Credit The ability to obtain goods now, based on an agreement to pay for them later.

Using Credit SSEPF4.a, SSEPF4.b, SSEPF4.c Loans and Credit Cards: Buy Now, Pay Later The U.S. economy runs on credit. Credit The ability to obtain goods now, based on an agreement to pay for them later.

It s Your Paycheck! Glossary of Terms

Annual percentage rate The percentage cost of credit on an annual basis and the total cost of credit to the consumer. APR combines the interest paid over the life of the loan and all fees that are paid

Annual percentage rate The percentage cost of credit on an annual basis and the total cost of credit to the consumer. APR combines the interest paid over the life of the loan and all fees that are paid

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account.

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account. Account fee the amount charged by a financial institution for the

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account. Account fee the amount charged by a financial institution for the

BUILD A SOLID CREDIT HISTORY

BUILD A SOLID CREDIT HISTORY WHAT IS CREDIT? Credit is money that you borrow, usually in the form of a credit card or loan, with the promise to pay it back. Why is it important to have good credit? There

BUILD A SOLID CREDIT HISTORY WHAT IS CREDIT? Credit is money that you borrow, usually in the form of a credit card or loan, with the promise to pay it back. Why is it important to have good credit? There

Chapter Objectives. Chapter 6. Short Term Credit Management. Major Topics. Reasons for Using Credit. How to Get Credit. Disadvantages of Using Credit

Chapter Objectives Chapter 6. Short Term Credit Management To evaluate reasons for and against using credit and decide whether or not credit is appropriate for you. To be able to take the necessary steps

Chapter Objectives Chapter 6. Short Term Credit Management To evaluate reasons for and against using credit and decide whether or not credit is appropriate for you. To be able to take the necessary steps

Students will devise a savings plan for college.

Lesson Description Students will analyze data to determine the relationship between level of educational attainment and weekly earnings and the relationship between level of educational attainment and

Lesson Description Students will analyze data to determine the relationship between level of educational attainment and weekly earnings and the relationship between level of educational attainment and

Lesson Description. Texas Essential Knowledge and Skills (Target standards) Texas Essential Knowledge and Skills (Prerequisite standards)

Texas Essential Knowledge and Skills (Prerequisite standards)") Lesson Description This lesson gives students the opportunity to explore the different methods a consumer can pay for goods and services. Students first identify something they want to purchase. They then

Lesson Description This lesson gives students the opportunity to explore the different methods a consumer can pay for goods and services. Students first identify something they want to purchase. They then

Housing Opportunities for Native Americans & Alaska Natives NativeNatives

Housing Opportunities for Native Americans & Alaska Natives NativeNatives The Section 184 Indian Home Loan Guarantee program is a home loan product for federally recognized tribal members, tribes, and

Housing Opportunities for Native Americans & Alaska Natives NativeNatives The Section 184 Indian Home Loan Guarantee program is a home loan product for federally recognized tribal members, tribes, and

William D. Ford Federal Direct Loan Program Direct PLUS Loan Borrower s Rights and Responsibilities Statement

Important Notice: This Borrower s Rights and Responsibilities Statement provides additional information about the terms and conditions of the loans you receive under the accompanying Federal Direct PLUS

Important Notice: This Borrower s Rights and Responsibilities Statement provides additional information about the terms and conditions of the loans you receive under the accompanying Federal Direct PLUS

Promoting the Health and Well-Being of Families During Difficult Times. Family Financial Management Planning for the Future

Promoting the Health and Well-Being of Families During Difficult Times Family Financial Management Planning for the Future DenYelle Baete Kenyon, Doctoral Student, Lynne M. Borden, Extension Specialist

Promoting the Health and Well-Being of Families During Difficult Times Family Financial Management Planning for the Future DenYelle Baete Kenyon, Doctoral Student, Lynne M. Borden, Extension Specialist

NetEffect. Serving the Financial Needs of Healthcare Providers. First Mortgage Home Loans We ll Make Sure You Get The Right One To Fit Your Needs

www.healthnetfcu.org Main Office: 1591 Chickering Ln. Cordova, TN 38016 Fax: (901) 226-1122 Walnut Grove Branch: 6025 Walnut Grove Suite 612 Memphis, TN 38120 Fax: (901) 762-0001 Southaven Branch: 84 Airways

www.healthnetfcu.org Main Office: 1591 Chickering Ln. Cordova, TN 38016 Fax: (901) 226-1122 Walnut Grove Branch: 6025 Walnut Grove Suite 612 Memphis, TN 38120 Fax: (901) 762-0001 Southaven Branch: 84 Airways

