ORSA Overall Solvency Needs and Implementation within the European Market

|

|

|

- Thomas Atkinson

- 7 years ago

- Views:

Transcription

1 ORSA Overall Solvency Needs and Implementation within the European Market Sam Morgan Principal Hong Kong 1

2 Contents Introduction Risk appetite and the overall solvency needs Selection of risk factors Definition of the scenarios Link with risk tolerance Conclusions 2

3 Contents Introduction Risk appetite and the overall solvency needs Selection of risk factors Definition of the scenarios Link with risk tolerance Conclusions 3

4 Introduction Over the past decade there have been a focus on Risk Based Capital around the world Solvency II in Europe RBC in Singapore C-ROSS in China One of the common features of each of these frameworks, is the concept of an ORSA Own Risk Solvency Assessment The concept is fairly straight forward The regulatory capital requirement, although Risk Based, is sometime a little blunt Companies need to understand all the risks that they are exposed to and integrate this into the risk management procedures Contains both quantitative and qualitative elements An ORSA report, signed off by senior management and containing the risk management procedures and analyses, is provided to the regulator The implementation however faces a number of technical issues This presentation outlines how companies have responded to these issues in the context of Solvency II in Europe 4

5 Introduction A brief introduction to Solvency II The Solvency II capital requirement is based on a the following fundamental principal The capital required today to ensure with a 99.5% probability that the company will not be in economic ruin over the next year Probability of Economic Ruin < 99.5% Current Available Capital Net Asset Value Economic ruin is defined as the situation where Net Asset Value = MV Assets - Fair Value of Liabilities <= 0 5

6 Introduction A brief introduction to Solvency II To calculate the fair value of liabilities, we need to perform an economic valuation of the liabilities : Risk neutral, "Market consistent valuation Explicit valuation of time value of embedded options and guarantees Requires stochastic simulations to define calculate a single point on the curve Therefore, in its purest form, should use some nested stochastic to find the 99.5% percentile 6

7 Introduction A brief introduction to Solvency II To avoid the nested stochastic requirement, the standard formula is set up such that Each of the risk capital charges are calculated as the difference between the NAV before shock and the NAV after shock (noting that each calculation is a stochastic calculation) The total SCR (Solvency Capital Requirement) is the aggregation of these individual risk charges Calculation of individual risk charge Aggregation of individual risk charges into total SCR - = 7

8 Introduction An introduction to ORSA within Solvency II Article 45 of the Solvency II directive states : As part of its risk-management system every insurance undertaking and reinsurance undertaking shall conduct its own risk and solvency assessment. That assessment shall include at least the following: (a) the overall solvency needs taking into account the specific risk profile, approved risk tolerance limits and the business strategy of the undertaking; (b) the compliance, on a continuous basis, with the capital requirements and with the requirements regarding technical provisions; (c) the significance with which the risk profile of the undertaking concerned deviates from the assumptions underlying the Solvency Capital Requirement In addition, the ORSA guidelines gives the following guidelines related to the overall solvency needs Guideline 8 : The undertaking should express the overall solvency needs in quantitative terms and complement the quantification by a qualitative description of the risks. Guideline 9 : The undertaking should subject the identified risks to a sufficiently wide range of stress test/scenario analyses to provide an adequate basis for the assessment of the overall solvency needs. Guideline 10 : The undertaking s assessment of the overall solvency needs should be forward-looking and at least cover separately each year of the business planning period. Guideline 14 : The undertaking should take the results of the ORSA and the insights gained in the process into account at least for the system of governance including long term capital management, business planning and product development and design. 8

9 Introduction An introduction to ORSA within Solvency II The overall solvency needs is the strategic solvency indicator at the heart of the risk management and decision making of the business Reflects the internally defined risk appetite Includes all risks, including those not included the regulatory capital calculation, and on a wider basis than the standard formula, most notably including future new business Contains a forward looking component covering the horizon of the business plan including capital management and future capital needs The key indicator when making strategic decisions within the company (eg. modification of the asset allocation, launching a new product, purchase of a new portfolio, ) Is used in the risk tolerance framework 9

10 Introduction An introduction to ORSA within Solvency II An expression of the company s global risk framework Breakdown of risk appetite into elements actionable by business line managers Expressed in the form of risk budgets and / or risk limits Covers continuous compliance requirement Internally defined measure reflecting the risk appetite Includes all material risks Forward looking Covers not just regulatory capital but a wider vision (ie. stressed scenarios) 10

11 Contents Introduction Risk appetite and the overall solvency needs Selection of risk factors Definition of the scenarios Link with risk tolerance Conclusions 11

12 Risk appetite and the overall solvency needs The definition of the overall solvency needs is the key quantitative element mentioned in Article 45 of the Solvency II Directive. It is based on a risk appetite which transfers the key aim of the insurer; this could be for example : To always be a going concern even after the impact of certain pre-defined adverse events 100 % coverage of the regulatory capital ; To conserve a sufficient rating after these same adverse events solvency ratio as a % of the regulatory requirement depends on the target rating Rating AA A BBB BB Equivalent solvency ratio 200 % 175 % 120 % < 100 % etc. Furthermore, two possible target levels can be considered : A target of X1 % in the case of a «central» scenario; A target of X2 % in the case of adverse events, the probability of which is to be defined. 12

13 Risk appetite and the overall solvency needs The definition of the risk appetite will usually take the following form : «a level of capital sufficient to maintain the available capital greater than X% of the internal capital requirement after the realisation of a scenario cumulating adverse events over a specific time horizon». The elements that need to be defined : Internal capital requirement : can include additional risks or be recalibrated to a different confidence level. Most commonly uses the regulatory requirement as this is the key driver in the management of the business and becomes difficult to create the link between the regulatory capital and the internal capital The use of Internal model or standard formula capital depends on the company situation Time horizon : length, method of application Definition of adverse events : risks covered, definition of amplitude and combination of shocks 13

14 Risk appetite and the overall solvency needs The elements that need to be defined (cont d) : X% : the impact of different choice s of X : Definition of the target level of solvency Target of X% where X is close to the initial solvency ratio Target of X% where X is far from the initial solvency ratio, possibly even <100% Advantages Ability to show a high solvency ratio, even after stress Ability to include relatively onerous stress tests. Disadvantages Risk being constrained in the definition of the scenarios > construction of a less useful risk framework If X < 100%, ORSA framework not coherent with the regulatory requirements Also depends on the value of X before shock => if the initial solvency ratio is low, no point in testing large stresses that give a solvency ratio < 100% of regulatory capital 14

15 Risk appetite and the overall solvency needs Some examples Example 1 : Risk appetite statement Available Capital > Target Capital Excess Capital Where Target Capital = Required Capital + Buffer Capital Required Capital = Max ( Regulatory capital, Internal Model (RBC) capital, Internal Rating Regulatory Required Buffer Target Available Rating Agencies) Model agencies model capital capital capital capital Buffer capital = Example 2 : Risk Appetite statement Capital required to be 90% sure that the available capital remains Available above Capital the required > X% capital internal (alternatively, model capital the 90% VaR of the required capital) And stresses defined as : Where X = Equity drop: Market values of all equity investments drop by 25%. Limit 1 Limit 2 Interest rates up: Parallel shift in yield curves by 250 bps up. Base case 140% 100% Interest rates down: Parallel shift in yield curves by 200 bps down. Credit: Operating entity specific 1-in-15 year credit event. Stresses * 130% 100% Combined scenario: Drop in market values of all equity investments by 10% and parallel shift in yield curves by 80 bps up. Limit 1 : Continuous monitoring when breached Limit 2 : Action must be taken when breached 15

16 Risk appetite and the overall solvency needs The overall solvency needs covers only one of the key strategic axes of the company => its solvency. Additional Key Risk Indicators will be included in the ORSA projections to help in making any business decisions : Profitability, based on the projected profits; Commercial performance, by looking at the credited rate for interest sensitive policies (in the case of a life company) ; Operational performance, based on the combined ratio or expense ratio ; Etc.. 16

17 Risk appetite and the overall solvency needs Benchmark (1/2) Bancassurer 1 Bancassurer 2 Traditional insurer Mutual Specialist insurer Reinsurer 1 International Group Bancassurer 3 Reinsurer 2 Solvency Profits Profitability (ROE, ) Bonus strategy Market Consistent Embedded Value (MCEV) Embedded Value with risk premium (real world) Rating 17

18 Risk appetite and the overall solvency needs Benchmark (1/2) Examples Profit / Profitability Maximum reduction in the IFRS profit Minimum constraints on the return on equity Minimum constraints on Return on Risk adjusted capital (IFRS Profit / SCR VIF) Risk Adjusted Return On Risk Adjusted Capital : MCEV / (PV projected SII capital requirement) Profitability must be > 3 month risk free rate + X basis points Maximum reduction in cumulative 5 year accounting profit Bonus strategy Impact within the scenarios on the future bonus rates and the bonus fund Capacity to pay a bonus rate > minimum level with a probability of X% Embedded Value (MC & RW) Maximum reduction of 30% Minimum level of Embedded value 18 18

19 Contents Introduction Risk appetite and the overall solvency needs Selection of risk factors Definition of the scenarios Link with risk tolerance Conclusions 19

20 Selection of risk factors Introduction The identification of risk factors is a key step in the ORSA process for those insurers using the standard formula for the calculation of their economic capital For those insurers that are using an internal model, this should have already been undertaken during the regulatory approval process For these insurers, the identification of risk factors should be summarised into the following: Cat. 1: Material risk AND included in the SCR calculation. Shocks on the risk factor in the ORSA calculations : Regulatory capital requirement : yes, in the case of future SCR or SCR after shock ; Stress scenarios : Yes, in order to calculate the capital after shocks or in the projections. Cat. 3 : Material risk BUT not in the SCR calculation. Shocks on the risk factor in the ORSA calculations : XRegulatory capital requirement : non, no change to the regulatory requirement within the projections ; Stress scenarios: yes, these risks specific to the insurer should be included in the shock or in the projections to ensure risk being adequately accounted for Cat. 2 : Non material risk BUT included in the SCR calculations. Shocks on the risk factor in the ORSA calculations :?Regulatory capital requirement : Yes, if a full calculation is being done, but might not be necessary if proxies are being used for projected SCR; XStress scenarios : non, do not want to unnecessarily to complicate the ORSA process. Cat. 4: Non material risk AND not included in the SCR calculation. Shocks on the risk factor in the ORSA calculations : XRegulatory capital requirement : non, no change to the regulatory requirement within the projections ; XStress scenarios : non, do not want to unnecessarily to complicate the ORSA process. 20

21 Selection of risk factors Risk mapping and quantification In Europe, the Solvency II standard formula has provided a very good starting point for the analysis of the risk Most of the major risks are already included All risks are considered to be evaluated on a consistent basis - at the 99.5% confidence level Some key risks not covered by the Solvency II standard formula Risks covered by the Solvency II standard formula 21 The identification of additional risks is primarily achieved through interviews with key stakeholders and decision makers across the business These risks should be evaluated on an equivalent basis to the standard formula (99.5%) Some risks not covered by the Solvency II standard formula European Sovereign risk : No capital charge is applied to European government bonds Volatility risk : Increased volatility has impacts on the economic balance sheet of the insurers Basis risk : primarily for VA writers Catastrophe Risk : specific forms outside of SF Liquidity risk Regulatory risk Reputation risk Strategic Risk Some risks are only evaluated using a qualitative framework

22 Selection of risk factors Classification of risks Each of the risks must be classified as material or not Between Category 1 and Category 2 for risks included in Standard Formula Between Category 3 and Category 4 for other risks Definition of materiality limits Fixed materiality limits can create volatility in the list of material risks Over time, between entities Usually aim to have an upper and lower limits and use expert judgment to classify risk between the two levels Upper materiality limit Lower materiality limit Material risk Use of expert judgment Non material risk 22

23 Contents Introduction Risk appetite and the overall solvency needs Selection of risk factors Definition of the scenarios Link with risk tolerance Conclusions 23

24 Definition of the scenarios Key concepts The calibration and composition of the scenarios should provide the ability to test the future solvency of the company in a number of realistic but varied stress scenarios. The calibration of the scenarios is based on the (i) selected risk measure and the (ii) intensity of the shocks being considered The composition of the scenarios gives the capacity to test multi-directional shocks in order to take into account the expected correlations between the risk factors 24

25 Definition of the scenarios Objective or Understandable? Trade-off between Objective versus Understandable nature of the scenarios Realistic scenarios can be constructed in three different manners : Simulation of past crises (for example, the tech crash in 2000, the subprime crisis, the property bubble crash in Japan, the Asian currency crisis ) Simulations of dreaded events which are linked to the economic situation or geopolitical situation (break up of the Eurozone, break out of war in Ukraine, continuation of political crisis in Thailand, ) ; Definition of scenarios based on percentiles (use of historical analysis to determine percentiles for individual risk levels). + Graphical representation of the trade-off between Objective / Understandable - Dread events Simulation of pas crises Understandable - Shocks based on percentiles Objective + 25

26 Definition of the scenarios Objective or Understandable? Trade-off between Objective versus Understandable nature of the scenarios (cont d) Some additional elements that must be considered when deciding on the appropriateness of the different approaches presented previously : Simulations of past crises Easy to understand, but only takes into account risks that have already occurred but doesn t take into account any new risks in the future (will history always repeat itself?) Dreaded events It is difficult to estimate the impact of the dreaded event on each of the risk factors ie. How are the correlations going to react? Shocks based on percentiles Need to dispose of a sufficiently long history of data points (the higher the percentile, the deeper the history that is needed) ; Where the risk factor or the history of data available makes an evaluation of the percentile impossible, need to turn to expert judgment -> ultimately, removes much of the objectivity of the scenarios. Can perform reverse stress tests -> illustration by «understandable» scenarios shocks that are initially based on percentiles 26

27 Definition of the scenarios Countercyclical scenarios A feature of Solvency II is that as the market conditions worsen, the capital position itself worsens, and vice, versa creating significant volatility in the regulatory solvency ratio of the company. A key objective of many insurers is to make the overall solvency needs capital less volatility than the SCR, a an often criticised feature of Solvency II. This can be done through the definition of the scenarios that take into account the relative position in the business cycle countercyclical scenarios 27

28 Definition of the scenarios Countercyclical scenarios example 1 : equity shock The equity scenario for the ORSA will be based on a «central» shock plus a cyclical adjustment factor : Step 1 : Calculation of the central shock The level of shock is based on the based on the relevant percentile as per the risk tolerance of the company The following table gives the example of the distribution of the MSCI Europe, assuming a normal distribution of the log returns based on a historic between 1973 and 2009 : Step 2 : Calculation of the adjustment factor Percentile 99.5% 99.0% 95% 90% Level of shock -43% -38% -25% -18% The adjustment factor is based on the current position of the index versus the average position of the index over the previous 3 or 5 years (corrected for the expected growth in the index) Current index above average index : adjustment factor is positive Expected growth line Current index below average index : adjustment factor is negative 28

29 Definition of the scenarios Countercyclical scenarios example 1 : equity shock 29

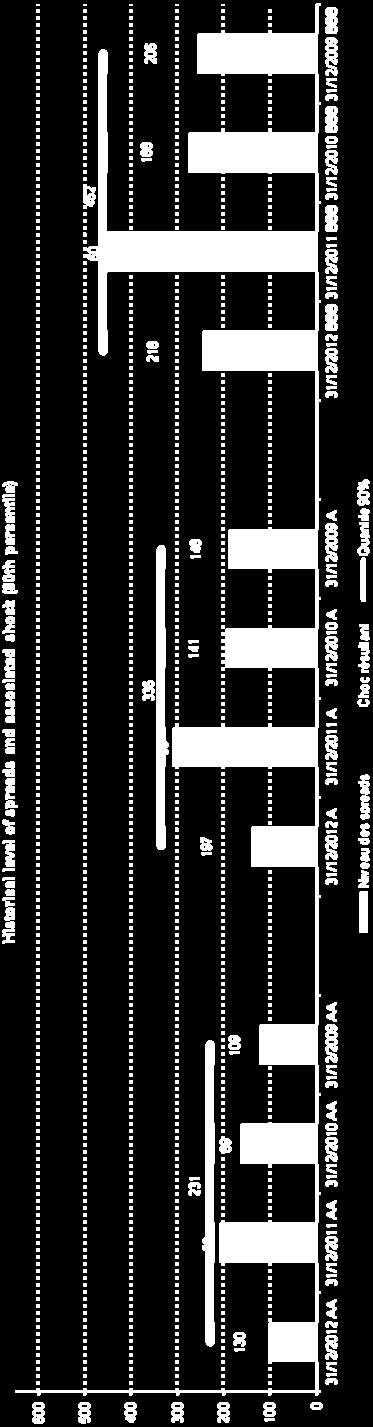

30 Definition of the scenarios Countercyclical scenarios example 2 : spread shock For certain financial risks, the counter cyclical effects can be of a different nature to the symmetrical adjustment, most notably for the spread shock. Example of how this can be implemented : 1/ Calculation of the absolute level of spread for each rating «AAA», «AA», «A», «BBB», for the percentiles 99%, 90% or 95% based on the historical level of a bond index (Markitt or other) ; 2/ The level of shock to be considered in the ORSA, is the absolute level of the shock at the percentile level in question less the current level of the spread. 2 bis/ In order to take into account particular cases, an absolute minimum shock equal to 50 basis points is applied. The following slides contain a numerical example of the, based on the iboxx index over the period