Open-Ended Problem-Solving Projections

MATHEMATICS Open-Ended Problem-Solving Projections Organized by TEKS Categories TEKSING TOWARD STAAR 2014 GRADE 7 PROJECTION MASTERS for PROBLEM-SOLVING OVERVIEW The Projection Masters for Problem-Solving

MATHEMATICS Open-Ended Problem-Solving Projections Organized by TEKS Categories TEKSING TOWARD STAAR 2014 GRADE 7 PROJECTION MASTERS for PROBLEM-SOLVING OVERVIEW The Projection Masters for Problem-Solving

SERVICES w w w. c o v e n a n t b a n k. c o m

SERVICES w w w. c o v e n a n t b a n k. c o m Mission To improve the quality of life for our citizens, businesses, shareholders, and the community through distinctive banking and financial services. Vision

SERVICES w w w. c o v e n a n t b a n k. c o m Mission To improve the quality of life for our citizens, businesses, shareholders, and the community through distinctive banking and financial services. Vision

Understanding Vehicle Financing

Understanding Vehicle Financing Understanding Vehicle Financing With prices averaging more than $31,000 for a new vehicle and $17,000 for a used model from a dealership, you might consider financing or

Understanding Vehicle Financing Understanding Vehicle Financing With prices averaging more than $31,000 for a new vehicle and $17,000 for a used model from a dealership, you might consider financing or

Personal Finance. Mao Ding & Tara Hansen

Personal Finance Mao Ding & Tara Hansen Banking Accounts Checking Account Checking account is either zero interest or very low interest bearing Checking account can have infinitely many transactions No

Personal Finance Mao Ding & Tara Hansen Banking Accounts Checking Account Checking account is either zero interest or very low interest bearing Checking account can have infinitely many transactions No

Financial Planning. Introduction. Learning Objectives

Financial Planning Introduction Financial Planning Learning Objectives Lesson 1 Budgeting: How to Live on Your Own and Not Move Home in a Week Prepare a budget and determine disposable income. Identify

Financial Planning Introduction Financial Planning Learning Objectives Lesson 1 Budgeting: How to Live on Your Own and Not Move Home in a Week Prepare a budget and determine disposable income. Identify

6.15.1.7 Describe and use the steps involved in the banking reconciliation process

ND BUSINESS EDUCATION FRAMEWORKS Financial Literacy Course Code Course Name/Course Description Grade Levels Accreditation Time/Credit Options 14095 Financial Literacy is designed to help students understand

ND BUSINESS EDUCATION FRAMEWORKS Financial Literacy Course Code Course Name/Course Description Grade Levels Accreditation Time/Credit Options 14095 Financial Literacy is designed to help students understand

Chapter 07 Interest Rates and Present Value

Chapter 07 Interest Rates and Present Value Multiple Choice Questions 1. The percentage of a balance that a borrower must pay a lender is called the a. Inflation rate b. Usury rate C. Interest rate d.

Chapter 07 Interest Rates and Present Value Multiple Choice Questions 1. The percentage of a balance that a borrower must pay a lender is called the a. Inflation rate b. Usury rate C. Interest rate d.

THE ABC S OF VEHICLE FINANCING CURRICULUM. Counting Your Money

Counting Your Money Section Objectives Counting your money and managing your money wisely is the most important part of your trip on the road to personal financial success. It is a critical step in achieving

Counting Your Money Section Objectives Counting your money and managing your money wisely is the most important part of your trip on the road to personal financial success. It is a critical step in achieving

1Planning Your Financial Future: It Begins Here

This sample chapter is for review purposes only. Copyright The Goodheart-Willcox Co., Inc. All rights reserved. 1Planning Your Financial Future: It Begins Here Terms Financial plan Financial goals Needs

This sample chapter is for review purposes only. Copyright The Goodheart-Willcox Co., Inc. All rights reserved. 1Planning Your Financial Future: It Begins Here Terms Financial plan Financial goals Needs

Home HOW TO BUY A WITH A LOW DOWN PAYMENT 3 % A consumer s guide to owning a home with less than three percent down. or less

A consumer s guide to owning a home with less than three percent down. 3 % WITH A LOW DOWN PAYMENT or less HOW TO BUY A Home If you re dreaming of buying a home, congratulations. You re in good company!

A consumer s guide to owning a home with less than three percent down. 3 % WITH A LOW DOWN PAYMENT or less HOW TO BUY A Home If you re dreaming of buying a home, congratulations. You re in good company!

Ohio s Learning Standards Financial Literacy Model Curriculum

Ohio s Standards Financial Literacy Model Curriculum Theme Financial literacy is defined as the ability to read, analyze, manage and communicate about the personal financial conditions that affect material

Ohio s Standards Financial Literacy Model Curriculum Theme Financial literacy is defined as the ability to read, analyze, manage and communicate about the personal financial conditions that affect material

PERSONAL FINANCIAL STATEMENT

PERSONAL FINANCIAL STATEMENT As of, 20 BUSINESS PLAN GUIDELINES Name: Residence Phone: Residence Address: City, State, Zip Code: Social Security Number: PERSONAL ASSETS PERSONAL LIABILITIES Cash in Bank

PERSONAL FINANCIAL STATEMENT As of, 20 BUSINESS PLAN GUIDELINES Name: Residence Phone: Residence Address: City, State, Zip Code: Social Security Number: PERSONAL ASSETS PERSONAL LIABILITIES Cash in Bank

Lesson Description. Texas Essential Knowledge and Skills (Target standards) Skills (Prerequisite standards) National Standards (Supporting standards)

Skills (Prerequisite standards) National Standards (Supporting standards)") Lesson Description Students will analyze families finances to identify assets and liabilities. They will use this information to calculate the families net worth and learn the benefits of having a positive

Lesson Description Students will analyze families finances to identify assets and liabilities. They will use this information to calculate the families net worth and learn the benefits of having a positive

NEFE High School Financial Planning Program Unit Two Budgeting: Making the Most of Your Money. Unit 4 - Budgeting: Making the Most of Your Money

Unit 4 - Budgeting: Making the Most of Your Money ? 2-A-1 Chart Recommendations Housing 30% Food 20% Clothing 10% Transportation 10% Savings 10% Misc. 20% 2-A-2 2-B-1 1 2 3 Some Money Facts The average

Unit 4 - Budgeting: Making the Most of Your Money ? 2-A-1 Chart Recommendations Housing 30% Food 20% Clothing 10% Transportation 10% Savings 10% Misc. 20% 2-A-2 2-B-1 1 2 3 Some Money Facts The average

Overview. Develop a plan Understand financial aid Be a responsible borrower Take charge of credit cards Understand your credit Prevent identity theft

Lisa Croat and Andrea Clark Lunch provided by the Higher One Financial Literacy Counts Grant Overview Develop a plan Understand financial aid Be a responsible borrower Take charge of credit cards Understand

Lisa Croat and Andrea Clark Lunch provided by the Higher One Financial Literacy Counts Grant Overview Develop a plan Understand financial aid Be a responsible borrower Take charge of credit cards Understand

Your Student Loan Record

Your Student Loan Record STUDENT LOAN RECORD There are lots of people ready to help with information about your student loans, if you need it Ombudsman: 1-877-557-2575 or www.ombudsman.ed.gov National

Your Student Loan Record STUDENT LOAN RECORD There are lots of people ready to help with information about your student loans, if you need it Ombudsman: 1-877-557-2575 or www.ombudsman.ed.gov National

What You ll Learn. And Why. Key Words. interest simple interest principal amount compound interest compounding period present value future value

What You ll Learn To solve problems involving compound interest and to research and compare various savings and investment options And Why Knowing how to save and invest the money you earn will help you

What You ll Learn To solve problems involving compound interest and to research and compare various savings and investment options And Why Knowing how to save and invest the money you earn will help you

MATHEMATICS Grade 6 2015 Released Test Questions

MATHEMATICS Grade 6 d Test Questions Copyright 2015, Texas Education Agency. All rights reserved. Reproduction of all or portions of this work is prohibited without express written permission from the

MATHEMATICS Grade 6 d Test Questions Copyright 2015, Texas Education Agency. All rights reserved. Reproduction of all or portions of this work is prohibited without express written permission from the

Maureen Baran SVP Business Development. Kris Bona Business Relationship Officer

Williams College Maureen Baran SVP Business Development Kris Bona Business Relationship Officer Agenda What is credit and why is it so important? Credit reports and credit scores Building credit Comparing

Williams College Maureen Baran SVP Business Development Kris Bona Business Relationship Officer Agenda What is credit and why is it so important? Credit reports and credit scores Building credit Comparing

Understanding Credit Personal Management Merit Badge

Understanding Credit Personal Management Merit Badge Kelsey Balcaitis Youth Financial Education Coordinator Class Rules Leave No Trace Wear your uniform to class A Scout is Trustworthy, Loyal, Helpful,

Understanding Credit Personal Management Merit Badge Kelsey Balcaitis Youth Financial Education Coordinator Class Rules Leave No Trace Wear your uniform to class A Scout is Trustworthy, Loyal, Helpful,

CLAT. At the end of the term of the trust, the remaining assets pass to the donor s heirs, spouse, or sometimes back to the donor, if living.