31 Definition of the scenarios Countercyclical scenarios example 2 : spread shock Absolute level of spread for corporate obligations at the different percentiles In bps AA A BBB 99.5% % % % Current end of year spreads for the period 2009 to 2012 En bps AA A BBB 31/12/ /12/ /12/ /12/ = Calibration of the shocks 95th Percentile En bps AA A BBB 31/12/ /12/ /12/ /12/ th percentile En bps AA A BBB 31/12/ /12/ /12/ /12/

32 Definition of the scenarios Countercyclical scenarios example 2 : spread shock 32

33 Definition of the scenarios Completeness All risk factors identified as material should be considered during the calculation of the ORSA capital Each risk from Category 1 or Category 3 should be included in at least one stress scenario. In order to define the ORSA capital based on a reasonable number of scenarios, it seems necessary to combine several shocks on different factors into the same scenario. The risk factors can be combined into a realistic scenario taking into account the existing interactions : Shocks based on percentiles : In combined scenarios, the marginal percentiles needs to be reduced such that the resulting scenario corresponds to the target percentile => a non-reduction will lead to overestimation of the overall combined scenario The simulation of past crises or dreaded events should, in themselves, be based on a combination multiple financial and / or technical shocks. 33

34 Definition of the scenarios Completeness combining scenarios A very simplified approach : Percentile of a normal distribution Assumption : The intensity of the shock follows approximately a normal distribution ( standard formula) The shocks can be correlated amongst themselves. The intensity of the combination of several shocks also follows a normal distribution but with different parameters ; A reduced percentile can be deduced based on the initial percentile for each of the individual shocks Number of risk factors included in the shocks Reduced percentile shocks Assumption : 0% correlation between the risk factors Reduced percentile shocks Assumption : 50% correlation between the risk factors 1 risk factors shocked 95% 95% 2 risk factors shocked 88% 92% 3 risk factors shocked 83% 91% 4 risk factors shocked 79% 90% 5 risk factors shocked 77% 90%!! Method is based on two strong assumptions : -The volatility of each individual risk not taken into account; -Impact of individual risk on capital not accounted for. 34

35 Contents Introduction Risk appetite and the overall solvency needs Selection of risk factors Definition of the scenarios Link with risk tolerance Conclusions 35

36 The link with risk tolerance The risk appetite gives the minimum level of excess capital that the entity / group wishes to maintain at any moment. In order ensure this, you cannot simply determine a posteriori at certain time intervals; on the contrary, an approach a priori must be used, that is to anticipate all future deviations of the risk profile which would bring about a non respect of the overall solvency needs capital requirement. Therefore, an operational framework for risk tolerance must be implemented. From a practical perspective, this framework should provide the risk takers with a set of tools to help them measure the impact of any decision on the ORSA solvency of the group and therefore validate or reject that decision 36

37 The link with risk tolerance The risk tolerance framework should meet the following criteria Risk tolerance framework 1. Fix limits that are both understandable and actionable by the risk takers 2. Give the possibility to the risk takers to know their position with respect to the limit at any time 3. Anticipate the change in the position with respect to the limit when considering a possible decision Two approaches have been developed to answer this question Risk tolerance framework Approach 1 Implementation and monitoring a risk budget framework Approach 2 Implementation and monitoring a series of risk limits 37

38 The link with risk tolerance In the risk limit approach, the aim is to fix a minimum / maximum level for each of the parameters that are in the hands of the risk taker: Example for financial risks : minimum level of Govt Bonds in the portfolio, maximum level of equity maximum concentration on a single issuer. Advantages Very easy to understand whereby the framework is based on the parameters in the hands of the risk taker (e.g. : equity asset mix) Disadvantages Gives little room for movement to the risk takers, especially in the case of risk mitigation techniques (by either reinsurance or derivatives) In the risk budget approach, simply a minimum level of ORSA surplus will be defined: Advantages Very wide latitude given to the risk taker : as long as the surplus remains over the defined limit, the risk taker can modify their decision as they desire Disadvantages System significantly less understandable : the notion of surplus is not directly related to the operational decisions => tools must be provided to risk taker to facilitate decision making 38

39 Contents Introduction Risk appetite and the overall solvency needs Selection of risk factors Definition of the scenarios Link with risk tolerance Conclusions 39

40 Conclusion An expression of the company s global risk framework «a level of capital sufficient to maintain the available capital greater than X% of the internal capital requirement after the realisation of a scenario cumulating adverse events over a specific time horizon». Breakdown of risk appetite into elements actionable by business line managers Expressed in the form of risk budgets and / or risk limits Covers continuous compliance requirement Internally defined measure reflecting the risk appetite Includes all material risks Forward looking Covers not just regulatory capital but a wider vision (ie. stressed scenarios) 40

Capital Management in a Solvency II World & the Role of Reinsurance

Capital Management in a Solvency II World & the Role of Reinsurance Paolo de Martin CEO SCOR Global Life IAA Colloquium Oslo June 2015 Overview Why I Focus today on Capital Management? Reminder key objectives

Capital Management in a Solvency II World & the Role of Reinsurance Paolo de Martin CEO SCOR Global Life IAA Colloquium Oslo June 2015 Overview Why I Focus today on Capital Management? Reminder key objectives

Solvency II: Implications for Loss Reserving

Solvency II: Implications for Loss Reserving John Charles Doug Collins CLRS: 12 September 2006 Agenda Solvency II Introduction Pre-emptive adopters Solvency II concepts Quantitative Impact Studies Internal

Solvency II: Implications for Loss Reserving John Charles Doug Collins CLRS: 12 September 2006 Agenda Solvency II Introduction Pre-emptive adopters Solvency II concepts Quantitative Impact Studies Internal

Standard Life plc. Solvency II and capital insight session

Standard Life plc Solvency II and capital insight session This presentation may contain certain forward-looking statements with respect to certain of Standard Life's plans and its current goals and expectations

Standard Life plc Solvency II and capital insight session This presentation may contain certain forward-looking statements with respect to certain of Standard Life's plans and its current goals and expectations

Solvency II for Beginners 16.05.2013

Solvency II for Beginners 16.05.2013 Agenda Why has Solvency II been created? Structure of Solvency II The Solvency II Balance Sheet Pillar II & III Aspects Where are we now? Solvency II & Actuaries Why

Solvency II for Beginners 16.05.2013 Agenda Why has Solvency II been created? Structure of Solvency II The Solvency II Balance Sheet Pillar II & III Aspects Where are we now? Solvency II & Actuaries Why

International Financial Reporting for Insurers: IFRS and U.S. GAAP September 2009 Session 25: Solvency II vs. IFRS

International Financial Reporting for Insurers: IFRS and U.S. GAAP September 2009 Session 25: Solvency II vs. IFRS Simon Walpole Solvency II Simon Walpole Solvency II Agenda Introduction to Solvency II

International Financial Reporting for Insurers: IFRS and U.S. GAAP September 2009 Session 25: Solvency II vs. IFRS Simon Walpole Solvency II Simon Walpole Solvency II Agenda Introduction to Solvency II

INVESTMENT FUNDS: Funds investments. KPMG Business DialogueS November 4 th 2011

INVESTMENT FUNDS: Impact of Solvency II Directive on Funds investments KPMG Business DialogueS November 4 th 2011 Map of the presentation Introduction The first consequences for asset managers and investors

INVESTMENT FUNDS: Impact of Solvency II Directive on Funds investments KPMG Business DialogueS November 4 th 2011 Map of the presentation Introduction The first consequences for asset managers and investors

This section outlines the Solvency II requirements for a syndicate s own risk and solvency assessment (ORSA).

.") Section 9: ORSA Overview This section outlines the Solvency II requirements for a syndicate s own risk and solvency assessment (ORSA). The ORSA can be defined as the entirety of the processes and procedures

Section 9: ORSA Overview This section outlines the Solvency II requirements for a syndicate s own risk and solvency assessment (ORSA). The ORSA can be defined as the entirety of the processes and procedures

Society of Actuaries in Ireland

Society of Actuaries in Ireland Information and Assistance Note LA-1: Actuaries involved in the Own Risk & Solvency Assessment (ORSA) under Solvency II Life Assurance and Life Reinsurance Business Issued

Society of Actuaries in Ireland Information and Assistance Note LA-1: Actuaries involved in the Own Risk & Solvency Assessment (ORSA) under Solvency II Life Assurance and Life Reinsurance Business Issued

The package of measures to avoid artificial volatility and pro-cyclicality

The package of measures to avoid artificial volatility and pro-cyclicality Explanation of the measures and the need to include them in the Solvency II framework Contents 1. Key messages 2. Why the package

The package of measures to avoid artificial volatility and pro-cyclicality Explanation of the measures and the need to include them in the Solvency II framework Contents 1. Key messages 2. Why the package

ERM-2: Introduction to Economic Capital Modeling

ERM-2: Introduction to Economic Capital Modeling 2011 Casualty Loss Reserve Seminar, Las Vegas, NV A presentation by François Morin September 15, 2011 2011 Towers Watson. All rights reserved. INTRODUCTION

ERM-2: Introduction to Economic Capital Modeling 2011 Casualty Loss Reserve Seminar, Las Vegas, NV A presentation by François Morin September 15, 2011 2011 Towers Watson. All rights reserved. INTRODUCTION

Bank Capital Adequacy under Basel III

Bank Capital Adequacy under Basel III Objectives The overall goal of this two-day workshop is to provide participants with an understanding of how capital is regulated under Basel II and III and appreciate

Bank Capital Adequacy under Basel III Objectives The overall goal of this two-day workshop is to provide participants with an understanding of how capital is regulated under Basel II and III and appreciate

Embedded Value 2014 Report

Embedded Value 2014 Report Manulife Financial Corporation Page 1 of 13 Background: Consistent with our objective of providing useful information to investors about our Company, and as noted in our 2014

Embedded Value 2014 Report Manulife Financial Corporation Page 1 of 13 Background: Consistent with our objective of providing useful information to investors about our Company, and as noted in our 2014

ORSA for Dummies. Institute of Risk Management Solvency II Group April 17th 2012. Peter Taylor

ORSA for Dummies Institute of Risk Management Solvency II Group April 17th 2012 Peter Taylor ORSA for - the Dummies heart of Solvency II Institute of Risk Management Solvency II Group April 17th 2012 Peter

ORSA for Dummies Institute of Risk Management Solvency II Group April 17th 2012 Peter Taylor ORSA for - the Dummies heart of Solvency II Institute of Risk Management Solvency II Group April 17th 2012 Peter

Public reporting in a Solvency II environment

Public in a Survey report August 014 kpmg.co.uk 0 PUBLIC REPORTING IN A SOLVENCY ENVIRONMENT Contents Page 1 4 5 Introduction Executive Summary Public Disclosures 4 Changes to Financial Framework 11 KPMG

Public in a Survey report August 014 kpmg.co.uk 0 PUBLIC REPORTING IN A SOLVENCY ENVIRONMENT Contents Page 1 4 5 Introduction Executive Summary Public Disclosures 4 Changes to Financial Framework 11 KPMG

Regulations in General Insurance. Solvency II

Regulations in General Insurance Solvency II Solvency II What is it? Solvency II is a new risk-based regulatory requirement for insurance, reinsurance and bancassurance (insurance) organisations that operate

Regulations in General Insurance Solvency II Solvency II What is it? Solvency II is a new risk-based regulatory requirement for insurance, reinsurance and bancassurance (insurance) organisations that operate

Actuarial Risk Management

ARA syllabus Actuarial Risk Management Aim: To provide the technical skills to apply the principles and methodologies studied under actuarial technical subjects for the identification, quantification and

ARA syllabus Actuarial Risk Management Aim: To provide the technical skills to apply the principles and methodologies studied under actuarial technical subjects for the identification, quantification and

Guidance Note: Stress Testing Class 2 Credit Unions. November, 2013. Ce document est également disponible en français

Guidance Note: Stress Testing Class 2 Credit Unions November, 2013 Ce document est également disponible en français This Guidance Note is for use by all Class 2 credit unions with assets in excess of $1

Guidance Note: Stress Testing Class 2 Credit Unions November, 2013 Ce document est également disponible en français This Guidance Note is for use by all Class 2 credit unions with assets in excess of $1

Solvency II and Money Market Funds

Solvency II and Money Market Funds FOR INSTITUTIONAL INVESTORS ONLY NOT FOR USE BY OR DISTRIBUTION TO RETAIL INVESTORS Background The new European insurance regulatory framework, Solvency II, will require

Solvency II and Money Market Funds FOR INSTITUTIONAL INVESTORS ONLY NOT FOR USE BY OR DISTRIBUTION TO RETAIL INVESTORS Background The new European insurance regulatory framework, Solvency II, will require

EIOPA-CP-11/008 7 November 2011. Consultation Paper On the Proposal for Guidelines on Own Risk and Solvency Assessment

EIOPA-CP-11/008 7 November 2011 Consultation Paper On the Proposal for Guidelines on Own Risk and Solvency Assessment EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel. + 49 69-951119-20;

EIOPA-CP-11/008 7 November 2011 Consultation Paper On the Proposal for Guidelines on Own Risk and Solvency Assessment EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel. + 49 69-951119-20;

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Standard No. 13 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS STANDARD ON ASSET-LIABILITY MANAGEMENT OCTOBER 2006 This document was prepared by the Solvency and Actuarial Issues Subcommittee in consultation

Standard No. 13 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS STANDARD ON ASSET-LIABILITY MANAGEMENT OCTOBER 2006 This document was prepared by the Solvency and Actuarial Issues Subcommittee in consultation

Solvency Assessment and Management: Capital Requirements Discussion Document 58 (v 3) SCR Structure Credit and Counterparty Default Risk

SCR Structure Credit and Counterparty Default Risk") Solvency Assessment and Management: Capital Requirements Discussion Document 58 (v 3) SCR Structure Credit and Counterparty Default Risk EXECUTIVE SUMMARY Solvency II allows for credit and counterparty

Solvency Assessment and Management: Capital Requirements Discussion Document 58 (v 3) SCR Structure Credit and Counterparty Default Risk EXECUTIVE SUMMARY Solvency II allows for credit and counterparty

Guidance on the management of interest rate risk arising from nontrading

Guidance on the management of interest rate risk arising from nontrading activities Introduction 1. These Guidelines refer to the application of the Supervisory Review Process under Pillar 2 to a structured

Guidance on the management of interest rate risk arising from nontrading activities Introduction 1. These Guidelines refer to the application of the Supervisory Review Process under Pillar 2 to a structured

EEV, MCEV, Solvency, IFRS a chance for actuarial mathematics to get to main-stream of insurance value chain

EEV, MCEV, Solvency, IFRS a chance for actuarial mathematics to get to main-stream of insurance value chain dr Krzysztof Stroiński, dr Renata Onisk, dr Konrad Szuster, mgr Marcin Szczuka 9 June 2008 Presentation

EEV, MCEV, Solvency, IFRS a chance for actuarial mathematics to get to main-stream of insurance value chain dr Krzysztof Stroiński, dr Renata Onisk, dr Konrad Szuster, mgr Marcin Szczuka 9 June 2008 Presentation

Effective Techniques for Stress Testing and Scenario Analysis

Effective Techniques for Stress Testing and Scenario Analysis Om P. Arya Federal Reserve Bank of New York November 4 th, 2008 Mumbai, India The views expressed here are not necessarily of the Federal Reserve

Effective Techniques for Stress Testing and Scenario Analysis Om P. Arya Federal Reserve Bank of New York November 4 th, 2008 Mumbai, India The views expressed here are not necessarily of the Federal Reserve

OWN RISK AND SOLVENCY ASSESSMENT AND ENTERPRISE RISK MANAGEMENT

OWN RISK AND SOLVENCY ASSESSMENT AND ENTERPRISE RISK MANAGEMENT ERM as the foundation for regulatory compliance and strategic business decision making CONTENTS Introduction... 3 Steps to developing an

OWN RISK AND SOLVENCY ASSESSMENT AND ENTERPRISE RISK MANAGEMENT ERM as the foundation for regulatory compliance and strategic business decision making CONTENTS Introduction... 3 Steps to developing an

Preparing for ORSA - Some practical issues

2013 Seminar for the Appointed Actuary Colloque pour l actuaire désigné 2013 Session 13 (P&C): Preparing for ORSA - Some practical issues Speaker: Jean-Marc Léveillé Vice-president Corporate Actuarial,

2013 Seminar for the Appointed Actuary Colloque pour l actuaire désigné 2013 Session 13 (P&C): Preparing for ORSA - Some practical issues Speaker: Jean-Marc Léveillé Vice-president Corporate Actuarial,

Potential for Systemic Risk in the Insurance Sector (Insurers, the Natural Shock Absorbers)

") Potential for Systemic Risk in the Insurance Sector (Insurers, the Natural Shock Absorbers) John C. Hele, Executive Vice President, Chief Financial Officer Banque de France-ACPR Conference Paris, September

Potential for Systemic Risk in the Insurance Sector (Insurers, the Natural Shock Absorbers) John C. Hele, Executive Vice President, Chief Financial Officer Banque de France-ACPR Conference Paris, September

CITIGROUP INC. BASEL II.5 MARKET RISK DISCLOSURES AS OF AND FOR THE PERIOD ENDED MARCH 31, 2013

CITIGROUP INC. BASEL II.5 MARKET RISK DISCLOSURES AS OF AND FOR THE PERIOD ENDED MARCH 31, 2013 DATED AS OF MAY 15, 2013 Table of Contents Qualitative Disclosures Basis of Preparation and Review... 3 Risk

CITIGROUP INC. BASEL II.5 MARKET RISK DISCLOSURES AS OF AND FOR THE PERIOD ENDED MARCH 31, 2013 DATED AS OF MAY 15, 2013 Table of Contents Qualitative Disclosures Basis of Preparation and Review... 3 Risk