Charitable Lead Annuity Trust CLAT In General A donor may transfer assets to an irrevocable charitable lead annuity trust (CLAT). The trust then pays a fixed dollar amount to a qualified charity for either

Charitable Lead Annuity Trust CLAT In General A donor may transfer assets to an irrevocable charitable lead annuity trust (CLAT). The trust then pays a fixed dollar amount to a qualified charity for either

Accounts payable Money which you owe to an individual or business for goods or services that have been received but not yet paid for.

A Account A record of a business transaction. A contract arrangement, written or unwritten, to purchase and take delivery with payment to be made later as arranged. Accounts payable Money which you owe

A Account A record of a business transaction. A contract arrangement, written or unwritten, to purchase and take delivery with payment to be made later as arranged. Accounts payable Money which you owe

Lesson 13 Take Control of Debt: Become a Savvy Borrower

Lesson 13 Take Control of Debt: Become a Savvy Borrower Lesson Description After reviewing the difference between term loans and revolving credit, students analyze a fictitious character s use of credit

Lesson 13 Take Control of Debt: Become a Savvy Borrower Lesson Description After reviewing the difference between term loans and revolving credit, students analyze a fictitious character s use of credit

www.refugees.org Protecting Refugees, Serving Immigrants, Upholding Freedom since 1911 BANKING ON THE FUTURE

U.S. COMMITTEE FOR REFUGEES AND IMMIGRANTS www.refugees.org Protecting Refugees, Serving Immigrants, Upholding Freedom since 1911 BANKING ON THE FUTURE BANKING ON THE FUTURE A FINANCIAL LITERACY CURRICULUM

U.S. COMMITTEE FOR REFUGEES AND IMMIGRANTS www.refugees.org Protecting Refugees, Serving Immigrants, Upholding Freedom since 1911 BANKING ON THE FUTURE BANKING ON THE FUTURE A FINANCIAL LITERACY CURRICULUM

CARDMEMBER AGREEMENT AND DISCLOSURE STATEMENT

CARDMEMBER AGREEMENT AND DISCLOSURE STATEMENT Part 1 of 2: Agreement About this Agreement Part 1 and 2 together make your Cardmember Agreement and Disclosure Statement ( Agreement ) and govern your Credit

CARDMEMBER AGREEMENT AND DISCLOSURE STATEMENT Part 1 of 2: Agreement About this Agreement Part 1 and 2 together make your Cardmember Agreement and Disclosure Statement ( Agreement ) and govern your Credit

Borrowing Money Standard 7 Assessment

1 Name: Class Period: Borrowing Money Directions: Match each description in the column below with the CORRECT term from the list. Write the letter of the term in the space provided. A. Interest B. Interest

1 Name: Class Period: Borrowing Money Directions: Match each description in the column below with the CORRECT term from the list. Write the letter of the term in the space provided. A. Interest B. Interest

5.1 Simple and Compound Interest

5.1 Simple and Compound Interest Question 1: What is simple interest? Question 2: What is compound interest? Question 3: What is an effective interest rate? Question 4: What is continuous compound interest?

5.1 Simple and Compound Interest Question 1: What is simple interest? Question 2: What is compound interest? Question 3: What is an effective interest rate? Question 4: What is continuous compound interest?

Section 8.1. I. Percent per hundred

1 Section 8.1 I. Percent per hundred a. Fractions to Percents: 1. Write the fraction as an improper fraction 2. Divide the numerator by the denominator 3. Multiply by 100 (Move the decimal two times Right)

1 Section 8.1 I. Percent per hundred a. Fractions to Percents: 1. Write the fraction as an improper fraction 2. Divide the numerator by the denominator 3. Multiply by 100 (Move the decimal two times Right)

Control Debt Use Credit Wisely

Lesson 10 Control Debt Use Credit Wisely Lesson Description In this lesson, students, through a series of interactive and group activities, will explore the concept of credit and the impact of liabilities

Lesson 10 Control Debt Use Credit Wisely Lesson Description In this lesson, students, through a series of interactive and group activities, will explore the concept of credit and the impact of liabilities

Comparing Simple and Compound Interest

Comparing Simple and Compound Interest GRADE 11 In this lesson, students compare various savings and investment vehicles by calculating simple and compound interest. Prerequisite knowledge: Students should