Modelling and Management of Tail Risk in Insurance

Modelling and Management of Tail Risk in Insurance IMF conference on operationalising systemic risk monitoring Peter Sohre, Head of Risk Reporting, Swiss Re Washington DC, 27 May 2010 Visit of ntuc ERM

Modelling and Management of Tail Risk in Insurance IMF conference on operationalising systemic risk monitoring Peter Sohre, Head of Risk Reporting, Swiss Re Washington DC, 27 May 2010 Visit of ntuc ERM

THE INSURANCE BUSINESS (SOLVENCY) RULES 2015

RULES 2015") THE INSURANCE BUSINESS (SOLVENCY) RULES 2015 Table of Contents Part 1 Introduction... 2 Part 2 Capital Adequacy... 4 Part 3 MCR... 7 Part 4 PCR... 10 Part 5 - Internal Model... 23 Part 6 Valuation... 34

THE INSURANCE BUSINESS (SOLVENCY) RULES 2015 Table of Contents Part 1 Introduction... 2 Part 2 Capital Adequacy... 4 Part 3 MCR... 7 Part 4 PCR... 10 Part 5 - Internal Model... 23 Part 6 Valuation... 34

SOLVENCY II LIFE INSURANCE

SOLVENCY II LIFE INSURANCE 1 Overview 1.1 Background and scope The current UK regulatory reporting regime is based on the EU Solvency I Directives. Although the latest of those Directives was implemented

SOLVENCY II LIFE INSURANCE 1 Overview 1.1 Background and scope The current UK regulatory reporting regime is based on the EU Solvency I Directives. Although the latest of those Directives was implemented

Financial Services Industry 2012. Solvency II How to conduct the ORSA Requirements, EIOPA responses and Industry views

Financial Services Industry 2012 Solvency II How to conduct the ORSA Requirements, EIOPA responses and Industry views Content Table 3 Foreword 5 ORSA overall considerations 6 ORSA key components, requirements

Financial Services Industry 2012 Solvency II How to conduct the ORSA Requirements, EIOPA responses and Industry views Content Table 3 Foreword 5 ORSA overall considerations 6 ORSA key components, requirements

SCOR inform - April 2012. Life (re)insurance under Solvency II

insurance under Solvency II") SCOR inform - April 2012 Life (re)insurance under Solvency II Life (re)insurance under Solvency II Author Thorsten Keil SCOR Global Life Cologne Editor Bérangère Mainguy Tel: +33 (0)1 58 44 70 00 Fax:

SCOR inform - April 2012 Life (re)insurance under Solvency II Life (re)insurance under Solvency II Author Thorsten Keil SCOR Global Life Cologne Editor Bérangère Mainguy Tel: +33 (0)1 58 44 70 00 Fax:

ALM Stress Testing: Gaining Insight on Modeled Outcomes

ALM Stress Testing: Gaining Insight on Modeled Outcomes 2013 Financial Conference Ballantyne Resort Charlotte, NC September 18, 2013 Thomas E. Bowers, CFA Vice President Client Services ZM Financial Systems

ALM Stress Testing: Gaining Insight on Modeled Outcomes 2013 Financial Conference Ballantyne Resort Charlotte, NC September 18, 2013 Thomas E. Bowers, CFA Vice President Client Services ZM Financial Systems

Assessing Sources of Funding for Insurance Risk Based Capital

Assessing Sources of Funding for Insurance Risk Based Capital Louis Lee Session Number: (ex. MBR4) AGENDA for Today 1. Motivations of Capital Needs 2. Practical Risk Based Capital Funding Options 3. Types

Assessing Sources of Funding for Insurance Risk Based Capital Louis Lee Session Number: (ex. MBR4) AGENDA for Today 1. Motivations of Capital Needs 2. Practical Risk Based Capital Funding Options 3. Types

Embedded Value Report

Embedded Value Report 2012 ACHMEA EMBEDDED VALUE REPORT 2012 Contents Management summary 3 Introduction 4 Embedded Value Results 5 Value Added by New Business 6 Analysis of Change 7 Sensitivities 9 Impact

Embedded Value Report 2012 ACHMEA EMBEDDED VALUE REPORT 2012 Contents Management summary 3 Introduction 4 Embedded Value Results 5 Value Added by New Business 6 Analysis of Change 7 Sensitivities 9 Impact

Capital preservation strategy update

Client Education Summit 2012 Capital preservation strategy update Head of Institutional Fixed Income Investments, Americas October 9, 2012 Topics for discussion 1 Capital preservation strategies 2 3 4

Client Education Summit 2012 Capital preservation strategy update Head of Institutional Fixed Income Investments, Americas October 9, 2012 Topics for discussion 1 Capital preservation strategies 2 3 4

LIFE INSURANCE CAPITAL FRAMEWORK STANDARD APPROACH

LIFE INSURANCE CAPITAL FRAMEWORK STANDARD APPROACH Table of Contents Introduction... 2 Process... 2 and Methodology... 3 Core Concepts... 3 Total Asset Requirement... 3 Solvency Buffer... 4 Framework Details...

LIFE INSURANCE CAPITAL FRAMEWORK STANDARD APPROACH Table of Contents Introduction... 2 Process... 2 and Methodology... 3 Core Concepts... 3 Total Asset Requirement... 3 Solvency Buffer... 4 Framework Details...

Risk-Based Capital. Overview

Risk-Based Capital Definition: Risk-based capital (RBC) represents an amount of capital based on an assessment of risks that a company should hold to protect customers against adverse developments. Overview

Risk-Based Capital Definition: Risk-based capital (RBC) represents an amount of capital based on an assessment of risks that a company should hold to protect customers against adverse developments. Overview

Understanding Currency

Understanding Currency Overlay July 2010 PREPARED BY Gregory J. Leonberger, FSA Director of Research Abstract As portfolios have expanded to include international investments, investors must be aware of

Understanding Currency Overlay July 2010 PREPARED BY Gregory J. Leonberger, FSA Director of Research Abstract As portfolios have expanded to include international investments, investors must be aware of

Guidance for the Development of a Models-Based Solvency Framework for Canadian Life Insurance Companies

Guidance for the Development of a Models-Based Solvency Framework for Canadian Life Insurance Companies January 2010 Background The MCCSR Advisory Committee was established to develop proposals for a new

Guidance for the Development of a Models-Based Solvency Framework for Canadian Life Insurance Companies January 2010 Background The MCCSR Advisory Committee was established to develop proposals for a new

IRSG Response to IAIS Consultation Paper on Basic Capital Requirements (BCR) for Global Systemically Important Insurers (G-SIIS)

for Global Systemically Important Insurers (G-SIIS)") EIOPA-IRSG-14-10 IRSG Response to IAIS Consultation Paper on Basic Capital Requirements (BCR) for Global Systemically Important Insurers (G-SIIS) 1/10 Executive Summary The IRSG supports the development

EIOPA-IRSG-14-10 IRSG Response to IAIS Consultation Paper on Basic Capital Requirements (BCR) for Global Systemically Important Insurers (G-SIIS) 1/10 Executive Summary The IRSG supports the development

Solvency II Own Risk and Solvency Assessment (ORSA)

") Solvency II Own Risk and Solvency Assessment (ORSA) Guidance notes September 2011 Contents Introduction Purpose of this Document 3 Lloyd s ORSA framework 3 Guidance for Syndicate ORSAs Overview 7 December

Solvency II Own Risk and Solvency Assessment (ORSA) Guidance notes September 2011 Contents Introduction Purpose of this Document 3 Lloyd s ORSA framework 3 Guidance for Syndicate ORSAs Overview 7 December

Market Consistent Embedded Value Principles October 2009. CFO Forum

CFO Forum Market Consistent Embedded Value Principles October 2009 Contents Introduction. 2 Coverage. 2 MCEV Definitions...3 Free Surplus 3 Required Capital 3 Value of in-force Covered Business 4 Financial

CFO Forum Market Consistent Embedded Value Principles October 2009 Contents Introduction. 2 Coverage. 2 MCEV Definitions...3 Free Surplus 3 Required Capital 3 Value of in-force Covered Business 4 Financial

Hans Wagner AXA Group Life Chief Risk Officer. Ferdia Byrne Partner, KPMG. June, 2010. Congrès Annuel des Actuaires

Hans Wagner AXA Group Life Chief Risk Officer Ferdia Byrne Partner, KPMG June, 2010 Congrès Annuel des Actuaires Contents Perspectives from an insurer Brief reminder of Solvency II Lessons from the Financial

Hans Wagner AXA Group Life Chief Risk Officer Ferdia Byrne Partner, KPMG June, 2010 Congrès Annuel des Actuaires Contents Perspectives from an insurer Brief reminder of Solvency II Lessons from the Financial

ORSA - The heart of Solvency II

ORSA - The heart of Solvency II Groupe Consultatif Summer School Gabriel Bernardino, EIOPA Lisbon, 25 May 2011 ORSA - The heart of Solvency II Developing the regulatory framework for Solvency II ORSA it

ORSA - The heart of Solvency II Groupe Consultatif Summer School Gabriel Bernardino, EIOPA Lisbon, 25 May 2011 ORSA - The heart of Solvency II Developing the regulatory framework for Solvency II ORSA it

Implementation of Solvency II: The dos and the don ts

KEYNOTE SPEECH Gabriel Bernardino Chairman of EIOPA Implementation of Solvency II: The dos and the don ts International conference Solvency II: What Can Go Wrong? Ljubljana, 2 September 2015 Page 2 of

KEYNOTE SPEECH Gabriel Bernardino Chairman of EIOPA Implementation of Solvency II: The dos and the don ts International conference Solvency II: What Can Go Wrong? Ljubljana, 2 September 2015 Page 2 of

An update on QIS5. Agenda 4/27/2010. Context, scope and timelines The draft Technical Specification Getting into gear Questions

A Closer Look at Solvency II Eleanor Beamond-Pepler, FSA An update on QIS5 2010 The Actuarial Profession www.actuaries.org.uk Agenda Context, scope and timelines The draft Technical Specification Getting

A Closer Look at Solvency II Eleanor Beamond-Pepler, FSA An update on QIS5 2010 The Actuarial Profession www.actuaries.org.uk Agenda Context, scope and timelines The draft Technical Specification Getting

Solvency Management in Life Insurance The company s perspective

Group Risk IAA Seminar 19 April 2007, Mexico City Uncertainty Exposure Solvency Management in Life Insurance The company s perspective Agenda 1. Key elements of Allianz Risk Management framework 2. Drawbacks

Group Risk IAA Seminar 19 April 2007, Mexico City Uncertainty Exposure Solvency Management in Life Insurance The company s perspective Agenda 1. Key elements of Allianz Risk Management framework 2. Drawbacks

Seeking a More Efficient Fixed Income Portfolio with Asia Bonds

Seeking a More Efficient Fixed Income Portfolio with Asia s Seeking a More Efficient Fixed Income Portfolio with Asia s Drawing upon different drivers for performance, Asia fixed income may improve risk-return

Seeking a More Efficient Fixed Income Portfolio with Asia s Seeking a More Efficient Fixed Income Portfolio with Asia s Drawing upon different drivers for performance, Asia fixed income may improve risk-return

Condensed Interim Consolidated Financial Statements of. Canada Pension Plan Investment Board

Condensed Interim Consolidated Financial Statements of Canada Pension Plan Investment Board December 31, 2015 Condensed Interim Consolidated Balance Sheet As at December 31, 2015 (CAD millions) As at December

Condensed Interim Consolidated Financial Statements of Canada Pension Plan Investment Board December 31, 2015 Condensed Interim Consolidated Balance Sheet As at December 31, 2015 (CAD millions) As at December

Rating Methodology for Domestic Life Insurance Companies

Rating Methodology for Domestic Life Insurance Companies Introduction ICRA Lanka s Claim Paying Ability Ratings (CPRs) are opinions on the ability of life insurance companies to pay claims and policyholder

Rating Methodology for Domestic Life Insurance Companies Introduction ICRA Lanka s Claim Paying Ability Ratings (CPRs) are opinions on the ability of life insurance companies to pay claims and policyholder

Summary of the Paper Awarded the SCOR Prize in Actuarial Science 2012 in Germany (2 nd Prize)

") Summary of the Paper Awarded the SCOR Prize in Actuarial Science 2012 in Germany (2 nd Prize) Title: Market-Consistent Valuation of Long-Term Insurance Contracts Valuation Framework and Application to

Summary of the Paper Awarded the SCOR Prize in Actuarial Science 2012 in Germany (2 nd Prize) Title: Market-Consistent Valuation of Long-Term Insurance Contracts Valuation Framework and Application to

INSURANCE RATING METHODOLOGY

INSURANCE RATING METHODOLOGY The primary function of PACRA is to evaluate the capacity and willingness of an entity / issuer to honor its financial obligations. Our ratings reflect an independent, professional

INSURANCE RATING METHODOLOGY The primary function of PACRA is to evaluate the capacity and willingness of an entity / issuer to honor its financial obligations. Our ratings reflect an independent, professional

Are Unconstrained Bond Funds a Substitute for Core Bonds?

TOPICS OF INTEREST Are Unconstrained Bond Funds a Substitute for Core Bonds? By Peter Wilamoski, Ph.D. Director of Economic Research Philip Schmitt, CIMA Senior Research Associate AUGUST 2014 The problem

TOPICS OF INTEREST Are Unconstrained Bond Funds a Substitute for Core Bonds? By Peter Wilamoski, Ph.D. Director of Economic Research Philip Schmitt, CIMA Senior Research Associate AUGUST 2014 The problem

Condensed Interim Consolidated Financial Statements of. Canada Pension Plan Investment Board

Condensed Interim Consolidated Financial Statements of Canada Pension Plan Investment Board September 30, 2015 Condensed Interim Consolidated Balance Sheet As at September 30, 2015 As at September 30,

Condensed Interim Consolidated Financial Statements of Canada Pension Plan Investment Board September 30, 2015 Condensed Interim Consolidated Balance Sheet As at September 30, 2015 As at September 30,

Final Report on Public Consultation No. 14/017 on Guidelines on own risk and solvency assessment

EIOPA-BoS-14/259 28 January 2015 Final Report on Public Consultation No. 14/017 on Guidelines on own risk and solvency assessment EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel.

EIOPA-BoS-14/259 28 January 2015 Final Report on Public Consultation No. 14/017 on Guidelines on own risk and solvency assessment EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel.

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2013

Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2013") Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2013 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial period from 1 January 2013 to 31 December 2013

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2013 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial period from 1 January 2013 to 31 December 2013

Impacts of the Solvency II Standard Formula on health insurance business in Germany

Impacts of the Solvency II Standard Formula on health insurance business in Germany Sascha Raithel Association of German private healthcare insurers Agenda 1. Private health insurance business in Germany

Impacts of the Solvency II Standard Formula on health insurance business in Germany Sascha Raithel Association of German private healthcare insurers Agenda 1. Private health insurance business in Germany

ERM from a Small Insurance Company Perspective

ERM from a Small Insurance Company Perspective NABRICO Sept 30, 2011 Agenda Section 1 Section 2 Section 3 Section 4 ERM Introduction Key Risks Streamlined Quantitative Process Other Influences 1 1 Section

ERM from a Small Insurance Company Perspective NABRICO Sept 30, 2011 Agenda Section 1 Section 2 Section 3 Section 4 ERM Introduction Key Risks Streamlined Quantitative Process Other Influences 1 1 Section

Market-Consistent Valuation of the Sponsor Covenant and its use in Risk-Based Capital Assessment. Craig Turnbull FIA

Market-Consistent Valuation of the Sponsor Covenant and its use in Risk-Based Capital Assessment Craig Turnbull FIA Background and Research Objectives 2 Background: DB Pensions and Risk + Aggregate deficits

Market-Consistent Valuation of the Sponsor Covenant and its use in Risk-Based Capital Assessment Craig Turnbull FIA Background and Research Objectives 2 Background: DB Pensions and Risk + Aggregate deficits

Central Bank of Ireland Guidelines on Preparing for Solvency II Pre-application for Internal Models

2013 Central Bank of Ireland Guidelines on Preparing for Solvency II Pre-application for Internal Models 1 Contents 1 Context... 1 2 General... 2 3 Guidelines on Pre-application for Internal Models...

2013 Central Bank of Ireland Guidelines on Preparing for Solvency II Pre-application for Internal Models 1 Contents 1 Context... 1 2 General... 2 3 Guidelines on Pre-application for Internal Models...

EIOPACP 13/09. Guidelines on Forward Looking assessment of own risks (based on the ORSA principles)

") EIOPACP 13/09 Guidelines on Forward Looking assessment of own risks (based on the ORSA principles) EIOPA Westhafen Tower, Westhafenplatz 1 60327 Frankfurt Germany Tel. + 49 6995111920; Fax. + 49 6995111919;

EIOPACP 13/09 Guidelines on Forward Looking assessment of own risks (based on the ORSA principles) EIOPA Westhafen Tower, Westhafenplatz 1 60327 Frankfurt Germany Tel. + 49 6995111920; Fax. + 49 6995111919;

1. INTRODUCTION AND PURPOSE

Solvency Assessment and Management: Pillar 1 - Sub Committee Capital Requirements Task Group Discussion Document 73 (v 2) Treatment of new business in SCR EXECUTIVE SUMMARY As for the Solvency II Framework

Solvency Assessment and Management: Pillar 1 - Sub Committee Capital Requirements Task Group Discussion Document 73 (v 2) Treatment of new business in SCR EXECUTIVE SUMMARY As for the Solvency II Framework

SWEDBANK FÖRSÄKRING AB. 2015 European Embedded Value

SWEDBANK FÖRSÄKRING AB 2015 European Embedded Value Content 1 Introduction... 2 2 Overview of results... 2 3 Covered business... 2 4 EEV results... 2 5 Value of new business... 4 6 Analysis of EEV earnings...