Comparing Simple and Compound Interest GRADE 11 In this lesson, students compare various savings and investment vehicles by calculating simple and compound interest. Prerequisite knowledge: Students should

ICASL - Business School Programme

ICASL - Business School Programme Quantitative Techniques for Business (Module 3) Financial Mathematics TUTORIAL 2A This chapter deals with problems related to investing money or capital in a business

ICASL - Business School Programme Quantitative Techniques for Business (Module 3) Financial Mathematics TUTORIAL 2A This chapter deals with problems related to investing money or capital in a business

Money Math for Teens. Opportunity Costs

Money Math for Teens This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education Foundation, Channel One

Money Math for Teens This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education Foundation, Channel One

A GUIDE TO PERSONAL BUDGETING

When it comes to improving your overall finances and economic wellbeing, there is nothing more important than knowing where your money is coming from and how you spend your income. The best way to attain

When it comes to improving your overall finances and economic wellbeing, there is nothing more important than knowing where your money is coming from and how you spend your income. The best way to attain

One Stop Shop For Educators Performance Task for Unit #6 Let s Make It Personal Enduring understanding: Interdependency: Incentives:

The following instructional plan is part of a GaDOE collection of Unit Frameworks, Performance Tasks, examples of Student Work, and Teacher Commentary for the Economics Course. Performance Task for Unit

The following instructional plan is part of a GaDOE collection of Unit Frameworks, Performance Tasks, examples of Student Work, and Teacher Commentary for the Economics Course. Performance Task for Unit

Being a Wise Borrower: The Importance of Managing Your Money

B2. Being a Wise Borrower: The Importance of Managing Your Money Introduction This lesson will help guide students through the process of borrowing and managing money in a responsible way so they are prepared

B2. Being a Wise Borrower: The Importance of Managing Your Money Introduction This lesson will help guide students through the process of borrowing and managing money in a responsible way so they are prepared

Understanding the Student Loan Explosion. Implications for students and their families. Sponsored by:

Understanding the Student Loan Explosion Implications for students and their families Sponsored by: Understanding the Student Loan Explosion: Implications for students and their families True wisdom is

Understanding the Student Loan Explosion Implications for students and their families Sponsored by: Understanding the Student Loan Explosion: Implications for students and their families True wisdom is

Opening a bank account

Section 6 - Money4_7_Layout 1 10/01/2011 11:42 Page 124 Money Section 6 Opening a bank account 125 Borrowing money 127 Budgeting and managing your money 129 124 Money Opening a bank account Opening a bank

Section 6 - Money4_7_Layout 1 10/01/2011 11:42 Page 124 Money Section 6 Opening a bank account 125 Borrowing money 127 Budgeting and managing your money 129 124 Money Opening a bank account Opening a bank

Building Your Future A Student and Teacher Resource for Financial Literacy Education

Building Your Future A Student and Teacher Resource for Financial Literacy Education Copyright 2009, 2011 The Actuarial Foundation About This Book Personal finance is part knowledge and part skill and

Building Your Future A Student and Teacher Resource for Financial Literacy Education Copyright 2009, 2011 The Actuarial Foundation About This Book Personal finance is part knowledge and part skill and

Name (Partner A): Name (Partner B): Address: Phone number:

: Name (Partner B): Address: Phone number:") Suze Orman - The Ultimate Protection Portfolio What Your Financial Advisor Must Ask You or You Must Ask if the Advisor is You 2003 Suze Orman Revocable Trust Name (Partner A): Name (Partner B): Address:

Suze Orman - The Ultimate Protection Portfolio What Your Financial Advisor Must Ask You or You Must Ask if the Advisor is You 2003 Suze Orman Revocable Trust Name (Partner A): Name (Partner B): Address:

You will be introduced to careers that are available in the Accounting and Finance Pathway.

In this unit you will discover ways to apply sound decision-making skills, discover stable saving and spending habits, and practice using bank accounts to manage your money. You will be introduced to careers

In this unit you will discover ways to apply sound decision-making skills, discover stable saving and spending habits, and practice using bank accounts to manage your money. You will be introduced to careers

Checking Account Overdraft Agreement

Checking Account Overdraft Agreement Account Name Account Number Share # This Overdraft Agreement ("Agreement") describes the circumstances when we (the Credit Union) will pay overdrafts in your checking

Checking Account Overdraft Agreement Account Name Account Number Share # This Overdraft Agreement ("Agreement") describes the circumstances when we (the Credit Union) will pay overdrafts in your checking

Helpful Information for a First Time Mortgage

Helpful Information for a First Time Mortgage Getting Started Many people buying their first home are afraid lenders don't really want to work with them. But that's simply not true. Without you, there