SWEDBANK FÖRSÄKRING AB 2015 European Embedded Value Content 1 Introduction... 2 2 Overview of results... 2 3 Covered business... 2 4 EEV results... 2 5 Value of new business... 4 6 Analysis of EEV earnings...

Disclosure of European Embedded Value (summary) as of March 31, 2012

as of March 31, 2012") May 25, 2012 SUMITOMO LIFE INSURANCE COMPANY Disclosure of European Embedded Value (summary) as of 2012 This is the summarized translation of the European Embedded Value ( EEV ) of Sumitomo Life Insurance

May 25, 2012 SUMITOMO LIFE INSURANCE COMPANY Disclosure of European Embedded Value (summary) as of 2012 This is the summarized translation of the European Embedded Value ( EEV ) of Sumitomo Life Insurance

Effective Stress Testing in Enterprise Risk Management

Effective Stress Testing in Enterprise Risk Management Lijia Guo, Ph.D., ASA, MAAA *^ Copyright 2008 by the Society of Actuaries. All rights reserved by the Society of Actuaries. Permission is granted

Effective Stress Testing in Enterprise Risk Management Lijia Guo, Ph.D., ASA, MAAA *^ Copyright 2008 by the Society of Actuaries. All rights reserved by the Society of Actuaries. Permission is granted

ORSA for Insurers A Global Concept

ORSA for Insurers A Global Concept Stuart Wason, FSA, FCIA, MAAA, CERA Senior Director, Actuarial Division Office of the Superintendent of Financial Institutions Canada (OSFI) Table of Contents Early developments

ORSA for Insurers A Global Concept Stuart Wason, FSA, FCIA, MAAA, CERA Senior Director, Actuarial Division Office of the Superintendent of Financial Institutions Canada (OSFI) Table of Contents Early developments

ORSA Implementation Challenges

1 ORSA Implementation Challenges Christopher Crombie, FSA, FCIA AVP ERM & Financial Risk Management Standard Life Assurance Company of Canada To CIA Annual Meeting June 21, 2013 2 Context Our Own Risk

1 ORSA Implementation Challenges Christopher Crombie, FSA, FCIA AVP ERM & Financial Risk Management Standard Life Assurance Company of Canada To CIA Annual Meeting June 21, 2013 2 Context Our Own Risk

Making progress towards our objectives

Making progress towards our objectives Scotiabank Financials Summit 2013 Donald A. Guloien President and Chief Executive Officer September 5, 2013 Caution regarding forward-looking statements This presentation

Making progress towards our objectives Scotiabank Financials Summit 2013 Donald A. Guloien President and Chief Executive Officer September 5, 2013 Caution regarding forward-looking statements This presentation

Technical Practices Survey 2015 Solvency II

FINANCIAL SERVICES Technical Practices Survey 05 Solvency II Contents Foreword Executive summary 4 3 Introduction 5 3.: Objectives 5 3.: Survey methodology 5 3.3: Topics of interest 6 3.4: Interpretation

FINANCIAL SERVICES Technical Practices Survey 05 Solvency II Contents Foreword Executive summary 4 3 Introduction 5 3.: Objectives 5 3.: Survey methodology 5 3.3: Topics of interest 6 3.4: Interpretation

Liquidity Coverage Ratio

Liquidity Coverage Ratio Aims to ensure banks maintain adequate levels of unencumbered high quality assets (numerator) against net cash outflows (denominator) over a 30 day significant stress period. High

Liquidity Coverage Ratio Aims to ensure banks maintain adequate levels of unencumbered high quality assets (numerator) against net cash outflows (denominator) over a 30 day significant stress period. High

02/06/2014. Solvency II update. Agenda. Recap: Solvency II three pillar approach. Nick Ford

Solvency II update Nick Ford 02 June 2014 Agenda Intro and brief recap Pillar 1 Main issues Impacts on products Pillar 2 Main issues Internal Model Approval Pillar 3 Actuarial forms and concerns Timelines

Solvency II update Nick Ford 02 June 2014 Agenda Intro and brief recap Pillar 1 Main issues Impacts on products Pillar 2 Main issues Internal Model Approval Pillar 3 Actuarial forms and concerns Timelines

PRODUCT HIGHLIGHTS SHEET

Prepared on 18 January 2016 This Product Highlights Sheet is an important document. It highlights the key terms and risks of this investment product and complements the Singapore Prospectus 1 ( Prospectus

Prepared on 18 January 2016 This Product Highlights Sheet is an important document. It highlights the key terms and risks of this investment product and complements the Singapore Prospectus 1 ( Prospectus

CEIOPS Preparatory Field Study for Life Insurance Firms. Summary Report

CEIOPS-FS-08/05 S CEIOPS Preparatory Field Study for Life Insurance Firms Summary Report 1 GENERAL OBSERVATIONS AND CONCLUSIONS 1.1 Introduction CEIOPS has been asked to prepare advice for the European

CEIOPS-FS-08/05 S CEIOPS Preparatory Field Study for Life Insurance Firms Summary Report 1 GENERAL OBSERVATIONS AND CONCLUSIONS 1.1 Introduction CEIOPS has been asked to prepare advice for the European

GN47: Stochastic Modelling of Economic Risks in Life Insurance

GN47: Stochastic Modelling of Economic Risks in Life Insurance Classification Recommended Practice MEMBERS ARE REMINDED THAT THEY MUST ALWAYS COMPLY WITH THE PROFESSIONAL CONDUCT STANDARDS (PCS) AND THAT

GN47: Stochastic Modelling of Economic Risks in Life Insurance Classification Recommended Practice MEMBERS ARE REMINDED THAT THEY MUST ALWAYS COMPLY WITH THE PROFESSIONAL CONDUCT STANDARDS (PCS) AND THAT

ERM Practice and Challenge in China Insurance Company. Zhang Chensong, FSA,CERA,FIA,FCAA Head of Risk Management Taikang Life Insurance

ERM Practice and Challenge in China Insurance Company Zhang Chensong, FSA,CERA,FIA,FCAA Head of Risk Management Taikang Life Insurance Agenda ERM development in China ERM framework Economic capital application

ERM Practice and Challenge in China Insurance Company Zhang Chensong, FSA,CERA,FIA,FCAA Head of Risk Management Taikang Life Insurance Agenda ERM development in China ERM framework Economic capital application

Deriving Value from ORSA. Board Perspective

Deriving Value from ORSA Board Perspective April 2015 1 This paper has been produced by the Joint Own Risk Solvency Assessment (ORSA) Subcommittee of the Insurance Regulation Committee and the Enterprise

Deriving Value from ORSA Board Perspective April 2015 1 This paper has been produced by the Joint Own Risk Solvency Assessment (ORSA) Subcommittee of the Insurance Regulation Committee and the Enterprise

Risk Management & Solvency Assessment of Life Insurance Companies By Sanket Kawatkar, BCom, FIA Heerak Basu, MA, FFA, FASI, MBA

Risk Management & Solvency Assessment of Life Insurance Companies By Sanket Kawatkar, BCom, FIA Heerak Basu, MA, FFA, FASI, MBA Abstract This paper summarises the work done in this area by various parties,

Risk Management & Solvency Assessment of Life Insurance Companies By Sanket Kawatkar, BCom, FIA Heerak Basu, MA, FFA, FASI, MBA Abstract This paper summarises the work done in this area by various parties,

An introduction to Value-at-Risk Learning Curve September 2003

An introduction to Value-at-Risk Learning Curve September 2003 Value-at-Risk The introduction of Value-at-Risk (VaR) as an accepted methodology for quantifying market risk is part of the evolution of risk

An introduction to Value-at-Risk Learning Curve September 2003 Value-at-Risk The introduction of Value-at-Risk (VaR) as an accepted methodology for quantifying market risk is part of the evolution of risk

Notes to the consolidated financial statements Part E Information on risks and relative hedging policies

SECTION 2 RISKS OF INSURANCE COMPANIES 2.1 INSURANCE RISKS Life branch The typical risks of the life insurance portfolio (managed by EurizonVita, EurizonLife, SudPoloVita and CentroVita) may be divided

SECTION 2 RISKS OF INSURANCE COMPANIES 2.1 INSURANCE RISKS Life branch The typical risks of the life insurance portfolio (managed by EurizonVita, EurizonLife, SudPoloVita and CentroVita) may be divided

SCOR Papers. Using Capital Allocation to Steer the Portfolio towards Profitability. Abstract. September 2008 N 1

September 28 N 1 SCOR Papers Using Allocation to Steer the Portfolio towards Profitability By Jean-Luc Besson (Chief Risk Officer), Michel Dacorogna (Head of Group Financial Modelling), Paolo de Martin

September 28 N 1 SCOR Papers Using Allocation to Steer the Portfolio towards Profitability By Jean-Luc Besson (Chief Risk Officer), Michel Dacorogna (Head of Group Financial Modelling), Paolo de Martin

M&A in a Solvency II World - An introduction to the S2AV methodology

M&A in a Solvency II World - An introduction to the S2AV methodology Presented by Ed Morgan March 17, 2016 Warsaw Contents 1. Why Solvency II can be very helpful 2. What we saw in recent projects 3. Issues

M&A in a Solvency II World - An introduction to the S2AV methodology Presented by Ed Morgan March 17, 2016 Warsaw Contents 1. Why Solvency II can be very helpful 2. What we saw in recent projects 3. Issues

Market and Liquidity Risk Assessment Overview. Federal Reserve System

Market and Liquidity Risk Assessment Overview Federal Reserve System Overview Inherent Risk Risk Management Composite Risk Trend 2 Market and Liquidity Risk: Inherent Risk Definition Identification Quantification

Market and Liquidity Risk Assessment Overview Federal Reserve System Overview Inherent Risk Risk Management Composite Risk Trend 2 Market and Liquidity Risk: Inherent Risk Definition Identification Quantification

SOLVENCY II HEALTH INSURANCE

2014 Solvency II Health SOLVENCY II HEALTH INSURANCE 1 Overview 1.1 Background and scope The current UK regulatory reporting regime is based on the EU Solvency I Directives. Although the latest of those

2014 Solvency II Health SOLVENCY II HEALTH INSURANCE 1 Overview 1.1 Background and scope The current UK regulatory reporting regime is based on the EU Solvency I Directives. Although the latest of those

Least Squares Monte Carlo for fast and robust capital projections

Least Squares Monte Carlo for fast and robust capital projections 5 February 2013 INTRODUCTION Reliable capital projections are necessary for management purposes. For an insurer operating in the Solvency

Least Squares Monte Carlo for fast and robust capital projections 5 February 2013 INTRODUCTION Reliable capital projections are necessary for management purposes. For an insurer operating in the Solvency

Session 9b L&H Insurance in a Low Interest Rate Environment. Christian Liechti

Session 9b L&H Insurance in a Low Interest Rate Environment Christian Liechti L&H Insurance in a Low Interest Rate Environment SOA Annual Symposium 24-25 June 2013 Macau, China Christian Liechti Swiss

Session 9b L&H Insurance in a Low Interest Rate Environment Christian Liechti L&H Insurance in a Low Interest Rate Environment SOA Annual Symposium 24-25 June 2013 Macau, China Christian Liechti Swiss

Jose Rodicio, ASA, CFA, FRM Deputy Chief Insurance Risk Officer ING Latin America Atlanta Actuarial Club March 26, 2009

Enterprise Risk Management and Economic Capital at ING A practical approach Jose Rodicio, ASA, CFA, FRM Deputy Chief Insurance Risk Officer ING Latin America Atlanta Actuarial Club March 26, 2009 Agenda

Enterprise Risk Management and Economic Capital at ING A practical approach Jose Rodicio, ASA, CFA, FRM Deputy Chief Insurance Risk Officer ING Latin America Atlanta Actuarial Club March 26, 2009 Agenda

Solvency II. Impacts on asset managers and servicers. Financial Services Asset Management. www.pwc.com/it

Financial Services Asset Management Solvency II Impacts on asset managers and servicers The Omnibus II proposal will amend the Solvency II Directive voted in 2009. It would probably defer full Solvency

Financial Services Asset Management Solvency II Impacts on asset managers and servicers The Omnibus II proposal will amend the Solvency II Directive voted in 2009. It would probably defer full Solvency

Subject ST9 Enterprise Risk Management Syllabus

Subject ST9 Enterprise Risk Management Syllabus for the 2015 exams 1 June 2014 Aim The aim of the Enterprise Risk Management (ERM) Specialist Technical subject is to instil in successful candidates the

Subject ST9 Enterprise Risk Management Syllabus for the 2015 exams 1 June 2014 Aim The aim of the Enterprise Risk Management (ERM) Specialist Technical subject is to instil in successful candidates the

CFA Institute Contingency Reserves Investment Policy Effective 8 February 2012

CFA Institute Contingency Reserves Investment Policy Effective 8 February 2012 Purpose This policy statement provides guidance to CFA Institute management and Board regarding the CFA Institute Reserves

CFA Institute Contingency Reserves Investment Policy Effective 8 February 2012 Purpose This policy statement provides guidance to CFA Institute management and Board regarding the CFA Institute Reserves

Quantitative Asset Manager Analysis

Quantitative Asset Manager Analysis Performance Measurement Forum Dr. Stephan Skaanes, CFA, CAIA, FRM PPCmetrics AG Financial Consulting, Controlling & Research, Zurich, Switzerland www.ppcmetrics.ch Copenhagen,

Quantitative Asset Manager Analysis Performance Measurement Forum Dr. Stephan Skaanes, CFA, CAIA, FRM PPCmetrics AG Financial Consulting, Controlling & Research, Zurich, Switzerland www.ppcmetrics.ch Copenhagen,

Best Estimate of the Technical Provisions

Best Estimate of the Technical Provisions FSI Regional Seminar for Supervisors in Africa on Risk Based Supervision Mombasa, Kenya, 14-17 September 2010 Leigh McMahon BA FIAA GAICD Senior Manager, Diversified

Best Estimate of the Technical Provisions FSI Regional Seminar for Supervisors in Africa on Risk Based Supervision Mombasa, Kenya, 14-17 September 2010 Leigh McMahon BA FIAA GAICD Senior Manager, Diversified

ERM Exam Core Readings Fall 2015. Table of Contents

i ERM Exam Core Readings Fall 2015 Table of Contents Section A: Risk Categories and Identification The candidate will understand the types of risks faced by an entity and be able to identify and analyze

i ERM Exam Core Readings Fall 2015 Table of Contents Section A: Risk Categories and Identification The candidate will understand the types of risks faced by an entity and be able to identify and analyze

Das Risikokapitalmodell der Allianz Lebensversicherungs-AG

Das Risikokapitalmodell der Allianz s-ag Ulm 19. Mai 2003 Dr. Max Happacher Allianz s-ag Table of contents 1. Introduction: Motivation, Group-wide Framework 2. Internal Risk Model: Basics, Life Approach

Das Risikokapitalmodell der Allianz s-ag Ulm 19. Mai 2003 Dr. Max Happacher Allianz s-ag Table of contents 1. Introduction: Motivation, Group-wide Framework 2. Internal Risk Model: Basics, Life Approach

Solvency II Own risk and solvency assessment (ORSA)

") Solvency II Own risk and solvency assessment (ORSA) Guidance notes MAY 2012 Contents Introduction Page Background 3 Purpose and Scope 3 Structure of guidance document 4 Key Principles and Lloyd s Minimum

Solvency II Own risk and solvency assessment (ORSA) Guidance notes MAY 2012 Contents Introduction Page Background 3 Purpose and Scope 3 Structure of guidance document 4 Key Principles and Lloyd s Minimum

Micro Simulation Study of Life Insurance Business

Micro Simulation Study of Life Insurance Business Lauri Saraste, LocalTapiola Group, Finland Timo Salminen, Model IT, Finland Lasse Koskinen, Aalto University & Model IT, Finland Agenda Big Data is here!

Micro Simulation Study of Life Insurance Business Lauri Saraste, LocalTapiola Group, Finland Timo Salminen, Model IT, Finland Lasse Koskinen, Aalto University & Model IT, Finland Agenda Big Data is here!

ASIAN PORTFOLIO INVESTMENT ADVISORY

ASIAN PORTFOLIO INVESTMENT ADVISORY This Asian Portfolio Investment Advisory service is set up to assist international financial advisory and planning organizations to create dedicated Asian investment

ASIAN PORTFOLIO INVESTMENT ADVISORY This Asian Portfolio Investment Advisory service is set up to assist international financial advisory and planning organizations to create dedicated Asian investment

EIOPACP 13/011. Guidelines on PreApplication of Internal Models

EIOPACP 13/011 Guidelines on PreApplication of Internal Models EIOPA Westhafen Tower, Westhafenplatz 1 60327 Frankfurt Germany Tel. + 49 6995111920; Fax. + 49 6995111919; site: www.eiopa.europa.eu Guidelines

EIOPACP 13/011 Guidelines on PreApplication of Internal Models EIOPA Westhafen Tower, Westhafenplatz 1 60327 Frankfurt Germany Tel. + 49 6995111920; Fax. + 49 6995111919; site: www.eiopa.europa.eu Guidelines

This chapter assesses the risks that were identified in the first chapter and elaborated in the earlier chapters of this report.

5. Risk assessment This chapter assesses the risks that were identified in the first chapter and elaborated in the earlier chapters of this report. 5.1. Qualitative risk assessment Qualitative risk assessment

5. Risk assessment This chapter assesses the risks that were identified in the first chapter and elaborated in the earlier chapters of this report. 5.1. Qualitative risk assessment Qualitative risk assessment