Helpful Information for a First Time Mortgage Getting Started Many people buying their first home are afraid lenders don't really want to work with them. But that's simply not true. Without you, there

Diving Into Spending Plans Grade Level 7-9

2.15.1 Diving Into Spending Plans Grade Level 7-9 Get Ready to Take Charge of Your Finances Time to complete: 60 minutes National Content Standards Family and Consumer Science Standards: 1.1.6, 2.1.1,

2.15.1 Diving Into Spending Plans Grade Level 7-9 Get Ready to Take Charge of Your Finances Time to complete: 60 minutes National Content Standards Family and Consumer Science Standards: 1.1.6, 2.1.1,

Lesson 8 Save and Invest: The Rise and Fall of Risk and Return

Lesson 8 Save and Invest: The Rise and Fall of Risk and Return Lesson Description This lesson begins with a brainstorming session in which students identify the risks involved in playing sports or driving

Lesson 8 Save and Invest: The Rise and Fall of Risk and Return Lesson Description This lesson begins with a brainstorming session in which students identify the risks involved in playing sports or driving

GCSE Business Studies. Ratios. For first teaching from September 2009 For first award in Summer 2011

GCSE Business Studies Ratios For first teaching from September 2009 For first award in Summer 2011 Ratios At the end of this unit students should be able to: Interpret and analyse final accounts and balance

GCSE Business Studies Ratios For first teaching from September 2009 For first award in Summer 2011 Ratios At the end of this unit students should be able to: Interpret and analyse final accounts and balance

Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money.

TEACHER GUIDE 7.2 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. It Is In Your Interest Priority Academic Student Skills

TEACHER GUIDE 7.2 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. It Is In Your Interest Priority Academic Student Skills

account statement a record of transactions in an account at a financial institution, usually provided each month

GLOSSARY GLOSSARY Following are definitions for key words as they are used in the financial life skills resource. They may have different or additional meanings in other contexts. A account an arrangement

GLOSSARY GLOSSARY Following are definitions for key words as they are used in the financial life skills resource. They may have different or additional meanings in other contexts. A account an arrangement

lesson three budgeting your money teacher s guide

lesson three budgeting your money teacher s guide budgeting your money lesson outline lesson 3 overview I m all out of money, and I won t get paid again until the end of next week! This is a common dilemma

lesson three budgeting your money teacher s guide budgeting your money lesson outline lesson 3 overview I m all out of money, and I won t get paid again until the end of next week! This is a common dilemma

Why rent when you can buy?

Why rent when you can buy? Are you unsure about becoming a HOMEOWNER? Thinking that you can t afford to BUY a home? Are you worried about whether homebuying is a good INVESTMENT? Buying a first home can

Why rent when you can buy? Are you unsure about becoming a HOMEOWNER? Thinking that you can t afford to BUY a home? Are you worried about whether homebuying is a good INVESTMENT? Buying a first home can

A financial statement captures a person s overall wealth at a specific point in time. In this lesson, students will:

PROJECT 3 CASH FLOW AND BALANCE SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

PROJECT 3 CASH FLOW AND BALANCE SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

A financial statement captures a person s overall wealth at a specific point in time. In this lesson, students will:

PROJECT 3 CASH FLOW AND BALANC E SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

PROJECT 3 CASH FLOW AND BALANC E SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

Welcome to Broward HealthCare Federal Credit Union

Welcome to Broward HealthCare Federal Credit Union what is a credit union? Credit Unions are member-owned cooperatives; in fact, that s why savings in a credit union are technically called shares. Unlike

Welcome to Broward HealthCare Federal Credit Union what is a credit union? Credit Unions are member-owned cooperatives; in fact, that s why savings in a credit union are technically called shares. Unlike

ONTARIO Court File Number. Form 13: Financial Statement (Support Claims) sworn/affirmed. Applicant(s) Respondent(s)

sworn/affirmed. Applicant(s) Respondent(s)") ONTARIO Court File Number at (Name of Court) Court office address Form 13: Financial Statement (Support Claims) sworn/affirmed Applicant(s) Full legal name & address for service street & number, municipality,

ONTARIO Court File Number at (Name of Court) Court office address Form 13: Financial Statement (Support Claims) sworn/affirmed Applicant(s) Full legal name & address for service street & number, municipality,

2. In solving percent problems with a proportion, use the following pattern:

HFCC Learning Lab PERCENT WORD PROBLEMS Arithmetic - 11 Many percent problems can be solved using a proportion. In order to use this method, you should be familiar with the following ideas about percent:

HFCC Learning Lab PERCENT WORD PROBLEMS Arithmetic - 11 Many percent problems can be solved using a proportion. In order to use this method, you should be familiar with the following ideas about percent:

Investigating Investment Formulas Using Recursion Grade 11

Ohio Standards Connection Patterns, Functions and Algebra Benchmark C Use recursive functions to model and solve problems; e.g., home mortgages, annuities. Indicator 1 Identify and describe problem situations

Ohio Standards Connection Patterns, Functions and Algebra Benchmark C Use recursive functions to model and solve problems; e.g., home mortgages, annuities. Indicator 1 Identify and describe problem situations

14 ARITHMETIC OF FINANCE

4 ARITHMETI OF FINANE Introduction Definitions Present Value of a Future Amount Perpetuity - Growing Perpetuity Annuities ompounding Agreement ontinuous ompounding - Lump Sum - Annuity ompounding Magic?

4 ARITHMETI OF FINANE Introduction Definitions Present Value of a Future Amount Perpetuity - Growing Perpetuity Annuities ompounding Agreement ontinuous ompounding - Lump Sum - Annuity ompounding Magic?

How Does Money Grow Over Time?

How Does Money Grow Over Time? Suggested Grade & Mastery Level High School all levels Suggested Time 45-50 minutes Teacher Background Interest refers to the amount you earn on the money you put to work

How Does Money Grow Over Time? Suggested Grade & Mastery Level High School all levels Suggested Time 45-50 minutes Teacher Background Interest refers to the amount you earn on the money you put to work

CHAPTER 5. Interest Rates. Chapter Synopsis

CHAPTER 5 Interest Rates Chapter Synopsis 5.1 Interest Rate Quotes and Adjustments Interest rates can compound more than once per year, such as monthly or semiannually. An annual percentage rate (APR)

CHAPTER 5 Interest Rates Chapter Synopsis 5.1 Interest Rate Quotes and Adjustments Interest rates can compound more than once per year, such as monthly or semiannually. An annual percentage rate (APR)

CHAPTER 10 Financial Statements NOTE

NOTE In practice, accruals accounts and prepayments accounts are implied rather than drawn up. It is common for expense accounts to show simply a balance c/d and a balance b/d. The accrual or prepayment

NOTE In practice, accruals accounts and prepayments accounts are implied rather than drawn up. It is common for expense accounts to show simply a balance c/d and a balance b/d. The accrual or prepayment

Your Money Matters! Financial Literacy Teacher Guide. Thanks to TD for helping us bring this resource to schools for free.

Your Money Matters! Financial Literacy Teacher Guide 2 Table of Contents: Introduction...3 Toronto Star epaper...4 Financial Awareness Inventory...5 SPENDING To Spend or Not to Spend Activity...6 I Need

Your Money Matters! Financial Literacy Teacher Guide 2 Table of Contents: Introduction...3 Toronto Star epaper...4 Financial Awareness Inventory...5 SPENDING To Spend or Not to Spend Activity...6 I Need

Chapter 22: Borrowings Models

October 21, 2013 Last Time The Consumer Price Index Real Growth The Consumer Price index The official measure of inflation is the Consumer Price Index (CPI) which is the determined by the Bureau of Labor

October 21, 2013 Last Time The Consumer Price Index Real Growth The Consumer Price index The official measure of inflation is the Consumer Price Index (CPI) which is the determined by the Bureau of Labor

Assist. Financial Calculators. Technology Solutions. About Our Financial Calculators. Benefits of Financial Calculators. Getting Answers.

Assist. Financial s Technology Solutions. About Our Financial s. Helping members with their financial planning should be a key function of every credit union s website. At Technology Solutions, we provide

Assist. Financial s Technology Solutions. About Our Financial s. Helping members with their financial planning should be a key function of every credit union s website. At Technology Solutions, we provide

Personal Finance Standards (Assignment Code #22210)

") Personal Finance Standards (Assignment Code #22210) Rationale Statement: A citizen that lives within his or her income has more control over his or her life while expanding choices. Having the knowledge

Personal Finance Standards (Assignment Code #22210) Rationale Statement: A citizen that lives within his or her income has more control over his or her life while expanding choices. Having the knowledge

Adding and Subtracting

Positive and Negative Integers 1 A 7 th Grade Unit on Adding and Subtracting Positive and Negative Integers Developed by: Nicole Getman December 1, 2006 Buffalo State: I 2 T 2 Positive and Negative Integers

Positive and Negative Integers 1 A 7 th Grade Unit on Adding and Subtracting Positive and Negative Integers Developed by: Nicole Getman December 1, 2006 Buffalo State: I 2 T 2 Positive and Negative Integers

How to Inform a Debt Collector You Are Collection-Proof

How to Inform a Debt Collector You Are Collection-Proof Note: Use these instructions and letter to inform a creditor or debt collector that they cannot use a court judgment to make you pay a debt, because

How to Inform a Debt Collector You Are Collection-Proof Note: Use these instructions and letter to inform a creditor or debt collector that they cannot use a court judgment to make you pay a debt, because

Jump$tart Coalition for Personal Financial Literacy. Goodheart-Willcox Foundations of Personal Finance 2014 by Sally Campbell and Robert Dansby

Jump$tart Coalition for Personal Financial Literacy correlation of standards with Goodheart-Willcox Foundations of Personal Finance 2014 by Sally Campbell and Robert Dansby This chart correlates the performance

Jump$tart Coalition for Personal Financial Literacy correlation of standards with Goodheart-Willcox Foundations of Personal Finance 2014 by Sally Campbell and Robert Dansby This chart correlates the performance

Lesson 9: To Rent-to-Own or Not to Rent-to-Own?

All About Credit Lesson 9: To Rent-to-Own or Not to Rent-to-Own? Standards and Benchmarks (see page C-61) Lesson Description Students review the elements of a contract. They discuss the characteristics

All About Credit Lesson 9: To Rent-to-Own or Not to Rent-to-Own? Standards and Benchmarks (see page C-61) Lesson Description Students review the elements of a contract. They discuss the characteristics

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. Find the present value for the given future amount. Round to the nearest cent. 1) A = $4900,

Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. Find the present value for the given future amount. Round to the nearest cent. 1) A = $4900,

JA BizTown Vocabulary

JA BizTown Vocabulary Unit 1 Community and Economy Citizen A member of a town, city, country, state or country. Community A place where people live, work, trade and share. Trade Exchange of goods and services,

JA BizTown Vocabulary Unit 1 Community and Economy Citizen A member of a town, city, country, state or country. Community A place where people live, work, trade and share. Trade Exchange of goods and services,

Total Monthly Income $ Miscellaneous Income Royalties, Trusts, and Other Investments $ Contributions from Others $ Dependent Children s monthly gross

District Court Denver Juvenile Court County, Colorado Court Address: In re: The Marriage of: The Civil Union of: Parental Responsibilities concerning: Petitioner: and Co-Petitioner/Respondent: Attorney

District Court Denver Juvenile Court County, Colorado Court Address: In re: The Marriage of: The Civil Union of: Parental Responsibilities concerning: Petitioner: and Co-Petitioner/Respondent: Attorney

MGF 1107 Spring 11 Ref: 606977 Review for Exam 2. Write as a percent. 1) 3.1 1) Write as a decimal. 4) 60% 4) 5) 0.085% 5)

3.1 1) Write as a decimal. 4) 60% 4) 5) 0.085% 5)") MGF 1107 Spring 11 Ref: 606977 Review for Exam 2 Mr. Guillen Exam 2 will be on 03/02/11 and covers the following sections: 8.1, 8.2, 8.3, 8.4, 8.5, 8.6. Write as a percent. 1) 3.1 1) 2) 1 8 2) 3) 7 4 3)

MGF 1107 Spring 11 Ref: 606977 Review for Exam 2 Mr. Guillen Exam 2 will be on 03/02/11 and covers the following sections: 8.1, 8.2, 8.3, 8.4, 8.5, 8.6. Write as a percent. 1) 3.1 1) 2) 1 8 2) 3) 7 4 3)

Finite Mathematics. CHAPTER 6 Finance. Helene Payne. 6.1. Interest. savings account. bond. mortgage loan. auto loan

Finite Mathematics Helene Payne CHAPTER 6 Finance 6.1. Interest savings account bond mortgage loan auto loan Lender Borrower Interest: Fee charged by the lender to the borrower. Principal or Present Value:

Finite Mathematics Helene Payne CHAPTER 6 Finance 6.1. Interest savings account bond mortgage loan auto loan Lender Borrower Interest: Fee charged by the lender to the borrower. Principal or Present Value:

Budgeting and debt advice handbook for residents

Budgeting and debt advice handbook for residents Step-by-step guide Contents Introduction...................... 3 Income maximisation List your income Can you increase your income? Income..........................

Budgeting and debt advice handbook for residents Step-by-step guide Contents Introduction...................... 3 Income maximisation List your income Can you increase your income? Income..........................

Glossary of Accounting Terms